10 Sazgar is the third largest auto company in Pakistan. How did it get here?

16 Fast Cables has been stuck in a rut. Will it be able to break the jinx?

19 Govts are initiating AI projects. Can Sovereign AI be a national utility? Frank Meehan, Amit Gupta, Bashar Qallab, Sameer Chishty

20 Cement exports from the south region finally ramp up again

22 Are Telcos too fat to grow?

26 Migration, money and the making of Pakistan’s remittance economy

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

A well-time bet on assembling Chinese cars, and hybrid electric vehicles, has allowed the rickshaw manufacturer to crack into the top three, though staying there may be about to get tougher

By Zain Naeem

For more than three decades, the hierarchy of Pakistan’s passenger-car market resembled a well-rehearsed Kabuki: Suzuki ruled the mass segment, Toyota presided over the upper-middle, Honda filled the aspirational middle-class niche – and everyone else fought for crumbs. That appears to have changed.

With the Pakistani auto market being more filled with nascent competitors, not all of whom are publicly listed, data on the industry as a whole is not as easy as once used to be when one only really needed to look at three companies. But based on a rudimentary analysis conducted by Profit, it appears that Sazgar may become the third largest auto company in Pakistan by revenue during the first quarter of calendar year 2025.

We have covered the rise of Sazgar – and indeed the other competitors to the Big Three Japanese car companies – before. But that was when it seemed like an interesting nascent set of challengers. Now the challengers are starting to have real heft. How did this come to pass?

To answer that question, we must first provide some context about the industry, and how it is doing.

A struggling industry

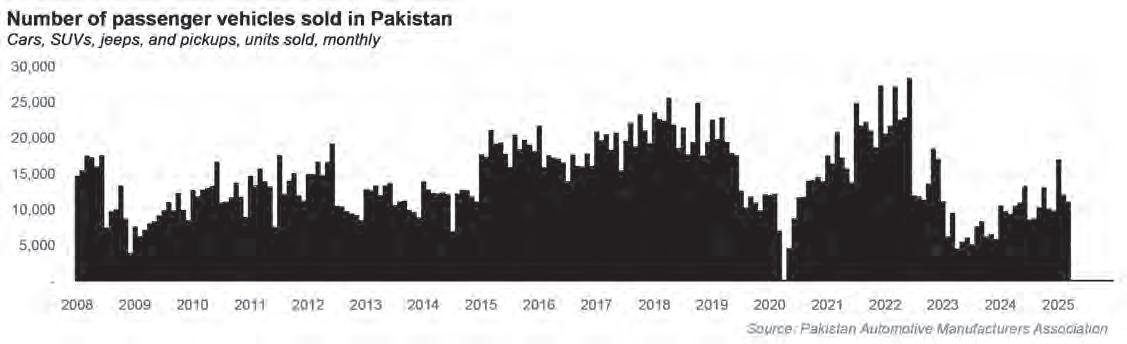

It would not be an exaggeration to say that the past few years have been tumultuous for Pakistan’s auto sector. The industry’s most recent up-cycle began in 2013, when manufacturers sold 118,830 units.

Sales rose every year, peaking at 216,786 units in 2018. After that, volumes slipped – and the pandemic amplified the downturn.

The sector finally seemed to regain its footing in 2022, when sales hit a record 234,180 units. The rebound was short-lived. A stronger dollar, soaring inflation, falling real wages and strict import curbs combined to crush demand, pushing deliveries down to just 81,579 units in 2024 –barely one-third of the 2022 tally, and the steepest decline since the global financial crisis of 2008.

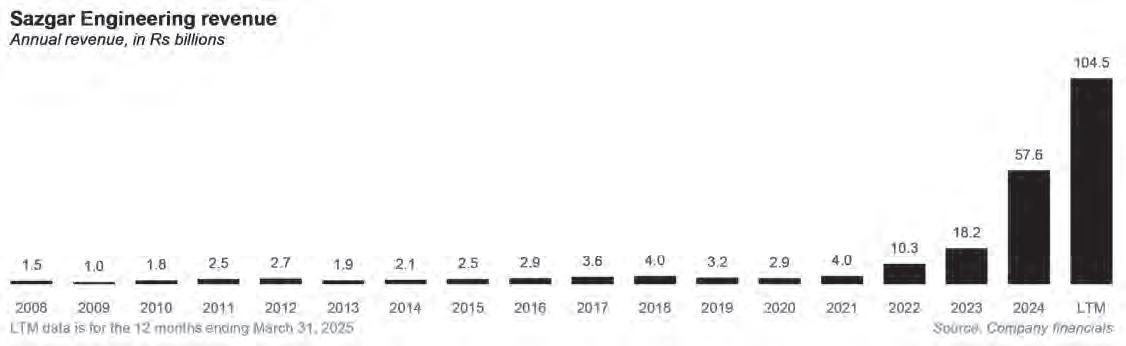

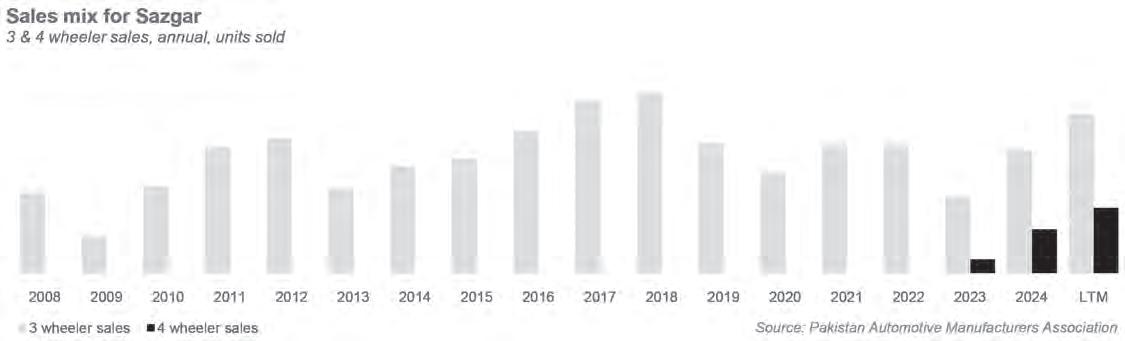

Amid this contraction, Sazgar Engineering Works staged a remarkable breakout. Before 2022, the Lahore-based firm was known almost exclusively for its three-wheeled rickshaws, a market it dominated but one that offered razor-thin margins. In 2018 it sold 22,000 rickshaws –impressive volume, but profits were constrained.

Between 2009 and 2022, Sazgar’s gross margin rarely topped 10 percent, and it dipped to a low of 8.7 percent in 2022; net margin hovered around 1 percent. Management realised the company could not survive on such modest returns and began laying the groundwork for a pivot.

Reinvention is woven into Sazgar’s DNA. Founded in 1991 to make auto parts and household appliances, the firm swung into rickshaw manufacturing in 2005 after years of losses. The National Bank of Pakistan’s “President Rozgar Scheme” – a subsidised-financing plan for rickshaw buyers – turbo-charged sales. In 2008, Sazgar earned Rs13 per share on roughly 10,000 units. When the scheme’s funds dried up the following year, EPS collapsed to Rs1.3 and volumes halved. Still, the seeds of future growth had been sown: from 2010 onward, Sazgar consistently sold at least 10,000 rickshaws a year, cresting again in 2018.

The problem was margin: the average rickshaw sold for about Rs175,000, and 90 percent of that price was cost.

Betting on four wheels

Opportunity knocked in the form of the government’s Auto Development Policy 2016-21, which offered tax breaks to firms building new assembly plants and aimed to weaken the long-standing stranglehold of Toyota, Suzuki and Honda. Lucky Motors, Hyundai-Nishat and Sazgar all set up factories under the scheme, benefiting from sharply reduced import duties on parts.

Sazgar signed joint-venture deals with Great Wall Motors (Ha-

val) and BAIC in 2017. Early on, it imported completely built-up (CBU) vehicles – an unprofitable strategy but a useful test of market appetite. Losses persisted until 2021, when locally assembled models finally rolled off the line. Patient investment began to pay off: Sazgar sold about 1,657 four-wheelers in 2023 and 5,319 in 2024, setting the stage for what could be a record year in 2025.

The timing could not have been sweeter. Spiralling fuel prices and chronic power shortages had nudged affluent buyers toward electrified options. With the H6 HEV priced at roughly Rs11.7 million – well below Toyota’s imported RAV4 hybrid – Sazgar found itself in a blue-ocean segment it effectively created.

By the fiscal year ending June 30, 2024 the company claimed 45% share of the hybrid-SUV space. That segment, once a statistical rounding error, ballooned to 16,000 units in FY24 and is forecast by JS Global to hit 25,000 in FY 2025.

Zooming in on the Latest Numbers

Recent results underscore the momentum. In the first nine months of FY 2025, revenue jumped 135 percent year-on-year to Rs81.5 billion while

unit sales climbed 155 percent to nearly 8,000. Gross margin, once stuck below 10 percent, rose to 30.5 percent. Operating margin expanded from 2.9 percent in 2022 to 26.7 percent, and net margin improved from 1.2 percent to 15.8 percent.

Why? Selling prices have held steady for nine months, implying that cost control –rather than price hikes – drove the fatter gross spread. Overheads grew in absolute terms but shrank as a share of sales, boosting operating margin. Finance costs were stable, and profits on sizeable bank deposits (around Rs11 billion) partially offset higher worker-welfare charges.

Earnings per share surged to Rs212.67 for the nine-month period, up from Rs73.59 a year earlier. Full-year results, due in September, and PAMA sales data, expected in July, are likely to confirm that the Sazgar juggernaut is still rolling.

While most assemblers raised prices merely to stay afloat during the 2022-24 slump, Sazgar swam against the tide – growing volumes as industrywide sales fell 59 percent in 2023 and another 16 percent in 2024 (from 234,000 to 82,000 units).

