Get the peace of mind and support it takes to self-fund your healthcare.

Self-insuring your healthcare benefits can open up new possibilities for your business — affording greater flexibility in how you manage your healthcare spend. Trust the expert team at QBE to tailor a solution that meets your unique needs.

We offer a range of products for protecting your assets, your employees and their dependents:

• Medical Stop Loss

• Captive Medical Stop Loss

• Organ Transplant

We’ll find the right answers together so no matter what happens, your business is prepared.

By Laura Carabello

Written By Kendall Jackson

Written By Lara Carabello

By Bruce Shutan

(ISSN

Written By Alston & Bird Health Benefits Practice

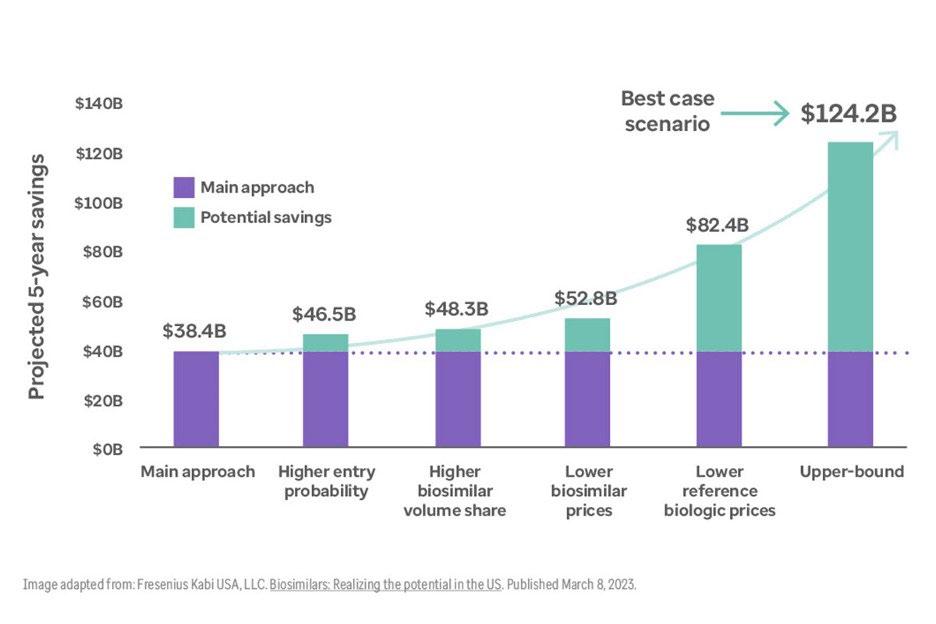

Biosimilars Offer Potential for Significant Savings for Health Plans

TheTWritten By Laura Carabello

buzz around biosimilars and their potential for health plan savings has been building since these drugs entered the market in 2015.

Fast forward to April 2025, when the US House Ways and Means Health subcommittee on the health of the biosimilar market reported that biosimilars had saved the entire US healthcare system over $23.6 billion. Committee members anticipate that biosimilars are poised to save the health care system up to $181 billion over five years if they are able to be adopted – although projected savings differ, depending upon the source, as shown to the right.

Witnesses testified that biosimilars lead to a 53 percent reduction in the average sales price for both the name brand and biosimilar medication and have added 344 million more days of therapeutic care than patients would have otherwise received. They reported that biosimilars launched at prices up to 35 percent lower than branded drugs and can drive further savings when they compete with drugs already on the marketplace. Biosimilars, say the legislators, will provide safe and effective treatment options for patients.

WHAT IS A BIOSIMILAR?

The Food and Drug Administration (FDA) defines a biosimilar as a biological product used in the prevention or treatment of disease and highly similar to an FDA-approved biologic (known as a brand reference product).

Biosimilars are medications with complex manufacturing compared to traditionally developed medications. They are intricately designed molecules that must demonstrate clinical similarity to their brand reference product. Biosimilars increase competition within a therapy class and will often drive down costs over time.

The biosimilar has no clinically meaningful difference from a reference product and is FDA-approved for use after rigorous evaluation and testing is demonstrated by the manufacturer applicant.

Source: Epiphany Rx

Lawmakers also contend that biosimilars help to increase drug supply and availability and have been used in nearly 700 million days of patient therapy. The committee calls for significant efforts going forward to ensure access -- from making drug reimbursement systems work correctly to incentivizing market competition to improve education and awareness among patients and providers.

As prescription medications represent the most influential part of the health plan spend, Glenn Fisher, CEO, NavMD, believes that biosimilars present a high-value, clinically equivalent alternative to costly biologics—especially in managing autoimmune conditions.

Glenn Fisher

Better outcomes. Long-term cost savings.

Mayo Clinic Complex Care Program

experienced a change in diagnosis 52% avoided a locally recommended surgery 23% 85% experienced a change in treatment plan

Discover how a customizable center of excellence program can help minimize healthcare costs while o ering high-cost, high-risk members exactly the care they need.

The Mayo Clinic Complex Care Program is for a small subset of a population with serious, complex or rare conditions who need subspecialized expertise that may not be available locally.

Learn more by calling 507-422-6103 or visit us online at mayoclinic.org/complex-care-program

“To maximize their impact, data analytics is key,” says Fisher. “By analyzing claims data, organizations can identify high-cost biologic utilization, model cost-savings scenarios, and track biosimilar adoption trends. Integrating clinical outcomes data ensures biosimilars are delivering comparable results.”

He observes that some employers are realizing 15–30% savings with no drop in care quality, noting, “PBMs are leveraging data to redesign formularies, align incentives, and drive education campaigns. Biosimilars do drive value without compromising outcomes. With data in hand, the question isn’t can you take advantage—it’s, will you?”

As more manufacturers continue to enter the biosimilar market, plan sponsors have unprecedented opportunities to control costs while maintaining access to the therapies members need most.

Beckie Fenrick, Pharm D, MBA, chief pharmacy officer, Navion, affirms, “Biosimilars deliver substantial market value—and at Navion, we strongly recommend that plan sponsors embrace proactive strategies to promote biosimilar adoption. By driving utilization toward clinically equivalent, lowercost options, organizations can enhance both affordability and access across their populations.”

She says biologics are a cornerstone in treating many autoimmune conditions—yet their high costs are often a barrier to care, adding, “The introduction of biosimilars has the power to reshape this landscape, injecting meaningful price competition and driving down treatment costs for patients and plan sponsors alike. Biosimilars make advanced therapies more accessible, ensuring that cost does not stand in the way of care.”

WHAT’S THE DIFFERENCE? BIOSIMILARS VS. GENERICS

Both biosimilar and generic drugs are unbranded versions of existing medications offered at lower costs. Biosimilars and generics are each approved through different abbreviated pathways that avoid duplicating costly clinical trials. However, biosimilars are not generics, and there are important differences between biosimilars and generic drugs.

Biosimilar drugs describe large-molecule medications that are extracted from living organisms and are often overly complex medications such as vaccines. Generic drugs involve small-molecule medicines, such as aspirin or ibuprofen, which use synthetic chemicals and are much simpler to reproduce.

Generics and biosimilars account for 90% of prescriptions dispensed in the US but only 13% of total drug spending, and their widespread adoption over the last decade has saved the healthcare system an astounding $3.1 trillion, reports the Association for Accessible Medicines.

Sources: 2025 Amneal Biosciences; Medical Packaging.

Beckie Fenrick

WHY BIOSIMILARS ARE FALLING BEHIND

Despite their proven value, biosimilar adoption has been slow, and there is a lot of finger-pointing to account for this trend. An AMA Journal of Ethics cites one strategy originator manufacturers have employed to limit biosimilar uptake: negotiating formulary exclusivity with payers. In one lawsuit, the originator manufacturer entered into contracts with commercial payers to exclude biosimilars from drug formularies or include “fail first” provisions, which would require a patient to have failed on the original product before a biosimilar could be reimbursed.

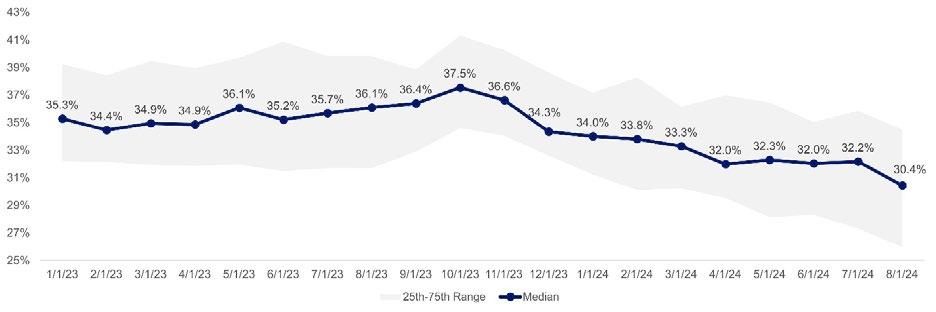

According to the Segal 2025 Trends Report on Biosimilars, for medications with available biosimilars, generally, less than 10 percent of prescriptions have been for a biosimilar. However, the percentage increased significantly in Q2 2024, resulting from changes in pharmacy benefit manager (PBM) practices.

