Our Strategic Analysis is designed to help you make better commercial property decisions in relation to this asset.

It is common that most investment properties for sale come with plenty of property specific detail, though it is often more difficult to understand where the property sits in the greater market. Our day to day involvement with the Moreton Bay commercial property market over the last twenty years gives us a unique perspective on the key drivers that impact this property and the tenants that operate in it, both now and in the years to come.

The report breaks our assessment into three sections:

What is impacting the retail investment sector nationally 1.

What is impacting the local area market for this sector 2.

What does it mean for this particular property 3.

It is very likely that information in this report will prompt more questions. We are on standby to provide you with whatever additional information you require to ensure you are comfortable that this asset will meets your investment goals.

Kind regards,

Chris Massie Director 0412 490 840

chris.massie@raywhite.com

Troy Sturgess Senior Agent 0432 701 600

troy.sturgess@raywhite.com

Property Address Lots 15-18/1 Regina Avenue, NINGI QLD 4511

Legal Description Lots 15-18 on SP107598

Unit 15 & 16: 170m²*

Unit 17: 71m²*

Area

Unit 18: 116m²*

TOTAL: 357m²*

Zoning General Residential - Suburban Neighbourhood

Local Authority Moreton Bay City Council

Gross Income P/A $171,885*

Net Income P/A $122,131

WALE 2.86 years

National anchor tenant

Property Features

Multi tenanted for continuity of income

Prominent corner location

The multi-tenanted, multi-titled nature of this property is what attracts me the most. Those who are risk averse should find comfort in this.

Agent Insights

*Approximately

ALH Group The Brew Shed Aidacare -

ALH Group are a true blue-chip tenant, with 350 licensed venues across the country. The long tenant history and 4 year remaining term of this anchor forms the backbone of this investment

Aidacare is comfortably under average market rents due to the fixed 2.5% reviews not keeping up with high CPI in recent years. This gives opportunity for growth at the next market review in two years.

The WALE is balanced well, with the largest, most secure tenant having the longest lease and the smallest tenant being next to expire

Lease expiries are staggered more than one year apart, which maxes multiple vacancies at any time in the next five years very unlikely.

Agent Insights

Land tax could potentially be avoided by purchasing the lots in two seperate entities to keep the combined unimproved land value under the taxable threshold.

Well established national anchor tenant with long tenure

Prominent corner main road location

Multiple tenant, multiple title flexibility

The convenience retail sector has been a stand out in terms of stability over the last four years. Post-COVID consumer behaviour has proven this sector to be bullet-proof int the face of massive change. People still need what they need and these centres continue to provide an irreplacable service.”

- Ashley Rees, Senior Analyst

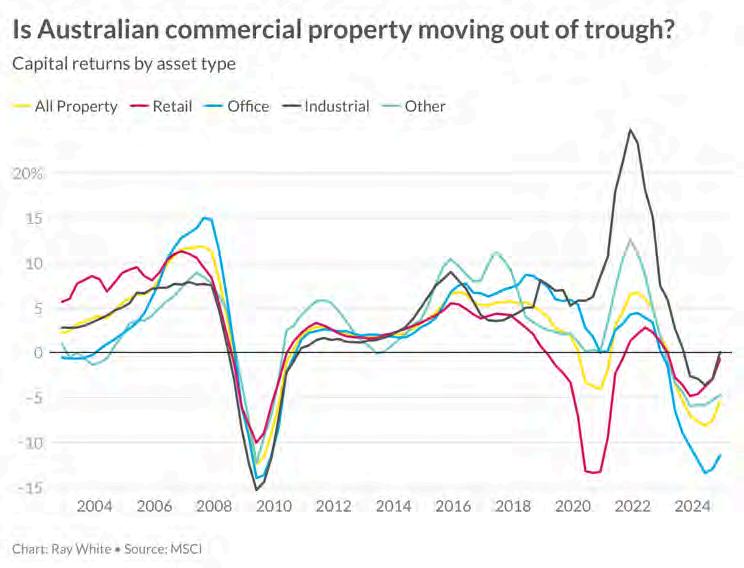

Retail and Industrial have dominated commercial investment performance in recent times. Retail assets have led total returns for two consecutive quarters, posting a 2.8 percent total gain in the latest results. While per-capita retail trade has decreased, limited new supply against strong population growth has driven improved occupancy and rental performance.

