21 Gandhara’s turn towards China begins to bear fruit

23 Mutual funds crowd into energy, cements and a handful of banks

25 Gatron merger attempt falls through

27 Is Pakistan’s freelance economy being held hostage?

30 Suzuki might have delisted from the PSX, but the rubble hasn’t quite cleared

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

The “Too Big For Pakistan” Problem

Four of Pakistan’s largest conglomerates find themselves in the awkward position of having too much cash, and not enough places to deploy it in the domestic economy. Outbound FDI should be made easier

By Farooq Tirmizi

In 2008, the year that we now know was likely the peak of this current bout of globalization, the rise of Corporate India was simply unmistakable. Not only was it the darling of the investing world, but Indian companies were seen as finally having arrived on the global stage, with perhaps no acquisition being more prominent than the acquisition of Jaguar and Land Rover – the iconic British automobile brands – by Tata Motors, the Indian automobile manufacturer best known for producing some of the world’s cheapest cars.

India’s economic heft was not just symbolized by how much foreign direct investment it could attract, or how much it could export, but also by what its companies had the capability of buying abroad. In other words, India’s strength was measured not just by how much money it could attract into India, but how much it had the capability of spending outside India.

Needless to say, this is a game that we in Pakistan know we cannot play. Pakistan does not have a local carmaker, let alone one that could buy a global rival. But we do, somewhat surprisingly, have companies that have clearly outgrown their ability to profitably invest in the Pakistani economy.

They are “too big for Pakistan”.

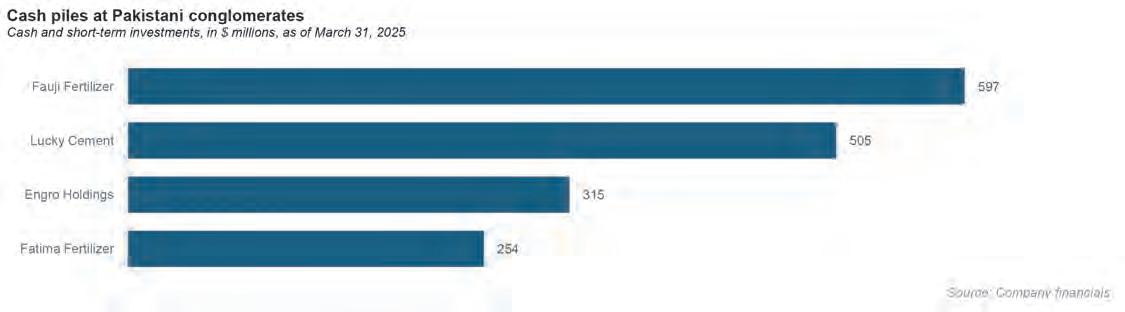

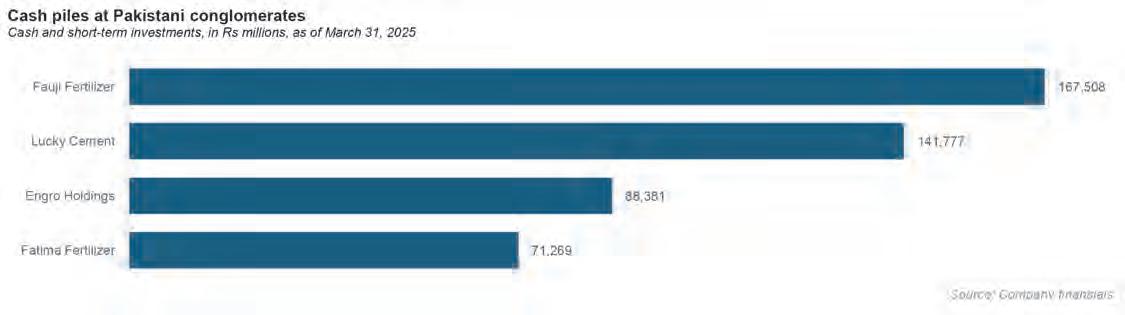

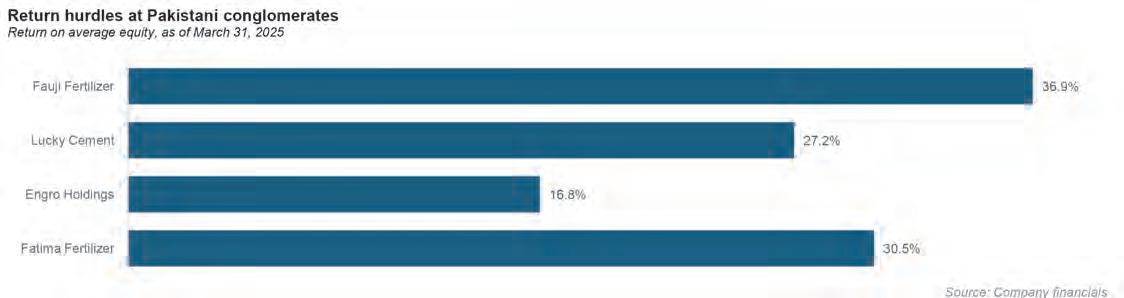

Four conglomerate holding companies fit this bill in Pakistan, in our view: the Fauji Fertilizer Company, Lucky Cement, Engro Holdings, and Fatima Fertilizer.

All four of these currently have more than $250 million in cash on their consolidated balance sheets right now, two of them currently have more than $500 million, and all four have had more than $500 million in cash on their balance sheet at least at some point over the past five years.

In this story, we will talk about the most cash-rich companies in Pakistan and why they are distinct from other companies that may even have higher profit margins, why we call them too big for Pakistan, and what, if anything, can be done about it. We will also address the very obvious fact as to why three of the four are fertilizer companies.

What is too big for Pakistan?

How did we arrive at this list? We looked at the cash balances on Pakistan’s largest non-financial conglomerate holding companies’ consolidated balance sheets, and looked for unusually large sums in absolute terms, specifically looking for companies that either currently have, or have recently had, more than $500 million in cash or short-term investments. The list is not long, but it is significant, as we explain below.

We excluded financial services companies because the nature of cash in financial institutions is very different from that in non-financial companies. Habib Bank, for instance, has a lot of cash, but most of that is needed to pay out withdrawal requests from its depositors and is not ordinarily available to the bank to begin undertaking large capital expenditure projects.

We also excluded government-owned or government-backed entities, since such entities often can rely on government support which renders their cash pile not solely something generated purely through economic surplus of productive economic output. Also, their capital expenditure capacity is often influenced by or can be supplemented with government funds.

Why is the $500 million number signif-

icant? There is not a particularly scientific explanation for this, except to note that, if you have $500 million in cash to deploy, you can probably raise at least as much in borrowed funds to finance a $1 billion project with a capital structure that – for most large scale ventures – would be considered conservative. And $1 billion starts to open up all sorts of interesting opportunities in most parts of the world, including Pakistan.

Within Pakistan, based on our possibly incomplete list, there have likely been fewer than 10 private sector investment projects that have cost $1 billion in capital expenditures or more, which suggests that it is not easy to deploy $1 billion into the Pakistani economy in obvious, commercially viable ventures. Not impossible, obviously. But not easy.

This is why this is our benchmark for too big for Pakistan: we cannot identify a single one of the handful of private sector investment projects over $1 billion – the 2010 Engro Fertilizers’ plant called Enven, the Thar coal mines and power plants (if considered a single project), the new Byco refinery, and the soon-to-be-initiated Reko Diq mines – that did not involve either a joint venture with a government entity, or at the very least some heavy government subsidies or guarantees.

If the size of transaction results in fewer than 10 projects in the country’s history – and all of them requiring massive government assistance – then perhaps it is accurate to deem that size of economic activity as simply being too big for the country.

This discussion also brings us to our next observation: why so much of this surplus of cash is stored on the books of fertilizer companies.

Why are these the first “Too Big for Pakistan” companies?

The most important question to address here is why three out of these four are fertilizer manufacturers. There are primarily two reasons why this is the

case. The first is that the government has several policies that make fertilizer manufacturing in Pakistan unusually profitable and the second is the fact that the industry has some specific dynamics that mean that expansion within fertilizer manufacturing domestically for such companies is very difficult.

Why is fertilizer manufacturing so profitable in Pakistan? Because the government provide the biggest raw material needed to manufacture fertilizer – natural gas – for an exceptionally low price, which s $0.75 per million British thermal units (mmBtu), the same price at which hydrocarbon-rich Saudi Arabia provides natural gas from Saudi Aramco to Sabic. By rights, Pakistan cannot afford to supply natural gas to its fertilizer companies at this price, and yet we chose to do so anyway.

