Fosters Mill Village Real Estate Market Report

COMPARING 2020 TO 2008

ARE THEY DIFFERENT?

COVID-19 has had a large effect on the economy – so much so that you might have heard talks of our country entering another recession. Due to the severity of the 2008 financial crisis and the ensuing recession, the term stirs up a lot of emotions for many, especially when it comes to the real estate market.

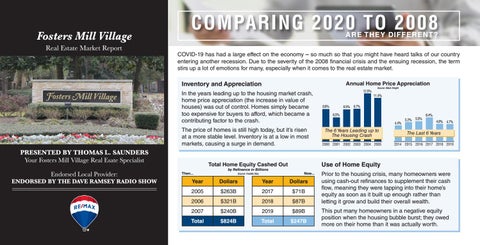

Inventory and Appreciation

Annual Home Price Appreciation

In the years leading up to the housing market crash, home price appreciation (the increase in value of houses) was out of control. Homes simply became too expensive for buyers to afford, which became a contributing factor to the crash. The price of homes is still high today, but it’s risen at a more stable level. Inventory is at a low in most markets, causing a surge in demand.

PRESENTED BY THOMAS L. SAUNDERS Your Fosters Mill Village Real Esate Specialist Endorsed Local Provider:

ENDORSED BY THE DAVE RAMSEY RADIO SHOW

by Refinance in Billions Source: Freddie Mac

Source: Black Knight

11.4%

8.5% 8.7%

8.6% 6.5%

4.4%

5.2% 5.5%

6.4% 4.8% 4.7%

The 6 Years Leading up to The Housing Crash

The Last 6 Years

2000 2001 2002 2003 2004 2005

2014 2015 2016 2017 2018 2019

Use of Home Equity

Total Home Equity Cashed Out Then...

12.5%

Now...

Year

Dollars

Year

Dollars

2005

$263B

2017

$71B

2006

$321B

2018

$87B

2007

$240B

2019

$89B

Total

$824B

Total

$247B

Prior to the housing crisis, many homeowners were using cash-out refinances to supplement their cash flow, meaning they were tapping into their home’s equity as soon as it built up enough rather than letting it grow and build their overall wealth. This put many homeowners in a negative equity position when the housing bubble burst; they owed more on their home than it was actually worth.