Program awarding mortgage-free homes to veterans

Non-profit has a home in Riverview Gardens open for applications

American staff

Operation Homefront is looking to award a mortgage-free home to veterans and their families in the St. Louis area. The homes will be awarded through the Homes on the Homefront program.

Right now the national non-profit has a home in the Riverview Gardens area that is open for applications.

Operation Homefront is looking for a veteran or military family from any era, with connections to the community, and meets the requirements listed on the

Homes on the Homefront website.

To date, the Homes on the Homefront program has handed over the keys to 108 mortgage-free homes across the nation, and has almost 100 more families currently in the process of moving into their new homes. Operation Homefront has already matched homes for three other families in the state of Missouri, and is thrilled for the opportunity to add another In Missouri specifically, already awarded three mortgage-free homes.

“It’s always an amazing feeling to award a mortgage-free home to a

veteran,” said Paula Pettibone, Director, Homes on the Homefront. “I am very excited to be involved in such an incredible program, and am even more excited to award a home in my hometown!”

The home application process will close soon, so get your applications in quickly. For more information on the Homes on the Homefront program, eligibility requirements, or to apply for this home, log on to www.HomesOnTheHomefront. net. If you have any questions about this program before you apply, please contact us at 210-659-7756.

HOME GUIDE

STAFF

Donald M. SuggsPublisher & Executive Editor

Kevin Jones - Sr. Vice Pres. & COO

Dina M. Suggs - Sr. Vice Pres.

Nathan B. Young (1894 -1993) - Founder

N.A. Sweets (1901-1988) - Publisher Emeritus

Bennie G. Rodgers - (1914 - 2000) Executive Editor Emeritus Melba Sweets (1909 - 2006) Editor Emeritus

Editorial

Chris King - Managing Editor

Kenya Vaughn - Website Editor

Earl Austin Jr. - Sports Editor

Sandra Jordan - Health Reporter

Rebecca S. Rivas - Staff Reporter

Bridjes O’Neil - Reporter Wiley Price - Photojournalist

Denise Hooks -Anderson, M.D.Health Editor

Dana G. RandolphContributing Editor

Fred Sweets - Contributing Editor

Sales / Marketing

Onye Hollomon- Sr. Acct. Exec.

Barbara Sills - Sr. Acct. Exec.

Pam Simmons- Sr. Acct. Exec.

Nevida Medina - Classified Ad Mgr

Angelita F. Jackson - Graphic Artist

Production

Mike Terhaar - Art Director

Melvin Moore - Graphic Designer

Administration

Robin Britt - Controller

Cathy Sewell - NIE Manager

Ishmael Sistrunk - Web/IT/Promotions

Coordinator

Kate Daniel - Exec Assistant

Loistine McGhee - Acct. Assistant

Mary Winbush - Receptionist

With the right mortgage, home ownership builds wealth

Research supports conventional wisdom of owning a home

– with responsible mortgages

By Katie Stalter

The Great Recession, characterized by devastating mortgage defaults, has challenged the conventional wisdom that home ownership is a good investment, particularly for those with low and moderate incomes.

But the conventional wisdom on the benefits of owning vs. renting still holds when done right, according to a newly published study led by the Brown School’s Center for Social Development (CSD) at Washington University in St. Louis.

Homeowners with low and moderate incomes who participated in this study conducted between 2005-08 achieved higher net worth than their counterparts who rent.

“This research provides new and important evidence for the current policy debate on low-income homeownership programs,” says Michal Grinstein-Weiss, PhD, associate director of the CSD and associate professor at the Brown School.

The research, published in April in the journal Housing Policy Debate, documents a study measuring the impact of sustained homeownership on net worth. The study uses data from the Community Advantage Program, which awarded prime mortgages to those who otherwise would only qualify for subprime mortgages.

The Community Advantage Program is made possible through a partnership between the Center for Community Capital at the University of North Carolina at Chapel Hill (a leading research and policy organization), Self-Help (a leading Community Development Financial Institution), the Ford Foundation, and Fannie Mae.