The government has a rationale for doing so: in a country as dependent and full of poor farmers, being able to provide fertilizer cheaper than global markets creates an implicit subsidy for farmers that likely boosts their income.

All of this has the effect of significantly boosting the profit margins of the domestic fertilizer industry, which is able generate high volumes of cash owing to its low cost basis.

Then we get into why fertilizer manufacturers uniquely struggle to deploy those profits into expanding within Pakistan. Well, firstly, this is a relatively new phenomenon. Prior to 2006, Pakistan relied heavily on imports to meet much of its fertilizer needs, despite having a significant domestic industry. So the country’s fertilizer manufacturers did, in fact, expand their core business lines, and Engro’s investment into its urea manufacturing expansion is, as we noted earlier, one of the single largest capital expenditure projects in the country’s history.

But urea is probably the only type of fertilizer that can be easily manufactured domestically. The three main elements that fertilizers seek to deliver are nitrogen, phosphorus, and potassium. The nitrogen in urea comes from the air, but the remaining two require mineral deposits which Pakistan does not possess in meaningful capacity, which makes it difficult to expand into manufacturing those domestically.

In other words, those high cash profits have likely reached the limit of how much they can finance domestic expansion inside Pakistan.

The fourth company – and the only one that is not a fertilizer manufacturer – is Lucky Cement. While cement manufacturing in Pakistan does not get much by way of government subsidies, and while it is a mostly competitive business in the country, Lucky Cement is at this point a conglomerate holding company that includes two divisions – Lucky Motors and its mobile assembly business – that both rely on heavy government protection in order to be economically viable.

Again, you may call this rent seeking, or you may call it industrial policy (it is most certainly not laissez-faire economics), but the government has a clear policy agenda for giving these protections. In the case of the automobile policy, the goal was clearly to break the oligopoly of the Big Three Japanese car assemblers in Pakistan which had been running a sclerotic industry reliant still on protection from imports while delivering an inferior product to Pakistani consumers with poor service quality.

One could argue that the experience of buying a car in Pakistan has significantly improved over the past five years, in no small part because Lucky Motors’ partnership with Kia, and Nishat Motors’ partnership with Hyundai, have introduced significant competition and force the legacy players to start improving product and service quality in order to stay competitive.

And in the case of mobile assembly, this is an industry where the payoff can sometimes take decades to materialize, but the fact that Pakistan can now assemble – and may soon begin the manufacturing of parts – for some of the most complex electronics ever conceived, is a capabilities enhancement for the economy that is worth pursuing in its own right.

In short, all four rely on government policy to create profit levels that would otherwise not exist, and have piled a cash pile so high, they are struggling to devise viable plans to suitably deploy the cash into productive businesses.

The dalliance with foreign investment

All four of these companies either currently have – or have previously very seriously explored – investment options outside Pakistan, long before their cash piles got this big.

In the case of Engro, as soon as they had completed and began commercial operations at the Enven plant in Dharki, they began talking about the next big expansion as being another $1 billion bet in North Africa, the region of the world known to have the largest deposits of phosphates.

“We want to go to invest where the rock is. The world’s largest phosphate deposits are all in north Africa. We are looking at Morocco, Algeria and Tunisia …We are looking at all three right now,” said Asad Umar, then the Engro CEO, and later federal finance minister, in an interview with the Financial Times, published in January 2010.

Perhaps it should not be surprising that Engro had those grand ambitions at that precise moment in time. It was completing one of the most technically ambitious projects of its kind – the largest single-train urea manufacturing facility in the world – and had high hopes of how much cash that venture would soon generate. It had also started gaining traction in its Engro Foods venture.

It became the first private sector Pakistani company to hire the global management consulting giant McKinsey for a project in Pakistan (to help it create a more efficient governance structure), and one imagines Husain Dawood (the leading shareholder and board chairman of Engro at the time) and Asad Umar looking at those headlines of Indian companies making waves in the global arena and wondering if there was something they could do to put Pakistan on the map

The North Africa project for Engro ended up going nowhere, particularly after Engro spent effectively the next three years begging the government to honour its commitment to supply 100 million cubic feet per day (mmcfd)

of natural gas to the new plant at Dharki.

Not one to be left behind, Fatima Fertilizers announced a similar North Africa ambition in 2012, though that also did not go anywhere. Fatima then did something rather bold, which was to begin a pursuit of a fertilizer plant in the United States, relying on the availability of some concessionary financing facilities made available by the US federal government for investment in specific disaster-hit states. Fatima spent a considerable amount of time and resources trying to develop a $2.6 billion fertilizer plant in southern Indiana, through a venture called the Midwest Fertilizer Company.

As of this year, however, the venture does not appear to have secured enough financing, and has not yet broken ground.

Both of these ventures were possibly at least partially inspired by Fauji Fertilizers’ joint venture in Morocco called Pakistan Maroc Phosphore S.A. (PMP), which is a phosphate mining company based in Morocco. Fauji invested $250 million in 2004 into that venture and currently owns a consolidated 37.5% of that mine. It is the only significant foreign investment by the Fauji group outside Pakistan.

Lucky Cement, meanwhile, has invested in cement manufacturing facilities in both Iraq and the Democratic Republic of the Congo.

Lucky Cement invested $230 million in its joint venture cement plant in the Congo, the Nyumba Ya Akiba S.A. And in Iraq, Lucky has developed two production facilities, the Al-Mabrooka Cement Company and Najmat Al-Samawah. The company has invested approximately Rs12.2 billion over the course of a decade in all of these projects combined.

Why more foreign investment may be needed

All four of these companies have invested considerable time and energy in pursuing foreign investment projects, and at least Lucky

Cement has been able to successfully deploy some capital outside the country, albeit in very small increments and most of the money moving during eras when Ishaq Dar was not a federal cabinet member. (Mr Dar’s obsession with controlling the precise exchange rate of the rupee does not lend itself well to requests to allow companies to invest substantial proportions of their cash abroad).

Given the size of these companies’ profits and cash hoards, three questions arise:

1. Why can these companies not invest in profitable ventures in Pakistan at that scale?

2. Why must all of the money be invested in a single venture rather than several smaller ones, if a scale venture is not available?

3. Why must these companies invest the money at all? Could they not simply pay it out as dividends to their shareholders and let those shareholders figure out where to invest the money instead?

Let us start with the first question: why can these companies not find large ventures within Pakistan in which they can invest?

There are two components to the answer to this question. The first is the risk-adjusted return requirements of these companies and their shareholders, and the second is the nature of what is available to invest in within Pakistan.

On the first component, these are some of the largest, most stable, and most profitable companies in Pakistan, which means that their investors expect relatively stable cash flows. That means that, while there are a considerable number of ventures into which they could deploy capital, ones where there is a proven track record of returns, or otherwise reasonable certainty of cash flows, do not quite exist.

In other words, many of the kind of ventures that could absorb this kind of cash flow have never been done before in Pakistan: things like industrializing the supply chain of the country, solar panel manufacturing, etc. They could potentially be quite lucrative, but the uncertainty is too high for the relatively more conservative shareholders of these major companies who expect more predictable cash

flows.

These companies earn relatively higher rates of return on equity capital invested in business lines that are quite stable. To go into ventures that would have greater uncertainty would require significantly higher hurdle rates, which would make it very difficult for them to justify risking their shareholders’ capital.

The second is the nature of investing in Pakistan itself: since Pakistan’s infrastructure is relatively under developed, one cannot simply decide to place a gigantic factory or warehouse in a random part of the country. Deploying large amounts of money involve coordination with the government on either developing the infrastructure in that place to catch up to what the company needs, or else at least defraying the cost of it through subsidies or tax breaks to make the project feasible.

You can run a small or even a medium-sized business in Pakistan with minimal government intervention. You absolutely cannot run a large one without help or at least acquiescence from the government.

And despite all the screeches of elite capture, it is not actually easy to get the government of Pakistan to move with any kind of speed, which means that one can only pursue projects that have very high rates of return and stability of return profile – again, similar to the constraints placed by the previous factor.

This then begs the question: why not invest in several smaller projects instead of one big one? To a certain extent, this has been Engro, Lucky, and Fauji’s approach already. They have invested in several smaller business lines that are somewhat tangentially related to their core business lines, and sometimes not related at all, but pursued simply because they would be able to absorb the surplus capital available and to do so profitably.

The problem with this approach is that it divides the attention of management across disparate business lines, which gets progressively harder to maintain as each business line scales. Human focus – particularly strategic focus – is the scarcest of all resources, and

companies that are focused on a narrow set of priorities will likely be able to grow more in those business lines than those who have a more diversified approach.

This brings us to the last question: why both investing it at all? Why not give the money to shareholders through dividends and let them decide where to invest it?

