The connections between Politics and Economics have never more greatly interested me than within the international perspective. From history to anticipation of future trade wars, economic sanctions, diplomacy and much more, the theme of international economics is one that contains a panoply of discussions, of which many insightful selects are reviewed in this journal. I extensively believe there is definitely something for every politics and economics enthusiast inside, and it is incredibly worthwhile to debate some of these topics in greater detail after having a read!

Isha Revindharan

In an increasingly interconnected global society, international economics has never been more important. The intersection of economics and politics on the international stage offers a nuanced lens that provides a more holistic understanding of the policies and interactions that shape society. Whether you are wellversed in economics and politics or a newcomer to these subjects, we believe that the thought-provoking articles within these pages will stimulate your curiosity, leaving you tempted to share your insights. We hope you enjoy!

Shinjitha Maganti

The global economic framework established after 1945 was built upon a strong notion: economic interdependence is essential, although not solely, for global peace and prosperity. Does this concept remain valid today? In today's evolving world, as we confront challenges such as the multiple wars, digital economy and climate change, will adapting this idea solve all issues? I am sure that you will enjoy delving into the articles in this journal in which insights into topical issues are uncovered. Enjoy!

Micah Sedghi

War. Conflict. Communism and Capitalism. Ideological divide. In a world of rapid globalisation, it is undeniable that the socio-economic position of the UK economy is largely determined by its relations to other countries. The articles in this journal certainly examine this in their discussion of how the political and economic worlds interact on the global scale. Indeed, it is through an examination of international economics that we may have an idea of our future economy, and, by extension, our very lives. In short, these articles are definitely worth a read, offering an interesting perspective to macroeconomics.

Exploring the Links Between Behavioural Economics and Environmental Economics

~ Wafi Ali, Year 13 ~

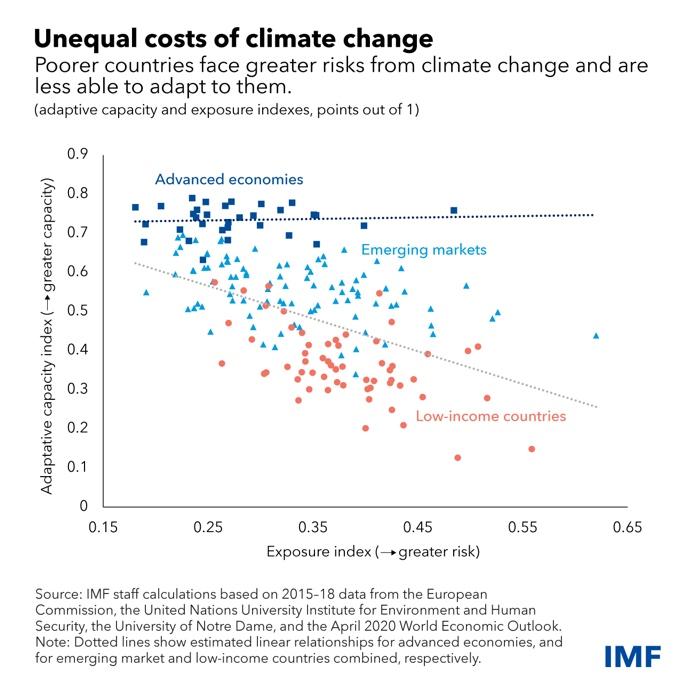

Behavioural economics analyses the deviations of human thinking and decision-making from rational choice theory, the standard economic decision-making model for Homo Economicus. In this brief article, I delve into some of the connections between concepts within behavioural economics and climate-related disaster mitigation, not just a topical issue, but a fundamental strand of research which can be used to explain (although it is a bit of a stretch) why many low income countries (which perhaps are also correlated with likelihood of climate disaster in some regions) tend not to expand as quickly and catch up with countries at the top of the charts. The graph (left) portrays that lower income and middle income countries tend to be more vulnerable and prone to climate disasters naturally, but economically, they have less capacity to adapt in accordance with their risk, whether this is through building disaster-proof infrastructure or by other means.

Graph source: (IMF, 2015)

Rational choice theory has an intricate link to climate disaster mitigation, especially in how much victims are likely, in preparation, to save for themselves and in protection for the relative good.

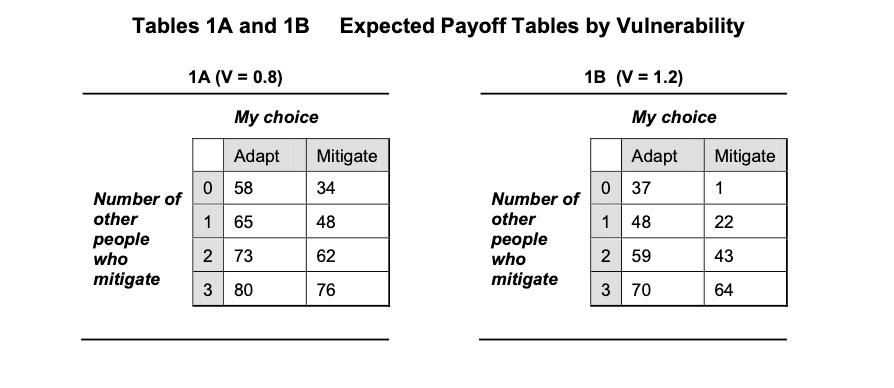

A study conducted by R. Hasson, A. Löfgren, and M. Visser, studied disaster mitigation as public good investment, and therefore initially used a prisoner’s dilemma matrix to depict the likelihood of investment, where ‘adaptation’ means to invest for oneself, and ‘mitigation’ is investment for the wider good. In the case of disaster, 100% investment in mitigation results in higher protection for everyone, higher than overall payoff if everyone invested 100% in themselves. The diagram below shows this, where the Nash Equilibrium is investing in oneself, according to rational choice theory.

Graph source: (Hasson, Löfgren, Visser, 2009)

Although for the diagram above, there are many more parameters that need to be valid for the exact numbers to show, both tables depict that in both levels of vulnerability, the prevailing option is to Adapt. Therefore, society ends up in a Pareto-inferior outcome. The socially optimum position of full mitigation is all investment in the bottom right cell. The risk/return ratios (the loss from free riding) are constant for both levels of vulnerability, yet the overall payoffs in the low-vulnerability table are greater than in the high vulnerability table.

The reason I start with this model is that deeper study within the model actually showed that there is a negative correlation between vulnerability of the potential victims and the amount they invest

in mitigation. Therefore, in countries that are the most likely to be affected heavily by climate change, smaller economies such as Bangladesh and Sri Lanka, for example, which are closer to sea level, the investment is more likely to be uncoordinated, ‘selfish’ investment, whereas these are the areas which have the greatest likelihood of natural disaster and greatest need for investment in mitigation. Yet this result is not surprising, firstly as it is more costly, in terms of a cost of a disaster, to mitigate in the high vulnerability scenario, and second as in both scenarios, less than 30% on average of participants in a separate questionnaire study, stated that they believed other participants would invest in mitigation. This certainly has implications for binding international commitments as the uncertainty regarding preferences for cooperation by others greatly reduces an individual agent’s own willingness to engage in cooperative measures.

