Growth of Value-Based Purchasing and Contracting for Cell & Gene Therapies

Get the peace of mind and support it takes to self-fund your healthcare.

Self-insuring your healthcare benefits can open up new possibilities for your business — affording greater flexibility in how you manage your healthcare spend. Trust the expert team at QBE to tailor a solution that meets your unique needs.

We offer a range of products for protecting your assets, your employees and their dependents:

• Medical Stop Loss

• Captive Medical Stop Loss

• Organ Transplant

We'll find the right answers together so no matter what happens, your business is prepared.

By Laura Carabello

Written By Laura Carabello

By Bruce Shutan

Written By Bruce Shutan

(SIPC).

(ISSN 10913815)

Growth of Value-Based Purchasing and Contracting for Cell & Gene Therapies

Editor’s Note: This is the second of a two-part article. Part one appeared in the March edition of the Self-Insurer. Also, for information on this subject, please consider attending SIIA's Cell & Gene Therapy Stakeholder Forum, scheduled for May 27-28 in Minneapolis. Details can be accessed at www.siia.org.

IIMPROVING

ACCESS AND AFFORDABILITY

WITHOUT BANKRUPTING THE HEALTH PLAN

As research and development of these cutting-edge therapies rapidly progress, employers have an opportunity to explore and implement cost-effective approaches for making these therapies available to employees and covered dependents who need them. Strategies include paying over time, negotiating rebates based on the therapy’s effectiveness and buying stop-loss insurance.

Value-based contracts (VBCs), also referred to as risk-sharing or outcome-based agreements, are newer, evolving payment models used by pharmaceutical manufacturers and payers to connect reimbursement, coverage, or payment to a therapy’s actual outcome in a real-world setting. VBCs are performance-based reimbursement agreements between payers/plan sponsors and pharmaceutical manufacturers in which the price, quantity and nature of reimbursement are tied to agreed-upon clinical, intermediate, or economic measurable objective endpoints.

"VBCs can help provide earlier access to therapies for patients while allowing employers, health plans and payers to reduce their uncertainty regarding clinical value and help manage the risk with the therapy and overall financial impact if the therapy was not successful," explains Bob Gilkin, Senior VP, Trade and Specialty Strategy, AscellaHealth. “Additionally, pharmaceutical manufacturers can utilize VBCs to demonstrate the effectiveness of their product while sharing risk for the therapy outcome. VBCs provide a potential solution to address escalating costs and uncertain real-world effectiveness of medications.”

The chart below demonstrates a sample of Value-Based Arrangements.

Value-Based Arrangements

Lenmeldy

$4.25m

Casgevy:

$2.2m

Lyfgenia:

$3.1m

Hemgenix:

$3.5m

Zolgensma

Source: 2024 AscellaHealth

$2.32m

The world’s most expensive drug, a one-time gene treatment for metachromatic leukodystrophy (MLD), that adds a missing gene to the bone marrow cells of children, reversing the condition’s root cause in the brain. Manufacturer offers innovative outcomesand value-based agreements to both private and government insurers to ensure broad, expedient and sustainable reimbursed access.

First cell-based gene therapy employing CRISPR-based gene-editing technology for treating sickle cell disease (SCD) in patients ages 12 and older who have recurrent vaso-occlusive crises (VOCs). Approved first in the UK, followed by the US.

Another cell-based gene therapy for SCD patients aged 12 and older with a history of vaso-occlusive events.

CMS oversees the Medicaid program and introduced a pilot “access model” for expensive CGTs designating sickle cell as its initial focus CMS will negotiate an “outcomes-based agreement” that links payment for a drug to the health benefit it delivers. In sickle cell, for example, the targeted outcomes could be continued elimination of pain crises over time.

First gene therapy, one-time treatment for adults with moderate to severe bleeding disorder hemophilia B.

Manufacturer anticipates discounts, including value-based agreements with commercial payers. Manufacturer and UK's National Institute for Health and Care Excellence (NICE) have agreed the English government will pay for the treatment under an outcomes-based model.

A one-time gene therapy treatment for spinal muscular atrophy (SMA) in children under the age of two

Manufacturer will allow payments over five years, at $425,000 per year, and will give partial rebates if the treatment doesn’t work.

Gilkin advises that VBCs may potentially increase drug costs because the drug therapy costs are typically separated from overall healthcare costs and do not take into consideration the impact of the potentially greater benefits of more expensive therapies on overall patient outcomes and healthcare costs.

“Since payers are responsible for their patients' total cost of care, they need to consider the impact that CGTs may potentially reduce downstream medical utilization costs, longer-term complications and additional healthcare costs that can impact premiums for employers and patients,” he adds. “VBCs may provide an avenue where payer and pharmaceutical manufacturers are aligned and can demonstrate the positive impact of these therapies from health and economic perspectives.”

With the low volume of patients currently impacted by VBCs, Gilkin says it is unlikely that these agreements will directly impact premiums in the near future, noting, “But they hold the potential that if they prove to demonstrate positive health outcomes and show overall healthcare savings, they could positively reduce premiums in the future.”

Jakki Lynch, CCM, CMAS, CCFA, director of Cost Containment, Carbon Stop-Loss Solutions, further explains that in an effort to address the upfront high cost of care and uncertainty of the clinical outcomes, the market has seen an emergence of a broad range of innovative proposed payment models in the form of therapy product carve-outs, pay-over-time methodologies, clinical warranty templates based on retrospective payment adjustments and cost rebates tied to patient outcomes with new market intermediary solution providers that facilitate these services on behalf of all payer types.

“Outcomes-based contracts are the preference but come with ambiguity secondary to challenges on establishing transparent and verifiable outcomes criteria," she continues. "They require substantial resources for tracking outcomes and do not address the total cost of care with provider markup, administration charges and additional costs for potential complications. Certain manufacturers are accepting innovative payments for their therapies, including Luxturna, Zolgensma, Zynteglo, Hemgenix and Roctavian.”

Based on the significant cost and the complexities of the therapies, Lynch says plans need a comprehensive approach that spans the full spectrum of management strategies with specialized financial and clinical resources to manage and mitigate this emerging complex and novel risk.

“Strategic focus and risk assessment should include treatment plan validation supporting optimal member outcomes and covered plan benefits as well as optimal all-inclusive contract rates with favorable terms inclusive of value risk-based rebates,” she advises. “Claim payment integrity microanalysis with comprehensive medical record reviews ensure correct health plan or third-party administrator payments and contract terms compliance.”

Bob Gilkin

Jakki Lynch

Lynch offers the following Branch Contract Optimization + Claim Payment Integrity Review (CPIR) that demonstrates the effectiveness of bespoke specialty financial and clinical solutions to address this complex risk.

Jesse Roderick

Jesse Roderick, senior vice president of Accident & Health Claims, QBE North America. thinks that depending on the plan sponsors’ risk appetite and financial strategy, they may decide to pursue VBCs that align payment with the outcomes achieved by the therapy, making this an effective strategy to manage the high costs associated with treatments while ensuring patients receive effective care.

“These contracts can mitigate some financial risks by tying payments to the therapy's success, making it more feasible for health plans to cover therapies and thereby increasing patient access to potentially lifesaving treatments,” he imparts. “There are several value-based purchasing models in the current market that meet payer requirements. These include outcomes-based agreements, where reimbursement is linked to clinical outcomes, performance-based contracts that require meeting predefined metrics, and installment payment plans which spread the cost over time.”

OTHER NOVEL SOLUTIONS

New programs are being developed to help finance the risk of gene therapy treatments. Many pharmacy benefit managers (PBMs) and carriers offer coverage of gene therapies for a fixed per member per month (PMPM) fee. Some insurance companies are selling Netflix-like subscriptions where companies pay a monthly fee — often less than $2 a month per employee — for access to gene therapy. One large PBM covers 10 gene therapies through a subscription-type model, requiring employers to pay $1.25 PMPM, and the PBM assumes any additional financial risk.

In some instances, a subscription model can also be structured to exclude patients with pre-existing conditions. While state and federal laws prevent insurance companies from denying coverage for preexisting conditions, like the inherited diseases that gene therapies target, organizations that self-insure aren't required to cover all treatments and may reject some as a way to save money.

Years of Powering What’s Next

There are also outcomes-based agreements that offer pricing flexibility through rebates tied to the therapy’s results or a series of payments that can be made over time. These arrangements are typically negotiated with payers or PBMs that offer employers supplemental coverage. Outcomes-based contracting with pharmaceutical manufacturers typically offers milestone-based and performance-based arrangements.

