There’s big money in global tech exhibitions. There’s also big corruption

Pakistan’s Future Food Security Tied to Strategic Palm Oil Partnerships

Classified: Govt looking for Digital Czars to rule your life

Pace Pakistan board approves major restructuring

Ghazi’s

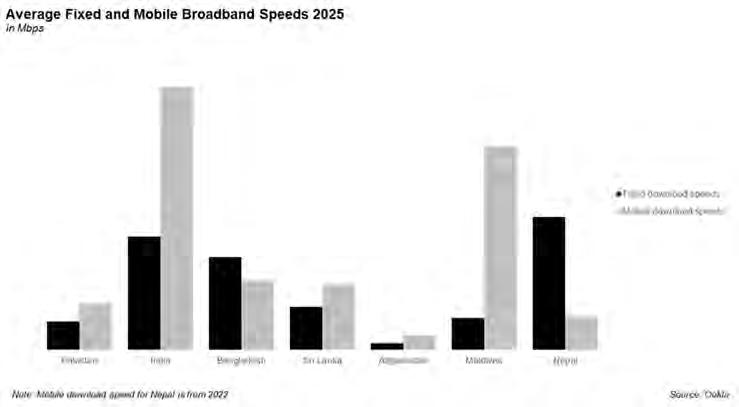

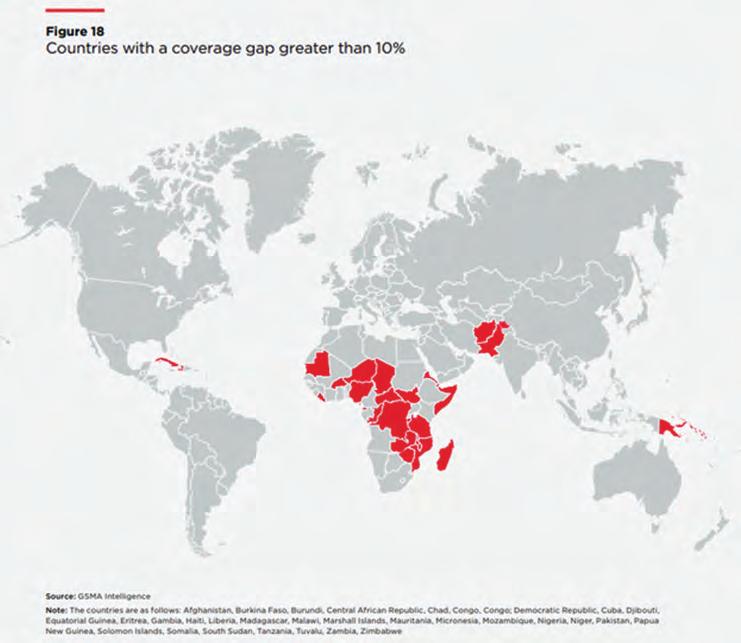

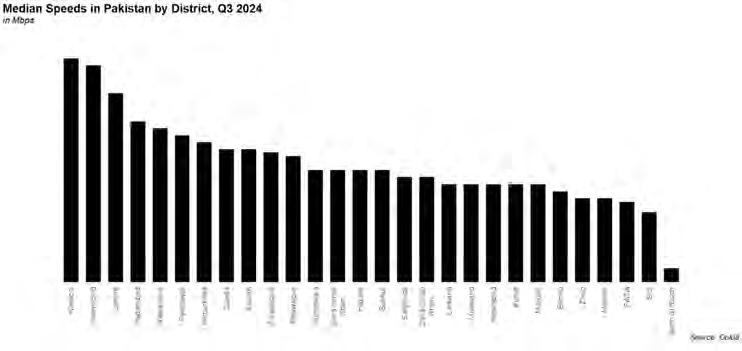

Eye on the sky: The race to connect Pakistan’s forgotten corners

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq

Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

How the courts hold back financial justice

A conviction handed down by the Sindh High Court in favour of the SECP can be considered a win as it will improve the perception of fairness in the capital markets. But the problem runs much deeper

By Zain Naeem

As Justice Ahmed Keerio announced the verdict inside a humid courtroom of the Sindh High Court last week, it marked an occasion that comes far too rarely: The Securities and Exchange Commission of Pakistan (SECP) had just won a case.

Victories enjoyed by the Securities and Exchange Commission of Pakistan (SECP) are few and far between when it comes to the capital markets. When they do end up getting a win in their column, it is a cause of celebration, even if the decision comes decades after the SECP first gives an order.

In Pakistan, the efficacy of the SECP is a major issue. The job of the SECP, for any reader that is unfamiliar, is to make sure that fairness and transparency is achieved in the capital markets like the stock exchange. You see capital markets work with certain sets of rules. Insider trading, bad faith deals, information exchange, and withholding material information are all white collar crimes that can unfairly disadvantage some investors. The idea is that the SECP keeps a check on such activities.

Unfortunately, even though the role is well defined, the track record of the regulator has been patchy to say the least when it comes to getting convictions in the courts of the country. The way it works is that when something suspicious comes up, the SECP carries out the relevant investigations and then pursues these cases to the full extent. They contact the people involved and try to get to the bottom of the matter. If they find wrongdoing they can issue orders against individuals or organisations involved.

While the procedures followed by the SECP have their own issue, a major obstacle in implementing these orders comes from the courts. If the SECP rules against someone, they can take the SECP to court for the decision. In most countries there are arbitration laws and procedures that make this process fast. In Pakistan, stay orders and judicial lag can drag them out for decades in some cases. On top of that, a lack of judges experienced in financial crimes can further delay an already painful process. But what went on in the recent case that the SECP has won? To understand the full story, we need to go back.

It takes ages

In 1997, a young man entered the bank branches of Habib Metropolitan Bank Limited (HMB). It is November in Karachi and the man has just been hired as a junior officer at the bank. As time went

by, he was able to climb the organizational hierarchy ending up as the Assistant Vice President (AVP) handling the investments of the bank in 2014.

The job description of the new AVP was to be able to carry out the decision making on the equity investments that were being carried out by the bank.

For anyone that is unaware, a bank, like any other business, is set up to earn a profit. Where a cloth manufacturer might use cotton or raw materials to manufacture cloth and earn a profit, a bank has money as its raw material. Depositors give funds to the bank and earn interest on these deposits. The bank then has to use these funds in order to earn a return from these funds. The better the banker, the better the investments that he will make.

After investing these funds in different classes of assets, the bank will earn income or revenues on the investments that it has made. After paying back the return to the depositors, the amount left can be considered the profit being earned by the bank. This means that the higher the return the assets generate, the higher the profit. This leads to the bank investing in safe classes of assets like Government bonds which will yield a consistent return while bundling them with investments in the stock market which can lead to a higher but risky return. This is the equity function of the bank which looks to invest in the best stocks which can yield a higher return for the bank. Zakir Hussain Somji was one of the individuals who was able to make the decision regarding which stocks or companies the bank could invest in. The power this position holds is huge as he has a large amount of funds owned by the bank which can be used to invest in.

That is why the SECP also exists. A bank has enough money that any investment or divestment they make in capital markets can spike or tank a stock. That means any person with prior information of what a bank is going to do has for all intents and purposes a crystal ball that can see the future. Theoretically they could buy stocks in a company right before their bank invests in it and make a killing from the raise in stock price that takes place after their investment. That is why the SECP keeps a check on the personal investments of individuals with access to this crystal ball. The case involving Somji has to do with something similar.

The offense

According to Criminal Complaint No. 29 of 2018, the SECP charged Somji with using his position and influence to make personal gains

which disadvantaged the bank. The Complaint, filed in the Special Court (Offences in Banks) Sindh, stated that there was a breach of Section 128 of Securities Act 2015 which had been breached and had to be punished under section 159 of the Securities Act 2015.

Section 128 states that no person can indulge in insider trading and any contravention of its rule shall be considered an offence. The definition of insider trading covers a vast region as many different types of trading can be seen as being insider trading. Fundamentally, insider trading is supposed to encompass trading where an individual has information available with him that is not available to the whole market. Based on using this information, he can make an investment decision which will benefit him while the remaining market remains oblivious.

In order to prohibit insider trading, SECP defines it as any transaction that is conducted on information that is only available to a select group of people. This leads to asymmetric information being available in the market. The asymmetric nature means that the information is limited in terms of its availability and gives an unfair advantage that can be traded on and profit can be earned.