This is a reasonable approach, and Fauji and Engro in particular have been adopting it, but there are two problems with this: first, it is the job of the CEO and board to continue looking for profitable ventures in which to deploy capital, so simply paying out dividends from a legacy business is an abdication of responsibility, doubly so in a developing country where there is a lot that still needs to be built.

And secondly, and perhaps most importantly, these companies have concentrated shareholding patterns, which means the dividends ultimately flow to large shareholders who are then stuck with the same problem: where to invest next? You simply move the problem a little further down the chain of ownership, but you do not actually get rid of it.

Let the money fly

Ultimately, the government of Pakistan needs to let Pakistani companies invest abroad, buying up both brand names, and building up expertise that can then be brought back home. The dividends – both literal and figurative – that this kind of outflow will bring, will more than make up for any short-term hit to the current account deficit.

For their parts, these companies should take advantage of the relatively benign current account environment right now, and present plans for outbound foreign investment to the government while they might be able to move money abroad without significant impact on the exchange rate. These windows of opportunity open for only short periods of time, and the handful of companies that are in a position to even consider such options should take advantage of them. n

Backed by Yango, Pakistan’s Trukkr raises close to $10mn to fuel freight tech growth

Trukkr has kept its head down and stayed away from media attention. Based on an exclusive interview, we look at how the freight tech startup has grown and where their future is

By Taimoor Hassan

In the Pakistani tech ecosystem marked by growing investor caution and lack of enthusiasm, one startup is literally keeping the wheels going. Karachi-based B2B logistics and fintech company Trukkr has raised close to $10 million in a mix of equity and debt, signaling both investor confidence and the startup’s endurance in digitising freight logistics in Pakistan.

The funding round included participation from Yango Group, the global logistics and mobility player operating in over 30 countries. Yango invested through its $20 million venture capital arm Yango Ventures. The rest of the round includes contributions from private investors, including Swiss backers. The company has chosen to keep the identity of investors in the round confidential. The company didn’t want to announce their fundraise. In fact, it took quite a lot of convincing to get them to agree. For a startup that prefers steering clear of headlines, Trukkr’s story is one of deliberate growth, strategic prudence, and business fundamentals over buzzwords. While much of the local startup ecosystem has been driven by a blitz of marketing, Trukkr’s approach has been to build quietly and scale steadily.

In an exclusive conversation, the founder emphasized their focus on operating a real business rather than chasing valuations or vanity metrics. “We’ve always been about building a sustainable company. We aren’t here for a two-year run. Logistics is a long game especially in Pakistan,” he said.

With Pakistan’s trucking freight logistics sector historically deeply fragmented, Trukkr launched with a Transport Manage-

ment System (TMS) which enables shippers to seamlessly find trucks, and truckers to find loads conveniently and digitally. On top of it, they embedded financial services which provide working capital loans and payments support for truckers.

Since its creation in 2019, Trukkr says it has onboarded roughly 30,000 truckers that use Trukkr platform to pick up goods from various manufactures and deliver them to dealers and distributors. In March 2023, Trukkr introduced fintech services for truck operators in Pakistan. As things stand in freight tech, Trukkr has become the frontrunner in this space.

The world of trucking fintech

For years, few in the startup or financial services world imagined that truckers, often seen as blue-collar workers rather than financial customers, could be among the most underserved but credit worthy

Pakistan’s logistics sector is full of potential, and Trukkr is helping move it forward by giving operators the financial tools they need to scale and succeed

Daniil Shuleyko, CEO of Yango Group

users of financial services.

In mature markets like the US, small freight operators regularly use credit to manage their working capital, especially due to long payment cycles from shippers. In addition, credit is used to get fuel advances. Truckers get access to credit lines or cards specifically for fuel, with repayments scheduled post delivery of merchandise. Truckers keep their wheels going even when their payments are stuck with shippers due to long cycles.

Credit is used for equipment leasing such as for trailers and other equipment used for loading and unloading of cargo. Because of long payment cycles, truckers can use invoice factoring services from financial services institutions where truckers get paid for their invoices by financial intermediaries. Then credit is used for maintenance of vehicles.

Trukkr’s fintech arm can offer similar products to cover immediate fuel expenses to keep trucks moving, for managing payments required at toll booths, for scheduled and

The potential that Pakistan has in terms of mobility – so, in ride-hailing, last-mile courier delivery, freight, and intercity – is huge. And we are not talking only about 2024 and 2025; the potential is long-term – because if you get into the market at an early stage, you have an enormous advantage in the long game

Daniil Petin, vice president at inDrive

unforeseen truck maintenance and repairs. For working capital to bridge cash flow gaps due to delayed payments and for fleet expansion. The lending here is less risky because vehicles can be used as collateral.

Why Yango entered the picture

Yango’s strategic investment is a significant vote of confidence not just in Trukkr, but in Pakistan’s logistics potential. Known globally for its B2C logistics and mobility offerings, Yango sees Pakistan as an untapped frontier for expansion.

“Yango is a B2C player. We’re a B2B operation. It’s a natural synergy. They want to be a super logistics app; we can power that with our tech and network on the B2B side,” says Sheryar Bawany, CEO of Trukkr. While Yango’s plans for Pakistan remain broad, the collaboration positions Trukkr as a second layer in a potential logistics ecosystem that could serve both corporate and end consumers, possibly even across borders where Yango has presence.

To understand Yango’s bet, you have to understand Yango. Founded as a global expansion arm of Yandex, the Russian search and tech behemoth known as “Google of Russia”, Yango Group is now a UAE-headquartered tech company operating in more than 30 countries, focused on logistics, mobility, AI,

and fintech. It’s behind major ride-hailing and delivery apps, AI-based commerce platforms, and fintech integrations in emerging markets from Latin America to Sub-Saharan Africa.

Trukkr, on the other hand, sits at the intersection of logistics and financial services in one of the most complex and biggest markets in the world. The company has quietly built a platform for freight logistics and embedded fintech services on top. That’s precisely where Yango sees opportunity. “Pakistan’s logistics sector is full of potential, and Trukkr is helping move it forward by giving operators the financial tools they need to scale and succeed,” said Daniil Shuleyko, CEO of Yango Group, in a statement announcing the investment.

The partnership may appear straightforward: a VC-backed startup raises capital, a global investor wants local presence in freight logistics. The deal here goes deeper, however. Yango isn’t just investing in logistics, it’s investing in ecosystem control just like Uber which moved into freight. Yango is building a “super app” for transportation and delivery services. Trukkr’s B2B logistics platform complements Yango’s B2C logistics capabilities, filling a critical piece in the logistics value chain. Yango can bring consumer-facing app for freight movement while Trukkr brings backend fleet management and credit services.

Yango’s biggest competitor in Pakistan currently is inDrive, which is also interested in building a similar superapp for logistics. Both

Yango is a B2C player. We’re a B2B operation. It’s a natural synergy. They want to be a super logistics app; we can power that with our tech and network on the B2B side

Sheryar Bawany, CEO Trukkr

Yango and inDrive are competing with each other in ecosystem control in logistics and whoever makes the first move gets the advantage in the long run.

“The potential that Pakistan has in terms of mobility – so, in ride-hailing, last-mile courier delivery, freight, and intercity – is huge. And we are not talking only about 2024 and 2025; the potential is long-term – because if you get into the market at an early stage, you have an enormous advantage in the long game,” Daniil Petin, vice president at inDrive had told Profit, expressing inDrive’s significant interest in different verticals including freight in Pakistan’s logistics sector. inDrive has earlier made an investment in Krave Mart, moving into grocery deliveries before Yango.

With the investment in Trukkr, Yango and Trukkr can digitize the entire freight logistics chain from shipper to driver to recipient with embedded financial rails at every step.

Trukkr’s plans after funding

Interestingly, against venture capital (VC) wisdom of expanding in new markets quickly, Trukkr has opted not to expand into other countries in the region. “Unless you’re killing it in Pakistan, I don’t see the value in rushing to Saudi Arabia. This market is big, complex and still full of opportunity,” says Sheryar candidly.

He pointed to Pakistan’s local conglomerates that grew steadily over decades without overseas distractions as examples of how patient, disciplined growth can yield lasting success. “You want Saudi funding? Be a Saudi company. That’s fair. But we’re a Pakistan company, and our eyes are still on this market.”

More than half of what Trukkr has raised is earmarked specifically for lending operations, fueling the company’s credit offerings to transporters. The remaining amount would be directed at product development, platform expansion, and tech infrastructure to bring more trucks and onboard more corporations onto Trukkr’s platform. n

expected impact of tax hikes on formal sector milk, while exempting loose milk,

Profit Report

FrieslandCampina Engro Pakistan (FCEPL) has reported a decline in quarterly revenue alongside a sharper drop in bottom line earnings, underlining the growing strain on the country’s formal dairy sector. The dairy producer’s latest unaudited results show that April–June (Q2) net sales fell year on year while gross margins improved, only for higher taxation to absorb most of the operating gains and pull down net profit. The board did not recommend any payout for the quarter.

