08 08 The cotton tale 12 The return of the auto-loan 19defaults?Adarkwinter Ammar H. Khan 20 20 Going the Thar route 26 Asking the wrong questions Uzair Younas 27 For the love of all that is good, leave Miftah alone! Ariba Shahid 28 28 OLX Group-backed CarFirst has shut down in Pakistan. Here’s why 31 Running out of options: The state of our telcos 12 31 20 CON TENTS Publishing Editor: Babar Nizami - Editor: Khurram Husain - Joint Editor: Yousaf Nizami Assistant Editors: Abdullah Niazi I Sabina Qazi - Sub-Editors: Mariam Zermina | Basit Munawar Editor Multimedia: Umar Aziz - Video Editors: Talha Farooqi I Fawad Shakeel Reporters: Ariba Shahid I Taimoor Hassan l Shahab Omer l Ghulam Abbass l Ahmad Ahmadani Shehzad Paracha l Aziz Buneri | Maliha Abidi | Daniyal Ahmad | Ahtasam Ahmad | Asad Kamran Chief of Staff: Maliha Abidi - Regional Heads of Marketing: Mudassir Alam (Khi) | Zufiqar Butt (Lhe) | Malik Israr (Isb) Business, Economic & Financial news by 'Pakistan Today' Contact: profit@pakistantoday.com.pk Profit

Setting perimeterswhat happened until 2020? The cotton crop has a certain status in Pakistan. It is not only a plant that is native to Pakistan, but it has had a storied history and has historically

8

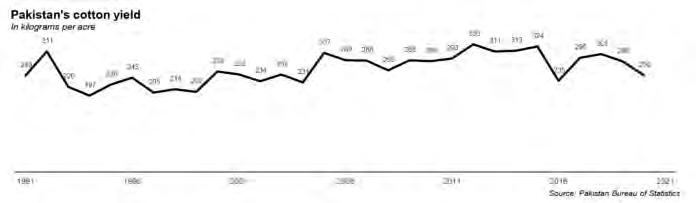

According to the Pakistan Cotton Ginners As sociation, figures from November 2021 showed that cotton outputs had increased by as much as 70%. In the first quarter of 2022, a sudden rise in demand and prices in the world market meant more farmers were growing cotton — and yield per hectare was increasing as well.

The improvement in the fate of the cotton crop has been noticed. The unfortunate part is that it has come on the back of an anomaly of international trade created by the Covid-19 pandemic. The government has done very little to improve the status of the cotton crop. Farmers, too, have been slow in adopting better farming practices that will produce more cotton per hectare. What this slight upward trend from this year does tell us, however, is that the cotton crop has a chance in Pakistan, one that can be seized. Buzt6 is anyone up to the task?

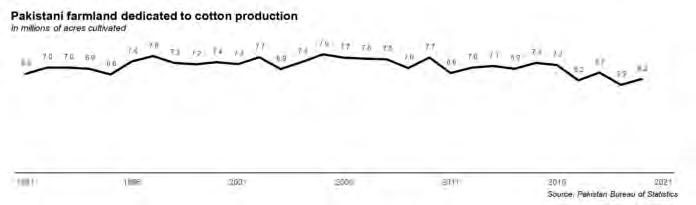

By Abdullah Niazi In October 2019, Pakistan’s cotton crop was on the ropes. The story was not a new one. Since at least 2015, cotton yield in the country has seen a downward trend. Between 2015 and 2020, Pakistan’s produc tion of cotton declined by nearly 35%, from nearly 14 million bales in 2015 to just over 9 million bales in 2020. Farmers over the past decade have aban doned cotton in favour of more profitable crops like sugarcane, and changing climatic condi tions have made the cotton seed in Pakistan less resistant and more likely to fail — which means growing it has become a bad business decision for a number of agriculturalists. This has posed problems. The cotton supply chain is a long and complicated one. It begins very simply from the cotton fields where the cotton plant is grown, harvested, picked, and taken to the large ginning facilities that exist in the country. Here it is ginned and converted into a form that can be used to man ufacture clothing and other cotton products. This is where the secondary market comes into play. In the secondary sector, the cotton-based textile industries have a 21% share in large-scale manufacturing and consequently a 2% share in the national GDP. In the past, these textile manufacturers would depend on local cotton to bolster their production and make their products cheaper. Over time, the textile industry has started re lying more and more on expensive imported cotton to meet their needs. For a while now it has been on the cards that Pakistani cotton might be on a very steady route to decline. That is, until, a bit of news this year gave hope to both the textile industry and cotton farmers that there may still be a chance for Pakistan’s cotton crop. In March 2022, it became apparent that the cotton crop in Pakistan had made gains.

The government of Pakistan is not a direct participant in the cotton supply chain at all, and implements no policies designed to benefit cotton farmers or the cultivation of cotton more broadly, and yet somehow, the bureaucrats in Islamabad think that setting a target is enough for them to help the country achieve higher production numbers. And the targets themselves are absurd: Over the past 30 years, only twice has Pakistan’s cotton production crossed 14 million bales, and yet somehow the government sets the target of 15 million bales of cotton the year after the country barely managed to scrape by with producing 9 million bales. Missing those targets is not the prob lem. No. The targets defy all reason and are not meant to be reached in the first place as it would be impossible. Even though Pakistan has low yields, the real surprise has been the fact that output this year is somewhat better, despite higher than usual rainfalls, gusty winds in certain regions, and pest attacks on standing crops.

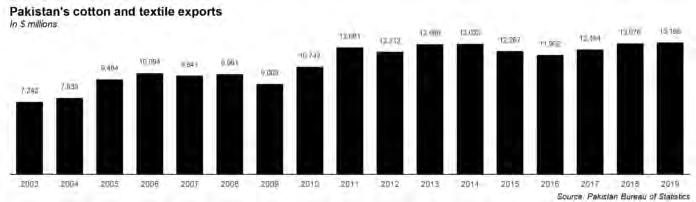

AGRICULTURE been a pillar for the textile industry of the country, which is one of the largest export orientedAccordingsectors. to a 2021 report of the International Food Policy Research Institute (IFPRI), raw cotton consumption grew at an annual growth rate of 7% between 1982 and 2008 to reach 15.6 million bales in 2007-08 in Pakistan. However, between 2007-8 Pakistan was hit by the global recession. The textile industry faced challenges due to high energy costs, rupee depreciation vis-à-vis the US $ and other currencies, and a high cost of doing business. As a result, there was a reduction in the number of textile mills operating in the country from about 450 units in 2009 to 400 units in 2019. This decrease has simultaneously seen the domestic demand for cotton dip in the country.Farmers and the textile industry up until the 2008 financial crisis had been dependent on each other. Farmers would produce the crop without the fear that demand would fall, and the government did not need to announce a support price either. But when mills started shutting down, suddenly there was more cotton and not enough buyers. After a harsh couple of years, farmers also began going back on cotton and its price fell, resulting in produc tion decreasing.Asaresult, exports were also affected. At the same time, since farmers were losing interest in cotton, very little cotton research was done in the country. This meant that other cot ton producing countries were able to use the latest seed technology and science to increase their yield while Pakistan fell behind. Here is a sobering statistic. Two decades ago, Pakistan’s cotton was in demand globally. However over those 20 years, countries such as Bangladesh, Vietnam and Cambodia have all used better growing techniques to get ahead of Pakistan. In 2003, when Pakistan’s textile exports were $8.3 billion, Vietnam’s textile exports were $3.87 billion, Bangladesh’s were at $5.5 billion. Now Vietnam is at $36.68 billion and Bangladesh is at $40.96 billion, while Pakistan is struggling to hit $25.3 billion in 2020. The explanations behind this are multiple. Pakistan needs to increase not just the amount of cotton it produces, but also improve the quality of the cotton crop. Currently, Pakistani cotton is considered second grade, and if the crop quality is improved there would be greater demand at a greater price. More im portantly, by improving the crop, the entire textile industry will benefit since the quality of all products will improve at Pakistansource.has been missing its export targets since last year. In 2019, the production target for cotton had been 15 million cotton bales, and only 10.2 million bales were produced. Bad weather at the end of the year meant that there were only 8 million bales at the end. The rea son behind this, again, is that the government places very little emphasis on how the cotton is grown. Factors like climate change, lack of proper research by local research institutes, and no cotton policy, and the loss of cotton production areas to other cash crops have all played a role in this, which is why it is so important to focus on techniques to grow more and better quality cotton. About those targets

Why was cotton ‘in’ this year? These problems in Pakistan’s cotton industry have been persistent for more than a decade now. We have discussed poor seeds, poor planning, bad target setting, and better crop options for farmers. This year, however, something hap pened that made cotton popular again — the impacts of Covid19 trickling through. You see, cotton has been on the decline since 2008, as we have seen. As mentioned earlier in the story, between 2015 and 2020, Pakistan’s production of cotton declined. This led to the textile industry claiming that they would thrive on imported cotton instead of depending on local cotton. This worked out especially since the cotton Pakistan produced was second grade. But when the pandemic hit, everything changed and the local industry found that importing cotton was no longer an option. International cotton prices (in rupee terms) during the last year have gone up by almost 30% — from PKR 12,606 on July 1, 2021, to PKR 18,259 by mid-February this year. The

There is, of course, an issue with these targets themselves. Of all the bad habits the government of Pakistan has, perhaps, one of the worst is the one picked up by the Ayub Administration in 1958 from the Soviet Union of building a government that assumes that it operates in a planned economy, even as it presides over at least a semi-open market economy. The habit is of introducing ‘targets’ for the economy. Every year, the government of Pakistan has announced an absurdly high cotton production ‘target’. This year, same as always, it will be seen to ‘miss’ its target, as the government of Pakistan does not own any cotton farms, most of the banks do not lend to farmers anyway, and there are no companies that supply farmers with what they need.

