By fully embracing technology, you can streamline processes and enhance compliance, allowing you to create personalised client experiences. From CRM to AI, we look at the latest trends in the market.

Cover story + pg 10-15

WHY DFMS ARE ESSENTIAL Discretionary fund managers (DFMs) take the complexity of fund selection and portfolio management off advisers’ shoulders. By outsourcing investment decisions, you can be freed up to grow your practice.

Pg16-17

KEEPING UP WITH UNIT TRUSTS Unit trusts remain a versatile building block for client portfolios, offering diversification, accessibility and professional management, making them suitable for both entry-level investors and high-networth clients.

Pg 18-22

OPPORTUNITIES OFF THE BEATEN PATH

Investors seeking uncorrelated returns and long-term growth opportunities should keep their focus on private equity. We take a closer look at the risks, liquidity constraints and potential rewards in the private equity space.

Pg 24-25

WANT MORE VALUE FROM YOUR INBOX?

Scan to subscribe to our weekly newsletters.

Future-proofing advice in an AI-driven era

Back in July 2001, Kobus Barnard, now Managing Director of Allegiance Consulting, wrote an article for MoneyMarketing that seemed more science fiction than reality. He spoke of a tool that could “calculate more than 7 million financial scenarios in less than a minute, predict your financial future, consider your ever-altering reality, be available 24/7, have the combined IQ of the world’s top experts, reach any client anywhere, and handle millions of clients at the same time – all without charging commission”.

“At the time, it felt like a dream,” recalls Barnard. “But I knew that technology would eventually make this possible. What strikes me is that it only took 24 years for those predictions to become reality. Today, it’s no longer a fantasy, it’s our everyday environment.”

Technology has not only caught up with financial services, it has enabled hyper-personalisation and scaling of traditional models of advice. From compliance and client onboarding to complex scenario planning, automation and artificial intelligence are redefining the role of the adviser.

For Allegiance Consulting, founded in 1999 as a small team of legal advisers supporting independent financial intermediaries, the journey into technology wasn’t about chasing trends. It was about solving a very practical problem: availability. “We were booked three months in advance. The only way to scale complex advice was through standardisation, simplification and automation – in other words, technology,” says Barnard.

That realisation sparked a transformation that took Allegiance from being 95% consulting-led in 2009 to 99% technology-led today. Along the way, they built a financial platform that helped advisers unlock billions in opportunities, and experimented with early AI engagement tools, laying the groundwork for the fintech-driven world we now inhabit.

From fragmented agendas to aligned commitment

In the early 2000s, when bank assurance was booming, Barnard noticed a fundamental gap. Despite housing short-term insurance, lending and investment products under one roof, banks struggled to align these services around a single client view. “It was like looking at a Venn diagram where the circles barely touched,” Barnard recalls. “There was no shared agenda between banker, adviser, auditor and client.”

To test the concept, Allegiance Consulting ran experiments with groups of advisers. The insight? Timing and alignment matter more than opportunity alone. “If you create a roadmap where everyone – client, adviser, bank, auditor – agrees on priorities, you achieve what we

call aligned commitment,” says Barnard. By breaking big opportunities into phased plans over time, clients are more likely to say “yes” consistently, priming them for long-term decisions.

Technology as the book of life

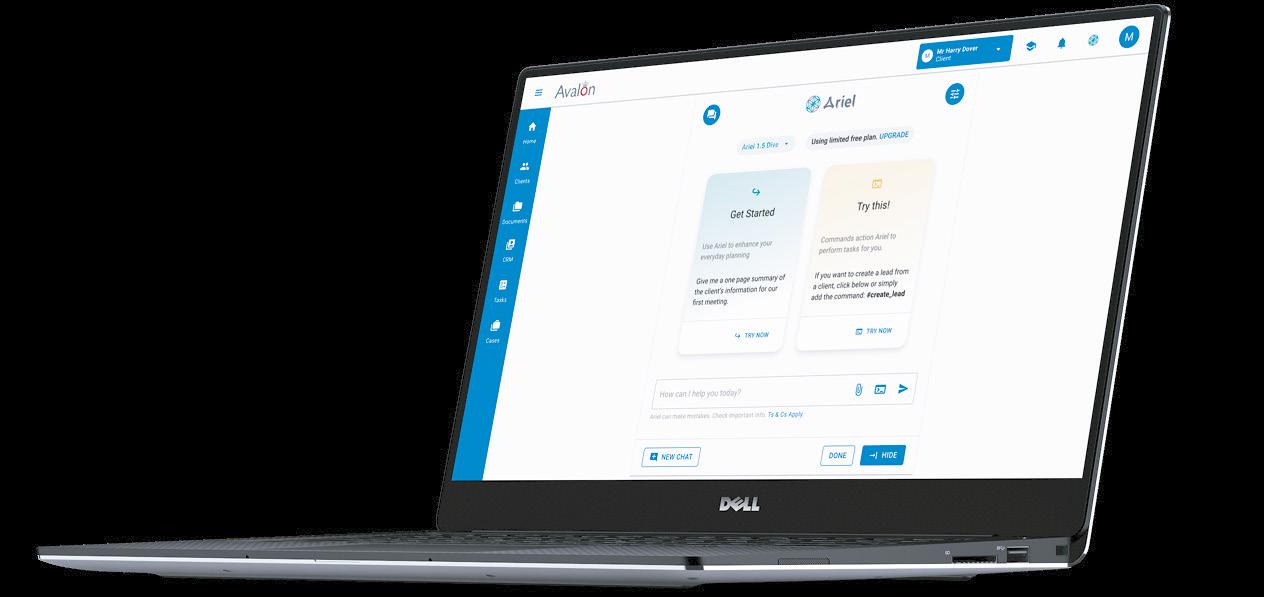

This philosophy shaped the development of Allegiance’s CRM system in Avalon. More than a contact manager, it became a collaboration framework to record what Barnard calls the “book of work” – a rolling five-year roadmap of a client’s financial life. The platform allows advisers to map opportunities, align them with client goals and track progress through ongoing conversations.