FCEPL’s Q2 revenue slipped to Rs26.47 billion from Rs27.56 billion a year earlier, a decline of just under 4%. For the first half (January–June), net revenue came in at Rs52.49 billion, down 4.6% versus the same period of 2024. On the face of it, the topline contraction points to demand softness in value added dairy, a trend the industry has been signalling since the sales tax regime was tightened last year.

Beneath the topline, however, the quarter shows a notable improvement in gross profitability. Gross profit for Q2 rose to Rs5.03 billion from Rs4.84 billion last year, lifting the gross margin to 19.0% from 17.6%. For the half year, gross profit improved to Rs9.78 billion (vs Rs9.47 billion), taking the January–June gross margin to 18.6% from 17.2%. The expan-

appears to be having the predictable impact

sion reflects lower input cost pressure relative to retail pricing, and some mix and efficiency effects that flowed through cost of sales.

Operating lines paint a mixed picture. Distribution and marketing spend was trimmed to Rs1.93 billion in the quarter (from Rs2.35 billion), while administrative expenses rose to Rs509 million (from Rs470 million). Crucially, finance costs dropped to Rs397 million from Rs1.06 billion, mirroring lower borrowing needs and a less punitive interest burden. Thanks to these moving parts, operating profit rose to Rs2.51 billion (from Rs2.03 billion).

Yet the quarter’s bottom line went the other way. Profit before tax climbed to Rs2.12 billion from Rs969 million, but the tax charge surged to Rs1.88 billion (from Rs381 million), taking the effective tax rate to roughly 89% versus about 39% a year earlier. As a result, profit for the period fell to Rs232 million (from Rs588 million), and earnings per share dropped to Rs0.30 (from Rs0.77). The company also disclosed no interim cash payout for the quarter and no bonus/ right issue.

On a first half basis, the pattern looks slightly sturdier: operating profit increased to Rs4.73 billion (from Rs4.00 billion), finance costs more than halved, and profit after tax edged up to Rs1.32 billion (from Rs1.25 billion), translating to H1 EPS of Rs1.72 (vs Rs1.63). Even here, though, the effective tax

rate stepped up to the mid 60s (per cent), capping what would otherwise have been a sharper earnings recovery.

Cash flow disclosures add texture. For the half year, cash generated from operations swung to a positive Rs2.84 billion (vs an outflow in the comparable period), though net cash still declined by about Rs2.06 billion, in part as the company settled a prior year dividend and made lease repayments. In short, the income statement is improving from gross profit down to operating profit, but tax and working capital dynamics are keeping a lid on distributable cash for now.

Company profile

FCEPL is among Pakistan’s most recognisable consumer staples names, tracing its roots to Engro Foods, set up in 2005 with a flagship UHT milk plant in Sukkur and, later, a second major site in Sahiwal. The company was built to formalise a slice of a vast, largely informal dairy market by collecting, processing and packaging milk to consistent standards at industrial scale.

In 2016, Dutch dairy co operative Royal FrieslandCampina acquired a majority stake in the business, bringing global expertise in farm networks, processing and packaging. A formal rebrand followed in 2019, with Engro Foods becoming FrieslandCampina Engro Pakistan.

As of this year, Engro Corporation remains a significant sponsor with about 39.9% ownership, while the Dutch parent is the company’s controlling shareholder. Head office operations are based out of Karachi’s Harbour Front building.

The corporate mission has been consistent: to expand the share of safe, traceable dairy in a market still dominated by loose milk, while improving the resilience of a cold chain that spans thousands of farmers and intermediaries. That mission now intersects with a harsher tax and cost environment than at any point since the brand’s launch.

Product line up

FCEPL’s brand architecture straddles mainstream and value segments. At the top sits Olper’s, a flagship UHT milk franchise that also extends into value added dairy such as cream. The brand is positioned on purity, consistency and everyday nutrition – a message that made UHT milk synonymous with convenience during the early 2010s and continues to anchor category advertising.

At the economy end, Dairy Omung targets price sensitive households with a low fat UHT proposition used in tea, plain drinking and basic desserts – a deliberate pitch at consumers who might otherwise default to cheaper loose milk. The Tarang tea whitener franchise, launched in 2007 and since expanded across pack sizes, remains a volume engine in tea heavy Pakistan, where “doodh patti” culture creates daily demand for a stable creaming agent.

The portfolio also includes Omoré, a frozen dessert range that pits FCEPL against both local dairy labels and multinational competitors in impulse and take home formats. Beyond these anchors, the company offers line extensions such as flavoured milk and value added dairy packs for cooking and baking; an in house e commerce storefront and modern trade listings reflect the breadth of SKUs now in market.

This spread is strategic. It lets FCEPL ride multiple demand curves: staple nutrition via UHT milk, tea consumption via whitener, and occasion based indulgence via frozen desserts – each with different price elasticities and seasonality. But it also means exposure to tax treatments that diverge across product types, a point that has come into stark relief over the past year.

Tax headwinds

The company’s latest figures arrive amid a structural tax shock to the formal dairy sector. In Budget 2024–25, the government imposed an 18%

sales tax on packaged milk and related dairy (including tea whiteners and powders), reversing years of zero rating meant to encourage formalisation and food safety. Industry bodies warned at the time that the move would lift shelf prices and push consumers back into the informal “loose milk” channel. The warning, by most accounts, has proved prescient.

Since the levy took effect, formal dairy volumes have shrunk, by some estimates around 20%, as households trade down. The Pakistan Dairy Association (PDA) and business groups have repeatedly urged the government to revisit the rate, citing both nutrition and investment risks; proposals ranging from a cut to 5% to targeted relief for infant foods have been floated in official and policy forums. Ministers have publicly acknowledged the pressure and flagged ongoing reviews, but the 18% rate remains in force for now.

Why does this matter so much for FCEPL? Because the informal sector – the neighbourhood doodh wala and an extended supply chain with minimal documentation –still accounts for over 90% of Pakistan’s milk consumption. That market is largely outside the GST net, faces looser compliance costs, and, crucially, can undercut packaged milk on price, especially when an 18% tax is layered onto formal products. The result is a structural price gap that formal processors struggle to close without eroding margins or sacrificing investment in quality and cold chain.

Policy analysts note that the removal of zero rating through the Finance Act 2024 specifically targeted serials under the Fifth Schedule of the Sales Tax Act, bringing infant milks and other fortified products into the 18% net alongside regular packaged milk. Industry and think tank voices have countered that global practice typically taxes milk lightly (if at all), and that Pakistan’s 18% rate is an outlier. In addition, “further tax” and withholding provisions on unregistered distributors add friction to the formal supply chain that the informal channel does not bear.

That context helps explain the paradox in FCEPL’s numbers: better gross margin and operating profit, but softer revenue and a much higher effective tax rate pushing net profit down in the quarter. The sales tax shift is a topline headwind in its own right; it also shows up indirectly as a tax expense burden, because weaker volumes limit operating leverage just as tax accruals rise. The company’s cash flow statement hints at the consequence: a return to positive operating cash in H1, but continued pressure on overall cash balances after dividends and lease outflows – hardly a crisis, but not yet the footing for aggressive expansion either.

For consumers, the policy has had predictable behavioural effects. By making packaged milk meaningfully pricier, it has nudged households to loose milk, even as public health agencies and nutrition advocates warn that unregulated supply chains carry higher risks of adulteration and spoilage. That risk reward trade off is amplified in a cost of living squeeze. Several stakeholders – from the PDA to chambers of commerce and policy institutes – have urged a rate cut to nudge consumption back into the documented, quality controlled channel, arguing that broader formalisation would widen the tax base over time while protecting nutrition.

What it means for the rest of 2025

The immediate read through is that FCEPL’s operational engine remains sound enough to extract margin despite slower sales – a useful buffer when inflation and input volatility are still in play. But the policy overlay is no longer a background factor; it is now central to demand. With informal milk still dominant, and with consumers price sensitive to a fault, the 18% GST is proving a decisive swing factor for category volumes.

For investors, the Q2 scorecard is a study in offsets. On the plus side: gross margin and operating profit improved year on year, finance costs fell sharply, and H1 earnings still managed to grow modestly. On the drag side: revenue contracted, the effective tax rate spiked, and quarterly EPS fell by more than 60%. Whether H2 can look better depends less on cost curves – which FCEPL has managed well this year – and more on volumes, which in turn are tied to tax and consumer purchasing power.