Since the impact of Covid was compara tively milder on Pakistan, its industry started almost eight months ahead of the rest of the world and so the entire capacity was booked within weeks. This sent the industry in a mad chase for cotton, hence improving local prices, explains Arshad. A big part, simultaneously, was that just a year before, Pakistan had started to focus on improved cotton production methods. This is what allowed it to cover the gap for the indus try when importing cotton was no longer fea sible, the Dawn report adds. “In 2021, acreage fell by 17% in Punjab — from 3.8 million acres in 2020 to 3.1m last year — but production fell by onlyThis2%.”means that average yield increased over time. The report quotes Dr Saghir Ahmad, director of the Central Cotton Research In stitute (Multan), as saying, “the average yield jumped from 15.68 maunds in 2020 to 19.62 maunds per acre in Punjab in 2021. In Sindh, it was even better; 30 maunds per acre, pushing the national average to 25 maunds per acre. This better production, along with a massive rise in world prices, has now set the stage for acreage expansion this year.”

ever-dwindling value of the rupee not only doubled the impact of import for Pakistani millers but also made it next to impossible to calculate the final cost of produc tion, rendering import commercially non-feasible for theOnindustry.topofthis, there were shipping concerns. A report in Dawn from March 2022 chronicled how it takes more than 120 days to ship cotton to Pakistan these days, against the 30-day hiatus in pre-Covid times. These circumstances deflated the textile industry’s claim that it could thrive, even survive, on imported cotton and forced it to value local crops, thus setting the stage for the cotton revival in the country. “‘In the first year-and-a-half (of Covid), all major world brands had their stocks exhausted as cotton supplies got squeezed quickly but demand died slowly — stripping the brands naked of their product,’ Kamran Arshad, owner of the Ghazi Fabrics, explains the demand side. With different governments incentivising their industry and compensating their people, the demand for textile products started coming back but, by that time, shipping lines had stopped and industry was closed. As the world textile industry started reviving, demand became too overwhelming for it to meet.”

10 AGRICULTURE

What does it mean The textile industry has stayed largely unimpressed with this. They have chalked the increase up to special circumstances, and are still relying on imports. According to them, local cotton does have the potential to cover local demand but unless solid steps are taken there will be no point to it. “This has not been a remarkable increase,” says Raza Baqir, the secretary gener al of the All Pakistan Textile Mills Association (APTMA). “There has been a marked increase in per hectare yield in some areas which is very en couraging, however, in some areas decreasing yields have also been observed, and overall the scale has barely been budged. We still need to import nearly half of our quantity from abroad, which with rising prices is difficult. We have observed a consistent improvement since at least 2019, but overall it has to be said it was all very marginal.”Thekeyhere is the minor improvement that has been seen over the past three years. Before this, for nearly a decade, Pakistan’s cotton crop suffered from multiple ailments. The narrow genetic base of cotton germplasm which are prone to insect and disease, along with reliance of Pakistan on a back-crossed 17 year old biotechnology have resulted in low yield per area. Lack of quality and advanced gene technology is a serious issue that has plagued cotton productivity in Pakistan. The attack of pests such as the locust attacks in the past couple of years and other consequences of climate change have all caused issues. This year, however, a peculiarity of the international supply chain made a case for Pakistani cottons. Just as the problems of this crop have been listed, its solutions are also readily available. Investment is required in cotton research. More importantly, this year the price of cotton was well above the support price of PKR 5000 per bale (40KG) but the early announcement of this support price gave farmers the confidence to pursue this crop. With all of these Pakistanconsiderations,canonceagain go back to its cotton glory days, and perhaps bolster its textile industry and exports along the way. n

12

BANKING With Kibor, inflation, interest rates and auto loans at historic highs, should borrowers and banks be worried?

for vehicles which will not go,” says Pervez Shahid, former co-chairman of Bank Alfalah’s central management committee, a seasoned banking professional who was the boss at Bank Alfalah during the 2008 financial crisis and auto-loan default. The problem is that the price of both cars and houses have seen an exponential rise in the past few years. As Pervez Shahid has explained, this has not killed the demand. It has only led to customers leveraging auto financing to bridge the gap between them and their desired vehicle. The problem is, with a global recession in full swing, people’s purchasing ability to buy luxury items like cars deteriorates. And if you are someone that had taken out a car loan back in December, the rising prices will by now be coming back to haunt you. But how does it work, and what are the signs? The anatomy of default “If you are early in your lease, that could effectively mean your monthly payment has increased significant ly. At the same time the price of everything (including fuel and maintenancewhich effectively increases your cost of vehicle ownership) has gone through the roof. Monthly budgets have gone completely out of whack. Some time in the next 6 months this will catch up and people will start defaulting on their car loans.” said Azam Khan, an investment profes sional, speaking to Profit. Khan’s comments are scary but they encapsulate what loan defaults on the auto market look like. People that get their vehicles financed are weighed down by a recession and general inflation, and when their monthly payments increase they find themselves unable to pay. As we’ve mentioned earlier, people in Pakistan will pay their car instalments because

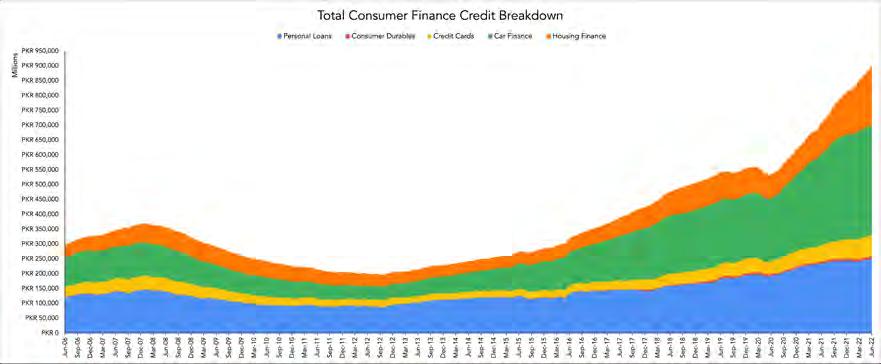

What’s the size of the pie? Over the course of the past 18 months, from January 2021 to June 2022, Rs 111 billion auto-loans have been dispersed by all banks for auto loans. In comparison, total consumer finance loans taken for housing in the same time period amounted to Rs 281 billion. On average, 40per cent of all personal finance loans in the past year and a half were auto loans. In short, the market is massive. As the graph of the SBP’s total credit in circulation data below shows, a majority of current loans in circulation are for cars. There are a lot of reasons for this. A house of one’s own and a car at the end of a salaried career is the height of most upper-middle class aspirations. In addi tion to this, in what is a peculiarity of our auto market, cars are considered both an asset class and a necessity in Pakistan. Since it is both a necessary means of transport in a country with no walkable cities or viable public transport, as well as a hedge against inflation, people will take out loans to get cars over anything else. “You need electricity, right? No matter how expensive it gets you will pay for it because you need it. In the same way, no matter what the cost is, there is a general demand

