Middlemen Markups:

A Bitter Pill to Swallow

Self-insured employers are moving beyond average wholesale price to better assess PBM value and secure true price transparency

Get expert support to self-fund your healthcare.

As your business grows, so will your healthcare expenses. Customized captive insurance from QBE creates strength to self-fund your employee healthcare coverage, allowing you to increase transparency and reduce the cost of risk. The QBE Captive Curve® solution model removes barriers to entry and allows you to move easily to new strategies.

Take advantage of QBE’s Captive Curve solutions:

• Fronted policy that is “A+” rated by S&P for singleparent and group captive programs.

• Reinsurance placement covering direct writing captive insurers assuming medical stop loss (MSL) risk.

• Agora, an open MSL group captive that makes it more efficient to participate in a group program.

Together, we’ll find a solution so no matter what happens next, you can stay focused on your future.

By Bruce Shutan

By Laura Carabello

Middlemen Markups: A Bitter Pill to Swallow

Self-insured employers are moving beyond average wholesale price to better assess PBM value and secure true price transparency

Written By Bruce Shutan

SignificantSchange is afoot in the pharmacy benefits management space, where self-insured employers have struggled for decades to assess the true value of PBMs amid yeoman efforts to pull back the curtain on Rx price transparency.

Average wholesale price (AWP) and other metrics for gauging PBM effectiveness have become obsolete as the market shifts to transparent solutions and PBMs face mounting pressure from regulators and lawmakers, according to Zac Hanson, senior director of revenue operations for RxPreferred Benefits.

Offering a glimpse of just how frustrating of a measure AWP has been, Rx insiders will wryly say the acronym stands for “ain’t what you pay” largely because it’s a made-up number for generic drugs, quips Amy Ball, president of Innovative Rx Strategies.

Understanding a competitive AWP discount requires insight into how pharmacies buy drugs, what they’re paying, a PBM’s profit margin when engaged in spread pricing and the discount employers are getting, she says.

While AWP may be on its way to intinction, it was never appropriate in the first place, opines Jim Lodge, senior vice president of sales and chief transparency officer for TakeCareRx. “If it’s a brand drug, it’s probably going to be AWP minus 20%,” he says. “If it’s a generic drug, it’s going to be AWP minus 80% or 90%. But here’s the deal: AWP just makes up a discount to get the price that they want it to be.”

Over the years, he says PBMs have tried to make discounts look better by inflating ADP as manufacturers eventually pushed certain drugs to treat various condition. “In the late ’80s and early ’90s, more and more PBMs took rebates and considered them a reward for putting certain drugs on their formulary and doing therapeutic alternative programs” with pharmacists recommending scripts to doctors, he explains.

Having been accustomed to revenue generated from rebates, PBMs then started doing spread pricing to pocket the difference between what it pays the pharmacy and charges the employer. Moreover, big PBMs operate their own group purchasing organization or wholesaler that simply aggregate rebates and rely on bulk purchasing to secure better deals. In the embrace of this model, there has been a movement away from rebates.

But they’re keeping much of the money in the form of marketing or formulary management fees, Lodge reports. As a consultant in the Rx space, his goal is to ensure that 100% of rebates are paid back to the employer client.

(WAC) with nine different ways to determine the cost of drugs and reimbursements.

The trouble with WAC, though, is not every drug has a WAC price, Ball notes. She says NADAC pricing is based on survey data from about 400 pharmacies across the country that routinely report on their acquisition cost.

“If you’re a large pharmacy like a Walgreens or CVS, you probably have a lot better buying power than some of the 400 pharmacies or chain pharmacies that are reporting on NADAC,” she observes. “If you buy better than NADAC, you make money as a pharmacy. If you don’t buy better than NADAC, then you’re losing money.”

National average drug acquisition cost, known as NADAC, is a newer standard that the Federal Trade Commission is using for comparisons to uncover price gouging. Published in November 2013, an updated version was released in 2023. “When we did an analysis of it across our entire book of business, it was nothing but NADAC plus 3%,” Lodge recalls.

What his organization does that most others do not is something called actual acquisition cost, reimbursing the pharmacy based on what it paid for each drug, plus a $10.50 professional fee for counseling the patient, as well as paying the light bill and for their technology. While most organizations use AWP or NADAC, he says there’s also wholesale acquisition costs

NADAC’s intention is to get closer than AWP to a price point that doesn’t put a pharmacy underwater on some claims and then have higher profit on other claims, Ball notes. And while the goal is to reimburse pharmacies in a more appropriate way, she cautions that there’s a much higher dispensing fee with NADAC.

Another measure that’s rarely used because it requires individually contracting with retail networks at the client level involves direct contracts with a pharmacy based on their acquisition cost plus a markup, Ball says.

Amy Ball

Jim Lodge

Depend on Sun Life to help you manage risk and help your employees live healthier lives

By supporting people in the moments that matter, we can improve health outcomes and help employers manage costs.

For over 40 years, self-funded employers have trusted Sun Life to help them manage financial risk. But we know that behind every claim is a person facing a health challenge and we are ready to do more to help people navigate complicated healthcare decisions and achieve better health outcomes. Sun Life now offers care navigation and health advocacy services through Health Navigator, to help your employees and their families get the right care at the right time – and help you save money. Let us support you with innovative health and risk solutions for your business. It is time to rethink what you expect from your stop-loss partner.

Ask your Sun Life Stop-Loss Specialist about what is new at Sun Life.

For current financial ratings of underwriting companies by independent rating agencies, visit our corporate website at www.sunlife.com. For more information about Sun Life products, visit www.sunlife.com/us. Group stop-loss insurance policies are underwritten by Sun Life Assurance Company of Canada (Wellesley Hills, MA) in all states, except New York, under Policy Form Series 07-SL REV 7-12 and 22-SL. In New York, Group stop-loss insurance policies are underwritten by Sun Life and Health Insurance Company (U.S.) (Lansing, MI) under Policy Form Series 07-NYSL REV 7-12 and 22-NYSL. Policy offerings may not be available in all states and may vary due to state laws and regulations. Not approved for use in New Mexico.

© 2024 Sun Life Assurance Company of Canada, Wellesley Hills, MA 02481. All rights reserved. The Sun Life name and logo are registered trademarks of Sun Life Assurance Company of Canada. Visit us at www.sunlife.com/us.

BRAD-6503-z

#1293927791 02/24 (exp. 02/26)

Lodge predicts a bright future for the net-cost model, citing as an example of this approach in action Rightway Healthcare’s permember-per-month guarantee that net cost will not exceed a certain amount. If it does, then he says the transparent PBM’s stop-loss will activate inside the self-funded plan to reduce that medical spend.

As AWP contracts disappear and give way to an acquisition-based model, however, the incentive to purchase at the lowest acquisition price is lost, which drives up prices, explains Kerri Tanner, chief pharmacy officer with PayerAlly.

She notes several areas of potential risk with acquisition cost plus models and contracts with PBMs because they don’t typically have the same level of guarantee language, nor are they well-defined in the industry. They also may be internally developed and prone to shifts in costsharing because members are used to paying a very low amount for some of the cheaper generics that carry a higher price.

DISCOUNTING INFLATED PRICES

Whatever pricing model is used, the Big Six PBMs are pushing rebate guarantees and discounts, many of which are artificially inflated through their pricing methodology, threatening employers’ ability to control costs, Hanson notes. These players include CVS Caremark, Express Scripts, OptumRx, Humana, Prime Therapeutics and MedImpact Healthcare Systems, with the top three controlling nearly 80% of the market.

With a spread-pricing model that lacks transparency, he says employers have no way of knowing how much they’re being overcharged. These practices, of course, are detrimental to both selfinsured employers and their health plan members and have led to litigation (more on that later).

“They can charge whatever they want for a drug, reimburse the pharmacy a set amount and charge the employer a higher amount,” Hanson explains. “Meanwhile, the plan has no control over whether it’s being overcharged and or the ability to track performance effectively.”