The company’s Haval-branded SUVs are classified as pickups for statistical purposes. Segment sales slid from 45,000 units in 2022 to 22,250 in 2024, but strip out Sazgar’s contri-

bution and the decline is even starker. Sazgar’s share of the segment rose from 5.5 percent in 2023 to 24 percent in 2024, and to 31.4 percent in the nine months to March 2025 (17,500 units sold). Without Sazgar, rival pickups saw sales stagnate – testament to the brand’s growing pull.

A new frontier: electrification

The latest auto policy sweetens the deal for electric vehicles, and Sazgar intends to capitalise. It is developing its own three-wheel EV and plans to introduce battery-electric versions of the Haval H6, Jolion and Ora 7. Management is betting that an early move into electrification will extend the winning streak.

Sazgar’s story is one of relentless adaptation. In the 2000s, it muscled into a crowded rickshaw market and won. When the 2016 policy opened a window into passenger cars, it built a plant and partnered with Chinese OEMs. Now it is gearing up for an EV future. Judging by past gambles, the newest one may well pay off, too.

The payoff is visible on every line of the income statement. Gross margin, once stuck below 10%, crossed 30% for the first time as

learning curves, a weaker yuan and localisation gains kicked in. Operating margin followed suit, expanding from 2.9% in FY22 to 26.7% this year. Much of the incremental cash –roughly Rs11 billion, according to company filings – sits in Islamic bank deposits, cushioning finance costs.

Sazgar is ploughing those profits back into brick and mortar: an Rs11.5 billion expansion will lift four-wheeler capacity from 15,000 to 40,000 units by 2026 and fund a dedicated “New Energy Vehicle” (NEV) line for full battery electrics.

Local content on the H6 HEV is already 29%, up from 12% at launch. Engine blocks, bumpers, seats and wiring harnesses are now made in-house or by a constellation of vendors in Punjab’s industrial triangle.

The SUV angle

Over the past two years, Pakistan’s passenger-vehicle recovery has been led not by city cars or family saloons but by crossovers and compact SUVs. In December 2024, for example, SUVs accounted for the lion’s share of the 69 percent year-on-year jump in nationwide sales, according to PAMA data. Ground clearance for rough roads, a commanding driving position and social prestige are all part of the appeal—but

so is price.

Today Sazgar’s Haval/BAIC line-up is the cheapest path into a brand-new SUV with turbo power or a full hybrid drivetrain: Sazgar is effectively offering an SUV for a sedan budget. Sazgar’s entry-level Jolion 1.5T costs only 5% more than a Corolla Altis X and undercuts the Kia Sportage Alpha (Rs95 lacs) by Rs15 lacs. Even the flagship H6 HEV is priced within shouting distance of a fully-loaded Honda Civic RS and actually undercuts Toyota’s imported Prius hybrids by a full million rupees.

It is also offering a hybrid without the premium. The Jolion and H6 hybrids sit at Rs93 lacs to Rs1.2 crore – below Hyundai’s Sonata 2.0 petrol (Rs99.3 lacs) and on par with Hyundai’s own Elantra Hybrid sedan. For buyers chasing fuel economy rather than badge prestige, that’s an easy upsell from a sedan to an SUV.

They are also playing on the psychology of the “size upgrade”. In a market where families are already paying Rs80 lacs to Rs1 crore for a Civic or top-trim Corolla, an extra half-million for a larger, higher-riding vehicle feels justified—especially when the Haval badge carries Chinese-tech novelty value.

By offering five SUV variants spanning a tight Rs79 lacs to Rs1.2 crore band, Sazgar captures customers moving up from B-sedans

(Alsvin/City) and those cross-shopping C-sedans (Corolla/Civic/Elantra).

It still boasts the cheapest locally-assembled full hybrid SUV; rival hybrids such as Toyota’s Corolla Cross HEV start around Rs90 lacs but remain partially imported and supply-constrained.

Showroom promotions pitch the Jolion HEV as “Civic money, Fortuner stance,” leveraging consumers’ willingness to stretch loans for perceived lifestyle gains.

By pricing its SUVs smack in the middle of mainstream sedan territory, Sazgar converts Pakistan’s growing SUV infatuation into hard sales—without forcing buyers into the Rs1.2 crore-plus bracket dominated by Korean and Japanese names. As long as that price gap holds, and fuel prices stay high, expect more sedan intenders to walk into a Sazgar dealership and roll out in an SUV.

The fuel price environment

All of these market developments are taking place against the backdrop of what looks like a long-term elevation in fuel costs in Pakistan, owing to what appears to be a shift in the government’s approach to pricing the commodity. Global crude is in retreat. Brent has

slipped from roughly $75 a barrel at end-March to around $60-65 in late April 2025, a drop of more than $14. Energy analysts calculate that, other things equal, the slide could shave about Rs 12 per litre off domestic petrol and diesel prices.

Yet on 16 April the federal government announced that it would keep petrol at Rs 254.63 and high-speed diesel at Rs 258.64 per litre for the next fortnight, effectively banking the import-cost savings instead of passing them on to consumers.

Prime Minister Shehbaz Sharif said the foregone relief would be channelled into “development and uplift projects,” citing, among others, upgrades to National Highway N-25 in Balochistan.

Behind the decision lie three fiscal pressures. Firstly, the petroleum levy is maxed out. The government is already charging the statutory ceiling of Rs 70 per litre on petrol and diesel; trimming pump prices would lower levy receipts at a time when the budget is hunting for every rupee.

Secondly, there is no GST cushion. Islamabad has kept the general sales tax on fuel at zero since early 2022 to blunt the political bite of previous price spikes. Re-imposing GST now would neutralise any cut and trigger fresh backlash, so officials prefer to lock in the levy windfall.

Consumer lobbies and the opposition have criticised the move, warning that high transport and logistics costs will keep headline inflation stuck near 20 percent. For now, however, the policy signals that revenue protection outranks price relief on the government’s priority list—even when the international market offers a brief breathing space.

Competition stiffens up

It is against this backdrop that Sazgar’s success in the market has prompted what looks like a daunting prospect of competing against a large number of companies trying to enter the market.

• Master Changan began road-shows for its low-cost Lumin city EV in October 2024 and plans CKD assembly in Karachi by early 2026.

• Regal Automobiles, backed by the Saifullah Group, rolled out Pakistan’s first locally-assembled Seres 3 electric SUV in December 2024.

• BYD–Mega Motors is investing in a Karachi plant to launch three EV models, with an aggressive goal of 50% national EV penetration by 2030.

• Toyota Indus has already localised the Corolla Cross hybrid (1.8-litre) at Port Qasim and is reportedly studying a 1.5-litre Yaris hybrid.

• Hyundai Nishat showcased the Elantra Hybrid and fully-electric Ioniq 5/6 line-up in

January 2025, billing itself “Pakistan’s first hybrid-sedan assembler.”

• Lucky Motors started road-testing the fifth-generation Kia Sportage Hybrid, hinting at a 2025 launch.

In short, the hybrid/EV battlefield that Sazgar once had to itself is getting crowded –fast.

Other constraints

Government incentives remain pivotal. The Auto Industry Development & Export Policy (AIDEP 2021-26) slashed duty on EV imports to 10%, helping brands test the waters with CBUs. Yet Islamabad is already drafting an EV-specific roadmap for 2025-30 that could tilt the playing field once again – perhaps by rewarding localisation over imports. Sazgar’s management publicly supports a localisation-weighted scheme, but rival assemblers lobby for extended CBU concessions to achieve scale first.

With 30% margins and single-digit leverage, Sazgar looks financially bulletproof –on paper. Yet two macro variables could spoil the party:

1. Exchange Rates. Each Rs10 slide in the rupee against the yuan erodes roughly 80 basis-points of gross margin, according to a BMA Capital sensitivity note.

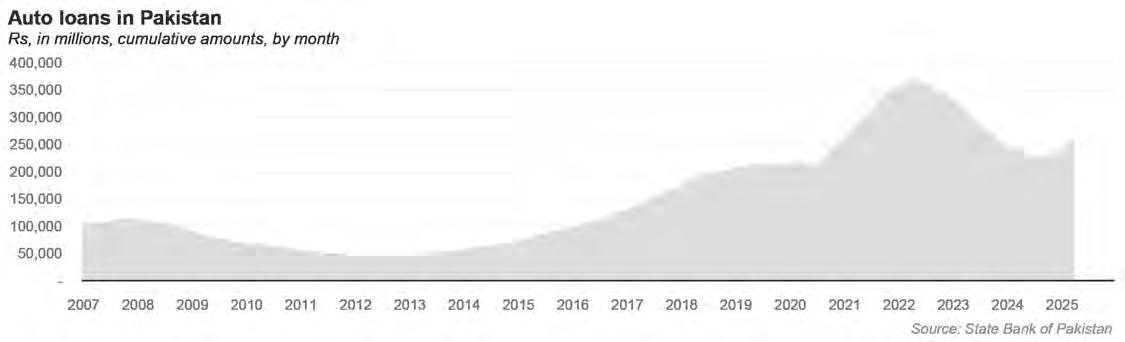

2. Interest Rates. Easing monetary policy has revived auto finance – installment volumes grew 20% QoQ in 1Q 2025 – but a reversal could sap demand.

Management says a localisation blitz will cut import content. Investors remain sanguine; SAZEW stock trades at 7.5 × FY25E earnings, a premium to the KSE Auto index.

Great Wall’s Tianjin export hub has faced container bottlenecks since the Red Sea rerouting. A January shipment delay forced Sazgar to idle its paint shop for five days, costing an estimated 300 units. “Single-sourcing drivetrains is our Achilles’ heel,” concedes COO Rana Irfan. The upcoming NEV plant intends to assemble e-motors locally and import only battery cells. But integrating a gigawatthours-scale battery line in an energy-starved country raises its own questions.

Unlike Toyota or Suzuki, Sazgar lacks decades of after-sales infrastructure. The company has expanded its 3S dealership network from 4 cities in 2021 to 17 today, yet spareparts shortages and software update delays still pepper owner forums. Consumer researchers at Ipsos Pakistan rank Haval eighth in “service satisfaction,” below Chinese peer MG but well ahead of Chery. Bridging that perception gap will require money – money that competitors are also willing to spend.

