08 For the average Pakistani household, loans are becoming a replacement for insurance

12 The ‘stable’ Gulf is gone. What comes next?

16 Shanghai Electric finally pulled the plug on K-Electric. What comes next?

20 After expansion bid, Bunnys braces for flood impact

21 Citi Pharma Dips Its Toes into Veterinary Medicine

23 The floods are already driving up the cost of living 24 Declining rates cause revenue and profit slump at Standard Chartered Pakistan 26 Barkat Frisian moves backward into its poultry farm supply chain

29 Pakistan’s 5G Mirage: The Spectrum Gamble Threatening Digital Dreams

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

For the average Pakistani household, loans are becoming a replacement for insurance

Pakistan’s financial inclusion numbers have shot up in the past decade but access to formal credit remains seriously misaligned with the average household’s needs

By Hasan Saeed

In 2014 only 7% of Pakistanis had access to financial institutions. In the decade since that number has gone up to 35%.

On the surface this is a massive shift. It means Pakistanis have been signing up for financial services in the droves. Why does this matter? Because access to financial services is a cornerstone of any growing economy. Access to capital is the basic building block of any developing economy. But Pakistan’s financial inclusion revolution harbours a secret. According to the Karandaz Financial Inclusion Survey 2024, Pakistanis have had increasing access to credit in recent years. But what is this credit used for?

K-FIS data shows that one in four adults reported they needed credit in the past year and when asked the reason, the responses pointed more towards survival than growth. The reasons range from health shocks, emergencies and family obligations. Weddings and funerals also appear in the same sentence as medical bills as central reasons for borrowing.

Let that sink in. People can get credit. Financial institutions are lending. Pakistanis actually borrow money quite frequently. But loans are availed but mostly as substitutes for insurance and not for investment. Loans, for the most part, are not utilized to grow a business. Capital is not being invested in productivity but to cover life’s shocks. In the case of Pakistan, credit is functioning as a substitute for formal insurance and filling in the gaps left by weak coverage and safety nets. This pattern is repeated over and

over again across demographics as well as the rural-urban divide. Households in Pakistan are united in borrowing reactively to absorb risks rather than to grow their wealth.

Getting a loan

There is a difference between requiring a loan and being unable to secure one, data from the survey shows there is a stark difference between demand and access. Of the respondents in the survey who said they required credit, 41% could not obtain a loan when needed. In all of these cases the people involved had to resort to selling assets or borrowing informally at higher costs.

Whilst these situations helped tide the shock over, it came at the price of future vulnerability. There are trade-offs when it comes to either selling assets or borrowing informally. Take the case of a rural household as an example. If a household is forced to sell livestock, they may survive the crisis at hand but their income will be depleted. With shrinking future earnings, the family will be at an even greater risk of capitulation the next time a smaller crisis arrives that they otherwise would have been able to cover with their regular income. In the case of informal borrowing, higher interest rates can force households to adopt strategies around resilience and hollow out their long-term security.

The survey shows there is even misalignment amongst the people who borrow, with 85% of the respondents citing friends and family as the most common source of loans. Banks and mobile money providers account for 13% and 8% cited informal moneylenders, while only

1% borrowed from committees or ROSCAs. This shows that Pakistanis borrow from those they trust and can approach quickly. Friends and family lend because social obligations bind them, informal lenders fill the urgent needs and formal institutions with their red tape are only a small part of the borrowing landscape. Households opting for informal credit over formal one has less to do with access and design and more with how informal credit is fast, flexible and built on trust. A relative might lend without a formal agreement apart from an expectation of reciprocity later. While these agreements are not without their own cost, they fit the needs of an average household.

On the other hand, formal loans are more structured and require proof of a monthly income. Unfortunately, for most Pakistanis, income is irregular and seasonal, farmers earn after harvests while service workers might have daily wages and households who receive remittances, might have to wait weeks at a time for the money. Formal loans require equal monthly installments or a borrower might face a penalty in lieu of a delayed payment. The K-FIS data shows that 34% of the respondents who borrowed, cited difficulties repaying on time.

The shock factors

These misalignments are brought into the spotlight when looking at financial shocks, experienced by households and how they dealt with them. As per K-FIS 2024, health shocks are the most common, followed by loss of income and social obligations. A surprising 35% of the respond-

ents said they had experienced at least one major shock in the past year and among these shocks, health expenses stood at 18%. These shocks, as discussed above, force families into borrowing but said borrowing has trade-offs as some households will borrow from multiple sources at the same time. This can create multi-layered debt obligations.

While others will look to sell assets or cut down on consumption, the data shows that the younger respondents opt for more digital savvy options like seeking advance salaries. The older demographic sticks to traditional networks. The one thing clear across all ages is that borrowing to cope with shocks is far more common than borrowing for planned investment. There are other untold consequences of households not opting for formal credit, when they choose to sell assets or reduce consumption. This hollows out the strength to deal with future issues and the lack of formal credit leads to further fragility.

Whilst formal borrowing exists, only a small number of respondents mentioned availing this option and taking loans directly from banks or formal financial institutions. The data shows that, when they borrow they tend to borrow larger amounts and find it difficult to repay it and this shows the mismatch. Formal loans are too big and have other issues. Any household in Pakistan that faces an unexpected external shock will prefer a loan that will be dispersed quicker compared to one that will take days or even weeks. This is another factor as to why people pick informal credit over formal credit despite the increase in financial inclusion. This issue is further compounded by loan limits. Informal loans are smaller, more flexible and can be tailored to fill the urgent need. These can be met by asking relatives or other informal lenders as a stop-gap measure. Loans by microfinance institutions are more structured and they have a relatively small cap. Loans by banks are much larger but difficult to avail. The data shows that an average household in Pakistan more often than not needs a small but immediate loan to stave off a crisis.

Furthermore, as discussed above, the financial inclusion in the country has increased from 30% in 2022 to 35% in 2024 and this increase is largely due to the increase in mobile money accounts – an increase from 30% to 19%. On the other hand, the usage of bank accounts has fallen from 17% to 16%. This shows that the story of financial inclusion in the country is increasingly becoming digital but it has not led to an increase in credit access. Regardless of account type, borrowing is still being led by informal credit. The gap between account ownership and access to credit highlights misalignment and inclusion being only limited to registration means creation of financial products that meet people’s needs are overlooked.

Financial inclusion in Pakistan

Prevalent gaps

This misalignment is further exacerbated, when we look at the data from a gender lens. The survey shows that only 14% of women in the country are financially included compared to 56% of the men – a 42% gap and one of the largest globally. This forces women to rely on accounts held by other people, typically male relatives, with 77% of excluded women saying they use family wallets. They are also limited not only by access but also design as lower SIM card and

multiple ways depending on circumstances. In the above sections, we have talked about health shocks or sudden loss of income which lead to borrowing but the data shows that a large number of loans are available for societal obligations such as weddings or funerals. This type of borrowing receives less of a spotlight as compared to the other reasons but in K-FIS 2024, they were put on almost equal footing as health expenses. This shows that in Pakistan credit is also a social tool, and it is wielded to not only manage household shocks but to also maintain societal standing and complete cultural duties. The idea that such type of borrowing is equivalent to health emergencies shows how intertwined financial lives are with social commitments.

This dichotomy, whereby credit is both survival and social glue, shows that borrowing is not just a private decision but a public necessity. For example, a household risks harm to its reputation by not throwing a grand wedding and even funerals have an expectation of a monetary contribution. Due to the cultural and societal norms, these obligations are mandatory and at times availing credit is the only way to bridge the gap between reality and expectation. While K-FIS 2024 captures the usage, it does not have the long-term consequences mapped apart from the fact that credit is woven into the cultural fabric as much as the economic.

How many Pakistanis needed credit in the past year?

phone ownership rate and weaker digital literacy has left them to rely on other people for access. This means that when it comes to credit, women in Pakistan are at a disadvantage two times over. They are excluded from formal credit channels and are on informal ones that are male dominated. If women want to borrow, there are no products that are tailor made for the issues they face whether in documentation, channels, or priorities.

