09 Fundraising, pivoting, migrating, scaling down or just cruising? This is what Pakistani startups are up to.

13 The govt of Pakistan and its farmers are in a toxic relationship. These are the exact mechanics of this year’s fight over wheat.

16 The problem is access to credit, not payments, claims Abhi CEO at World Economic Forum

19 KIA Stonic’s price fall is a tale of lobbying, regulatory capture, and high margins. Here’s what went down.

25 Can fashion retailers cut costs by relying on AI models?

27 Despite litigation, consistent losses, and auditors raising red flag after red flag, Dewan Farooq Motors has remained a stable stock market investment. How in the world?

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi Director Marketing : Mudassir Alam - Regional Heads of Marketing: Agha Anwer (Khi)

Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

Fundraising, pivoting, migrating, scaling down or just cruising?

This is what Pakistani startups are up to Profit surveys all major Pakistani startups, and the results are in

Taimoor Hassan and Nisma Riaz

In the labyrinthine world of startups, Pakistan's budding entrepreneurs face a formidable array of challenges as they strive to carve their niche in the global marketplace. From economic volatility and regulatory hurdles to funding constraints, the landscape is fraught with obstacles that test the mettle of even the most seasoned founders.

As the spectre of a global downturn looms large, Pakistani startups find themselves at a critical juncture, grappling with the harsh realities of an unforgiving market. To put things into perspective, global startup funding has slowed down to a record low level, dropping to $285 billion in 2023, marking a 38% drop from $462 billion invested in 2022, according to Crunchbase News. This is the lowest point for VC investments in the last five years.

The first quarter of 2024 saw $75.9 billion invested in startups, which was the lowest amount of such investments since the first quarter of 2019, as the US Fed keeps the interest rates at record high of about 5.3% to fight stubborn inflation. The US Fed is expected to keep the rates unchanged until the end of this year, meaning that new VC investments will remain low for some time.

The cut down in funding meant that startups were required to prove their sustainability and generate their own profits. This would ideally lead to a better chance at fundraising for these startups as investors would consider them less risky bets if they had proven their sustainability.

But things seem to be very very difficult for Pakistan. Officially no new investments came into Pakistan in Q1 of 2024. The startup funding has seen a drastic drop in Pakistan. From its peak of over $380 million in 2021, startup funding dropped to $332.4 million in 2022 and stood at a meagre $75.6 million in 2023. As the second quarter of 2024 has kicked off but Profit has learned some announcements could be coming soon. Nonetheless, investors and founders predict a bleak funding outlook for the entire year.

In the background though, as per Profit’s findings, while the investment was extremely scarce for startups in Pakistan, startups were also struggling with achieving profitability and despite some level of profitability, startups were struggling with fundraising. Why is that the case and how are startups trying to navigate this scenario? Profit explains.

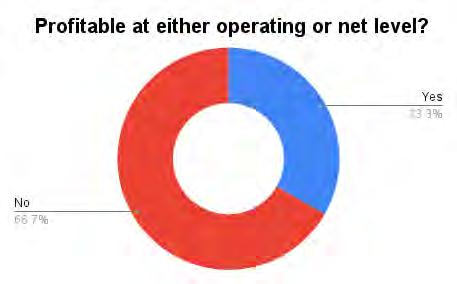

In a survey carried out by Profit in which 46

startups responded, only 8 (17%) startups said that they were profitable at operating level. Most of these startups shared this info confidentially and requested not to be named hence none of the names are mentioned. The startups shared this info with the understanding that the data would be aggregated.

On the net profitability side, only four said that they had achieved net profitability. Two of them, Pakwheels and Rozee have been around for over a decade or more and have been generating profits for a while now. Profit was able to verify Rozee’s profitability after

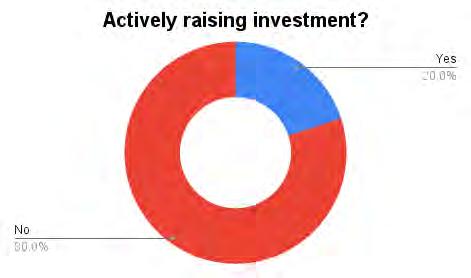

A majority of these startups, 36 (82%) out of 44 that responded, said that they were not actively fundraising for the reasons explained below. But what was rather more surprising was that most of the startups that had claimed operating profitability were also not actively fundraising. But through investors, Profit has learned that some of these startups were actively raising funds and were even close to closing rounds.

tax directly with the company which showed its audited financial accounts to confirm their profitability. The other two, PriceOye and PostEx that claimed net profitability, are recent companies and are navigating the downturn on the back of funding raised in 2021 and 2022.

Interestingly, 16 (36%) out of 44 of these startups had expanded abroad mostly to the countries in the Middle East. What’s in such expansion is explained below. Some of the names that had expanded abroad were Trukkr which has expanded to Bahrain, MedIQ which

has expanded to Saudi Arabia, edtech Outclass has also expanded to the Middle East, and EzWifi, which has expanded to Europe as well as the US. Savyour, which offers cashbacks and discounts, was also in the process of expanding its presence in the Middle East.

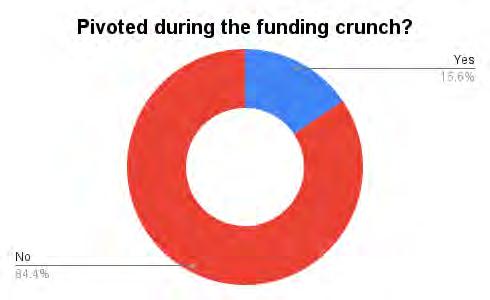

Out of 44 startups that responded, six (13%) had pivoted from their core business altogether and were now working on different models. A prominent name in this list is DGlobal, which in an earlier interview with Profit, had disclosed that it had moved towards building a banking software platform called DCore. DGlobal had earlier planned to become a digital bank and was one of the first applicants for the digital bank license that they were unable to get.

Another pivot is of Truckistan which has moved out of the transportation business and has moved towards a SaaS (Software as a Service) model.

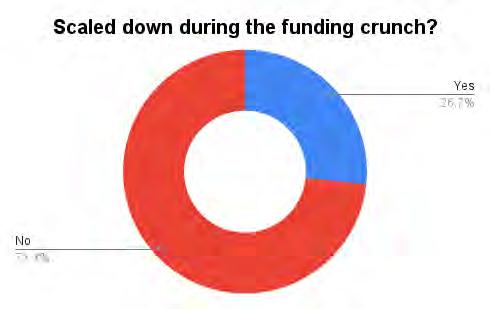

Surprisingly, out of the 45 startups that responded to this question, only 10 (22%) said that they had scaled down their operations during the investment downturn. None of these startups said that they were looking at a situation where they would have to shut down their operations. Earlier Profit has covered shutdowns of notable startups such as Airlift, TAG, Munchies and Cheetay. Some of the scale downs that have happened earlier and covered by Profit include ones at Dastgyr, Retailo, Paymob and Daraz.

On a case by case basis, startups had different reasons why their startups were not profitable, mainly pertaining to milestones that they had set for themselves. But the general complaint was the Pakistan baggage. That somehow, things have not been working for them in Pakistan where there is an economic uncertainty and slowdown.

To a great extent, that is true. Rising inflation is bound to take a hit on the topline and bottomline of companies. But what is also true is that every startup that started during the near zero-interest rate VC boom took the money to keep growing and try to outcompete the others, with hope that incremental capital will keep on coming, giving rise to unsustainable models. When such funding is raised, startups set milestones that with a certain amount of funding raised, they would be able to achieve a certain growth milestone. Investors would also

invest with the understanding that the capital would be spent on growth. That the startup will penetrate the market without worrying about profits, with the understanding that once these milestones are achieved, the money raised in the next round would be raised with the objective of monetizing.

“When such expansion had been achieved and it was time to focus on profitability, the market dried down. On top of that, Pakistan’s economic situation also started deteriorating,” said a founder in background conversation with Profit. “The foreign VCs had predicted that they would give money to the Pakistani market based on growth metrics, just like they would do in America, without realising that if things go down, they would go down very badly in Pakistan.”

Faisal Aftab, founder of Zayn VC said that investment with such a mindset can work in countries like the US where the business cycle runs for around 10 years and there is certainty around how things would work out. In countries like Pakistan, the business cycle goes on for around 36 months. That is to say that there is more certainty in VC circles in the US about the business cycles and how they would play out. In Pakistan, that certainty is lacking.