Beyond opportunity management, the CRM incorporates task management, document and forms libraries, integrated e-signatures, service ticketing and seamless collaboration with network partners. It has been fully refreshed in the past four years on a modern technology stack, ensuring both depth and usability. It is in the financial planning component where the platform truly excels beyond our wildest expectations. For planning, Avalon offers comprehensive modules: retirement saving, investment planning, risk analysis, estate planning, and business needs analysis. All of these components work cohesively to give advisers both breadth and depth of financial insight. It allows advisers to scale their own practice with hyper-personalisation.

“The Avalon platform in its entirety is built around our Massive Transformative Purpose – empowering advisers to help clients discover, achieve and live remarkable lives,” explains Barnard.

“We see it as the foundation of a Contextual Financial Identity™ for every client – a living, breathing model that integrates their data, goals, values and behaviours. That means advice is not just productdriven, but deeply personal, scalable, and always aligned with client outcomes.”

Looking ahead

Allegiance’s focus is now shifting to expand with a client engagement app, called Dreamzter™, which will become the tool for advisers to connect to their clients at scale. Dreamzter captures a client’s goals, passions, and dreams in an intuitive ‘wheel of life’, creating what Allegiance calls a contextual financial identity – a kind of digital financial twin of the client in the cloud.

Continued from previous page

The next step in that evolution is Ariel, an Artificial Intelligence entity. “Ariel has two personalities,” says Barnard. “It’s a super Artificial Intelligence assistant in the hands of the advisers – deeply integrated into Avalon. This phase is complete and is entering into wider testing now.”

The second personality of Ariel is to act as an Artificial Intelligence Super Adviser. “We have fused Ariel with the Contextual Financial Identity™ of the client, giving it access to our full planning suite. It will allow advisers to scale vertically because Ariel knows the client so understands how to unlock more value, and that translates into unlocking opportunities for the advisers in their same base. It also allows you to scale horizontally,” he says. “Ariel can act as an integrated paraplanner, legal adviser and admin clerk rolled into one. Advisers can ask Ariel to prepare for a meeting, analyse opportunities, or draft documents in real time, all while staying secure and compliant.”

Importantly, AI operates in the background. “Advisers don’t need to feel they’re dealing with a bot,” Barnard explains. “The client experience remains human, but powered by intelligence that saves time and unlocks personalisation.”

Scaling advice with simplicity

But technology alone isn’t enough. As Barnard acknowledges, when faced with a comprehensive system with many features, it may overwhelm users. “The key is design,” he explains. Allegiance introduced a dual approach: a shallow end, known as Advice on Rails™, and a deep end for complex planning. Advice on Rails is a guided, storyboard-style process for producing plans in minutes, intuitive enough to use without training. At the same time, power users can dive into advanced estate planning and scenario modelling.

Training is also embedded in the system through Just-in-Time learning: bite-sized videos, PDFs and contextual prompts triggered by where the user is in the platform. “We’ve built the experience so that an adviser can get going in 10 minutes, without needing a manual,” Barnard says.

Security and compliance by design

With banks and corporates entrusting client data to the platform, security was non-negotiable. Allegiance partnered with

leading cyber-defence specialists, conducts regular penetration tests, and operates on a secure Azure infrastructure with a special dispensation for localised disaster recovery. “We never believe we’ve arrived on security,” Barnard stresses. “We’re always alert, always testing.”

Compliance has also been built into the DNA of the system. “We are actively driving ‘Compliance through Convenience’,” explains Barnard. Allegiance’s advice transaction framework captures every step of the financial planning process; from needs analysis to product selection, ROAs and supporting documents, in a structured, auditable container. For corporates, this provides full compliance oversight; for independent advisers, the same framework is now being rolled out to simplify recordkeeping and reporting. Compliance becomes a safety net, not a burden.

With the COFI Act set to reshape adviserclient relationships around enforceable contracts, Allegiance is already positioned for the shift. Its nine-step process, rooted in the traditional six-step financial planning model, aligns directly with COFI’s emphasis on agreements, SLAs and transparent client outcomes.

Scaling advice, injecting hope

For Barnard, the true promise of technology is not just efficiency, but accessibility. South Africa’s 61 million people include millions who live in financial misery, excluded from quality advice simply because it was too expensive to deliver. Allegiance’s mission is to change that.

“Financial wellness starts with hope,” he says. “Our dream is to give people, even in the most difficult circumstances, a spark of a better tomorrow.” By combining scalable AI-driven advice with human empathy, Allegiance believes advisers can reach clients previously left behind and help them make the consistent micro-decisions that compound into financial security over time.

The technology has the potential to quantum leap advisers into explosive growth. Our message is to embrace it to the fullest extent, and you may just be pleasantly surprised as to how it will unlock previous opportunities that was hidden in plain sight.

ED'S LETTER

Technology is no longer a ‘nice to have’ for financial advisers; it’s a necessity. As the industry continues to move forward, those who embrace digital solutions are finding themselves better positioned to meet client expectations, scale their practices, and remain compliant in an increasingly complex environment. In this month’s issue, we take a close look at how technology is transforming advice – from client engagement tools and CRM systems to AI-driven insights that support better decision- making.

Alongside this, we turn the spotlight on unit trusts, which are still one of the most versatile building blocks in client portfolios. With shifting regulations, growing appetite for offshore diversification and increasing demand for cost-effective passive options, advisers have much to consider when navigating this space. We also explore the role of discretionary fund managers (DFMs), who are helping advisers sharpen their value proposition by outsourcing investment expertise and freeing up time for client relationships.

Private equity is a space that continues to capture attention from family offices, institutions and high-net-worth investors looking for differentiated returns. We unpack where the opportunities lie and what advisers need to know when considering private equity in a client’s portfolio. Enjoy the read and, as always, let us know your thoughts. Stay financially savvy,

Sandy Welch Editor, MoneyMarketing

Note: If you subscribe to our MoneyMarketing newsletter, see QR code on the cover, you will receive a special discount off a News24 or Netwerk24 subscription*.

*Offer available to new subscribers only.

EARN YOUR CPD POINTS

The FPI recognises the quality of the content of MoneyMarketing’s October 2025 issue and would like to reward its professional members with 2 verifiable CPD points/hours for reading the publication and gaining knowledge on relevant topics. For more information, visit our website at www.moneymarketing.co.za

Stephan le Roux Financial Planning Specialist at Old Mutual Wealth

How did you get involved in financial services – was it something you always wanted to do?