When legacy PBMs are incentivized with high rebate guarantees or by retaining rebates, he says it positions them to prefer higher-cost medications to retain more profit. Employers can avoid this perverse model of misaligned incentives by partnering with a transparent, passthrough PBM that is independent of an insurance carrier and doesn’t own pharmacies – unlike the vertically integrated model that has dominated the U.S. healthcare system.

"They need to understand that their PBM will prioritize true drug costs over discounts and rebates, allowing them to use their data to identify areas of opportunity for the plan while ensuring that the PBM's philosophy and processes align with plan goals," he observes. "Every plan needs to have access to claim-level detail when it comes to all claims and rebate payments."

Independent pharmacies are losing significant amounts of money on a number of drugs because their reimbursement is far below the actual cost to them, and therefore, they no longer can afford to carry those scripts, Lodge explains, noting how patients are instead referred to large drugstore chains to purchase them.

With some drugs costing as much as $20,000 to $30,000 a month, he says even if reimbursement is $5,000, they’re still taking a terrible beating every time they fill that drug. He compares this dilemma to car dealerships covering their profit margins after selling vehicles below the manufacturer’s suggested retail price.

Kerri Tanner

These market challenges have caught the attention of Optum Rx, a Big Three PBM that recently announced it is shifting to a cost-based model to better align with the costs pharmacies face based on drug manufacturer pricing. The move, which will be fully implemented by January 2028, was initiated to help support more than 24,000 independent and community pharmacies the PBM works with, along with its members.

AUDITING PBM CONTRACTS

Given how PBMs represent one of an employer’s largest vendors and areas of risk, Tanner suggests it’s important to audit PBM contracts on an annual basis. She says there are typically changes in PBM contracts from one year to the next that go undetected, involving clinical rules being coded or priorauthorization rules not being put in place, as well as drugs moving on and off a formulary. The result may be that an employer pays for drugs it didn't intend to pay for, she says, adding that PBMs must be held accountable for not following their contractual terms.

Standard audits will examine business practices that are creating risk, as well as compare the output of claims activity to clinical rules and contractual obligations. A comprehensive PBM audit would include not only a financial component that examines rebate guarantees, plan design and cost-shares, but also a clinical rules validation involving adhering to prior authorization or monthly formulary updates, Tanner says.

Your Trusted Navigator to Better Benefits Solutions

"Typically, the errors that we see in the audit of PBM contracts fall into a few different categories," she reports. They include not reporting on rebate guarantees, failing to abide by a new amendment that was signed or updating pricing in year-over-year changes.

Another involves offsetting values when it comes to meeting a guarantee when dispensing in retail, mail-order and specialty channels and being very specific in the contract as to what is or isn’t allowed, but then not replicated in the actual guarantee that they’re delivering to the payer. In addition, there’s often a failure to follow contract definitions around limited distribution or what is considered a specialty drug “that blow through into the exclusionary language,” she says.

But an annual audit isn’t enough. Tanner notes that there also needs to be ongoing monitoring of the contract, PBM performance and consideration of other yardsticks by which to measure them or contract arrangements.

Advocacy in Action

The entity that’s auditing a current contract and entity that’s providing strategic advice and modeling future contract capabilities should be two separate organizations to avoid any conflicts of interest, Tanner suggests. “So even at our own company, there’s a firewall,” she says. “We don’t share databases or details. They’re different humans. They’re different companies.”

In today's environment, Hanson says the PBM or organization that owns the PBM is in control of patients from the time they're examined by a doctor to determine which prescription they can take, where they can get it filled and how much it costs. Since this has led to higher healthcare costs, he says there's a need to separate those responsibilities into independent organizations that will ultimately level the playing field, and that's going to be the only way to be able to have accountability within healthcare and rebuild trust.

Zac Hanson

Lodge says employers must understand their PBM contracts and do a reprice with a third party, as well as tailor a formulary around the medical profile of their employee base. In addition, he says it’s best to separately manage specialty drugs, which typically drive 50% and 60% of costs and are huge rebate drivers but only affect 3% to 5% of plan members.

AVOIDING LEGAL LANDMINES

Mindful of high-profile class-action lawsuits against JPMorgan, Johnson & Johnson and Wells Fargo Bank over inflated prescription drug pricing and a breach in their fiduciary duty as health plan sponsors, Ball emphasizes the importance of fee disclosure. For example, oftentimes there’s back-end incentivization under coalition deals.

"They get paid by PBMs to bring in and retain new business," she explains, "and those fees are not often fully disclosed. So, having an independent consultant who's not paid by anybody else in the supply chain is very important."

What she finds interesting about specialty generics, which sparked these lawsuits in the first place, is that the non-specialty space historically had been teeming with brands and generics. Since blockbuster generics began flooding the market in the 1990s, she says prices dropped significantly when there were multiple competitors.

Rounding out expertise may be the most prudent strategy of all when seeking partnerships. Finding experts who understand the intersection of pharmacy claims data with a PBM contract is critically important, according to Ball. “Just because you’re an attorney doesn’t mean you understand the business side of pharmacy,” she cautions, noting that as a pharmacist she lacks the knowledge to reconcile a client’s contract.

Bruce Shutan is a Portland, Oregon-based freelance writer who has closely covered the employee benefits industry for more than 35 years.

Not Afraid To Spill Some Milk

When your culture drives you to get comfortable being uncomfortable, you’re going to spill some milk to deliver innovation. ‘Yes, and…’ we embrace spilled milk to enable smarter, better, faster healthcare.

Learn more about how we’re delivering innovative solutions to simplify healthcare.

Centers of Excellence Deliver Value for Cancer Care

Employers Proactively Address Employee Cancer Diagnoses, Take Steps to Control Costs

WhenWWritten By Laura Carabello

the diagnosis is cancer, employees may be more worried about the cost of their cancer treatment than suffering or dying from the disease. Faced with financial toxicity, the overwhelming burden of bills for cancer care and persistent debt collectors -- even after the individual passes away -- can impact mental health and job performance.

But employer health plans that have an oncology Center of Excellence (CoE) in place lessen the anxiety and cost impact. Half of the employers surveyed by the Business Group on Health added a CoE option for cancer in their health plans in 2023, while another 26% indicated their intention to do so by this year.

Employers increasingly recognize the importance of making this designation, especially with American Cancer Society predictions that there will be more than two million new cancer diagnoses in 2025 -about 5,600 new cases each day -- with the rate of cancer in people under the age of 50 expected to increase 31% by 2030.

NUMBER OF NEW CANCER CASES IN 2025

Though recent medical breakthroughs in oncology have led to more effective cancer treatment and better prognoses, cancer care costs have captured an outsized proportion of healthcare expenditure charts.

The American Association for Cancer Research reports that costs for cancer-related medical services and drugs are expected to reach nearly $250 billion in the U.S. by 2030 — a 34% increase since 2015. While oncology accounts for only 1% of claims volumes, it makes up 15% of the overall employer healthcare spend, advises the Mahoney Group.

Nationwide costs attributable to cancer care are expected to surge by over 30% from 2015 to 2030. One in two employers identifies cancer care as the number one driver of employer healthcare spend, with 86% ranking it among their top three cost concerns.

Adding a CoE to the group health plan is often the pathway to better manage that cost and translates into relieving plan sponsors from dealing with huge cost discrepancies or inconsistent outcomes for the same procedures. It is also an opportunity for employers to demonstrate their support for employees since cancer is complex and challenges workers to identify high-quality providers, manage care coordination and make multiple decisions about their care and treatment.

INNOVATIVE APPROACHES SUPPORT EMPLOYERS

Oncology benefits for the employer market are a critical topic in healthcare that has been historically under-researched, maintains the consultants at PwC. Responding to this need, they conducted primary research with U.S. benefits managers to better understand challenges and forward-looking priorities for cancer care for employees. Their research shows that employers rank oncology as a priority: 85% of benefits managers ranked oncology as a top three cost driver, with 43% rating it as the health specialty driving the greatest cost.

Consultants advise that while oncology CoEs are relatively new in the market, they offer the potential to provide greater value in employers’ benefits and help overcome the difficulties patients and their families face regarding integration, ease of use and results. Upon diagnosis, a CoE program coordinator can manage all aspects of a member's care, including care navigation.

