Market CommentThat was good news… and there’s more to come. 06.

Auckland Central Sales & Statistics - August 2025

10. Grafton & Eden Terrace Sales & Statistics - August 2025

18.

Article – Tony Alexander: Reserve Bank’s OCR shock treatment - is it working?

16. Auction Update with Cameron Brain

22.

Article – Kelvin Davidson: New mortgage rules from Dec 1: What they mean for the housing market

20.

Our month in Review Top Stories & Events from the City Realty Group

24.

LoanMarket Update: Big 0.50% Rate Cut Lands

26. Ray White SuperCity Property Management Spring Update 28. Our Awards & Accolades Ray White Auckland Central & Wynyard Quarter

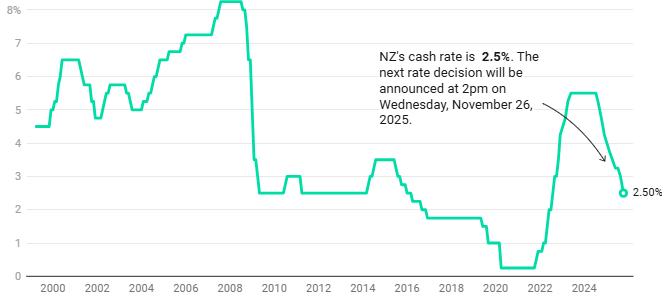

On 8 October 2025, the Reserve Bank of New Zealand (RBNZ) delivered a welcome boost to the housing market, cutting the Official Cash Rate (OCR) by 50 basis points to 2.5%.

With another review due on 26 November, Daniel Horrobin, Director of City Realty Group, says: “It would not be a surprise if there’s another reduction of some description.”

Adding to the positive sentiment, the RBNZ has also confirmed it will ease mortgage loan-tovalue ratio (LVR) restrictions from 1 December 2025, signalling greater flexibility for both buyers and investors.

“There’s no doubt the economy is dragging its feet, but good things do take time,” says Daniel.

Economist Tony Alexander, writing in NZ Herald OneRoof, noted that “the economy is improving, but there is a high degree of impatience about the slowness of the upturn, and this has generated considerable pressure on the Reserve Bank to speed things along with extra lowering of borrowing costs.”

Positive Indicators Across the Market

While economic conditions remain cautious, multiple industry reports point to renewed confidence in the New Zealand housing market: Cotality (formerly CoreLogic) reported on 8 October that “Investors have been returning to the market over the past year, encouraged by the shorter Brightline Test, reduced LVR requirements, the reinstatement of mortgage interest deductibility, and lower mortgage rates.”

Interest.co.nz (9 October) observed that “Hopeful vendors surged into the housing market in September, with new Trade Me listings up 24% compared to August, and 5.9% higher than September 2024.”

The REINZ September Property Report headlined: “Market momentum builds as sales rise and days to sell drop.”

A NZ Herald article on 15 October shared encouraging data from Westpac’s business and household survey, showing that the economy is showing early signs of lifting, with households and businesses reporting still challenging but improving conditions.”

Auckland City Centre – Confidence Rebuilding

As Auckland’s city centre prepares for summer, confidence among business owners is mixed but trending upward.

A recent Heart of the City Business Owners Survey highlighted challenges for central-city operators — “news council and city leaders need to hear,” says Daniel.

“Let’s hope there’s meaningful action from leadership to support those living and working in the heart of the city.”

Despite challenges, optimism is returning. The coming months will see an exciting line-up of events and milestones that are expected to reignite foot traffic and vibrancy across the CBD:

• The $1 billion SkyCity International Convention Centre opens February 2026, with 95 events already booked for its first year.

• Auckland Domain will host a full calendar of major events from February through March 2026, showcasing the park’s renewed vitality.

• The Laneway Festival returns to Western Springs in early February.

• The world-class SailGP Yachting Event will light up Auckland Harbour mid-February.

