Other County staff whose contributions made this document possible:

Carolyn Ascheman, Aushmyr Greenhouse,

Paula Manning, Janet Pierce, Kyle Schmidtke

Budget Document Overview

The beginning of this document includes the Adopting Ordinance, followed by the General Overview and the Financial Overview. These sections provide a comprehensive review of the Pierce County 2026-27 Biennial Budget, including the policies, process, strategic plan, and assumptions utilized to craft the budget.

Between the Financial Overview and the Appendix is a detailed presentation of all the individual budgets. These individual budget sections have been grouped into ten main organizational or functional categories: General Government, Finance, Public Safety, Legal and Judicial, Parks and Recreation, Human Services, Planning and Public Works, Facilities Management, Health Services, and Capital Improvement Program.

The Appendix contains a Glossary of Terms, Abbreviations, and Workload and Performance Data.

For additional information contact: Pierce County Finance Department

1501 Market Street, Suite 420 Tacoma, WA 98402

Email: budget@piercecountywa.gov

Website: www.piercecountywa.gov/budget

Distinguished Budget Award

The Government Finance Officers Association of the United States and Canada (GFOA) presented a Distinguished Budget Presentation Award to Pierce County, Washington for its biennial budget for the period January 1, 2024 through December 31, 2025. In order to receive this award, a governmental unit must publish a budget document that meets program criteria as a policy document, as an operations guide, as a financial plan, and as a communications device. Pierce County also received Special Strategic Goals and Strategies recognition.

This award is valid for one budget period only. We believe our current budget continues to conform to program requirements, and we are submitting it to the GFOA to determine its eligibility for another award.

This page is intentionally left blank.

Adopting Ordinance

This section is intentionally left blank. The ordinance will be inserted upon adoption by the Pierce County Council.

Executive’s Message

To the people of Pierce County:

I’m pleased to submit my first biennial budget to the Pierce County Councilmembers for their review, revision and final approval.

As Pierce County moves forward under the banner of “Forward Together,” our focus remains steadfast on building communities that are safe, welcoming and connected. At the same time, we must be cognizant of the very strong economic headwinds and uncertainties we face.

The County continues working with legislators and departments to prevent a future deficit as costs have outpaced revenue in recent years. Despite lean staffing and cost-cutting measures — including a hiring freeze and limits on out-of-state travel — expenses still exceed revenue growth.

This budget proposal reflects the economic uncertainties we are facing:

• Limited revenue streams that don’t keep pace with costs

• End of COVID-19 pandemic funding sources

• Federal budget cuts and grant losses or rescissions

• Recent state laws that are costly to implement

• State budget challenges

I believe this budget allows us to responsibly navigate these uncertainties while we continue working with legislators and departments on the structural deficit. When developing this budget, our guiding principles were to minimize legal risk, fulfill essential obligations, keep vulnerable people safe, and make progress on our strategic priorities.

Our top strategic priority is building safe communities for everyone. Pierce County’s General Fund is overwhelmingly dedicated to public safety and justice. The Sheriff’s Office receives the single largest share (about 42% or approximately $380M). When combined with the Prosecuting Attorney’s Office, Assigned Counsel, Juvenile and Superior Courts, District Court, Emergency Management, and related services, more than 77% of the General Fund supports public safety and criminal justice services.

Looking ahead, the next two years will be a period of collaboration, partnership and progress as we work together to:

• Build more affordable housing. Pierce County needs about 5,700 additional units per year to keep up with growth, and about half of those need to be affordable for people with lower and modest incomes.

• Continue expanding behavioral health and detox services, such as our new mobile units and 10-day treatment options. We want every resident to have access to treatment and recovery resources if and where they need it.

• Reduce crime with proven strategies for lowering recidivism, providing young people more access to out-of-school programs, and finding sustainable funding for law enforcement and the justice system.

• Advance Vision Zero projects, making lifesaving safety improvements to county roads and infrastructure so that everyone arrives home safe at the end of the day.

We also remain committed to supporting our hard-working employees and bringing new job opportunities to the families of Pierce County. Within County offices and along cities’ and towns’ main streets and squares, I meet people every day whose dedication and passion for their work make Pierce County such a special place. Investing in our people and communities helps us all feel proud to call this home.

Particularly during these financial challenges, engagement with our residents remains a cornerstone of our administration. Through surveys, boards and commissions, roundtables, constituent messages and more, we seriously consider input from the people most likely to be affected by the decisions we make. This ongoing collaboration and partnership is at the heart of our “Forward Together” approach.

Together, we are building a region where opportunity, compassion, and safety are shared by all. I thank the County Council, our staff, community partners, and residents for your trust and collaboration in this journey.

Sincerely,

Ryan N. Mello Pierce County Executive

Budget Summary Highlights

Pierce County’s vision is simple but powerful: a place people are proud to call home. Our mission — Forward Together: Building communities that are safe, welcoming, and connected — guides every decision we make and every dollar we spend. Together with our values of Collaboration, Integrity, Excellence, and Transparency, this mission shapes the 2026–27 biennial budget and the 14 strategic objectives that direct our work.

These objectives are organized around three key priorities: communities that are safe for all, an economy that works for everyone, and effective, welcoming, and responsive services. This budget invests in the programs, services, and infrastructure that bring these priorities to life while recognizing the economic challenges ahead.

Communities that are safe for all

When we talk about safe communities, we mean “safe” in the broadest meaning possible. Of course, this means law and justice systems that are effective and fair. But it also means safe roads, sidewalks, parks and trails. It means safe housing that people can afford. Air and water that’s clean and healthy. Access to behavioral health services if and when a loved one needs them. Programs that keep our kids safe and help them thrive.

This work makes up more than 76% of the total County budget. More than $2.8 billion of the nearly $3.5 billion total biennial budget is dedicated to work that ensures communities that are safe, clean, just, healthy and livable.

Within the County’s General Fund, about 76% directly supports law enforcement, courts, and related justice system programs. These are the areas with the largest increases in 2026-27 General Fund spending.

Investments designed to foster communities that are safe for all include:

• Sheriff’s Office Staffing: Fill 76 vacancies and continue hiring incentives.

• Special Team Pay: Increase compensation for SWAT and Swiftwater Rescue teams.

• Facility Upgrades: Fund design work for aging justice facilities like the County Jail and Remann Hall.

• Legal Support: Add 19 positions in Assigned Counsel to meet new caseload standards, plus two County Attorneys and 17 continuing positions in the Prosecutor’s Office for tort claims, complex litigation, and Supreme Court rulings.

• Juvenile Services: Continue mental health and family support for justice-involved youth.

• Blight Response: Support code enforcement handling 3,500+ reports of dumping and nuisance issues.

• Aging Services: Expand Aging & Disability Resources and increase funding for Senior Centers.

• Shoreline Protection: Enhance the Shoreline Master Program to address sea level rise and storm impacts.

• Urban Forestry: Launch a Tree Canopy Program in Parkland to mitigate extreme heat.

An economy that works for everyone

In a place where the economy works for everyone, residents can reach their full potential and make meaningful contributions to their community.

American Rescue Plan Act (ARPA) funds provided $26.2M to support the economy through programs including the Small Business Accelerator, Community Navigator, Small Business Safety and Security Grants, Small Business Grants, Innovation Grants, and Workforce Development Internships and Upskilling. In total, 2,208 small businesses received relief grants, 259 received safety and security grants, 578 completed accelerator training and grants, and 1,650 businesses were visited by community navigators.

Although ARPA funds are winding down, the 202627 budget still provides funding for young adult internships and employment opportunities.

Pierce County is committed to hiring highly qualified employees, supporting our employees to do their best work, and providing excellent customer service, with a focus on increasing accessibility for residents.

Priority areas that provide the foundation for this work include accountability and good governance, regional leadership, tribal partnerships, hiring and maintaining a talented workforce in a welcoming environment, and customer-focused services.

In addition, the County is prioritizing modest investments to maintain or improve some of the back-end systems that allow employees to efficiently and reliably do their work.

