Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business,

Contact us: profit@pakistantoday.com.pk

By Farooq Tirmizi

However bad you think Procter & Gamble leaving Pakistan is, we suspect after reading this story, you will see that it is worse. There are no two ways to say it, so we will start with the uncomfortable truth first: P&G is important for Pakistan, but Pakistan is not important enough for P&G.

P&G’s presence in Pakistan is perhaps one of the best examples of how a global multinational started off in the country with a miniscule presence and barely any resources and ended up becoming one of the largest manufacturers in the nation. Indeed, P&G had gone from being mainly an importer, to a domestic manufacturer, and had already begun to be an exporter.

It was one of the best examples of attracting foreign direct investment into the country: allow imports to start with, let them build up their market, and slowly they will start manufacturing, technology transfers, and even exports. It was working.

Until it stopped.

This is one of those stories where there is not one person or party to blame. Did the government’s policies drive away the company? They certainly did not help, and we will explain the specific policies that hurt P&G’s business. But a detailed examination of the company’s financials indicates a much more complex story, one that indicates that Pakistan’s consumer goods market may be a lot smaller, and growing a lot slower, than the headline numbers may indicate.

In this story, we take a look at what P&G built in Pakistan, and how they moved from importers to manufacturers and net exporters. We then examine the recent downturn in the company’s performance in the Pakistani market, as well as its generally sluggish growth globally. Finally, we take a look at reasons why P&G may have made the decision to leave the country.

Procter & Gamble in Pakistan

P&G is one of the largest consumer goods companies in the world and the owner of a set of brands that tend to be among the dominant ones in their respective market segments. It started life in 1837, when two Irish immigrants – William Procter and

James Gamble – to Cincinnati, Ohio in the United States met each other through their wives: Olivia and Elizabeth Norris. Prior to meeting, Procter had been a candlemaker and Gamble had been a soap maker. Their father-in-law Alexander Norris persuaded them to become business partners, which is how Procter & Gamble was founded – as is still headquartered – in Cincinnati.

The company owns such iconic brands as Always, Ariel, Gillette, Head & Shoulders, Olay, Pampers, Pantene, and Vicks, in addition to many others. It owns 20 brands that each individually have sales exceeding $1 billion.

It started its existence in Pakistan on August 5, 1991, when it first imported a set of cleaning products into the country for the first time. Since then, for much of its history, Procter & Gamble remained largely a trading and branding presence in Pakistan.

Its Pakistan operations in its early years were mainly a corporate office that would help market its brands to a Pakistani audience, with a handful of employees who helped import the products from manufacturing facilities around the world, and then distribute them through large distribution companies in the country.

Over time, it has consolidated its operations and expanded them, setting up lo -

cal manufacturing for a variety of products, including Ariel, which was the first product the company started manufacturing locally, and Safeguard. Over the first 25 years of the company’s presence in Pakistan, it invested $150 million into local manufacturing facilities to help localise its revenue streams.

In 2013, the company’s global parent announced a list of top 10 emerging markets on which it would focus over the next decade for investment, and Pakistan was on that list. In an interview with The Express Tribune, P&G Pakistan Country Manager Faisal Sabzwari said: “We have a very clear intention that we will continue to increase localised manufacturing in Pakistan.”

Among the factors he cited for the focus on Pakistan: urbanisation and a youth bulge. “If you compare the urbanisation rate in Pakistan with other developing countries, you will see that we are getting urbanised faster than others,” said Sabzwari back then. “Pakistan is one of the top countries adding 20-year-olds to the world, and these are the people establishing new families and helping market sizes grow,” he added.

In 2019, the company announced that it would invest $50 million in the local manufacturing of Pantene and Head & Shoulders brands of shampoo locally, through a 58-acre production facility locat -

ed at Port Qasim.

At the time, Sami Ahmed, vice president at P&G Pakistan said, “We are committed to contributing our share in the economic development of the country. Our latest investment is testimony to our longterm commitment to Pakistan. For over 25 years, we have been serving consumers with high quality products and have made significant investments of over $150 million in fixed assets to date while nurturing and developing Pakistan’s finest talent and making them business leaders.”

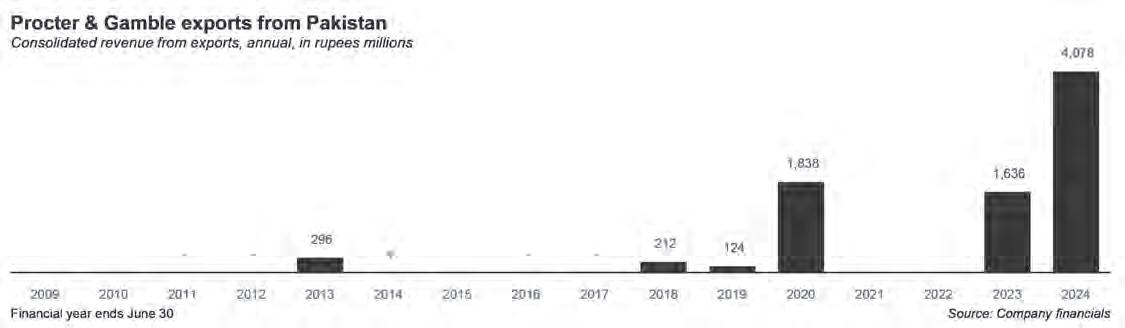

Later in 2019, the company achieved another milestone: not only had it gone from ceasing its imports of Safeguard from other countries and started local manufacturing of the product, but it also began exporting Safeguard from Pakistan to 20 countries in Europe. For the financial year ending June 30, 2020, total exports of Procter & Gamble Pakistan products clocked in at Rs1,838 million ($11.6 million), the bulk of that being the exports of Safeguard.

That is correct, ladies and gentlemen: Pakistan did a complete 180-degree turn on Safeguard. It went from being an importer, to being a domestic manufacturer, and now to an exporter.

“This is an important milestone for our local operations. Our plant in Pakistan

is one of the few locations in the P&G world where Safeguard is manufactured and exported from and it is the only site from which P&G is acquiring Safeguard for export to Europe,” said Sami Ahmed at the time. “Since the establishment of our soap manufacturing facility in Hub over 20 years ago, this facility has served Pakistani consumers with high quality products that has improved everyday life which has now become a lucrative export item as well.”

The manufacturing juggernaut

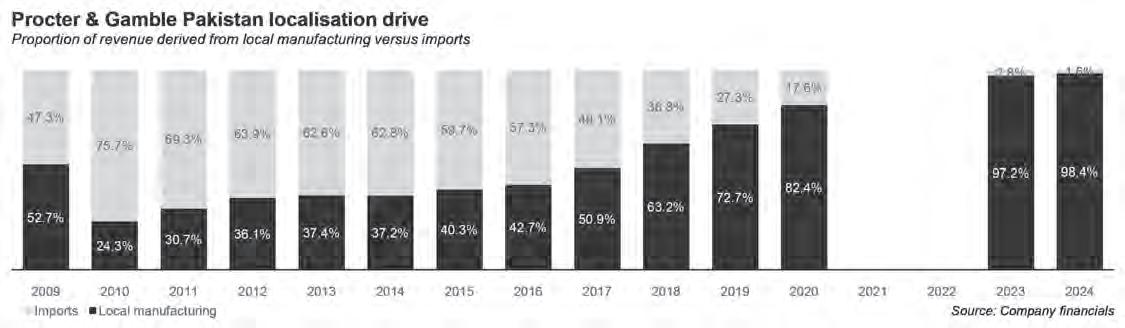

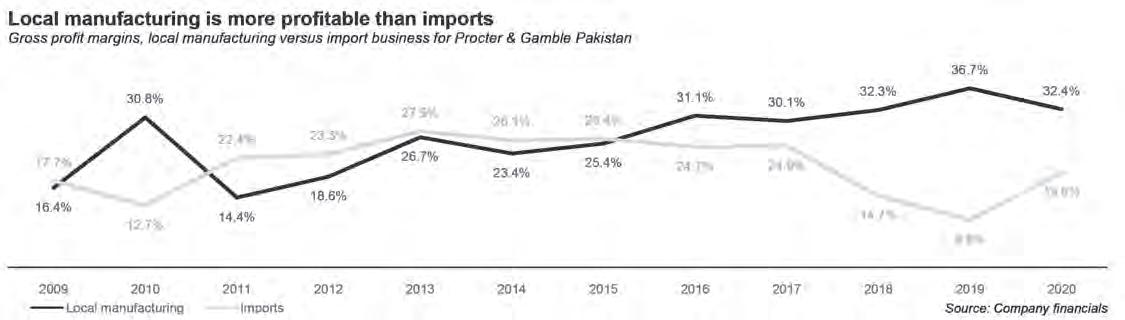

Over the past decade and a half, Procter & Gamble has completely turned around its business strategy with respect to imports versus local manufacturing. In 2010, more than 75% of the company’s revenues came from imports and less than 25% from local manufacturing. By 2024, the latest year for which financial statements are available, those numbers had been more than reversed: more than 98% of its revenues now come from local manufacturing and less than 2% from imports.