By Daniyal Ahmad

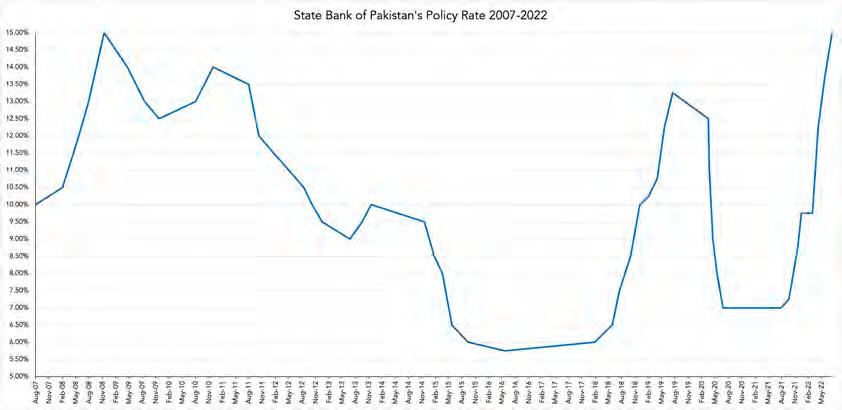

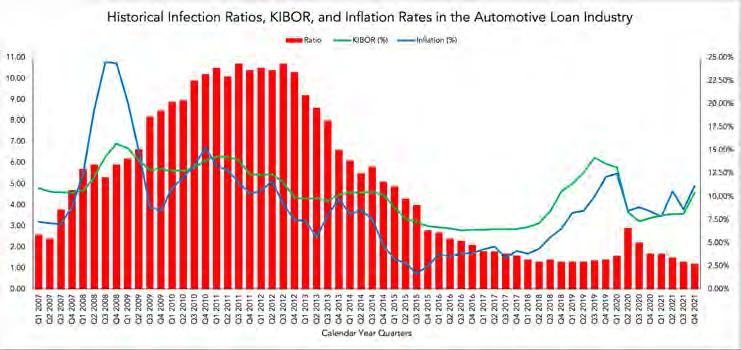

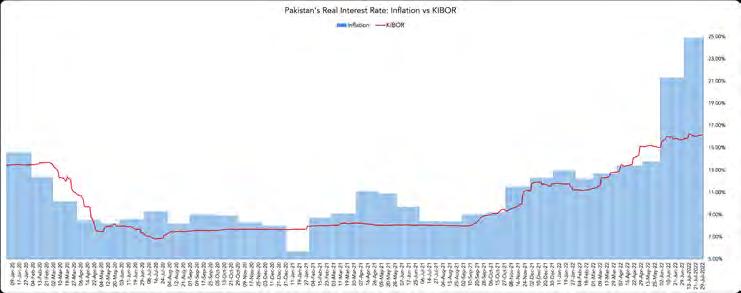

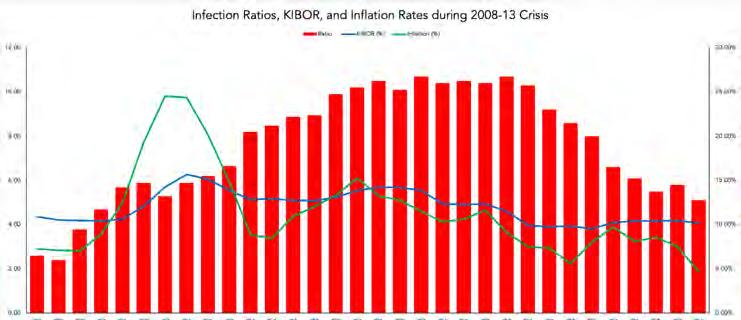

The State Bank of Pakistan’s (SBP) policy rate has hit 15%. This is a decade after it last did so in 2008, and this time it hap pened almost instantly.There will indeed be a shock for the economy like no other. There are now murmur ings in the banking industry, and all of them point towards the same thing — sometime in the next six months the auto-loans market will receive a stress test. How will this play out? Because of rising inflation, and the spiking cost of borrowing money after the massive increases in the policy rate over the past one year, people that have had their cars financed by banks will suddenly find that their monthly payments have skyrocketed. How much, you ask? Profit calculates that customers with auto loans taken in 2021 on 5 year tenors could see a 30-35% increase in their monthly payments going forward. General inflation has already led people to tighten their purse-strings, leading to low purchasing power. On top of this, when the banks come knocking with massive auto-loan bills, people will have difficulty repaying the loans, raising the spectre of rising defaults in consumer loans. If this happens, it will not be the first time Pakistan’s auto-loans market has seen large scale defaults. The last time the auto loans were swept by a wave of defaults was in the aftermath of the financial crisis of 2008. Back then, according to a 2011 report of the State Bank of Pakistan (SBP), nearly 50% of all personal finance loans defaulted. The reason behind the default was pretty standard. There was an economic crisis led by inflation, interest rates were hiked rapidly to reach an all time high, the country was roiled by political turmoil, and fuel prices were high after being artificially deflated earlier. Interest rates have shot up in the past one year at a virtually un precedented rate. From 7 percent last July, the key Policy Rate shot up to 15pc by July 2022. There have been two other episodes of sharply rising rates in the recent past. In 2018, for example, the poli cy rate shot up from 6pc to 13.25pc in a matter of 18 months, sharply slowing the economy and leading to a rising “infection ratio” in the banks as the cost of borrowed funds spiked with this rise. Sound familiar? Yes, the set of circumstances that led to nearly half of all personal finance related loans defaulting in 2008 are eerily similar to the circumstances in the country right now. Profit spoke to bankers and investment professionals to determine whether the auto-loans market is once again headed to wards a similar situation. Opinions were split. Some said it could happen within six months. Others said that while the circumstances were similar to 2008, market dynamics have changed since then, with banks becoming more prudent about who they lend to, which means defaults will happen but minimally. Profit investigates the state of the auto-loan market, to assess the likelihood of this happening all over again.

14

-

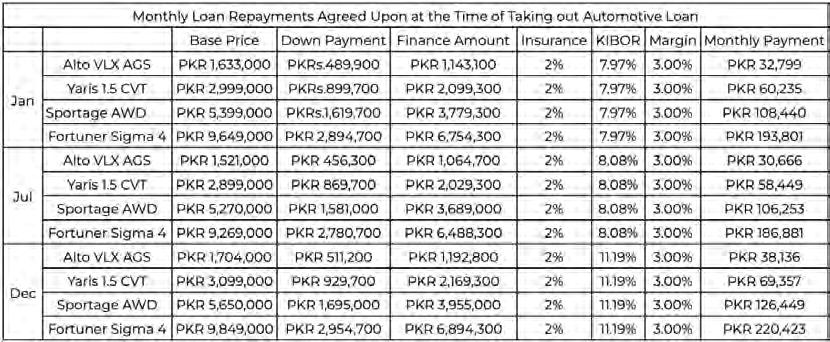

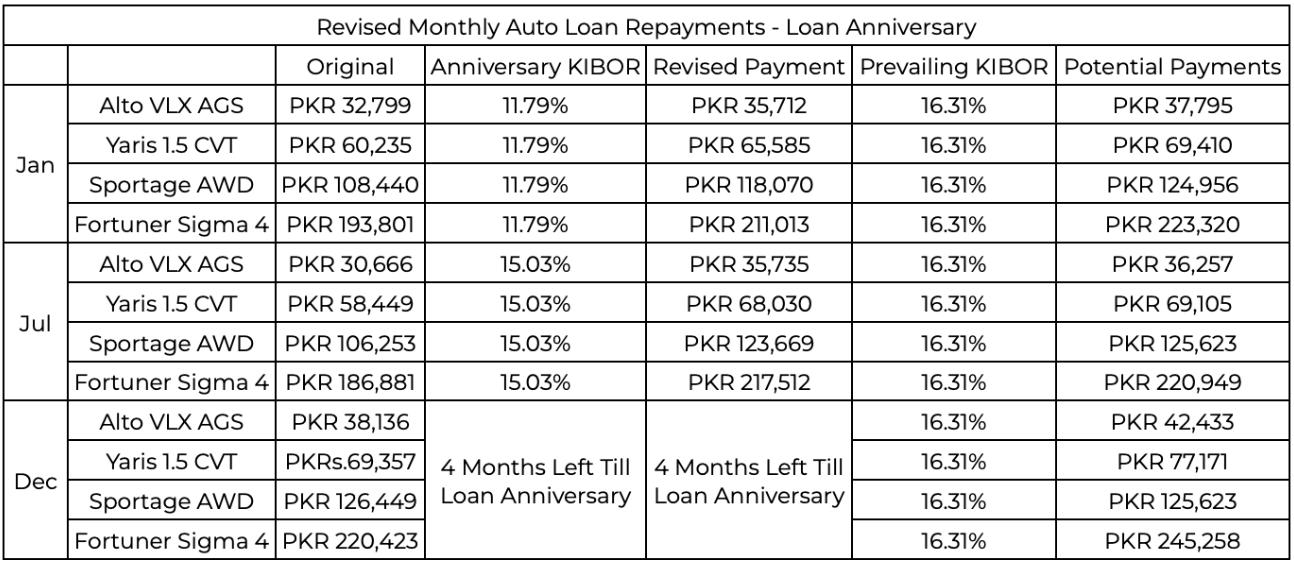

-

Babbar Wajid, Head of Consumer Banking at Habib Metropolitan Bank

BANKING the car is both a necessity and asset. However, defaults do occur when it is mathematically impossible for people to make their payments, and that is when banks start repossessing cars. The common assumption is that you miss a payment and your car gets repossessed. Now that is not incorrect but it’s also an oversimplification. Profit looked at what happens during a default process so that you do not (hopefully) have to. In the SBP Fair Debt Collection Guidelines, banks begin the process of repossession if the client does not make contact 30 days past due (DPD). Once the car itself has been repossessed, they are auctioned off. In the end, banks don’t lose out on this process at all. It is correct that banks would like to maintain relationships with their clients but on account of the relationship being severed, then liquidating the car is not a loss making venture for the bank either. The main loser in the situation is the borrower whose car and investment both go. The reality is that the instalments have gone up significantly. Profit reconstructed potential auto loans for a Suzuki Alto, Toyota Yaris, KIA Sportage, and Toyota Fortuner. The payment schedule is based on a 7-year loan period for the potential customers. The prices used for the listed automobiles are the prices for the top variant on the last day of the respective month. The base year taken for the automotive loan is Reconstructing2021.the loans for multiple back dates spanning a greater number of calen dar years is possible, however 2021 happens to see the greatest volume of increase in automotive credit looking at the aforementioned SBP credit data. For the sake of brevity and to avoid this becoming a complex jumble of numbers, the data from 2021 sheds more than enoughWhylight.have these prices gone up the way they have? At the centre of the whole thing is a little something called KIBOR. For those un initiated into the world of finance, the KIBOR (Karachi Interbank Offered Rate) is the rate at which money is borrowed by institutions in Pakistan. It is determined by the State Bank, which releases policy rates that then determine interest rates. The KIBOR hit a 13 year record high in April when the SBP raised it to 14.1%. There were speculations that it would at least go as high as 15% which it did in June. It is 16.31% as of the filing of this report. The chang es in the above mentioned rates are staggering. The breakdown is below. It is important to first understand that KIBOR changes lead to price revisions at different intervals during a customer’s loan; on the loan anniversary or calendar anniversary. The difference comes down to the product that one opts for. Profit is in no position to tell you which of the two you ought to get. However, Profit did do the maths on both types of the loans to see how much customers would have to pay more. Let’s first look at outstanding customer loans that have the KIBOR rate fixed in accor dance with their loan anniversary. Profit also looked at the potential pay ments that customers would have to pay if the current KIBOR rate was levied on them. The thing is that, this KIBOR rate will most likely be levied on the customers that took out their loans last January and December. I’m being optimistic with this KIBOR rate, and you’ll see why shortly.Now,onto customers with calendar anniversary automotive loans. On first glance, customers with calendar anniversary loans seem to be insulated from the matter. For now, at least. Things, however, could get worse. The KIBOR is changing on a whim everyday, and with negative interest rates abound, the rates could get much Becauseworse. we are still trading at negative interest rates, the SBP is still incen tivising borrowing rather than saving. Odd considering the current economic deci sions are aimed at dampening demand, right? Well the SBP knows this as well, and Inflation is obviously very high right now so people have to choose. They have to choose between consumption spending; things that are nice to have and things that they absolutely need. As a sector also, auto financing is largely skewed towards salaried customers who will feel the impact of the increase in taxation from July onwards. This double whammy will turn into a triple whammy in January when the KIBOR on the installments is revised.

