10 The stalled arrival of working women in Pakistan

16 From textile seth to freelancer: the evolution of Bilal Fibres

18 Electricity generation finally stabilizing after two years of declines

20 First Dawood completes first building

22 What is happening to KP’s tobacco farmers?

25 Rating agencies back Pakistan’s recovery story ahead of international debt push

28 Crypto exchanges need to earn Pakistan’s trust with on chain protection Maha Shah

30 Much ado about Matcha

Publishing Editor: Babar Nizami - Editor Multimedia: Umar Aziz Khan - Senior Editor: Abdullah Niazi

Editorial Consultant: Ahtasam Ahmad - Business Reporters: Taimoor Hassan | Shahab Omer

Zain Naeem | Saneela Jawad | Nisma Riaz | Mariam Umar | Shahnawaz Ali | Ghulam Abbass

Ahmad Ahmadani | Aziz Buneri - Sub-Editor: Saddam Hussain - Video Producer: Talha Farooqi

Director Marketing : Muddasir Alam - Regional Heads of Marketing: Agha Anwer (Khi) Kamal Rizvi (Lhe) | Malik Israr (Isb) - Manager Subscriptions: Irfan Farooq Pakistan’s #1 business magazine - your go-to source for business, economic and financial news. Contact us: profit@pakistantoday.com.pk

By Farooq Tirmizi

TThe stalled arrival of working women in Pakistan

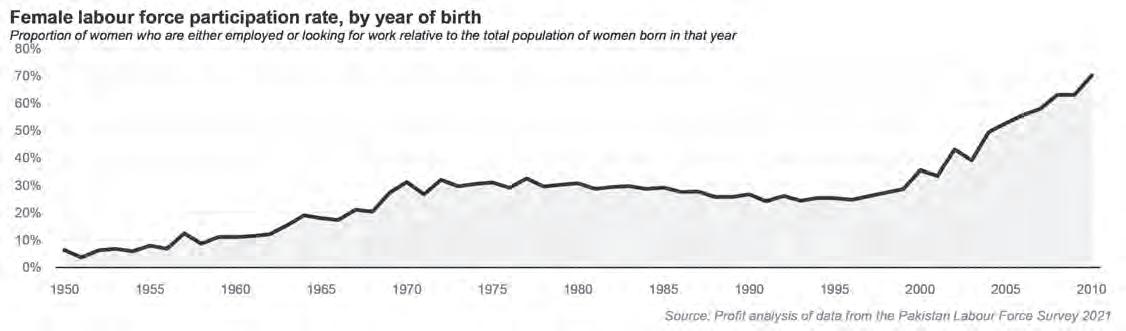

After rising rapidly in the first decade of this century, female labour force participation in Pakistan has flatlined. What drives that stagnation?

he image of twentieth and twenty-first century modernity is the two-income household: a man and a woman both earning an income and perhaps sharing in child-rearing responsibilities. The modal household in Pakistan is also a two-income household, but more often than not, the two incomes come from two related men – a father and son, or two brothers, or even two male cousins. Some households have a man and woman bringing in an income, but not many.

In 2012, then writing for The Express Tribune, this scribe wrote about the rising female labour force participation rate in Pakistan, which had doubled over the first decade of the century. It seemed as though Pakistan’s labour force was about to join that image of modernity.

That revolution in household economic relationships – and the social revolution it would undoubtedly have precipitated – did not come to pass. The female labour force participation rate in 2021, the latest year for which data is available, was at 21.3% of the working age population, according to data from the Pakistan Bureau of Statistics’ Labour Force Survey, somewhat lower than the 24.4% it reached in 2011.

Effectively, the last decade and a half has seen no changes in the economic status of women in Pakistan, even though some key leading indicators – notably literacy and education – would have predicted a continued rise in labour force participation and income levels.

So, what happened? Why have Pakistani women not seen their economic fortunes rise? What is the scale of this stagnation, and what factors may have contributed to it? This article is not an academic paper seeking to establish causality, but we will lay out some variables that we believe may be relevant and are correlated to the stagnation.

More than anything else, this may be one of the most important economic stories about Pakistan: what is happening with women in the country?

The rise of the female workforce

In the year 2000, the proportion of Pakistani women in the labour force was around 16.3%, according to data from the Pakistan Bureau of Statistics (PBS). Over the next decade or so, that number steadily kept on rising until 2011, when it peaked at 24.4% of working age women were in the labour force.

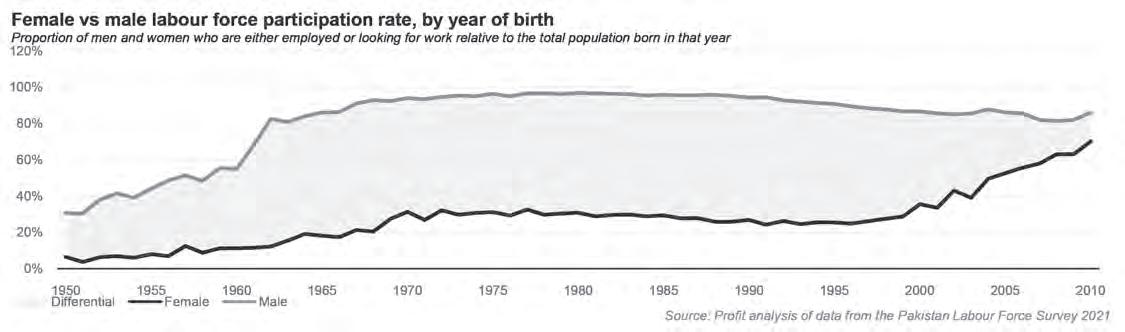

To understand how this happened, it helps to first understand what happened to men.

In 2000, the proportion of men in the Pakistani labour force who worked in agriculture was around 43.4% of economically active men. By 2011, that proportion was down to 34.9% of economically active men. That is an 850 basis point (8.5 percentage points) swing away from agriculture. Where did those men go?

The numbers are relatively evenly split: about 55% of the men who moved away from agriculture went into jobs in manufacturing, and the remaining 45% went into jobs in the services sector.

It makes sense that industry took the majority of that increase in male employment, since this was an era when the share of manufacturing in the total size of the economy grew. Industry as a percentage of gross domestic product (GDP) went up from 18.2% in 2000 to 21.9% in 2011.

Strictly speaking, though, the actual number of men employed in agriculture did not fall during that decade. In fact, it rose by about 1.8 million. But total employment in agriculture in Pakistan

rose by about 7.1 million people during that time, which meant that the incremental 5.3 million women entered the agricultural labour force in the country.

This movement of men into different sectors had a deep impact on women’s economic prospects. Not only were more women drawn into the workforce, the unemployment rate for women – the proportion of women who want a job but do not currently have one – also fell dramatically, from about 15.8% in the year 2000 to a still high, but relatively lower, 9% in the year 2011, according to PBS data.

In short, the economy grew rapidly, and created more opportunities for better paying jobs in sectors that had previously been smaller. Men moved into those jobs, and women took the jobs that the men left behind.

In Pakistan, as in other countries, women moved into spaces that men had vacated.

The stagnation

What followed next was a stagnation, and indeed a slight decline. The female labour force participation rate went from its peak of 24.4% in 2011 to 21.3% in 2021, the latest year for which data is available. What is somewhat surprising is that this happened despite the fact that the trend of men moving

away from the farm to work in factories and service sector jobs in the cities and small towns continued.

The proportion of men who work in agriculture has fall to just 28.4% of economically active men in 2021, which represents about 14.7 million men. That means there are 1.1 million fewer men working in agriculture in 2021 than there were in 2011.

What’s more surprising is the fact that the agricultural labour force itself has been relatively stagnant even in absolute terms. Indeed, the total number of people in Pakistan employed in agriculture has declined by about 372,000 people during the decade between 2011 and 2021. The total number of women working in agriculture went up slightly, by about 728,000 people.

It is not as though the Pakistani economy has not created jobs during this decade. Indeed, the total number of jobs created between 2011 and 2021 was about 13.4 million, according to Profit’s estimates based on PBS data. It is just that the entirety of those new jobs came in the services sector and manufacturing.

Women’s share of those industries also rose during this period. In 2011, about 74% of economically active women worked in agriculture, a number that had declined to 67% by 2021. In other words, at least some proportion of the net new jobs created in manufacturing

and services did go to women. It was just that it was a small fraction of those jobs.

Of those 13.4 million net new jobs created in services and manufacturing during the period between 2011 and 2021, only about 2.5 million went to women. The total number of women employed during this period went up by slightly more: about 3.2 million, driven in part by the fact that female employment in agriculture continued to rise even as male employment in that sector fell.

What is clear is that the number of jobs created for women did not keep pace with the rise in the female population. This is despite the fact that several factors such as literacy rates are rising even among Pakistani women. But perhaps given the nature of job creation in Pakistan, the difference in male and female literacy rates may at least be a factor.