Because the VCs were investing on growth metrics, it meant that unstable companies were incentivised. When things got tough and the money started drying, converting unsustainable business models into sustainable ones was always going to be a tough task, hence the high number of companies that haven’t been able to achieve profitability in Pakistan.

“So this was a major problem on the side of VCs as well that they did not forecast correctly. Converting a product and a service that you were offering on negative economics for a long time to positive economics is not an easy job.”

This again is happening in an economy that is not functional. Would things have been better if the economy was working well?

A founder explained that to a certain extent, things would have been better but unsustainable models would collapse at one time or another.

When the investment downturn started, investors started looking for profitable companies and it was a belief that if you turn profitable, you had a better shot at securing investment. But that is not turning out to be the case. Founders that Profit spoke to say fundraising is coming with extremely harsh terms despite profitability. Hence the number of startups that are actively raising is low.

To hear directly from two prominent founders, both of whom chose to respond

“Most investors are just not interested in Pakistan only,”

Kalsoom Lakhani, Co-founder i2i Ventures

anonymously, in their experience, investors had backed out of investing not in their startup but investing in a startup in Pakistan after signing SAFE documents. Their primary concern being that Pakistan had suddenly turned into a risky country to invest in because of the political and economic uncertainties.

For those that had some investments in the pipeline, bureaucratic hurdles had prevented them from coming to Pakistan. One of the founders explained that his company tried to secure venture debt for his company from foreign investors that could not come into his startup because the founder could not guarantee if the debt payment, in dollars, would be allowed out of the country at the time of repayment.

“We tried to do a transaction from an earlier debt that our parent company had raised. We couldn’t transfer a single dollar back to Singapore even after almost a year of efforts with multiple banks,” said a founder. “So the regulations are there but on ground execution is very difficult.”

“As a consequence, we told that investor that we can not guarantee if we would be able to send the debt back or not. And obviously if you can not guarantee, the investor is going to back off.”

In another case, the startup was promised a tax exemption by the government but the startup’s respective tax office did not know that these exemptions existed and has been unable to get it still. The founder was of the view that foreign investors have also had a change of opinion about the Pakistani market since the 2021 funding boom. That things do not work out the way they were told they would and this dampened the enthusiasm of investing in Pakistan.

Kalsoom Lakhani also explains that Pakistan only startups are having a very tough time with fundraising even if their economics are good. “Most investors are just not interested in Pakistan only,” she explains. In her experience, it is because of the tough macroeconomic situation of the country.

On the other hand, local VCs are not rich enough to invest in startups all on their own and are reportedly struggling with raising new money. Interestingly, there has been a growing interest among rich industrialists to become part of the tech investment community but according to one founder, they are reluctant to

take the initiative because tech investments in startups are done in dollars. But with earnings in rupees, a currency that has depreciated over the years, investments in tech in dollars is a tough task from industrialists, limiting local sources of investments in Pakistan.

Asizable number of startups that were surveyed by Profit said that they had either expanded outside of Pakistan, were in the process or were thinking about doing so. Because one of the risks for startups is that their revenues take a hit in dollar terms because of the continuous decline in value of rupee against the dollar.

With revenues taking a hit, investors that are already cautious about inflated valuations and are bringing them to a more realistic level, spook off when they see revenues that have declined in dollar terms because the company was making revenues only in rupees. So if founders want to build valuations in dollar terms again, they have to seek sources of income other than in Pakistani rupee.

That could be achieved through expansion to a country outside of Pakistan or through exports. “So the expansion abroad is a hedge against currency devaluation in Pakistan,” the founder explained.

Most of the startups surveyed had expanded to countries in the Gulf. One of the reasons why was because there was certainly opportunity in those countries but these countries are also flush with cash and have rich local sources of capital to support companies that operate in these countries.

Take Saudi Arabia, for instance, where the government last year launched a $200 million fund to invest in local as well as foreign startups. If Pakistani founders expand into any of these countries, not only does it provide them a different source of revenue, it also helps them with securing funding there. “When you have a presence in a country like Saudi Arabia, within six months or a year, you would be able to raise funding in that country. Foreign investors also look kindly towards these countries as compared to Pakistan.” n

The govt of Pakistan and its farmers are in a toxic relationship. These are the exact mechanics of this year’s

As the biggest buyer of wheat, the government of Pakistan holds all the cards. So what went down to bring farmers out onto the streets?By Ghulam Abbas

Pakistan’s farmers are in a toxic relationship with the country’s government. Every year the government announces they will buy wheat from farmers at a particular rate and the price that they set is what flour mills buy the wheat at as well.

This means year in and year out farmers are dependent on the prices announced by the government. Normally, the government has a lot of interest in buying this wheat. For starters they can use this wheat to support farmers, keep an eye on shortages, and have a steady supply of the commodity to control any shortages or possibly any problems with the market.

At the same time, the farmers know that so long as they can keep producing wheat they will have the government ready and available to buy wheat from them at a good price and when that price is announced flour mills will also be forced to buy at the prevailing market rate being set by the government as the major buyer.

It is all hunky-dory most years. Except when it isn’t.

Just take this year as an example. The government of Pakistan has refused to pick up as much wheat as they normally do. The big reason for this has been that, as the government claims, the caretakers imported far too much wheat last

year and the surplus has meant the government does not know what to do with all the wheat that the farmers want them to buy.

The immediate results have been catastrophic. Farmers have come out in protests. Instead of giving them a helping hand, the government has used police to beat them purple and blue and send them back home with stern warnings. The farmers on the other hand have no other option. They are expecting a major bumper crop this year and their biggest buyer is saying they’ve imported wheat from outside. So what exactly happened?

The entire matter boils down to some 3.6 million metric tons of wheat that the government ordered in surplus to expected figures. Why did they order the extra wheat? What do the farmers have to say and how did this come about? Profit dives into the mechanics of.

The process is normally very simple. The government procures wheat from producers directly; it releases wheat to flour mills directly and wheat flour consumers through publicly owned utility stores.

Our current crisis can be traced back to the floods of 2022. Following devastating floods in Pakistan in 2022, the impact on wheat farming caused a shortage of wheat in early 2023. While Pakistan consumes around 30 million tonnes of

wheat per year, only 26.2 million tonnes were produced in 2022, pushing up prices and resulting in long queues of people in cities trying to buy wheat. There were even instances of people being crushed in crowds trying to access wheat.

As a result, the government decided to allow the private sector to import wheat. Before the 18th constitutional amendment, the practice of fixing support prices was with the federal government (now provinces are free to fix their support price). Now, the Provincial food departments and PASSCO procure wheat in harvest months at the government’s announced price. The provincial food departments release wheat in lean months at the ‘issue price’. Until recently issue price was the same throughout the year and now the government has introduced cascading price mechanism to smooth out seasonal variation and cover the transaction cost. The public sector procures on average about six million tons of wheat or nearly 24% of total production.

The part where there is controversy is a small period between September 2023 and March 2024, more than 3.5 million tonnes of wheat were imported into Pakistan from the international market, where prices were much lower.

Documents reveal that the decision to allow regulatory duty free imports of wheat by

With a bumper crop, we are expected to grow nearly 32 million metric tonnes of wheat this year, but with the government’s coffers already full of wheat, we will be able to sell not more than 50 percent of our crop. This could result in losses of nearly 380 billion rupeesKhalid Mehmood Khokhar, Pakistan Kissan Ittehad (PKI) President

the private sector, coupled with an absence of restrictions on import volume and timelines, was taken by the caretaker government and has exacerbated the situation, causing significant losses to both farmers, badly affected procurement drive of the province food departments and the national exchequer.

According to documents obtained by this publication, a summary initiated by the Ministry of National Food Security and Research (MoNFS&R), subsequently approved by the Economic Coordination Committee (ECC) and the Federal Government, permitted unlimited import of wheat in the country with waiver of regulatory duty and taxes even after bringing in estimated shortfall quantity of 2.4 million metric tons first time ever in the history of Pakistan under the garb of escalating prices of wheat due to shortfall. This move allowed private entities to flood the market with additional wheat stocks available at much less prices internationally than the reserved domestic wheat stock, consisting of politically motivated support price, marks up of banks, storage cost as incidental charges.

Despite an estimated shortfall of 2.4 million metric tons by the Ministry of National Food Security and Research, Pakistan reportedly imported around 3.6 million metric tons of wheat, resulting in import of surplus wheat of 1.2 million metric tons without duty and taxes also. This continuous arrival and surplus stock of wheat after shortfall without RD kept halting release and maintaining the procured strategic reserves of provinces and PASSCO being procured at higher prices than the import. As per past practice, the provinces complete maximum releases by March of each year to procure new crop but this time, due to coincidence of wheat import with the peak domestic wheat season and leftover stock of wheat compelled the provinces to drop their strategic wheat procurement targets that sparked indignation among the farmers country wide and give rise to this wheat crises.