And unlike, for example, the automotive industry in Pakistan, which imports more than 50% of the price of the car, P&G’s manufacturing really was almost

entirely local: less than 5% of the total cost of production involved imported raw materials. If you bought a P&G product, you were paying employees and suppliers almost entirely within Pakistan.

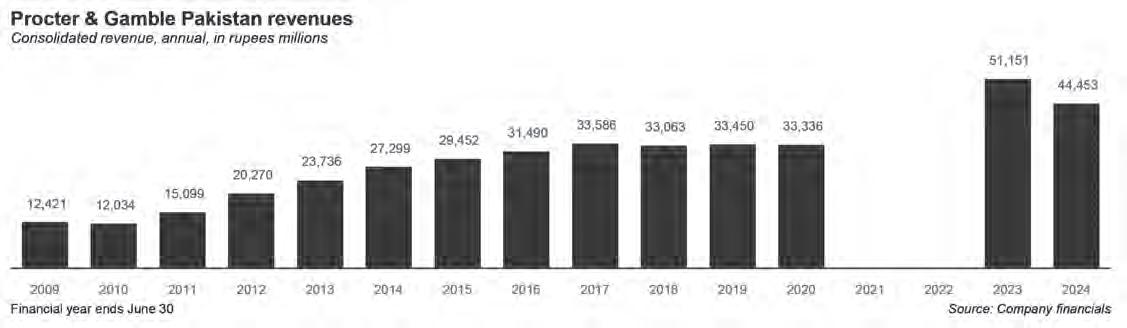

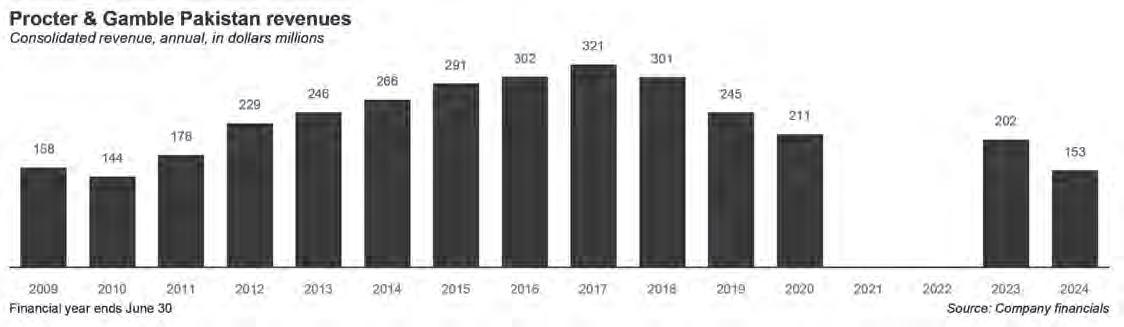

And the size of the business is nothing to sneeze at either. In 2023, the company clocked in Rs51 billion in revenue, which would make it comfortably one of Pakistan’s top 50 manufacturing companies. Revenue then declined in 2024 to Rs44.5 billion, but this remains a sizeable company, and one that was beginning to export some of its production.

Unfortunately, the plant that was engaged in the exports – the soap manufacturing unit in Hub, Balochistan – was sold to Nimir Industrial Chemicals in September 2024, for Rs816 million. So what happened?

Financials: weaker than they look

When Profit last did a deep dive into P&G Pakistan in January 2021, the company was coming off a 5-year period where its revenue essentially did not grow at all. And while we do not have the financial statements for 2021 and 2022, the data from 2023 and 2024 indicate that the company did eventually break out of its

performance slump, with revenue growing 53% between 2020 and 2023. That sounds impressive until you realise it is a 15.3% annual average growth rate at a time when inflation averaged 19.8% per year.

And the numbers must look absolutely abysmal to P&G’s holding company, which is based in the United States and hence measures its revenue and profits in US dollars. On that metric, P&G’s revenue in Pakistan peaked in fiscal year 2017 at $321 million, and since then have declined every single year, and hit $153 million in 2024, the latest year for which numbers are available. That number is especially abysmal when one considers the fact that it is lower in USD than the company’s revenues in 2009, when it made $158 million in revenue. Effectively, all of the gains made in building up its market from 2009 through 2017 was wiped out over the next seven years.

(Note: Profit’s convention for converting income statement figures into US dollars is to divide the rupee number by the average exchange rate over the year in question, using the open-market exchange rate, as published in Business Recorder every trading day.)

What caused this slump?

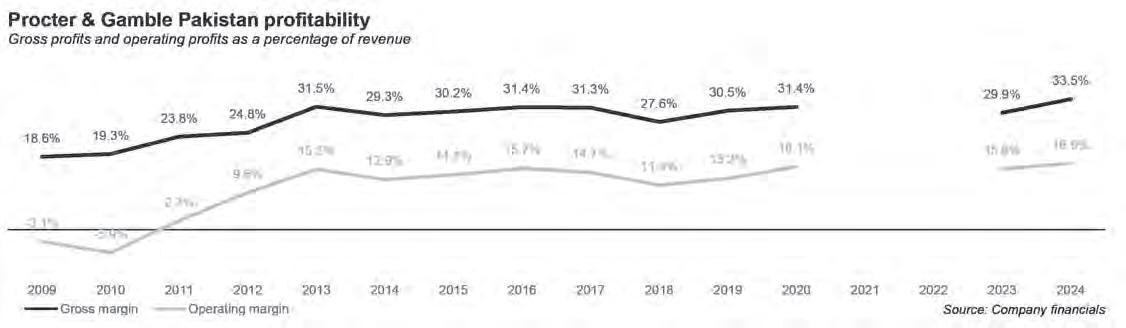

Could it be competition from other brands? This one can be ruled out. Gross margins during this whole time were

remarkably steady, which means that the company did not face enough competition to feel the need to cut prices in order to grow.

Could it be that P&G made a mistake in not cutting prices and was therefore losing market share? It is possible, but unlikely when you consider the fact that it maintained gross margins while growing revenue by less than inflation, because that combination of data points represents two things:

1. It did not feel sufficient pressure from lower priced competitors to cut prices that would eat into its margins.

2. It also did not arrogantly continue increasing prices beyond what the market would be willing to bear, which we know because its revenue increased by less than inflation even as total production increased, meaning the unit price got cheaper relative to overall inflation levels in the country.

That second point may be the key to understanding what happened: P&G’s brands have enough strength that they do not need to engage in a price war with other companies, but they cannot defy economic gravity. The consumer’s ability to withstand high consumer prices was declining substantially, and that got reflected in P&G’s financial results in the form of declining revenue, as measured in USD.

Is P&G overreacting to a cyclical eco -

nomic slowdown in Pakistan? Possibly, but look at the data from P&G’s perspective. They invested about $94 million in Pakistan starting around 2019, shortly after their best year in the country. But then after that, their revenue – as measured in their home currency – keeps declining every single year for the next eight years.

That feels like an investment that just is not working out. How long can a company wait for the returns on its investment? Eight years is not a hasty decision. It seems like a measured response to what the data indicates, which is that Pakistan may have demand for P&G’s products, but likely not enough to continue investing in the country.

P&G’s global struggles

As tempting as it might be to look at just the local context, the fact of the matter is that the decision to pull out of Pakistan was likely made by someone looking at P&G’s global financial performance, not at Pakistan in isolation. And on that front, the news is rather clear. Over the past 10 years, P&G’s revenue growth has come entirely from its home market in the United States, while

its revenue from the rest of the world – as measured in US dollars – has declined.

The numbers are rather stark: US revenue for the 10 years ending June 30, 2025 grew by about 4% per year, but overall revenue grew by only 1% per year during that same period, meaning that the US was carrying the weight of the non-US markets as they declined.

In other words, P&G can grow faster by getting rid of its non-US businesses. So that is exactly what they are doing. P&G has been publicly disclosing to its shareholders for several quarters now that it is undertaking a review of its global portfolio and would be shedding assets as a means of focusing its energy and resources on its strongest markets.

Pakistan is simply one of the many markets from which it will be exiting.

What comes next f or P&G’s assets in Pakistan

This then leaves the big question: having already invested in setting up manufacturing facilities in Pakistan, what happens now? Will P&G simply shut them all down and leave? Will Pakistan have to begin importing

products it was previously manufacturing domestically?

Luckily, given the fact that P&G has already sold its soap manufacturing plant in Pakistan to Nimir, we have a reasonable estimate of what is likely to come next, which is – in some ways – less catastrophic than the news might appear at first glance.

In the case of the Nimir deal, P&G sold the factory as an asset to Nimir. It then gave a contract to Nimir to keep manufacturing the same product (Safeguard soap) and even label it the same name, with P&G retaining ownership of the brand.

Here is how Safeguard is working right now: Nimir manufactures the soap in the plant that was previously owned by P&G. It then sells the finished product to P&G’s exclusive distributor in Pakistan – which is the Pakistani subsidiary of the Abu Dawood Group of Saudi Arabia. Abu Dawood will then distribute Safeguard all throughout Pakistan, same as it did while P&G directly owned and operated the factory in Hub.

