the companies in question and reproduced in good faith.

the companies in question and reproduced in good faith.

Welcome to Spotlight, a bonus report which is distributed eight times a year alongside your digital copy of Shares.

It provides small caps with a platform to tell their stories in their own words.

This edition is dedicated to businesses powering the global economy, whether that be in mining, oil and gas, the renewables space, infrastructure or energy provision.

The company profiles are written by the businesses themselves rather than by Shares journalists.

They pay a fee to get their message across to both existing shareholders and prospective investors.

These profiles are paid-for promotions and are not independent comment. As such, they cannot be considered unbiased. Equally, you are getting the inside track from the people who should best know the company and its strategy.

Some of the firms profiled in Spotlight will appear at our webinars and in-person events where you get to hear from management first hand.

Click here for details of upcoming events and how to register for free tickets.

Previous issues of Spotlight are available on our website

Members of staff may hold shares in some of the securities written about in this publication. This could create a conflict of interest.

Where such a conflict exists, it will be disclosed.

This publication contains information and ideas which are of interest to investors.

It does not provide advice in relation to investments or any other financial matters.

Comments in this publication must not be relied upon by readers when they make their investment decisions.

Investors who require advice should consult a properly qualified independent adviser. This publication, its staff and AJ Bell Media do not, under any circumstances, accept liability for losses suffered by readers as a result of their investment decisions.

Gold has continued its strong run since our January 2025 thematic note, pushing above $3,050/oz. We now argue that investors should shift focus to gold mining equities to maximise returns.

With Gold Fields’ recent bid for Gold Road Resources at a 28% premium, we believe a sector consolidation phase is beginning, offering compelling opportunities across the mining spectrum.

We explore a structured approach to gold equity investment, examining optimal timing within the cycle and offering a tiered strategy for portfolio construction across streamers, majors, mid-tiers, and selective juniors.

In January, we presented a three-pillar framework for understanding gold price movements.

Our analysis pointed to potential upside to $3,300–4,500/oz, with gold now having passed $3,050/oz.

This confirms our thesis that we are in the early stages of a major rebasing rather than approaching a peak, with parallels to the 1970s cycle when gold surged during the transition from negative to positive real rates.

Central bank buying has continued to provide structural support, with demand remaining above the long-term trend of 500 tonnes annually, contributing 7–10% to gold’s price performance. While gold has performed exceptionally well, our analysis now suggests

that the most compelling opportunities lie in the mining equities space.

Historical analysis demonstrates distinct waves in which rising gold prices flow through different segments of the market. Understanding this progression is crucial for timing investments and maximising returns in each phase of the cycle.

From our analysis of market performance since 2019, a clear pattern emerges:

1. Gold price appreciation: the initial phase of any bull market starts with the metal itself.

2. Major producers respond: after approximately nine months, large-cap miners begin to outperform.

3. Mid-tier producers follow: as major producer outperformance wanes, mid-tier producers accelerate.

4. Junior explorers’ surge: the final and often most explosive phase of outperformance is from the juniors. This differs from historical patterns of a generation ago, when juniors, mid-tiers and majors would move more in tandem.

Today’s more sequential progression allows investors to strategically rotate through the sector as the bull market matures.

Constructing an optimal precious metals portfolio requires balancing concentration for

maximum returns against diversification for risk management.

Gold itself should be considered the ‘riskfree’ asset within the precious metals space, providing a foundation upon which to build additional exposure through mining equities.

For investors already holding physical gold, a more concentrated approach to mining equities is appropriate.

Our analysis suggests that within a portfolio of 10 junior exploration stocks, holding just one to three positions may optimise returns without substantially increasing risk, as gold provides downside protection.

For investors without a gold position, we recommend greater diversification, with perhaps five junior positions or even full diversification across all 10 potential holdings. This approach acknowledges that losses at the portfolio’s weaker performers will likely be more than offset by gains from the strongest positions.

This risk-conscious approach can be proportionally applied to larger portfolios. For example, in a universe of 100 potential junior stocks, an investor with gold holdings might concentrate on 30 positions, while those without might opt for broader exposure.

Looking at performance since March 2019, gold has outperformed most mining indices over the full period. However, this masks significant periods of outperformance within specific segments.

HUI Gold Bugs Index and FT Gold Mines Index (representing major unhedged producers) were the first to respond to gold’s move in late 2019, with junior explorers (proxied by the S&P/ TSX Venture Composite) initially lagging but eventually delivering superior performance.

As we assess the current market positioning, with gold having sustained levels above $3,000/ oz, we believe investors should now be rotating capital towards the mining equities, with a particular focus on quality majors and select mid-tiers, while beginning to build positions in juniors ahead of their typical outperformance phase.

