Latin America is often regarded as one of the world’s regions with the greatest potential for financial innovation. We have seen this trend begin to play out in recent years with the emergence of countless fintechs, especially in countries such as Brazil and Mexico, which are paving the way for other markets in the region. Latin America, however, faces deep-rooted cultural challenges as it modernizes and becomes more financially inclusive. To prevent reversing recent advances and to guarantee that women play an active role in the economic recovery, this issue must be addressed.

There is an opportunity for this gender gap to be mitigated with the support of banks and lenders. By leveraging technology such as alternative data and machine learning, financial institutions can support female-led businesses through a more comprehensive analysis of behaviors beyond traditional data points to evaluate their real potential as clients. This, in turn, provides greater credit opportunities for women entrepreneurs by streamlining lending processes, including quickly and accurately assessing credit risk.

To that regard, banks and financial institutions should begin to adopt genderconscious strategies and technologies by re-examining market conditions to determine the financial services that are required by women. Entrepreneurship should be nurtured in today’s womenled firms and systematically developed within financial institutions. By building an investor economy for female entrepreneurs, organizations can better address persistent funding gaps.

Gender inequality is a significant hinderance to Latin American societies, as it prevents the emergence of potentially groundbreaking new companies and ideas.

According to the Inter-American Development Bank (BID), 54% of women use their own savings to start a project since only 15% manage to start their companies with the support of a private bank. The entity states that among the main barriers for women who want to start a business are the fear of failure, household responsibilities and a lack of motivation. Women also tend to have

fewer assets under their name than men, which makes it more difficult to prove to banks their ability to pay for loans.

Many Latin American women are often subjected to an environment where they are told that they cannot get ahead on their own and are prohibited from making any economic decisions.

The World Bank’s latest “Women, Business and the Law” report states that women in the region have often faced discriminatory laws, although progress has been made, and still face challenges in many cases. The research concluded that in 16 countries in the region, women are prohibited from doing the same jobs as men. Such is the case in Belize, where they cannot work at night in factories, or in Colombia, where they are prevented from carrying out activities considered to be dangerous.

Reaching a level of financial inclusion that addresses existing barriers and results in substantial change is the way forward for women in the region to gain access to diversified business opportunities and services.

In Brazil, a survey conducted by Sebrae indicated that the surge in the number of women who decided to open their own business increased by 124% between 2014 and 2019. One of the

most significant recent examples of a successful female entrepreneur in the region is Cristina Junqueira, cofounder and recently appointed CEO of Brazil for Nubank, the largest fintech in Latin America. She co-founded the company in 2013 out of dissatisfaction with the high interest rates and service of large Brazilian banks, and the fintech now has more than 34 million customers after tripling its number of users in less than two years.

Estimates by the Inter-American Development Bank (IDB/BID) indicate that greater inclusion of women in the workplace, with equal wages and greater access to financing, can increase the size of the economy by up to 22% and would give the banking system greater stability. Bank platforms that specialize in supplying financial training and products that work for women are proven to be successful business models in advancing women’s entrepreneurial dreams, which have a wide and demonstrable influence on society in many cases.

With the insights offered by experts on the topic within the region, an improved approach for lenders to support women in their ventures is detailed as the role played by lenders to support women in Latin America through technology continues to be explored.

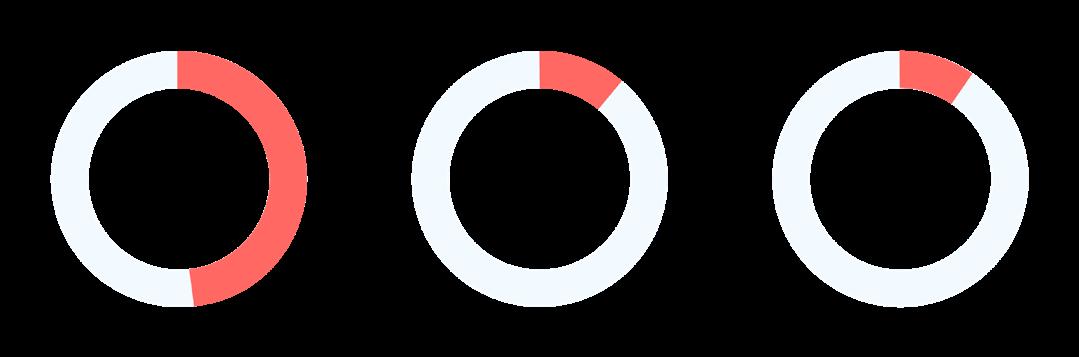

The figures point towards inequality when it comes to financing and women: “In Latin America and the Caribbean (LAC), according to the World Bank, only 49% of women have a bank account, 11% save and 10% have credit.”

This data was presented at the XIV Meeting of the Regional Conference on Women in Latin America and the Caribbean in 2019, and has been further exacerbated by the pandemic.

Alicia Bárcena, executive secretary of the Economic Commission for Latin America and the Caribbean (ECLAC), recognized that the reduction of 9.1% in Gross Domestic Product (GDP) in the region shows the precariousness of employment, and that women are the most affected by representing 56% of informal employment.

In fact, the pandemic represents a setback of more than 10 years in the participation of women in the labor market. It is important to add that “women work up to double or triple in their homes and this is also due to the suspension of classes that places additional burdens on women.” Furthermore, “the costs of health care have been transferred to households and the insufficient supply of health services, or fragmentation, has multiplied the dedication of women to care.”

María Noel Vaeza, regional director of UN Women, has explained in different forums that women are marked by stereotypes such as being a mother. This reality prevents them from having equal access, in a 70% / 30% ratio in favor of men. The reality is that 96% of women are compliant and have their credits up to date. “Investing in gender is good business,” she says.

formal companies owned by women, and Latin America is the region with the largest gap: $85,638 million.