Inside information is defined as any information that can have an impact on the price of the share that has not been made public. This is the asymmetric nature of such information. As certain portions of the investing public have the information, the SECP is allowed to investigate such activities which create an unfair advantage.

The SECP raised the charges against the accused and asked for punishment under section 159 of the Securities Act 2015 which would have meant a jail term of maximum 3 years and a fine of three times the gains earned by the individual.

Investigation carried out

The case that was filed by the SECP revolved around the fact that the individual had carried out inside trading and used fraudulent practices which ended up making gains for him while it led to a loss to the bank. The investigation that was carried out used the KATS (Karachi Automated Trading System) data which records all the trading carried out in the stock exchange. From January 2014 to February 2016, the investigation team gathered the data that was related to the trading carried out.

The investigation was initiated after it was seen that trading activities being carried out were suspicious and there was a need to scrutinize the trade data in relation to that. Before trading was automated, brokers would

gather in a trading pit and shout buy or sell orders at each other. The system was crude and basic, however, it allowed the traders to recognize who was trading with each other. With the inculcation of automated trading, this aspect went away as buyers and sellers had no knowledge who the counter party was. This led to trading being carried out on anonymous terms as the interface changed from faces to computer monitors.

With the advent of technology, it became virtually impossible to carry out trades between buyers and sellers on a consistent basis.

This basic understanding was the reason that the activities of Somji were recognised as a breach. In a period of two years, the SECP saw that the bank and Somji’s personal account matched trades around 173 times. The chances of this happening are astronomically impossible.

The probability of the same accounts trading with each other was very low which showed that there was some influence of management being carried out to make this possible. This was already a breach of the code set out by the SECP. In addition to that, Habib Metro had also restricted its employees from carrying out trading in their personal accounts which was also being violated.

In terms of shares being traded, the investigation found out that out of 11,795,100 shares of different companies bought by Somji, around 1,230,900 were bought from Habib Metro which was more than 10% of purchases. On the other hand, Somji sold 11,836,600 shares of different companies from which 4,915,200 were sold to Habib Metro. This accounts for 41.52% of the shares sold.

Inside trading was being carried out by front running the bank. Bought from market and sold to HMB or bought from HMB and then sold in the market. The profit earned was around Rs 28 lakhs.

Front running and impact on the market

Even though the charges levelled by the SECP seem to be concerning inside trading, the sophistication level of the offence was much lower than the one that insider trading entails. When insider trading is mentioned, the picture that comes to mind is surreptitious information being exchanged in hush whispers that leads to trading being carried out.

The inside trading that was being carried out was based on the sole element that Somji had a large amount of funds that he could use to invest. With such a large amount of finances, Somji could buy the shares of a company and lead to an increase in the share price by carrying out a buying in the specific

share. Similarly, once he decided to sell his position, the fall in price could be substantial based on the value of trade that was to be carried out.

Having this power, the SECP claimed Somji started to use front running in order to make personal gains for himself. Before he would carry out a large purchase, he had the information that the buying was to be carried out. Using this information, he would buy the shares in his personal account beforehand. Once the share price would increase, he would either sell the shares to the bank or back into the market at a higher price.

Similarly, when he was about to sell the shares of the bank in the market, he would sell the shares in his personal account before the bank was going to do so. He would sell them at a higher price before the bank would and end up selling at a higher price. This all might seem like a victimless crime, however, he was actually breaching a fiduciary duty that he had. Rather than thinking of the bank first, he was looking to make a personal gain. Somji should have executed the trades for the bank first rather than trading for himself. As an officer of the bank, he was not only trading in violation of the policies but also earning personal gain.

The defense presents its own case

In response to the allegations made, the defense had certain arguments on their own part. First of all, they claimed that there was no money trail in relation to the Rs 28 lakhs that was being claimed by the prosecution. The prosecution had failed to substantiate the gain that was earned. The defense also contended that the account that was being used for trading was a joint account between Somji and Shayan Ahmed. While investigation was carried out against Somji, no such action was taken against Shayan Ahmed.

In the same line, the bank account that was used for trading was a joint account with Farhan Ahmed who was also not investigated by the SECP.

The defense also contended that the trading activities that were being carried out by the bank were being approved by Farhan Aslam who was the superior of Somji at the bank while the head of department, Intikhab Hussain, also gave the approvals while the SECP did not make any of these individuals part of the investigation. In response to the investigation, the accused was made the Area Compliance Officer and the bank did not fire him after the alleged offence came to light.

The court has its own word

After the case came in front of the court, it had to consider both sides of the arguments being made by the SECP and the accused. The court boiled down the whole case to four points. First of all, it tried to prove if Somji had the power to place the orders and did he earn gains from these trades? Secondly, it tried to see if any offence had been committed and lastly what the final decision of the case should be.

The court gave a detailed analysis in regards to the points that were in front of it.

The court admitted on record that the accused admitted he had the power to place the orders and also admitted that matching of orders on such a consistent basis was highly unlikely. Use of KATS meant that trading was supposed to be anonymous which was not being seen in this case. One of the witnesses of the case was the Chief Compliance Officer of Habib Metro who provided the trade data, disclosed the bank’s investments processes, the team responsible for the equity decision making and the process of decision making in the investments.

One of the persons named was the accused. When the witness was deposed, he stated that the accused confessed his guilt to the superiors, however, the confession could not be admitted into court as it was considered as being extra judicial in its nature.

When this witness was cross examined by the defense, he contended that the accused had been made the Area Compliance Officer by the bank, however, this was after the bank had carried out its own investigation and had terminated him in June of 2017. The investigation put the blame squarely on Somji which led to his termination in the equity department.

In regards to the defense’s contention that only Somji was investigated, phone recordings had been obtained which showed that only the accused was placing the orders on behalf of the bank. In regards to the trading account being joint in nature, the witness stated that all the trading activity was linked to the CNIC of the accused which meant only he was responsible for the trading being carried out in his personal account.

The fact that the bank and its compliance was accepting all the trades being carried out by Somji was due to the fact that he was only showing them the trades that were being carried out on behalf of the bank and his personal trades were not being disclosed. These trades were not even allowed to be carried out in the first place.

The defense never questioned the trade

data that had been compiled which pointed towards the fact that it was correct and could not be contended.

The decision and punishment

After considering both sides of the argument, the court finally passed its judgement as it found Somji guilty of the breach that he had carried out. The court punished Somji under section 159 of the Securities Act 2015 which allowed him to be punished up to three years and fined for the offence. The court found Somji guilty of breaching Section 128 and handed down a fine of Rs 8,599,938 which was three times the gain that he had earned.

In terms of passing a jail sentence, the court felt that the case had been ongoing since 2017 and that the accused had suffered mental anguish due to the case. In light of this, he was given no jail time and only a monetary fine. Still, under section 162 of the Securities Act 2015, the court stated that it could recover the fine within seven days. If the fine had not been paid, the convicted could be remanded in jail till the amount had been paid.

As the court is dismissed and the convicted contemplates his fate and future, the decision can be considered a landmark decision for the capital markets of the country. The country has been marred by countless stock market meltdowns in the past which have seen the guilty not being punished and made an example out of. When Somji was carrying out these offences, there might have been hubris at play which allowed him to act in the way he did. The damage is that participants keep breaching the rules and are never punished while the public trust starts to decay. This can be considered a small notch of victory for the regulator as they have been able to get a conviction on its record. Hopefully this will be the first of many such cases going forward

On the heels of the judgment the Chairman of SECP, Mr Akif Saeed, stated that the judgment will boost investor confidence in Pakistan’s capital markets and, in turn, facilitate capital formation. He also expressed hope that the ruling will set a precedent for pending cases and ongoing inquiries into insider trading and market manipulation.

Everyone loses

Alot of this story has been details of the court case in question. Over here, we need to make a very important clarification: the case in question could be appealed further by the accused if he wants to prove his innocence. Of course, as the court noted, going through a seven year trial is a

ridiculous and painful process. In Pakistan, the judicial system is so sluggish and mind boggling that going through the process is punishment enough, as the court has noted.

The figure given of Rs 28 lakhs is also not a very large one, and it took seven years to get to this decision. The courts are a pain both for the SECP and those accused. And this is a case that has been decided relatively quickly. Back in November 2024, the Islamabad High Court upheld an order of the SECP 24 years after it was first issued.

This was a case that originated in 2000. In the 90s and the early 2000s, the capital markets of Pakistan were like the Wild West. There was little that existed in terms of rules and regulations and there was a blase attitude towards having a formalized manner of trading. Brokers were not mandated to ask the source of financing for the client, trading could be carried out without any sort of uniform account opening and custody of shares was mostly kept by the brokers rather than giving them over to the clients.

