4 | From black-tie dinners to inclusive dialogue – A journey with ICISA Benoît des Cressonnières, Allianz Trade

INSIGHTS

6 | Navigating tariffs and trade uncertainty: Economic insights and risk mitigation strategies for Canadian businesses Ioana Arnautu, Marsh Canada and Marcos Carias, Coface North America

10 | Verified Organizational Identity and Data – enhancing trade finance risk management Alexandre Kech, GLEIF

ICISA UPDATES

16 | ICISA’s 83rd Annual General Meeting in Prague: Strong growth, new leadership, and a renewed commitment to support global trade Raluca Ezaru, ICISA

INTERVIEW

18 | Serving the industry beyond borders: Interview with Jan Mueller, the new ICISA President

22 | Welcoming new voices: TransRe and SMABTP join the ICISA community

ANNOUNCEMENTS

Disclaimer

All articles in the ICISA Insider represent solely the opinions of the individual authors, not ICISA, unless otherwise stated. Original articles appearing in the Insider may not be reprinted without the express permission of the author and ICISA. When citing articles, please refer to the title of the article, the author, and the relevant edition of the Insider, including a full url to the magazine page.

Foreword

Dear Reader,

As we move through the summer months, I’m pleased to share with you a new edition of The Insider; a publication that continues to spotlight the people, topics, and developments shaping the future of credit insurance and surety.

In this issue, we proudly introduce two of ICISA’s newest members: SMABTP and TransRe. Through a joint interview, they reflect on their motivations for joining ICISA and share their vision for contributing to our growing community. Their addition highlights the continued relevance of our association in a rapidly evolving market.

We’re also honored to feature a personal column by Benoît des Cressonniers, former President of ICISA, who shares reflections from his long-standing involvement with the association. With decades of experience, Benoît offers thoughtful insights on ICISA’s evolution and the value of collaboration within our network.

At the same time, we look to the future with an interview with our newly elected ICISA President, Jan Muller, who shares his priorities and ambitions for the association in the years ahead. Among the contributions in this edition, you’ll also find:

• An article on Verified Organizational Identity and Data, exploring how enhanced identity verification can strengthen risk management in trade finance.

• An insightful article examining the impact of tariffs in Canada, highlighting their implications for cross-border business and credit risk.

• A recap of our recent Annual General Meeting in Prague, which brought members together to exchange ideas, strengthen partnerships, and set strategic goals for the coming year.

As always, we are grateful for the contributions of our members and authors, who make The Insider a true reflection of the dynamism of our industry.

Looking ahead, preparations are already underway for our Trade Credit Insurance Week, set to take place this autumn. This flagship event will once again bring together industry leaders, policymakers, and practitioners for a series of insightful discussions and forward-looking sessions. More details will follow soon—we hope to see many of you there!

Thank you for reading, and for being part of the ICISA community.

Warm regards, Richard

Wulff

From black-tie dinners to inclusive dialogue –A journey with ICISA

Column by Benoît des Cressonnières, Allianz Trade

With a blend of humility and pride, I’ve embraced the role of Chairman of ICISA’s Management Committee. For more than two decades, I’ve been part of this Associationwatching it evolve from a somewhat exclusive circle into a vibrant, diverse, and future-facing community. It’s been quite a journey, and I’d like to share a little of that with you.

I still vividly remember my very first ICISA AGM: blacktie dinners, formal speeches, and a room full of familiar faces who had known each other for years. It felt like a closed community, rooted in tradition and ceremony. The atmosphere resembled a NATO meeting—very formal, with participants seated in alphabetical order according to their company names. Occasionally, the neighbours would change as company names evolved, but the structure remained rigid. While this setup upheld tradition, it wasn’t always the most effective for real exchange or networking. But times change—and so did we.

Fast forward to today, and ICISA meetings look and feel very different. You’ll see sneakers next to suits, seasoned leaders exchanging ideas with young professionals, and more women not just participating – but leading discussions. Initiatives like Women in Trade Credit Insurance and the Women’s Surety Network are helping ensure female voices are not only represented but actively encouraged to speak

up, share ideas, and take the stage. Our committees now reflect a broader mix of experiences, backgrounds, and perspectives, and through our growing training efforts, we’re welcoming a new generation into the industry – diverse, engaged, and ready to shape what comes next.

Technology has also played a defining role in our transformation. Following the COVID-19 pandemic, we quickly adapted - webinars and virtual meetings are now a core part of how we engage. This shift paved the way for some of our most impactful initiatives: Trade Credit Insurance Week and Surety Week. These events have grown into major annual campaigns, bringing together regulators, brokers, insurers, and both new and long-standing ICISA members. They’ve become true platforms for dialogue, where stakeholders from across the globe meet, debate, and share expertise – building stronger connections across the ecosystem.

Over the past four years, I’ve had the honour of serving first as Vice-President and then as President of ICISA. Throughout this time, we remained focused on what matters most: advocating for our industry, strengthening our network, sharing expertise, and supporting the professional development of our members. But what I’m most proud of is the progress we’ve made—not just in ideas, but in action.