As part of its cost, Nimir will pay a licensing fee to P&G for the brand, and for technical assistance in manufacturing the product should any future changes be needed to the production process. Everything else stays the same.

This is the most likely formula for how P&G’s other two factories. The one in Port Qasim manufactures Pantene and Head & Shoulders, its best-selling shampoo brands, and the one in Korangi, Karachi, manufactures Pampers (diapers) and Always (feminine hygiene products). It is unclear who the buyers will be at this stage and P&G has about a year to find suitors. But when it does, Pampers, Always, Pantene, and Head & Shoulders will continue to be manufactured in Pakistan, largely with local raw materials and labour, the same as it is right now.

What changes then? The P&G Pakistan headquarters staff in Karachi will ei -

ther be laid off or moved to Dubai, as brand management and technical supervision moves entirely off shore. The actual job loss will be less than it appeared at first glance from the announcement.

One more substantive thing will change: while P&G’s factories are currently working at between 40% and 50% capacity utilization rates, when they start reaching their limits and need expansion, the capital for the expansion will not come from P&G but rather the local company who owns the plant (such as Nimir for Safeguard). In other words, P&G’s financial risk for these business lines is going to be much lower, since it will not be the one putting up the money to expand them.

If, at this point, you are tempted to think that this may not be so bad, hold that thought. The core set of reasons that compelled P&G to leave still say something bad about Pakistan, the fact of the company leaving will still hurt the country, and while the government of Pakistan is not the main cause, it certainly did make matters worse.

Why the departure matters for Pakistan

The broadest possible way to summarize the data we presented above is that Pakistan’s middle class grows in fits and starts, and is not a linear progression upwards. The government’s obsession with trying to control inflation through the exchange rate has created a highly distorted economy and one that is prone to extreme shocks. Our economic booms are followed by very sudden, and very sharp, recessions, and they seem to have gotten worse over the past two decades.

That means that the number of middle class consumers that would be customers of companies like P&G expands and shrinks, meaning that the risk associated with setting up a factory in Pakistan is higher

than in an economy where growth might be slower, but more steady. This is why P&G is not leaving the Pakistani market, but it is taking measures to shift the risk of setting up a factory in Pakistan.

That, more than anything else, is the worst thing about this departure. It says that Pakistan is a market you want to sell to, or maybe buy from, but one where the risk of investing serious amounts of capital in setting up productive capacity is too high. That even a company with decades of in-market experience cannot make it work.

So even though Head & Shoulders and Pampers will still be locally made, the next stage of the leap beyond this level of productive capacity is now uncertain. Will whoever buys these factories have the capital and risk-taking appetite to grow them? Will they have the appetite to seek P&G’s cooperation in taking these factories to the next level and try to compete for P&G’s regional production goals, meaning making the product fully export-worthy?

Maybe, but the uncertainty around the answer is greater than it would have seemed had P&G never left.

And finally, while these are factors not entirely in the government’s control, it really would be nice if the government were able to come up with a better way to control inflation than messing with the currency exchange rates, which cause wild gyrations in the purchasing power of ordinary Pakistanis. We do not expect them to change their behaviour, so we will not dwell on this point too much.

The British economist Charles Robertson once told Profit that Pakistan needs to graduate from being a trade to becoming an investment. A trade being a short-term transaction, and an investment being a long-term place to park one’s money.

What P&G did this past week was to downgrade Pakistan from being an investment to being a trade. And that, for Pakistan, is a crying shame. n

The mistake was admitted within 24 hours, however, the damage seems to have been done

By Zain Naeem

Aseemingly simple arithmetic error has landed the Treet Corporation in trouble with investors and possibly the subject of an investigation by the Securities and Exchange Commission of Pakistan (SECP).

Treet announced its financial results early in the afternoon of the 30th of September. After posting a loss of Rs 11 crore the previous year, the company had managed to make Rs 1 billion profit this year. The excitement was compounded when the earnings per share were listed in the document as Rs 4.8 — up from Rs -0.49 the previous year.

The results caused a bit of a rally. Treet’s share price, which had been trading at Rs 29.8 before the results were announced, began to move upwards. It eventually touched a high of Rs 32.65. The stock was trading near its upper lock which means that it had seen a price increase of 10% and could not go any higher than that for the day.

Investors that had Treet in their portfolios were buoyed. The improvement in yearon-year performance had increased interest in the stock. The price of the stock closed at Rs 31.85 and there was a feeling more investors would gravitate towards Treet stocks when the markets opened today (Wednesday October 1st).

That never happened. Before the markets opened the next day, Treet put up an announcement on the Pakistan Stock Exchange. They had been mistaken. The earnings per share rate of Rs 4.8 was a miscalculation. The actual number was Rs 2.82.

The mistake was significant enough that after Treet made the revision, the share price fell back to the levels it was at before the results had been announced on September the 30th. The company was trading at Rs 29.8 before the announcement and fell back to the same levels after the correction was made.

Caught in the lurch were investors who had bought shares in Treet on the basis of their mistaken results. Once the revision was made, they would have seen immediate loss in their investment due to a calculation error made by someone at the company.

As a result, the SECP has received multiple complaints about the error. Reports from within the SECP claim the commission has begun collecting data to determine what to do next. No formal investigation has been launched yet, and it is expected for the SECP to track and look into any unusual changes in stock price.

But questions remain. How did the mistake come about? Is there any remedy for investors that were misled by the announce-

ment? And is a company liable for misrepresentation even when it claims it was an honest mistake?

The sequence of events

The mistake seems quite simple. Treet had scheduled a meeting for 2PM UAE time on the 30th of September to announce their results. The meeting was being held in Dubai.

The next morning, the meeting was brought forward to 11 30 AM UAE time. There had already been some excitement surrounding the announcement since investors were expecting improved results from the previous year.

Less than 45 minutes after the start of the meeting, the results were announced. At 1:10 PM Pakistan time, it was announced that the company had ended up making a profit of Rs 1 billion. This was a huge turnaround from the loss made last year of almost Rs 11 crores. The earning per share had gone from -0.49 per share to Rs 4.8 per share in 2025.

The market rallied and the stock price began trading near its upper lock. But someone at Treet eventually realised they had made a mistake. Sometime between 3 30PM on the 30th of September and 8AM on the 1st of October, Treet sent a new notification to the stock exchange.

We do not know the exact time that the new notification was sent. While the responsibility to make all material announcements rests with individual companies, the PSX has developed a system called PUCARS (Pakistan Unified Corporate Action Reporting System) which allows the company to report their corporate announcements directly to the exchange.

In the past, physical notifications had to be sent by the company to the exchange on their official stationery which would then be forwarded by the exchange to the investing public. PUCARS was developed to cut down on the time it took to disseminate this information and would make the announcements in a swift manner. This system shuts down after 3:30 PM and starts operating again at 8:00 AM the next day.

From the close of day on Tuesday to the start of business on Wednesday, no company could upload any new notification to the exchange. In the space of 16 hours, someone at the company realized that a mistake had been made. Treet had earned Rs 1 billion in profits, however, the number of shares taken to calculate the earnings per share had been taken to be much lower than the actual number of shares the company had outstanding.

Earnings per share is a shorthand metric that is used by companies to disclose

how much profit they have earned based on the number of shares they have issued. The financial markets operate on an understanding that everything has to be relative and has to be put into context of the market as a whole. So if a company makes a profit of Rs 1 billion but has 1 billion shares, it will have an earnings per share of Rs 1. Meaning a shareholder will have made a single rupee from every share they own. Similarly if another company makes the same profit of Rs 1 billion but with 100 million shares, the earning per share will be Rs 10. The higher the earning per share the better a company is for investors.

As the PUCARS became operational at 8 AM, the announcement was made that Treet had made a mistake and had stated that its earning per share had been recorded as Rs 4.8 per share. In actuality, a typographical error had been made and the company should have stated its earning per share as Rs 2.82.

This announcement led to more questions being raised. How did the company end up making such a huge mistake? What was the error that led to the earning per share being recorded incorrectly?

The profit earned by the company was around Rs 1 billion. In both the statements, the profit stayed the same. The error was made in the shares that were considered for the calculator. The company had 371,028,800 outstanding shares. If these numbers of shares had been used, the earning per share should have been Rs 2.82. In the earlier announcement, the number of shares used seem to be around 217,816,667 shares.

So where did this figure come from and how could 154 million shares be ignored?

The reason for the mistake

It seems like the people at the finance department at Treet failed to polish up on their financial fundamentals.

One important thing to note here is that the number of shares considered in the calculation are supposed to be the average number of shares outstanding over the period of the year. This is a correction made to the formula as it will allow any additional shares being issued during the year to be taken into account. If the company had 100 shares at the start of the year and 200 shares at the end of the year, the best course of action is to take 150 shares in the calculation to make sure that an average of these two figures is considered. This is added to make sure that the true number of shares are reflected rather than understating or overstating the number of shares.

The error that has been made here is rooted in something that happened almost two years ago.

