16 Power companies worth less than the cash on their balance sheet

20 Pakistan’s circular debt strategy unfolds through unprecedented banking alliance

25 InDrive invests $10mn in Pakistan’s Krave Mart to accelerate super-app ambition in emerging markets

28 A national effort is needed for a sustainable future Sahar Aman

29 What happened during Symmetry’s closed period?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

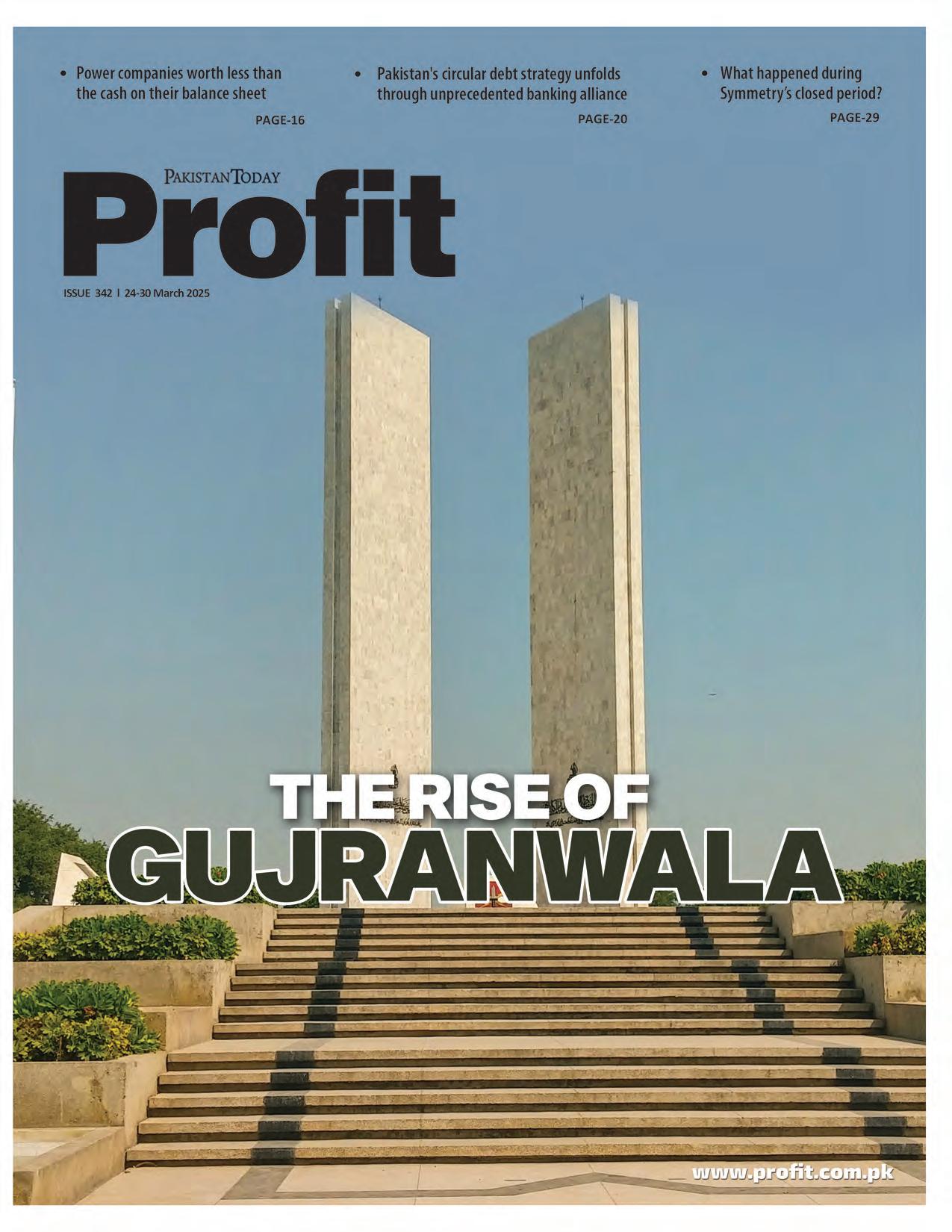

The rise of Gujranwala

It used to be Pakistan’s eighth largest city. It is now the core of the fourth largest metropolitan area. And it is done living in Lahore’s shadow

By Abdullah Niazi and Farooq Tirmizi

Muhammad Yousaf moved to Lahore in 2009. At the time, he was 11 years old and living with his khala. He had visited Lahore many times before, mostly as a treat to see his relatives that lived in the ‘big city’. He himself lived in Gujranwala.

They were a land owning family. His grandfather and great grandfather before him were both wheat farmers, but his father had begun diversifying the family business around the same time Yousaf moved to Lahore. Gujranwala’s population was growing, and so was the city. Yousaf’s father grew their subsistence level dairy farming operation, increasing his herd with imported cows and began selling milk to large milk producers. With the money he made from this, the family began selling ceramic bathroom tiles. That business, initially set up by bringing materials in from other cities and selling to people building homes and businesses in the city, has grown to a point where builders from neighbouring districts such as Narowal, Sialkot, and Hafizabad are regular customers.

Throughout this period of growth for the family, Yousaf remained in Lahore. He had been sent there to study at Lahore Grammar School. Over time, his younger brothers also started moving to Lahore and before long their father bought and set up a house for them in Lahore’s Johar Town area. Their mother moved in with them when the house was done, and then their father also began staying with the kids. Very quickly they began spending more time in their Lahore home than in Gujranwala. The father would commute back and forth while the kids studied.

Eventually, Yousaf went to LUMS and graduated with a degree in economics in 2023. For two years after, he worked in the accounts department of an multinational company’s Pakistan subsidiary based in Lahore. In 2022, he went to pursue his masters degree to Durham University in the UK.

During this time, Yousaf barely spent any time in Gujranwala. The city he remembered was associated with languid summer vacations spent at the family’s farm on the outskirts of the district’s main urban area. While he was away for his masters, Yousaf’s parents moved back to Gujranwala where they built a one-kanal house in Citi Housing Society. The house cost Rs8 crore and was built with all the trappings of a “Spanish” style house with Italian marble tiles and imported fixtures for the bathrooms.

By the time Yousaf returned after completing his education in 2023, he was coming back to a very different city.

“The moment I realised this was a very different Gujranwala was when my brother told me they had opened up a second Baskin Robins here. I didn’t even know about the first one.”

The rise of Gujranwala

In the 1998 census, Gujranwala was ranked the eighth largest city in Pakistan, smaller than Hyderabad, Multan, and Peshawar. In the 25 years between that census and the one in 2017, Gujranwala the city had leapfrogged all three of those cities and is now the fifth largest in the country, with a city proper population of just over 2 million people, only a few thousand shy of the population of Rawalpindi. In the 2023 census, its population had risen to 2.5 million.

The Pakistan Bureau of Statistics does track domestic migration, but through surveys that are not directly part of the census, so it is not possible to say this with certainty, but it is very likely that that the vast majori to that very rapid growth in the city’s population has been due to domestic migration into the city from adjoining areas, and perhaps even further afield.

But even those population growth numbers hide the bigger picture: Gujranwala is the core of a metropolitan area that is the fourth largest in the country, behind Karachi, Lahore, and Faisalabad, and ahead of the Islamabad metropolitan area, based on data from the 2023 census.

The Gujranwala metropolitan area, which we at Profit define as the districts of Gujranwala, Gujrat, and Sialkot, has a population of 13.7 million people as of 2023, according to the population census from that year. Since you have probably never heard of the Gujranwala metropolitan area – because we just publicly started talking about it and are not aware of anyone else ever defining it as such – it probably deserves an explanation as to why we are talking about it this way.

The Gujranwala metropolitan area

The earliest indication of the fact that Gujranwala, Gujrat, and Sialkot were becoming part of a single metropolitan area was in 2001, when planning for the Sialkot International Airport began. The backers of that airport were mostly from Sialkot, but they kept talking about the “export triangle” of Gujranwala, Gujrat, and Sialkot as the market they want to serve.

Look at the airport on a map, and it becomes immediately obvious that while its name may be Sialkot International Airport, it is meant to serve all three cities, and their smaller adjoining suburbs. It is on the road between Gujrat and Sialkot, a bit closer to Sialkot than

Gujrat, but then also quite conveniently connected by highway to the wealthier neighbourhoods of Gujranwala.

This region was once part of what was called Gujranwala Division, back when divisions were a level of government that existed. And it is served by the same electric utility company, the Gujranwala Electric Power Company (GEPCO). And that airport serves as connectivity for the region not just to other parts of Pakistan, but to the wider region and world. For a brief period, it was possible to catch a direct flight from Sialkot to Barcelona, for example.