The goal of these specialty care centers is to provide high-value, coordinated care for complex conditions with better outcomes and more effective cost management. These trends point to the value of services that are positioned to play an important role in employer cancer support strategies. The following COE programs demonstrate employer support:

ACCESS HOPE

AccessHope, for example, connects employees and their local oncologists to world-class expertise from NCI-Designated Comprehensive Cancer Centers, regardless of geography. This approach aligns with employer needs in a number of ways:

• Expert clinical decision support from specialists who advise on the best possible treatment plans, optimizing patient outcomes while reducing unnecessary tests and treatments.

• Insights on precision medicine to treat complex cancers, providing expertise and support on targeted treatments and interpreting genetic tests to help complement the growing employer focus on precision medicine.

• Identification of relevant clinical trials to provide insights on the newest personalized treatments to help improve outcomes and advance cancer care.

• Cost management to optimize treatment plans and reduce unnecessary interventions, helping to manage the growing costs associated with cancer care and address employers’ financial concerns.

Brian Beran, SVP, Growth & Client Success, Access Hope, further explains the value of this model, “High quality cancer care usually requires travel and can introduce inefficiencies into cancer care delivery. AccessHope modifies the COE model to deliver value without the need for patient travel.”

Brian Beran

AccessHope exports knowledge from top-tier subspecialists at National Cancer Institute-designated Comprehensive Cancer Centers to the local treating oncologist to improve quality of life and outcomes.

“This model—constructed around timely, personalized expert opinions—promotes health equity and closes the gap in cancer care knowledge while avoiding the costs and challenges of site-of-care steerage,” says Beran. “AccessHope empowers the treating oncologist with evidence-based recommendations that reduce low-value interventions and improve outcomes and survivorship. AccessHope now serves more than 700 employers nationwide and growing!”

EMPLOYERS CENTERS OF EXCELLENCE NETWORK (ECEN)

Another example is the Employers Centers of Excellence Network (ECEN), established by members of the Purchaser Business Group on Health interested in supporting value-based purchasing. The program provides employees access to demonstrated high-quality care for elective surgeries at meticulously selected CoEs across the United States. Through the ECEN, patients receive care at little or no cost, and their employers gain predictable healthcare costs and downstream

Initially, the program selected hospitals and surgeons throughout the nation for hip and knee replacements and later expanded to offer spine and bariatric procedures and certain oncology services.

Quality improvements and decreased costs resulted from improved professional care coordination, team attention to evidence-based guidelines, better discharge planning to avoid preventable readmissions, increased uniformity of practice and measurement and feedback of patient outcomes.

Expect More FROM YOUR PARTNERS

Oncology COEs provide expert confirmation of diagnosis and development of a recommended treatment plan in collaboration with home oncologists and local care teams, including proactive longitudinal follow-up.

Contigo Health® Centers of Excellence 360 Program

The program gives employers an evolved specialty-care solution designed around the individual needs of health plan members and the business model. The cancer program puts a powerful advocate in the plan member’s corner, helping to guide them through the complexities of cancer care and make informed decisions throughout their journey.

Designed to enable the right diagnosis and the right treatment plan, the program gives members

“You have become a key partner in our company’s attempt to fix what’s broken in our healthcare system.”

- CFO, Commercial Construction Company

“Our clients have grown accustomed to Berkley’s high level of customer service.”

- Broker

“The most significant advancement regarding true cost containment we’ve seen in years.”

- President, Group Captive Member Company

“EmCap has allowed us to take far more control of our health insurance costs than can be done in the fully insured market.”

- President, Group Captive Member Company

“With EmCap, our company has been able to control pricing volatility that we would have faced with traditional Stop Loss.”

- HR Executive, Group Captive Member Company

People are talking about Medical Stop Loss Group Captive solutions from Berkley Accident and Health.

Our innovative EmCap® program can help employers with self-funded employee health plans to enjoy greater transparency, control, and stability.

Let’s discuss how we can help your clients reach their goals.

This example is illustrative only and not indicative of actual past or future results. Stop Loss is underwritten by Berkley Life and Health Insurance Company, a member company of W. R. Berkley Corporation and rated A+ (Superior) by A.M. Best, and involves the formation of a group captive insurance program that involves other employers and requires other legal entities. Berkley and its affiliates do not provide tax, legal, or regulatory advice concerning EmCap. You should seek appropriate tax, legal, regulatory, or other counsel regarding the EmCap program, including, but not limited to, counsel in the areas of ERISA, multiple employer welfare arrangements (MEWAs), taxation, and captives. EmCap is not available to all employers or in all states.

access to leading experts who can collaborate with their existing providers or take the lead in developing a treatment plan. Virtual options can make access to care easier, broaden quality-of-care options, and help balance costs.

National Comprehensive Cancer Network (NCCN)

NCCN is a not-for-profit alliance of 33 leading cancer centers devoted to patient care, research, and education. NCCN is dedicated to defining and advancing quality, effective, equitable, and accessible cancer care and prevention so all people can live better lives.

REVOLUTIONIZING CANCER CARE: THE IMPACT OF COES

When it comes to fighting cancer, CoEs are transforming the landscape with world-class expertise, stateof-the-art treatments, and the potential to significantly improve patient outcomes. For employers and their members, the advantage of guiding members to a COE is undeniable: these elite facilities unite leading oncologists, cutting-edge technology, and groundbreaking clinical trials conveniently located in one place.

"CoEs provide the highest level of specialized cancer care," says Christy Carey, Director of Acute Case Management for MedWatch. “Patients receive more precise diagnoses, better treatment options, and often experience faster recoveries. With multiple specialists collaborating in a single location, members benefit from seamless care coordination and the peace of mind that comes from being treated by top-tier experts."

Maximizing CoE Benefits

Carey points to the role of her organization to administer medical management across a range of health plans, each with different policies on CoE utilization.

“While CoE treatment isn’t always required, the impact is clear: patients who receive care at these specialized centers tend to achieve superior results,” she asserts.

Amy Tennis, senior vice president of Medical Management at MedWatch, emphasizes, "CoEs provide a level of expertise and care coordination that can be life changing. These facilities streamline treatment, reducing fragmented care pathways that can negatively impact patient outcomes."

She says that a common concern with CoEs is cost flexibility, adding, “These institutions are less inclined to offer deep discounts for out-ofnetwork members or negotiate single-case agreements. However, the longterm value is undeniable. There are fewer complications, lower hospital readmission rates, and more effective treatment strategies to ultimately help control overall healthcare spending.”

Amy Tennis

The Bottom Line: Why CoEs Matter

Carey and Tennis concur that patients who receive care at CoEs typically:

• Receive top-tier, coordinated, patient-centered care

• Gain access to groundbreaking treatments and clinical trials

• Experience shorter hospital stays and faster recoveries

• Achieve significantly better health outcomes

• Benefit from lower long-term healthcare costs

• May qualify for employer-sponsored incentives, reduced deductibles, or waived coinsurance

“While CoEs may have a more structured cost model, the long-term benefits -- improved patient experiences, better health outcomes, and reduced overall spend -- make them an invaluable resource for plan sponsors looking to optimize their care management strategies,” they add. “When it comes to cancer care, investing in excellence isn’t just an option -- it’s a game-changer.”

FUELING THE RISE IN CANCER CARE COSTS

Aon’s Global Medical Trend Rate report that addresses cancer risk and treatment warns that it "won't be easy" for companies looking to control costs in the coming years. With a vast pipeline of new therapies in development, Aon forecasts an 11-21% increase in the cost of cancer care every year.

What’s fueling this unprecedented rise in cancer care costs? There appears to be a combination of factors that include:

1. More people diagnosed with cancer than ever before:

An increasing number of Americans are receiving cancer diagnoses, with more than two million new cancer cases reported in 2024 alone. More diagnoses are happening at a later stage as the American Cancer Society reports that advanced-stage cancer diagnoses have been on the rise since the mid-2000s, with another study showing 18% of larger employers reporting a higher prevalence of advanced cancers due to delayed screenings and 41% anticipating a similar impact.

