9 minute read

A region of untapped potential

Elfride Covarrubias Villegas, Head of Market Area, Italy & East Med Area, Energy Systems at DNV, details the findings of a report comparing the oil and gas industry in the Eastern Mediterranean region to the rest of the world.

The discovery of huge natural gas reserves in the East Mediterranean in recent years has whetted the appetite of neighbouring countries. Large fields in the region include the Tamar (discovered in 2009) and Leviathan (2010) in Israel; Zohr (2015) in Egypt; and Aphrodite (2012), Calypso (2018) and Glaucus (2019) in Cyprus. Collectively, they hold almost 200 billion m3 of gas, not including yet-to-find resources.1

Whilst the area has the potential to be a gas province of global significance and drive prosperity for the region’s bordering economies in the coming decades, the demand for oil and gas has exacerbated geopolitical tensions and raised scrutiny on the area’s intentions to address climate change.

According to numerous news reports, there are growing concerns that the proposed EastMed pipeline linking the Aegean’s enormous gas reserves to Europe, which has won EU backing, could lead to more carbon emissions in one year than the Belchatòw coal-fired power plant in Poland, which is viewed as Europe’s most polluting energy project.2 Its aim is to transfer between 9 and 12 billion m3 a year from offshore gas to be pumped between Israel and Cyprus to Greece, and then on to Italy and other southeastern European countries.

As part of DNV’s annual outlook report for the global oil and gas industry: “Turmoil and Transformation: The outlook for the oil and gas industry in 2021” the independent energy expert and assurance provider produced a dedicated East Mediterranean report.3 This presents an overview of the region’s activity, sentiment on digitalisation and decarbonisation, as well as future investment intentions.

East Mediterranean projects DNV’s Energy Transition Outlook estimates that global oil will decline gradually and still supply 16% of world energy in 2050.4 The important question is how the industry in the East Mediterranean can and will respond if demand grows or falls faster – or slower – than expected. With such a diversified industry, and organisations moving in a number of different strategic directions, there is no universal answer; what will be a driver of better prospects for some organisations in the industry, will be a barrier to growth for others.

We see signs of this in DNV’s survey findings, where over a quarter (26%) of respondents say that the outlook for oil and gas supply and demand is the factor that most positively influenced their assessment of their own organisation’s prospects for 2021. The global economy and the oil price are the top barriers to growth for East Mediterranean respondents, with concerns around the global economy being significantly higher than globally (Figure 1).

DNV’s forecast suggests an increasing pivot away from oil and towards gas. In the survey, 39% of respondents in the region say their organisation is increasing investments in gas projects (compared to 37% globally).

The Levant basin has been an explorer’s paradise in the past decade, with giant low-cost gas discoveries. The opportunity to capitalise on these has made the region a magnet for major operators. However, there are challenges around the geopolitical situation and security of supply, which threaten to stall or even block full-scale commercialisation of the region’s resources.

Furthermore, any potential investments come with risks, given the uncertainty around gas demand from the EU’s plan to be carbon neutral by 2050.

Connecting the Mediterranean Across 1900 km, the EastMed pipeline project will link the gas reserves of the East Mediterranean to Greece, Italy and other South-east European countries. It will have an initial capacity to transport ten billion m3/y of gas which is expected to be increased to a maximum of 20 billion m3/y in the second phase.5 In May 2021 it was announced that DNV has been appointed for the design appraisal of the front end engineering design (FEED) output

Figure 1. Comparison of barriers to growth globally and in the East Mediterranean.

Figure 2. Industry confidence has fallen dramatically among East Mediterranean respondents, bringing it in line with global sentiment.

for the offshore and onshore pipeline, and accompanying structures and facilities.

The energy ministers of Greece, Israel and Cyprus signed the final agreement for the £5.1 billion project in January 2020 and it is being developed by IGI Poseidon, a 50:50 joint venture between Public Gas Corporation of Greece and Edison International Holding.