“The central city will get the summer it deserves,” says Daniel. “And with the longawaited City Rail Link set to open in 2026, these are exciting times for Auckland — and for everyone who lives, works, and invests here.”

Final Thoughts

While New Zealand’s economic recovery may feel slow, the combination of lower interest rates, easing lending conditions, and growing market momentum are all signs that confidence is returning.

For buyers, sellers, and investors alike — now is the time to prepare for renewed activity heading into 2026.

Auckland Central Market Statistics.

Source: REINZ SEP 2025

Total Sales

September 2025

46

September 2024

There was a -49% decrease in the total number of sales year on year.

Total Sales Value Median Sales Price Median Days On Market

September 2025

$15,075,250

September 2024

September 2025

$243,250

September 2024

91 $49,952,964 $416,000 45.5

There was a -69% decrease in the total sales value year on year.

There was a -41% decrease in the total median sale price year on year.

September 2025

53

September 2024

There was an 16% increase in the total median days on market year on year.

Recent Sales.

Eden Terrace

RECENT SALES

EDEN TERRACE MARKET STATISTICS. AUG 2025

Total Sales

5

SEPTEMBER 2025

Median Sale Price

$740,000

SEPTEMBER 2025

Total Sales Value 79.5 Median Days on Market

$4,775,000

SEPTEMBER 2025

EDEN TERRACE - RECENT SALES.

Address

310/43 Virginia Avenue, Eden Terrace 2

411/15 Rendall Place, Eden Terrace 2

810/47 Randolph Street, Eden Terrace

202/59 France Street South, Eden Terrace 1

201/59 France Street South, Eden Terrace 1

SEPTEMBER 2025

Source: REINZ

$530,000 29-Sept-25

$945,000 23-Sept-25

$1,950,000 19-Sept-25

$740,000 18-Sept-25

$610,000 18-Sept-25

RECENT SALES

MARKET STATISTICS.

Total Sales Median Sale Price

AUG 2025 12

$481,250

Total Sales Value

$5,364,250

GRAFTON - RECENT SALES.

30 Median Days on Market

STATEMENT:

Ray White repeatedly achieves higher sales prices than other agencies, and it’s not just our claim— here are the facts:

301/83 Halsey Street, ‘Lighter Quay’

1 1 0

SOLD WITH RAY WHITE

Sale Price: $150,000 + GST

($172,500 incl GST)

Sale Date: 24th of October 2024

201/83 Halsey Street, ‘Lighter Quay’

1 1 0

SOLD BY ANOTHER AGENCY

Sale Price: $50,000

Sale Date: 6th November 2024

* IMPORTANT NOTE: Both units are identical with just one floor level separating them, yet Ray White sold for $122,500 more than the other agency.

Request an appraisal today.

Ray White Auckland Central is your home for apartments.

305/8 Ronayne Street, ‘The Landings’

SOLD WITH RAY WHITE

Sale Price: $157,500

Sale Date: 1st August 2024

* IMPORTANT NOTE:

803/8 Ronayne Street, ‘The Landings’

SOLD BY ANOTHER AGENCY

Sale Price: $105,300

Sale Date: 7th August 2024

The unit sold by the other agency included a car park, yet it still sold for $52,200 less than the price Ray White achieved for a property without a car park.

110/8 Ronayne Street, ‘The Landings’

SOLD WITH RAY WHITE

Sale Price: $135,000

Sale Date: 12th September 2024

* IMPORTANT NOTE:

205/8 Ronayne Street, ‘The Landings’

SOLD BY ANOTHER AGENCY

Sale Price: $116,500

Sale Date: 21st August 2024

The unit sold by the other agency included a car park, yet it still sold for $18,500 less than the price Ray White achieved for a property without a car park.

There’s an old saying: “You get what you pay for.”

In these case studies, maybe saving a little on commission upfront led to a significantly higher loss in the end.

List with Ray White for the best results and more money in your pocket. And if fees are a concern for you - let’s talk.

