Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) GM Special Projects Zulfiqar Butt - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

How urban is Pakistan?

A new World Bank study suggests that Pakistan may have been majority urban for decades now. How accurate is that assessment, and what does it say about the country?

By Farooq Tirmizi

One of the stale Pakistan Stud-

ies textbook “facts” that most Pakistanis know about the country is that “the majority of the population is rural”.

Some people go so far as to say the exact number: “70% rural”.

A provocative new study by researchers at the World Bank argues that – far from being majority rural – Pakistan is not just majority urban already, but may have been majority urban for the past 40 years.

Both of these represent the two poles of views about how urban Pakistan is, but it does provoke the following set of questions: what exactly is an urban area, how urban is Pakistan, how long has it been majority urban, and what does it mean about our economy?

We will lay out the case made by the World Bank researchers and add some additional data points which we think may be relevant, but it is important to start off by talking about why this matters: majority-urban countries tend to be rich, and countries tend to become more urbanized as they get richer. There is no such thing as a majority rural rich country.

Fundamentally, we are talking about how far along Pakistan is on its path to becoming a rich country.

The dissatisfying answer we find is, sadly, “farther than most Pakistanis think, but still a long way to go.”

But first, let us examine just how the landscape of urban Pakistan has been changing over the past few decades.

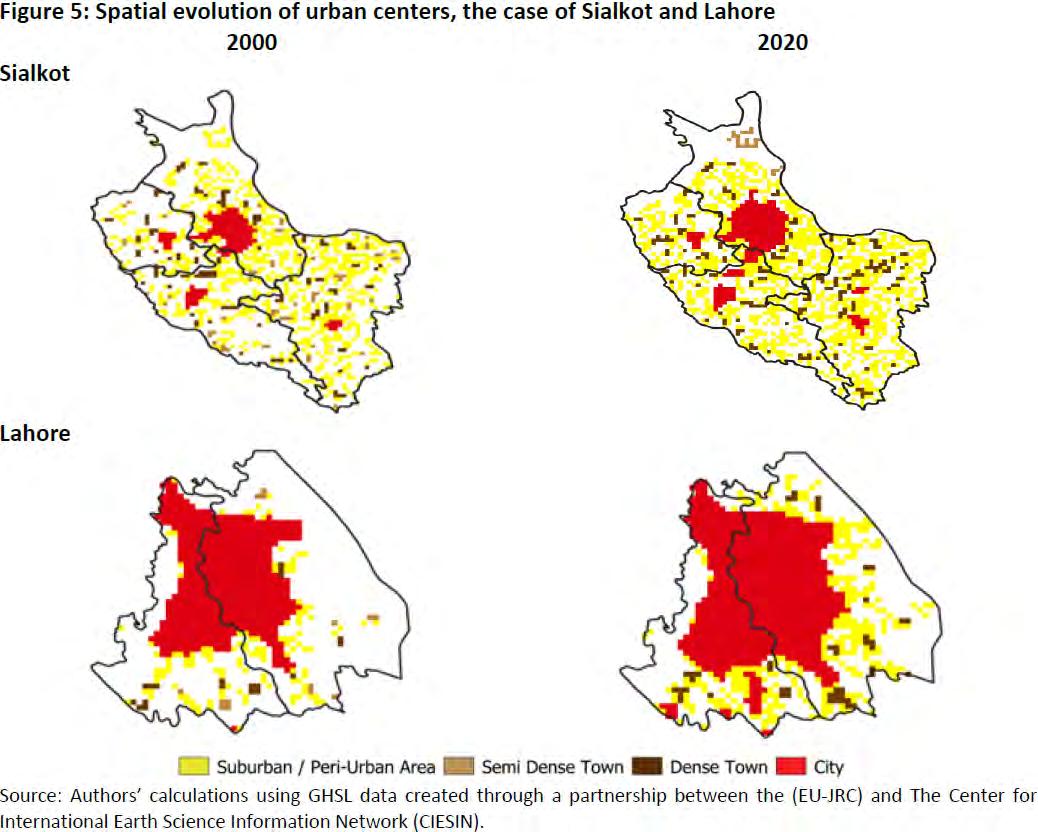

The evolution of the Pakistani metropolitan area

The boundary between city and village is never completely sharp, but up until the late 1990s, that boundary used to blur in favour of the

village. City limits would extend far beyond the denser neighbourhoods that characterize urban areas and significant portions of the jurisdiction of “municipal” governments would actually consist of farmland. And indeed even now, it is possible to see cows walking on the side of streets in the middle of even the largest cities in Pakistan, and not just before Eid ul Azha.

But the nature of that boundary is now changing, and it appears that cities are claiming a larger share of the physical space of this country. And more specifically, while it was once the norm for the city to end and be immediately abutted by farmland, now it is much more common to see suburbs, followed by perhaps a small green belt followed by the suburbs of another city that is so close as to feel functionally an extension of the larger city in its vicinity.

This blurred sense of place for urban locations is a metropolitan area, something that functionally did not exist prior to the Musharraf Administration. As recently as 25 years ago, Pakistan had cities, towns, and villages. Now, it has metropolitan areas, each with dense urban cores, with suburbs and exurbs. Some of these metropolitan regions are even part of the one (and a half) mega regions in the country.

Indeed, these non-core areas of urban Pakistan have been the fastest growing parts of the country for much of the past two decades.

Comparing the population data for cities and sub-division jurisdictions within cities from the censuses between 2017 and 2023, one can arrive at a picture of what are the fastest growing urban localities in Pakistan, and which ones are rapidly declining.

Almost all of the localities that have grown by an average annual growth rate in the double digits is an outer lying area of a major city or metropolitan area. These include places like Mauripur in Karachi (20.81% average annual growth between 2017 and 2023), Kunjah in Gujrat (18.7% per year), Dijkot in Faisalabad (16% per year),

Quetta Cantt in Quetta (10.3% per year), and so on. And the heavyweight is Raiwind.

Strictly speaking, Raiwind is not the fastest growing part of Pakistan, since there are many smaller urban areas that had faster growth (too small to be identifiable as part of a clear trend), but Raiwind stands out in being a 1-million-person urban borough effectively sprouting out of thin air. The scale of what has happened there has simply not happened at quite that speed anywhere else in Pakistan. It is the closest Pakistan has come to the Chinese miracle of major global cities emerging out of the rice paddy.

Among the larger parts of existing cities, some of the most impressive growth has come in Ferozabad (7.4% per year), Manghopir, Gulshan-e-Iqbal, and Lyari in Karachi and the urban cores of the cities of Gujrat, Okara, and Sargodha.

And these places are not just around the major cities in central Punjab and Karachi either. South Punjab’s towns are also consolidating into metropolitan areas. Some of the fastest growing parts of Pakistan are the suburbs of Bahawalpur and Rajanpur.

Are we majority urban?

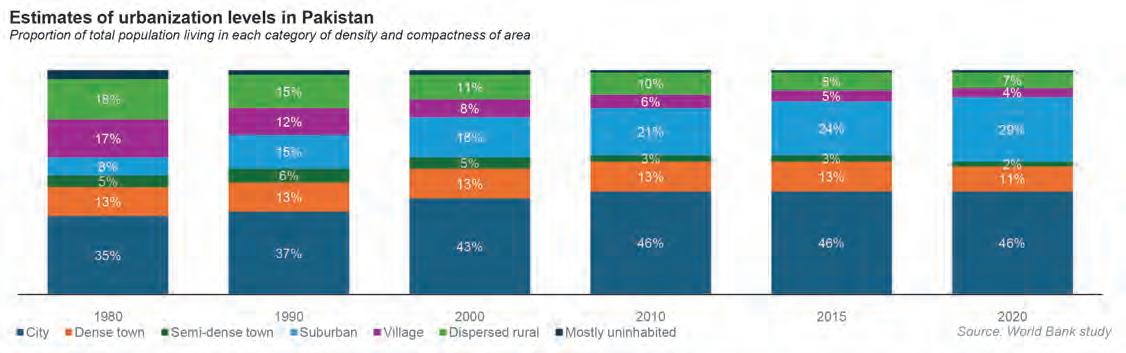

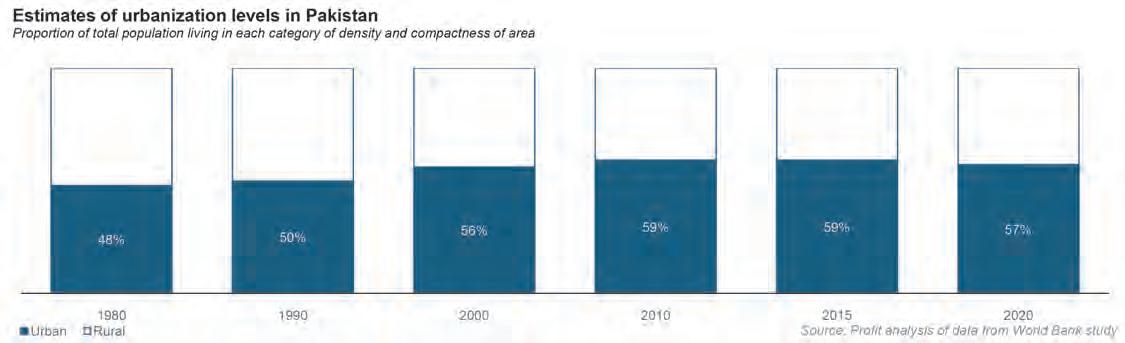

According to the 2023 census, the government of Pakistan estimates that the country’s population is about 39% urban and 61% rural. A new working paper by some researchers at the World Bank titled “When does a village become a town? Revisiting Pakistan’s urbanization using satellite data”, published in October 2025, suggests that the real number is closer to 88% urban, and that the country can be said to have been a majority-urban country as early as 1980.