Jeff Auten, director of Clinical Consulting (PharmD) at Leaf Health, concurs that multi-year performance-based contracts will be the mainstay of reimbursement models for gene therapies. “…allowing self-funded plan sponsors to spread therapy cost over several years and annual payments based on defined clinical metrics.”

Lockton, the world’s largest insurance broker, says these solutions will be challenging for employers, especially those with high employee turnover, since the member may leave the plan before the multi-year contract ends. For these payers, milestone-based or warranty-based arrangements may be appropriate, although these solutions may be challenging to operationalize since they require ongoing patient monitoring and a system that connects the provider, payer, and manufacturer to track outcomes and reconcile with the payment contract.

At Custom Design Benefits, Terri Martin and Alberta Manga, Medical & Risk Management, also observe this trend: “Our clients have demonstrated their commitment to value-based contracts during this plan year’s renewals. Employers and health plans are increasingly adopting valuebased contracts to enhance member access to treatment, anticipating that these arrangements will help manage the overall cost and access to quality facilities for their members.”

They do not point to any specific payment model and say there have not been any guarantees associated with the contracts.

“To establish guarantees, members who receive treatment must be monitored by Case Management for at least a year,” they caution. “This ensures that their progress and outcomes can be accurately tracked and evaluated. If a member changes employers, they can no longer be followed. Even monitoring for a year is not enough time to evaluate if the treatment is a cure.”

ROLE OF STOP-LOSS INSURANCE

Lockton maintains that the main payment option to pay for these therapies for a self-funded plan sponsor is their stop-loss policy, which should be evaluated on a year-to-year basis to reflect a material change in experience or price adjustments. They say that none of the carriers are denying coverage outright for CGTs or requiring the plan to transfer the liability to

Jeff Auten

Terri Martin

Alberta Manga

Zero in on catastrophic claims risks.

Curv® can isolate risk above a specified individual stop-loss threshold, giving finely tuned insight into potential high-cost claims. Depend on Curv’s predictive analytics for more accurate pricing across your spectrum of underwritten groups.

rxhistories.com/curv/group-health

another entity, such as a carve-out program. They also say it is critical to align the terms of the underlying health plan and the stop-loss coverage to ensure stop-loss reimbursement of claims related to these expensive treatments.

Stop-loss policies can protect the underlying health plan, at least temporarily, by transferring the risk of high-cost claimants. In some cases, stop-loss insurers can “laser” a specific enrollee or drug to set higher coverage thresholds, effectively removing financial protection for the employer. Consulting actuaries at Milliman observe a slowdown in demand for CGTs and believe the surge will emanate only from patients who tend to have the most severe cases or conditions with no other treatment options. For the foreseeable future, they recommend coverage under traditional means like stop-loss.

Jamie L. Holowka, B.S., Pharm.D., director of Clinical Strategy, Complete Captive Management Services, says that through her experience in medical stop-loss and re-insurance, she has participated in the payment and contracting process of more than two dozen gene therapies and hundreds of cellular therapies.

"I have observed the facts fall out through the medical data showing that some recipients had no response, but serious consequences, other recipients had a temporary response, also with serious consequences, and some had a response for a limited durability (limited amount of time) and supportive therapy, and treatment is still ultimately necessary," she explains. "Because of these lesser discussed outcomes to promote science, manufacturers contract with providers and carriers to authorize the therapies.”

HIGH-COST MEDICAL CLAIMS REQUIRE HIGH-POWERED NEGOTIATIONS

Lower your expenses on in- and out-of-network claims with savings as high as 90%

Our expert attorney negotiating team helps you avoid overpayment and achieve exceptional savings on your claims—even the highest cost treatments.

H.H.C. Group is your trusted partner to verify costs and ensure billing accuracy – more savings on more claims.

Jamie L. Holowka

Between these entities, she says there could be 340b contracts or traditional rebates and outcomesbased contracting. Since carriers may front the payment (at best) but stop-loss (and re-insurance) is the actual payer, she maintains that it is unacceptable that current contract participation does not extend to the stop-loss and re-insurance carriers.

“For all the CGTs, the manufacturer is not able to bill IF they are unable to produce enough product to meet FDA approved specifications (doses),” she continues. “For CGTs, IF a recipient passes away after a pre-determined amount of time, a 100% refund is returned to the carrier. If a recipient dies or the disease progresses, depending on onset and time, the carrier will receive a 75%-100% refund for the therapy.”

Although gene therapies are still limited to a one-in-alifetime dose, regardless of effectiveness, she believes that many providers still maintain or start their competitor therapies before or after the gene or cellular therapy, including bone marrow transplantation and other specialty therapies.

She contends that although we are living in an amazing medical science space, the risk is completely on the employer covering the products while the network retains all the incentives, adding, “For most of these diseases, the only potential

cure remains known to be stem cell transplants, like a bone marrow transplant. Potentially eligible recipients would be so much better served with a donor match campaign.”

Roderick concurs, “The availability of stop-loss coverage can encourage plan sponsors to provide benefits for CGTs. Knowing there is a mechanism to manage the financial risk associated with these treatments makes it more feasible for plan sponsors to include them in their coverage options.”

When plan sponsors partner with the right medical stop-loss insurance providers, he feels it supports the implementation of VBCs by covering the financial risk of high-cost claims.

“This enables plan sponsors to confidently enter into value-based agreements, aligning financial protection with value-based care models to help ensure that members receive the best possible outcomes while managing costs effectively,” he comments.

MANAGEMENT SOLUTIONS

A debate continues on whether to cover gene therapy under the medical or pharmacy component of the plan. Some argue that the pharmacy component enables plan sponsors to better manage the cost, although this option requires a full understanding of the programs that the administrator has in place. For instance, if

outcomes-based contracting is under consideration to cover gene therapy, the medical component of the plan may be preferred since the member’s outcomes will likely be tracked through the medical claims experience.

Lockton cites other management solutions, including providing access to specific, high-value network providers, limiting out-of-network facility coverage, and adding a travel benefit to enable ease of access to high-value providers. Coverage for cancer gene therapy should be accompanied by robust programs for cancer care navigation, expert medical opinion, cancer decision-support services and identification of gene therapy clinical trials for members.

Lockton advisors say it may also be possible for some self-funded employers to cap the amount their plan will pay for specific gene therapy treatments. They explain that the Affordable Care Act’s ban on dollar limits applies only to “essential health benefits” (EHBs), as defined by the plan’s relevant “benchmark state,” and self-funded plan sponsors may choose which state’s benchmark plan they’ll use to determine their plans’ EHBs. Some state benchmark plans, for example, require that merely some, but not all, drugs in a specific therapeutic class be treated as EHBs.

Holowka characterizes CGTs as “interesting progressions and treatment options in the medical arsenal” but cautions, “We are still "scraping the mold off the petri dish; we have not formulated penicillin yet. They are great motivation for the development of other treatments for these rare diseases.

She advises that carrier formularies should be applied as standard to CGTs as they are with any other treatment policy and protocol in healthcare: “Clients should understand that other therapies are not inferior to CGTs and clients should not feel obligated to cover for ALL options of treatments available, when they are all considered equivalent. We need to consider that a handful of recipients does not provide solid evidence of safety or efficacy and that CGT options are being directed at our most vulnerable and most desperate populations.”

COVERAGE: A WEIGHTY LIFE OR DEATH DECISION

Denying CGT coverage triggers many consequences, primarily compliance and public relations risks. Some disabilities-based discrimination claims are surfacing, even if the exclusion is targeted at a member’s dependent. By amending a plan mid-year to exclude coverage because of an existing claim or impending claim, there is a risk of a HIPAA violation. Furthermore, if a self-funded employer chooses to exclude gene therapy but then determines an exception and offers coverage as a result of extenuating circumstances -negative publicity, the child of an executive needing the treatment, etc.-- the claim will not be eligible for stop-loss reimbursement because the service is not listed as covered in the underlying health plan.

Public relations nightmares are becoming all too common since these treatments are now viewed as essential, and many are for children. Imagine the headlines for not covering an FDA-approved gene therapy for a baby with a life-threatening condition with limited, if any, treatment options. When workers think they have coverage and are then denied access to a CGT, there are life or death implications.

OTHER OBSTACLES

Self-insured plans encounter multiple obstacles to providing access to these potentially lifesaving therapies. However, the extended treatment journey for most CGTs is one barrier to utilization since

medical appointments for the individual or their loved ones could interfere with work schedules and requirements.