One underrated asset in Sazgar’s arsenal is diversification. Three-wheelers remain a cash-cow: volumes totalled 22,170 units in 9MFY25, and an e-rickshaw variant – licensed

in January 2024 – will enter pilot production this summer. (Sazgar bets on e-rickshaws for Pakistan’s EV future - Rest of World)

Price-sensitive urban commuters could propel that product into a mass-market hit, providing a revenue buffer if SUV demand cools.

What could go wrong?

Several changes in circumstances could prove to be risky for the company. If the new EV policy rewards late entrants with new tax breaks, Sazgar’s first-mover investment could become a sunk cost. Great Wall is simultaneously pursuing CKD plants with Egyptian and South-African partners; a strategic pivot away from Pakistan could choke SKD kit supply.

The Rs11.5 billion expansion is entirely debt-financed; cost overruns or demand shocks could stress cash flows. Even at Rs9–12 million, hybrid SUVs are out of reach for 97% of Pakistani households. Mass adoption hinges on lower-priced NEVs or robust auto-finance schemes – variables Sazgar cannot fully control.

Broker consensus sees Sazgar’s four-wheeler sales hitting 20,000 units by FY27, implying a 27% CAGR – fast, but slower than the 140% pace of FY24. Profit growth is forecast to trail volume growth as competition trims pricing power and localisation savings plateau. If those projections hold, Sazgar will remain the perennial bronze-medalist – profitable, innovative, but no longer an industry disruptor.

Sazgar’s journey from tin-bodied tuktuks to premium hybrid SUVs is a feat of entrepreneurial audacity and policy arbitrage. Its rise exposes long-standing inefficiencies in the Japanese incumbents’ playbook and lights a path for other Pakistani conglomerates hungry for Chinese technology transfers.

Yet the very factors that fuelled that ascent – open policy windows, a China cost advantage, a green-mobility vacuum – are now available to every aspiring assembler. With BYD breaking ground in Karachi, Changan hawking sub-Rs3 million EV hatchbacks and Toyota localising hybrids, the competitive moat around Sazgar is narrowing by the quarter. Sustaining its new-found third place will hinge on staying several product cycles ahead, localising deeper, and translating rickshaw-era hustle into Big-Auto discipline.

If management pulls that off, the chapter you are reading will mark the beginning of Sazgar’s transformation, not its climax. If not, historians may someday record 2024-25 as a glorious – but brief – episode when a rickshaw upstart shocked the establishment and proved, however fleetingly, that David could sprint with Goliaths.

Fast Cables has been stuck in a rut. Will it be able to break the jinx?

The cable manufacturer has failed to spark the expected interest but things seem to be changing for the better

By Zain Naeem

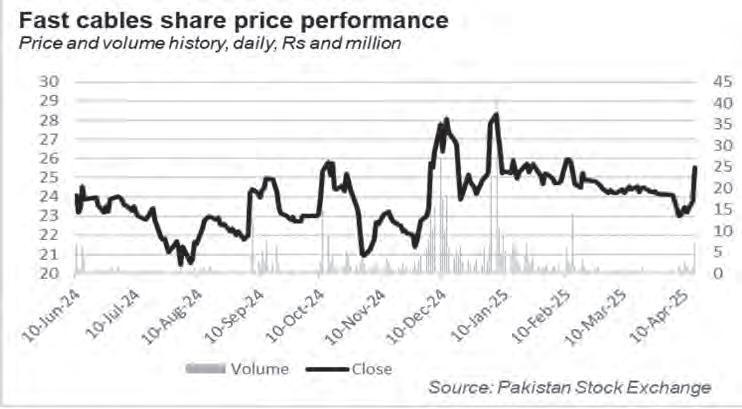

Fast Cables is the leading cable manufacturer in the country with sales in excess of Rs 36 billion. Based on its market domination, it should have seen the market react positively to its listing. However, considering its share price performance, the company has failed to replicate its results in the market. Since Fast Cables was listed in the exchange back in June of 2024, the share price started at Rs 24, saw a low of Rs 20 and a high of Rs 28 before settling back at Rs 24 in the start of April 2025. In a space of 9 months, the share price has shown an underwhelming response and has been stuck between a tight range. In the same period, the KSE 100 index has increased by almost 60%.

Now it does seem that things are changing for the better due to internal and external factors which can have an impact on its future price performance. Will the market react to these changes? The first step seems to be in the right direction.

History of Fast Cables

The history of the company can be traced back to 1985 after which Fast emerged as a large player in the electrical wiring market by targeting both domestic and commercial customers directly. Up until this point there were very few companies that directly sold electrical cables to consumers who relied on contractors and wholesalers to get unbranded electrical wiring. Fast Cables shook things up in the country’s cable industry and soon bagged a number of large clients particularly in the oil, gas, and telecommunications sectors.

The company went public in December 2008 and based on the performance of the benchmark index, decided to get listed in the market with an Initial Public Offer (IPO) of Rs 3 billion carried out in June of 2024. The goal of the IPO was to capitalize on the KSE 100 index reaching new highs and to divert some of this enthusiasm towards the shares of Fast as well.

The purpose of going to the public was to raise funds which could be used to acquire new land, construct a state of the art factory building and to install new plant and machinery in order to increase production capacity. Additional funds were to be used to retire some of the debt taken and to meet any working capital requirements.

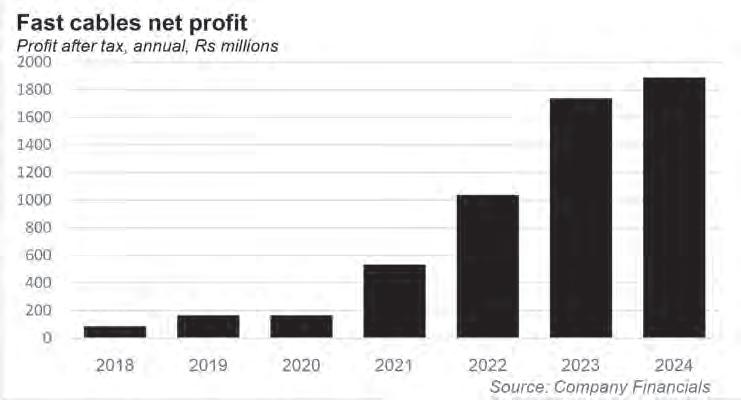

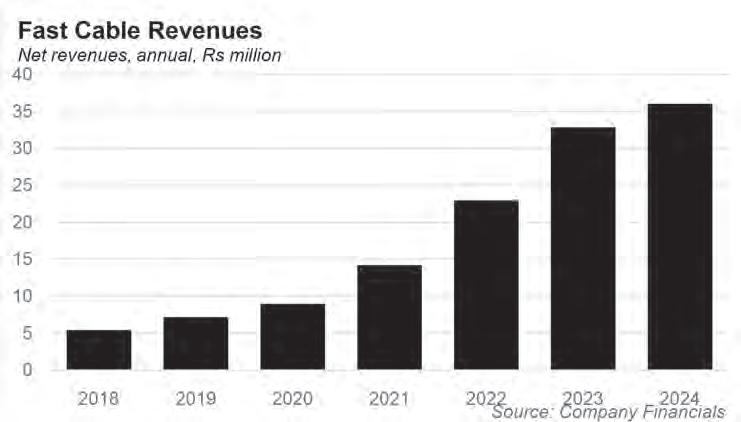

For a market leader, the underwhelming market performance does seem a little bit baffling. In terms of revenues, Fast cables has been able to post good topline numbers. In 2018, Fast cables registered revenues of Rs 5.4 billion which have grown steadily to Rs 36 billion by June of 2024. This is a growth of more than 6 times in a space of six years. This can be translated to a compound annual growth rate of 37%.

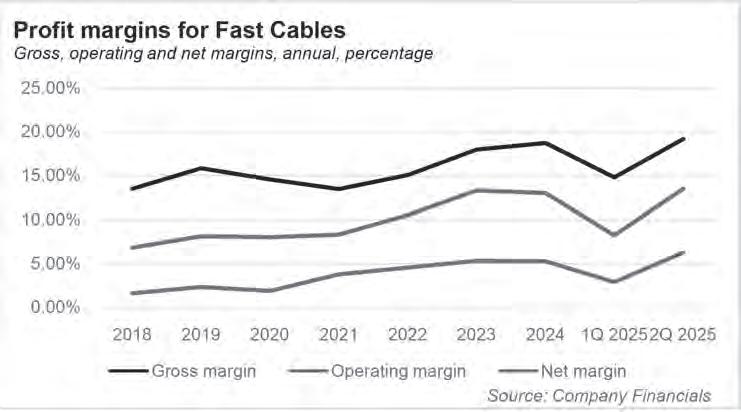

The good news for the company does not just end there. In terms of the gross profit margin, Fast has actually been able to increase its gross profit margin from 13.45% in 2018 to 18.69% in 2024. An expansion in gross profit margin shows that Fast has been able to increase its prices more than the increase it has seen in its costs.

With copper and aluminum prices increasing from 2018 to 2024, this is a positive point as the company was not able to maintain its gross profit margin but actually able to increase it. In 2018, copper price averages were hovering around $2.71 per pound which increased to $4.39 by the end of June 2024. Aluminum prices also saw a similar trend trading at $2,000 per ton in 2018 and increasing to $2,400 per ton by end of 2024.

The maintenance of this gross margin becomes even more monumental when it is considered that from 2018 to 2024, the dollar appreciates against the rupee going from Rs

120 per dollar to Rs 280 by the end of June 2024. In the face of increasing commodity prices and depreciating rupee, Fast Cables was able to import the raw materials while being able to expand its gross profit margin as well.

One of the biggest challenges the company has faced, however, is the fact that it has seen many of its indirect expenses increase during the same time which has led to its net margin actually falling while its gross margin has increased. In 2018, Fast cables was able to retain 1.6% out of its gross margin of 13.5%. In 2024, the net margin should have been around 7% with a gross margin of 18.7%.

The trend could not be copied and Fast was only able to show a net margin of 5.2%. The reason for this fall is the biggest hurdle that is faced by the company.