In order to place an order with the broker, the client would contact their agent and place a trade with them. These agents are people who have been hired by the brokerage house and act as a liaison between the company and the client. The client would contact the agent and ask them to place a trade. Any trust the client had in the brokerage house was based on his relationship with the agent and the agent would be the only point of contact. As the controls were not stringent, the agent could buy the shares for the client and place them in their own account rather than being mandated to deposit them in the client’s account. This is where the story of this case starts.

Much of this has changed since.

Accounts are only opened after a thorough Know Your Client (KYC) procedure has been carried out. Brokers need to record the orders being placed with them by the client and the shares of the clients are deposited with the Central Depository Company (CDC) once they are bought or sold. Any movement in these shares is communicated to the clients on that day and, in case they feel something untoward has happened, they can report this discrepancy to the relevant authorities.

While the SECP has caught up in some ways, our court system remains as paralysed as it was decades ago. An overflow of cases, a lack of technically trained judges and lawyers, and corrupt practices mean that neither the SECP, nor any defendant or complainant acting against them can look forward to anything but an arduous process. Without judicial reform, cases like this will continue to languish, and justice will be delivered late if it ever is. And we’re pretty sure there is a very famous saying about what it means when justice is delayed. n

The returnsdeclining to emigration

For decades, Pakistanis have defined success as getting out. But the cost have been going up, and the returns have been declining. At what point does it stop making sense?

By Farooq Tirmizi

We will give you the punchline quickly for those of you who will click on the headline but will not be able to read beyond the paywall since you do not want to pay: if you – like most Pakistanis – still believe that professional success means first and foremost being able to get out of the country, here is what you should know about the outside world.

• America is a tremendously rich country and will make you rich if you can somehow make it there, but is closed to the outside world for the foreseeable future.

• Canada and Australia are less lucrative, but easier to get to and still worth considering.

• The Middle Eastern countries are even easier to get to, will yield more financial wealth for you in the long run, are closer to home, but are not a permanent escape, since they will never give you citizenship (fine if you want to move back home).

• Migration to Europe, dear reader, is an objectively stupid decision in the long run, even if it seems easier to accomplish in the me-

dium term. All those people going to masters programs in Germany, Ireland, Italy, and the UK? Making bad, uninformed choices.

Now that we have gotten the most provocative statements out of the way, let us explain what this article is about: it is a story of how Pakistanis have defined success, why it was defined that way, and why that definition needs to be revisited in light of recent trends in the relative economic and demographic health of countries around the world.

Emigration as economic success

The region that now constitutes Pakistan has been poorer than Europe for much of the past 200 years, but since about the 1860s onwards, has also had a small elite that was connected to Europe, and then later North America in a manner sufficiently close enough that they knew exactly how far behind Pakistan is compared to the most advanced countries in the world.

That resulted in a culture of elite longing for a life at the cutting edge of human economic progress, which meant a desire to move outside the country. In other words, there has never been a time in Pakistani economic history when there was not a substantial portion of its elite that wished it lived in London (and later, New York and Dubai).

The culture of an elite has a way of percolating down to lower strata of society, and this particular desire is no different. When a young high school student in Pakistan imagines a bright future for themselves, they imagine themselves outside the country, not inside it.

Migration, in short, is the very definition of having “made it”.

For a long time, this has made economic sense. Opportunity within the country was limited, the wage differential between what was available inside Pakistan and outside Pakistan was large, and for some countries over some decades, was actually growing: meaning Pakistan was actually getting poorer relative

to some European countries for the first few decades of its history.If you could get to North America, Europe, or the Middle East, there was absolutely no question that you would be economically better off than had you stayed inside Pakistan. Any family that could send a son or daughter abroad did so.

Here is an example of how absolute the superiority of migration is in the Pakistani mind. If a person is thinking about switching jobs and interviewing at different places, they will actively seek to hide it from their employer, and most of their colleagues. If, however, that same person is applying for immigration to another country, they will feel completely free to discuss it with anyone at the company they work at, even though, from a company’s perspective, both events involve an employee leaving the company.

And the viability of migration for Pakistanis has become available to a larger and larger swathe of the Pakistani population over the past several decades. Given the fact that immigration can take many different pathways, it can be hard to quantify just how much easier it has gotten. But one way would be through the use of some anecdotes from my family history.

In 1983, my parents went to London for their honeymoon. The ticket cost them about $1,000 at the time – unadjusted for inflation. In that year, that amount was equal to twice the per capita GDP of Pakistan. Indeed, so small a percentage of the Pakistani population could afford to even reach the UK that my parents were able to go there without a visa.

(For a long time, visas were not considered necessary because the thing that kept large, uncontrolled waves of migrants at bay from developed countries was simply the cost of getting there. The UK imposed its visa requirement on visitors from Pakistan in 1986. Prior to that, all you needed to travel to the UK was your Pakistani passport.)

By 1990, when my family was moving to the United States for one year, the ticket we bought cost around $1,500 – again, unadjusted for inflation. That amount was about 2.5 times

Pakistan’s per capita GDP, though the destination was different and farther away.

By the time I went to the US for college in 2004, the amount of money it took was roughly the same – about $1,400 for a roundtrip ticket to the United States east coast – but the ratio was different: about 1.67 times per capita GDP. By the time I left for the US again for graduate school in 2013, the ticket price was just $1,100 (not adjusted for inflation), and it was 0.8 times the per capita GDP of Pakistan that year.

The above example, while not very scientific, does lay out a simple fact: a larger and larger percentage of the Pakistani population can conceive of traveling outside the country, which is why a larger and larger share of Pakistanis participate in the conversation about wanting to move outside the country, which in turn reinforces the belief that it must be a good idea to move outside the country.

When a belief is that widespread, and that absolute, it is generally a good idea to periodically test it: do the underlying facts still support this belief?

As we stated at the outset of this article, the answer depends on which part of the world you are talking about. We have bucketed the categories of countries to which Pakistanis generally migrate into four, based on shared characteristics of how desirable it still is to migrate to those countries.

Methodology

How do we determine what makes a country more attractive to migrate to? We examine what you might call the “size of the prize”: what is its per capita income, adjusted for purchasing power parity (PPP), relative to Pakistan? We look at this data for countries across several decades.

Why several decades and not just the most current data? Because immigration is generally a multi-decade commitment, or at least starts out that way. To know the size of the prize, you should not just look at the differentials between incomes in Pakistan and your

target country, but also how that differential has changed over time so that you can at least see what the trendline is, which in turn will give you an estimate of where you can expect the differential to be by the time your children enter the workforce.

(The assumption here is that your children are likely to enter the workforce in the same country that you have migrated to, because presumably a big part of why you want to move is to give your children opportunities from the very beginning that you did not have.)

For the per capita income, adjusted for purchasing power parity, we relied on data from the World Bank, and then calculated the ratio of each country’s per capita income in PPP terms relative to Pakistan’s per capita income in PPP terms.

All of the countries we examined are richer than Pakistan, but the magnitude by which they are richer has been declining in almost all of them (meaning Pakistan’s economy and incomes are growing faster than theirs). The speed with which the ratio is declining determines the relative attractiveness of a given economy.

America: no longer open

It is difficult to describe how unfathomably rich America is relative to the rest of the world these days, and how much easier it is to get rich in America if one has talent, ambition, and focus. The broad numbers are easy to see: the United States is about 4% of the world’s population, but holds 35% of the world’s wealth, according to the 2025 Global Wealth Report by UBS, the Swiss investment bank and wealth management firm.

America’s advantage is even more concentrated when one looks at the concentration of millionaires worldwide. According to UBS’ calculations, about 60 million people around the world have a net worth exceeding $1 million, and 24 million of them live in the United States.

The American labour market is also

the most flexible in the world, which makes employers much more willing to hire, and so getting a job in America tends to be much easier than just about any country you might be able to move to. Starting a business, raising capital for that business, all are much easier in America than other parts of the world.

Small wonder then that the average net worth of an American is about twice as high as that of the average European, and incomes are significantly higher as well. Average incomes in nearly all European countries are lower than in the poorest US state, which is Mississippi.

The prize in America, in other words, is worth having.

It is not, however, available anymore to people from outside the United States, and certainly not to most people in Pakistan, even our most globally competitive talent who, in a previous generation, would have had a much smoother path to moving to the United States than they do now.