Financial services was not a career path I had initially considered. My passion was opera, and I pursued it wholeheartedly by enrolling at the UCT College of Music, where I completed a Performer’s Diploma in Opera. While I thoroughly enjoyed my time at opera school, I began to question in my final year whether a career in performance would be financially sustainable in the long term.

During this period of reflection, I met a manager from Old Mutual Personal Financial Advice who encouraged me to explore the possibility of becoming a financial adviser. Initially, I was hesitant because I thought the role was purely sales-driven, and I didn’t see myself fitting into that environment. However, after engaging in further conversations, I decided to give it a chance.

I joined Old Mutual the year after completing my studies and was impressed by the structured training and clear learning pathway offered. I obtained all the necessary qualifications, including postgraduate diplomas in both Financial Planning and Investment Planning. What started as an unexpected opportunity has since evolved into a deeply rewarding career.

What was your first investment – and do you still have it?

In Grade 8, I invested R600 into the Old Mutual Investors’ Fund. I held the investment for about nine years, and when I cashed it out to put down a deposit on my first car, it had grown to four times its original value.

Later, during my first year of university while working as a waiter, I took out my first endowment policy. That contract is still active today and continues to form part of my long-term financial planning strategy.

What have been your best – and worst –financial moments?

My worst financial moments occurred when I was chasing easy returns without a solid understanding of investment principles. As a student, I fell for a pyramid scheme and later invested in a small business without conducting proper due diligence – both decisions resulted in significant financial losses. These experiences made me overly risk-averse in the early stages of my investment journey, which limited my growth potential.

My best financial moments have all been tied to education. Gaining financial knowledge, whether formally through qualifications or informally through self-study, has empowered me to make informed decisions.

What are some of the biggest lessons you have learnt in and about the finance industry?

I’ve been involved in thousands of financial plans, and one of the most consistent lessons I’ve observed is the long-term value of early, quality financial advice. Individuals who engage with a competent financial planner early in life are far more likely to retire with financial security and peace of mind. Conversely, those who attempt to manage their finances independently often fall short, because their decisions are shaped by personal beliefs and assumptions that aren’t grounded in facts. These biases can lead to inaction or emotionally driven choices that undermine their financial wellbeing.

A key insight I’ve gained is that we all need someone to act as a mirror that reflects our behavioural patterns, challenges our assumptions, and offers new perspectives. This is the true role of a skilled financial planner: not just to provide technical advice, but to guide clients toward more empowering financial beliefs and behaviours. Finding the right planner is essential.

What makes a good investment in today’s economic environment?

A good investment is one that helps a client achieve their personal financial goals. As financial planners, our role begins with understanding what truly matters to the client: their goals, dreams and aspirations. Through coaching techniques, we help bridge the gap between where they are now and where they want to be.

Once we’ve clarified their objectives, we model the required investment return – above inflation – that’s necessary to achieve those goals based on their current financial circumstances. This required rate of return then informs the appropriate asset allocation. With that allocation comes inherent risk, which must be clearly understood and agreed upon by the client.

A key part of our responsibility is to ensure the client is well-informed about this risk and that their expectations are managed accordingly. If the client feels uncomfortable with the level of risk required to sustain their desired lifestyle, we work with them to reassess and potentially adjust those lifestyle goals. Ultimately, a good investment in today’s environment is one that

balances growth potential, risk management and inflation protection, while remaining aligned with the client’s personal values and long-term objectives.

What finance/investment trends and macroeconomic realities are currently on your watchlist?

One of the most significant trends I’m observing is the rise of AI and techdriven investing and advice. While these innovations offer powerful tools for financial planners, they also present new risks. For clients, caution is essential due to the increasing prevalence of AI-powered scams and deepfakes. Another concern is the growing number of individuals taking financial advice from online influencers who lack formal financial training or experience. From a macroeconomic perspective, longevity and demographic shifts are reshaping financial planning. With people living longer and many caught in the responsibilities of the sandwich generation, there’s a growing need to work well beyond traditional retirement age. This reality requires a fundamental shift in how we approach retirement planning.

What are some of the best books on finance/ investing that you’ve ever read – and why would you recommend them?

One of the most impactful books I’ve read is The Psychology of Money by Morgan Housel. What sets this book apart is its focus on the emotional and behavioural aspects of money, which are areas often overlooked in traditional financial literature. Housel illustrates how mindset, discipline and habits play a far greater role in financial success than intelligence or technical knowledge. In my experience, developing a healthy relationship with money begins with improving financial habits and mindset, and this book provides an excellent foundation.

By Sandy Welch Editor, MoneyMarketing

When Guy Opperman was appointed by former UK Prime Minister

Theresa May as the world’s first Minister for Financial Inclusion in 2017, he knew the challenge ahead was immense. He was stepping into a role that highlighted one of the greatest challenges facing both developed and emerging economies: how to ensure that everyone, not just the middle and upper-middle classes, can access meaningful financial products and secure their long-term futures. “The UK had nearly 10 million people who didn’t have £100 saved,” he recalls. “And that’s in a country with relatively high financial literacy. The question was: how do you make insurance, savings and pensions accessible to low-income workers, and how do you make it easy?”

Opperman’s dual focus on pensions and financial inclusion reshaped the conversation around financial services, especially in a post-COVID world where technology, accessibility and simplicity are no longer ‘nice-to-haves’ but essential components of long-term resilience.

Tackling the inclusion gap

For Opperman, pensions and inclusion became a “day job and night job” combination: managing a £120bn state pension system alongside a £1.5tn private market, while also pushing to create simple, mobile-based solutions for those excluded from the system entirely.

“The reality is, if it doesn’t work on your mobile phone, particularly for younger and lower-income families, it’s not going to work,” he says. “Education must be bite-sized, accessible and relatable because people are busy, and they don’t have time for hour-long lessons on financial products.”

His efforts included creating community banks to counter payday lenders, promoting workplace auto-enrolment, and designing financial education initiatives that could be rolled out in both government and corporate settings.

One of the biggest challenges governments and employers face today is how to attract, retain, and support older workers in the labour force. In the UK, Guy Opperman says, that has meant tackling both bias and incentives.