Ray White City Realty Group Auction Market Update

As we closed out September, the strength of the auction process once again proved its value in driving engagement and competitive results across our group.

During the month, the Ray White City Realty Group conducted

638 Open Homes across 398 properties, meeting 443 active buyers.

Of these, 20% of all Open Homes were Auction Campaigns , yet they accounted for an impressive 45% of total buyer attendance — highlighting that buyers remain drawn to the transparency and opportunity auctions provide.

We successfully conducted 20 auctions in September, achieving a clearance rate of 55% , consistent with our year-to-date performance and well above private treaty benchmarks.

Momentum Building into October and Beyond

October has seen renewed momentum, with auction bookings up 55% month-on-month , indicating both confidence among vendors and continued demand from buyers seeking certainty before year-end.

Looking ahead, our team is preparing for the next Ray White CRG Auction Event on November 26 and 27, where we anticipate showcasing 40 auctions across two highenergy days

This event will once again unite our offices and highlight the power of collaboration within the City Realty Group.

Upcoming Event: Auckland Apartment Buyers Evening

For those considering a move into Auckland’s apartment market, our Auckland Central Team will host an Auckland Apartment Buyers Evening on Tuesday, 11 November at 6:00pm at our Auckland Central office (Level 3, 246 Queen Street).

This session will provide valuable insights into the current apartment landscape, finance options, and the lifestyle advantages of city living.

If you’d like to attend, please email cameron.brain@raywhite.com to secure your place.

Cameron Brain.

Director of Sales & Auctions 027 424 1782 cameron.brain@raywhite.com

Is it time to rethink renting?

What do the experts say about buying in the city?

What should you know before buying an apartment?

We’ve brought together experienced investors, apartment owners, central city residents, and trusted finance and legal experts for an in-depth discussion and interactive Q&A session.

6PM, TUESDAY 11 TH NOVEMBER 2025

Tony Alexander: Reserve Bank’s OCR shock treatment - is it working?

Figures suggest Kiwis are planning to spend more and that house prices are stabilising.

ANALYSIS: Last week, the Reserve Bank dropped the Official Cash Rate 0.5 percentage points to 2.5%. The question now is: will this shock treatment have any impact on the economy? So far, based on the results of two surveys I ran immediately after the cut, the economic outlook looks marginally more positive than it had been.

On Friday, I asked my subscribers if they planned to buy more or less stuff over the coming three to six months. This measure was at a horrible net 42% negative in the middle of last year, when the economy was in the process of shrinking 2%.

It then jumped to +10% in December as people falsely assumed the simple removal of high interest rates would solve many problems. But, as the reality of a weak jobs market kicked in and feelings

NZ’s Official Cash Rate Drops To 3.25%

of employment insecurity returned, the measure fell to -18% in April. It recovered to just -1% a month ago and now has risen to +13%. This is the best reading in almost four years and tells us that retailers can start to more realistically talk about light at the end of their long and dark tunnel. But until the employment situation improves, the actual boost in consumer spending is likely to be constrained.

So, will businesses start thinking about hiring more people? I am partway through another of my monthly surveys which looks at business concerns and plans. The net proportion of businesses anticipating better revenue in a year has lifted to 53% from 48% a month ago. Again, the direction of travel is good, but the improvement is quite mild.

The graph shows the OCR since its introduction in 1999.

Chart: OneRoof.co.nzSource: Reserve Bank of New Zealand

Tellingly, the net proportion of businesses planning to spend more on new investment in plant and machinery has actually fallen to 4% from 10% and the measure looking at planned stock levels has also worsened slightly.

Looking at employment, there is a hint of positivity with a lift in plans to spend more on remuneration to a net 22% positive from 18%. But the labour market traditionally lags the economic cycle so we may not see much happening in this and other surveys until the New Year, when hopefully there will be greater feedthrough from higher farm incomes and sustained lower interest rates.