The broader policy debate is already in motion. Government officials have signalled willingness to review the tax on packaged milk; industry bodies are lobbying for a cut to 5% to restore affordability and stem down trading to the informal market. If that debate tilts toward relief, formal players like FCEPL could see topline stabilise without surrendering the margin gains they have eked out this year. If not, the current pattern – leaner marketing, tight working capital, and a reliance on price/mix rather than volume – may define the remainder of 2025.

For now, the company’s headline speaks for itself: revenue is down, margins are up, and net profit is caught in the cross currents of a tax regime that favours the informal over the documented. In Pakistan’s dairy aisle, that is more than an accounting outcome – it is a policy choice with real consequences for what, and how safely, families drink. n

Gandhara’s turn towards China begins to bear fruit

The former Nissan affiliate now assembles Chinese cars, and is beginning to regain ground

Profit Report

After several lean years and a strategic reset, Ghandhara Automobiles Limited (GAL) is stepping back into the limelight of Pakistan’s auto industry. The company, long associated with Japanese marques through its previous incarnation as Ghandhara Nissan, has retooled its portfolio around Chinese partners in both passenger and commercial vehicles. Early evidence suggests the pivot is paying off: earnings are improving, launches are landing in receptive market niches, and the commercial-vehicle franchise is riding a cyclical upturn. At the same time, a premium pick up –priced to undercut the segment incumbent by a wide margin – has given the storied Karachi assembler something it has not enjoyed in years: momentum.

The numbers tell the story of a company shifting out of neutral. From a modest revenue base of Rs9.4 billion in FY24, GAL’s top line is on course to almost triple to roughly Rs27.0 billion in FY25, with another sizeable step up to around Rs43.0 billion pencilled in for FY26. The earnings line has turned decisively as well: profit after tax, which stood at Rs365 million in FY24, is tracking in the ballpark of Rs3.8 billion this year and above Rs5.5 billion next year, helped by both volume growth and a stronger product mix. Gross margin expansion – from 12.0% in FY24 to above 20% in FY25–26 – underlines the operational shift behind the headline figures.

On a per share basis, the transformation is striking: EPS jumping from Rs6.83 in FY24 to an estimated Rs66.39 in FY25 and Rs96.55 in FY26 reflects the combined effect of a recovering commercial franchise and the addition of a high ticket pick up line. Management has the balance sheet headroom to begin rewarding shareholders as well, with dividends of Rs5 per share indicated for FY25 and Rs7 in FY26, signalling confidence in cash generation.

Valuation metrics capture the market’s catch up phase. On FY26 assumptions, the shares change hands at roughly 5–6x forward

earnings – below the company’s five year average multiple and a discount to sector norms –leaving scope for a re rating if delivery continues. The improvement is underlined by a step up across profitability ratios (including net margin trending into the mid teens in the outer years) and by a sturdier current ratio as inventories and receivables turn more efficiently. The earnings engine has several pistons. The first is the resurgence in light commercial vehicles (LCVs) and trucks, where the company’s own JAC models and its heavy duty Dongfeng line are seeing a cyclical tailwind from revived trade activity and project spending. The second is the newly launched premium pick up, which carries high revenue per unit and adds an aspirational halo at a disruptive price point. The third, often overlooked outside institutional circles, is GAL’s stake in its associate Ghandhara Industries Limited (GHNI), the country’s dominant truck maker, which continues to send a steady stream of equity accounted income back to GAL.

A premium pick up priced for a broad audience

In January 2025, GAL entered Pakistan’s premium pick up segment with the JAC

T9 Hunter, a model pitched squarely at buyers who want the stance and capability of the class leader without its price tag. Priced at Rs10.5 million, the Hunter undercuts Toyota’s Revo GR S (about Rs15.84 million) and is also more affordable than Isuzu’s D Max variants (around Rs13.39 million), while offering a feature set designed to resonate with both fleet and lifestyle buyers. The truck combines a 1,999 cc diesel with an eight speed automatic gearbox, 4×4 drivetrain and seven airbags – an unusual bundle at this price point – along with an interior specification aimed at family and executive use alike.

The segment backdrop is favourable. After shrinking to roughly 4,000 units in FY24, premium pick up sales rebounded to an estimated 5,500 units in FY25 as macro stability improved and replacement demand returned.

Market response to the Hunter was strong enough that GAL briefly paused bookings to manage delivery timelines before resuming them – an early sign of traction. Volumes of about 3,200 units in FY26 (roughly 267 units per month) are within reach if supply holds steady, giving the pick up line a material earnings contribution in the company’s near term mix.

Below the headline pick up, the JAC X 200 has quietly become a growth driver in the LCV niche. Volumes climbed 75% year on year in FY25, supported by e commerce logistics, intra city distribution and SME fleet renewals. While the X 200 sits at a slightly higher price point than the Hyundai Porter and Suzuki Ravi, it justifies the premium with a 1.2 tonne payload, a 92 HP engine, electric power steering and fuel efficiency near 11 km per litre – attributes that appeal to operators watching both uptime and operating costs. Since FY20, the model’s volumes have compounded at 26.6% annually, and further growth is expected as industrial activity and last mile delivery networks scale.

In medium trucks, GAL’s JAC 1020K and 1042K have carved out a high growth niche; in heavy trucks, Dongfeng units – assembled locally through subsidiary Ghandhara DF – have proven resilient. Sales of Dongfeng trucks improved to about 600 units in FY25 on channel checks, with 650–670 units projected over the next two fiscal years in a base case recovery. JAC truck volumes are similarly expected to rise as the investment cycle gathers pace. A milestone project such as Reko Diq – one of the world’s largest undeveloped copper gold deposits – should drive multi year demand for haulage and support vehicles as production phases ramp up later in the decade, a tide that lifts both GAL’s own truck lines and GHNI’s Isuzu franchise.

The company’s manufacturing footprint is sized for growth on a single shift basis –4,800 commercial vehicles and 6,000 passenger cars annually – backed by a 3S (sales, service and spares) network of 26 outlets across the country. That reach matters, not only for retail sales but for warranty and parts revenue in a market where after sales support shapes brand

From Nissan roots to the current era

For decades, the “Ghandhara” name has been entwined with Japanese brands. Incorporated in 1981, the company – then Ghandhara Nissan – assembled Nissan heavy trucks locally and handled imports of Nissan CBU vehicles, building a reputation for reliability in a market dominated by Japanese engineering and parts ecosystems. It listed on the Pakistan Stock Exchange in 1992, expanding its industrial footprint and dealer reach.

The portfolio diversified as the local competitive landscape shifted. By 2013, the group had added Dongfeng trucks through the subsidiary Ghandhara DF, and in 2018 it began assembling JAC commercial vehicles, opening the door to a broader Sino Pakistani industrial alignment. The move into Chinese passenger SUVs followed: in 2022, local production of Chery’s Tiggo 4 Pro and Tiggo 8 Pro went live. That partnership ran its course in January 2025, just as a new Chinese pick up (the JAC T9 Hunter) was ready to roll out, marking a baton pass from one Chinese marque to another in the consumer facing portfolio.

A formal rebranding – Ghandhara Nissan to Ghandhara Automobiles – came in April 2023, underscoring the shift away from a single principal identity. Ownership today sits within the Bibojee Group, via parent Bibojee Services (Pvt.) Ltd., whose industrial interests span commercial transport and allied sectors. The shareholder roll is broad – about 57 million outstanding shares – but control lies with associates (57.8%), with local public investors at 26.9% and foreign companies around 6.4%. Free float is roughly 40%, providing decent liquidity for institutions.

The group connection to GHNI is strategically important. GAL owns 17.91% of GHNI, whose Isuzu line dominates Pakistan’s truck market. That equity stake delivers a meaningful share of profits back to GAL and ties its fortunes to the country’s capex and logistics cycles – often more reliable drivers of earnings than consumer credit.

Why the China pivot matters: cost, content and cadence

The significance of GAL’s turn towards Chinese partners is not merely stylistic branding – it is a reset of the company’s cost base, product cadence and target customer. On price to specification, the JAC T9 Hunter illustrates

the new equation. At Rs10.5 million, the truck comes to market at a discount of roughly Rs5.3 million to the segment’s long established leader, Toyota’s Revo GR S. Yet the Hunter’s equipment level – seven airbags, an eight speed automatic, robust torque delivery and 4×4 capability – places it squarely within premium expectations, tilting the value conversation in its favour for both corporate fleet buyers and status conscious households.