For example, the infrastructure required to deliver sickle cell therapy is extremely specialized and currently only available at very few centers, typically bone marrow treatment facilities with sickle cell expertise. Younger patients have also been reluctant to embark on the demanding treatment process that lasts more than one year and requires periodic hospitalization – disrupting school schedules and apprehension about adding additional medical burdens to their routines. Furthermore, many sickle cell patients are so advanced in their disease that gene therapy is not clinically warranted.

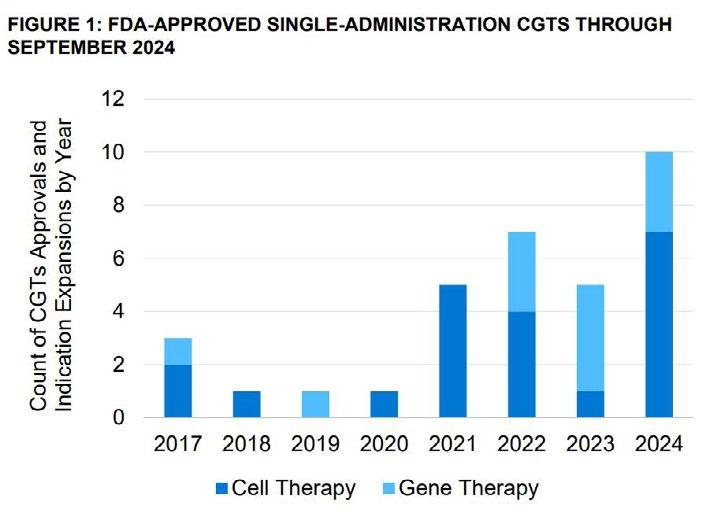

The advent of single-administration (CGTs) has the potential to change the landscape of treatment. A Milliman study reported that the FDA has approved 23 single-administration cell and gene therapies since 2017, totaling 35 approvals with additional expansions. Most approvals have come in the past two years, and roughly 60 more could hit the market in the next three years.

Milliman points out that these gene therapies are typically infused in one session, holding the promise of a cure that would avoid a lifetime of treatment. However, some employers, particularly retailers, hospitality, or trucking companies, where there is a large employee turnover, may hesitate to shoulder the hefty cost of a one-time treatment. Drug manufacturers argue the prices are justified because they offset a lifetime of medical costs patients would otherwise face.

Of the 17 one-time therapies approved by the FDA at the end of 2023, only eight had been used by more than 10 patients, according to Milliman’s analysis of 60 million commercially insured enrollees. Kite Pharma Inc.’s $425,000 lymphoma CAR T-cell therapy Yescarta had the most claims, at just 413 since its 2017 approval.

Source: Milliman DNA Gene and Cell Therapy Forecasting; v3.3.0, September 2024 release.

THE PRICE TAG FOR A CURE

CGTs potentially offer a cure for many diseases for which traditional approaches, medicines and surgery have simply halted disease progression or modulated the course of the disease. For diseases caused by mutations in single genes that a person is born with, it is estimated that there are more than 6,000 such diseases affecting over 350 million people worldwide.

Braving the gene therapy headwinds, attendees at the recent JP Morgan investor conference heard from the Alliance for Regenerative Medicine president Tim Hunt who offered a rosy outlook for CGTs, predicting 10 such treatments will become blockbusters by 2030. Peter Marks, director of the FDA’s Center for Biological Evaluation and Research, commented that 2024 was also a “good year” for gene therapy approvals, emphasizing that the agency is focused on boosting accelerated approvals with the launch of two pilots to aid gene therapies and treatments for rare diseases.

“The industry needs to think differently about CGTs,” says Keri Schoenbrun, Chief Engagement Officer, Actum Pharma, a company founded by a consortium of biopharma leaders that is committed to enabling the development and market introduction of novel therapies that effectively address patient suffering from debilitating and life-threatening conditions. “Because CGTS are in a completely pioneering space, virtually all of these therapies will be unfamiliar, on some level, to the entire ecosystem. CGT companies need to

Leading National TPA

Our decades of experience have taught us how to elevate member health and drive down costs.

How we do it:

• Specialized, in-house teams— implementation through renewal

• Tailored point solutions and a la carte programs

• Custom-built, scalable plans and network options

See what sets us apart from other

Not

Keri Schoenbrun

Better outcomes.

Long-term cost savings.

Mayo Clinic Complex Care Program

experienced a change in diagnosis 52% avoided a locally recommended surgery 23% 85% experienced a change in treatment plan

Discover how a customizable center of excellence program can help minimize healthcare costs while o ering high-cost, high-risk members exactly the care they need.

The Mayo Clinic Complex Care Program is for a small subset of a population with serious, complex or rare conditions who need subspecialized expertise that may not be available locally.

Learn more by calling 507-422-6103 or visit us online at mayoclinic.org/complex-care-program

think differently about many aspects of commercialization, but particularly stakeholder education, which will need to be conducted early and often.”

She says that even companies with deep experience launching products, like small molecule therapies, will need to think very differently about some fundamental work streams, especially payer education.

“Education will be about much more than articulating outcomes,” explains Schoenbrun. “Drug manufacturers need to be prepared to explain diseases that may be treatable for the first time, unique methods of administration and a broader view of benefits to both patients and payers.”

She advises the conversations between CGT’s and payers should begin with a single premise: all options are on the table and none of the parties can be constrained by previous models.

“Start by effectively painting a picture of the overall cost of care,” she continues. “Robust health economics and outcomes research studies may be needed to quantify the full burden of current treatment options relative to the emerging CGT. It starts with data but will likely require working with patient advocacy groups to understand the details and nuance of living with a given condition.”

She cites recent work focused on a rare skin condition where, for example, the cost of bandages alone could reach $25,000 per patient.

Schoenbrun also points to the role of genetic testing, adding, “Expect the role of genetic testing to also evolve. Historically, payers were reluctant to reimburse for genetic testing. But as CGTs evolve, smart payers will increasingly embrace genetic testing as a way to identify patients who are likely to benefit from a given therapy. This becomes an important way for payers to manage the risk associated with high-cost interventions. Drug manufacturers will need to do their part by ensuring related genetic tests are reliable and meet increasingly stringent standards set out by the industry."

A prediction for the future from Schoenbrun: “It is important to remember we are standing at the frontier of a whole new way to treat patients. While some of the costs might seem outrageous now, these are growing pains for the industry. We will soon see improvements in process, automation and testing begin to lower costs for patients and payers.”

Expounding on this topic, Dan Winkelman, Director, Offering Design Suite, IQVIA, says the decision to cover these therapies must be made on a plan-by-plan level and by disease state due to different levels of cost, efficacy, and alternative therapies.

“In some cases, the unprecedented efficacy results in positive economic models due to the likelihood of a reduction of hospital stays and/or reduced need for ongoing chronic care therapy,” he advises. “For example, the economics are seemingly clear for CAR T-Cell therapy for DLBCL because it can replace Stem Cell therapy which involves longer hospitalization (3 months vs. 1 month) and has curative potential, which we call “one and done”.” Another example is Luxturna for RPE65-mediated inherited retinal dystrophies. If patients have the biomarker, then this treatment can cure their blindness, resulting in a significant impact on their lives and their support system.”

Dan Winkelman

STOP LOSS INSURANCE

MANAGE THE RISK.

Prudential’s Stop Loss insurance helps reduce unpredictable risks from self-funded medical plans. This way you can focus on giving your employees the coverage they deserve, while helping to reduce your worries about the increased frequency of catastrophic claims.

Get Stop Loss insurance from a partner you can rely on:

• A highly rated, experienced carrier recognized for 150 years for strength, stability, and innovation

• Efficient, responsive service with streamlined processes across quoting, onboarding, and reimbursements

• A dedicated distribution team that works hand-in-hand with your existing relationships

• Flexible policy options so we can build a coverage plan that meets the unique needs of your organization

Did you know, medical and prescription drug costs are expected to rise 8.5% annually?* See how Prudential can help you manage the risk from your self-funded medical plan.

For more information, contact us at stoploss@prudential.com or visit our website: www.prudential.com/stoploss

In contrast, in other disease areas and therapies, he says the same efficacy could be achieved with lower cost therapies, noting, “One unique factor about these therapies is that they tend to target smaller patient populations which can buffer the budget impact despite the individual high cost of the treatment. Innovative models are required to understand the true value of treatment and must be updated regularly.”

Laura Carabello holds a degree in Journalism from the Newhouse School of Communications at Syracuse University, is a recognized expert in medical travel and is a widely published writer on healthcare issues. She is a Principal at CPR Strategic Marketing Communications. www.cpronline.com Get the most out of your healthcare plan and finding cost-saving opportunities with PAI Analytics.® Visit paisc.com to learn more.

