22 minute read

INDIA’S ENERGY DILEMMA

India is perhaps the first major economy in human history to try to achieve three energy goals simultaneously-one, to end energy poverty and provide affordable energy access to over a billion people, second to do this while exercising “planetary responsibility with an accelerated transition to cleaner energy and decarbonisation and, third, to do it while maximising energy self-sufficiency, and being cognizant of energy security.

Advertisement

No other large country has had to do all three simultaneously. The experience of China, the USA, Europe, Russia etc. with their massive contribution to global emissions, pollution, exploitation of other people’s resources, energy wars etc., is another story, following a totally different script.

Historical Context

Energy self-reliance, or at least taking the first recourse to domestically available resources, has been the aim since our first PM assumed office. He oversaw the stepping up of hydropower on a massive scale and laid the foundation for nuclear energy. In the first 3-4 decades after independence, India expanded coal production, built an oil industry, started on gas, and created the Ministry of New and Renewable Energy. We were oil importers, but in an era of slow economic growth, energy demand also grew relatively slowly, and we learnt to live with constant energy problems (‘load shedding’ became part of our everyday language!). There were some anxieties about oil product supplies during the 1971 war, but apparently not enough to start a new energy policy. (Refineries run by American companies in India were nationalised after the war, though)

Energy Poverty is a critical component of India’s energy crisis and is not often spoken about. It is estimated that in the whole world, there are 1.3 billion people who rely on basic biomass-wood, crop wastes, charcoal, dung etc. for cooking to stay alive; about 250 million are in India (the number can go up to 300 to 400 million -when kerosene/LPG costs go up).

India was hit hard by the oil price crises of the 1970s. It went through austerity and an Emergency, and constant worries about escalating prices and trade deficits, till the Bombay High oilfield provided some relief in the early 1980s. However, we did not actually face a crisis till 1990 when economic growth accelerated faster than the energy supply for many years. The financial crisis of 1991 began with an oil crisis.From my vantage point heading the Indian Embassy in Iran in the first few months after Saddam Hussein occupied Kuwait, I was witness to the panic in Delhi over oil supplies, not just prices, as the prospect of war briefly closed shipping out of the Gulf. The 1991 financial crisis started with an energy crisis.

The 1990s thus highlighted the importance of energy for a now fast-growing Indian economy. Some reforms were initiated- private sector coal production, oil and gas sector reforms, beginnings on wind and solar power, and plans for scaling up hydropower and nuclear energy etc. Energy efficiency was emphasised, and from 1990 onwards, the energy intensity of economic growth was reduced, and Energy Efficiency became an industry, or service, on its own.

2003-2009 were boom years for the economy. This was the era when the Indo-U.S. nuclear accord was signed, and India and the rest of BRICS were supposed to initiate a new world order by 2020. For us, that era ended with the global economic crisis, oil price inflation and domestic scandals- including, significantly the intensely political one over coal production. This was also a period when global attention to climate change increased western pressure on India to conform to a new set of rules on carbon emissions relating to energy and industry; made by western rule-makers- which we argued back and forth.

And then the issues we analyse here took their present shape- economic growth, climate and planetary responsibility, strategic autonomy and energy sufficiency, making up the Quad of India’s dilemmas.

Energy Poverty

Energy Poverty is a critical component of India’s energy crisis and is not often spoken about. It is estimated that in the whole world, there are 1.3 billion people who rely on basic biomass-wood, crop wastes, charcoal, dung etc. for cooking or just to stay alive; about 250 million are in India (the number can go up to 300 to 400 million -when kerosene/LPG costs go up).

With 18 per cent of the world’s population, India consumes only 6 per cent of global primary energy. Targeted economic growth will raise this to at least 11 per cent by 2040, i.e., doubling India’s share of global consumption even while the rest of the world is also growing.