This is, needless to say, a provocative assertion, but the authors have a wealth of data to back up their claim. But first, a note on their methodology, which primarily decides what is an urban area by population density, but on a highly granular level.

To measure what constitutes an urban area, the researchers ignore government categorizations, and instead use highly detailed satellite imagery from the Global Human Settlement Layer (GHSL), produced jointly by the European Commission’s Joint Research Centre and Columbia University’s CIESIN. GHSL combines satellite imagery of built-up areas with census data to estimate population counts on a one square kilometre grid over time. For Pakistan, it is calibrated using 1998 census data and 2010 population estimates.

Using this data, they then compile a measure called the Degree of Urbanization methodology, which the UN Statistical Commission recommends for cross-country

comparison. DoU classifies every square kilometre on the planet based on its estimated population density and then stratifies those into seven categories, ranging from the densest (urban centers) to the least dense (mostly uninhabited).

When an area exceeds 1,500 people per square kilometre and has at least 50,000 people living in a contiguous area, it classifies the area as being part of a city. By this measure, 46% of Pakistan’s population lives in cities. If an area has the same density, but has a total contiguous population less than 50,000 but greater than 5,000, it classifies that as a dense town. About another 11% of Pakistanis live in such areas.

The paper then describes clusters of

at least 5,000 people – located as a distance less than 2-3 kilometers from such cities and dense towns – and with a population density of at least 300 people per square kilometer, which it calls semi-dense towns or suburban / peri-urban areas. These constitute another 31% of the population.

Combined, all of these constitute about 88% of the population.

What is interesting is the authors’ calculations on historical data, which suggest that these urban and suburban areas used to constitute about 61% of the population as far back as 1980.

So are the authors right? Is Pakistan really that urbanized? For context, that would imply that Pakistan is more urbanized than the United States, which is about 86% urban and suburban, according to the US Census Bureau.

We are not demographers or experts, but that comparison makes it seem unlikely that the assertion about Pakistan’s degree of urbanization should be taken at face value. It does, however, clearly point to the fact that the country’s population lives very differently from the image we have in our heads of what constitutes rural life in Pakistan.

What is rural Pakistan?

One other way to arrive at this is to try to figure out how much of Pakistan is rural, and then arrive at how much is urban by a process of elimination.

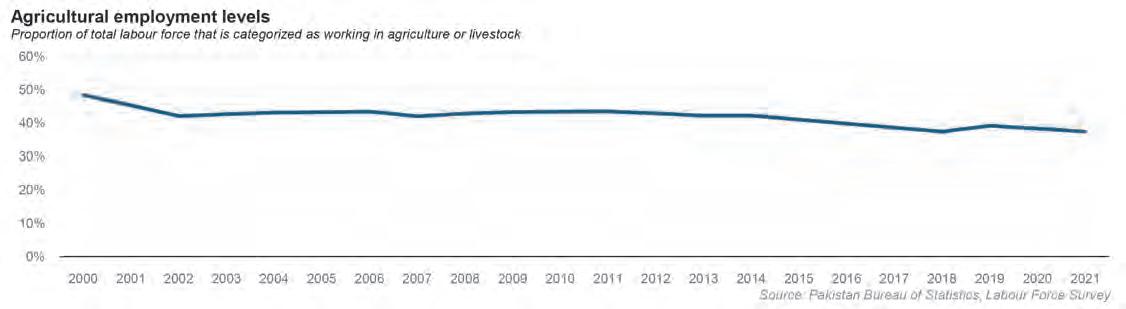

Let us start out with an assumption that we feel is uncontroversial: that anyone engaged in agriculture or livestock as their primary means of earning a livelihood can be safely characterized as living in a rural area, regardless of how dense or close to a city it

may be.

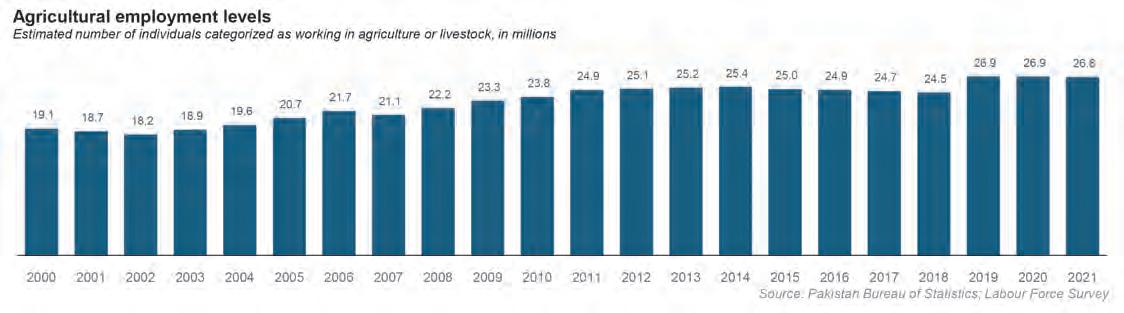

According to the Labour Force Survey from the Pakistan Bureau of Statistics, in 2021, about 37.4% of the Pakistani labour force was engaged in agriculture or livestock as their primary occupation. Now, strictly

and the approximately 63% that would be implied by a generous reading of the labour force data.

Of course, there is a vast difference even between those two numbers, so we will attempt to narrow it down further still. But itself has been relatively stagnant even in absolute terms. Indeed, the total number of people in Pakistan employed in agriculture has declined by about 372,000 people during the decade between 2011 and 2021. The contrast

women working

people, the proportion

A narrower interpretation of suburbia

We would posit that the World Bank research team should consider a slightly modified interpretation of their data, which would yield a slightly less dramatic end-result, but perhaps a more accurate representation of the rural-urban boundary in a country like Pakistan. Specifically, their inclusion of what they call semi-dense towns and suburban areas is rather too generous and should be excluded from the definition of what constitutes urban.

Here is our rationale for why: urban spaces need more than just density. Specifically, they require being part of an urban supply chain of a set of amenities, where people tend to have access to markets for most consumer goods. Given the relatively low purchasing power of Pakistani consumers, it seems unlikely that such markets would be sufficiently developed in agglomerations that are less dense than 1,500 people per square kilometer, even if such areas are 2-3 kilometers from larger, more dense urban centers.

Then there is also the fact that Pakistani population centers tend to be naturally more dense than most developed parts of the two world for two reasons. The first is that Pakistanis have larger family sizes, and so each individual dwelling contains more people than would be typical in richer countries. The second is the fact that Pakistanis are relatively poorer, and can therefore afford smaller dwellings, which means that each street has more houses, causing density to rise further still.

Of course, this analysis has been performed using global data, so no doubt it includes many countries that have characteristics similar to Pakistan. But the data that the authors put forward for other countries seems to indicate estimates of urbanization that

seem too high, given their levels of income and complexity of their respective economies.

If we relied on this narrower definition of what constitutes urban in Pakistan, we arrive at a measure that seems more plausible: Pakistan is about 57% urban as of 2023, a number that has been slowly – but less dramatically – rising over the past few decades.

If we adopt this narrower definition, Pakistan crossed over to become majority urban around 1990, so the increase over the past three decades has been a slow, but steady increase in urbanization. This data then seems more aligned with the scale of movement in other measures of economic activity that are correlated with increased urbanization, most notably the proportion of the population engaged in agriculture or livestock farming.

In short, yes Pakistan is likely significantly more urban than the government’s estimates, and yes, it is majority urban, and yes it has been majority urban for at least three decades now. But no, it has not yet surpassed the urbanization levels of the United States as might have been implied by the World Bank paper.

So, what are these denser rural areas?

We do not mean to discount the World Bank study’s methodology completely. What they are measuring is something real, which is the fact that the single biggest increase in Pakistan’s population has come from the rise in the number of people living in these not-quite-dense areas that are very close to dense cities and towns.

This is a phenomenon worth understanding, and one that we are still aiming to compile more reporting and research about. But some initial observations come to mind.

Firstly, there is the fact that many small towns on the outskirts of major cities have become parts of the city proper, such as the examples we cited earlier in the article. The

villages that used to be close to these virtually non-existent urban areas in the past have now started to be characterized as suburban, and in some senses, that is not an inaccurate description. However, perhaps it mischaracterizes the degree to which they have changed relative to simply their surroundings having changed.

This is an important distinction, and one that has significant ramifications for the Pakistani economy. Urban Pakistan has been growing, and acquiring a greater diversity of types of neighbourhoods and dwellings than in decades past, but rural Pakistan has not changed nearly as fast as the rest of the country (though, of course, some change has happened).

This is something that we have been noting in our coverage of Pakistani agriculture: production has risen, but not by much, employment levels rose slightly but have stagnated even in absolute terms, and productivity levels in Pakistani agriculture have not meaningfully risen at all, and indeed in some cases have tragically even declined slightly.