For example, not only are colorectal cancers rising in people under 50, but most of the colorectal cancer diagnoses for this age group are at an advanced stage – leading to more complicated and costly treatment.

2. Aging Population:

As the U.S. population continues to age, cancer rates are expected to increase. Since 2000, the national median age has jumped by more than three years, and as people age, their cancer risk climbs and contributes to increased prevalence. In fact, researchers report that increased age is the most important

corporatesolutions.swissre.com/esl

cancer risk factor. The chance of a cancer diagnosis climbs from 350 in 100,000 at age 45–49 to 1,000 in 100,000 after age 60.

3. Advancements in Cancer Treatments:

A cascade of new treatments is being discovered, approved, and utilized more frequently, contributing to the projected cost of healthcare, which is growing at the highest rate in a decade, rising to nearly 8% in 2025. Scientists are working to improve the treatment and diagnosis of cancer, using AI, DNA sequencing and precision oncology, among other techniques. But this wave of medical advancements and innovation comes with a great financial burden.

4. Rising Drug Prices:

The cost of cancer medications, including both oral and injectable drugs, is a significant factor in the overall increase in cancer care costs. The vast majority of cancer treatments are provided via the standard fee-for-service model, meaning there is little incentive to keep costs to a minimum. And since most cancer drugs are reimbursed on a buy-and-bill basis, with providers administering pre-purchased medications to patients on site, there's a strong incentive to use them.

5. Increased Prevalence of Chronic Diseases:

Recognized as a chronic disease, cancer requires more frequent visits to specialists, expensive imaging tests and constant monitoring, driving roughly 30% of medical costs. The growing prevalence of cancer in younger patients may be troublesome to employers and their working-age population. The American Cancer Society annual report showed younger adults to be the only age group with an increase in overall cancer incidence between 1995 and 2020—the rate rising by 1% to 2% each year during that time period.

6. Focus on Prevention and Early Detection:

While screening and early detection can improve outcomes, they also contribute to increased costs as more people are diagnosed and require treatment.

CHOOSING A COE

Industry experts affirm that oncology COEs and bundled payments improve outcomes and cost predictability. As value-based solutions for oncology have finally emerged, employers are increasingly looking to them to address their growing healthcare costs. Specialists at Carrum Health say here’s why:

Using a bundled payment model ensures that employees receive care from high-quality, highvalue physicians who deliver evidence-based, guideline-concordant care rather than those who are incentivized to provide more care and prescribe high-cost cancer drugs in the traditional fee-forservice model.

Receiving care from a COE is linked to improved quality of life and survival rates, as well as more cost-effective care, which is vital since there can be a significant variation in these measures between oncology providers.

With a tremendous variability in costs especially in the first year of a cancer diagnosis, these solutions give employers and patients full visibility, more control, and greater predictability when it comes to their oncology spend.

Patients never receive a surprise medical bill and usually have their cost-share waived, meaning that financial toxicity is no longer an issue.

Criteria for Identifying a Value-based COE Solution

When considering a partner, employers should look for those that prioritize high-quality, evidencebased, multidisciplinary care and can demonstrate improved outcomes, survival rates and optimal patient experience scores.

In order to reduce costs, the program should incorporate both guidance and the actual treatment.

Guidance plays a critical role in driving higher-value cancer care that ensures proper diagnosis and effective, individualized treatment plans.

Employers should also look for programs that include diagnostic workups, the creation of the treatment plan and expert opinions and review.

Assess the duration of the support. Many available solutions only cover an upfront expert review of the diagnosis and treatment plan. However, best-in-class platforms will provide longitudinal support for both patients and their treating oncologists because cancer is often unpredictable and requires ongoing monitoring and changes to the treatment plan.

Look for risk-takers – COEs that:

o Incentivize providers to deliver cost-effective care and explore opportunities to reduce costs.

o Demonstrate a commitment to reducing unnecessary care.

o Endeavor to keep patients out of the emergency room and hospital for treatment-related complications.

o Provide proactive symptom management, including systematic, timely follow-up for high-risk patients

o Offer remote patient monitoring (RPM) and urgent care clinics devoted to symptom management and supportive care.

o Add value to the patient experience, providing employees and their families with exceptional engagement that may include a patient care team, coordination of care and travel.

o A digital option with on-demand accessibility via an app.

Financial arrangements vary, depending upon the COE. In many cases, the CoE partner will provide a warranty that covers the costs of treatment-related should complications arise. Ideally, these costs are included in the bundle and not paid for separately.

claim-doc.com

Carmie Johnson Coding Auditor

BOTTOM LINE: PREVENTION IS A KEY STRATEGY TO IMPROVE CANCER CARE

While CoEs are ready to provide quality care, cancer prevention is a smart move for employers: 45% of all cancer deaths are caused by risk factors that can be potentially modified by changes in diet, exercise, and medication.

Early detection discovers cancers at more treatable stages, potentially reducing long-term costs while improving outcomes. Studies show that 87% of employers plan to have at least one cancer screening method in place by 2025.

Providing plan participants with current information helps to resolve barriers and ease any reticence around screenings. As an example, the perception persists that tests like colonoscopies are difficult or painful, even though some tests are available at home and many procedures are designed to be as comfortable as possible.

In 2025 and beyond, risk managers at WTW recommend these proactive strategies to promote early detection and use data-driven technology to support cost-containment, including:

Leverage and know how to use forms of data available — from electronic medical records and claims analysis to lab results and predictive analytics. Payers have the opportunity to guide members to appropriate forms of testing or treatment before cancer further progresses, reducing the potential for costly late-stage treatment protocols.

Implement effective risk management strategies that manage overall population health risk through thoughtful care management programs and steerage to quality care. such as COEs.

Embrace precision medicine, genetic testing and advanced diagnostic and treatment options: family history for genetic testing, such as BRCA testing; genomic testing for cancer treatment; coverage for immunotherapies, such as CAR-T cell therapy, and pharmacogenomic tests.

About the Author

Laura Carabello holds a degree in Journalism from the Newhouse School of Communications at Syracuse University, is a recognized expert in medical travel and is a widely published writer on healthcare issues. She is a Principal at CPR Strategic Marketing Communications. www.cpronline.com

SPRING FORUM | 2025

State of the Industry | Live Polling Results

SIIA MEMBERS SHARE OPINIONS AND UPDATES

As part of SIIA's recent Spring Forum in Tampa, hundreds of attendees participated in a live audience polling session. They were asked to share anonymous opinions about various industry developments and updates about their own companies.

The results were displayed in real time to those in attendance. Given that many self-insurance industry professionals were unable to attend the session, we are republishing the results here.

How was your Company’s Financial Performance in 2024?

What is Your Company’s Workforce Arrangement?

What is Your General Outlook for the Self-Insurance Industry Over the Next 5 Years?

What is the Single Biggest Threat to the Self-Insurance Industry?

What is the Single Biggest Opportunity for the Self-Insurance Industry?

What Problem are you Dealing with for Which You Would Love an “Easy” Button?

Regarding Fiduciary Liability Litigation...

Regarding the Stop-Loss Market...

Regarding Cell & Gene Therapy Developments...

