2023 Benefits ENROLLMENT GUIDE January 1, 2023 December 31, 2023

Table of Contents This Benefits Guide contains a summary of the benefits available to all full time employees and their eligible dependents. If there is any conflict between the summary of benefits included in this Guide and the Plan Document, the Plan Document will govern. Your Health. Your Family. Your Benefits. Benefits Eligibility 3 Enrollment Instructions 4 Your Cost 5 NEW CARRIER! UHC Medical Plans 6 UHC Mobile App 7 UHC Telehealth 8 UHC Apple Fitness Discount 9 UHC Peloton Discount 10 Flexible Spending Accounts 11 Health Savings Accounts 12 NEW CARRIER! UHC Dental Plan 13 NEW CARRIER! UHC Vision Plan 14 Life Insurance & Disability 15 Additional Benefits Accident, Hospital, Critical Illness 16 22 Principal 401(k) 23 24 Benefits 101: Understanding Insurance 25 Benefit Contacts 26 Plans 9 12 NEW CARRIER! (Accident, Hospital, Critical Illness) 23 Benefit Contacts Employee Benefits GuidePage 2

Benefits Eligibility

LendingPoint is committed to providing comprehensive and competitive benefit programs that are flexible enough to meet the needs of you and your family. This guide includes information to help you understand your options plus resources to contact for questions and further assistance.

BENEFIT ELIGIBILITY

All full time employees working a minimum of 30 hours per week are eligible for benefits the first day of the month following date of hire, (on the 1st if hired the 1st of the month). You may also enroll your legal dependents, including your spouse and dependent children under age 26. Coverage for domestic partners is also available. Please contact HR for details.

QUALIFYING LIFE EVENT

Unless you experience a life changing qualifying event, you cannot make changes to your benefits until the next Open Enrollment period. If you experience a qualifying event, you must submit your request to change your benefits within 30-days of the date the event occurred. Qualifying events include:

• Marriage, divorce or legal separation

• Birth or adoption of a child

• Change in child’s dependent status

• Death of a spouse, child or other qualified dependent

• See HR for additional life events such as loss of employment.

ENROLLMENT CHECKLIST

Are you eligible for benefits?

• Full time employees working 30 hours or more per week are eligible for all benefits. Have your information ready.

• Have Social Security numbers and birth dates for you, your spouse & your dependent children ready when you enroll. Some benefits cannot be issued without this information. This information is also needed for your beneficiary.

Are

you waiving coverage?

• You will still need to record your decision to waive coverage. Make your Elections.

• Enrollment can be completed 24/7 in Employee Navigator or by speaking with a Benefits Counselor by making an appointment: https://calendly.com/lending point 1/oe

Employee Benefits Guide Page 3

Enrollment Instructions

Enrollment can be completed 24/7 in Employee Navigator or by speaking with a Benefits Counselor by scheduling an appointment.

If you have not yet registered, follow the instructions below. If you do not remember your login credentials use the forgot username/password option.

SCHEDULE AN ENROLLMENT SESSION

If you would like to learn more about the benefits being offered to you or need assistance enrolling, use the link below to schedule a time to speak with a professional Benefits Counselor!!

https://calendly.com/lending-point-1/oe

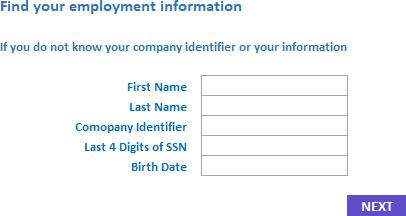

ENROLL ONLINE VIA EMPLOYEE NAVIGATOR

Once you are ready to make your elections, you can create an account and/or login to Employee Navigator by clicking the below link:

https://www.employeenavigator.com/benefits/Account/Login

• Click the 'Register as a new user' link.

• Enter the information requested on the registration screen. The Company identifier is "LendingPoint".

• Enter your desired password on the resulting screen. Please note the password requirements. You may also set/change your username here it will default to your email address if that has already been entered in the system.

• If you have successfully completed the registration, you will receive a notification on the next screen and will be able to log in using your new username and password.

• Once logged in, click the "Start Benefits" link.

Open your camera app and point your phone’s camera at the code above to schedule a Benefit Counseling session:

Employee Benefits GuidePage 4

Your Cost UHC Medical Plan Options $750 Deductible $1500 Deductible HDHP/HSA EE Pays Bi Weekly EE Pays Bi Weekly EE Pays Bi Weekly EE Only $30.92 $5.00 $5.00 EE + Spouse $124.15 $58.62 $24.00 EE + Children $107.54 $48.00 $19.85 EE + Family $209.54 $112.15 $46.62 UHC Dental PPO Plan Employee Pays Bi Weekly EE Only $0.00 EE + Spouse $3.00 EE + Children $3.00 EE + Family $6.46 UHC Vision Plan Employee Pays Bi Weekly EE Only $0.00 EE + Spouse $2.99 EE + Children $3.00 EE + Family $6.46 Employee Benefits Guide Page 5