Back in 2023, Treet had 178,721,100 outstanding shares. Between 2023 and 2024, the management decided to carry out a right share issue to the tune of 107%. This meant that for every share held, the investor was going to get 107 additional shares for which they would have to make an additional investment of Rs 13 per share in order to avail this facility. An investor holding 100 shares was going to get 107 right shares and would have to make an investment of Rs 1,391.

Once the right share had been made, the number of shares were going to jump from 178 million to 371 million. To keep things relative, the earning per share in 2023 should have used the 178 million figure and the number of shares should have increased in 2024. This is where the first error was made. In the annual report for 2024, the company should have used the 178 million figure when it was reporting its earnings per share of 2023. In the accounts of 2023, the earning per share was Rs 0.75. In the next report, the earning per share fell to Rs 0.61. This was due to the fact that the company took the revised average shares for both 2024 and 2023 which should only have been considered for 2024. The right share had not taken place by June 2023 and due to that those shares should not have increased.

A cursory view of the accounts would have allowed the finance department at the company to realize its mistake. The weighted average shares for 2024 were accurate as Treet had deposited the shares in January of 2024 which should have been weighted and then taken into consideration. The weighted average number of shares came to around 217 million.

If this mistake had been caught on earlier, the recent mistake could have been prevented. This never happened. The formula used for 2024 was copied and then used for 2025 as well. Due to this mistake, the formula took 217 million shares when the true number of 371 million shares should have been taken. The number of shares stayed the same throughout 2025 which meant that the average would have remained the same from July 2024 to June 2025.

This was not done and the same weighted average number of shares considered for 2024 were again taken for 2025. This was a compounding of two mistakes. The figure for 2023 should have stayed lower leading to higher earnings per share in 2023 as shown in the annual report of 2024. As the same number of shares were carried forward for 2025, the earning per share ended up being overstated when they had been much lower.

The error seems to be caused by a haste and lack of proofreading while preparing the accounts which ignored the basics that had changed from 2023 to 2025 and failed to take

everything into account.

A representative at Treet was contacted in relation to this. The source stated that the matter was being investigated currently and the results will be shared once it has been looked into thoroughly. The source also stated that the market performance of the company before the announcement was contingent on the fact that a bonus was expected. Some of the price decrease was also due to the fact that no such entitlement was announced.

Treet’s tough spot

In terms of repercussions and consequences of this mistake, it is expected that the Securities and Exchange Commission of Pakistan (SECP) will look into this issue in order to reprimand the company that has made such a mistake. Only after an action has been taken will investors be given assurance that regulators are looking out for the investors and that anyone who makes such a costly mistake will be made to pay for it.

A contrarian view that can be stated in this case can be that well when so much money is involved, why would investors not double check what they are being presented and verify the results that are being disclosed? The answer to that is reaction time. The stock market and its trading is measured in a matter of seconds. The market reacts to any new information instantly. If people start to doubt and question the information they are being presented, they will lose out on the ability to make a profit.

The dictum at the market is “you snooze, you lose”. Be a second late in reacting to an opportunity and lose out on making money. Even the reaction of the market following the announcement shows that the share price jumped by almost 10% in less than an hour. People who would have missed out on buying at Rs 29.8 would have lost out on making a good amount of profit.

For Treet, what appears to be a mistake in calculation is sullying what should have been a moment of recovery for them. The time before their ill-fated announcement on the 30th of September was one of optimism. The company has long dominated the local steel blade market and claims a huge chunk of the market share. Due to this, it feels that it has a steady stream of revenues that it can depend upon. There have been efforts made in the past where they have tried to diversify their company profile, however, it has always made sure the blade business was its cash cow.

In its initial years, the company was providing a cheap alternative to the market which was looking towards high quality imports in order to fulfil their need. Treet identified a market gap as they were the only ones who were able to provide high quality products at

a much cheaper price. Due to its high standard at a low price, barbers around the country start to rely on Treet. This was the reason which led to the success of Treet as the company expanded its production footprint.

Recently, the company has faced some challenging times. There has been a trend for men to grow beards and to shun the blade in the name of fashion. The impact of this can be seen on the sales volume of Treet as it has seen its sales shrink in response to this. So what did Treet do to counter this trend? They started to go from low margin, high volume strategy towards high margin, low volume one. This meant that as their sales started to decrease, Treet was able to charge a higher price leading to higher profits being earned per unit.

This fact can be seen in the fact that in 2010 the gross margins had fallen to 18% which have consistently been above 30% since 2019. WIth similar costs, Treet is charging a higher price for its product which is leading to higher gross margins. In conjunction with this, production for the company has steadily decreased from 2 billion blades in 2021 to 1.7 billion blades in 2023.

In the same period, the revenues of the company went from Rs 7.5 billion in 2021 to Rs 11 billion in 2024. Even with a decrease in production of 30%, revenues actually increased by 46%. Based on the growing revenues, it was expected that the same trajectory would continue and Treet would see better revenues in 2025 as well.

Another reason for optimism around the company and its results was higher administrative and marketing expenses due to inflation in the country. These costs were compounded by interest rate expenses which were increasing as interest rates were increasing in 2023 and 2024. June 2024 saw the highest interest rates in the country in the history of 22%.

The impact of these costs was that operating margin fell from 14% in 2023 to 8% in 2024 while net margin went from 1.3% in 2023 to -1.7% in 2024. The net margin in 2023 was already on the downward trend as it was 11.6% in 2022. This constant decrease was caused by finance cost which was 10% of sales in 2022 increasing to almost 15% in 2023 and to 17% of sales in 2024. Since June 2024, the interest rates halved from 22% to 11% by June of 2025.

As it was expected that a major chunk of finance cost was going to decrease, it was expected that the company would be able to announce better results for the year 2025. This was clearly the case because the problem was never the profit they had made. While the mistake regarding the earnings per share was admitted within 24 hours, the damage was very much already done. n

The Audi Pakistan controversy: How not to deal with a disgruntled customer

Premier Systems, the official importer of Audi AG in Pakistan, dealt with a loud and disgruntled customer by suing him for criminal defamation. Now, the customer has responded in kind. Here is what happened

By Abdul Hameed Niazi

The customer, it seems, is not always right. At least that is what Audi Pakistan would have you believe. In fact, not only is the customer not always right, sometimes the customer is so wrong they deserve to be slapped with a criminal defamation suit.

Just over a year ago in July 2024, Naeem Afzal received notice that he was the defendant in a criminal defamation case under Pakistan’s draconian defamation laws. These laws govern the expression of thoughts and opinions in print, as well as on social and electronic media in Pakistan. In most countries, defamation is a civil matter not a criminal one. In fact, even in Pakistan most defamation cases are tried in civil courts. But because these criminal defamation laws exist, a person can be accused in a much more serious criminal trial that requires them to appear in court regularly under threat of arrest.

Naeem Afzal’s accuser was a company called Premier Systems Pvt Limited. Premier is the official importer of Audi AG, the German luxury car manufacturer, in Pakistan. They also exclusively operate the several Audi

showrooms all over the country. Premier runs on a very basic business model. Audi AG has them listed as their official import partner in Pakistan on their website. They market Audi AG products in Pakistan and when a customer walks in looking to get hold of an Audi car, they take an advance payment and place an order with the manufacturer in Germany. Premier gives the customer a timeframe for how long it will take to import the car and the remaining payment is made upon delivery.

That is the relationship that was first established between Naeem Afzal and Premier in May of 2022. But how in the world did this seemingly simple transaction snowball into a messy legal battle stuck in three different civil and criminal courtrooms, with arrest warrants issued for both parties? More importantly, exactly what makes a company sue their client in a criminal capacity, and can it possibly be considered a good business strategy?

Importing hazards

The story starts simply enough. Naeem Afzal wanted to buy an Audi. A resident of DHA Lahore, he went to Askari Towers off Liberty Chowk and walked into the Audi showroom. He met with a representative of the dealership, he told

them what car he wanted, and they told him they could get it for him. On the 16th of May 2022 he put down a deposit of just over Rs 1 crore (Rs 1 crore 3 lakhs and 29 thousand to be exact) for an Audi E-Tron 50 Quattro.

The colour was supposed to be Manhattan Grey.

He paid with a banker’s cheque issued by Habib Metropolitan Bank DHA Phase VI Branch. The pay order was made out to Premier Systems (Private) Limited. The offer letter he received had the letterhead and branding of “Audi Pakistan”. All pretty run of the mill.

It turned out this was the worst possible time to try and buy an imported car. Three days after Naeem Afzal put down the deposit, the government of Pakistan formally announced it was running out of dollars. The State Bank’s foreign exchange reserves were running on fumes and with loan repayments just around the corner, the word default was being thrown around quite casually.

The government’s answer to this was to shut everything down until they had time to think. A ban was imposed on all but the most essential imports such as fuel. Luxury cars were the second item named on the list. In the offer letter sent by Audi Pakistan to Naeem Afzal, the expected delivery time was men-

tioned as 30-32 weeks. With the temporary import ban now in place, it was likely to take longer.