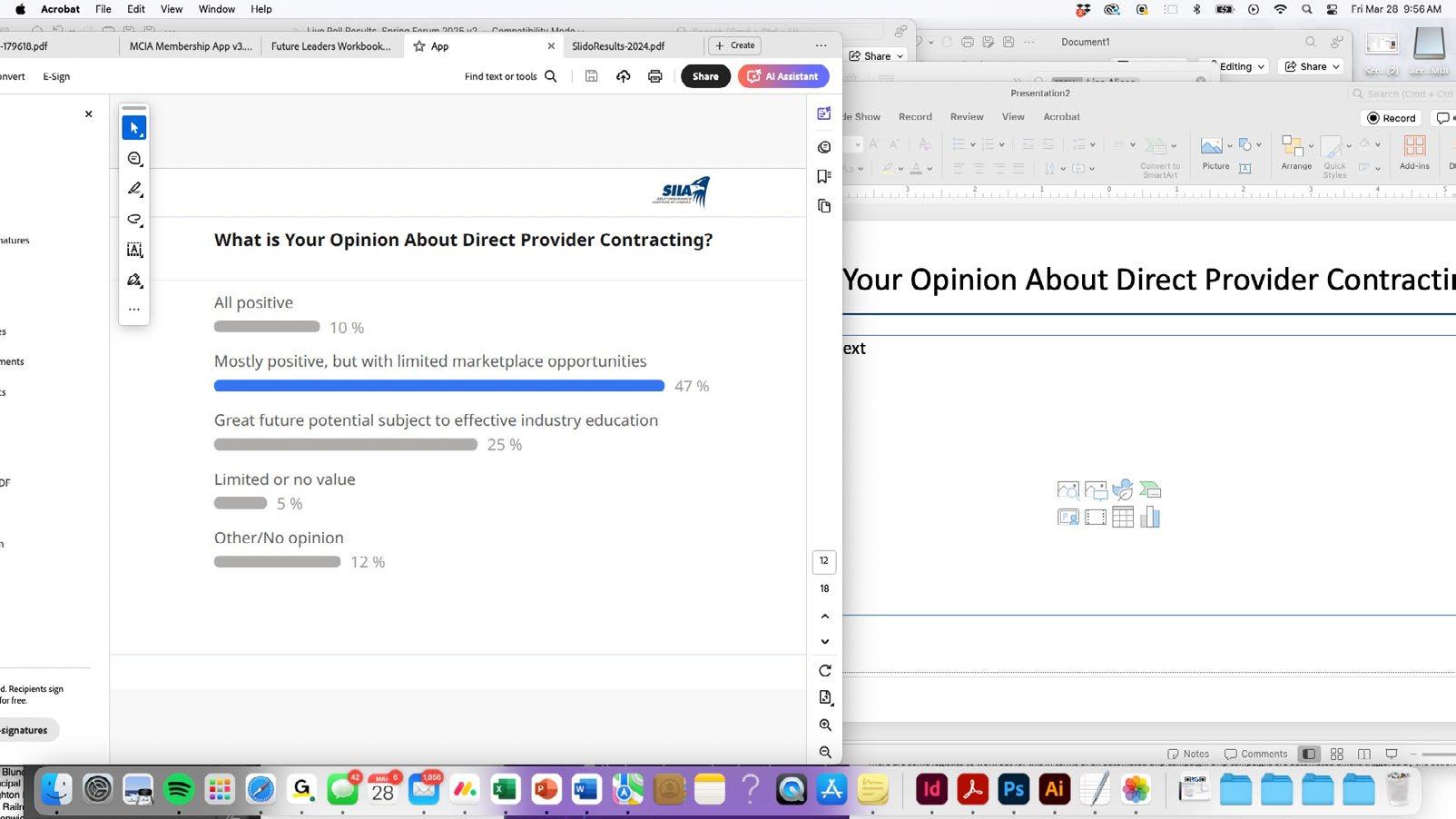

What is Your Opinion About Direct Provider Contracting?

What is Your Opinion About Direct Primary Care?

What is Your Company’s Experience with Artificial Intelligence?

Regarding Your Company’s Involvement with Captives...

Regarding the Accelerated Pace of Industry Mergers/Acquisitions...

Is Your Company Planning/Positioning for a Merger/Acquisition?

Urgent Care in 10 Minutes or Less No long waits for non-emergency care

Seamless Tech Integration

Easy to implement, no hassle

Prescriptions Available

Short-term, non-DEA controlled medications may be prescribed as needed

24/7/365 Availability Care anytime, even on holidays & weekends

Conditions Treated Colds, the flu, allergies & more

NIGEL WALLBANK NAMED SIEF CHAIRMAN EMERITUS

Long-time SIIA member Nigel Wallbank was recognized for his lifetime service to the association during the opening session at SIIA’s recent Spring Forum in Tampa. He was specifically named chairman emeritus of the Self-Insurance Educational Foundation (SIEF)

Nigel has been a SIIA member for more than three decades. He previously served on the association's board of directors, including board chairman. His participation also included participation on multiple committees, and he was a big supporter of SIIA's international initiative.

For the last several years, Nigel's focus has been on the Self-Insurance Educational Foundation (SIEF) through his service as board chairman. The foundation complements the work of SIIA in a variety of ways and Nigel has been a steady hand ensuring that it has stayed focused while strengthening its financial position.

Field

Choose speed and savings with Stealth Advance! We fund claims up to $5 million within 72 hours of loss notification— no complex forms needed. Enjoy cash flow stability without being tied to any specific carrier, TPA, or PBM. Get the rapid reimbursements of bundled stop-loss combined with the flexibility of direct writers. As your program manager, Stealth Partner Group simplifies the process with one transparent PEPM fee—no hidden costs. Experience the Stealth Advance difference: fast reimbursements, competitive rates, and complete vendor freedom!

FINAL MENTAL HEALTH PARITY RULES: A PLAN SPONSOR’S IMPLEMENTATION GUIDE

PART III: OVERVIEW OF NETWORK COMPOSITION GAPS, GHOST NETWORKS AND COMPLIANCE BEST PRACTICES

Editor’s Note: This is the third installment in a three-part series. The first two installments were included as part of the March and April editions of the Self-Insurer.

Written By Alston & Bird, LLP Health Benefits Practice

InISeptember 2024, the U.S. Departments of Labor, Treasury, and Health and Human Services (the "Departments") issued a Final Rule under the Mental Health Parity and Addiction Equity Act of 2008 (MHPAEA). The Final Rule has a general effective date of the first day of the plan year beginning on or after January 1, 2025, though most of the requirements for completing the comparative analysis were first due as of February 10, 2021, under the Consolidated Appropriations Act, 2021 (CAA). Additional new requirements, including those related to network composition, are effective within the first plan year starting on or after January 1, 2026.

This article is the third in a three-part series designed to inform plan sponsors of self-insured plans about the key components of the Final Rule and compliance steps for satisfying regulatory requirements. In Part I, we provided a high-level overview of the essential elements of the Final Rule, focusing on the two-part test for nonquantitative treatment limitations (NQTLs). In Part II, we provided an overview of compliance action steps, timeframes, and requirements for the Final Rule in further detail and highlighted the Department of Labor’s (DOL) 2024 Report to Congress, released in January 2025. In this Part III, we will home in on the network composition of NQTL and provide a high-level overview of “ghost networks,” insurance directories listing inactive or nonexistent mental health providers that create the illusion of accessible care, which violates MHPAEA by creating coverage gaps within networks.

We will close by providing compliance best practices for agreements with administrative service organizations (ASOs) and third-party administrators (TPAs), as the Departments have not issued new compliance tools to date. For purposes of this article, "mental health/substance use disorder" is referred to as "MH/SUD," and "medical/surgical" is referred to as "Med/Surg.”

ADDRESSING MATERIAL DIFFERENCES IN NETWORK COMPOSITION UNDER MHPAEA

One of the most challenging aspects of this Final Rule is the Departments’ expectation that plans collect data on their networks and address gaps between MH/SUD and Med/Surg providers and facilities. Ideally, the Departments would like participants to be able to access a network MH/SUD provider or facility just as easily as they can access a Med/Surg provider or facility. Plans are left trying to figure out how

to “quantify” this “nonquantitative” treatment limitation based on relevant data that plans are required to collect and analyze, yet the Final Rule itself provides only a few brief data elements for this purpose (which we covered in Part I of this series). The Departments had promised additional guidance with “adequate” time for plans to prepare, but so far, no guidance has been issued, and no updates have been made to the Employee Benefits Security Administration’s (“EBSA”) online Self-Compliance Tool.

In addition to the data elements listed in the Final Rule itself, the Departments stated in the preamble that they would “expect” that a plan might collect and analyze data on:

• For in-network and out-of-network utilization, compare the ratio of inpatient, in-network and outpatient, in-network MH/SUD and Med/Surg claims to inpatient, out-of-network and outpatient, out-of-network MH/SUD and Med/Surg claims.