The literacy factor

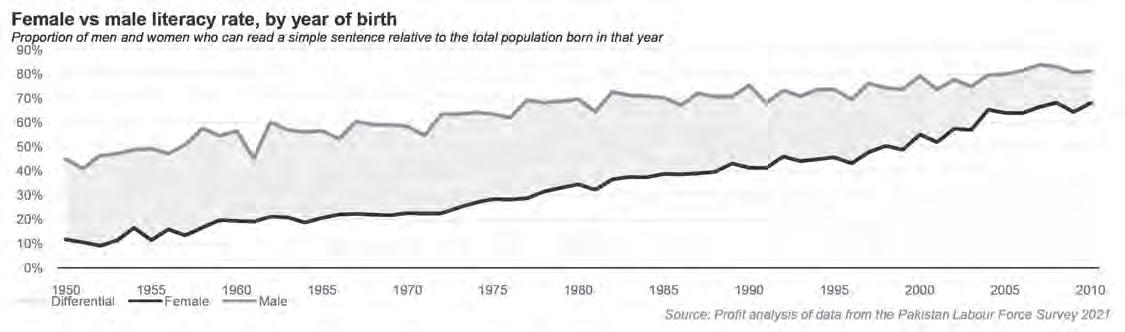

Female literacy in Pakistan is considerably lower than that of men in Pakistan: 46% for women compared to 71% for men, according to PBS data. This gender gap in literacy may explain a substantial portion of why female labour force participation rates rose in the first decade of the twenty-first century, but has since stagnated.

As we’ve stated above, between 2000 and

2011, the increase in female labour force participation was driven by the fact that men were moving into services and manufacturing jobs, and leaving behind agricultural jobs that not only still needed to be done, but were an area of continued employment growth. Almost all of that increase went to women, which in turn increased their labour force participation rate.

To work on a farm does not require literacy, which meant that Pakistani women’s disadvantage in literacy did not inhibit them from moving into the farming jobs vacated by men. What has come next, however, has been much more complicated, and that literacy disadvantage has become more relevant.

Jobs in both manufacturing and the services sector do not universally require literacy, but it is generally much more likely that they do, and even if literacy is not a strict requirement, it is certainly helpful to be able to read and perhaps even write.

Over the previous decade, the entirety of the net new creation of jobs in Pakistan has come in services and manufacturing, which advantages those who are literate over those who are not. In Pakistan, that means men have an advantage over women in this matter, at least for now.

The historical effects of the literacy disadvantage of women in Pakistan can be judged by the following fact: a women in Pakistan

born in 2010 is as likely to be literate as a man born in 1978: both cohorts have a 68.3% literacy rate. At least historically, women were a full generation behind men in terms of literacy.

But what does this bode for the future?

The catch-up period

By most measures, female literacy rates in Pakistan are rising. The rate was as low as 35% in 2005 and has risen considerably in the two decades since then. The increase is driven largely by the fact that younger women and girls are far more likely to be educated than their older counterparts. Indeed, in urban Punjab, the gender gap in literacy among adolescents and young children is virtually non-existent.

Illiteracy, especially female illiteracy, is concentrated among the old and the rural population. The younger and more urban a population gets in Pakistan, the more likely they are to be literate.

Meanwhile, it is very likely that agriculture, the one area where literacy is not a material advantage, has completely stalled out as a job generation engine for the Pakistani economy. In fact, it is likely that agriculture will ne a net drain on job creation in the country over the next few decades as more automation means fewer and fewer people need

to work on farms.

That means that this past decade, and likely part of the next one, are a temporary lull in the economic activation of women in Pakistan. It happened during a unique phase when agriculture ceased to generate more employment opportunities, but women’s literacy had not caught up for them to be able to take advantage of the jobs being created in services and manufacturing.

But a 13-year-old girl in urban Punjab, the province with the highest population, is just as likely to be educated as a 13-year-old boy: both at 88% literacy rates. In the next five years, both of them will enter the labour force, and neither will have an advantage over the other.

At that point, the rise in female labour force participation is likely to resume, and income levels across Pakistani households are likely to begin rising at a faster pace than they have over the past few decades.

Combined with the fact that Pakistani households have fewer – but not a catastrophically low number of – children means that not only are household income levels likely to rise, but also household savings, which ultimately will increase the among of capital available in the economy for investment in growth.

This is an idea we have previously covered in our story “The bull case for Pakistan”, so we will not go through the details again

here. But the added layer to that analysis we present here is the fact that a key ingredient in that rise is the realisation of benefits of educating women and girls in Pakistan.

We want to emphasise one thing: we are not saying that this rise in female labour force will happen because at some point in the future, a sufficient number of girls will be attending schools. We are saying it will happen because girls who have already been in school long enough to have become literate will grow up and enter the labour force because they are qualified for the jobs that are opening up in the economy.

The family and marriage factor

In our analysis, we wanted to examine one other factor: do patterns relating to marriage and family formation have an impact on women’s ability to enter the labour force? To reiterate, this is not an academic exercise where we have been able to establish a direction and pattern of causality. However, some variables are relevant and correlated to female labour force participation and we present them here in the hopes that researchers may take the analysis forward in a more rigorous manner.

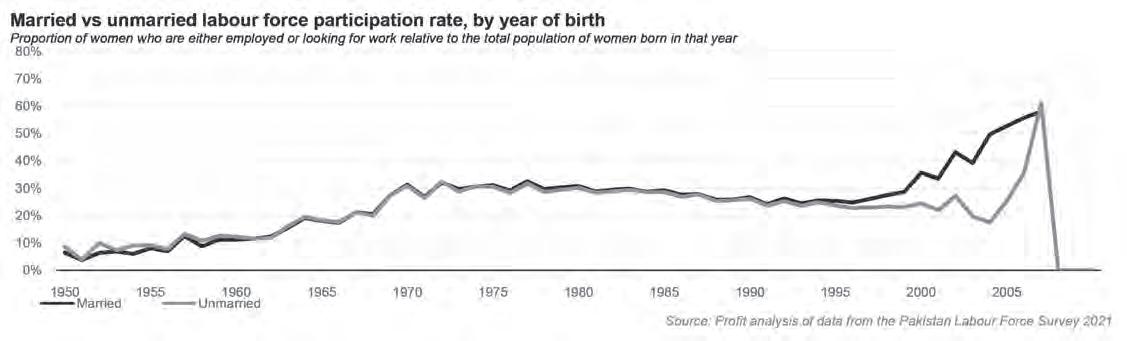

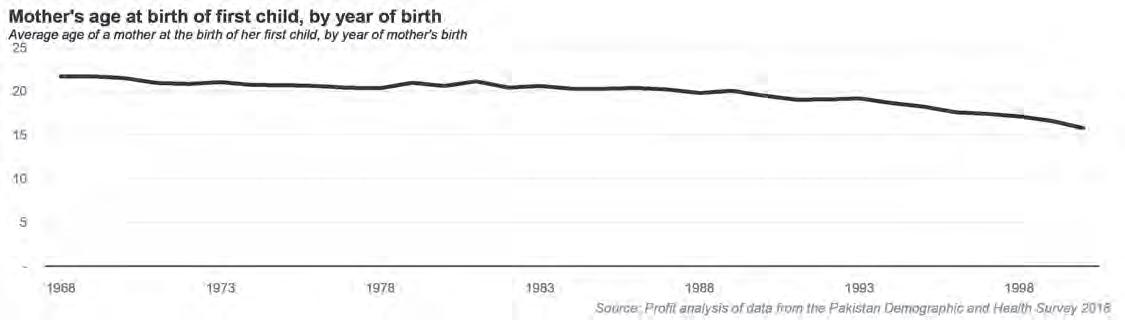

One of the most surprising findings based on our analysis of the Labour Force Survey data is that female labour force participation rates do not appear to be materially different for married versus unmarried women older than the age of 27. Younger than that, female labour force participation rates are sharply lower.

Why might this be? Well, the average age of a Pakistani mother at the birth of her first child has hovered between 19 and 21 for the past 50 years and has not materially risen during that period. The number of children the average Pakistani women has is currently 3.3 and has historically been higher. It seems reasonable to assume that a woman who has her first child at age 21 is done having her third

child by age 27 and may be ready to enter the labour force in one form or another.

This is an important point to highlight: the data suggests that even in a traditional society like Pakistan, while women take time away from the labour force during the early years of their children’s lives, having children does not preclude them from entering it after their children reach their school-going years, at least in the modern era.

What has been a more limiting factor is the historical reticence of parents to send their daughters to schools at the same rates as their sons, and even in this, it appears the story appears to be more complicated.

Take a look at enrolment rates for girls and boys at the primary school level, even going back several decades, and one notices that about 90% of children get enrolled in some form of school and that the difference between girls and boys that young is not material: even in rural Pakistan, most parents are equally likely to send their 6-year-old daughter and 6-year-old son to the village primary school.

The problem arises from an interaction of two factors: the poor quality of primary education in most of Pakistan, and the lack of availability of sanitary pads for girls reaching puberty.

Literacy levels among students who have had even five years of primary school education in Pakistan are atrocious. Simply put, the kids do not learn much for the first few years of their schooling. Students who complete at least eight years of schooling, however, are almost universally literate, but a sizeable plurality of people with fewer than eight years of schooling remain illiterate.

In other words, schools in Pakistan are so bad that it takes, on average, eight years to learn how to read basic sentences and achieve basic literacy.

The problem for girls is that the eighth year of schooling often falls after they have hit puberty, a point at which the vast majority of their parents pull them out of school. Why? It is unclear exactly what makes them make that

decision, but in 2011, when Procter & Gamble started distributing free sanitary pads to girls in rural Sindh, school enrolment rates for those girls in middle school went up sharply.

For whatever reason, at the onset of puberty, parents pull their girls out of school, but if they find a convenient means of their daughters being able to manage their menstrual cycles, their reticence to send them to school disappears.