-

If you are early in your lease, that could effectively mean your monthly increases by 60-70%. At the same time the price of everything (including fuel and maintenance - which effectively increases your cost of vehicle ownership) has gone through the roof. Monthly budgets have gone completely out of whack. Some time in the next 6 months this will catch up and people will start defaulting on their car loans. Azam Khan, Investment Professional

let’s just say that they have the ground for an other hike if they so choose. Particularly given, how Pakistan is reinitiating its IMF program. To catch up, your monthly interest loan payment is about to increase, if it has not already increased. Now ceteris paribus, the increase in the amount of what you have to pay is worrying but not apocalyptic. What is worrying, as Khan pointed out, is that the price of everything has increased. “Inflation is obviously very high right now so people have to choose. They have to choose between consumption spending; things that are nice to have and things that they ab solutely need. As a sector also, auto financing is largely skewed towards salaried customers who will feel the impact of the increase in taxation from July onwards. This double whammy will turn into a triple whammy in January when the KIBOR on the instalments is revised.” said Babbar Wajid, Head of Consumer Banking at Habib Metropolitan Bank, when asked about the matter. Wajid in particular is referring to customers with automotive loans that are revised on calendar anniversaries. However, needless to say that is similarly applicable to customers availing loan anniversary products. They may be feeling it already looking at the aforemen tioned sample repayment structures Profit created. The ‘08 example Let’s take a step back and try to get a hold of the larger picture. As we’ve mentioned before, a similar situation met the auto-loan industry back in 2008, and the crisis stretched over a five year period all the way to 2013. At the centre again was KIBOR and inflation. So, what exactly happened back then? To put it simply, Pakistan, like much of the world, found itself in an economic crisis. Only our crisis also had the additional pain of a political crisis and a failure of wonky oil economics. This in turn led to a spike in inflation and the cost of borrowing, which shall be henceforth referred to as the Karachi Interbank Offered Rate (KIBOR). What did the spike in these two do? Well, let’s do a deep dive into banking vernacular first so that the rest of the piece is more Defaultspalatable.arealsoknown as non-performing loans (NPL); Loans that are subject to late repayment or unlikely to be repaid by the borrower in full. Subsequently, the ratio of NPLs to a total lending portfolio is known as the infection ratio. That’s all we’ll need. What the two aforementioned increases did was it led to an increase in the infection ratio across banks’ auto lending portfolios. It actually set off a round of infection ratios that only started to taper off in 2014. Following 2014, the market has been relatively stable due to inflation and KIBOR never exactly hitting similar levels. There was a short-term spike in 2020 following a hike, though smaller than the one seen in 2008, which led to a rise in infection ratios again. This, however, only strengthens the hypothesis that there is a strong correlation between all the aforementioned aspects. On a longer term horizon, the market has remained relatively stable on account of normalised KIBOR and inflation rates. Looking at the longer term horizon in conjunction with the SBP’s credit, we see it is during this time that the automotive lending space also picked up pace.What’s the situation now? The KIBOR is at 16.31% as of writing and the Pakistan Bureau of Statistics reported inflation to clock in at 24.9% for July of this year. And this is why speculations are rife that we may be headed towards another round of defaults very soon. Will 2023 be any different? Well, maybe. “I do not think defaults will take place. The basic reason for this is that if you bought a car 2-3 years ago then its price has more or less doubled. You would be much better off selling that vehicle or giving it to somebody else and still earning a premium than to go into default” said Parvez Ahmed Shahid, former Co-Chairman of the Central Management Committee at Bank Alfalah, to Profit when asked about the differences between the situation now and in 2008. Shahid posits that vehicles have become an asset class between the 2008 crisis and now. Well, they indeed have. Profit has already documented how automobiles are investments in the Pakistani market. It is common knowledge amongst anyone with an interest in the sector as to why automobiles are an asset class in Pakistan.Read more: The lopsided market structure of the automobile industryHowever, let’s do a quick recap on the context still. Just so the following points can be understood better. Automobiles for better or worse, depending upon who you ask, are almost entirely imported 16

The thing with the 2008 crisis is that the KIBOR and inflation were able to set off rounds of defaults for years to come because Pakistan, like much of the world, was reeling from the 2008 financial crisis. Pakistan, like the world, may again be on the precipice of a global economic crisis. How different this crisis in the coming will be to the one in 2008 is anyone’s guess. However, going into the crisis, for customers to continuously service debt it is perhaps a necessity that they do not fall on any hard times. That doesn’t tend to be the case with economic crises but it is an assumption that we will have to rely on to forecast a sectoral apocalypse. Saviour of Last Resort It’d be remiss to not highlight, but does a default even matter if the bank renegoti ates with the customer? Banks, like any corporate entity, value the relationship with their clients.

Parvez Ahmed Shahid, Former Co-Chairman of the Central Management Committee at Bank Alfalah

Wajid and Shahid make valid and prudent statements. However, their assumptions rest solely on the financial position of customers.

Maximising customer lifetime value is not only an aim but also Marketing 101. Therefore, banks are not actively rooting for customer’s to default at all. The entire lending model is based upon the assumption that the client will be able to provide the bank with a steady stream of cash flow for years to come. They’re really not in an industry where trust issues are fair game. The SBP is cognizant of this as well. They’ve actually made it quite easy for banks to to renegotiate outstanding loans with custom BANKING I do not think defaults will take place. The basic reason for this is that if you bought a car 2-3 years ago then its price has more or less doubled. You would be much better off selling that vehicle or giving it to somebody else and still earning a premium than to go into default

commodities in gross and net terms. As an im ported commodity, its price is decoupled from the PKR and tied to global commodity prices or the USD for an umbrella term. Given how the PKR is susceptible, if not guaranteed, to depreciate, vehicles thus act as an inflationary hedge. In a country as starved for investment avenues as Pakistan, the automobile sector provides a means to accrue wealth.Furthermore, given that automotive companies operate on a Just in Time (JIT) model, there is an oversupply of vehicles in the market. This in turn also makes them a very liquid asset. A trip to Lahore’s McLeod or Lawrence Roads would give anyone unfamiliar with the entirety a live example. Maybe visit us whilst you’re there as well? “Look at the increase in car’s price from 2008-11 and compare it with the past two years. You will see a fantastic increase percentage wise and nominally as well.” said Parvez further if asked if the prices of cars were the only difference between then and now. Looking at Shahid’s statement, Profit looked at how much our aforementioned vehicles of choice have gained in value since our potential customers may have taken out their loans.Across the aforementioned vehicles, the average increase in value is 40%. The question then is, how many other investments yield similar results? These results are also likely to be even higher if we used a 2-3 year horizon rather than just look at Automobile2021.customers, whether they know it or not, they probably do, are financing an asset at the end of the day. The asset also has the added utility of being, well, a car as well. There is supposedly very little incentive that customers with outstanding dues might have to forsake their car. Particularly, if they have already paid a substantial amount. “Absolutely” said Shahid when Profit asked if it’s a rational choice for an individual to retain their car through the loan. Similarly, “The underlying asset will actually gain in value which means we’re less likely to see defaults and more likely to see contract terminations. I think this makes more economic sense for customers who are going through distress rather than have the bank run after the car” said Wajid when Profit asked what customers would choose between forsaking the car or continuing to pay. Contract termination means the custom er buys out the remainder of the contract.

Now I say this because it’s important. Another problem in 2008 was that the automotive loan market was effectively the wild west. It was a nascent industry and banks really just wanted to acquire as many clients as possible. They have, however, learnt since then. “Banks’ expertise on the consumer lending side was very limited. It was a learning period for financial institutions. I don’t see a repetition of the mistakes then to happen now” said Shahid when Profit asked about whether banks were also cognisant of their mistakes. “I don’t think banks are as ill-prepared as they were at the time and the portfolios are better managed and cleaner. There’s a lot more insight that goes into it and a lot more data now available with us with other banks to be able to help understand their client” said Wajid when asked if banks had matured and abandoned their old lending habits. Pakistani banks have not undergone a stress test similar to the 2008 crisis to really test Wajid and Shahid’s claims. However, it would be incorrect to believe that banks have undergone that maturity. This is because their entire profitability model has changed after the 2008 crisis. Profit has documented the transi tion, however, it falls outside the scope of this particular piece. Read more: Banks that don’t bank However, the tldr is that banks do not actively seek out customers to lend to relative to their other divisions. Therefore, the custom ers that they do lend to are probably thorough ly vetted because that is at best an additional revenue stream for the bank. At least you now know why your local bank isn’t investing to reduce queue sizes.

