Market Report.

04. Market CommentOCR Drop Sparks Market Optimism.

08. Mount Roskill Sales Statistics January 2025

14. Article – Tony Alexander: What the OCR cut means for the housing market and home loan costs

20. Article – Kelvin Davidson: Is The floor for mortgage rates is approaching fast

06.

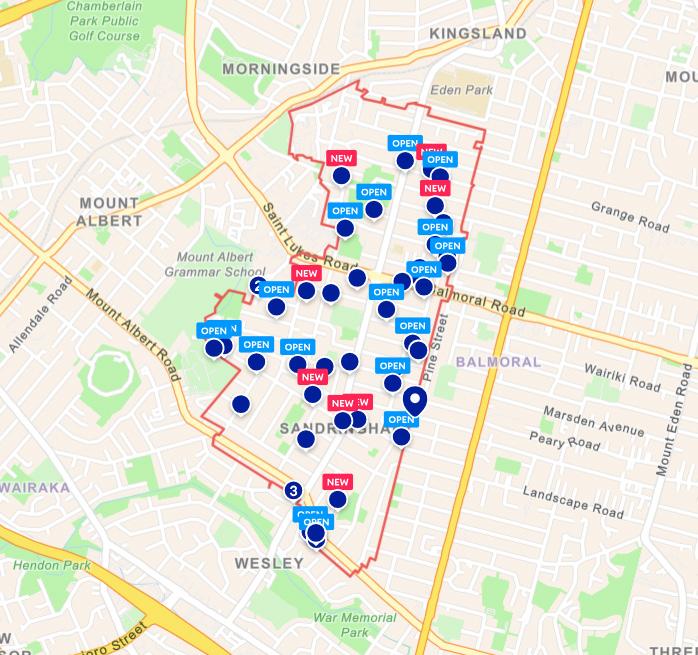

Sandringham Sales Statistics January 2025

12. Case Study & Auction Update with Cameron Brain

16. Our month in Review Top Stories & Events from the City Realty Group

22. LoanMarket Update

24. Property Management Update: The annual student migration is upon us! So what better time to discuss

26. Why choose us? Ray White Sandringham & Mount Roskill team

OCR Drop Sparks Market Optimism

The

Reserve Bank’s much-anticipated Official Cash Rate (OCR) cut on February 19 did not disappoint, says Daniel Horrobin, Director of City Realty Group.

As reported by Stuff on February 20, the OCR was lowered by 50 basis points to 3.75%, with banks quick to respond by matching the drop. This move was widely expected, and many banks had already been reducing interest rates ahead of the announcement.

At exactly 2pm, as soon as the Reserve Bank confirmed the cut, Kiwibank was the first to adjust its home loan and business lending rates, setting off what the NZ Herald has since described as a “Mortgage War” as banks across the board followed suit.

Across the industry, confidence is on the rise. According to Realestate.co.nz, January 2025 saw new listings surge to levels not seen in a decade, signaling renewed momentum in the market.

Chief Executive of the Real Estate Institute echoed this sentiment, stating that while January is typically slow due to the holiday period, sales and listings were higher than in January 2024, with strong open home attendance and positive buyer sentiment nationwide.

Economic commentator Tony Alexander also sees a clear market turnaround, noting that annual residential property sales in New Zealand have climbed from 59,000 in mid2023 to nearly 71,000 today.

“Taking all of this into account,” says Daniel, “we’re looking ahead to a big year. Both sellers and buyers can take confidence from the noticeable increase in activity, and perhaps most importantly, a sense that a market recovery is well underway.”

“We’re looking ahead to a big year. Both sellers and buyers can take confidence from the noticeable increase in activity...”

Total Sales

January 2025

2

January 2024

There was a -77% decrease in the total number of sales year on year.

Total Sales Value Median Sales Price Median Days On Market

January 2025

$2,090,000

January 2024

January 2025

$1,045,000

January 2024

9 $11,555,000 $1,200,000

There was a -81.9% decrease in the total sales value year on year.

Source: REINZ

There was a -12% decrease in the total median sale price year on year.