Operating cycle issues

The business model of Fast cables is such that it has a very long operating cycle. The operating cycle is the length of time it takes from procuring the raw materials to manufacture the product, sell it and then recover the money from the sales. For Fast Cables, the operating cycle was 58 days in 2019 which has worsened to 79 days in 2024. Breaking down this figure, it took the company 147 days to convert inventory into a finished product and around 77 days for the customers to pay back the amount that they owed. This meant that the company was out of cash or money for around 224 days. The saving grace during this time was its creditors were asking for their due amounts in 166 days. The result of this was that the company was out of cash for only 58 days.

The trend has shifted greatly since then. In 2024, it took the company 110 days to convert raw materials into finished goods while its debtors took 82 days to pay back their dues. In comparison, the creditors were asking for their dues back earlier which meant that Fast paid them back in 114 days. The result of this was that the operating cycle stretched to 79 days.

This performance of Fast Cables can be

compared to another listed cable manufacturer called Pakistan Cables. In 2019, Pakistan Cables had an operating cycle of 146 days which has decreased to 100 days by 2024. In absolute terms, Pakistan Cables is worse compared to Fast Cables, however, the trend is opposite where Pakistan Cables is looking to shorten its operating cycle while it is being lengthened for Fast Cables.

The impact of longer duration in recovery of cash has a direct impact on the working capital. As the cash is taking longer to recover, Fast has to rely on borrowing in order to be able to raise the necessary working capital in order to operate. In 2021, the company had short term borrowings of Rs 3.2 billion on its books which had increased to Rs 8.3 billion by end of June 2024. The dependence on borrowing has continued as it had short term borrowings of Rs 11.4 billion by the end of December 2024.

As the borrowings started to mount, the finance cost began to rise. From 2021 to 2024, the interest rates were rising hitting a high of 22% from June 2023 to June 2024. The finance cost stood at around Rs 283 million in 2021 which increased to Rs 1.4 billion by end of June 2024. In order to put this into context, interest expense was 2% of sales in 2021 and ended up at 3.8% by the end of 2024. In terms of profits, interest rates made up more than 50% of net profits in 2021 and nearly three quarters by the end of June 2024.

From June 2024, the interest rates have been on a steady decline which should have led to a fall in the finance cost. However, Fast started to take out more debt in this period in order to fill the gap that existed in its resources. In 2023, the company had paid out around Rs 585 million for the 6 months ended December 2023. In the latest year, it has already raked up 50% higher cost of debt of Rs 900 million as it has increased its short term debt in the face of falling interest rates.

This is the key reason why Fast seems to

be falling behind in terms of its performance. A major chunk of the profitability is being lost in the form of finance cost. Another metric which shows how the company is falling behind is by considering its cash flow from operations. This is the amount of cash that the company is gaining or losing based on its working cycle management. For Fast, the figure has been mostly negative from 2018 to 2024 with the latest year recording a net cash outflow from operations of Rs 4.1 billion.

This is the gap that is left once the creditors are paid off while the debtors take their time to pay back. Considering the operating cycle in a simple manner. Fast places an order with its creditors who send the relevant raw materials to the company over time. These suppliers are mostly in foreign countries while there are a few local suppliers that are used as well. Once the materials have been sent, the creditors start to count the days before they are supposed to be paid back. As the materials are sent, they have to be shipped and sent to the factory which then processes them. Once these are processed, they are sent to the branches and outlets selling Fast Cable

products. After these are sold, the debtors take away the goods and then take their time to pay back the company.

While the recovery from the debtors has to be made, Fast needs to keep churning more revenue from the system which means it has to borrow to keep ordering and then get more materials for more products. As the cycle is slow to generate cash, the cycle keeps elongating with the use of banks and other short term debt options. This keeps on increasing the finance cost and eats into the profit margin being earned.

Fruits of IPO start to trickle in

When the IPO was carried out, the goal was to raise ample amounts of funds which could then be used to establish a new plant and to expand the production capacity of the company. On 15th of April 2024, the share price of the company started to rally and closed at a new high of Rs 25.5 which had not been seen for a few months. The impetus for the increase was the fact that Fast announced to the exchange that they had completed the commissioning of their new copper upcasting plant which would boost their production from 5,000 tons per annum to 10,000 tons per annum.

The plant had been in the works for some time and the funds raised from the public allowed the company to pay off some of its debt and establish the new plant. The new plant would add efficiency and would be used to meet growing demand for international and domestic market.

There is also a buzz around the fact that Fast is expanding into the exports market by targetting the Middle East in order to meet the international demand that is sprouting up in Saudi Arabia and adjoining Gulf states. The company has started to export to these mar-

kets and with added capacity, it will be able to meet the additional needs.

By looking to expand beyond the borders, Fast will be able to manufacture and export to countries while the local demand dips. The company was expecting the solarization drive and infrastructure development to be able to increase local demand. As the power sector of the country looks to take a breather, international markets can be explored and expanded into which will ensure growing revenues for the company going forward.

Fast Cables also has the privilege of being the first and only cable manufacturer in the country which has the British Approvals Service for Cables (BASEC) certification. The certification is given by the UK based organization after testing the cable manufacturing process and facilities of a company. The certification means that the product being manufactured meets quality and safety standards on an international level. The certification can be used to market the products into international markets and opens up an avenue for export into foreign markets.

In addition to better demand, there are also a few solutions that the company can contemplate which can look to improve the current situation existing at the company.

Ways to mend their ways

In order to get out of the debt spiral, there are certain solutions that can be carried out which can help in such a situation.

The first option is to start using long term debt rather than short term debt to finance this gap. The interest rate on long term debt is usually lower and can help cut down on the cost that is being faced by the company. Fast used to rely on long term debt but has steadily paid it off in order to decrease this burden. Now it can look to use this avenue in order to take future loans.

In addition to that, Fast should also consider issuing long term finance certificates (TFCs) or even sukuks in order to finance their needs. Sukuks or TFCs are like bond issues that can be carried out by companies which allow banks and other corporations to invest in the bond. In comparison to loans, mutual funds and Shariah compliant asset management companies are also allowed to invest in these instruments as they give a steady flow of income against low risk. Fast Cables can use it like Mughal Steel does in order to finance working capital requirements. Steel industry is another industry which sees high working capital demands and uses sukuks and TFCs to fill this gap.

Sukuks or TFCs are flexible in terms of the tenor till their maturity and allow the company to gain access to a pool of funds which was not available to it before. TFCs are also favourable for investors as they can hold or sell these instruments in the market which allows them to recover their investment while a new investor is ready to hold onto this instrument. The company gets access to a new source of funds while the investors get access to a new financial instrument which yields a stable

income to them.

Another avenue for improvement of the company is that it can sign contracts with foreign suppliers which can provide them a manner to shorten the operating cycle. The company does not have any long term contracts with its suppliers which can provide a guarantee that the suppliers will be paid in time which can extend the credit terms being offered to Fast. If such a contract was signed, it can decrease some of the burden to take out loans. This coupled with contracts for plant and machinery and engineering, procurement and construction (EPC) can decrease the cost and make sure they are completed on time.

One opportunity that has sprouted up for the company is the recent tariff war which can actually prove to be beneficial for Fast Cables. Around 92% of the cost of production of Fast is made up of its raw materials which have to be purchased. The tariff war has meant that copper and aluminum have seen their prices fall in recent days. Copper hit a high of $5.25 per pound slumping to $4 per pound in a matter of weeks. Similarly, aluminum was trading at $2,700 per ton falling to $2,300 per ton. Both these materials getting cheaper will be able to help the gross margin of the company in coming months.

Being the market leader and earning revenues in excess of Rs 36 billion, Fast should be a company that is performing much better in the market. Considering such a strong background, the stock market has not reacted to the share like it should have and there is a fair reason for this. The company has certain weaknesses internally which need to be addressed to counter some of the headwinds that have been faced by its performance. Depending less on short term debt and looking for more flexible alternatives will provide an impetus to the company going forward. In the short term, the commodity slump can provide some of the spark that is needed to take Fast cables in the right direction. n

Frank Meehan, Amit Gupta, Bashar Qallab, Sameer Chishty

Govts are initiating AI projects. Can Sovereign AI be a national utility?

The adoption of AIis accelerating globally, revolutionizing companies and governments with an emerging “super intelligence” making decisions faster and allocating resources more efficiently, while technologies like ChatGPT and Perplexity are enhancing daily productivity and entertainment for people. But, at the same time, AI is becoming of huge importance geopolitically as American protectionist policies spur countries into action – to innovate, invest and develop AI systems locally, ensuring that such an important national technology is not reliant on foreign powers.

India is set to build the world’s largest AI data center, a USD 30 billion facility—three times larger than any U.S. counterpart. The DeepSeek Open Source AI model developed by a hedge fund in China, is now securely deployed in U.S. companies and global governments through localized, independent versions. Meanwhile, nations like France, India, Thailand, and Indonesia are launching Sovereign AI initiatives, spending billions on secure, domestically operated AI infrastructure. In 2024 alone, national governments invested $10 billion in AI GPUs, with nearly a quarter of new computing capacity dedicated to national AI use.

AI-driven defense systems—autonomous drones, cybersecurity protocols, and predictive analytics—are reshaping military operations, as seen in Ukraine. These technologies enhance real-time threat assessment, precision targeting, and casualty reduction. In healthcare, AI optimizes medical record analysis, disease prediction, hospital resource allocation, and surgical assistance. Machine learning accelerates drug discovery and personalizes treatments, improving patient outcomes and reducing costs. However, as AI continues to shape industries in profound ways, the importance of ensuring that a nation's sensitive national and personal data has never been clearer.

This is pushing national and state governments around the world to invest in what is known as “Sovereign AI” – a term that refers to the combination of AI software and state of the art AI-optimized datacenters built locally with cyber-security, localized AI models and secure applications as the software powering these centers. Enabling countries to maintain sovereignty over core digital assets, while providing the technology for government, companies and startups to innovate fast and effectively.