The fact that more Pakistani villagers are living on the outskirts of cities and towns instead of being further away may be a physical manifestation of something more profound in the Pakistani economy: that all its citizens have their view towards life in the city, and hardly anyone is investing in improving the lives and livelihoods of rural Pakistan.

To be clear, as Pakistan progresses, much of the action will be taking place in cities as hubs of dynamism. But we seem to be seeing a larger proportion of our population in this halfway house, engaged in agriculture, but close enough to the towns that they seem more interested in a transition out of rural life rather than getting the best of it, leaving the country worse off for having both a disengaged effort in agriculture, but without the concomitant increase in urban activity.

The urbanization story is real, important, and positive. But the Pakistani farm deserves better than to be abandoned. n

Descon Oxychem takes a hit as imports flood the market

Some

exporting customers are allowed to purchase foreign competitors’ products, causing Descon to lose market share

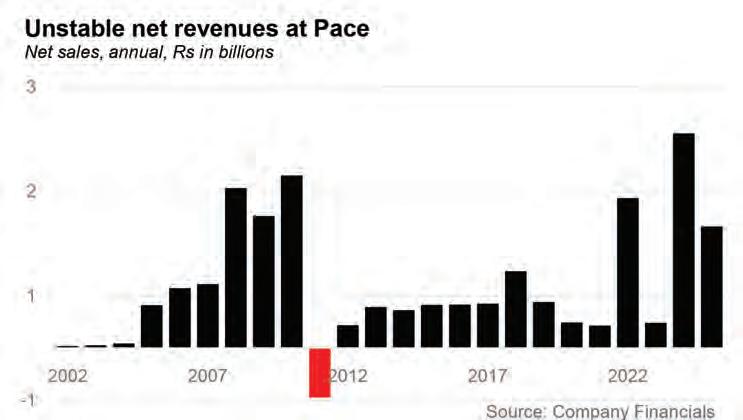

In the quiet language of quarterly accounts, reversals often announce themselves without fanfare. For Descon Oxychem Limited (DOL), Pakistan’s sole dedicated producer of hydrogen peroxide, the first quarter of fiscal year 2026 did precisely that. What had been a slow, uneasy trudge through FY25 now appears to be turning into a retreat.

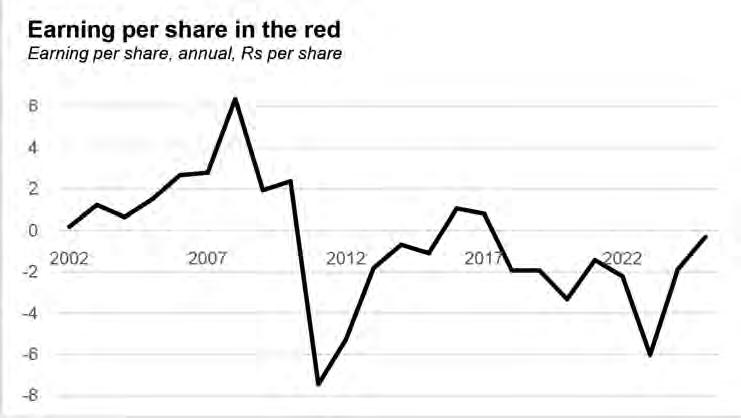

Revenue for Q1 FY26 fell seventeen percent year-on-year to PKR 1.25 billion, down from PKR 1.50 billion during the same period last year — a stark reversal for a company whose full-year FY25 revenue had at least managed nominal growth of four percent despite an inflationary environment that made such growth effectively contractionary in real terms. The firm’s latest briefing to investors lays out the contrast bluntly: operating profit for the first quarter fell forty-seven percent, while profit after tax slid thirty-eight percent to PKR 109 million. Earnings per share declined from PKR 1.00 to PKR 0.62 .

These numbers tell a story of pressure building on multiple fronts. FY25 had been an odd year — revenue barely inched forward, but profitability improved meaningfully. Gross margin rose from twenty percent to twenty-nine percent, operating profit jumped seventy-two percent, and earnings per share rose to PKR 4.51 from PKR 2.69. The company cut costs aggressively, benefited from improved gas availability, and squeezed higher efficiency

from its operations. It was a year of making do, not a year of expanding horizons.

Yet as FY26 begins, even those modest gains appear precarious. The fall in sales signals not merely a cyclical dip but something structural: domestic demand is being eroded not by weakness in end-user industries alone but by a surge of cheaper imports entering the country through regulatory channels never intended to become a backdoor for market access.

DOL, once accustomed to a fairly predictable competitive environment, now finds itself fighting for its own home market. And unlike the typical industrial downturn — driven by business cycles or raw-material volatility — this one is shaped by policy misalignment, price arbitrage, and the rising openness of Pakistan’s import regime via the Export Facilitation Scheme (EFS).

A brief history of a quiet industrial player

Descon Oxychem was born of an era when Pakistan’s industrial ambitions still carried a strong streak of self-reliance. Established as a subsidiary of the broader Descon conglomerate, DOL was envisioned as a specialised chemicals manufacturer with a focus on hydrogen peroxide — a compound essential to textile bleaching, paper processing, disinfection, and increasingly, food-grade applications.

Operating from its plant near Lahore, the

company positioned itself as a stable supplier to Pakistan’s massive textile ecosystem, which alone accounts for roughly ninety percent of domestic hydrogen peroxide consumption. Over the years, DOL attempted to diversify modestly: experimenting with product grades, exploring regional export markets, and periodically expanding production capacity to stay ahead of demand.

But unlike cement, steel, or fertiliser, hydrogen peroxide has never been an industry of national strategic focus. It remains a narrow-use chemical with limited public visibility. As a result, DOL’s operational story has always been one of incremental improvements, quietly executed turnarounds, and small shifts in the margins.

Still, for a long time, this was enough. With limited domestic competition and a consistent base of textile mills reliant on local supply, the company carved out a market position that seemed durable. Even export volumes — though low in margin — offered a supplementary avenue for growth.

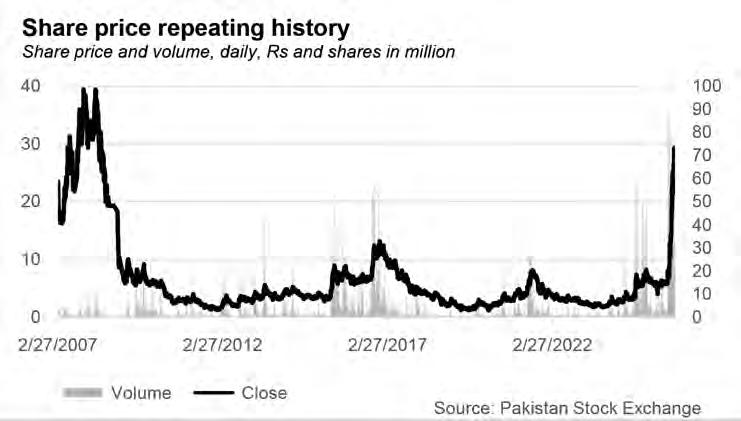

The company’s profile is, by any measure, that of a mid-sized industrial firm: its equity is valued at PKR 5.67 billion, its share price trades near PKR 32, and its annual domestic market of oxygenated chemicals hovers around 80,000 tonnes. These numbers say little about glamour but much about reliability.

Today, however, reliability is precisely what has been disrupted.

Product lines and production capacity

Hydrogen peroxide — H2O2 — is a deceptively simple molecule, yet its industrial uses vary widely. Descon Oxychem manufactures primarily two categories: technical-grade peroxide, used largely in textile bleaching, and food-grade peroxide, which is purer and commands higher prices in sanitisation and packaging applications.

The company has recently emphasised the development of a “spray-grade” product tailored for the food-processing industry. Management believes this segment offers significant margin potential, noting that food-grade peroxide sells at a premium compared to technical-grade volumes. Early progress suggests that new volumes from this product line may help diversify revenue in later quarters.

Production capacity has also grown over the years. DOL expects combined output this year to reach around 67,000 tonnes, a meaningful share of Pakistan’s total demand but still short of full import substitution. Complicating matters is the recent entry of a new domestic competitor expected to add another 36,000 tonnes of supply — ostensibly displacing imports from Bangladesh but also tightening competition within Pakistan’s borders.

One signal of Descon’s attempts to remain cost-competitive is its investment in renewable energy: a two-megawatt solar plant now nearing completion, intended to offset a portion of the company’s three to 3.5 MW power requirement. Solar is a hedge, partly against volatility in grid electricity tariffs and partly against the company’s dependence on gas. For FY26, the government has revised the gas blend from a seventy-five percent RLNG and twenty-five percent system-gas combination to a fifty-fifty mix — a change that may lower costs but also introduces operational complexity.