Attention is firmly fixed on neighbourhood and sub-regional centres like this property, demonstrating particular resilience when anchored by the right retail mix. For the first time, retail transactions now represent 41.1 percent of all commercial transactions this quarter - a rapid shift reflecting renewed confidence in the sector after a long term average of just 28 per cent.

The last two years saw a softening of the overall commercial property market from the highs of 2021-22. In this time though, neighbourhood centres saw the smallest cap rate movement of just 39 basis points, while super/major regional centres experienced only a 51 basis point increase.

The latest interest rate cut indicates the start of the cycle shift where a widening spread between capitalisation rates and government bond yields will create an increasingly attractive risk premium for investors. As interest rates fall, this spread is poised to drive renewed investment activity, particularly from buyers seeking relative value compared to other investment options.

These are the market factors that are shaping the landscape for this property in the coming years”

- Ashley Rees, Senior Analyst

We have the population of Rockhampton moving to North Moreton Bay over the next few decades. Caboolture West and Morayfield South will house more than 100,000 new residents. Add to this the continued expansion of the Southern Sunshine Coast and you have one of the most significant residential growth corridors in Australia.

The topographic nature of the Ningi area, combined with the strict remnant vegetation protection policies in place, mean there is limited suitable land available for new greenfield residential or commercial ventures. Flooding and koala protection overlays constrain the bulk of the land between Caboolture and Bribie Island. The result is a push to increased density and refurbishment of existing properties.

Construction prices have been a major source of the CPI issues that drove the interest rate hikes of 2023. There has been a perfect storm of international conflict, labour shortages, fuel, materials and competing infrastructure projects impacting all facets of commercial construction. We can expect a trend towards higher density zoning with mixed use commercial precincts. These are traditionally more expensive to construct than slab-on-ground strip retail like your property, meaning our required rents will be significantly cheaper than any new build competition.

Affordable housing will continue to be a hot topic for Australia and SEQ in particular. Cost of living pressure in Brisbane is forcing lower income nad first home buyers further north, which will give stability to the Bribie Island residential market. Expanding employment bases in Caboolture means Bribie is perfectly positioned to provide high density, low cost housing for those wanting affordability with short travel time to these nearby employment hubs. This increasing population will naturally increase gross convenience retail spend in the region, benefiting your tenants.

We have prepared the following summary of key observations on this particular property, based on what we know about the national market trends and local market drivers,

Rent vs Market & Tenant Demand

Lease Structure & WALE

Replacement Cost & Capital Growth

Potential

Outgoings, Maintenance & Management

The strongest tenant has the largest footprint and the longest lease, which should be reassuring. Aidacare is a specialist in aged care equipment provision. Bribie Island and surrounds house a large retirement community. The main road visibility and on-ground easy access make this a perfect location for them or operators like them who service this dempgraphic.

Rents are in line with or under market rates. Aidacare in particular could see a significant rental uplift at their next market review in 2027

The weighted average lease expiry (WALE) is close to three years, but more importantly, the lease expiries for each tenant are more than a year apart. This ensures continuity of income throughout the life of your investment. The Gross nature of the lease structures has good and bad elements to it. Tenants have the certainty of fixed monthly costs but your true net return can be impacted by unexpected changes in outgoings rates. We can reduce the impact of this through pro-active asset management to control these costs.

The Replacement cost and land constraints previously mentioned ensure any new developments in the region will need to achieve rent rates 70-100% higher than those being achieved in this centre. This drives capital growth through comparable rental market reviews and tenant demand for affordable alternatives.

The investment should prove to be a relatively low maintenance property, in spite of its age. Tenants are responsible for their internal fit out maintenance and the Body Corporate is responsible for external repairs, maintenance and refurbishments through the sinking fund. It will be important to stay pro-active in your follow up of maintenance obligations for both your tenants and body corporate if you self manage. Alternatively, our property management team can continue to manage these items (the cost of which is already factored into the true net return).

We hope this assessment has helped you better understand this property and the market drivers for the region. We expect the information we have provided to prompt as many questions as it answers for you. With this in mind, we are happy to arrange a time to discuss in as much detail as necessary to ensure you are comfortable this asset will help you achieve your investment goals.