Investments over the next biennium that will advance this work include:

• Continuing the taxation software replacement project in the Assessor-Treasurer’s Office

• Digitizing decades of paper records in the Clerk of the Superior Court’s Office

• Improving the sewer billing system

• Implementing a Contract Lifecycle Management system

• Modernizing the County’s website to improve access and make it more user-friendly

Looking Ahead

While this budget makes significant investments in the priorities residents value most, Pierce County continues to face a structural deficit. Despite lean staffing and cost-cutting measures, including restrictions on out-of-state travel, the cost of salaries, benefits, and core services continues to grow faster than property and sales tax revenues — the County’s two primary funding sources

The 2026–27 budget maintains reserves through 2029, but projections show those reserves will fall below recommended levels in later years. Without new, stable funding sources, the County will face difficult tradeoffs that could affect public safety, courts, and essential services. This budget reflects both optimism and realism — optimism about the investments that will make Pierce County safer, healthier, and more connected, and realism about the fiscal challenges we must work together to solve.

Open Pierce County lets residents track progress, budgets, and services with transparency. Open.PierceCountyWa.Gov

Community Engagement

The Proposed 2026–27 Biennial Budget was shaped by a communityinformed process deeply rooted in access to opportunity, transparency, and responsiveness. Since taking office on January 1, 2025, Executive Ryan Mello has sought varying perspectives and input from the people most likely to be affected by the County’s decisions and actions. Rather than conducting a standalone budget engagement survey, the Executive’s Office embedded community engagement into the daily work of governance.

Throughout 2025, the Executive and his team conducted district tours, site visits, and roundtable discussions with mayors, city councilmembers, nonprofit leaders, educators, business owners, law enforcement, and residents. These conversations offered a place-based understanding of the challenges and opportunities facing Pierce County communities—from housing and public safety to behavioral health, infrastructure, and economic development.

To complement these in-person meetings, the County also analyzed results from the 2025 Pierce County Resident Perception Survey. This statistically valid survey captured a broad cross-section of resident perspectives and priorities. Top concerns included housing affordability, crime, mental health and substance use treatment, job creation, and traffic congestion. Residents expressed a strong desire for visible improvements in safety, affordability, and access to services, along with greater transparency and responsiveness from government.

These insights directly informed the Executive’s budget priorities, including investments in behavioral health, housing, youth services, infrastructure, and economic opportunity.

General Fund

The County’s General Fund receives undesignated revenues, which can be budgeted for any appropriate County purpose. This fund finances many of the traditional services associated with County government.

A. GENERAL FUND REVENUES

A detailed listing of General Fund revenues is presented in the Financial Overview section of this budget document. A summary of the 2026-27 revenues, with a comparison to the 2024-25 biennial budget, is shown in the table below.

Moderate growth in tax collections, increased charges for services, and one-time transfers provide for a 2.7% increase in General Fund revenues. Though revenues are moderately increasing, rising costs continue to outpace revenue growth. The budget includes the planned use of $33.9 million in fund balance reserves.

General Fund Revenue Summary

The 2026–27 revenue forecast is built on the following key economic assumptions:

1. Retail Spending: Retail activity is expected to remain subdued as slower income growth and rising prices constrain household spending, with tariffs and weak consumer confidence presenting additional risks to the forecast.

2. Housing Market Outlook: The housing market remains under pressure from high interest rates, elevated inventories, and increasing construction costs, though anticipated rate cuts in late 2025 and 2026 may bring a temporary rebound in construction and real estate activity.

3. New Construction Trends: New housing starts are projected to decline through 2025 and 2026, limiting broader economic momentum, though modest gains in new construction will contribute incremental property

4. Interest Rate Environment: The Federal Reserve began reducing interest rates in September 2025, earlier than previously expected, providing some relief to borrowing costs and housing-related activity.

5. Unemployment: Higher forecasted unemployment in Pierce County is expected to dampen consumer spending, resulting in slower sales tax growth and increased

uncertainty for the 2026–27 biennium.

The following summarizes the changes in each major category of revenue:

• Property Tax collections are projected to increase by 4.3%, or $14.4 million, from the 2024-25 biennial budget. Projected growth above 2025 actuals is 2.6% each year. This level is based upon the 1.0% increase available under state law and growth from new construction and improvements.

• Sales Tax revenue is projected to increase by 6.6%, or $17.8 million, from the 2024-25 biennial budget. Sales tax collections in 2025 are anticipated to come in 4.4% below budget. Projected growth above 2025 actuals is 2.8% in 2026 and 3.0% in 2027. An additional $16.7 million in collections is anticipated in 2026-27, based on new revenue from the implementation of SB 5814, which expanded taxable services and removed certain exemptions.

• License and Permit revenues are projected to decrease by $1.9 million, or 17.7% due to declining cable tax revenues as customers shift to non-cable services.

• Intergovernmental Revenues are projected to decrease by $4.2 million, or 7.1%. Revenues reflect anticipated grant funding in 2026-27.

• Charges for Services are estimated to be 13.9%, or $16.8 million, above 2024-25. This change reflects higher public safety revenues and increased document recording fees attributed to HB 1858, which removed exemptions from certain real estate and lending-related filings.

• Court Fine and Penalty Revenue is projected to be 26.1%, or $1.2 million, above the 202425 biennial budget. This change reflects an increase in the volume of civil infraction penalties.

• Miscellaneous Revenues are projected to decline by $1.6 million, or 2.5%, in 2026-27 due to lower projected interest earnings.

Comparative revenue changes for the last four budget periods are shown in Figure 1. The figures below exclude the budgeted use of fund balance. The increase of 32.4% in 2020-21 is largely attributed to the receipt of federal pandemic relief funding. Revenue growth in 2026–27 is expected to be slower than in 2024–25.

Figure 1: Percent Change in General Fund Revenues

B. GENERAL FUND EXPENDITURES

The 2026–27 General Fund expenditure budget is $25.6 million, or 2.7%, higher than the 2024–25 level. This moderate growth reflects the removal of one-time contingency funding provided in 2025 to address federal funding risks. When excluding that one-time funding, General Fund expenditures increase by $54 million, or 6%.

To balance rising costs against slower revenue growth, the budget applies a 1%–7% annual vacancy rate adjustment to General Fund appropriations, generating $18 million in savings. These resources are reallocated to support public safety, criminal justice, and other core general government services.

Departmental appropriations, with the exception of the Sheriff’s Office, do not reflect the full cost of operations, as funding for non-interest arbitration bargaining is held in reserve within the Miscellaneous Current Expense budget.

As in prior budgets, Public Safety and Legal and Judicial functions remain the largest share of General Fund spending in 2026–27, comprising 75.5% of the total budget.

General Fund Expenditures by Department

C. FUND BALANCE

Figures 2 and 3 present the financial results for the General Fund for the 2016-17 to 202223 period, the estimated amount for 2024-25, and the budget for 2026-27. In prior years, a strong economy, favorable revenues, and under-expenditures due to vacancies resulted in an increase in the unassigned fund balance. Looking forward, rising costs and slowing revenues are projected to reduce the unassigned fund balance.

Based on estimated revenues and expenditures, the unassigned General Fund balance is projected to be $185.5 million at the end of 2025 (see Figure 3). The 2026-27 biennial budget assumes $33.9 million in use of fund balance. The 2027 unassigned General Fund balance is projected to be $151.6 million.

It is the County’s policy to maintain a fund balance of at least 10% of the upcoming year’s General Fund budgeted expenditures with a long-term goal of 15%. A minimum of 10% is needed to maintain cash flow. The County has been able to maintain a level higher than 15% since 2016-17 and expects to be at 29.9% at the end of 2027 (see Figure 4). This level enables the County to continue providing essential services should the region confront an economic downturn.

Figure 2: Difference Between General Fund Revenues and Expenditures

Figure 3: Unassigned General Fund Balance

Figure 4: Unassigned General Fund Balance as a Percent of the Budget

D. OUTLOOK FOR 2026-27

The County uses an interactive risk model to evaluate how budget decisions affect revenues, expenditures, and unassigned fund balance over time. This tool provides a six-year outlook that supports long-range financial planning, giving County leaders a clear picture of the fiscal impact of resource allocation decisions before they are made.