January 2025

163

January 2024

70

There was a 132% increase in the total median DOM year on year.

Sandringham Recent Sales.

Sales data is from REINZ and covers the Sandringham property market. Sandringham Listings.

February 2025

Up 23 from last month

Listing data is from RealEstate.co.nz and covers the Sandringham property market.

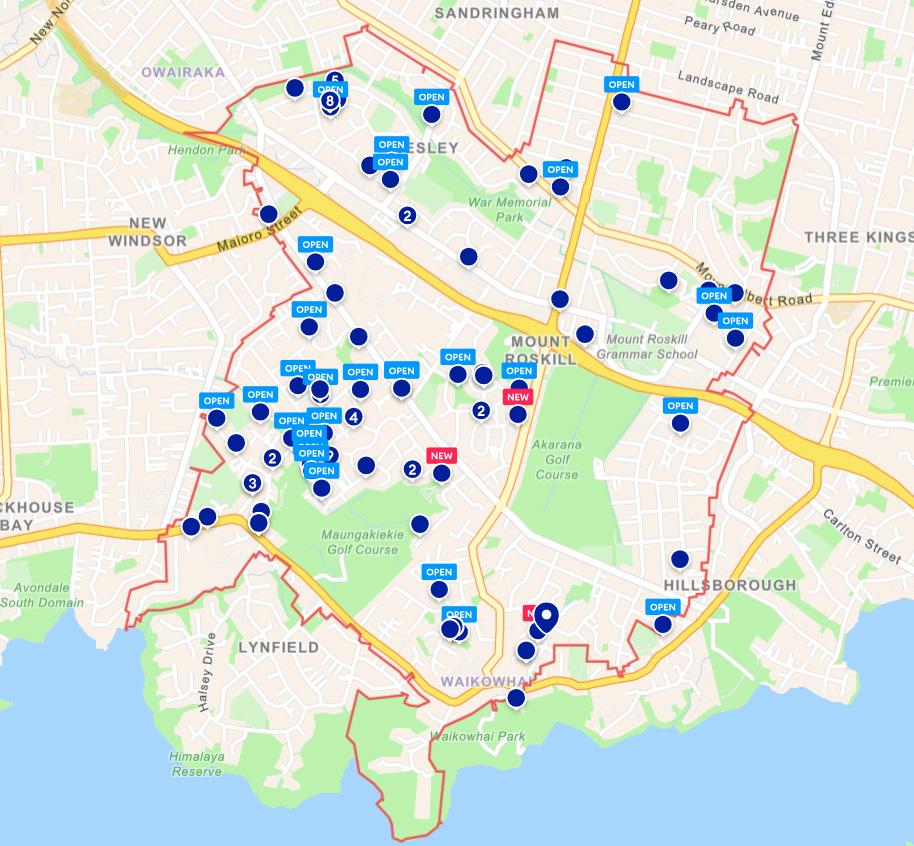

Mount Roskill Market Statistics.

Total Sales

January 2025

15

January 2024

17

There was a -11% decrease in the total number of sales year on year.

Total Sales Value

January 2025

$15,129,500

January 2024

$17,619,000

There was a -14% decrease in the total sales value year on year.

Source: REINZ

January 2025

$905,000

January 2024

$970,000

There was a -6% decrease in the total median sale price year on year.

Median Sales Price Median Days On Market

January 2025

77

January 2024

49

There was a 57% increase in the total median DOM year on year.

Mount Roskill Recent Sales.

Total Number of Properties Listed 1120

Total Number of Auction Properties 248 % of Auction Properties Listed 22.14%

Success Rate: 66.22%

Total Number of Sales for 2024 528

Total Sales Value

$325.7M

Total number of Auctions Sold in 2024 296 56% of all sales in 2024 were as a result of an Auction

Total Auction Sales Value

$179.2M 55% of the Total Sales Value was as a result of an Auction Sale

*Rounded to nearest $100,000 *Rounded to nearest $100,000

City Realty Group Auction Report.

Earlier this month, we released our 2024 Sales & Auction Results for City Realty Group, covering our four offices: Auckland Central, Wynyard Quarter, Sandringham, and Mt Roskill.