Beyond these aspects of infrastructure, however, lies the fact that these cities have industries that are similar to each other, rely on overlapping supply chains, and have populations and businesses that have both personal and economic ties to each other.

As noted in our previous cover story about metropolitan areas in Pakistan, one of the clearest ways to determine whether a particular urban agglomeration is functioning as a cohesive economic unit is to look at it from space at night. And the entire Gujranwala metropolitan area is one of the brightest lit parts of urban Pakistan – almost completely contiguous, indicating that the space between these cities consists almost entirely of their respective suburbs.

It is undeniable that that this is now a metropolitan area. Call it the “export triangle”, the Gujranwala metropolitan area, or the Tri-City Area (similar to how sometimes the New York City metropolitan area is called the Tri-State Area), this is a region that businesses plan on serving as a single unit, not three separate markets.

And that, more than anything else, is the value of urban agglomeration: it makes it possible for what might previously have been a niche product or service available only at a very high price to become more widely available.

The value of a metropolitan area

Why does it matter that so many people live in close proximity and that cities that used to be seen as somewhat distant from each other are now closer together? Many reasons, but best illustrated with one example: if you supply anything other than food or basic essentials, you are better of supplying it to a large contiguous population center than serving the same number of people spread out.

This, in turn, improves the quality of what is available, and the price at which it is made available to a larger share of the population.

For families like Yousaf’s, Gujranwala has grown to be a city that can offer educational, recreational, and residential opportunities

that are on par with what they would find in Lahore. The city has multiple malls and shopping plazas packed with almost all of the shopping brands you would find in Lahore.

It can be as simple as more options for dining out or order in, a favourite social activity in Pakistan. In Gujranwala, there are now multiple franchises of international chains such as McDonalds, KFC, Dominos and others.

It can be more complex, like housing and neighbourhoods of a higher quality of comfort than what was previously available. Gujranwala now has private housing societies with homes that are as expensive as those in Lahore, and it has the supplies needed to fit and decorate up-scale houses.

(Prices may be equivalent to Lahore for an interesting reason, though. Lahore is Pakistan’s most developed city, and in terms of physical infrastructure, the best one to live in. As a result, upper middle class demand has many, many neighbourhoods from which to choose, which distributes that demand and thus keeps Lahore real estate prices lower relative to Karachi and Islamabad, which have far fewer high quality real estate options. Gujranwala is similar in Lahore on pricing likely because its upper middle class neighbourhoods have risen in price to Lahore’s levels, but in terms of structural unevenness of pricing between the upper middle class and other parts of the city are more similar to Karachi and Islamabad.)

And, perhaps most importantly for people deciding where to build a family life, it has educational opportunities for children on par with the high end of what one might find in Lahore or Islamabad.

The city has multiple private schools with large campuses offering O and A levels, with multiple branches for schools such as Bea-

conhouse and The City School. And these are upper middle class schools. There are still many other smaller and franchise schools which have English as the medium of instruction.

“When I first moved back from Gujranwala, I was confused by why my family spent so much money building a house here,” Yousaf tells us. “Now I only really go to Lahore to attend weddings for my friends. There is no lack of city life I feel here, and if I need to go back to the family farm, it barely takes me 45 minutes.”

Yousaf, who recently got married, told us he recently remarked to his father that unlike him, his kids would not have to go to Lahore for their education until they were in University. His friends, who travelled to Gujranwala for his wedding and stayed at Falettis and Avari in the city for Rs 20,000 a night, concurred with the sentiment.

A history of the city

Look a little deeper at the city’s history and you will see this is not entirely unexpected. Gujranwala is a relatively modern city. It was established in the 18th Century and provided Gujjar warriors to the Sikh Kingdom in Punjab. Perhaps the city’s greatest claim to historical relevance is that it was the birthplace of Maharaja Ranjit Singh, who was born there in 1780. The few historical monuments it has date back either to Sikh or British rule, but the city by no means carries the weight of history in the same way that Lahore, or even smaller districts such as Sargodha, Kasur, or Sheikhupura do. In that sense it is more reminiscent of Faisalabad (Lyallpur).

After Partition, the city underwent a rapid transformation, with new suburban districts emerging to accommodate a growing population. One of the earliest developments,

Satellite Town, was established in 1950, catering primarily to wealthy and upper-middle-class refugees.

A few years later, in 1956, D-Colony was constructed to provide housing for poorer Kashmiri refugees. The expansion continued into the 1960s with the creation of Model Town, further reshaping the city’s landscape. This era also marked a period of remarkable industrial growth. In 1947, the city was home to just 39 registered factories, but by 1961, that number had soared to 225. The colonial-era metalworking industry thrived, while hosiery manufacturing—led by skilled refugees from Ludhiana—flourished, solidifying the city’s reputation as a growing industrial hub.

By all accounts Gujranwala was poised and growing into this metropolitan area for many decades. The difference now is that there was a time when those that made money in Gujranwala would want to live life in Lahore, now there is less reason to move there. Defining a metropolitan area in a developing country is a difficult task. None of your cities are really going to have the New York Philharmonic or the Met, but any city that can comfortably provide a clean, upper-middle class existence ticks all the boxes.

When Profit’s correspondent visited Gujranwala for this assignment, for example, they were encountered with the unenviable position of their phone battery dying right as they entered the city. Unaided by maps and following off GT Road, it was only a 5-10 drive into the main city before a large shopping centre with shiny billboards advertising mobile phones became visible.

In size and intensity, it was not too far off from Hafeez Centre in Lahore. Inside, the shops sold all kinds of mobile phones — from cheap Redmi phones from China to high-end

Apple and Samsung products fully packaged and proudly displayed. It was ridiculously easy, for example, to find an original charging wire for an iPhone.

Other signs were obvious as well. There were car showrooms in abundance, with Suzuki, Toyota, and Honda having more than one dealership in the city. There were also plenty of showrooms with second hand and refurbished Japanese cars as well as brand new cars being sold at hefty ‘on’ prices. Boards for private housing societies were everywhere, and booking offices for plots were boldly advertised.

While the more posh housing societies within Gujranwala City are clearly different from the rest of the district, it is clear that the growth of Gujranwala City has had an effect on the rest of the district, with clear trends of activity in neighbouring areas such as Saddar, Wazirabad, Kamoke, and Nowshera. Once very clearly rural areas, there has been a blurring of lines between the rural and the urban in the overall district as well.

Diffusion of Punjab’s elite

For much of the century and a half since the construction of the Canal Colonies transformed Punjab, the moneyed elite of Punjab – which historically used to mean landed aristocracy –lived in a manner similar to the nobles in the court of France’s King Louis XIV: they may have lands that gave them aristocratic privileges in other parts of the country, but they all chose to live in one city, and their concentrated presence in that city redirected government resources to making it the most pleasant place to live in.

In the case of pre-Revolution France, that place was Paris and Versailles. In the case of post-1880 Punjab, that city was undoubtedly Lahore. That concentration of the elite

that could nonetheless rule and economically control other parts of the province made the province – and, by extension, the country –easier to rule, since you only needed to corral the support of people who all lived within a 20-minute drive of each other.

This is no longer the case. The Gujranwala elite is undergoing two major changes:

1. They no longer derive the bulk of their income from owning agricultural land, and more people than ever before have access to economic opportunities in the city.

2. They no longer want to live in Lahore. They expect the comforts of Lahore to be available to them in Gujranwala.

This is reflected in how people live in the city, but also in what kinds of businesses exist there, and therefore what kinds of jobs are available in Gujranwala.

The economic uplift of agglomeration

Businesses beget other businesses, and one of the surest ways of seeing if the formal sector of an economy is growing in a particular region is to look for businesses that provide services to other businesses. The easiest example of these are accounting firms, and law firms.

The first accounting firm in Gujranwala was set up in 1986, and now there is a high concentration of them located in offices near the railway station. Law firms are more common even in smaller towns, but there are now lawyers specializing in company and contract law in Gujranwala as well. Some of the older ones have been around for decades, but most are new and were established within the last 15 years.

What does this mean for people in this region? It means there is white collar employment in Gujranwala, which means there is more economic opportunity for an educated upper middle class to not just live there, but

build careers there.

In terms of your career, are you better off being a chartered accountant in Karachi than in Gujranwala? Yes, of course. But before 1986, that was not even a question. You could not be a chartered accountant in Gujranwala back then because there was not a single firm with offices there. Now there are several.

This is a sea-change from decades past when the scope of employment in Gujranwala was restricted to being a labourer at a factory, or else working in small, informal retail outlets in the city. A handful of white collar jobs would exist at such places, but not many. Now, there are entire categories of white collar careers open to people who want to live and work in Gujranwala.

That rise of white collar professions then has a downstream effect: they want to live in those nicer homes, drive the newer cars that result in those auto showrooms, and since it was education that got them those jobs, they are the ones who pay the fees for the better private schools. Each family that fits this description adds more demand for services that make it possible for yet more families to join the ranks of the upper middle class.