What comes next

Here is the punchline: female economic activity stalled out over the last decade because of decisions made in decades prior to that to not educate girls at the same rates as boys. It is clear from more recent data that, while the gap has not been eliminated completely, and certainly not nationwide, it may be narrowing enough that the next few decades may see more of the newly educated cohorts of girls age into educated young women able to participate in the workforce at the same rates as their male counterparts.

The big social revolution – driven by increased female economic power – is yet to come in Pakistan. And while it is not unfair to decry the fact that Pakistan lags even its geographic peers in achieving comparable levels of female economic power, perhaps we can take advantage of being behind by working now to address some of the problems that typically arise when this happens.

Most notably, in most countries, men do not react well to a loss of relative economic power, which in turn leads to a fraying of the social fabric. By virtue of the fact that progress in Pakistan has been slower, perhaps Pakistani men will have more time to adjust to the rising economic power of women and have less negative reactions compared to their counterparts in other regions of the world.

What is clear, however, is that the past is a different country, and the future holds an entirely new way of life for Pakistan. n

From textile seth to freelancer: the evolution of Bilal Fibres

The mill shut down a long time ago, but the sponsors of Bilal Fibres now want to move into the kind of services business that has recently taken off in Pakistan

Profit Report

Four days ago Bilal Fibres Ltd (PSX: BILF) – once a modest spinning mill on the dusty Sheikhupura Road – told the Pakistan Stock Exchange it had approved a Rs10 million business plan to create an in-house IT division. The nine-page filing sketches a start-up more reminiscent of a co-working loft than a ginning shed: five laptops, two software engineers, a marketing specialist, and a go-to-market playbook that explicitly name-checks Upwork, Fiverr and other online labour platforms for client acquisition.

Management says the cash will cover basic kit, registrations and one year of salaries; breakeven is pencilled in for “12–18 months” on the back of website builds (Rs100–250 k each), mobile-app minimum viable products (Rs300 k–1 m) and monthly IT-support retainers. Board minutes show annual revenue potential of Rs12–70 million if the team lands even a handful of contracts each quarter.

The announcement follows an earlier progress report stating that spinning operations remain suspended and that the mill’s revival would hinge on “Technology/ICT… in view of limited financial resources”. External coverage quickly framed the shift as “a textile manufacturer entering IT” and highlighted the board’s hope of tapping SME demand at home

and in the Gulf.

If the plan sounds quixotic, investors do not seem fazed: BILF shares are still up more than eight-fold year-to-date, trading at Rs21.3 compared with Rs2.3 last October, despite the company recording zero yarn sales for two straight years.

Pakistan’s rise in the global freelancing league

Bilal Fibres is not alone in betting on Pakistan’s digital piece-rate economy. The country now accounts for 15.1 per cent of all workers on global

freelancing platforms, behind only India and Bangladesh, according to the University of Oxford’s Online Labour Index. Government data tell a similar tale: freelance remittances officially topped US$ 400 million in the first nine months of FY-25 and are projected to cross US$ 500 million by June, outpacing many manufactured-goods exports.

This surge rests on three pillars. First, a youth bulge – 65 per cent of Pakistanis are under 30 – is comfortable selling code, design and analytics services abroad. Second, state-run training such as the DigiSkills.pk programme has certified 4.6 million learners, creating a conveyor belt of entry-level talent. Third, an uncertain domestic jobs market makes dollar-denominated gigs attractive: average freelance hourly rates on Fiverr hover around US$ 23 for full-stack developers, five times the local minimum wage.

The model is not friction-free. Platform outages earlier this year – when Fiverr briefly labelled many Pakistani profiles “unavailable” amid nationwide bandwidth throttling –exposed how sensitive earnings are to policy blips. Payment channels likewise remain patchy in a country still waiting for PayPal. Yet the momentum is unmistakable: the IT-, ITeS- and freelance-export pie hit a record US$ 4.6 billion in FY 2024-25, up 26 per cent on the year.

Against that backdrop, Bilal Fibres’ plan to fish on Upwork looks less like a lark and more like a low-capex attempt to catch a proven wave.

A brief corporate history

Founded in 1987 and listed on the Karachi bourse soon after, Bilal Fibres spent three decades churning out poly-cotton and viscose yarn for Asian and European buyers. At its peak the Jaranwala mill boasted 20,000 spindles and employed 500 workers.

The trouble started with the postCOVID energy crunch and rising borrowing costs: gas rationing idled looms, while markto-market losses on cotton inventory blew out working-capital lines. By FY 2023 the company had already suspended production; FY 2024 accounts record zero sales, a Rs20 million net loss and accumulated deficits of Rs586 million.

In October 2024 directors approved an asset-disposal scheme to sell the entire Sheikhupura Road complex – plant, land, even right-of-use assets – and plough the proceeds into a new tech venture. The same resolution authorised a change of name and object clause, though that legal paperwork is still pending with SECP.

Investors initially greeted the pivot

with scepticism; the scrip traded under Rs3 until January. But a speculative buying spree, fanned by social-media chatter about a potential “mini-Systems Ltd”, has since turned BILF into one of 2025’s best-performing small-caps.

Remote work, AI and the market Bilal Fibres hopes to enter

Pakistan’s telecom network now reaches 91 per cent of the population, while 4G coverage sits above 96 per cent of live cell sites. Affordable fibre in Lahore means Bilal Fibres can run a fully remote stack with minimal on-premises hardware. At the same time, generative AI is accelerating developer productivity: Deloitte’s 2025 TMT Predictions note that code-generation copilots can cut development time by up to 45 per cent, pushing more projects towards fixedprice delivery models that suit freelancers.

With even conservative forecasts showing Gen-AI “embedded into nearly every company’s digital footprint by 2027”, small shops that master the tooling early enjoy a genuine arbitrage against slower incumbents. Bilal Fibres’ filing hints at that advantage, promising “cost-effective, high-quality IT solutions” powered by lean teams and AI-augmented workflows.

Yet the same AI democratisation also lowers entry barriers, flooding gig sites with auto-generated bids and squeezing margins.

Platform dependence is a second hazard. The Fiverr “unavailable” episode shows how a single API tweak or geopolitical flareup can wipe a month’s pipeline overnight. Diversifying into direct enterprise contracts or building proprietary SaaS products – both flagged in the board’s business plan – will therefore be critical for durability.

Third, capital. Even after this week’s rally, Bilal Fibres’ entire market cap is just Rs300 million (≈US$ 1 m) and the balance-sheet is thin: the mill land is earmarked for sale, cash reserves are minimal, and previous losses have eroded equity. A Rs10 million seed budget may suffice for proof-of-concept apps but not for chasing enterprise-grade contracts where six-figure dollar invoices –and working-capital buffers – are the norm.

Industry data suggest the addressable market is still expanding. Global spending on outsourced software development is forecast to grow at 7 per cent CAGR through 2028, and Pakistan’s IT & ITeS exports have delivered double-digit growth for seven consecutive years. (Profit by Pakistan Today) Within that pie, freelance platforms remain the fastest-growing channel because they de-risk vendor onboarding for overseas SMEs.

On the flip side, text-to-app AI tools

threaten to commoditise entry-level work such as static websites – precisely where Bilal Fibres hopes to win its first clients. The firm’s plan to evolve into subscription SaaS and staff-augmentation services will therefore need to materialise quickly if it wants to avoid a race to the bottom on gig portals.

Balance-sheet headroom for the pivot

Because yarn production is mothballed, Bilal Fibres’ assets today are mostly idle plant and land. The October 2024 board resolution lists “property, plant & equipment, right-of-use assets, investment property, stock-in-trade and other assets” for disposal – a fire-sale expected to yield Rs250–300 million net of liabilities, according to brokers following the notice.

Assuming the mill finds a buyer at book value, management could fund two additional Rs10 million tech pods without fresh equity, and still clear legacy bank debt. But that optimistic scenario depends on appetite from larger textile players already nursing their own overcapacity.

Meanwhile, the IT venture’s initial outlay – roughly three per cent of market cap – is small enough that a failure would not bankrupt the company; success, however, could transform its multiples. For now, the share price implies investors grant Bilal Fibres an option premium on the digital future rather than on polyester-cotton yarn.

Whether Bilal Fibres’ reinvention inspires copy-cats across Pakistan’s struggling textile belt will hinge on execution. Converting looms into laptops is not unprecedented – Crescent Textile spun off an IT wing in 2019 – but it remains rare. The company will need to:

• Hire and retain talent against stiff competition from established software houses in Lahore’s Arfa Software Technology Park.

• Shift corporate culture from shift-based factory routines to agile sprint cycles and remote Git workflows.

• Navigate regulatory hoops: IT exports now qualify for a 0.25 per cent tax rate, but only if certified by the Pakistan Software Export Board – paperwork the board has yet to complete.

If those hurdles are cleared, Bilal Fibres may go down as the first listed Pakistani mill to swap cones of yarn for lines of Python – a micro-signal of how even legacy manufacturers can pivot when the global gig economy beckons. Conversely, if the plan falters, sceptics will chalk it up as another speculative detour by a loss-making penny stock. n

Electricity generation finally stabilizing after two years of declines

Government policy may finally be encouraging more use of grid electricity by industrial users

PProfit Report

akistan finally has a growth line instead of a skid mark on its power-generation chart. Fresh numbers compiled by the National Electric Power Regulatory Authority (NEPRA) show total grid output at 127 159 GWh for fiscal year 2025, essentially flat year-on-year after a twoyear slide. The real story lies in the turnaround of the final quarter: April-to-June deliveries jumped 7% compared with the same period a year ago, clawing back the losses recorded in the first nine months of the fiscal year.