Streaming companies

For investors seeking their first exposure to the gold equities sector, streaming companies offer

an appealing entry point. While they typically command premium valuations compared to traditional miners, they provide significant advantages:

1. Reduced operational risk through diversified streaming agreements.

2. Limited exposure to capital expenditure overruns.

3. Geographic diversification across multiple mining jurisdictions.

4. Attractive dividend yields exceeding many majors.

5. Exposure to exploration upside without direct exploration costs.

Wheaton Precious Metals exemplifies this model, offering a combination of gold exposure, yield, and growth potential. While its current P/E ratio appears elevated compared to major producers, this reflects the market’s forward-looking assessment of production growth and its lower risk profile rather than overvaluation.

producers

When evaluating major gold producers, investors should look beyond simple P/E ratios to assess the relationship between quality (measured by historical earnings outperformance relative to gold) and current valuation metrics.

Our analysis of major producers from 2010–24 examines adjusted earnings per share outperformance versus gold price appreciation. Agnico Eagle Mines, for example, has delivered EPS (earnings per share) growth approximately 30% greater than gold’s price movement over this period, reflecting superior operational execution and capital allocation.

Written by analysts, Andrew Keen, Neil Shah, Lord Ashbourne at Edison

This is an excerpt from a report: From gold to gold miners: Extracting higher returns in the current bull run by Edison, first published in April 2025.

Other thematic reports are available at www.edisongroup.com/thematics

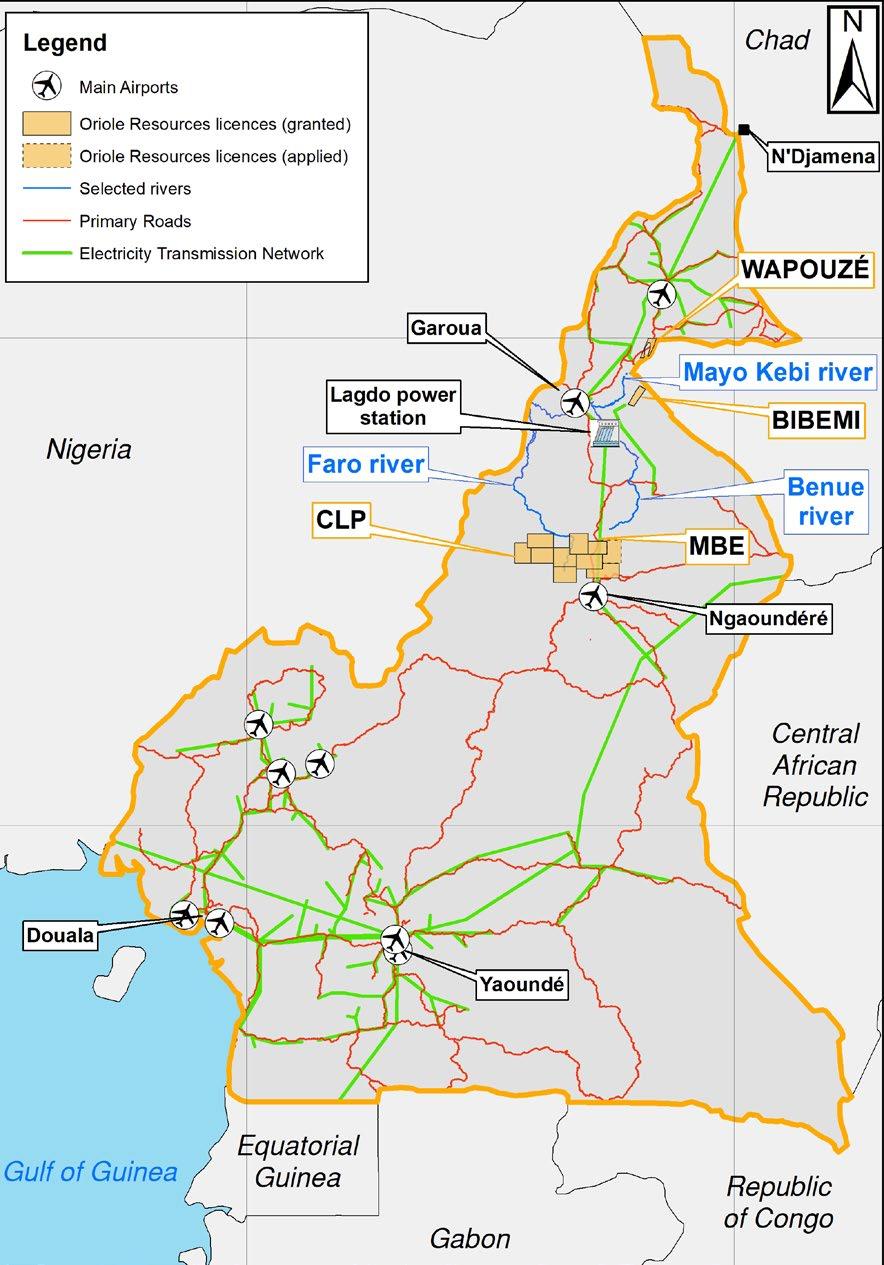

The success of Oriole Resources’ (ORR:AIM) systematic but efficient approach to exploration is shown by the progress at its two main gold projects in Cameroon, Central Africa.