The "awakening" of sovereign AI is being led by key industry

The authors are co-founders of Frontier One AI, a technology company based in Silicon Valley and Dubai that works with governments and state-owned enterprises in establishingnational “AI Factories” https://www.goldmansachs.com/insights/articles/ generative-ai-could-raise-global-gdp-by-7-percent https://www.pwc.com/gx/en/issues/analytics/ assets/pwc-ai-analysis-sizing-the-prize-report.pd

figures, such as Jensen Huang (CEO of NVIDIA) and Michael Dell, who emphasize the necessity for nations to control their AI intelligence and data. AI has emerged as a new strategic resource, much like oil or natural gas, and it’s crucial for countries to safeguard their access to this valuable asset. The global recognition of AI’s potential extends from Southeast Asia’s tech hubs like Singapore to resource-rich countries such as Saudi Arabia and aspiring AI powerhouses like Argentinawith the establishment of powerful AI Factories (highly specialised data centers) in countries with abundant energy. This then gives nations the power to develop AI tools that are powerful, protected, and, under their control – using open-source AI models such as DeepSeek, Qwen and Llama whichprovide a cost-effective way to maintain data security while promoting national AI development, at costs considerably lower than OpenAI with the benefit of full control over the resulting models and data.

However, Sovereign AI is not about excessive government control Overregulation in Europe has stifled AI innovation, forcing startups to navigate a complex web of legislation before launching products—often making them obsolete upon release. A well-implemented Sovereign AI strategy instead prioritizes cybersecurity, local data centers, and AI models with minimal regulatory friction, fostering innovation while ensuring national security. In practice, this means that nations still adopt the latest global innovations but maintain independent operational capabilities – such as national AI models handling defense, finance, agriculture, and health data, while tasks like writing, video creation, and research can leverage platforms like ChatGPT or Perplexity.

Strategic Implementation of Sovereign AI

At Frontier One we are working with governments around the world to implement Sovereign AI solutions customized for their national requirements. What we are seeing is that countries that move quickly to implement these solutions are able to secure access to scarce talent, and cutting-edge technology and chipsets, while slower adopters risk falling behind their regional counterparts or rivals.

To help countries move forward swiftly and clearly, we have developed a five-step program that we recommend for our global national customers:

1. Immediate Announcement: Countries must act swiftly, as announcing an AI initiative can spark interest and attract global AI players.

2. Develop a National AI Strategy: Define clear national goals, such as economic growth, public service improvements, or enhanced security, and outline a roadmap to achieve them.

3. Invest in Data Security Solutions: Identify where critical data will be stored and develop strong security protocols to protect it.

4. Build Digital Infrastructure: Invest in a national AI Factory (highly specialised data centres), cloud infrastructure to host AI models, and ensure data residency.

5. Develop Talent and Research: Cultivate local talent and fund AI research through universities, R&D centers, and technical training programs.

This pragmatic, results-driven framework guides governments in their AI strategy, drawing from our team’s extensive experience in AI across global markets. We must emphasize, that as the AI race intensifies, and the geopolitical landscape rapidly changes, integrating AI into national infrastructure is no longer optional—it’s the essential utility for prosperity and security. Goldman and Sachs predicts that AI will lift global GDP by 7% over the next decade, and that’s a conservative prediction with PWC estimating that AI could contribute up to $15.7 trillion to the global economy by 2030. However, in summary, this advancement must not come at the cost of data privacy and security. By adopting a strategic approach to Sovereign AI that prioritizes both innovation and protection, nations can harness the full potential of AI while safeguarding their most valuable assets: their people and their data.

Cement exports from the south region finally ramp up again

The bank’s annual financial results showed growth amidst a tough macroeconomic environment, and ambitious expansion plans

FProfit Report

or most of the past decade the centre of gravity in Pakistan’s cement business lay solidly in the north. Punjab and Khyber-Pakhtunkhwa supplied the lion’s share of domestic demand, while whatever trickle of exports the country managed usually slipped across land borders into Afghanistan. Karachi-based plants were the industry’s junior partners – handy for coastal clinker purchases, but rarely trend-setters, a fall from grace from the Musharraf era heyday when they were exporters helping build out the construction boom in the Middle East during that period.

That hierarchy has flipped back. Over the first nine months of the current fiscal year (9MFY25) Pakistan shipped 6.5 million tonnes of cement and clinker abroad, up 28% year-on-year. Southern plants – essentially the Karachi–Thatta strip plus a clutch of facilities around Hub in Lasbela – were responsible for

5.4 million tonnes, a 33% surge that sprinted far ahead of anything produced inland. Exports now make up 54% of all sales booked by the southern cluster, vs. a ten-year average of just 34%.

In other words, the south no longer supplies the north; it supplies the world. And in a year when domestic cement offtake is stuck in the doldrums – government development spending remains frozen and private real-estate projects ration cash – foreign buyers are underwriting local profits.

What triggered the export renaissance?

A new research report from Arif Habib Ltd (AHL), released to clients on 22 April 2025, offers a neat three-part explanation: subsidy realignment, supply disruption and the mild return of a war-damaged market. The cocktail has created a rare pricing window; Karachi’s kiln lines are running harder, and freight brokers on Chundrigar Road are fielding more enquiries than at any time since the 2007 Gulf construction boom.

The first ingredient in AHL’s narrative

is the disappearance of export rebates in competing supply hubs. Several Middle-Eastern and Asian economies had been reimbursing producers for freight or offering per-tonne cash incentives to push surplus cement into Africa. Those programmes quietly expired in late2024. Without the subsidies, ex-factory prices in those countries snapped back toward global parity. Pakistani clinker – produced in plants already running on low-cost local coal and hooked to Karachi’s efficient bulk-handling terminals – suddenly looked cheap again.

North Africa added a second tail-wind. Algeria, which had flooded West-African markets with subsidised bagged cement as recently as 2022, now faces internal shortages after maintenance overruns sidelined two state-owned lines near Oran. AHL calculates that every one-percentage-point swing in sub-Saharan market share translates into 100–120 thousand additional tonnes a quarter for Pakistan’s south. The pivot is already visible in port statistics: stevedores at Port Qasim handled a record 39 Panamax-class cement

loaders in March, up from just 16 a year earlier.

The third piece is a modest revival in Syrian reconstruction. While most Western sanctions remain, limited humanitarian exemptions for cement have opened a channel for Pakistani bagged product via Lebanese intermediaries. Volumes are nowhere near Africa’s scale but, according to AHL, they have moved the needle at the margin, especially during slack weeks when West-African buyers are awaiting letters of credit.

With so much of the new demand funnelling through coastal ports, the biggest beneficiaries are the four manufacturers that dominate southern capacity: Lucky Cement, DG Khan’s Hub line, Power Cement and Thatta Cement. All four shipped more clinker than they sold domestically last quarter. Lucky’s Karachi works – already one of the most efficient plants in the world – reported kiln utilisation at 72% in February, versus 45% a year earlier.

Northern players are not entirely left out. Bestway and Maple Leaf have restarted dormant arrangements to truck clinker down the M-5 motorway to Karachi for onward shipment, but the freight arbitrage is thin; at current diesel prices it costs Rs2,000–2,200 per tonne simply to reach the port gates. Unless domestic demand collapses entirely, Punjab-based plants will still prioritise local bag sales.

Exporting cement from Pakistan has historically been an exercise in volume over margin. Prices quoted for West-African tenders in FY22 averaged US $34 per tonne FOB Karachi – squeezing contribution margins to low single digits after adjusting for bag cost, wharfage and sample testing. The latest fixtures compiled in AHL’s report tell a fresher story: bulk clinker is clearing at US $41–42, while bagged cement fetches US $49–50, levels unseen since 2015.

Part of the lift is pure market shortage, but currency math deserves credit. With the rupee oscillating above 300 to the US dollar, every extra greenback earned abroad drops almost rupee-for-rupee to the gross profit line.

Margin optimism must, however, be tempered by cost volatility. Pakistani proteins of kiln flame – notably Afghan and Thar coal – have been unusually stable since December, hovering around US $85 a tonne delivered plant. An unexpected spike would hit exporters first because freight rates are non-negotiable once a tender is won. Shipping itself is another wild card. The Red Sea security premium that jolted container traffic has also nudged bulk-carrier rates; a Cape-size run from Karachi to Douala now costs roughly US $28/t, up from US $23/t six months ago.

Lucky and DG Khan mitigate freight creep by loading larger Panamax vessels at scales where per-tonne costs fall by 7-8%; smaller outfits such as Thatta Cement typically charter Handysize carriers, surrendering a

chunk of margin.

While exports bloom, local dispatches remain anaemic. Government development outlays are frozen under an IMF-backed austerity plan, and private builders complain that 20-plus-percent mortgage rates have vaporised consumer demand. Yet even here the south is outperforming.

Domestic sales in the southern zone –read: Karachi, Hyderabad and lower interior Sindh – slipped only 4% in 9MFY25, compared with a bruising 18% slide in the north, AHL data show. The resilience is partly demographic (Karachi’s in-migration remains the country’s largest) and partly logistical: mega projects such as the Malir Expressway are federal-priority and thus shielded from provincial cash droughts. The mismatch further reinforces the south’s utilisation edge; when local orders do slow, plants can pivot to exports with scarcely a kiln-stop.

Export momentum is, of course, a convenient hedge against rupee weakness, and CFOs are quick to remind investors that every dollar earned abroad helps service dollar-denominated debt at home. But the currency sword cuts both ways.

Still, AHL’s base case assumes the rupee will stay within a 5% band of its current value through end-FY25, implying that forex risk is manageable.

The sector’s old nemesis is oversupply. Pakistan’s nameplate capacity sits near 90 million tonnes, while even a ‘normal’ domestic market rarely absorbs more than 50 million. Exports have absorbed the surplus for now, but capacity creep is no footnote: a 1.8-million-tonne brownfield line at Attock’s South expansion is slated for test-runs in July, and Cherat Cement’s 2.1-million-tonne Nowshera module is pencilled in for December. Analysts differ over whether these additions will cannibalise exports or simply crowd out older, less efficient kilns. What is clear is that southern plants have a structural freight advantage; an exporter in Peshawar must truck clinker 1,200 km to Port Qasim – undoable unless FOB prices skyrocket.