Financial inclusion, DC pensions and the Midlife MOT

He was instrumental in ensuring the UK government created a favourable environment for companies employing people beyond retirement age. Other countries, like Japan and those in Scandinavia, have gone further, either offering pension top-ups for continued work or framing it as a civic duty to keep contributing. “Every government has levers it can pull,” Opperman notes, “but the message is clear: older workers are an asset, not a burden.”

The midlife MOT of wealth, work and wellbeing

One of Opperman’s most talked-about policy innovations during his time in office is the Midlife MOT, a simple but effective checkup for employees aged 45 to 60. Developed with Aviva, the initiative looks at three pillars: wealth, work and wellbeing. “Most people leave it too late to plan for retirement,” he says. “But if you sit someone down at 47 and show them their pension position, explain the lifestyle changes they might face, and give them 20 years to make adjustments, that’s transformational.”

“Every developed country has already moved, or is moving, to DC”

The MOT also tackles retention challenges. “Companies were losing middle managers who wanted early retirement. By offering financial planning, health checks, and retraining opportunities, businesses kept critical experience while employees gained a pathway to stay engaged on their own terms.”

The health aspect is particularly powerful. “We used to say: we’re all going to die, but don’t die of negligence. A 10-minute cancer screening at work can save lives and cut healthcare costs. Combine that with flexible working and reskilling, and you’ve got a workforce that stays productive into their 60s and 70s.”

This ties directly into his current work with Smart Pensions, a UK-based firm that runs a multi-employer retirement savings platform and oversees one of the country’s largest master trusts, with more than £5bn under management.

“Smart operates a two-stage business,” he explains. “In the UK, they run workplace pensions. But their real innovation is Keystone, a fintech platform that lets countries and corporates build modern, flexible savings and retirement systems. It’s automated, integrated,

and can be adapted for local markets.”

Already live in the UK, UAE and Hong Kong, Keystone is being pitched to African and Middle Eastern markets. Opperman believes this is where the future lies. The global shift away from defined benefit (DB) pensions towards defined contribution (DC) pensions is inevitable. “DB schemes are simply unaffordable in the long run. Longevity is increasing everywhere, and that makes liabilities unquantifiable. As life expectancy rises, final salary pensions become an impossible promise to keep. Every developed country has already moved, or is moving, to DC. Africa, including South Africa, will follow.”

For Opperman, the lesson is clear: governments and corporates that act early in transitioning to DC structures – while ensuring accessibility through simple, mobilefirst solutions – will be best positioned to safeguard both retirement security and economic resilience in the decades ahead.

Lessons for South Africa

Opperman sees strong parallels between the UK’s journey and the challenges South Africa now faces. “Australia’s DC pension system has been running for over 30 years. The average retiree there has half a million dollars in private savings. Compare that to South Africa, where too many people still retire with little more than the state safety net, and you can see why the transition to DC is so important.” He also highlights the corporate opportunity. “Employee benefits are no longer just about pensions. Younger workers may want help with housing deposits, cars or education savings. If companies can build flexible savings products into their benefit offering, it’s a win for retention and a win for employees’ long-term security.”

Looking ahead, Opperman is confident. “The world is moving to DC without a shadow of a doubt,” he says. “The state and corporates can’t carry the burden forever. Individuals must take more responsibility for their financial future, but they need the right tools. That means mobile-first, simple, and adaptable platforms.”

Whether through corporate innovation, government regulation or fintech partnerships, the path is clear. As Opperman puts it: “Inclusion and retirement aren’t two separate agendas, they’re one. If you get it right at midlife, you change the outcomes for millions in later life.”

Empowering investor success through advice

By Sandy Welch Editor, MoneyMarketing

Financial advisers are often misunderstood. To many, their role is reduced to picking funds or timing markets. But for Mark Sanderson, managing director of Morningstar in EMEA, the true essence of advice is far deeper.

“An adviser is often 90% psychologist and 10% planner,” he says. “It’s about helping people make better choices, set goals, stick to them, and not panic when markets get volatile. That fundamental role of support and coaching is the same everywhere – no matter the country.”

Morningstar, which spans investment management, platforms and advice software, has built its business around supporting advisers – from large banking groups to small independent practices. Sanderson is a firm believer in getting out of the boardroom and spending time with advisers in their own environments. “It’s easy to guess what advisers need. But you don’t have to guess because you sit with people, and they will tell you. Our job

is to solve problems, not to create products in search of a problem.”

That focus on problem-solving has practical impact. He recalls speaking to a young adviser whose biggest challenge was not being able to put her children to bed at night. “That’s a time problem. If we can take away the inefficiencies in her day – all the swivel-chairing, the endless rekeying of data – we can give her that time back. And that’s just as much a part of our mission as building world-class models or platforms.”

How do you solve a problem like South Africa?

South Africa presents unique regulatory and economic challenges – from tax complexity to grey-listing concerns. However, Sanderson still feels there is reason for optimism here. “When you consider what this country has been through, you can’t ignore the progress. South Africans have a fundamental confidence in their country, in the community of people, to navigate and

“Our mission is simple – to empower investor success”

achieve difficult things. You only need to look at the Springboks to know that, right?”

He says that although sometimes it feels like one step back and two steps forward, as long as we’re moving in the right direction, that’s what matters. “Household wealth is higher than it’s ever been, and fewer people live in poverty than ever before – those are good stories we need to recognise.”

Sanderson notes that the similarities across markets are more striking than the differences. “Investors everywhere want the same things: to support their families and retire comfortably. Household wealth is higher than ever, demand for advice is rising, but supply isn’t keeping pace. Succession is a challenge globally; I would say one of the top two or three issues facing advisers in Australia, UK, US and South Africa. We need to make financial planning attractive to younger generations – to show them it can be a noble profession – valuesdriven as well as commercial.”

That values-driven focus is one reason Morningstar invests in financial literacy initiatives, piloting programmes in schools and communities. “Once you start teaching young people about money, you quickly realise teachers and parents also want to learn. The advice community can play a huge role here,” Sanderson says.

Why advice is important right now

In an era of geopolitical uncertainty and volatile markets, advisers play a critical role in keeping clients calm and invested. “While every generation thinks their situation is unique, uncertainty isn’t new,” Sanderson points out. “Wars, politics, volatility – they’ve always been with us. The only certainty is that uncertainty will persist. That’s exactly when advisers are most valuable: helping clients stay the course when panic could lead to crystallising losses. The pilot gets paid when there’s ice on the wings, not when it’s smooth flying.”