Consequently, they say, rebates create a perverse incentive where physicians are able to make money on the higher-cost drug because of the rebate, while biosimilars are "underwater" because the physician's reimbursement is less than their cost. Relatedly, insurance plans with a PBM frequently limit the number of biosimilars covered by their formulary, which further restricts patient and physician choice.

Biosimilars as a Percentage of Monthly Biologic Prescriptions

Source: 2024 Segal’s SHAPE data warehouse, https://www.segalco.com/consulting-insights/q1-2025-trends-focus-biosimilars

Advisors at Segal say that manufacturers often use stalling tactics to delay the launch of competing biosimilar drugs, utilizing various tactics that include patent litigation and settlement agreements that effectively extend the monopoly period of the originator biologic. These tactics, often referred to as "stalling tactics," can include exploiting patent loopholes, engaging in "pay-for-delay" schemes or utilizing complex “patent thickets” to create an overlapping of patents that makes it difficult for others to develop or commercialize competing products without infringing on those patent rights.

Segal also says the way biosimilars are positioned within the formulary and represented in the PBM contract may discourage their use. To maximize rebates, PBMs and insurers may favor more expensive brand-originator products over lower-cost biosimilars.

As a result, the rebates create a contrary incentive where physicians are able to realize profits on the higher-cost drug because of the rebate, while biosimilars are marginalized because the physician’s reimbursement is less than their cost. Health plans with a PBM frequently limit the number of biosimilars covered by their formulary, which further restricts patient and physician choice.

Additionally, Segal advisors voice concerns that prescribing providers may be hesitant to convert to biosimilars due to efficacy concerns and often find inconsistency in insurers’ policies. Some physicians may not want to disrupt a prescription for a patient whose condition is stable, while patients may be reluctant to switch because they don’t understand biosimilars, including their safety, efficacy, and potential cost savings. Plan sponsors may also wish to avoid disrupting participants’ treatments.

WHAT IS AN INTERCHANGEABLE?

A manufacturer developing an interchangeable product must demonstrate that its product is expected to produce the same clinical result as the reference product in any given patient. Evaluation is required to determine the risk of administering a product to a patient more than once. This assessment is critical in terms of the safety and reduced efficacy of switching back and forth between an interchangeable product and a reference product.

While pharmacy laws and practices vary from state to state, interchangeable products may be substituted at the pharmacy level without the intervention of the healthcare provider who prescribed the reference product. A healthcare provider can also prescribe an interchangeable product just like they would prescribe a biosimilar or a reference product.

Source: 2025 Drugs.com

The Biosimilars Council cites two additional barriers to biosimilar adoption:

• Regulatory Burdens: The FDA’s approval process for biosimilars is still plagued by redundant and costly requirements, including unnecessary clinical efficacy studies and confusion about biosimilars vs interchangeable biologics. This slows down development and drives up costs, deterring investment in biosimilar pipelines.

• The Inflation Reduction Act’s Unintended Consequences: Instead of fostering biosimilar adoption, the IRA’s drug pricing policies have actually discouraged development by making it less financially viable for manufacturers to enter the market.

The new IQVIA report identifies yet another challenge with respect to sites of care (SOC). Hospital outpatient departments–which typically receive higher overall payments than physician offices–are less likely to adopt biosimilars, in part driven by higher relative reimbursement ratios for reference products. Furthermore, a Bernstein Research report finds that hospitals increase the charges for reference products with biosimilar competition more than for biosimilars. This creates a financial incentive for hospitals to stock reference products.

The highly anticipated Stealth State of the Market Report

Leveraging exclusive thought leadership and insights derived from our $2.3B+ portfolio of stop-loss business, along with data from leading stop-loss carriers and industry surveys, our report offers timely intelligence on market trends and actionable insights to help you stay at the forefront of meeting your clients’ needs.

This years report explores:

Economic Conditions

High Level Market Outlook

Strategic Stop Loss Procurement & Renewals

High Cost Claim Conditions

Cell, Gene and CAR-T Therapies

Carrier Insights

Exclusive Benchmarking Data from Stealth’s Book of Business

Recommended Best Practices and much more!

Sabine Enright, PharmD, VP of Integration, Payer Business Unit, AscellaHealth, shares, “The adoption of biosimilars and the optimization of SOC strategies are both highly effective in reducing costs individually. When combined, their impact on cost reduction is significantly greater.”

She says that focusing on both strategies is essential for lowering expenses while ensuring the continued delivery of high-quality patient care and effective disease management: “While both strategies may encounter resistance from members or providers on different fronts, this can be overcome through education and increased awareness in the marketplace.”

Finally, regulatory burdens in the form of the FDA approval process for biosimilars are still plagued by redundant and costly requirements. This includes unnecessary clinical efficacy studies and confusion about biosimilars vs interchangeable biologics, slowing down development, driving up costs and deterring investment in biosimilar pipelines.

AVOIDING THE “BIOSIMILAR VOID”

While biosimilars have delivered billions in savings for patients, employers, and taxpayers, a new analysis from the IQVIA Institute has revealed a massive ‘biosimilar void’: a staggering 90% of biologic drugs losing patent exclusivity over the next ten years have no biosimilar competition in the pipeline.

This year, 25 high-revenue drugs, including Ozempic, Keytruda, and Eliquis, are set to lose patent protection, paving the way for biosimilar manufacturers to expand their portfolios and cater to a growing demand for affordable treatments. Moreover, the Biosimilars Council discloses that 118 biologics will lose patent protection between 2025 and 2034, but currently, only 12 of these medicines have biosimilars in development.

If action is not taken quickly, analysts at these organizations warn that millions of patients will be locked out of potential savings and forced to pay higher prices for essential medications.

THREAT OF PRIVATE LABEL BIOSIMILARS

Concerns have emerged around the growing use of these PBM-driven private-label biosimilars as being detrimental to future biosimilar development. By selling their own private-label products, the PBMs are incentivized to market (and cover) their own products over others, raising issues of transparency and conflict of interest. The biosimilar makers who do not reach private-label agreements with these PBMs may be blocked from sales to a large portion of the covered population, which can jeopardize biosimilar competition and, thus, biosimilar savings for all. Limiting the growth in biosimilars available or closing off a manufacturer’s pathway to future revenue can stunt interest by manufacturers to pursue new biosimilars. Commentary from Dr. F. Randy Vogenberg, Principal, Institute for Integrated Healthcare, and board leader, Employer Provider Council, reveals, “In this scenario, PBMs can sell private-label, low-wholesale acquisition cost (WAC) versions to their employer clients, thereby offering a "savings" opportunity. However, PBMs and manufacturing firms share the remaining revenues with contracted distributors,

Sabine Enright

creating additional income back to the PBM. For example, a product sold at an 80% WAC discount leaves 20% left for revenue sharing with the PBM's distributor and biosimilar manufacturer. This new income to the PBM's parent can offset potential losses to rebate revenue or audit efforts by employer plans.”

Recently, the BR&R Biosimilar Report published an update that demonstrates the impact of PBMdriven private-label biosimilars. Optum Rx will exclude Humira and prefer FDA-approved adalimumab biosimilars effective January 1, 2025, for patients new to therapy. Amjevita®, the unbranded version of this biosimilar, will be the primary biosimilar covered on its commercial formularies and will also be offered as a private-label product through Nuvaila, a subsidiary of UnitedHealth Group. All other adalimumab biosimilars (and Humira) will be excluded from its Premium and Select formularies.

Vogenberg says the promotion of PBMs’ private-label biosimilars may offer some savings today for plan sponsors, but it may also be threatening future savings opportunities, adding, “In the US, employer plan sponsors and their vendors have more than $100 billion in potential savings with a competitive, fully open, and transparent biosimilars marketplace. That opportunity derives from growing biologic patent expirations, increasing access to biosimilars across populations, and eliminating unnecessary middlemen pricing policies that can hinder long-term savings associated with biosimilars.”

IN DEFENSE OF PBMS

“Leading PBMs are deploying a variety of innovative tactics to accelerate biosimilar adoption and drive down drug spend,” says Fenrick, offering the following strategies that not only lower costs but also increase access to life-changing therapies for members:

• Formulary Strategy: Preferring or exclusively covering biosimilars over higher-cost originators.

• Utilization Management: Requiring step therapy or trials of biosimilars before allowing access to reference products.