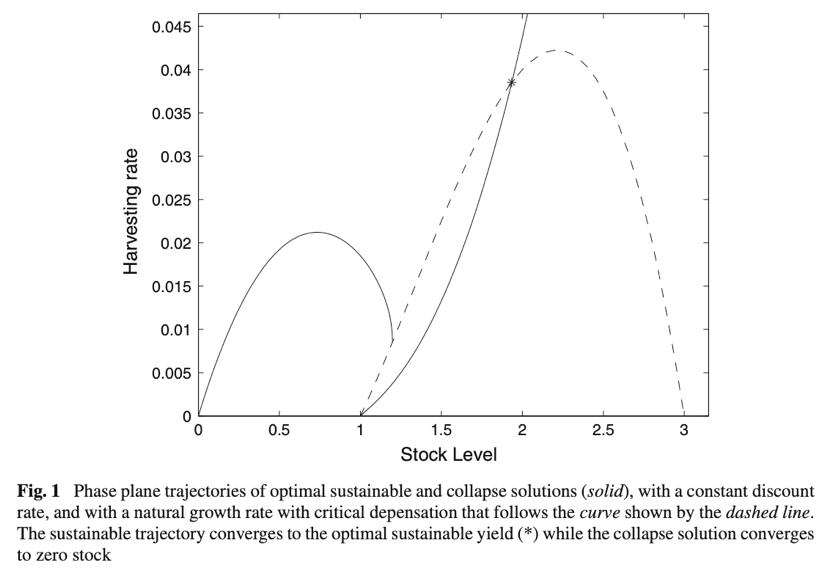

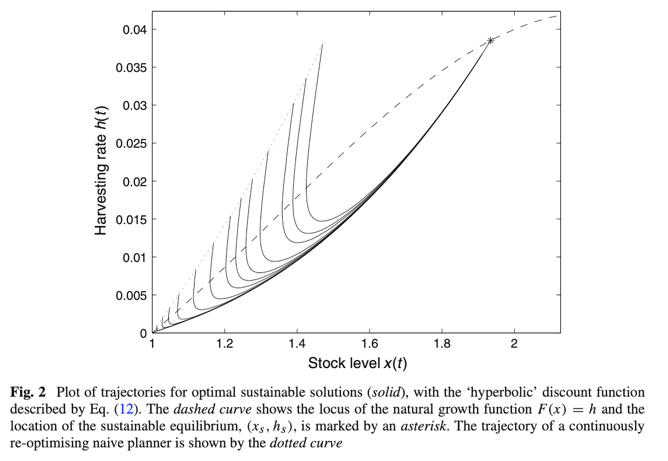

Behavioural economics also links into business decision-making when it comes to the cognitive bias of hyperbolic discounting, which, in simple terms, refers to the tendency to value immediate, though smaller, rewards more than long-term larger rewards, implying an inverse relationship between the discount rate and the size of the delay. Perhaps the discount rate is not actually a function of relative location in time, but a function rather of time delay. In any case, the application of hyperbolic discounting in the real world is in human self-control problems, for example, substantial credit-card borrowing at high interest rates, and substantial illiquid wealth accumulation at lower interest rates. These issues inextricably link to resource management in environment-related sectors, fishing being one. I will below briefly explain how the bias of hyperbolic discounting can differentiate the business sustainability of the committed businessman and the business collapse of the naïve hyperbolic discounter businessman. The renewable resource of fishery is used in this example, but within environmental economics, this same model could be representative for problems such as water scarcity, forestry, and the Earth’s carbon cycle. The model determines consumption (in the form of harvesting of stock) and stock pathways for a businessman who is either committed, in the sense that they choose an optimal path planned for, or naïve, in that they believe themselves to be committed but in fact re-optimise and adjust their plan continuously as time passes, believing the discount rate to be relatively high and continuing to harvest. Assuming that there is constant elasticity of utility in this model, there are two trajectories that form. The graph Fig.1 shows the solid line of the committed businessman, who’s harvesting rate is high in the initial period, when the discount rate is high. The result is that fish stocks initially decrease. Yet, as the discount rate falls over time, the businessman will reduce the harvest rate temporarily, to allow the stock to rise to equilibrium level. Yet, the hyperbolic bias affects the naïve businessman, who succumbs to the temptation to reoptimize as time passes. This naïve businessman will discount the future hyperbolically, such as that the discount rate ‘now’ is high, while the future discount rate will be lower: this statement if consistently used, will mean that the harvest rate continues to increase. The dotted curve on the graph Fig.2 shows this trajectory. The initial harvest rate is also set to lead to the *equilibrium point, yet with very short intervals, the businessman is starting on a

new path to equilibrium, and every new curve represents this new intention per change. As time passes, stock levels fall.

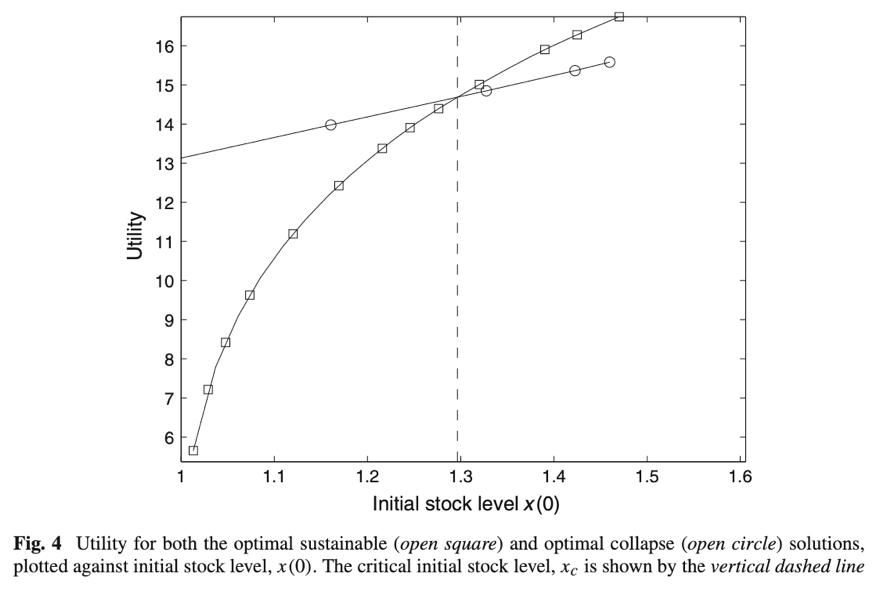

There are some cases where a collapse pathway however, is stable: if the productivity of the stock is not high enough to justify the ‘investment’ (in the form of foregone consumption) necessary to return stock levels to the sustainable equilibrium. This would mean that at some point, the businessman will reach a critical initial stock level, below which returns on the stock are not high enough, after which the collapse pathway will provide greater utility than sustainable management. This is analogous to liquidating the asset and investing in an alternative higher-yielding asset. The graph Fig.4 shows this, depicting the same critical initial stock level 1.3, but the more efficient solution once this is reached being the collapse pathway which more quickly ends the business, saving overall opportunity cost.

The hyperbolic discounting bias has been found in many cases of fishing, one of which being the 1977 Canadian Cod management. In 1977, Canada extended its jurisdiction and took a wider role in the management of Newfoundland fish stocks, and during the course of the 1980s, fishery organisations employed virtual population analysis to estimate and forecast Atlantic cod stock. This, even after advanced population analysis, was continually an overestimation in the years 1982, ‘83, ’84, ’86, and ’91. These overestimations encouraged harvesting at higher than optimal levels and was one of the principal factors in the demise of the northern Atlantic Cod. This was incredibly indicative of the hyperbolic bias among profit-seekers through the consistency of overestimations, even with innovation in technology.

In conclusion, behavioural economics clearly has multiple intricate links with environmental decisionmaking and resource management, yet many would question whether in fact this behavioural failure on our part could be considered market failure. Some argue that market failure itself leads to behavioural failure, which leads to continued market failure, fundamentally because people are not isolated decisionmakers usually, rather their decisions are made in the context of markets, rewards, habits, and social rules. Therefore, the tests of rational behaviour must be considered holistically with the links with the experience provided by an institution, hence, researchers interested in policymaking should think about the power of ideas of rationality spill-overs and rationality crossovers. Studies have shown that arbitrage within an economy can have immediate effects on pushing people’s rationality towards rational choice theory, hence, many policymakers in the future may want to think about whether market-like arbitrage can reduce behavioural failures in the environmental sector, or whether artificial arbitrage -like government intervention or solution could be used to reduce behavioural failures. Yet, when questioning market failure and behavioural failure, there are many more questions that arise: for example, the theory of second-best that if behavioural failure and market failure are simultaneously existing, could solving one but not the other decrease social welfare even more? Out of the many behavioural failures, what if there is some degree of behavioural complementarity or substitutability across all the biases? Does that mean we must intervene to limit ineffective decision-making in regards to all the biases, or just some, and in what proportions. What is the curvature of the probability weighting function for each person in the target market? This topic is clearly one that has only made a ripple in the surface, and a colossal expanse of findings yet to discover.

Foreign Aid: Good or Bad?

~Isha Revindharan, Year 13 ~

Foreign aid is the transfer of capital, goods, and services from one government (or aid agency) to a recipient country. As the gap between the world’s richest and poorest conknues to grow, aid has been subject to great scrukny as people queskon how effeckve aid has been in global redistribukon efforts. Within the foreign aid discussion, there are a range of differing voices and viewpoints to consider: some advocate for a ‘laissez-faire’ approach, arguing that the risk of recipient countries becoming dependent on aid far outweighs any possible benefits (therefore developing countries should be len alone to allow the market mechanism to distribute resources) while others argue that foreign aid corrects market failures and provides ‘one big push’ for individuals living in poverty within developing countries, providing them with more opportunikes. Foreign aid has proven to be successful in some instances, however, ignorance on the part of aid workers and local policymakers onen causes aid to be ineffeckve (and in some cases completely counter-effeckve).