We’ve grown. Even with our modest size and resources, ICISA has grown significantly. The increasing number of new member applications – from both insurers and reinsurersis a testament to the credibility and relevance we’ve built together. Each new voice strengthens our platform and fuels our momentum. ICISA has become a place where everyone can contribute, regardless of job title, gender, or years of experience.

Only looking at the past 20 years, our industry has been through a lot—and so have the people working in it. We’ve faced the financial crisis, a global pandemic, a war in Europe, energy shortages, inflation, political turmoil, and

sudden election shocks. Still, we showed up. We kept trade moving, backed projects, and gave businesses the confidence to keep going. That’s what makes this industry special: no matter how tough things get, the people behind credit insurance and surety are always there, quietly making sure the economy keeps running.

As we approach ICISA's 100th anniversary in 2026, one thing is clear: resilience is in our DNA. We’ve adapted, we’ve opened up, and we’ve grown stronger as a result.

Finally, I extend my heartfelt gratitude to the ICISA team and all members for their contributions and encouragement. Together, we can move mountains!

Navigating tariffs and trade uncertainty: Economic insights and risk mitigation strategies for Canadian businesses

Article by Ioana Arnautu, Marsh Canada, Marcos Carias, Coface North America

Introduction

As global trade tensions persist, Canadian businesses are grappling with the ripple effects of tariffs and increasing market volatility. In this joint article, Coface North America economist Marcos Carias explores the economic impact of tariffs on Canada, highlighting the most-affected sectors and what the macroeconomic signals suggest for the months ahead. Completing the analysis, Ioana Arnautu, Senior Vice President and National Trade Credit Insurance Practice Leader at Marsh Canada, shares five actionable insights, that Marsh Canada has focused on due to the current climate, explaining how companies can leverage trade credit insurance to mitigate risk, protect cash flow, and uncover opportunities amid market uncertainty.

Together, their perspectives provide a comprehensive roadmap for navigating today’s evolving trade landscape with both insight and confidence.

Economic impacts of tariffs on Canada and how the most-affected sectors are responding

The strengthening growth momentum at the end of 2024 signaled that the Bank of Canada’s (BoC) rate cuts were finally managing to spur a recovery. Unfortunately, we expect this momentum to be short-lived, as the effects of tariffs progressively ripple throughout the industry. Gross domestic product (GDP) growth ended 2024 and started 2025 on a strong footing, keeping a healthy pace slightly above 2% (quarter-over-quarter annualized). While this Q4 figure was largely driven by consumption and investment, it was inventories that accounted for the lion’s share of growth in Q1. Likewise, the positive contribution of net exports is

primarily the result of American importers trying to get ahead of tariffs. Meanwhile, the domestic front of the economy began trending downward, with a noticeable slowdown in consumption and a mild contraction in investment. We expect these negative trends to deepen in Q2 and Q3. Indeed, the labor market was already fragile, with unemployment at its highest since January 2017 at 6.9%.

Manufacturing employment has shed workers for four consecutive months, and the share of Canadian workers worried for their job is at its highest on measure (20%). This year’s record-setting April contraction in exports heralds that the benign movements of Q1 will correct in the forthcoming months; the likelihood of a technical recession is high.

The general climate of uncertainty created by the U.S. President Donald Trump administration’s unpredictable swings in trade policy is especially consequential for Canada, where the U.S. accounts for roughly three quarters of total exports, or around 18% of GDP. The country was one of the earliest targets, being hit by a 25% blanket tariff, as well as 25% tariffs on the auto and metal sectors raised to 50% as of June 4. An important exemption was introduced on goods compliant with the United States-Mexico-Canada Agreement (USMCA) free-trade agreement, estimated to cover around half of exports, with coverage expected to increase as firms rush to qualify. At the time of writing, the legality of the blanket tariff is being contested by U.S. courts. Their repeal would come as substantial relief for Canada, but markets would remain vulnerable to sectoral tariffs under section 232 and 301, where key industries such as copper and lumber are already in the crosshairs. And the White House may yet win the appeal.

Furthermore, the upcoming review of the USMCA agreement (likely to be brought forward at the end of 2025) has the potential to drag on. Indeed, the Trump administration’s likely demands would force the Canadian government to contemplate some uncomfortable tradeoffs. Access to Canada’s dairy market, an issue that long predates Trump, will be one such point of tension. This, along with issues surrounding stricter rules of origin in the manufacturing sector and other matters of contention, could lead to a long negotiation, and a prolonged uncertainty environment. Recent events suggest that the Trump administration is discovering its own preferences and constraints as the trade war evolves. As such, making hard bets on how dead set they are on their positions even a few months in advance is speculative. A best-case scenario would be one where pressure to secure deals quickly makes them flexible on their demands. But one can just as easily imagine the U.S. driving a hard bargain if the administration ends up being perceived as “soft” on China once the dust settles on that front.

In the long run, the trade war might come as a wake-up call that yields some silver linings, namely the liberalization of inter-regional trade and a modicum of diversification of Canada’s export destinations. This year, we still see few reasons to expect that uncertainty will dissipate meaningfully, and the data should progressively reveal the extent of the damage already incurred.

Fives ways trade credit insurance helps Canadian businesses mitigate risk and accelerate growth in an unpredictable market

In an increasingly interconnected global economy, tariffs have emerged as a pivotal factor-shaping trade dynamic, particularly for Canadian enterprises. As companies grapple with the complexities and uncertainties of international trade, they encounter a myriad of challenges that can jeopardize their financial stability.