• The number of providers (or facilities) within specified MH/SUD and Med/Surg provider categories (or categories of facilities) per 1,000 participants and beneficiaries who have actively submitted claims within the past 6 months.

• Comparing MH/SUD and Med/Surg turnaround time for applications to be approved for a provider to join the plan’s network as well as approval and denial rates for applications to join the network;

• Percentage of participants and beneficiaries who have access, within a specified time and distance by one (or more) in-network providers who are available to accept new patients comparing MH/ SUD providers and Med/Surg providers;

• Median in-network MH/SUD and Med/Surg reimbursement rates for services with the same CPT codes;

• Median in-network reimbursement rates for inpatient MH/SUD and Med/Surg benefits, as compared to Medicare rates;

• Median in-network reimbursement rates for outpatient MH/SUD benefits and Med/Surg benefits, as compared to Medicare rates.

Once a plan has collected and analyzed this data, the plan will need to address any “material differences” between MH/SUD and Med/Surg benefits by taking affirmative steps to close network gaps. In Example 10 of the Final Rule, the Departments outline the following “reasonable actions” that a plan can take, "as necessary," if the relevant data suggest that the NQTLs related to network composition, in the aggregate, contribute to material differences that are likely to have a negative impact on access to MH/SUD benefits as compared to Med/Surg benefits:

• Strengthen efforts to recruit and encourage a broad range of available providers and facilities to join the plan’s network of providers, including by taking actions to

o increase compensation and other inducements,

o streamline credentialing processes,

o contact providers reimbursed for items and services provided on an out-of-network basis to offer participation in the network and

o develop a process to monitor the effects of such efforts;

• Expand the availability of telehealth arrangements to mitigate overall provider shortages in certain geographic areas;

• Provide additional outreach and assistance to participants and beneficiaries enrolled in the plan to assist them in finding available in-network providers and facilities and

• Ensure that the plan’s provider directories are accurate and reliable. The plan also needs to document these efforts and include the documentation as part of its comparative analysis submission.

Even beyond the hypothetical example in the Final Rule, EBSA, in the 2024 Report to Congress, approvingly highlighted similar efforts that a plan had taken, stating that the plan was “committed to taking significant steps toward actively monitoring its network composition and filling gaps” by:

• Providing live support for participants who have difficulty finding available in-network providers.

• Providing arrangements for the plan to pay for out-of-network care when in-network providers are not available.

• Identifying network gaps through ongoing review of network composition and utilization data, including appointment wait times and out-of-network provider use.

• Taking affirmative steps to close network gaps, such as targeted provider recruitment.

• Measuring progress to close network gaps using the same data-based measures used to identify them.

• Expanding telehealth services.

• Expanding a supplemental network of substance use disorder treatment facilities.

• Soliciting proposals through the RFP process to evaluate the suitability of other networks and network administrators outside of the plan’s then-current network administrator.

EBSA stated that it “applauds the plan’s commitment to parity and its efforts to ensure its participants and beneficiaries have meaningful access” to MH/SUD benefits as compared to Med/Surg benefits. EBSA

Discover Excellence. pinnacletpa.com/excellence

found the plan’s response to be “constructive because it focused on processes, strategies, evidentiary standards, and other factors (including resources) it could control to address access disparities, rather than simply pointing to provider shortages, general arguments about market forces, or how its network administrator controlled many aspects of network composition.”

GHOST NETWORKS

The Departments also expressed concern about “ghost” or phantom networks where a plan may list MH/ SUD providers as being in network when they actually are not, or are unreachable by participants based on the information in a provider directory, or are not accepting new patients. The preamble includes some examples of “secret shoppers” calling MH/SUD providers listed in provider directories to see if the information was correct or whether the secret shopper could get an appointment. EBSA’s survey results, as described in the DOL’s 2024 MHPAEA Report to Congress, closely mirrored the findings of the Senate survey results examining the availability of MH/SUD listed providers.

Ghost networks can cause other compliance failures for ERISA employer group health plans. ERISA Section 720 requires plans to maintain an updated provider directory. If a plan participant receives otherwise covered services from a provider or facility in the directory that is not part of the network, the plan cannot impose cost-sharing greater than cost-sharing for an in-network provider or facility and must count cost-sharing amounts toward any in-network deductible or in-network out-of-pocket maximum. Plans also must establish a process to update and verify provider director accuracy at least once every 90 days and establish a protocol for responding to telephone and electronic requests about a provider’s network status (and to retain communication in such individual’s file for at least 2 years). The list of providers must be up-to-date, accurate, and complete (using reasonable efforts) and must be distributed

Proceed With Confidence Mind Over Risk

We study it, research it, speak on it, share insights on it and pioneer new ways to manage it. With underwriters who have many years of experience as well as deep specialty and technical expertise, we’re proud to be known as experts in understanding risk. We continually search for fresh approaches, respond proactively to market changes, and bring new flexibility to our products. Our clients have been benefiting from our expertise for over 50 years. To be prepared for what tomorrow brings, contact us for all your medical stop loss and organ transplant needs.

Tokio Marine HCC - A&H Group

HCC Life Insurance Company operating as Tokio Marine HCC - A&H Group

to participants. It may be distributed as a separate document that accompanies the plan's SPD if it is sent automatically, the insured is not charged, and the SPD contains a statement to that effect.

RECENT LITIGATION

Regulators aren’t the only ones enforcing compliance with network composition and provider directory requirements. Lawsuits highlighting network inadequacies and provider directories are on the rise. One recent complaint, filed on October 22, 2024, as a class action in federal court, also details the use of “secret shoppers” who purportedly discovered deficiencies in a plan’s provider directory on access to MH/ SUD providers (for autism and ADHD, specifically).

The complaint focuses on ghost networks and alleges that the provider directories are grossly inaccurate (secret shoppers succeeding in scheduling only seven appointments out of calls to 100 providers), leading to significant barriers to accessing mental healthcare. Plaintiffs’ claims include breach of contract, deceptive acts, false advertising, violation of New York Insurance Law, fraudulent misrepresentation, and unjust enrichment. Among other things, the plaintiffs ask the court to declare the defendant’s actions violate federal law, including the No Surprises Act, the Public Health Services Act, ERISA (including section 720), and the Code See Doe v. Anthem, S.D.N.Y., No. 1:24-cv-08012.

COMPLIANCE BEST PRACTICES FOR PLAN SPONSORS – ASO AND TPA AGREEMENTS

As mentioned in past installments, the Final Rule provides even more impetus to have conducted an updated, compliant comparative analysis, given that plans were required to complete a comparative analysis as of February 10, 2021. Remember, there are very short turnaround times if a department, a participant, or a beneficiary asks for this comparative analysis. Comparative analyses will need to be updated to cover these requirements, effective January 1, 2026, for calendar year plans, including requirements imposed

because of:

• The meaningful benefits standard.

• The prohibition on discriminatory information used in the design and application requirements.

• The relevant data evaluation requirements.

Agreements with service providers need to be reviewed—in particular, ASO and TPA agreements—to make sure that they are clear on the allocation of responsibilities for preparing a comparative analysis.

Plan fiduciaries should be made aware of the certification requirement and the need to engage in “a prudent process to select one or more qualified service providers to perform and document a comparative analysis.”

This is also a good time to make sure that ASO/TPA agreements spell out who is responsible for quantitative treatment limitations (QTL) testing/analysis (e.g., might a qualified service provider other than the ASO/TPA prepare the analysis) and that the plan sponsor retains a copy of that testing. QTL testing does not have to be done every year but needs to be performed if there is a change in plan benefit design, cost-sharing structure, or utilization that would affect a QTL within a classification (or subclassification).

Work with your ASO or TPA to identify any areas where there may be a plan design issue with the meaningful benefits/core treatment standard, and be prepared to address those for plan years beginning in 2026. For the design and application requirements, seek verification from the TPA/ASO that they are not using any biased or discriminatory information in designing the NQTL, including historical data.