The data shows that the younger adults are more likely to adopt digital tools with 37% of the respondents being aged 25-34 compared to 20% of those over the age of 55 but when it comes to the borrowing patterns, everyone will still turn to family and friends in times of need. While one can hypothesize the reasons for this but one is clear that digital adoption alone has not yet shifted credit access in a major way.

We have seen that the story of credit in Pakistan is about misalignment and the data in the survey shows that this plays out in

The shocks that lead to borrowing in the country are no longer just personal or household-specific but they are now tied to climate change. The survey shows that a number of respondents availed credit due to shocks related to climate change, be it the form of floods, crop failure or weather-related loss of income. The respondents in rural areas cited availing credit due to climate changes on a slightly higher scale than their urban counterparts. Given the devastating floods in 2022 and ones happening at the time of writing, rural households having to borrow due to climate change will only increase. Pakistan is already at the forefront of climate change and these emerging patterns show that climate-related financial volatility is becoming a part of life. Soon, people will be borrowing not only due to health shocks or loss of income but also to survive and stave-off climate uncertainty. Nothing could make this more obvious than the devastation of this year’s floods.

This relationship matters as it increases in how we know and understand demand for credit in the country because while other shocks might be one-off, climate related ones are not. A farmer having to borrow after flooding or drought is not borrowing as a one time thing, for him it is to navigate a pattern of environment instability. For people, who might be living in flood hit areas will have to borrow to rebuild or replace livestock, losing income in the process. As discussed above, the data shows that 35% of respondents have suffered

at least one major financial shock in the past year and while health leads the way, climate is not far behind. This will only push households to borrow not just to survive but also to recover from events that will keep repeating.

The issues with formal credit

Now we turn to the pertinent question of why households do not turn to formal credit in the face of these shocks and the data from K-FIS 2024 has a detailed account of the reasons put forward by the respondents. The reasons are as much practical as they are a matter of perception. Many respondents felt they lacked the required documentation or the collateral to qualify. Another reason was the feeling that the application process was arduous, and complex. A large number of respondents felt they would not be approved and did not bother applying. Others felt that the time it would take the formal loan to be approved did not meet the urgent need.

These host of reasons show that the bottleneck is not only about misalignment or supply but also about perception. While people may be financially registered, they remain excluded as they perceive formal credit to be inaccessible or ineffective. This hesitance is also explained by the level of trust in financial institutions when it comes to borrowing, with respondents more likely to borrow from friends or family or even informal money lenders over formal financial institutions. We can see this in the borrowing patterns with 85% of the respondents borrowing from friends and family compared to 13% from banks or mobile money providers.

This point is underscored by the repayment experiences as shown by the data with 34% of the borrowers saying that repayment was difficult. A deep dive into the numbers show that 72% of the people who borrowed from informal lenders said it was very difficult to make the repayments compared to 29% for people who borrowed from family and 25% who borrowed from formal borrowers. This shows that while people do not avail formal credit on a large scale, the ones they do, they do not find it harder to repay compared to the other sources. Pointing to the fact that the real issue is not about repayment but getting households to apply for such loans in the first place.

The data on the size of the loan size availed adds another layer with the survey showing that majority of the loans are under Rs 10,00 and not many over the Rs 50,00 range. This tells us that there is a structural mismatch as informal loans, while being flexible and being availed by the majority are smaller in size. On the other hand, formal loans which could be larger in size, are not availed due to a number of reasons ranging from barriers of application, perception and trust. This leaves

41%

The number of Pakistanis that could not access a loan

the household sin a bod, they can avail all the credit they can get but the amounts are only good enough to deal with an immediate shock and not help them their trajectory.

What it comes down to

On the surface, the findings from K-FIS 2024 showcase the strides that have been made to increase the number of financially included

Top sources of loans for Pakistani households: Friends and family 85% Banks and mobile money providers

13% Informal moneylenders

8%

*Many families borrow from multiple sources at a time.

people in the country with the number of 35% in 20204, a five-time increase from 7% in 2022. The data shows that mobile wallets have become a handy tool in daily life, reshaping the way people handle money. On the other hand, once we scratch the number, we come across the fact that the structure of credit is misaligned with the needs and realities of Pakistani households. Households and people have been borrowing and the number has increased over time but they are not going to formal institutions but turning towards friends and family. These loans are flexible, small and reactive; not for growth but to deal with shocks.

The survey along with the trajectory of the data tell us that now the major hurdle is not of exclusion but of misalignment. There is a demand for credit but access to formal credit is low, due to a number of reasons ranging from documentation, collateral, perception of not getting one or even delays in approval. On the other hand, informal lending is thriving as they prioritize expediency and flexibility but the repayment is not easy. As aforementioned, 34% of the people who borrowed money, majority of them said it was very difficult to make repayments to informal lenders.

Another level of complexity is added by climate changes with a growing number of respondents having to avail credit due to climate related events. This highlights how financial instability is as environmental as economic and while economic shocks could be on or off, climate change is a recurring pattern. The pattern shows that households in Pakistan will have to borrow repeatedly to survive these climate related changes; adding another level of distress in households who were already borrowing to react against economic shocks. Whilst, K-FIS 2024 does not have the dataset to map out the full implications of this just yet but we have enough evidence to show that the current credit structure does not have the capacity to meet the requirements of a climate-stressed populace.

At the heart of this tale lies trust, we have seen that the average household when it comes to the availability of credit, will turn to someone they know instead of banks or formal financial institutions. This is one of the major reasons that can explain why registration of bank or mobile money accounts has not led to the increase in the usage of credit. Access to credit cannot be increased without dealing with underlying issues discussed here. The conclusion that one can draw from the survey is that whilst financial inclusion is scaling up, transformation remains out of grasp. Credit is disjointed and misaligned and it will remain a means to survive one crisis to the next unless the design of financial products starts considering climate shocks, irregular incomes and the lived realities of women and excluded groups. n

The author works at Karandaaz.

The ‘stable’ Gulf is gone. What comes next?

Pax Americana is well and truly dead as far as the Middle East is concerned, which means that the Gulf’s much-vaunted stability is gone. What does that mean for Pakistan’s economy?

By Farooq Tirmizi

If you still harbour any illusions that the Gulf Arab countries are a stable safe haven, that illusion should have been shattered by the Israeli bombs that landed in Qatar this past week. If you are thinking “but I own property in Dubai, and that is still quite safe,” you are engaging in what might charitably be described as a coping mechanism.

The ‘stable’ Gulf Arab states are now a thing of the past, and while this may sound like an overreaction to what is, for now, an isolated air strike, it represents something much bigger: the collapse of the order that has underpinned the security that made Pakistanis launder their money out to Dubai, buy property there, and seek any kind of residence visa there. And over the long run, it will also mean a diminished opportunity for Pakistani labour to work there, which will eventually hit the country’s largest source of remittances.

In this story, we will lay out to you why the stability of the Gulf was an American gift that has been withdrawn likely permanently, why the Gulf Arab states – and therefore Pakistani people and assets there – are now vulnerable, and how this could negatively impact Pakistan. We then try to lay some possibilities of what the future could hold for the region, and for its relationships with Pakistan.

The Gulf was built by America

Your relatives who live in Dubai or Saudi Arabia may tell you fantastical tales of the competence of Arab royals, but there is one undeniable truth: the Gulf went from being a poor backwater made significant only by the Kaaba and the Hajj to a rich part of the world purely because Americans decided to drill there for oil.

The company that made the region is Aramco, the state-owned Saudi oil company. It began its life in a dingy little office in San Francisco, as the subsidiary of Standard Oil of California. For the first 30 years of its existence – including more than a decade after striking oil in Saudi Arabia – the company maintained its headquarters in the United States.