Arif Habib’s earnings model assigns an average **Rs25–28 per-share boost to the profit forecasts of Lucky Cement and DG Khan over the next two quarters**, driven almost entirely by seaborne sales. Power Cement is expected to turn cash-positive for the first time since FY21. In percentage terms, Thatta Cement is the most leveraged play: a one-million-tonne export award could quintuple its net income, albeit from a tiny base.

Northern producers are predicted to muddle through, cushioned by strong retail pricing (bagged cement in Punjab still commands Rs1,300 for a 50-kg sack) but hampered by lower utilisation; most will see earnings flat to slightly negative year-on-year.

Islamabad’s role has been, at best,

neutral. AHL’s report notes that **no export rebates or government freight-subsidy schemes are in place**; the uptick is purely market-driven. That insulates the boom from fiscal whim – but it also means port fees, customs documentation and shipping-agent charges remain as high as ever. There is talk of reinstating a reduced wharfage tariff for clinker, but National Tariff Commission officials hint they “do not wish to pick winners” in a politically sensitive pre-budget season.

Conversely, there is a real threat from the regulatory front: if OGRA hikes gas tariffs again in July, captive-power units could face a cost squeeze. Lucky has coal-fired CPP backup; Power and Thatta rely more on gas.

What could derail the export train? Four factors:

• Price war in the Gulf: Should Oman or Saudi Arabia reinstate freight subsidies, FOB prices could fall below Pakistani break-even.

• Freight shock: An escalation in the Red Sea security crisis would feed directly into bulk-carrier tariffs, crimping margin headroom.

• Coal spike: South African coal futures have been edging higher on weather-related supply glitches. A jump above US $120 would hurt.

• Algeria catch-up: A quick fix at SONATRACH’s Oran kilns could flood Africa with cheaper bagged cement again.

Each risk, however, offers some notice period; the sector’s nimbleness in the past three quarters suggests producers can hedge contracts or redirect cargoes if warning lights flash early enough.

The core takeaway from AHL’s dossier is not merely the 28% jump in national exports, or the south’s 54-percent sales share. It is the sector’s newfound **export elasticity**: the ability to swing clinker from Satkhirabad to Senegal in a matter of weeks, smoothing utilisation curves that once yo-yoed with every government budget cycle. That agility has bought breathing space while Pakistan’s domestic construction sector searches for its next growth catalyst.

Whether exports will remain the primary profit engine is less certain. Africa’s shortage is cyclical; Syrian reconstruction may plateau; freight volatility is a permanent companion. But the current window has allowed cash-strapped mills to deleverage, fund kiln upgrades and, crucially, prove to investors that Pakistani cement can compete on a world stage without subsidies.

For now, Karachi’s skyline of grainy grey silos – once derided as “capacity without customers” – suddenly looks like the launch-pad of Pakistan’s most quietly successful export turnaround story of the year. The kilns are hot, the ships are waiting, and the south’s cement bosses are in no hurry to close their order books. n

Are Telcos too fat to grow?

With limited growth and thinning margins, can cost optimization be the key to long-term sustainability?

By Hamza Aurangzeb

Pakistan’s telecom industry finds itself at a crossroads with mobile penetration approaching saturation and average revenue per user (ARPU) stagnating. Such traditional growth levers are running out of steam, while operational costs continue to rise. This has led to the margins of telcos being squeezed, with profitability becoming endangered. In this taxing environment, streamlining operations and reducing inefficiencies is no longer optional, but essential for survival.

Global telecom trends underscore a growing reliance on simplifying offerings, digitizing customer journeys, and adopting technologies like AI to boost productivity. These strategies could serve as a framework for Pakistani telcos to become more prolific and agile in unlocking additional value. They need to meaningfully bend their cost curve instead of just chasing elusive top-line growth, a shift that will not only protect their bottom lines but also ensure long-term relevance in a rapidly evolving digital economy.

Profit brings you a deep dive into the evolving landscape of the telcos in Pakistan, exploring the diverse range of relevant global schemes that could assist the local operators in minimizing costs and enhancing operational efficiency.

How rising costs are stalling growth for Pakistani telcos?

At the dawn of the new millennium, the telecom sector in Pakistan witnessed a spectacular growth, numerous gigantic tower structures were erected, and the adoption of mobile phones became rampant across the country. However, as the popularity of cellular services surged, the average revenue per user of telcos started to decline, while their costs kept escalating at a brisk pace for various reasons.

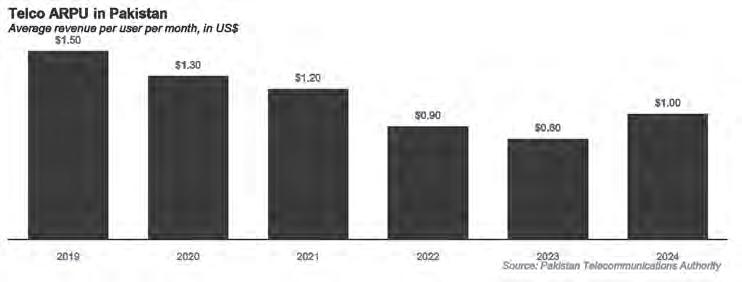

When telcos entered the Pakistani market in the early 2000s, the Average Revenue per User (ARPU) hovered around $9, but over the past two decades, it has dwindled to around $1. The introduction of high-speed

mobile broadband (3G/4G) in the country relegated the telcos to mere pipes, which connected customers to apps and OTT services that allowed them to make voice calls and send messages, cannibalizing the primary source of revenue for the telcos.

To counter the impact, telcos are transitioning towards a ServiceCo. model, where they have ventured out in diverse spheres, including streaming, fintech, business analytics, and cloud infrastructure. Although the strategy has ameliorated the telecom landscape but overall it has yielded mixed results with limited revenue growth.

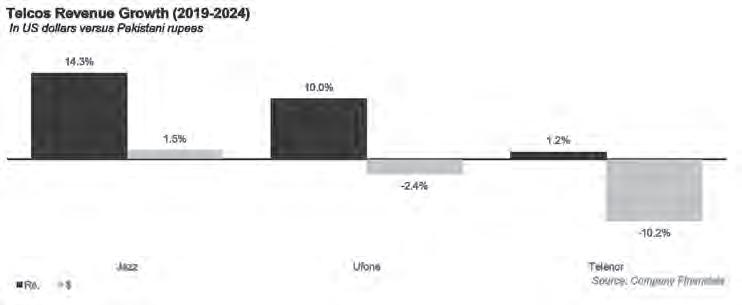

While analyzing the financials of Jazz, we find that the company has grown at a rate of 14.3% annually from 2019 to 2024 in rupee terms, while it has expanded at a sluggish rate of 1.5% in dollar terms. However, Ufone fared worse, where its topline has enlarged by 10% in rupee terms but depleted at a rate of 2.4% in greenback terms. Nevertheless, the worst out of the lot was Telenor, whose revenue witnessed a modest growth of 1.2% in rupee terms and decayed at 10.2% per annum in terms of dollars, no prizes for guessing why they were so eager to close shop in Pakistan.

The telecom industry in Pakistan is reaching maturity, where it has reached 195 million subscribers. If you add 6 million subscribers of AJK and GB, the number exceeds 200 million, taking the saturation rate above 80%. Thus, it has become abundantly clear to telcos that it will be a strenuous task to acquire more customers and produce additional revenue. Hence, the telcos have reoriented their strategy towards augmenting operational efficiency and trimming costs to enhance profitability.

But what are the factors contributing to the high costs of telcos?

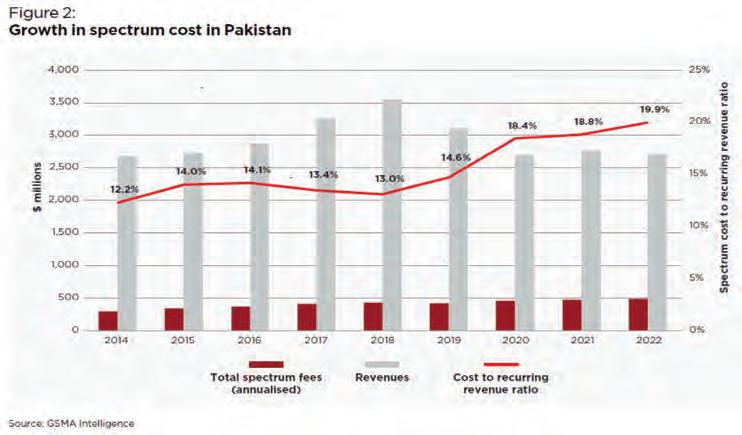

To begin with, the telecom business is a capital intensive industry, where the local telecom operators have contributed significantly in terms of capital expenditure to establish a vast network of towers, lay fibre optic infrastructure and build data centers, which reigns heavily on their financials. Apart from that, the spectrum fees for telcos are denominated in USD, contrary to global trends. Hence, the spectrum fees paid by telcos has doubled in less than a decade, increasing from 11% in 2014 to 20% in 2022. Although there are a variety of reasons for this complication, the deteriorating operator revenue per MHz of spectrum and unprecedented depreciation of the Pakistani Rupee remain primary contributors.

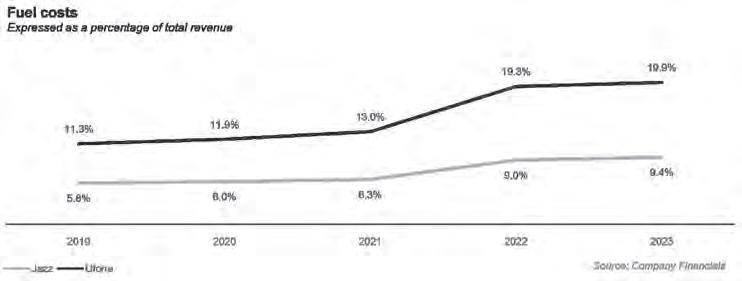

And then the energy crisis; the electricity tariff in the country has increased by more than 155% between fiscal year 2022-2024. This abrupt upswing in energy prices has affected all industries and households in the country. Its adverse impact is evident in the financials of telecom operators, where the energy costs of infrastructure as a percentage of total revenue have increased from 5.8% in 2019 to 9.4% in 2023 for Jazz, while for Ufone, it has spiked vigorously from 11.3% in 2019 to 19.9% in 2023.