Looking at the housing market the question becomes whether owner-occupiers will finally step forward and join the many firsthome buyers who have been active since the start of 2023. Without a strong labour market, it seems unreasonable to expect more than a lightly more positive feeling for the next few months.

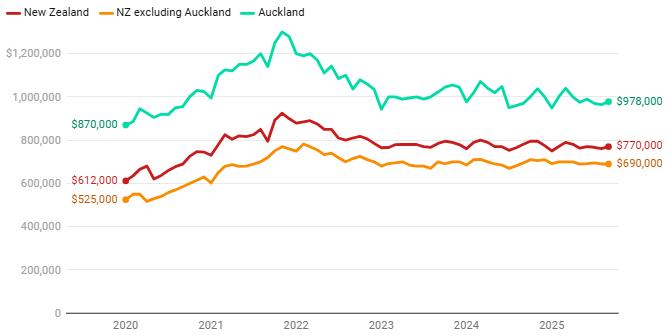

Median House Price Changes Since 2020

For investors, the lower financing costs will go some way to offset the sustained higher spending on council rates, maintenance, and insurance. But continued weakness in net migration flows will act as a strong restraint as will the evidence of rents falling and good tenants still being in short supply.

For housing, the ducks are starting to line up for a better performance. But it feels too soon to expect anything particularly solid in the near future.

Having said that, the data suggests house prices have at least stopped falling and are starting to creep slightly higher. The REINZ House Price Index for the country as a whole rose 0.8% in September after gaining 0.4% in August. That sounds good, but merely offsets falls of the same magnitude in the previous two months. Assuming prices are stabilising seems the best bet for now.

The chart shows the monthly change in the median sale price since January 2020.

- Tony Alexander is an independent economics commentator. Additional commentary from him can be found at www.tonyalexander.nz

@raywhiteaucklandcentral

@raywhitewynyardquarter

@raywhitesandringham

@raywhite.mtroskill

30 years with Ray White!

Congratulations Ivan! Your dedication, passion, and commitment have truly shaped the success and culture of our team. Here’s to three decades of excellence, and many more milestones ahead!

Winner, winner!

Moon Festival Colouring Competition Winner Announcement! We received so many wonderful and creative entries — thank you to everyone who took the time to share your beautiful colouring with us!

Congratulations to Isabella Chen! Your colouring was absolutely beautiful and captured the Moon Festival spirit perfectly.

Celebrating Diwali!

Ray White Mt Roskill kicked off their sales meeting with a vibrant celebration of Diwali at the office! It was wonderful to see our workplace come alive with Indian music, delicious food, and colorful traditional clothing.

Our award winners...

Congratulations to Habeeb & May who both received Customer Service awards at the recent Ray White Annual Awards night.

Kelvin Davidson: New mortgage rules from Dec 1: What they mean for the housing market

The five things you need to know about the housing market this week.

1. Surprise! LVRs to loosen

The Reserve Bank sent out a surprise email last week, announcing its intention to loosen the LVR (loan-to-value ratio) rules from December 1. Twenty-five percent of lending to owner-occupiers (up from 20%) will be allowed at less than 20% deposit, with 10% of lending to investors (up from 5%) able to be done at less than 30% deposit.

However, this seems unlikely to produce a fresh surge in the housing market. After all, first-home buyers are already strong, even though only around 12-13% of overall owner-occupier lending is currently being done with less than a 20% deposit. I’m not sure it means too much for that group, because even the current, lower speed limits aren’t really binding.

To be fair, low deposit finance is currently very hard to come by for investors at the moment, so the looser speed limit may be more noteworthy for them. Even so, there are still other credit restraints in place, including debt-to-income ratio caps and banks’ internal serviceability testing, so looser LVRs are unlikely to unleash a fresh surge of investor activity either.