The discussion over the economic viability of the EastMed pipeline has taken centre stage since the very beginning of the proposal.6 The ambition of the contentious project is to improve Europe’s energy security by diversifying its routes and sources and providing direct interconnection to the production fields. It will also support the economic development of Cyprus and Greece by providing a stable market for gas exports. Likewise, it will enable the development of gas trading hubs in

Greece and Italy and facilitate gas trading in southeast Europe. In July, as part of the groundwork, Greece,

Cyprus and Israel leased a research vessel to conduct seismic surveys between Cyprus and Crete, and also between Cyprus and Israel.7 Another major pipeline project is also being considered in Turkey. The country’s Energy and Natural

Resources Minister Fatih Donmez, announced in

July that it plans to construct 169 km of natural gas pipelines across the seabed at the 250 km2 Sakarya

Gas field in 2022. Discovered in 2020 and located 150 km from the Black Sea coast, reserves were initially announced as 320 billion m3, and later increased to 405 billion m3 as a second deeper reservoir was located, with Ankara targeting delivering first gas to customers a year later.8 In June 2021, Turkey’s state oil company unveiled another major deepwater gas discovery in the Black

Sea that will be incorporated into its two-phase

US$3.6 billion Sakarya gas project.9 The fresh Amasra find has boosted discovered gas reserves in this frontier play to 540 billion m3, almost on par with

Chevron’s Leviathan gas discovery offshore Israel.

Gas from the subsea wells on Sakarya will be sent to an onshore processing plant at Filyos in Zonguldak province via a pair of 155 km pipelines.

Crisis and competition There’s no doubt that all oil and gas companies were challenged in 2020. Global demand for products and services had been decimated by the pandemic and the Russia-Saudi Arabia price war forced an oversupply disaster, collapsing prices and pushing US oil into

Figure 3. Green investment intentions differ between those surveyed in East Mediterranean than globally.

Figure 4. Compared to its global counterparts, the East Mediterranean is more focused on short-term rather than long-term strategies.

Figure 5. The oil and gas industry is shifting towards a greener future.

negative territory for the first time in history. The market crash left the entire oil and gas value chain in disarray. As the year progressed, demand and prices slowly stabilised, but far below the levels at the start of the year.

Like other regions, industry confidence has fallen dramatically among East Mediterranean respondents – this number is now close to the global level, after being significantly higher a year ago. Those surveyed are less confident than their peers globally, with 37% stating they were confident about industry growth. This is compared with just 39% globally (Figure 2).

Investing in a greener future The DNV study also shows that focusing growth on the renewables market is a significantly greater priority for oil and gas businesses than decarbonising fossil fuels and/ or operations. However, this is not the case for midstream organisations, where there is bigger emphasis on lowering carbon emissions and operations. Integrated oil companies especially, with operations across the value chain, place more importance in this area going forward.

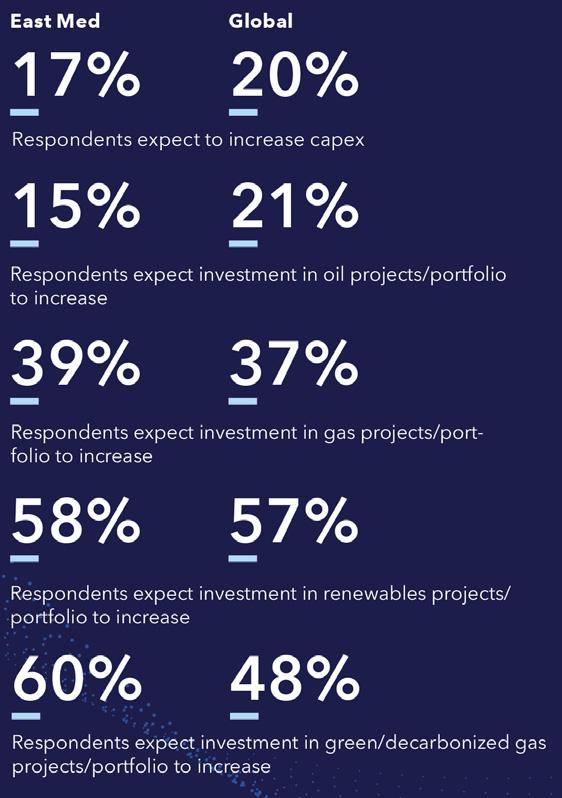

Respondents in the East Mediterranean region are less likely than the global sample to say their business will increase investment in oil projects/portfolios in 2021 (15% versus 21% globally). By contrast, 60% of respondents far more likely to invest in green/decarbonised gas projects/portfolios, compared to 48% globally (Figure 3).