What changed? Analysts at Topline Securities point to an “off-grid levy” introduced in February 2025. The surcharge makes self-generated units (mostly gas and furnace-oil captive plants behind factory gates) pay a contribution to national capacity charges. That single stroke nudged many industrial users back onto the network, boosting dispatch volumes in Q4.

Monthly data from Arif Habib Ltd (AHL) capture the pivot: in June 2025 the system produced 13 744 GWh, up 2% on the prior year and 8% on May. Hydel output led the gain, surging 14% year-on-year, while imported-coal plants ran 119% harder, plugging the gap left by gas and RLNG turbines that slowed

on feed-stock constraints.

Alongside volume stability, average fuel cost for the year dropped to Rs8.6 per kWh, down 2% on fiscal year 20-24. June’s headline fuel cost was even lower at Rs7.87; once transmission losses and prior adjustments are factored in, consumers will see a refund of roughly Rs0.65 per kWh in their August bills.

The mix, meanwhile, continued its slow tilt toward domestic resources. Hydropower supplied 31% of units, nuclear 18%, indigenous coal 12% and wind about 3%; expensive furnace-oil generators accounted for a token 0.4%. Three small hydel schemes (SK, Pehur and Marala) plus the revived 150-MW Lakhra mine-mouth plant eased onto the bars during the year.

Why grid stabilisation matters in the age of rooftops

Aflat production line would hardly be news in most markets, yet in Pakistan it signals a break in a worrying trend: large customers have been unplugging themselves. High tariffs, dollar-linked “capacity” payments and chronic load-shedding pushed industries toward gas engines and diesel gensets long before the rooftop-solar boom arrived.

Then came net-metering (2017) and a solar price crash. Imports of photovoltaic panels crossed US$1 billion in calendar 2024, and unofficial estimates put rooftop and captive solar at more than 5 GW—roughly one-third of last year’s grid summer peak. DisCos from Peshawar to Hyderabad now record daytime reverse flows that would have been unimaginable five years ago, forcing them to curtail central plants or spill hydel water.

The grid’s rescue in fiscal year 20-25 therefore carries outsized strategic weight. First, it slows the death spiral in which fleeing kilowatt-hours leave behind the same fixed capacity bill to be divided among fewer paying units. Second, it buys planners time to integrate variable renewables without stranding multi-billion-dollar thermal assets built in the post-2015 China-Pakistan Economic Corridor (CPEC) boom.

None of this erodes the logic of distributed generation. Solar’s share of utility-scale dispatch is still below 1% (1 185 GWh, up 15% year-on-year), a statistic that says more about Pakistan’s planning lag than about potential. But by showing that grid energy can be cleaner and cheaper than many diesel or gas captives— thanks to hydel and nuclear dominance—the fiscal year 20-25 numbers make the national network relevant again in corporate boardrooms planning their next energy strategy.

Policy nudges: from self-generation back to the wires

Islamabad’s toolbox over the past 18 months has included carrot, stick and accountancy sleight-of-hand:

Measure

Off-grid levy on captive units

Tariff rebasing and temporary relief

Fuel cost adjustment (FCA) refunds

PDL on furnace-oil imports for captives

round of talks concluded in December 2024 cut return on equity for 12 early CPEC plants by 150 basis points and converted dollar indexation to Rsfor local cost components. The savings, Topline notes, helped finance the Q4 tariff relief without widening the circular-debt hole.

With merit-order enforcement and outages, RLNG plants ran at 17% share, down

Details & timing

Imposed February 2025 under the Finance Act; set at Rs1.25 per kWh equivalent, indexed to national capacity cost

Savings from Independent Power Producer (IPP) renegotiations and a re-routed Petroleum Development Levy (PDL) allowed Rs3.23 per kWh cut on industrial peak rates (Apr-Jun 2025)

Lower-than-forecast RLNG and coal prices delivered a Rs0.65 per kWh negative FCA for August bills

From March 2025, FO cargoes attract Rs10 000/tonne PDL unless destined for licensed IPPs

Add to this the long-delayed launch of competitive trading in bilateral contracts (CTBCM), scheduled for pilot phase early next year, which will let industrial buyers contract energy directly from generators while still paying a wheeling fee to the grid. Together the measures are redrawing the calculation that once made a 20-MW gas engine more attractive than a KE or FESCO connection.

Cost control after the capacity splurge

Even as units sold stabilise, policymakers still face the elephant of overcapacity—roughly 44 GW of installed generation against a system peak below 30 GW. Capacity payments to IPPs now eat more than half of every tariff rupee. The government’s multi-pronged response is beginning to show in the cost curve.

Hydel, nuclear and local coal together provided 61% of fiscal year 20-25 energy at sub-Rs5 per kWh marginal cost, pushing imported oil to the margin at just 0.4% of dispatch. A 28% drop in coal-fired generation cost, thanks to cheaper seaborne prices, shaved another Rs6-7 billion off the monthly fuel bill.

On IPP tariff renegotiations, the second

macro recovery and the central bank’s ratecut cycle. AHL’s models, meanwhile, suggest the fuel-cost component of tariff will stay below Rs9 throughout the fiscal year, assuming Brent averages US$75 and Newcastle coal US$130. That combination—rising units and contained cost—would finally let the power sector’s cash wheel turn forward instead of backwards.

Intended effect

Neutralise the “free ride” captives enjoyed on grid reserves; make grid power cost-competitive

Sweeten grid tariffs for bulk users during peak cooling season

Early evidence

Q4 generation rose 7% after the levy; analysts attribute much of the jump to captive diversion

AHL cites “reduced tariffs” as a driver of June demand rebound

from 19% a year earlier, because dispatchers finally honoured the lower variable cost of Thar lignite units (now 12% share) and kept many FO plants cold-stacked.

On curbing “missing” units, NEPRA’s data show actual fiscal year 20-25 generation was 6% below the reference plan, leaving 7.8 TWh of capacity payments uncompensated by energy sales. By improving collections and reallocating PDL, the finance ministry plugged the cash-flow gap without adding to sovereign guarantees—at least for now.

Still, risk lingers. Roughly 46% of dispatch relied on RLNG, imported coal and pipeline gas at an average fuel cost of Rs16.5 per kWh. If commodity prices rebound, the fledgling stability could unravel. Moreover, renewable penetration must accelerate to hit the government’s 60-30-10 (renewables-hydro-thermal) 2030 target, or the grid could swap one expensive dependency for another.

Outlook: fragile equilibrium, but a credible floor

Topline projects 5-8% growth in electricity consumption in fiscal year 20-26 on the back of continued captive migration, early signs of

Refund will hit corporate ledgers in Q1-fiscal year 2026

Analysts expect 5-8% extra grid demand in fiscal year 20-26 from FO captives switching over

Three caveats temper the optimism:

• Circular debt still tops Rs2.6 trillion. Lower fuel cost does not automatically clear the backlog of unpaid capacity invoices unless DisCos improve collection and the finance ministry sustains subsidy payments.

• Solar’s silent march. Even with the levy, captive and rooftop systems can undercut grid energy at today’s module prices. Unless the CTBCM framework lets developers sell surplus solar at a fair wheeling fee, the exodus could resume.

• Climate volatility. Hydel now provides nearly one-third of units, leaving the grid exposed to drought risk. Early snow-pack readings for 2026 are encouraging, but another dry spell like 2022 would force costly LNG spot buys.

For the moment, however, the narrative has flipped. What looked like a terminal decline in national-grid relevance has paused—perhaps even bottomed out. The June quarter’s bump may be modest, but it arrives at a crucial inflection point for a country racing to decarbonise, reindustrialise and keep its sovereign balance-sheet afloat. After two years of contraction, Pakistan’s electricity sector has shown it can still steady the ship when policy, pricing and physics finally row in the same direction. n

First Dawood completes first building

Company likely invested Rs80-90 million in the new project, with the objective of receiving Shariah compliant rental income

Profit Report

After three decades on the Pakistan Stock Exchange, First Dawood Properties Ltd (FDPL) has finally put bricksand-mortar to its name. In a regulatory notice on 22 July 2025 the company confirmed that it has “successfully completed construction of its first property project in Ayubia Commercial, Phase VII (Ext.), DHA, Karachi” and is now courting tenants for Shariah-compliant rental income. Standing on a 100-square-yard corner plot bought for roughly Rs35 million six months earlier, the five-storey mixed-use block adds around 4,500 sq ft of lettable space to one of the Defence Housing Authority’s

tightest commercial grids. Similar plots on the same strip have recently fetched Rs3.5–5 crore, according to Zameen.com listings, with grey-structure construction in DHA Karachi now costing between Rs3,500 and 5,500 per square foot. On that basis, estate advisers interviewed for this article place FDPL’s all-in investment at roughly Rs80-90 million (US $280-310 k), excluding fit-outs – a manageable outlay for a balance-sheet that now exceeds Rs1 billion.

Management is marketing the property as a “riba-free” income stream, emphasising fixed rentals and an avoidance of interest-based escalation clauses. Sources close to the company say two national retail chains and a regional micro-finance bank have separately expressed interest, with opening rents guided

around Rs450-500 per square foot per month –enough to deliver a gross yield of 25-30 percent on cost once the building is fully occupied. For FDPL, the hand-over is more than a ribbon-cutting: it is proof-of-concept for a long-promised pivot from dusty investment banking licences to bricks, leases and NAV re-ratings.