As sources M/o National Food Security and Research in the past has been proposing to the federal government for imposing of regulatory duty on import of agricultural goods particularly wheat, maize, sugar, etc., when

they are produced in surplus in the country for bringing price of the imported produce at par with the domestic produce to regulate import and protect domestic industry. It suggests the Federal Government for exemption of RD to allow import of agricultural products which are insufficient and in great demand for the country to meet shortfall and ensure food security. As RD is linked with the availability of the agricultural merchandise in the country, it necessitates constant and regular review by the Ministry of National Food Security and Research ensuring convenience of goods.

According to the Import Policy Order (IPO), wheat is not classified under banned items for import in Pakistan. However, it has been classified under restricted commodities for import in Pakistan and can be imported in Pakistan from any country approved by Department of Plant Protection (DPP) and Ministry of National Food Security and Research (MNFSR) with certain sanitary and phytosanitary measures.

The DPP prepares and establishes phytosanitary import conditions for import of agricultural commodities in Pakistan. These are issued to the importers in terms of import permit. These phytosanitary requirements are needed to have been complied in the country of origin to mitigate pests associated with the import possessions. If on arrival of consignment, if any condition is not fulfilled in the country of origin or insects are detected in the consignment, DPP issues Emergency Disinfestation Notification to the importers and after disinfestation, it gives biosecurity clearance and plant protection release order. These measures are taken with an objective to prevent entry of invasive biosecurity risks i.e., insects, plant pathogens, weeds, contaminants in the country and safeguard domestic agriculture, natural resources and public health like other countries under guidelines of International Plant Protection.

Currently, neither Pakistan Plant Quarantine Rules, 2019 (PPQR, 2019) nor IPO nor any other SRO or law nor the Federal Government has stipulated any quota or capping on import of wheat in Pakistan. It is MNFS&R that decides quantity and timeline for import of wheat in-

cluding other agricultural goods after estimating availability and shortfall of wheat and other goods in Pakistan. It also decides when and to what extent RD will be levied on importable wheat in order to regulate its import in view of Pakistan’s own wheat harvesting season.

Notably, the summary initiated by the former M/o NFS&R Secretary and current Ministry of Information Technology Secretary, Capt. (Retd.) Muhammad Mahmood and endorsed by former Minister, Dr. Kausar Abdullah Malik includes unprecedented proposal for permitting unlimited import of wheat without regulatory duty even beyond arrival of shortfall wheat of 2.4 million metric tons and without fixing and limiting timeline somewhat by February for import of wheat that led to the unprecedented loss to foreign reserves of more than one billion US dollar and inflicted similar loss to farmers abandoning procurement of their produce by the government.

Furthermore, the absence of caps on import quantities and timelines incentivized importers to continue their operations unabated, even after the arrival of domestic wheat in the market because there was continuous profit for wheat in the market till end February.

Usually, the government purchases around 20 percent of all the wheat produced by local farmers at a fixed price (about 5.6 million tonnes, based on a 2023 yield of 28 million tonnes). These interventions are typical and normally appreciated by wheat farmers. But this year the situation is rather dire. The government of Pakistan is refusing to buy wheat from these farmers. The government initially announced they would only buy around 2 million tons. This, going by last year’s figures, is barely 7% of the total crop. And farmers are expecting a bumper crop this year.

The crisis has prompted widespread protests from farmers, particularly in Punjab, demanding government procurement of their wheat stocks at approved rates. The government, however, citing the surplus created by im-

ports, has scaled back its procurement targets, exacerbating tensions.

Addressing the Punjab Assembly, Food Minister Bilal Yasin acknowledged the wheat crisis, attributing it to the influx of imported wheat, particularly near the harvesting season. He pledged government support for small farmers but provided no specifics on the nature or timeline of this assistance. A fact-finding probe into the import process has been promised, with the findings to be presented to the assembly.

In its justification for the wheat imports, the Ministry highlighted an estimated shortfall of 2.4 million metric tons against the national requirement for the year 2023-24 and initially recommended importing 1.00 million metric tons of wheat through the Trading Corporation of Pakistan (TCP), aiming to balance strategic reserves with PASSCO while maximizing private sector involvement in wheat imports. However, the ECC deferred this decision in August 2023. Subsequent consultations with both public and private sectors resulted in a revised strategy.

As per the revised summary, Capt. Retd. Muhammad Mehmood, former Secretary, M/o NFS&R recommended the ECC to approve import of 1.00 MMT of wheat through TCP in two phases. Immediate import of 0.50 MMT under G2G arrangements by adopting options like: deferred payments, multi-currency option and arrival on need basis. Revision of import requirement in January 2024.

a) PASSCO will be the recipient agency for TCP to maintain strategic reserves of the country.

b) Private sector will be encouraged to import specified milling wheat to cater the shortfall in the present customs and duties exemption structure., in order to stabilize wheat/Atta prices.

c) Import of specified milling wheat shall be allowed in the country subject to import conditions regarding “Commodity and Specification” as provided under Notification of MinFA dated 14th November 2008 and import requirements under Import Policy Order 2022 (Annex-J (i) & J (ii), for both public and private sector.

d) Monitoring mechanism of private sector will be supervised by the Department of Plant Protection through Import permit and Biosecurity clearance and release order issuance and opening of LC’s in commercial banks.

e) Ministry of Maritime Affairs may be directed to provide priority berthing to imported wheat on arrival at the Sea-Ports.

Prime Minister Shehbaz Sharif has ordered an investigation into the wheat crisis. Bilal Yasin, provincial food minister for Punjab, told the provincial assembly earlier this week that the crisis had been caused by decisions made by the caretaker gov-

Those people who allowed the import of the wheat close to the wheat harvest season are responsible for this crisis. How¬ever, despite this, the government will fully support the small farmers

Bilal Yasin, provincial food minister

ernment that took over in August last year after the tenure of the previous elected government came to an end. Elections, which should have been held within three months, were delayed by the need to redraw constituencies following the latest census. They were eventually held in February this year. “Those people who allowed the import of the wheat close to the wheat harvest season are responsible for this crisis. How¬ever, despite this, the government will fully support the small farmers,” the minister said.

Following the wheat import issue, Prime Minister Shehbaz Sharif on Thursday, changed the Secretary of the food ministry. Interestingly, instead of taking action against real culprits, Mr. Muhammad Asif, present secretary incharge of the Ministry has been made scapegoat by making him OSD. The former secretary Mehmood, is considered close to the ruling party and liked by Shahbaz Sharif.

Muhammad Asif has been replaced by Fakhar Alam, a BS 22 officer.

Sources within the Ministry of National Food Security have claimed that the import of wheat took place allegedly in league with flour mafia and wheat importers. and defrauded the country of more than one billion dollars of foreign exchange.

This import has inflicted a loss of above Rs 300 billion to the farmers and Rs 104 billion to the government exchequer, according to sources privy to the development. Sharing details, the sources said wheat stocks with PASSCO and provincial food departments were 43,65,220 metric tons on April 1, 2024 and there was no need for private import of wheat.

They said as the private sector and flour millers imported wheat, PASSCO and provincial food departments could not sell their stocks of 43,65,220 metric ton and have incurred average incidental charges of Rs 950 per maund/40 kg, and total loss to government because of incidental amounted to Rs 104 billion which has allegedly indirectly gone to the pockets of flour millers, traders and bureaucracy.

They said due to unnecessary and un-

wanted import, prices of wheat have crashed to Rs 2800-3000 per maund against government price of Rs 39,000/maund and the farmers will be forced to sell 50 percent i-e 16 million metric tons out of estimated 32 million metric tons of total produce as government is allegedly purchasing very little wheat.

Thus, more than Rs 300 billion will allegedly be looted from the farmers and will go to the pockets of flour millers, import traders and bureaucracy, said sources.The import was kept uncapped and ships continued to dock at Karachi even during the entire month of March, 2024 when wheat from Sindh province was coming to market, the sources added.

It is also learnt from the sources that 71 cargos of wheat were imported from Russia, Ukraine, Bulgaria and private importers continued the import of wheat till March 31 instead of March 15. They said that over 3.5 million tons of wheat was imported under the pretext of importing one million tons of wheat.

They said live insects were found during the inspection in 26 cargoes of wheat out of 71 cargoes of wheat imported from September 2023 to March 2024. Inspection of imported wheat was done by a subordinate department of the Ministry of National Food Security, said sources.