Our diverse portfolio includes everything from storage lockers and car parks to multi-million-dollar apartments and waterfront homes.

In 2024, CRG listed 1,120 properties for sale, with 22.14% of these taken to auction. While this was a decrease from our 2023 auction listings, we observed a higher number of withdrawn properties compared to the previous year. Despite this, our auction performance remained strong, with a clearance rate of 66.22%—a significant contrast to the 15.5% clearance rate for non-auction properties.

Of the 528 properties sold in 2024, 296 (56%) were secured through an auction campaign, reinforcing the value of auctions as a powerful sales strategy.

In total, our sales volume reached $325.7 million, with auctions contributing $179.2 million (55%).

With the first quarter of 2025 nearly upon us, we are in a strong position for what promises to be a busy and exciting year. If you’d like to gain deeper insights into the Auckland property market or explore the benefits of auctions, I’d welcome the opportunity to discuss further.

Tony Alexander: What the OCR cut means for the housing market and home loan costs

The housing market is improving but Kiwis still feel wary about the state of the economy.

ANALYSIS: The state of New Zealand’s housing market is mildly improving – and the Reserve Bank’s decision today to drop the Official Cash Rate 50 basis points to 3.75% could bring further solace to the sector.

The market turnaround is best seen in the annual number of residential property sales in New Zealand, rising from a low of 59,000 in mid-2023 to close to 71,000 now. Prices have yet to show much improvement overall, with an average gain of about 2.5% since the middle of 2023.

The data tell us that first-home buyers are active in the market, but owneroccupiers are still hesitant. Concerns about employment are likely to be an element in play along with general low confidence in the outlook for the economy.

My monthly Spending Plans Survey, for example, shows a net 10% of people plan to cut their spending in the next three to six months compared with a few months ago when a net 10% of people were planning to spend more.

A more realistic assessment of the economy’s likely performance has occurred, though business surveys still show businesspeople are highly optimistic about what lies ahead. Their reality check may just be starting.

While the absence of owner-occupiers from the market is probably temporary, there is a chance that the so-far low presence of investors could be a characteristic of this cycle. My most recent survey of real estate agents undertaken with support from NZHL showed that a net 48% of agents

First-home buyers have been strong in the market compared to other buyer groups. Will the cut to the OCR encourage more action? Photo / Fiona Goodall

were seeing more first-home buyers in the market. But only a net 12% were seeing more investors.

The interesting thing is that while the reading for first-home buyers is down only slightly from December, the reading for investors is a sharp fall from net 36% positivity before Christmas.

Why are investors hesitant to buy? One reason is that few will feel the need to beat price rises. Prices are only just edging upward at a very slow pace. Investors will feel that time is on their side, but they will also feel that holding an investment property while waiting for the tax-free capital gain will cost a lot more than it had done in the past.

Councils (which have the power of monopolies) have sharply increased their prices (rates), insurance premiums have soared, and look set for a further boost following the California fires, and maintenance costs are escalating. These cost rises are occurring at the same time that rents in many locations are falling, and landlords are finding it very difficult to secure a good tenant.

Feedback from real estate agents indicates that one or two investors are starting to

bump up against the new debt-to-income rules, which limit total investor debt to seven times their income. The numbers are so far quite small given the lack of house price gains. But there will be restraint on the ability of investors to buy to an increasing degree as this upward leg of the housing cycle progresses through 2025.

One important consideration is of course the cost of borrowing money to finance one’s investment. The Reserve Bank has cut the OCR from 4.25% to 3.75% and brought forward by one year to the end of 2025 its prediction of reaching the end-point for cuts this cycle.

The recent revisions to economic growth data in New Zealand have encouraged the Reserve Bank to accept that there is more spare capacity and therefore less inflationary pressure in the economy than it had previously thought.

Will the earlier achievement of the cyclical low for interest rates spur much extra investment? At the margin, some investors will look to purchase earlier than they had been planning. But the numbers may not be large, and it still seems reasonable to expect only mild growth in average property prices this year and next.