A wider re-rating of property on the PSX

The Karachi tower surfaces at a moment of re-awakening for listed property vehicles. After years in which developers preferred unlisted Special Purpose Vehicles (SPVs), the PSX is again seeing real-estate capital raisings:

Listed platform

Dolmen City REIT (DCR)

TPL Properties (TPLP)

Javedan Corporation (JVDC)

Pace Pakistan (PACE)

806k sq ft mall & offices, Clifton

13 m sq ft dev. & REIT fund

1,366-acre Naya Nazimabad Township

Retail malls (Lahore, DHA City)

Together these counters have added Rs72 billion to market capitalisation over the past twelve months – a 37 percent sector rerating that analysts attribute to falling interest-rates, the first successful REIT exits and a government amnesty on construction income. FDPL’s micro-project is minute beside Dolmen’s Clifton mall, yet its timing taps straight into this sentiment.

FDPL’s management has already flagged a small-but-scalable strategy: replicate the Ayubia build-and-rent model on multiple 100–200 sq yd plots in DHA, and seed the resulting rental cash flows into a Shariah-compliant development REIT within three years. If the yields on its maiden block hold, that plan could find backers.

How a leasing house became a landlord

To understand the significance of a single building, one must rewind to June 1994 when Dawood Leasing Company Ltd listed in Karachi with a Rs 250 million floatation that was oversubscribed by 47 per cent. Re-named First Dawood Investment Bank Ltd (FDIBL) two years later, the firm rode Pakistan’s credit boom to a Rs 12 billion balance-sheet and regular dividends.

The 2008 global liquidity crunch abruptly punctured that trajectory. With local banks refusing to roll money-market lines, FDIBL faced a creditor run and spent 2009–13 liquidating assets to reduce liabilities “from Rs 10 billion to well under Rs 400 million”. Equity survived – mainly in the form of deferred tax assets – but the investment-bank licence expired, and what remained of management began scavenging for a new business model.

Real estate, long a sideline for the Dawood Group, provided the answer. In March 2024 shareholders voted to rename the company First Dawood Properties Ltd and rewrite its objects clause to include prop-

Broke ground on 400-acre mixed-use Mangrove project; all assets to be LEED Gold

Launched phase-IV apartments; 40 % dividend FY-24

Board approved asset sales & debt-equity swap in June 2025

erty development, management and trustee services. A 1-for-20 rights issue in June 2024 raised modest fresh capital, but – as insiders concede – the real aim was to unlock a market rerating by dragging legacy NBFC equity into the higher-multiple property peer group.

The completed Ayubia block is therefore both a revenue test and a branding exercise: proof that the ticker FDPL now stands for towers, not term-finance certificates.

What the balance-sheet says about expansion headroom

Aglance at FDPL’s latest balance sheet (period ended 31 March 2025) shows why management chose a compact first project.

Two points leap out. First, cash is negligible – barely Rs190,000 – because FDPL deploys every rupee it raises or recovers. Second, more than Rs560 million sits in a liquid, mark-to-market portfolio, half of it quoted shares in group vehicle 786 Investments Ltd and Dawood-managed mutual funds. Management has already sold 2.25 million 786 shares since March, generating an estimated Rs40 million cash inflow, and confirms further stake sales are “on the table” to fund new plots.

On the liability side, total debt is Rs278 million – a modest 27 percent of assets – and chiefly legacy settlement paper. With NAV per share at Rs4.82 against a market price of Rs6.30, the company still trades at a 31 percent premium to book, implying equity markets expect those investments to crystallise at higher values or to be recycled into higher-yielding property assets.

Assuming each Ayubia-scale project requires Rs85 million and 30 percent equity, FDPL could, without new borrowings, finance roughly three similar builds from investment sales alone. Should rental cash flows arrive on

schedule, the company could in theory lever them at 50 percent loan-to-value via Islamic diminishing-musharaka structures, doubling the rollout pace to six buildings over the next 24 months.

Yet risk abounds. Deferred tax assets –13 percent of the balance sheet – only crystallise if the company generates taxable profits; long-term investments remain vulnerable to Pakistan’s famously volatile equity market; and the loan-book, while shrinking, continues to carry legacy disputes.

Sector context: lessons from the majors

What FDPL lacks in scale, it hopes to offset with agility and financial conservatism. It observes three cautionary tales on the same exchange:

• TPL Properties turned its 2013 Centrepoint tower into a bank head-office sale, then parlayed the proceeds into a 13 million sq ft REIT pipeline – but only after raising equity, partnering with IFC, and adopting LEED standards for premium rents.

• Dolmen City REIT enjoys near-full occupancy because it ring-fenced assets, instituted professional management and distributes 90 percent of rents as dividends.

• Pace (Pakistan) Ltd illustrates the cost of over-extension: fire damage, stalled malls and a June-2025 emergency asset sale to cut debt. The company’s objective is not to create Pakistan’s next mega-mall overnight but to compound stable, halal rental income – one plot at a time – and package that yield for institutional investors.

Karachi’s DHA sub-market remains undersupplied in new-build Class-B commercial inventory, and rents have risen in the past twelve months.

But execution will be everything. FDPL’s five-person staff must juggle land acquisition, contractor management, tenant onboarding and asset recycling while still chasing non-performing loan recoveries that fund the programme. Investors will want to see more detail on pipeline, funding sources and a clear dividend policy before according the stock a REIT-style valuation.

For now, though, a modest five-storey tower in Ayubia Commercial serves its purpose: it tells the market that First Dawood’s long-trailed reinvention is no longer theoretical. In bricks, mortar and a freshly painted façade, the company has literally raised its flag. The next 24 months will show whether those foundations are strong enough – and scalable enough – to support a genuine property franchise. n

What is happening to KP’s tobacco farmers?

Farmers in KP are alleging there is no transparency in the grading and procurement process of tobacco. The crop is highly important to the province’s agri-based economy

By Aziz Buneri

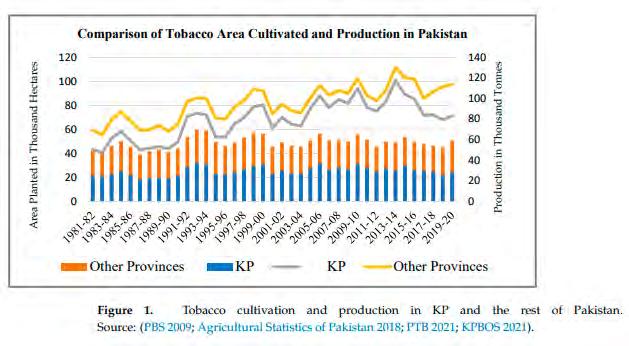

In Khyber Pakhtunkhwa’s four-district cluster of Charsada, Mardan, Swabi, and Charsadda, tobacco is a lifeline. The local economies in these districts are heavily dependent on tobacco farming.

In fact, most of the 50,000 hectares where tobacco is grown in Pakistan are concentrated in this little square of KP.

Tobacco is a massive industry in Pakistan. It is one of the rare crops in which Pakistan has a competitive advantage. Both the quality and yield of Pakistani tobacco is significantly better than the world average. A big portion of the tobacco procured by manufacturers in Pakistan comes from these four

districts. Large players like Pakistan Tobacco Company (PTC) and Phillip Morris as well as dozens of smaller local tobacco manufacturers depend on the health and productivity of the tobacco crop.

But all is not well in Pakistan’s tobacco belt. Last week marked a major escalation between the province’s tobacco growers and the buyers that provide their crop to tobacco companies. The farmers are concerned the tobacco supply chain has become beholden to middlemen who use grading (quality checks) and unfair pricing to keep the growers down.

Growers say the system benefits middlemen while pushing small-scale farmers into losses, particularly after a season of weather-related crop damage.

“The first and last leaves have lower quality and affect grading. Once the middle leaves enter the market, grading issues ease,”

Owais Afridi, representative of Pakistan Tobacco Board

Tobacco the crop

This is not the first time this publication has covered the tobacco industry. For the most part, Pakistan’s tobacco industry is easy to understand. This is mostly the case because there is one central conflict in the industry. The two big companies, PTC and PMI, hold most of the market share and pay most of the tax. However, they claim local competitors operate a cash based business and evade tax. In fact, the MNCs spend a lot of money advocating for stricter tax measures on the tobacco trade.

But this story is not really about them. It is not about cigarettes. This is about the farmers that produce the tobacco. Pakistan grows tobacco on nearly 50,000 hectares. Pakistan’s yield per hectare stands at nearly 2.3 tonnes per hectare with a total production of 113.6 million kilograms. In comparison, the world average production for tobacco is 1.84 tonnes per hectare. Meanwhile KP in 2021 produced 71.38 million kilograms on 28,089 hectares of land, giving an average yield of 2.5 tonnes per hectare — a 66% rise on the global average.

The tobacco plant is a great, big, leafy beast that can grow to surprising heights. From afar, it may even look like some kind of mutated crop of lettuce. After harvesting, however, it is taken to dry, crushed, and turned into the grainy brown substance that is rolled into cigarettes, lit, and smoked by millions of people everyday giving them a buzz in the short-run and chronic health problems in the long-run.