Sources also informed that the private sector was given an open exemption for the import of wheat instead of a fixed limit allegedly on the recommendation of the Ministry of Finance.

They said that the Ministry of National Food Security had ignored the important suggestions of the Ministry of Commerce and Trading Corporation of Pakistan (TCP). Additional wheat was imported under the systematic plan, which caused billions of rupees loss to the country, said sources.

Khalid Mahmood Khokhar, President Pakistan Kissan Ittehad has requested the Prime Minister Shehbaz Sharif to conduct an inquiry into this mega scandal through a high-powered committee and those who made proposals and gave permission for import of wheat must be punished. n

Representing Pakistan’s fintech community at World Economic Forum, Omair Ansari claims it is a fallacy that Pakistan has a big unbanked population because of the impact of the telcos

The first question that was posed to Finance Minister Muhammad Aurangzeb at a recent session of the World Economic Forum was about cash. Around 40% of Pakistan’s economy still runs on cash, what does the government intend to do about it?

Mr Aurangzaib gave a measured but brief answer. He explained that digitising payments and moving away from cash were one of the top priorities of the current government in Pakistan. As a former banker, he is well placed to understand just how important financial inclusion is not just for the banking sector but the health of the economy.

The more detailed answer, however, was perhaps given by the other Pakistani on the panel. Omair Ansari, the CEO of Karachi based fintech company ABHI , said that the democratisation of payments only happens when there is zero fee which then causes mass adoption. According to Ansari, the problem bigger than payments was that of providing access to credit to individuals and merchants.

ABHI has been a part of Pakistan’s payments industry since June 2021 when the startup raised $2 million in seed funding with an aim to salary advances through a web-page or an application. The company was incubated at the prestigious YCombinator in 2021. In April 2022, the fintech company raised a $17 million Series-A round which valued the company at a $90 million valuation. In May last year, ABHI raised the first-ever Rs2 billion sukuk bond by a fintech company. Just today the company has also announced it has joined hands with the TPL Corporation to try and acquire a majority stake in FINCA Microfinance Bank.

The presence of ABHI ’s CEO on the panel provided a non-governmental perspective on fixing the financial inclusion problem. What made it interesting was Mr Ansari’s claim that the problem was not payments, but rather access to credit.

“If you go to a stall, they will accept cash which is a frictionless form of payment than digital. However, what we focus on is credit-led. An average person needs credit, they don’t need an easy way to pay another person,” Ansari said in response to

a question.

Giving the example of ABHI , he explained the company was a credit-led fintech focusing on providing credit as a means to create mass adoption as opposed to forcing payments on individuals. Ansari was of the opinion that payments were not what people in Pakistan were complaining about. Their complaint was rather that they don’t have cash to improve their lifestyle.

“Our focus across geographies and Pakistan specifically where we have been able to push adoption is being a credit first solution in that geography,” Ansari added. ABHI ’s business model is that they provide salary advances to salaried workers at the end of the month to tide them over and then cut those advances from their next month’s salary. It is essentially a system that allows people to borrow from their own future earnings.

Ansari outlined that it was a fallacy that Pakistan had a big unbanked population. It was a fallacy because telcos had reduced such population through their digital wallets.

“Telco wallets are an alternate form of banking that we partner with to digitise the lending aspect of our business,” he said. “The second aspect is the alternate scoring mechanism. Traditional banks will look at a customer in a very different way than how we look at the telco data that an individual or a business has. How worthy are you of credit?”

Responding to a question about whether ABHI had a better appetite for risk than traditional banks, Ansari, responding in affirmative, explained that banks would rather give a multi billion dollar loan to a stable company considered risk free instead of giving out 100,000 loans of a smaller ticket size.

Now, banks have started partnering with ABHI as a distribution model which lets ABHI give out smaller loans to SMEs and individuals for banks. “That’s essentially our [ ABHI ’s] target market because they can not get access to financing. They are just underbanked and unbanked.”

On a question about how to increase digital adoption to people at a mass scale, Ansari said that omni-channel was the answer.

“There is a fallacy again that is around that when people think about fintechs in emerging markets, that suddenly everything is digital and you are going to leapfrog. That is not happening.

“NuBank is acquiring a telco. Why? Because of physical presence. The point is if you don’t go omni-channel in these markets and there is no physical presence, your

If you go to a stall, they will accept cash which is a frictionless form of payment. An average person needs credit, they don’t need an easy way to pay another person

Omair Ansari, CEO ABHI

ability to scale fintech is going to be limited. A branch network is actually required. It’s a different branch than what existed 5 years ago.”

Ansari said that his fintech company was also in the process of acquiring a microfinance bank in Pakistan to have a branch

presence. He was of the view that a physical presence was especially necessary to extend credit to the agricultural segment of Pakistan.

“It is impossible for you to do it all through digital means because they [farmers] also trust going to a branch. They don’t

trust a digital interface. It is going to evolve and it is going to take time and you need to work with time instead of dreaming about the future and waiting for that to happen.”

Abhi, Pakistan’s first embedded finance platform founded in 2021, has pioneered the concept of Earned Wage Access (EWA) in Pakistan. It has revolutionized the financial landscape by benefiting over 550 companies, including industry giants like Unilever, Martin Dow, and Artistic Milliners, and positively impacting thousands of lives. Currently, ABHI offers a comprehensive suite of solutions, including Earned Wage Access (EWA), Payroll Solutions, SME financing, and AbhiPay.

Recently, in partnership with foodpanda and Daraz, ABHI has introduced platform-based financing, empowering vendors and merchants with quick access to working capital, further solidifying its position as a fintech innovator.

Since 2021, ABHI has emerged as a prominent fintech company, earning recognition as one of the Future 100 companies in the UAE. Expanding its global reach, ABHI was included in Hub71, a prestigious tech ecosystem in the UAE, and launched its Global HQ in Abu Dhabi with support from ADIO (Abu Dhabi Investment Office). It is also the first to be awarded the Technology Pioneer 2023 Award by the World Economic Forum, a first for fintech in the MENAP region. Furthermore, ABHI’s founders, Omair Ansari and Ali Ladhubhai, recognized for their entrepreneurial expertise, were selected as 2nd Endeavor Entrepreneurs from Pakistan at the 38th International Selection Panel (ISP). n

KIA Stonic’s drastic price fall is a tale of lobbying, regulatory capture, and high margins.

Here’s what went down behind the scenes

For the past year, Pakistan’s car manufacturers have been at war with each other, using every trick in the book. Has KIA just ended it with a masterstroke, or is it just getting started?By Babar Nizami and Talha Farooqi

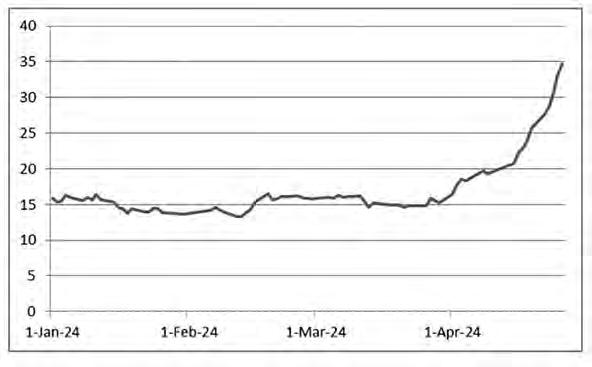

The announcement by Lucky Motors Corporation that they were slashing the price of their subcompact crossover SUV, the KIA Stonic, by over Rs 15 lakhs was nothing short of a declaration of war.

After all, they weren’t supposed to.

The government of Pakistan had announced in March this year they were increasing the tax on cars with a factory price of more than Rs 40 lakhs. One might have expected cars like the Toyota Yaris, the Suzuki Swift, or the Honda City to cut their prices by a few lakhs to take advantage of the lower tax.

What wasn’t expected was that the KIA Stonic, priced at Rs 62.8 lakhs after tax, would drop its after tax price by 24% down to Rs 47.67 lakhs overnight. The response has not been disappointing. Buyers made a beeline towards KIA showrooms and conservative estimates confirmed by KIA’s management to Profit claim the company sold over 700 cars in three days.

KIA had to close bookings over the weekend and now plan to open them up again on Monday or Tuesday. As of now, the company has taken bookings for up until September and it seems the KIA Stonic might be the car of this summer season. And it isn’t just customers that have had to jump out of their seats for the Stonic.