Grinstein-Weiss led a team of researchers who examined data from those who received these prime mortgages, as well as a group of renters in the same income bracket. Her team – Clinton

Key and Shenyang Guo, PhD, of the University of North Carolina; Yeong Hun Yeo, PhD, of Jeonbuk National University in the Republic of Korea; and Krista Holub of the CSD – found evidence that low- and moderate-income homeowners experience greater short-run increases in net worth, assets and nonhousing net worth than renters do.

“Our findings do not argue that all homeownership is beneficial, but rather that low-income homeowners with mortgages that are carefully underwritten with responsible terms, including low upfront costs and low interest rates –or what we like to call ‘responsible mortgages’ – can experience increased financial security and independence,” Grinstein-Weiss says.

The article points to skepticism that, although home equity represents a large amount of total wealth among the middle-class, potential benefits to low- and moderate-income homeowners are questionable due to challenging mortgage terms and lower home value and appreciation rate.

Grinstein-Weiss’ study addresses this skepticism by examining homeowners in

this income bracket who have received “responsible mortgages” and comparing effects with a set of renters.

The study explores changes in five outcomes over a three-year period (2005-08): Total net worth, total assets, total debts, total liquid assets and total non-housing net worth. Over the three years, the homeowners in the study gained an average of $15,000 in total net worth, while the renters gained less than $11,000. Homeowners increased their total assets by $20,000 and total debt by $5,000, and those figures for renters were $15,000 and $4,500, respectively. Homeowners also showed greater increases in total liquid assets and total non-housing net worth, amounting to $3,660 and $3,036 higher, respectively, than renters’ increases.

These findings are particularly noteworthy because the period of the study coincides with the Great Recession. Low- and moderate-income households were most affected by the housing market downturn, however those involved with this study saw gains in net worth, indicating that homeownership may be “a pathway to asset security,” as

Grinstein-Weiss puts it.

“Whereas paying rent guarantees a place to sleep, paying a monthly mortgage eliminates a portion of the principal of the loan, reducing debt and potentially increasing net worth,” she says.

A key element of the findings lies within the loan itself. The data shows evidence that a low-cost, low-interest mortgage can help households in the lowand moderate-income bracket build assets.

“Policymakers should note the loan characteristics offered by the program and consider policies that increase the number of quality affordable loan products on the market, particularly in low- and moderateincome communities,” Grinstein-Weiss says.

This study demonstrates that, with the right type of loan, even those with relatively few assets can begin to build their wealth. The security that comes from this increase in wealth may have great future bearing on these households’ ability to weather an unexpected major expense or loss of income.

This reaffirms that homeownership is a path that can lead to economic security.

Must-have homeowner insurance

By Jason Alderman

Many people adopt a “penny wise, pound foolish” mentality when it comes to buying insurance. When trying to lower expenses, some will drop or reduce needed coverage, gambling that they won’t become seriously ill, suffer a car accident or fall victim to a fire or other catastrophe. But all it takes is one serious uncovered (or under-covered) incident to potentially wipe you out financially.

Here are insurance policies no household should be without:

Homeowner/renter. Faulty plumbing, theft and home-accident lawsuits are only a few catastrophes that could leave you without possessions or homeless. A few tips:

• “Actual cash value” coverage repairs or replaces belongings, minus the deductible and depreciation, whereas “replacement cost” coverage replaces items in today’s dollars. Depreciation can significantly lower values, so replacement coverage is probably worth the

extra expense.

• Jewelry, art, computers and luxury items usually require additional coverage.

• Review coverage periodically to adjust for inflation, home improvements, new possessions, change in marital/family status, etc.

• The market is competitive, so compare your rate with other insurance carriers. Get “apples to apples” quotes since policies may have varying provisions.

Medical. This is the most critical –and unfortunately, the most expensive – coverage you need. When comparing plans, consider:

• Are your doctors in their provider networks? If not, can you afford out-of-network charges – or are you willing to find new doctors?

• Are your medications covered under the plan’s drug formularies?