India will perhaps have the world’s largest population by the end of this year and will be 3rd largest economy by 2030. But our national economic growth target is to become a developed nation by 2047, which is something else. This goal requires many prerequisites like modern agriculture with less human load, a shift to manufacturing -possibly as a global hub and greater exports, advanced service sectors beyond IT, quality and affordable healthcare & education, modern infrastructure and efficient logistics- which translate into “Energy, Energy, Energy”, just as Lenin summarised the ambitious economic plans of the USSR in its early days as “Elektrifitzia, elektrifitzia!”

Adequacy of energy means that domestic energy production and use must expand more rapidly and with greater reliance on domestic resources than ever in our history. Simply put, Indians must use every available commercial energy source. This is necessary both in the domestic and the global contexts; the energy scene will become ever more challenging, with access to resources being a primary challenge in the context of both domestic and foreign policies.

The global context shifts from globalisation and offshoring of economies towards increased competition or conflict and a concomitant shift towards self-reliance and “friendshoring”. And energy is now a weapon of competition and perhaps war.

So, the domestic context has to change if we want Strategic Autonomy; or, more simply, to retain our independence of action based on national priorities.

Green Energy

On Climate Change, India has ceased to be on the defensive and has sought to be a leader. Under PM Modi and with industry and public leadership of civil society organisations, India has embarked on a truly worldclass expansion of green energy, signing on to the Paris Accords, setting Nationally Determined Contributions (NDCs) targets and creating the International Solar Alliance (ISA) etc.

First, the target for Renewable Energy (RE) was raised to 175 GW from 100GW (The current total power capacity is 360-400 GW). From 175 GW earlier, PM has now raised the target to 500 GW by 2030 – out of a likely total of 820 GW. This means almost tripling present production of RE, which today stands at 165 GW. (Solar 59, Wind 41, Hydro 50, Biomass/co-generation 10). The PM also committed India to achieve Net Zero Emissions (NZE) by 2070 and raised India’s ambition to be among the leaders of the Green Transition.

India can marry the self-sufficiency target to achieving Net Zero Emissions (NZE) by 2070 by speeding up solar (including solar thermal), wind power, and nuclear and natural gas. (Both of the latter must be included in clean, if not technically green, energy.) It will also of

RANJAN MATHAI Former Foreign Secretary of India.

need Energy Storage Systems (ESS), Electric Vehicle (EV) infrastructure, Hydrogen and synthetic fuels (including from biomass) for transport and the chemical industries.

These are massive opportunities for manufacturing industries of the future. But they will require massive investments, which is recognised, as well as newer and more affordable technologies, which is less recognised. And they will create new dependencies not only on items like solar panels, heliostats, and electrolysers but also critical minerals, metals for catalysts, rare earths, minor metals like tellurium, cadmium etc., which, if at all recognised, are not talked about.

The solar industry – basically solar Photovoltaics (mainly crystalline PVs-for power plants, and some solar thin film PVs), solar rooftop plants, etc.- has grown fast and can be considered a success story of scale and affordability.

India now has solar parks producing 2500 MW(2.5 GW) each, among the largest in the world. But the constraint is that the plants are based on imports of modules/panels etc., and the industry is now facing difficulties in the switch to self-reliance.

India is now learning that the constantly repeated story of the decline in solar electricity prices owes as much to Chinese mass production as to technological ad vancement.

Plentiful sunshine makes solar an obvious option for India. To be self-sus taining, the solar industry needs vertical integration like China-starting from processing polysilicon to making modules and panels and setting up the power plants using more Indian equipment. There is also a greater need for R&D on new materials like perovskites which can increase the efficiency of the solar conversion of panels etc. India can learn from the experience of Morocco, Spain etc in establishing large solar thermal plants (500MW) using concentrated heat/steam to drive turbines.

The Wind sector in India can grow, with a theoretical capacity of 300GW. Realistic capacity is a fraction of that because of space limitations, wind speed in suitable onshore locations, efficiency of turbines, and intermittency.

The industry needs domestic investment in materials for giant wind blades suitable for both onshore and offshore wind, as well as turbines and permanent magnets for high efficiency. Energy Storage Systems (ESS-mostly battery storage) are needed to deal with the problem of intermittency of solar and wind power. The issue has received policy attention, but the challenge undertaken by the National Mission for ESS is massive- to increase from 1 GWH capacity in 2019 to 33 GWH by 2032.