And to the benefit of Pakistan, that upper middle class is no longer concentrated in the KLI cities (Karachi, Lahore, and Islamabad). Faisalabad was perhaps the earliest iteration of a non-KLI city with an elite that liked living in the city itself and created demand for the upper middle class life there. Now Gujranwala and Multan have joined their ranks, and judging by some other metrics, we may soon be writing similar stories about Bahawalpur and Peshawar.

Gujranwala, for its part, is done playing second fiddle to Lahore. It is determined to rise as one of Pakistan’s major metropolitan areas in its own right. And regardless of whether or not you live there, all of us in Pakistan benefit from this. n

Power companies worth less than the cash on their balance sheet

The recent cancellation of CPPA-G related contracts have spooked the markets to future prospects, leading investors to think that the worst is not yet over for these companies

By Zain Naeem

His eyes sting from the sweat dripping down his face. He takes interrupted, shallow breaths as it hurts to take deep ones; a mark left by the beast which now lies dead and vanquished. He looks down at the weapon in his hand. There is little in the way of differentiating his own blood from the one whose lifeless body is near his feet. A crowd cheers loudly as the arena around him echoes with the cheers and jeers around him but his focus is steady. All his concentration is fixated on the exalted emperor sitting on the throne. His gaze is stuck on the thumb. The thumb and gesture that will decide his fate. The emperor rises and his arm protrudes from his ceremonial garb. As the arm is raised, his fate is sealed. It might seem barbaric and treacherous now that the life and death of someone can be decided by a chosen few. But the reality still exists. Just like the blood absorbed by the dirt that lays at the gladiator’s feet, the truth is also there that the future of a company can be decided by investors in the stock market.

Power generation companies have recently seen their Central Power Purchasing Agency (CPPA-G) contracts end with the government which has meant that a huge chunk of their revenues and income has been taken away. Based on that decision, there are companies listed on the stock market which are seeing their price plummet. So much so that there are a few companies which are worth more dead than alive based on their stock price.

The polleo is held by the investors in the market and they seemed to have voted that with a resounding thumbs down to some of these companies.

Background of power generation

It might seem like a thing of the past but loadshedding used to be a persistent annoyance well into the mid-2010s in most of Pakistan. Power breakdowns and failures were an everyday occurrence and it was not uncommon for people to suffer through the hot summer months with no electricity. The government was battling with investment and infrastructure to develop its power generation capability.

This shortfall can be traced back to 1985 when the government formulated a long term strategy for development of the power sector. The purpose of this strategy was to spur economic growth and to make sure the

power sector was able to meet the demand. In the next 10 years, demand for power grew at 12 percent while supply lagged behind at 7 percent. The gap reached a peak of 1,500 MW by 1994.

To address this increasing problem, the 1994 Power Policy was developed. The aim of this policy was to help attract private sector investment in the power sector in order to bridge the generation capacity shortfall.

The new solution was to encourage the private sector to set up power plants which could be used to power their own factories while the government would buy electricity from these companies as well. This led to the creation of a Central Power Purchasing Authority which was responsible for buying and paying for the power produced.

Since this first step into this foray, there have been supplemental policies made in this area in 1995, 2002 and in 2015. At each step, more and more IPPs were established which sold to a single buyer which was the government. It was the government which then sold this power to different distribution companies.

In return for providing the electricity, the IPPs were given a set compensation based on their capacity of production rather than the power that was actually being bought. In order to attract investment, the power producers were given the right to charge based on their capacity rather than their sale. This decision was a stop gap solution as it was expected that all their capacity would be bought owing to the shortfall in demand and production.

Another caveat in the contracts was that these contracts would be made for 30 years after which they would be renewed considering the circumstances that existed. The first contract that was signed would expire in the 2020s when it would be reviewed. These agreements were skewed to provide benefits to the IPPs in order to make them attractive and lucrative.

The latest wave of IPPs which entered the market took place in 2015 which led to the establishment of 13 IPPs mostly by Chinese companies. By 2018, 40 IPPs were operating in the country and the contracts that had been done with them had some time before they would lapse.

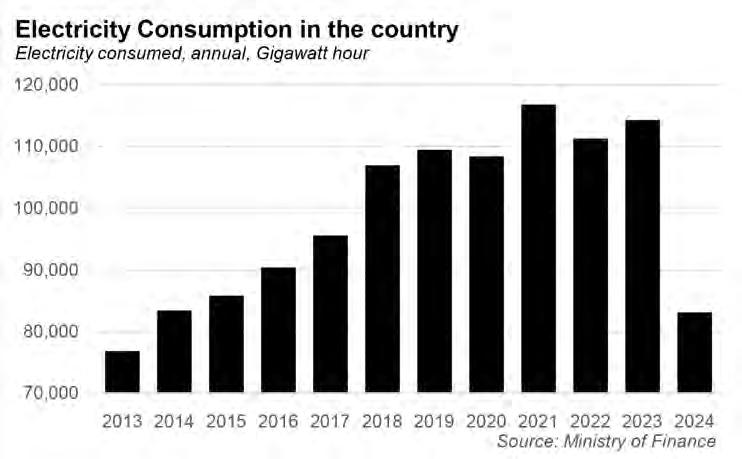

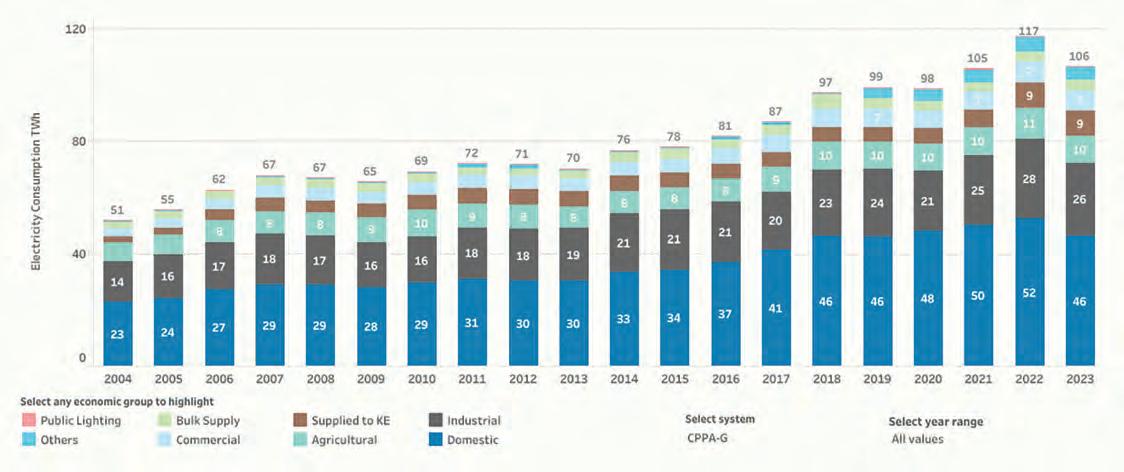

When these contracts were being made, there was little expectation that demand for power would actually start to fall. In 1991, the demand stood at around 31,534 gigawatt-hours (GWh). By 2014, this demand had more than doubled to 76,789 GWh. From 2014 to 2021, this demand steadily increased to 116,816 GWh. If this trend had continued, demand could be

expected to keep rising.

This, however, did not take place. In 2022 and 2023, demand slightly fell to 114,000 GWh before plummeting to only 83,109 GWh in 2024. If the trend had continued, the increase in demand would have been met with the help of the IPPs and the capacity charges would have been triggered. Demand failed to increase and actually fell to levels seen in 2015.

To put things into context, the IPPs that came online after 2015 became obsolete to a huge extent as their production was not required anymore. With no demand to meet, these plants could be shut down by the owners as there was no need to keep operating them. A new issue started to rear its head when lower demand was matched by capacity charges that still had to be paid.

Pakistan was already grappling with circular debt in the power sector due to line losses, power theft and inefficiencies in the supply chain. With the address pressure of the capacity charges, the whole infrastructure would have collapsed. In order to relieve some of this pressure, the basic unit cost of consumers was increased.

This brought the country to an impasse. On one hand, they had to honour the contracts that they had signed with the IPPs. On the other hand, some relief had to be provided to the country as electricity was becoming too expensive to pay for. Residential consumers were getting exorbitant high bills which had to be subsidized to ease some of their pain. Industries had to buy expensive power in order to carry out production but it made them uncompetitive compared to other exporting countries.

Something had to give and the decision was taken to renegotiate the contracts that had been signed in the past. A new model of take and pay was going to be adopted which would reduce the cost that was being incurred in terms of the capacity charges. The government paid off what it owed to the IPPs at a discount, cleared their dues and terminated the old contracts. New contracts were drawn up which had much more stringent terms leading to a formula based on usage alone.