• Do they restrict specialized

services you might need like maternity, mental health or weight reduction treatments?

• If you choose catastrophic coverage to lower premiums, can you afford the high deductible in case of an accident or major illness?

Vehicle. You probably can’t even get a

Insurance Continued...

driver’s license without demonstrating proof of insurance. Consider these coverage options:

• “Liability” pays if you cause an accident that injures others or damages their car or property.

• “Uninsured motorist” pays for damage caused to you or your car by an uninsured motorist.

• “Collision” pays for damage to your car resulting from a collision and “comprehensive” pays for damage caused by things like theft, vandalism and fire. However, they only pay up to the actual cash value (ACV) minus deductibles. Because the ACV for older cars is low, repairs often cost more than the car is worth.

• Common ways to lower premiums include: Raising deductibles; discounts for good drivers, exceeding age 55 or installing security systems; comparison shopping; and buying homeowner and car insurance from the same carrier.

Life insurance. If you’re single with

no dependents, you may get by with minimal or no life insurance. But if your family depends on your income, experts recommend buying coverage worth at least five to 10 times annual pay. Other considerations:

• Many employers offer life insurance, but if you’re young and healthy you may be able to get a better deal on your own.

• After your kids are grown you may be able to lower your coverage; although carefully consider your spouse’s retirement needs.

• You probably don’t need life insurance on your children, but you might want spousal coverage if you depend on each other’s income.

• If your divorce settlement includes alimony and/or child support, buy life insurance on the person paying it, naming the receiving ex-spouse as beneficiary.

Don’t gamble your future financial stability by passing on vital insurance coverage – the odds aren’t in your favor.

Jason Alderman directs Visa’s financial education programs. To Follow Jason Alderman on Twitter: www.twitter.com/PracticalMoney.

Buying in the county

St. Louis County Homebuyer Assistance Programs

American staff

With interest rates at record lows and special homebuyer programs available through St. Louis County’s Office of Community Development now may be the time to buy a home. Why rent if you can own a beautiful- almost like new home- and have a house payment probably less than your current rent payment?

If you are looking to buy a home in North County, have at least $1,000 to invest, and average-to-good credit, take advantage of this limited-time opportunity. St. Louis County has several programs available that will provide, to qualified purchasers, $5,000-$15,000+ towards down payment and closing costs. Current home sale prices range from about $55,000 - $100,000, and total monthly house payments range from about $450 to $750 (subject to changes in interest rates and program qualifications). Based on current home prices, minimum income required starts at approximately $16,500 (maximum

income limits do apply).

Currently there are about 10, extensively renovated, homes available to purchase through these programs. Typical home improvements, which will vary per home, include: new roofs, siding, windows, high-efficiency heating and air conditioning systems, updated electric and plumbing, new appliances, beautiful new kitchens and baths, hardwood floors, carpeting, ceramic tile, 6-panel doors, ceiling fans, and much more. Plus, receive an additional $7,500 in homebuyer assistance through the Hometown Hero’s Program. This program is available for these homes if you are now, or a retired: police officer, firefighter, active military or veteran, primary and secondary teacher, nurse, EMT, or certified medical technicians. For additional information, to view photos, and to start the easy process to becoming a homeowner, please visit: www.StLouisCo.com and look for the “Properties for Sale” in the lower right section of the homepage; or contact Adam Roberts at 314-615-4427.