The model incorporates a wide range of economic factors and external influences, including changes in property and sales tax collections, intergovernmental revenues, service charges, fines, licenses and permits, as well as growth in salaries, benefits, and operating costs such as supplies and services. As part of each biennial budget cycle, revenue and expenditure assumptions are extended four years beyond the biennium, allowing the County to anticipate and prepare for emerging fiscal challenges.

Unassigned fund balance is a critical measure of financial stability. County policy requires maintaining a fund balance equal to at least 10% of the upcoming year’s General Fund budgeted expenditures, with a long-term goal of reaching 15%. Maintaining a reserve at or above this level ensures the County can continue essential services during periods of economic slowdown or fiscal stress. The risk model helps policymakers monitor compliance with this policy and signals when corrective actions may be necessary to sustain reserves at prudent levels.

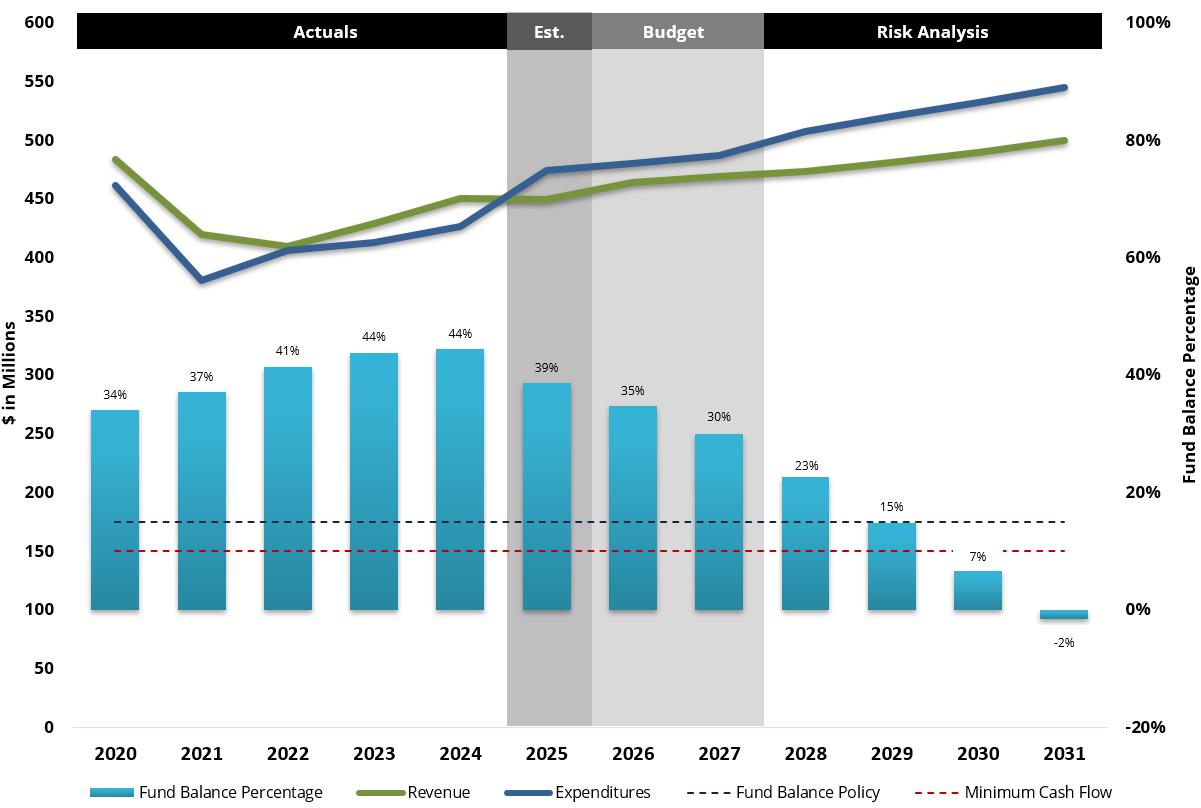

Risk model assumptions for the six-year period from 2026 through 2031 include:

1. Property tax revenue increases by 2.6% per year.

2. Sales tax revenue increases of 2.8% in 2026, 3.0% in 2027, and a long-term average annual increase of 4.0% per year through 2031.

3. Interest earnings stabilize at a lower level consistent with history.

4. Compensation increases between 2.0% and 3.0% per year based on employee group.

5. Employer-paid medical cost increases by 5% per year.

6. State retirement contribution rates remain stable.

Figure 5: Executive Proposed Budget Risk Model Results

The County continues to face a structural budget deficit, as revenue growth lags behind rising costs. The Executive Proposed General Fund budget for 2026–27 maintains reserves above 15% through 2029, as shown in Figure 5. However, projections indicate that without new, stable funding sources or reductions to essential services, reserves will fall below policy levels in future biennia.

In response to rising operational costs and slower long-term revenue growth, the proposed 2026–27 biennial budget applies targeted reductions of 1%–7% per year to departmental General Fund personnel budgets, consistent with historical vacancy trends. The resulting $18 million in savings are reallocated to priority programs and services, with an emphasis on maintaining critical public safety, legal, and judicial functions. This approach helps the County balance near-term budget pressures while positioning itself to thoughtfully address long-term financial sustainability.

Property and sales taxes are projected to grow at moderate levels during the 2026-27 Biennium. The regional economic outlook anticipates minimal growth amid continued uncertainty, with 2025 sales tax collections projected to finish 4.4% below budget. Sales tax revenues are partially strengthened in the new biennium by the passage of SB 5814, which broadens the base of taxable services and eliminates certain exemptions.

While current fund balance levels are sufficient to sustain County services through 2026–27, maintaining service levels will require adjustments to future spending. The County will need to explore options to continue to provide critical support for sustaining vital public safety and justice system functions in the years ahead.

Taken together, these factors underscore the need for disciplined fiscal management in the 2026–27 Biennium. While the County maintains a strong near-term position—with reserves above policy thresholds, targeted vacancy savings, and modest revenue growth—the long-term outlook remains uncertain. Moderate revenue growth, rising service demands, and ongoing economic uncertainty will continue to challenge the County’s financial position. By leveraging the risk model, adhering to fund balance policies, and strategically reallocating resources, the County is well positioned to sustain essential services in the near term while preparing for more significant adjustments in future biennia.

Other County Funds

Many of the County’s programs are financed from sources outside of the General Fund. These funds have combined expenditures well in excess of the General Fund budget. However, the nature of the revenue sources mandates that these monies can only be used for specific activities. Hence, they are budgeted and accounted for in separate funds. Summary figures for all funds can be found in the Financial Overview section along with detailed information in the individual budget sections.

A. Human Services

The Human Services Department is the County’s major provider of community and social services programs, funded primarily by state and federal grants, recording fees, and sales tax. Due to changes in state and federal grant funding levels, these budgets can vary significantly from year to year. The budgets reflect the following significant changes from 2024-25:

• An overall 5.5% growth in Human Services programs.

• An increase in document recording fees due to the implementation of HB 1858, which eliminates certain exemptions in the state’s document recording fee structure.

• A 37.6% increase in Housing and Related Services to support affordable housing due to the reappropriation of funding from the prior year to complete projects.

• Investments in the County’s Aging and Disability Resources and Developmental Disabilities programs within the Human Services Fund.

• The receipt of additional opioid settlement funds to support opioid prevention, intervention, and treatment services.

B. Transportation Services

The Planning and Public Works Department has major transportation responsibilities, which are supported by a variety of funds. The 2026-27 program budgets, with comparisons to 2024-25, are shown in the table to the right. The following items summarize the significant changes from 2024-25:

• An overall increase of 10.4% for transportation services based on available revenues and the planned use of fund balances.

• Increases in the Airport and Ferry Services funds to support capital projects.

• Reappropriation of fund balance from the Second REET Roads Fund and the Traffic Impact Fee Fund to support capital projects carried forward from 2024-25. Second REET and impact fee

are expected to modestly increase in 2026-27.