• Prescriber Engagement: Providing academic detailing and outreach to support evidence-based transitions to biosimilars.

• Specialty Pharmacy Support: Facilitating member transitions with dedicated outreach and copay assistance for eligible members.

• Concierge & Digital Tools: Offering member support services and digital resources to spotlight costsaving opportunities with biosimilars.

• Expanded Pharmacy Access: Including disruptors like Mark Cuban’s Cost-Plus Drug Company to broaden access to affordable medications, including biosimilars.

Jay Gulley, PharmD, President, LeadwayRx, a 20-year-old transparent PBM that utilizes RxLogic claims processing, characterizes the challenge: "The original biologic product has name recognition with the

doctors plus the TV ads and commercials during the Super Bowl that attract consumers. When the drug loses its patent, and depending upon the manufacturer, a biosimilar can be introduced. Initially, there may not be significant adoption, but when employers start to calculate the savings of adding a biosimilar to the formulary, they are readily convinced."

He says PBMs typically support the employer in evaluating the opportunity. Some self-insured companies may not want to make any of their members switch to a biosimilar, while others say they need all the savings they can get and want the least expensive option – although the least expensive option is still costly.

STELARA

Everyone working or observing the biosimilar industry is watching the seven FDA-approved Stelara biosimilars, with two others under FDA review and a third in late-phase clinical development.

Some analysts say the experience that payers have had with Humira biosimilars may make for earlier and broader coverage of the Stelara biosimilars. The catch: No payer has announced plans to remove the brand name Stelara from 2025 formularies.

The uptake of Stelara biosimilars will largely depend on how quickly brand-name Stelara is removed from formularies — not when biosimilars are added — and that may not happen until 2026.

Source: IPD Analytics LLC

A key point of discussion is transparency regarding rebates.

Gulley continues, "Historically, there has been very, very little transparency in that space, but I think it has grown over the last couple of years as the drug spend has continued to climb and become such an issue for employers. People are starting to look a lot closer at these expenditures and wondering why it is so high. It is probably above their medical and hospital spend.”

With so many factors impacting a high drug spend, employers and brokers are really starting to hammer down and look a lot more closely at transparency for rebates.

“There's a big role for PBMs to work with pharmacies -- not against them -- to help lower drug costs for the employers, not just to pull in as much money as they can,” he quips. “PBMs are well-positioned to take on the complex challenges of advancing adoption of biosimilars. There may even be some manufacturers who say if you exclude a certain drug, you're not going to get rebates on any of our other ones. It's a big game. But when you start to see much lower prices, there is no argument. “

When it comes to interchangeability with biologics, he maintains that doctors will prescribe whatever biosimilar the insurance will pay for. Some states will even allow the pharmacist to make that change without a new prescription, while other states still require a new prescription for that particular biosimilar.

“I think there is great potential for biosimilars, especially with the newer pricing models that you're starting to see that carry some very significant discounts as opposed to the original branded product,” says Gulley.

“With more discounts resulting in lower costs, the more utilization there's going to be – and much of that has to do with transparency.”

SCALING THE REBATE WALLS

Rebate “traps” occur when a drug manufacturer pays list price discounts to health plans or pharmacy benefit managers (PBMs) based on meeting market share targets. Health policy analysts at Duke University explain that while such practices appear to lower net costs in the short term for a particular drug or biologic, they also have the effect of blocking patient use of competing, lower-priced products – like biosimilars.

Duke analysts maintain that rebate walls are particularly challenging in the context of biosimilar competition: "While biosimilars are as safe and effective as the originator biologic and offered at a reduced list price, demand for products has been slow to shift from incumbents, especially if clinicians and patients do not regard the products as clinically equivalent. The result can be harmful to patients and the healthcare system through reduced access to drugs that are just as safe and effective but cost less. Furthermore, growth in rebates has been linked to a growth in list prices, and highly rebated products are often accompanied by higher out-of-pocket costs for patients."

Fenrick concurs, “While rebate structures can complicate formulary decisions, the net cost advantage of biosimilars is clear. Many biosimilars are priced 85% to 90% below the originator brands, often yielding deeper savings even after rebates are applied to the innovator. Navion advises clients to carefully analyze net costs, not just rebates when evaluating formulary options. In nearly every case, biosimilars deliver superior value—helping plans achieve both clinical and financial objectives."

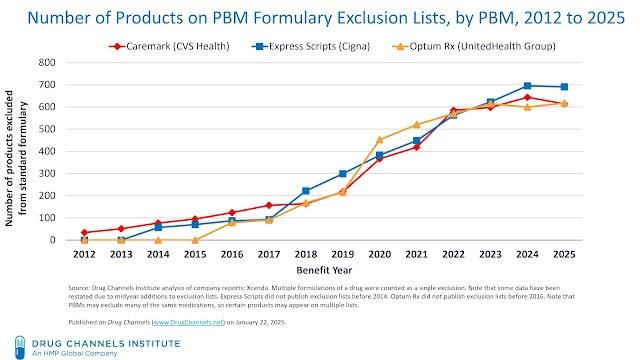

Employers should be aware that CVS/Caremark, Express Scripts and OptumRx have all formed joint ventures to manufacture private-label biosimilar drugs. It may be prudent to confirm that the PBM contract specifies that the formulary includes low-cost biosimilars from companies unaffiliated with the PBM.

PLAN SPONSORS CAN ENCOURAGE BIOSIMILAR ADOPTION

Despite this myriad of challenges, biosimilars are projected to generate substantial cost savings as adoption increases. Segal suggests several strategies that plan sponsors can use to encourage their utilization:

• Education and awareness campaign. Educate stakeholders, including providers, pharmacies, and participants, about the safety and increased availability of biosimilars. Interchangeable biosimilars may be automatically substituted by a pharmacist for the original biologic or reference product, like a generic substitution for brand-name medications, while non-interchangeable biosimilars require prescriber approval. Note that applicable laws vary by state.

• Plan design and utilization management. Revise the plan design to include incentives that encourage adoption. Consider the use of utilization management, such as step therapy, to require patients to try lower-cost options first or prior authorization for expensive biologics and include biosimilars as preferred alternatives.

• Financial incentives. Introduce provider incentives, either through a direct contracting arrangement or by working with the insurer or third-party administrator (TPA) to ensure that the contracted

providers are aware of and are considering biosimilars as a treatment option.

• Formulary management. Place biosimilars in preferred tiers with lower copayments to incentivize their use or remove the originator product from the formulary. Regularly update the formulary to include newly approved biosimilars and remove (or deprioritize) more expensive reference biologics.

• Real-time benefit programs. Consider implementing real-time benefit programs that integrate with prescribers’ electronic health record systems and provide comparative pricing for originators and biosimilars when providers e-prescribe.

• Monitoring and reporting. Ask the medical administrator and PBM for a current utilization report showing biosimilar vs. reference product utilization under both the medical and pharmacy benefits. This will help identify opportunities to encourage more biosimilar use.

Barbora P. Howell, Co-founder & CEO, True Claim, offers this guidance, “Biosimilars offer meaningful savings, but realizing their value depends on making the switch easy for members and financially aligned for all stakeholders. In an ideal world, that means no new prior authorizations, no changes in how the medication is administered, and no revenue compromised by any vendor involved.”

She also thinks that plans should "walk the talk" and offer financial incentives to members, such as lower copays.

“Finally, PBMs must support biosimilar adoption through formulary design and aligned contracting...so selecting the right PBM partner is key,” continues Howell. “When switching to a biosimilar is simple, transparent, and cost-effective, companies and members can save money without disrupting care.”

CHALLENGES AND OPPORTUNITIES

While biosimilars offer significant potential for cost savings, there are also challenges to consider, such as the need to address potential interchangeability issues and the potential for brand-name manufacturers to offer discounts to counter biosimilar competition. The role of members – as healthcare consumers – is equally important.

“Drug costs have increased every year, forcing consumers to evaluate their options,” observes Joe Dore, President, USBenefits Insurance Services. "This would include generic brands and other options, such as biosimilars. Unfortunately, due to financial considerations, some consumers drop the needed medication.”

Today, the cost of prescriptions represents about 20% of the healthcare expenditures on average, as Dore predicts, “This is expected to worsen, especially with increased usage of high-cost drugs, which will only increase the pressure on the employer groups to seek out alternative risk management strategies. It will also force the insurance industry to manage

Barbora P. Howell

Joe Dore

Systems That Don’t Sweat

towards premium adequacy for the additional exposure.”

He invites this topic for discussion on pharmaceutical company earnings, drug distribution channels, PBM models and potential conflicts of interest that affect the cost to the consumer.