But even beyond the company, think about what the Gulf has historically been, and still is to a large extent: the source of a substantial portion of the world’s oil supplies. You can believe the Saudi and Emirati stories about ‘diversification’ if you want to, but the fact of the matter remains that all of those ‘diversification’ initiatives are – despite decades of trying – still a small fraction of their respective economies.

The Saudis, Emiratis, and Kuwaitis are rich because of oil, and the Qataris are rich because of natural gas, and if the outflow of energy stopped, so too would most of the rest of the incidental attention they get from other parts of the world.

That wealth – coupled with America’s historical willingness to offer explicit and implicit security guarantees to these countries – is the foundation of their much-vaunted stability. And that also means that the Saudi riyal and Emirati dirham are essentially just the United States dollar with different graphics on the currency notes. It is moonlight: reflection from the faraway sun that is the United States.

Well, the Americans are gone. The money – and the stability – might soon follow.

In 2005, half of Saudi Arabia’s oil exports went to just three countries: Japan, the United States, and South Korea, in that order. Most of the rest was taken up by American allies in East Asia, and India and China. In order to protect those supplies, the United States Navy maintains carrier groups in or near the Persian Gulf, and bases in Bahrain, Qatar, and patrolled the Straits of Hormuz and Malacca to allow the oil tankers to pass through unmolested from the Persian Gulf to ports on the Pacific Rim.

In 2024, half of Saudi Arabia’s exports went to China, Japan, and South Korea, in that order. And America’s desire to maintain the carrier fleets and bases to protect the economic interests of others is effectively gone.

The United States itself is once again energy self-sufficient, which means it no longer needs to offer security guarantees to the Gulf Arab states for its own sake. In a previous era, it might have cared somewhat about Japan and South Korea, but that is less and less important to America today, as are the rest of its nominal allies in East Asia. And caring about China’s energy supplies is absolutely not a priority for the United States.

How many people will be flying in to those cool conferences in Riyadh or Abu Dhabi if oil that Aramco and ADNOC are pumping out of the ground cannot get to its end-markets after the Americans withdraw their protection? (For those of you who might argue that Dubai is not as dependent on oil, you would be wrong. Dubai is a service economy whose end-clients are all in the oil-dependent parts of the Gulf.)

The underlying economics has been true since roughly 2014, when the shale revolution in the United States took off to the point where global oil prices collapsed because American production increased so much. The politics of the American alliance system, however, maintained the entirety of its façade until at least the end of the Obama Administration in 2017, but had begun slowly eroding since the beginning of the first Trump term.

The economic imperative is no longer there for America to care, and the political alliances built on top of that economic imperative are gone in practice, even if they still exist in theory.

The vulnerability

In comes Israel to test just how far gone those alliances are with a single bombing raid on Doha. One might be tempted to dismiss this as a single raid that, while shocking, does not necessarily represent the rise of Israeli military dominance over the Gulf Arab states. And one might also argue that this is a vulnerability unique to Qatar, since all of the other states in the region do not have any direct animosity with Israel.

That view is mistaken for two reasons: first, just because Israel does not currently have a reason to quarrel with the Saudis and Emiratis does not mean it may not discover one in the future. Without the American security umbrella, these countries do not have the ability to defend themselves on their own, and they know they cannot rely on China to step in, even though China has now taken the mantle of their biggest customer, and the country most dependent on oil and gas from the Middle East.

If you cannot defend yourself, your old patron is gone, and your new patron refuses to protect you, you are at the mercy of your powerful neighbours.

And those powerful neighbours include not just Israel, but also Turkey and Iran. The government in Ankara aspires to be heirs to the Ottoman sultans, and the Persian imperial habit has never really gone away, so a return of the Arabian peninsula to the status of pawn in imperial wars between the powers in Persia and Anatolia, with a new interloper in Tel Aviv, is not out of the question. At the very least, it is a risk now facing every government in the region.

To maintain their security, the Gulf Arab states need to either find a way to placate the three powerful states in the region, or else build up a way to defend themselves.

Because here is the most important observation about the Israeli attacks on Qatar: where was the Qatari military when this happened? The Qataris have bought some of the most advanced equipment the Americans make, and have military personnel presumably trained in how to use it. Why did they not scramble planes?

When India attacked Pakistan in May, yes some drones and bombs fell on Pakistani territory and some people were killed. But the defining story was that Pakistan had the ability to strike back and extract a cost for attacking that blunted any future desire to continue attacking Pakistan.

If you punch Pakistan, Pakistan can punch back hard. If you punch Qatar, that is not the case. And the Saudis and Emiratis may not want to admit this, but it is unlikely they would have fared any better if they were on the receiving end.

What that means is that you can no longer assume that a shopping trip to Dubai Mall will not involve a missile or two dropping near you.

And who will want to buy those apartments in the Marina if that risk exists? What is the value of a UAE golden visa if it is not as safe anymore? Not zero, but less than before that risk was known.

The perception will not vanish overnight. Indeed, if one had to estimate how long it will take, it will be about a decade before the market fully prices in the increased risk of living in and maintaining assets in the Gulf Arab states. Which means the best time to sell those assets is probably some time over the next five years.

Pakistan’s exposure to the GCC’s vulnerability

But this is not just an article about the Pakistanis who own Dubai real estate or maintain bank accounts there. Pakistan’s relationship with the Gulf matters a lot, and economic vulnera -

bility there can have ripple effects on us. Let us take a look at what those might be.

Foremost is the fact that Pakistan gets about 55% of its remittances from the Gulf Arab countries, which represents two things:

1. Macroeconomic stability for the country, and one of the largest ways we earn the ability to pay for our imports, including the energy we import from the GCC. Indeed, in calendar year 2024, Pakistan imported $17.8 billion worth of oil and gas, mainly from the GCC, but also received $18.6 billion in remittances from those countries.

2. Income support to households that might otherwise have considerably lower income had their expatriate family members ended up staying back within Pakistan.

Pakistan does export a significant amount to the GCC countries, but those countries are, somewhat surprisingly, not among Pakistan’s major export markets, which remain the United States, the European Union, and the United Kingdom.

One might argue that Pakistan also has a fuel import vulnerability, since conflict could interrupt oil and gas exports from these countries to Pakistan. This is likely a relatively low risk, however, mainly due to geographic proximity, which acts in two ways.

Firstly, given the fact that Pakistan and the Persian Gulf are so close, there are fewer points of hazard that need to be navigated, and really only the Staits of Hormuz. And secondly, even if the route became insecure, convoying energy imports is a realistic possibility even for a navy as small as the Pakistan Navy.

Let us explain: global trade has been able to expand rapidly over the past century because the United States Navy patrols the world’s oceans and makes them safe to sail for anyone and everyone. It maintains law in an otherwise lawless environment. But given the fact that the United States is withdrawing from that role as the world’s policeman, what replaces it?

What replaces it is a much older way of doing things, and the reason navies exist in the first place: to protect not just the shoreline of a country from attack, but also its maritime trade. Currently, the way trade happens is that ships just sail into the deep blue ocean knowing they have been made safe by the Americans somewhere over the horizon. The older way involves ships moving in convoys, with naval ships protecting commercial ships throughout their entire voyage.

This is both expensive, and also limits how much and how many countries any given country can trade. It is also possibly not the future for all trade, but some level of convoying is likely to return to global seaborne trade in the near future.

So, given the fact that this may be needed, can Pakistan manage convoying for its trade needs? The answer is, in a limited manner, and for short stints, yes.

Pakistan imports roughly the equivalent of one oil tanker a day in energy supplies, and Karachi is only a three days’ sail away from nearly all ports in the Persian Gulf. A three day sail one way means approximately a 7-day roundtrip. The Pakistan Navy would only need to escort 5-7 tankers through the Straits of Hormuz at a time. That is not something it has ever had to do, but even with its limited capabilities, the Navy could manage that task.

Could this be something that the Navy could do on a permanent basis? No, but it is also probably not something it would need to do on a permanent basis. The only power hostile to the Arab countries that has a presence in the Straits of Hormuz is Iran, and Iran has neither the motivation not the capabilities to keep the straits closed for too long, which suggests that this risk, while not zero, is minimal.