2. Net migration and rents are both still sluggish

Another headwind for investors at present is the weakness of rents, which are currently falling in many of our main centres (based on MBIE’s new bonds lodged data). This partly reflects the pre-existing affordability challenges for tenants, with the

From December 1, the Reserve Bank’s loan-to-value ratio rules will be looser, allowing more lending to low-deposit home buyers. Photo / Fiona Goodall

level of rents still at a record high in relation to household incomes, as well as a higher supply of available rental listings.

But the drop in net migration and slower demand growth for rental property have been key factors as well. The latest Stats NZ figures showed a net migration inflow of just 10,600 in the year to August, versus a long-term average of 31,500.

3. Construction costs are still pretty flat

The latest Cordell Construction Cost Index showed a relatively flat result, with house-building costs only up by 0.4% in the three months to September, and by 2% from the same period in 2024. Both those figures were less than half their long-term averages. Of course, that shouldn’t be too surprising, given that the construction industry has been in a slowdown phase for about three years now, with some spare capacity restraining labour and materials costs.

However, things should look better for builders in 2026 with interest rates down and the lending rules (LVRs, DTIs) still

encouraging people to look at new-builds. In that environment, construction costs may start to rise a little faster, but a repeat of the post-COVID spike in building costs is unlikely.

4. Pushing the 3% upper limit?

The key economic release this week will be Q3 inflation data from Stats NZ on Monday. The Reserve Bank anticipates that the headline rate may well get to 3% (the top of the target range), which is a bit awkward given they’ve been cutting the Official Cash Rate. However, this lift in inflation should prove temporary (given spare capacity across the economy), so look for the next CPI to soften.

5. More bank switching?

On Friday, I’ll be watching September’s mortgage lending data from the Reserve Bank. ‘Refi’, or bank switching, has been a key focus lately, so it’ll be interesting to see if this rise in activity continued last month, as existing borrowers chase a cashback at another lender.

Cotality chief economist Kelvin Davidson: “There may be some modest increases in property values as we get into 2026.” Photo / Peter Meecham

Jamie Maclennan

027 742 5227

jamie.maclennan@loanmarket.co.nz

Big 0.50% Rate Cut Lands

The Reserve Bank of New Zealand (RBNZ) has cut the Official Cash Rate (OCR) by 0.50%, bringing it down to 2.50%. This move was widely expected — the only question was how much the cut would be. While the RBNZ has generally preferred smaller 0.25% changes, the weaker economic outlook has led to a larger 0.50% cut this time.

Why the cut?

• Economic growth has slowed more than expected.

• Inflation is under control both in New Zealand and overseas.

• Other central banks are also lowering rates, giving the RBNZ room to act.

• The goal is to support businesses and consumer confidence heading into the summer period.

Although the economy is in a tough spot, this move should help create some optimism and encourage spending and investment.

What about inflation?

• Inflation remains a risk, but the RBNZ is choosing to “look through it” for now.

• If inflation doesn’t stay under control, rates could rise again in the future.

What’s next?

• Since the last OCR cut in August, the economy has worsened further,

making today’s decision unsurprising.

• The RBNZ has also left the door open for more cuts if conditions continue to deteriorate.

• The next OCR update and last for the year is November 26th, then there is a break through until mid Feb 2026.

What does this mean for you and your loan?

• The banks had already lowered their rates in anticipation of this move.

• We may still see further small reductions in fixed rates over the next few days.

Current best-value rates:

• 1-year and 2-year fixed terms are sitting around 4.49%.

• The 6 month & 1-year options give flexibility to review your situation next year, but as we have said in the past, don’t leave it too long before you take advantage of some longer term rates.

• Splitting between shorter and longer terms can be a smart approach for larger loans.

A few things to keep in mind:

With rates falling, break fees on existing fixed loans are increasing.

If you’re planning to sell, refinance, or repay debt, make sure your fixed terms line up with your plans to avoid extra costs.

In summary

• The OCR is now 2.50% after a 0.50% cut.

• The RBNZ is acting to boost growth and lift confidence, despite inflation risks.

• Short-term fixed rates remain competitive, and now’s a good time to review your lending strategy.