As expected, Toyota and Honda had decreased their prices when the new tax on cars above Rs 40 lakh were announced. But almost immediately after KIA reduced the price of Stonic, Suzuki had to approve a 13% drop in the price of its top variant to Rs 47.2 lakhs, down from Rs 54.3 lakhs. The price adjustments by Honda and Toyota have been less drastic, but both have also knocked a few lakh rupees off their prices.

KIA had made the challenge very clear: They were here to take on the Big Three’s prized price segment, even if they had to reduce their margins to do so.

But this does raise questions. For starters, if KIA was able to reduce the price of the Stonic by 24%, what kind of margins were they charging on it before? Why did it

take so long for KIA to get to what is clearly the right price on this car? What effect will this have on cars like the Toyota Yaris, the Honda City, and the Suzuki Swift now that a new car has entered this price range? And is it wishful thinking to wonder if this could mean a cascade effect for the rest of the industry?

Over the past few weeks, Profit has had exclusive access to and studied KIA’s financial statements. Interviews with the company’s CEO, Muhammad Faisal, and other sources within the car market have shown that KIA not only had the margins to make the price cut happen, but also to make other players follow suit.

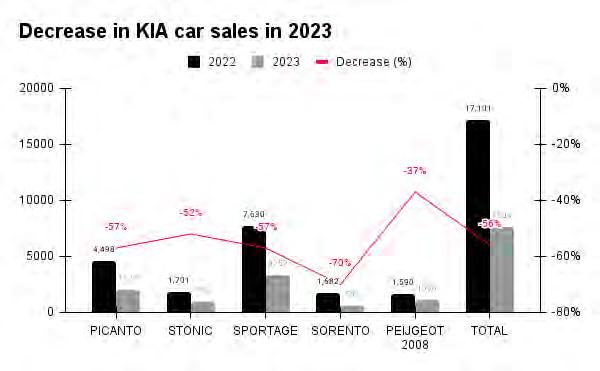

Up until a few months ago, KIA was dead in its tracks. It was a pretty big fall from grace considering the shockwaves the Korean car manufacturer had caused in Pakistan just a few years ago.

most in-demand car, in 2022 the Sportage sold over 7300 units. This number fell by more than half to only 3200 units in 2023. The steep fall in sales was natural. Since 2021 the entire car market has seen prices skyrocket and sales plummet as a result. But the initial success of the Sportage, and its entrenchment in Pakistan’s car market as a mainstay, was very simple.

KIA priced the car brilliantly.

When it was first launched in 2019, the KIA Sportage came out at a tag price of just over Rs 45 lakhs. This was a massive shakeup. Back in 2019, the main SUV being offered was the Toyota Fortuner, which was priced at around Rs 75 lakhs. Similarly, when the Tuscon was later introduced by Hyundai, it was also priced at around Rs 70 lakh. That is now the price of the Sportage in 2024.

In the Rs 45 lakh to Rs 50 lakh range, the Sportage was competing not with these SUVs but rather with the Toyota Corolla and the Honda Civic, both of which are sedans. The KIA Sportage provided a quality

It wouldn’t be inaccurate to say that KIA changed the landscape of how we view cars in Pakistan entirely. And the vehicle of this success for KIA was their flagship car, the Sportage. Between August 2019 and August 2021 the KIA Sportage sold over 25,000 units at more than 1000 cars a month.

Since then things haven’t been quite so good for the Sportage. Even though it is their

Source: Autojournal and company financials

SUV in the same price as a sedan and people absolutely lapped it up. The car was the latest shape (something neither the Toyota Corolla or the Honda Civic could claim at the time) and offered a bucketload of features (by Pakistani standards) that made it an incredibly good deal. That is why the KIA Sportage worked, it allowed other competitors to be braver, and it outsold the Toyota Corolla.

It was like KIA had done some sort of magic trick. Different auto companies had been trying for years to break the hold of the Big Three car manufacturers and somehow KIA came in and did everything right. But it wasn’t like the existing players were going down without a fight. And that is where the story of the KIA Stonic actually begins, with KIA’s first real mistake.

The Big Three weren’t exactly going to sit around and watch KIA demolish their market. They had for years known exactly what was wrong with their product line and knew how to fix it too. It was just that because there was no competition, they felt no urgency to do so.

Toyota was the first to clap back with the launch of the Toyota Yaris. Essentially, they discontinued the cheaper variants of the Toyota Corolla with 1300cc engines, and launched a new car from scratch that was cheaper. Now, people could either buy a Toyota Corolla in the Rs 3.5 – 4 million range, or a Toyota Yaris in the Rs 2.5 – 3 million range. Essentially, Toyota did to the sedan exactly what KIA did with the SUV. KIA offered an SUV at a comparable price to a sedan and people went crazy for it. Toyota offered a sedan at just a little over the price of a hatchback.

Honda and Suzuki took different approaches but still had to do something. Suzuki pushed the new design of the Swift, a hatchback with a 1.2 litre engine. Honda decided they would relaunch the City in its new shape and market that heavily and price it in the same category as the Toyota Yaris. The KIA Sportage had come in to try and break the market for the Corolla and the Civic by being in the same price range. Suzuki, Honda, and Toyota suddenly launched cars that were newer and cheaper than the Sportage and their sedans, suddenly opening up a whole new market.

So while KIA dominated the market from 2019-21, the Toyota Yaris emerged as Pakistan’s hottest car after this. In its first 14 months, the car sold nearly 30,000 units. In 2022, the car continued this trend and sold around 22,000 units. In 2023, when prices increased drastically, they weren’t even able to sell an exact 10,000 cars. But by this point all manufacturers were facing the heat. Honda City sold around 5900 units in 2023.

With this new challenge, KIA also decided it was time to launch a new car and compete with the Yaris and its ilk. For this they decided to follow the Sportage model in all but their pricing. They introduced the KIA Stonic, a subcompact SUV which is a sort of cross between a hatchback and an SUV.

They offered the car in its latest global shape and it immediately hit the markets. The only problem was the pricing.

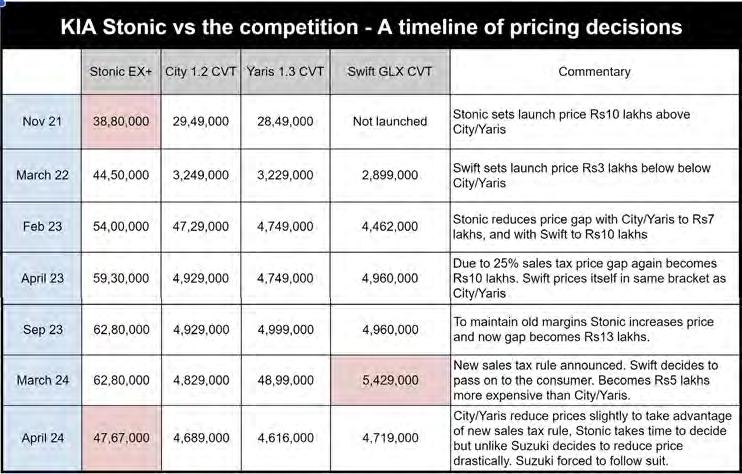

This is a pretty straightforward system. KIA messed up the price. When they launched the car in November 2021, KIA brought it out at a price of Rs 38.8 lakh. This was almost 10 lakh more expensive than both the Honda City 1.2 CVT and the Toyota Yaris 1.3 CVT. The Suzuki Swift had not been launched at this point.

By the time the Suzuki Swift came out in March 2022, the prices of the City and the Yaris had risen to over Rs 32 lakhs. The Swift was launched at a price of over Rs 28 lakh to compete with these cars. The Stonic, on the other hand, was at Rs 44.5 lakh, making it nearly 40% more expensive than the City and the Yaris, and around 43% more expensive than the Swift.

The prices between the cars closed a little around July 2022 when Toyota and Honda hiked prices up by as much as 10 lakhs. At the same time Suzuki only increased their prices to around 32 lakhs which made this an attractive time to buy the Swift. The Stonic was now around Rs 8 lakh more expensive than the Toyota Yaris. By January 2023, the prices of the Yaris had gone up to Rs 45 lakhs but the Stonic had also crossed the Rs 52 lakh mark. Over time, this trend continued. Even the Suzuki Swift kept catching up.

But the real game changing moment came in March 2023. In that month, the government made a notification announcing that all cars that were either above 1400cc or categorised as SUVs in Pakistan would have a 25% sales tax on them instead of the previous 18%. Even though Stonic’s engine size was slightly below the 1400cc threshold, this was a hit for the Stonic since it billed itself as an SUV. As a result, the price of the Stonic in March 2023 went up to nearly Rs 60 lakhs in April 2023. KIA was having to pass down this new tax to its customers. Meanwhile, the price of the Honda City and the Toyota Yaris remained absolutely stable throughout this period with the exception of one Rs 2 lakh increase by Toyota.