Brad Hansen VP of Provider Relations

Questioning Authority

High court ruling that limits grip of federal agencies could affect regulatory landscape for self-insured employers

BBefore

Written By Bruce Shutan

Donald Trump won a second term as president and vowed to continue disrupting politics, the U.S. Supreme Court seeded a major disruption limiting the authority of federal regulators that continues to reverberate across the self-insurance industry.

In late June 2024, the justices overturned a 40-year-old judicial precedent known as Chevron deference – named after the American multinational energy corporation. In Chevron U.S.A. v. Natural Resources Defense Council, courts were directed to defer to federal agencies' interpretations of ambiguous laws. That practice ended with a 6-3 decision led by Chief Justice John Roberts in Loper Bright Enterprises v. Raimondo. Although widely applauded, it also has stirred questions about compliance with both old and new employee benefit laws.

As such, Loper Bright presents both challenges and opportunities for self-insured health plans, as observed by Kristy Wrigley-Durer, senior counsel at Crowell & Moring. She suggests working closely with corporate counsel or government affairs experts to closely monitor what's happening in the courts in terms of the impact on existing regulation and being nimble in responding to any changes. She's also sanguine about a new pathway to challenge any issued guidance that is considered less favorable and work toward getting out in front of issues by influencing new legislation.

One such opportunity involves reforming pharmacy benefit management practices, which she describes as a hot topic with bipartisan support in Congress. “We’re going to see something on that and probably not just PBMs, but all service providers to ERISA plans,” she surmises.

Fred Karlinsky, shareholder and chair of global insurance regulatory and transactions with Greenberg Traurig, describes the post-Chevron deference climate as a positive development that will help level the playing field when it comes to challenging agencies since courts will view cases from a more de novo perspective, which removes any reliance on previous case law. He adds that it doesn’t mean courts won’t take into account an agency's position; it just removes the practice of deferring to an agency's interpretation of a statute or regulation.

“I think that keeps true the notion that there are three separate but co-equal branches of government” wherein each one will stay in its lane to work in the best possible way, Karlinsky says. In effect, he believes it will help protect innovation and be good for consumers of products and services in the self-insurance space.

His experience with this issue actually dates back to 2017 and 2018 when serving on Florida’s Constitution Revision Commission during which time voters

overwhelmingly supported a ballot measure overturning Chevron deference in Florida.

FOCUSING ON NEW REGS

What the Loper Bright case essentially means is it will be easier to argue that newer issued regs are arbitrary and capricious than those that have been in place for at least three years or more and were subject to Chevron deference, explains SIIA Washington Counsel, Chris Condeluci. One example is that the provider community has filed a lawsuit over surprise-billing rules in the No Surprises Act and could challenge other parts of the law now that Chevron deference has been overturned. The other involves mental health parity.

“We thought that the administration exceeded its authority and rewrote the statute through the reg – irrespective of Chevron deference,” he says. “We would have argued that anyway but feel that much more confident in our legal arguments in trying to get the reg set aside based on Chevron deference and a recent lawsuit spearheaded by the ERISA Industry Committee [ERIC].”

Advocacy in Action

Legal services and innovative technology combined to defend health plans, plan sponsors and member participants nationwide aequum advocacy programs & services successfully resolve surprise billing and unreasonable out-of-network and balance billings

On average, aequum resolves claims within just 244 days of placement. Unmatched Savings aequum has achieved a remarkable 95.6% savings off disputed charges for self-funded plans. National Expertise aequum has successfully handled claims in all 50 states.

ERIC filed a lawsuit in January that seeks to invalidate the final rule issued under the Mental Health Parity and Addiction Equity Act of 2008 and the Consolidated Appropriations Act of 2021, known as the CAA. The lawsuit argues that the rule exceeds the Department of Health and Human Services authority, violates the due-process clause in the Fifth Amendment, is "arbitrary and capricious," and violates the Administrative Procedure Act.

Tom Christina, executive director of the ERISA Industry Committee’s Legal Center, hopes there’s a rethinking of these regulations, which self-insured health plans consider highly draconian. “They were drafted in the hopes of impeding non-quantifiable treatment limitations,” he says. Noting that the process of dialoguing with these agencies about these limitations is very prolonged, he says it suddenly picks up speed “almost before the employer knows that they find themselves staring at a determination that they’re in violation, which is a very big deal under the regulations.” That’s because employers are required to inform plan participants within just 10 days of receiving notice that they have violated the statute.

“None of this has any basis in the statutory language, in particular the remedy of notifying your employees,” Christina says. “You could read the act 100 times and won’t find anything that even suggests that the regulatory agencies have that power.”

Mental health parity is the one area where industry practitioners expected some of the first Loper Bright challenges as they would apply to ERISA plans, Wrigley-Durer observes. “It’s interesting to note that the DOL finalized those rules after the Loper Bright decision, and Loper Bright doesn’t seem to have particularly tempered their approach,” she explains. That case didn’t necessarily remove the authority of

agencies, she says, adding that they’re still issuing guidance. “It simply noted that they don’t get to interpret law, which is the role of the courts.”

Overturning Chevron deference has thus far not “opened the floodgates” to ERISA litigation of any kind, including litigation involving self-insured health plans, Christina notes. Loper Bright, however, has quite a few escape hatches, he adds. He's not surprised that a few district courts upheld the application of claims procedures regulations after the Loper Bright case was decided.

There have also been other ERISA cases in which he says enunciate principles that, if applied to self-insured health plan cases, would dampen the effects of Loper Bright. As one example, he cites a recent court decision upholding some Pension Benefit Guaranty Corporation (PBGC) regulations that faithfully follow Loper Bright – stressing “the longevity of those regulations as a reason for upholding them.”

While that case involved PBGC regulations pertaining to withdrawal liability in multiemployer pension plans, he explains that it illustrates how courts have limited the effect of Loper Bright on any area within ERISA, which would include selfinsured health plans.

Christina suggests the chief implication would be to expect

that long-standing regulations, including claims procedures, will be upheld, while fairly recent regulations are more vulnerable to being challenged in court. The best example he can think of involves analyses of non-quantitative treatment limitations for the purpose of achieving mental health parity.

When the Department of Labor issued regulations under ERISA 408(b)(2) in 2012 setting out disclosure obligations for retirement plan service providers, it noted that special guidance would be forthcoming to address the uniqueness of health plans. Part of the challenge is that the DOL may be thinking post-Loper Bright about whether it still has the authority to issue guidance, according to Wrigley-Durer. If Congress passes legislation on PBM reform or service provider disclosures, she expects clarity on what the DOL needs to do in terms of issuing guidance about those disclosures, their level of authority and even how aggressive they want the DOL to be.

In addressing concerns about recent ERISA preemption battles in various states, Wrigley-Durer says it's a statutory issue and is not likely to be implicated by regulations. Noting how ERISA has been around for 50 years, she doesn't expect that there will be huge swings in preemption challenges other than "it's interesting to watch what's happening in the PBM space because that's the first real place we're seeing it being chipped away at a bit."

MORE RIGOROUS REVIEW

Since the Loper Bright ruling is still relatively new, Wrigley-Durer believes it remains to be seen whether it could have a chilling effect on the development of products and services to contain group health plan costs. But she adds that there could be some hesitation to take potentially risky positions based on existing guidance if there’s any concern that it could later be challenged.

It’s worth noting that the Supreme Court itself hadn’t actually cited Chevron in nearly a decade before the Loper Bright decision. “So, there are a good number of practitioners in the space who don’t really view it as that big of a deal,” she says. “I think we’ll need a few court cases under our belt to see if it really starts shaking out that way.”

Christina also believes that, at least during the Trump administration, federal agencies are going to be much more rigorous about ensuring that their regulations conform to statutory language or at least have a basis in the statute before they even issue net by notice of proposed rulemaking.

"It's going to have an effect on the executive branch's thinking about how to go about regulating, and that'll be across the board, particularly because there will be a lot of OMB and DOGE supervision," he opines. "Loper Bright is going to be foremost in the minds of regulators."

The first step he'd recommend for self-insured health plans is to continue to assume the validity of all existing regulations, then give any proposed regulations much more than a cursory glance by having outside counsel review the proposal.

Field

Choose speed and savings with Stealth Advance! We fund claims up to $5 million within 72 hours of loss notification— no complex forms needed. Enjoy cash flow stability without being tied to any specific carrier, TPA, or PBM.

Get the rapid reimbursements of bundled stop-loss combined with the flexibility of direct writers. As your program manager, Stealth Partner Group simplifies the process with one transparent PEPM fee—no hidden costs.

