13 minute read

2.2 Evaluate the need for budgeting of financial and non-financial resources

Croft, C., (2013) Project Management in 8 Minutes. YouTube. Video accessed on 20/1/2020 at: https://www.youtube.com/watch?v=qkuUBcmmBpk

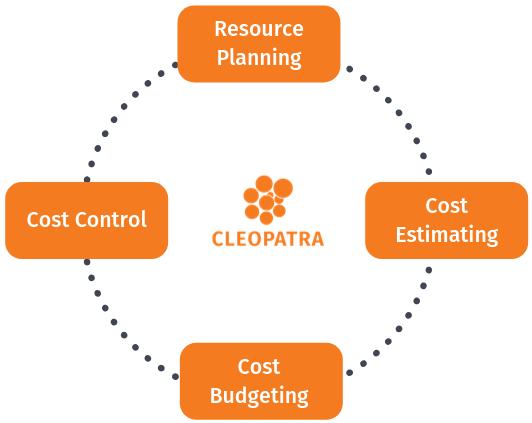

The Project Management Institute publishes the "Project Management Body of Knowledge," which defines how to calculate the budget at completion, budgeted cost of work performed, and budgeted cost of work scheduled (PMI: 2017). These standard calculations help the project manager monitor project progress, stay within the budget and report the project's status using universally recognized terms. An easy way to visualise a framework for cost management has been provided by project management specialists, Cleopatra:

Advertisement

Figure 1: Cost Management lifecycle framework:

Source: https://www.costmanagement.eu/blog-article/198-cost-managementexplained-in-4-steps)

1. Scoping

The first step to an effectively managed project budget is ‘scoping’, to ensure project requirements are accurately identified, documented and confirmed with all stakeholders — and that these are communicated to all parties involved. This crucial step should be completed before budgets are set. Many projects have been initiated around needs but executed around wants, automatically putting projects at risk of budget overruns that leave everyone disappointed.

2. Resource Planning

This is a more detailed step. Resource planning begins in the scope and execution plan development process during which the work breakdown structure, organisational breakdown structure (OBS), work packages, and execution strategy are developed. The OBS establishes categories of labour resources or responsibilities; this categorisation facilitates resource planning because all resources are someone’s responsibility as reflected in the OBS. Resource estimating (usually a part of cost estimating) determines the activity’s resource quantities needed (hours, tools, materials, etc.) while schedule planning and development determines the work activities to be performed. Resource planning then takes the estimated resource quantities, evaluates resource availability and limitations considering project circumstances, and then optimizes how the available resources (which are often limited) will be used in the activities over time.

3. Cost Estimating

Cost estimating is the predictive process used to quantify, cost, and price the resources required by the scope of an investment option, activity, or project (Yescombe: 2013). It involves the application of techniques that convert quantified technical and programmatic information about an asset or project into finance and resource information. The outputs of estimating are used

primarily as inputs for business planning, cost analysis, and decisions or for project cost and schedule control processes. The cost estimating process is generally applied during each phase of the asset or project life cycle as the asset or project scope is defined, modified, and refined. As the level of scope definition increases, the estimating methods used become more definitive and produce estimates with increasingly narrow probabilistic cost distributions.

4. Cost control

Cost control is concerned with measuring variances from the cost baseline and taking effective corrective action to achieve minimum costs. Procedures are applied to monitor expenditures and performance against the progress of a project. All changes to the cost baseline need to be recorded and the expected final total costs are continuously forecasted. When actual cost information becomes available an important part of cost control is to explain what is causing the variance from the cost baseline. Based on this analysis corrective action might be required to avoid cost overruns (Yescombe: 2013).

Other Project Management budgetary considerations:

Expect the unexpected: Budget for contingencies

When it comes time to estimate costs, consultants are required to be realistic. They should ensure that they get input from all significant stakeholders. More importantly, build in contingencies. This step is essential. You need to factor in things outside of your control, such as external environmental considerations that may impact pricing of supplies, resources, labour, financing, product/service shortages, currency exchanges and so on (Bingley: 2015). For example, as the UK prepared to exit the EU, the value of the UK Pound rose and fell more turbulently than was usual. This generated extra supply costs for some business, but (as the Pound fell) yielded more customers for UK services and products because they became cheaper on international markets.

Today’s price or exchange rate therefore may not carry through to the later stages of a project. They are impacted by events such as election results and risks of economic uncertainty. Project Managers must also ensure that vendors

can deliver on their promises and prepare a backup plan. Getting input from other stakeholders and vetting suppliers and vendors can go a long way to setting a more realistic budget that can be met, even if there are unforeseen circumstances that impact costs.

We will see towards the end of this section, that many project managers get caught off-guard with escalating costs, with suppliers that couldn’t meet quoted obligations or other major cost issues. Consultants in charge of project budgets often use free project management budget software, to help with this, such as SmartSheet, Project Budget Manager or AceProject, to draft and debate project expenses.