Data collection will be the most challenging aspect of the Final Rule. There are still many unknowns about the type of data that must be collected. The Final Rule is limited in the list of these requirements, but at the very least, plans should start collecting the data identified in the Final Rule as well as other relevant data suggested in the preamble and examples—especially related to the network composition NQTLs, as discussed above.

Discuss with the TPA/ASO their ability to collect and analyze the data, including whether they have the technology required for data collection. Include in the RFP proposals to evaluate the suitability of the network composition for MHPAEA. Be prepared to review and revise TPA/ASO agreements for the NQTL comparative analysis. These service provider agreements should go beyond that to address responsibilities for the meaningful benefit requirement, data collection, and whether the TPA/ASO is using any discriminatory data.

CONCLUSION

As we conclude this three-part series, we will continue to keep an eye out for the promised further clarifications and guidance from the departments on the NQTL data to be collected and analyzed and watch for developments in the courts and challenges to the Final Rule under Loper Bright or otherwise— particularly challenges to the relevant data evaluation and meaningful benefits requirements.

Attorneys John Hickman, Ashley Gillihan, Steven Mindy, Amy Heppner, Laurie Kirkwood, and Bria Smith provide the answers in this column. John is partner in charge of the Health Benefits Practice with Alston & Bird, LLP, an Atlanta, New York, Los Angeles, Charlotte, Dallas and Washington, D.C. law firm. Ashley and Steven are partners in the practice; Amy and Laurie are senior members in the Health Benefits Practice; Bria Smith is an associate in the Employee Benefits Practice. Answers are provided as general guidance on the subjects covered in the question and are not provided as legal advice to the questioner’s situation. Any legal issues should be reviewed by your legal counsel to apply the law to the particular facts of your situation. Readers are encouraged to send questions by E-MAIL to John at john.hickman@alston.com

NEWS FROM SIIA MEMBERS

SIIA MEMBER NEWS, MAY 2025

SIIA boasts a very active and dynamic membership. Here are some of the latest developments from the companies powering the self-insurance industry.

QBE Expands Leadership Team

QBE North America has announced an expansion of its Accident & Health (A&H) leadership team to enhance operational efficiencies and maintain its exceptional service levels to customers.

"I am excited to announce these leadership appointments as we continue to enhance our ability to deliver superior service to our customers," said Tara Krauss, President of Accident & Health. “We are committed to providing meaningful support and exceptional value to our broker partners and customers.”

• Andrea McNamara steps into the newly created role of Head of A&H Underwriting, where she is responsible for overseeing all traditional underwriting accountabilities, including MSL, Taft Hartley and Organ Transplant.

• Mike Jacobs has been appointed to Head of Operations, A&H, where he oversees the development and execution of underwriting operations, product delivery, and clinical risk management strategies.

• Jake Thiesse, former VP of Business Development for QBE’s Northwest region, stepped into the newly created role of Head of Sales for A&H.

• Nichole Sivigny has been appointed SVP, Underwriting Leader for the Northwest region. She will be succeeding Jon Tolzin, who will be transitioning to a consultant role after 30+ years in the industry.

• Zach Sullivan is succeeding Mike Jacobs as SVP, Underwriting Leader of the East region.

MedWatch Earns URAC Accreditation

MedWatch announced that it has once again earned URAC accreditation for Health Utilization Management, Case Management, and Disease Management. URAC is the independent leader in promoting healthcare quality by setting high standards for clinical practice, consumer protections, performance measurement, operations infrastructure, and risk management.

"Earning URAC re-accreditation reflects the hard work of our team and unwavering commitment to improving healthcare quality," said Sally-Ann Polson, President and CEO of MedWatch. “We are honored to uphold URAC’s high standards and remain a trusted partner in healthcare transformation.”

Caryn Rasnick to Lead Operation at Boon-Chapman

Boon-Chapman announced the appointment of Caryn Rasnick as Chief Operating Officer.

Caryn is a veteran employee benefits executive with over 35 years of experience in the TPA industry. Prior to joining Boon-Chapman, Caryn worked as a Chief Client Relations Officer at MedWatch, where she oversaw the company's client engagement strategy, with a focus on building and maintaining strong, longterm relationships with key clients.

Amalgamated Life Insurance Company Medical Stop Loss Insurance— The Essential, Excess Insurance

As a direct writer of Stop Loss Insurance, we have the Expertise, Resources and Contract Flexibility to meet your Organization’s Stop Loss needs. Amalgamated Life offers:

• Specialty Rx Savings Programs and Discounts

• “A” (Excellent) Rating from A.M. Best Company for 49 Consecutive Years

• Licensed in all 50 States and the District of Columbia • Flexible Contract Terms

• Excellent Claims Management Performance

• Specific and Aggregate Stop Loss Options

• Participating, Rate Cap and NNL Contract Terms Available

Better outcomes. Long-term cost savings.

Mayo Clinic Complex Care Program

experienced a change in diagnosis

experienced a change in treatment plan

avoided a locally recommended surgery

Discover how a customizable center of excellence program can help minimize healthcare costs while o ering high-cost, high-risk members exactly the care they need.

The Mayo Clinic Complex Care Program is for a small subset of a population with serious, complex or rare conditions who need subspecialized expertise that may not be available locally.

Learn more by calling 507-422-6103 or visit us online at mayoclinic.org/complex-care-program

"Caryn's people-centric leadership approach, deep understanding of operational efficiency and excellence, and dedication to building highperformance teams will drive our executive strategies forward. As we lay the foundations for continued value creation in Boon-Chapman's ambitious plan for long-term growth, I can't think of a better person to take on these responsibilities than Caryn," said Kari L. Niblack, President of Boon-Chapman.

Zakipoint Promotes Jaclyn Mains

Zakipoint Health Inc. announced the promotion of Jaclyn Mains to Chief Revenue Officer. In this role, Jaclyn will drive revenue growth, partnerships, and sales expansion, further advancing the company’s mission to transform employee benefits.

Caryn Rasnick

"I'm passionate about bridging the gap between healthcare and benefits, ensuring that employers and members not only understand their plans but engage with them proactively to make informed decisions," said Jaclyn Mains. "At zakipoint Health, we deliver transparent, real-time insights that drive action, optimize costs, and enhance the healthcare experience. I’m excited to advance our vision and foster partnerships that create lasting impact.”

Ramesh Kumar, CEO of Zakipoint Health, added, "Jaclyn has been incredible in driving growth and client success. Her ability to blend deep healthcare knowledge, strategic execution, and a customer-first mindset makes her the ideal leader to take us to the next level. I am thrilled to have her as our Chief Revenue Officer.”

Liviniti’s LeAnn Boyd Receives Prestigious Award

Liviniti announced that its CEO, LeAnn Boyd, has been selected for the Inc. 2025 Female Founders 500, which recognizes the most dynamic women entrepreneurs in America who are leading their organizations to success. The announcement puts LeAnn in the company of US-based women entrepreneurs whose achievements defy obstacles and position them as leaders in their industries.

Protection and peace of mind with Wellpoint Stop Loss

Our highly experienced team can help you customize policies focused on cost control, administrative efficiency, and better employee outcomes.

What you can expect

• Faster reimbursement, with an advance funding option to help with cash flow concerns

• Lower claim costs, with a dedicated team to seek out cost-mitigation opportunities

• Solid protection with no surprises, so you can budget with confidence

• Industry leadership, as a top-5 stop loss carrier with our family of companies*

To learn more about our stop loss offering, contact your WellPoint Stop Loss sales executive.

Jaclyn Mains

"The Inc. Female Founders recognition is a reflection of our entire Liviniti team as we work together to deliver pharmacy benefit savings to employers and their plan members," says LeAnn. "Pharmacy care has the power to improve the well-being of people and communities, and Liviniti is making a difference in the lives of the people we serve. I am excited to be in the company of such impressive women leaders honored by Inc."

Berkely A&H Adds to Sales Team

Berkley Accident and Health, a Berkley Company, announced the appointment of Chris Pinto as Regional Sales Manager for the New England states. In this role, Chris will be responsible for driving growth and developing new Stop Loss relationships and Captive Insurance programs in the region.

phiagroup.com

LeAnn Boyd

"We are thrilled to welcome Chris to our team," said Brad Nieland, President and CEO of Berkley Accident and Health. “Chris’s extensive experience with both national carriers and his time as a broker make him an invaluable asset. His successful track record in business development and his deep understanding of the insurance landscape will greatly benefit our clients.”