Since the year 2000, the production of tobacco in Pakistan has increased at a rate of 1.90% per annum mainly because of the improvement in per ha yield (at 1.64% per annum) as area under the crop expanded at 0.26% per annum. In KP, where 63% of total tobacco area lies, the growth in tobacco area during 2000-16 was highest at a rate of 0.63% per annum, while in Punjab which contributes about 32% of the total tobacco area, growth in tobacco area was on a declining trend. The tobacco area in Balochistan is also declining from a very small base, while in Sind it is increasing also from a very small base. The highest growth in tobacco production also came from KP at 2.03% followed by Punjab and Sindh.

Pakistan’s tobacco history

Tobacco’s trajectory in Pakistan has been quite impressive. In 1947, it was not grown anywhere in Pakistan. From 1948 onwards some efforts were made to try and grow the crop, beginning with an experimental 20 acre farm. It was very quickly discovered that KP’s land and climate was ideal for growing tobacco, and by 1968 Pakistan was no longer a net-importer of tobacco. However, at this point the quality of tobacco being grown was not good enough for production by major companies and was used mostly by smaller local cigarette companies.

In 1968, the Pakistani government took serious steps to support, improve, and develop the country’s tobacco industry by establishing the Pakistan Tobacco Board (Ali et al. 2015). The formation of the Pakistan Tobacco Board (PTB) was the first step towards promoting and developing tobacco production and export. Since the establishment of the PTB, the board has been protecting the rights of tobacco growers, buyers, manufacturers of tobacco products, and traders engaged in tobacco processing. The effects were far reaching.

A report of the planning commission from 2020 explains how during 2000-16, the production of tobacco in Pakistan has increased at a rate of 1.90% per annum mainly because of the improvement in per ha yield (at 1.64% per annum) as area under the crop expanded at 0.26% per annum. In KP, where 63% of total tobacco area lies, the growth in tobacco area during 2000-16 was highest at a rate of 0.63% per annum, while in Punjab which contributes about 32% of the total tobacco area, growth in tobacco area was on a declining trend. The tobacco area in Balochistan is also declining from a very small base, while in Sind it is increasing also from a very small base. The highest growth in tobacco production also came from KP at 2.03% followed by Punjab and Sindh. The highest growth in per ha tobacco yield was in Punjab.

According to a study by the Abdul Wali Khan University in Mardan, the area under tobacco cultivation in Pakistan was 43,134 hectares in 1980–1981 and 50,800 hectares in 2019–2020, indicating that the area under tobacco cultivation expanded over time due to its profitable nature. The same study found that tobacco production in KP increased from 43,408 tonnes in 1980–1981 to 71,410 tonnes in 2019–2020, while the area under cultivation only rose by around 4,000 hectares between that time. This means that while the area under cultivation grew by around 16%, the total production rose by a comparative 65%. This means that in this time a lot of attention was paid to improved production techniques in the province which resulted in the significantly higher yields.

The problems

Not all is well and good. While tobacco has been a big earner, in recent years it has been suffering. In fact the crop has seen particular troubles in KP. For the past few years, per hectare yield has actually been better in Punjab than in KP. In 2020, for example, a massive part of the tobacco crop in Swabi was decimated by unpredictable hailstorms. Swabi produces tobacco that sells in its raw form worth Rs 8.5 billion — a major injection into the small district’s economy.

Climate change is not the only challenge. The farm-profitability of tobacco is not as high as it should be given the yield numbers. This is because when farmers produce tobacco, they

“About 70,000 families in Swabi depend on tobacco farming. The law states that prices should rise annually. But without strong leadership, companies dictate rates”

Asad Qaiser, former Speaker of the National Assembly

do not process the leaves into the substance that is rolled into cigarettes themselves. Tobacco companies buy green leaves from the farmers and then process them into smokeable tobacco. These green leaves are purchased at a very low rate, and on top of that tobacco farming requires a lot of expensive inputs such as fertilisers, labour, mechanical power, pesticides etc which discourages existing farms from expanding and new farmers from planting the crop.

A 2020 study by the Planning Commission actually found that even though it was generally profitable, the margins in tobacco farming were so thin that “tobacco production is not very lucrative at the farm level.” The study also concluded that a price increase for green tobacco leaves would significantly increase the demand for farm inputs such as fertilisers, labour, mechanical power, pesticides, and farmyard manure. Tobacco production is negatively affected by the increasing input prices in the study area.” On top of this, there has been a regular demand among the tobacco farmers in KP to give tobacco ‘crop status’ which would protect it in many ways, and also give it a greater share of cess from the federal capital.

“About 70,000 families in Swabi depend on tobacco farming. The law states that prices should rise annually. But without strong leadership, companies dictate rates”

Asad Qaiser, former Speaker of the National Assembly

The current saga

So what is going on in KP’s tobacco districts to cause concern? Muhammad Ali Dagai, provincial organiser of the Kisan Jirga, said recent hailstorms and rain affected the quality of the tobacco crop, complicating grading. “As soon as the crop was ready, unexpected weather hit. That reduced output and triggered grading disputes,” he said. He added that the Pakistan Tobacco Board announced procurement prices and demand just two weeks before buying started—despite legal provisions requiring this to be done in October.

According to Muhammad Ali, some companies are relying on agents to purchase tobacco below official rates instead of fulfilling their declared quotas. He said this practice

“As soon as the crop was ready, unexpected weather hit. That reduced output and triggered grading disputes,”

Muhammad Ali Dagai, provincial organiser of the Kisan Jirga

leaves farmers without direct access to the market and at the mercy of intermediaries.

Growers also allege that companies delay payments beyond the one-month limit set by law. Dagai claimed that, despite repeated violations, no action has been taken. He further criticised what he described as a decades-long imbalance in favour of companies, stating that farmers were often unaware of how production forms were being filled on their behalf.

Tobacco remains one of Pakistan’s largest tax-contributing sectors, and growers argue that KP produces most of the crop. However, they say many manufacturing units operate outside the province, and local farmers struggle to meet company demands set elsewhere.

Farmer Sarir Khan said many producers are forced to sell through agents at prices lower than the government-mandated rates. “The cost of growing tobacco on one acre is around Rs 9.2 lakhs. Unless we get at least Rs 920 per kilogram, we’re in loss,” he said. The government has set the per-kilo rate at Rs 903 in Buner, Rs 952 in Mansehra, and Rs 743 in Mardan, Charsadda and Swabi.

The Pakistan Tobacco Board’s spokesperson, Owais Afridi, acknowledged that grading challenges occur early in the season due to the nature of the crop. “The first and last leaves have lower quality and affect grading. Once the middle leaves enter the market, grading issues ease,” he said. Afridi added that while this is one of the most profitable crops in agriculture, it also draws the most complaints. “Sugarcane and vegetable growers often work at a loss, but

they don’t raise as many concerns.”

Responding to the allegations, Imad Ud Din, Head of Leaf at Pakistan Tobacco Company, said the company strictly adheres to the grade standards set by the Pakistan Tobacco Board. “PTB officials are making unannounced visits to our buying stations to ensure that purchases comply with the Marketing Rules,” he said. He added that PTB had issued advisories via digital and print media to educate farmers about proper grading and avoiding the mixing of damaged or non-tobacco materials.

“We remain focused on high-quality production and long-term sustainability of the crop, which ultimately benefits farmers,” he said. “We are purchasing tobacco from our agreement-holder farmers strictly in line with grade specification”,and provide proper communication and valid reasons for any rejections.”

Company sources, when contacted separately, attributed some of the unrest to political interference. “Each year this issue arises, partly due to political figures who push farmers to protest. Some agents have links to these individuals and use protests to pressure companies,” one source said.

Former National Assembly speaker Asad Qaiser said about 70,000 families in Swabi depend on tobacco farming. He criticised the delay in setting prices and the absence of a director at the tobacco board, calling it a governance gap. “According to the law, prices should rise annually. But without strong leadership, companies dictate rates,” he said.

This year, the board fixed the quota for KP at 74.8 million kilograms. Despite weather damage, production is expected to reach 95 million kilograms—down from initial projections of 125 million. Farmers say companies already hold large stocks from previous years, reducing their buying this season.