Page 6 Employee Benefits Guide UHC Medical Plans Your health is an investment in your future. We are pleased to offer you freedom to choose your own path on a journey towards becoming your best self. Choose between three UHC medical plan options based on the specific needs of you and your family members. UnitedHealth Care BENEFITS (In Network) $750 $1,500 HDHP/HSA Deductible Deductible Deductible Individual $750 $1,500 $3,000 Family $2,250 $3,000 $6,000 Coinsurance (after deductible) 20% 20% 20% Out-of-Pocket Maximum (includes copays, co-insurance & deductible) Individual $5,000 $5,000 $6,900 Family $10,000 $10,000 $13,800 Professional Services Primary Care $25 $25 20% after ded Specialist $50 $50 20% after ded Urgent Care $75 $50 20% after ded Emergency Room $350 $500 20% after ded Lab/X Ray (Outpatient) 0% after ded 0% after ded 20% after ded High Tech Radiology (CT, PET, MRI) 20% after ded 20% after ded 20% after ded Outpatient Surgery Facility 20% after ded 20% after ded 20% after ded Professional Fees 20% after ded 20% after ded 20% after ded Pharmacy Benefits* Pharmacy Deductible None None Medical Ded Applies Retail Tier 1 $10 $10 20% after ded (30 Day Supply) Tier 2 $35 $35 20% after ded Tier 3 $75 $75 20% after ded Tier 4 $150 150 20% after ded Mail Order Tier 1 $25 $25 20% after ded (90 Day Supply) Tier 2 $87.50 $87.50 20% after ded Tier 3 $187.50 $187.50 20% after ded Tier 4 $375 $375 20% after ded NEW CARRIER!!

A health plan that’s always with you

Digital tools to keep you connected

Get the most out of your benefits

Register for your personalized website on myuhc.com® and download the UnitedHealthcare® app. These digital tools are designed to help you understand your benefits and make informed decisions about your care.

• Find care and compare costs for providers and services in your network

• Check your plan balances, view your claims and access your health plan ID card

• Access wellness programs and view clinical recommendations

• 24/7 Virtual Visits – Connect with providers by phone or video to discuss common medical conditions and get prescriptions*,* if needed *

• View your health care financial account(s) such as HSA, FSA or HRA

• Compare prescription costs and order refills Download the app Available for iPhone and Android

Register today

Scan the QR code or go to myuhc.com and click Register Now See next page for registration steps

Employee Benefits Guide Page 7

Visit with a doctor 24/7 — whenever, wherever With 24/7 Virtual Visits, you can connect to a doctor by phone or video1 through myuhc.com® or the UnitedHealthcare® app. A convenient and faster way to get care Doctors can treat a wide range of health conditions — including many of the same conditions as an emergency room (ER) or urgent care — and may even prescribe medications,2 if needed. With a UnitedHealthcare plan, your cost for a 24/7 Virtual Visit is usually $0.3 Consider 24/7 Virtual Visits for these common conditions: • Allergies • Flu • Sore throats • Bronchitis • Headaches/migraines • Stomachaches • Eye infections • Rashes • and more $0 cost An estimated 25% of ER visits could be treated with a 24/7 Virtual Visit — bringing a potential $2,000 4 cost down to $0. Get started Sign in at myuhc.com/virtualvisits | Call 1-855-615-8335 Download the UnitedHealthcare app Please note: the cost for employees on the HDHP is $49 Page 8 Employee Benefits Guide

Helping add value to youremployee health plan at no additional cost

Eligible employees have access to a 1-year Apple Fitness+ subscription at no additional cost.* The first fitness service powered by Apple Watch.

Adding value to your benefits may help inspire healthier behavior:

• $79 value per employee can be shared with up to 5 family members.

• A single, comprehensive offering for various fitness levels powered by Apple Watch.

• Access to on-demand workouts on iPhone, iPad and Apple TV, with new workouts and meditations added every week.

Only 50% of

Employee Benefits Guide Page 9

adults get the exercise needed to help reduce and prevent chronic diseases1

Adding value and inspiring healthierbehavior

Discover a wellness offering designed to help make fitness more accessible for your employees. It adds value to your benefits and may help them take ownership of their health and well-being.

UnitedHealthcare is bringing quality digital fitness classes right to your employees’ fingertips. It’s a program that helps them lead more active lives and it’s available at no additional cost to them.

• UnitedHealthcare plansinclude 1 year of Peloton® App Membership*

• $155 value per employee and each covered family member

• Single,comprehensive offering for various fitness levels, no equipment required

• Access to Peloton’s engaging digital fitness and meditation classes

• Members and participants may purchase Peloton Bike, Bike+ or Tread at special pricing*

Taking exercise to a new level

Peloton’s immersive live and on demand digital classes may help employees of all fitness levels get motivatedto achieve theirhealth goals. The digital experience makes it convenient to jump into a workout anywhere, anytime, from a phone, tablet or TV.

• Engaging variety of classes to choose from

• Flexibility that may fit any schedule with classes from 5 to 90 minutes

• Exciting workouts led by expert instructors who bring their knowledge, personality and curated playlists

• Help for achieving goals through progress tracking with workout metrics

• Motivating challenges and training programs

• Engaging social features to connect with others

The reality of inactivity

Only 50%

of adults get the exercise needed to help reduce and prevent chronic diseases1

per year is spent on health care costs associated with inadequate physical activity1

$117B

Health Management | 1-year Peloton App Membership

Employee Benefits GuidePage 10

Flexible Spending Accounts

What is an FSA?

Flexible spending accounts (FSAs) allow you to pay for non reimbursed healthcare and eligible day care expenses on a pre tax basis before Federal, State, Social Security and Medicare taxes. Flores and Associates administers the LendingPoint FSA(s).

How Does an FSA Work?

There are two types of flexible spending accounts: medical and dependent care. You may participate in one or both. You decide how much you want to deposit into your account. That amount is deducted on a pre tax basis evenly during the calendar year from your paycheck. You must re-elect this benefit each year if you want to participate.

Medical FSA

Your medical FSA reimburses you for eligible, out of pocket medical, dental and vision expenses for yourself and your covered dependents. When you have a qualified expense, you can use your Flores Debit Card to pay for expenses on a pre tax basis.