One effective instrument for mitigating these risks is trade credit insurance, which serves to protect businesses against the adverse consequences of buyer defaults and payment delays. This form of insurance not only safeguards receivables but also provides critical insights into customer creditworthiness and enhances cash flow management.

In the context of tariffs, it is imperative for Canadian exporters to recognize the specific risks they face and how trade credit insurance can offer viable solutions.

1. Protection against non-payment. One of the foremost risks associated with tariffs is the heightened likelihood of payment delays. The imposition of tariffs often results in increased costs for goods, which can strain the cash flow of buyers in the U.S., leading to delays or defaults in payments. Trade credit insurance provides protection against non-payment, ensuring that exporters can recover a substantial portion of their receivables, thereby stabilizing their cash flow.

2. Reliable credit assessment of buyers. Due to the additional costs imposed by tariffs, the financial health of U.S. buyers may deteriorate, complicating Canadian companies' ability to accurately assess a buyer’s creditworthiness. To mitigate this risk, trade credit insurers are able to conduct real-time comprehensive credit assessments of buyers, offering Canadian companies invaluable insights into their customers' financial stability and empowering exporters to make informed decisions.

3. Strengthened market position. Tariff uncertainty increases market volatility, leading to fluctuations in demand for Canadian goods. By securing trade credit insurance, Canadian companies can decrease the risk of insolvency and enhance their cash flow management. The knowledge that a company’s receivables are protected enables the ability to offer more favorable payment terms to buyers, potentially bolstering sales and enhancing competitiveness. On the flip side, in the event of an unexpected supply chain disruption, trade credit insurance also enhances a company’s ability to secure financing from banks and financial institutions because lenders often regard insured receivables as lower risk.

4. Expand into new markets confidently. As tariffs reshape the competitive landscape, Canadian companies may confront intensified competition from domestic U.S. suppliers who benefit from reduced costs. With trade credit insurance, Canadian companies can confidently explore new trade markets and expand their customer base, assured of protection against payment risks.

5. Free-up internal resources. Changes in trade regulations and compliance requirements stemming from tariffs can heighten the risk of non-compliance and associated

penalties for Canadian companies. In the event of a payment default, trade credit insurers often provide support in managing claims and recovering outstanding debts, thus alleviating the administrative burden on Canadian businesses.

It’s no secret that the current imposition of tariffs presents a multifaceted array of challenges for Canadian businesses. Unquestionably, trade credit insurance is an indispensable tool for navigating these turbulent waters. As businesses adapt to these changes, a nuanced understanding and strategic utilization of trade credit insurance will be crucial for sustaining growth and maintaining competitiveness in the face of uncertainty.

For more economic insights on North America, follow Marcos Carias on LinkedIn and subscribe to Macro with Marcos for the latest updates.

Ioana Arnautu can be reached at ioana.arnautu@marsh.com

Verified Organizational Identity and Data –enhancing trade finance risk management

Article by Alexandre Kech, GLEIF

Geopolitical shifts, new trade corridors, and the rise of digital public infrastructure are transforming how companies operate across borders – and how risks are assessed. One notable consequence of these changing conditions is the rapidly growing demand for trustworthy, verifiable business data.

In response to global trade rules becoming more complex, several forces are converging. International standards are developing fast and trade-related legal frameworks are being updated. In parallel, the fields of digital identity and open public data continue to sprint forwards. Together, these developments are enabling trading partners, investors, logistics firms, and insurers not only to verify the legal identities of counterparties, but also to connect these identities to other data points to assess risk, trade status, and compliance more effectively.

According to a recent update from the McKinsey Global Institute on the Geometry of Global Trade , for example, new “south-south” trade flows – such as between Latin America and Asia or Africa and the Middle East – are expanding rapidly, driven by digitization, economic diversification, and regional trade agreements. These shifts are accompanied by a rise in digital platforms across emerging markets, providing levels of access that traditional credit bureaus and data providers have often been unable to establish.

At the same time, government-backed digital public infrastructure – including real-time registries, customs APIs, and digital identity systems – is helping unlock data that was once siloed.

Availability, then, is no longer the challenge. Data integrity and interoperability are now the new frontiers.

Meanwhile, digital trade agreements continue to proliferate. Many of these explicitly aim to alleviate barriers to the crossborder flow of data, access to government data, and the assurance of e-signatures. Policy frameworks even refer to the advent of data generated by IoT devices to help manage

risk and optimize operations of freight logistics and supply chains.

This growing access to, and array of, data may disrupt traditional business models for risk assessment; but it also opens new opportunities. By embracing verified digital identity, insurers and trade intermediaries can deliver faster, smarter, and more adaptive services – all powered by a more connected, standards-based data ecosystem.

Introducing the Legal Entity Identifier (LEI)

This is where the Legal Entity Identifier (LEI) comes in. The LEI is a globally recognized, open, and non-proprietary identifier that uniquely identifies legal entities engaged in financial and commercial activities.

The LEI system, governed by the Global Legal Entity Identifier Foundation (GLEIF), offers a universal way to answer a foundational question in any trade transaction: Who is this company?