Chinese OEM partnerships also allow shorter product cycles and more flexible localisation of parts in segments where Japanese incumbents have sometimes focussed their localisation efforts on higher volume models. In commercial vehicles, the alignment with JAC and Dongfeng makes strategic sense given China’s depth in workhorse platforms and its supply chain for drivetrains and components. For a local assembler, this alignment offers a pathway to defend margins even when currency volatility raises the landed cost of imported kits – provided volumes scale.

There are competitive realities, too. The premium pick up lane is drawing new entrants: BYD’s Shark and Sazgar’s Canon Alpha are on the horizon, setting up a more crowded field where pricing power will need to be earned through after sales, parts availability and perceived durability. That puts a premium on the very things Ghandhara has invested in – an established 3S footprint and a multi decade service culture – even as it recalibrates away from Japanese principals.

Crucially, the pivot does not abandon the company’s Japanese heritage so much as it redeploys it. The service ethos honed in the Nissan years, the manufacturing discipline, and the dealer relationships built over decades are the scaffolding for Chinese brand launches. The result is a portfolio that stretches from value driven LCVs to aspirational pick ups and project ready heavy trucks – exactly the spread needed in a market where household sentiment and project capex rarely move in lockstep.

Market share in the broader Pakistani automobile market

Afull reading of GAL’s competitive position requires stepping beyond showroom chatter to the shares it and its associates command in their respective lanes.

Trucks and buses through GHNI. In the heavy duty end, GHNI’s Isuzu franchise continues to reign, holding about 67% of the domestic truck market in FY25. Bus manufacturing is another pillar, where GHNI’s share is roughly 27%, and both categories saw outsized growth in the latest year as volumes

rebounded off a low base (truck sales up 2.3×; bus sales up 2.4× to 216 units). For GAL, which consolidates GHNI via equity accounting, that dominance translates into a steady contribution to the bottom line – estimated at around Rs11.2 per share in FY26.

LCVs: JAC’s share is now firmly double digit. The light commercial market has undergone a quiet reshuffle. Where Suzuki’s Ravi once dominated, share has bled toward both Hyundai’s Porter and JAC badged X 200s assembled by Ghandhara. By FY25, JAC’s LCV share had climbed to roughly 13%, up from single digits a few years ago, with Suzuki at about 54% and Hyundai at around 30%; Dewan’s Shehzore also re entered the frame at near 13%. Such shifts validate the X 200’s traction among fleet buyers who prioritise payload, fuel economy and financing availability.

Premium pick ups: a right sized prize. The premium pick up segment is smaller than the mass market sedan or hatchback categories but carries outsized impact on revenue and brand. Annual volumes, which fell to about 4,000 units in FY24, recovered to an estimated 5,500 units in FY25 as supply improved and deferred purchases came through. In that context, the Hunter’s targeted run rate – roughly 3,200 units in FY26 assuming stable parts supply – would amount to a meaningful slice of a still recovering niche, even before factoring in further growth in the category. The out of pocket saving versus the segment leader is large enough to invite cross shopping by buyers who previously saw the premium pick up as a stretch purchase.

Heavy trucks: Dongfeng holds the line. On the heavy haul side, Dongfeng’s locally assembled units logged about 600 sales in FY25, with 650–670 envisaged across the next two years in an environment that includes energy, mining and infrastructure projects. The long dated Reko Diq development is emblematic of a demand pipeline that can sustain truck share even if retail auto cycles wobble. Taken together with GHNI’s Isuzu dominance, the Chinese heavy duty component gives Ghandhara a durable foothold in the most capex sensitive corner of the market.

The broader picture. The breadth of Ghandhara’s coverage – LCVs for city distribution, premium pick ups for corporate and lifestyle use, and medium to heavy trucks for project logistics – means its “market share” story is really a portfolio of shares across distinct sub markets. In the consumer mindshare stakes, the Hunter brings a nameplate that can sit in the same conversation as the Revo or D Max at a lower entry price. In the workhorse lanes, the X 200 is increasingly a default pick for SMEs, while the Dongfeng and Isuzu labels are well known in freight yards from Karachi’s port terminals to the motorway weigh stations ringing Punjab. n

Mutual funds crowd into energy, cements and

a handful of banks

A look into what the most sophisticated money managers in Pakistan are investing in and shying away from

Profit Report

In a month still dominated by macro cross-currents – from inflation prints to energy price headlines – the industry’s positioning has a clear centre of gravity: energy, power and a tight cluster of blue-chip cyclicals, according to Arif Habib Ltd’s analysis of mutual fund equity holdings.

Among the ten most widely owned shares across funds, state-linked oil and gas champion OGDC, cement bellwether Lucky Cement (LUCK), energy marketer PSO, explorer PPL and Meezan Bank (MEBL) form the top five. In breadth terms, OGDC appears in 87 mutual funds; by depth, funds collectively hold 20.2% of the company’s free float. LUCK features in 79 funds with 13.1% of its float owned by funds, while PSO and PPL are each in 69 funds – and, strikingly, funds account for 43.9% of PSO’s free float and 14.8% of PPL’s. MEBL rounds out the top five with 57 funds and 10.7% of its free float in institutional hands.

There is some evidence as to how “institutionalised” some mid-caps have become in this cycle. Cement producer Kohat Cement (KOHC) has 27.5% of its free float owned by funds; textile player Kohinoor Textile (KTML) is close behind at 24.2%. Sui Northern Gas Pipelines (SNGP) clocks in at 18.7% and Mari Petroleum (MARI) at 13.2%, underscoring the

industry’s comfort with energy infrastructure and E&P cash-flows. On the flip side, big banks such as UBL and MCB have only 2.6% and 2.1% of their free float owned by funds, respectively – far lower than PSO’s 43.9% – a gap that speaks to a different kind of conviction (or caution).

Equity mutual funds’ assets under management represent 12% of the overall asset-management industry as of July 2025. Within the equity segment, National Investment Trust (NIT) remains the largest player by exposure, followed by Al Meezan Investment Management and NBP Fund Management (NAFA). This concentration matters: what these three do tends to ripple through prices and peer behaviour.

The report also maps, manager by manager, how funds tweaked positions over the month. That month-on-month lens is where the “favoured” and “disfavoured” narratives come alive.

Energy stays king –across strategies

The case for energy exposure is visible across the product spectrum. The tilt is hardly confined to a single house.

The AWT Islamic Stock Fund also sets OGDC, PPL and LUCK at the top, alongside HUBC and SYS; SNGP appears in its top ten, too. This suggests a cross-house consensus on earnings visibility (and dividend carry) in

energy and power.

Even multi-asset and pension products reflect the same gravitational pull. AWT’s Islamic Pension Fund’s July equity sleeve still lists PPL, OGDC and LUCK at the top, with SYS and HUBC in the supporting cast; the month saw a gentle uptick in OGDC and a slight trim to Lucky and Fauji Cement (FCCL).

Cements and fertilisers: the second ring of consensus

Cement has been the cycle’s high-beta proxy, and funds are leaning into it – but selectively. Lucky Cement’s ubiquity is one sign; the fund-held share of KOHC’s float is another. Alfalah Asset Management’s flagship equity fund, for instance, nudged up positions in PSO and UBL in July, but kept LUCK among its top holdings and increased exposure to Cherat Cement (CHCC).

Fertilisers are well represented, though weights vary by style. Across several MCB funds, FATIMA and EFERT appear as durable top-ten names; MCB’s Alhamra Islamic Stock Fund’s July top-ten includes EFERT (3.4%) alongside CHCC and SYS, while FATIMA remains a meaningful line.

NIT’s giant National Investment Unit Trust (NIUT) also keeps a foot in fertilisers

(FFC) while maintaining outsized concentrations in PSO and MARI. In July, NIUT’s top holdings were led by PSO (13.6% of fund size), MARI (10.1%) and BAHL; the cement and pharmaceutical names (GLAXO) remain in the mix.

Banks: the barbell between underownership and selective conviction

One of the more intriguing threads is how funds are treating banks. UBL and MCB have only a low single-digit share of their free float owned by funds – 2.6% and 2.1%, respectively – despite their size. In contrast, some second-tier banks are far more popular: BAFL appears repeatedly in top-ten lists, and AKBL shows a 12.0% free-float ownership by funds. That split suggests a barbell: some managers prefer high-beta or lower-valued plays in the financials, while others stay underweight the big three.

But there is movement under the surface. MCB’s flagship Pakistan Stock Market Fund, for example, increased its weight in BAFL from 7.3% in June to 8.8% in July, and lifted NBP from 5.9% to 7.9%, even as it trimmed FATIMA (from 5.3% to 4.0%).

Funds dedicated to financials are, unsurprisingly, leaning into the theme. UBL’s Financial Sector Fund is anchored by UBL (19.1%), MCB (14.4%) and MEBL (12.1%), followed by HMB and BAFL – an explicit tilt to banks that some generalist funds have under-owned relative to their free floats.