-

18 BANKING

-

-

ers. The SBP’s Prudential Regulations for Consumer Financing mandate that a loan has to exist for 9 months for it to be eligible for a refinancing scheme. The only restrictions that the SBP has on refinancing are that it should not be “rescheduled/ restructured more than once within 12 months and three times during five year period.”

Customers in the used car market in 2023 and possibly 2024 might just be the only beneficiaries of all this. They would benefit from banks auctioning off vehicles, so just maybe. n

Finally, the SBP only mandates that banks deem a loan to be a loss when a customer reaches 90 dpd within one year. Honestly, if you’re missing that many payments then you might have just taken the wrong loan.

The crux of the matter then is that the potential customers with outstanding dues are perhaps far more likely to be in a financial position to continue debt servicing despite additional strain in comparison to their coun terparts in 2008. Particularly, because, again unlike their 2008 counterparts, they are financ ing an asset which may either allow them to weather the storm or get back on their feet whenever the economic turmoil does subside.

-

What can we expect ahead then? It’d be good to end on a bright note and say defaults are not on the horizon. Profit cannot say that. Well, because if nothing else then the SBP has not pro vided infection ratios for this calendar year and did not respond to Profit’s request. Under standable given the storm of problems they’re combating right now really. Profit has already predicted more in flation for the remainder of the year that may even bleed into 2023. Just turning the tv alone is enough to ascertain the economic turmoil that not just Pakistan but the world is in. If there is to be a verdict given then it seems very likely that infection ratios i.e. defaults will increase. Whether they will be comparable to the ones seen during 2008-11, now that is something that really depends on how the economy plays out which is anyone’s guess really at this point.

The Russian invasion of Ukraine created a ripple effect in the energy markets as the largest producer of energy in the world was suddenly taken out of the market due to economic sanctions. However, such sanctions did not hamper its ability to generate export earnings as an acute shortage of energy in the market led to a massive spike in the price of oil, and gas alike. Europe which was (and still is) heavily dependent on Russian gas to fire up its economic growth, and heat its homes was in for a rude awakening as wholesale electricity prices increased by more than five times in many jurisdictions, taking a heavy toll on both commercial and residential electricity bills. More recently, wholesale electricity prices in Germany have exceeded a fresh high of EUR 500 per MWh, against an average of EUR 50 per MWh only about twelve months back, increasing by almost ten times. Household electricity bills are expected to quadruple in many jurisdictions within Europe during the next few months as the continent pays a premium to ensure uninterrupted access to electricity in the tightest energy market in decades. A massive surge in electricity bills comes at a time when inflation across the developed world is at its two decade high, and real incomes continue to erode. As disposable incomes squeeze, a downward shift in aggregate demand has the potential to kickstart a recession – which can’t be fixed by printing more money. Central banks can certainly print more money, but they cannot print more electrons which can generate electricity. An inadvertent consequence of the same is an insatiable growth in demand for LNG, wherein prices for LNG cargoes on the spot market continue to post new highs, more recent being US$ 50 per mmbtu (million British thermal units), compared to an

19COMMENT

In such a scenario, the winter will be dark, and it is time that the policy makers prepare accordingly, whether that is through energy conservation, recalibration of the mix, or through reallocation of energy sources from one economic sector to another. A recession in Europe will inadvertently have an adverse impact on Pakistan’s exports as well given that Europe remains a key market. A multiyear strategy needs to be in place in view of existing, and emerging global macroeconomic risks.

A dark winter Ammar H. Khan

The upcoming winter will be dark, but whether the next winter, and the one following that and so on will also be dark largely depends on policy decisions that are taken during the next few months. There needs to be a pivot towards energy security in the near term, and that means fast tracking exploration and utilization of indigenous coal. Similarly, there needs to be a well thought out conservation and public transportation strategy to reduce reliance on imported energy in the mid to long term. Inability to take such decisions will threaten our energy, and economic security further weakening an already fragile economic position. n

average of US$ 11 per mmbtu pre pandemic. As Europe contin ues to buy every available molecule of gas in the spot market, it is essentially pricing out other developing countries. To avoid blackouts in Europe (which has considerably high consumption of electricity per capita relative to other developing markets), blackouts are materializing in developing markets, including Pakistan, Bangladesh, and other jurisdictions which cannot buy cargoes in the spot market and are totally priced out.

There are instances where energy traders are redirecting cargoes which were originally directed towards developing markets to Europe, given the availability of higher prices there. In-effect, Europe is exporting blackouts to the developing world, as it wakes up from its excessive reliance on cheap natural gas provided by Russia.Pakistan being a low to middle income economy struggling with perennial external deficits and priced out of both energy and debt markets. As electricity generated from hydropower tapers off during winter, and as demand for natural gas grows during winter, extended lockdowns cannot be ruled out given unavailability of LNG, and depleting natural gas reserves. The country continues to get LNG cargoes from Qatar at a fixed slope on a long-term con tract, but inability to buy cargoes on the spot market due to being priced out will continue to weigh heavily on the ability to generate uninterrupted electricity during the colder months. Similarly, heightened coal prices given a tight market for coal in decades also makes imported coal unaffordable for the country, due to which we may also not see any significant generation of electricity via the coal fired power plants.

OPINION

The writer is an macroeconomistindependent and energy analyst.

20

The state of the sector It starts with the dams. Pakistan is, for the first time since at least the completion of the Tarbela dam in 1976, on the precipice of having a majority of its electricity generation coming from imported prima ry fuel sources rather than domestic ones. Following the Indus Water Treaty in the 1960s, immediately began working on the Mangla dam, on which construction started in 1961 and ended in 1965. The much larger, and more ambitious Tarbela dam was

-

By Asad Ullah Kamran I t is a simple problem. Pakistan relies heavily on imported fuel sources such as reliquified natural gas (RLNG) to produce electricity. Whenever there is an international crisis, such as the Russia-Ukraine war, Pakistan’s energy sector is rocked by the ripple effect. There is a simple solution. Cheaper fuel — something like coal perhaps. And the source is right there too. Spread over more than 9000 km2, the Thar coal fields are one of the largest deposits of lignite coal in the world — with an estimated 175 bil lion tonnes of coal that according to some could solve Pakistan’s energy woes for, not decades, but centuries to come.The question is, if this rich natural resource is available, why has it not been utilised more than it is currently? Discovered in the early 1990s by the Geo logical Survey of Pakistan (GSP), Thar Coal accounts for around 660 MW of electricity produced in the country. The potential is much greater. If new projects that are currently under construction become opera tional, in the next year electricity production from the Thar coalfields is expected to increase to as much as 2000MW.Inshort, Thar Coal offers a cheap, alternative, local source of energy that can be used to produce electricity and help Pakistan escape its topsy-turvy re liance on international markets to maintain its energy supply. Of course, choosing to rely on a fossil fuel like coal comes at a price. It is one of the most environmen tally damaging sources of energy there is, and will give pause to environmental scientists — particularly given the state of the smog-addled Punjab region. But let us be very real here. Environmental reasons are not why the potential of the Thar coalfields have not been realised. In fact, in the wake of the current commodity supercycle, the government has attempted to increase its already existent reliance on coal as an energy source. To do that, the government is relying on imports of coal. And while this is a queasy thing for environmentalists to think about, if coal is going to be used to produce electricity in Pakistan, it might as well be domestic coal rather than imported coal — at least electricity will be cheap that way.

-

Pakistan is continuing to import its fuel sources to produce energy because it has been unable to build the necessary infrastructure that would be required to use coal from the Thar fields. So what will it take, and how good of an idea is it?

ENERGY

-

“This is one of the major advantages of using Thar Coal, as it is the most economically viable source of fuel for the country. Thar coal expansion could also provide a huge relief for FOREX reserves of Pakistan with savings of approximately USD 2.5 billion, while it will result in the reduction of more than PKR 100 billion in circular debt on an annual basis.”

The potential, of course, is huge. “Currently, Pakistan is generating around 660 MW of electricity from Thar Coal. Within a year, the electricity generated from Thar Coal is expected to increase to 1,800-2,000 MW when new projects currently under construction become operational. Particularly, power projects on indigenous coal are promising a cheaper future for the country,” according to a statement given to Profit by HUBCO. As of now, there are only two power plants configured to use domestic coal, having a combined capacity of 1,320MW. The power plants owned by Thar Engro Coal Power Project (660MW) and Lucky Electric Power Company (660MW), both are considered to be critical for the grid. Although the Lucky plant, located at Karachi’s Port Qasim, is currently utilising a blend of imported and domestic

“The country’s energy mix needs an urgent overhaul with more indigenous sources like Thar Coal added to it. This will save precious foreign exchange reserves and put Pakistan on the path of sustainable energy security.”

22 constructed between 1968 and 1976. The truly mind-blowing fact about these two dams? If every single coal-fired power project in Thar came online today, all of them combined would produce less electricity than Tarbela and Mangla. These two dams – and the spree of dam construction that followed over the next two decades – meant that the bulk of Pakistan’s electricity needs were met by clean, domestically produced hydroelectric power plants. Yes, in the 1980s, the government began setting up oil-fired power plants, but the vast majority of Pakistan’s electricity came from water until at least the early 1990s.