Despite these improvements, DOL remains vulnerable to global pricing differentials. Imported Korean hydrogen peroxide lands in Pakistan at around USD 450 per tonne; Bangladeshi imports are even cheaper at roughly USD 325 per tonne. Local manufacturing costs — tied to gas, labour, and financing costs — make such prices difficult for Pakistani producers to match. This vulnerability becomes fatal when import channels are liberalised beyond their intended scope.

and the flood of imports

The core challenge facing Descon Oxychem today is not simply that imports exist; it is that the regulatory environment has effectively

subsidised access to those imports for certain customers. Through the Export Facilitation Scheme — a programme originally designed to help exporters access raw materials duty-free — foreign producers have gained a foothold in Pakistan’s domestic market. Nearly eighty percent of imports now enter the country through EFS channels, according to DOL’s recent briefing to analysts .

For a chemicals producer whose fortunes depend on consistent domestic demand, this shift is enormous.

The logic of EFS was straightforward: export-oriented businesses were allowed to import inputs without paying duties, on the understanding that these inputs would be used exclusively to produce goods for foreign markets. But enforcement has been porous, and the distinction between export-linked usage and domestic substitution has eroded. Some textile exporters — DOL’s core customer base — are legally permitted to import hydrogen peroxide from abroad, only a portion of which is tied to export production. The result is a shadow market within the formal market: imported peroxide sells at prices below domestic manufacturing costs, and exporters can simultaneously consume imported chemical and compete with domestic firms for local sales.

For Descon, the economic impact is straightforward. Domestic production costs are higher than import prices; export sales earn lower margins because the company must absorb freight charges to compete with international suppliers; and regulatory gaps allow foreign suppliers to undercut the company within its own market.

The firm’s export margins have always been lower than domestic margins — a fact it openly acknowledges. Freight absorption is a structural necessity in its international business. But in past years, exports at least grew incrementally, providing a pressure valve during periods of weak local demand.

Now even that avenue is narrowing. Export volumes have declined over the past few years. Management’s current target — to rebuild exports by fifty percent — is aspirational, not reflective of immediate market conditions. Competition in the Middle East, especially in surface-water treatment and food-packaging segments, offers pockets of opportunity, but they are not large enough to counteract the losses inflicted by imports entering Pakistan through EFS.

The company’s tone in its investor communications has become increasingly insistent. It is “engaging with regulatory authorities” to address misuse of the EFS and lobbying for the extension of anti-dumping duties to “counter unfair competition.” These are not the words of a firm operating in equilibrium; they are the words of a firm seeking state intervention to

restore a competitive balance that has tipped sharply against it.

The larger question is whether Pakistan’s broader industrial policy favours firms like DOL at all. Hydrogen peroxide imports — particularly from Bangladesh — reflect lower energy costs and cheaper labour, structural advantages difficult for Pakistani manufacturers to overcome without help. The entry of a new domestic competitor may soften the blow by replacing some low-cost imports, but it also intensifies competition in a market that is already contracted by regulatory arbitrage.

The situation leaves Descon in a paradox: it is the country’s primary domestic producer, yet it is simultaneously unprotected and uncompetitive.

A company at an inflection point

The story of Descon Oxychem today is not one of mismanagement or strategic miscalculation. It is a story of structural asymmetry. Its revenue decline in Q1 FY26 is not a result of falling demand for hydrogen peroxide — textiles still consume vast quantities — but of imported supply crowding out local manufacturers. Its margins fell not because it raised costs irresponsibly but because global competitors enjoy advantages in scale, energy pricing, and regulatory arbitrage.

The company has taken steps to adapt: solar power investments, product diversification, attempts to rebuild export volumes, and operational efficiency gains. But adaptation has limits when policy regimes enable foreign suppliers to redefine market pricing.

Descon’s appeal to regulators is part economic argument, part existential plea. Without controls on the misuse of EFS, the domestic market becomes a sieve. Without anti-dumping duties on products priced far below Pakistan’s cost of production, no amount of efficiency can make a local producer competitive. Without updated industrial policy, Pakistan’s chemicals sector risks becoming dependent on the very imports it once sought to replace.

The irony is sharp: a manufacturing company built to supply Pakistan’s largest export industry now finds itself asking the state to compel that industry to buy locally.

Whether policymakers heed that request will determine more than Descon’s next quarterly earnings. It will shape whether Pakistan can sustain any meaningful chemical manufacturing capacity in the face of global competition and liberalised import channels.

For now, the numbers tell their own story — a profitable FY25, a precarious FY26 beginning, and a future uncertain enough to make even stable chemical molecules feel volatile. n

Attock Petroleum steadies outlook

Market headwinds shape refined fuels, EV shift

Attock Petroleum Limited (APL), one of Pakistan’s leading oil marketing companies, is entering fiscal year 2026 with mixed indicators as recent financial results highlight pressure on margins, shifting product dynamics and the sector’s ongoing transition away from furnace oil. While annual earnings and sales declined in FY25, the first quarter of FY26 shows signs of recovery, indicating that the company’s operational adjustments and diversification efforts may be cushioning the broader industry slowdown.

APL closed FY25 with earnings per share of Rs 83.5, down from Rs 111.1 in FY24, reflecting a 25% contraction in profitability over the year. The fall in earnings mirrors a 10% decline in net sales, which dropped to Rs 474.1bn from Rs 526.3bn, and a 15% reduction in gross profit as furnace oil volumes continued to shrink. The company’s net margin eased to 2%, compared with 3% the previous year.

However, the opening quarter of FY26 reverses part of that trend. APL posted an EPS of Rs 30.6 in 1QFY26, up 60% from Rs 19.2 in 1QFY25. Net sales increased by 4% year-onyear, reaching Rs 117.8bn, while gross profit nearly doubled to Rs 7.6bn on the back of stronger margins in petrol and diesel, which together form the backbone of the company’s product mix. Operating profit grew by a remarkable 195% to Rs 5.2bn, and EBITDA rose 163%, pointing to improved throughput and stronger non-fuel contributions.

Even so, the company’s financials remain constrained by rising costs and fixed margins. Since November 2023, OMCs have operated under a fixed margin of Rs 7.87 per litre on premium motor gasoline and high-speed diesel. With average retail prices around Rs 275 per litre during FY25, the fixed margin now constitutes under 3% of the final consumer price — lower than the industry’s historical minimum of 3.5%.

This margin freeze has directly affected APL’s bottom line, despite its position as the country’s third-largest OMC by market share, holding 9.3% by FY25. Though the company experienced a 9% dip in overall market share owing to the steep decline in furnace oil, its share in core products strengthened modestly, supporting a more balanced revenue mix.

The pressure on net finance income also weighed on FY25 results. A significant drop in bank profit rates — from an average of 21.7% in FY24 to 15.1% in FY25 — cut APL’s finance income by 35%. The lower interest environment is consistent with the broader monetary easing cycle that began after Pakistan entered a more stable phase of its IMF programme.

Overall, APL’s FY25 performance reflects both the structural challenges facing Pakistan’s OMC sector and the company’s reliance on regulated margins at a time when operating costs continue to climb. Yet the strong rebound in 1QFY26 signals that its diversification investments, strategic locations and expanding product lines are positioning the company more favourably for the years ahead.

A legacy shaped by the

Attock Group and Pakistan’s evolving fuels sector

Attock Petroleum Limited was incorporated in 1995 as part of the Attock Group, a vertically integrated energy conglomerate with upstream, refining and downstream footprints. The Group’s lineage stretches back to the early twentieth century, with Attock Oil Company pioneering oil production in the region during the British colonial period. This legacy has allowed APL to leverage integrated supply chains — from crude extraction to refining and distribution — a characteristic that sets it apart from many newer OMCs.

The company formally commenced operations in 1998 and has since grown into one of Pakistan’s most strategically located petroleum retailers. While its national footprint is smaller than state-run Pakistan State Oil (PSO), APL has carved out a niche in high-throughput corridors, particularly on motorways and in major urban centres, where the company owns and operates 45 COCO (company-owned, company-operated) outlets. These sites include locations along M1, M3, M4, M5, M9, M14, E-35 (Hazara Motorway) and key cities where consistent traffic flow ensures dependable volumes.

Its business model prioritises owning retail sites rather than franchising them, a strategy that requires large amounts of capital upfront

but yields stronger control over pricing, branding and throughput practices. This approach was recently illustrated when the company secured a premium retail outlet at a Capital Development Authority auction on the Kashmir Highway, costing approximately Rs 3.3bn.

APL’s current portfolio also spans aviation fuels, non-fuel retail, lubricants and specialty products. Its participation in the aviation fuel market, where margins align closely with those earned in PSO’s joint venture operations, provides a stable high-margin revenue stream in a segment where competition is limited.

Alongside fuel marketing, APL’s non-fuel retail segment — comprising tuck shops, tyre shops and allied services at COCO sites — contributes nearly Rs 500mn annually. This area has become increasingly important as global OMCs shift towards lifestyle-oriented retail formats, using forecourts as consumer spaces rather than pure fuel points.

Products, capacities and expanding investments in LPG and EVs

Although the decline in furnace oil has suppressed revenue over the past two years, APL’s core products remain high-speed diesel (HSD) and premium motor gasoline (PMG), which collectively account for between 70% and 80% of its total portfolio. These products have proven more stable and continue to deliver reliable volume growth in urban centres despite fluctuations in macroeconomic conditions.

The company has also strengthened its role in aviation fuels, where margins range from USD 6 to USD 10 per barrel, based on previous disclosures from PSO. This provides a high-value contribution to APL’s product mix, partially balancing the volatility seen in motor fuels.