By September 2023, the Stonic was Rs 62.8 lakhs. In comparison, the Toyota Yaris was Rs 49.3 lakhs and the Honda City was Rs 49.9 lakhs. The price gap between KIA Stonic and its sedan competitors had gone up to Rs 13 lakhs. Surprisingly, the Suzuki Swift had also increased its price to Rs 49.6 lakhs, now billing itself in the same league as Toyota Yaris and Honda City.

At this point market dynamics had

been established. The Toyota Yaris was at the top, the Honda City was next, and the KIA Stonic’s sales were in the absolute dumps. But KIA had persisted with their pricing strategy. They believed their product was better, had a higher value, and was more upmarket than the cars it was competing with. It was also more highly taxed.

Insiders have told Profit that the tax had been levied after extensive lobbying on the part of one of the Big Three companies. The source told us the name of the company but requested it be kept anonymous for reasons of confidentiality. The March 2023 notification hurt the Stonic even more than its original pricing had. That is why KIA also put on its lobbying shoes and went to the government. They tried to explain that the car was not a luxury SUV and hence should be exempt from the tax. All of their efforts led to another notification in March 2024, but even this one had the influence of other players. The new notification held that any car that was priced over Rs 40 lakh (before tax) would be charged 25% sales tax. This meant the Stonic still had the same old problem, unless they chose to drastically reduce their price.

A little point of order here. Back in March 2023, only the Stonic had been affected because it was an SUV while the Yaris, City, and Swift were not and had engines below 1400cc. But the March 2024 notification changed this. The price excluding tax of all of these cars was over Rs 40 lakhs, which meant they would now be subject to 25% sales tax instead of the previous 18%. When the price of a car is brought down to just a rupee under Rs 40 lakh, then with the 18% tax rate the price goes up to Rs 47.7 lakhs. This was an easy decision for Toyota and Honda as they only had to decrease their prices slightly to bring them under the Rs 47.7 lakhs threshold. This is where KIA had a decision to make. They could either continue keeping the manufacturing of the Stonic down and keep it at its price, or reduce it significantly. Toyota and Honda had already brought their prices down to around the same level with the difference of less than a lakh. KIA chose the latter, bringing it down by an astonishing 24% to Rs 47.67 lakhs after tax at the end of April 2024, just last week. The real hit was the Suzuki Swift. In March when the notification came, Suzuki had decided to initially pass on the price to the consumers and the car’s price rose to a staggering Rs 54.3 lakhs — more than Toyota Yaris and Honda City. Amongst the three, the car that had started as the cheapest was now the most expensive, and that too by a margin. So when KIA decided to slash the Stonic’s asking rate, Suzuki had to eat humble pie and go back on

It is a bold step by Lucky but we have done our working and the company feels there is great potential in this move. If i may add, this player is capable of doing anything that you can’t even think of

Muhammad Faisal, CEO, Lucky Motors Corporation

the increase within a month and bring their price back down to Rs 47.2 lakhs.

There were plenty of theories going around when KIA first announced that the Stonic was going to have a fourth cut off from its final price. Most people initially thought this meant that the car was being discontinued. That the sales had been bad enough for KIA to call it quits and this was an attempt to get rid of existing stock. This has been proven wrong because KIA is taking advanced bookings as well and clearly intends to keep making the car. There was another theory that KIA might be having capacity issues. But as we’ll get into a little later, KIA is well within their capacity capabilities. If anything they are pretty underused. There was also speculation that perhaps KIA knew something about the dollar going down and wanted to get a head start on downgrading their pricing. That seems more of a wishful thinking than anything else.

That really only leaves the room for

one possibility. That KIA always had enough of a margin on the Stonic to reduce the price and still make a decent profit. And the margins are what it all comes down to.

This is the crux of all business. Go to a roadside vendor and try to haggle with them and they’ll give you the same old spiel.

“Itna toh mere laga hai iss par koi munafa nahi rakh raha”

Consumers like to buy products with low margins. They went to get it for as close to the cost it took to produce the product as possible because they don’t want to value or pay for the manufacturing, the overheads and the profits. And those selling want to increase this margin as much as possible because, well, because they want to make money.

The auto industry would also like to pretend that they work on small margins. But if the KIA Stonic and now the Suzuki Swift prove anything, it is that this assumption is incorrect. “The company has taken a very bold step. The car is still contribution positive. We’re not going to be making much money on this because that we would have done at the previous price. But we did feel

there was an opportunity with this particular car at this price point. And the recovery of our fixed costs will also be better if we achieved the volumes” says KIA’s CEO Muhammad Faisal.

The reduction in the Stonic’s price is 24%. Of course, we have been talking about the after tax price up until now. To understand this, remember that the price of Rs 62.8 lakhs has two components — the sales tax and the factory price. The government’s notification held that any car over Rs 40 lakh factory price would have 25% sales tax on it. The factory price of the Stonic was around Rs 49 lakhs, on top of which 25% tax gave it the price of Rs 62.8 lakhs. The final price adjustment of 15 lakhs has a reduction of both tax and factory price. KIA essentially reduced the price by 9.75 lakhs on the factory price bringing it just under 40 lakhs. This was around a 20% deduction in the price. Now that it was less than 40 lakhs, the sales tax was also reduced by a little over 5 lakhs bringing the price of the car to Rs 47.67 lakhs. That means we can safely assume the contribution margin KIA was charging for the Stonic was greater than 20%.

The reduction of Rs 9 lakh from their production cost means KIA was producing the car for even less money. In fact, as the company’s CEO Muhammad Faisal has told Profit, the price of the car is still contribution positive.

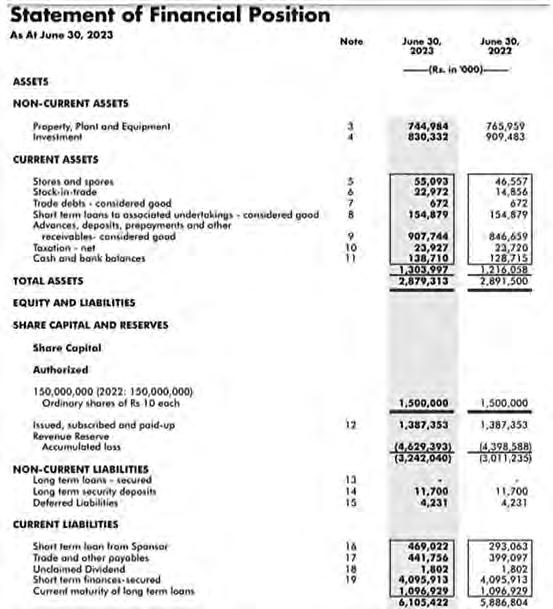

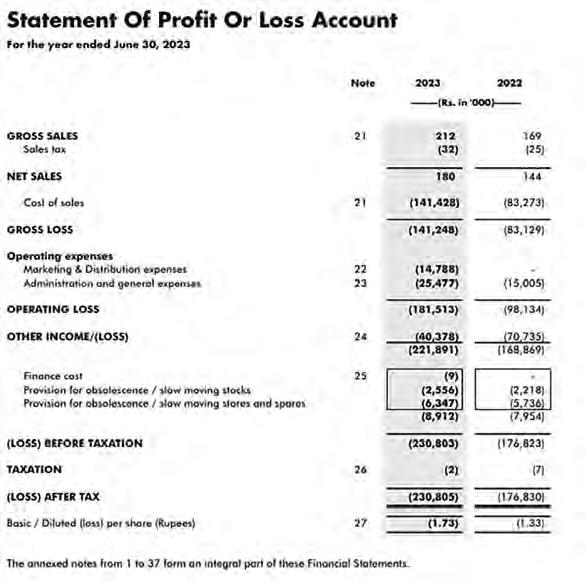

It is something that becomes clearer from KIA’s 2023 financial results. In the document available with Profit, the company reports its sale at Rs 82 billion. Their total cost of sales in comparison are Rs 73 billion. However, around Rs 6.1 billion of these costs are overheads, so the actual variable production costs come out to around Rs 16 billion. This amounts to a margin of around 20%. In the case of the KIA Stonic, as displayed above, we can assume the margin was even higher than this.

This isn’t the only detail that can be gleaned from KIA’s financials. It is telling of

the state of affairs in Pakistan’s car market. KIA currently has the production capacity for 50,000-60,000 units. In 2023, they only utilised 21,984 units from this capacity. This figure fell by more than half in 2023 to 10,264.