C. Parks and Recreation

Parks and Recreation Services are supported by several County funds, including $24.3 million from the General Fund in 2026-27. The 2026-27 biennial budgets for these funds are shown to the right and reflect the following significant changes from 2024-25:

• An overall decrease of 0.5% based on the slowing of sales tax growth, impact fees, and Second REET revenues and a reduction of fund balance for capital projects.

by Fund

• An increase in the Chambers Creek Regional Park budget to support higher rounds of golf and expanded recreation programming.

• The consolidation of the Paths and Trails Construction Fund into the Parks Construction Fund to account for capital improvements in the trail system and park facilities in one fund.

• An increase in the Second REET Parks budget based on actuals performing higher-than-budgeted in 2024-25. Additional revenue is used to support capital projects.

D. Environmental Services

The Planning and Public Works Department has seven funds that address environmental issues. These funds and budgets are listed to the right. The budgets reflect the following significant changes from 2024-25:

• An overall increase of 15.2% to support environmental programs and services.

Expenditures by Fund

• A 10.6% increase in the Blighted Property Maintenance Fund due to an additional transfer from the General Fund for nuisance property cleanup.

• Increases in the Surface Water Management and Surface Water Management Construction budgets for capital expenditures and operations.

• A 19.4% increase in the Sewer Utility Fund that includes $26.0 million in the use of fund balance to support operations and capital projects.

E. Internal Service Funds

Internal service funds provide services, supplies, and equipment to other County departments, which pay for these services through various billing systems. These funds operate under the enterprise fund business model, except that customers are internal departments. The goal is to establish rates that will pay for all operating and capital costs and to ensure that the General Fund does not subsidize these activities. Some of these internal service funds rely upon prior fund balances to support their 2026-27 biennial budgets. Significant changes include:

• An overall increase of 3.9% to provide services, supplies, and equipment countywide.

• An 11.9% increase in Fleet Rental due to an increase in the costs of vehicle replacements and materials in 2026-27.

• An increase in the General Services budget to support the digitization of the Clerk of the Superior Court’s records.

• An increase in Radio Communications attributed to the Three Sisters Radio project.

• A reduction in Self Insurance due to a higher level of claims in 2024-25.

Conclusion

The 2026-27 biennial budget supports the County’s priorities of public safety, criminal justice, homelessness, affordable housing, behavioral health services, sustainability, and parks and recreation programs.

A total biennial budget of $3.5 billion, and a General Fund biennial budget of $967.1 million, make strategic investments to create communities that are safe for all, foster an economy that works for everyone, and deliver effective, welcoming, and responsive services for the residents of Pierce County.

While an adequate fund balance is available to support County services through the 202627 Biennium, the County will closely manage its finances to ensure reserves meet the 15% fund balance minimum in future biennia.

An overview of the County’s strategic plan is included in the General Overview section, and additional details are available at Open.PierceCountyWA.gov

County Government Overview

The structure of government in the United States is divided into separate branches (legislative, executive, and judicial) and levels (federal, state, and local). Each branch and each level are partially independent of the others. Local government is further divided among general-purpose entities such as cities and counties, and special purpose districts such as schools, utilities, and fire districts, all working collaboratively to deliver services to the public.

A county is a political subdivision of the state. Counties derive their existence from state law and from powers expressly conferred by the state constitution and state laws. Counties act as agents of state government, performing functions such as collecting property taxes and appraising property values for tax purposes on behalf of the state.

Pierce County is a home rule county established by the people in 1980. The County has all the powers authorized under the state constitution and laws of the State of Washington for a home rule form of government. The Charter separated executive and legislative responsibilities by establishing the position of County Executive to serve as the chief executive officer and a seven-member County Council to serve as the legislative branch.

The County Executive supervises and manages administrative operations, presenting budgets and plans. The County Council, as the legislative body, holds the authority to adopt plans, levy taxes, and adopt budgets. Superior Court handles felonies, civil cases, and other matters, while District Court handles various cases, including traffic infractions and civil matters.

The executive branch is comprised of the County Executive and all executive departments established by the Charter or by ordinance. County executive departments include four elected positions (Assessor-Treasurer, Auditor, Prosecuting Attorney, and Sheriff), with other department directors appointed by the County Executive and confirmed by the County Council.

The County Council is the policy-setting body of the County and has all the powers of the County that are not otherwise reserved to the people, the County Executive, and general law. County Councilmembers are elected by the voters of seven districts in Pierce County. Legislative authority is exercised by the adoption and enactment of ordinances or resolutions.

According to the Charter, all executive departments are subject to the personnel, budgeting, expenditure, and any other policies of general application established by the County Executive. Responsibility of County finances is under the authority of the County Executive and the Finance Department.

The voters of Pierce County elect 43 officials, including 7 County Councilmembers, a County Executive, 23 Superior Court Judges, 8 District Court Judges, a Prosecuting Attorney, an Auditor, an Assessor-Treasurer, and a Sheriff.

Elected Officials

Legislative Branch | Pierce County Council

Jani Hitchen

7 Robyn Denson

District 1

Dave Morell

District 2

Paul Herrera

District 3

Amy Cruver

District 4

Rosie Ayala

District 5

Bryan Yambe District 6

Mello

Organizational Overview

The chart below provides a high-level organizational overview of Pierce County Government, including its branches and associated departments.

Funds by Department Organization Chart

Executive Departments

Departments with Dual Accountability

The following provides a list of the elected officials and departments by branch of government, and the appropriated funds that are managed by each. Pierce County produces other financial documents that include funds not appropriated in the biennial budget.

Legislative Branch

Council (Elected Officials)

Executive Branch

Executive (Elected Official)

• 911 System Fund

• Assessor-Treasurer (Elected Official)

• Assigned Counsel

• Auditor (Elected Official)

» Election Stabilization Fund

» Elections Equipment Replacement Fund

• Clerk of the Superior Court

» Pierce County Law Library Fund

• Communications

» Rainier Communications Commission Fund

• COVID-19 American Rescue Plan

• Criminal Justice Fund

• Economic Development

» 1% For Arts Construction Fund

» Tourism Promotion and Capital Facilities Fund

» Tourism Promotion Area Fund

• Emergency Communications Sales Tax SS911 Fund

Executive Branch (Cont.)

• Emergency Management

» Emergency Communications Network Fund

» Emergency Management Grants Fund

» Radio Communications Fund

• Facilities Management

» Capital Improvement Projects Fund

» Clear Zone Land Acquisition Fund

» Government Services Capital Fund

» REET Capital Improvement Fund

• Finance

» Auditor’s Maintenance and Operations Fund

» Finance and Performance Management

» Fleet Rental Fund

» General Services Fund

» Information Technology Fund

» Medical Self Insurance Fund

» REET Electronic Technology Fund

» Self Insurance Fund

» Workers Compensation Fund

• Health Services

• Human Resources

• Human Services

» Affordable and Supportive Housing Fund

» Affordable Housing Document Recording Fee Fund

» Behavioral Health and Therapeutic Courts Fund

» Behavioral Health Partnership Fund

» Community Action Fund

» Community Development Fund

» Homeless Document Recording Fee Fund

» Housing and Homeless Fund

» Housing and Related Services Fund

» Human Services Fund

» Opioid Settlement Fund

» Prevention Services and Programs

» Taxpayer Accountability Fund

» Veterans Relief Fund

» WSU Pierce County Extension

• Judson Family Justice Center Fund

• Limited Tax G.O. Bond Redemption Fund

• Medical Examiner

• Miscellaneous Current Expense

• Parks and Recreation

» Chambers Creek Regional Park Fund

» Conservation Futures Fund

Judicial Branch

Superior Court (Elected Judges)

• Juvenile Court

District Court (Elected Judges)