Regards,

Chris Massie Director

0412 490 840 chris.massie@raywhite.com

Troy Sturgess Senior Agent 0432

701 600

troy.sturgess@raywhite.com

Ray White Commercial Northern Corridor Group positions itself as a leading commercial real estate and property management agency offering unparalleled market knowledge and expertise from Gympie to Pine Rivers.

With a competitive team of sales agents, property managers, project managers, marketing, public relations, and administration professionals all working towards the shared goal of providing expertise in market intelligence and excellent results, Ray White Commercial Northern Corridor Group prides itself on a reputation of integrity and a strong work ethos.

Our sales and leasing agents are motivated, focused and willing to go the extra mile to achieve exceptional results and be the best in the industry. They are all experts in their respective areas and can provide you with up to date market reports so that you have a solid understanding of where your property sits in the market. Our market knowledge sets us apart from others within the market and assists us in delivering on clients expectations of Ray White Commercial Northern Corridor Group being leaders within our field.

The Ray White Group is now one of Australasia’s largest real estate focused businesses and has grown to more than 1,000 offices with 8,000 staff and an annual turnover of A$30 billion across Australia, New Zealand and Indonesia and through offices in Delhi, Bangkok, Hong Kong, Shanghai, Dubai and Abu Dhabi.

NORTH BRISBANE

Unit 4

257 Leitchs Road

Brendale QLD 4500

SUNSHINE COAST

Level 1

172 Brisbane Road

Mooloolaba QLD 4557

MORETON BAY

Unit 1

2-12 Alta Road

Caboolture QLD 4510

1.

2.

The information contained in this Strategic Analysis and any other verbal or written information given in respect of the property (“Information”) is provided to the recipient (“you”) on the following conditions:

North Coast Commercial Properties Pty Ltd, trading as Ray White Northern Corridor Group and or any of its officers, employees or consultants (“we, us”) make no representation, warranty or guarantee that the Information, whether or not in writing, is complete, accurate or balanced. Some information has been obtained from third parties and has not been independently verified. Accordingly, no warranty, representation or undertaking, whether express or implied, is made, and no responsibility is accepted by us as to the accuracy of any part of this or any further information supplied by or on our behalf, whether orally or in writing.

3.

All visual images (including but not limited to plans, photographs, specifications, and artist impressions) are indicative only and are subject to change. Any measurement noted is indicative and not to scale. All outlines on photographs are indicative only.

4.

The Information does not constitute, and should not be considered as, a recommendation in relation to the purchase of the property or a solicitation or offer to sell the property or a contract of sale for the property.

6.

You should satisfy yourself as to the accuracy and completeness of the Information through your own inspections, surveys, enquiries, and searches by your own independent consultants, and we recommend that you obtain independent legal, financial and taxation advice. This includes as to whether any listing price is inclusive or exclusive of GST.

5. We are not valuers and make no comment as to value. “Sold/leased” designations show only that stock is “currently not available” – not that the property is contracted/ settled. If you require a valuation, we recommend that you obtain advice from a registered valuer.

7. Interested parties will be responsible for meeting their own costs of participating in the sale process for the property. We will not be liable to compensate any intending purchasers for any costs or expenses incurred in reviewing, investigating or analysing any Information.

The Information does not and will not form part of any contract of sale for the property. If an interested party makes an offer or signs a contract for the property, the only information, representations and warranties upon which you will be entitled to rely will be as expressly set out in such a contract.

8. We will not be liable to you (to the full extent permitted by law) for any liabilities, costs or expenses incurred in connection with the Information or subsequent sale of the property whatsoever, whether the loss or damage arises in connection with any negligence, default or lack of care on our part.

9. No person is authorised to give information other than the Information in this Information Memorandum or in another brochure or document authorised by us. Any statement or representation by an officer, agent, supplier, customer, relative or employee of the vendor will not be binding on the vendor or us

10. To the extent that any of the above paragraphs may be construed as being a contravention of any law of the State or the Commonwealth, such paragraphs should be read down, severed, or both as the case may require, and the remaining paragraphs shall continue to have full force and effect.

11. You may not discuss the Information or the proposed sale of the property with the vendors or with any agent, friend, associate or relative of the vendor or any other person connected with the vendor without our prior written consent. We accept no responsibility or liability to any other party who might use or rely upon this report in whole or part of its contents.

13.

12. The Information must not be reproduced, transmitted or otherwise made available to any other person without our prior written consent.