Despite this, KIA made a profit of over Rs 9 billion in 2023. In comparison, their profit for the year 2022 had been Rs 9.5 billion. Despite production being cut by more than half, profits only really fell by 5.2%. At the same time, during its worst year, the company made a profit of Rs 9 billion with an equity of Rs 33 billion, giving it an ROE value of 27%. Not bad at a time when the company is doing poorly.

That is because the company earns in other ways too. The deposits that they receive from customers that are waiting for their cars are stored in short-term investments and interest bearing bank accounts and they make a steady revenue off them. Assuming that for the 700 plus Stonic cars that have been booked right now, the average delivery will be in August. And assuming 50% advance amount on these bookings, and the latest 3 month T-bill rate of 21.6%, KIA will make an additional Rs 125,000 on each Stonic sold.

In 2023, at a time when KIA was not making so many bookings, they made Rs 1.8 billion off such income by investing such money. This was more than enough to cover for all non-manufacturing overheads, including administrative, marketing, and even finance costs for the year 2023. This means the company made a Rs 9 billion gross profit, and was able to make the same Rs 9 billion in profit after tax.

We are now at a situation where there is essentially a new entrant in the mid-market price segment. The Toyota Yaris, the Honda City, and the Suzuki Swift have been joined by the KIA Stonic. This means that the market will now be split. Already the Stonic has made some headway, but the method to their madness is relying on volumes over margins.

“It is a volume game now. The company has brought the car into a price segment where there are already three cars. It is a bold step but we have done our working and the company feels there is great potential in this move,” explains Faisal. “This is a strategic decision that probably only a group like Lucky could take, and we will definitely take a hit on our profits and losses but it is a no brainer for the customer as in this price segment Stonic is superior.”

And that isn’t all. There are other moves that KIA plans on making. There are already very reliable reports that KIA is planning on launching new cars in addition to their current line of products. Such a move would diversify the market and perhaps bolsters consumers that have felt a semblance of excitement and desire to buy after some years. The past few years have proven to be taxing on the auto sector largely because buyers have refused to agree to the pricing on behalf of the auto manufacturers.

The decision by KIA to reduce the price of the Stonic might have broken that mould. On top of the possibility of more cars bringing in diversity, KIA might also follow up on their current move and change up their pricing on other cars as well. Maybe not to the extent they did in the case of Stonic, as there is no sales tax incentive in their other product lineup. But if they have been charging margins of over 20% on their cars, they have the capacity to reduce prices on some of their other cars as well. At the same time, their production capacity is far higher than their production numbers. So if they decided to focus on volumes over the margins then KIA will not only increase their sales, but also manage to force the rest of the industry to play catch up.

Honda and Toyota will take some solace in the fact that they can decrease their prices further if need be without being as much of a cut as KIA had to make. So if their margins were as high as KIA’s, they would be able to make more money. But losing out on customers is still losing out on customers. In particular one of the pain points will be Suzuki, which has been outclassed when it comes to the Suzuki Swfit. A hatchback competing with sedans at the same price was strange enough, it cannot now also hope to compete with a subcompact SUV as well.

KIA will also have a perception advantage in all of this. Since its launch, KIA has priced Stonic well above the cars it is now competing with. If nothing else, the customer perception might be that the Stonic is much better than the rest of these cars if not worth more. This will also help them make sales.

But there is a catch to all of this. We are assuming that Toyota and Honda are losing out on customers. What we’re not acknowledging yet is that KIA has just created customers. Up until this point, car sales were dead in their tracks. All cars except the Haval Hybrid had seen their fortunes take huge dips. The new price of the Stonic has pumped some much needed adrenaline into the car market. Buyers have gone out because of the new option and it has also changed the dynamics of the second hand market which was fast becoming nearly as unaffordable as the original market.

The only question that remains to be answered is how far the tremors of this shakeup will carry. Already, Suzuki having to adjust the price of the Swift is a sign. Similarly, news has already come in that Changan has reduced the price of their SUV, Oshan X7 by Rs 4 lakh, which interestingly is not even in the Stonic league.

The move by KIA was a risky one but it has clearly paid off. Will other car assemblers try and replicate this success? KIA already has tasted some success with this strategy before. They have taken the first steps to replicating it with the KIA Stonic, and they might not stop here. In fact, without elaborating much, this is how Faisal chose to end his interview, “this player is capable of doing anything that you can’t even think of.”

It is yet to be seen how the rest of the industry will respond. After all, the Big Three had an answer last time. And they are more than okay going blow for blow. n

ast month, Generation did something unexpected. A brand widely popular for its inclusive campaigns, with an intentional focus on representing real bodies and real people, was now experimenting with AI models.

Online shoppers scrolling through the website were quick to realise that something was different. Before we knew it, X, formerly known as Twitter, was blowing up with users pointing out that Generation seems to be generating AI models of their own.

The only problem was that AI is not yet sophisticated enough to produce results that would align with Generation’s ethos, which largely combines Pakistani culture and inclusivity.

When Profit reached out to the brand, they declined our request to comment, saying that it was a small experiment and they would require toying with the AI tool for longer before they can provide insights into the potential of it.

However, our interest had already piqued, so we sought others who could talk about the potential benefits and drawbacks of replacing human models with AI generated ones.

Is Generation the only fashion brand that is dabbling with AI or are there more?

Wasay Hasan, director at Lulusar, told Profit, “Over the past seven to eight years, we’ve closely witnessed technological advancements, with AI emerging as a prominent topic in the last one to two years. At Lulusar, we’re exploring AI’s potential to enhance efficiency, particularly in reducing costs and lead times, a key aspect of our brand identity. We aim to be early adopters, observing various AI applications showcased at events like a fabric procurement fair in Germany.”

He added that, “From pattern making to marketing campaigns, AI offers transformative possibilities, evident in trials where entire

collections can be designed in under a month. Our firsthand experience shows the rapid technological strides made in AI within the industry.”

Hasan admitted that Lulusar has not experimented with AI to generate human models, but they definitely plan on doing so soon. “We want to be the first, amongst the first to adopt it in Pakistan,” he said.

“At Lulusar, we work at a very fast rate. We have a collection come out every week. With AI, we could streamline this process, conducting shoots digitally and rendering them on the same day, enabling immediate publication. This transformative integration could parallel Lulusar’s initial market entry eight years ago,” Hasan divulged.

He added, “Globally, no fashion brand matches our weekly release rate. AI could enhance our inventory management algorithm, optimising our ability to forecast and clear stock efficiently. Currently, we clear 90-95% of inventory within the launch weekend. AI could further increase efficiency, refining our operations based on data analysis. For instance, during peak periods like Eid, AI could predict increased demand and advise on production volume, potentially surpassing our current output estimations. Through a yearlong AI implementation, the system could adapt to our business model, improving order projections and operational efficiency.”

Hasan believes that by aligning AI insights with historical data and business practices, Lulusar could exceed growth projections, potentially achieving 1.5 times our current growth rate annually. He admitted that AI’s potential to revolutionise not only Lulusarr’s operations but also those of other brands by optimising production and forecasting processes.

Commenting on the drawbacks of leveraging AI, Hasan told Profit, “Despite AI’s potential, unethical applications pose concerns due to the lack of regulations, allowing competitors to replicate campaigns. Such misuse can result in misaligned campaigns, targeting the wrong audience or failing to reflect brand identity accurately. Additionally, the misconception of AI’s simplicity undermines its complexity, requiring specific commands and a deep understanding of its capabilities. While AI offers opportunities for innovation, its effective use demands

expertise and caution, making it unsuitable for every team. As someone familiar with AI applications like chat GPT, I can attest to the necessity of meticulous commands for desired outcomes, dispelling the notion of effortless implementation. So, while AI holds promise, its ethical and technical challenges necessitate careful consideration before integration into a brand’s operations.”

He also told an anecdote about an applicant who had used AI to replicate Lulusar’s own campaign when putting together his portfolio. “There was an interview where we had someone come and ask us what we thought of their design aesthetic. And maybe you can argue that to their disadvantage, we are a brand that’s very technologically advanced and we know how to use our technology. So, we found out that in this portfolio that was sent to us from one of these interviewees, they just AI generated our whole collection and pasted it onto their portfolio. How were we able to pick on that? I could tell the backgrounds were very similar. The proportions for the windows were the same. The clothes were also the same, just the colours were different.”