Please note: The Limited F.S.A. (covering dental and vision expenses) is available to H.S.A. participants.

Dependent Care FSA

The dependent care spending account is a pre tax way for you to pay for eligible dependent care expenses so you (and if you are married, your spouse) can work. You can set aside tax-free income to pay for qualified dependent care expenses, such as daycare, that you normally pay for with after tax dollars. Qualified dependents include children under 13 and/or dependents who are physically or mentally handicapped.

Funds in this account are available as contributions are made. Expenses may only be reimbursed after the dependent care services have been performed. For example, if a dependent care provider requires payment at the beginning of the week, the employee may not seek reimbursement until the end of the week.

Note: For more information on qualified expenses, visit the Flores site at: www.flores247.com

Medical:

Dependent Care: $5,000

2023 FSA Contribution Limits

$3,050

Employee Benefits Guide Page 11

Health Savings Accounts

Health Savings Accounts (HSAs) are a great way to save money and pay for medical expenses. HSAs are tax advantaged savings accounts that accompany high deductible health plans (HDHPs).

HSA money can be used tax free when paying for qualified medical expenses, helping you pay your HDHP’s larger deductible. At the end of the year, you keep any unspent money in your HSA. This rolled over money can grow with tax deferred investment earnings, and, if it is used to pay for qualified medical expenses, then the money will continue to be tax free. Your HSA and the money in it belong to you, not your employer or insurance company.

Flores & Associates administers the HSA. You must be enrolled in the High Deductible Plan in order to enroll in the HSA. For the HSA, you have the option to set up your HSA bank account with Flores & Associates. You decide how much you want to contribute to your HSA bank account, up to the IRS limits.

Deductions are taken from your paycheck on a pre tax basis and sent directly to your Flores HSA bank account. You monitor and access your HSA bank account 24/7 through the Flores & Associates online portal and mobile app. You will be issued a Debit Card (with your contributions loaded). You can also order checks for a small fee.

HSA Advantages

Affordability

your monthly

when you switch

higher deductible, and these

paired with

Flexibility

for current medical expenses,

deductible and expenses

your insurance

not cover, or you

save your funds for future medical expenses.

Savings –

triple tax savings: 1. Tax

2. Tax free earnings

3. Tax

expenses

–

portable,

if

are

for

to save for future medical expenses

3

Contribution Limits: Individual Account:

Family Account:

Here are some of the many advantages an HSA provides you with: Security Your HSA can provide a savings buffer for unexpected or high medical bills.

In most cases, you can lower

health insurance premiums

to health insurance coverage with a

HDHPs can be

an HSA.

You can use your HSA to pay

including your

that

may

can

Tax

An HSA provides you with

de ductions when you contribute

through investment

free withdrawals for qualified

Portability

Accounts are completely

meaning you can keep your HSA even

you change jobs, change your medical coverage, become unemployed, or move to another state. Ownership There

no “use it orlose it” rules

HSAs, making ita greatway

202

HSA

$3,850

$7,750

Employee Benefits Guide Page12

If you are age 55/older you can contribute an additional catchup amount of $1,000.

UHC Dental Plan Dental Benefits Deductible (calendar year) Individual $50 Family $150 Annual Maximum $1,650 Coinsurance Preventive & Diagnostic 100% Basic Services 80% Major Services 50% Orthodontic Services (child only coverage) Lifetime Max 50% $1,200 In addition to protecting your smile, dental insurance helps pay for dental care and includes regular checkups, cleanings and X rays. Receiving regular dental care can protect you and your family from the high cost of dental disease and surgery. Page 13 Employee Benefits Guide Dental coverage is offered for basic, major, and orthodontic treatment. The dental plan also includes 100% coverage for preventive care. You and your eligible dependents may enroll in dental coverage administered by UHC. NEW CARRIER… SAME GREAT BENEFITS!

UHC Vision Plan Driving to work, reading a news article and watching TV are all activities you likely perform every day. Your ability to do all these things, though, depends on your vision and eye health. Vision insurance can help you maintain your vision as well as detect various health problems. Your vision plan includes coverage for routine eye exams, eyewear, contact lenses and more. You and your eligible dependents may enroll in vision coverage administered by UHC. Employee Benefits Guide Page 14 Vision Benefits IN-NETWORK Service Frequency Exam, Lenses, Contacts Once every 12 months Frames Once every 12 months Co pays Exam Materials $10 $25 Frames Allowance Private Practice / Retail Chain $150 allowance, then 30% off any balance Lenses Single Vision $25 copayBifocal Trifocal Contact Lenses In lieu of lenses andframes Allowance $150 allowance Elective (conventional) Medically Necessary Allowance $25 copay NEW CARRIER

Life & Disability

BASIC LIFE INSURANCE

Life insurance can help provide for your loved ones if something were to happen to you. LendingPoint is pleased to provide all full time employees with $50,000 in group life and accidental death and dismemberment (AD&D) insurance.

VOLUNTARY LIFE INSURANCE

In addition to basic life insurance, some employees may want to purchase additional coverage. With voluntary life insurance, you are responsible for paying the full cost of coverage through payroll deductions. You can purchase coverage for yourself, your spouse or your dependent children. The chart below outlines your benefit options for voluntary life insurance.

Life

Insurance Increment

$10,000 $100,000

Spouse

Child

$5,000 increments to a maximum of $100,000, not to exceed 50% of the employees benefit amount $5,000 $25,000

Options of $1,000, $2,000, $4,000, $5,000 or $10,000 (at 6 months old) Child 15 days to 6 months old $100

*Amounts over the Guarantee Issue are subject to Evident of Insurability.