So Pakistan could at least protect its imports of fuel from the Gulf Arab countries and prevent the country from a complete shut down.

But could it do more than just that and offer a replacement for American protection? The short answer is no, and it should be cautious about even offering this.

Can Pakistan be the GCC’s protector?

Pakistan has always liked the idea of playing a larger leading role in the wider Islamic world. Even after independence, Foreign Minister Zafarullah Khan led an initiative to use Pakistan’s diplomatic presence to help other Muslim countries. Among the more notable early uses of this was the issuances of Pakistani passports to leaders of the independence movements of Morocco and Algeria, in 1952 and 1956 respectively, so that they could make the case for their countries’ independence at the United Nations in New York.

Pakistan has also had military collaborations with Arab countries in the past, having helped train GCC military leaders as recently as the 1980s. And there was the quiet involvement in the Arab-Israeli wars in the 1960s and 1970s.

But recently, talk in Islamabad has turned towards something different. When Qatar was attacked, one of the first foreign leaders to call was Prime Minister Shehbaz Sharif, and his attention was very much welcomed. There is nothing formally in place, but one thought is on the minds of many in Islamabad, and a few in Gulf capitals: if Pa -

kistan can defend itself against aerial attack from India, can it also defend allies in the Gulf from Israel?

The answer is not yet known, but there is an eagerness in Islamabad to try to find out, perhaps as a means of getting the Gulf governments to subsidize Pakistan’s defence budget as a replacement for lost American money that went away after the US withdrawal from Afghanistan.

Is that eagerness reciprocated in the Gulf? Pakistanis want to believe that the answer is yes, but remember: the GCC is used to American forces being their defenders, and the Americans still maintain bases in their countries. Pakistan is not being courted as a replacement of the United States, merely as a backup in case the Americans cannot be persuaded to renew their security commitment.

That renewal is not forthcoming, and it is not just the Trump Administration that has a nonchalant attitude towards the concerns of its allies in the GCC: any incoming Democratic administration in the United States is unlikely to take the alliance back to pre-2014 levels.

It will, however, take time for the Gulf Arab states to truly begin to look for alternatives, and while Pakistan is likely to get some interest, it may not be the only country approached, and Pakistan’s penchant for being candid in asking for financial support upfront (translation: we start begging too quickly), means that it can be rather off-putting to prospective allies, even when there is a mutual need for collaboration.

The point: Pakistan is clearly enjoying a moment where it is getting some interest in defence collaboration from the Gulf Arab countries, but it would be wise to offer help without seeming too eager or too desperate for Arab cash.

For their part, the Arab countries would be wise to seek help from Pakistan. It is one of the few countries that has a large military that is trained on both American and Chinese equipment. So, for example, Pakistani pilots could operate the Gulf countries’ own American-made equipment as well as any new Chinese equipment they might buy.

And that is before one even gets to the cultural affinity Pakistanis have for the Gulf Arab countries.

In short, a collaboration may be mutually beneficial, but the positioning will need to be navigated carefully. Given how much of Pakistani capital is tied up in Dubai real estate, and how much Pakistan relies on remittances from the GCC, one could argue that it is in Pakistan’s economic interest to do what it can to help protect these countries.

But let’s try to do it without the begging bowl this time. n

Shanghai Electric finally pulled the plug on K-Electric. What comes next?

The withdrawal of Shanghai Electric has been a foregone conclusion for at least two years now, but it still marks a dark moment in Pakistan’s business history

By Abdullah Niazi

The official announcement by Shanghai Electric that they were terminating their purchase of a majority stake in K-Electric should not come as a surprise to anyone. The deal to sell KE to Shanghai had been on life-support for the better part of a decade.

This was just them finally pulling the plug. First signed in 2016 the deal to sell KE was masterminded by Arif Naqvi and the Abraaj Group. In the nine years since then Shanghai Electric has made regular attempts to pay the $1.77 billion sum agreed upon to acquire the company. The government of Pakistan has responded to these efforts by running circles of red tape around them that effectively paralysed the entire transaction.

During this decade of paralysis the reality of KE has changed drastically. Abraaj, the group responsible for turning KE around and making it something worth selling to a foreign investors in a multibillion dollar sale, has collapsed and its founder Arif Naqvi is in prison. Abraaj’s stake in KE went into a fund in the Cayman Islands which is now owned by AsiaPak Investments — the investment arm of Sheheryar Chishty, the owner of Daewoo and the Thar Coal-1 project in Pakistan. While Mr Chishty emerges as the clear majority owner of the company, the government’s continued paralysis when it comes to KE has meant no clarity in terms of who gets real management control. At the same time, the current management of KE in Pakistan has been asleep at the switch. They have failed to deal with the rising problem of users that default on their bills and have absolutely failed to account for the massive solar revolution that has emerged in residential electricity consumers. A recent scandal involving the company’s CEO over workplace harassment has also raised questions over the power company’s corporate governance.

So where does that leave things now?

“This is not a happy story for anybody,” Sheheryar Chishty tells Profit. As the largest stakeholder in KE he has a lot to lose. “I have been frustrated by this entire process but Shanghai’s exit should give the senior leadership in the country a lot of pause and fruit for thought on how the country conducts itself.”

His words are a chilling indictment of the worst qualities the Pakistani government has often displayed as an international business partner. These qualities have persisted across the political divide and over many years. Pakistan has had five different prime ministers since the deal with Shanghai Electric was struck in 2016 and not one has been able to push the deal through. What makes it worse is that the government did not have to do much since the actual hard work of both fixing KE and finding a buyer

was done by Abraaj. The government’s only role in all of this has been dragging its feet and refusing to accept a multibillion dollar sale to go through.

Shanghai Electric’s withdrawal comes at a period when the country’s leadership has been pushing hard to shed its reputation as an unreliable business partner. The formation of the Special Investment Facilitation Council (SIFC) and a number of diplomatic successes in recent months have helped improve its impression on the world stage. However these efforts will not be helped by the fact that Shanghai Electric’s withdrawal almost coincided with the recent B2B conference in China and the launch of CPEC 2.0. The Chinese company did not mince its words in the official statement issued to kill the deal. “Given that the counterparty has consistently failed to meet the conditions precedent for closing and the changes in the business environment in Pakistan have rendered this transaction no longer aligned with the company’s international development direction, after careful study and analysis, in order to effectively safeguard the interests of the company and all its shareholders, the company has decided to terminate this major asset purchase,” it read.

As Pakistan’s leadership continues to pursue its goals of opening Pakistan up to foreign investment, it will be vital that they can prove what happened with KE is a relic of the past. The only way to do this is for the

company’s board to get its act together and focus on turning KE’s fortunes around once again. The first step to doing that will be figuring out exactly who gets to run Pakistan’s only vertically integrated power producer.

A miracle turns into a nightmare

The story of KE started more than a hundred years ago in 1913 when it was first founded as the Karachi Electric Supply Company (KESC). It was nationalized in 1952 and was passed around different ministries and government departments (including WAPDA) until 2005 when the Musharraf Administration decided to privatize it. The government sold off 66.4% of KE to a consortium of the Al-Jomaih Holding Company, a diversified Saudi Conglomerate, and the National Industries Group, a publicly listed Kuwaiti financial conglomerate (which also owns a large stake in Meezan Bank). For three years, the Saudi-Kuwaiti conglomerate failed to make any headway in turning around the company, finally turning in 2008 to Arif Naqvi, the former Karachiite who had gone on to create Abraaj Capital in Dubai.

Abraaj was already the largest private equity firm in the Middle East by then, and had previously made forays into the Pakistani market before. In October 2008, Abraaj bought out half of the Jomaih-NIG stake in KESC, injecting $391 million into the company. It then began a turnaround effort the likes of which have never been seen in Pakistan before.