Within two years of the first drill hole at the Bibemi project in northern Cameroon, Oriole published Cameroon’s first JORC Compliant Mineral Resource Estimate (MRE) for gold.

While rapidly progressing the Bibemi project, Oriole also expanded its operations into central Cameroon with the acquisition of a contiguous licence package covering more than 4,000km2 of highly prospective ground.

Within this licence package, the Mbe project became Oriole’s flagship, and has been rapidly advanced over the last four years, from a greenfield site to a maiden drilling programme that is already revealing the potential to host a multi-million-ounce deposit.

Oriole’s exploration at these two projects has ramped up significantly since January 2024, following the signing of earn-in agreements with Ghana-based BCM International which is funding up to $8 million in total exploration expenditure, split equally across the two licences.

Initial systematic surface exploration has delivered excellent results, with two priority targets identified for follow-up. The southernmost target, MB01-S, is currently the subject of a 6,590 metres maiden diamond drilling programme that is approximately 70% complete.

Results from the first ~3,500 metres of drilling have been impressive, delivering best intersections of 86.50 metres at 1.36g/t gold,

21.30 metres at 1.61g/t gold, 2.00 metres at 25.77g/t Au and 2.50 metres at 10.31g/t gold.

In fact, almost 200 mineralised intersections have been reported by the company to date, equating to one gold intersection for every 18.5 metres drilled.

The Mbe system has been proven over a strike length of 200 metres, up to 400 metres width, and to at least 290 metres vertical depth; it remains open at depth and along strike.

Exploration to date has demonstrated the potential for narrower high-grade zones within wider envelopes of lower grade gold mineralisation.

Oriole has recently completed a Phase 5 drilling programme, increasing the total drilling to over 13,000 metres across the project.

Since the maiden drilling programme in 2018, much of the drilling has focused on the ~1kmlong BZ1-MRE zone within the Bakassi Zone 1 prospect, where the company has defined a MRE of 460,000 ounces contained gold in the JORC Indicated and Inferred categories.

Outside of the MRE, an additional JORC Compliant Exploration Target has been defined at between 145,000 and 400,000 ounces

contained gold, which covers a further three prospects and highlights the upside potential within the licence area.

Oriole’s flagship Mbe project is located within one of nine contiguous licences forming the CLP (Central Licence Package).

Regional-scale exploration has been conducted across the five eastern licences (inclusive of Mbe), with multiple kilometre-scale gold-in-soil anomalies identified within all licences. As such, the package has district-sale potential for further major gold discoveries.

Oriole’s other Cameroon asset, Wapouzé, has recently been renewed with a focus on assessing the economic potential for cementquality limestone that’s been identified within the licence.

A shift towards sourcing material in-country, and the proximity of Wapouzé to existing cement plants, means that the project should be attractive for industry partners and has the potential to deliver a royalty-based income from a commercial quarrying operation.

Oriole has a non-controlling beneficial ownership of the Senala project, Senegal, with a wholly owned subsidiary of Managem Group retaining the controlling ownership.

In 2021, it completed a JORC compliant MRE estimate for Faré South (one of three prospects at Faré) at 155,000 ounces contained gold.

Earlier this month, the company also published a JORC Exploration Target range, for material outside of the MRE, of 17 to 24 million

tonnes at a grade of 0.69 to 0.84g/t Au for 380,000oz to 650,000oz contained Au.

Discussions on the formation of a joint venture company are underway.

In addition to the Cameroon and Senegal operations, Oriole also retains interests and royalties in companies operating in East Africa and Turkey that could deliver future cash payments.

This year has the potential to be a significant one of achievement for Oriole. The maiden drilling programme at MB01-S is scheduled for completion in the third quarter, at which point Oriole anticipates preparing a maiden pit constrained JORC resource estimate for publication in the fourth quarter.

Later this year, the company also plans to start drilling at MB01-N, a second substantial target only 500 metres to the north of MB01-S that offers significant upside potential, and is targeting a multi-million-ounce, open pitable resource.

The company is also progressing the exploitation licence application for Bibemi, by conducting various technical studies, including an environmental and social impact assessment and economic studies during the iterative negotiation period of the application.