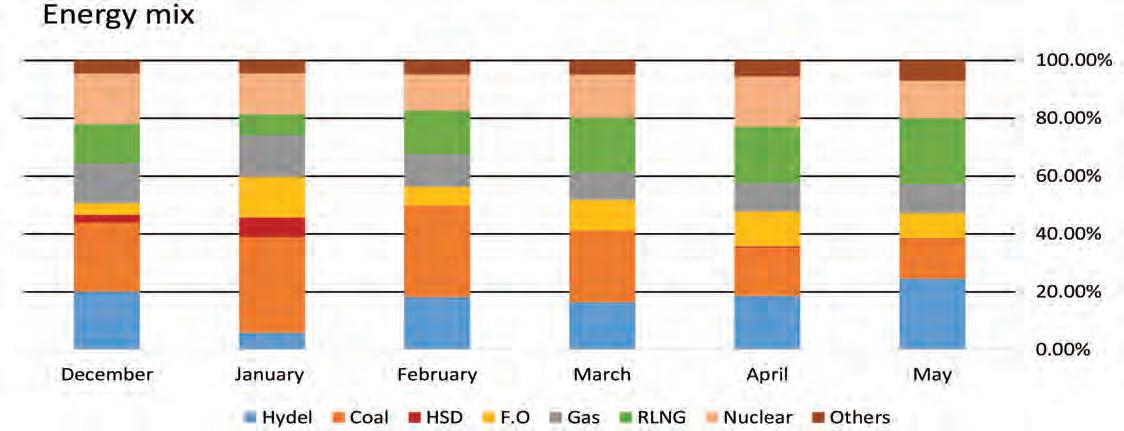

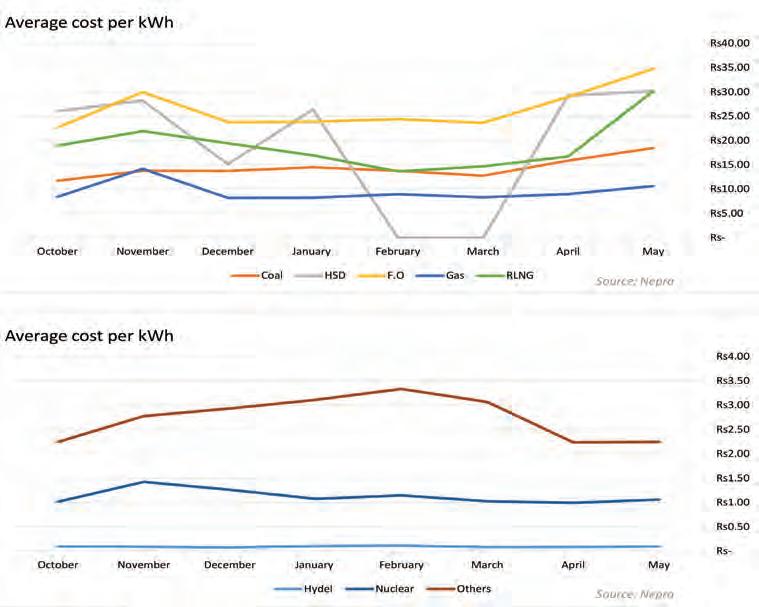

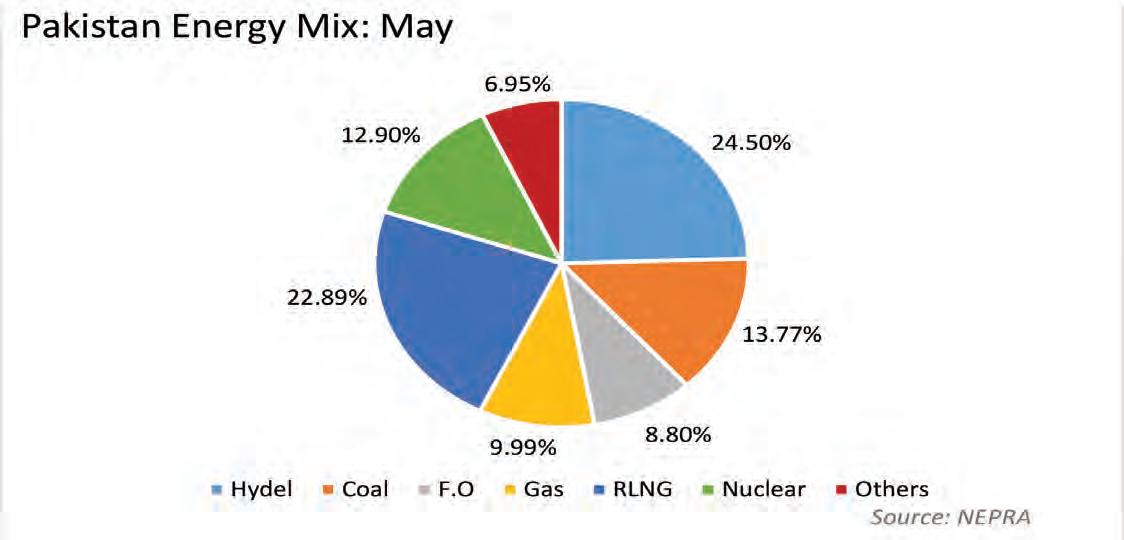

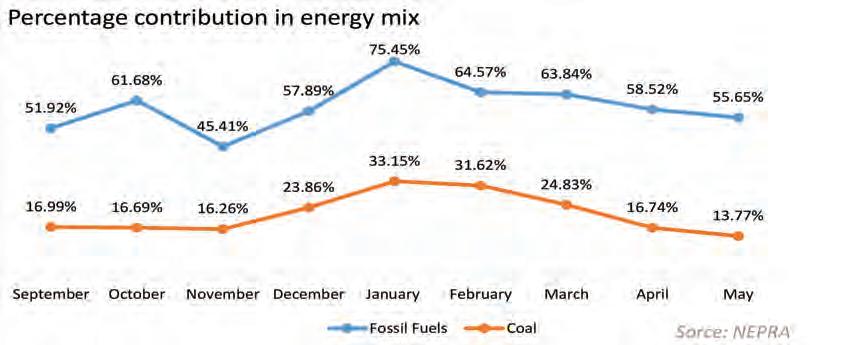

What followed on from now was a string of bad decisions beginning from setting up IPPs reliant mainly on oil, and then in the early 2000s the Musharraf Administration decided to convert at least some of that thermal power generation capacity from imported oil to do mestic natural gas, under the assumption that Pakistan had abundant domestic reserves. Throughout this time, coal was not a priority, even though the Thar fields had been discovered in the 1990s. “The total reserves from Thar Coal are more than the combined oil reserves of Saudi Arabia and Iran. The reserves are around 68 times higher than Pakistan’s total gas reserves. Compared to this potential the current utilisation of Thar Coal in the total power generation mix is less than 10% which means that there is huge opportunity to expand in this sphere,” explains Amir Iqbal, CEO of Sindh Engro Coal Mining Company. “That means Thar Coal has the potential to produce approximately 100,000 megawatts of electricity for 200 years – enough to make Pakistan self-sufficient in the energy sector.” In fact, it would not be until 2013 when the Nawaz Sharif administration introduced power plants reliant on imported coal. For more details of what happened to lead Paki stan to where its energy sector is, read: The end of cheap energy. What matters is that we are currently in a situation where we are dependent on RLNG. When RLNG was introduced into Pakistan’s energy mix, it was relatively cheaper and also environmentally friendlier than coal. Although long-term agreements with Qatar still provide gas at a relatively affordable rate, the spot market is a blood bath. Pakistan has been turning more and more to the spot market to address the growing local demand for gas. Considering the data published by Nepra in the monthly fuel charge adjustment reports, RLNG at its lowest point in the past nine months in February cost Rs 13.65/kWh, whereas in June the costs rose to Rs 29.87/kWh. The average cost of gas is rising at a very rapid pace, as this particular fuel is in short supply due to the war in Ukraine. Sanctions imposed on Russia have crippled the global energy supply chain as Europe is attempting to shift to RLNG, which is transported via spe cially designed ships, not to be mixed with the piped gas being supplied to Europe by Russia. Now, RLNG is a significant contributor to Pakistan’s electricity production. Enough so that the rising price of RLNG on the spot market has caused havoc in Pakistan. RLNG on av erage has amounted to 17.73% over the course of the past 10 months. This is a considerable contribution to the grid in terms of electrici ty; the inability to secure any new cargoes at affordable prices threatens the already fragile energy situation of the country. But it is still not the Most of the electricity produced in Pakistan is done through fossil fuels. From September last year to June of the current year, fossil fuels on average have accounted for about 60% of our energy pro duction, as per Nepra fuel charge adjustment reports.If we look at the average cost per kilo watt hour (kWh) an upward trend is visible. However, compared to the cost of electricity generated using other fossil fuels, coal is a lot less expensive. In fact, it is the cheapest after local gas. At the same time, the adverse impact on the environment is higher. On average, coal costs Rs 15.17/kWh and local gas ends up at about Rs 9.5/kWh for the recorded period. Local gas is depleting at a very high rate and hence our reliance on RLNG has been increasing over the past decade. Coal plants in Pakistan But then why aren’t we using more coal, particularly the domestic kind? To get a better understanding of Pakistan’s position on coal plants, it would be prudent to understand how many plants we have and how much they contribute to the national grid. At the moment the country is running five operating coal power plants owned by; Thar Engro Coal Power Project (Thar, Sindh), Lucky Electric Power Company Limited (Karachi, Sindh), Port Qasim Electric Power Company (Karachi, Sindh), China Power Hub Generation Company (Hub, Ba lochistan) and Huaneng Shandong Rui Group (Sahiwal,ApartPunjab).fromthe Engro coal power plant in Thar, all other plants are currently relying on imported coal to produce electricity. Although it must be noted that the Lucky Electric power plant is configured to use domestic coal; it is temporarily importing coal and will shift to coal extracted from Thar once the second phase expansion of the mine is completed. Data from the Nepra website indicates the contribution of coal in the overall energy mix fell significantly after February 2022. This was primarily due to the fact that Engro’s Thar coal plant as well as the Sahiwal coal power plant owned by a Chinese firm were both in operative. It contributed to the overall energy shortage in those months. The Engro plant had stopped producing electricity earlier in the year due to a major technical fault resulting in an explosion, whereas the Sahiwal plant was unable to procure coal, industry sources told Profit. The combined capacity of these plants is 1,980 MW. They however are expected to be back online over the year and the contribution of coal will increase. However, imported coal will still be a problem. Coal was priced at $200-250 per tonne before the Russia-Ukraine war, and as of August 17th it costs $400-450 per tonne, a monumental increase of about 80%. And that takes us to Pakistan’s indigenous coal option: Thar coal. Thar coal Amir Iqbal, CEO Sindh Engro Coal Mining Company (SECMC), told Profit that “The recent global supply chain disruptions have brought to light how Pakistan’s reliance on imported fuels is detrimental to its long-term economic growth,” says Engor Mining boss Amir Iqbal.