‘Us’ and ‘Them’

Working with an Afghan Women’s Associakon in 2002, Dr Maliha Chishk circulated a needs assessment survey asking Afghan women what they needed from the Toronto-based NGO. Upon receiving an overwhelming response asking for access to basic healthcare, Dr Chishk drew up a plan for a mobile health clinic with a modest budget. However, her proposal was denied by the Canadian government, who offered her a much larger budget on the premise that she would instead provide a human rights training program for Afghan women. Aner arriving in Afghanistan, Dr Chishk found many other aid agencies offering workshops idenkcal to hers, and yet there was not a single mobile health clinic to be seen. If the aid agencies had chosen to listen to the requests of the Afghan women, their resources could have made a huge impact, however, they chose instead what they believed was necessary for the local women, leading to a wasteful duplicakon of resources.

Aid establishments determine the priority to offer one program instead of another based on their wishes regarding the future of a developing country. Ignoring the local cikzens, aid agencies are onen able to step in and implement policies whilst knowing very liple about the local context (e.g. the role of religion and tradikon, the polikcal history, and the language) with the goal of reforming these countries to become more like their own. This can cause aid to be completely ineffeckve: it can lead to wasteful expenditure, unankcipated responses to changes, or simply a harmful power imbalance that can lead to further consequences. By dismantling this assumpkon that we know what is best for them, aid is more likely to work in favour of the recipients, as the policies revolve around providing help where it is wanted and needed by the local cikzens rather than booskng the egos of the developed world.

A Guide to Enktlement

In some instances, aid is not just ineffeckve, it can harm economies.

Grants are onen given to developing countries with the aim of injeckng money into the economy (e.g. via government investment projects that have mulkplier effects) and bringing about growth. However, individuals tend to assign value to things that come at an expense to them, and since these grants are viewed as ‘free’ funding for their governments, some economists argue that individuals subject to governments in receipt of grants care less about the ackons of their governments. This allows corrupkon to run rampant, with a clear example being Jacob Zuma (former president of South Africa) who spent US$16 million on security updates for his house. The reasoning behind this expenditure may have seemed somewhat reasonable at first, however, further inveskgakon revealed a large proporkon of the money was put towards construckng himself a swimming pool. When queskoned, Zuma claimed it was a ‘firepool’

that served as a fire proteckon device, yet reporters found the ‘firepool’ to bare no significant difference from an ordinary swimming pool.

Although Zuma did eventually have to repay the government money he had spent, he faced no real disciplinary ackon and his presidency conknued for a year. If Zuma’s ackons were presented as though tax-payer money had been used to fund his extravagant expenditures, Zuma would likely have faced repercussions for his ackons. However, since it was money donated to the country, individuals were much less concerned. In both scenarios, the gravity of the situakon should be equal, as Zuma had used money intended to increase the welfare of the cikzens for his own private gain. However, individuals tend to be loss-averse. Since tax represents a direct loss for individuals, they feel more enktled in regards to what the money is spent on. On the other hand, the aid income is simply a gain, and individuals typically care more about losses than gains. It could be argued, therefore, that aid switches off accountability demands.

I am by no means suggeskng the solukon is to raise taxes in developing countries. Those earning lower incomes tend to already be the most affected by exiskng indirect taxes (such as VAT and excise dukes). Perhaps if individuals were made more aware of how much tax they were paying, they would feel more inclined to demand that their governments take ackon and implement policies that skmulate growth across the country. In turn, corrupkon would be much harder to ignore, therefore, over kme, aid contribukons could be redesigned to work with the cikzens of an economy.

Success stories

‘Gavi’ (the Global Alliance for Vaccines and Immunisakon) was established in 2000 by the Bill & Melinda Gates Foundakon with the aim to ensure access to vaccines for all children around the world. Although countless new and effeckve vaccines were entering the global market, many developing countries simply could not afford them. Gavi stepped in to address this market failure. As the organisakon grew in size (by working with governments and NGOs as well as various partners such as the World Health Organizakon, UNICEF, and the World Bank) they became increasingly able to negokate more affordable vaccine prices for developing countries. Addikonally, they share the costs of implemenkng these vaccines and, as a result, have helped to halve childhood mortality rates by averkng more than 17.3 million future deaths. As children become healthier, their families, communikes, and countries are in turn more able to become economically prosperous, helping to boost the economies of lower-income countries.

Gavi has managed to successfully overcome many of the issues typically associated with foreign aid. By working with local governments, Gavi ensures systems are in place to efficiently distribute the vaccines once they are delivered. By directly providing vaccines, there is no risk of corrupt polikcians being the only ones to benefit from the aid. As of 2022, 19 countries have transikoned out of Gavi support and are now able to fully self-finance the vaccine programmes.

Conclusion

The world consists of countries, each at their own stage of development, working to sustain their growth and improve the future prospects and living condikons of their cikzens. There is no ‘end goal’ that these countries are trying to achieve, as even some of the most developed countries are skll pursuing economic growth. Foreign aid, when implemented aner careful considerakon and mekculous planning, can help to ensure there is equal access to opportunikes for all, regardless of the level of the development of their country. Working directly with local governments and monitoring the effects based on how the policies work with respect to standards and expectakons set by local people is vital in order to effeckvely help the developing world towards a path of economic prosperity.

Classist Alienation: Marxist Literary Theory and Kafka

~ Micah Sedghi, Year 13 ~

Franz Kafka was a modernist writer and existentialist writer who lived a rather mundane proletarian life; fulfilment was low, and modern term “Kafkaesque” specifically refers to systems of dystopian bureaucratic nightmare. So, what was Kafka thinking and feeling as one who experiences and observes this system of the Kafkaesque? In this short piece, I will examine how Kafka depicts class struggle and alienation in his magnum opus Metamorphosis (whilst his pieces, like The Trial, also centre bureaucratic dystopia). In this case, in terms of the legal, the sector in which Kafka worked, it is the novella Metamorphosis which best expresses the psychological and emotional manifestations of an economy idealising “high mass consumption” (with reference to Rostow’s modernisation theory).

In the text, the protagonist, Gregor, awakes to find that he has been turned into a human sized dung beetle. He is late for work. And when he manages to open his door, after hours of his family’s calling, his family (and manager) are repulsed. He spends the remainder of the text in his room, dissociated from the familial sphere. His sister tends to him, giving him rotten food (which beetle-Gregor is partial to), whilst being repulsed by the sight of him. The beetle makes his way out of his room a couple of times, the father terrorises him, throwing an apple at him which lodges in his body. Eventually, all artifacts are removed from his room, and there are 3 tenants who seem superior in the home. One evening, the sister performs violin (badly) and where the 3 tenants snicker, Gregor comes out in love and congratulations. A secondary row commences, days later, the beetle expires (beetles don’t last long in such a cruel world). The sister starts working at the shop, and the mother and father begin working to. Economic activity commences.

How morbid Micah! Concluding the traumatic events of the Samsa’s in such an unfeeling way!

Gregor is the proletarian slave before he turns beetle. His working is central to the family’s financial security. His whole human persona is characterised by the worker (quite literally, living to work), which is how his family, and society, values him. As soon as he can no longer work, he is presented as repulsive, a literal creature of rot. His manager visits his home because of his supposed lateness on the first day, an extremely dystopian thought which puts into perspective the gravity of the strain of glamorous dreams of “high mass consumption”. To the unnamed elite, such “high mass consumption” may be a game, perhaps Tetris for a new GDP high score; but for the likes of the worker, for Gregor, this is dissolving the essence of personality, hobbies, love, and relationship for the sustaining of biological life.

In some senses, his adoption of the beetle form can be read as his rejection of the capitalist system of oppression. This too is met with strain. Though a potential communist, he is stuck within a class system, and familial system, which expects him to provide (and thus, conform to the proletariat-bourgeois divide). When he doesn’t do this, he is outcast and replaced by the newly valued three tenants, who fulfil this function.

The final familial scene speaks most beautifully of the shifting values of man due to the strains and expectation of economic demand. The sister’s musical skill (though bad) is mocked by the three tenants, and only praised by the alienated socialist beetle monster. In a system which values labour, skill, and growth, beautiful things - such as art, and music - are devalued (just as emotional connection, and empathy is). Therefore, the laughter of the (very rude) tenants is an exemplum of a developing social fabric which seeks to oust all which may be “imperfect” or which are “not aiding neoliberal goals”. Specifically, the fact that it is Gregor himself who comes to the praise of his sister shows that in the rejection of the singular identity of “proletarian worker”, one can gain depth, appreciation of music, and, on the most basic level, empathy (arguably, the only case of empathy we see in the text).

After the altercation which ensues, Gregor is weakened, and passes. The family find respective work, and the lives of mother, father, sister, continue. The Samsa’s (except the protagonist) continue. The economy continues as it did before, and the Samsa’s (except the protagonist) are the same as before.

The difference? We as the reader are not the same as before. Kafka has clearly curated an aesthetic masterpiece in this novella. Providing us with a lens to surpass capitalist myopia, and, perhaps, appreciate the real loss of humanity which is accompanied by the hedonistic materialism of capitalism.