LendingPoint provides full time employees with short and long term disability income benefits. This coverage provides income protection for regular expense items, which are typically covered by your paycheck. If you experience a disability that impacts your ability to work and earn a paycheck, disability insurance helps cover the gap. At LendingPoint, we want to do everything we can to protect you and your family. That’s why we pay for the full cost of short and long term disability insurance meaning that you owe nothing out –of-pocket.

Coverage Effective Date Benefit Cost

Short-Term

Employee Benefits GuidePage 15

SHORT & LONG-TERM DISABILITY INSURANCE Guaranteed Issue

Amount*

Employee $10,000 increments to a maximum of the lesser of 5x pay or $500,000

Disability

Disability

As noted based on options $10,000

Coverage begins after 14 days of disability Duration: 11 weeks 60% of your pre disability weekly earnings up to $500 Employer Paid Long-Term

Coverage begins after 90 days of disability or the date your short term disability ends 60% of your pre disability monthly earnings up to $2,500 Employer Paid

Additional Benefits

ACCIDENT INSURANCE

Accident insurance provides a financial cushion for life’s unexpected events. You can use it on anything you want, such as to help pay costs that aren’t covered by your medical plan. It provides you with a lump sum payment when you or your family need it most. And best of all, the payment is made directly to you, and is made regardless of any other insurance you may have. It’s yours to spend however you like, including for you or your family’s everyday living expenses.

HOSPITAL INDEMNITY

If you are out of work unexpectedly, you may also have trouble meeting household expenses like your mortgage payments, car payments, childcare expenses or household upkeep expenses due to lost or reduced income while you recover. Hospital indemnity insurance can help you be better prepared by providing you with a payment to use as you see fit if you experience a covered event and meet the policy and certificate requirements. Typically, a flat amount is paid for the day that you are admitted to a hospital and a per day amount is paid for each day of a covered hospital stay, from the very first day of your stay.

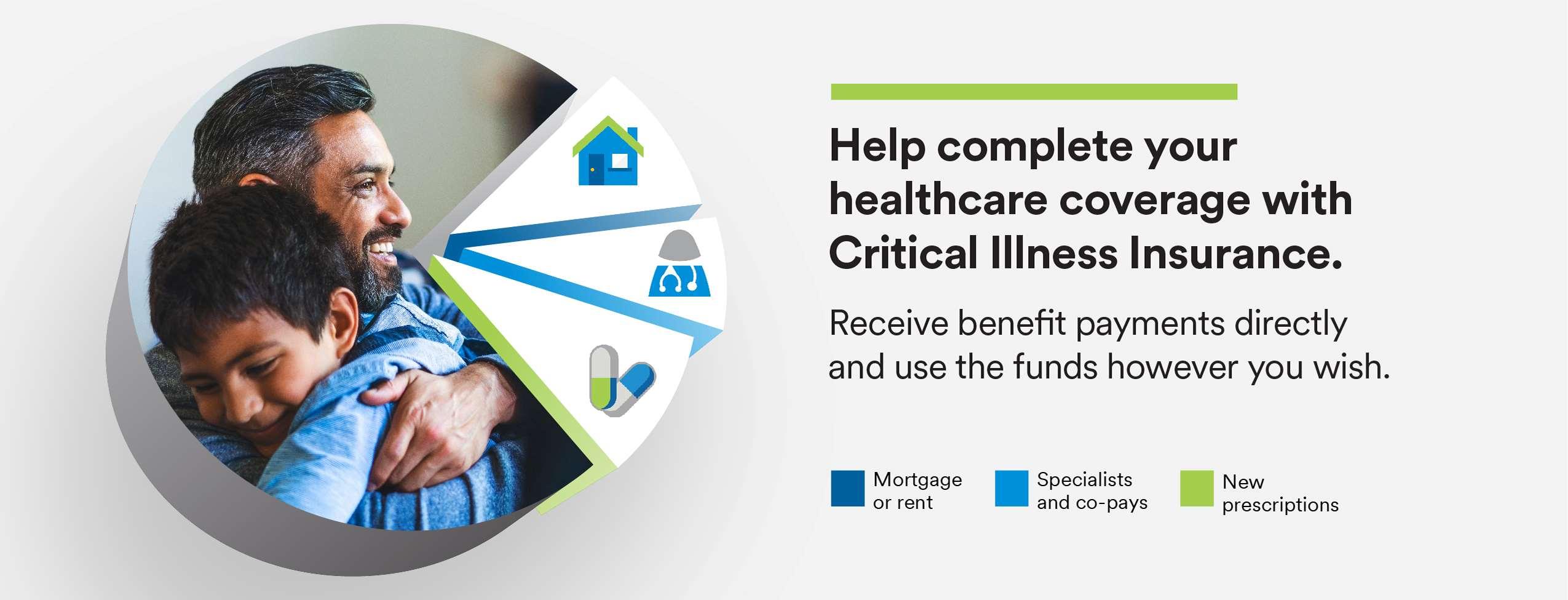

CRITICAL ILLNESS

Critical Illness Insurance is coverage that can help safeguard your finances by providing you with a lump-sum payment — one convenient payment all at once when you or your loved ones need it most. The extra cash can help you focus on getting back on track without worrying about finding the money to cover the costs of treatment. The payment is made directly to you and is in addition to any other insurance you may have. It’s yours to spend however you like, including for everyday living expenses. While recovering, critical illness insurance is there to make life a little easier.