Unlike many proprietary databases or national registries, the LEI system:

• is borderless and globally interoperable;

• offers verified, structured reference data including ownership relationships;

• is free to access by anyone, anywhere;

• is purpose-designed to be embedded into digital workflows.

The LEI is already widely used in regulatory reporting, especially in financial markets. But its potential goes far beyond compliance – it is fast becoming a cornerstone of modern organizational risk management and digital trade infrastructure.

The rise of Digital Organizational Identity: Enabling interoperability in a fragmented world

The LEI is part of a broader shift toward digital organizational identity – enabling legal entities to be uniquely and reliably identified across systems and borders. When coupled with its cryptographically verifiable counterpart, the verifiable LEI (vLEI), it becomes possible to instantly confirm not only an entity’s identity but also the authority of its representatives in real time.

Consider a few examples:

• A credit insurer can use the Legal Entity Identifier (LEI) to accurately identify the buyer—for example, distinguishing A GmbH & Co KG from A GmbH. Though similar in name, these are separate legal entities, and cover only applies to the one with an approved credit limit. The LEI ensures the correct entity is covered.

• A logistics provider can confidently match data from ports, customs, and shipping platforms using a shared legal identity.

• A bank or trade platform can reduce due diligence time by automating onboarding and mandated Know Your Business (KYB) compliance processes.

One of the biggest obstacles in trade finance and insurance is fragmentation: data is often trapped in national registries, stored in varying formats, and subject to redundant verification processes. In a cross-border setting, there can be restrictions on access to data sets by foreign entities. The LEI addresses this by making so-called level 1 entity data, such as the entity’s official name and registered address, discoverable1 across nationally authorized sources, linking disparate systems under a globally recognized, trusted framework.

In short, the LEI and vLEI combination form a digital trust layer essential for innovation in trade, compliance, and risk management. They support better visibility into counterparties, improve fraud detection, streamline claims handling, and simplify regulatory reporting – helping organizations navigate a more interconnected and more complex global trade environment.

1 For further information on how D-R-V identifiers – Discoverable, Resolvable, and Verifiable – enable trustworthy and structured data exchange across global trade networks please visit the White Paper on Globally Unique Identifiers in Supply Chains published by UNCEFACT here

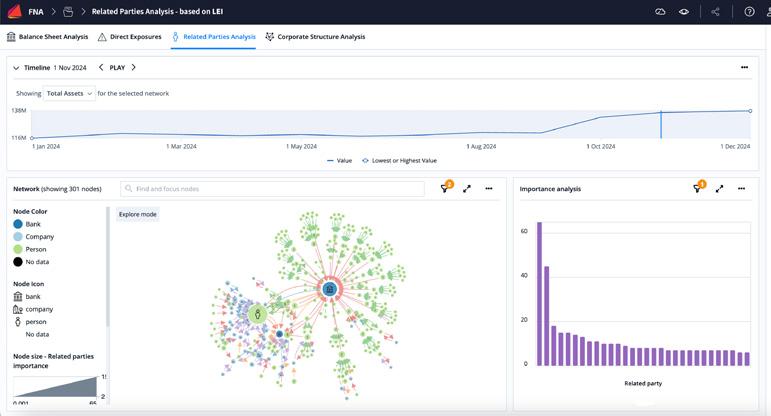

Using LEI and Network Science to explore related parties across economic agents, sectors, and jurisdictions21

The LEI, a global, independent, non-proprietary, and universal identifier for legal entities, enables scalable, secure mechanisms to verify the identity and prove the actions of counterparties. However, the amount of data to explore may escalate very quickly, making analysis, reporting and case management particularly difficult.

Network Science, comprising network visualization and analytics, allows any user to ingest vast amounts of LEI data to rapidly, flexibly and comprehensively explore direct relations and to uncover indirect relations that are obscured by higher orders of (indirect) relationships from a given institution.

As displayed in the dashboard below, starting from an institution under examination, it is possible to use the LEI to uncover direct and indirect relations with other institutions based on information corresponding to different dimensions of connectedness and influence, such as ownership, corporate control, cross-board directors (i.e., interlocking directorates), credit exposures, etc.

Visualization is conveniently complemented by the use of algorithms that calculate the network importance of the institutions. These algorithms enable measuring the role of the institution under examination and those that are directly and indirectly connected to it.

Communication of results and decision-making is enhanced by being able to visualize and quantify how different institutions are directly and indirectly interrelated. This augments the analytical capabilities of different economic agents, such as financial authorities, governments, corporations, and academia.

2 Source: Related Party Analytics dashboard, provided by Financial Network Analytics (fna.fi). Based on the LEI of different types of agents, network analytics and visualizations enable a user to rapidly, flexibly and comprehensively explore direct relations and to uncover indirect relations that are obscured by higher orders of (indirect) relationships from a given institution. Also, the importance of the different institutions is calculated according to their contribution to the network by using different algorithms.

Implications for Trade Credit Insurers

For ICISA members, accurate, reliable identity verification is not just a compliance issue - it’s a commercial necessity. As new trading relationships emerge and regulatory complexity increases, being able to quickly and confidently identify counterparties is central to pricing and managing risk.