Experience the Stealth Advance difference: fast reimbursements, competitive rates, and complete vendor freedom!

“In the future,” Condeluci predicts, “people are going to be very quick to file a lawsuit against a reg even if it’s pretty crystal clear that the department got it right.” As for whether Loper Bright complicates compliance with older regs, he says employers are still expected to comply, even if there’s a lawsuit filed against a particular regulation.

"You must comply until a court says that you don't have to comply anymore," he says, noting that it applies to ERIC's mental health parity litigation. "It doesn't matter if there's a lawsuit filed. It's still business as usual." It's also important to understand that litigation takes a long time, and regs still apply until an appeals court invalidates them, he adds.

CHANGING OF THE GUARD

Condeluci doesn’t think significant reductions in the federal workforce will have much of an impact on compliance. Instead, the background, experience and policy priorities of agency personnel moving into senior roles will have a much greater influence over what happens next inside the beltway.

At the top of that list is Lori Chavez-DeRemer, a former Republican U.S. Rep. from Oregon, who now serves as labor secretary and is a big proponent of requiring provider network owners to share health claims data with self-insured plans and their business associates. Another key player is Daniel Aronowitz, who was nominated to serve as assistant secretary of labor for the Employee Benefits Security Administration, which has jurisdiction over rules and compliance relating to self-insured health plans. He has expertise in stop-loss insurance and fiduciary liability and has been a critic of the plaintiffs' bar going after plan sponsors over fiduciary breach issues.

His view of Robert F. Kennedy Jr., who heads the Department of Health and Human Services, is that he probably will wield more influence over public health programs than the commercial insurance market. What will be more impactful is those in senior roles who report to him, he adds.

Years before any type of judicial deference was in effect, Karlinsky notes that there was more cooperation in Congress, which ran more efficiently. "Hopefully, we'll get back to that type of an era where some of these interpretations frankly aren't even necessary moving forward," he adds.

Bruce Shutan is a Portland, Oregon-based freelance writer who has closely covered the employee benefits industry for more than 35 years.

Do you aspire to be a published author?

We would like to invite you to share your insight and submit an article to The Self-Insurer! SIIA’s official magazine is distributed in a digital and print format to reach 10,000 readers all over the world.

The Self-Insurer has been delivering information to top-level executives in the self-insurance industry since 1984.

Articles or guideline inquires can be submitted to Editor at Editor@sipconline.net

The Self-Insurer also has advertising opportunties available. Please contact Shane Byars at sbyars@ sipconline.net for advertising information.

Not Afraid To Spill Some Milk

When your culture drives you to get comfortable being uncomfortable, you’re going to spill some milk to deliver innovation. ‘Yes, and…’ we embrace spilled milk to enable smarter, better, faster healthcare.

Learn more about how we’re delivering innovative solutions to simplify healthcare.

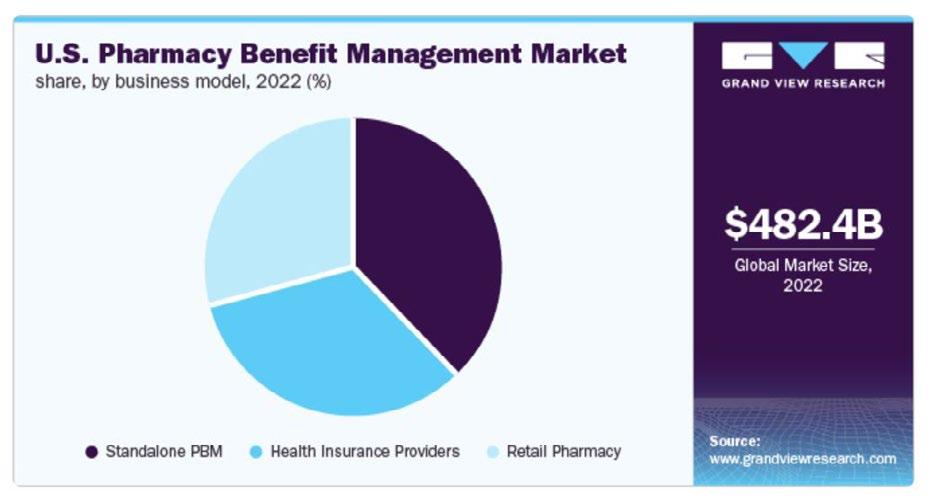

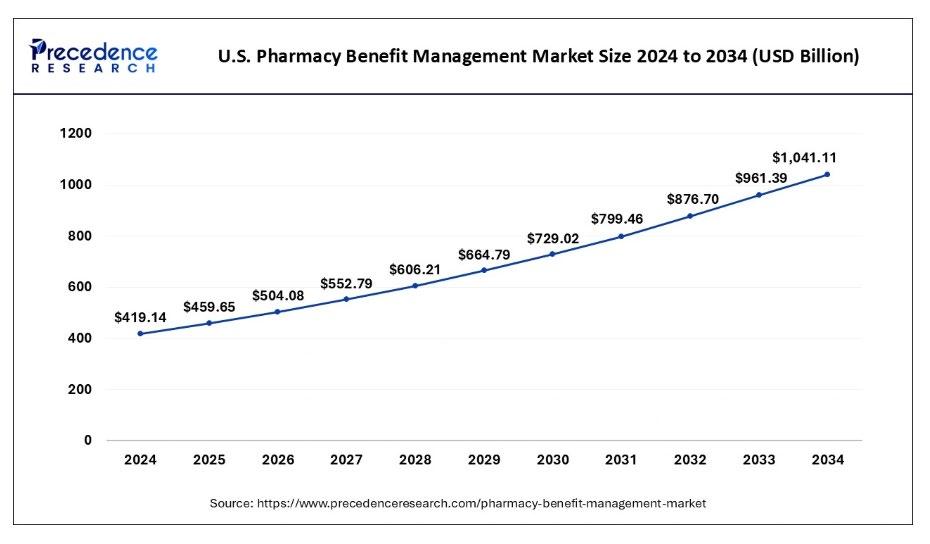

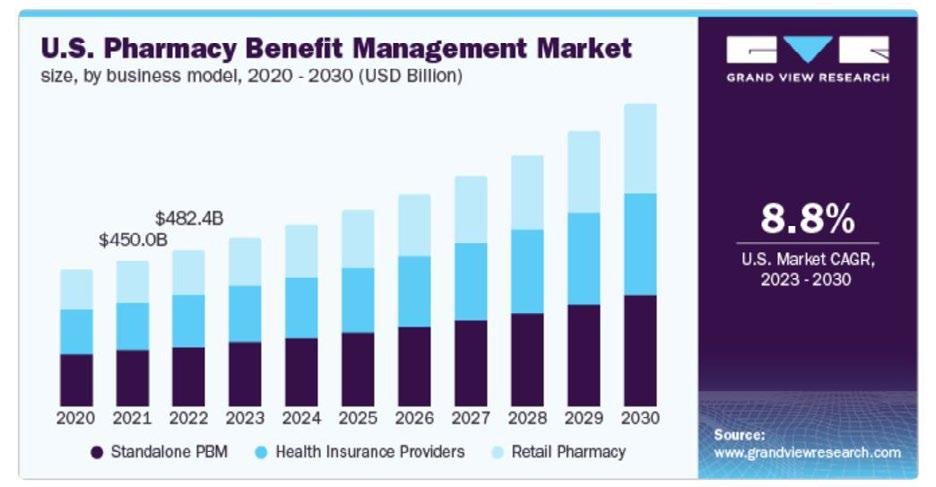

PBM QUAGMIRES TROUBLE EMPLOYERS

Editor’s Note: For more information about this topic, please plan to attend SIIA's High-Cost Drug Stakeholder Forum, scheduled for May 28-29 in Minneapolis. Event details can be accessed at www.siia.org

Written By Laura Carabello

AmidAa barrage of high-profile lawsuits, legislative challenges and widespread employer/payer dissatisfaction with escalating drug prices, the Pharmacy Benefit Management (PBM) industry is awash in negative publicity and uncertainty. In the wake of these complaints, the Pharmaceutical Care Management Association, a trade group representing the six-largest PBMs and others, said in a statement that the industry welcomes competition from newer entrants.