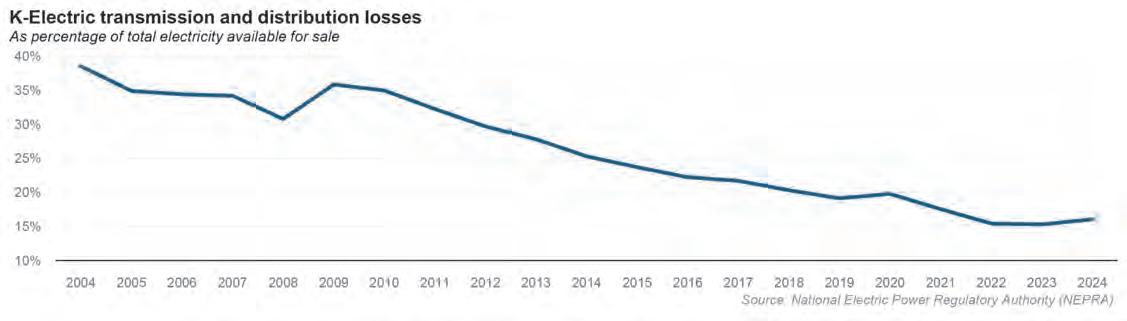

Abraaj spared no expense in trying to turn around KESC, investing upwards of $1 billion in the company’s power generation and transmission infrastructure, which brought the utility’s power generation efficiency rate from 30% in 2008 to 37% in 2016, and its transmission losses from 4% to 1.4% in the same period.

It was a remarkable turnaround that this publication has covered in quite some depth in the past. After a ten year stint in which KE returned to its former glory, Abraaj found a buyer. And not just any buyer. Arif Naqvi managed to bag Shanghai Electric. This was a state-owned Chinese multinational that was willing to invest a significant amount of money in purchasing KE. The deal also came at a time when the China Pakistan Economic Corridor (CPEC) was at its peak.

Abraaj had managed to find the perfect buyer, and at $1.77 billion this would be the second largest acquisition in Pakistani history and the largest in a decade, after Etisalat’s $2.6 billion acquisition in 2006 of management control in Pakistan Telecommunications Company Ltd.

At first glance, K-Electric’s sale by Abraaj Capital is the epitome of a successful private equity-led turnaround story. Indeed. It is the very reason private equity firms came into existence in the first place. A storied company, sullied by bad management but still serving a unique economic purpose, bought out by a skilled private equity firm at its nadir, turned around through a combination of strategic capital investments and modern management techniques, and then sold off in a healthy, relatively unleveraged state to a strategic buyer. And a Harvard Business Review case study to document it all.

But then came the roadblocks. To cut a very long story short, consistent delays on the part of the government meant the Shanghai deal could not go through. What should have taken a year or two at most was dragged on for three years. Despite no lack of political lobbying on the part of Abraaj’s Arif Naqvi, the deal was dead in its tracks. And then came the crash. In 2019, Arif Naqvi and Abraaj were involved in an international scandal that ended with the company utterly bankrupt. If the deal had gone through, it is possible Arif Naqvi would have been able to stave off his debts for

some time longer, but the deal’s paralysis made this impossible. Eventually Abraaj, and along with it the Shanghai Electric deal, went kaput.

Signs of life

The fall of Abraaj is when the Shanghai Electric deal really went on life support. Up until 2019, Shanghai had been pursuing the deal aggressively but nothing seemed to make the Pakistan government budge and the deal remained stuck in bureaucratic red tape and regulatory paralysis. There have been many theories regarding what happened in those three years but nothing in the realm of public record has really been proven beyond the Government of Pakistan being an impossible business partner.

Despite this, even after Abraaj fell apart, Shanghai Electric did keep renewing their interest in the KE deal every year. It is important here to understand exactly what they were buying. When the government had first privatised KE in 2005, its buyers, the Al Jomaih Group, created a company called the KES Power Limited (KESP) in the Cayman Islands.

This company paid the government of Pakistan directly and acquired a 66.4% stake in K-Electric in Pakistan. The government of Pakistan controls 24.36% shares in KE, while the rest is owned by institutional investors and the general public.

In 2009 when Al Jomaih decided to sell, Abraaj funneled over $370 million in foreign

direct investment into KE through the KESP company in Cayman. To date, the US$360 million invested by Abraaj in KE (routed through KESP) remains the only equity FDI invested into KE as new capital used principally to fund capital expenditures driving efficiency. Abraaj’s investment in KE was undertaken through the Infrastructure & Growth Capital Fund L.P. (“IGCF”), a $2 billion Cayman Islands private equity fund with investment contributed by over 100 different international investors, managed then by Abraaj Investment Management.

When the IGFC fund was created, it only bought 53.8% shares in the holding company called KESP with the rest of the amount remaining with investors from Al Jomaih. To clarify, 66.4% of K-Electric was owned by a holding company in the Cayman Islands called KESP. When Abraaj entered the picture in 2009, they purchased 53.8% of that holding company. This means that even though Abraaj did not have the majority shares in K-Electric (their total ownership comes out to around 35%) they did control the majority of the holding company that controls them, giving them management control and rights over KE.

When Abraaj went bankrupt, their share in KESP was up for liquidation. This is when Sheheryar Chishty enters the picture. In 2022, through a special purpose company called Sage Ventures registered in the British Virgin Islands, his company called AsiaPak Investments acquired Abraaj’s former stake in the holding

I have been frustrated by this entire process but Shanghai’s exit should give the senior leadership in the country a lot of pause and fruit for thought on how the country conducts itself

Sheheryar Chishty, CEO at AsiaPak Investments

company called KESP, becoming the ultimate beneficial owners of KE.

“I took the plunge in KE back in October 2022 when Pakistan was going through a perilous moment. The IMF programme was under threat and there were economic and political troubles everywhere. It was a time when people inside and outside Pakistan had written this country off. I took the plunge as a vote of confidence in Pakistan but I am also frustrated that the board has not gotten its act together,” Chishty explains to Profit.

What he is referring to is the fact that despite the change in material ownership, KE in Pakistan has failed to hold board elections or recognise that the new owners need their own representation on the board of directors of the K-Electric in Pakistan. The government has played a silent role in keeping the Cayman investors out of the boardroom and have continued to manage the company.

The Shanghai equation

In the background of this entire fiasco the Shanghai deal was still on the table.

Shanghai Electric would regularly send notices to KE and the stock exchange expressing its continued interest in buying the company out.

“Shanghai was going to buy shares directly in KE. They were going to buy the 66.4% in KESP. They would have been the sellers in addition to any shareholders that would want to be part of the freefloat. In KESP, the Abraaj fund had 54% and Jomaih and the others had 46%. Since KESP was selling, and we have bought Abraaj’s share, we would be a joint seller to Shanghai along with the others. The sales proceeds would be divided amongst us and then amongst all the investors and the funds etc of which we are the majority anyways,” claims Chishty.

The sale would have given Chishty and the other investors a good exit from the company but Shanghai’s withdrawal has put that possibility to rest. “I can empathise with

Al Jomaih as well. They have been there for 20 years with no dividends. A deal was about to go through and nothing became of it for 10 whole years,” says Chishty.

But where does that leave us? The Shanghai Electric deal had been in limbo so long it had become an excuse to ignore KE and let it languish with no clear leadership or ownership. As unfortunate as it is that a deal of this nature has officially fallen through, the silver lining is that the crutch is also gone. There is no buyer for K-Electric now. No one is coming to clean up the mess. That leaves only one option: clean up the mess.

“The Shanghai deal has been kept in limbo by the Pakistani government since October 2016. They should have rejected it in a year or two if they did not want to pursue it but for nine years it stayed in limbo. Shanghai stopped giving notices last year so we pretty much knew the deal was dead. This was just the official confirmation,” Chishty laments. “The stakeholders need to hunker down now for the long haul and figure out how to run this company for the betterment of its customers and its shareholders.”