Develop relevant KPIs

You can’t effectively manage a project budget without establishing key performance indicators (KPIs). KPIs help you ascertain how much has been spent on a project, the extent to which the project’s actual budget differs from what was planned, and so on. Here are just a few commonly known and used project KPIs that are essential to effective project budget management:

• Actual cost (AC), also known as actual cost of work performed (ACWP), shows how much money has been spent on a project to date. • Cost variance (CV) indicates whether the estimated project cost is above or below the set baseline. • Earned value (EV), aka budgeted cost of work performed (BCWP), shows the approved budget for performed project activities up to a particular time. • Planned value (PV), aka budgeted cost of work scheduled (BCWS), is the estimated cost for project activities planned/scheduled as of reporting date. • Return on investment (ROI) shows a project's profitability and whether the benefits have exceeded the costs (Yescombe: 2013).

Revisit, review, re-forecast

A project left to run without budget management and re-forecasting will lead to failure. Frequent budget oversight is essential in preventing budgets from getting too far out of hand. For example, a 10 percent budget overrun is far easier to correct than a 50 percent overrun, and if you don’t keep an eye on your budget and re-forecast, that 10 percent overrun can turn into a 50 percent overrun before you know it. Your chances of keeping a project on track with frequent budget review are far greater than if you forecast once and forget about it.

Other Management Practices

Just as a project’s budget needs to be constantly revisited to keep it on track, so too do the project’s resource usage, since the people working on a project contribute to its cost (Tecce: 2009). Project managers should review the number of people currently working on a project and the project's future resource needs on a weekly basis. Doing so will ensure that you're fully utilising the resources you have and that you have the right resources ready for the rest of the project. Regularly revisiting the resource forecast will help keep your project budget on track. Scope creep is one of the leading causes of project overruns. As unplanned work finds its way into your project, billable hours mount, and the project budget can get out of control. Project managers must carefully manage scope by creating change orders for work that isn't covered by the project's initial requirements. Change orders authorise additional funding for the project to cover the cost of extra work and thus keep the project aligned with its new budget.

Keep everyone informed and accountable

An important part of staying on budget is to make sure all team members are aware of the current budget status as well. Keep the project team informed of the project budget forecast. An informed team is an empowered team that takes ownership of its projects. By keeping the team informed of the budget status, they will be more likely to watch their project charges and far less likely to

charge extra “grey area” hours to your project — hours they know they worked but weren’t clear about what they were working on.

The project budget must be a living part of your projects — something you review with your team and stakeholders on a regular basis. Project managers who carefully watch budgets throughout the lives of their projects will keep stakeholders and management happy and thus experience greater project and career success (Yescombe: 2013).

Consultant’s in charge of procurement

Often, when you come into a project, there is already an expectation of how much it will cost or how much time it will take. When you make an estimate early in the project without knowing much about it, that estimate is called a rough order-of-magnitude estimate (or a ballpark estimate). This estimate will become more refined as time goes on and you learn more about the project. Here are some tools and techniques for estimating cost (Yescombe: 2013):

• Determination of resource cost rates: People who will be working on the project all work at a specific rate. Any materials you use to build the project (e.g., wood or wiring) will be charged at a rate too. Determining resource costs means figuring out what the rate for labour and materials will be.

• Vendor bid analysis: Sometimes you will need to work with an external contractor to get your project done. You might even have more than one contractor bid on the job. This tool is about evaluating those bids and choosing the one you will accept.

• Reserve analysis: You need to set aside some money for cost overruns. If you know that your project has a risk of something expensive happening, it is better to have some cash available to deal with it. Reserve analysis means putting some cash away in case of overruns.

• Cost of quality: You will need to figure the cost of all your quality-related activities into the overall budget. Since it’s cheaper to find bugs earlier in the project than later, there are always quality costs associated with everything your

project produces. Cost of quality is just a way of tracking the cost of those activities. It is the amount of money it takes to do the project right.

Once you apply all the tools in this process, you will arrive at an estimate for how much your project will cost. It’s important to keep all of your supporting estimate information. That way, you know the assumptions made when you were coming up with the numbers. Now you are ready to build your budget plan.

Overruns: Why projects go bad According to management consultancy firm, McKinsey, there are three main reasons for failure (Flyvberg: 2014).

Over optimism and overcomplexity. In order to justify a project, sometimes costs and timelines are systematically underestimated and benefits systematically overestimated. Infrastructure project expert B. Flyvbjerg (2014) argues that project managers competing for funding, massage the data until they come under the limit of what is deemed affordable. Stating the real cost, he asserts, would make a project unpalatable. According to Flyvberg, a McKinsey & Co. contributor, from the outset, such projects are on a fast track to failure.

A common example of this comes when big projects cross state or national borders and involve a mix of private and government spending. For example, a new railway could involve three national governments, numerous local governments, different environmental and health standards, varied degrees of skills and wage expectations, and dozens of private contractors, suppliers, and end users. Just one issue can stall the process indefinitely. In one case, for example, it took two countries a decade to work out the diplomatic considerations that allowed them to build a hydroelectric dam. All too often, these complicating issues are not deeply considered or priced to the fullest before launching a project (Flyvberg: 2014).