• Dispute Resolution Center Fund

» Golf Courses Fund

» Parks Construction Fund

» Parks Impact Fee Fund

» Parks Sales Tax Fund

» Paths and Trails Construction Fund

» Paths and Trails Fund

» Pierce County Fair Fund

» Second REET Parks Fund

• Planning and Public Works

» Airport Fund

» Blighted Property Maintenance Fund

» Building and Development Fund

» Conservation Futures Capital Fund

» County Road Fund

» Equipment Rental and Revolving Fund

» Ferry Services Fund

» Historical Preservation and Programs Fund

» In-Lieu Fee Wetlands Mitigation Program Fund

» Planning and Code Enforcement

» Public Works Construction Fund

» Second REET Roads Fund

» Sewer Revenue Bonds Fund

» Sewer Utility Fund

» Sewer Utility Construction/Reserve/Preservation Fund

» Solid Waste Management Fund

» Surface Water Management Fund

» Surface Water Management Construction Fund

» Traffic Impact Fee Fund

» Transportation Facilities Fund

» Water Utility Fund

• Prosecuting Attorney (Elected Official)

• Real Estate Excise Tax Fund

• Sheriff (Elected Official)

» Corrections Bureau

» Detention Center Commissary Fund

» Drug Enforcement Fund

» Drug Investigation Fund

» Federal Forest Services Fund

» Law Enforcement

» Marine Services Fund

• State Auditor

Strategic Planning and Performance Management

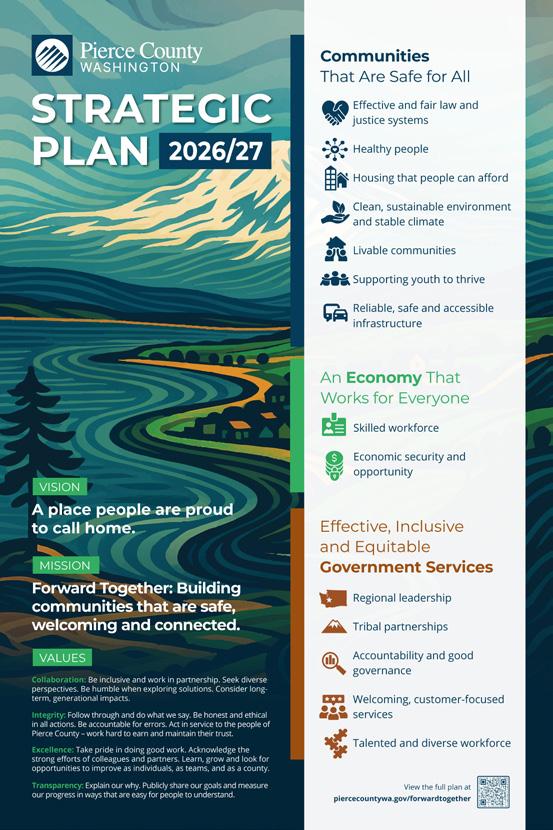

In 2025, Executive Mello led a countywide update of Pierce County’s Strategic Plan to reflect the needs and priorities of our residents. The plan sets a clear path for building communities that are safe, welcoming, and connected for everyone.

The Strategic Plan establishes priorities, aligns resources, and guides departments toward our vision of a place people are proud to call home. Organized into three priority areas with 14 objectives, it reflects our mission of Forward Together: Building communities that are safe, welcoming, and connected. Our values of Collaboration, Integrity, Excellence, and Transparency shape both what we do and how we serve.

Performance measures track progress on each objective, helping us improve services, allocate resources wisely, and remain accountable to residents. Open Pierce County, our interactive website, shares this information with the public, offering clear insight into performance, budgets, and spending.

Learn more at www.piercecountywa.gov/open

Communities that are safe for all

Bookings with charges filed

EFFECTIVE AND FAIR LAW AND JUSTICE SYSTEMS

People have confidence they are safe and that the justice system treats everyone equally and fairly.

Eligibility for pretrial release

Crime rate

Vacancy rates in the Sheriff's Office

Sheriff response time

Participation in diversion or alternatives to jail

Opioid overdose rate

HEALTHY PEOPLE

Residents are healthy across all zip codes and income levels.

Co-responder request response

10-day detox client count

Monitors the percentage of jail bookings leading to formal charges. Lower rates may waste resources and disrupt lives, especially for vulnerable populations. Tracking ensures fairer, more efficient use of County resources.

Measures how many individuals qualify for release before trial. High eligibility reflects fair risk assessment, balancing public safety with individual rights while reducing unnecessary incarceration.

Tracks overall community safety and quality of life. Lower crime rates suggest effective law enforcement, prevention programs, and community engagement.

Monitors staffing gaps that affect response times, community policing, and officer wellbeing. High vacancy rates strain staff and reduce public safety effectiveness.

Tracks the average response times emergencies. Faster responses save lives, prevent escalation, and build trust in public safety services.

Measures use of programs that address issues like substance abuse and mental health. Diversion can reduce recidivism, cuts costs, and provide positive interventions.

Tracks opioid-related deaths per 1,000 residents. Lower rates reflect effective prevention and treatment, guiding targeted investments in public health.

Measures how often mental health co-responder teams are deployed. High response rates improve crisis outcomes, reduce arrests, and support mental health equity.

Counts residents served in 10-day detox programs. Higher participation shows accessible treatment options that support recovery and reduce substance-related harms.

HOUSING PEOPLE CAN AFFORD

Everyone in Pierce County has a place to call home.

Communities that are safe for all (Cont.)

Affordable units constructed

New home starts

New lots created

Days to approve a residential building permit

People exiting homelessness successfully

Returns to homelessness

Water quality

Stream restoration

CLEAN, SUSTAINABLE ENVIRONMENT AND STABLE CLIMATE

Current and future generations enjoy clean air, clean water, and a healthy natural world.

Acres conserved by the County

Counts affordable housing units built or restored. More units prevent displacement, support workforce housing, and keep communities accessible.

Tracks new single-family homes built each year. Construction rates show housing supply, economic health, and ability to meet demand.

Measures new residential lots added annually. More lots expand capacity for future housing and support planned community growth.

Shows median days to approve residential permits. Faster approvals reduce costs and speed up needed housing development.

Counts individuals moving from homelessness to permanent housing. Higher rates show effective services restoring stability and reducing costs.

Tracks the share of people re-entering homelessness within a year. Lower rates reflect durable housing solutions and effective support.

Tracks the share of streams and lakes with above-average water quality. Clean water supports public health, ecosystems, and long-term sustainability.

Measures acres of streams restored. Restoration improves water quality, supports wildlife, reduces flooding, and creates recreation opportunities.

Counts total acres of land conserved. Conservation protects habitat, air and water quality, and open space for future generations.

LIVABLE COMMUNITIES

People of all ages and abilities feel connected to their community and the outdoors.

Utilization of Pierce County trail system

Access to recreational facilities and parks

County ADA projects on track for completion

Code/nuisance violations resolved

Tracks trail usage. Higher use shows successful investments in recreation, supporting health, quality of life, and sustainable transportation.

Measures how many residents live near a park and recreation facility. Better access supports health and community connections.

Shows ADA project completion rates. Timely progress ensures accessible public spaces and compliance with federal standards.

Tracks resolution of violations within 90 days. Quick action preserves safety, property values, and neighborhood livability.

SUPPORTING YOUTH TO THRIVE

Pierce County’s children and young adults are physically, mentally, and socially healthy.

Communities that are safe for all (Cont.)

Violence prevention program effectiveness

Juvenile Court diversion rate

Participation in County-funded outof-school enrichment programs

County roads in good or fair condition

Tracks participants who reduce risk of violence or re-offense. Effective programs address root causes, support youth, and build safer communities.

Measures how often juvenile cases are diverted from court. Higher rates reflect a focus on rehabilitation, preventing future offenses, and supporting youth well-being.

Counts youth in County-funded enrichment programs. Strong participation supports safe spaces, skill-building, and educational opportunities.

RELIABLE, SAFE AND ACCESSIBLE INFRASTRUCTURE

High quality, safe infrastructure makes it possible for every resident to connect to jobs, education, health care, and more.

Proximity to public transit

Wastewater connections per new home start

Serious injuries and fatalities on County roads

Tracks the share of County roads in good or fair shape. Well-maintained roads improve safety, reduce costs, and support access to jobs, healthcare, and education.

Measures how many residents live near bus stops, park-and-rides, or micro-transit. Better access reduces car reliance and connects people to opportunities.

Tracks wastewater hookups for new homes. Adequate connections protect health, support growth, and ensure essential services for new residents.