In the meantime the Rs 1 crore deposit remained with Premier. At the time this accounted for about 60% of the car’s value. Premier’s estimate had placed the final price at around Rs 1.72 crore including all duties and taxes. This price was subject to change depending on the exchange rate or any change in the taxation schedule. Premier as an importer makes payments to Audi AG in Euros. Because of the volatility of the rupee, the sales contract for Audi and other luxury cars always include a devaluation clause protecting the importer from forex shocks.

Naeem Afzal was well aware of this. When the import ban hit, the value of the rupee was also dropping fast. He knew the devaluation cost would hit him eventually. He kept in touch with Premier and they continued to give him updates. In July 2023, 76 weeks after Naeem Afzal made the Rs 1 crore deposit, Premier told Naeem Afzal he could have his car in December if he agreed to get it in black instead of the grey he had ordered it in. He agreed. Premier said the car would arrive at Karachi port by the end of December.

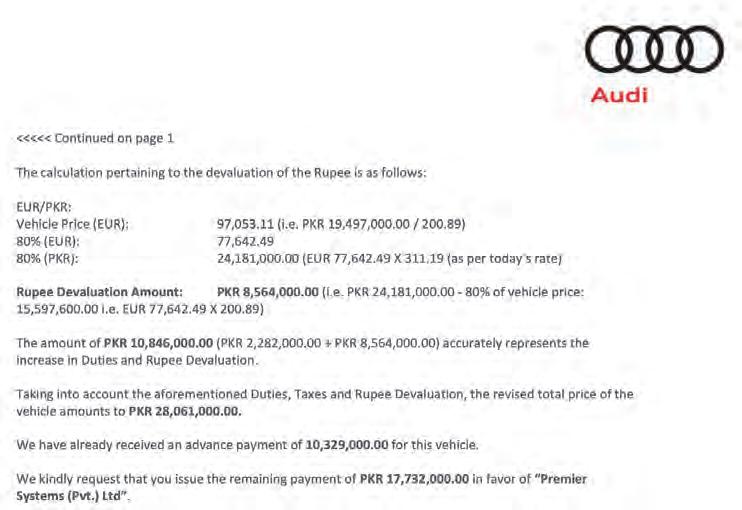

On the 4th of December, they sent a revised estimate for the final price of the car. The devaluation charges were high. Much higher than Naeem Afzal expected. In fact, according to Naeem Afzal, the devaluation charges were applied not just on the 40% remaining payment, but also on the initial Rs 1 crore he had paid. This quickly became a major sticking point between both parties.

Look at it this way. Naeem Afzal had paid Rs 1 crore in May 2022 which was supposed to be 60% of the cost of the car. The price of the Euro was Rs 200.8 on the day the deposit was made. In his mind, that Rs 1 crore was worth €51,371. At the time, the estimate for the car including duties was Rs 1.72 crores. If we convert even that entire amount (including the duties meant to be paid in rupees) into Euros the price of the car comes out to €85,693. That means his maximum remaining payment was another €34,322 or Rs 72 lakhs. By the time the car was ready to arrive in December, the exchange rate had gone up to Rs 311.19. This meant the remaining Rs 72 lakh was now Rs 1.06 crores. On top of this, as the revised estimate sent by Premier details, another Rs 22 lakhs had been added in new duties. The price of the car had gone from the estimated Rs 1.72 crores in May 2022 to Rs 2.31 crores in December 2023. Since a little over Rs 1.03 crore had already been paid, Naeem Afzal assumed he would have to pay another Rs 1.29 crores to get his car.

He was wrong. Premier’s revised estimate asked him to pay Rs 1.77 crores – nearly

Rs 50 lakhs more than what Naeem Afzal expected, bringing the overall price of the car to Rs 2.8 crores. What was Premier’s logic? While the company did not speak with Profit on the record, we were able to get some information from senior Premier executives on the condition of anonymity. This executive explained to Profit that the Rs 1 crore was simply a deposit meant to function as a holding price on the order. It did not indicate partial payment on the vehicle. In other words, if you wanted to park an Audi in your garage, you first had to park Rs 1 crore in Premier’s bank account.

While no official comment came from Premier, this dispute was discussed in an email exchange between Naeem Afzal and Syed Farhan Hassan, the company’s Country Lead, and the executive that had been in touch with Naeem Afzal throughout this time. In this email thread, one statement from Farhan Hassan is quite clarifying.

“The advance payment made at the time of the vehicle order is a minimum requirement for booking the vehicle. The percentage of the advance payment is irrelevant because, upon arrival, we will assess customs duties, taxes, and the exchange rates in effect for the vehicle,” it reads. “Any corresponding charges due to changes in duty, taxes, and/or exchange rate fluctuations will be passed on to you. If there are no changes in customs duty, taxes, or exchange rates, we will not impose any additional charges on our customers. Conversely, if there are decreases in duty, taxes, or exchange rates, we will gladly reimburse you accordingly.”

The message here is clear. That Rs 1 crore was exactly that – one crore rupees. It did not indicate value in euros at the time nor was it

inflation protected. The estimate document from Premier sent to Naeem Afzal is actually a very fascinating document. It provides an interesting calculation that seems to lump together the new duties and convert them into Euros before arbitrarily deciding to calculate 80% of the car’s cost at the original rate and then subtracting that from the 80% cost of the car at the new exchange rate. The document does not clarify why the devaluation charges were applied on only 80% of this total value instead of on the entire 100% (as was being claimed by Naeem Afzal). According to one source within the Premier management, this had been their way of extending a favour to a customer that had to wait longer than expected even though the circumstances of that wait had been out of their hands. The calculation can be seen below.

It’s a favour: In an official revised estimate sent to Naeem Afzal, Premier charged devaluation on 80% of the value of the car. They claim this was a favour to a customer that had to wait longer than expected even though the wait time was not in the importer’s control.

In any case, Premier insisted its remaining payment was Rs 1.77 crores and Naeem Afzal insisted it was no higher than Rs 1.29 crores. The two parties were now locked in a battle of wills.

Where’s my money

Naeem Afzal was livid. He did not understand why his money had just been sitting with Premier losing value when it could have either converted it to foreign currency or at the very least put it in a bank account and gotten interest

off it. Instead, Premier either had that money parked in a bank account and was collecting interest on it, or was using it in their regular cash flows, or had possibly even invested it somewhere. In any case, the money was with Premier and they were now claiming Naeem Afzal would have to pay for the devaluation of that money.

Premier immediately pointed towards the contract Naeem Afzal had signed. Standard Audi sales contracts include clauses that protect them from situations exactly like this. Indeed, there is a price fluctuation clause which shields Premier the importer from any kind of financial hit due to rupee devaluation or duty changes. Premier also claims ownership of the car remains 100% theirs until 100% of the payment is made. Add to that a standard force majeure clause, which protects them from unexpected (but in Pakistan, very expected) delays or expenditures. Then there’s the kicker: the right to cancel the contract rests with Premier.

These contracts are designed exactly for situations like this. It might seem like a harsh deal, but Premier’s iron-clad contract would indicate they are protected from liability in such situations.

When Premier sent him the revised estimate in December 2023, Naeem Afzal said he was not paying a devaluation price on the Rs 1 crore he had paid back in May 2022. The dealership decided they would cancel the contract and send him his Rs 1 crore back. Naeem Afzal did not want this as well. The Rs 1 crore was now worth at least Rs 1.25 crores even if he had done nothing but put it in a savings account. He went to court against the cancellation and got a stay order.

The matter is still subjudice. The legal merits of the case will be determined by the court. One might sympathise with Nadeem Afzal. After all, it was not his fault imports got banned and his money stayed tied up with Premier when he could simply have been collecting interest on it. However, one must keep in mind that the clauses in the sales contract go to great lengths to protect the importer and Audi AG. It is designed to protect against shocks like this. There is no knowing what way the court might lean in this civil case. At this point, one might accuse Premier of pushing some harsh terms on their customers, but is that also illegal?

What happened next, however, is actually quite shocking.

Facebook criminal

What do you do with a disgruntled customer? This single question, more than anything else, is what matters in this story. Up until now we have detailed a dispute

between a customer and a company. No big deal disputes like this are common enough. Anyone in business knows that customers can sometimes be annoying, entitled, unfair, and downright dense.

Perhaps that is how Premier saw Naeem Afzal. Perhaps they were trying in earnest to explain something that he simply was not understanding. And when the matter could not be solved by talking, it ended up in court. This finally made Premier sweat. And no, it was not necessarily because the legal case against them was particularly potent. When Naeem Afzal filed his case, he filed a petition against Audi Pakistan, which was the name of the company he thought he was dealing with. He also made Audi AG, the company in Germany, a party to the case. When he filed this case he discovered no entity by the name of “Audi Pakistan” existed. His complaint should have been addressed against Premier Systems (PRIVATE) Limited. Audi Pakistan was simply a branding term Premier was using on their letterheads and in their communications.

To Naeem Afzal this seemed to be a smoking gun. Up until this entire point, all of the dealings Naeem Afzal had with the dealership was under the letterhead of “Audi Pakistan”. The only time Premier Systems Lim-

ited was mentioned was when he made the Rs 1 crore payment. According to Afzal, when he had asked the dealership what Premier was, he claims they had told him that was the name of their importer without clarifying the dealership itself was run by Premier.