He praises the South African advisory community for remaining extremely strong, and being a beacon. “They are kind of like a lighthouse,” he says.

At the heart of Morningstar’s philosophy is independence. “We’re not here to push products. Our mission is simple: to empower investor success. That means being on the same side of the table as the adviser and their client, connecting the industry, and raising standards together. South Africa’s advice community is remarkably resilient and collaborative, and that gives me huge optimism for the future.”

Mark Sanderson

Goodbye JIBAR, hello ZIRONIA

South Africa’s financial markets are entering a new era. The Johannesburg Interbank Average Rate (JIBAR), long the anchor of domestic funding and lending, will soon be replaced by the South African Rand Overnight Index Average (ZARONIA). This transition is reshaping how interest rates are priced, aiming for greater transparency, reliability, and alignment with global best practice.

Historically, JIBAR has been central to loan agreements, preference shares, bonds, and structured products. However, given that it is based on indicative quotes from banks rather than actual trades, it no longer meets international standards for robust benchmarks. By contrast, ZARONIA is calculated from actual overnight unsecured interbank lending transactions, providing a more transparent, transaction-based measure.

The South African Reserve Bank (SARB) first published ZARONIA on 2 November 2022, and since then, the Market Practitioners Group (MPG) has mapped out a detailed transition plan. Milestones include the launch of the ‘ZARONIA First’ initiative for derivatives in April 2025, the introduction of fallback methodologies for JIBAR-linked contracts in both cash and derivatives markets, and legal amendments to address so-called ‘tough legacy’ contracts.

The transition will unfold in phases. A formal announcement of JIBAR’s cessation is expected in December 2025, followed by an active transition period in 2026. After a directive of ‘no new JIBAR transactions’ comes into force, JIBAR will be discontinued, with the cessation expected by December 2026. This will ensure that institutions have time to renegotiate contracts, update treasury and risk systems, and adapt hedging strategies.

A critical issue is contract fallback. In March 2025, the MPG confirmed that JIBAR fallback rates will be based on compounded ZARONIA plus a credit adjustment spread (CAS), mirroring global ISDA conventions. Without such provisions, contracts could face pricing uncertainty once JIBAR disappears. Legislative amendments are also being prepared to safeguard contracts lacking adequate fallback language.

The shift is more than regulatory housekeeping – it affects corporate funding costs, covenant calculations, refinancing terms, and capital strategies. Institutions that move early by adopting ZARONIAlinked instruments and restructuring exposures will reduce uncertainty and gain an advantage as liquidity deepens in the new benchmark.

The fall of JIBAR and rise of ZARONIA is a defining shift in South Africa’s financial architecture – it’s not only the end of an era, but also the beginning of a more transparent, resilient, and internationally consistent future.

By Zamani Ngidi Business Unit Manager for M&A and Cyber Solutions at Aon South Africa

GNavigating buy-side success in a shifting M&A landscape

lobal mergers and acquisitions (M&A) activity is regaining momentum, driven by pent-up demand and the reallocation of sidelined capital. However, while deal flows are accelerating, buyers face an increasingly complex environment where success depends on deep preparation, strategic clarity and adaptability.

The 2025 Deal Market View report surveyed senior executives from corporate development teams and private equity firms involved in buy-side transactions, comprising 40% of respondents from EMEA and 60% from North America. The report found that: 100% of respondents view due diligence as extremely important for M&A success

56% of respondents prioritise longterm strategic goals in exit planning, especially corporates (69%)

56% of respondents expect near-term valuation increases, with 24% anticipating significant rises

48% foresee widening gaps between buyer and seller valuation expectations.

Key factors shaping today’s M&A market

The dynamics of the buy-side environment are being reshaped by a combination of financial, competitive and strategic forces. Understanding these drivers is essential for buyers seeking to identify opportunities, manage risks and position themselves for success in a crowded market. Among the most significant factors influencing dealmaking today are:

1. Pent-up demand and sidelined capital

Delayed transactions from recent years are now materialising, while significant amounts of uncommitted capital are being deployed. This surge is fuelling stronger deal flows across global markets.

2. Increased deal complexity

Heightened scrutiny around due diligence, consideration of long-term exit strategies, and widening valuation gaps are making buy-side processes more intricate and demanding.

3. Rising valuations

With expectations that valuations will continue to rise, a disconnect is emerging between buyer and seller pricing, complicating negotiations and deal closures.

4. Competitive environment

Private equity firms are entering the market with record levels of dry powder, intensifying competition with corporates for high-quality assets.

Strategic alignment

More than ever, buyers are prioritising acquisitions that fit seamlessly into their long-term strategic objectives to secure sustainable value creation and competitive advantage.

Strategies for a competitive edge

While the challenges are clear, so too are the opportunities for those who take a disciplined and forward-looking approach. To succeed in this competitive and fastmoving market, buyers must go beyond transactional thinking and adopt strategies that emphasise long-term value creation, risk management and strategic fit. Proven approaches include:

In-depth due diligence

Comprehensive analysis of operational, compliance, ESG and supply chain risks ensures that buyers avoid overpaying while strengthening their negotiation and postmerger integration positions.

• Focus on strategic fit

Evaluating whether a target aligns with long-term strategic objectives helps ensure the sustainability and resilience of the investment.

• Managing valuation gaps

Creative mechanisms such as purchase price agreements are being used to bridge differences in buyer and seller expectations while reflecting real market conditions.

• Strategic reviews

Corporates are increasingly conducting strategic reviews to clarify and communicate their long-term goals, improving confidence among stakeholders and positioning themselves more strongly in deal negotiations.

• Market monitoring

PE firms and corporates alike are closely tracking financial projections and industry trends to optimise deal timing, maximise valuations and enhance exit strategies.

Today’s buy-side M&A landscape is defined by both opportunity and complexity. While competition, valuations and shifting market dynamics pose challenges, buyers who embrace disciplined due diligence, strategic alignment and innovative deal structures are better positioned to achieve successful, value-creating outcomes. In this fast-moving environment, preparation and foresight are the keys to securing a competitive edge.