Measures roadway deaths and serious injuries. Lower numbers show effective safety improvements and safer travel for all residents.

An economy that works for everyone

Workers have access to affordable career-training and businesses have access to skilled employees.

Participation in County internship program

Tracks the number of participants in County internships. Participation reflects investment in workforce development, career pathways, and civic engagement. SKILLED WORKFORCE

People start and grow businesses here, and residents have sufficient income or resources to meet their basic needs and save for their future.

Changes in minority, veteran, and womenowned businesses

ECONOMIC SECURITY AND OPPORTUNITY

Days to approve a commercial building permit

Access to healthy food

Tracks the number of certified businesses. Growth strengthens the economy, creates jobs, and supports opportunities in our community.

Shows median days to approve commercial permits. Faster approvals support business growth, job creation, and timely development.

Measures residents living within 2 miles of healthy food retailers. Better access supports nutrition, community health and well-being.

ACCOUNTABILITY AND GOOD GOVERNANCE

Effective, welcoming, and responsive services

REGIONAL LEADERSHIP

Pierce County positively influences others in the region.

TRIBAL PARTNERSHIPS

We engage, consult, and partner with tribes to achieve mutually-beneficial outcomes.

Measurement and public transparency drive improved decisions, performance, and fiscal responsibility.

Ending general fund balance percentage

Proportion of Open Pierce County datasets updated on time

Average procurement processing time

Shows the share of unspent General Fund dollars. Healthy balances ensure stability, protect services, and demonstrate responsible fiscal management.

Tracks how often open datasets are updated as scheduled. Timely updates support transparency, accountability, and public trust.

Measures average days to complete procurement. Faster processing improves efficiency, reduces costs, and supports timely project delivery.

WELCOMING, CUSTOMERFOCUSED SERVICES

Our high-quality services address the needs of our customers while responsibly stewarding County resources.

Measures the share of projects with translation. Higher rates help more residents access and understand information and services.

Shows the share of residents reporting no service barriers. Higher percentages reflect smoother, customer-focused service delivery.

TALENTED AND REPRESENTATIVE WORKFORCE

Our employees are productive, innovative, and reflect the communities we serve.

Vacancy rate

Employee satisfaction

Employee turnover rate

Employees receiving leadership training

Employee representation index

Tracks the share of unfilled County positions. Lower rates show effective recruitment, retention, and service capacity.

Measures employees satisfied with their work. Higher satisfaction supports retention, productivity, and service quality.

Shows the percentage of employees leaving the County. Lower turnover reflects stability, engagement, and cost savings.

Tracks staff participation in leadership programs. Higher rates build internal talent, succession planning, and management capacity.

Measures the range of employee backgrounds. Greater variety strengthens the County’s ability to reflect and serve the community.

Financial Planning

Importance of Financial Planning

The County as an institution has multiple partners, including residents, taxpayers, businesses, employees, and other governments. As a major institutional, economic, and service force in the region, it is important for the County to strengthen its relationships with its partners by adopting clear and comprehensive financial policies.

Pierce County is accountable to the public for the use of tax revenue. County resources should be used wisely to ensure adequate funding for the services, public facilities, and infrastructure necessary to meet the community’s present and future needs.

The 2026-27 Biennial Budget is intended to serve as the County’s financial plan to meet community needs, strategic objectives and established policies.

Fund Types

Governmental

• General Fund

• Special Revenue Funds

• Debt Service Funds

• Capital Projects Funds

• Custodial Funds

Proprietary

• Internal

•

Budget as a Financial Planning Document

Budgets serve a wide variety of purposes. They can serve as policy-making tools, management tools, planning tools, and communication devices. Ultimately, however, budgets are financial documents. The Budget Summary Highlights and Financial Overview section provides a snapshot of the overall financial condition of the County and of its financial plan for the 2026-27 Biennium. Other sections of the document present the budget in terms of services, programs, and organizational structures.

The 2026-27 biennial budget is a product of a strategic planning process that, through its statement of fiscal policies and budget objectives, provides a framework for funding decisions.

Financial Structure of Pierce County

Fund Accounting – Like most governmental entities, Pierce County organizes its finances on the basis of “funds.” A fund is a self-contained, independent financial entity with its own assets and liabilities. Each fund has its own balance sheet and, in effect, is treated as a separate “business” for accounting purposes.

The 2026-27 biennial budget includes expenditures for 82 funds, ranging from the General Fund ($967.1 million) to a small special revenue fund ($14,000). A description of each fund is provided later in this document.

Fund Types – Funds can be classified according to the accounting conventions which apply to them.

“Governmental” funds are governed by accounting standards developed specifically for government. “Proprietary” funds are controlled by the same accounting standards that apply to private business (for more detail on this distinction, see Basis of Accounting and Budgeting on the following page). Within these categories, there are seven fund types (listed on the left).

Governmental – The General Fund is the primary County operating fund and accounts for all general government financial resources, except those required to be accounted for in another fund type.

Special Revenue Funds are used to account for and report the proceeds of specific sources that are generally legally restricted to expenditure for specific purposes other than debt service or capital projects.

Debt Service Funds are used to account for the accumulation of resources for payment of principal and interest on County general obligation bonds.

Capital Projects Funds account for the acquisition, construction, and remodeling of major capital facilities and for major capital equipment purchases.

Custodial Funds are used to account for assets held in a trustee capacity or as an agent on behalf of others.

Proprietary – Internal Service Funds account for central services provided to County departments or agencies on a cost reimbursement basis. Centralized intragovernmental services include heavy equipment and vehicle acquisition and maintenance; information technology; operation of County facilities and communications systems; risk management; and general administrative services.

Enterprise Funds account for various business-type activities for which a fee is charged to external users for services such as sewer utilities, solid waste collection, ferry and airport operations, and public golf courses.

Basis of Accounting and Budgeting

The “basis of accounting” and “basis of budgeting” determine when revenues and expenditures are recognized for the purposes of financial reporting and budget control. Accounting on a “cash basis” means that revenues and expenditures are recorded when cash is actually received or paid out. This method is used by many small businesses, but it has limitations that make it unsuitable for larger, more complex organizations. Most large businesses employ “full accrual accounting,” in which revenues are recorded when earned (rather than when received), and expenditures are recognized when an obligation to pay is incurred (rather than when the payment is made). Capital expenses (the costs of acquiring tangible assets) are recognized over the life of the asset, not when the asset is purchased.

Governments typically employ a hybrid basis of accounting termed “modified accrual.” Under this system, revenues are recognized when the obligation to pay is incurred, for example when a bill is issued. However, capital expenditures are recognized at the time of the purchase. This means that governments may experience significant increases and decreases in total expenditures from year to year because

capital expenses tend to be large and unevenly timed. To help explain year-to-year expenditure trends, governments frequently report capital expenditures separately from operating costs in their budget documents.

Pierce County uses modified accrual accounting and budgeting for its governmental fund types, including the General Fund, special revenue funds, debt service funds, and capital project funds. For proprietary fund types, including enterprise funds and internal service funds, the County uses full accrual accounting and budgeting.

Accounting for Internal Transactions

One consequence of fund accounting is the existence of inter-fund transactions, including transfers, internal service payments, loans, and capital contributions. These transactions record the movement of money between County funds. Internal (inter-fund) transactions represent non-cash expenditures and non-cash revenue when the budget is viewed as a whole because no cash enters or leaves the County.

Internal transactions have the impact of increasing the apparent size of the County budget. The 2026-27 biennial budget, which totals $3.5 billion, includes $779 million of these internal transactions, or 22.5% of the budget. These transactions impact expenditure trends.

Washington State Budgeting Accounting and Reporting System

State law empowers the State Auditor to prescribe a uniform chart of accounts and a uniform budgeting, accounting, and reporting system for all local governments in Washington. This system is known as the Budget Accounting and Reporting System (BARS).

Part Two of Volume One of the BARS Manual pertains to budgeting and contains general principles of budgeting and detailed procedural guidelines. These principles and guidelines are reflected in the County’s budget process.