Favoured vs disfavoured: where the money is moving

“Favoured” in this dataset isn’t about stock-picker rhetoric – it’s about repeated appearance and rising weights. “Disfavoured” shows up as exits from the top ten or steady trims

Across these examples, “favoured” reads as: OGDC, PPL, PSO, HUBC, and a set of selective banks (BAFL, NBP, MEBL) plus LUCK. “Disfavoured” in July shows up particularly in cement sub-bets (DGKC/MLCF/PIOC trims in specific funds) and in the refineries held by the JS ETF a month earlier.

While large-caps anchor the consensus, a long tail of mid and small-cap names repeatedly appearing in funds’ top-ten lists. GlaxoSmithKline Pakistan (GLAXO) shows up in nine funds; Kohinoor Textile (KTML) in eight; The General Tyre (TGL) and Ghani

Global (GAL) are in six each; while niche plays such as Ghani Glass (GHNI), Service Industries (SRVI), TPL Trakker (TPLT) and Flying Cement (FLYNG) make cameo appearances. The breadth hints at diversified risk-taking beyond the headline trades.

For asset allocators, the “free-float capture” metric is a useful risk compass. With funds owning nearly 44% of PSO’s free float and more than a quarter of KOHC’s, those counters can become crowded – liable to amplify moves when flows turn. Conversely, under-owned big banks (by this metric) might have more room for incremental institutional demand if the earnings or rate narrative breaks their way.

What the “disfavoured” list looks like – reading between

the lines

The report doesn’t label any stock “disfavoured”. But the month-on-month tables and the free-float capture exhibit let us infer which corners funds leaned away from in July:

• Selective cement trims: Multiple funds cut or de-emphasised DG Khan Cement (DGKC) and Maple Leaf (MLCF). JS’s ETF swung from June’s heavy weights in MLCF (18.2%) and DGKC (17.3%) to zero in its July top-ten – a dramatic de-risking of cement beta in that vehicle.

• Refineries rotation: The same ETF dropped refineries (PRL, NRL, ATRL) from its top cohort as it pivoted into banks and gas distribution – again speaking to a shorter-term view on those value chains.

• Marginal easing in select cements inside MCB’s book: PIOC fell from 12.4% to 9.9% in the MCB Dividend Yield Plan. The same fund also trimmed BAFL and NBP a touch, though both remain large positions.

• Banks still under-owned at the industry level: Despite idiosyncratic increases (e.g., BAFL and NBP inside MCB’s flagship), the page-three free-float exhibit shows UBL, MCB and HBL with only 2.6%, 2.1% and 0.9% of free float in fund hands, respectively – arguably “disfavoured” relative to their index heft.

None of this means funds have turned bearish on the sectors outright. It does, however, suggest a more tactical stance – especially in cements – after a strong run.

The concentration question

Apoint to watch is how much of certain companies’ tradable float is already in mutual-fund hands. The funds owning 43.9% of PSO’s

free float and more than a quarter of KOHC and KTML. High “float capture” can be a double-edged sword: supportive on the way up, but compressing liquidity when exit doors get crowded. Conversely, companies like UBL and MCB – under-represented in mutual-fund ownership – could see powerful incremental flows if the earnings or policy backdrop turns in their favour.

Within the manager universe, a handful of houses account for the lion’s share of equity AUM, led by NIT, then Al Meezan and NBP (NAFA). That concentration is unsurprising given the breadth of their product suites – NIT’s NIUT alone had a July fund size above Rs94bn and 99% equity allocation. As their positioning goes, so often does market tone.

Reading July’s book of record, three themes stand out.

First, dividends and defensible cashflows remain the anchor. E&P and power exposures dominate across managers, with OGDC, PPL, PSO and HUBC recurring across styles and mandates. Even balanced and pension funds lean that way.

Second, managers are selective rather than blanket bullish on cyclicals. LUCK remains a near-universal anchor, but position-sizing within the broader cement complex looks more tactical, with trims to DGKC, MLCF or PIOC in several portfolios. Fertilisers retain a core role, particularly FATIMA, EFERT and FFC, but weights ebb and flow with macro signals.

Third, the financials story is bifurcated. On one side, funds’ aggregate ownership of the floats of UBL, MCB and HBL remains low.

On the other, several funds increased exposures to BAFL and NBP in July, and dedicated financials vehicles are overweight the sector leaders. That barbell leaves room for dispersion – and alpha – if the earnings trajectory or policy rates move.

Bottom line

July’s positioning paints a consistent picture. Pakistan’s mutual-fund industry is clustering around energy and power cash-flows, keeping LUCK as the cement of choice, and treating fertilisers as sturdy ballast. Banks are a tale of two cohorts: under-owned blue-chips by free-float share, and more aggressively owned mid-tier names where managers see valuation or beta appeal. There are exceptions at the margin – ETFs that pivot aggressively month to month, or dividend funds that prune positions to manage payouts –but the aggregate keeps circling the same set of liquid, earnings-visible counters. n

Gatron merger attempt falls through

Corporate restructuring of two of its major shareholders called off, unlikely to have a major operational impact

Profit Report

Gatron (Industries) Limited said this week that a proposed restructuring with two of its key corporate shareholders has been called off, drawing a line under a months long process that would have simplified the polyester maker’s shareholding tree. In a notice to the Pakistan Stock Exchange dated 13 August, the company reported that the boards of Nova Frontiers Limited and Ghani & Tayub (Private) Limited – both identified as corporate shareholders of Gatron – had resolved to withdraw the planned Scheme of Arrangement. Gatron’s own board then rescinded its previous consent by circular resolution. The company emphasised that the withdrawal would not affect its day to day operations, assets or the rights of remaining shareholders, and said any court proceedings initiated for the scheme would be withdrawn. The firm added that a trading blackout tied to the process had ended with the disclosure.

While the brief notice did not spell out the “latest developments” behind the decision, it caps a sequence that began in February when Gatron authorised management to pursue a three party scheme with Nova Frontiers and G&T, subject to approvals from shareholders and the High Court of Balochistan at Quetta. That authorisation effectively set the stage for an intra group capital tidy up rather than an operational merger.

At the heart of the now abandoned plan

was a corporate housekeeping exercise among Gatron and two of the entities that sit above it in the group chart. The March quarter consent from Gatron’s board described a scheme to be presented to shareholders and the court; this week’s update says Nova Frontiers and G&T have chosen to stand down, prompting Gatron to withdraw its own earlier approval. The company stated explicitly that there is no impact on its business or assets from the withdrawal, and that the parties will move to unwind court proceedings begun for the scheme. In market terms, the company also lifted a “closed period” that had been in place, allowing insiders to trade again under the usual rules.

Business media had flagged the authorisation back in February, quoting the same PSX filing and emphasising that any restructuring would depend on court sanction and shareholder votes. By August, the tone had reversed: industry outlets reported that Gatron had withdrawn the scheme. Taken together, they bookend a process that never left the procedural lane.

Gatron and its history

Gatron is one of Pakistan’s longest standing polyester players. Incorporated in 1980 and listed in the early 1990s, the company manufactures polyester filament yarn (PFY) and related polyester products from its complex in Hub, Lasbela, Balochistan, and has also developed lines in PET preforms and ancillary power generation. The firm’s operating footprint sits

within Pakistan’s synthetic textile and packaging supply chains, with PFY as the historic anchor and PET related products complementing the portfolio.

The group’s public facing materials frame Gatron as part of the broader “G&T” (Gani & Tayub) business family – a network whose activities span polyester chips, PET resin and films, and related synthetics, and which often markets under the “Gatronova” banner. That lineage is important: it explains why corporate shareholders such as Nova Frontiers and G&T feature so prominently on Gatron’s register and why internal capital moves sometimes require court blessed schemes rather than simple board resolutions.

Over the decades, the Gatron Novatex ecosystem has seen multiple reorganisations designed to keep capital and capacity aligned with market cycles. In 2020, for instance, the High Court of Balochistan approved a combination involving Gatron and Novatex – a reminder that formal schemes are well worn instruments in this corporate family. The group’s manufacturing history, meanwhile, traces a steady expansion from PFY into PET resin, films and downstream packaging inputs, providing an industrial base that serves both domestic buyers and, via associated companies, export markets.

The merger partners

Nova Frontiers Limited (NFL). Nova Frontiers is a public, unlisted company active in investing in shares and related securities. In March

2024, NFL notified Gatron that it had become a substantial shareholder after subscribing to 31.89 million Gatron shares – an update the polyester maker relayed to the PSX at the time. The following year, a board level scheme was floated to realign holdings among NFL, G&T and Gatron, with NFL’s position central to how shares might be redistributed. Competition authorities have previously identified NFL as an investment company and Gatron as a manufacturing concern, underscoring that the proposed scheme was about ownership plumbing rather than industrial overlap.