Bridging the generational divide in financial advice

Speaking at the recent Glacier IdeasLab 2025, Rudolph Geldenhuys, CFP®: Director & Financial Planner at Firecrest Group, and 2024/2025 South African Financial Planner of the Year, spoke on the importance of bridging generations when it comes to the financial advisory industry. Here are some of his key takeouts.

In every financial planning practice, there are two worlds that often seem at odds: the experienced planners who built their businesses with discipline, professionalism, and structure, and the next generation of planners who favour flexibility, mobility and a more casual approach to client engagement. It’s a divide that runs deeper than wardrobe choices or office setups. It touches on philosophy, professionalism, client expectations and even what “work” looks like. One seasoned financial adviser recently vented his frustration after observing his younger colleague at work: “These youngsters just want to sit in coffee shops all day and call it work.” Behind the humour was a serious concern, about professionalism, client confidentiality and what it takes to earn trust. For decades, financial advisers built credibility through in-person meetings, paper-based reports and the quiet rituals of office life. That legacy deserves respect.

“It requires genuine collaboration across generations of advisers within a practice”

But the younger adviser wasn’t wrong either. Flexible work environments, smartphones, instant communication, and digital-first tools aren’t signs of laziness; they’re signs of evolution. Clients increasingly expect ondemand updates, quick responses and advice delivered through the same channels they use daily, whether that’s WhatsApp, Zoom, or an app notification. To younger planners, sitting in a coffee shop with a laptop and client dashboard isn’t casual – it’s efficient.

Tradition

vs innovation

This is where the tension lies. The experienced generation often sees younger advisers as lacking the gravitas that financial planning requires. The younger generation sees established advisers as slow to adapt, overly

rigid, and resistant to tools that could free up time for more meaningful client work.

Neither is completely right or completely wrong. The truth is that both generations are looking at the same profession through different lenses. The older adviser risks clinging too tightly to tradition; the younger one risks the assumption that technology can replace wisdom. Both have blind spots, but both also bring invaluable strengths.

The client’s perspective

For clients, what matters most hasn’t changed: trust, reliability, and the confidence that their adviser understands them. But how that trust is built has shifted. A Baby Boomer client may still prefer to sit across the table with a leather-bound report. A Millennial client might feel more at ease reviewing a portfolio summary on their phone while commuting. Gen Z clients, entering the workforce now, may expect financial advice to feel as seamless as ordering food through an app.

The challenge for advisers is to serve all these preferences without compromising the integrity of their advice. That requires more than tolerance – it requires genuine collaboration across generations of advisers within a practice.

Where generations meet

The art of financial planning – the empathy, listening, and human connection – remains timeless. The science of financial planning, which includes analytics, compliance, and technology, continues to evolve rapidly. The real opportunity lies in blending these two dimensions.

Imagine a practice where the experienced adviser mentors on the nuances of client relationships, ethical dilemmas and longterm strategy, while the younger adviser drives efficiency with digital tools, automated workflows and fresh marketing ideas. One ensures the advice is wise; the other ensures it is relevant. Together, they provide continuity that reassures clients their financial wellbeing will outlast market cycles, leadership transitions, and even generational shifts.

From succession to legacy

Many practices talk about succession planning as a handover of business. But the generational divide highlights something more important: legacy. A firm that cannot bridge internal generational gaps will struggle

Questions to ask your team

Do we serve clients in the ways they prefer – or only in the ways in which we are comfortable?

• How are we preparing to retain the next generation of our clients’ families?

• Where could we save time with technology, and where is the human touch non-negotiable?

• Younger advisers: Digital fluency, accessibility, fresh ideas, new ways to connect with younger clients.

• Together: A blend of wisdom and relevance that builds continuity across generations.

Bridging the divide –three practical steps

1. Mentorship circles: Pair experienced advisers with younger team members for two-way learning.

2. Client segmentation: Match clients with advisers based on preference –traditional or digital-first.

3. Technology with training: Don’t just adopt tools – ensure all generations in the practice are comfortable using them.

to retain client families across generations. Conversely, a firm that integrates the strengths of both experienced and nextgeneration advisers positions itself not just to survive, but to grow.

Ultimately, financial planning is not about transactions, it’s about transformation. It is about guiding families through life’s most difficult choices, across decades. To achieve that, advisers must first cross the generational divide within their own ranks. When they do, the reward is more than business continuity. It is the ability to offer clients a partnership that feels both timeless and forward-looking, a rare balance in a world where change is the only constant.

By Francois du Toit CFP® PROpulsion

Business first, technology second

Most financial advisory practices operate like three separate businesses under one roof. They have a financial planning process, a client engagement process, and various technology tools – but these elements rarely work together. This creates inefficiency, compliance risks, and missed opportunities that competitors are starting to exploit.

Here is the secret: when you properly align your planning process, client engagement model, and technology stack, you create a competitive advantage that becomes very difficult for others to match.

The problem hidden in plain sight

Many South African advisory practices struggle with alignment because they start from the wrong place. They see a flashy new CRM system or AI tool, get excited about its features, and make the purchase. Only later do they realise the technology does not fit their actual business processes or client needs.

This backwards approach explains why so many technology implementations fail. The practice has invested significant money and time into systems that end up being used as expensive digital filing cabinets.

The root issue is not knowing what problems you are trying to solve. Before looking at any technology, you need clarity on your current challenges:

• Where do clients get frustrated with your process?

• What manual tasks eat up your advisers’ time?

• Which compliance requirements create bottlenecks?

Without this clarity, you will be overwhelmed by options and make decisions based on features rather than fit.

Why alignment matters more than ever

The Financial Sector Conduct Authority has moved beyond tick-box compliance to focus on fair client outcomes. The upcoming Conduct of Financial Institutions Bill will require practices to show consistent, defensible advice processes across all client interactions. Manual, paper-based systems that rely on individual adviser discipline will not meet these expectations.

Regulators increasingly expect systems that can provide comprehensive audit trails and show they have quality control.

Technology and artificial intelligence have become the only equaliser in this environment, as Anton Swanepoel of Trusted Advisors shared with me, and I cannot agree more.

Smaller practices can now compete with larger firms by using technology to automate compliance checks, streamline workflows, and deliver consistent service quality.