Budget Process

Under the County Council/County Executive form of government, the County must adhere to the following procedures in establishing the budget:

• At least 135 days prior to the end of the fiscal year, all agencies of the County government must submit to the County Executive information that is necessary to prepare the biennial budget. By County Executive request, all departments submit preliminary budget information to the Finance Department for initial departmental review. The Director and staff then evaluate the proposed budgets and present the information to the County Executive’s Office for budget decisions.

• At least 100 days prior to the end of the biennium, the County Executive must present to the County Council a recommended budget which includes all appropriation ordinances and proposed tax and revenue ordinances that are necessary to raise sufficient revenues to balance the budget.

• The budget includes all fund balances, revenues, and expenditures. It is also divided into categories, programs, projects, or objects of expense and shows the actual expenditures of the preceding biennial period, the estimated expenditures of the current biennial period, and the requested appropriations for the next biennial period. The expenditures included in the proposed biennial budget shall not exceed the estimated revenues, including carry-over fund balances.

• Prior to the adoption of the budget, the County Council holds a series of public hearings to consider the budget presented by the County Executive. Public comment on the budget is received at each meeting.

• At least 30 days prior to the end of the fiscal year, the County Council must adopt the appropriation and property tax ordinances for the next biennial period. The appropriation ordinances that the County Council adopts shall not exceed the estimated revenues of the County for the next biennial period for each fund, including available fund balances.

Budget Preparation Instructions

Prior to actual budget preparation, every department receives an instruction manual that incorporates the budget process calendar, special instructions, sample forms, timelines, and summaries of certain costs and/or rates that will impact each departmental budget. In addition to the instruction manual, meetings are held with Department Directors and key personnel to discuss the budget preparation process.

2026 - 27 Budget Calendar

April 1 - April 30, 2025

Department meetings with the County Executive and Finance to align on strategic spending priorities.

May 7

Base budgets and instructions released to departments.

June 5 – June 23

Departments submit budget proposals to Finance.

June 30

Capital Facilities Plan templates due back to the Finance Department.

July 1 – August 8

Budget meetings with the County Executive and Finance.

August 11 - September 19

Executive’s Proposed Budget is finalized and the budget book prepared.

September 23

Executive’s Proposed Budget is submitted to Council.

October

Council begins hearings on the budget and Capital Facilities Plan.

November

Council budget hearings conclude. Council considers amendments to the budget and votes to adopt the budget and Capital Facilities Plan.

Budget submittal due dates are staggered with the majority being submitted over a three-week period in June.

Budgetary Control

Budget Appropriation Control and Amendment Procedures

All appropriations lapse at the end of the biennium. Unspent funds for capital projects funds may be reappropriated until project completion. Legal budgetary control is maintained at the department level in the General Fund and at the fund level in all other funds. A budget increase or decrease to a fund (or to a department in the General Fund) must be approved by the County Council. However, budget transfers within a fund (or within a department in the General Fund) may be authorized by the County Executive.

State law RCW 36.40.250 designates that counties adopting a biennial budget must provide for a midbiennial budget review and modification for the second year of the budget cycle. For a request for increased expenditure authority to be considered, departments must show:

• There has been a substantial change in circumstances since the County Council adopted the biennial budget;

• There is a clear and convincing need for the proposed expenditure; and

• The object of the request cannot be reasonably accomplished within the department’s existing spending authority.

The Pierce County Charter requires the County Executive to provide the County Council with a quarterly report comparing budgeted revenues and expenditures to actual results. If actual revenues

fall short of projections, the Council may reduce appropriations as needed to ensure spending remains within available resources. In addition, the Council may adjust the budget by appropriating contingency funds, recognizing revenues received in excess of budgeted amounts, or allocating other legally available resources in the event of an emergency.

Throughout the biennium, departments actively monitor budgets to ensure proper control of expenditures. The budget monitoring system allows departments to regularly update revenue and expenditure projections, improving management of variances and their impacts. Finance also conducts ongoing reviews of budgeted versus actual expenditures, making transfers or adjustments as needed to maintain alignment with budgetary goals.

Encumbrances

Encumbrances are recorded at the time a commitment is made to purchase goods or services, providing an important tool for budgetary control. Encumbrances lapse at year-end, and any related expenditures must be charged against the following year’s operating budget.

Budget Position Control

The budget position control system works in coordination with the personnel and payroll system to track the status of every budgeted position. This integration ensures accurate monitoring of filled and vacant positions and preserves control over authorized staffing levels.

Fiscal Policies

The Pierce County Finance Department’s fiscal and budget policies, compiled below, set forth the basic framework for the overall fiscal management of the County. Operating independently of changing circumstances and conditions, these policies assist the decision-making process of the County Executive and the County Council. Most of the policies represent principles and practices that have guided the County in the past, helped maintain financial stability, and provided criteria for evaluating both current activities and proposals for future programs.

Budgetary Policies

• Present a complete financial plan for the budget period. The budget will be prepared as one comprehensive management and balanced financial plan, including operating requirements, financing requirements, and debt service funding.

• Provide estimates of all taxes to be collected for the budget period and all revenues derived from other sources.

• Prepare and present a budget in such a manner that it serves as a policy document, a financial plan, an operations guide, and a communication device to staff, public officials, and residents.

• Include quantifiable performance measures to be achieved within a defined time frame.

• The County shall adopt a balanced biennial budget which is defined as a budget where planned expenses do not exceed the amount of revenue or funding available in accordance with state law. The budget will be monitored regularly to identify changes in revenues and expenditures so that necessary balancing corrections can be made.

Fund Balance Policies

• The County shall retain a General Fund balance in accordance with Resolution No. R2011-96s, which calls for an unassigned fund balance of at least 10% of the upcoming year’s General Fund budgeted expenditures with a long-term goal of 15%.

• Fund Balance in the General Fund will be utilized to fund one-time activities such as, equipment outlay, capital construction, and one-time operational projects.

• The County shall retain reserves in all other funds (non-General Fund) to allow for adequate cash flow, support designated mandates, finance infrastructure needs, meet equipment replacement schedules, and comply with other minimum requirements as may be established specifically for each fund.

• The County shall, to the extent allowable, use available balances in the following order: Restricted, Committed, Assigned, and Unassigned.

Revenue Policies

• The County shall seek to maintain a diversified and stable revenue structure.

• The County shall calculate and consider the full cost of services provided when establishing user charges and service rates. Such charges and rates will be reviewed regularly.

• Grants and contracts shall be pursued only for those programs and activities that address recognized needs and are consistent with the County’s policies and scope of services.

• Billable revenues shall be processed in a timely manner to minimize negative cash flow impacts.

• One-time non-recurring revenues (from such items as asset sales, court settlements, and windfalls) should only be allocated for one-time projects or expenses.

• Revenues that are difficult to accurately predict shall be conservatively estimated to avoid serious budget adjustments later in the year if the budgeted revenues do not materialize.

Expenditure Policies

• The County shall strive to maintain current service delivery levels, especially for essential services, and improve priority services as finances permit.

• The County shall make every effort to minimize expenditure growth through the use of sound management techniques. Implementation of technological or process improvements is encouraged to reduce service costs without reducing service quality or quantity.

• Expenditure budget increases and reductions will be considered on a case-by-case basis.

• Expenditures shall be accounted for as necessary and appropriate to ensure adequate documentation for related revenue collections such as grant reimbursements, fee calculations, etc.

• Expenditure payments shall be processed within necessary timelines to avoid late fees and maximize positive cash flow.

• Capital budgets will be developed with the consideration of, and proactive planning for, the impact of capital spending upon the biennial operating budget.

• The County shall pursue partnerships with other entities to increase the quality and/or quantity of services and eliminate redundancies.

• Capital assets will be replaced on a costeffective and scheduled basis.

Debt Management Policies

• The County shall seek to maintain our current Aaa bond rating so our borrowing costs are minimized and our access to credit is assured.

• The County will issue long-term debt only for the purpose of acquiring land; acquiring or constructing capital assets or improvements; making major repairs or renovations to existing capital assets; acquiring capital equipment or systems whose life extends beyond one year; or refunding existing long-term debt.