I recognize that I am perhaps not a good messenger for this information. I only recently become a US citizen, having moved to the US to start my MBA in 2013. It may sound like me telling others not to pursue what I recently acquired myself.

But I think about every single step that I took to get to this point, and frequently talk to people who are a few steps behind me in the process, and every year, every single step gets progressively harder and harder. The scholarships for foreign students – like the one I got for my MBA – are getting more and more difficult to get. The student visa I came on is harder to come by. The work visa I started my first job on is now subject to a lottery. The green card process is longer, and involves more scrutiny than before. And that was all before Donald Trump was re-elected US president and made it all harder still.

At some level, Pakistanis recognize this because when smart, ambitious young Pakistanis get together and talk about the thing that all of them talk about – how to migrate out of Pakistan – America is talked about by very few of them, and every year there

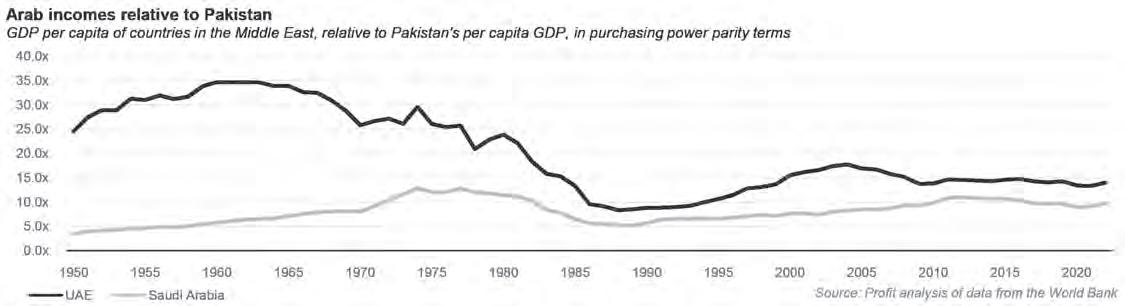

are even fewer who even consider it an option. This is despite the fact that, even adjusting for purchasing power, average incomes in America are 10.6 times higher than in Pakistan, and while Pakistan has been catching up, it has been much slower than with most other rich countries.

Canada and Australia: still (mostly) open

The next most attractive economies are Canada and Australia, at least in terms of income. GDP per capita in Australia is 9.4 times higher than Pakistan on a purchasing power parity basis, and 8.2 times higher in Canada. Both countries have clear immigration pathways that make it a relatively straightforward process to become citizens of those countries, and sometimes it is possible to apply for permanent residency directly rather than the norm in America, which involves trying to move there through other means first.

The advantage that both of these countries have over Pakistan in terms of economic opportunity has declined over the past few decades. The average Canadian made 15 times more money than the average Pakistani in 1979, adjusted for purchasing power, and the average Australian made 13.5 times more than the average Pakistani around the same time.

Clearly Pakistan has converged somewhat with these countries, but the differential is still relatively wide, and narrowing slowly enough than one can conceive of these countries as still being much richer than Pakistan even 25 years from now.

If immigration channels remain open, and per capita income differences will remain wide enough over the next two to three decades, it makes sense to pursue migration to these countries if one qualifies for the criteria they lay out in their official policies for migration.

One thing to consider: property prices in these countries have skyrocketed over the past two decades and made it much harder to

buy a home.

The Middle East: the favourite option gets even better

By far, the largest Pakistani population outside Pakistan lives in the Middle East, with Saudi Arabia hosting the largest expatriate Pakistani population, followed by the United Arab Emirates. These countries are geographically close, so much cheaper and faster to get to, have currencies pegged to the US dollar, as well as very high per capita incomes.

Indeed, per capita GDP in the UAE is actually higher than that of the United States, and hence it is 14 times higher than Pakistan on a purchasing power parity basis. And while Saudi Arabia is not quite that high, at 9.7 times Pakistan’s per capita GDP, Saudi Arabia does offer considerable income arbitrage to anyone who has the ability to move there.

Both of these countries appear more attractive than Canada and Australia from a purely income differential perspective, but they, of course, famously come with some drawbacks. The most well-known of these is the policy of almost never granting citizenship to anyone who is not from there, so we have stories of families who have lived in Saudi Arabia and the UAE for decades but still do not have the right to call it home. But even beyond that, the GDP per capita number is perhaps a little less precise a measure of the relative differences in income than other countries. Part of this is the fact that a substantial portion of the GDP of both of these countries is oil revenue that goes directly to their governments, and hence inflates the actual income differences between these countries and Pakistan, especially on a PPP basis.

But the other, perhaps more concerning, difference is the fact that salary levels at many organizations in these countries depend on the citizenship of the person doing the job: people from richer countries tend to get offered higher salaries while citizens of countries like Pakistan tend to be offered lower salaries, even for com-

parable jobs. So while overall incomes may be higher, those higher incomes are not necessarily made available to Pakistanis.

There is also the volatility that comes with oil prices. When oil prices are high, incomes in these countries tend to get significantly higher, and when they are low, economic activity can slow down rapidly. And given the lack of citizenship options, those commodity price driven economic downturns can mean a sudden, unplanned relocation back home, as happened to many people following the 2008 crisis.

But since most people know that these countries are not – nor will they ever be – permanent homes, most people tend to go there psychologically prepared to move back to Pakistan. So even though the long-term trajectory of income differentials between these countries and Pakistan favours growth in Pakistan, it may still be worth it to explore moving to these countries, since any stint there is likely to be shorter, and hence requires less long-term planning.

Europe: Let it die

We now turn to the continent with which we started the discussion of income differentials: Europe. And on this front, sadly, the picture is now so unfavourable that it makes no sense to even consider moving there, especially when one factors in the fact that even wealth individuals from the continent are moving out.

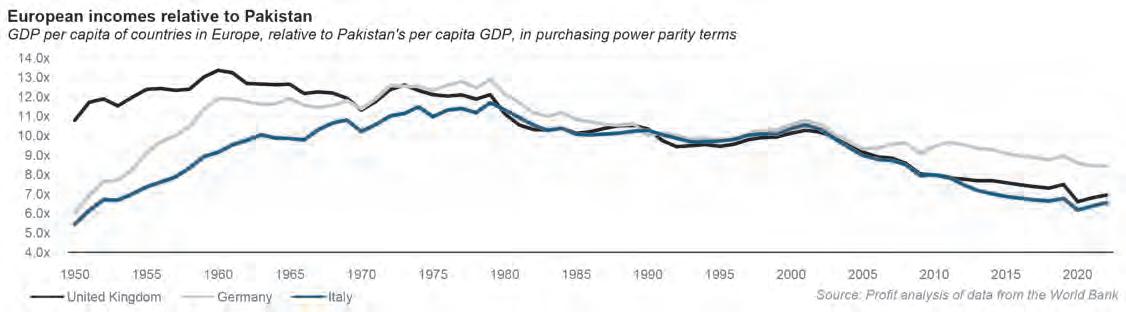

The raw numbers themselves are rather telling: a Pakistani moving to the UK can expect an average purchasing power parity-adjusted income boost of just 6.9 times their Pakistani income. For Germany, the number is a bit better at 8.4 times, but for Italy, it is worse, at 6.5 times Pakistan’s per capita GDP on a purchasing power parity basis.

It gets worse if you look at the trajectory Europe has been on. Between 1950 and roughly 1980, Europe actually grew faster than Pakistan, largely on the back of the American-financed reconstruction of the continent following the end of World War II. Pakistan

started very slowly catching up between 1980 and 2000 as European growth slowed and Pakistani growth speeded up.

By starting around the year 2000, the direction has been one-way and negative: Pakistan’s per capita incomes have consistently outgrown those in the three major European economies mentioned above, and a trend that is unlikely to abate for the simple reason that these countries are, quite literally, dying.

Childlessness occurs at high rates in most European societies, which means these countries are getting older and with each passing year, fewer and fewer children are born, which in turn means the countries keep on getting even older.

Not having the right balance of young and old people means these countries are effectively waiting for the deaths of the bulk of their population. That does not mean these countries will not have rich economies for the foreseeable future, but it does mean that countries like Pakistan will consistently outgrow them. These countries have gone from being almost as rich as the United States to being not just poorer, but on track to hit parity with countries like Pakistan for the wrong reasons: because they declined too rapidly.

Conclusion

Migration remains an enormously personal decision, and this newspaper recognizes that it has negative effects for Pakistan, particularly with respect to the brain drain, so we will never encourage it. But we do recognise that it is a topic of conversation du jure among many people, so we think proving sufficient information to help empower better decision making is a role we can help play.