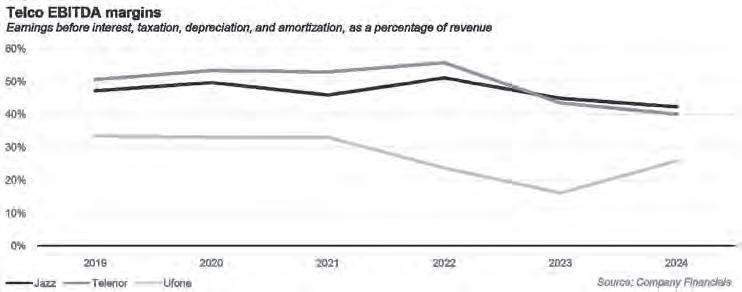

The books of telecom operators appropriately reflect this trend, where the EBITDA margins of telecom operators are declining year on year due to the rising operating costs, including fuel costs and spectrum prices. Moreover, the operating margins of telecom operators have plummeted simultaneously due to the devastating impacts of depreciation and amortization costs.

Jazz appears to be doing better than the

rest, but its EBITDA margin has declined from 47.2% in 2019 to 42.3% in 2024, while its operating margin has shrunk from 32.6% in 2019 to 26.6% in 2024. If we talk about Telenor, its EBITDA margin has contracted from 50.6% in 2019 to only 40.0% in 2024, whereas its operating margin has dropped from 22.1% in 2019 to 19.1% in 2024. While Ufone’s EBITDA margin has declined from 33.4% in 2019 to 25.8% in 2024, its operating margin has fallen further from 5.2% in 2019 to 3.9% in 2024.

There is an increasing pressure of rising costs on the telecom sector overall. Hence, they are moving towards an asset-light strategy to restrict capital expenditure along with depreciation and amortization costs. Furthermore, they are also working on improving operational efficiency and reducing operating expenses to boost profitability and ensure long-term sustainability.

Modernizing network infrastructure and field operations

Pakistan’s telecom sector has made considerable strides in coverage and connectivity but the underlying network infrastructure for technologies

like 4G still largely relies on legacy architecture. These outdated systems are heavily hardware-dependent, rigid in design, and slow to scale, making network upgrades expensive and time-consuming. Many operators continue to depend on proprietary equipment and siloed systems, which limit their ability to swiftly adapt to evolving consumer demands like highspeed data, video streaming, and cloud-based services.

To overcome these inefficiencies, Pakistan’s telecom sector needs to shift towards modern and modular network architectures. Globally, operators are moving away from rigid, hardware-centric models to software-driven designs that leverage artificial intelligence, cloud computing, and emerging technologies like 5G. These newer systems are not only more energy-efficient but also offer dynamic scalability and smarter network planning aligned with customer usage patterns. In Pakistan, Jazz has collaborated with Huawei to test cloud-native network functions, while Zong has invested in next-generation network planning in partnership with ZTE but the scale of such advanced systems remains limited.

In addition to an archaic network infrastructure, the escalating costs of maintaining cellular tower networks pose another challenge for the telcos. Tower sites that were once prized possessions for telcos have over time become a liability for them due to the steep rise in fuel costs and significant dependence on manual field operations. The traditional approach of running a tower network involves multiple challenges. Firstly, since the towers are tall structures, they consume mammoth amounts of electricity. Secondly, telecom companies often have to dispatch teams to remote tower sites for routine maintenance and fault resolution. Thirdly, legacy systems lack automation, cloud integration, and real-time monitoring, while predictive maintenance and

remote troubleshooting remain underdeveloped. This translates to high operational costs and delayed issue response times for telcos.

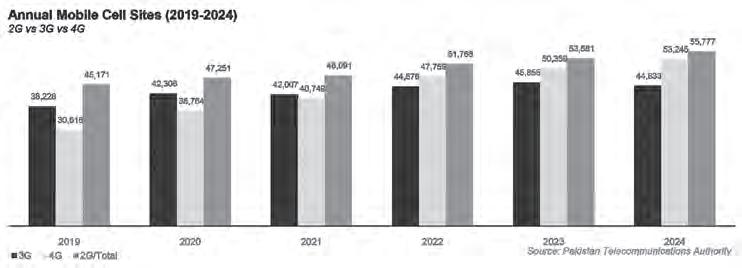

As a result, tower sharing has emerged as a viable option. Jazz, for instance, has initiated the sale of their tower infrastructure to Engro and plans to utilize it through a long-term lease, while other companies have also commenced tower sharing and powering the tower infrastructure through solar energy to increase efficiency and reduce costs. Moreover, if the merger of Ufone and Telenor is approved, they intend to optimize their tower infrastructure by eliminating duplicate sites. Telcos are channelizing their efforts to reduce the burden of cell sites, which is manifested in the modest growth of 4.3% of mobile cell sites overall since 2019. Furthermore, introducing AI-powered tools, predictive maintenance, and self-healing network technologies. could further assist in augmenting the efficiency of tower networks. These solutions can detect and resolve faults proactively, often without the need of human intervention.

Enabling the transformation of the IT architecture

The evolution of telecom networks from legacy infrastructure to modular, software-defined, and cloud-native architecture is not just a technical upgrade — it lays the groundwork for a broader transformation across the entire IT landscape of telecom operators. Traditionally, networks in Pakistan and elsewhere were hardware-heavy, rigid, and fragmented, making IT systems equally inflexible and slow to adapt to changing business needs. However, as telecom companies embrace modular network architecture, they can unlock the potential to modernize their IT infrastructure in parallel. Modern networks that are designed with scalability and software interoperability in mind can seamlessly integrate with cloudbased IT environments. This allows telecom operators to transition from monolithic and proprietary IT systems towards public cloud

platforms that support open-source and lowcode development tools such as Apache Kafka and Microsoft PowerApps. These platforms bring agility, making it possible to develop internal applications faster, streamline operations, and reduce vendor lock-in. For instance, real-time data from cloud-enabled network components can be fed directly into unified analytics platforms, replacing previously fragmented data systems and enabling more insightful, data-driven decision-making — a shift that can significantly rationalize costs for telcos.

Moreover, modern networks enable centralized management of infrastructure, which aligns well with IT architecture that leverages multicloud strategies. This means that both network and IT resources can be scaled up or down depending on demand, ensuring cost-efficiency, while maintaining high performance. In Pakistan, where most telecom operators are still reliant on legacy IT setups with outsourced support models, the shift towards automation and embedded security is becoming increasingly crucial.

We have examples like PTCL’s investment in cloud and enterprise services through partnerships with companies like IBM and Red Hat, which reflects its ambition to build a more secure and agile IT environment, whereas Zong in partnership with Huawei, has implemented cloud infrastructure and big data platforms to automate operations, centralize analytics, and strengthen cybersecurity. Additionally, telecom operators can proactively manage system performance, enhance security,

and respond to customer needs in real time through the integration of AI-powered tools within both network and IT domains.

This convergence also simplifies cross-functional collaboration. For example, with a unified cloud ecosystem, customer service platforms, billing systems, and network diagnostics tools, all can communicate effortlessly, reducing operational delays and improving user experience. Hence, telecom companies, which have begun investing in modular network upgrades and 5G trials, are well-positioned to advance their IT ecosystems in tandem, which will lead to major cost savings for them in the future.

The modernization of network architecture is a necessary first step that unlocks the flexibility, scalability, and efficiency required to transform IT systems. As these changes take hold, telecom companies can become leaner, more secure, and digitally mature, ready to meet the evolving demands of the hyper-personalized preferences of the customer base.

Reimagining customer engagement with AI

Operators are increasingly pivoting to digital-first, customer-centric models that align with global trends. The rapidly growing mobile customer base of 200 million, majority of which have become accustomed to digital interactions, demands for a more elegant and hyperpersonalized engagement.

The adoption of AI powered digital platforms among telecom operators has accelerated in recent years to engage customers and recommend service bundles and promotional offers based on their preferences. It has reduced the telcos’ dependence on sales development representatives on the ground. They run automated hyperpersonalized marketing campaigns via SMS, push notifications, and social media, backed by AI driven segmentation and machine learning algorithms. This approach not only reduces operational costs but also accelerates customer acquisition.

All telecom firms in Pakistan are utilizing AI-based advanced tools to gradually move away from standard bundles to more customizable offerings tailored to diverse consumer needs. The operators have launched multiple apps and schemes, which leverage AI to decipher customer preferences and allow users to curate their own packages for voice, data, or hybrid—through dynamic pricing models.

Telecom operators are embedding AI agents into their networks and equipment, which can remotely spot customers’ needs for software updates and renewal of offers, automatically notify subscribers via app or SMS, and even push remote fixes. This proactive approach means fewer customers need to visit service centers or wait on the helpline for routine technical support.

At the same time, innovative chatbots have begun handling a large share of inquiries, balance inquiry, plan adjustments, and SIM replacements right within mobile apps or web portals. AI-powered chatbots are rapidly becoming the industry standard, particularly for customer service in Pakistan’s telecom sector. Jazz recently signed an MoU with NUST and NITB to develop Pakistan’s first indigenous Large Language Models (LLMs) for Urdu, Punjabi, and Pahsto, which will further empower AI chatbots and abridge the digital divide in the country through granting access to technology to the masses in their local languages.

As per current trends, it appears likely that these chatbots will evolve into digital cyborgs in the coming years, where chatbots will embrace human avatars, possibly famous personalities and characters. Imagine if Saturo Gojo from manga Jujutsu Kaisen or Captain Jack Sparrow from Pirates of the Caribbean could resolve customer issues in their own eccentric styles, you bet Gen-Z would throw their money just to witness them in action. Moreover, it would make the whole customer engagement a lot more pleasant instead of a fiery exchange.