The role of providers cannot be discounted. Physicians and hospitals play a critical role in biosimilar adoption, highlighting the importance of examining ways to remove obstacles that may discourage providers from utilizing lower cost biosimilars with their patients.

Source: 2025 Innovative Rx Strategies

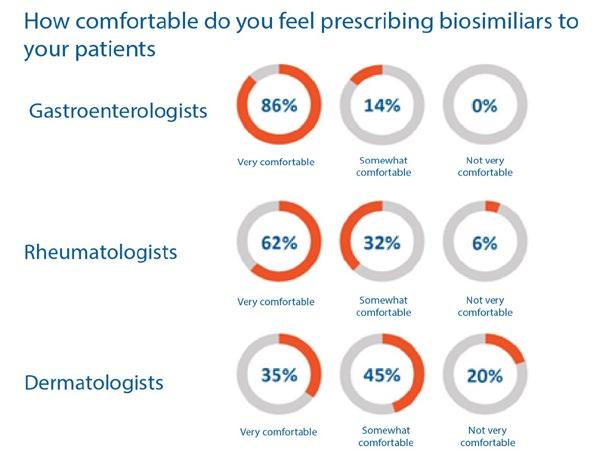

Case in point: In a survey of US rheumatologists' beliefs and knowledge about biosimilars, nearly all respondents were familiar with the FDA definition of a biosimilar product. They were aware that an infliximab biosimilar -- an unbranded version of Remicade indicated for the treatment of adults living with moderately to severely active rheumatoid arthritis (RA) -- was FDA-approved.

Most respondents (84%) understood that an approved biosimilar was not automatically deemed interchangeable by the FDA. Researchers concluded that rheumatologists were more likely to initiate biosimilar treatment for a biologic treatment-naïve patient with RA (73%) than they were to switch to the biosimilar for a patient with RA doing well on the reference product (35%).

Other similar surveys have found that patients are satisfied with the outcomes achieved with biosimilar products, including those patients who had begun treatment on a reference product. The only major concerns reported for switching included not knowing enough about the medication (38%), potential side effects (35%), and loss of disease activity control (35%). Patients still have concerns regarding safety and efficacy, and their involvement in the switching decision-making process may allay concerns and enhance biosimilar uptake.

WHAT TO DO NOW

Kathy Oubre, MS, chief executive officer of Pontchartrain Cancer Center, Louisiana, suggests that the current landscape presents an opportunity for employers to revisit the inclusion of biosimilars in their formularies and to develop strategies that will allow their increased use and/or help manage ongoing utilization.

Employers can play a significant role in promoting biosimilars as an alternative to more expensive biologic drugs, where medically appropriate, by 1) Increasing understanding of biosimilars by health plan

participants and health care providers through education and incentives, 2) Adopting clinical management programs, 3) Designing the payment feature of prescription drug benefits to account for biosimilars 4) Addressing biosimilar drugs when negotiating PBM contracts.

There is widespread consensus throughout the industry that employers can maximize savings from biosimilars. Oubre and others suggest starting with these questions when developing and implementing strategies to promote their utilization and then initiating communications with the PBM to encourage biosimilar use:

• What is my PBM's strategy, and how flexible is it in adopting biosimilars?

• Should biosimilars be added as a preferred or non-preferred formulary option?

• Does a brand or generic copayment apply?

• If the plan offers copayment assistance, how will that impact costs?

• Should it be added only for new patients?

EDUCATE MEMBERS -- ENCOURAGE BIOSIMILAR USE

Bruce D. Roffé, President and CEO, H.H.C. Group, a cost containment company using claim negotiation, repricing, and independent review solutions, suggests that employers can provide meaningful education to plan participants regarding biosimilar adoption, highlighting biosimilar use and potential cost savings as well as real-time benefit lookup tools and cost calculators.

Proactively explain to members who started taking a brand-name version before a biosimilar was available that there should be no adverse impact from switching to the biosimilar.

“With a robust pipeline and steady stream of newly launched biosimilars, plan sponsors may find it appropriate to provide updated biosimilar education and demonstrate how biosimilars fit into their plan benefit design,” says Roffé. "This type of education can also be communicated to healthcare providers as an opportunity to promote awareness and consideration of biosimilars as a preferred treatment option. The FDA is a great resource for these materials, which can be readily accessed at www.FDA.gov/biosimilars.”

REFINE FORMULARY STRATEGY

Ensure PBM formulary includes available biosimilars, will adopt new ones as they are introduced and base their selection on which product offers the lowest net cost to the member and plan. Formularies may exclude coverage for name-brand versions or create a tier that includes them but with significantly higher copays.

Clarify how your plan will handle biosimilars not designated by the FDA as “interchangeable,” meaning

Bruce Roffé

that pharmacists (in most states) can substitute them for brand-name biologics. Confirm that your PBM has procedures to encourage doctors to prescribe biosimilars that haven’t yet been classified as interchangeable. This issue also impacts “rebate credit” since PBMs may use these provisions to reduce your rebate payments if members switch from high-rebate biologics to no-rebate biosimilars.

Require PBMs to be fully transparent about the rebates they receive and return back to the plan. If the PBM is handling Prior Authorizations, confirm that biosimilars are included in the process as a high-quality, less costly alternative to more expensive biologic drugs.

PLAN DESIGN

Plan design can be used to help mitigate growing prescription drug costs with the goal of balancing quality and cost savings. “Tiering” places equally effective drugs in different tiers to incentivize the use of the least costly tiers and is designed to further drive consumerism around the price of a medication. As the number of biosimilars in the market grows, there may be increased use of multi-tier plan designs, especially for specialty drugs.

During PBM negotiations, there may be consideration of inflation-protection caps, which are intended to shield plans from the full impact of year-over-year price increases. This is a good opportunity for employers to understand how their plan’s inflation cap is calculated by the PBM and confirm the PBM delivers these protections to all specialty drugs, including biosimilars.

When it comes to manufacturer rebates associated with biosimilar inclusion, plan sponsors should use this opportunity to ensure that biosimilars are included in rebate payment calculations, review their PBM contract provisions with their benefit advisors and legal counsel and confirm inflation-protection caps and manufacturer rebates.

Finally, employers should confirm that biosimilars are included in the payment provisions of their prescription drug benefit, either through plan design or formulary strategy.

INTRODUCE CLINICAL MANAGEMENT PROGRAMS

By including biosimilars in their utilization management strategies, employers can help safeguard the appropriate use of selected drugs. Prior authorization, one of the most common UM strategies used by employers and payers to contain cost, can advance the adoption of these high-quality, less costly alternatives to more expensive biologic drugs.

Advocacy in Action

Legal services and innovative technology combined to defend health plans, plan sponsors and member participants nationwide aequum advocacy programs & services successfully resolve surprise billing and unreasonable out-of-network and balance billings

Efficient Claim Resolution

On average, aequum resolves claims within just 244 days of placement.

Unmatched Savings

aequum has achieved a remarkable 95.6% savings off disputed charges for self-funded plans.

National Expertise

aequum has successfully handled claims in all 50 states.

| www.aequumhealth.com

No Guarantee of Results - Outcomes depend upon many factors and no attorney can guarantee a particular outcome or similar positive result in any particular case.

As noted earlier, Site of Care (SOC) management is also a viable clinical management program, enabling employers to evaluate the cost differences among hospitals and community-based practices that dispense the same drug. Several studies show that the outpatient hospital setting incurs higher charges than community-based physicians or home-based administration for the same treatment. This cost differential could lead to potential savings for employers through site-of-care analysis, plan design, and contracting strategies, which avoid high-cost settings.

EMPLOYERS FOLLOW MARKET TRENDS

As of April 30, there have been 74 biosimilars approved by the US Food and Drug Administration (FDA), including at least 15 that are designated by the FDA as interchangeable products. So far this year, 10 biosimilars have already received FDA approval, a robust start on the heels of a record-breaking 19 approvals in 2024.

If the three largest PBMs are any bell weather of what’s in store for biosimilars, they have again each excluded hundreds of drugs from their standard formularies. This blocks access to specific products on a PBM’s recommended national formulary and emerges as a powerful tool for PBMs to gain additional negotiating leverage against manufacturers.

In turn, manufacturers offer deeper rebates to avoid having their products cut from the formulary. A drug’s appearance on an exclusion list does not guarantee that all patients will lose access. Plan sponsors— the PBM’s clients— can choose not to adopt their PBM’s standard formulary but would then face reduced rebates and/or higher plan costs. It is anticipated that each PBM’s formulary will give plan sponsors the option of a high-list-price biosimilar, a lower-priced private label product and a low-list-price unbranded biosimilar. The combination of formulary exclusion and private labels is creating an increasingly puzzling and crowded

biosimilar marketplace. Whether employers agree or disagree, the financial benefits from these private-label products align with the benefits to plan sponsors and patients. The complexity of the drug pipeline and market dynamics means progress for biosimilar adoption is gradual.