Stock markets’ reaction

As new contracts are being drawn up, the stock market has reacted to the development by showing its disapproval. There are companies listed on the stock exchange which have seen their prices fall. Some of the companies have seen a fall so large that they are trading below their net book value, net current asset value and net cash value. Seeing such a strong reaction to the stock prices does beg the question. Why are the companies being traded at such a low value?

To answer this question, the financial statements of 15 of the listed power generation companies have been considered. Three distinct values are being derived from the balance sheets to see the amount of assets less liabilities the company holds. These are net asset value, net current asset value and net cash value.

Net asset value is the value of the company once all the assets are sold off and are used to pay off all the liabilities. The remaining amount is owed to the shareholders and this amount is divided by the number of shares in order to determine the net asset value or book value per share.

Net current asset value considers only the current assets of the company and subtracts all the liabilities from the current assets. The amount remaining is then divided over the number of shares to determine how much each investor can expect in terms of the current assets held. The logic of using this metric is that it considers assets which can be sold easily and quickly within one year. By taking out the fixed assets, only the more short term assets are considered using this measure.

Lastly, the most liquid measure can be determined which only considers bank balance, short term investments and trade debts. The understanding is that these assets can be converted into cash within a months’ time and can be recovered. Once the cash amount is determined, current liabilities are deducted from this cash value and then divided by the number of shares. This can be considered the most drastic measure as it considers the least amount that can be liquidated and then given to the shareholders.

But what is the significance of these measures?

The stock market is the best reflection of how a company is perceived and what people are willing to pay for it. The investors carry out a collective decision in terms of what a company is worth to them. This value is based on the worth they attach to the company and its shares. A share price prevailing shows what value the market attaches to the company.

Investors combine the recent results, the assets on the books of the company and future prospects and then ascertain the value that they should be tied to a company. Based on all the expectations combined, they bid or sell the share as they feel this is the true value.

One thing that has to be mentioned here is that all these three elements taken into consideration by the investor can be given a numerical value as well. The asset value is the base value of what the company is worth. The net book value can be considered this starting point for the valuation. The recent results of the company can be priced into the value of the share. A profitable company will trade at a

high price as it can earn more in the next quarter and further add to this value. Lastly, future prospects of the company, its profits and dividends given out in the future can be discounted back and can help in giving a number to the investor at which he wants to invest.

So what about a company which is trading below its net cash value?

A company trading at a value below its net cash value means that the company is being seen by the market as being virtually dead. The company would be worth more today if it stopped operations, settled its accounts and paid out the excess to its shareholders. Consider a company XYZ which is trading currently at Rs25. Analysis shows that this company had a net book value per share of Rs64, a net current asset value of Rs40 and net cash value of Rs27.

Based on the accounts alone, the investor should be willing to pay at least Rs27 to Rs64 for such a company. The price can go even higher for a company which is making and earning profits and has good future potential to grow on these profits. But the market is valuing such a company at only Rs25. This means that not only are they ignoring all the three measures mentioned but in terms of forward looking, they expect the company to make losses in the foreseeable future.

A loss made by the company starts to weigh down on their assets and increases their liabilities. The market is giving its verdict that they do not want to pay for even the lowest amount of assets that are held by the company. The reason behind this is that they expect the next few years to be lean and expect the losses to eat into the assets accumulated. Now substitute the company name from XYZ to Nishat Chunian Power which actually disclosed this situation in its most recent accounts.

These companies are termed as being better dead than alive. Just by selling their assets, these companies can expect to get a much better price compared to how they are being perceived if they keep operating. The net cash value can be used as the litmus test for such a company as it is the least amount that can be recovered even if all the remaining assets are ignored. For a company to be trading at such a low price, it would be better to end the hemorrhaging of profits rather than keep functioning.

But why such a sudden fall? That is connected to the fact that Nishat Chunian was one of the earliest IPPs that was established in the 1990s and expects most of its revenues from selling its power to the government. Even when demand fell by the wayside, Nishat Chunian was able to earn capacity charges which meant it was not producing electricity at any cost and was able to earn as it had a power plant that could provide power. Now

that its contract is being cancelled, these revenues would no longer be a guarantee. Even if they chose to go into a take and pay model, they would see their costs rise leading to lower profits and even losses.

So the market is passing a judgement on whether they see a company surviving into the future or see much bleaker prospects for their future.

The detailed analysis that has been carried out looks to grade each of the listed IPPs which are categorised as part of the power generation segment. The market price is then compared to the book value, net current asset value and net cash value. Companies whose share prices are above their net book value are graded as A. This is due to the fact that the market sees their future prospects being much brighter which is why they are willing to pay more than their total assets are worth.

Based on this scale, Altern Energy, Mughal Energy, Hubco Power, Pakgen Power and S.G. Power Limited get an A grade. Among these, Altern,Mughal and S.G. Power actually made losses this year, however, still the market expects these companies to rebound and get better results in the future. They are voting with their cash book by paying a higher price for these companies as it is.

On the scale, a B grade is given to companies that have market price below their book value but higher than their net current assets. Based on the current assets held, the investors feel that these companies have value and can be profitable in the future. A B grade is earned by Engro Qadirpur, Kohinoor Energy, Kohinoor Power, Saif Power and Tri-Star Power Limited. These companies can be seen as ones who might have suffered losses for consecutive years and due to that, the share price has fallen below their book value.

C grade is given to companies which have at least been able to have a market price above the net cash value. These companies can have issues in terms of their profitability but are still worth more in the market than being sold for parts by liquidating their short term investments and cash. A C grade has been earned by Sitara Energy and Lalpir Power.

The last are the companies which got a D grade as their market value has fallen below its net cash value. These companies have a better value if they are liquidated rather than continue working as their prospects are not going to improve any time soon in the future. It would be better to sell off the assets and pay back the investors as they can expect a better return rather than selling their shares in the market. The market judges that this grade should be given to Kot Addu Power, Nishat Chunian Power and Nishat Power.

The worst of these companies is Kot Addu which is trading at a discount of 25% be-

low their net cash value. Investors are actually losing value as it is and based on the fact that the contracts of all three of these companies have been cancelled, there is little likelihood that the prospects are going to change anytime soon.

So why does this situation exist and what is stopping the management from liquidating the company?

The answer is that the management is dependent on the company for their livelihood and selling off the business would mean that their stream of income will end. The job of any management is to carry out their functions within the organizational hierarchy and are compensated for the services that they render. If the company shuts down, this compensation will not be paid out any more.

In its most recent annual results, the Chief Executive of Nishat Chunian earned around Rs2.4 crores for the year while its 42 executives earned Rs11.7 crores or 28 lakhs individually. If the company is sold off, this income will have to be forgiven which seems highly unlikely. Kapco gave their Chief Executive Rs9.4 crores in 2024 while their 53 executives took home Rs46.6 crores or 88 lakhs each. Nishat Power gave Rs3.4 crores to its CEO while 104 of its executives took Rs41. 6 crores or almost 40 lakhs each.

On the other end of the spectrum are the shareholders or investors who have invested in the company expecting it to perform and earn profits. Once the contracts have ended, they would expect the management to either look towards new streams of income or to give them their investment back. The management and the shareholders will be at odds with each other over the future of the company.

To bridge the gap between the two parties, the owners get to elect a board of directors who overlook and monitor what the manage-

ment is doing and act in the best interest of the shareholders. If they feel shareholders can be better off through the liquidation, they would start working on that process.

Again this is a reality which seems highly unlikely as most of the boards at these companies are the original owners who established the companies in the first place. In addition to that, many of the board members are connected to the original owners which makes it highly unlikely that dissolution will even be thought about.

So it is clear to see that even when the best course of action would be to return the investment back, there is little chance that the status quo can be changed by the minority shareholders. But what if someone else enters the market. In the 1980s Leveraged Buyout days of Wall Street, these companies were the meat and drink. A big investor would swoop in and buy the shares at a low price. Once the control was gained, the company would be stripped of its assets which would actually add to the return earned by the large investor.

A simple back of the envelope calculation shows that shares can be bought at Rs25 and then the assets can fetch a value of Rs65 netting around Rs40 per share to the large investor. There is engrained value that exists at the company but based on its prospects, it is better to liquidate rather than destroy some of this value going forward.