Blackwell Captive Solutions Appoints New Marketing Executive Blackwell Captive Solutions, a leader in group medical stop loss captives, is pleased to announce the promotion of Ashley Sheble to Chief Marketing Officer. In this role, Sheble will spearhead strategic marketing initiatives to elevate Blackwell’s presence, expand partnerships, and deliver innovative solutions that provide greater control and cost predictability in a rapidly evolving benefits landscape.

Ashley brings 15 years of experience in the employee benefits industry, where she developed a deep understanding of employer-driven healthcare solutions. Sheble also brings innovation expertise gained from her studies at Harvard University and involvement in the Harvard Innovation Lab, applying forward-thinking strategies to develop cutting-edge solutions, strategic partnerships, and cost-containment programs that help employers proactively address rising healthcare costs.

Ashley Sheble

Chris Pinto

STOP LOSS INSURANCE

MANAGE THE RISK.

Prudential’s Stop Loss insurance helps reduce unpredictable risks from self-funded medical plans. This way you can focus on giving your employees the coverage they deserve, while helping to reduce your worries about the increased frequency of catastrophic claims.

Get Stop Loss insurance from a partner you can rely on:

• A highly rated, experienced carrier recognized for 150 years for strength, stability, and innovation

• Efficient, responsive service with streamlined processes across quoting, onboarding, and reimbursements

• A dedicated distribution team that works hand-in-hand with your existing relationships

• Flexible policy options so we can build a coverage plan that meets the unique needs of your organization

Did you know, medical and prescription drug costs are expected to rise 8.5% annually?* See how Prudential can help you manage the risk from your self-funded medical plan.

For more information, contact us at stoploss@prudential.com or visit our website: www.prudential.com/stoploss

TJ Carrender Named President at Virtue Health Virtue Health announced the appointment of TJ Carrender as its new President.

With a proven track record in transformational leadership, go-to-market strategies, and business turnarounds, Carrender will lead Virtue Health into its next phase of innovation and growth.

Carrender steps into the role with over 20 years of executive leadership, bringing expertise in scaling operations, driving market expansion, and propelling business growth. Previously, as President of Authorify, he tripled revenue in three years, and as VP of Sales for Konica Minolta, he drove significant sales growth. At Virtue Health, Carrender will accelerate the company’s mission to mitigate healthcare costs for midsized employers while delivering superior benefits and financial stability.

"TJ Carrender’s appointment marks a bold step forward for Virtue Health,” said John W. Sbrocco, CEO of Virtue Health. “His knack for transformation and operational excellence will amplify our ability to empower employers and benefits consultants with smarter, more affordable healthcare solutions.”

a Leading National TPA

Creating solutions for better healthcare outcomes is at the heart of everything we do.

In-house client support from implementation through renewal

Tailored point solutions and a la carte programs

The latest in navigation tools and concierge services

Member advocacy solutions

hpiTPA.com

TJ Carrender

SIIA NEW MEMBERS

MAY 2025

NEW CORPORATE MEMBERS

Nicholas Syhler Co-CEO, Co-Founder Embla Georgetown, TX

Patrick Williams CEO

Fiduciary In A Box Palm Beach Gardens, FL

Nicole Semeraro CEO Karias Health Awendaw, SC

Steve Keresztes VP, Client Services Medlitix Wexford, PA

Troy Vincent Founder & CEO Navigate Wellbeing Solutions West Des Moines, IA

Shannon Rich VP, Client Strategies

Northwind Pharmaceuticals Indianapolis, IN

Natalya Gertsik VP, Partnerships Private Health Management Cranford, NJ

Kristin Asche Director of Legal Services Sourcewell Staples, MN

Wendell Strickland CEO

Strongside Solutions Alpharetta, GA

NEW EMPLOYEER MEMBERS

Michael Quernemoen Owner & CFO

Triple Crown Products Mukwonago, WI

Do you aspire to be a published author?

We would like to invite you to share your insight and submit an article to The Self-Insurer! SIIA’s official magazine is distributed in a digital and print format to reach 10,000 readers all over the world.

The Self-Insurer has been delivering information to top-level executives in the self-insurance industry since 1984.

Articles or guideline inquires can be submitted to Editor at Editor@sipconline.net

The Self-Insurer also has advertising opportunties available. Please contact Shane Byars at sbyars@ sipconline.net for advertising information.

2025 SELF-INSURANCE INSTITUTE OF AMERICA

BOARD OF DIRECTORS

CHAIRMAN OF THE BOARD*

Matt Kirk

President

The Benecon Group

CHAIRPERSON ELECT, TREASURER AND CORPORATE SECRETARY*

Amy Gasbarro

President

ELMCRx Solutions

DIRECTOR

Mark Combs

CEO/President

Self-Insured Reporting

DIRECTOR

Orlo “Spike” Dietrich

Operating Partner

Ansley Capital Group

DIRECTOR

Jeffrey L. Fitzgerald

Managing Director

SRS Benefit Partners

Strategic Risk Solutions, Inc.

DIRECTOR

Mark Lawrence

President

HM Insurance Group

DIRECTOR

Matthew Smith

Managing Director Risk Strategies

DIRECTOR

Beth Turbitt

Managing Director Aon Re, Inc.

VOLUNTEER COMMITTEE CHAIRS

Captive Insurance Committee

George M. Belokas, FCAS, MAAA President

Beyond Risk

Future Leaders Committee

Erin Duffy Director of Business Development

Imagine360

Price Transparency Committee

Christine Cooper CEO

aequum LLC

Cell and Gene Task Force

Ashley Hume President

Emerging Therapy Solutions®

* Also serves as Director

Zero in on catastrophic claims risks.

Curv® can isolate risk above a specified individual stop-loss threshold, giving finely tuned insight into potential high-cost claims. Depend on Curv’s predictive analytics for more accurate pricing across your spectrum of underwritten groups.

rxhistories.com/curv/group-health

2025 BOARD OF DIRECTORS

SIEF CHAIRMAN

Nigel Wallbank President New Horizons Insurance Solutions Wellington, FL

SIEF PRESIDENT

Dani Kimlinger, PhD, MHA, SPHR, SHRM-SCP

Chief Executive Officer MINES & Associates, Inc Littleton, CO

DIRECTORS

Les Boughner Chairman Advantage Insurance Management (USA) LLC Charleston, SC

Matt Hayward Office President Ryan Specialty Benefits Greenwood Village, CO

Elizabeth Midtlien Vice President, Emerging Markets AmeriHealth Administrators, Inc. Bloomington, MN

Jonathan Socko President East Coast Underwriters, LLC Spartanburg, SC

Care that Goes Beyond Coverage

Working as a case manager with a special focus in behavioral health, it is so important to ensure that these patients are provided with adequate support and outpatient linkage so they can live healthy and fulfilling lives. There is so much love and compassion in the field of nursing. Being there to help another human being, sometimes during the most difficult points in their life, is the most fulfilling part of my job.”

—Nova Case Management Nurse

Managing claims, payments, and networks doesn’t have to feel like an endless struggle.

See the Zelis difference: Empowered teams focused on high-value tasks. Happy clients who see the results.

Supercharge Your TPA Operations with Zelis. Call us today at (888) 311-3505 or scan the QR code to get started. Stay ahead with solutions that work with

Seamless systems that work together.

Stop Loss helps protect his self-funded employer.

Catastrophic claims can arise unexpectedly. Unforeseen complications can take a routine surgery from $25,000 in costs to nearly $1 million.* When the self-funded employer has the right Stop Loss protection in place, focus can remain on achieving business goals and welcoming John back when he’s able to return.

When you work with the experts at HM Insurance Group, you can be confident that claims will be paid. We process 99% of Stop Loss claims within six business days, with more than 99% technical and financial accuracy. Find more at hmig.com.