Lady Justice was not the only avenue this customer turned to. Sans money and sans car, Naeem Afzal did the only other thing he could: posting on social media. He became active in groups like Voice of Customers on Facebook which have become the boogeyman for many businesses afraid of getting bad reviews. He started writing emails to Audi AG but received no reply. He took to twitter and began tagging Audi AG with details of the case he had filed against Audi Pakistan and against them as well. Eventually he received confirmation from Audi AG in Germany through a twitter reply and through an email. They said their local partners are completely separate legal and economic entities with no ties to the Audi AG group. They were simply allowed to use the Audi branding because they were displaying their products.

Audi AG uses this technique elsewhere in the world as well. They want to sell their cars in markets that they do not want to enter directly, so they strike a deal with an investor

that becomes their importer in that country. In this case, it was Premier. Audi AG wants to have a “presence” in these countries through these importers and allow them to use their branding without actually having any legal skin in the game. For the local importer, it is a matter of prestige to be running the presence of an international brand with its branding at home. This was turning out to be a problem for Premier. Naeem Afzal’s crusade threatened to sour their relationship with Audi AG, which naturally does not want to have its name dragged in the courts and in the media. On top of this, these import agreements can prove to be fickle. This would not be the first time a luxury car importer would have their position threatened. A few years ago, when Porsche’s importer in Pakistan got in trouble over a similar issue, the Mansha Group wanted to take over the contract from Porsche Germany. This campaign was beginning to hit Premier where it hurt.

But there was no stopping Naeem Afzal. With a background in textiles, Naeem Afzal claims there is a difference between being an importer of a foreign company and claiming you are that company’s Pakistan arm. According to him, the term “Audi Pakistan” was misleading and gave him the impression he was directly doing business with the German car manufacturer and not with an importer. He points towards how other car sellers in Pakistan deal with this.

Mercedes’ official importer, for example, brands themselves as Mercedes Shahnawaz Motors. Similarly, BMW is known as BMW Dewan Motors. Even in the case of assemblers, the names are branded as Toyota Indus Motors, and Honda Atlas Motors. Suzuki is the only company that refers to itself as just Suzuki or Suzuki Pakistan, and that is also because Suzuki Japan owns the majority of the Pakistani company. In all these cases the names these importers or assemblers use are the names of actual legal entities (read companies), but that was not the case for Audi Pakistan. There is no entity called Audi Pakistan registered anywhere.

Naeem Afzal took this discrepancy and ran with it. It is entirely possible that he knew this was the case and had picked up on Premier using the “Audi Pakistan” branding earlier as well. After all, he has been involved in the import-export heavy business of textiles himself for many years. But once his dispute with Premier picked up, he decided to go after them for it. Since the case has become public, Premier has started using letterheads that use the Audi Logo and say “Premier Private Limited” instead of the Audi Pakistan branding.

In Naeem Afzal, Premier had found one of the most annoying things a business can face: a vigilante customer. Most companies

have the good sense to ignore such people. Sometimes they will send a quiet message and try to resolve the issue. Other times they will simply not give it the time of day. If the matter persists and attracts attention they might put out a professionally written statement. Premier’s response was to send a legal notice. It accused Naeem Afzal of defamation and told him to cease and desist and pay them damages. Naeem Afzal’s attorney responded to the letter. Normally, a legal notice is an out of court method employed by companies and people when they feel they are being criticised in public. It is actually quite simple.

A person says something about you on the internet. You send them a legal notice. You don’t actually have to spend money and take them to court but next time someone asks you about the accusation you can simply say “I have initiated legal proceedings and will wipe the floor with them in court”. A legal notice is, after all, the first step to initiating legal proceedings. Once you have that handy line in the bag there is no reason to actually take a contentious matter to court. So if a customer asks you about that man on Facebook that keeps telling him not to do business with you, you can always respond by telling them it is being handled by the lawyers. For that matter, you could even go ahead and pursue a civil case which can then be argued for years in the courts.

But Premier did not stop there. The company went ahead and pursued a case. Not only that, they significantly escalated the situation by filing a case against Naeem Afzal on criminal defamation charges under Sections 499 and 500 of the Pakistan Penal Code. The case was filed in Karachi.

As journalists around the country know all too well, this is a technique used by many to make a defamation case hurt as much as possible. You see, in Pakistan when a criminal case is filed, the defendant has to appear in person in court. The person filing the case, conveniently enough, does not have to do anything of the sort. It is a law designed to hurt the accused and cripple them even before a case is decided upon. Even though the showroom was in Lahore and so was Naeem Afzal, the case was filed in Karachi so he would be forced to undertake the expensive business of travelling to Karachi regularly. By March 2025, the court had issued warrants for his arrest, which by the way is standard procedure in any criminal case to summon the accused by a court.

Naeem Afzal was now implicated in a serious legal battle. The civil case he had filed was not so important. He now had to fight for his name which he felt had been sullied. That was far more important to him than the Rs 50 lakh he had been fighting over up until now. He responded by filing criminal cases of forg-

ery and deception against the leadership team of Premier as well. His argument was the same one he had been making on social media: How could Premier use the name “Audi Pakistan” when they were just an importer? According to him this was criminal misdirection. The entire saga was now spread over one civil court and two different criminal courts.

For Premier, their decision to pursue a criminal case was about to seriously backfire.

Can businesses afford bruised egos?

Let us take a break here for a second. A simple transaction between a buyer and an official importer has become a nasty legal battle. Court cases are nothing new in the world of business but most of them occur at times when there is some sort of financial dispute or fraud involved. Most businesses don’t exactly enjoy having their business dragged around in the courts.

But what did Premier achieve by pursuing this case? On the surface some of it makes sense. Naeem Afzal’s complaints and constant posts against Premier are not great for PR. People actually take reviews and customer feedback on Facebook very seriously. In a fast evolving market for automobiles, they do not want to have their credentials as “Audi Pakistan” questioned and would want to put an end to it. An even bigger problem would be if this affected their relationship with Audi AG in Germany. Premier sent notices to express displeasure and possibly scare Naeem Afzal but it did not seem to have the desired effect.

One might argue that Premier had no other choice. But the results of this single decision are not going in their favour. The first thing to happen was that the added attention from the legal battle resulted in misinformation spreading. On the 19th of September, PakWheels reported that Pakistan’s Customs Authority had suspended Premier’s rights to issue price evaluations on imported Audi cars. This is important because when a used Audi car is imported to Pakistan from, say Japan, customs charges duties based on the value of the car. This value is judged by Audi’s official importer. Similarly if it were a Mercedes or a BMW their official importers, Shahnawwaz and Dewan Motors, would make the assessment. These importers have it in their interest to set higher values since they want people importing cars through them and not directly from sellers in other countries.

The news spread quickly. Speculations began that Premier was in trouble with Audi AG and they might be stripped of their official importer status. Audi customers began to panic. They were worried about what would happen to their warranties and car service if the importer they had bought the car from was

suddenly out of business. With Premier not saying anything, shows began to air on television and posts began to circulate on social media with all sorts of unfounded rumors.

PakWheels said in a story three days later that “Earlier reports suggested that Customs Pakistan had suspended the Premier’s right to set import trade prices (ITPs). This has now been clarified: Premier retains its authority, and ITPs are still being issued by the dealership.”

Similarly, the news of warranties being suspended had no basis. The legal battle had aired what was up until that point a private matter into a public one and the facts of the case were lost in all of the noise.

Then there is another matter besides misinformation. How was this going to affect customer perception? Think of it this way. On the one hand, there is a person out there, a customer, that is saying negative things about your company. Perhaps he is taking personal pot shots against the company’s leadership. A company can be worried this will affect their market and spook away customers. But just how spooky can one guy (not an influencer by any measure, just a regular internet user) be for an entire company that has the backing of an international luxury car brand?

What this does do is create an atmosphere of mistrust. A customer might see a man ranting on the internet against a car brand which could raise some alarms for them. They might want the brand to clarify or ask for an explanation before conducting business with them. But then this same customer finds out that the brand has sued a former customer in a criminal capacity for posting about them on the internet. All of this after the brand was unable to provide the customer with their product at the original agreed upon price. That might actually end up spooking the customer more.

Even when it comes to their relationship with Audi AG, and overly aggressive response that complicates and delays a solvable dispute will not inspire confidence among the German executives.

On top of this, the clientele for Premier is high end. People buying Audis in Pakistan have wealth. No one is spending multiple crores on a car when they don’t have many more lying around. So even though a car manufacturer like Suzuki might theoretically be able to bully their customers, Premier might have a harder time taking on some of their clients. Then there is the fact that any high profile client that might be a public figure would not want to touch a car company with a messy legal battle on their books with a ten foot pole.