Laura Carabello holds a degree in Journalism from the Newhouse School of Communications at Syracuse University, is a recognized expert in medical travel and is a widely published writer on healthcare issues. She is a Principal at CPR Strategic Marketing Communications. www.cpronline.com

Capturing savings from biosimilars: What to do now. | Alliant https://waysandmeans.house.gov/event/health-subcommittee-hearing-on-lowering-costs-for-patients-the-health-of-the-biosimilar-market/

US rheumatologists' beliefs and knowledge about biosimilars: a survey - PubMed Patient Perspectives on Switching from Infliximab to Infliximab-dyyb in Patients with Rheumatologic Diseases in the United States - PubMed https://biopharmaapac.com/analysis/60/5727/25-high-value-drugs-losing-patent-protection-in-2025-what-it-means-for-healthcare.html

The Biosimilar Void: A Crisis in Patient Access and a Call to Action — Biosimilars Council https://medpak.com/biosimilar-vs-generic-drugs/

Why Are Biosimilars Not Living Up to Their Promise in the US? | Journal of Ethics | American Medical Association https://biosimilarscouncil.org/resource/the-biosimilar-void-a-crisis-in-patient-access-and-a-call-to-action/

PBM Private Labeling: A Boon or Bane to Biosimilar Drug Makers? | BR&R https://natlawreview.com/article/sick-healthcare-healthcare-benefit-update-employers-what-watch-2025

Isaac Leanos Member Advocate

Leveraging the Power of Group Purchasing Association

health plans and multiple employer welfare arrangements gaining traction for small and midsize employers seeking to pool risk

WhileWWritten By Bruce Shutan

self-insurance is built on wresting control of an organization’s medical claims from third parties that muddle the supply chain with added layers of cost, some vehicles gain strength in numbers. Small and midsize employers in the 100 to 500-employee range, for instance, may want to pool their risk through a homogeneous or heterogeneous group captive arrangement with like-minded employers and reap dividends from wise investments.

But there also are other self-insured avenues leveraging the power of group purchasing that are better suited to small or midsize groups so they can manage their risks as effectively as large employers.

Two such solutions that allow groups to share resources and have earned renewed attention include association health plans (AHPs), which were developed in the late 1990s and promoted during President Donald Trump’s first term, and multiple employer welfare arrangements (MEWAs), which have survived periodic headwinds dating back to their 1983 creation.

AHPs also may be classified as MEWAs, depending on how they're structured and are considered a type of group health plan that allows small businesses or self-employed individuals to band together (often by industry or geography) through a bona fide association to purchase insurance. They're typically governed under ERISA and can sometimes avoid some Affordable Care Act requirements if classified as a large group plan.

MEWAs, on the other hand, involve two or more unrelated employers that provide health or welfare benefits to their employees under a single plan that can be fully insured or self-insured. They’re also governed by ERISA but subject to both federal and state regulation, often more heavily than AHPs.

These vehicles offer a large enough risk pool wherein healthy enrollees theoretically counterbalance the claims experience involving unhealthy members of the group. Actuaries will develop premiums based on the blend of individuals and their health claims experience that will sufficiently handle each risk pool.

PARSING OUT SIMILARITIES AND DIFFERENCES

While the differences between AHPs and MEWAs are slight from both a regulatory and risk standpoint, deciding whether to adopt one or the other approach comes down to risk pooling, according to David Wilson, president and senior actuary of Windsor Strategy Partners, Inc. He believes groups with fewer than 100 lives “may have some financial benefits from working at a well-run MEWA or AHP vs. staying in a larger insurance pool.”

SIIA Washington Counsel Chris Condeluci estimates that there are at least hundreds of self-insured MEWAs operating today, while Department of Labor (DOL) M-1 reporting forms MEWAs must file suggest that about three million employees and family members are covered by both fully insured and self-insured arrangements. Estimating the number of AHPs is another story. “It’s not easy to get the data or accurate enrollment number,” he explains.

While AHPs and MEWAs are essentially one and the same, he says many MEWAs that could be characterized as AHPs offer a comprehensive range of major medical health coverages that mirror a large employer's benefits offering.

While some arrangements offer a series of limited benefit plans with indemnity, disability, short-term or so-called “skinny plan” coverage that a broker ties into an association, he doesn’t consider them an AHP. That distinction is important because opponents of self-insured MEWAs and AHPs, which include insurance regulators and health insurance companies tied to the fully insured market, argue that they don’t provide good coverage.

EASING PLAN RESTRICTIONS

When Rene Alexander Acosta served as labor secretary in Trump’s first administration, the hope among MEWA advocates at that time was to allow these arrangements to easily cross state lines. That meant breaking free of the patchwork of 50 state regulatory requirements – an aspiration that never was realized.

Bill Dyer, co-founder and VP of member relations for the MEWA Association of America and co-founder and VP of HCP National, who is sometimes known as “Mr. MEWA,” notes that risk-retention groups through which associations acquire liability insurance have been crossing state lines for 40 years.

“I don’t understand why this particular class of business could be any different if they’re meeting the reserving requirements of the state that is also regulating them?” he wonders about MEWAs, adding that it has stunted the industry’s growth.

Asked when it would make sense to adopt a single-employer AHP, Condeluci notes that the DOL treats employers in the same industry that have pooled their purchasing power as a single plan, whereas that’s not the case for non-industry-based employers sponsoring a health plan. However, he adds that actuaries still pool everybody together, irrespective of this distinction.

The first Trump administration sought to treat non-industry-based plans like industry-based ones as part of a single risk pool – a streamlined definition currently being worked on that hope will find its way into congressional legislation. "That would, in theory, increase adoption by providing more legal certainty and less ambiguity for employer members of associations and chambers of commerce and for insurance regulators," he adds.

AHP bills recently introduced in the House and Senate seek to help employers work around federal rules that restrict employers and individuals teaming up to buy health coverage. Sen. Rand Paul’s (R-Ky.) proposal, similar to a health marketplace pool bill he introduced last November, is nearly identical to a version from Rep. Tim Walberg (R-Mich.), who chairs the House Education and the Workforce Committee.

THREAT OF INSOLVENCY

While there are merits to pooling risk, the fact is that it can be a risky business. In groups of about 500 lives, Dyer explains that a few significant catastrophic claims could knock a MEWA upside down, whereas one with 20,000 to 30,000 lives would involve a bigger spread of risk and more predictability. If a MEWA is well run, he says rates will decrease, stay the same or increase only slightly.

Whatever the circumstances might be, he says there are five key ingredients to a successful MEWA. First, an association must have at least $1 million for actuarial and legal expenses, as well as paying for stop loss and having adequate reserves. Secondly, the group has to be fully integrated to a point where it can drive volume very quickly by having at least 1,000 lives but, ideally, 5,000 in order for a greater spread of risk that will help sustain success over the long run. Thirdly, it helps to be located in a state that allows underwriting so that a higher premium can be charged to insure risky health conditions. Finally, it’s important to have adequate stop-loss and liability coverages, as well as hire the right management company to handle compliance.

"That's a huge issue, and there's no clear guidance as to what entity is required to disclose both direct and non-direct fees under the CAA [Consolidated Appropriations Act of 2022)." But it also could be extremely difficult for self-insured plan sponsors to attest what they're paying in fees that are bundled and understand how they're calculated, he explains. Moreover, problems could arise when there's a potential conflict between delegating fiduciary obligation and not periodically assessing plan data.

Apart from the CAA’s impact, COVID also has been a significant factor in that it caused some plans to shut down. For example, Wilson notes that while many MEWAs had enough capital to absorb random fluctuations in their business, they fell short of the mark when it came to the larger impact of the pandemic.

“Nobody anticipated a pandemic, and then the government’s response where maybe they were doing the right thing from a population health standpoint, but plans were asked to cover expenses that were never part of their mandate,” he explains.

Since that time, he says rates have stabilized, and his firm has done several feasibility studies suggesting a desire to expand these plans to more states or start new ones altogether.

Another issue that arose soon after MEWAs were introduced and continues to be a concern involves intentional misrepresentation or fraud. If the fees being paid are nearly 100% opaque, Flores can’t imagine how a group of plans would ever be able to properly identify and reconcile what they’re paying in fees –and, therefore, be caught up in malfeasance.

Steadfast protection for the unpredictable

Our Stop Loss Insurance mitigates the impact of costly medical claims through flexible contracts, customizable plans and a consultative, client-focused approach. Our experience and service in the Stop Loss market has provided a guiding hand for 50 years - while maintaining a pulse on new trends. We work with self-funded groups down to 100* lives and individual deductibles down to $25,000. Our Stop Loss Edge program offers an innovative way to take advantage of self-funded health plan coverage for employers with 100*-500 employees. Whether you’re carving out Stop Loss for the first time or an experienced client looking for cost containment solutions, we can help. We’ll be by your side every step of the way.