To break the country’s addiction to imported fossil fuels, renewable energy and Thar coal are necessary components of a well planned out energy mix. The current account deficit and global fuel dynamics have reinforced that reliance on imported fuels is not sustainable Rahmat Kamal Ghanghro, legal expert on energy and natural resources

lignite coal, the impact on the overall forex savings is still noteworthy. Talking to Profit, Hubco also said that it is expected that another two power plants owned by the company, namely Thar Energy Ltd and Thal Nova Power Thar (Pvt) Ltd would come online within a few months. Both of the plants would be operated by HUBCO and utilise domestic coal adding a further capacity of Another660MW.1,320MW power plant at Thar block 1, which was conceived even earlier than Engro’s project, would also be operational later this year, said Shamsuddin Shaikh, CEO National Resources Limited, and an expert in the sector. These delays have been hugely detrimental for Pakistan’s economy.

“Sindh Engro Coal Mining Company (SECMC) is operating the country’s first open pit lignite mine in Thar Block II with the cur rent mine capacity of 3.8 Mt/a providing coal to Engro’s power plant producing 660MW of power for the country as of today. As the mine expands and doubles its capacity to 7.6 MTPA by end of this year it would help add another 660 MW to the grid making the cumulative to tal to 1320 MW. As the project in Thar Block I comes online, another 1320 MW will be added to the grid,” says SECMC CEO Amir Iqbal. “Over 65% of Pakistan’s electricity is generated using imported fossil fuels, which exposes us to international supply chain shocks and fuel price fluctuations. The longterm solution for this problem is to increase the reliance on local sources of fuel such as Thar Coal, exploring alternate sources of natural gas, expanding hydel power plants and other sources of renewable energy”. The inability of the government to promote domestic coal is a critical factor in the underutilisation of Thar coal. He said that the government was advised to increase the reliance on domestic coal back in 2016-17, this could have been possible by retrofitting coal plants with the ability to process a blend of both imported and local coal. The existing plants can accommodate a blend of imported and domestic coal in certain ratios, without undertaking major capital ex penditures to retrofit plants. However to con vert completely to domestic coal would require the companies to incur capital expenditures for altering the configuration of the plant. Using domestic coal to produce electric ity would be one way to save precious dollars, according to HUBCO officials, it is esti mated that Pakistan has been able to save foreign exchange worth $200 million since the commercial operations of first Thar coal plant i.e. Engro Powergen Thar Limited. Imported vs domestic The difference in the cost of producing electricity from domestic coal and imported coal is substantial. The cost of producing electricity from the Engro plant, which uses domestic Thar coal, is Rs 10.44/kWh, whereas the Lucky Electric plant which uses the same type of coal (lignite) but imports it costs Rs 20.92/kWh, according to data from Nepra’s latest monthly fuel cost adjustment report. The other three coal plants, which use imported coal, owned by Port Qasim Electric Power Company (Karachi, Sindh), China Power Hub Generation Company (Hub, Ba lochistan) and Huaneng Shandong Rui Group (Sahiwal, Punjab), cost Rs 25.94, Rs 24.96 and Rs 28.88 per kWh respectively. As per information received from HUBCO: “The current price of Phase I of Thar coal is around USD 65/tonne which is significantly lower than the imported coal price of approxi-

-

-

TEXTILES24 mately USD 400/tonne. As the mine will be expanded with Phase II and Phase III becoming operational, the economies of scale will further reduce the cost of coal to approximately USD 27/tonne, resulting in an overall lower cost of electricity“Onegeneration.”ofthemajor advantages of using Thar Coal, as it is the most economically viable source of fuel for the country. The coal expansion could also provide a huge relief for Forex reserves of Pakistan with savings of approximately USD 2.5 billion, while it will result in the reduction of more than Rs 100 billion in circular debt on an annual basis” says Amir Iqbal.ThePhase II expansion of the mine is set to be completed later this year coinciding with the new coal power plants scheduled to be operational later this year as well. This can be seen as a huge development for the economy as it would help in decreasing reliance on imported fuels.

Amir Iqbal, CEO Sindh Engro Coal Mining Company

An economist, Dr. S. M Naeem Nawaz, an expert in tariff determination, while talking to Profit says, “the only way forward should be to align the power policy with the global climate change vision by focusing on renewable resources (primarily hydel and solar) to transform the primary fuel mix from fossil fuels to renewables in the long run.”

The country’s energy mix needs an urgent overhaul with more indigenous sources like Thar Coal added to it. This will save precious foreign exchange reserves and put Pakistan on the path of sustainable energy security

Another relevant point is made by Rah mat Kamal Ghanghro, legal expert on energy and natural resources with over a decade of experience in the sector. “To break the country’s addiction to imported fossil fuels, renewable energy and Thar coal are necessary components of a well planned out energy mix. The current account deficit and global fuel dynamics have reinforced that reliance on imported fuels is not sustainable,” she explained.When asked about the role Thar coal can play, Ebrahim said that in the interim, indigenous Thar coal could make a huge difference in securing the country’s economic and energy requirements. However, it must be underscored that a comprehensive renew able energy plan must be developed at an accelerated pace to eventually replace fossil fuels forever.But,practically speaking, she believes that if emission reduction requirements are raised now for projects which are already in the pipeline, the end user would have to bear the brunt of the costs. The fact of the matter is that the planning process related to these strategically vital projects has to be majorly revised, all factors and stakeholders have to be involved and be on the same page to make emission reduction a priority in our national psyche.

Ideal vs workable I n a discussion with Profit, Zofeen T. Ebrahim, an independent journalist, known for her dedicated contributions to areas of environment, and her interest in renewables stated that, around the world, the global energy crisis is compounded with climate-related disasters prompting developed countries to shift to renewable sources. It can mean the end of the dominance of fossil fuels. With plenty of sunlight and wind, Pakistan has the good fortune of transitioning and rid ing the renewable energy wave, she believes. Ideally, Pakistan should be moving towards renewable energy, or at least more envi ronment-friendly fuels, is the unanimous opinion that different stakeholders have voiced in discussions with Profit. However, as the situ ation stands, the world is running low on gas, and prices are spiking, hence necessitating a strategy that can insulate Pakistan’s energy sector from international price fluctuations.

Data published on the Nepra website corroborates the fact that renewable energy is cheaper, and because renewables require no additional fuel to run they would free the country from expensive fuel imports.

In response, even SECMC has acknowledged the reality of coal. “As a company we never deny that coal is not the best source of fuel but considering the needs of the country and for its sustained economic growth; de veloping coal and other sources of indigenous resources is the need of the hour,” says the SECMC CEO. “Over 50% of the total pow er generation of China, over 40% of total power generation of India and over 25% of the total power generation of Australia relies on coal amongst other developed countries of the world. These countries have realised the need of going back to coal and Pakistan should also follow suit by prioritising the energy security of the country. It is pertinent to say over here that the contribution of the Thar Coal power project to the overall carbon emission of Paki stan is less than 0.10%.”

The way forward M aintaining energy security all while ensuring sustainability and affordability is a very tough nut to crack, countries around the world have made a lot of headway, yet there’s a long way to go globally. In the context of Pakistan, energy security has been a question of the ages. As far as public policy and government initiatives go most of them have lacked oversight and have failed in adopting a long-term approach on the issues of Regardless,energy. discussions with stakeholders and experts have all ended on the same note; the most economically feasible and sustainable approach would be to focus on renewables and Thar coal. Utilising domestic resources rather than relying on imports is invaluable to forex reserves in the long run. Additionally, it would significantly bring down the cost of electricity, based on calculations of Rs/kWh of electricity mentioned earlier in the article. At the same time, the environmental impact of burning coal is a real and present danger but that requires mitigation through policies.Renewable energy such as wind and hydel energy cost significantly less than even Thar coal, but also have limitations. For starters, renewables are unreliable sources to handle the base load, which is the minimum demand of electricity over a period of 24 hours. Electricity being produced by wind or solar farms is susceptible to variations in efficiency based on weather conditions and time of the day. Additionally, establishing renewable projects on a larger scale would involve massive capital investments to develop infrastructure.Aworking combination of Thar coal and renewable energy can ensure a sustainable long-term solution. The Indicative Generation Capacity Expansion Plan (IGCEP) 2021 also states that, “inclusion of variable renewable energy, hydro and Thar coal will help in lower ing the basket price of the overall system thus providing much needed relief, though in the long run, to the end consumers”. Iqbal, was also of a similar point of view stating that, “by creating a long-term strategy and attracting investors through consistent policy related decisions, Pakistan will come out of its energy crisis and embark on the path to sustained economic growth as cheaper electricity is one of the most essential components of a growing and developing country”. Though the role of Thar coal in the country’s overall energy mix is on the rise, there is potential for the government to do more and fast track development plans. n

OPINION

Rarely is the more important question asked: why is it that Pakistan is not integrated with global supply-chains?