If you are going to disrupt your like by moving countries, and take on that multidecade commitment, your horizon for data should also be multi-decade.

Do whatever you deem best for your and your family’s needs. But for the love of all that is holy, do not move to Europe.

There’s big money in tech-exhibitions.

There’s also big conflict

Pakistan’s independent tech exhibitors are being squeezed out by a state-backed monopoly. What are they doing to

By Taimoor Hassan

If you have worked in the IT industry, chances are you have either been to or seen colleagues jet off to exhibitions in foreign countries. Exhibitions are a part and parcel of any industry. These events, usually hosted at large hotels or dedicated expo centres in both large and small cities all over the world, are essentially meant to connect buyers and sellers.

Manufacturers and sellers get a chance to display their products, show off advances, advertise themselves, and make connections that might serve them in the future. There are far more of these exhibitions and conferences than one might expect. Exhibitions in and of themselves are big business. Organising them, planning them, running logistics and marketing for them is an economy of its own. In the United States alone there are more than a million meetings and events each year, which includes conferences, conventions, and tradeshows. Add hotel stays, marketing, travel, and all kinds of other costs and it comes out to a $330 billion industry. Pakistan is by no means a global hub for exhibitions, but there are plenty of Pakistani businesses that need international exposure, and attending these conferences and getting access to them involves big money too. Perhaps nothing exemplifies this better than Pakistan’s tech industry. Every year, Pakistani tech companies attend countless conferences and exhibitions all across the world. To get to these exhibitions, you have to apply, buy space, set up a pavilion and have a strategy.

But for tech companies, getting to these exhibitions is simply a matter of paying a fee. Because all of the logistical work involved is done by third parties — companies that specialise in organising exhibitions for participants. In the last three years, a number of companies in the exhibition industry have popped up in Pakistan. These companies have been quietly reshaping how Pakistan shows up on the global tech map with grit, design sense, and a business model that makes international visibility possible for companies that would otherwise never afford it.

The gig is far from easy. While these companies have grown in the past three years, they have been up against government machinery. It is an uphill battle against a system that favors monopoly over merit, and connections over competence. And it begins with an organisation called the Pakistan Software Export Board (PSEB).

Say hello to the gatekeeper - the PSEB

Every year when the government presents the budget, one of the most ridiculous parts in a document that is generally taxing on the mental faculties

of anyone with half a brain or more is the IT budget. It allocates money to ridiculous things such as IT parks, and other strange schemes the government thinks are what promotes tech. Part of the allocations are subsidies that the government gives to promote Pakistani tech abroad. How is Pakistani tech promoted abroad? Through exhibitions of course, and the government is willing to spend money subsidising companies going to these exhibitions.

Now, this money from subsidies should ideally go to the companies organising them or to the companies directly. But the government needs an arm to do this. This is where a single publicly owned firm called the Pakistan Software Export Board (PSEB) comes in. The board is the de facto gatekeeper for all “official” international participation by Pakistani IT companies. The way it works is that the Trade Development Authority of Pakistan (TDAP) works with the PSEB whereby the TDAP gives the PSEB money from the government to spend on the promotion of Pakistan’s IT industry. The PSEB does that under the Tech Destination Pakistan banner.

TDAP in coordination with P@SHA, the official representative body of Pakistan’s IT industry, chooses the international events where they think representation of Pakistan’s IT industry makes sense. The recommendations are sent to the PSEB which then finalizes the events where Pakistan’s IT industry is going to be represented by securing exclusive spaces called pavilions where IT companies from Pakistan are called to join and show to the participants the benefits of working with Pakistan’s IT industry. The said pavilions are required to be set up by companies from the private sector. These companies can offer their services and get government approval to be the “official” partner that is responsible for setting up the pavilion where Pakistan’s IT companies showcase themselves at these events. The list of these exhibitions in a year can vary and past years have seen more than 20 such exhibitions such as Gitex in Dubai and Berlin, London Tech Week and LEAP in Saudi Arabia where the government decided that it will showcase Pakistan’s IT industry.

For each event, the Pakistan Software Export Board has to choose one company from the private sector and give them the permission to set up the Pakistan pavilion. There can be as many companies that the PSEB can choose as there are events in a calendar year. Once chosen, the company would then tap into their network of IT companies and reach out to them, inviting them to join the event happening in Dubai or London or some other global destination where they are exhibiting the Pakistan pavilion. The companies first get the cost of joining the event happening in say Dubai from the organizers of the event and would then reach out to IT companies in Pakistan, quote them a cost of joining

these events including a reasonable margin for themselves.

These pavilions include booths that the company sets up for one IT company. The pavilion would include as many booths as the IT companies that agree and accept the company’s price to join the event.

If a company is unable to get the government’s approval to become its official company, also called agent, the company can bid to secure a space at the event for representation from Pakistan’s IT industry on its own. In this case, the company reaches out to the event organizer, say organizers of LEAP in Saudi Arabia, and tries to secure a space where IT companies from Pakistan can exhibit. But the company in this case is not the official nominee of the government. The official nominee of the government would bid separately from the non-government approved companies and try to secure the space for themselves with an added unique proposition that they carry the support of the government with them. With the support of the government, the equation changes. The event organizers are likely to look more favourably towards the government’s official agent instead of someone from the private sector. Both pay the same price to the event organizer but one comes with more weight whose booths would be attended by ambassadors and ministers. When the government is involved, it becomes about national liaison and not just a for-profit enterprise. Access and optics would be better for the one that has the government support.

There are monetary benefits too. According to the MoU between TDAP and the PSEB, the PSEB receives cash fromTDAP to subsidise costs for the official agent selected by the PSEB by up to 60%.

In a fair system, public funding, especially large subsidies for international marketing and export promotion, is distributed through open, competitive processes. The global standard for this is the RFP: Request for Proposals. Government agencies invite proposals from organizers, compare costs, evaluate performance, and select the best plan. It prevents corruption, creates transparency, and ensures public money is used well.

But in Pakistan’s case, no such process exists. The same agent is repeatedly handed most of the exhibition contracts, without any competition. No calls for proposals. No budget comparisons. No performance evaluations.

At the same time, there is also the perception issue. Tech companies are likely to trust the government backed organiser rather than the ones doing it without their approval. As an official of one organising company tells us, in their first year, the industry response was tepid at best. Very few companies were willing to risk joining an unrecognized platform, especially one without the safety net of government endorse-

ment. Exhibitions abroad especially in tech hubs like Dubai and Singapore are expensive and high-stakes. Why take the risk?

But over time, trust was built the hard way: through delivery. Each event was run like a startup launch. Hands-on, detail-driven, and focused on outcomes. Companies weren’t just given a booth and forgotten. They were helped with branding. Connected with investors. Introduced to buyers. Given practical, affordable options. Word spread.

Three years in, participation surged. Events like fintech festivals and startup showcases began drawing over 150 participants, a testament to the model’s success. More than a commercial enterprise, the platform became a gateway for Pakistan’s IT and tech ecosystem to be seen, engaged, and considered internationally.

Meet the agent

On paper, it looks like a success story: Pakistan’s IT industry is increasingly visible on the international stage, with local companies participating in global exhibitions from Singapore to Dubai, Istanbul to Amsterdam. On paper, it also looks that the government is promoting the IT industry at all these events when in reality it is a third party that the government gives a contract to.

Subsidies from the government cover up to 60% of the cost, allowing more businesses to represent the country abroad. It’s meant to be a support system, a way to elevate Pakistani technology into the global spotlight. But dig deeper, and a different story unfolds.

One where a single private agent, without any formal tender process or competitive bidding, controls the lion’s share of these international tech showcases. Where inflated budgets, opaque approvals, and unchecked authority turn public support into private profit. And where those actually building value independent organizers without government handouts are sidelined, blacklisted, or simply erased from the map. The agent is an individual by the name of Dawar Khan, whose companies Eventage, Event Management and Event Champ, have secured most of the exhibitions abroad to represent Pakistan’s IT industry.

This unchecked access to public funds allows the agent to inflate costs with impunity.