Visit voya.com/workplace-solutions/stop-loss-insurance for more information

* 150 enrolled employee minimum for policies issued in CA, CO, CT, NY, or VT.

When Healthcare Works as ONE, Patients, Payers, Providers,

Plans

and

“I think there’s ample legal evidence over the past few years that this is actually happening,” he observes, noting that many employers are suing carrier TPAs that are refusing to provide them any clarity with respect to their own plan data. “Ultimately, they may be suing them because they know that they’re probably going to get sued themselves by their own members if they don’t go after this money.”

Other issues beneath the surface that must be addressed include whether a group or trustees will be tasked with hearing and deciding on an appeal that complies with ERISA and who is liable if that process is not followed. “It just creates a Pandora’s box of issues as to who’s accountable,” he says.

Where captives would be more useful than AHPs or MEWAs is when small employers actually purchase medical stop-loss insurance through the captive – a growing part of the market – and the price tag makes more sense to them.

"The reason why it's not a MEWA is because stop loss is not major medical coverage, and therefore, it doesn't meet the definition about distinguishing major medical vs. limited benefit plans," Condeluci explains. Those small employers that worry about plan administration, want to be hands off or feel it’s important to support their trade association will want to choose an AHP or MEWA, he adds.

STATE OBSTACLES TO PLAN CREATION

Dyer, meanwhile, laments the sad state of affairs in some states where insurance companies with tremendous political power create barriers to even starting a MEWA. In California, where he's based, it costs $5 million just to launch a MEWA. "Who has that kind of money?" he asks.

He admits "there was a lot of shenanigans going on" in the salad days of MEWA when brokers would naively start them, not realizing they had to go through their state department of insurance and the federal government. Some nefarious brokers, along with other individuals, would even charge steep commissions, keep premiums, and not pay claims. "Most of the stop-loss insurers told us to get lost because they thought MEWAs were prone to fraud and abuse," Dyer reports.

But today, he says the majority of MEWAs are legitimate, and many have been around for a very long time. They're subject not only to state regulatory requirements but also filing with the DOL, which he says does its share of audits to catch illegal activities.

One caveat to consider along the way to starting a MEWA is the importance of vetting stop-loss carriers. “We have seen three clients that had claims denied because the insurer used language in their policy that is oriented toward a self-insured single employer, not a MEWA,” he says. Employers, therefore, need to know what a MEWA is, how to find the right stop-loss insurance and how to get an insurer to rewrite their policy.

Being in a self-insured MEWA can be a costly proposition for employer members relative to a fully insured MEWA arrangement because they’re the ones that hold all the liability as fiduciaries, even though another service provider is being paid to adjudicate claims and fill in some of these roles, Flores cautions.

Without clear guidance from the federal government on who’s responsible for what in a MEWA, he believes it opens the door to chaos. However, he doesn’t expect any clear guidance from the Trump administration because it’s not a simple issue, nor is it a priority relative to the dozens of other new policy initiatives that have been seeded.

“The best people in the country disagree about the best ways to do this – even those with the best intentions,” Flores opines. "We need a sophisticated advocate on the government side who understands this and, at minimum, could provide accountability."

Bruce Shutan is a Portland, Oregon-based freelance writer who has closely covered the employee benefits industry for more than 35 years.

You know the name — let’s talk numbers. Here’s what sets us apart as a true plan administration partner:

Some firms are just now introducing themselves to TPAs. The Phia Group has been building partnerships for years and our results speak for themselves.

3x More cases identified (1 per 150 EEs)

5x More dollars recovered ($25 PEPM)

of services designed for TPAs

We don’t just identify opportunities — we deliver outcomes.

BUSINESS ASSOCIATE AGREEMENTS -A CASE EXAMINING OBLIGATIONS

IWritten By Kendall Jackson

In the self-funded industry, the prevalence of business associate agreements (“BAAs”) is undisputed, as covered entities and business associates regularly execute them. The Health Insurance Portability and Accountability Act (“HIPAA”) generally requires covered entities and business associates to enter into contracts with their business associates. The BAA is integral to the relationship between a covered entity and business associate, as it defines the contractual obligations for the use and disclosure of protected health information (“PHI”).

Elements of a BAA are quite standard, although the parties do have some flexibility when drafting other contractual provisions, such as indemnification or audits language. As for the standard elements, HIPAA lists ten mandated provisions that must be included and also generally requires that the contractual language adequately establish the permitted and required uses and disclosures of PHI. These provisions are not only essential for compliance with HIPAA but are also important when considering the liability of the business associate. Deviating from the uses and disclosures permitted in the BAA or those required by law can have significant repercussions and may result in civil or criminal liability.

Through a complaint filed on April 11, 2025, in the United States District Court, Western District of Texas, Austin Division, a business associate recently experienced this situation. In CareNexa, LLC v. Ntirety, Inc., CareNexa, LLC, dba Molecular Testing Labs (“MTL”), alleged that its business associate, Ntirety, Inc., failed to safeguard the PHI of its patients and satisfy the indemnification provision within their BAA. Within the complaint, MTL asserted its identity as a “covered entity,” as defined by HIPAA, by virtue of being a healthcare provider that collects, manages, and stores PHI. The complaint notes that Ntirety, a data hosting and security provider, is a business associate of MTL. As such, the parties entered into a BAA on September 28, 2018.

MTL’s complaint discusses Ntirety’s alleged failure to use appropriate safeguards to prevent the unauthorized use or disclosure of PHI, a provision that is required to be within the BAA. As noted above, of the ten mandated provisions, HIPAA requires that the BAA state that the business associate will “use appropriate safeguards and comply, where applicable, with [the HIPAA Security Rule] with respect to electronic protected health information, to prevent use or disclosure of the information other than as provided for by its contract.” Guidance from the United States Department of Health and Human Services (“HHS”) indicates that the phrase “appropriate safeguards” includes reasonable and appropriate administrative, physical, and technical safeguards for securing electronic PHI. Rather than dictating specific safeguards, HHS provides that, when establishing such safeguards, regulated entities should consider several factors, such as the entity’s size, capabilities, technical infrastructure, hardware and software security capabilities, security costs, and the probability of potential risks to electronic PHI.

MTL alleges that Ntirety failed to implement these administrative, physical, and technical safeguards, resulting in a violation of the BAA and the HIPAA Security Rule. MTL’s allegation is based on information it received notifying it of a material breach of data that was required to be secured by Ntirety per the BAA. The forensic investigation performed at the request of MTL indicated that electronic PHI under Ntirety’s management, control, and protection was obtained by unknown threat actors.

As a result of this breach, the threat actors demanded a ransom payment from MTL. Failure to pay the ransom would result in public disclosure of the electronic PHI. MTL insists that the investigation confirms that the threat actors took advantage of the deficiencies in Ntirety’s safeguards, allowing them to access PHI from both Ntirety’s and MTL’s computer systems. Consequently,

MTL argues that the investigation’s findings are evidence of Ntirety’s violation of the BAA and the HIPAA Security Rule.

MTL’s complaint also asserts that Ntirety breached its obligations under the BAA by failing to indemnify MTL. As noted above, the indemnification provisions within a BAA are separate from HIPAA's required provisions, and the parties may draft the language in a mutually agreed-upon manner. The complaint offers a glimpse into the BAA by describing the relevant portions of the indemnification provision for purposes of Ntirety’s alleged breach. MTL asserts that the relevant contractual provisions require Ntirety to indemnify and hold MTL harmless from any losses, expenses, damage, or injuries sustained as a result of Ntirety’s breach of the BAA, including any unauthorized use, disclosure, or breach of PHI, as well as Ntirety’s negligence or failure to perform its obligations as a business associate under the BAA and HIPAA. MTL outlined a series of damages it has or will incur and seeks indemnification from Ntirety.

This case is in its infancy, as it was only filed last month. It is important to note that with only the complaint and no response yet filed on behalf of Ntirety, the situation is only represented through the point of view of one party, and Ntirety’s position remains unknown. Despite being in its early stages, the themes within this complaint function as key reminders for both covered entities and business associates.

The complaint emphasizes the importance of a BAA as a means of protecting the covered entity when PHI may be mishandled by the other party. It also creates awareness for business associates to confirm they are utilizing processes that are thorough and adequate for the safeguarding of PHI under HIPAA and their BAAs. Fundamentally, implementing appropriate safeguards is necessary for compliance with HIPAA, but this case serves as a reminder that adequate and appropriate safeguards can insulate the business associate from what could otherwise be a source of contractual liability for the business associate under the BAA.