However, when a complex issue does arise, human agents could step in equipped with advanced guidance tools that analyze each customer’s usage history and sentiment in real time. This hybrid model would allocate

human expertise where it’s most valuable, while routine interactions remain fully digital.

Predictive analytics adds another layer of personalization by flagging subscribers who show signs of dissatisfaction or churn risk. It allows operators to deliver tailored retention offers and targeted support directly through preferred digital channels rather than waiting for customers to dial in or walk into a store. Collectively, these AI enabled strategies streamline support workflows, reduce overhead from retail outlets and call centers, and provide a more cultivated and engaging experience that aligns with today’s digital first customer mindset.

Consolidating and rationalizing

Telco operations

For telcos, competition is intense and margins remain under pressure; operational efficiency serves as a key lever for sustainable growth. While network modernization and customer experience transformation are the cornerstones of technological innovation, local telecom companies are now beginning to focus on streamlining internal operations as well to boost productivity and lower costs. However, these companies still lag behind global peers who have already restructured their internal functions significantly. Pakistani telcos now stand at an inflection point where both basic and advanced optimization strategies can deliver substantial gains in operational efficiency. One important step forward is the

adoption of modern AI systems in back-office operations, particularly for automating repetitive tasks such as invoice processing, data entry, and customer case routing. AI-powered tools can help reduce turnaround times and administrative overhead, unlocking significant cost savings, where automating routine work can allow telcos to redirect employee efforts towards high-value activities such as analytics, strategic planning, and product innovation.

Moreover, the digitization of company-wide systems, especially through modernized enterprise resource planning (ERP) and human resource (HR) platforms, can reduce reliance on manual processes, improve transparency, and enable faster decision-making. Furthermore, the consolidation of fragmented support functions across departments or business units can further enhance this impact.

For instance, the two telecom operators, Ufone and Telenor, are undergoing a merger. Currently, they have separate HR teams managing recruitment and payroll for their respective corporations. However, after the merger they are likely to integrate these functions into a centralized HR shared services model, which will allow the merged company to eliminate redundancies, standardize the employee experience, and leverage automation at scale. Similarly, it could streamline procurement by shifting to a centralized digital procurement center that forecasts supply needs, manages vendor contracts, and ensures consistent purchasing decisions across departments.

Such enterprise-wide restructuring not only simplifies workflows and reduces duplication of effort but also ensures consistent execution across the organization. This frees up operational bandwidth, making it possible for telecom operators to allocate resources towards strategic growth areas such as service innovation, curated customer experience, and workforce upskilling. As Pakistan’s telecom players embrace this dual approach—powered by AI automation and centralized support— they can unlock new levels of efficiency and agility required to compete in a fast-evolving digital landscape. n

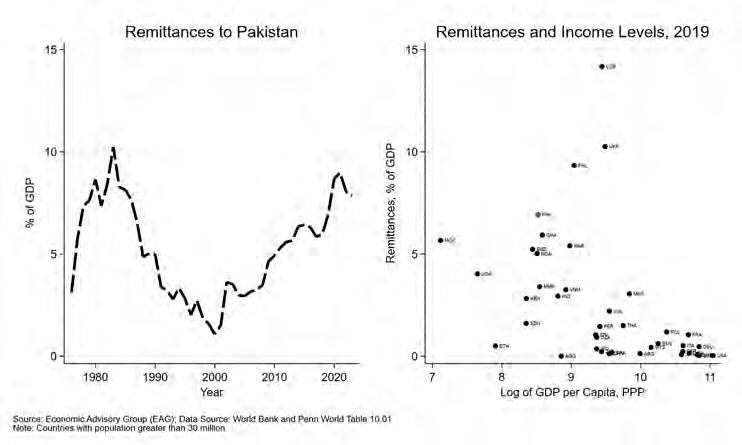

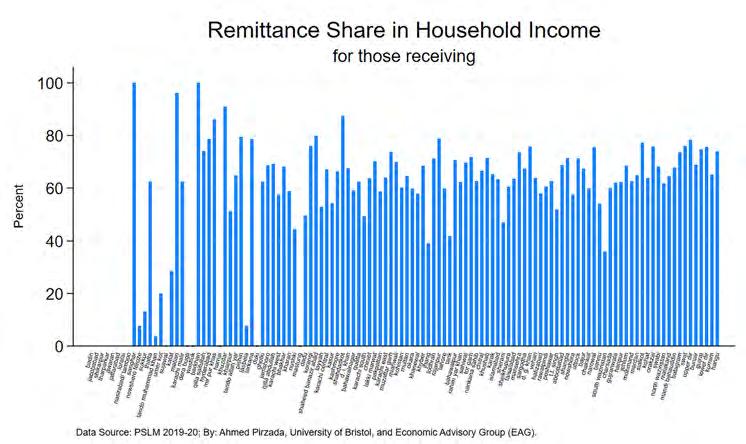

Migration, money and the making of Pakistan’s remittance economy

How economic downturn is fueling both emigration from Pakistan and the subsequent inflow of remittances

By Nisma Riaz

For decades, remittances have acted as a financial stabiliser for Pakistan, supporting household consumption, cushioning the current account, and providing relief during crises. But behind the record-breaking inflows lies a deeper story: the accelerating pace of emigration and the structural vulnerabilities driving it.

Far from being a passive byproduct of globalisation, Pakistan’s remittance economy reflects a persistent pattern of outward migration, shaped by economic stagnation, political instability, and security concerns. As more Pakistanis pursue opportunities overseas, the remittances they send are supporting not just their families, but also sustaining the state’s financial health. In this way, remittances are both a symptom of crisis and a coping mechanism.

This assertion was proven by a March 2025 surge, when remittances hit a record $4.1 billion, a 37% year-on-year jump. According to a recent report by JS Global, over the first nine months of FY2025, total inflows reached $28 billion, up 33% from last year. These transfers are now central to rebuilding foreign exchange reserves, which the State Bank expects to reach $14 billion by June, aided by anticipated IMF support.

Keeping in mind seasonal factors like Ramadan and Eid played a role, the real driver appears to be a sharp rise in emigration, especially to Saudi Arabia, which accounted for 70% of all outbound labor in early 2025. Meanwhile, the UAE’s share dropped to 4%, down from a historical average of 35%, amid tightening visa rules. Still, remittance flows from both countries remain robust, with Saudi and UAE contributions now making up 46% of the total.

This article places remittance trends under a microscope to highlight the growing interdependence between migration and remittances, and what it tells about Pakistan’s social and economic trajectory.

Remittance trends in the last two decades

In times of crisis, whether global or domestic,, Pakistan’s economy has consistently leaned on one dependable pillar: remittances. These financial lifelines from abroad reflect not only economic necessity but a deep sense of familial duty. “Remittances act as a lifeline during economic instability,” noted Mustafa Pasha, former executive director at Lakson Investments. This pattern has repeated across several moments of disruption over the last two decades.

During the 2007–08 global financial crisis, triggered by the U.S. housing market collapse, remittance inflows to Pakistan defied expectations. Despite job losses and global uncertainty, overseas Pakistanis sent more money home, with inflows rising from $6.45 billion in FY 2008 to $7.81 billion in FY 2009, a 21% increase.

According to Pasha, “Remittances seemed immune to the global financial crisis,” growing from around $5 billion to $8 billion despite domestic turmoil, a 20% currency depreciation, and soaring interest rates. At the same time, corporate defaults surged as mutual funds, heavily invested in corporate debt, collapsed, sparking the birth of money market funds.

During the height of terrorism and internal displacement in Pakistan between 2011 and 2014, remittances displayed remarkable resilience. As violence surged and hundreds of thousands were uprooted, inflows climbed significantly, rising from $11.2 billion in FY 2011 to $13.18 billion in FY 2012, and nearly doubling to $17 billion by 2014. This surge was aided by the Pakistan Remittances Initiative, a policy effort aimed at promoting formal transfer channels through banking partnerships and incentives like remittance cards. According to Mustafa Pasha, “That likely converted a lot of unofficial flows into official ones,” reducing reliance on informal networks like hawala and bolstering foreign exchange reserves.

“But the ongoing economic crisis that began in 2022 tells a different story. While individual months have posted record inflows, like $4.1 billion in March 2025, overall growth has stalled. Remittances have plateaued,” Pasha noted, rising only modestly from $30 billion to $36–37 billion, far below historical trends of 15–20% annual growth.

Yet the drivers remain consistent. The ongoing economic crisis from 2023 to 2025, defined by inflation, unemployment, and a weakening rupee, has pushed more Pakistanis

to seek work abroad. Meanwhile, those already overseas are sending more money to protect their families from rising living costs.

Dr. Ahmed Jamal Pirzada, Senior Lecturer in Economics at the University of Bristol, observed, “Since COVID-19, there’s been a sharp rise in emigration from Pakistan, with around 700,000 to 800,000 people leaving annually over the past 2–3 years.” He emphasized that most new immigrants send substantial remittances early on, driven by obligations to support family back home. “Notably, around 40–50% of these emigrants are considered ‘skilled’ in official data, meaning they possess vocational or professional capabilities, even if not formally educated.” Skilled workers tend to earn more, thus having greater remittance potential.

Migration data also underrepresents undocumented departures, which have risen amid tighter global visa regimes. “There’s a whole shadow migration happening,” Pasha pointed out, suggesting that the true scale of outflows, and their remittance potential, may be larger than official figures suggest. “This crisis is different. Remittances aren’t responding the way they used to.”

On the other hand, peaking remittances in March 2025, can be attributed to a few other factors as well.

Religious occasions such as Ramadan and Eid regularly trigger seasonal spikes. Remittances hit $3.16 billion in June 2024 during Eid-ulAzha, a 44% year-on-year increase, while March 2025 saw a record $4.1 billion, up 37.3% from the previous year. Informal channels like hundi/ hawala often gain traction during exchange rate volatility due to better rates and speed, but recent crackdowns and reduced gaps between official and market rates have boosted formal flows.

Still, currency depreciation presents a double-edged sword. While it increases the rupee value of remittances, it can also fuel instability. Past episodes in 1998, 2008–09, 2018–19, and 2022–23 often saw stagnation or