Evs

Transport is a major source of pollution in addition to carbon emissions. Ensuring a switchover from petrol/diesel to EVs is therefore vital for a sustainable Green Option. A few figures will illustrate the size of the challenge ahead of us. India has 1.3 million EVs, which is great, but we have 270 million vehicles of all types, i.e., penetration is less than 1 per cent if all forms of transport are considered. In the two-wheeler segment, EVs are now 5 per cent of new purchases, but our EV targets for 2030 are: 2/3 wheelers -70 per cent, buses -40 per cent, and cars -30 per cent.

According to one calculation, this level of penetration with current battery technology will require 500,000 charging stations; today there are approximately 2500 charging stations! And 65,000 petrol stations have been set up over the last seven decades. Looks like another long road ahead.

Growth of the 2/3-wheeler EV industry has been very rapid, but batteries are imported from China. We have a long way to go to build the necessary EV infrastructure, but this is one area where Govt-industry partnership is beginning to show results. But the battery story takes us from batteries to battery materials, i.e. critical minerals

Interlinkages With Critical Minerals

Critical minerals are essential for converting solar and wind energy into usable electricity because of their electronic, optical or magnetic properties.

China currently dominates the global market for the mining, processing and manufacturing industries of critical mineral industries needed for future energy requirements. (In the Solar energy sector, China’s manufacturing has grown from about 1-2 per cent of world capacity in 2000 to almost 80 per cent today; similarly, China dominates the production of EV batteries). The reason is that these processes, from mine to final product, are not just technically complex but dirty, polluting and energy intensive.

So, the world was, until now, happy to leave the dirty work to China; it is now waking up to a new risk as geopolitical tensions grow. India, in particular, cannot afford to be complacent about its dependence on China. Replacing dependence on the Gulf for oil, with dependence on China for newer energy requirements, is a national security hazard: whether it is for rare earths, products made from rare earth like permanent magnets, solar modules/panels, and even polysilicon etc. Vertical integration is needed to guarantee security and friendly foreign supply chains such as the ones initiated with Australia.

In 2019, a joint venture company namely Khanij Bidesh India Ltd. (KABIL) was set up with the participation of three Central Public Sector Enterprises, Na- tional Aluminium Company Ltd (NALCO), Hindustan Copper Ltd (HCL) and Mineral Exploration Company Ltd (MECL). The objective of constituting KABIL was to ensure a consistent supply of critical and strategic minerals to the Indian domestic market. Apart from making some desultory efforts in Latin America, KABIL has not achieved anything significant.

Exploration, mining, refining and processing of critical minerals in India are essential for the green transition. There are many critical minerals in which 3-4 countries dominate world output. OPEC’s monopoly or cartel will look weak compared to what a critical mineral monopoly could be.

Some minerals like rare earths have uses in defence, telecom etc., in addition to energy, and a supply squeeze would mean an economic and security crisis-not just an energy crisis, which is why President Trump regenerated the U.S. Strategic Mineral Stockpile in 2017.

Does the earth have enough of some minerals like platinum if a transition on the scale now envisaged takes place? (The OECD says production of the platinum group of minerals must increase by 150 times!) Perhaps there are technological alternatives to the minerals, but right now, whether research has viable answers is not available in the public domain. Most tech alternatives take years to pass the ‘Valley of Death’ before commercialisation; a process which could take decades.

Hydrogen

Hydrogen can be a real game changer among green energies with its uses for heat in industry, fuel cells for transport etc. In addition to the Govt’s National Green Hydrogen Mission, the private sector has ambitious plans to make India a world champion in Hydrogen production and affordability. But there are serious technical challenges before Hydrogen can be scaled up.

Green hydrogen producers find Proton Exchange (PEM) tech more suited to the intermittent green electricity supply, even though it uses costly, scarce metals like platinum, compared to the cheaper Alkaline Electrolysis technology. So, switching to grey or blue or green Hydrogen on a mass scale may need more R&D. This will not be easy to scale up quickly. A partnership with Japan would be useful.