While both growers and companies continue to present conflicting positions, calls are growing for stronger regulatory oversight to ensure that pricing, procurement, and payment systems remain transparent, timely, and within legal frameworks. n

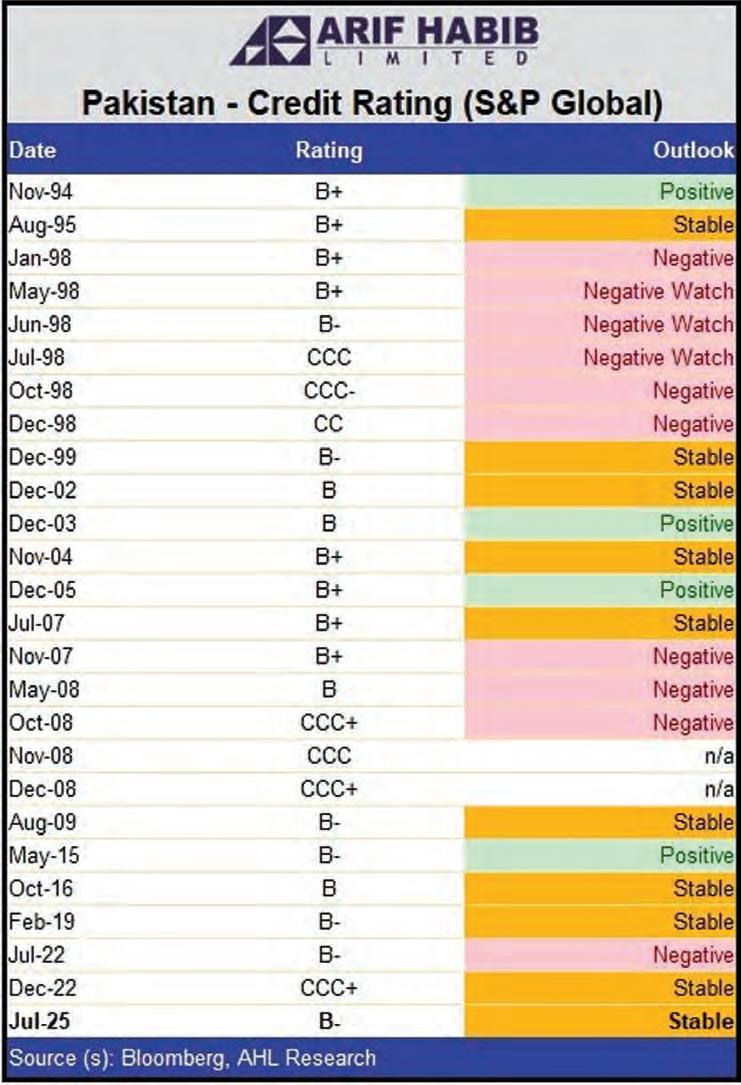

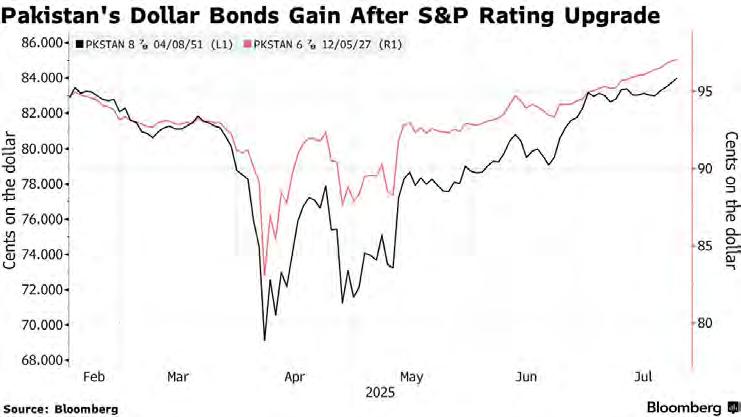

Rating agencies back Pakistan’s recovery story ahead of international debt push

Following Fitch, S&P upgrades Pakistan’s rating as the country prepares for global bond market return

By Ahtasam Ahmad

Three years ago, Pakistan teetered on the edge of economic collapse. Credit rating agencies delivered a devastating verdict, with S&P downgrading the country to ‘CCC+’ in December 2022 as foreign reserves crashed to a multiyear low of just $6.7 billion. The message from global markets was clear: Pakistan had become uninvestable.

The eurobond market laid bare the severity of the crisis. Pakistan’s dollar bond was trading at fire-sale prices as investors scrambled to exit what many had written off as certain default territory. The country appeared destined to join the growing list of emerging market casualties: Sri Lanka, Ghana, and Zambia.

The crisis was years in the making, but 2022 delivered the perfect storm. Russia’s invasion of Ukraine sent oil prices soaring past $130 per barrel, devastating floods submerged one-third of the country, and the dramatic ousting of Prime Minister Imran Khan in April 2022 plunged domestic politics into chaos. The rupee collapsed, inflation exploded to nearly 30%, and the government’s financing options evaporated as foreign reserves dwindled to cover barely one month of imports.

Yet Pakistan’s story has taken a remarkable turn. The economy that seemed beyond salvation is not only surviving but showing genuine signs of recovery. The panic that gripped markets in 2022 has given way to cautious optimism and this shift is being validated by the very rating agencies that once wrote Pakistan off.

Following Fitch’s upgrade earlier this year, Standard & Poor’s has now followed suit, upgrading Pakistan’s sovereign credit rating and citing “improved economic fundamentals and reduced near-term default risks.” The transformation couldn’t be more stark: foreign reserves have more than tripled to $20.5 billion, Pakistan achieved its first current account surplus in 14 years, and inflation has plummeted from a peak of 29% to just 4.5%.

“The ratings upgrade reflects our view that Pakistan is now less reliant upon favorable macroeconomic and financial developments to meet its obligations,” S&P stated, acknowledging what many thought impossible just two years ago.

But as Pakistan eyes a return to international capital markets for the first time since the crisis, questions remain: Is this recovery sustainable, or are we witnessing a temporary reprieve? Profit examines the forces behind Pakistan’s remarkable turnaround and the

challenges that still lie ahead.

From crisis to recovery

The rating upgrade marks a significant turnaround from Pakistan’s precarious position in late 2022, when S&P downgraded the country to ‘CCC+’ as foreign reserves plummeted to critical levels. “At the time of our downgrade of Pakistan to ‘CCC+’ in December 2022, foreign reserves had plummeted to a multi-year low of US$6.7 billion,” the rating agency noted.

The contrast with today’s situation could not be starker. As of July 4, 2025, Pakistan’s foreign reserves have surged to $20.5 billion, including the central bank’s gold holdings. This represents more than a three-fold increase and provides substantial coverage for the government’s immediate obligations. S&P confirmed that these reserves are “sufficient to cover the government’s external principal and interest payments of US$13.4 billion for fiscal 2026.”

The transformation has been so significant that the agency observed: “Pakistan has replenished its foreign reserves over the last 12 months and near-term default risks have abated.”

IMF program delivers results

The cornerstone of Pakistan’s economic recovery has been the successful implementation of the IMF’s Extended Fund Facility (EFF), which S&P described as “instrumental in restoring much needed macroeconomic stability to the country.” The $7 billion program, approved in September 2024 over 37 months, represents a continuation and extension of the previous $3 billion Stand-By Arrangement that Pakistan successfully completed in April 2024.

The program’s comprehensive nature extends beyond simple financial assistance. “The EFF and RSF run concurrently over 37 months and give the country a total package of $8.4 billion,” S&P noted, referring to the additional $1.4 billion Resilience and Sustainability Facility that runs alongside the main program. The agency emphasized that “these disbursements, in combination with new and rollover of deposits from bilateral partners, have helped to rebuild Pakistan’s foreign exchange reserves from critical lows.”

The program’s impact on government finances has been particularly impressive. “The IMF program-related reforms have significantly increased the government’s tax revenues by as much as 3% of GDP in the last 12 months,” S&P reported. This revenue boost included innovative measures such as the Agriculture Income Tax and expanding the tax net to include more retail sector participants, described as “widening of the tax net to bring in more registrants in the retail sector.”

The results speak for themselves: “General government revenue to GDP reached 15.7% in fiscal 2025, an all-time high, from 12.6% the year before.” Combined with expenditure controls, these improvements have enabled Pakistan to substantially reduce its fiscal deficit. “Alongside expenditure controls, we forecast general government deficit to decrease to 5.1% of GDP in fiscal 2026 from 7.9% in fiscal 2022,” S&P projected.

Progress tracking has been encouraging, with “the IMF completed the first review of Pakistan’s EFF-tied economic reform program in May 2025.” This successful review “facilitated a disbursement of $1 billion, bringing total disbursement to date to $2.1 billion,” demonstrating that Pakistan is meeting its program commitments.

Historic external balance achievement

Perhaps the most remarkable turnaround has been in Pakistan’s external accounts. For the first time in over a decade, the country achieved a

current account surplus. “Pakistan’s current account posted a surplus in fiscal 2025, the first time in 14 years,” S&P noted, describing this as a historic milestone.

The surplus, though modest at 0.5% of GDP, was driven by exceptional remittance flows. “The small annual surplus of 0.5% of GDP was driven by record-high remittances totaling $39 billion (9.5% of GDP) over the period,” the rating report explained. This represents a dramatic shift from the troubling deficits of recent years, particularly “the high shortfall of 4.7% of GDP in fiscal 2022.”

The agency emphasized the broader significance of this achievement: “In all, these

developments have strengthened Pakistan’s external metrics and alleviated near-term external stress.”

International support has been crucial to this turnaround. S&P highlighted that “the IMF program, along with strong support from bilateral partners, has boosted foreign reserves considerably.” The backing from key allies has been substantial, with “support from bilateral creditors, including China, Saudi Arabia, United Arab Emirates, and Kuwait” proving “critical to Pakistan to meet its high external financing needs.”

The scale of this support is remarkable: “The total support from these four partners in

the form of central bank deposits and swaps reached US$16.8 billion as of end-fiscal 2025.” However, S&P noted that “we add this sum to the government’s total stock of debt,” acknowledging that this support comes with future obligations.

Beyond bilateral support, multilateral institutions have also re-engaged with Pakistan. “The progress of the IMF program had drawn in other multilateral and bilateral financiers to resume their aid to Pakistan,” S&P observed. Notably, “in January 2025, the World Bank approved a 10-year Country Partnership Framework with Pakistan, committing $20 billion in funding,” representing a massive vote of confidence in the country’s reform trajectory.

Inflation conquered, monetary policy normalized

Pakistan’s success in taming inflation represents one of the most impressive aspects of its economic stabilization. The country has emerged from a period of devastating price pressures that threatened economic stability. “With inflation having subsided from a peak of 29% in fiscal 2023, we envisage Consumer Price Index (CPI) growth to average 6.5% over the next two to three years,” S&P forecasted.