Another possible problem is the pervasive accessibility of AI that may pose challenges as it is marketed as a universally applicable solution. Over the next five to ten years, the acceptance and effectiveness of AI applications will become apparent, given its capacity to create visually engaging content that may attract viewers’ attention more for its artificiality than the actual product.

Hasan, speaking on the matter, said, “A striking ad featuring AI-generated imagery may garner attention but may not necessarily translate into increased sales or engagement. While platforms like Instagram feature novel AI-generated content, its effectiveness in traditional media like billboards or TV ads can not be commented upon yet. Despite AI’s potential to revolutionise industries like fashion, its misuse can perpetuate unrealistic beauty standards, reminiscent of past practices of digitally altering models.” So you might get eyeballs on your advertisement, but not for the right reasons. People might only engage with it because it’s different, not necessarily because the product you are marketing got their attention.

The fact remains, it is volatile and that

raises concerns regarding its influence on societal perceptions and values. If unchecked, AI could reinforce harmful stereotypes and ideals, shaping consumer behaviour in a negative way. It also has the potential to dictate cultural standards, driven by the preferences and biases of its creators. So, careful consideration and regulation are necessary to ensure AI’s potential benefits are maximised while mitigating its negative impacts on society.

The most salient feature that helped shoppers identify the use of AI in Generation’s experiment was limbs and fingers. It is, more often than not, details, such as hands and feet that give it away. If you remember the Kate Middleton fiasco and her unexpected Mother’s Day post that sent the internet into a frenzy, you would know that getting the smaller details of the human body is something that artificial intelligence is not so intelligent in replicating.

Profit asked Soban Raza, CEO of AI company Antematter, why AI always gets the hands wrong? He explained, “It’s widely acknowledged that in AI datasets, human hands are often less prominently featured compared to other body parts. They tend to appear smaller and less frequently in source images, making them challenging for AI models to grasp. While AI learns and replicates patterns, it lacks a true understanding of concepts like finger count, focusing instead on pattern recognition and arrangement.”

He continued, explaining that as a consequence of AI’s lack of understanding of the aforementioned characteristics, if hands or finer details are poorly represented in the dataset, it’s likely that current AI models struggle to generate accurate images. “The variability in human body movements, influenced by factors like age, gender, and individual characteristics, further complicates matters. Additionally, in motion pictures, body parts interact intricately rather than moving independently, posing another challenge for AI comprehension. Subtle nuances, such as the impact of a slightly bent finger, often go unnoticed in datasets, hindering AI’s ability to learn such patterns effectively. Consequently, hands, fingers, and subtle movements tend to be overlooked by AI models,” he concluded.

But is the flaw inherent to the model itself, or is it due to the limitations of the commands provided?

We asked Raza if sophisticating our commands can solve this issue. If we were to feed more detailed instructions and provide distinct components separately, such as feeding pictures of hands separately from images

of the full human figure, will the dataset become clearer?

Raza answered, saying, “This question is a focal point for many well-funded startups and agencies, attempting to strike a balance between dataset refinement and model optimization. Correcting training data might help AI models to get the finer details right, however, such commands may risk model overfitting. This is where proficiency in one task compromises others.”

We learnt that aggressively refining training data may lead to overfitting, focusing on hands and fingers at the expense of other body parts or generative capabilities.

Current AI tools are not advanced enough to perform both these tasks, however, companies dedicated to building and improving AI tools are working to strike the perfect balance.

Another issue you are likely to run into when using AI to generate images, especially of humans and certain cultures, is that AI is largely unregulated and frankly racist. It absorbs internet data leading to stereotypes, often generating images that are inaccurate and biassed, for example traditional Indian women in orientalist scenes. Can this problem be tackled by teaching AI broader, culturally nuanced perspectives beyond traditional, biassed portrayals?

While responding to this question, Raza highlighted, “I think what you mentioned is a very challenging problem. It’s not a problem that is for one startup to solve. It’s actually at the core of the biggest challenges that are currently attacking AI, so to speak, because think about it. The problem that is generative AI has been built from this massive amount of data– the Internet.”

So if we complain that the data fed into AI is biassed, correcting this bias at such a massive scale is insanely complex. Raza elucidated, “So just to make the consumption of this data on the internet possible for creating image, video and audio files took us decades, right? Consumption of such a scale of data to build something was actually remarkably difficult. Now, to debias it and remove stereotypes at that scale presents an open challenge.”

According to Raza, this is an open technological problem that is being worked on at this point in time. Huge loads of money is being thrown at it. “There is no easy answer to say that we should do this or that. It’s just going to unfold as regulations unfold, as technological advancements unfold, maybe big companies like open AI can figure something out on that front. But I think you’ll have to keep worrying about it for the time being.”

When asked what he envisions as the trajectory for developing nations, like Paki-

stan, to harness AI effectively and how can we transition from conventional methods to AI-driven solutions, such as image generation and other generative services, Raza said, “Businesses can gain a significant competitive edge by effectively integrating AI into their workflows, particularly in industries like IT services. By enhancing internal processes with AI, companies can boost productivity and outperform competitors, securing business opportunities they might have otherwise lost.”

He informed that currently, AI serves primarily as an assistive technology, streamlining tasks and increasing operational efficiency by up to 30-40%. The focus lies on improving internal operations rather than developing AI products for external markets, which still requires significant development. Initial steps involve leveraging AI to enhance productivity and operational excellence before expanding into AI product development. Regulatory challenges and other external factors are currently less relevant in the Pakistani economy compared to internal productivity improvements through AI integration.

So, businesses should prioritise optimising internal processes with AI before exploring broader market applications.

We also asked Raza whether fashion brands are a target market for companies like Antematter based in Pakistan, to which he replied, “Many businesses rely on AI software for tasks like trend analysis, market patterns, or accounting, catering to a broad range of industries. However, when it comes to human image generation for ad campaigns, particularly in the fashion sector, the focus may not be as prominent. This isn’t due to a lack of interest from companies like ours but rather a need to understand how such ventures would unfold.”

He confirmed that if fashion brands in Pakistan show interest and traction in this area, AI companies would undoubtedly shift focus. Raza also pointed out a potential issue with this, “The complexity lies in addressing challenges like high-quality training data, transforming 3D data into 2D, and capturing movements effectively. The sophistication of technology, real-time processing capabilities, and attention to model fidelity are critical considerations. The readiness of Pakistani fashion brands to embrace AI will ultimately dictate the pace of progress in this direction, given the country’s historical cautiousness in adopting cutting-edge trends.”

After all these considerations, we concluded that AI, while bursting with the potential to revolutionise content creation, curation and marketing, it will take quite a lot of investment, in terms of capital, efficiency and practice to be able to smartly use the tool for generating AI models and images. n

Despite litigation, losses, and audit troubles, Dewan Farooq Motors has remained a stable PSX investment.

Lots of people claim to know the secret, but the reality is that understanding the stock market is a difficult and inexact science. It doesn’t help when certain shares are feeding the problem.

By Zain NaeemThere are few mysteries in the world that are assumed to be unravelable. UFOs, Loch Ness Monster and our purpose on this planet are just to name a few. Maybe we can add Ishaq

Dar and his cockroach-like ability to never die or fade into oblivion to the list as well. Winston Churchill once famously said that Russia was like a riddle wrapped in a mystery inside an enigma. This Matryoshka doll of a conundrum can also be used to describe the Pakistan Stock Exchange. Or more particularly certain stocks that

are listed on the PSX.

Take, for example, the case of Dewan Farooque Motors. In the past 10 years the company has gone through litigation, their auditor raising red flags, and consistent losses. Despite this, their stock has remained surprisingly strong on the market. That means individuals that have invested in this particular company

have made profits. So why does something like this happen on the stock market?

Dewan Farooque Motors is part of the Yousuf Dewan Group which is involved in manufacturing of cement, textile, spinning, fiber and sugar. Dewan Farooque was established in 1998 as a publicly listed company and entered into contracts with Hyundai Motor Company and KIA Motors Company. The company assembles, manufactures and sells Hyundai and KIA vehicles in Pakistan. For the Gen-Z, know that both these companies were already introduced to the Pakistani Market back in early 2000s. In the earlier version, cars like Santro, Shehzore, Sportage, Spectra and Classic were launched.

The production plant was set up in 2000 and operations started in 2001. Initial sales and profits from the company were nothing short of remarkable. With sales growing steadily from Rs 5.5 billion in 2003 to Rs. 10.6 billion in 2006, the company was able to maintain a steady stream of profits. The company made a profit of Rs 6.63 per share in 2005 and had a track record of giving out healthy dividends in the form of cash and bonus shares as well.