Over the past year, there has been a rise in the proportion of respondents saying their organisation is more focused on the short-term (Figure 4). This is understandable as the pandemic and oil price crash created so many urgent and critical issues. As the crisis subsides, it may well revert to the relatively more even balance reported last year.

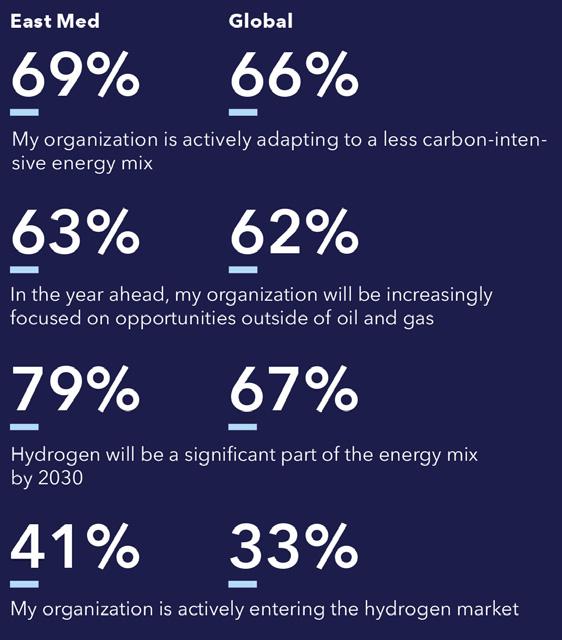

DNV’s research reveals an industry that is increasingly shifting towards decarbonisation and the energy transition (Figure 5). Some 80% of respondents globally reported that they now plan to increase or maintain investments in renewable energy projects and portfolios in 2021 – up from 71% one year ago. Within that, the proportion that are planning increases (57%) is much higher than last year (44%), and far higher than those planning to finance either oil (21%) or gas (37%) in 2021. Overall, 63% of those respondents in the region are now actively looking for opportunities outside of oil and gas – up from 45% a year ago.

Changing attitudes towards a broader energy mix

It is worth noting that gas operations across the East

Mediterranean area are intended to grow in the coming years as benefits from the expansion of new gas fields are realised. However, nearly nine in ten respondents in the region believe that the industry needs to develop new operating models to achieve further cost efficiencies, while three-quarters believe cost cutting will be more challenging than ever in 2021 and beyond. With political tensions abounding between the different players in the region, the East Mediterranean is a challenging and turbulent market, albeit one full of potential with trillions of cubic meters of gas to produce. Therefore, according to industry analysts, the prospects for the wide-scale development of the region remain uncertain, with drilling plans on hold, a setback for Lebanon’s fledgling exploration programme and stubborn geopolitical challenges.10

Ultimately, questions remain as to whether neighbouring nations can move past their differences and establish trustworthy supply routes before EU customers become far more exacting on carbon footprint ahead of 2050’s net zero deadline.

References

1. https://www.woodmac.com/news/the-edge/monetising-the-east-medsgiant-gas-finds/ 2. https://www.theguardian.com/environment/2020/oct/30/scrap-gaspipeline-eastern-med-due-climate-cost-report-turkey-greece 3. https://industryoutlook.dnv.com/2021/download 4. https://www.dnv.com/Publications/dnv-s-oil-and-gas-industry-outlook-forthe-east-mediterranean-2021-200433 5. https://www.nsenergybusiness.com/projects/eastern-mediterraneanpipeline-project/ 6. https://www.euractiv.com/section/energy/news/athens-and-cairo-mullchanging-the-route-of-eastmed-pipeline/ 7. https://www.ekathimerini.com/news/1164383/athens-moves-in-the-easternmediterranean/ 8. https://www.aa.com.tr/en/energy/natural-gas/turkey-to-lay-169-kms-ofseabed-gas-pipeline-at-sakarya-gas-field/33283 9. https://www.offshore-energy.biz/turkey-unveils-new-gas-discovery-inblack-sea/ 10. https://www.spglobal.com/platts/en/market-insights/latest-news/naturalgas/052220-feature-prospects-uncertain-for-further-east-mediterraneangas-development