$0.42 $0.67 $0.60 $0.86

$0.48 $0.77 $0.67 $0.96

$0.59 $0.94 $0.78 $1.13

-

-

-

-

$0.74 $1.17 $0.93 $1.36

$1.02 $1.58 $1.21 $1.77

$1.43 $2.19 $1.62 $2.38

$2.06 $3.14 $2.25 $3.33

$2.90 $4.40 $3.09 $4.59

$4.07 $6.15 $4.26 $6.34

- 69 $5.70 $8.60 $5.89 $8.79

$7.69 $11.59 $7.88 $11.78

$10.65 $16.02 $10.84 $16.21

Making sure your will is up to date can help ensure that your assets are distributed the way you want. You do not need to have access to an attorney to create a binding will. MetLife’s online Will Preparation Services provided by SmartLegalForms helps you create a binding will, living will, or assign a power of attorney. Visit www.willscenter.com and register. WILL PREPARATION Monthly Low Plan Rates Type Accident Hospital Indemnity Employee Only $8.96 $10.02 Employee + Spouse $17.66 $22.14 Employee + Children $21.29 $16.36 Employee + Spouse and Children $25.10 $28.48 Monthly High Plan Rates Type Accident Hospital Indemnity Employee Only $12.20 $20.05 Employee + Spouse $23.93 $44.28 Employee + Children $28.70 $32.72 Employee + Spouse and Children $33.88 $56.95 Attained Age Employee Only EE + Spouse EE + Child(ren) EE+ Spouse & Child(ren) <25

25

30

35

40

45

50

55

60

65

70

75+

Multiply the per $1,000 rates shown above by the benefit amount divided by $1,000 (e.g.,15 for $15,000 of coverage) and round to two decimals to calculate rates for the quoted benefit amounts. Employee Benefits Guide Page 16

- 29

34

39

44

49

54

59

64

74

Accident Insurance

Coverage that helps with unexpected expenses, such as those that may not be covered under your medical plan.

Accident insurance: why is it so important?

Accidents can happen when you least expect them. And while you can’t always prevent them, you can get help to make your recovery less expensive and stressful.

In the U.S. there are approximately 29.4 million trips to the emergency room annually due to injuries.1 These visits can be expensive — in fact, ER bills average around $1,389 per visit,2 and even seemingly small injuries can come with unexpectedly high hospital bills.

You may be thinking — that’s why I have health insurance. But even the best medical plans may leave you with unexpected expenses like deductibles, copays, extra costs for out-of-network care, and non-covered services.

You can’t plan for accidents, but you can try to handle them better by being financially prepared.

How it works

Accident insurance provides a financial cushion for life’s unexpected events. You can use it on anything you want, such as to help pay costs that aren’t covered by your medical plan. It provides you with a lump-sum payment — one convenient payment all at once — when you or your family need it most. The extra cash can help you focus on getting back on track, without worrying about finding the money to help cover the costs of treatment.

And best of all, the payment is made directly to you, and is made regardless of any other insurance you may have. It’s yours to spend however you like, including for your or your family’s everyday living expenses.

Whatever you need while recovering from an accident or injury, accident insurance is there to make life a little easier.

PRODUCT OVERVIEW

Enroll today! [For

[1

[1

Why should I enroll now? •Competitive group rates •Guaranteed acceptance4 •Easy payroll deduction •Portable coverage so you can take it with you3 Page 17 Employee Benefits Guide

questions, please call MetLife at

800 GET-MET8]

800 438-6388]

Accident Insurance

With MetLife Accident Insurance, you can take your coverage with you if you change jobs or retire.3

Accident insurance can help you manage unexpected expenses

— so you can focus on getting well.

Our accident insurance is designed to cover a wide array of events, medical services, and treatments.5

This plan provides a lump-sum payment for over 150 different covered events, such as:

•Fractures6

•Dislocations6

•Second and third degree burns

•Skin grafts

•Torn knee cartilage

•Ruptured disc

•Concussions

•Cuts or lacerations

•Eye injuries

•Coma

•Broken teeth

You’ll receive a lump-sum payment when you have these covered medical services or treatments:7

•Ambulance

•Emergency care

•Inpatient surgery

•Outpatient surgery

•Medical Testing Benefits (including X-rays, MRIs, CT scans)

•Physician follow-up visits

•Transportation

•Home modifications

•Therapy services (including physical and occupational therapy, speech therapy)

This plan provides protection 24 hours a day — while on or off the job.

See your Disclosure Statement or Outline of Coverage/Disclosure Document for full details on your coverage.

1. Centers for Disease Control and Prevention: Emergency Department Visits. CDC/National Center for Health Statistics. Accessed July 2020.

2. "Emergency Rooms vs. Urgent Care Centers” Debt.org. Last updated November 12, 2019.

Help protect yourself, your family and your budget from the financial impact of unexpected injuries.

3. Eligibility for portability through the Continuation of Insurance with Premium Payment provision may be subject to certain eligibility requirements and limitations. For more information, contact your MetLife representative.

4. Coverage is guaranteed provided (1) the employee is actively at work and (2) dependents to be covered are not subject to medical restrictions as set forth on the enrollment form and in the Certificate. Some states require the insured to have medical coverage. Additional restrictions apply to dependents serving in the armed forces or living overseas.

5. Covered services/treatments must be the result of an accident or sickness as defined in the group policy/certificate. See your Disclosure Statement or Outline of Coverage/Disclosure Document for more details.

6. Chip fractures are paid at 25% of Fracture Benefit and partial dislocations are paid at 25% of Dislocation Benefit.

7. Covered services/treatments must be the result of a covered accident as defined in the group policy/certificate. See your Disclosure Statement or Outline of Coverage/Disclosure Document for more details.