The noise around the criminal case and Naeem Afzal’s crusade on social media seems to have done more damage for Premier. Details of the case were warped. Existing Audi customers began to worry about what would happen if Premier’s import agreement would

get revoked. Would their warranties still hold? Rumors began circulating that had no basis. Media coverage remained confusing and Premier was not speaking with anyone or issuing a statement.

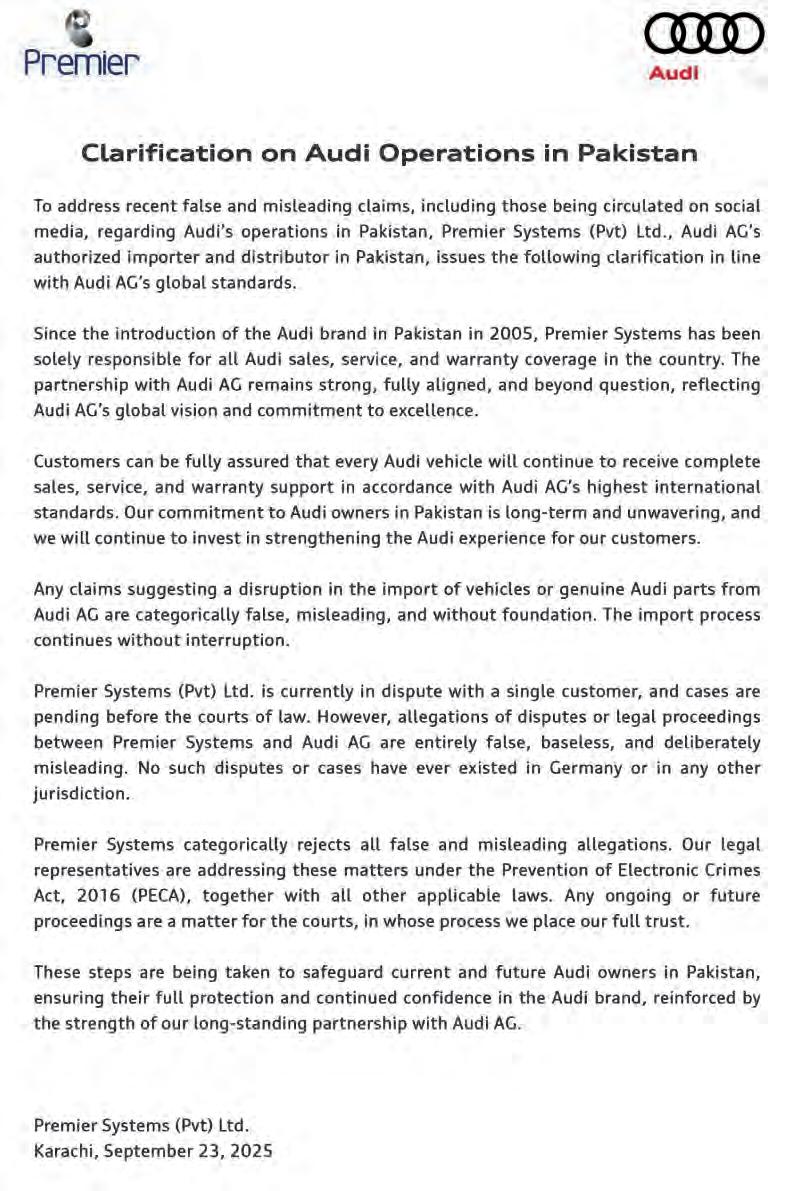

From a PR perspective, Premier was in a very good position to make a simple statement clarifying the matter in a simple and professional tone. Instead, they took serious legal action that put an already disgruntled customer in a tough corner. Naeem Afzal has responded in turn. He has filed criminal cases against Premier’s executives under Sections 420 and 468, entailing forgery and cheating. He also lodged complaints with the SECP and the CCP. And that is where it stands currently. After all of this came to the fore, Premier did finally issue a statement. It has been shared in full below.

The statement, which interestingly enough has the letterhead of “Premier” along with the Audi logo and no mention of the term Audi Pakistan, is belligerent in tone. While the press release clarifies issues surrounding Pre-

mier’s status and relationship with Audi AG, it also alludes to “false and misleading claims” being circulated on social media. It does not specify or get into the dispute with Naeem Afzal but does mention that PECA is a tool at their disposal. Essentially, Premier is trying to beat out the flames that their case had fanned. It was also a clear indication that they were not ready to put this matter aside and reach an out of court settlement. The cases would continue to be pursued.

This is where we stand. Premier and Naeem Afzal got in a tit-for-tat legal escalation match over a financial dispute worth Rs 50 lakh. For Naeem Afzal, the dispute has cost him time and money. He also feels the need to defend his honour. For Premier, their decision to pursue the case has magnified the issue far beyond any social media posts that their disgruntled customer might have been making. Even as the legal battles rage on, it is unlikely that the entire ordeal will end up being worth it to either party. n

Tepid growth for Colgate Palmolive Pakistan

Weakened consumer spending sentiment hit the company’s pricing power, though it was able to extract efficiencies and continue to grow profit margins

Profit Report

Colgate-Palmolive (Pakistan) closed its financial year with numbers that speak to a market stuck in second gear but an operator that has learned to squeeze more from every rupee it spends. Net sales for fiscal year 2025 edged up just 2.0% to Rs116.0 billion from Rs113.2 billion a year earlier – nearly flat in real terms given inflation – but gross profit rose 10.0% to Rs40.7 billion, lifting the gross margin to 35% from 33% and signalling cost and mix efficiencies across the portfolio. Operating profit climbed 11.0% to Rs27.4 billion, while after-tax profit increased 6.0% to Rs18.4 billion. Earnings per share improved to Rs75.8 from Rs71.2, and the full-year dividend per

share ticked up to Rs61.5 from Rs57.0.

The year’s final quarter told a more subdued story, underscoring the delicate balance between pricing and volume. Fourth-quarter net sales slipped 1.0% year-on-year, gross profit fell 7.0%, and profit after tax was down 17.0% versus the same three months of last year. Net margin for the full year nevertheless rose to 16% from 15%, pointing to structural gains that persisted despite a soft exit to the fiscal period. Management characterises the topline performance as “in line with inflation” for the year ahead, a hint that volume-led growth remains hard to conjure in the current consumer climate.

Peel back the layers and the drivers are clear. The company says it remains heavily dependent on imported raw materials –about 75% of inputs – so the relatively stable exchange rate during the year was a tailwind

for margins, particularly in oral care, which management identifies as the highest-margin category. Detergents, by contrast, carry the thinnest margins and were the most disrupted this year by a growing cohort of non-compliant, unregistered retailers who benefit from a structurally lower cost base and have pressured prices and shares for tax-compliant producers.

Even so, Colgate-Palmolive (Pakistan) kept investing behind the franchise. It quietly diversified further into cleaning supplies, test-marketing a new detergent brand –Toofan – during the year, and commissioned in-house solar capacity at its Sundar plant capable of generating 367 MWh annually, a small but symbolic hedge against energy volatility and an operational efficiency lever that complements the margin story.

Meanwhile, the company continued

category development work in its crown jewel, oral care. Management puts Pakistan’s per-capita toothpaste consumption at just 85 grams a year – well below developed market benchmarks – and is running usage-raising awareness campaigns to expand the category rather than relying solely on price and promotions. The strategic logic is simple: if oral care is the fattest-margin franchise, nudging usage habits upward can compound both social benefits and financial returns over time.

In market terms, management estimates a detergents share in the 30–38% band and a commanding 50–60% share in dishwashing, testament to brand equity and distribution muscle, even in a price-sensitive environment. Yet those same numbers also reveal the battleground: categories with big informal-sector footprints and high elasticity will continually test how much pricing power any branded player can wield.

Colgate-Palmolive hardly needs an introduction worldwide: a 200-year-old consumer goods house whose red-and-white smile is almost a lingua franca for toothpaste, and whose Palmolive equity has long anchored personal and home care aisles across continents. In Pakistan, the subsidiary’s journey reflects the classic multinational template – transfer of brands and processes, localisation of manufacturing and sourcing where possible, and a long march of route-to-market refinement to make premiumised hygiene and home-care habits affordable for a mass-market consumer.

The Pakistani arm’s evolution over the past decade has mirrored the push-and-pull of the local macro cycle. Episodes of rupee depreciation forced procurement and pricing pivots; fiscal measures widened the price gap versus untaxed informality in select categories; and energy costs swung from painful to manageable and back again. Against that backdrop, the fiscal year 2025 margin expansion stands out. With 75% of raw inputs imported, a calmer currency provided relief at the factory gate, while the company’s portfolio management, cost discipline and operational tweaks (including the new solar installation) show up directly in the 200-basis-point lift in gross margin and the 11.0% gain in operating profit –despite only 2.0% sales growth.

The company has also been willing to experiment. The Toofan detergent test signals a readiness to refresh the lower-margin end of the mix and defend relevance in a segment where the non-compliant channel has nibbled aggressively at share. Such launches seldom rocket to scale overnight in a cluttered aisle, but they hint at a tactical blend of innovation and localisation that can help hold the line on volume without giving away the store on price.