The government can bid to secure some space at a global exhibition, say Gitex Dubai, where they would set up booths for each tech company from Pakistan that agrees to join the event in Dubai. The government would give the contract to set up these booths to a private company like Eventage. Eventage would give a price to the PSEB for setting up one booth. Say that the company gives a price of Rs 20 lakh to the PSEB. The Rs 20 lakh covers the company’s cost of setting up the booth, branding, lighting, carpets etc with add ons like networking op-

portunities arranged by PSEB and government bodies like TDAP and the respective embassy of Pakistan. This price would also include profit of the private company which is organizing everything on behalf of the government of Pakistan. The PSEB would reduce this cost by 60%. In this case, it would come down to Rs 8 lakh. In this way, the difference of Rs 12 lakh is paid by the government and that is where the money set aside in the budget for these subsidies goes. This cost after subsidy is quoted to tech companies in Pakistan, encouraging them to join the said exhibition at an affordable cost. It is a simple enough system. However, industry insiders claim that the prices quoted to the PSEB by companies like Eventage are inflated. They claim that PSEB does not allow for competitive bidding which does not allow a fair field of competition. Estimates received by Profit claim that instead of the Rs 20 lakh, a single booth at an event like Giltex in Dubai could be organised by other companies at a cost as low as Rs 3 lakh to Rs 4 lakh per booth including their profit. The difference is massive. Add to this the fact that PSEB would pay for 60% of this and the cost for tech companies to have a booth at such an event comes down to Rs 1.2 - 1.6 lakhs. This actually means that the amount set aside for the subsidy can be distributed to a lot more companies which can then go to a lot more events.

As things stand, in the past three years, Dawar Khan’s companies have organised a majority of the events that the government has been involved in. The government can give work to any of the companies out there, but Dawar Khan has been the agent for 36 events out of 51 in the last three years. That’s 70% of the exhibitions where the PSEB decided it would showcase Pakistan’s IT industry and chose Dawar to do it subsidized by the government. Keep in mind that dozens of IT companies attend these exhibitions. If say 100 companies attend Gitex Dubai, under the Dawar Khan model, Rs 8 crore are being given to Dawar to set up 100 booths. According to market sources, this Rs 8 crore covers the cost and is enough to give him a decent profit. By quoting the price at Rs 20 lakh, the agent is pocketing an extra Rs 12 lakh. Multiply this to 100 companies attending the exhibition, we are looking at Rs12 crore in unearned profits through subsidies.

Correspondence seen by this reporter confirms that events such as LEAP and Gitex that could be organized for $150,000 are routinely quoted at $700,000 by the above-mentioned companies. With the government offering a 60% subsidy, that means the state pays nearly five times more than it should. The agent pockets the difference, often taking home more than $100,000 to $400,000 in commissions per exhibition based on the size of the event, their importance and how many companies from Pakistan attend it.

Multiply that by 36 events in total that Dawar’s companies have been chosen to be the government’s official agent, the numbers become staggering. We are talking about at least $3.6 million that Dawar has possibly earned in profits if all events are small. However, that is not the case. We have created a tier-based categorisation of these events where costs and eventually subsidy amount increases as the events move up in a tier. If all events are Tier C, Dawar has pocketed $3.6 million. If all events are assumed to be Tier A, Dawar pockets $14.4 million. Stay in the middle and Dawar would have pocketed $9 million. The $9 million (Rs2.5 billion in today’s dollar rate) number is the best unbiased estimate of the amount that Dawar possibly pocketed through his companies in three years because of an unfair system. This amount is close to the entire PSEB budget of Rs3 billion in 2024-2025.

This isn’t just unfair. It’s expensive. Let’s unpack the scale of this hidden cost and how much it’s draining from the system.

Pakistan supports international exhibition participation through subsidies that cover 60% of the event costs, designed to reduce the financial burden on already rich tech companies, earning millions of dollars annually. It can be a good idea when applied fairly. But what’s happening instead is a textbook example of budget inflation and corruption.

While independent organizers manage full-featured international showcases for $150,000 or less, the monopoly agent regularly quotes $700,000 or more for similar events. And since there’s no RFP process and no mechanism to invite competitive bids, these inflated invoices are either accepted without scrutiny or through collusion.

Real money but illusionary advertising?

It gets worse. Even with the inflated prices, there are serious questions about where all of this money is being spent.

In a startling discovery, this reporter has uncovered what appear to be fabricated promotional materials for Pakistan’s IT industry events in locations like Saudi Arabia, Toronto, and Berlin. Using error-level analysis, a forensic image technique, several of the billboards and digital ads masterminded by PSEB’s ad partner, M&C Saatchi show signs of manipulation. Searches on fakeimagedetector also show anomalies in these pictures and question their authenticity. Industry sources also say that the pictures aren’t real.

The PSEB budget is roughly Rs 3 billion which it can spend on subsidies, grants, and global marketing. According to sources in the advertising industry, the rule of the thumb is

that 30% of all spend is on marketing. On these estimates, roughly Rs 90 crore is being spent on global marketing. This amount is firstly being spent on exhibitions. Secondly, there are now questions on whether the marketing actually happened or not.

The pictures that have turned out to be fake as well as ones that appear to be real also reveal that the campaigns, costing tens of crores, appear to be weak. Sources familiar with and directly working for advertising companies in Pakistan say that the campaigns appear designed for local consumption - people who see billboards and paid social ads aimed at passersbys rather than the global tech community. “It looks more like the campaign is aiming at an audience to sell them a consumer good product like a shampoo or a soap instead of an IT service.”

Profit asked M&C Saatchi MD for Pakistan Afzal Hussain on the inauthenticity of the pictures. He answered without giving any rational explanation for why the pictures appeared fake. Profit also asked Hussain to provide a third party audit report of the advertising campaigns for the government. Profit couldn’t reach out to PSEB to share these findings and ask for an audit report from them but Hussain said that he was meeting PSEB officials on Friday after which he would be able to comment on the effectiveness of the campaign. Later, when the pictures were shared, Hussain said that it was unlikely even after his meeting with the PSEB that he could share anything with Profit because confidentiality clauses with the client restricted them from sharing any details.

Our understanding is that PSEB officials would have received our queries on the questionable authenticity of their advertising campaign through Saatchi. We will include their version if they choose to give any response.

Visa support as leverage

Beyond inflated costs, there’s another, subtler form of control: visas. International exhibitions require participants to travel and that means securing business visas. For events officially endorsed by the government, visa facilitation is often coordinated directly through embassies. Participants receive priority processing, letters of support, and diplomatic endorsement. But for independently run events, no matter how credible, this support is denied.

This gives the official agent an unspoken but powerful tool: exclusivity by restriction for others. Companies may want to join better, cheaper, more impactful exhibitions, but hesitate because visa success isn’t guaranteed. For startups and SMEs, that uncertainty is often enough to walk away.

This isn’t hypothetical. It’s happening. In

one case, a Pakistani exhibition organizer had to refund over one crore rupees, nearly $35,000, out of pocket after visa refusals derailed participation. Meanwhile, the official agent continues to run government-backed events that deliver poorer results, face no scrutiny, and still retain monopoly control.

In some cases, independent success has led to outright theft. One organizer, after successfully running an exhibition for two years, was abruptly shut out. The name, target audience, even the format all copied and relaunched by the government’s preferred organizer. Pressure was exerted on the exhibition organizers to cut ties with the original host. Suddenly, the event that had been built from the ground up with relationships, planning, and investment was removed from official support lists and replaced with a government-backed duplicate. This is not a competition. This is erasure.

A system designed to exclude

The problem isn’t limited to one firm or one set of events. It’s a systemic issue. The same agent is repeatedly awarded contracts. They submit “internal lists” to ministries, which become the basis for subsidies, recognition, and visa facilitation. Events that aren’t on these lists don’t exist, at least as far as the government is concerned.

There is no transparency in how events are selected, how much public money is spent, or what value is actually delivered. Audits are either ignored or never conducted. And even when credible organizers present evidence of success photos, feedback, metrics, real industry traction they are quietly removed from official records the following year. Replaced by the same agent. A WhatsApp conversation seen by this reporter showed Shahbaz Hameed, the head of business development at PSEB, actively discouraging an event organizer in Singapore to not work with a private company and instead work with the Government of Pakistan’s agent.

The possible illegality in London Tech Week 2024-25

For two consecutive years, London Tech Week was listed in PSEB’s annual reports as a key international engagement. But in the most recent cycle (2024–25), the event was conspicuously missing from the official calendar issued by the Trade Development Authority of Pakistan, the very authority responsible for approving such expenditures. Despite this, PSEB went ahead and poured hundreds of thousands of pounds into subsidizing and marketing the event. This was done without

the required clearance from TDAP, making the spending not just irregular but legally questionable. The government’s official agent for the event was Dawar Khan.