The company’s most significant new investment is its expansion into liquefied petroleum gas (LPG) storage and distribution. APL has completed construction of a 200-tonne LPG storage and filling facility in Morgah, with initial consignment decantation already underway. Full operations are scheduled to start in the first week of December.

The company aims to sell between 600 and 800 tonnes per month initially, targeting northern regions before expanding capacity to between 3,000 and 4,000 tonnes within six months. Future installation plans include mid-country zones and Karachi, signalling an ambition to become a significant player in Pakistan’s LPG retailing landscape.

This expansion comes at a time when the LPG market is expected to soften slightly following the introduction of RLNG, which is currently about 35% cheaper. The price

difference may compress LPG’s competitiveness in lower-income segments, but household reliance on LPG in off-grid regions is expected to maintain demand momentum.

Perhaps the most strategically important development for APL is its expansion into electric vehicle charging infrastructure. Pakistan’s federal EV policy mandates that charging stations be established every 80 kilometres on motorways, a requirement that leans heavily on OMCs with existing motorway presence. APL, uniquely positioned with multiple motorway COCO sites, has already installed three operational EV charging stations.

The company has entered partnerships with Hub Power Company (Hubco) and Huawei to roll out more stations, targeting over 30 operational EV chargers by the end of 2026. This ties directly into the government’s broader clean mobility goals, which encourage the shift to electric motorcycles, rickshaws and passenger cars.

While EV adoption in Pakistan remains limited, APL’s early investments are a long-term hedge against declining fossil fuel demand. The company’s motorway-centric strategy also positions it as a convenient charging provider for inter-city transport once EV adoption accelerates.

Navigating a market in transition

APL’s current performance cannot be separated from the headwinds facing Pakistan’s wider oil marketing sector. Furnace oil, once a key contributor to OMC revenues, has been in structural decline for years due to its diminishing role in power generation. The shift towards LNG-fired plants, hydropower expansion and greater renewable penetration has left furnace oil sales volatile and frequently depressed.

APL, along with PSO, has historically held a strong share in furnace oil; as a result, the decline has disproportionately affected both companies. This explains the 9% dip in APL’s overall market share, despite strengthening its position in petrol and diesel.

Yet, the broader market is shaped by more than just furnace oil. The OMC sector is grappling with:

• Stagnant regulated margins on petrol and diesel for nearly two years.

• High operating costs driven by inflation, freight charges and security expenses.

• Growing competition from new entrants seeking high-throughput sites.

• Demand fluctuations tied to GDP momentum, dollar parity and transport sector performance.

At the same time, the government’s policy direction is nudging OMCs towards cleaner fuels. The EV policy, in particular, is pushing

companies to invest in charging infrastructure even before demand fully materialises. For APL, this is both a challenge — due to upfront installation costs — and an opportunity, thanks to its motorway footprint.

The introduction of RLNG as a cheaper alternative to LPG, meanwhile, is forcing OMCs to reassess their gas marketing strategies. For APL, which is entering LPG storage and distribution for the first time, the market shift introduces additional pricing pressure, but also opens up opportunities to supply mixed-fuel households in regions where piped gas is unavailable.

Overall, Pakistan’s downstream petroleum market is in a phase of transition. Diesel and petrol remain dominant, but long-term trajectories show increasing electrification, tighter margins, and diversification into gas and non-fuel retail. Companies with strong infrastructure ownership — like APL — may be better positioned to navigate this shift, especially if regulatory changes eventually allow for more flexible pricing.

APL’s significant cash reserves, retained for mergers, acquisitions and high-value location purchases, also provide optionality. The company has indicated a preference for inorganic expansion, allowing it to secure sites like the Kashmir Highway outlet without compromising liquidity.

A cautious but adaptive outlook

While FY25 underscored the pressures of operating in one of Pakistan’s most regulated sectors, APL’s first quarter FY26 results offer cautious optimism. The company has shown that improving product mix, operational efficiency and strategic investments can offset some of the structural weaknesses in the sector. Its growing EV infrastructure footprint, new LPG investments and continued emphasis on motorway-centric COCO outlets indicate a forward-leaning strategy.

Nevertheless, risks remain. Continued delays in revising OMC margins could constrain bottom lines further, while the shift to RLNG may slow LPG profitability. Meanwhile, the broader macroeconomic environment — including currency volatility and energy policy shifts — will continue to influence sales volumes.

APL’s immediate trajectory will hinge on execution: scaling EV charging stations; achieving targeted LPG throughput; and maintaining volumes in premium motor gasoline and diesel as economic activity fluctuates. As Pakistan’s energy mix evolves, APL’s diversified approach suggests that adaptation, rather than dependence on traditional fuel streams, will define the company’s competitive edge. n

Ghani Chemworld seeks to replace Pakistan’s imports of calcium carbide

One of the largest importers of the chemical now wants to manufacture as much of it domestically as possible

When Ghani Chemworld Ltd (GCWL) listed on the Pakistan Stock Exchange in April 2025, it did so with a single-minded purpose: to build Pakistan’s first large-scale plant dedicated to manufacturing calcium carbide and its derivatives, and in the process turn one of the country’s more obscure import lines into an exportable surplus.

The company is a freshly minted public limited concern, incorporated in July 2024 as a wholly owned subsidiary of Ghani Chemical Industries Ltd (GCIL). Under a court-sanctioned demerger and merger scheme, GCIL’s in-progress calcium carbide project was carved out and transferred into Ghani Chemworld, with GCIL shareholders receiving shares in the new vehicle. In other words, what investors are buying on the stock market today is essentially a pure play on one project: a greenfield calcium carbide complex at the Hattar Special Economic Zone (SEZ) in Khyber Pakhtunkhwa.

According to a recent corporate briefing, the plant has a planned annual capacity of roughly 25,000 tonnes of calcium carbide, making it the first facility of this scale devoted to the product in Pakistan. The project enjoys a ten-year income tax exemption under the SEZ regime, a concession that applies to both domestic sales and exports and is central to the company’s profitability calculations. Management expects commercial production to begin in early December 2025 after commissioning and test runs under the supervision of Chinese and European technical advisers.

The factory relies on an electric arc furnace rather than coal gasification, making electricity its primary fuel. Ghani Chemworld estimates power demand at around 11-12 megawatts (MW) and is keen to benefit from any subsidised industrial tariff packages that the government may extend over the next few years. The decision to avoid coal gasification aligns with a broader shift in Pakistan’s industrial policy towards cleaner, grid-based energy for new projects, even as the company still depends on imported coke or semi-coke from China as a key raw material.

Raw materials are, in fact, where the company believes it can build a cost edge over the imported product it wants to displace. Limestone, one of the two main inputs, is procured locally from mine owners at an all-in cost of about Rs3,000 per tonne, including transport to Hattar. Ghani Chemworld does not mine the limestone itself and therefore avoids royalty payments, treating it as a straightforward procurement expense. The other major input, coke or semi-coke, is imported, typically from China, at around $325-350 a tonne for the required quality. Management says it is shunning cheaper Iranian material because higher sulphur content would compromise product quality and downstream customer processes.

The plant will not only produce calcium carbide. The process also yields lime (calcium oxide) and precipitated calcium carbonate (PCC), which Ghani Chemworld intends to market into industries ranging from paper and packaging to paints, plastics, food and pharmaceuticals. If utilisation on the main lines does not reach the targeted eighty percent in the second full year of operations, management plans a “Phase II” to add secondary products such as acetylene gas, hydrogen, magnesium oxide and carbon black, using finer calcium carbide fractions as feedstock. Additional capital expenditure for hydrogen and carbon black is estimated at roughly Rs1.2 billion, with another Rs500 million for magnesium oxide.

The ambition, however, is clearest in the market share numbers. Ghani Chemworld estimates Pakistan’s domestic calcium carbide consumption at around 12,000-15,000 tonnes a year, of which more than ninety 5% currently arrives as imports, largely from China. Ghani Group companies have been trading the product for about 15 years and currently handle around 40% of the local market through imports. With the new plant, management is targeting nothing less than ninety percent of domestic demand, along with exports to the Middle East, Central Asia, Eastern Europe and Turkey.

To reinforce that import-substitution thesis, Ghani Chemworld says it will lobby Islamabad to reset customs duty on imported calcium carbide. The duty had previously stood at 16% but was lowered to around 7-8% in recent years; management argues that

reinstating the higher rate would support local industry and conserve foreign exchange, especially now that a domestic producer is emerging.

Calcium carbide sits at the heart of several industrial value chains. At the most basic level, it is used to generate acetylene gas when reacted with water. Ghani Chemworld’s briefing describes acetylene as the main intermediate, widely used for precise metal cutting and welding applications across manufacturing, construction and automotive repair.

Acetylene also serves as a building block for a range of downstream chemicals. One of the most important is polyvinyl chloride (PVC), the plastic used in pipes, cable insulation, flooring and countless other products. Industry reports and stock-exchange filings note that calcium carbide, often referred to as calcium acetylide, is an established route to acetylene for PVC production, especially in countries where coal and limestone are abundant. That gives the material strategic importance in emerging economies whose infrastructure booms are PVC-heavy.