Looking ahead, management’s near-term

growth guide – “in line with inflation” – is realistic. It implies that the story for fiscal year 2026 will likely be one of continued margin housekeeping, tight execution, and selective bets to cultivate usage and defend share, rather than a return to heady double-digit real growth. That framing aligns with the company’s experience in 4Qfiscal year 2025: demand remains elastic, and the trade structure – especially where informality thrives – keeps threatening to turn price passes into share leaks.

A scan of the detailed fiscal year 2025 scorecard shows the levers at work. Cost of sales fell 1.0% to Rs75.3 billion even as net sales inched up, yielding that 10.0% gross profit increase. Selling and distribution outlays rose 9.0% to Rs12.0 billion – intelligible in a year of brand support and test launches – while administrative expenses rose 18.0% to Rs1.4 billion, together lifting operating costs but not enough to offset efficiency gains. Other income, which can be lumpy, decreased 23.0% to Rs3.9 billion; other charges ticked up 2.0% to Rs2.0 billion. Finance charges were essentially flat at Rs0.2 billion, reflecting a balance sheet that remains conservatively run. Profit before tax advanced 5.0% to Rs29.1 billion; tax expense rose 4.0% to Rs10.7 billion. Free cash flow is not disclosed in this note, but the stable dividend progression – from Rs57.0 per share to Rs61.5 – speaks to confidence in cash generation.

The category read-through is equally instructive. Oral care, the highest-margin vertical, benefited most from exchange-rate calm and the company’s category-building programmes. Detergents, by contrast, faced the pincer of informal competition and margin drags, underscoring why Colgate-Palmolive keeps nudging its mix towards categories where brand, formulation and habit formation yield defensible economics. Dishwashing – where management claims a 50–60% share – sits somewhere in the middle: still competitive, but with a brand moat substantial enough to defend price architecture more effectively than in laundry.

On the manufacturing side, Colgate-Palmolive operates facilities that enable local production of key lines, reducing lead times and currency exposure. During fiscal year 2025 it augmented the Sundar plant with a solar installation expected to generate 367 MWh annually, a modest contribution that nonetheless lowers grid dependence and provides a visible sustainability marker at a time when energy availability and cost remain strategic variables for Pakistani manufacturers. Beyond the energy project, there were no splashy factory announcements in the note, but the test-market work in detergents suggests ongoing line-level investments and retooling as the company iterates.

The headcount is not disclosed in the briefing note and recent public materials have been light on specifics; however, the footprint implied by the company’s nationwide distribution and multi-category operations suggests a sizeable direct workforce complemented by third-party partners across logistics and retail activation. What is explicit is the import intensity of inputs – three-quarters of raw materials – which continues to shape both cost structure and working-capital management. Any sustained rupee volatility would therefore ripple quickly through gross margin, while import frictions can complicate production planning.

Colgate-Palmolive’s fiscal year 2025 narrative lands at the intersection of three realities in Pakistani consumer goods.

First, pricing power is not what it used to be. After two inflation-heavy years, households remain cautious; the replacement cycle even in low-ticket FMCGs has stretched, and down-trading is pronounced in categories like laundry. That makes every rupee of price increase an invitation to volume trade-offs unless brand salience and product superiority are unmistakable. The final quarter’s dip in sales and profit illustrates just how quickly elasticity can bite when the market tightens.

Second, the informal channel is more muscular. Management’s reference to “unregistered retailers” is a pointed reminder of the structural tax and compliance asymmetries that tilt unit economics in favour of non-compliant players. In laundry especially, that can mean shelf prices that compliant brands struggle to match without destroying margins. The result is a grinding competitive equilibrium where share defence relies on innovation, pack-price architecture, and relentless costout to fund consumer value.

Third, operational efficiency is the currency of resilience. The 200-basis-point gross margin expansion on anaemic sales growth demonstrates that procurement, formulation, manufacturing yields, energy management and freight discipline are not back-office niceties; they are the P&L. The energy initiative at Sundar is small in absolute terms, but symbolises a broader philosophy: bring volatility under control where you can, even at the margin, to defend profitability when the topline cannot pull its weight.

The result is a company that eked out higher profits on flat sales, protecting margins while preparing the ground for when demand finally re-accelerates. If inflation continues to cool and FX remains broadly steady, fiscal year 2026 could look like fiscal year 2025 but with slightly more sunshine: modest nominal sales growth, a disciplined cost base, and a tilt towards categories where science, trust and habit change create durable value. n

Trump tariffs expected to boost PEL’s exports to the US

High tariffs on China and Mexico offer PEL the opportunity to enter export markets in a way it has previously struggled to in the past

Profit Report

Pak Elektron Ltd (PEL) has done something it has seldom managed in its nearly seven decades of manufacturing: it has begun to export at scale. In March this year, the Lahore-based company shipped its first batch of distribution transformers to the United States – an inaugural consignment that caps a stream of orders worth about $44 million and puts PEL on track, by its own and analysts’ estimates, for $50 million in export sales in calendar 2025 and potentially $100 million in 2026. For a business whose fortunes have traditionally risen and fallen with Pakistan’s domestic cycles, this is a step-change: exports that could contribute roughly a fifth of group revenue next year, with export gross margins materially above what PEL earns in the local market.

The context matters. Washington has maintained steep tariffs on Chinese electrical equipment and has tightened scrutiny on supply chains crossing Mexico (and to a lesser degree Canada), even as North American utilities grapple with transmission bottlenecks and long replacement cycles. That combination has created a price and capacity gap into which a cost-competitive, compliant supplier with shorter delivery times can walk. PEL, analysts argue, has arrived with a tariff advantage –the landed duty for Pakistani shipments is set at about 19% – and with a logistical pitch built around delivery in eight to nine months, against an industry norm that can stretch to two years. For a US grid chasing a surge of building to keep pace with the voracious electricity needs of the artificial intelligence boom while replacing ageing hardware, that timing matters as much as price.

What sets the new phase apart is not just the dollar value of orders, but their quality. The export book spans units from 225 kVA up to 9,000 kVA, including higher-capacity models worth about $3 million, indicating PEL is not merely offloading low-end inventory. Margins tell the same story. Where domestic gross margins in the power division have hovered in the mid-20s (about 25–26%), exports are pencilled

in at above 40%, with the blended group gross margin projected to climb from about 28.5% in CY25 towards 30% in CY27 and beyond, as exports scale to nearly one-fifth of total sales. The margin uplift is visible even in the company’s in-year progression: net margins in the power division improved from 5% in CY24 to just under 10% in the first half of CY25.

This is unusual territory for PEL. For most of its life, the company’s export line was more aspiration than anchor, susceptible to price squeezes abroad and forex shocks at home. The US transformer orders do not erase those old vulnerabilities, but they do reframe the risk-reward. If PEL delivers consistently – on quality, certifications, after-sales and timelines – the export channel could become a structural complement to its domestic base, rather than a cyclical side bet.

PEL’s journey from grid gear to fridges

PEL’s story starts in 1956, when Malik Brothers set up an electrical manufacturing shop in collaboration with Germany’s AEG. Commercial production of transformers began in 1958; air conditioners followed in 1981 as the Saigol Group, which acquired PEL in 1978, diversified the product set into consumer appliances. The company listed on the Karachi bourse (now Pakistan Stock Exchange) in 1988 and, by 1992, had secured an ABB USA licence to produce energy meters – an early signal of the technical direction that would later underpin its US pitch. A timeline of product milestones – refrigerators in 2011, inverter air conditioners in 2016, 4K smart Android TVs in 2018, semi-automatic washing machines in 2019, and the entry to the US market in 2024 – reads like the long, iterative arc of a manufacturer learning to move up the value chain while broadening its consumer footprint.

Today, PEL straddles two distinct but complementary businesses. Its power division designs and manufactures power and distribution transformers, switchgear, grid-station equipment and energy meters, and also undertakes EPC assignments. Its appliances

division produces refrigerators and deep freezers, air conditioners, microwave ovens, washing machines, water dispensers and LED televisions. The split has swung between the two over cycles – pandemic-era squeezes and import controls hurt appliances, for instance – but management expects power to reclaim share as exports scale, with division revenue contributions converging again over the medium term. A product map on page 7 of the analyst note lays out the full catalogue across both divisions.

Ownership remains firmly with the founding group: the Saigol family controls about 53%, with foreign companies holding roughly 12%, financial institutions 10%, and the general public about 12%. That concentrated but diversified base has historically allowed PEL to ride out rough patches without dilutive equity raises, while leaving room for market float and institutional coverage.

In the power business, PEL claims strong domestic shares across categories: roughly 90% in power transformers (a figure that speaks to installed base and tender performance), about 17% in distribution transformers, 25% in switchgear and 18% in energy meters. Historically, that dominance has not translated into export heft, largely because global tenders favoured scale and long-standing supplier relationships. The US opening resets some of those entry barriers. Analysts estimate export revenue could reach Rs12–15 billion in CY25–26 on current order visibility, amounting to about 19% of total revenue next year. The power division’s net margin, which improved to about 9.8% in the first half, is expected to trend higher as the export mix deepens.