Which brings us to the conversation around debt, which was weaponized as an economic issue by Imran Khan and his po litical party in the run-up to the 2018 elections. Once again, while concerns are raised about Pakistan’s indebtedness, especially to foreign creditors which then are believed to undermine the country’s sovereignty and policy independence, the right questions are never asked. Inquiry should focus on why is Pakistan reliant on debt-financing and why is this reliance continuing to increase?

26 COMMENT through this approach are ignored, leading to long-term structural imbalances in the economy. Rather than seeking to mobilize more resources, the more important question is why does Pakistan have a low tax-to-GDP ratio? Ask this question and a lot of structural issues about the economy are revealed. For example, the country’s policy makers refuse to make the real estate sector pay a fair share of taxes. This is why the city of Pune, with a population of roughly 7 million people, raises more in property taxes than the entire province of Sindh, which is home to nearly 50 million citizens!

The answer to this question is complex but suffice to say that high tariff and non-tariff barriers, lack of investment in boosting total factor productivity, and barriers to attracting foreign direct investment all play a role in exacerbating this issue. But because the right questions are not asked, the optimal solution is never implemented, leading to a policy that sinks scarce resources into a bottomless pit where the only ones getting enriched are those who have gamed the system for themselves.

Another case in point is the retail sector which successfully resisted the last dictator the land of the pure had seen. With a significant segment of a consumption-driven economy untaxed, is it any wonder that Pakistan struggles to mobilize sufficient re sources? A similar issue plagues the conversation around current account deficits. It is common for people to argue that current ac count deficits are high because Pakistan does not export enough goods, the reason being that the country is not integrated into global supply-chains. Inquiry stops with this rationale, meaning that year after year more incentives are provided to exporters in a bid to increase export earnings.

Asking

Uzair Younus

-

Exploring this question reveals that the issue is not only linked to low tax-to-GDP ratio and limited export earnings, but to the very nature of economic growth in the country, which is driven by increased deficit spending by the sovereign. Because deficit spending is mainly focused on areas that barely increase total factor productivity of the economy, it is not surprising to see that this reliance continues to grow as policymakers seek to fuel growth in a bid to create a feel-good factor about their economic performance. The ongoing crisis is one of a recurring series of crises where the economic discourse has focused on the wrong set of issues. As a result, it is no surprise that the choices made to deal with the crisis in the immediate term are the same as the ones made in the past. With the same experiment being repeated once more, it would be insanity to expect a different outcome. n

Where is the dollar headed to? Should I buy a car now before it gets expensive? Is the economy out of the woods? Will this be the last bailout Pakistan’s economy needs? Many of us, this writer included, have been asked the above questions and then some over the last few weeks. The dramatic decline in the value of the rupee, paired with scenes of chaos and upheaval from Sri Lanka, fueled concerns that Pakistan’s economy was staring into the abyss. There is, however, a major flaw in Paki stan’s economic discourse: many of us are asking the wrong questions. Which is why it is no surprise that the solutions that are pursued only exacerbate the decades-long economic crisis that Pakistan is grappling with today.Three topics that are frequently discussed in mainstream media, newspaper commentary, and drawing rooms are enough to prove the point: taxation, current account deficits, and debt. Spark an economic conversation with folks ranging from a Seth sitting in a market to current and former prime ministers, and within minutes they are likely to say that a key issue is that Pakistanis do not pay taxes. This in and of itself is a falsehood: every single Pakistani who buys a liter of petrol or diesel, tops up their mobile phone, or pays electricity bills is a taxpayer. But let us not digress. What folks in Pakistan continuously bemoan is that the country has a low tax-to-GDP ratio, meaning that it just does not mobilize enough resources to pay for its expenses. As a result, successive budgets and bailout packages seek to raise more taxes, picking arbitrary targets simply to balance the books. This author maintains that Pakistan has accounting, not finance ministers. As a result, policy uncertainty becomes the norm, not the exception when it comes to taxation, with governments simply trying to find immediate ways to meet their revenue targets. The distortions created the wrong questions

The writer is Director of the Pakistan Initiative at the Atlantic Council, a Washington D.C.-based think tank, and host of the podcast Pakistonomy. He tweets @uzairyounus.

-

The finance minister’s job entails dealing with various stakeholders. Sometimes this includes negotiating and engaging. Acts like these make it seem like the position of finance minister is irrelevant. It takes away the bargaining power that the minister has. Some segments of society might choose to engage with the top leadership instead of the minister because they feel decisions are made top down. The finance ministry is a key ministry. Some argue that it is more powerful in terms of impact than any of the ministries combined. After all, it presents the budget, interacts with every ministry and takes key economic decisions that impact everyone.

-

Regardless of who is in government, taking credit for a decrease in the price of petrol or taking the blame for an increase in the price of petrol is childish. These are merely movements in international markets being passed on. Then again, the political economy works in such a way that fuel prices, which eventually also act as an indicator of inflation for a layman, are used for political point scoring.

The very fact that Ismail was indirectly yet publicly criticised by his political party leadership shows how important pandering to the general public is. Instead of making this a moment to educate citizens on the importance of market-based pricing and deregulation, the party decided to take away some credibility from the finance ministry. This is also not the first time that the ministry has been undermined. Maryam Nawaz often tweets at Miftah telling him to take notice or fix things. Something that could’ve been a WhatsApp message is done publicly in a derogatory way which further undermines the Thisministry.givesthe impression that the ministry takes dictation which should not be the case. The political signalling here could not be any worse. Now you’re probably wondering why this is important.

Ariba Shahid OPINION

27COMMENT so not just by the opposition but by the ruling party as well! Maryam Nawaz and by extension the Sharif family patriarch Mian Nawaz throwing his party’s finance minister, Miftah Ismail, under the bus for increasing prices might be a first. Of course, much can be said about the state of Jati Umra and the murmurings about PML-N and PML-S that have gone from whis pers to loud laughs. But that’s not what we’re talking about here. No. There is only one principled stance here: the finance ministry is not a scapegoat for fuel price hikes. Very briefly put, Pakistan is a price taker when it comes to petrol prices. While the import composition of Pakistan primarily consists of fuel, the quantum of fuel imports by Pakistan in the global arena is a spec of dust. This means that when prices move in the international market Pakistan has no option but to buy at those prices.

I t is like clockwork. Every time there is an increase in the price of petrol, minor or major, the government is faced with a series of challenges that dominate the news cycle. It goes something like this. First, the opposition benches in parliament rail against the price hike in petrol, accusing the government, the prime minister, and the petroleum minister of being anti-people. Then, the news channels send out television crews to petrol stations where people have queued to buy petrol at the old price before the stroke of midnight. There, they interview people that rant and complain about the increase in the price of petrol. After this, opposition parties send their talking heads on televi sion. They spend hours doing live TV in which they rant and complain and hurl vague accusations of corruption. The government, in the meantime, sends meek explanations and mutters about international market dynamics determining prices, not them. Nobody listens. The arguments, the news cycle, the process is all nearly set in stone, no matter who is in power and who is in the opposition. Just like birds sing, and Karachi floods in the monsoons, and Saqib Nisar cries himself to sleep every night, it is a fact of life that politicians politicise petrol prices. It is such a regular feature in Pakistani politics that even the saner voices in public discourse have said ad nauseum that there should be no politicisation of fuel prices, and instead, governments should be criticised and encouraged to make cities more walkable and provide better public transport. This year around, however, we’ve got a new level of crazy in the house. Not only have fuel prices been politicised, they have been done For the love of all that is good, leave Miftah alone!

The writer is a business journalist at Profit. She can be reached at com/AribaShahidcom.pkshahid@pakistantoday.ariba.orattwitter. Petrol prices should never be politicised. But for them to be politicised within one’s own party is a new kind of wacky

I’m also not arguing that a finance minister should be hailed a hero for taking the right decisions. Appreciation is warranted, but scapegoating is unnecessary and damaging Political parties when in government need to ensure they put on a unified face. Last month we saw how uncertainty created havoc in the financial markets in Pakistan. Stability is important for economic progress.

The notion that party leadership and the finance minister are not on the same page is not confidence-in ducing for businesses. It doesn’t matter who is in the finance minister seat, whether Hafeez Sheikh after taking tough economic reforms or Miftah Ismail after increasing fuel prices - they should be backed when taking the right decisions. They shouldn’t be given unceremonious exits for taking tough decisions.

OLX also shut down FCG’s Berlin office last year where it was based. While how much of CarFirst is owned by OLX is not known to us, a source at OLX in Pakistan told Profit that OLX Autos in Pakistan was CarFirst, which means that OLX effectively controlled CarFirst in Pakistan.

28