Standardized legal identifiers such as the LEI are critical in this process. As noted in ICISA’s own policy recommendations:

“Creating and advancing systems of legal identifiers for companies… is essential not only for various commercial purposes, but also for underwriting. This may take the form of a national identification number… or a supra-national identification number, such as the LEI. Where such systems are in place and standardised, credit insurers are better able to offer their services in these markets.”

Here’s how LEIs and vLEIs can improve core activities:

Area

Entity onboarding

Risk assessment

Fraud prevention

Compliance

Claims management

LEI Benefit

Unique, reliable ID

Access to public reference data

Avoids entity confusion

Standardized ID for reporting

Confirms legal identity

vLEI Enhancement

Instant digital verification

Cryptographic trust in data source

Verifies authority of signatories

Secure, interoperable credentials

Speeds up digital workflows

Insurers can reduce the cost of KYB by leveraging LEIs as a standardized identity layer. They can also track risk exposure across complex supply chains by mapping LEI relationships (e.g., parent-subsidiary links). This is especially critical when dealing with smaller or unfamiliar counterparties in emerging markets.

What can credit insurers do now?

To stay ahead, credit insurers should consider:

1. Integrating LEIs into internal systems for onboarding, monitoring, and reporting.

2. Using vLEIs in digital documentation and contract verification processes.

3. Collaborating with new platforms that support LEI integration to streamline access to trusted data and enable data sets from different sources to be aggregated.

4. Engaging in industry forums and standard-setting bodies to promote interoperability and adoption.

One proposal from the Global Digital Finance (GDF) group and GLEIF suggests that greater LEI use could reduce KYB costs by over 50%, particularly for SMEs and in highvolume, low-margin transactions like single-invoice finance.

Conclusion: Trust in trade starts with identity

Trade credit insurance is built on one foundational principle: knowing your counterparty. In an era of digital trade documents, real-time data sharing, and emerging markets, that principle is more relevant than ever. Yet it is increassingly difficult to uphold with traditional tools.

The LEI and vLEI combination offers a scalable, secure, and globally consistent solution to this challenge. They enable faster, smarter, and more reliable decision-making by tying legal entities and authorized individuals to a trusted digital identity.

The future of trade risk management won’t be built by one institution alone. It’s the result of collaboration between governments, platforms, regulators, and the insurance industry. For ICISA members, that collaboration starts with recognizing identity as the foundation of trust – and the LEI as a tool ready to scale that trust globally.

Supporting the economic powerhouse

By the International Credit Insurance & Surety Association

This insightful whitepaper from the International Credit Insurance & Surety Association (ICISA) offers a comprehensive look at the vital role Trade Credit Insurance (TCI) plays in supporting small and medium-sized enterprises (SMEs). Written by a team of industry experts, this document provides a detailed analysis of how TCI can protect businesses against non-payment of trade receivables and enable access to financing. It highlights the importance of TCI in both developed and developing markets, offering practical recommendations for policymakers, regulators, insurers, and SMEs.

Readership

This whitepaper is primarily aimed at policymakers, regulators and SMEs to help improve their knowledge and understanding of this critical risk management tool. It is particularly relevant for those working with SMEs or in markets where access to finance is a challenge.

Importance

• Focuses on the role of TCI in supporting the SME sector, the backbone of the global economy

• Provides practical recommendations for stakeholders to enhance the effectiveness of TCI

• Covers emerging trends, including the impact of technology and artificial intelligence on the TCI sector

• Includes actionable insights for policymakers aiming to improve access to finance for SMEs

About the Author(s) / Editor(s)

The International Credit Insurance & Surety Association (ICISA) represents the world’s leading companies providing Trade Credit Insurance and Surety Bonds, along with their reinsurers. ICISA is dedicated to promoting industry excellence, innovation, and the integrity of products while addressing the business challenges presented by evolving regulations.

Where to read the full whitepaper?

The whitepaper is free of charge, available on ICISA website

ICISA’s 83rd Annual General Meeting in Prague: Strong growth, new leadership, and a renewed commitment to support global trade

Article by Raluca Ezaru, ICISA

This June, ICISA’s global family of trade credit insurance and surety leaders gathered in the beautiful city of Prague for the 83rd Annual General Meeting — a moment to celebrate a year of remarkable resilience, growth, and shared purpose amid ongoing global challenges.

Expanding membership and industry impact

Last 12 months marked a milestone year for ICISA, with eight new members joining the association: Ageas Re, Beazley, EDC (Export Development Canada), KODIT, Markel, Sofimex, SMABTP and TransRe. This expansion underscores ICISA’s growing global footprint and its role as the hub for key industry players.

“The steady increase in the number of insurers and reinsurers joining ICISA is a clear testament to the impact of our members’ commitment.”

This was said outgoing President Benoît des Cressonnières, highlighting the sector’s vital role in securing global trade and development.

New leadership to guide future growth

The AGM also marked an exciting leadership transition. Jan Muller, Managing Director at Hannover Re, stepped into the role of ICISA President for 2025/2026, bringing fresh energy and a clear vision for the future, after serving as Vice President for two years. Dekker Buckley from Chubb joins as Vice President, promising new insights and perspectives to guide the association forward.