Ghani & Tayub (Private) Limited (G&T). G&T is the long standing holding vehicle behind the group that sponsors Gatron and its associates. Corporate records describe it as incorporated in the 1950s; it has served as a key shareholder in group companies and, as such, was named alongside NFL in the aborted scheme. Recent statutory disclosures also list G&T as a “person acting in concert” with Novatex (another group flagship), reflecting the tight governance ties within the G&T universe. Novatex’s emergence as a shareholder. A separate but highly relevant development landed in late June this year: Novatex Limited disclosed that it had acquired 31,895,139 Gatron shares at Rs133 apiece, instantly taking a 29.33 per cent stake. The disclosure also noted common directorships between Novatex and Gatron, again highlighting the dense interlocks across the group. While Novatex was not a named party to the now withdrawn scheme, its arrival on Gatron’s register is a material change in the ownership mosaic.

Why the merger

may

have made sense –and why it may have fallen

through

To understand the commercial logic, it helps to look at the mechanics originally proposed for the scheme.

A board report prepared in May outlined a capital restructuring and shareholding realignment among NFL, G&T and Gatron. In essence, the plan would have cancelled certain NFL shares and issued Gatron shares directly to NFL’s outgoing and remaining shareholders and to G&T’s shareholders, thereby eliminating intermediate holding layers and giving beneficiaries direct voting and liquidity in Gatron. An independent valuer (KPMG Taseer Hadi & Co.) set a swap ratio of 6.56 Gatron shares for every one NFL share surrendered, and the documentation emphasised that existing Gatron shareholders would not be diluted on a net basis – the company would issue new shares but cancel the equivalent block held by NFL. In addition, the 3.24 million Gatron shares already held by G&T were to be

cancelled and reissued directly to G&T’s own shareholders through reserves, again with the aim of simplification.

Put differently, the scheme’s industrial impact would have been zero – Gatron would still make PFY and PET related products from Hub – but its capital structure impact would have been tidy: fewer layers, more direct ownership, and for those receiving allotments, the prospect of better liquidity in a listed stock. For governance minded investors, these are not trivial benefits. Reducing look through complexity can sharpen accountability, ease related party transaction scrutiny, and enhance the stock’s appeal to institutions who prize clean cap tables. The board report explicitly framed these as positives for shareholder alignment.

So why did it fall through? The company’s letter points to “latest developments” – a catch all that, in the absence of further detail, leaves room only for inference. One clear development is Novatex’s late June entry as a 29.33 per cent shareholder, which arrived just weeks after the board report laid out a scheme in which 31.9 million Gatron shares (the exact quantum NFL held) would be cancelled and effectively redistributed. Novatex’s block is 31,895,139 shares – the same tally cited in the board report when describing NFL’s holdings to be unwound and reissued. It is reasonable to hypothesise that once Novatex took that stake directly, the logic of cancelling NFL’s position and allocating shares across NFL and G&T shareholder cohorts may have needed to be substantially reworked – or became moot – within the originally envisaged scheme. That reading aligns with Gatron’s own emphasis that its role in the scheme was “administrative and consequential”, since the primary transaction was among the corporate shareholders above it.

There are also the practical frictions that accompany any court sanctioned arrangement. A scheme of arrangement demands synchronised approvals: boards, shareholders across multiple entities, and a court – in this case, the High Court of Balochistan. Timelines can stretch, assumptions can age, and valuations can look stale if market prices move or if new transactions (like Novatex’s stake building) intervene. In such a fluid setting, it can be more expedient for sponsoring shareholders to change tack using other lawful instruments, rather than press on with a scheme whose underlying parameters have shifted. The PSX notice makes clear only that Nova Frontiers and G&T themselves opted to withdraw; it does not allege regulatory hurdles or shareholder opposition.

Beyond ownership choreography, strategic rationale for the original plan seemed solid. Gatron’s shareholder base sits within a wider polyester and packaging platform that includes Novatex and affiliated brands. The group has

historically used formal schemes to streamline and occasionally integrate assets as markets evolve. A simplified cap table at Gatron – with ultimate owners holding directly rather than through intermediaries – could have improved transparency and potentially widened the investor base. As noted above, the board report explicitly touted the benefits of eliminating intermediary holding structures and improving shareholder alignment, with the swap ratio grounded in third party valuation work. Those aims are perfectly orthodox in Pakistan’s courts and markets.

What it means now. For suppliers, customers and employees, the company says nothing changes: no operational assets move, and no business lines are affected by the decision to withdraw. For the market, the more consequential headline is who owns what. With Novatex now on the register with almost a third of the stock – and with directors common across the two companies – governance will continue to be shaped by familiar group actors, just more directly. Whether that paves the way for a different, perhaps simpler, reorganisation in future is an open question. What is clear is that, as of mid August, the court driven scheme among Nova Frontiers, G&T and Gatron is off.

The bigger picture

Textiles and packaging are cyclical businesses, and corporate structures around them often evolve with the cycle. Gatron’s operating profile –polyester filament yarn as a core, PET related lines as complements – has not changed with this aborted attempt at simplification. The sponsorship backdrop – the G&T group and its constellation of companies – also remains in place, with various entities holding shares in one another in ways that occasionally call for formal clean ups. Pakistan’s competition regulator has, in the past, assessed transactions involving Gatron and its group companies by noting the distinct roles of each entity (manufacturing versus investment), giving comfort that these intra group moves are typically about how ownership is held, not about suppressing competition on the shop floor. For investors, the key takeaway is not drama but continuity – continuity of operations, of sponsorship, and of the long running pattern in which the group periodically refashions its cap table to match strategy. If anything, the “latest developments” that prompted this withdrawal have clarified the picture: Novatex now sits visibly on Gatron’s share register, and the scheme that might have redistributed NFL’s holding is no longer the chosen instrument. As always in this corner of the market, watch the PSX notices – they tend to be the first and clearest signals of how group ownership is evolving. n

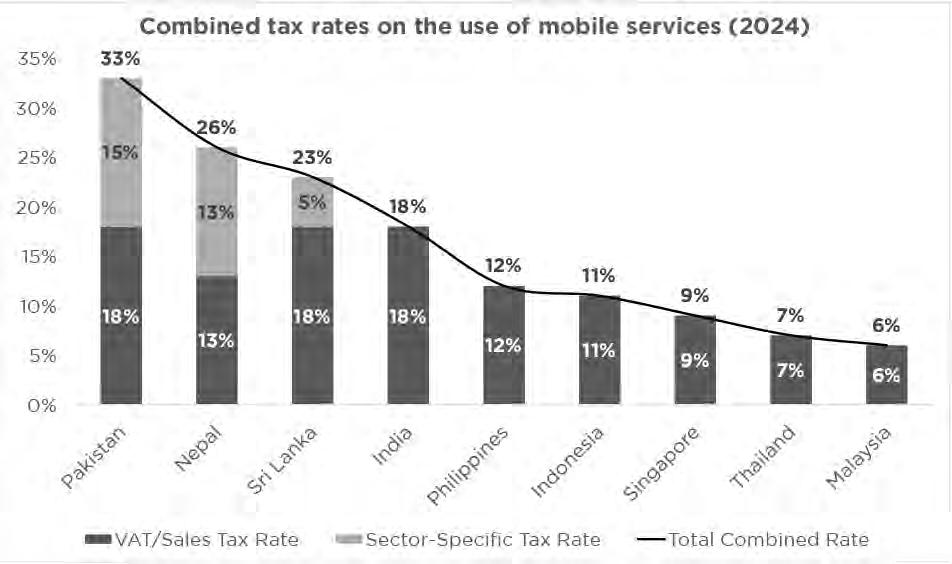

Is Pakistan’s freelance economy being held hostage?

The country’s 600,000 IT professionals and thriving freelance economy are paralysed by regulatory inaction and punitive taxation

By Ahtasam Ahmad and Ahmad Ahmadani

The scene at the recent GSMA Summit in Islamabad should have been a celebration of Pakistan’s digital potential. Instead, it became a wake-up call that the country’s ambitious “Digital Pakistan” vision is colliding with harsh policy realities. The most telling moment? The conspicuous absence of IT Minister Shaza Fatima Khawaja from an event designed to chart the nation’s digital future.

Julian Gorman, Head of Asia Pacific at the GSMA, didn’t mince words about the minister’s no-show, calling it “unfortunate” given the summit’s critical importance. But his warning carried far greater weight: “Investors will walk away, and the people of Pakistan will pay the price if policy stagnation continues.”