Assessing female-led businesses differently to provide them better credit alternatives would be a response to the reactivation of the economy. “Studies indicate that there would be a growth of 26% of GDP if women are allowed to enter the economy and barriers are broken” such as financing.

The International Finance Corporation (IFC) has estimated that worldwide there is a gap of $287,000 million for financing small and medium-sized

According to ECLAC data, from 2014 to 2019 Mexican women increased their participation in funding by 14.4%, but there is still a significant gender gap, especially given the impact of the pandemic on SMEs. The size of Mexico’s potential SME lending market is estimated at more than $100 billion (McKinsey Global Institute). However, the current market is below $45 billion.

More and more women are participating in high-impact businesses or technology, but in general, they continue to focus on traditional and local models (economic kitchens, commerce). This is due to psychosocial circumstances (such as traditional education in the region) and the lack of more investment funds focused on women.

It should be noted that one phenomenon that has been highlighted in recent months due to the pandemic is that of the “nenis”, micro-businesses that sell through social networks. According to UNAM, these sellers generate 9 million pesos per day in the country.

There are many initiatives to boost entrepreneurs, such as accelerators, hackathons, incubators and support networks, but a more concerted effort is needed in education to have more presence in STEM areas and have more female tech entrepreneurs. For this it is essential to establish more and better mentoring networks.

Women tend to be better credit payers (according to ASEM), but they tend to ask for it less because they are less open to risk than men. In the country, of 100 female entrepreneurs applying for a credit, 99 liquidate it. However, 70% of women-led SMEs do not receive these loans.

70% of women-led SMEs don’t receive loans

Equity will be achieved when we understand that women face different expectations than men and therefore require specialized instruments.

According to HSBC’s “She is the Business”:

• Women get 5% less capital than enterprising men.

• The biggest concern of female entrepreneurs in getting investment is being denied for being a woman. The second biggest fear is an inadequate business plan.

• Discrimination can be avoided with the help of investors through periodic reviews of their investment options and the creation of mixed investor groups.

• Female entrepreneurs believe that having access to business networks can help them facilitate relationships and connections to expand their businesses.

• Female entrepreneurs would like greater clarity on the specific investment criteria to be included in the submission of proposals and greater transparency throughout the investment process.

and it affects women more than men. The difficulties begin in communications with the bank manager or professional responsible for analysis and credit granting.

According to the accounts of women entrepreneurs in various reports in the press, the approach in this context usually includes questions about marital status, whether they have children, age of the children, whether they are responsible for managing the house, whether someone takes care of their children while they are working – questions not normally asked

of male credit applicants. This happens because women have a “double shift,” but also double capacity to withstand this challenge.

There is no doubt that this double shift affects the businesses led by women. A survey carried out by Rede Mulher Empreendedora (RME) and by Instituto Locomotiva to entrepreneurial women during the pandemic confirmed this, revealing that 80% of domestic care is still the responsibility of women. They often suffered from reduced earnings with their businesses in a difficult place, along with children at home and household chores, and all this has an impact on the business.

The same survey shows that the crisis interrupted activities for 39% of the businesses they command. Another

80%

47% managed to continue but are struggling to stay afloat. If they had access to credit, many would have been able to save their businesses.

When there is a need to create special lines of credit for women, it is because, in fact, there are restrictions on the granting of credit to women. The situation is discriminatory, but the market is beginning to open with opportunities, such as the one recently offered by Banco da Mulher Paranaense.

The institution has launched the Banco da Mulher Paranaense program, which aims to stimulate female entrepreneurship in the state, with lower interest rates to support. The credit may be accessed by industrial, commercial, or service undertakings that have the participation of women as owners or partners. It is a positive step, but we need more – to sit at the negotiating table to obtain credit with true gender equality.

As the “fintech revolution” continues to spread throughout Latin America along with ever-rising internet and smartphone usage, there will be more options for women to receive credit when they previously would not have been able to. In this way, technology is a catalyst for financial inclusion, especially for those who have been historically excluded economically.

Considering the sheer size of the SME sector in the region, entrepreneurs in this vertical have the potential to benefit the most from modern technologies. And institutions can support women entrepreneurs in particular, as they can significantly contribute to society with new ideas and innovations if given the opportunity, as has been seen in many instances.

By adopting risk decisioning technology such as Provenir’s Cloud Suite, financial institutions and lenders can quickly and accurately assess credit risk for both personal and business loans and establish specific criteria to assess women’s creditworthiness more adequately.

The use of alternative data to assess credit risk is a trend that has continued to gain momentum recently, and it will play a key role in granting credit to those who would not have traditionally been considered creditworthy. As big data and machine learning continue to advance, it will become increasingly simple and reliable to make risk decisions with the appropriate insights.

Technology’s pervasiveness in today’s corporate environment greatly boosts firms’ ability to leverage new data streams in order to improve organizational performance and outcomes. The no-code, cloud-native SaaS technologies from Provenir make it easy to quickly design, deploy and iterate risk decisioning workflows. Provenir has turbocharged decisioning speed with a global data marketplace for seamless data integration, real-time analytics and insights, and sophisticated AI and machine learning models.

The potential societal benefits of greater economic inclusion and opportunities for women are clear. It is now up to institutions to adopt the right technology to support them in order to allow for more innovations and business opportunities, modernize the lending landscape and close the gender gap in Latin America.

Want to know more about how Provenir’s cloud-native data, decisioning and analytics solution can help you tap into this market opportunity? Visit us at www.provenir.com/possibilities.