So…what now? Well, sadly, there is not much we can change. But, most importantly perhaps, we may change our behaviours and ideas and empathies. I am certain that- under the simplistic syntax, and dense atmosphere of Gray, Kafka’s is a belief in love. An observation of a loveless society. And invoking questions, and hopes, of a society of love. A society which we may foster in our own action.

The Unequal Impact of Globalisation

~Bhavya Krishna, Year 13 ~

The term "globalisation" refers to the growing interdependence among nations, individuals, and businesses worldwide, brought about by cross-border trade in goods and services, technology, flows of investment, people, and information. The primary cause of the current increased rate of globalisation is the sharp increase in international trade and investment. However, other drivers are also responsible for shaping globalisation today, such as the development of global financial markets, the emergence of multinational organisations, and technological advancements in transportation and communication. A globalised world is emerging because of a combination of these factors, creating more interconnected economies worldwide.

New markets have emerged due to globalisation, giving businesses the chance to expand their reach beyond domestic boundaries. Lower trade barriers, such as tariffs and quotas, have made it easier for goods and services to move across international borders, enabling businesses to tap into a global customer base. Numerous economies have experienced increased trade volumes and economic growth because of this increased market access. This has allowed countries to take advantage of their comparative advantages and specialize in producing goods and services that they are most efficient at , lowering prices, improving competitiveness, and enabling countries to increase their productivity. Specialisation drives economic growth and raises living standards.

The establishment of the World Trade Organisation (WTO) in 1995 has played a pivotal role in promoting global trade. Trade liberalisation agreements, negotiated through the WTO, aim to reduce barriers to trade and create a more open and predictable international trading system. While this fosters economic growth and efficiency, it also means that economic changes in one country can have significant repercussions globally and has intensified competition among nations in the international marketplace. Some countries, particularly major economies, may experience trade surpluses, while others face trade deficits. Trade imbalances can lead to tensions as nations seek to protect their domestic industries from foreign competition. In response to perceived economic threats, some nations adopt protectionist measures to shield their domestic industries. These measures can include tariffs, quotas, and subsidies. Trade restrictions can disrupt global supply chains, forcing companies to find alternative suppliers or reevaluate their production strategies, leading to increased costs and reduced efficiency. Trade wars, therefore, raise questions about the future of globalisation, some companies may consider reshoring production or shifting towards regional supply chains to reduce dependency on global suppliers and mitigate risks.

The benefit of globalisation is not universal. Globalisation leads to increased competition between companies, which can result in closures, offshoring, and job losses. The manufacturing sector, basic metals and fabricated metal products, footwear, leather goods, textiles, and apparel industries are the most at risk due to the prevalence of low-skilled occupations in these sectors. Manufacturing is the sector that is the most exposed to offshoring because of competition from low-wage countries. Although international trade liberalisation has positive overall outcomes, certain sectors may face significant challenges, undermining the initial benefits. The "China trade shock," has hurt many American workers as Chinese exports to the US have substituted for comparable American-made products. Despite the increase in U.S. exports to China over time, a substantial trade deficit has emerged, primarily because the U.S. imports more from China than it exports. This has led to a decline in employment within U.S. manufacturing industries, and the United States has missed opportunities to generate new jobs in this sector due to the rapid surge in Chinese imports compared to U.S. exports. These brought the two largest economies in the world into a trade war, in which, the United States is accusing China of a series of breaches; from unfair trade (dumping goods at low costs) to intellectual property theft (patent copying); which has now become more of a political issue than an economic issue.

Overall, while globalisation has brought about numerous economic benefits to nations, it has also created challenges and tensions, leading to trade wars. The interconnectedness of global economies requires careful navigation of trade policies to balance the advantages of open markets with the need to protect domestic interests. Negotiation and international cooperation are essential for resolving trade conflicts and maintaining a stable global economic environment.

Over the last 20 years, has rapid economic growth in China also increased happiness?

~ Aryaman Singh, Year 13 ~

China is a country located in East Asia with a communist government led by President Xi Jin Ping. Over the last 20 years it has experienced drastic economic growth, making it the second largest economy in the world, based on current prices (real GDP). By 2025 it is predicted to account for 30% of Global economic growth, as opposed to its competitor, USA, at 10% (whom it is also predicted to economically dethrone within the next decade). This has been influenced by its socialist economy which integrates both a private and state sector, a big advantage over the much more privatized western economies. This allows it, in Xi Jing Ping’s own words, to “use both the visible and invisible hand.” However, the sustainability of such rapid economic growth must also be considered. This is because, although the people of China may enjoy the benefits of more advanced and independent living, it must be brought into question whether the stresses and pressures on the working population to stimulate this growth will allow there to be a net increase in happiness.

Most certainly, China’s economic growth has been remarkably linear and unbreakable. It was the only front running economy to grow during the pandemic. Whereas many pre-established economies like the UK sank considerably (by 20%), China steadily reached a growth rate of 4.9% by September 2020. We often see that - due to the circular nature of economies - increases in productivity like this allow the government to make withdrawals and put money into developing social schemes. In China’s case, one could argue that by refraining from prioritising consumer goods and instead saving and investing this money back into the economy, China has been able to make a shift away from primary industry (i.e. agriculture) and instead focus on secondary industries like manufacturing and exports. This is evidenced as China invests more than 40% of its economy (double that of USA) which leads to constant innovations in capital and automation, which we can witness as globally 1/3 of all new industrial robots are being installed in Chinese firms, per year. This incentive directly combats China’s Demographic dividend where, in the 1980’s, there were three times as many people in their 20s as those in their 60s, a figure that has now become equal. Moreover, we saw a 20% decrease in birth rate from 2020-21.

However, this can play out in the working population’s favour as the dual influence of rapid industrialisation/more profitable jobs and fewer workers has led to an overall increase in incomes (controlled demand-pull inflation). There are several ways that this can increase happiness. Firstly, from a social standpoint this leads to much more financial freedom: people are more confident in moving to and starting families in the city (leading to 64% of people now living in urban areas, compared to just 50% 10 years ago, where they enjoyed a greater variety of services (e.g. healthcare) and opportunities. This is a big step up from the situation just a generation earlier where people of working age would be allocated jobs and given permission to marry by party-led groups known as Danwei. As a result, economic growth has increased happiness for the working population as people now have far greater autonomy over the career path they chose or whether they want to get married (as more independence increases quality of life). In addition to this, higher wages also increase security within families. Over the last 20 years, China has become the largest economy in the world, based on purchasing power parity (PPP). This means that the ‘basket’ of goods that people can now buy for a set price within China has increased ($1000 in China buys more things in the UK). This makes a higher salary (stimulated by China’s aforementioned economic growth) much more valuable, as it leads to a more pronounced improvement in standard of living (people can afford a broad variety of material goods). More specifically this also leads to better living standards (and thus longer life expectancy) which means people are less likely to suffer from life changing illnesses etc. which accumulate to leave the average person feeling far more secure about how they live their lives/luxuries that they can afford. However, perhaps a more important influence on happiness has been the steps the government has had to take to sustain this rate of growth. For example, the aforementioned shift from agriculture to service sector has meant that the government has needed to prioritise the upskilling of the workforce, which can be seen as the number of higher education institutes in China has

gone from 1022 to 2263 in the past decade, leading to a doubling in the number of graduates since 2010. Not only does this change the global perception of China away from just being the ‘workshop of the world’ but it also means that there is now less need to study overseas. This increases happiness by reducing the stress involved with affording international education, as well boosting family unity (as people don’t have to leave each other behind).