Expecting the status quo to change any time soon can be considered a distant dream (read nightmare for the management) which will never come to pass. In terms of hypothesizing a theory, it can be seen that the concept of better dead than alive is pertinent to the power sector of the country and some value can be realized through this process. As this will not happen, the value can be expected to wither away in the near future. n

Pakistan’s circular debt strategy unfolds through

Government’s new plan is built on the foundation of compliance from commercial banks

By Ahtasam Ahmad and Hamza Aurangzeb

In Pakistan’s macroeconomic circus, the power sector has taken center stage. As the government works to stabilize the economy, resolving power sector issues has emerged as a critical priority. This focus was evident during recent negotiations with the IMF for the First Review of the 37-month extended arrangement under the $7 billion Extended Fund Facility. A key highlight was the government’s plan to address Pakistan’s power sector circular debt crisis by injecting Rs1.5 trillion to clear outstanding liabilities.

Where will this money come from? Almost Rs 1.25 trillion of this injection will come from Pakistan’s commercial banks. The same banks that already have significant exposure to circular debt through previous lending to the energy sector. As part of a deal negotiated between the government and the banks, this financing will happen at below-KIBOR rates, potentially reducing the government’s debt servicing costs by 3-5%. Despite a report in Dawn claiming that banks have been pressured into the deal, Profit has been reassured by high-ranking banking executives and government functionaries alike that this is not the case.

While the jury is still out on what happened during these negotiations, the real question is, how does the scheme actually work? How will this refinancing take place? And perhaps most intriguingly, what convinced banks to accept what appears to be an unfavorable deal?

Making of the crisis

Pakistan’s power sector struggles with a persistent circular debt problem rooted in a complex web of unpaid obligations that has grown increasingly intricate over the years. At its core lies

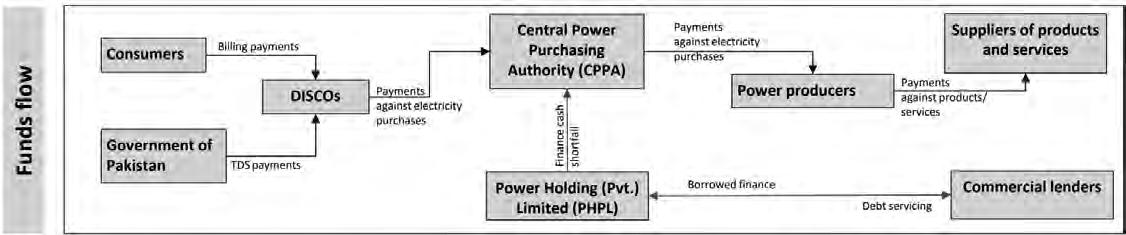

the unfunded outstanding liability of power distribution companies (DISCOs) and K-Electric (KE) to the Central Power Purchasing Authority-Guarantee (CPPA-G), a situation that has become more precarious with each passing year.

When DISCOs fail to clear their dues to CPPA-G, it creates a cash shortfall, prompting Power Holding Private Limited (PHPL) to borrow funds to cover CPPA-G’s liabilities. This cycle of delayed payments represents the accumulated circular debt in the country.

The PHPL is a state owned entity that serves one main function: managing and holding circular debts, which are essentially outstanding payments within the power sector. It is essentially a place where the government can park its circular debt and think about it later.

The growth of this circular debt and the need to park it somewhere can be attributed to five fundamental factors that have created a perfect storm in Pakistan’s power sector. High power generation costs have severely undermined DISCOs’ ability to effectively collect revenues and manage their operations, creating a persistent gap between costs and collections.

Compounding this problem are the

chronic issues and delays in tariff determination, which have left the sector struggling to maintain financial equilibrium. The situation is further exacerbated by high transmission and distribution losses, coupled with poor revenue collection by the DISCOs, which have steadily widened the funding gap beyond sustainable levels.

The government’s partial and often delayed payment of tariff differential subsidies has added another layer of complexity to the sector’s financial woes, while high borrowing costs for PHPL and expensive late-payment penalties on CPPA-G’s payables have created an additional burden.

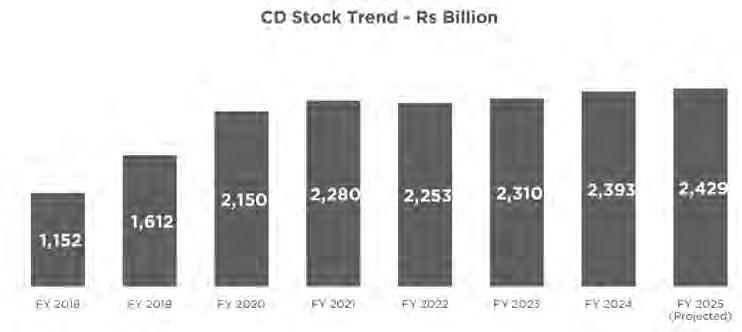

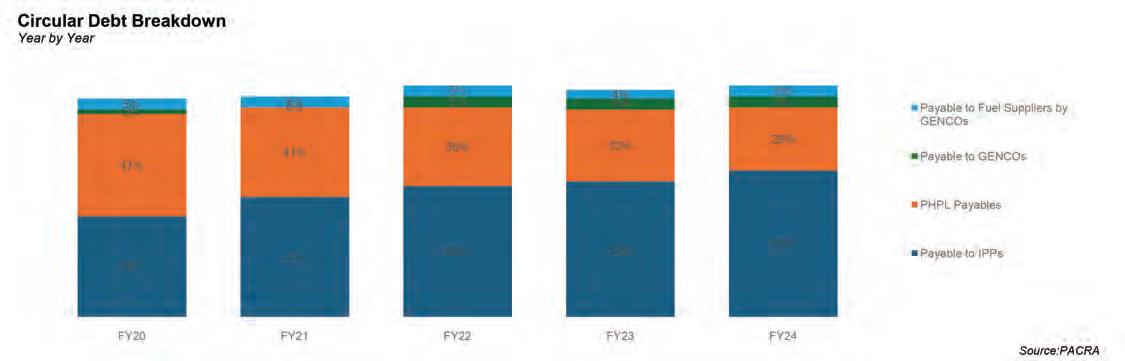

In Pakistan’s power market, consumer-end tariffs are deliberately set below actual electricity supply costs, with government subsidies attempting to bridge the gap. However, as costs persistently exceed revenues, the sector’s financial deficits have averaged an alarming 2.8% of GDP during FY14–FY24. By June 2024, the total circular debt reached Rs2.4 trillion, equivalent to 2.3% of GDP, representing an almost 50% growth from FY19. The debt stock is divided into payables to power producers, outstanding debt on PHPL books and amount owed to fuel suppliers by generation companies.

Source: Asian Development Bank

The current debt service surcharge is only enough to pay the interest on the outstanding stock of circular debt, given the current financing rate that ranges from KIBOR +2% to KIBOR +4%. However, when the government refinances this existing stock of debt at a rate of KIBOR-0.90, the same debt service surcharge will be sufficient to pay off both the principal and interest over time.

Mustafa Pasha, CIO at Lakson Investments

Exhibit: Sensitivity Analysis

Source: Media, AHL Research, * based on 106 bn KWh

This rapid acceleration in debt accumulation began in earnest in 2018 with the signing of “take-or-pay” contracts for imported coal and gas power plants, a decision that increased capacity payments by 50% and exposed the country to the volatile whims of international fuel prices—a vulnerability that became painfully apparent during the global energy crisis of 2022.

The implications of these structural energy sector problems extend far beyond the power industry itself, creating a complex

web of challenges that affect Pakistan’s entire economic landscape.

Numbers behind the idea

The government of Pakistan has received a conditional nod from the International Monetary Fund (IMF) to borrow Rs1.25 trillion from commercial banks to address the country’s power sector circular debt. This borrowing is part of

a broader Rs1.5 trillion debt resolution plan, with the remaining Rs250 billion coming from existing budget allocations.

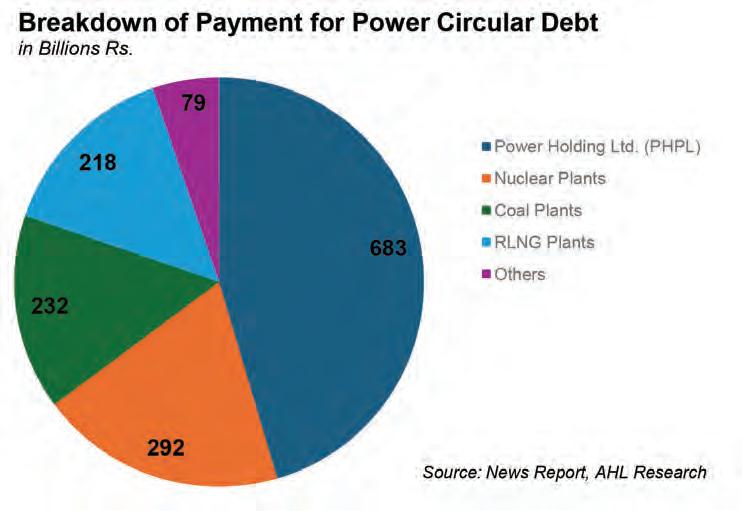

The new financing will be secured at KIBOR -0.9% on CPPA-G’s books, offering substantial savings compared to current PHPL borrowings at KIBOR +2% and late payment surcharges to IPPs that goes up to KIBOR +4%. The funds will be distributed across the energy sector with Rs683 billion for PHPL, Rs 292 billion for nuclear plants, Rs232 billion for coal plants, Rs218 billion for RLNG plants, and Rs79 billion for other facilities.