The magnitude of this achievement becomes clear when considering recent performance: “CPI growth came in at 4.5% for fiscal 2025, substantially lower than the 23.4% in the previous fiscal year.” This dramatic moderation has enabled the State Bank of Pakistan to reverse its aggressive tightening cycle.

“The State Bank of Pakistan (SBP) undertook aggressive monetary policy tightening to tame surging inflation of over 20% annually during fiscal years 2023 and 2024,” S&P noted. However, “with inflationary expectations better anchored, the SBP has reduced the policy rate by 1,100 basis points since June 2024 to the current 11%.”

This monetary easing is already yielding fiscal benefits. “As a result, monetary conditions will further ease and with lower domestic interest rates, the government’s interest payments will decrease to average 41% of revenue over the next three years from a peak of above 60% in fiscal 2024,” S&P explained.

The government has strategically used this improved interest rate environment to manage its debt profile. “Consequently, the government, which had eschewed long-term debt issuance during the period of high rates, started to reprofile its debt stock from shortterm paper to longer dated bonds,” S&P noted, highlighting improved debt management practices.

Debt dynamics and fiscal sustainability

While fiscal metrics have improved substantially, Pakistan continues to grapple with elevated debt levels and servicing costs. S&P projects that “Pakistan’s average annual change in net general government debt will average 5.1% of GDP from fiscal 2025 through to fiscal 2028,” indicating that “Pakistan’s net debt stock is likely to remain fairly high at over 60% of GDP.”

The agency identified the core challenge: “But the main pressure on debt sustainability is the extremely high interest expense relative to fiscal revenue. This is a major constraint on our assessment of the government’s debt burden.” However, there are signs of improvement, as “we anticipate lower funding costs and a stable rupee to gradually bring down this ratio to 45.8% in the current fiscal year from 49% the prior year.”

The historical context of Pakistan’s debt burden is important to understand. “The government’s hefty interest burden arose from historically high domestic interest rates,” S&P explained, directly linking current fiscal pressures to past monetary policy decisions necessitated by inflation control.

Persistent challenges and constraints

Despite these remarkable improvements, the rating agency emphasized that significant challenges remain. The debt servicing burden, while improving, continues to constrain the government’s fiscal flexibility. “Nevertheless, Pakistan’s interest servicing-to-revenue ratio remains one of the highest globally among rated sovereigns,” the agency cautioned.

Political stability remains a critical factor for continued progress. “Pakistani politics has

been in a state of flux since the ouster of former Prime Minister Imran Khan of the Pakistan Tehreek-e-Insaf party in a parliamentary no-confidence motion in April 2022,” S&P noted. The agency emphasized that “the political turmoil hampered the government’s efforts to deal with economic challenges previously, damaging the sovereign credit metrics” and stressed that “we believe a stable political environment in Pakistan is an important precondition to further improvements in the government’s creditworthiness.”

Security concerns also persist as a rating constraint. “The ratings on Pakistan remain constrained by elevated domestic and external security risks,” S&P stated. While acknowledging that “the country’s security situation has improved since the early 2010s,” the agency warned that “the potential to deteriorate remains.”

Looking ahead

Pakistan’s economic recovery demonstrates the effectiveness of reforms when implemented consistently and with the right intent. The country has successfully navigated from the brink of default to a more stable footing, with rebuilt foreign reserves and improved fiscal metrics. However, sustained progress will require continued commitment to reforms, particularly in expanding the tax base and maintaining expenditure discipline. Pakistan’s ability to manage upcoming external debt maturities while maintaining reserve levels will be crucial, likely necessitating continued reliance on bilateral support and successful completion of the IMF program.

The rating upgrade reflects genuine progress, but Pakistan’s journey toward investment grade status will depend on maintaining reform momentum while navigating ongoing political and security challenges. For now, the country has bought itself valuable time to build on these early successes and establish a more sustainable economic trajectory. n

OPINION

Maha Shah

Crypto exchanges need to earn Pakistan’s trust with on‑chain protection

Pakistan’s newly minted Virtual Assets Ordinance has sparked headlines, but retail confidence will not be won in parliament. With over 25 million users and a consistent ranking among the top 10 countries for grassroots crypto adoption, Pakistan holds a strong position to become a major force in the global digital economy.

Yet, after losing an estimated $100 million to a nationwide Ponzi scheme, local investors have become allergic to invisible guarantees. As Pakistan builds its regulatory future, it must demand a higher standard from the industry. Accepting fuzzy assurances of security is no longer viable; the future of Pakistan’s digital-asset boom must be built on verifiable Proof of Protection.

The limits of today’s trust model

For years, the primary trust signal has been Proof of Reserves. Through Merkle-tree tools, exchanges prove they hold user assets on a 1:1 basis. However, PoR only answers “Are my coins there?” but not “Will they survive a breach?” It proves existence, not resilience.

Maha Shah is a finance and crypto journalist who has worked at Bloomberg and Forkast News. She covers the fast-moving intersection of digital assets and global finance, focusing on blockchain innovation, market trends, and the forces shaping the digital economy

A platform can show full reserves one moment and lose them to an exploit the next — with users left holding nothing but an old snapshot.

Exchanges that stop at solvency audits are betting that legislation will force competitors to do the same. Market discipline moves faster: in a country processing more than $30 billion in annual remittances and hosting an estimated tens of millions of crypto users, money will flow toward venues that show — in real time — how user safety is funded and insulated from discretionary delays.

Building compensation into code

The new standard should be a transparent framework that undergoes third-party security audits and clearly shows how user safety is funded, governed, and delivered. Rather than relying solely on a simple balance sheet check, this Proof of Protection should demand a comprehensive audit of a platform's entire security posture.

Traditional insurance relies on actuarial tables, claims adjusters, and weeks of paperwork. Web3 can collapse that stack into deterministic logic. A smart contract can watch a platform’s hot-wallet address, and if an exploit drains more than, say, 0.5 % of user assets, it automatically releases matching funds from a well-capitalized cold-wallet reserve.

This verifiable compensation fund should be the cornerstone of the Proof of Protection model. Many platforms claim to have “insurance” or “protection funds” to reimburse users in case of a catastrophic loss. But these are often little more than press releases. If the logic, liquidity, and governance of these funds are hidden, they offer no real assurance.

A safety net that cannot be inspected is just another empty promise.

Under a PoP model, any platform claiming to have a user protection fund must make it as transparent and auditable as its reserves. This means publishing the on-chain wallet addresses of the fund for all to see. Users, regulators, and third-party analysts should be able to verify its balance in real time. Anything less should be dismissed as legacy thinking in decentralized clothes.

Multi-signature schemes distribute control so no single insider can divert that pool, while public block explorers let anyone audit balances and payouts block by block. The result is coverage that behaves like open-source software: open to inspection, impossible to fudge.

The architecture behind the user security

True Proof of Protection goes further than a simple compensation fund. It is an entire security philosophy built on layers of verifiable safeguards. The platforms that win the next era of trust will treat user safety as a core product feature, not a legal contingency — and they will be able to prove it. For example, MEXC’s Proof of Trust initiative pairs a publicly verifiable $100 mil‑ lion Guardian Fund with third‑party auditing to demonstrate how protection can be made transparent by default.

The process begins with a non negotia ble technical foundation. The vast majority of user assets must be held in offline cold wallets, physically isolated from online threats. The movement of any funds should require multi‑signature authorization from several keyholders, making theft by a single bad actor — internal or external — nearly impossible. These are not optional extras; they are the bedrock of security standards demanded by custodial banks and licensed exchanges.

Building on that foundation, a modern platform must operate an intelligent immune system. Advanced AI‑powered systems should monitor for threats 24/7, detecting abnormal logins, suspicious transaction patterns, or signs of market manipulation. This allows

threats to be contained before they can cause cascading damage.

User‑side education matters, too. Urdu language guides on two factor authen tication, phishing defense, and wallet hygiene give investors the knowledge to partner with platform safeguards, closing the final gap human error can open.

The economic power of provable trust

The economic case for provable secu‑ rity is overwhelming. Global capital is famously cautious; it flows away from ambiguity and toward certain ty. When platforms can verifiably prove how they protect user assets, they de‑risk the entire ecosystem. This crucial step helps transform digital assets from a high stakes speculative bet into a viable class for institutional portfo‑ lios, attracting the venture funding needed to build sustainable companies.

This creates a powerful network effect that extends beyond trading. A trusted ecosys tem becomes a magnet not just for exchanges, but for the entire Web3 supply chain — the “picks and shovels” of the digital gold rush. This includes on-chain analytics firms, digital identity startups, specialized cybersecurity providers, and compliance tech companies. The resulting industrial base is deep and resilient, establishing innovation from the ground up.

For a nation with a youthful and

tech savvy population like Pakistan, this is the most direct path to creating thousands of high‑value jobs that remain relevant even as technology evolves. A verifiable security stan dard does more than protect traders; it builds the bedrock for a new digital economy.

Pakistan’s investors will vote with wallets

The Virtual Assets Ordinance is valid for 120 days unless parliament renews it. Legislation can lapse, but market discipline is immediate. If even one major exchange exposes a live protec‑ tion fund address and code controlled payout logic, every rival will be forced to follow or watch liquidity migrate overnight.