On the other hand, one may argue that the drastic economic growth in China has not translated to an increase in happiness. Perhaps the biggest issue is the stress that is put on the Chinese workforce to sustain this growth. A prime example of this is the ‘996’ scheme where people, particularly in sectors like IT and in office jobs, are forced to work from 9am to 9pm 6 days a week. This can significantly reduce the quality of life of younger adults who may have young children for whom they simply do not have the time to care for. Moreover, the intensity of such a work structure can also pose serious detriment to people’s mental and physical wellbeing (a factor which directly decreases quality of life). In addition to this, the Chinese government itself has also proven to not always prioritise the safety of citizens if it puts economic growth in jeopardy. For example, during the pandemic where China impressively saw continued economic growth, the government took very drastic measures to get its economy back on track, such as cutting off access to cities of 60 million people, which led to it announcing that the disease was under control by March 2020. Although this would be quite an achievement, the intentions of the government must also be considered. This is because the measures taken by the government were not actually fully successful, leading to Covid still having significant impacts on the health of Chinese people 2 years later (i.e. there are still lockdowns occurring in major cities such as Beijing) whereas places like the UK despite not taking as drastic initial steps, have far greater control over the virus due to the success of their vaccine programmes. Moreover, China also refrained from rolling out a Covid stimulus package of $1 trillion like the USA and Japan. This is significant as it suggests that China, due to its prioritisation of economic growth (which is increasingly overshadowed by its demographic dividend which is constantly reducing it working age population) often finds itself not prioritising the long-term health and wellbeing of its citizens. This can decrease happiness and life satisfaction as people are now being forced back into lockdowns, upturning their ways of life and social security, all of which could have been avoided if the government had prioritised an effective vaccines scheme/longer initial lockdown rather than keeping up economic growth rates. Furthermore, the urbanisation of cities also brings about its own issues. For example, in Shanghai the average house price is 23 times the median income, twice the ratio in London. This poses an issue as it reinforces the mentality of just making ends meet, meaning that people are less encouraged to have more than one child (which is evident as the 1 child policy was lifted in 2016 yet the birth rate continues to slip) and can force families to have to change plans as it is simply unaffordable- reducing life satisfaction and thus happiness. Moreover, in order to combat low birth rates, the government has planned a 3-child policy which will improve maternity benefits, lower education costs and increase state funded nursing homes. Although on the surface this would significantly improve the lives of women within China, China has clearly prioritised economic growth over the last 20 years, which has meant that it will be really hard to develop schemes (like state subsidised healthcare or pension systems) from scratch for a country of 1.398 billion as there was never any real funding or plans to set them up in the first place. This means that when these changes do occur, they will be much harder to implement across the whole country. This reduces happiness, as clearly there has never really been any successful public welfare schemes and the only real incentive for the government to set them up in the first place is to ensure China’s economic growth does not halt (e.g. 3 child policy).

To conclude, I believe that economic growth can increase happiness. However, these are only symptoms of a country getting richer (e.g. more developed healthcare) and clearly governments are much more likely to prioritise economic growth to the detriment of happiness.

Is China Manipulating the Value of its Currency?

~ Garv Gupta, Year 12 ~

No country has officially been named a currency manipulator by the US since Bill Clinton's administration did so to China in 1994. In 2019, following a prolonged signalling of desiring an exchange rate stronger than seven yuan to the dollar, China intentionally changed its stance and allowed the yuan to depreciate beyond this mark. It then fell to an eleven-year low against the dollar, and the Trump administration once again labelled China as a currency manipulator. Speculators have criticised China for having a surprisingly weak currency when compared to the vast size of its economy, and with China being the second largest economy in the world after USA, the debate, whether China have been manipulating the value of its currency in order to increase economic activity through injections in terms of exports, has been ongoing for years as it is seen as an unfair advantage in the game of international trade.

Background

As an economy that is heavily dependent on manufacturing and exports, China runs a trade surplus. Chinese exporters receive payments in U.S. dollars (USD) for their goods, yet they have local expenses and payroll obligations in the Chinese yuan to pay for labour, capital, resources etc that are used in the making of these goods and services. Given the substantial influx of USD and the persistent demand for yuan, the exchange rate between the two currencies may tilt in favour of the yuan. If this appreciation in the yuan continues, Chinese exports may become costlier, potentially decreasing their com petitive advantage on the stage of international trade. Such a scenario poses significant challenges for the Chinese economy which is centred around exports in order to run their economy, potentially leading to reduced sales of manufactured goods, an increase in unemployment rates, and a potential economic shutdown. To avoid such a situation, the People's Bank of China (PBOC), the nation's central bank, takes strategic measures to regulate exchange rates, employing carefully considered interventions to maintain a favourable exchange rate environment. The PBOC’s ability to take these measures to essentially manipulate the worth of their currency to maintain competitive trade advantages is the core of this debate.

Pegs

The historical context of China's currency management is pivotal in understanding the ongoing debate. In the past, China operated under a fixed exchange rate system, pegging the yuan to the USD. China, along with 66 other countries, use this system of pegging their currency to the American Dollar which comes with clear advantages, such as preventing excessive volatility in a country’s currency due to market conditions and hence prevents a potential currency crisis. Additionally, a currency peg maintains the competitiveness of a country’s exports for major importing destinations, such as the US and EU, as pegging keeps the value of a currency low compared to other countries. A currency peg that keeps the yuan's value lower compared to other currencies enables consumers using foreign currencies to purchase more of China's exports. This is especially notable when the PBOC intentionally keeps the yuan's exchange rate relatively weak against the U.S. dollar, allowing consumers using the dollar to acquire more Chinese goods, where exports play a pivotal role in any economy as they signify an injection of capital into an economy.

Though, alongside the clear advantages from which the Chinese economy thrive from, there are distinct disadvantages such as in the case of sizeable fluctuations in the reference currency (USD), the domestic currency also experiences significant volatility. More importantly, if a currency is pegged at an overly low exchange rate, it deprives domestic customers the purchasing power of buying foreign goods. Though foreign consumers are able to buy goods and services at lower rates in China, it is at the sacrifice of the Chinese people who do not have the same opportunity – they are deprived of the purchasing power when it comes to purchasing foreign goods. This system helps keep the yuan undervalued and secure Chinese exports, and it seems pegging is a legitimate route for China to maintain an undervalued currency. Thus far, it is clear China is not breaking any rules through this system, though their economic success through pegging should not just be seen at face value.

China’s Unfair Regulation of the Yuan

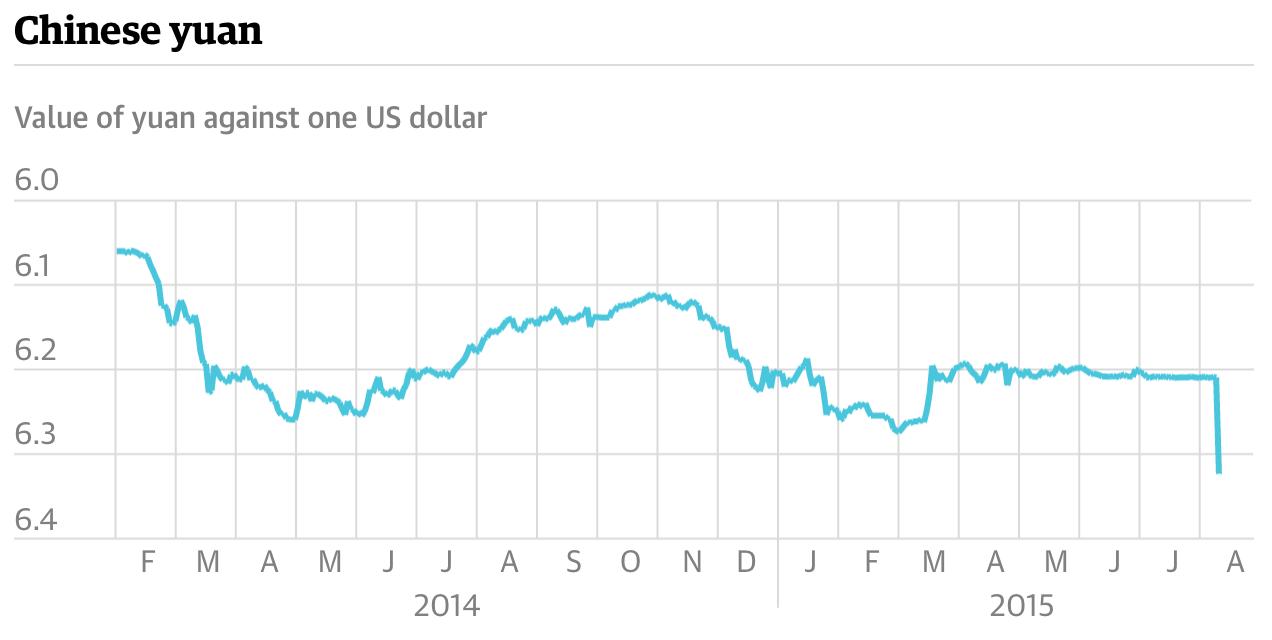

On July 2015, China experienced an 8.3% fall in their exports. China’s central bank responded by devaluing the yuan by nearly 3% against the US dollar in August, as shown in the figure below.

China’s efforts to devalue its currency were purposeful and strategic, as it increases the purchasing power for foreign customers, therefore a greater number of customers will buy goods from China which in turn increases their exports, alongside increasing their competitiveness in international trade. The deliberate devaluation of the yuan prompted an angry response from the US and other countries, as a weaker yuan damages US exports. This is because domestic Chinese firms will have a lower purchasing power and are less likely to source product from overseas, in addition to other countries preferring Chinese goods (due to their extremely low price through a favourable exchange rate) over American goods. As a result, injections into foreign economies are reduced, whilst injections into the Chinese economy are increased.