METLIFE'S ACCIDENT INSURANCE IS A LIMITED BENEFIT GROUP INSURANCE POLICY. The policy is not intended to be a substitute for medical coverage and certain states may require the insured to have medical coverage to enroll for the coverage. The policy or its provisions may vary or be unavailable in some states. There is a preexisting condition limitation for hospital sickness benefits, if applicable. MetLife’s Accident Insurance may be subject to benefit reductions that begin at age 65. And, like most group accident and health insurance policies, policies offered by MetLife may contain certain exclusions, limitations and terms for keeping them in force. For complete details of coverage and availability, please refer to the

Metropolitan Life Insurance Company | 200 Park Avenue | New York, NY 10166

Employee Benefits Guide Page 18

Critical illness insurance: Why is it so important?

Medical bills have contributed to 58% of bankruptcies.1 In 2020, one in four working-age adults with insurance coverage reported medical bill problems or debt in the past year.2

The financial consequences of surviving a critical illness are something few people are prepared for. Expenses that may not be covered by medical plans, such as co-pays, deductibles, childcare, mortgage, groceries and experimental treatments, could cut into your savings.

When critical illness affects your family, you’ll have the support you need when it matters most with MetLife Critical Illness Insurance

How it works

Critical Illness Insurance is coverage that can help safeguard your finances by providing you with a lump-sum payment — one convenient payment all at once — when you or your loved ones need it most. The extra cash can help you focus on getting back on track without worrying about finding the money to cover the costs of treatment.

And best of all, the payment is made directly to you, and is in addition to any other insurance you may have. It’s yours to spend however you like, including for everyday living expenses.

While recovering, critical illness insurance is there to make life a little easier.

Enroll today!

For questions, call MetLife at 1 800 GET-MET8 [1 800 438-6388]

BenefitOverview WhyshouldI enrollnow? •Competitivegrouprates •Guaranteedacceptance3 •Easypayrolldeductions •Portablecoverageso youcantakeitwith youifyouchangejobs orretire4

ADF# CI2586.20Page 19 Employee Benefits Guide

Hospital Indemnity Insurance

Coverage to helppay forexpenses associated with ahospitalization that may not becovered underyourmedical plan.

Why hospital indemnity insurance makes sense

People may not budget for hospital1 bills. But you can be prepared.

Because even the best medical plans may leave you with extra expenses. No one ever expects to be in the hospital. And your stay can require a variety of treatments, testing, therapies and other services — each of which can mean extra out-of-pocket costs, beyond what your medical plan may cover.

With an average cost of just over $10,700 per hospital stay in the U.S.,2 it’s easy to see why having hospital indemnity coverage may make good financialsense. Just think about the possibility of havinga hospital stay due to an accident or illness3:

•Your child gets hurt on the school playground

1.Hospital

•You experience chest pains while exercising and are admitted to the hospital to be checked and monitored

•Your spouse4 undergoes an emergency appendectomy

Some of the expenses you may not expect include:

•Medical plan deductibles and co-pays

•Extra expenses associated with out-of-network care and treatment.

If you are out of work unexpectedly, you may also have trouble meetinghousehold expenses like yourmortgage payments, car payments, childcare expenses or household upkeep expenses due to lost orreduced income while you recover.

Hospital indemnity insurance can help you be betterprepared by providing you with a payment to use as you see fit if you experience a covered event and meet the policy and certificate requirements.

Typically, a flat amount is paid for the day that you are admitted to a hospital and a per-day amount is paid for each day of a covered hospital stay, from the very first day of your stay. This payment can help you focus more on your recovery and can help you focus less on the extra expenses associated with a hospitalization resulting from an accident or illness may bring.

See your Disclosure Statement or Outline of Coverage/Disclosure Document for full details.

Why enroll now?

•Acceptance is guaranteed for you and your eligible family members.5

•Competitive group rates

•Premium payment through payroll deductions

METLIFE'S HOSPITAL INDEMNITY INSURANCE IS A LIMITED BENEFIT GROUP INSURANCE POLICY. The policy is not intended to be a substitute for medical coverage and certain states may require the insured to have medical coverage to enroll for the coverage. The policy or its provisions may vary or be unavailable in some states. Prior hospital confinement may be required to receive certain benefits. There may be a preexisting condition limitation for hospital sickness benefits. MetLife’s Hospital Indemnity Insurance may be subject to benefit reductions that begin at age 65. Like most group accident and health insurance policies, policies offered by MetLife may contain certain exclusions, limitations and terms for keeping them in force. For complete details of coverage and availability, please refer to the group policy form GPNP12-AX, GPNP13-HI, GPNP16-HI or GPNP12-AX-PASG, or contact MetLife. Benefits are underwritten by Metropolitan Life Insurance Company, New York, New York. In certain states, availability of MetLife’s Group Hospital Indemnity Insurance is pending regulatory approval. Hospital does not include certain facilities such as nursing homes, convalescent care or extended care facilities. See your Disclosure Statement or Outline of Coverage/Disclosure Document for full details.

PRODUCT OVERVIEW

include certain facilities such as nursing homes, convalescent care or extended care facilities. See your Disclosure

or

Coverage/Disclosure

and

Debt.org.

costs/#:~:text=Hospital%20costs%20averaged%20%243%2C949%20per,are%20related%20to%20medical%20expenses..

does not

Statement

Outline of

Document for full details. 2.Hospital

Surgery Costs.

https://www.debt.org/medical/hospital-surgery-

Accessed September 2020. 3.There is a pre-existing exclusion for covered sicknesses. See your Disclosure Statement or Outline of Coverage/Disclosure Document for full details. 4.Coverage for Domestic Partners, civil union partners and reciprocal beneficiaries varies by state. Please contact MetLife for more information. 5.Coverage is guaranteed provided (1) the employee is actively at work and (2) dependents are not subject to medical restrictions as set forth in the Certificate. Some states require the insured to have medical coverage. Additional restrictions apply to dependents serving in the armed forces or living overseas.