Kendall Jackson is a Health Benefits Consulting Attorney with the Phia Group.

Do you aspire to be a published author?

We would like to invite you to share your insight and submit an article to The Self-Insurer! SIIA’s official magazine is distributed in a digital and print format to reach 10,000 readers all over the world.

The Self-Insurer has been delivering information to top-level executives in the self-insurance industry since 1984.

Articles or guideline inquires can be submitted to Editor at Editor@sipconline.net

The Self-Insurer also has advertising opportunties available. Please contact Shane Byars at sbyars@ sipconline.net for advertising information.

Proceed With Confidence Mind Over Risk

We study it, research it, speak on it, share insights on it and pioneer new ways to manage it. With underwriters who have many years of experience as well as deep specialty and technical expertise, we’re proud to be known as experts in understanding risk. We continually search for fresh approaches, respond proactively to market changes, and bring new flexibility to our products. Our clients have been benefiting from our expertise for over 50 years. To be prepared for what tomorrow brings, contact us for all your medical stop loss and organ transplant needs.

Tokio Marine HCC – A&H Group

HCC Life Insurance Company operating as Tokio Marine HCC – A&H Group

PREVIEWING THE FUTURE OF HEALTH SCREENINGS

NWritten By Lara Carabello

No-cost-share coverage for preventive care and health screenings may have narrowly escaped the chopping block as the Supreme Court of the United States (SCOTUS) seems likely to uphold a key Affordable Care Act (ACA) mandate.

But the jury is still out.

Hearings held in mid-April and then again in May -- Kennedy v. Braidwood Management— focused upon the statutory relationship between the HHS secretary and the members of the US Preventive Services Task Force (USPSTF) – not the value of screenings. The question centers on the issue of whether Congress has 'by law' vested the secretary of the HHS with the authority to appoint members of the USPSTF. The outcome of the case is expected to impact various federal advisory panels rather than on employers' preventive services benefits.

A ruling expected by the end of June will determine the fate of these benefits, affecting employers with 50 or more full-time employees. ACA provisions cover medications and screenings recommended by several sources:

USPSTF: a volunteer panel of experts that works to improve the health of people nationwide by making evidence-based recommendations about clinical preventive services.

Health Resources and Services Administration (HRSA): recommends a variety of screenings for women, including HIV, syphilis, and anxiety and for newborns, encompassing a wide range of heritable disorders; supports screenings for conditions like urinary incontinence and breast cancer, alongside contraceptive care, and domestic violence screening.

Advisory Committee on Immunization Practices (ACIP): a federal advisory committee that develops recommendations on the use of vaccines in the US civilian population.

BACKGROUND ON THE “BRAIDWOOD” CASE

The lawsuit challenged the ACA’s process for determining which services must be covered by health insurance, arguing whether a volunteer expert panel can dictate insurer coverage mandates without presidential or congressional approval. Plaintiffs argued that because USPSTF task force members aren’t appointed by the president and confirmed by Congress, it’s unconstitutional for this body to have the authority to dictate what health insurers must cover.

Instead, they claimed only “principal officers” who go through that process, like the secretary of Health and Human Services (HHS) and those under these officers' command, should have that power. A ruling against the ACA provision could shift power to the HHS secretary, enabling future administrations to approve or veto preventive care coverage, depending upon political priorities.

The lawsuit reached the Supreme Court after the Fifth Circuit Court of Appeals sided with employers, who had argued they should not be required to provide certain services. These employers also challenged the mandate on religious grounds, arguing that the ACA’s requirement that plans cover medication for HIV prevention violated the Religious Freedom Restoration Act (RFRA).

Proponents of the mandate argue that covering these benefits at no cost-share leads to earlier detection of serious medical conditions, earlier medical intervention, and more positive patient outcomes, which can decrease the number of high-cost claims in the population and deter costs. Critics oppose the increased costs to employers/plan sponsors and may also oppose certain preventive services on religious grounds, such as the requirement to cover pre-exposure prophylaxis for HIV (PrEP) or birth control.

While some expect that SCOTUS will uphold the mandate, legal and medical experts say that either way the court decides, the ruling could have profound ramifications for the future of preventive health care in the United States. If SCOTUS sides with the Justice Department, the mandate will remain in force.

But affirming the authority of the Secretary of HHS to overrule the expert panels may empower this cabinet-level executive branch department of the federal government to deviate from

how this policy is implemented. The outcome could give the administration broader latitude to shape the recommendations issued by the entities that were originally established with the goal of providing independent analysis and review.

FATE OF SCREENINGS

Kevin Conroy, the chief executive officer of screening test firm Exact Sciences, thinks that quality rating programs and market forces will cause employers and other payers to continue to cover common cancer screening tests -- even if the SCOTUS kills the mandate.

"Payers are highly motivated to get patients screened," Conroy told analysts during a recent meeting. Screenings are considered a subset of preventive care services and interventions that also include routine check-ups, vaccinations, health counseling and lab tests, all designed to help people stay healthy, detect health problems early, determine the most effective treatments and prevent certain diseases. They also include programs for health monitoring, along with counseling and education to help individuals take care of their own health.

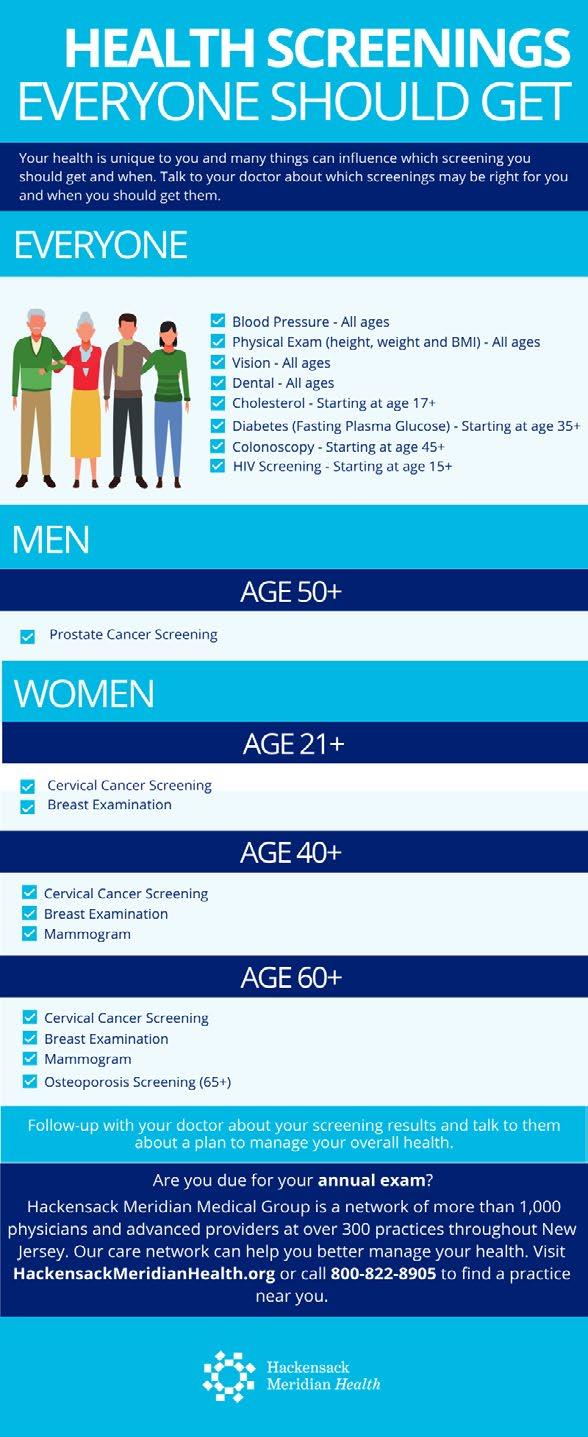

Most health plans extend coverage to a wide range of screenings, including those for cancer, diabetes, cholesterol, and other conditions, at no cost to the employee – no deductible, co-payment, or coinsurance.

The ACA also mandates coverage for women's preventive care, including screenings for cervical cancer and prenatal care. The USPSTF now advises that women should have the option of taking their own test samples for cervical cancer screening, and US regulators recently approved the first cervical cancer testing kit from Teal Health. This test allows women to collect their own samples at home before shipping them to a laboratory to detect the HPV virus that causes cervical cancer. Women in their 20s should get a Pap test every three years, but from age 30 to 65, they can get an HPV test every five years.

On a positive note and further endorsement of the value of screening, a new study presented at the American Association for Cancer Research Annual Meeting 2025 found that mortality from breast cancer decreased in women ages 20 to 49, from 9.70 per 100,000 in 2010 to 1.47 per 100,000 in 2020, even though the incidence has increased. The research attributed the mortality decline to advances in treatment and detection.