If you’d like to discuss how this change affects your loan or refix options, get in touch — we’re happy to help you run through your choices.

Central City Bucking the Rental Market Trends

If you’ve been listening to the news—or eavesdropping at your local weekend BBQ—you’d be forgiven for thinking the rental market has hit a slump. Reports of high vacancy rates, flatlining rents, and a flood of new housing stock dominate the headlines. And yes, in some outer suburbs where building has boomed, that may be the case.

But in Auckland’s central city, we’re seeing a different story entirely. The market here is not just resilient—it’s gaining strength.

Across the Ray White Supercity Property Management portfolio, vacancy rates are trending towards 1%, a level we haven’t seen consistently since pre-COVID times. Rents are rising again, driven by growing demand and a shift in tenant quality. After years of uncertainty, 2025 has marked a turning point.

The Students Are Back – And So Is Stability

The student population is once again a major driver of the central city market. International student numbers at the University of Auckland increased by 8% in 2024, with further growth projected into 2026. This demographic not only values proximity to campus, but also tends to be stable, respectful, and reliable—especially when well-managed.

Gone are the days when landlords had to choose between two bad options. In the difficult postlockdown period, some were forced to accept less-than-ideal tenants simply to keep properties occupied. But now, with demand surging and a deeper pool of well-qualified applicants, our landlords are no longer put in that position.

A Safer Environment for Investors

We’ve also seen encouraging signs from the private sector. Insurers have begun applying higher excesses for malicious damage claims involving emergency housing tenants— effectively discouraging unsuitable tenancies in

large apartment complexes and body corporates. These changes are helping restore confidence in central city investments and protect long-term capital value.

What does all this mean? It’s a strong time to own property in the Auckland CBD—especially when it’s professionally managed by a team that knows how to attract and retain top-tier tenants.

At Ray White Supercity, we don’t just manage properties—we protect your investment and grow your returns. Our team specialises in the nuances of central city tenancies, from student lettings to executive apartments, and we’re proud to be helping shape the recovery of the inner-city rental market.

Thinking of Switching Property Managers—or Just Curious About the Current Market?

Whether you’re in the process of buying an investment property or simply wondering how your current rent stacks up in today’s market, we’re here to help.

At Ray White Supercity Property Management, we offer a free, no-obligation rental appraisal service to give you clear, expert insight—no pressure, just good advice.

Get in touch with our team today and discover how we can help protect your investment, reduce vacancy, and attract high-quality tenants. Let’s chat about what’s possible.

Rate My Agent Awards

RAY WHITE AUCKLAND CENTRAL ARE PROUD TO BE ACKNOWLEDGED BY RATE MY AGENT FOR THE BELOW AWARDS

CURRENTLY PLACED

#1

Auckland Central

Agency of the Year 2025

#1

Agency of the Year 2025 Grafton

#1

Agency of the Year 2025 Eden Terrace

RateMyAgent is Australia’s leading real estate ratings and reviews website. It collects and verifies reviews from buyers, sellers, and landlords to provide an accurate and reliable assessment of real estate agencies. RateMyAgent Awards are independently judged based on verified customer reviews and sales data.

Meet the team.

SALES TEAM - AUCKLAND CENTRAL OFFICE

Daniel Horrobin

Pauline Bridgman

Ady Huang

Craig Warburton

Dom Worthington

Dusan Valenta

Habeeb Urrahman

Carlos Del la Varis

Chris Cairns

Grant Elliott

Joon Kim

Wynyard Quarter & Sandringham

Belinda Henson

Casey Chen

Firmin

Dayal

Judi Yurak

Anchit Sharma

Erin Dayal

Leo Zhu

Krister Samuel

SALES TEAM - WYNYARD QUARTER OFFICE

OUR LOANMARKET MORTGAGE ADVISOR

WE CAN NEGOTIATE A LOWER RATE. WORK WITH A QUALIFIED AND COMPETENT MORTGAGE ADVISER