Employee Benefits Guide Page 20

Legal Plans

with a Legal Plan.

Legal experts on your side, whenever you need them

Quality legal assistance can be pricey. And it can be hard to know where to turn to find an attorney you trust. You can have a team of top attorneys ready to help you

MetLife Legal Plans gives you access to the expert guidance and tools you need to handle the broad range of personal legal needs you might face throughout your life. This could be when you’re buying or selling a home, starting a family, dealing with

Reduce the out-of-pocket cost of legal services with MetLife Legal Plans.

How it works

Our service is tailored to your needs. With network attorneys available in person, by phone or by email and online tools to do-it-yourself — we make it easy to get legal help. And, you will always have a choice in which attorney to use. You can choose one from our network of prequalified attorneys, or use an attorney outside of our network and be reimbursed some of the cost.1

Best of all, you have unlimited access to our attorneys for all legal matters covered under the plan.

When you need help with a personal legal matter, MetLife Legal Plans is there for you to help make it a little easier.

Estate planning at your fingertips

Our website provides you with the ability to create wills, living wills and powers of attorneys online in as little as 15 minutes. Answer a few questions about yourself, your family and your assets to create these documents instantly. In states where available, you also have access to sign and notarize your documents online through our video notary feature.2

How to use the plan

1.Find an attorney

Create an account at legalplans.com to see your coverages, select an attorney and get a case number for your legal matter. Or, give us a call at 800.821.6400 for assistance.

2.Make an appointment

Call the attorney you select, provide your case number and schedule a time to talk or meet.

3.That’s it!

There are no copays, deductibles or claim forms when you use a network attorney for a covered matter.

Product Overview

Cover the costs on a wide range of common legal issues

Page 21 Employee Benefits Guide

Access experienced attorneys to help with estate planning, home sales, tax audits and more.

With MetLife Legal Plans, you, your spouse and dependents get legal assistance for some of the most frequently needed personal legal matters — with no waiting periods, no deductibles and no claim forms when using a network attorney for a covered matter.

Money Matters

Home & Real Estate

• Debt Collection Defense

• Identity Management Services

3

• Boundary or Title Disputes

•

• Identity Theft Defense

• Negotiations with Creditors

• Personal Bankruptcy

• Home Equity Loans

• Mortgages

• Property Tax Assessments

• Promissory Notes

• Tax Audit Representation

• Tax Collection Defense

• Sale or Purchase of Home

• Security Deposit Assistance

• Tenant Negotiations

•

Family

•

• Refinancing of Home

• Zoning Applications Estate

• Powers of Attorney (Healthcare, Financial, Childcare, Immigration)

•

• Name Change

• Parental Responsibility Matters

•

• Disputes Over Consumer Goods & Services

• Incompetency Defense

• Revocable & Irrevocable Trusts

• Simple Wills

• Prenuptial Agreement

• Protection from Domestic Violence

• Review of ANY Personal Legal Document

• Pet Liabilities

• Small Claims Assistance

• Powers of Attorney

• Prescription Plans

•

• Habeas Corpus

• Repossession

To learn more about your coverages and see our attorney network, create an account at legalplans.com or call 800.821.6400 Monday – Friday 8:00 am to 8:00 pm (ET).

Your account will also give you access to our self-help document library to complete simple legal forms. The forms are available to you, regardless of enrollment.

1. You will be responsible to pay the difference, if any, between the plan’s payment and the out-of-network attorney’s charge for services.

2. Digital notary and signing is not available in all states.

3. This benefit provides the Participant with access to LifeStages Identity Management Service provided by Cyberscout, LLC. Cyberscout is not a corporate affiliate of MetLife Legal Plans.

4. Does not cover DUI.

Group legal plans provided by MetLife Legal Plans, Inc., Cleveland, Ohio. In certain states, group legal plans are provided through insurance coverage underwritten by Metropolitan General Insurance Company, Warwick, RI. Some services not available in all states. No service, including consultations, will be provided for: 1) employment-related matters, including company or statutory benefits; 2) matters involving the employer, MetLife and affiliates and plan attorneys; 3) matters in which there is a conflict of interest between the employee and spouse or dependents in which case services are excluded for the spouse and dependents; 4) appeals and class actions; 5) farm and business matters, including rental issues when the participant is the landlord; 6) patent, trademark and copyright matters; 7) costs and fines; 8) frivolous or unethical matters; 9) matters for which an attorney client relationship exists prior to the participant becoming eligible for plan benefits. For all other personal legal matters, an advice and consultation benefit is provided. Additional representation is also included for certain matters. Please see your plan description for details. MetLife® is a registered trademark of MetLife Services and Solutions, LLC, New York, NY. [MLP3wHC]

Deeds

• Eviction Defense

Foreclosure

Planning

• Codicils

• Complex Wills

• Healthcare Proxies

• Living Wills

& Personal

Affidavits

• Adoption •

Conservatorship

• Demand Letters • Garnishment Defense • Guardianship • Immigration Assistance

Juvenile Court Defense, Including Criminal Matters

Personal Property Protection

• School Hearings Civil Lawsuits

• Administrative Hearings

• Civil Litigation Defense

Issues Consultation & Document Review for your parents:

Deeds

Leases

Elder-Care

•

•

• Medicaid • Medicare • Notes

• Nursing Home Agreements

& Other Matters

• Wills Traffic

Defense of Traffic Tickets

Driving Privileges Restoration

4 •

• License Suspension Due to DUI

you navigate

and unplanned events. Employee Benefits Guide Page 22

Helping

life’s planned

Checkouttheplan's investments

Eachinvestmentisdifferent,andyoucan choosebasedonyourgoalsandhowyou feelaboutrisk.Youcanalsopickfrom theplan'sinvestmentoptionslater.But bypickingitlater,youunderstandthat untilyoumakeanewinvestment selection,you'redirectingcontributions totheplan'sdefault.*

Forafulllisting,refertothe InvestmentOptionSummary.

principal.com/Welcome mobile app/ text Enroll

to the Team! Enroll in the

Plan today!

a few steps you'll be on your way! Plan ID Number: 473024 Visit Principal.com/Welcome or call 800-547-7754 (M-F 8 am - 10 pm ET)

principal.com/Welcome

•

•Readingimportantplannotices

Welcome

LendingPoint LLC 401(k)

In just

Reviewyourcontribution Yourorganizationhassetacontributionrate foryou.Login,takealook,andmakechanges toyourcontributionrateifyouwant,orvisit principal.com/MatchEnrollmentWebinar. Getyouraccountsetup Visit

orusethePrincipal®app.Youcanalsotext ENROLLto78259 SitiowebdisponibleenEspañol. Beginby:

Settingsecuritypreferences

Page23 Employee Benefits Guide

Keep going!

You've got this, and we've got your back when it comes to educational resources.

To learn more, visit principal. com/Welcome or use the Principal mobile app. You can also text ENROLL to 78259. Sitio web disponible en Español.

See

your retirement savings in one place

We’ll help you roll eligible outside retirement savings into your retirement account.

Designate a beneficiary

Don’t leave the decision up to someone else if something happens to you before retirement. Always designate a beneficiary to ensure the money in your account goes to a loved one.

Keep in touch

Staying in the know when it comes to retirement planning is a pretty good idea. We’ll send you educational information about what’s important to you.

234-73024/LendingPointLLC401(k)Plan Employee Benefits Guide Page24

Benefits 101: Understanding Insurance

In order to get the most out of your health care benefits, you need to understand the terms used by insurance companies, the government, health plans and health care providers. This way, you can make better decisions and ultimately receive better care.

Claim A request by an individual (or his or her provider) for the insurance company to pay for services obtained.

Coinsurance – The money that an individual is required to pay for services after the deductible has been met. It is often a specified percentage of the charges. For example, the employee pays 20% of the charges while the health plan pays 80%.

Copayment – An arrangement where an individual pays a specified amount for various health care services and the health plan or insurance company pays the remainder. The individual must usually pay his or her share when services are rendered. Copayments are usually a set dollar amount (such as $20 per office visit), rather than a percentage of the charges.

Deductible A set dollar amount that a person must pay before insurance coverage for medical expenses can begin. They are usually charged on an annual basis.

Dependent Any individual, adult or minor whom a parent, relative or other person may choose to cover on his or her insurance plan.

Generic Drugs A prescription drug that has the same active ingredient formula as a brand name drug. Generic drugs usually cost less than brand name drugs. The Food and Drug Administration (FDA) rates these drugs to be as safe and effective as brand name drugs.

In network Typically refers to physicians, hospitals or other health care providers who contract with an insurance plan (usually an HMO or PPO) to provide services to its members. Coverage for services received from in network providers will typically be greater than for services received from out of network providers, depending on the plan.

Out of network Typically refers to physicians, hospitals or other health care providers who do not contract with an insurance plan to provide services to its members. Depending on the insurance plan, expenses incurred for services provided by out of network providers might not be covered, or coverage may be less than for in-network providers.

Out of pocket Maximum (OOPM) The total amount paid each year by the member for the deductible, coinsurance, copayments and other health care expenses, excluding the premium. After reaching the out of pocket maximum, the plan pays 100% of the allowable charges for covered services the rest of that calendar year.

Premium – The amount of money charged by an insurance company for coverage.

Preventive Care – Any medical checkup, test, immunization, or counseling service used to prevent chronic illnesses from occurring.

Primary Care Physician (PCP) A health care professional who is responsible for monitoring an individual’s overall health care needs. Typically, a PCP serves as a gatekeeper for an individual’s medical care, referring him or her to specialists and admitting him or her to hospitals when needed.

Page25 Employee Benefits Guide

Benefit Contacts ResourceName How to Contact UHC Medical Benefits 800 411 1143 www.myuhc.com UHC Dental Benefits 888 679 8925 www.myuhc.com UHC Vision Benefits 800 638 3120 www.myuhc.com MetLife Life & Disability Group Policy #: 5392656 800 GET MET8 metlife.com/mybenefits Flores Spending Accounts 1-800-532-3327 Flores247.com MetLife Voluntary Benefits Accident, Critical Illness and Hospital Indemnity 800 GET MET8 metlife.com/mybenefits Principal 401(k) 800 547 7754 Principal.com/welcome The Benefit Butler (404)991 6070 benefitbutler@palmerandcay.com Page 26Employee Benefits Guide benefitbutler@palmerandcay.com (404)991 - 6070 The Benefit Butler is an expert on claims processing, coverage and anything benefits related. Our benefits partner and consultant, Palmer & Cay, provides this service to you at no cost. The Benefit Butler is available via phone or email and can help explain your situation and seek a resolution. Have a question? Scan the QR code to email the Benefit Butler.