Jan warmly thanked Benoît for his dedication and leadership, promising to continue building on this strong foundation.

“ICISA is a community where every member’s commitment counts — together, we make a real difference,”

Jan said.

Robust market performance reflects industry strength

Despite continued geopolitical and economic challenges, ICISA members reported strong market results:

• Surety: Insured exposure increased by 9.3% to EUR 1.5 trillion, while premiums grew by 7.4% to EUR 8 billion. Claims paid fell by 12.6%, reflecting better risk management.

• Trade Credit Insurance: Insured exposure rose 7.5% to EUR 3.5 trillion, supporting record global trade volumes. Premiums remained steady at around EUR 9 billion, with claims decreasing slightly.

Richard Wulff, ICISA’s Executive Director, emphasized that these figures go beyond business success:

“They represent our members’ commitment to supporting the economy even when facing uncertainty. Together, we build a stronger foundation for global trade and financial stability.”

Looking ahead: innovation and collaboration

With growing membership and a robust industry outlook, ICISA aims to increase collaboration, promote innovation, and enhance resilience across the trade credit and surety markets. The Prague AGM reinforced the association’s dedication to enabling businesses worldwide to navigate complex risks and seize emerging opportunities.

Serving the industry beyond borders: Interview with Jan Mueller, the new ICISA President

ICISA welcomes a new President at a time when global trade, regulation, and risk are evolving rapidly. With more than three decades of experience in the credit, surety, and political risk insurance sector, the newly elected President brings expertise, international perspective, and a strong sense of purpose. In this interview, we speak with him about his professional journey, the priorities he envisions for ICISA, and his message to our membership.

Could you briefly introduce yourself and your professional journey leading up to this new role?

I’m 59 years old, married, and the proud father of two daughters aged 28 and 25. My professional journey began in 1990 at Hannover Re, where I joined as a trainee. Over the years, I helped build and shape the company’s credit, surety, and political risk business. In 2000, I became General Manager for all regions excluding North America, and in 2008, I took on the role of Managing Director for the entire operation.

Being married to this industry for 35 years, it was always clear to me that I wanted to contribute beyond my role at Hannover Re. That motivation led me to serve as VicePresident and then President of PASA from 2014 to 2018. Now, after two years as ICISA Vice-President, I am truly honored to continue serving the industry in this new capacity.

What does it mean to you personally and professionally to be elected as President of ICISA?

Personally, I feel honored. It’s a meaningful milestone and certainly an enrichment to my professional life. Our industry has given me so much throughout my career, and working for it through ICISA feels like the right way to give something back.

As President, what are your top priorities for ICISA over the next years?

Our focus will continue to be shaped by the voices and needs of our members. Advocacy remains at the core of our strategy – working toward level playing fields in different markets and advocating for regulatory frameworks that reflect the unique characteristics of our products.

We’ll also strengthen our commitment to education and best practice sharing, both within the membership and with external stakeholders who want to better understand our industry.

Networking remains a major priority as well. The growing attendance at our in-person conferences shows just how much our members value these opportunities to connect. None of this would be possible without the tireless work of our committees and working groups, and I want to encourage all members to actively participate. The more voices we include, the more relevant and impactful our work will be.

We also aim to deepen collaboration with partner organizations like PASA and Berne Union, and foster exchanges that benefit the broader ecosystem.

How do you see ICISA’s role evolving in today’s fastchanging economic and geopolitical landscape?

Credit, surety, and political risk insurance are more relevant than ever. Our products help mitigate risks in trade and investment – something businesses increasingly rely on in today’s uncertain global environment. ICISA plays a key role in representing this value to external stakeholders, while providing members with advocacy and platforms for knowledge exchange.

Are there any particular topics or strategic goals you hope to achieve during your presidency?

In addition to the broader goals I mentioned, there are a few key areas of focus. We plan to implement a structured educational offering across credit insurance, surety, political risk, and reinsurance. This will help raise awareness and promote understanding of our industry globally.

Advocacy will also expand beyond Europe, as more members now come from outside the region. And as technology continues to impact our industry, we will spotlight innovations and share best practices to help members adapt and grow.

What do you see as the biggest challenges and opportunities facing the credit insurance and surety sectors today, and how can ICISA help navigate them?

The increase in global uncertainty is driving more demand for our products. However, in many markets, product penetration remains low, and regulatory challenges persist. These are obstacles, but they’re also opportunities to raise awareness and expand.

ICISA will support members by advocating for better regulatory frameworks, communicating the value of our products, and building bridges with neighboring organizations that influence our ecosystem.

ICISA is known for increasing international collaboration. Are there new partnerships or areas of engagement you would like to explore?

Absolutely. ICISA already has strong relationships with neighboring organizations, and we’ll deepen those where relevant. We also want to enhance our contact with local industry specialists in national associations, ensuring that our efforts are coordinated and mutually reinforced.

How do you plan to engage with the broader ICISA community, including working groups, member companies, and younger professionals?

I plan to attend all ICISA events and stay closely connected to our members. We’re considering a new in-person survey in 2026 to stay aligned with member priorities, including those of the next generation. It’s important to understand and support the professionals who will shape the future of our industry.

Finally, is there a message you’d like to share with ICISA members as you begin your presidency?