Hydrogen is also explosive and needs to be handled with care. Risks should be recognised upfront, which is not seen in the media coverage.

BIOMASS /WASTE TO ENERGY

The use of ethanol for adding to petroleum is being actively promoted. But caution would be advised as using grains or sugar to extract ethanol is a food diversion at a time of hunger and is wasteful of water in a water-poor country. Using crop residues for biofuels or waste-to-energy is a better solution.

Still, it requires more advanced enzymes than are currently available or new gasification technology (like high-temperature plasma gasification-already being used- but must be made affordable). Otherwise, we will face more ‘NIMBY’ protests over waste-burning plants than at present. Work has just started on methanol, which is great, and like the waste-to- energy, it can solve

Grid Management

Grid management will be another real challenge once green energies take up a bigger share of electricity generation. It is universally recognised as a key, and ongoing challenge, which brings to fore the issue of baseload management and the continuing role of fossil fuels in meeting India’s requirements for at least three decades more -till 2047 or beyond.

Hydro And Nuclear Options

Hydropower capacity has grown from 2.5 GW at independence to over 50 GW today. But there is a huge social cost behind the success story. And maybe environmental costs too, which are yet to be calculated- but we have seen disasters in fragile Himalayan ecosystems. So, we will continue on this route, but we must move ahead cautiously on large hydro projects involving storage systems.

Nuclear power grew from 0 in 1947 to around 7000 MW in 2020. We can be proud of the creation of a Vertically Integrated full cycle created by Indian scientists/ engineers; and their advanced level of R&D for taking India on an independent path.

But more recently, despite promises after Indo-U.S. nuclear accord, growth has been slow because of cost factors, public apprehensions and problems created by our liability law. It may be recalled that in 2005 it was hoped to reach 20,000 MW by 2020.

Today Small Modular Reactors are being presented as the future. India has built nuclear plants with units producing 225 MW each, so the plans for making smaller plants of 100- 200 MW should be no big deal. The Modular element could be a game changer introducing time and cost efficiencies, and India should seek out partners who are implementing such models.

It must be stressed that nuclear is an optimal solution for reliable, large-scale, baseload electrical capacity in a post-coal era, as the French experience from 1970 to 2020 has shown. (And shows up the hypocrisy of the German ban on nuclear, as they bought French nuclear-generated electricity!)

India needs to step up its indigenous 700 MW reactors and find a publicly acceptable way to go beyond the great achievements of Indo-Russian collaboration and start planned projects with France and the USA. This will, however, require the import of enriched uranium, which can create dependencies; it may be noted that today everyone in the world is looking around for alternatives to Russia for nuclear fuel; India does not want to go down that path a few decades later!

Hence strategic autonomy requires going back to the long-term vision of Dr Bhabha’s three stages: First Pressurised Heavy Water Reactor (PHWR), second Fast Breeder Reactor (FBR) and third, the Thorium based

KUMAR NAIK, IAS

Additional chief secretary at the Energy Department, Govt of Karnataka

One of the important routes is to produce largescale hydrogen and export it by ship. So, if that were to happen, we need to have a green source of energy and transmission of this green source of energy to the place where the hydrogen is being produced, and mostly it would be along the coast.

Advanced Heavy Water Reactor (AHWRs).

Suppose we can get to stage 3 and use our vast domestic thorium reserves. In that case, we would have solved two energy challenges- energy availability and access, self-reliance and security! Affordability remains to be tested and requires speeding up the thorium programme. (there are also new Thorium-based reactors like the Molten Salt Thorium SMRs being built).

Fusion energy is for the distant future. India has only has a small experimental programme, but it has been included in ITER (the International Thermonuclear Experimental Reactor), which plans to set up an operational magnetic fusion plant by 2035. As the Indian Ambassador in Paris I was privileged to interact with Indian teams setting up the facility in Cadarache, in southern France.