- Tony Alexander is an independent economics commentator. Additional commentary from him can be found at www.tonyalexander.nz

@raywhiteaucklandcentral

@raywhitewynyardquarter

@raywhitesandringham

@raywhite.mtroskill

Auction Action!

Another successful auction campaign, this time 1/2 Springbank Lane, Te Atatu Peninsula - 21 days on the market! 3 active bidders! Sold under the hammer!

Congratulations to our vendor and first home buyer purchasers!

Birthday Shoutout!

Birthday wishes went to our Commander in Chief this month. Happy Birthday Dan!

Did you Say.... Another Sold. Another successful Auction campaign this time at 21 Millais Street, Grey Lynn. Congratulations to our vendors and purchasers of this lovely property.

Our Superstars.

We recently hosted the City Realty Group Quarterly Awards across all our offices. Congratulations to everyone who earned accolades this past quarter!

Kelvin Davidson: The floor for mortgage rates is approaching fast

The five things you need to know about the housing market this week.

1.

The OCR is dropping faster

Clearly, the biggest news on the economics front last week was the Reserve Bank’s decision to cut to Official Cash Rate from 4.25% to 3.75%. More important was the Reserve Bank’s prediction that the OCR will fall to around 3% by the end of 2025 rather than the end of 2026. That’s a big pull-forward in terms of timing and seemed to reflect the Reserve Bank’s view that there’s more spare capacity in the economy than previously thought – hence more underlying, disinflationary pressure than before.

Not much else changed in terms of bigpicture economic projections: GDP growth is set to improve slowly this year; the unemployment rate is now thought to be more or less at its peak this cycle; and house prices are set to rise by around 4% this year and by 5% next year. Headline inflation may bump upwards temporarily in the near term, as the lower the dollar pushes up imported prices, but the Reserve

Bank thinks it will be able to “look though” that blip.

So in a nutshell, look for more OCR cuts over the coming months, perhaps a series of 0.25% falls from April onwards, depending on how the data evolves. The revised OCR forecast also suggests there are also further falls to come in mortgage rates, but they’re unlikely to be as large or fast as those seen to date – especially since banks were already cutting in advance of last week’s OCR change anyway.

In other words, the floor for mortgage rates (possibly in the range of 4.5-5% for many rates) is now a lot closer, and at some stage soon more borrowers may well start to fix longer again – after a flurry of floating or short-fix activity in recent months.

2. First-home buyers losing their edge

The latest CoreLogic data shows that firsthome buyers’ share of property purchases dropped a touch in January, with relocating owner-occupiers (movers) and mortgaged

Further cuts to home loan rates are on the cards following the Reserve Bank’s revised forecast for the Official Cash Rate. Photo / Alex Burton

multiple property owners (including investors) taking a higher share. At face value, that’s not a great result for first-home buyers. But as we’ve been highlighting often in recent weeks, market share isn’t the full story – with the overall number of deals still trending higher, I think first-home buyers have every chance of buying more properties in 2025 than 2024, even if their share edges lower.

3. Property market still in a holding pattern

Speaking of sales volumes, we recorded just short of 4,300 deals across real estate agents and private activity in January. That was around 7% higher than the same month last year – the 20th rise in the past 21 months – but still below the long-term average. And with values generally still not rising just yet (albeit not falling much either), the data continues to point to a market in something of a holding pattern. On one side, most vendors aren’t in a forced selling position, yet on the other side many buyers don’t seem willing or able to meet their price expectations – and hence the stock of available listings on the market remains elevated.

4. Net migration finding a floor?

Last week’s Stats NZ figures showed

that the 12-month running total for net migration continued to drop in December, hitting 27,100 – the lowest since December 2022 (24,900). However, looking at the recent ‘run rate’, departures from NZ have just slowed a little, and arrivals have edged higher – meaning the net figure has stabilised at around 2,0002,500 per month, which is consistent with long-run norms. In other words, migration has certainly dropped a long way from a very high peak, which has taken the heat out of property rents (alongside a rise in the supply of rental listings), but it is now showing signs of stabilising.