Beyond acetylene, Ghani Chemworld’s process will spin out two co-products that feed quietly into many everyday items. Precipitated calcium carbonate, or PCC, is used as a filler and coating pigment in the paper industry, a stabiliser in plastics and rubber, and a key ingredient in paints and coatings to improve whiteness and gloss. It is also used as a supplement or stabiliser in certain food and pharmaceutical formulations. Lime or calcium oxide, another output, finds demand in leather tanning, sugar refining, and the paper and pulp industry, and in various environmental and water-treatment applications.

Globally, the calcium carbide market is projected to grow at a steady pace, with research firms forecasting mid-single-digit annual growth over the latter half of this decade, driven by chemical and metallurgy demand in Asia. Pakistan, despite being only a mid-sized industrial economy, ranks among the world’s larger importers of the compound: trade data suggest it brought in about $8 million worth of calcium carbide in 2023, making it one of the top dozen importers worldwide. Those imports increasingly originate from a small cluster of suppliers. China alone

accounts for roughly two-thirds of Pakistan’s calcium carbide imports, with Mexico and Slovakia providing much of the remainder. The result is a classic vulnerability: a critical industrial input, used across welding shops, fabrication yards, PVC production and various chemical plants, is largely dependent on a few foreign sources and on the country’s limited foreign-exchange reserves.

Ghani Chemworld’s project aims to change that equation by placing a sizeable chunk of capacity within Pakistan’s borders. With nameplate output higher than estimated domestic demand, the company envisions a base load of local customers supplemented by export contracts into neighbouring regions where there is either no local producer or where producers are operating at tight capacity. If the plan works, calcium carbide could move from being a pure import line for Pakistan to a minor but useful export earner.

Behind Ghani Chemworld stands one of Pakistan’s more quietly influential industrial families. Ghani Group of Industries traces its roots back more than half a century, with a reputation built primarily in glass. Based in Pakistan but with a presence in the United Arab Emirates, the group operates multiple glass plants, producing container glass, float glass, pharmaceutical glass and value-added products such as tempered and bent glass.

The group’s narrative has often centred on import substitution. Its glass businesses are credited with replacing a large portion of Pakistan’s mirror and speciality glass imports by investing early in domestic capability and introducing technologies like “spectrum” coated mirrors. Over time, Ghani entities have spread across the stock exchange: Ghani Glass, Ghani Global Glass, Ghani Global Holdings and various associated companies in industrial gases and allied sectors.

Ghani Chemical Industries, the parent from which Ghani Chemworld was spun out, itself grew out of the group’s diversification into industrial, medical and speciality gases. As that business gained scale, management identified calcium carbide as a natural adjacency: the compound is not only a raw material for acetylene gas but also interacts with several chemical value chains the group already serves.

For around 15 years, Ghani Group companies have been among Pakistan’s leading traders and importers of calcium carbide, handling roughly 40% of the domestic market. That trading background has given them an intimate view of price cycles, quality differentials and customer requirements. It has also laid bare the country’s dependence on imported supply, especially during periods of currency stress when dollar-denominated inputs become more expensive overnight.

The decision to build a domestic plant, and later to spin it into a separately listed company, fits within this broader pattern. In November 2024, shareholders of Ghani Chemical Industries approved a demerger that would transfer the calcium carbide project into Ghani Chemworld. The Lahore High Court subsequently sanctioned the scheme in February 2025, with formal confirmation in March, clearing the way for the project to be shifted wholesale – assets, liabilities, incentives and all – into the new subsidiary.

By April 2025, Ghani Chemworld was listed on the PSX as a separate entity, giving investors a direct line into the project. For the Ghani Group, this structure does several things at once: it ring-fences project risk, creates a specialised platform for future expansions in carbide and derivatives, and taps public equity to help fund the sizeable capital expenditure involved. Investors, in turn, get a focused bet on an import-substitution story backed by a group with a track record of building and operating heavy industrial plants.

As of the first quarter of financial year 2026, Ghani Chemworld remains in the pre-commercial stage, with no sales recorded from the calcium carbide plant.

The real story, therefore, lies in management’s projections for when the plant starts running. For the first seven months of commercial operations – effectively the remainder of FY26 after the December start-up – Ghani Chemworld is targeting production of 10,00011,000 tonnes of calcium carbide, equivalent to utilisation in the low-to-mid forties as a percentage of nameplate capacity. By the second full year, the company hopes to ramp up to around 80% utilisation, which would put annual output close to 20,000 tonnes.

On the revenue side, management is guiding to between Rs3-4 billion in sales in that initial seven-month period, rising to roughly Rs8-9 billion in the following year once the plant is operating for twelve months at higher utilisation. Net profit margins, excluding the contribution from associates, are expected to be in the 6-7% range in the partial first year, before climbing towards 10% as scale benefits, tax exemptions and process optimisation kick in.

These numbers hinge on several moving pieces. Power costs are an obvious variable: with an electric arc furnace consuming more than ten megawatts, any volatility in industrial tariffs will feed quickly into unit costs. Ghani Chemworld hopes to benefit from discounted industrial power schemes, at least in the early years, though such incentives are always subject to fiscal pressures and policy change. Raw material prices, especially imported coke, are another risk factor, given their linkage to global commodity cycles and freight rates.

A strengthening rupee would cushion those costs; a renewed bout of currency weakness would have the opposite effect.

Competition is, paradoxically, both limited and intense. On the one hand, there is no domestic competitor of similar scale; Ghani Chemworld’s plant will effectively define Pakistan’s local capacity. On the other hand, imported calcium carbide is a commoditised product with multiple overseas suppliers, so local producers must maintain quality and cost discipline to avoid being undercut despite tariffs. The company’s long history as an importer gives it a benchmark for landed costs and quality standards, which may help in calibrating pricing strategies.

Policy, too, will play a decisive role. Ghani Chemworld’s call to raise customs duty on imported calcium carbide back towards sixteen percent is justified, in management’s view, by the need to protect a nascent domestic industry and conserve foreign exchange. But regulators will have to weigh that request against downstream users’ concerns over input prices, particularly in welding, fabrication and PVC-related industries that are already grappling with energy and financing costs. A balance will need to be struck to ensure that one piece of the industrial ecosystem is not strengthened at the expense of another.

For investors, the appeal of Ghani Chemworld is straightforward: a newly listed company with a single, clearly defined project that addresses a tangible import bill. Pakistan imported about eight million dollars’ worth of calcium carbide in 2023; if Ghani Chemworld can replace most of that with domestic production and also carve out a niche in export markets, the earnings potential is obvious. The tax holiday, SEZ incentives and low-cost limestone supply add further upside to the economics, provided the company can manage execution risks and keep the project on schedule.

Yet it is equally clear that the business will be exposed to commodity cycles, energy policy and regulatory decisions on trade. In that sense, Ghani Chemworld is a microcosm of Pakistan’s broader industrial challenge: how to move from trading imported materials to making them at home, without simply shifting risk from the customs gate to the factory floor.

What is different here is that the sponsor group has walked this road before. Ghani’s glass businesses are now an integral part of Pakistan’s manufacturing landscape, and its gas operations have carved out their own space. If the same playbook of disciplined execution, technology partnerships and market development can be applied to calcium carbide, the company may yet turn a niche chemical into a small but symbolically important success story for local industrialisation. n

IBL Healthcare aims to triple revenue by 2030

The company’s focus for growth is artificial sweeteners, and cold and flu medications

When IBL Healthcare Ltd (IBLHL) sat down with analysts in November, the message was a mix of celebration and caution. The health and wellness distributor has just posted its strongest year on record, riding the same wave of deregulated prices and volume recovery that lifted much of Pakistan’s regulated healthcare sector in 2025. But the first quarter of financial year 2026 already hints at a slower tempo — and a future in which growth will depend less on price resets and more on a deliberate push into artificial sweeteners, cold and flu remedies, and new wellness categories.

At the heart of the strategy is a bold target: to triple the size of the company by 2030, anchored in Stevia-based sweeteners and overthe-counter cold, cough and flu brands, with women’s health and holistic adult nutrition as the next frontiers.

IBL Healthcare’s full-year FY25 numbers underline just how strong the recent upswing has been. Net sales climbed from about Rs3.6 billion in FY24 to roughly Rs4.3 billion in FY25, a rise of 20 percent. Gross profit jumped 52% to Rs1.4 billion, lifting the gross margin from 26% to 33 percent. Profit after tax surged from a token Rs8 million in FY24 to Rs208 million in FY25, taking the net margin to 5 percent. Earnings per share moved from almost break-even — roughly Rs0.1 — to about Rs2.1.

For a company that complained that profits were still constrained by Pakistan’s minimum-tax regime, this was nonetheless a banner year. A healthier product mix and tight control of operating costs did a lot of the heavy lifting: selling and distribution expenses grew 24% and administrative expenses 37 percent, both slower than the rise in gross profit, so operating profit almost trebled to Rs445 million.

The latest quarter, however, tells a more subdued story on the top line. In 1QFY26, net sales were Rs1.1 billion, up only 4% from the Rs1.1 billion recorded in the same quarter of FY25. Gross profit, by contrast, rose a brisk 18%, pushing the quarterly gross margin

further up from 32% to 36%. Profit after tax improved from Rs60 million to Rs70 million, with earnings per share edging up from Rs0.6 to Rs0.7.