His message is clear. There is no exit for anybody right now. “It is time to read the writing on the wall and get on with the programme.”

Fixing KE

What exactly will getting on with the programme entail?

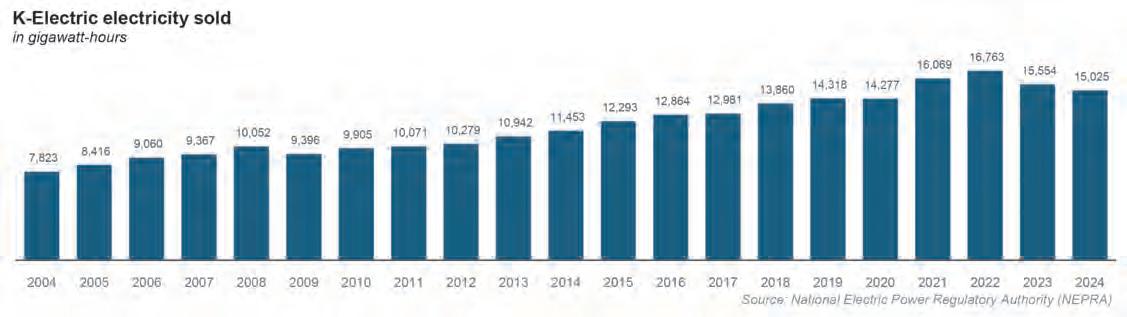

K-Electric is a far cry from the hot product it was in 2016 when Shanghai Electric first wanted to pay $1.77 billion to buy it. Nearly a decade of neglect has made this a company that needs a lot of attention.

In fiscal year ending June 30, 2024, the latest full year for which data is available, K-Electric’s bill recovery rate – the total amount of bill payments collected as a percentage of the total amount of bills issued – was about 91.5% across all of its customers, according to data from the National Electric

Power Regulatory Authority (NEPRA). That number sounds impressive, and indeed represents a sharp increase in bill recovery rate relative to where the company was privatized in 2005, but is down from the 96.7% it had achieved just two years prior, in fiscal year 2022. And when one looks at the source of this decline, it is driven in very large part due to a decrease in collections from household consumers, which has seen a relatively sharp deterioration in the past four years, going from 92.2% collection in 2020 to just 82% in 2024.

This is bad, to say the least, and so bad, in fact, that K-Electric has gone from having a bill recovery rate about 700 basis points above the state-owned electricity companies’ average (which basically means all other companies in the country since K-Electric is the only privately-owned electric utility) in 2021 to now being 1,000 basis points below the state-owned companies. It is a 10% drop in just three years. And it does not seem to be improving either. In the first half of the fiscal year ending June 30, 2025, K-Electric’s bill recovery rate dropped even further, with a household consumer bill recovery rate now at 78.4%, a sharp decline in just six months.

This publication has done an in-depth analysis of the problems plaguing KE back in June.

To put a long story short, KE has been suffering from a serious problem of not having adapted to the solar revolution. Its best customers, the ones that would always pay their bills, are rapidly shifting away from the grid and moving towards solar energy. On top of this, a bruising fight over ownership has left the company with no clear leadership that has a mandate to turn things around.

There is a lot that can be done at KE. There is also proof of precedent that turning this company around is not impossible – what Abraaj did between 2009 to 2016 was as difficult if not more so than the current situation. But the first act must be to fix KE’s corporate governance problems. If no consensus can be reached on this issue, KE can forget another turnaround. n

After expansion bid, Bunnys braces for flood impact

The recent flooding has raised fears the prices of wheat will increase making margins for food companies like Bunny’s smaller

BProfit Report

unny’s Limited, one of Pakistan’s leading packaged bread and bakery producers, has reported a sharp reversal in its bottom line. For the financial year ending 2024, the company posted a loss per share of PKR 1.6, compared to earnings per share of PKR 2 in the previous year. The decline reflects not only rising input costs but also heavier spending on distribution and administration.

The figures underline the pressures that have accompanied expansion. For the third quarter of FY25, however, there was some respite. The company earned PKR 0.6 per share, a turnaround from a loss of PKR 1.9 in the same period a year earlier. Net sales in FY24 rose 23% year on year to PKR 7 billion, but the cost of sales surged 29%, eroding margins.

Despite these financial headwinds, Bunny’s has pressed ahead with new investments aimed at lowering long-term operating costs. The company has installed a 200 KVA solar power system, with an additional 200 KVA expected to come online soon, covering part of its 1 MW total energy requirement. Alongside this, it has begun using biogas fuel, estimated to be about 30% cheaper than conventional alternatives due to the plant’s proximity to its factory. Management intends to increase reliance on biogas as capacity expands, creating a buffer against future energy price shocks.

The company has also undertaken strategic distribution changes. After pausing snack distribution for more than five months, it plans to relaunch the category nationwide in September, backed by a revamped model better aligned with market demand. In its core bread and bun segment, Bunny’s holds a 32% market share in Punjab. Bread accounts

for around 60% of revenue, while cakes contribute about 20%.

These developments highlight a company balancing short-term pressures with longer-term bets on energy efficiency and distribution scale. Yet looming challenges — particularly from climate-related shocks to agriculture — threaten to weigh heavily on margins.

Profile of Bunny’s Limited

Bunny’s traces its history to the late 1980s, when industrial baking in Pakistan was still largely fragmented. The company began as a family-led venture in Lahore, initially serving a small urban market with packaged bread at a time when unbranded alternatives dominated. Over three decades, it has expanded operations across Punjab and more recently into

Islamabad.

The company has positioned itself not only as a large-scale supplier of staple breads but also as a trusted partner for multinational clients. Bunny’s holds a Gold Certification from the American Institute of Baking, the only Pakistani firm to possess such accreditation. This certification boosts credibility and has been instrumental in securing order-based sales from international buyers, who demand consistent food safety and quality standards.

Operationally, Bunny’s has tended to follow a model of incremental expansion. Its recent move into Islamabad addresses shelf-life concerns raised by distributors, and management notes that while it currently operates on a single shift, it retains flexibility to add a second shift if demand rises. Ample vacant land also allows for further capacity expansion.

The company’s evolution reflects both the growing formalisation of Pakistan’s food industry and the rising role of branded packaged foods in urban consumption. Once a niche player, Bunny’s has become a household name, particularly in central Punjab where it commands strong brand recognition.

Product portfolio

Bunny’s core strength lies in packaged bread, which forms the backbone of its revenue base. White bread, brown bread, and wholemeal varieties dominate shelves, with buns, rolls, and sandwich bread further broadening the portfolio.

Cakes and other bakery products, accounting for around a fifth of revenues, represent an important diversification. These include packaged tea cakes, pound cakes, and festive lines that cater to seasonal demand. Snack items form a smaller portion of overall sales, but management is keen to revive this segment with an adjusted distribution model that separates the shorter sales cycle of bread from the longer cycle of packaged snacks.

This segmented approach recognises the challenges of managing perishable and non-perishable product lines simultaneously. Bread requires rapid turnover and a tight distribution chain, while snacks offer scope for longer shelf life and nationwide reach. By retooling its logistics, Bunny’s aims to strengthen its presence across categories without cannibalising its bread operations.

The breadth of its product line has been vital in navigating Pakistan’s competitive food market, where both multinational and local players vie for share. While bread remains a regulated product, limiting the company’s ability to raise prices freely, cakes and snacks provide relatively more flexibility in pricing.

Market realities and wheat price pressures

The company’s prospects are now overshadowed by broader market realities. Recent floods have damaged wheat crops and raised concerns that flour prices will climb in coming months. For Bunny’s, whose revenues depend overwhelmingly on bread, this presents a serious threat. Management has warned that margins could decline by 1–2% if flour costs continue rising, since the regulated status of bread prevents passing these costs fully to consumers.