5. Borrowers still shopping around

There’s plenty of interesting data coming up this week – including ANZ business and consumer confidence surveys, as well as the NZ Activity Index and filled jobs figures from Stats NZ – but we’ll also get my favourite (non-CoreLogic!) dataset on Thursday, which is the Reserve Bank’s detailed mortgage lending figures for January. Will high debt-to-income ratio lending have ticked up as mortgage rates have fallen further? But alongside that, I’ll also be focusing on the bank switching data, with recent months having seen a lot of borrowers jump ship to a competing lender.

CoreLogic chief economist Kelvin Davidson: “Look for more OCR cuts over the coming months.” Photo / Peter Meecham

Jamie Maclennan

027 742 5227

jamie.maclennan@loanmarket.co.nz

No surprises here!

In another decisive move to stimulate New Zealand’s flagging economy, the Reserve Bank of New Zealand (RBNZ) has again reduced the Official Cash Rate (OCR) by 50 basis points, bringing it down to 3.75%. This marks the fourth consecutive cut since August 2024, aimed at countering recessionary pressures and rising unemployment.

The RBNZ’s decision aligns with market expectations, as a recent poll indicated a majority of economists anticipated this cut. The central bank’s aggressive monetary easing reflects concerns over the nation’s economic trajectory, with growth forecasts for 2025 at a modest 1.2% and a slight improvement to 2.6% in 2026. Inflation remains within the target range at 2.2%, providing the RBNZ with the flexibility to implement such stimulative measures

Last week our friends in the Australian Federal Reserve bank only reduced their rate by -0.25% and were hawkish on whether they would do further easing anytime soon, showing how much stronger they feel their economy is doing compared to ours here in New Zealand. This is the first reduction Aussie have made since November 2020.

On a more positive note, Farmers’ confidence is at a 10 year high and given our reliance on the agricultural sector in New Zealand, this can be

seen as a strong positive for the market in general due to the flow-on effects across other sectors of the economy.

So what do we expect next?

Firstly, we expect the Reserve Bank to ease rates again at the next two OCR’s in early April and late May, but probably only by -0.25% each time.

Secondly, if you are looking to fix, we are now probably ending the low point in the rates market, so as we have said previously, don’t leave it too long to look at longer term fixed rate options.

The annual student migration

is upon us! So what better time to discuss...

Here are our top 7 tips to get your apartment student-ready. The start of 2025 is in full swing and it’s that time of the year when students return to University to start the new semester. With this newsletter we aim to provide insights for Auckland property managers and apartment owners on how to prepare rentals for returning students.

Tips to get your apartment student-ready:

Clean appliances

• Check appliances and clean if needed, to provide a cleaner and healthier cooking environment for students.

• Ensure air-conditioning service is up to date as the air conditioner will be useful when students stay indoors to focus on their studies during hot summer/autumn days.

Cool Off

• Make sure the apartment’s insulation and weather strips are up to standard. This will keep the apartment cool during summer just as it keeps it warm during winter. It will prevent cold air from escaping the room when the air conditioner or fan is used.

Create an inviting indoor space

• Replace lighting with energy efficient light bulbs such as LED fittings. Lighting is essential for students to excel in their studies. Change out old lightbulbs if required or provide a lamp on the study desk.

• Bring a touch of nature to your indoor space with plants. A variety of indoor plants will create a fresh summer vibe in the apartment. It will not only add visual interest to the room but can also improve air quality.

Create an outdoor space

• Inspect the patio or decking, make sure it’s clean and check if the flooring of the deck is up to standard.

• Create an inviting outdoor space by adding decorations and planters to provide more colors. In apartments and apartment buildings with outdoor space, students will enjoy getting some fresh air in their spare time.

Repaint apartment walls

• Repaint walls with lighter colors. We recommend using neutral colors as it will create a bright and inviting apartment space which will be beneficial for students studying indoors.

Furniture

• Think about what students need in a functional living space. Furniture like a study desk, comfortable chair, bookshelf etc. is essential for student life.

Remodel or renovate

• Is the apartment outdated and in need of remodeling? Transform the living space into a stylish, comfortable and practical apartment for current or new tenants. Benefits of renovating include an increase in property value of a current investment and provide an advantage for future sale.