Future Of Fossil Fuels

Transitioning to Green may take 2-3 decades but ending the energy poverty of Indians cannot be delayed that long. Which means we have to increase energy output from fossil fuels now! Even with increased electrification and energy generated from renewables, our accelerating growth in energy use will increase coal, oil and gas requirements very substantively for at least the next 2-3 decades.

Coal is well known as the most polluting fossil fuel. But coal is the foundation of our power system, and any coal shortage will cause an economic crisis in the short term. India must invest massively in clean coal technologies. We also must find socially acceptable ways of mining enough coal in India rather than resorting to imports, as we have done, ever since political controversies and judicial intervention have slowed down the domestic coal mining industry over the last decade.

More emphasis has to be given to natural gas as the bridge fuel for reaching Green goals by 2040. (The U.S. lowered its emissions and passed on to China the Gold Medal of becoming No1 polluter of the world because it began the shale gas revolution from 2006-2015 and gas replaced coal).

The problem of lack of support for the exploration and production (E&P) of natural gas must be overcome, and a maximum possible increase in domestic gas production achieved. That alone can make gas more affordable and become the solution to increased access to LPG, CNG, city gas, cleaner electricity, and lower subsidies for fertilisers and food.

Oil is the economy’s lifeblood for all modes of transport, pharmaceuticals, chemicals for everyday life, petrol/heavy fuel, oil/aviation fuel for the defence forces and national security. (Green activists have not yet got viable alternative feedstock for paracetamol!).

And we should never forget that diesel generators are the standby for all electrical shortages/emergencies in India and literally keep us alive.

(It is estimated that private users have put 90 GW of diesel generators in place- almost equal to solar and wind power capacity combined). Studies by the International Energy Agency (IEA) in 2020 showed that even in best-case scenarios for energy transition, in 2040, India will consume even more oil than the 5 million barrels per day that we presently use.

Should we risk continuing to be over 85 per cent dependent on foreign crude oil suppliers for our defence needs when facing two enemies on our borders? What if another crisis leaves the Hormuz Straits closed for even a few weeks?

The current oil market turmoil in India reflects our failure to produce more oil since production peaked in 2010-11. The present Government started with the luxury of low oil prices from mid-2014 when prices crashedand much of its economic agenda was achieved by continuous petroleum tax increases, which now cannot be reversed without causing a serious fiscal crisis - close to 25 per cent of indirect taxes are from petroleum.

The oil import bill will now soar higher than the $130 billion of last year, and there will be an increased trade deficit (Current Account Deficit is reaching a high of 4.6 per cent of GDP) and pressure on the rupee.

Other countries are lecturing us about buying Russian oil, and remember, the entire world will soon depend on a handful of suppliers if the Greens stop investments in the West, and by International Oil Companies elsewhere in the world.

Strategic autonomy as a goal will need a step up in the domestic production of crude oil. We must also expand our strategic reserves to at least three months’ requirements from the present three weeks.

The domestic oil and gas production sector face critical challenges of extraordinary taxation (e.g., service tax on royalty) and regulation. Strangely, importing oil is easy from the standpoint of regulatory controls and tax burden, but producing oil in the country is full of rules and taxes! Why this persists leads to questions difficult to answer; but the relentless decline in domestic oil production over the last 10 years points to abject failure of government policy.

Role Of Public Leadership

Public leadership of energy cannot- in the 21st century – be left to political leadership. The Govt obviously has the first role- to provide laws, regulations etc., to make India a developed nation with adequate energy as the sine qua non.