• The County may issue short-term debt in anticipation of a subsequent definite source of revenues. Such definite revenue sources include, but are not limited to: approved grants; authorized but unsold long-term debt; taxes anticipated to be received later in the current fiscal year; and asset sales.

• Short-term debt should not have maturities greater than three years, should not be rolled over for a period greater than one year, and should not be issued solely upon speculation that interest rates will rise in the near future.

• If long-term debt is issued to finance capital improvement projects, to the maximum extent possible, it shall be only for those projects referenced in the County’s Capital Facilities Plan.

• Long-term debt will be issued for a period not to exceed the useful life of the projects or improvements financed but in no event beyond 30 years.

• The amount of non-voter approved General Obligation debt principal outstanding to be retired by the General Fund shall not exceed 1% of the County’s total assessed valuation.

• The ratio of annual non-voter approved General Fund Debt Service to the total General Fund budget should not exceed 5% in any fiscal year.

• Bond maturity schedules should be structured to achieve total debt service payments that are level or only slightly increasing over time.

• To the extent possible, given the unique nature of each bond issue, the County will attempt to issue bonds through a competitive bid sale.

• The County shall attempt to maintain a general obligation direct net debt per capita ratio, which is 90% or less of Moody’s Investor Service published median for counties of comparable size.

Budget Book Format

Departmental Summary - Provides a narrative description of major functions and responsibilities of the department or fund.

Budget Highlights - Outlines significant changes in the departmental or fund budget from the prior biennium. The narrative identifies anticipated reallocation of resources, staffing changes, and/or changes in revenues or expenditures.

Workload Service HighlightsMeasures reflect various workload figures and performance indices that quantify, to the extent possible, the demands placed upon the department or fund and the services that must be, or should be, provided. Where possible, unit cost figures are included in the data.

A full list of input/output measures and performance ratios is included in the Appendix. Performance ratios are quantitative metrics highlighting trends in resource growth versus service demands, with a ten-year average provided for context.

Performance Measures - Used to monitor actual results and outcomes, and identify any adjustments needed to service delivery or operations. Performance measures align with the County’s Strategic Plan objectives and are stated in specific terms so that achievement or non-achievement of the target is easily discernible. Performance measures are tracked on an annual basis and provide two years of actuals, an estimate for the current year, and a target for each year of the biennial budget.

Funding Sources - Displays summary revenue information for a department or fund. For General Fund departments, this table’s purpose is to indicate the extent to which specific revenue sources related to the department’s activity fully support that department’s programs, or whether General Fund support is needed to finance those expenditures. Funding Sources tables for funds other than the General Fund indicate the various revenue sources that finance that budget.

Information Technology (IT) oversees County technology, including procurement, management, and security. Revenue is collected from other Pierce County departments that utilize services.

• Client Technology Services supports servers, cybersecurity, hardware, and the IT Service Desk.

• Platform Services manages systems services, network services, and distributed systems.

• Software Development designs, develops, and maintains custom software and cloud systems, focusing on integration and security.

• Spatial Services handles the County’s geographic information system (GIS) and asset management system, providing map data to departments and the public.

• Applications and Project Management acquires and manages third-party software, offers project management for large system deployments, and coordinates with IT units.

• IT also manages project requests, technology services, and the IT cost allocation model.

Budget Highlights

The 2026-27 biennial budget for the Information Technology Fund is 11.8%, or $10.6 million, above the 202425 level. The budget includes one new IT Analyst position and resources for a contract lifecycle management system to support the procurement process. The budget includes funding for a new financial case management system to support the Clerk of the Superior Court and modernization of the Pierce County public website.

Information Technology Workload Service Highlights

For a full list of input/output measures, view Appendix Section 3.

16.6K Service Desk Requests 1.1K Total Systems Supported 4.0K Active Computers of all Types 1.8K Hours

Expenditures

Expenditure Summary - Provides budget information at an object of expenditure level for each department or fund budget.

Program Expenditures are included for certain departments and funds and display budget information at a project, activity, or function level.

Special analyses are prepared in certain instances to provide additional detail relating to revenues and/or expenditures of funds or departments. Typically, the analysis will summarize construction projects, services or programs, or types of activities.

Staffing Summary - Presents comparative personnel data for the six-year period 2022 through 2027. The summary identifies the number of full-time equivalent (FTE) positions authorized in the budget for each job classification within a department.

Pierce County Profile

Pierce County is home to an estimated 959,160 people, the second largest county in Washington.

Approximately 53% of Pierce County residents live in cities and towns.

In the last decade the median age has increased 4.8%.

Pierce County’s median income is 8% below Snohomish County and nearly 19% below King County.

About Pierce County

Pierce County covers nearly 1,800 square miles, stretching from the shores of Puget Sound to the 14,410-foot summit of Mount Rainier. More than 960,000 people live here, making it Washington’s second-largest county by population. Since time immemorial this area has been home to the Indigenous peoples whose descendants include today’s Nisqually (dxʷsqʷaliʔabš), Puyallup (spuyaləpabš), Muckleshoot (bəqəlšuɬ), and Squaxin Island (sqʷax̌sədabš) Tribes whose stewardship and cultural traditions remain central to the region today.

The County is home to 23 cities and towns—including Tacoma, Lakewood, and Puyallup—along with many unincorporated communities. Its economy is anchored by Joint Base LewisMcChord, the Port of Tacoma, health care, education, logistics, and a diverse mix of employers.

Pierce County government provides services countywide and in unincorporated areas, including public safety, courts, parks and trails, transportation, wastewater management, human services, and tax administration. Since adopting Home Rule in 1980, the County has been led by an elected Executive, Council, and other officials.

With natural beauty, cultural diversity, and strong communities, Pierce County is a place where residents can live, work, and thrive.

Financial Overview

The Pierce County 2026-27 Biennial Budget totals $3.5 billion, a 2.9% increase over 2024-25. The General Fund portion is $967.1 million, up 2.7% from the prior biennium. The General Fund’s share of the total budget has declined from 43.7% in 2020–21 to 38.8% in 2026–27, reflecting the expiration of one-time appropriations in 2024–25 and slower revenue growth relative to other funds. 2026-2027

Total County Budget

The $3.5 billion 2026-27 biennial budget is 2.9%, or $96.7 million, higher than 2024-25. Approximately 23% of the biennial budget reflects internal transactions between Pierce County departments. These internal transactions are also referred to as non-cash transactions because no cash leaves the County. They are used primarily to keep track of operating support or charges for internally provided services.

The following table summarizes County revenues and expenditures for the 2022–23, 2024–25, and 2026–27 biennia. Actuals are reported for 2022–23, with budgets shown for 2024–25 and 2026–27. Revenues are presented by major source (excluding fund balance), and expenditures are presented by major category.

All Funds Revenue and Expenditure Summary

Total County Budget (Cont.)

The following table provides a high-level summary of resources and services by fund type. The General Overview, at the front of this document, includes highlights of the various budgets within each of these fund types. The individual budget sections, found later in this document, provide additional detail. Refer to the Total Expenditures summary table in this section for a detailed list of the funds by fund type and department.

Internal Service Funds support County operations by providing centralized services such as information technology, self-insurance, vehicle and equipment pools, facilities maintenance, routing, and mail processing. Revenues to these funds are generated primarily through charges to other County departments, which means their budgets are also reflected as expenditures in the receiving funds. To calculate the net County budget, Internal Service Fund budgets must therefore be excluded—except for fund balance usage and revenues from external sources.

After accounting for these adjustments, the “netted” 2026-27 Biennial Budget for Pierce County is $3,147,783,670. This is derived from the total budget of $3,457,573,470, less $339,134,910 in Internal Service Funds, plus $29,345,110 in Internal Service Fund use of fund balance.

Fund Type Comparison

Revenues/Other Financing Sources Expenditures

Total revenues and expenditures projected for 2026-27 operations and capital are summarized and compared to prior years on the following pages. In total, the County’s budget is $96.7 million, or 2.9%, more than the 2024-25 level.

The 2026–27 budget focuses on preserving essential services, investing in capital improvements, and addressing rising salary and benefit costs.