Now in the crosshairs of Congress, as well as State legislators such as Illinois, PBMs face a host of pending regulations to address criticisms such as steering patients toward their own pharmacies, requiring patients to use an in-network pharmacy or paying a pharmacy an amount less than the national average drug acquisition cost for the drug dispensed. Congress is tackling these issues, with proposals under consideration that include:

Requiring PBMs to charge flat fees that are not linked to drug prices

Creating standard pharmacy performance metrics on which fees are based

Requiring PBMs to disclose negotiated drug rebates and discounts -- and requiring those rebates and fees to be passed through to employers

Prohibiting spread-pricing

Employers lay blame on PBMs, generally described as “behind-the-scenes middlemen” that negotiate discounts with drug manufacturers and reimbursement rates with insurers to determine which medications qualify for coverage. Accusations include demanding discounts and rebates from drugmakers, which leads the manufacturers to charge higher list prices, which can drive up the price patients pay at the pharmacy. Concurrently, retail pharmacies say PBMs are literally driving them out of business by paying them less than what the PBMs charge health plans — a practice known as spread-pricing, where PBMs charge more to health plans than they pay pharmacies for prescription drugs.

Julie A. Wohlstein, M.A.S., CSFS ®, President and CEO, Centrix Benefit Administrators, Inc., specifies the challenge, “PBMs often present self-funded employers with a double-edged sword. While they play a critical role in managing prescription drug plans and negotiating discounts, their opaque practices often lead to hidden costs and misaligned incentives.”

She says PBMs typically steer members toward higher-cost drugs as way to maximize rebates, a practice which inflates the overall costs.

“Employers are burdened by complex contractual terms that obscure true drug prices and make it difficult to identify cost-saving opportunities,” she continues. “Furthermore, the adoption of narrow pharmacy networks may limit employee access, which creates dissatisfaction among the workforces.”

Across the board, plan sponsors say they have no idea what a drug will cost because many PBM contracts contain nondisclosure clauses. There are varying reports regarding the stranglehold on the industry. According to the American Medical Association, together, the big three -- CVS Caremark, Cigna’s Express Scripts and United Health’s OptumRx -- hold nearly 60% of the pharmacy benefits market based on their control over rebate negotiations, retail network management, and claims adjudication.

Furthermore, a recently released report from the Federal Trade Commission (FTC) shows that these three PBMs processed almost 80% of the 6.6 billion prescriptions filled nationwide last year, and the top six players control more than 90% of the market. The FTC found that those companies use tactics to point patients toward drugs that are more costly.

Wohlstein maintains that a major challenge lies in the lack of transparency in rebate structures, adding, “PBMs frequently retain a significant portion of manufacturer rebates rather than passing on the savings to the employer or employees, creating an environment where profitability outweighs patient outcomes. To navigate these challenges, self-funded employers must prioritize transparency and explore innovative solutions such as pass-through PBMs or carving out pharmacy benefits for direct negotiation. By adopting proactive measures, employers can better align PBM practices with their financial goals and the health needs of their workforce.”

In this current environment, employers are certainly scrutinizing PBM policies and capabilities more closely.

Lori Daugherty, CEO, RxLogic observes, “Employers select PBMs based upon transparency, cost savings, service quality, and alternative solutions. A transparent PBM ensures clear pricing, eliminates hidden fees, and passes through negotiated savings. While rebates may seem attractive, employers should assess total cost impact rather than just rebate amounts.”

She says that superior service and clinical support help optimize medication access while controlling expenses, noting, “Additionally, PBMs offering alternative pricing models, such as direct manufacturer savings and pass-through pricing, providing additional cost-cutting opportunities. Our model powers PBMs with the technology and services needed to meet these employer demands, enabling PBMs to deliver transparency, cost-efficiency, and advanced analytics, ensuring a superior service model for their clients.”

Re-cap of Some Issues to Date:

Last year, the FTC sued the three jumbo PBMS for anti-competitive practices, alleging that their practices artificially raised the price of insulin drugs. While the PBMs asked a Missouri district court to block the agency’s suit, as of mid-February, the lawsuit was slated to move forward after a federal judge declined to halt the case. Later in the month, the Big Three elevated their suit and asked the Missouri district judge to halt the FTC's administrative case against them. Stay tuned to the see-saw battle.

In 2024, The House Oversight Committee kept pressure on PBMs during hearings that criticized industry practices to steer patients to PBM-owned pharmacies while underpaying competing pharmacies. There is increased scrutiny on the way PBMs treat independent pharmacists, who say

they’re being drummed out of business by PBMs.

PBM executives were also summoned before Congress and reproved for creating corporate entities in Switzerland and Ireland to centralize the negotiation of rebates and fees. They were grilled with accusations of creating entities in Ireland and the Cayman Islands to manufacture and market certain highly profitable generics and biosimilars -- locations purportedly lacking in financial transparency and movement of operations that would be subject to impending regulations.

A group of legislators called upon the Department of Justice to investigate whether PBMs played a role in the opioid epidemic, pointing to reports that suggest the three largest PBMs worked together to steer patients to OxyContin prescriptions in exchange for $400 million in rebates and fees from Purdue Pharma across a yearlong period ending in late 2017.

Tangentially, in welcome news for the employer community, the Groom Law Group reported that the US District Court for the District of New Jersey dismissed in January 2025 a putative ERISA class action lawsuit in a much-followed case involving Johnson & Johnson (J&J). The plaintiff alleged that the plan fiduciaries for J&J’s group health plan violated ERISA by mismanaging its self-funded health plan’s prescription drug benefit. The Court found that the plaintiff's allegations that she paid too much in premiums, copays, and coinsurance and that her wages were adversely impacted by prescription drug costs were speculative "at best," and that her allegations regarding higher out-of-pocket costs for prescription drugs were not redressable.

At year-end 2024, while Congressional lawmakers reached a deal to put guardrails around these socalled “middlemen,” the agreement fell apart because it was tacked onto a larger spending package that

crumbled during a final vote. The employer PBM provision would have created new reporting requirements for employers' PBMs and required employers' PBMs to pass all rebates on to the employers' plans rather than keeping a percentage of the discounts they negotiated. When the spending package stripped out this provision, PBMs got a temporary reprieve -- but it’s likely to be a short honeymoon for them in Washington.

The issues are bubbling up in 2025 with bipartisan efforts that press the FTC to be tough on PBMs. The FTC’s ongoing campaign, which most recently focused on charges for high-cost specialty drugs, accused the three biggest PBM pharmacies of collecting $5.9 Billion in specialty drug mark-ups.

Chairman of the House Energy and Commerce Committee recently declared that he and his colleagues hope to pass new versions of the bipartisan health bills, many that have lingered for more than a year without final action. One measure that could be included is a bill that would regulate how PBMs serve employersponsored health plans.

The latest salvo came in February when A broad coalition of healthcare companies, employers, labor unions and trade associations called upon the White House and Congress to enact legislation to curb PNMs: Blue Shield of California, employers represented by the ERISA Industry Committee, pharmacies represented by the National Association of Chain Drug Stores and the National Community Pharmacists Association, and an umbrella group called America’s Agenda that includes the insurers Elevance Health, Centene and Kaiser Permanente along with unions and drugmakers, made their plea.

There’s even proposed legislation in Texas that could stop health insurers or other coverage issuers in the Lone Star State from requiring patients to use the carriers' own pharmacy benefit managers.

Amid all this market uncertainty, pharmacy spend is expected to rise 3.8%, with specialty pharmaceutical costs as the main driver and price increases to classic specialty drugs that treat oncology conditions and autoimmune disorders. A Vizient study showed that Humira, Stelara and Skyrizi, which all can treat Crohn’s disease, are projected to have the largest price increases.

GAUGING EMPLOYER DISSATISFACTION

Faced with projected healthcare cost pressures, employers are trying to hold their PBMs accountable –especially for pharmacy costs. According to the Business Group on Health, pharmacy costs accounted for more than a quarter of healthcare costs in 2023, with rising drug costs largely driven by expensive specialty medications, cell and gene therapies (CGTs) and GLP-1s.

A survey by the National Alliance of Healthcare Purchaser Coalitions, an advocacy organization for employers and purchasers, substantiates these perceptions: about 99% of respondents listed drug prices as a significant threat to affordability. Purchasers cite PBM vertical integration and opaque practices as the culprits.

Every size employer-sponsored health plan is facing increasing healthcare costs, but the impact on small employers and their employees is more acute and likely to continue. Many believe their PBM isn’t always looking out for their needs.

The National Alliance of Healthcare Purchaser Coalitions survey also documented employer dissatisfaction with their PBMs: 52% are considering changing their PBM in the next one to three years. According to their leadership, PBMs use “opaque business practices” that allow them to change the status of a drug from generic to specialty to name brand without the employer’s consent. They also point the finger at the big three PBMs that all own their own specialty, retail, and mail-order pharmacies and "strategically price drugs to maximize revenue to their internal pharmacy chains.”