While India has made the Green Option the primary goal with new vigour, we must remember we are in 2-3 decades of transition and must get energy from every source. And civil society, including Think Tanks like Synergia, have a role in getting public support for the

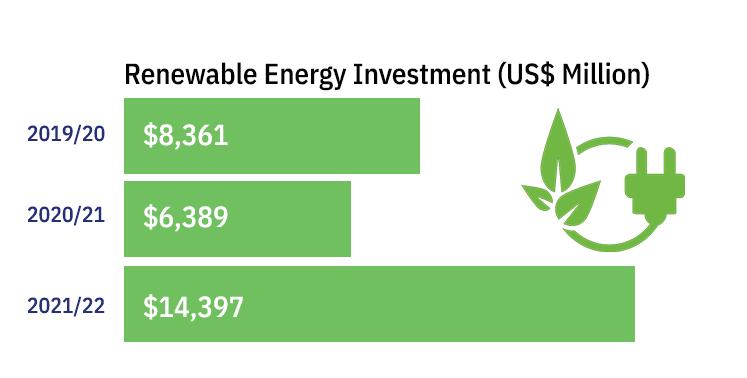

RENEWABLE ENERGY INVESTMENT SINCE FY2019/20

compromises necessary for energy production and distribution, access and affordability. The industry has a greater responsibility; to implement best-in-class practices for minimising environmental impact and making local communities’ stakeholders.

The E&P of natural resources- whether lithium for green batteries or oil- must start with an “end of mine” plan, which requires producers to work ahead on reducing the environmental impact of their operations and restoration of the mined areas. But mining cannot remain a synonym for quasi-criminal activity in popular perception.

Conclusion

The world has to act on the belated recognition that saving the planet through the Green Option can work ONLY based on climate equity and justice in sharing the remaining carbon space left for the planet before 2050. The latest IPCC report still leaves India way behind (20-25 per cent of the West’s GDP/energy consumption per capita) to keep the planet at 1.5C higher than pre-industrial levels.

The Indian Prime Minister has promoted the concept of LIFE- Lifestyle for Environment as the principle for the world to live attuned to the environment: But I think we have to be blunter- who created the mess we find ourselves in? And how do we end our poverty? Our insistence on Common but Differentiated Responsibilities goes back a long way- reread the script of PM Mrs Indira Gandhi at the very first UN/International Conference on the Human Environment -1972 Stockholm. ( She was one of only two Heads of State/Govt who cared enough to attend; the other was Sweden’s PM- the host!).

It is from there that economic/social development was deemed a co-equal pillar of the Human Environment and poverty deemed one of the worst forms of pollution-albeit not of carbon emissions.

Can we implement drastic energy reform at home and get a new global compact on technology and resource management for a new Green Era? This is a saga that is still unfolding. But for India it is important to recall Barack Obama’s words: “A nation that can’t control its energy sources can’t control its future”.

EXCLUSIVE CONVERSATION WITH MAURICE GOURDAULT -MONTAGE

SMALL MODULAR REACTORS (SMRS) AS THE WAY FORWARD?

Considering the necessity of increasing power generation and handling the climate change issue with more nuclear power in the energy mix, the SMR appears to be the “smart” and “small” solution. It represents a turning point for the nuclear sector. Being amongst the few countries which have been running nuclear power plants for decades, India has proved its skills in the field of engineering. It already has all the capabilities to manage the whole industrial process of building big nuclear plants mastering all the liabilities. This is to be seen in building six EPR plants of 1100 MW each in Jaitapur (Maharashtra) in cooperation with French EDF following the “make in India” concept. These six plants will cover the power requirements of about 70 million people.

Now the SMR with a production capacity from about 30 MW up to 300 MW represents the next step on which many countries are trying to develop a prototype. If the development costs are still high, waste treatment is less, and building delays are shorter. So far, only two countries have commissioned SMRs with their technology - Russia with a floating SMR and China. Some other countries like the U.S. with the Japanese Hitachi, France, the UK, Romania and Canada are developing their own projects. India, as the Government has announced it, is in the capacity to build its own SMR in the future. As for every country, it is a matter of in-

Future Of Fusion Energy In Practical Terms

Fusion has been a dream for the last 50 years. During the cold war, the U.S. and Russia were allocating significant amounts to the development of fusion. The main advantage is that this way of generating power is completely clean, with no carbon emissions or nuclear waste. Indeed, the U.S. has recently achieved an important step forward: a research laboratory has announced that the produced energy was more than the energy consumed during the experiment.