But how did China manage to shift the value of their currency? China allows its currency to be traded within a band, where the PBOC set a new midpoint for the yuan every day. On August 11th , the PBOC then set the yuan's midpoint fix significantly lower than the previous day's closing rate, which led to an immediate depreciation of the yuan against the USD, as well as worldwide anger due to the unfair advantage China gave itself by devaluing its currency.

Conclusion

China is evidently an export-driven economy which hinges on maintaining a competitive edge in the global market. The relationship between the demand for yuan and foreign currencies, particularly USD, directly impacts China's export competitiveness. The intervention of the PBOC to decrease the value of its currency in 2015 reflects its urge to maintain a competitive edge, regardless of whether they have to bend or break certain unwritten rules. Additionally, China’s method of currency management, through peg ging, allows them to maintain this favourable exchange rate which will ensure injections are brought into the economy through exports, and therefore China’s excessive control over their currency, coupled with the pegging system, allows China to keep an unusually favourable exchange rate for an economy of its size.

China and its Youth Unemployment Crisis ~ Ray Yin, Year 13 ~

When it comes to education standards for primary and secondary education, China has become the world leader, boasting an impressive PISA score of 591. In context, even countries which boast advanced and developed educational systems fall short of this number, with the UK scoring 502. In theory, this should then translate into a highly skilled youth workforce, and while China is a leader in many sectors, disparities are starting to show between the requirements for top earning jobs in China and elsewhere, creating an insurmountable wall that many young prospecting Chinese people simply cannot overcome anymore.

The start of this problem can be found in the college entrance exam, the Gaokao. Regarded as the most competitive exam in the world, each paper contains questions of extraordinary difficulty, and as such students in China prepare with everything, they have for it, and it is common for the average student to spend over 13 hours per day preparing for the exam up to 3 years in advance. However, the sheer population of China’s population, coupled with a limited number of vacancies for college, means that even with high education levels compared to their global counterparts, many students cannot even get into tertiary education. In fact, with a low 58.4% enrolment rate, it falls short of countries such as the USA, with 87%, even accounting for its notoriously average secondary education standards.

With limited vacancy comes exorbitant costs, leading to the second issue. Many students who may be accepted into college may, in the end, not go due to the high costs. China has a middling GDP per Capita of $12,000, falling short of many advanced countries. It is no surprise that many people, especially in rural areas, cannot go to college even if they want to, and instead may be trapped in their village to continue working in agriculture.

These 2 factors can create a feeling of demotivation for many students across China, and many complain that they feel as if they had wasted their entire lives after failing to go to college. The reality is that they are not entirely wrong, as without college degrees, job opportunities for them are extremely limited. This can result in these students choosing instead to not work, in a movement called “Tang Ping” in protest of the unfairness of their situation, which contributes significantly to the youth unemployment problem.

Even if you are going to college, you still aren’t safe. As a result of the high demand for college degrees, lower achieving students may pick out courses that are not useful to them or that are not useful in general. In the rare case, lower achieving Gaokao candidates may have government assigned degrees for them. As these courses offer minimal utility in the jobs that they pursue, a skills mismatch is created, where the skills they obtained from college do not offer them competitive advantages in their jobs. This put them at high risk of being fired or let go as they are not as useful to the firms who employ them for the most part and means that there is a likely chance that they also end up underemployed or even unemployed.

Let’s say then, that you are in the small percentile that made it through a great college with a good degree, and you are ready to start working for the technology firm of your dreams. Are you safe now? Unfortunately, the answer to the question is you are still not guaranteed a good job. Successful graduates still compete to take spots in the Big 3 sectors: Technology, finance, and hospitality, each having a huge employee demand. This means that not everyone can apply successfully to these sectors, and the cycle of having a skill mismatch begins anew, albeit the employee is of a higher calibre. Once again, they are likely to lose motivation and join in on the Tang Ping movement, contributing once more to the Youth Unemployment levels.

Overall, China has a large demographic issue with not enough high-level jobs, creating a problem where many cannot attend college and thus do not have the motivation to work. It will be interesting to see what measures the CCP puts in place to combat this topical issue.

Dear Mr Khan,

Solutions to Supply Chain Issues

~ Tommy Farmer, Year 13 ~

We have seen the weakness of our global supply chains exposed recently, through the COVID-19 Pandemic impacting everyday items such as toilet roll and the invasion of Ukraine hurting oil prices and therefore a rise in all consumer goods, pushing the national CPIH (Consumer Price Index with Housing) to 9.2% in December 2022. As people across the UK are being more and more severely impacted, this letter offers you options to try and reduce the impact of the exogenous events, for example, pot ential alternative supply chains or making the UK more productive to make the country less reliant on imports.

In order to develop existing supply chains, we must boost relations between the UK and the exporter. Referring back to problems set out in the introduction, one reason recent inflation has been so severe is due to oil importation issues. Currently, the UK takes over 20% of its oil imports from countries determined to be high risk or worse in the S&P index. This leaves the UK exposed to losing one fifth of our oil potentially overnight, through other countries instability.

To combat this, I would suggest a policy of trying to make deals exclusively with countries with a rating of A or higher: this means the country is very unlikely to default overnight, so if circumstances get worse for that country, the UK can prepare a contingency plan in order to reduce the immediate impact of losing a key exporter of oil. Furthermore, it makes the UK more dependable as a country in and of itself: by having more dependable trade partners, the UK becomes a more reliable place to invest, borrow from and loan to. As external investment increases, there’s more money in the Circular Flow of Income, leading to a higher GDP. This is best seen in Chile: Chile’s main trade partners outside of South America are the US, Germany and South Korea, all of which have a rating of AA or above. This has kept Chile out of the trouble that its close-by countries have found themselves in, such as Venezuelan hyper-inflation or the demonstrations in Buenos Aires. Clearly, focusing trade on reliable partners has a tangible effect on debt security, which, after the recent reports of schools needing to be rebuilt, may be necessary for the UK.

Another way to strengthen supply chains is to diversify the supply chains a country uses. The UK currently imports 13.2% of all imports from China. This gives China power over the UK; they can decide to increase export fees, which could hurt the UK. Therefore, the UK should look to import comparable items from different countries. This could include the emerging supply chain in East Asia, involving countries such as Japan, Malaysia and Indonesia using their synergies to try and compete against the market monopoly that China has over everyday items. This could be particularly relevant given China hasn’t been as strong in condemning the Russian invasion of Ukraine as the UK, potentially causing a rift, as well as fears of an invasion of Taiwan. By using the alternative supply chain, any reason to cut down on imports from China would be easier on the average person in the UK as price rises wouldn’t be as severe as if the UK were completely reliant on China. Using other supply chains is oftentimes more expensive, however, opening up an opportunity cost.

What I believe to be the most efficient way of improving productivity is investing in capital. The struggles from the recent COVID and Ukraine crises have come from specific items: toilet roll, energy or, most

recently, vegetables. By investing in new machinery and technology for these specific items, more of these can be produced at a lower cost to human work hours. The benefits of this are twofold: firstly, more units produced for less hours worked is the definition of boosting productivity. By having more units of goods in the country itself, the supply chain is shortened and therefore more resilient. However, it seems that recently GFCF (Gross Fixed Capital Formation) has been focused on replacing old capital, which many place at the fault of the years of austerity. As a result, government has had to spend a lot of its income on simply replacing (old trains for example, with new CityBeams) rather than replacing while simultaneously updating. It is clear, therefore, that to improve productivity, we will need to spend even more than we already are. According to the ONS, GFCF rose 1.3% in Q1 2023, which surpasses all years in recent memory, apart from Covid. This may signal the start of a shift to improving capital, but with time lags we will have to wait patiently and see.

Furthermore, people can work for less time but still have the same or even improved output levels. This decreases stress, so people are more willing to work and, as a result, the labour market increases, leading to more jobs being filled and unemployment decreasing. This hints that the holes in the UK economy will be filled, leading to even more units of goods/services being produced: a multiplier effect.

There are a couple of drawbacks to this idea. Namely, the opportunity cost/information gap risk. Governments can never guarantee the outcome of their investments, the most infamous example being the huge cost increase and delay of CrossRail. If the government did invest in vegetable enhancing technology, there would be a risk of the investment failing and the government being inept, all due to the fact they didn’t have enough information on how to best invest the money.

Another way of trying to improve productivity is through incentives. Incentives provide encouragement to workers so that for a number of units of good or service produced, they receive some reward. Therefore, they try harder to produce more, leading to a greater number of units, all of which I explained earlier. But this doesn’t have the secondary benefit: in fact, it has the opposite impact. When you try to give people rewards for their work, it can often lead to people overworking themselves or being burnt out more quickly. Currently, incentives exist to improve education: focused on T-Levels and apprenticeships. Yet, apprenticeship levels have been steadily decreasing since 2015. I would argue that, if we are to use incentives, we need to refocus them on something with proven success: such as productivity levels. For example, a Deposit Return Scheme for plastic beverage packaging has seen remarkable success across the EU and Mexico especially, providing meals for those in meal poverty, but also meeting environmental targets. Incentives can be used: we just need to find the gaps where incentives would have the greatest impact.