In other words, the early months of FY26 are seeing slower revenue growth but continued margin expansion. Management was explicit about why: the company has been pruning lower-margin businesses. It has divested traditional pharmaceutical products and its ophthalmology portfolio, lines that were “more oriented toward a pharmaceutical company than a health and wellness company”, and is redeploying focus and capital towards higher-margin wellness and consumer-health franchises.

That shift is already visible in the income statement. Cost of sales rose only 8% in FY25 against the 20% rise in sales, and actually fell 2% year-on-year in 1QFY26 despite the increase in revenue. The result is a business that is growing more slowly in rupee terms than last year, but earning more from each rupee of sales.

For investors coming off a heady 2025, the deceleration in first-quarter revenue growth is a reminder that the sector-wide tailwinds — higher regulated prices, restocking after shortages and a rebound in demand post-Covid — may not be repeatable at the same pace. The task now is to show that the new, leaner portfolio can support sustained double-digit profit growth even if sales grow in the mid-single digits some quarters.

IBL’s management seems acutely aware of that imperative. The corporate briefing repeatedly emphasised that the company is not “solely a distribution company” but a brand-owning, marketing-driven organisation that arranges manufacturing through tolling and partners such as The Searle Company, while using the broader IBL Group’s distribution arm for physical logistics. That distinction matters because, unlike a pure distributor, IBL Healthcare can shape its portfolio, prices and promotions, not merely pass through someone else’s decisions.

The same briefing laid out the growth blueprint in unusually clear terms. The long-

term goal is to triple company size by 2030. In the near term, the emphasis is squarely on Stevia-based sweeteners and cold, cough and flu remedies, with women’s health and holistic adult nutrition identified as the next wave of expansion.

A quick scan of IBL’s product line-up explains why management is so fixated on sweeteners. On the company’s own website, the health and wellness category is dominated by sugar substitutes: multiple variants of Canderel — tablets, jars, sachets, sucralose and Stevia versions — sit alongside Equal in similar forms, as well as vitamin waters and other low-calorie beverages.

IBL is the marketing affiliate in Pakistan for Canderel, a global tabletop sweetener brand originally developed in Europe, and promotes it as a zero-calorie alternative to sugar for people with diabetes and those trying to reduce their sugar intake. The Canderel Stevia range, in particular, is positioned as a “natural” sweetener, using plant-based glycosides to deliver sweetness without calories.

In a country like Pakistan, the addressable market for such products is huge. The International Diabetes Federation estimates that about 31.4% of Pakistani adults live with diabetes — roughly 34.5 million people — giving the country one of the highest diabetes prevalence rates in the world. A 2023 commentary using the same IDF data described Pakistan bluntly as “the world’s number one country for diabetes prevalence”, with more than 33 million adults affected.

Against that backdrop, it is not surprising that IBL’s “healthier sugar alternatives” segment is outpacing the rest of the business. According to the company’s 2025 annual report, sales of these healthier sugar alternatives — led by Canderel and Equal Stevia variants — grew 50% in FY25, compared to 20% growth in overall revenue that year. That means sweeteners are not only aligned with public-health needs; they are also one of IBL’s fastest-growing profit centres.

On the cold and flu side, IBL markets a cluster of brands: Remac syrups and tablets, Remac Plus, and Lebon cough syrups, among

others, are all listed in its product catalogue under consumer health. These remedies, distributed through pharmacies and general trade, slot into a familiar Pakistani pattern of self-medication during winter and viral outbreaks. Post-Covid, consumer willingness to spend on symptomatic relief and immunity boosters has risen markedly, giving these lines fresh momentum.

A third pillar of growth is infant and specialised nutrition. IBL is the local partner for Mead Johnson’s Enfamil and Enfagrow formulas, as well as Prep-up baby cereals and Nestlé’s medical nutrition products such as Peptamen and Novasource Renal. The “biggest current item”, management told analysts, is the price repositioning and relaunch of the Mead Johnson portfolio. After years at the “super-premium” end of the infant-formula market, prices have been moved down into the mainstream premium bracket, which has already started to deliver a “significant upside” in both revenue and units.

All of this sits on top of a sizeable medical devices and disposables business – ranging from haemodialysis consumables to IV sets, surgical gloves and syringes – and a growing ophthalmic portfolio of vision-care products and contact lenses.

Crucially, IBL does not manufacture most of these products in-house but “owns” the brands locally and arranges for their production through toll manufacturers or Searle factories. For the actual physical distribution, it relies on IBL Operations, the group’s distribution arm, allowing the listed company to behave more like a marketing, brand-management and supply-chain co-ordinator than a warehouse operator.

Even so, localisation is becoming a bigger theme. The company says it is focusing on increasing local production to mitigate the impact of foreign-currency swings and imported inflation; exports, it stresses, will follow localisation rather than precede it. The closure of the Afghan border in recent months, which has disrupted some cross-border trade and smuggling, has had little direct impact on IBL because it does not export to Afghanistan. If anything, management believes, it could see a marginal benefit if parallel-imported or smuggled products are squeezed out of the domestic market.

IBL Healthcare sits at the junction of two powerful corporate ecosystems: The Searle Company Limited, one of Pakistan’s larger pharmaceutical players, and the International Brands (IBL) Group, a distribution and brand-building conglomerate.

The company was incorporated as a private limited entity in July 1997 and for many years operated as a wholly owned subsidiary of Searle, focusing on healthcare nutrition and medical disposables. In November 2008 it con-

verted into a public limited company, and in 2011 it listed on the Pakistan Stock Exchange, giving investors a direct route into a portfolio that was increasingly skewed towards overthe-counter healthcare, nutrition and medical devices rather than prescription drugs.

From the outset, the idea was to “tap the potential of healthcare nutritional products and medical disposables” while leveraging IBL’s distribution expertise. Over time, the company has stitched together a roster of global principals – from Mead Johnson and Nestlé in nutrition to Bausch + Lomb in vision care and various international device manufacturers – and layered on its own brands in sweeteners, vitamin waters and wellness products.

Today, IBL describes itself as a marketing-led healthcare company “committed to improve our community’s well-being and quality of life with world-class nutrition, medications, medical devices and other healthcare products”. It employs teams of marketing and sales specialists rather than armies of repackagers, aiming to “maximise the value of health through innovative products, devices and education that meet the changing needs of the population across Pakistan”.

Financially, the path has not been linear. Margins have swung over the years as exchange-rate shocks, imported inflation and regulatory price caps buffeted the sector. According to PSX data, IBL’s gross margin in FY23 was just over 33% and net margin almost 7.7 percent; in FY24, net margin fell sharply to 0.2% before rebounding to 4.8% in FY25 as the latest round of price adjustments and portfolio pruning kicked in.

The decision to double down on consumer-facing health and wellness, while trimming pure pharmaceutical lines, is the latest step in that evolution. It is a bet that brands like Canderel, Equal, vitamin waters and cold-and-flu remedies will prove more resilient and scalable than low-margin prescription products in a volatile regulatory environment.

If IBL’s strategy seems tailor-made for its time, that is because the broader context in Pakistan is changing rapidly.

On the one hand, the country is grappling with a full-blown diabetes crisis. The IDF estimates that more than a third of adults are living with diabetes or pre-diabetes, and recent research in Clinical Diabetes and Endocrinology describes an “alarming and rapidly increasing prevalence” driven by urbanisation, sedentary lifestyles and diets high in refined carbohydrates and sugar. A separate analysis notes that Pakistan now ranks among the top four countries globally by number of adults with diabetes.

On the other hand, awareness – and anxiety – about diet, weight and chronic disease is slowly rising, especially in urban middle-class households. Social media, gym culture and a

post-Covid preoccupation with immunity have all helped to put “sugar-free”, “low-calorie” and “vitamin-fortified” labels on the radar of consumers who might previously have ignored them.

IBL’s 2025 annual report captures this shift in numbers: healthier sugar alternatives, primarily Stevia and sucralose-based sweeteners sold under Canderel and Equal brands, saw sales jump 50% during FY25, more than double the company’s overall revenue growth of 20 percent. That suggests consumers are not merely trading down within existing categories; they are actively seeking out products they perceive as healthier.

In that context, a product like Canderel Stevia is more than just another sachet on the shelf. For millions of Pakistanis living with diabetes or at risk of it, replacing sugar with a non-caloric sweetener is a small but tangible lifestyle change. Online pharmacy listings explicitly pitch Canderel as an artificial sweetener “used by diabetic patients as replacement of normal sugar”, while IBL’s own marketing emphasises convenience and taste alongside calorie-free indulgence.

Similarly, vitamin-fortified waters, adult nutrition supplements and immune-support formulations tap into anxieties that have only deepened since the pandemic. IBL’s portfolio includes Searle Vitamin Water in multiple flavours, specialised nutrition drinks for renal and diabetic patients, and adult multivitamin brands such as Essential Plus and Pregna Essential.

The cold and flu franchise also stands to benefit from more health-conscious behaviour. Frequent viral outbreaks, poor air quality in major cities and growing distrust of unbranded syrups have nudged consumers towards recognised brands with corporate backers. Here, IBL’s Remac range and related products give it a direct stake in seasonal spikes in demand.