I’m genuinely looking forward to serving ICISA and all its members. Being part of this community is a privilege, and I’m excited about what we can achieve together.

One last personal note—what has been the most rewarding experience with ICISA so far?

Without a doubt, it’s the people. Meeting the ICISA family is always a highlight and a reminder of why this work matters.

ICISA Presidents and Vice-Presidents are elected by ICISA membership and serve a one year mandate. It is common that after a year of mandate they are reelected for a second mandate.

A Guide to Trade Credit Insurance

By the International Credit Insurance & Surety Association

A practical and accessible industry-wide reference on Trade Credit Insurance, written by a team of industry experts.

This compact volume is a practical guide for anyone interested in Trade Credit Insurance. The International Credit Insurance & Surety Association (ICISA) presents an approachable but detailed guide written collaboratively by carefully selected industry experts. The guide describes the lifecycle of the credit insurance product, from the initial application stage to the expiration phase of the policy, including practical use aspects for credit managers. The volume offers compact information on the history of trade, the need for protection against trade credit risks, and solutions offered by credit insurance providers. The focus is on short term credit, including whole turnover policies and single risk policies.

Readership

Suitable for anyone interested in Trade Credit Insurance, from credit managers to policymakers.

Importance

• Collaboration of a diverse group of experts from top organisations around the world

• Written in an approachable style, accessible to the non-specialist

• Includes extended glossary of key terminology

• Includes a list of relevant resources for further reading

Content

Foreword; Introduction; Disclaimer; 1.What is trade?; 2. What is trade credit insurance?; 3. Product types; 4. Risk types; 5. Typical set-up of a trade credit insurance contract; 6. Premium, the price for cover; 7. Day-to-day policy management; 8. Buyer risk underwriting in trade credit insurance; 9. Debt collection; 10. Imminent loss and indemnification; 11. Renewal, expiry, termination of a policy; 12. Single risk business; 13. The single risk insurance market: Private and public players; 14. Reinsurance of Trade Credit Insurance; Trade Credit Insurance resources; Glossary of trade credit terminology

About the Author(s) / Editor(s)

The International Credit Insurance & Surety Association (ICISA) brings together the world’s leading companies providing trade credit insurance and surety bonds and their reinsurers. ICISA promotes technical excellence, industry innovation and product integrity, as well as addressing business challenges generated by new legislation.

Where to order my copy?

The book can be ordered from Barnes&Noble, Amazon and Bol.com

Welcoming new voices: TransRe and SMABTP join the ICISA community

ICISA is proud to welcome two new members — TransRe and SMABTP — each bringing unique strengths and fresh perspectives to the global network of credit insurance and surety professionals. In the upcoming paragraphs you can read the answers of Sarah Cuffy, Senior Underwritter AVP at TransRe and Olivier Nifle, Director at SMABTP.

TransRe is a leading global reinsurance company, writing $5.9 billion in annual premiums with over 650 employees across 21 offices in 16 countries, headquartered in New York. Founded in 1977, TransRe has built a strong reputation in Surety, Trade Credit, and Political Risk, with specialized underwriting teams based in New York, Miami, London, and Paris. The company’s strategy focuses on deepening its expertise in these sectors, partnering with established teams that can navigate economic cycles. With a history of growth and expansion, TransRe has become a key player in its markets, supported by solid financial strength and a commitment to flexible, solutions-oriented reinsurance.

SMABTP is a mutual insurance group specializing in property insurance, professional liability, and personal insurance for the construction and real estate sectors. It provides tailored coverage for professionals such as construction firms, developers, architects, and property managers. With a strong local presence across France and overseas territories, SMABTP offers dedicated support through nine regional departments and specialized teams in areas like surety, marine, and transport insurance. Its construction expertise is backed by Socabat GIE, a network of consultants and technicians, and the EXCELLENCE SMA foundation, which promotes quality and safety. SMABTP also manages financial and real estate investments through its subsidiaries, focusing on sustainable income generation and high-quality properties.

TransRe: Global Reinsurance expertise with a specialist focus

With more than 30 years experience reinsuring Credit and Surety lines and offices in 21 countries worldwide, TransRe stands as a global leader in reinsurance, including credit insurance and surety lines. “We joined ICISA because it is a long-standing and reputable institution,” explains Sarah Cuffy. “ICISA offers the opportunity to connect with key industry players and engage in discussions around the most pressing topics facing our industries today.”

As a reinsurer, TransRe often operates a step removed from direct market action, yet values the broad industry insights ICISA provides: “ICISA’s forums allow us to gain a wider perspective beyond individual cedants and better understand the evolving landscape.” Their AA+ rating and knowledge, built from decades of underwriting experience, position them to be a dependable partner within the ICISA community.

Looking ahead, TransRe representatives are eager to both contribute to and learn from members’ insights on industry threats and opportunities, underlining the dynamic environment of credit insurance and surety despite their long histories.

SMABTP: Construction expertise rooted in mutual values

SMABTP, a mutual insurance group born in the 19th century and France’s number one insurer in real estate and construction, brings a distinct niche expertise to ICISA. “Surety is a strategic growth path for us, including international ambitions,” says Olivier Nifle, highlighting the natural fit with ICISA’s values of independence and memberfocused expertise.