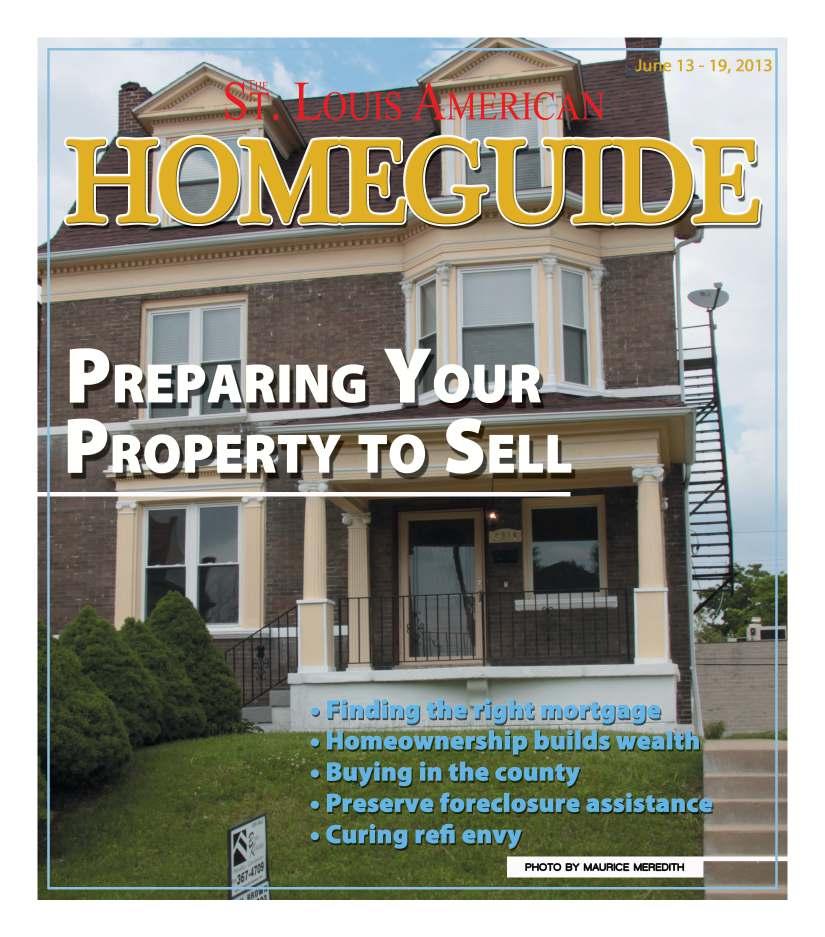

Did you know…? Professionally staged homes sell faster!

It’s a fact: homes that are well staged sell at a higher price in a shorter period of time. If you’re looking to sell your home, it’s time to get it prepared for showing.

A perfect example of a home that’s ready to sell is located 4315 Washington in the Central West End (pictured on the cover). Stop by Sunday, June 23 from 2 to 4 p.m. for the Open House. This wonderfully restored turn-of-the- century home features a grand entry foyer with a fireplace, 5 spacious bedrooms, 3.5 baths, and an additional 1st floor room that could be used as a library, family room or office. The must-see kitchen features granite countertops, custom cabinetry, marble tile floors, and stainless steel appliances. The master bedroom suite is fitted with a fireplace, wet bar, and luxury bath, which includes a jet tub and

separate shower. Beautiful hardwood floors are featured throughout the first floor of this home that’s priced to sell at $360,000. A lender will be available to provide useful information to buyers on financing this dream home.

In addition to viewing the CWE property for inspiration, here are a few tips for getting your home “market-ready” to sell faster:

1. Paint and trim – Create curb appeal with neatly trimmed lawns, hedges and bushes. Make a great first impression by painting wood trim and gutters. The front door, porch and walkway should be clean and welcoming. A bit of landscaping, paint and tidying can go a long way towards creating a “wow effect” enticing potential buyers to want to see the inside.

2. Clean and de-clutter the interior – Less is more and fresh is best! With clutter and excess furniture removed, the buyer can move around with ease. When buyers enter, you want the home to look and smell fresh.

3. Neutralize and de-personalize – Paint rooms a neutral color. We all have our

preferences and in many cases they should remain our preferences. Remove personal pictures and keepsakes. The buyer should make a connection and envision creating happy experiences in the house.

4. Restore and repair – Make sure heating and cooling systems are working

properly. Most buyers will get a building inspection to check all major systems. Costly repairs that come up once the property is under contract could kill the deal.

5. Price your home to sell – Even a well staged home has to be competitively priced in order to sell.

For professional staging, pricing your home to sell or finding your next home, contact Brown-Kortkamp at (314) 367.2899 or infor@brownkortkamp.com. To view current listings or for more info on our real estate brokerage; residential and commercial moving & storage; insurance; land acquisition and relocation services visit www.brownkortkamp.com.