According to Flyvberg, a useful reality check is to compare the project under consideration to similar projects that have already been completed. Known as “reference-class forecasting,” this process addresses confirmation bias by forcing decision makers to consider cases that don’t necessarily justify the preferred course of action. For example, if a city wants to build a ten-kilometre metro line

with four stations, it should look at other cities that have built similar lines to understand the true cost and time dynamics.

Poor execution. Having delivered an unrealistically low project budget, the temptation is to cut corners to maintain cost assumptions and protect the (typically slim) profit margins for the engineering and construction firms that have been contracted to deliver the project. Project execution, from design and planning through construction, is riddled with problems such as incomplete design, lack of clear scope, ill-advised shortcuts, and even mathematical errors in scheduling and risk assessment. A McKinsey study of 48 troubled megaprojects showed that poor execution was responsible for cost and time overruns in 73 percent of the cases; for the rest, these were due to politics, such as new governments or laws (Flyvberg: 2014). In part, execution is poor because many projects are so complex that what might seem like routine issues can become major struggles. For example, if steel does not arrive at the job site on time, the delay can stall the entire project.

Another challenge is low productivity. While the manufacturing sector has approximately doubled its productivity over the past two decades, construction productivity has remained flat or even declined. Wages, however, have continued to rise faster than inflation in many markets, resulting in higher costs for the same results.

Weakness in organizational design and capabilities. Many entities involved in building megaprojects have an organizational setup in which the project director sits four or five levels down from the top leadership. The following structure is common:

• Layer 1: Subcontractor to contractor

• Layer 2: Contractors to construction manager or managing contractor

• Layer 3: Construction manager to owner’s representative

• Layer 4: Owner’s representative to project sponsor

• Layer 5: Project sponsor to business executive

This is a problem because each layer will have a view on how time and costs can be compressed. For example, the first three layers are looking for more work and more money, while the later ones are looking to deliver on time and budget. Also, the authority to make final decisions is often remote from the action.

According to McKinsey & Co., capabilities, or lack thereof, are another issue. Large projects are typically either sponsored by the government or by an entrepreneur with bold aspirations; they can take 10 to 15 years to finish. Even individuals who build large infrastructure projects for a living may execute only three or four megaprojects in a lifetime. Because each one is unique, the learning curve is steep every time, and the skills needed are scarce. All these problems are compounded by the speed at which projects get started. Starting from scratch, megaprojects may have to create organizations of several thousand people in 12 to 18 months—a significant operational and managerial challenge equivalent to creating a new start-up company.

Reflective Learning

For a list of the largest cost overrun projects in history, please conduct further reading at: https://en.wikipedia.org/wiki/Cost_overrun

Then scroll down to find case studies in your area of residence.

UK examples can be found at:

https://en.wikipedia.org/wiki/NHS_Connecting_for_Health

https://en.wikipedia.org/wiki/Scottish_Parliament_Building

https://en.wikipedia.org/wiki/Edinburgh_Trams

Exercise – identify a case study that involved serious cost overruns. Explain how and where the budgeting for resources went wrong. (Spend one hour writing notes in your notebook.)

Further Reading:

PMI (2017) A Guide to the Project management Body of Knowledge. Accessed on 19/1/2020 at: https://www.amazon.co.uk/guide-Project-ManagementKnowledge-Guides/dp/1628251840/ref=pd_sbs_14_t_0/259-35841874519039?_encoding=UTF8&pd_rd_i=1628251840&pd_rd_r=e069f1da-131e4998-addc5978d97a89db&pd_rd_w=SVweZ&pd_rd_wg=yk64H&pf_rd_p=e44592b5-e56d44c2-a4f9dbdc09b29395&pf_rd_r=3KDYAV3WQQFGYFT2DX69&psc=1&refRID=3KDYAV3W QQFGYFT2DX69

Yescombe, E., (2013) Principles of Project Finance. US: Academic Press

References:

PMI (2017) A Guide to the Project management Body of Knowledge. Accessed on 19/1/2020 at: https://www.amazon.co.uk/guide-Project-ManagementKnowledge-Guides/dp/1628251840/ref=pd_sbs_14_t_0/259-35841874519039?_encoding=UTF8&pd_rd_i=1628251840&pd_rd_r=e069f1da-131e4998-addc5978d97a89db&pd_rd_w=SVweZ&pd_rd_wg=yk64H&pf_rd_p=e44592b5-e56d44c2-a4f9dbdc09b29395&pf_rd_r=3KDYAV3WQQFGYFT2DX69&psc=1&refRID=3KDYAV3W QQFGYFT2DX69

Yescombe, E., (2013) Principles of Project Finance. US: Academic Press

Bingley, R., The Security Consultant’s Handbook. Ely: IT Governance Press

Tecce, D. (2009) Dynamic Capabilities. Oxford: OUP

Flyvbjerg, B., (2014) “What you should know about megaprojects and why: An overview,” Project Management Journal, 2014, Volume 45, Number 2, pp. 6–19

Infrastructure Productivity (2013) How to save £1 trillion per year. McKinsey Global Institute January 2013