Despite all of this, the independent organizers persist. With a database of over 9,000 contacts, active marketing, and 10– 12 committed companies per event, they continue to prove that good work doesn’t need subsidies to survive just fairness.

They charge fees around 1.5 to 2 lakh rupees per client and focus on value, not volume. Their margins are slim but sustainable. They don’t need handouts. They need a level playing field.

If they were offered the same 60% subsidy and visa facilitation that the official agent receives, their events would be nearly free for participants, opening the door for hundreds more Pakistani companies to compete internationally.

But the system isn’t built for equity. It’s built for control.

Senior officials at the PSEB, including CEO Abu Bakar, chief marketing officer Amir Anzur and head of business development Shahbaz Hameed did not respond to Profit’s request for comments on the matter. Instead, Profit has received credible reports that the said team at the PSEB has initiated a cover up to avoid accountability. Profit also reached out to Dawar Khan but received no response.

What needs to happen

The government must issue open RFPs for all subsidized international exhibitions. Let organizers compete on cost, quality, and performance. Publish budgets. Evaluate outcomes. Make it public.

If the goal is to promote Pakistan’s tech sector, visa support should be available for all credible events, not just the ones rubber-stamped by a single gatekeeper. Every rupee spent on subsidizing exhibitions must be accounted for. Let the industry choose where to go. If one organizer consistently delivers better outcomes, they should rise and not be removed from the list.

At stake is not just money, it’s Pakistan’s global image. Every time an inflated, poorly-run exhibition is passed off as “official,” it damages the credibility of our IT sector. It makes us look unserious, unreliable, and politicized.

But there’s another way. One where value is rewarded, not connections. One where public money uplifts the industry, not a monopoly. One where the people building platforms quietly, consistently, with real results are allowed to do what they do best: help Pakistan be seen, not silenced. n

By Council of Palm Oil Producing Countries

Q. What is the global significance of palm oil today and how does CPOPC play a role in this evolving landscape?

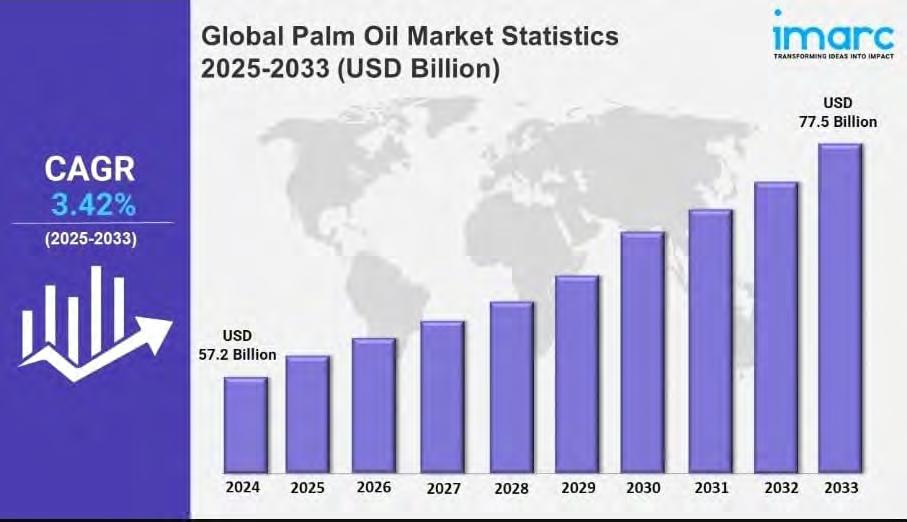

Palm oil holds immense global significance as one of the most productive oil crops in the world due to its versatility, efficiency, and widespread use. It has become one of the key ingredients in food products, household goods,cosmetics, and biofuels . Its high yield per hectare makes it a crucial crop for meeting the needs of a growing global population while using relatively less land compared to other vegetable oils. The oil used by over 3 billion people daily, either directly (in cooking) or indirectly (in processed goods).Nations such as India, China, Pakistan, Indonesia, and the European Union rank among the top importers, underscoring the global dependence on this vital commodity.

The Council of Palm Oil Producing Countries (CPOPC) is playing a pivotal role in shaping the future of the global palm oil industry. Founded by Indonesia and Malaysia, who together account for over 80% of global production has now five member countries and three countries as observers. These countries collectively produce nearly 90% of the global palm oil. As such, CPOPC aims to harmonize the voices of producing nations and ensure the industry grows in a sustainable, inclusive, and equitable manner. More importantly CPOPC is seen as the face of palm oil champion in the global stage.The rising demand for palm oil has also brought increased scrutiny regarding environmental and social impacts. This is where the CPOPC plays a vital role in safeguarding the interests of palm oil producing nations by promoting sustainable production practices and supporting inclusive growth, especially for smallholders.

The Council has adopted a ‘triple-track approach’ in advancing its international agenda. First, it leverages existing palm oil platforms across member states, other producing nations, and key consuming countries to strengthen cooperation and influence. Second, the CPOPC collaborates with producers of other vegetable oils to promote a unified front on sustainability.

Third, it actively engages with United Nations platforms to reshape the global narrative on palm oil, advocating for a more balanced and science-based perspective.

CPOPC promotes and supports national certification schemes like Malaysian Sustainable Palm Oil (MSPO) and IndonesianSustainable Palm Oil(ISPO) which uphold environmental and social responsibility in palm oil production. These standards ensure traceability, reduce deforestation, and protect workers’ rights, aligning with international sustainability expectations.Among other core task of CPOPC is to actively counter misinformation, foster international cooperation, and ensure that palm oil continues to be produced in a way that respects people’s right and protect the planet.

CPOPC also acts as a united front to respond to discriminatory trade practices, negative campaigns, and non-tariff barriers faced by palm oil in international markets. Through international meetings, policy platforms, and South-South cooperation, CPOPC strengthens collaboration among producing and consuming countries. It works to align palm oil development with the UN Sustainable Development Goals (SDGs), emphasizing food security, poverty reduction, and climate action.

Q. Can you share insights on current trends in palm oil consumption globally and what this means for

importing nations like Pakistan?

Palm oil has emerged as the most globally significant agricultural commodities due to its exceptional high yield as compared to other vegetable oils. It has become a cornerstone of global supply chains, due to its affordability and functionality making it critical for ensuring food security, especially in developing countries. Global palm oil consumption is experiencing a notable shift, particularly in Asia, which has significant implications for importing nations like Pakistan.

Asia-Pacific region’s consumption of palm oil has surged to 66 million tons in 2024, a 21% increase from the previous year. This growth was driven by rising demand in countries like India and China, where palm oil is favored for its affordability and versatility in food and industrial applications. Whereas, Pakistan also heavily relies on palm oil imports, with approximately 90% of its 3 million-tons vegetable oil requirement fulfilled through palm oil, sourced from Indonesia and Malaysia. Pakistan has imported 2.489 million tons between July 2024 andFebruary2025 recording an increase of 10%.

There are evolving dynamics to global palm oil consumption, particularly in Asia, which presents both challenges and opportunities for Pakistan. While increased demand in neighboring countries may strain supply and elevate prices, they also highlight the strategic

importance of securing stable import channels and investing in domestic production capabilities to ensure food security and economic stability. Pakistan’s domestic edible oil demand stands at 4.5 million tons per year, while local production is only around 0.5 million tons. To bridge this gap, Pakistan imports approximately 3 million tons of edible oil annually, with palm oil accounting for 2.9 million tons in 2023. This underscores the role of palm oil in ensuring food security in Pakistan.

Q. How does the palm oil supply chain work? and what value does it bring to countries like Pakistan?

The palm oil supply chain is a complex and integrated system that begins with cultivation and spans through processing, refining, logistics, and distribution, supporting various value-added industries. For importing nations like Pakistan, this supply chain offers significant economic and industrial development potential.

Pakistan as net importer of edible oil for its food security is dependent on crude or semi-refined palm oil. Numerous refineries in Pakistan can refine these products into edible form, which is widely used as cooking oil and in manufacturing value-added products like vanaspati ghee, soaps, surfactants, and personal care items. Since palm oil is affordable than other edible oils in the market, it has become a key ingredient in processed foods, supporting bakeries, snack producers, and confectionery companies.

Q. What frameworks like ISPO and MSPO ensure palm oil is sustainably produced, and how can Pakistan benefit from engaging with these mechanisms?