Of course, rising health consciousness is not an unalloyed positive for companies like IBL. As people read more about diet and disease, they also become more sceptical of ultra-processed foods, artificial sweeteners and aggressive marketing claims. Global debates over the long-term safety and metabolic impact of certain non-nutritive sweeteners can spill over into local conversations, even if regulators such as Pakistan’s DRAP continue to permit their use.

For now, though, the immediate pressures are more mundane: currency volatility, minimum-tax rules that bite even when profits dip, and the perennial risk of regulatory tinkering with prices. IBL’s response has been to push for localisation of manufacturing where feasible, refine its portfolio to favour higher-margin wellness products, and lean into categories where structural health trends offer natural tailwinds. n

As Panadol prices stabilise, Haleon’s revenue growth slows

The boost from deregulated drug prices is stalling, causing Haleon to look at new product launches in nutraceuticals and export markets for growth

Haleon Pakistan rode a powerful pricing wave over the past two years. The company behind Panadol, Sensodyne and CaC 1000 has seen its earnings swell as the government loosened control over many medicine prices and granted long-requested increases on paracetamol. But the latest numbers suggest that the easy part of the story may be over, and that future growth will depend much more on new products, exports and plain old volume rather than on price hikes.

Haleon Pakistan’s most recent published accounts – the nine months of calendar 2025 to September – show just how strong the deregulation windfall has been.

Net sales rose from Rs27.5 billion in 9MCY24 to Rs32.2 billion in 9MCY25, a robust increase of 17 percent. Management told investors that roughly 10 percentage points of that growth came from higher prices, with the remaining 7 percentage points driven by volume gains.

The impact on profitability has been even more striking. Gross profit climbed 35% over the same period, taking the gross margin from 33% to 38%. Net profit after tax jumped 43% to Rs4.6 billion, lifting the net margin from 12% to 14%. Earnings per share for the nine months rose from Rs27.4 to Rs39.2, while dividends per share for the period tripled from Rs5 to Rs15.

These results build on an already strong 2024. According to market data compiled from Haleon Pakistan’s 2024 annual report, the company booked net sales of about Rs43.6 billion that year, with net income of roughly Rs4.6 billion – both solid increases on 2023 and achieved before the full impact of deregulation had flowed through. In other words, 2024 was the set-up year; 2025 is turning into the “banner year” in which those policy changes fully hit the P&L.

But buried in the same briefing note is the first hint that the sugar rush is already fading. In the quarter ended September 2025, net sales grew by 8% year-on-year, from Rs9.8 billion to Rs10.6 billion – still respectable, but less than half the pace seen over the ninemonth period. EPS grew 21% in the quarter, compared to 43% for the nine months.

Part of that slowdown is simple arithmetic: once prices have been reset, there is only one chance to book the step-change. Subsequent quarters are measured against the new, higher base. That is exactly what investors are now seeing in Haleon’s numbers: price-led growth has peaked, and the company must increasingly rely on volume growth and mix.

Management appears to recognise this. The briefing note stresses that the strategic focus “moving forward” is a robust, volume-led growth strategy rather than repeated price increases, acknowledging that volume is the main driver for acquiring and retaining consumers in over-the-counter categories.

At the same time, Haleon believes it can sustain much of the recent margin improvement. The company is targeting gross margins of around 38% on a continuing basis, supported by efficiency gains, cost optimisation and selective, inflation-linked price adjustments rather than a new round of aggressive hikes.

Analysts modelling the company now expect that when the first quarter of 2026 is eventually reported, revenue growth will look far more subdued than the double-digit gains seen through much of 2025. The strong 2025 base, public frustration with rising medicine prices and the political sensitivity of a product as basic as Panadol all point in the same direction: the deregulation windfall is unlikely to be repeated, and Haleon will have to work harder for every rupee of incremental sales.

If the deregulation story looms large over Haleon’s financials, it is because of one product family above all others: Panadol.

The company’s own breakdown shows that Panadol accounts for 49% of Haleon Pakistan’s revenue mix, with calcium supplements under the CaC brand contributing 22% and oral-care products such as Sensodyne and Parodontax adding another 17 percent.

Using the 9MCY25 net sales figure of Rs32.2 billion and that 49% share, Panadol alone generated roughly Rs15.8 billion in sales in Pakistan during the first nine months of 2025. By the same logic, Panadol sales in 9MCY24 would have been about Rs13.5 billion. On a simple annualised basis, that puts Panadol’s 2025 Pakistan sales in the region of Rs21.0 billion – an extraordinary number for a single over-the-counter brand in a country

where per-capita incomes remain modest. These calculations assume that virtually all of Haleon Pakistan’s sales are domestic. That is a reasonable approximation given the current scale of its export business – historically only around mid-single digits as a share of sales, with management targeting 10% in the next couple of years. Even if exports were somewhat higher today, the order of magnitude would not change: Panadol is a tens-ofbillions-of-rupees franchise in Pakistan.

That scale is underpinned by market share. Haleon estimates that Panadol holds more than 40% of the analgesics segment in Pakistan, while about three-quarters of its Panadol portfolio is categorised as “essential”, which makes it more politically sensitive and more exposed to policy decisions on price control.

Alongside Panadol, CaC 1000 is the company’s other workhorse. The effervescent calcium and vitamin D supplement, together with sister brand Qalsium-D, accounts for around 22% of revenue and more than 30–35% market share in Pakistan’s bone and joint segment. Oral-care products, led by Sensodyne with over 70% share of the sensitivity category, provide a profitable third pillar.

These are mature categories, but Haleon is not standing still. On pain management, the company rolled out Panadol Ultra nationally in March–April 2025 after a soft launch in Karachi, positioning it as a premium, fast-acting formulation aligned with global Panadol variants. Management is also preparing to enter the menstrual-pain and migraine-relief sub-segments with new Panadol line extensions – a move that both deepens its reach in pain and ties the brand more closely to women’s health.

The other major growth vector is nutraceuticals. Haleon has launched Centrum – the world’s largest multivitamin brand – in Pakistan in Adult and Silver variants, initially as imports from Italy. A Reuters interview with the company’s chief executive last year revealed just how ambitious these plans are: Haleon already commands roughly Rs7.5 billion of Pakistan’s Rs24 billion vitamins and minerals market through CaC 1000 and Qalsium-D, and aims to capture a further 7–8% of the remaining market once Centrum is fully rolled out.

Local manufacturing is central to those ambitions. At present, Centrum tablets are imported because Pakistan’s regulator, the Drug Regulatory Authority of Pakistan (DRAP), insists that nutraceuticals must be produced in separate facilities from pharmaceutical drugs, making it uneconomic to manufacture Centrum locally. Haleon is lobbying DRAP to allow nutraceutical production in pharmaceutical plants – arguing that the higher standards of drug facilities should more than satisfy any safety concerns – and has signalled that it would in-house all Centrum production if rules change.

Even without policy relief on nutraceuticals, Haleon is already investing heavily in manufacturing. About 36% of its product portfolio is currently outsourced, but CaC 1000 is fully made in-house, and the company has spent roughly US$10 million upgrading its Jamshoro factory so that Panadol can be shifted from toll manufacturing to local production. Some Panadol SKUs are expected to move inhouse in the third quarter and the remainder in the fourth, reducing the outsourced share of the portfolio to around 4 percent.

That change should not only protect margins by cutting conversion costs; it also gives Haleon more control over quality and supply – crucial in a country that has repeatedly grappled with paracetamol shortages whenever price disputes between manufacturers and the state flare up.

Exports are the final piece of the growth puzzle. Haleon already exports CaC 1000 and Voltral Emulgel (a topical pain-relief gel) to Vietnam and the Philippines, and is in the process of opening channels to 18–19 countries across South-East Asia and Africa. Management wants exports eventually to account for at least 10% of sales, up from the 5–6% peak reached in 2022, although it acknowledges that the approvals process for each new market can take two to five years.

In short, Haleon’s product and capacity strategy is clear: defend and extend Panadol, deepen CaC 1000’s grip on the vitamins segment, add nutraceuticals like Centrum, and leverage an upgraded Jamshoro plant to push both domestic and export growth.

Haleon Pakistan’s story cannot be separated from the global reshaping of GlaxoSmithKline’s consumer healthcare business over the past decade.

Globally, Haleon was created in stages. First came the 2019 merger of GSK’s and Pfizer’s consumer healthcare units into a single joint venture, with GSK holding 68% and Pfizer 32 percent. Then, in July 2022, GSK demerged that business, listing Haleon plc as an independent company on the London Stock Exchange and New York Stock Exchange.

Since then, both legacy parents have pro-

gressively exited. GSK sold its remaining stake in Haleon in 2024, while Pfizer announced and then completed the sale of its final 7.3% holding in early 2025, with a portion bought back by Haleon itself and the rest placed with institutional investors.

In Pakistan, the restructuring has been equally involved. GlaxoSmithKline Consumer Healthcare Pakistan Limited (GSKCH) was incorporated in 2015 after being demerged from GlaxoSmithKline Pakistan Limited, and listed on the Pakistan Stock Exchange in 2017. Following the global demerger, the local company’s ultimate parent changed from GSK plc to Haleon plc, and on 3 January 2023 the Securities and Exchange Commission of Pakistan formally approved a name change to Haleon Pakistan Limited.