Wheat is Pakistan’s most politically sensitive crop. Government interventions, ranging from price supports for farmers to regulated bread pricing for consumers, leave companies like Bunny’s squeezed between higher input costs and capped retail prices. This dynamic intensifies during natural disasters, when supply chains are disrupted and speculation drives volatility.

Beyond wheat, other costs are also climbing. Selling and distribution expenses rose 15% in FY24, while administrative costs jumped 47%, reflecting both inflationary pressures and the expenses of expansion. Finance costs climbed 31% due to higher interest rates, further denting profitability.

Still, there are positives. Gross profit increased 5% in FY24, and gross margin improved to 28% in 3QFY25, up from 13% a year earlier. This indicates some operational efficiencies and potential benefits from cost

management measures such as the biogas initiative. If energy self-sufficiency projects mature, they may provide a cushion against rising input costs.

Yet for now, the reality remains: margins are thin, the regulatory environment is rigid, and climate-driven shocks are worsening.

Looking ahead

The next phase for Bunny’s will be defined by how well it can balance expansion with resilience. Its investments in renewable energy, accreditation-driven quality standards, and expanded geographic footprint show a company intent on long-term growth. But external risks, particularly wheat supply and price stability, may dictate its near-term trajectory.

For shareholders, the volatility of recent years underscores the tightrope food companies must walk in Pakistan. Net margins turned negative in FY24, and only a modest rebound has been seen in quarterly results. With a market capitalisation of PKR 9.1 billion and a current share price of PKR 136.6, investors will be watching closely whether operational efficiencies can offset rising costs.

Ultimately, Bunny’s story is emblematic of Pakistan’s food sector. Strong demand for packaged staples ensures growth opportunities, but regulatory constraints and climate shocks create vulnerabilities. For a company that has built its reputation on steady expansion, the coming year may test its ability to adapt more than ever. n

Citi Pharma Dips Its Toes into Veterinary Medicine

Profit Report

In a significant development within Pakistan's pharmaceutical sector, Citi Pharma Limited (CPHL) has announced its foray into the veterinary healthcare market through its wholly owned subsidiary, Citi Veterinary Limited (CVL). This strategic move not only diversifies Citi Pharma's portfolio but also signals a growing recognition of the importance of animal health in the country.

Entering pet care

On September 12, 2025, Citi Pharma disclosed to the Pakistan Stock Exchange that CVL has commenced operations, launching an initial lineup of 32 veterinary products, including vaccines. The company has already established Letters of Credit (LCs) for eight of these products to ensure timely availability and supply. For the fiscal year 2025-26, CVL projects a turnover of approximately PKR 1.5 billion, with a gross profit margin of 13%. Looking ahead, the

company aims to scale operations and achieve a turnover target of PKR 10 billion within the next three years.

This expansion into veterinary medicine is noteworthy, especially considering the evolving landscape of pet ownership in Pakistan. Traditionally, pet ownership in the country was limited, often due to cultural perceptions and a lack of awareness regarding animal welfare. However, recent years have seen a shift, with an increasing number of households adopting pets, particularly dogs and cats. This change is driven by factors such as urbanisation, changing lifestyles, and a growing awareness of the companionship and emotional benefits that pets offer.

The entry of a major pharmaceutical company like Citi Pharma into the veterinary market is expected to further stimulate this trend. By introducing a range of veterinary products, CVL aims to address the growing demand for quality pet care solutions. This move not only caters to the needs of pet owners but also contributes to the broader objective of improving animal health standards in the country.

Profile of Citi Pharma

Founded in 2012, Citi Pharma Limited is a prominent player in Pakistan's pharmaceutical industry. Headquartered in Lahore, the company engages in the manufacture and sale of pharmaceutical, medical chemical, and botanical products. Citi Pharma has established itself as the largest Active Pharmaceutical Ingredient (API) manufacturer in Pakistan, with a diverse portfolio that

includes antibiotics, cardiovascular medicines, and over-the-counter drugs.

The company's manufacturing facility, located in Kasur, spans 46.2 acres with a covered area of 527,384 square feet. Built to international standards and compliant with current Good Manufacturing Practice (cGMP) guidelines, the facility includes separate units for formulations and distinct API production units. This infrastructure supports Citi Pharma's commitment to producing high-quality pharmaceutical products and positions the company for future expansions, including its recent venture into veterinary medicine.

Citi Pharma's leadership comprises experienced professionals, with Rizwan Ahmad serving as the Chief Executive Officer and Nadeem Amjad as the Chairman. The company's strategic direction focuses on innovation, quality, and expanding its product offerings to meet the evolving healthcare needs of Pakistan's population.

Product lineup

Citi Pharma's product portfolio is extensive, encompassing a wide range of pharmaceutical products. The company's API segment includes essential medicines such as Paracetamol, Amoxicillin, Levofloxacin, Cefixime, Ciprofloxacin, Cephradine, Norfloxacin, Aspirin, Ibuprofen, and Ascorbic acid. In the formulation department, Citi Pharma produces tablets, liquids, and capsules, catering to various therapeutic areas including antibiotics, analgesics, and cardiovascular health.

With the establishment of Citi Veter-

inary Limited, the company is expanding its product range to include veterinary medicines. The initial 32 products launched by CVL cover a broad spectrum of animal health needs, including vaccines and treatments for common ailments in pets. The company's strong and long-standing supply partnerships in China play a vital role in ensuring consistent and reliable supply availability in Pakistan's veterinary healthcare market.

Looking forward, CVL plans to establish Pakistan's first dedicated veterinary Active Pharmaceutical Ingredient (API) plant during fiscal year 2026-27. This move is expected to enhance local manufacturing capabilities, reduce reliance on imports, and improve the availability of veterinary medicines in the country. Upon commencement of in-house production, the company anticipates an increase in its gross profit margin to approximately 25%, reflecting stronger value addition and enhanced operational efficiency.

Citi Pharma's entry into the veterinary medicine market marks a significant milestone in the company's growth trajectory and reflects the evolving dynamics of pet ownership and animal healthcare in Pakistan. By leveraging its manufacturing expertise and established supply chain partnerships, Citi Pharma is poised to make a meaningful impact on the veterinary sector, offering quality products that meet the needs of pet owners and contribute to the overall improvement of animal health standards in the country. As the market continues to expand, Citi Pharma's strategic initiatives are expected to play a pivotal role in shaping the future of veterinary healthcare in Pakistan. n

The floods are already driving up the cost of living

As floodwaters wreak havoc on Pakistan’s agriculture, prices for essential goods soar. With crops destroyed and the full extent of the damage yet to be seen, the economic fallout could worsen

Profit report

The floodwaters in Pakistan have claimed more than just lives; they have swept away crops, livelihoods, and, as it turns out, much of the nation’s ability to keep prices steady. As the country grapples with the devastation of floods that have torn through fields, the retail cost of essential goods is skyrocketing. The Sensitive Price Index (SPI), which tracks inflation in the short term, has shown a 5.03% rise in prices year-on-year by the week ending September 11. While some of that increase can be attributed to typical inflationary pressures, the devastation caused by the floods has pushed prices even higher, with perishable goods like vegetables and meat taking the brunt of the impact.

In Islamabad, the price of tomatoes has surged to Rs280 per kilogram. The nation’s staple crops like onions, potatoes, and rice have similarly seen unprecedented price increases. These spikes are not simply the result of seasonal trends or market fluctuations; they are the consequence of devastating natural disasters that have ravaged key agricultural regions.

The extent of this damage is still unclear, and that uncertainty is unsettling. What’s certain, though, is that the immediate impact on the domestic market is only the tip of the iceberg. The destruction of stock and crops could lead to even higher prices in the future, with the full scope of the devastation yet to be determined.

Flooding in Pakistan is hardly a new phenomenon, but the scale of this year’s catastrophe has proven to be a massive setback for the all important agricultural sector. Over the past several weeks, floods have overwhelmed crops that were already struggling under the strain of a harsh climate. Tomatoes, once considered an affordable everyday vegetable, have become a luxury in many households. Prices of onions and potatoes have followed suit, with many of these key ingredients now costing more than double what they did just weeks ago. The poor will bear the brunt of this price hike, as they already grapple with the growing cost of living.