To repay this debt, the government will utilize the existing Rs3.23/KWh debt servicing surcharge already being collected from consumers. Based on Pakistan’s 2023 electricity sales of 106 billion KWh, this surcharge generates approximately Rs342.8 billion annually. With annual financing costs of Rs138.75 billion under the new arrangement, Rs204.1 billion will remain available for principal repayment. If this surplus is fully directed toward paying down the debt, the government could potentially clear the obligation within about six years.

“The current debt service surcharge is only enough to pay the interest on the

Now cash flows in the shape of an already existing debt service surcharge in the electricity bills will be utilised by the lenders to be recovered at source for loan repayment. There will be no new burden on consumers and this deal will help in clearing up all the new and old debt in the next four to six years, depending on where the interest rates stand. Lower the interest rates, quicker the payment of this 1.25trn debt

Masud, Pakistan Banks’ Association Chairman

outstanding stock of circular debt, given the current financing rate that ranges from KIBOR +2% to KIBOR +4%. However, when the government refinances this existing stock of debt at a rate of KIBOR-0.90, the same debt service surcharge will be sufficient to pay off both the principal and interest over time,” remarked Mustafa Pasha, CIO at Lakson Investments.

The Bank’s perspective

Pakistan’s banking sector already shoulders a significant burden from the circular debt stock. Banks maintain exposure to long-standing PHPL borrowings with no clear repayment streams in sight. Additionally, Independent Power Producers rely on short-term bank financing to address working capital shortfalls caused by payment delays.

Zafar Masud, Pakistan Banks’ Association chairman, explained: “Now cash flows in

Source: Pakistan Energy and Climate Insights Dashboard

Zafar

the shape of an already existing debt service surcharge in the electricity bills will be utilised by the lenders to be recovered at source for loan repayment. There will be no new burden on consumers and this deal will help in clearing up all the new and old debt in the next four to six years, depending on where the interest rates stand. Lower the interest rates, quicker the payment of this 1.25trn debt.”

The primary concern for banks is that this debt lacks government guarantees due to IMF-imposed restrictions. These same fiscal limitations prevented the government from converting existing power sector debt into public debt despite recommendations floating around last year. That would have involved issuing long-term government securities against outstanding power sector liabilities, potentially securing favorable rates than current PHPL terms or the steep late payment surcharges from power producers.

Moreover, the substantial sum being directed to the public sector might further crowd out private sector credit, which stood at approximately Rs9.3 trillion by February 2025’s end.

“The amount of Rs.1.25 trillion is indeed a significant amount to lend to the government but the banks have already lent a big chunk of this amount to PHL which is being refinanced and put on the books of CPPA-G. Therefore, the net impact would be significantly less. As far as the crowding out of the private sector is concerned, banks don’t want to lend to the private sector and the private sector does not want to borrow in the current environment. Banks traditionally have not lent to the private sector unless they are a blue chip corporate with solid credit rating and pledgeable assets. If lending to the private sector is viable and there is a conducive environment, banks will be able raise adequate liquidity and deposits to expand their asset bases to lend to the private sector,” Pasha added.

Further, the current repayment strategy appears well-structured, but faces a significant risk: Pakistan’s declining power consumption trends. February 2025 data reveals a 15% reduction in power output, driven by multiple factors including elevated energy tariffs, economic deceleration, and consumers transitioning to off-grid solutions. This downward trend could substantially reduce future revenue generated through the debt servicing surcharge, potentially undermining the viability of the proposed repayment timeline.

However, this isn’t the first attempt at the debt clearance. In 2013, the government paid off Rs480 billion to settle outstanding liabilities. However, the debt soon began accumulating again because the fundamental issue remained unresolved: the cost of electricity generation continues to exceed what

Particulars FY 25 Rs Billion

Base Case Scenario - CD Flow

consumers pay, creating an ongoing structural imbalance in the sector’s finances.

Fixing the rot?

While bringing down the stockpile of circular debt is important for fiscal cohesion, it is equally important that the underlying factors contributing to the accumulation of debt are also addressed. The government has already introduced Pakistan’s circular debt management plan 2024-25 to curb this accumulation. The salient features of the plan include improvement of DISCO losses, additional subsidy, markup savings, PHPL debt repayment, and clearance of a portion of power producers’ stock, to reduce the net flow to only Rs36 billion.

Currently, approximately 85-90% of end-consumer costs stem from generation expenses. Reducing these costs would require a shift towards least-cost technologies, particularly renewables, strict adherence to economic merit order, and avoiding further investment in excess capacity that could increase capacity payments, which already account for roughly 60% of generation costs.

While these measures appear promising on paper, the government’s true intentions might be better gauged through the Indicative Capacity Expansion Plan released last year. Unfortunately, the country’s energy planners appear to have overlooked many of these considerations, instead opting for expensive projects likely to increase generation costs.

The rapid pace of solarization also suggests that demand projections may be overestimated. Perhaps most tellingly, the CDMP document’s opening disclaimer that “The Plan also assumes that GoP committed subsidies will be budgeted properly and released in a timely manner”, suggests these projections may be optimistic at best.

To its credit, the government has imple-

(275)

mented bold measures to address electricity cost issues, with a rate reduction expected in the coming days. The termination of Power Purchase Agreements for five power plants has already yielded savings of Rs0.57/KWh in tariffs. Additionally, the government has successfully negotiated with 18 Independent Power Producers to transition from a “take or pay” to a “take and pay” mechanism, potentially generating further tariff reductions of Rs0.67/KWh.

Analysts suggest several potential strategies to further drive down electricity costs. Redirecting gas from the 1,500 MW of inefficient captive power plants to more efficient IPPs could potentially double the generation capacity to 3,000 MW while reducing electricity costs by Rs3.35/KWh.

The government’s recent decision to maintain petroleum prices while increasing the Petroleum Development Levy from Rs60 to Rs70 per liter is expected to generate Rs53 billion in additional revenue. This could facilitate a power tariff reduction of Rs0.84/KWh across the board, or a more substantial Rs2.60/KWh specifically for domestic consumers using up to 300 units.

For FY25, if the base case for the government is to sell 106.14 billion units, a 5% increase in power consumption could lower the average tariff by Rs1.17/KWh.

Debt restructuring with Chinese IPPs, which constitute 20% of total power capacity, presents another opportunity—extending the repayment periods for front-loaded debts could yield savings of Rs277 billion and reduce tariffs by Rs2.61/KWh.

The approved transmission and distribution losses for FY25 stand at 11.43%. Reducing this threshold by 5% could result in tariff reductions of Rs1.90/KWh. Current transmission infrastructure challenges, including overloading and insufficient capacity, continue to contribute to system inefficiencies. n

InDrive invests $10mn in Pakistan’s Krave Mart to accelerate super-app ambition in emerging markets

Investment to support Krave Mart’s expansion in Pakistan and potentially venture into other markets

By Taimoor Hassan

InDrive, the global ride-hailing giant, has made a strategic $10 million investment in Krave Mart, a rapidly growing Pakistani grocery delivery startup, two sources confirmed. This move underscores InDrive’s growing focus on expanding its reach and identifying growth opportunities in emerging markets. The investment is part of InDrive’s broader venture capital strategy launched in 2023, with the company allocating $100 million to invest in startups in developing countries like Pakistan.

Founded in 2021, Krave Mart operates as an online grocery delivery platform, or quick commerce, offering fast and efficient services to urban households in Pakistan.

Speaking to Profit, Kassim Shroff, the founder and CEO of Krave Mart, said that since the investment, Krave Mart has been able to grow by three-times. “The company has been able to improve its delivery times which suffered during the investment crunch.”

Shroff emphasized that the company has also maintained slow cash burn, a crucial factor in ensuring long-term sustainability, while also enhancing its assortment of products and competitive pricing.

As the company looks ahead, it will likely continue to focus on its growing product portfolio, faster delivery times, and more competitive pricing to stay competitive in the evolving online grocery delivery market.

With this new funding, Krave Mart plans to expand its operations within Pakistan and potentially venture into other markets. The startup’s growth comes amid the challenging backdrop of Pakistan’s economic landscape, yet Krave Mart has managed to outperform many competitors, including Airlift, which shut down its operations in the country.

Similarly, Cheetay also faced an unfateful end in quick commerce.