EMPLOYERS MAKING A SWITCH

A growing number of employers would rather ‘switch than fight’ with their PBM partners, opting for a vendor that is more agile and offers alternative network models with greater price and quality transparency. Status quo PBM contracts may go by the wayside in favor of dropping the “Big Three” PBMs to “transparent PBMs,” which don’t camouflage their pricing and drug choice decisions.

In the Business Group on Health's annual survey published in late January, respondents indicated concerns about a lack of transparency in contracts with PBMs. While 6% of employers plan to change PBMs next year, nearly one-third said they will reassess their partnerships next year. Switching drug benefit policies at larger companies takes time since PBM contracts with the big three typically last three to five years. PBMs pay benefit plan consultants and brokers handsomely to steer business their way.

A few big employers are already changing their drug plans. Back in 2019, the State of Connecticut became CVS’ first PBM customer to negotiate a transparent fee structure. Its contract required 100% of drug rebates to be passed along to the state and eliminated spread pricing.

Other payers may be following this lead and learning from the Connecticut experience. The CT State Comptroller's office reported a further step in the new contract for its 214,000 employees. Instead of discounts and rebates, it demanded the lowest net cost per employee, with projected savings of up to $70 million a year. Of the three big PBMs, only CVS bid on the contract, edging out a few “transparent PBMs” and signaling that CVS wants to stay in the game.

Other examples include:

Highlighting the growing demand for change, Blue Shield of California made headlines by dropping CVS Caremark as its PBM in favor of a more transparent and innovative strategy. Partnering with companies like Amazon Pharmacy and Mark Cuban’s Cost Plus Drugs, Blue Shield aims to bypass traditional PBM structures, focusing on value-based pricing and direct relationships with pharmaceutical partners.

Purdue University, which sought control over the drug formulary to provide more lower-cost options for its 25,000 employees and dependents. They recently switched from CVS Caremark to AffirmedRx.

Capital District Physicians' Health Plan dropped CVS Caremark two years ago to partner with CapitalRx to administer pharmacy benefits for its 400,000 members. The non-profit health experienced a 9% drop in costs for commercial members under the contract, noting that at times, CVS Caremark would recommend excluding a generic medication over a brand drug in favor of a higher rebate.

The non-profit, 600,000-member health plan UCare ended its 13-year relationship with Express Scripts and in January began a multi-year contract with Navitus Health Solutions, a pass-through PBM owned by St. Louis-based SSM Health and Costco Wholesale Corporation. Citing another motivation for the switch, UCare sought to support local pharmacies, which have called out the major PBMs for forcing unfair contract terms that deliver lower reimbursements than those delivered to PBM-affiliated pharmacies.

Geisinger Health Plan has 600,000 members, and while they never contracted with one of the major PBMs, it doesn’t dismiss them when re-evaluating contracts. One of Geisinger's biggest challenges is persuading employers to adopt the transparent approach, saying it has lost employer

clients to health plans operated by the major players pitching large rebates.

Investment company Voya Financial, with 7,200 U.S.-based employees, was rethinking its relationship with CVS Caremark and began a multi-year contract with retailer Costco Wholesale Corporation's PBM Costco Health Solutions. Voya anticipates 10% savings for both its employees and the company.

Throughout the industry, many groups are dealing with this issue. Wohlstein explains that as a TPA, her organization was faced with this conundrum and made the decision to look for another PBM.

Transparency was a top priority in their decision to make a change.

“Hidden fees, spread-pricing and unclear rebate structures were having a significant impact on our plan costs,” she continues. “Ensuring rebates are passed directly to the plan and eliminating unnecessary administrative charges are crucial in managing overall drug expenses and maintaining trust. Pharmacy spend was the highest claims increase trend for our Plans,” she continues.

While large PBMs bring scale, broad networks, and deeper manufacturer relationships, Wohlstein found this is often at the cost of transparency and member customization.

“Boutique PBMs, on the other hand, excel in personalized service, flexible solutions, and often better alignment with employers' goals,” she insists. “The trade-off depends on the employer's specific priorities, such as cost control or member satisfaction. As a TPA, we must align the PBM vendor with the employer’s benefit strategy to determine the best critical path forward for their plans.”

She further contends that because their current large national PBM was not meeting their clients’ needs, as stated above, “…we selected a boutique vendor who was more innovative, and their offerings could be more tailored to the needs of our clients. I think PBMs will face heightened scrutiny for their opaque practices, and therefore, government intervention seems increasingly likely.”

The power to get it done.

AmeriHealth Administrators is one of the largest national third-party administrators. We provide innovative, value-based health benefits programs and outsourcing services for self-funded health plans and other organizations.

Whether locally focused or on a national level, our scalable capabilities allow us to service many unique customers, including self-funded employers, Tribal nations, international travelers, and labor organizations.

Learn how we can help you successfully navigate and thrive in today’s complex health care environment. Visit amerihealthtpa.com.

As with any regulatory mandate, Wohlstein cautions that while such intervention might improve transparency and curb unethical practices, “This could also lead to unintended consequences, such as reduced flexibility or increased administrative burdens. The outcome will depend on how well regulations address the root causes of misaligned incentives without stifling innovation, and that is what is truly important to the self-funded community.”

On a related front, Walgreens outlined its corporate turnaround strategy to include renegotiating contracts with PBMs and reports having renegotiated all contracts up for renewal in 2025, about a third of its total contracts. Walgreens says it is working with PBMs to balance brand-name drugs and generics, carve out new categories for high-cost drugs such as GLP-1s and implement alternative payment models.

INTEREST SPIKES IN SMALLER PBMS

Many smaller PBMs are seeing an uptick in interest, but the newer entrants will continue to face stiff competition and significant obstacles as they seek more business in the employer marketplace ---- from massive employers to small-to-midsize groups. These smaller PBMs usually offer more restricted drug formularies that can become a frustration point for members, while larger vendors typically feature attractive rebates and greater access to branded drugs resulting from their buying power to obtain medications at lower prices.

On the plus side, smaller PBMs are looking to attract customers by giving them more control over formularies and providing access to data. Many tout potential savings for employers between 30-50% on their pharmacy spend. These smaller companies are passing along drug rebates, disclosing cost negotiations with drugmakers, reimbursing pharmacies at higher rates and rejecting spread pricing.

Questioning the value of large PBMs, Rachel Strauss, VP of Strategic Development at Employee Health Insurance Management, Inc., says, “The big PBMs operate like monopolies, with complex systems that obscure true costs and limit choice for the employer. Their contracts often read like mortgages and have even harder-to-understand terms. However, when the correct contract is executed, they can offer the buying power the boutiques do. But this is often without guardrails. Would you rather get a bigger discount on a more expensive item, to begin with, or less of a percentage, but on a lower net cost product?”

Conversely, she thinks boutique PBMs are "…refreshingly straightforward, prioritizing transparency and a tailored approach to optimize costs and care for their clients. Employers often find they get far more value from the smaller, hands-on players with the creativity and flexibility they offer.”

Strauss believes the government and new administration will step in during 2025 to implement regulations aimed at reining in the PBM industry, adding, “This will be a positive shift for the self-insured community which can hopefully transfer to the patient itself. Increased oversight and transparency will help eliminate hidden fees and conflicts of interest that have long driven up costs without adding value.”

She thinks these regulations could empower employers to make better-informed decisions, negotiate more effectively, and ultimately provide their members with more affordable, high-quality care.

“While change can be hard, these reforms are a necessary step to level the playing field and prioritize the needs of patients and employers over PBM profits – finally,” concludes Strauss.

Staying the course, Nick Soman, CEO of Decent, reports that they proudly partner with DisclosedRx, a PBM committed to transparency through full rebate pass-through and no hidden fees.

corporatesolutions.swissre.com/esl

“Their exceptional member services team and Prescription Navigators provide 24/7 support, expert advice, and consistent follow-through, ensuring a seamless experience for members," says Soman. “DisclosedRx aligns with our mission of delivering affordable, transparent healthcare by prioritizing the well-being of employers and their members.”

With tailored solutions, flexibility, and an innovative approach, Soman says DisclosedRx stands out as a trusted partner.

“Their commitment to clear, predictable pricing drives cost savings and satisfaction across the community,” he states.

For John Wiklund, FSA, MAAA, Vice President and Actuary, Small Business Benefits, a preferred PBM is offered to clients so they can access the financial benefits and programs.