SMABTP operates through an extensive local network across France and overseas territories, supporting construction and real estate professionals with tailored insurance solutions –from property damage to surety guarantees and financial completion bonds. Their unique blend of insurance and surety products, combined with a strong customer-centric culture, sets them apart.

“We have successfully melded insurance and surety in a single offer, guided by partnership at our core,” they note. For SMABTP, collaborating through ICISA opens doors to share their specialized know-how and explore new opportunities and partnerships worldwide. “Local expertise, especially around legislation and business practices, is a real strength – partnerships help us overcome the challenges globalization presents.”

A shared commitment to sharing expertise and best practices

Though coming from different corners of the industry, TransRe and SMABTP share a commitment to advancing credit insurance and surety through collaboration. Both highlight ICISA’s role as a vital platform for exchanging expertise and tackling evolving market challenges.

TransRe’s global reinsurance perspective and SMABTP’s experience in construction insurance enrich ICISA’s collective knowledge, offering members access to fresh insights and potential new partnerships.

As both members settle in, they look forward to engaging with ICISA’s events and initiatives, bringing their voices to the conversation and learning alongside their peers.

Together, TransRe and SMABTP and other new members, reinforce ICISA's mission: to be the trusted platform where industry leaders connect, innovate, and shape the future of credit insurance and surety worldwide.

MEMBER ANNOUNCEMENTS

In this section, we highlight the latest updates and milestones from ICISA members. From leadership changes and new partnerships to product launches and rebranding initiatives, these announcements reflect the ongoing innovation and evolution within our industry. Stay connected with what’s happening across the network!

Atradius announces changes in Management Board

Atradius has announced changes in the distribution of responsibilities and the composition of the Management Board with effect from 1 September 2025.

Andreas Tesch, currently Chief Market Officer (CMO), has been appointed as the new Chief Risk Officer (CRO). He replaces Christian van Lint, who is stepping down after a 42-year career at Atradius, including 13 years as a board member. Christian will remain an advisor to the company's highest executive body until 31 December 2025.

The CMO position will be split across Marta Nodal, currently Director of Spain, Portugal and Brazil, and Marc Henstridge, currently Chief Insurance Operations Officer (CIOO). Marta will join the Management Board and oversee operations in the commercial regions of Spain, Portugal, and Brazil; Germany, Central and Eastern Europe; the Netherlands and the Nordics; France, Belgium, and Luxembourg; and Italy. Additionally, she will be responsible for Collections, Surety and Instalment Credit Protection. Marc will lead the commercial regions of the United States, Mexico, and Canada; Asia; Oceania; and the United Kingdom and Ireland. He will also manage Global, Credit Specialties, and Atradius Re.

Claus Gramlich-Eicher, Chief Financial Officer (CFO), will take on the supervision of Enterprise Risk Management, including Outward Re in addition to his existing duties. David Capdevila, Chief Executive Officer (CEO), will take on the oversight of Information Technology Service and Group Marketing and Communication.

With these changes Atradius aims to leverage the unique strengths and expertise of each member, strengthen its ability to achieve the strategic objectives and continue delivering exceptional value to its customers and stakeholders.

Andreas Tesch

Marta Nodal

Marc Henstridge

CGIC appoints a new Chief Executive Officer

Gideon Bochedi, newly appointed Chief Executive Officer of Credit Guarantee Insurance Corporation (CGIC), brings 25 years of leadership in credit insurance, debt restructuring, and claims management. His career at CGIC has been marked by progressive roles, including leading special risk initiatives and driving operational efficiencies.

Known for his strategic vision and ethical leadership, Gideon is committed to strengthening stakeholder trust and guiding CGIC towards sustainable growth and innovation in a constantly evolving market.

Credendo appoints new Country Manager for the UK and Ireland for Credendo – Trade Credit Insurance

Rakesh Dozo has rejoined Credendo – Trade Credit Insurance as the new Country Manager for the UK and Ireland, effective 29 April 2025.

With over 15 years of experience in trade credit insurance, along with expertise in multinational risk pooling for employee benefits, Rakesh brings a wealth of knowledge to his new role. His deep passion for the industry, honed through working alongside leading industry figures, brokers, and clients, positions him well to lead the UK and Ireland team. In his role, Rakesh will be responsible for expanding Credendo’s shortterm credit risk solutions across both markets.

Rodrigo Jimenez appointed new Allianz Trade APAC CEO

Rodrigo Jimenez will take over the Hong Kong based role in October following Paul Flanagan’s retirement after more than three decades with the firm. He has been named regional chief executive for Allianz Trade in Asia Pacific and will take up the post on 1 October 2025, following a three-month transition period beginning in July. Jimenez replaces Paul Flanagan, who is retiring after 34 years with the trade credit insurer.

The appointment is subject to regulatory approval.

Rodrigo Jimenez joined Allianz Trade in 2014 as chief executive in Brazil Since 2021, he has been regional commercial director for Northern Europe and a member of the regional management team. In that role, he has helped strengthen distribution channels and forge closer ties with the risk department to support growth and retention. He has also played a central role in digital transformation initiatives across the region.

Jimenez holds an MBA from Fundação Dom Cabral and a degree in economics from the University of São Paulo.