The aligned practice advantage

When your three core elements work together, you create what industry experts call a ‘high tech, high touch’ model. Here is how it works. Your financial planning process defines the structure:

• The six-step framework ensures thorough, compliant advice

• Your client engagement model brings this process to life through meaningful conversations and trustbuilding activities

• Your technology enables both by automating administrative tasks and providing the data insights needed for personalised service.

The magic happens when all three work together. Client information entered once flows automatically through your CRM to your financial planning software to your client reporting tools. This eliminates doublehandling, reduces errors, and creates capacity for higher-value activities.

More importantly, this creates a feedback loop. Your technology captures rich data about client interactions and outcomes. This data helps you refine your processes and identify new service opportunities. Your improved processes generate better client engagement, which produces even richer data.

Others using isolated systems cannot match this level of efficiency and insight.

Overcoming implementation barriers

The biggest barriers to alignment are not technical, but psychological and strategic. Many use their age

or perceived technology limitations as excuses for avoiding necessary changes. Others claim they lack time or resources to implement new systems.

These excuses miss a fundamental truth: the cost of not changing far exceeds the investment required for alignment. Practices that continue with manual, disconnected processes will find themselves unable to compete on service quality, efficiency, or compliance standards.

“The biggest barriers to alignment are not technical, they are psychological and strategic”

The solution is a phased approach. Start with establishing a robust CRM as your single source of truth. Once this foundation is solid, add your core planning tools. Then add clientfacing technology like secure portals. Finally, experiment with AI tools to boost your capabilities. Each phase builds on the previous one, creating sustainable progress without overwhelming your team or budget.

Bonus tip: Speak to your existing providers, present the problem you want to solve or process you want to implement, and ask them to show you how they do it. In most cases, your existing system can already do what you need.

My final thoughts

Alignment is about creating systematic competitive advantages. When your planning process, engagement model, and technology work together seamlessly, you free up time for the high-value human interactions that build lasting client relationships.

The question is not whether you need alignment, but how quickly you can achieve it before your competitors do.

Stay curious!

By Boland Lithebe Security Lead for Accenture, Africa

AFour essential actions to safeguard AI adoption in South Africa

rtificial intelligence has become one of the most transformative forces shaping business today. From banks rolling out AI-driven fraud detection, to retailers using algorithms for personalised recommendations, and hospitals adopting diagnostic tools, AI is now woven into the fabric of South Africa’s economy. But with these gains come new risks. The same systems that promise efficiency and innovation also open doors to cyber threats, model manipulation, and data breaches. For South African businesses, securing AI is not only about safeguarding operations, but also about protecting customer trust, meeting regulatory requirements, and ensuring competitiveness in an increasingly digital economy. Four actions stand out as critical for organisations looking to build confidence in AI while mitigating its risks.

1

Build trust through security and governance

The first action is to develop and deploy a fitfor-purpose security governance framework and operating model that accounts for the realities of an AI-disrupted world. Too often, AI adoption in South Africa is happening faster than the frameworks designed to govern it. While regulations such as the Protection of Personal Information Act (POPIA) set guardrails around data usage, they were not built with generative AI and large-scale machine learning in mind. A modern governance model must bridge this gap, establishing clear accountability across boards, executives, and technology leaders. For instance, if an AI credit-scoring model unintentionally discriminates or is manipulated, who is responsible – the CIO, the data science team, or the board? Defining these lines of accountability ensures risks are not overlooked. Governance should also align AI security with business objectives, recognising that secure, trustworthy AI is not only a compliance issue but also a competitive differentiator. In South Africa’s highly regulated industries like financial services and healthcare, organisations that can demonstrate strong AI governance will build trust faster with customers, regulators, and investors alike.

2 Embed security in development and deployment

The second action is to design a digital core that is generative AI secure from the onset by embedding protection into AI development, deployment, and operational processes. Many South African companies are eager to experiment with generative AI tools to drive efficiency, whether for customer service

chatbots, content generation, or supply chain optimisation. But adopting these technologies without embedding security upfront is risky. Consider a retailer using a generative AI model to interact with customers online – if that model is not secured, it can be manipulated through prompt injection attacks, leading to reputational damage or even fraudulent transactions.

By embedding security into development and deployment from the beginning, businesses can avoid costly retrofits. Secure coding practices, adversarial testing, data validation, and strong identity access controls must be treated as standard. South African organisations building digital cores should also focus on interoperability, ensuring that AI systems integrate securely with legacy infrastructure. This approach not only reduces vulnerabilities but also allows businesses to innovate with confidence, knowing that their AI is designed for resilience rather than patched as an afterthought.

3 Counter emerging threats

The third action is to maintain resilient AI systems with secure foundations that proactively address emerging threats. AI environments are dynamic, and so too are the risks. A model trained today can be vulnerable tomorrow as attackers find new ways to exploit it. South Africa has already seen an uptick in cyberattacks targeting critical infrastructure and the financial sector. Adding AI into the mix multiplies the threat landscape. To counter this, businesses must enhance detection capabilities, enable robust model testing, and improve response mechanisms.

Continuous monitoring is key – systems must be able to detect anomalies in both inputs and outputs, such as attempts to feed poisoned data into training sets or unusual behaviour in live models. Beyond monitoring, response mechanisms must be agile. A static security approach will not keep pace with evolving AI threats. Instead, South African businesses need to invest in AI-specific incident response playbooks, red-teaming exercises, and resilience testing to ensure they can recover quickly when incidents occur. Building resilience also means planning for systemic risk: if one AI system fails or is compromised, there should be contingency measures in place to keep core business functions running.

4 Use AI to protect AI

The fourth action is to reinvent cybersecurity with generative AI by leveraging it to automate security processes, strengthen

defences, and detect threats sooner. This is where AI becomes both the problem and the solution. While generative AI introduces risks, it also offers powerful tools to combat them. In South Africa, where cybersecurity skills are in short supply, generative AI can help close the gap by automating routine security tasks such as log analysis, anomaly detection, and threat hunting. This frees up skilled professionals to focus on higher-value activities like strategy and response.

Generative AI can also improve threat intelligence, parsing vast amounts of data from across industries to identify emerging risks before they impact businesses. For example, local banks could use AI-driven monitoring systems to identify fraudulent patterns across multiple payment networks in real time, while telecoms could deploy AI to detect anomalies in traffic that might indicate a breach. By adopting generative AI defensively, South African businesses can build cyber resilience while easing the burden on overstretched teams.