Furthermore, USPSTF now recommends physicians screen pregnant and postpartum women for domestic or intimate partner violence, pointing to the value of behavioral interventions to effectively reduce domestic violence in postpartum and pregnant women and women of reproductive age. In a sign of the times, syphilis cases are at a 3-year high despite widespread adoption of screening guidelines as the USPSTF just renewed its recommendation for early and universal screening for syphilis during pregnancy.

At Northwell Direct, a wholly owned subsidiary of Northwell Health, the largest health care system in NY as well as the largest private employer in New York State, Sandy Balwan, MD, chief medical officer, says, “Screening and prevention are foundational and are critical components of our population health strategy. The USPSTF guidelines are built into the foundation of our initiatives, especially those with level A and B recommendations such as breast cancer, colorectal and hypertension screening.”

She insists that screening costs are affordable for most, as many plans are required to cover these tests under the ACA. Common screenings like mammograms, colonoscopies, Pap smears and others are often free of charge to the members if performed in the plan's network.

“By definition, good screening tests should be cost-effective, accurate (low false positive results and false negative results), safe to administer, able to detect a high number of cases or preclinical diseases that are common, have high morbidity and mortality and lead to demonstrated improved health outcomes,” continues Dr. Balwan. “Therefore, if a screening test is implemented, diseases that burden a significant portion of the population would be detected early, lead to improved health outcomes, and lower total cost of care for patients over time.”

She points to one study in which the annual screening of employees and spouses found that for every 10,000 participants screened, 287 (2.9%) had previously unrecognized hyperglycemia (laboratory evidence of diabetes; A1C >6.4% or FG >125 mg/dL), and estimated that within 1 year, for every 1000 patients with confirmed diabetes, about 105 would experience complications. Within 5 years, about 489 would experience complications, including 50 patients with CVD, 68 patients with retinopathy, 168 patients with neuropathy, and 203 patients with nephropathy. The average annual cost of diabetes with complications is about $30K.

SOCIAL MEDIA MISINFORMATION

In a cross-sectional study of social media posts on Instagram and TikTok, most posts about five popular medical tests were misleading or failed to mention important harm, including overdiagnosis or overuse. As reported in JAMA, the tests included full-body magnetic resonance imaging, the multicancer early detection test and tests for Anti-Mullerian hormone (produced by the ovaries in females and the testes in males}, gut microbiome, and testosterone.

WHAT’S AT STAKE?

Self-insured employers have a vested interest in keeping employees healthy since the price tag that accompanies extensive and pricey medical care can impact their health plans with significantly higher financial burdens than preventing medical emergencies or diseases with a routine check-up or screening.

Joe Dore, President, USBenefits Insurance Services, emphasizes, “It’s likely that everyone agrees that any preventative healthcare measure is a positive to ensure illness is discovered in the earliest possible stages. Simple coughs, aches, and unexplained illness can be signs of serious concerns, such as autoimmune issues, heart disease, diabetes, cancer, and mental health.”

He says health screenings should be a part of an annual check-up, noting, “However, for most people, this isn't the case and is often unaffordable. Healthcare screenings should become a part of an employer's wellness program, possibly with some form of financial assistance and/or incentives to encourage this practice. This is especially true for self-funded groups, who can have more control of their risk management and financial objectives.”

Reinstating cost-sharing or declining coverage for screening services would discourage preventive care and increase costs for those who receive them, according to a report from the Employee Benefit Research Institute (EBRI). As a leading nonpartisan, tax-exempt organization dedicated to research and education on employee benefits, EBRI expressed concern that reintroducing cost-sharing could deter care on the individual beneficiary level and likely worsen health inequities, with little impact on employers’ overall spending.

Joe Dore

A CLOSER LOOK AT SCREENINGS

“The most valuable screenings are those that target conditions that can lead to chronic diseases, such as diabetes, hypertension, and high cholesterol,” offers Dr. Balwan. “Early detection through screenings like blood pressure checks, cholesterol panels and glucose tests can help prevent the progression of these conditions, which are often costly to manage long-term.”

She adds that cancer screenings, such as breast cancer and colorectal cancer, are crucial for early detection and can save lives by identifying cancers before symptoms appear or in early stages, where treatment can be curative. The value of these screenings lies in their ability to catch potentially serious conditions early, leading to better outcomes and lower treatment costs in the long run.

Source: Hackensack Meridian Health

CANCER

The American Cancer Society stresses that early detection of breast and cervical cancer through screening can improve survival and reduce mortality by finding cancer at an early stage when treatment is more effective and less expensive.

One study of the patient population of Kaiser Permanente of Northern California affirmed that when free cancer screenings became available, the incidence rate of colorectal cancer declined by 17%, and outcomes have improved. Moreover, the CDC said that modern mammography programs can lower breast cancer mortality by more than 40%, and Pap smears have helped to decrease more than 50% in cervical cancer incidence and mortality over the past 30 years.

What’s especially relevant and sometimes troubling for employers is that cancer is occurring in more adults at younger ages— before they turn 40 or 50 and sometimes even earlier. Researchers at Yale Medicine

characterize this trend as “early-onset” cancers, which are diagnosed in adults between the ages of 18 and 49. Because advancing age is the top risk factor for cancer in general, they view the recent rise in early onset as worrisome.

A new government study conducted by scientists from the National Cancer Institute provides the most complete picture yet of early-onset cancers in people 15 to 49 years old. Findings show the largest increases are in breast, colorectal, kidney and uterine cancers. Of 33 cancer types, 14 cancers had increasing rates in at least one younger age group and about 63% of the early-onset cancers were among women.

When it comes to determining the right age for screening, experts say to be aware of family history. For example, women who are at average risk for breast cancer may start biennial mammography screening at age 40, according to the newest USPSTF recommendations. However, women with a family history of breast cancer are generally advised to start when they are 10 years younger than the first-degree relative (a mother and/or sister) was at their time of diagnosis.

Unfortunately, more women are hearing the words ‘late-stage, invasive breast cancer’ when they’re initially diagnosed. A new study from the Radiological Society of North America finds that late-stage breast cancer, which has metastasized or spread to other parts of the body, is much harder to treat. The results showed women 20-39 years of age experienced the largest annual increase in late-stage breast cancer diagnosis at initial presentation (2.9%).

GENETIC CANCER SCREENINGS

Genetic testing for cancer without requiring a co-payment is a mandated benefit under the ACA for individuals who meet specific criteria outlined by the USPSTF. This includes genetic counseling and BRCA testing to assess the risks of developing breast and ovarian cancer for individuals with relevant personal or family cancer histories.

Up to 10% of cancers are thought to be related to inherited genetic factors and can be readily identified by commercially available multigene tests; as Dr. Balwan points out, “Primary care practices are often a point of contact for patients. As such, they are well-suited to risk-stratify and offer genetic cancer screenings to individuals. Patients with a strong family history of cancer, certain early-onset cancers, or specific genetic syndromes should be prioritized for risk assessment and testing. By preventing more advanced and costly cancer treatment, integrated genetic cancer screenings can be cost-effective in the long run. “

She cautions that it is important for primary care practices to balance this with cost-effectiveness and ensure that genetic screenings are used in the right populations to avoid unnecessary testing. It should be part of a broader personalized care strategy alongside other screenings and preventive measures.

DECLINING CANCER SCREENINGS

Among the reasons cited for patients missing their cancer screening are lack of awareness that they need to be screened for a certain type of cancer, don’t have any symptoms of disease or lack family history of illness. People also express fear of bad news, personal embarrassment, inconvenience, logistical barriers -- difficulty finding a babysitter, taking time off from work, or finding transportation -- and distrust/dislike of doctors or skepticism of the healthcare system, especially among younger adults.

2025 Prevent Cancer Foundation Survey: Only half of Americans are getting regular cancer screenings and routine medical care, a significant 10 percentage-point downswing from last year’s survey. Only 65% of women over age 40 had a routine mammogram; just 32% of men are up to date on their

testicular cancer screenings; only 36% of adults said they are up to date on skin cancer checks.

Aflac’s third annual 2025 “Wellness Matters Survey”: Most Americans (94%) put off getting a health check-up or screening. There is also widespread confusion regarding what insurance does and doesn't cover. Previous Aflac surveys show that millennials are most lax about health or wellness screenings, and millennials avoided tests such as pap smears, STD screenings, full body skin cancer exams and blood tests at much higher rates than other generations.

“A UNION ON A MISSION”

Preventative cancer care is not always convenient, especially for employees with unique schedules outside the traditional nine-to-five. Blue-collar workers in industries such as trucking and warehouse and supply can find it challenging to make time for cancer screenings and other types of care because of the amount of time they spend on the road or the timing of their shifts.