Today, Krave Mart competes with giants like Foodpanda, backed by Delivery Hero, in some urban centers, owing to its emphasis on private-label products and operational efficiency.

On the other hand, InDrive’s investment in Krave Mart is aligned with its long-term ambition to become a superapp. Andries Smit, the head of InDrive’s New Ventures unit, had earlier emphasized that the company’s investment approach is focused on identifying opportunities that align with this vision. “Our strategy is to become a super app, and we are optimistic that our partnership with Krave Mart will contribute significantly to that vision,” Smit stated.

As part of this strategy, Krave Mart would also be listed on the InDrive app, fueling

the emergence of InDrive’s super app ecosystem in Pakistan.

InDrive, which has rapidly expanded to 46 countries, has built its success on allowing passengers and drivers to negotiate fares, making it the second-most downloaded ride-hailing app globally in 2024, according to data.ai. Its investment in Krave Mart follows an earlier partnership with micro-insurer MIC Global, reinforcing its commitment to exploring opportunities that align with its business model.

Additionally, InDrive’s venture arm has made a similar investment in Kazakhstani grocery delivery startup Ryadom, continuing to strengthen its footprint in emerging markets. n

Note: This article follows up on a previous report published in December 2024, confirming that InDrive’s

OPINION

Abdullah Niazi

Punjab’s changing urban reality requires empowered local governments

If you start driving on the M3 from Multan, carry on towards Lahore before getting on to the M2 and drive all the way up to Talagang near Rawalpindi, you will pass over the Ravi, Chenab, and Jheulum rivers in that order.

For anyone that has travelled frequently from Lahore to Islamabad, these rivers are important landmarks in the journey. And all the way up to the federal capital, both sides of the road are framed by lush fields of wheat, mustard, and other cash crops. While the greenery of the Punjab is as familiar as it is ancient, the demographic and agricultural landscape of the province are vastly different to what they were in living memory.

At least up until the end of the 19th century, much of Punjab was arid or semi-arid land, including many of the very fertile and valuable agricultural lands we know today. The birth of the Punjab we know from our social studies textbooks took place in 1886, when the British Colonial government built the Punjab Canal Colonies.

Much of what we know today as Pakistan is a result of the British appetite for wheat. The British constructed railways in what is now Pakistan in 1855, in no small part due to a desire to connect the wheat-growing parts of Punjab and Upper Sindh to the port in Karachi. In 1886, the British were able to start building the Punjab Canal Colonies, which were a series of large, previously sparsely inhabited areas in Punjab, that were brought under cultivation through the use of canals that diverted water from the province’s five rivers. Those canals allowed for previously landless and poor farmers to settle in newly cultivable regions, and the railways helped them sell their surplus crop to the rest of the British Empire.

After partition, the landowners in these new canal colonies (many of whom had been reluctant accepting these lands) were the new elite of the province. By virtue of being landowners, they exercised great political and economic control over their areas. However, most of these landed elites chose to live in Lahore. After all, their lands were in areas that were vastly underdeveloped. Their yields were high but the British had designed these colonies for agricultural efficiency, not for living. Lahore is where Punjab

The writer is senior editor at Profit. He can be reached at abdullah.niazi@ pakistantody.com.pk

Politics came to a boil, this was the old seat of power that had been a crown jewel of the Mughals, Sikhs, and British alike. This is where the party was and it is where people wanted to build their homes, educate their children, and live their lives.

For decades, the centrality of Lahore remained. But as the past few weeks of Profit’s coverage has shown, this is rapidly changing. This week, our cover story focuses on Gujranwala and its speedy ascent to becoming one of the largest cities in Pakistan, and a clear Metropolitan area within Punjab. The week before, our coverage focused on the rise of other such ‘greater’ metropolitan areas in the province. Our findings show that smaller districts that once orbited Lahore are now exerting their own gravitational pull, with the creation of business and immigration taking place. What is more, these cities offer many of the same upper-middle class amenities that people would once move to Lahore for. All of this has happened naturally. The Punjab has gone from a semi-arid province with a mighty river system single handedly running its agriculture, to a region with a complex network of canals that turned it into a colonial bread basket, and now into a province that is quickly blurring lines between rural and urban. As this new iteration of Punjab manifests itself, one must remember that it can only really thrive through efficient local governments. Just take a look at the Gujranwala Metropolitan Area discussed in this week’s story which includes Sialkot and the Sialkot Airport. There is a clear will among these regions to develop their districts, and a pride in them that cannot be understood by a government in Lahore. In every conceivable way, local governments make sense. We are not speaking here specifically of any local government acts that have been passed in Pakistan, but generally of a third tier of democracy as a concept. It is a more efficient administrative system and adds another tier to the democratic process, making accountability and access to said administrators a less arduous process than it currently is. It also allows communities to look out for and administer themselves in accordance with their own best interests.

By this we do not just mean governance on a UC level about street repairs and sewerage (even though these topics are often more important than macro problems). What we mean to say is that if Gujranwala can develop at this pace by itself, imagine what it could do with an empowered and elected Metropolitan Corporation collecting taxes, spending money, and directing policy for the growth of these districts which have already proven their mettle.

Local governments have been another issue highlighted in this publication recently. Only two weeks ago Profit reported on how nearly a trillion rupees earmarked for local governments have been misappropriated by the provincial government in the last eight years. Last week, Dr Javed Younas pointed out how local governments can be gamechangers in combatting extremism. Unfortunately, despite the clear benefits and the obvious mishandling of this subject, local governments remain elusive. One can only hope that the stakeholders in a changing Punjab, particularly those in these new metropolitan areas, can realise it is in their best interest to advocate for strong local government. n

A national effort is needed for a sustainable future Sahar Aman

Pakistan is transforming its energy sector by emphasizing renewable energy to promote sustainability, enhance energy security, and provide economic relief. The government is renegotiating outdated energy agreements to establish a fair pricing model supported by a team of technical experts and policymakers. These efforts aim to reduce dependency on costly fossil fuel imports and create a sustainable energy landscape that fosters long-term environmental resilience and economic growth, ensuring a prosperous future for its citizens.

By the end of FY 2024, Pakistan’s total installed renewable energy capacity had reached 13,640 MW at the utility level, contributing 31% to the national energy mix. With net metering additions, this figure rises to 16,091 MW, 35% of total capacity and 36% of total energy generation. These advancements result from strategic government policies, regulatory frameworks, and private sector participation, demonstrating the country’s commitment to a cleaner, more affordable energy future. According to the latest Indicative Generation Capacity Expansion Plan (IGCEP 2024-34), Pakistan has set ambitious targets for the next decade, projecting that 89% (17,456 MW) of total capacity additions will come from renewable energy sources by 2034. By that time, renewables will constitute 55% of Pakistan’s installed capacity, with clean energy sources (including hydropower) making up 73% of total generation.

Pakistan's renewable energy reform focuses on addressing inconsistent tariffs. Older projects, especially wind power plants, were developed under policies with higher tariffs that now exceed market rates. This leads to higher costs for consumers and the national power sector, while newer projects benefit from lower tariffs due to technological advancements. A government task force is working to renegotiate these outdated agreements to align tariffs with current market conditions and maintain investor confidence in the energy transition. It is important to address misinformation suggesting that the

Pakistan Army is involved in these negotiations. These discussions are conducted exclusively by government authorities and regulatory bodies such as the National Electric Power Regulatory Authority (NEPRA) and the National Transmission and Dispatch Company (NTDC). A dedicated task force comprising energy sector professionals and financial analysts oversees the renegotiation process to ensure the agreements are revised transparently and fairly. The government has emphasized that military institutions are not part of these negotiations, as this is purely a policy-driven and regulatory matter under civilian governance.

One of the most significant advancements in Pakistan’s renewable energy shift has been the rapid adoption of net metering and distributed solar energy. By FY 2024, the country had integrated 2,451 MW through net metering, marking a 148% growth rate in just one year. This momentum continues into FY 2025, with an average addition of 283 MW per month in the first quarter alone. Initial estimates from IGCEP 2024-34 projected an additional 2,107 MW in net metering by 2034. Still, recent trends suggest this figure could exceed 8,000 MW, driven by increasing public demand, government incentives, and falling solar panel costs. Additionally, off-grid and behind-the-meter solar installations have expanded significantly, with estimates suggesting that 12,027 MW of solar energy capacity operates independently of the national grid. This transition empowers businesses, households, and industries to generate power, reducing dependency on expensive grid electricity and lowering consumer costs.

Pakistan's renewable energy expansion offers significant economic benefits. By reducing fossil fuel imports, the country can save foreign exchange and ensure greater stability. The long-term affordability of renewable sources will lead to lower electricity costs for households and businesses. Additionally, the sector will create jobs in solar panel manufacturing and maintenance, supporting local industries. Increasing clean energy will also help reduce air pollution in major cities like Lahore and Karachi, addressing environmental and health issues.