To conclude, I would argue there are two primary ways to combat the recent supply chain difficulties faced by the UK: first of all, you could try to diversify supply chains. I believe this would be the best course of action as it would lead to new relations as a country which could be useful in the future, but also decrease our dependencies on other countries. Alternatively, you could try to boost national efficiency, however, as a government, there are severe risks to this.

Yours faithfully,

Tommy Farmer

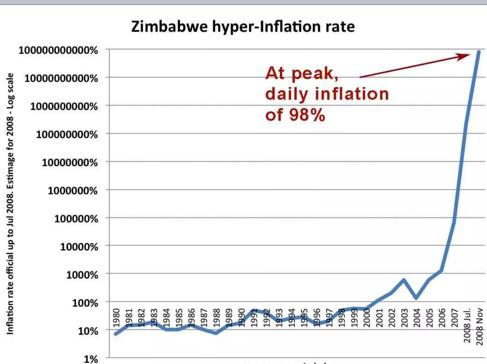

The Zimbabwe Hyperinflation Crisis of 2008

~ Rutwik Meda, Year 13 ~

Inflation. It’s a word that has become rather common in society, mainly due to the Virus and other international events such as Brexit. By the way, for those wondering inflation is defined as the sustained rise of prices for goods and services within a country’s economy, in other words the value of money decreases. And you’ve guessed it, hyperinflation is basically this process, but far more accelerated and random. It was very much a word on the tip of the lips for the Zimbabwean people during 2008.Before I introduce you to the once in a generation event and how it came about, I feel it would be adequate to understand a pre-hyperinflation world in Zimbabwe first.

Zimbabwe before the Crisis

The country by no stretch was the best performing country economically, but there was somewhat of a foundation that had already been built. Inflation was steadily rising year upon year but did not reach 100% until 2001 when the inflation rate performed at 112.1%, and this would have meant that consumers would not receive too much of a ludicrous price for their goods. However, it was from this point till 2008 where the real hike in prices were seen. This was mainly due to the demanding nature of employees asking for higher wages, so that their income would be worth more. Prices would need to ascend again and increase inflation further so that firms would make the same level of profits. Another huge concern for the country was the sluggish negative economic growth since 2001, leading to decreasing revenues for firms as lower incomes for households meant that they consumed less, which lead to heightening the already shameful unemployment rate that was increasing year upon year 4.39% in 2004 to 2008, as companies would need to reduce their costs of production to make sure they were making some form of net profit in order to survive. This led to further reduced incomes for households, and therefore the marginal propensity to consume for households decreased, which would mean that AD (aggregate demand) would fall and cause further negative economic growth through the negative multiplier effect.

The Causes

The name Robert Mugabe should be one that is familiar to us all. I can guarantee you that it is a name that will be mentioned throughout the article. Mugabe and his advisors in the government decided to implement new economic reforms, as part of a larger monetary policy to revamp the country. One example was land reforms, which made white farmers in the country redistribute land to black farmers in a post-apartheid world. However, these farmers did not have much experience within the industry and therefore they produced lower yields and a lower output of crops, and this led to food production falling by an eyewatering 60 per cent in 10 years. As a result, this led to the price of food to increase as the quantity became scarcer. During this period, the IMF, EU and the US imposed sanctions on the financial sector of the country, meaning that there was no opportunity for Zimbabwe to receive a loan and the save the livelihoods of farmers. Coupled with this, the fact that the country’s

own banks refused to lend out cash due to the political instability within the country at the time led to banks being more uncertain in getting a return on their loan. Naturally, this attracted less hot money, therefore FDI (Foreign Direct Investment) decreased by 440.2 million in the space of 5 years. Because the economy was in clear deterioration, the debt was rapidly increasing by the second and therefore the government thought they were left with only one option - to print more money. The rate of Zimbabwean Dollars being printed had never been seen before on the planet. At the same time, there were not many goods being produced within the country at this time and this meant that too much money was chasing too few goods. This led to prices rising even further - a clear example of demand-pull inflation.

The Outcome

There is no doubt that the situation caused monumental damage and divided a nation. One particular of group stricken were households who put mass amounts of money into savings accounts. They were hamstrung by this situation as the present value of their money would be worth far less than before. Also, people with savings in foreign currencies would not be allowed to exchange their cash. Moreover, goods and services became so expensive that people could not afford the basic necessi ties in life such as food and water. This led to the death of millions and those who survived had a much worse standard of living, as seen by the very low GDP per capita. When inflation peaked at 79.6 billion in November 2008, this caused both shoe leather and menu costs to rise but because inflation was doubling every day, the price of one good or service on one day could be somewhat affordable one day, then significantly above workers income the next day. This meant that consumers had to find alternative products almost every day. Anticipation of further inflation led to the incentive for consumers to buy more goods and services, further exacerbating it. The competitiveness of the country’s currency was also weakened from inflation as it had increased the MPI (marginal propensity to import) as imports became cheaper and exports became more expensive. This caused total imports to increase and total exports to decrease, leading to a deficit in the balance of payments of over $730 million. The hyperinflation also created uncertainty for businesses and along with the increase in interest rates to counteract inflation. This caused AD to decrease and a decrease in LRAS, hindering the potential future growth for the country, as the factors of production would not have been upgraded at a sufficient pace to keep up with capital depreciation.

Tackling Hyperinflation

Zimbabwe went through multiple reforms to solve the problem, with the main and first solution being the use of new currency. Zimbabwe had adopted the use of foreign currencies including the: US dollar, South African rand, and even at one point the Euro. The new funds would prove to have a less volatile exchange rate and as a result bring economic stability to the country as there was less uncertainty within the economy, especially for businesses as they were beginning to invest more and take advantage of the accelerator effect and thus create new jobs. As well as this, Mugabe and his mates decided to stop printing any Zimbabwean dollars at all, a sight that some could not believe would happen as there had previously been 100 trillion (yes trillion) bank notes. This was very similar to the Weimar Republic response in Germany to the Great Depression, as a new currency (The Renten mark) was created and the economy in response to this recovered. Mugabe believed that inflation was down to ‘Greedy Businesses’ raising their prices and decided to impose price controls, so that goods would have maximum values. However, this didn’t work as it created shortages and a black market, meaning that goods were sold back at even higher than their original prices.

Post-Hyperinflation

In 2014, the government introduced convertible coins, essentially Zimbabwean bonds, to prevent farmers from charging higher prices that had been rounded up. However, just a couple of years later, it was apparent that the coins were highly illiquid, rendering them unusable. Adding to the economic challenges, the COVID-19 pandemic delivered another blow, with inflation soaring to almost 600% in 2020, primarily due to supply shortages and an increase in oil prices. This proved to be another kick in the teeth for the economy. Consequently, the government once again introduced gold coins to stabilize the economy and provide reliability. To be fair, this initiative has significantly reduced inflation. Nonetheless, it remains at a level still considered very high by anyone's standards. Time will tell if inflation ever returns to 'normal' in Zimbabwe, but I guarantee that Zimbabwe and inflation will once again be featured together in the news.

What Would Happen if we Banned Billionaires?

~ Haran Iyer, Year 13 ~

Billionaires are truly a point of controversy in the modern world. Many economists (and the public) argue that the world’s 2,640 billionaires (collectively worth $12 trillion)1 represent the failings of economic policy and the free-market capitalist system which is prevalent in the West. They argue that the existence of billionaires exacerbates inequality, as their indulgence into a luxury lifestyle comes at the cost of people around the world being unable to access entitlements such as education and healthcare. In a survey conducted by Vox Media2, an overwhelming 72% of Americans agreed that it was unfair that the rich got wealthier during the pandemic, indicating a general distaste towards billionaires and their continuous wealth accumulation. And this opinion is also reflected by certain politicians; US Senator Kirsten Gillibrand stated3 that “no one deserves to have a billion dollars”, while former presidential candidate Bernie Sanders said that he doesn’t “think that billionaires should exist”4. Calls for abolishing billionaires have become increasingly prominent, and in this essay, I will examine the impact that banning billionaires will have on the economy, the environment, and society.