A perfect example of a home that’s ready to sell is located 4315 Washington in the Central West End (pictured on the cover). Stop by Sunday, June 23 from 2 to 4 p.m. for the Open House.

Photos by Maurice Meredith

Curing refi envy

Calculate before you cry over fixed mortgage rates

By Michelle Singeltary Washington Post

Do you have refinance envy?

Come on, you can admit it. You’ve been at an event or to church or having lunch with co-workers and someone brags about the interest rate she just got when refinancing her mortgage. You stay silent, grieving that you can’t take advantage of the low interest rates for mortgages.

You grumble when you read news stories like this one from The Associated Press on April 18: “Average U.S. rates on fixed mortgages fell closer this week to their historic lows, making homeownership more affordable and refinancing more attractive. ... The average rate for the 30-year fixed loan dipped to 3.41 percent from 3.43 percent last week. That’s not far from the 3.31 percent rate reached in November, which was the lowest on records dating back to 1971.”

loan term and your effective interest rate as a result of making extra payments. The LowerRate calculator can be used if you want to aim for a specific interest rate.

“If you can’t refinance your mortgage but can afford to pay some additional money each month, that prepayment might save you as much as an actual refinance,” said Keith Gumbinger, vice president of HSH.com.

Gumbinger said he got the idea for the calculators because he was contemplating whether he should refinance his own mortgage. But he’s so far along in paying the mortgage down and the amount is so small, he wondered if it was worth the time and cost of refinancing.

Michelle Singletary

The rate for 15-year fixed mortgage was 2.64 percent, not far from the record low of 2.63 percent posted last November.

As mortgage rates fall, people are rushing to refinance. But what if you can’t refinance because you don’t qualify or your home is worth less than what you owe, meaning you are underwater? Or maybe you are 15 or 20 years into a 30-year mortgage and you don’t want to stretch the payments out again. Still, you can’t stand it that you are stuck at a 5 percent or 6 percent interest rate.

But there is a way to cut the amount you’ll pay in mortgage interest to achieve savings as if you refinanced. HSH.com, which publishes mortgage and consumer loan information, has created two calculators for homeowners who are unable to refinance at today’s low interest rates.

The company’s “PreFi” and “LowerRate” calculators help homeowners figure out how to attain a lower effective mortgage interest rate through prepaying their mortgage principal.

The PreFi calculator will help if you have a specific dollar amount available for prepayment each month. It calculates your interest savings over the remaining

“It’s hard to achieve measurable savings when you are in my situation and not interested in restarting the mortgage,” he said. Let’s say you took out a $200,000 mortgage two years ago at 4.5 percent, which was the average 30-year fixed rate in mid June 2011. You have an extra $200 a month you could apply to the mortgage principal. Without prepayment, you will pay off your loan in 337 months (28.08 years). Total amount of interest you’ll pay: $147,819.88. With prepayment, you will pay off your loan in 244 months (20.33 years). Total amount of interest you’ll pay: $102,216.80. Your effective interest rate over those 244 months: 3.843 percent. Here’s an example of how the LowerRate calculator works, using the same information. You want that 3.41 percent interest rate. So in the calculator, you would enter 3.41 to find out exactly how much extra you’ll need to pay each month.

To get the equivalent interest cost of a 3.41 percent refinance over a term of 28.08 years, you would have to prepay $167.10 every month -- or just a little over $2,000 a year.

If you are not well positioned financially – you’re not saving for retirement or college for your children, paying down other debts, such as credit cards – then prepaying your mortgage may not make sense, Gumbinger said. Still, try out the calculators and prepay on your principal. The next time someone is bragging about the lower interest rate they got, you won’t have to be envious.

Readers can write to Michelle Singletary c/o The Washington Post, 1150 15th St., N.W., Washington, D.C. 20071. Her email address is singletarym@ washpost.com. Follow her on Twitter (@ SingletaryM).