Despite these positive developments, challenges remain in achieving a seamless transition to renewable energy. Grid integration remains a key issue, as managing variability in solar and wind generation requires advanced forecasting, battery storage solutions, and modernized grid infrastructure. While renewable energy technology costs are declining, initial investment barriers still pose challenges for widespread adoption. Expanding green financing options and streamlining the regulatory framework will be critical in overcoming these hurdles. Bureaucratic inefficiencies have historically slowed the progress of energy reforms, and ensuring stable, transparent policies will be essential to attracting continued investment in the sector.

The writer is a freelance columnist

The government remains committed to ensuring the transition to renewable energy is fair and sustainable. This means ensuring that past agreements are reviewed in a structured manner while maintaining investor confidence. The renegotiation process is not about undermining energy companies or discouraging investment but rather about making energy pricing fairer for consumers. Investors who entered the market under previous policies will be given reasonable adjustments rather than being subjected to forced revisions that could harm business confidence. At the same time, the government recognizes that Pakistani citizens should not have to bear the burden of unnecessarily high electricity costs due to outdated agreements.

Pakistan’s renewable energy transformation is driven by strong governance, technical expertise, and policy reforms, rather than military involvement. With a focus on fair energy deals and sustainability, Pakistan aims to build a resilient energy sector. If effectively managed, this transition to renewables will enhance energy security, stimulate economic growth, and promote environmental sustainability for future generations. n

What

happened during Symmetry’s closed period?

A line was stepped over and the overstepping was acknowledged. What will the SECP do in response?

By Zain Naeem

An unseasonably chilly February evening in Karachi. A generic looking conference room in Corporatistan. The frosted glass creates an impenetrable bubble for the corporate executives from the outside world. A junior accounts officer fidgets in his chair once more as he is unsure of the protocol he is supposed to follow. His senior sitting next to him sits lower in his chair browsing his phone to kill some more time. A secretary sits in the corner of the room waiting for the board members to join. The meeting was called at 5 PM but it will eventually begin once the board members actually show up.

As the door opens, the first of the board members arrives. Salutations and greetings are shared before he takes his designated seat at the table. As more members start to arrive, there is a buzz of low conversation. Once the table is complete, the secretary is asked to commence the meeting as she starts to read the agenda items for the day.

It might seem like the meeting is taking place in February but the seeds of this meeting were sown nearly two months back when

the company closed its accounts at the end of December. Once January started, the accounting department at the company started to tally up its revenues and expenses that need to be recorded. The junior staff at the company started to post the entries and carry out a reconciliation of its accounts with reality.

As January turned into February, the juniors would have started to pass on the data to their seniors who would start to sign off on the important documents. According to the regulations set by the Securities and Exchange Commission of Pakistan (SECP), financial statements need to be finalized and submitted to the regulator and the stock exchange within a stipulated time period. For a company with its half year ending in December, this would be somewhere by the end of February.

Once the accounts have been finalized, they need to be approved by the board members and then released to the investing public. In order to approve and disseminate the accounts, a board meeting has to be called where the board members sit together, study the accounts and then approve them.

This development causes a huge wrinkle. There are insiders to the company who are purview to the accounts and knowledge of the company earlier than it is announced to the

public. The fact that the announcements of the results will cause the share price to change makes this information material in its nature. The fact that only a few people know it makes it non-public and hence allows them to foresee how the share price is going to react. Once the meeting has been called, it is the right of any board member to get a look at the accounts that have been finalized before the meeting takes place.

Due to their exalted positions, there are certain members on the inside of the company who are aware of developments taking place in the company which can help them earn an easy buck. A new contract being signed, a new plant being set up or a new client placing an order have the potential to increase the share price. Insiders can use this information to earn an easy profit.

In order to create a barrier for the insiders, the Pakistan Stock Exchange (PSX) mandates that any trades being carried out by the insiders have to be disclosed to the public as soon as possible. The trading pattern can hint towards a development that has not been announced and can guide the investors in terms of any new development that could be taking place.

Section 5.6.4 of the PSX rulebook dic-

tates that a director, CEO, substantial shareholder and executive of the listed company in addition to their spouse have to disclose any trading activity they have carried out in the shares of their own company. The individual is supposed to notify the company secretary who then has to disclose the price, number of shares, nature of transaction and market traded into the exchange within seven days of the trade being carried out. This is a manner in which the market can be informed in time.

Another provision of the same section is concerned with companies which are looking to carry out a board meeting. When accounts are being finalized, insiders have access to information that has not been distributed to the market. This leads to asymmetric information that the insiders have that outsiders are not aware of. This can give an unfair advantage to these insiders as they can trade using this information and get to make a profit by using this information.

So what is the cure to this? According to Section 5.6.4 of the PSX rulebook, companies have to restrict these insiders from trading by instituting a closed period. The closed period starts from the announcement of the meeting all the way up to the accounts being released. The rationale behind this is that as the insiders have the knowledge, they are not allowed to use this to trade and make a profit.

The purpose of this law is to present an environment of transparency and openness where no investor is disadvantaged. From the announcement of the meeting all the way to the release of the accounts, the investors are not aware of what is going to be released. Once it is released, both sides are then able to act on that information. Neither side gets to have a leg up on the other in this situation.

So what exactly took place at Symmetry?

On 19th of February 2025, the company announced that they would be holding their board meeting to review its December accounts on the 26th of February 2025. Within the announcement, there was a note that the closed period would go from 19th of February till the 26th when the results would be announced at 5 PM in the evening. The notification also stated the regulation that no insider was allowed to trade while the closed period was being observed.

The meeting took place on the 26th of February as scheduled, however, as the exchange had closed, the results were uploaded on the 27th of February at 8:35 AM before the market opened. The delay was due to the fact that when the exchange closes, no new announcements are uploaded until the next morning. This is a measure carried out as the release of the accounts would not have a huge impact as the market is closed.

The results showed a slight bump in the earnings for the company compared to last

year. The closed period had ended and the trading could go back to normal. On the 3rd of March, the company secretary at Symmetry sent a letter to the stock exchange that one of its directors had traded in the shares of the company. Everything seems to be above board until the date of the trades is seen. The trades were carried out on the 25th and 26th of February 2025. An executive director at Symmetry looked to sell shares of the company before the accounts had been released. On the 25th of February, he sold 1,182,530 shares at the rate of Rs 18.02 per share. The next day, he sold a further 1,005,000 shares at Rs 18.07 per share.

In terms of the regulation, the law had already been broken. As soon as the trades were executed, the director fell foul of the closed period that he had violated. In addition to that, the director subsequently bought back these 2,187,530 shares on the 28th of February at Rs 16.28 per share. Not only was the law violated but, after the results were announced, the director ended up making a gain.

How was that might you ask? The director had more than 2 million shares before the closed period. Once the closed period started, he ended up selling his holdings for Rs 39,469,541. Once the price dropped, he bought back these shares at Rs 35,612,988. This meant that he was able to net a gain of Rs 3,856,553 and held the same number of shares he held before. If he had kept his shares through the price fall, his portfolio would have lost value which he was able to avoid by selling and buying later at a lower price.

In reality, the director not only violated the law but also made a gain from this violation.

The question then raised is how was such a violation carried out and what did the company do in regards to it. The management at Symmetry was asked to provide an explanation in relation to the trades and how such a trade was allowed to go through.

In response to these questions, the company stated that “We acknowledge that our Executive Director inadvertently executed a trade during the closed period. This was a result of a genuine oversight due to limited understanding of trading regulations as a relatively new market participant. Upon realizing the mistake, he promptly informed the Pakistan Stock Exchange (PSX) and submitted a voluntary disclosure, acknowledging the unintentional nature of the transaction.”

The company further added “The matter was reported transparently, and corrective measures were immediately taken, including internal compliance notification and further education on PSX and [Securities and Exchange Commission of Pakistan] (SECP) regulations to ensure strict adherence moving forward. We want to emphasize that there was no ill intent or deliberate violation of regula-

tions, as evidenced by the swift self-disclosure and corrective action.”

When asked about the shares being bought back at a later date, the company answered that “(r)egarding your query on share repurchase, we wish to clarify that the company does not influence individual investment decisions made by directors or shareholders. Furthermore, any fluctuation in stock price post-results announcement cannot be attributed to this transaction, as Symmetry Group’s financial results demonstrated strong profitability growth.”

A follow up question was also sent in regards to the gain that was earned by the director and whether that had been compensated, paid back or surrendered. No response was received on this question from the company.

The trade is being presented as a whoopsie by the management and being chalked up to naivete of its directors and their lack of knowledge of market norms and regulations. The management also carried out the necessary education of its members to make sure the mistake will not take place again in the future.