Billionaires and the Political Economy

In a video on his YouTube channel, the Former American Secretary for Labour, Robert Reich, explains5 that the ways to become a billionaire are the results of failings in the economic system, rather than “Free Market Capitalism”. He outlines four methods of becoming a billionaire, and how each of these methods can be prevented by changes to economic policy. The first method is exploiting a modern monopoly; Reich uses Jeff Bezos and Amazon as examples. Amazon can be considered a modern monopoly, accounting for approximately 40% and 35% of e-commerce sales (as of 2022) in the USA6 and the UK7, respectively. According to Reich, Amazon would not let suppliers sell at a lower price elsewhere for the first 25 years. Due to the patents granted by the US government and the lack of anti-monopoly enforcement, Amazon grew to dominate the e-commerce market and Jeff Bezos8 became a billionaire. Reich states that this same concept applies to talk-show host Oprah Winfrey and Star Wars creator George Lucas. This idea is also reflected in an opinion piece from the New York Times9 which focuses on the technology industry. Writer Farhad Manjoo argues that banning billionaires can mitigate the effects of tech-driven inequality. He states that the few tech corporations account for the bulk of American corporate profits, and that most of these shares of economic growth have gone to a small number of the country’s richest people. Manjoo explains that advancements in technology and AI are creating a new industry that won’t employ many people; he believes that uncontrolled technological advancements will lead to a world where a few billionaires will hold vast shares of global wealth. Reich argues that removing monopolies (through tighter enforcement and regulations) will remove billionaires, as it prevents what happened with Amazon and the future of the tech industry. This will also have a positive effect on the economy, as monopolies can raise their prices as high as they wish (because there are no other alternatives); if monopolies are removed, then producers will have to adhere to the price mechanism, allowing for consumers to pay fairer prices. This links to the general opinion that the existence of billionaires exacerbates the inequality gap, and this argument from Reich shows that abolishing billionaires will have a positive spillover effect on the public and consumers.

The second method (to become a billionaire) outlined by Reich is through making investments based on insider trading information which is unavailable to other investors. His case study here is the downfall of SAC Capital Advisors, a hedge fund company run by Steven A. Cohen. Insider trading at SAC was “substantial, pervasive and on a scale without known precedent in the hedge fund industry”, with Cohen reportedly paying big commissions to banks in exchange for new information10, so that he could have an edge over other investors and hedge funds when trading. Eight of Cohen’s present and former employees pleaded guilty and were convicted of insider trading, while Cohen himself managed to get away with a fine of $1.2 billion11. He still remains in the hedge fund industry, with a net worth of $17.5 billion12. Reich’s solution in this scenario is to increase sanctions on insider trading. If left unregulated, it allows for individuals (such as Cohen) to manipulate financial markets and make huge fortunes from it. This

highlights that banning billionaires could have a positive impact on the financial sector, as it’ll promote fair play amongst investors, and it’ll reduce the power that billionaires can achieve through the returns gained from insider trading.

This alludes to Reich’s third method, which also focuses on the disproportionate power wielded by billionaires; he states that billionaires can sustain their huge net worths by paying off politicians. The Trump tax reforms13 were estimated to save Charles and Dave Koch $1-1.4 billion USD per year. In return, the Kochs and their affiliated groups spent approximately $20 million lobbying for the tax cuts and making major donations to politicians. As a result, they were able to keep large amounts of their wealth, while the middle and working classes had to pay much more. This represents the evident corruption among politicians, which is fuelled by billionaires who wish to keep as much money as possible. Banning billionaires can therefore be a massive step towards reducing corruption among politicians, therefore highlighting another positive impact of banning billionaires. Overall, banning billionaires will have a significant impact on the political economy, because it’ll mean that many failures in economic policy would have been rectified. Furthermore, achieving this will lead to reduced corruption among politicians, highlighting that billionaires have a vast amount of influence, and therefore showing the importance of abolishing them.

Billionaires and Society

Reich’s final method for becoming a billionaire is through inheritance. In the US, 60% of wealth is inherited, while a third is inherited in the UK. Reich states that billionaires can accumulate their massive shares of wealth through avoiding taxes on their inheritances, and states that billionaires can be banned through high levels of taxation. This idea is the most common proposition for abolishing billionaires, as they currently pay very little through taxes. Bernie Sanders called14 for an income tax of 100% for those who earn over $1 billion. The effects of this will be massive, as governments will suddenly have a larger budget through the tax revenue generated from banning billionaires. They can spend this money on improving general welfare, such as spending on education and healthcare. In the UK, increased spending on the NHS will infinitely beneficial, as the money can go towards more hospitals and staff and counter its many problems (such as the long wait times)15. The improvements that can be made using the tax revenue can drastically improve welfare amongst society, therefore showing another positive impact of abolishing billionaires.

Another area that the existence of billionaires affects is the environment. Asfhaq Khalfan, the Climate Justice Director at Oxfam, explains16 that the activities of billionaires have “locked the world into a highcarbon future”. He argues that the distribution of carbon footprints within society is unbalanced, with billionaires being more responsible for carbon emissions than the average person. Indeed, a sample17 found that, as of 2021, 125 billionaires were responsible for as many C02 emissions as the entire country of France (France’s population at the time was 67.5 million). This is because billionaires tend to indulge in lavish lifestyles, purchasing cars, yachts, and private jets etc; this is reflected in this statement from Beatriz Barros (a gender and environmental researcher at Indiana University): “Getting rid of the C02 emissions of 2000 billionaires would be way more significant than getting rid of the C02 emissions of 2000 average persons”. Through increased taxation, billionaires will have a smaller disposable income, therefore meaning that they’ll be able to invest less in these polluting industries. Abolishing billionaires will therefore be a massive step in improving the world’s carbon footprint, as a large source of carbon emissions will be reduced.

Overall, the impact of removing billionaires will be extremely positive for societal welfare; the continuous investment by billionaires towards pollutants is causing excessive damage to the environment, and through taxation, their carbon footprint will reduce massively. This means that abolishing billionaires will have a direct impact on the economy, and this is echoed by the potential of improved infrastructure, education, and healthcare that could be provided by the tax revenue from taxing billionaires.

Are there any positives in keeping billionaires?

A key point of defence for billionaires is the idea of altruism; billionaires have the power and influence to support charities, donate to causes, and to organise schemes to help those in need. Therefore, taxing and (by extension) removing those with the ability to make a difference could potentially be more detrimental than beneficial, and billionaires could have a place in society if they intend on addressing problems such as poverty and inequality. Indeed, this is reflected in certain billionaires; Bill Gates and Warren Buffet set up the Giving Pledge18, which calls for billionaires to dedicate the majority of their wealth towards philanthropy either during their lifetime or in their will. This indicates that billionaires can have a positive impact on society, as they have the power and influence to make change through philanthropy. However, it can be argued that billionaires will not fully commit to philanthropy and that they won’t make any significant difference. Anand Giridhara Das, writer of the bestselling book Winner Takes it All, argues19 that many billionaires see philanthropy as something more akin to a “branding exercise”, rather than anything genuine. Furthermore, less than 200 of the 264020 billionaires in the world have signed the Giving Pledge, reflecting that most billionaires will not commit to altruism if it involves them sacrificing too much of their wealth.

Another argument in defence of billionaires is that their investments could stimulate economic growth in more effective ways than what governments could achieve. In an essay,21 which is against banning billionaires, Jessica Flanigan (University of Richmond) and Christopher Freiman (College of William and Mary, Williamsburg) argue that billionaires can have a positive impact on the economy and societal welfare regardless of whether they are philanthropic or not. They state that non-philanthropic billionaires will still make investments into wide varieties of companies. These companies can use this to invest in improving capital and productivity, therefore increasing output and the quantity supplied to the market. From a macroeconomic perspective, this means an increase in aggregate supply, therefore leading to economic growth, showing a positive impact of billionaire activity. This could be much more effective than subsidies provided by the government, as billionaires have been shown to wield a considerable amount of influence.

In conclusion, abolishing billionaires through taxation will have extremely positive effects on the economy, the environment, and society. The potential of billionaires stimulating economic growth and committing to philanthropy is nullified by the beliefs, and statistics, which show the disregard that billionaires have for the wider world to indulge in their lavish lifestyle. Taxing billionaires will drastically benefit the world’s carbon footprint, suggesting that banning billionaires is essential for the future of the planet. For C02 emissions to be reduced, billionaires must be taxed so that the purchases of goods such as private jets can be mitigated. These taxes will also help governmen ts generate revenue to address key issues, such as poverty, inequality, and the shortcomings of healthcare and education systems. Furthermore, billionaires represent failures in economic and political policy; fixing these issues to remove billionaires will also increase fairness in economic and financial markets. Overall, banning billionaires will have many positive effects, and despite the genuine efforts of individuals such as Gates and Buffet, the impact of banning them will always outweigh the risks of letting them continue to exist.

The Price of Belonging: The Golden Passport Phenomenon ~

Yuti

Kumar, Year 12 ~