To ensure palm oil is produced responsibly, sustainability certifications such as the ISPO and the MSPO standards have been established by producing countries. These national certification schemes are designed to align palm oil production with internationally recognized principles of environmental stewardship, social responsibility, and economic viability. Both ISPO and MSPO promote transparency, reduce deforestation, and protect the rights and livelihoods of smallholder farmers.

For a country like Pakistan, which is a major consumer and is exploring opportunities in palm oil processing and cultivation, engaging with frameworks like ISPO and MSPO can offer several advantages. By adopting or benchmarking these standards, Pakistan can enhance the sustainability and traceability of its palm oil value chain; this could open doors for technology transfer, capacity building, and

Source: Imarc Group, January 2025

stronger trade relationships with leading producer countries like Indonesia and Malaysia.

Moreover, aligning with established sustainability standards would position Pakistan as a responsible player in the global palm oil landscape, attract environmentally conscious partners, and support the development of local certification systems tailored to national needs.

Q. What would you say to critics concerned about palm oil’s health effects and environmental impact?

Criticism surrounding palm oil often centers on its health implications and environmental footprint. While these concerns are not unfounded, it’s important to reframe the debate with science-based evidence and recognize the significant progress being made in sustainability across the palm oil industry.

Palm oil is frequently criticized for being high in saturated fats, but in nuanced reality palm oil is roughly 50% saturated fat, 40% monounsaturated, and 10% polyunsaturated—comparable to animal fats but with no cholesterol.Additionally, red palm oil contains tocotrienols (a form of Vitamin E) and beta-carotene, which have antioxidant properties. Numerous scientific studies have shown that moderate consumption of palm oil does not raise LDL cholesterol. In fact, it may help maintain a healthy ratio between LDL and HDL cholesterol.

On the other hand, legitimate environment concerns exist,regarding deforestation and habitat loss, particularly in Southeast Asia. Significant reforms have been initiated by the palm oil producing countries to address these issues which are;

• Many major producers and traders have adopted No Deforestation, No Peat, No Exploitation (NDPE) policies, which ban

the clearing of primary forests and protect workers’ rights.

• Traceability and Certification systems have been put in place. Roundtable on Sustainable Palm Oil (RSPO) Certification now covers nearly 20% of global production. While advanced traceability systems and satellite monitoring are being used to track the origin of palm oil and ensure compliance. While RSPO is volunteer basis, both Malaysian and Indonesian Governments has taken pro-active steps in making MSPO and ISPO as a mandatory requirement for all palm oil industry players.

• Palm oil is the most efficient vegetable oil crop, requiring 4–10 times less land than soybean, sunflower, or rapeseed oil for the same output. Globally, palm oil utilizes about 29 million hectares for cultivation while soybean more than 136 million hectares, rapeseed 44 million hectares and sunflower 30 million hectares as of 2023. When responsibly produced and consumed in moderation, palm oil is nutritionally sound and environmentally viable and can be part of a more sustainable and healthier global food system. The real solution lies not in boycotts, but in supporting sustainable production, transparency, and encouraging policy engagement.

Q. How is technology shaping the future of sustainable palm oil-from farm to frying pan to biofuel?

Technology has transformed the palm oil industry across its entire value chain from plantations to processing to end-use applications; ensuring greater sustainability, transparency, and efficiency. Lately, global expectations have risen for responsible production and climate-smart agriculture, innovative tools are

also reshaping how palm oil is grown, traded, and consumed.

Palm oil industry has started adopting various technological aids to improve the entire value chain and making palm oil more sustainable, accountable, and future-ready. Following are few examples of technologies are being used;

1) Digital traceability systems are now integral to tracking palm oil from plantation to final product. These systems use blockchain, QR codes, and integrated supply chain software to a) Map origins of fresh fruit bunches (FFB); b) Monitor custody transfers across mills, refineries, and distributors; c) Provide real-time data to regulators, buyers, and consumers. This transparency builds trust and ensures that palm oil is produced without contributing to illegal land use or deforestation.

2) Introduction of satellite imagery and remote sensing technologies allow near real-time monitoring of palm oil plantations. This helps to detect- a) Illegal land clearing or encroachment; b) Deforestation in high conservation value (HCV) areas; c) Fires and land degradation risks. These tools enforce sustainability commitments and quick response to environmental threats.

3) Digital certification and smart auditing tools are being used in palm oil certification processes to reduce bureaucracy and increase integrity. Tools such as- a) Mobile apps for field assessments; b) Digital dashboards for compliance tracking; c) AI-enabled audit systems. These help smallholders and companies to meet national and international sustainability standards more efficiently and cost-effectively.

Technology is also enabling palm oil to contribute to low-carbon energy transitions. The advanced processing techniques are improving the quality and yield of palm-based biodiesel and hydro-treated vegetable oil (HVO). Currently, research is underway into second-generation biofuels that utilize palm oil waste such as empty fruit bunches and palm kernel shells to generate clean energy. These developments align with global climate goals and also diversify palm oil’s role beyond food use. By embracing above mentioned tools, the industry is striving to enhance its global image, protect the environment, and ensure long-term economic viability—truly transforming palm oil “from farm to frying pan to fuel” in a sustainable way.

Q. Beyond food-what are some industrial and non-food applications of palm oil relevant to Pakistan’s growth sectors?

While palm oil is widely recognized as a staple in the global food industry, its non-food appli-

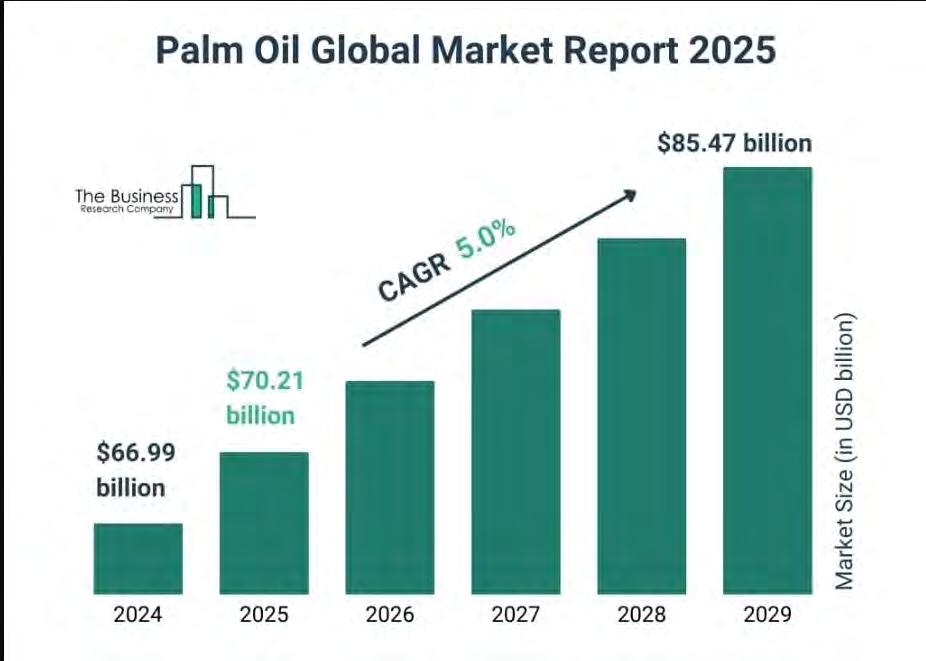

Source: The Business Research Company, January 2025

cations play an equally critical role in powering industrial growth in emerging economies like Pakistan. These applications span across cosmetics, personal care, pharmaceuticals, and bioenergy, offering immense value-added potential for domestic industries and export diversification.

Palm-based methyl esters are a viable alternative to fossil fuels. While biodiesel adoption in Pakistan is still in its early stages, the country has ambitious renewable energy targets. Palm oil-based biodiesel could offer a cleaner energy source for industrial fleets and agricultural machinery, especially if supported through government incentives.

With proper lobbying, Pakistan can align its industrial policy with global sustainability goals while unlocking new economic opportunities.Palm oil’s non-food applications offer Pakistan a chance to deepen industrial linkages, reduce reliance on imports, and move up the global value chain. By strategically investing in oleochemical processing and fostering public-private collaboration, Pakistan can transform palm oil from a raw import into a cornerstone of industrial innovation and sustainable growth.

Q. How does CPOPC currently engage with Pakistan, and what shared interests guide this collaboration?

CPOPC engages with Pakistan through a combination of policy dialogue, trade relations, and cooperative initiatives aimed at strengthening the palm oil supply chain and fostering mutual economic interests.