Marketing your home.

A COMPREHENSIVE MARKETING STRATEGY TO REACH ACTIVE & PASSIVE BUYERS.

The marketing strategy is designed to reach the breadth of the active and passive buyer pool in the most effective manner, based on their Media consumption.

Our marketing strategy comprises of 3 key components; property portals, social and multi-channel digital strategy and print media.

Property Portals.

PRIMARILY ACTIVE & SOME PASSIVE BUYERS

There are 3 key portals, TradeMe Property, Realestate.co.nz and Oneroof.co.nz.

Property Portals generally attract active byers in the market, OneRoof has a unique position as it reaches both active and passive property buyers due to the diversity of information it has on the platform including property

Digital Marketing.

ACTIVE

& PASSIVE BUYERS

The Ray White City Realty Group has introduced a state-of-the-art digital solution that is powered by artificial intelligence to reach the breadth of the active and passive buyer pool across social media and multiple digital channels, including news and other high traffic websites. The programme is fully automated in the back end, it creates an audience

Print Media.

listings, estimated property values, market news and commentary. It is important to run campaigns across all 3 to effectively cover the breadth of the active buyer pool and a part of the massive buyer market. None of the property portals have complete market coverage and each of these portals have a set of unique audiences.

segment of active buyers specific to the property as well as reaching the passive buyer pool. The campaign is structured to deliver quality leads for the property, and it auto optimises spend across social media and multiple digital channels, skewing the spend towards channels that are performing the best.

PRIMARILY PASSIVE & SOME ACTIVE BUYERS

Print continues to play an important role to cover the breadth of the market reaching quality and highly engaged audiences. It takes criteriabased search out of the equation with respect to the active market and is the most effective medium to reach the all important passive buyer

market. This is clearly evidenced by the fact that the New Zealand herald has seen a massive 48% increase in its print readership over the last 18 months and average time spent reading the paper is over 50 minutes. The value of print is also well supported by agent feedback.

Why choose us?

City Realty Group is the largest Ray White franchise in New Zealand with offices throughout Auckland. It is the group with the ‘family factor’ - we’re family owned and we treat people like family. We’re all about open doors and open minds. We encourage a unifying atmosphere where opportunities are created, individuals are recognized and everyone grows - from our team to vendors, investors and tenants.

Our experienced and established team service the market Auckland wide -from Residential, Luxury Apartments, waterfront properties and rentals. With a dedicated property management team and marine brokerage teams. City Realty Group has a strategic partnership with Loan Market to provide clients with the best mortgage advice and rates through brokers.

+64 (9) 281 4707

www.rwsandringham.co.nz

+64 (9) 308 5551

www.rwmtroskill.co.nz

Leaders in the Auckland Residential market.

Ray White Sandringham

Ray White Mount Roskill

Meet the team.

SALES TEAM - SANDRINGHAM OFFICE

Pauline Bridgman

Amy Tsai

Kate Jiang

Diane Goer

Emily Hu

Ivan Koulin

Hugh Free

Daniel Chen

Lauren Indrisie

Alastair Hubbard

Ash Anandani

Jay Nair

Susan Woods -Markwick

Rosa Solano

Ren Agnew

Tracey Potter

Tim Cai

Yuhei Umezaki

Sammy Agnew

Claire Firmin

Lakhbir Singh

SALES TEAM - MOUNT ROSKILL OFFICE

OUR LOANMARKET MORTGAGE ADVISORS

WE CAN NEGOTIATE A LOWER RATE. WORK WITH A QUALIFIED AND COMPETENT MORTGAGE ADVISER

LoanMarket Mortgage Adviser

Damon Pooley Ethan Li

Jon Clark

Lisa Hui

Mark Li

Nana Li

May Ma

Eva Yin

Benjamin Liu

Pantea Wilson

Sara Wang

Tony Liu

Grant Harvey

Shubhrta Khanna

Ross Harvey

Maggie Liu

Anna Dong

LoanMarket Mortgage Adviser

Jo Price

Davy Chen

Evie Gao

Jamie Maclennan

Ibrahim Khazi

Minnie Zhu