“Important considerations are the pharmacy network, formulary disruption, administrative capabilities, customer service, adaptability to legislative actions, access to mobile apps and cost comparison tools,” expands Wiklund. "Transparency is important for a great user experience, though its true impact on pharmacy spend is unknown. We currently utilize rebates to offset admin costs, keeping coverage affordable. Regulatory changes could potentially jeopardize the cost offset structure we implement today.”

Wiklund and his colleagues continually evaluate their choice of PBM, emphasizing, “Prescription drugs are the largest category of health plan spend and represent a high volume of members’ interactions with the plan. We need to be vigilant with our plans’ funds, offer stateof-the-art coverage options, and feel confident in the value of our pharmacy services.”

He observes that despite partisanship, “The government’s strong focus on PBMs will likely lead to regulation. State and federal proposals could increase transparency but may also result in higher costs for plans and members.”

Employers often require guidance when choosing a PBM and establishing benchmarks to support a decision.

Paige Zimmer. EVP of Business Development, RxLogic, explains, “We empower employers with data-driven solutions to optimize pharmacy benefits while reducing costs. Employers should prioritize transparency, flexibility, and analytics-driven decision-making when selecting a PBM.”

The organization provides a PBM claim adjudication platform that is tailored for self-funded employers, allowing for customized, cost-effective pharmacy benefit management. Through rebate

Depend on Sun Life to help you manage risk and help your employees live healthier lives

By supporting people in the moments that matter, we can improve health outcomes and help employers manage costs.

For over 40 years, self-funded employers have trusted Sun Life to help them manage financial risk. But we know that behind every claim is a person facing a health challenge and we are ready to do more to help people navigate complicated healthcare decisions and achieve better health outcomes. Sun Life now offers care navigation and health advocacy services through Health Navigator, to help your employees and their families get the right care at the right time – and help you save money. Let us support you with innovative health and risk solutions for your business. It is time to rethink what you expect from your stop-loss partner.

Ask your Sun Life Stop-Loss Specialist about what is new at Sun Life.

For current financial ratings of underwriting companies by independent rating agencies, visit our corporate website at www.sunlife.com. For more information about Sun Life products, visit www.sunlife.com/us. Group stop-loss insurance policies are underwritten by Sun Life Assurance Company of Canada (Wellesley Hills, MA) in all states, except New York, under Policy Form Series 07-SL REV 7-12 and 22-SL. In New York, Group stop-loss insurance policies are underwritten by Sun Life and Health Insurance Company (U.S.) (Lansing, MI) under Policy Form Series 07-NYSL REV 7-12 and 22-NYSL. Policy offerings may not be available in all states and may vary due to state laws and regulations. Not approved for use in New Mexico.

administration services, a copay program, eVoucher programs, discount card network and commercial network partners, employers can provide solutions that can be essential to lowering their costs, as well as their employees.

“Employers also seek advanced analytics and reporting tools that provide insights into medication usage, cost trends and opportunities to optimize their plans,” says Zimmer. “Employers need ways that deliver transparency, efficiency, and innovative solutions. By equipping employers with these capabilities, we help employers access the best financial and healthcare outcomes."

JUMBO PBM RESPONSE

One large PBM is taking the rebate criticism off the table. Optum Rx announced that it will soon pass all rebates it gets from prescription drug manufacturers on to employer health plan sponsors and other clients. Leaders maintain that the PBM already passes 98% of the rebates it negotiates on to the customers, but customers that account for about 2% of the rebates have voluntarily chosen compensation arrangements that let UnitedHealth keep about 2% of the rebates.

UnitedHealth does not post details about the cash flow related to drug debates, but it reported in its annual financial statement for 2023 that it accumulated $11 billion in prescription rebate receivables on its consolidated balance sheets as of the end of 2023, up from $8.2 billion at the end of 2022.

Signaling change, CVS Health continues to undergo significant leadership shuffling as it navigates challenges in its insurance and PBM segments. Its Caremark PBM ushered in a new president as part of the executive shifts as the company grapples with increased medical costs and heightened regulatory scrutiny.

Laura Carabello holds a degree in Journalism from the Newhouse School of Communications at Syracuse University, is a recognized expert in medical travel and is a widely published writer on healthcare issues. She is a Principal at CPR Strategic Marketing Communications. www.cpronline.com

M&A MANIA INFUSING SELF-INSURANCE WITH POWER PLAYS

Private equity investment leads the way as partnerships scale their presence

Editors Note: For additional M&A-related content, please consider attending SIIA's Corporate Growth Forum, scheduled for June 9-10 in Charleston. Details can be accessed at www.siia.org

Written By Bruce Shutan

TheTself-insurance sector is rapidly approaching a $40 billion premium market – nearly three times what it was valued in the late 1990s, observes Dan Bolgar, CEO of Carbon Stop Loss Solutions. That makes it palatable for investors seeking a solid return on their investment. In turn, all the money pouring into this space is expected to help self-insured employers level up their efforts to contain costs and improve clinical outcomes.

He says major players include the BUCAs (Blue Cross Blue Shield UnitedHealthcare Cigna Aetna), Tokio Marine HCC, Voya, and Sun Life, while about 80% of reinsurance premium is written by the top 20 market players and roughly 50 MGUs have invested in this space.

“PE [private equity] firms and investors love a business that’s organically growing at 12% or 13% a year, and I don’t see that stopping anytime soon,” Bolgar explains. Another big driver is the massive need for efficiency in healthcare. "It's much easier for them to go after it as an independent MGU [managing general underwriter] than it is to pick up a carrier,” he says, noting how carriers that take on risk associated with massive balance sheets can become a volatile investment, whereas MGUs are fueled by fee income. MGUs are also significantly smaller and easier to invest in than a large carrier, and they can flip the investment after five to seven years of growth, he adds.

There’s no doubt that M&A activity is heating up in the reinsurance space, whose total stop-loss market is currently valued at $37 billion and posting annual double-digit growth as more employers self-fund their group health plans, according to Bob Black, executive managing director for Aon, which last year acquired NFP, the owner of four stop-loss MGS.

VERTICAL INTEGRATION

The most interesting and innovative M&As in the selfinsurance space centers around vertical integration that pairs cost-containment, clinical capabilities and additional products on top of an administrative platform, says Trey Marinello, managing director for Houlihan Lokey. “Companies in the lower middle market, especially cases or groups of 50 to 200 lives, tend to have pronounced profitability relative to those focused up market,” he explains. “The next phase will be the introduction of risk-taking to round out a closed-loop system.”

Employers are pursuing levelor self-funded strategies in partnership with forwardthinking insurance brokers and independent third-party administrators (TPAs) to help take ownership of their healthcare costs, Marinello notes. The goal is to make the company more profitable while at the same time elevating member benefits by improving the health of the member population preventively and reactively. “As time goes by,

claims data informs the TPA as to how to better control costs without sacrificing benefits,” he adds.

Regulatory changes and a new administration could serve as a catalyst for new opportunities within the healthcare market, notes Vinny Esposito, CEO at S&S Health who has a hedge fund background. “We see a ton of activity in the TPA and technology space,” he says. “You got companies like Valence that have been very acquisitive over the past few years. Companies with really solid execution operations are finding homes, whether it be through private equity, a PE-backed asset or BUCA.”

Esposito sees money flowing into telehealth mostly around behavioral health aspects, as well as on the captive side and TPA space. Two standout deals in his view include the merger of Virgin Pulse and HealthComp – rebranded Personify Health – and recapitalization of Allied Healthcare Products when it was acquired by Flexicare (Group) Limited. “There’s a lot of big money going into everything within the supply chain for product to service components,” he reports.

PE powerhouses such as Blackstone, KKR and Apollo Global Management have been actively investing in healthcare and insurance-related companies. Stop-loss now includes health plans, health systems, traditional health insurers, aggregators, reinsurers, wholesalers, venture capitalists and PE firms that have entered the market through entities that they own or brokers, Black explains.

The lines of demarcation are often blurred. For example, he says Unum sold its block to Amynta Group, which is an aggregator, and then Amynta hired Byron Way from Skyward Accident & Health to lead the firm and partner with Crum & Forster. Once they’ve established a stronghold, many of these entities then buy other blocks of business.

Prudential and Old Republic are new entrants into the stop-loss market over the past year, which Black says opens up quite a bit of opportunity. As companies become acquired, individuals who control portfolios from large writers like Sun, Symetra or Voya sometimes start their own entities, which he says happened with Evolution Risk Partners, an MGU formed by underwriters at a much larger organization. Some recent players in self-insurance have tried to develop almost like a health system, Black observes, citing as examples Gravie, Angle Health and Sana Benefits.

A COMMON THREAD