But nuclear fusion is a long quest. It will still take many years to replicate what is seen as the equivalent of solar energy. With ITER as the international venture based in the south of France and using a civil nuclear research Tokamak reactor, one carries out peaceful cooperation gathering 35 countries, including the U.S., India, China, Japan, and Russia. ITER, by its size, has been compared to the Apollo project. The first plasma pro duction should take place in 2030.

Then a second research reactor will be needed before production. The reality is that some more years will be needed and that one is still far from commercial

MAURICE GOURDAULT-MONTAGNE

Former adviser to President Jacques Chirac and Principle Coordinator for the Nuclear deal with India

On Maintaining Strategic Autonomy In Energy Security

We are in a new age of great competition by superpowers. The Russian invasion of Ukraine pushed the world into the first truly global energy crisis: 1973 was only an Oil Shock, but now Oil, Gas, Coal, and electricity prices are skyrocketing unprecedentedly. Governments’ commitment towards carbon neutrality does complicate the situation.

Security of energy supply basically rises in diversification. The lowest-hanging fruit is energy efficiency and conservation. Then comes diversifying energy sources with diversified origins and transportation methods. Countries are taking different approaches due to their different resource availabilities. Many countries enhance energy security by accelerating decarbonisation using indigenous renewable energy sources. Governments’ active intervention under the name of green industrial policies is replacing liberal and open market-based trade systems.

There are Winners and Losers. EU will be a winner if the REPowerEU plan succeeds and Carbon Border Adjustment Measures be enforced. The U.S. will be a winner. Fatih Birol said that Inflation Reduction Act is the single most important energy and climate action by any country since the Paris Accord in 2015. China is trying to be a Renewable Superpower as a major player in the supply chain of the low carbon economy. Saudi Arabia may avoid stranded-assetization of oil and gas if it invests in CCUS and blue Hydrogen. ASEAN needs an af- fordable and sustainable transition with LNG, H2 and CCS. Rus- sia seems least prepared for the climate shock. West - ern Sanctions on technolo - gy, self-withdrawal of invest- ment, expanding military expenditures, and increasing brain drain may hurt its ability to adapt. India can be a winner if enough investment happens to extend the use of solar and Hydrogen.

For Japan, probably the most important but difficult test to be a winner may be if nuclear power gets public trust back. PM Kishida’s chairmanship at G7 Hiroshima summit may trigger retaliation by Putin to stop the LNG supply from Sakhalin. Can Japan restart nuclear reactors before the summit? Who knows.

HYDROGEN FOR THE GREEN FUTURE?

In the race for decarbonisation, Clean Hydrogen will be a solution for hard-to-abate sectors in emerging economies where heavy industrial infrastructure is still young relative to developed countries. To make this game-change, we need to scale up the demand and cost reduction for clean Hydrogen. Japan started importing Liquid Natural Gas (LNG) 50 years ago from Alaska and, since then, commoditising LNG and enabling its golden age. Japan is trying to do the same for Hydrogen by introducing three ways of transporting Hydrogen: Liquified Hydrogen, MCH (Methylcyclohexane) and Ammonia. We don’t know which method prevails, but ammonia seems to lead the race with JERA’s co-firing clean ammonia at its coal thermal power plant. This can be a model for Asian countries that continue to use coal or gas-firing power plants for now.

With its huge potential for solar power,, India may have a different option. Solar electricity has become cheaper and generates affordable Hydrogen by large-scale electrolysis, then transported to industries through a dedicated pipeline. The distance of transportation by pipeline is much shorter than oversea transportation by liquified Hydrogen or MCH; thus, the cost would be affordable. Clean Hydrogen can be used to generate electric power as peak load electricity and as a backup for volatile solar or wind, low carbon transportation by commercial FCV fleet and clean fuel for heat in heavy industries. To make this happen in a timely manner, government intervention in deploying the hydrogen market with carbon pricing is essential. Investment by private sectors would happen only when government signals provide certainty of future prices. Predictability by direct deployment policy becomes more essential than R&D support measures.

NOBUO TANAKA Executive Director of the International Energy Agency