Perishable goods like tomatoes and potatoes are particularly vulnerable in Pakistan’s climate, where monsoons can cause widespread damage. The flooding this year has hit at the most inopportune time for crops,

which were already being strained by high temperatures and water scarcity in many parts of the country. For farmers, many of whom are already operating on razor-thin margins, this year’s floods have been a brutal blow.

The retail prices of sugar, rice, and chicken have also followed the upward trajectory, largely driven by the logistical challenges that floods create. As roads become impassable and transportation networks are disrupted, the movement of goods becomes slow and costly. These factors combine to make it even more expensive for the average Pakistani to purchase daily necessities.

This is a story of two groups being affected in equal measure: the flood victims themselves and those who will face the secondary consequences in the form of higher prices. Farmers who have lost their crops face not only immediate losses but also a future fraught with uncertainty. The people in cities, who rely on these agricultural products for sustenance, will have to tighten their belts as the cost of food climbs. Those living paycheck to paycheck are often the first to suffer when inflation takes hold, and they are already feeling the pinch of escalating prices.

As the government begins to assess the scale of damage, many will be left wondering what can be done to stem the tide of rising prices. Already, the Pakistan Bureau of Statistics has noted a decline in certain products, such as wheat flour and chicken, but these decreases pale in comparison to the overall inflationary pressures on essential goods. The sharp rise in the cost of living is becoming a daily reality for many, as salaries remain stagnant and the purchasing power of the rupee shrinks.

There is a sense of inevitability about the weeks to come. The SPI’s seven consecutive weeks of rising inflation show that prices aren’t likely to come down anytime soon. In fact, the immediate future looks even worse, with the full impact of the flood damage yet to unfold. As crops continue to rot in submerged fields, the prospects for a stable market in the coming months remain bleak.

Pakistan’s economy, which has long been subject to volatility, is once again at a crossroads. The country’s reliance on agriculture for its food supply means that the nation is

vulnerable to the effects of natural disasters like floods. While this year’s flooding is particularly severe, it’s a reminder of the fragility of a supply chain that’s all too easily disrupted by weather events. The government’s ability to respond will be tested in the weeks and months to come.

In the meantime, Pakistanis are forced to make do with the higher prices that are now commonplace in markets. The everyday grocery shopping trip, once a routine task, has become a carefully considered decision for many families. Those who used to rely on cheaper options like rice and potatoes now find themselves unable to afford even the basics. As the cost of living continues to rise, the gap between the wealthy and the poor in Pakistan grows wider, as inflation punishes the most vulnerable.

What is clear is that the long-term effects of the flooding will be far-reaching. It’s not just about the crops that have been destroyed or the loss of income for farmers. The ripple effects of this disaster will be felt throughout the economy, as inflationary pressures mount and the cost of living increases. With the worst of the damage still to be quantified, it’s difficult to predict just how high prices will go before they stabilize.

In the coming weeks, the Pakistani government will need to consider what steps can be taken to address both the immediate and long-term effects of this crisis. The damage caused by the floods is not just a natural disaster—it’s an economic one as well. With food security increasingly at risk and prices rising, Pakistan’s policymakers will need to find innovative solutions to protect vulnerable citizens from the worst of this crisis. As for the flood victims, they will have to rely on government support, aid, and the resilience of the people to get them through what is proving to be one of the hardest years in recent memory.

It is a sobering reminder that the floodwaters don’t just destroy physical infrastructure; they wreak havoc on people’s livelihoods, their daily routines, and their ability to make ends meet. The full extent of the damage will unfold in the coming months, but for now, it is clear that the economic ripple effect of this year’s floods will be felt for a long time to come. n

Declining rates cause revenue and profit slump at Standard Chartered Pakistan

Lower rates bite as deposits fail to keep pace at the oldest bank continually operating in the country

Profit Report

Asteep fall in domestic interest rates has knocked a visible hole in Standard Chartered Bank (Pakistan) Ltd’s top line for the first half of calendar 2025, with net interest income sliding 33% year on year to Rs32.5 billion as mark up revenue fell 41%. While non funded income rose 21% to Rs11.9 billion on the back of fees, gains on securities and derivatives, it was not enough to offset the pressure on margins. Total income contracted 24% to Rs44.4 billion.

Profit before tax fell 33% to Rs32.9 billion, and profit after tax declined 23% to Rs16.6 billion; earnings per share were roughly Rs4.3 versus Rs5.6 in the same period last year. The bank nevertheless maintained its cash payout rhythm with an interim dividend of Rs3.5 per share.

Costs moved higher but remained tightly contained relative to peers. Operating expenses increased 17% year on year; even so, the cost to income ratio was 27.2%, still among the best

in the sector, while return on equity eased to 28.8% from 43.8% a year earlier. Management commentary in the briefing suggested most of the earnings impact from monetary easing was concentrated in the second quarter; further sizeable cuts are not anticipated, which could stabilise margins in coming quarters.

The revenue slump was compounded by a smaller funding base. Since December 2024, the balance sheet shrank 11% to Rs944 billion as deposits fell 17% to Rs697 billion. The bank intentionally shed expensive, low margin savings deposits to protect spreads as rates fell, a choice consistent with its ‘returns not size’ stance. The funding mix improved—current accounts now make up 59% of deposits and overall CASA remains a lofty 97%—but the absolute deposit shortfall limited any ability to offset the rate driven compression in asset yields. The advance to deposit ratio stood at 30.2%, with management signalling a plan to deploy more liquidity into private sector credit rather than parking it predominantly in government paper.

Standard Chartered traces its presence in what is now Pakistan to 1863 and is commonly

described as the country’s oldest international bank. Its current listed entity—Standard Chartered Bank (Pakistan) Ltd (SCBPL)—was formed in December 2006 when the group amalgamated its Pakistan branches with Union Bank Ltd, following State Bank approval. The bank notes that its shares are listed locally and that the amalgamation marked the start of SCBPL’s modern footprint under the British headquartered group.

Today SCBPL operates as the Pakistan subsidiary of Standard Chartered PLC, serving corporate, institutional, commercial and retail clients. As part of a global network spanning more than 50 markets, it positions itself as a leading provider of transaction banking, foreign exchange and wealth solutions for multinational and local clients alike, while also expanding its Islamic banking under the Saadiq brand.

If the balance sheet has been trimmed for returns, the physical network has been streamlined even more decisively. In early 2016 the bank reported 101 branches across 11 cities. By mid 2021, that figure had fallen to 45 branches (235 total “touch points”). At the end of 2024,

company materials referenced 41 branches (173 touch points), and the mid 2025 half yearly report shows a further nudge down to 40 branches and 170 touch points across 10 cities.

Management has tied this branch optimisation to the rapid shift toward digital channels—over 90% of transactions are already digital—arguing that a leaner footprint aligns better with client usage and service economics. The bank has signalled that rationalisation will continue to be guided by “customer voice and usage patterns,” rather than a quest for sheer scale.

SCBPL’s current playbook is explicit: prioritise quality over size; deepen digital and affluent retail; expand Islamic financing; and redeploy liquidity into the real economy as conditions improve. On funding, the bank chose to let costly savings deposits run off as rates fell, improving the share of current accounts to 59% and keeping CASA at 97%. That strengthens structural margins in theory, but in practice the 17% drop in deposits meant there simply was not enough low cost funding base to counter lower asset yields—hence the 33% slide in net interest income.

Where the strategy did cushion results was outside the spread. Non funded income rose 21% on stronger fees, market gains and derivatives, partially blunting the revenue hit. Meanwhile, costs rose but the bank still posted a sector leading cost to income ratio, reflecting ongoing discipline even as it invests in systems and talent. The return on equity, at 28.8%, remains high for the industry despite the year on year drop, suggesting underlying profitability is intact if rates stabilise.