A clear way forward

Taken together, these four actions provide a roadmap for South African organisations navigating the complex intersection of AI and cybersecurity. Governance frameworks ensure accountability and alignment with local regulatory realities. Secure digital cores embed resilience from the ground up, avoiding costly fixes down the line. Resilient AI systems keep pace with evolving threats through continuous monitoring and agile responses. And generative AI, used wisely, strengthens defences in a market facing both growing cyber threats and a shortage of skilled security professionals. For South African business leaders, the urgency is clear. AI adoption will only accelerate, with the potential to transform industries from mining to healthcare. But without robust security, the risks could undermine both trust and progress. By acting now, organisations can position themselves not just as adopters of AI, but as leaders in secure, responsible, and innovative AI deployment. In doing so, they protect not only their own operations but also contribute to a safer and more competitive digital economy for the country.

How atWORK empowers advisers in a tech-driven world

Technology has quietly but fundamentally reshaped the way financial advisers operate. From sole proprietors running lean practices to large corporates with thousands of advisers, the needs are as diverse as the clients they serve. Yet, one truth remains: effective advice today cannot exist without robust, secure and integrated technology.

“Advisers are becoming increasingly dependent on software,” says Niclaas Roets, from atWORK, a company that specialises in technology solutions for the financial advice industry. “Your client data, your compliance, your reporting – all of it lives in the system. That’s why it’s critical to know whether the technology partner you choose has the security, infrastructure and expertise to support that responsibility.”

For Roets, the shift to cloud-based systems has been a game-changer. No longer burdened by firewalls and in-house infrastructure, advisers now benefit from environments safeguarded by major providers such as Microsoft Azure or AWS.

“We have to balance innovation with accessibility”

But while the technology is available, he cautions that not all advisers fully appreciate the risks: “Many advisers don’t think about cybercrime until something goes wrong. They log in, upload client documents, and trust that it’s all safe. But behind the scenes, we’re running penetration tests, monitoring security policies and making sure the data is protected. That’s the invisible part of advice tech that clients and advisers rarely see, but it’s crucial.”

At the core of this transformation lies one thing: client data. Roets describes it as the most valuable asset an adviser has. A modern CRM system not only houses personal details, but integrates reminders, workflows, campaigns, compliance records and even digital signatures into one secure space. “It’s about centralising the heartbeat of the adviser’s business,” he says. “The more seamlessly those tools work together, the more time advisers have for what really matters, which is their clients.”

As digital tools reshape the advice landscape, one of the biggest shifts underway is the

development of client-facing platforms that simplify communication and improve access to information. For atWORK, this is where Client Zone comes in.

“Client Zone is essentially a portal where advisers can allow their clients to log in, view relevant information and even exchange documents securely,” explains Roets. “It’s completely white-labelled, so from the client’s perspective, it looks and feels like their adviser’s own website. They can log in, check values, access investment statements, or upload FICA documents, all in one place.”

The platform has been designed with flexibility in mind: advisers decide exactly what their clients can and can’t see, ensuring control remains firmly in their hands. It also replaces clunky email processes, offering clients peace of mind with greater security and convenience.

Sara-Lee Prinsloo, Marketing Manager at atWORK, notes that Client Zone was developed in direct response to client demand. “Younger clients, in particular, want a more interactive relationship with their advisers. They’re less comfortable with sensitive information being sent over email. Having a secure, easy-touse portal meets that expectation while strengthening trust.”

Bridging the generational gap

Technology adoption is never a one-size-fitsall. The advice profession remains weighted towards older advisers, many of whom aren’t naturally tech-savvy. “In general, advisers tend to be conservative with tech,” says Roets. “And that makes sense because this is an industry built on trust and handling people’s money. With scams and fraud in the news, many advisers are understandably cautious.”

That’s why usability is key. atWORK has rebuilt its CRM platform with simplicity, speed, and stability at the centre. “The easier and cleaner we can make it, the more time advisers can spend where it really matters – talking to clients,” says Roets.

This dual reality – in which older advisers need straightforward solutions, while younger advisers and clients expect more digital interaction – has shaped atWORK strategy. “We have to balance innovation with accessibility,” he says.

Where AI fits in

Artificial intelligence is on everyone’s lips, but how does it really apply to advisers? atWork’s answer lies in using AI to reduce admin and surface insights. Currently, AI is being deployed on the back end to assist developers, but forward-facing applications are also being piloted. One example is the ability to drag and drop policy documents into the system and have client information automatically populated, saving hours of manual data entry.

“This is where AI can be a real game-changer,” Roets explains. “Think about the time advisers spend capturing information from different insurers or investment providers. Soon, all they’ll need to do is upload the policy, and the system will do the rest.”

AI also opens the door to more intuitive insights. Advisers could log into a client’s profile and instantly see key prompts, such as clients approaching retirement, those due for reviews, or those who may benefit from additional retirement annuity contributions. “The tech in the background is complex, but for the adviser, it should feel effortless,” says Roets. “That’s where AI is heading.”

Keeping the human touch

Despite the rise of AI and client portals, both Roets and Prinsloo emphasise that technology is not replacing advisers, it’s empowering them. “Tech should free up time for advisers to focus on what they do best: building relationships and giving personalised advice,” says Prinsloo. “atWORK is a tech company, but we’re also a human company. Adoption support, training, and after-sales service are just as important as the software itself.”

She adds: “Ultimately, clients still choose their advisers because of trust, empathy, and human understanding. Technology is there to enable that relationship, not replace it.”

After nearly three decades in business, atWORK remains clear about its mission: to empower advisers with tools that make their businesses stronger while keeping the client relationship at the centre. “Technology changes fast, but one thing hasn’t changed,” concludes Roets. “Advisers want to spend less time on admin and more time with clients. Everything we do is designed to make that possible.”

Niclaas Roets

How AI is reshaping the investment landscape

The world of investing has always been a hotspot for innovation, but the pace of change has reached unprecedented heights in recent years. From the rise of digital assets to the use of artificial intelligence (AI) in trading, the barriers that once kept everyday people from participating in the financial market are gradually lowering. In 2025, this shift has become even more clear, as innovative platforms and smarter tools are making trading more accessible, transparent and effective.

The new wave of traders In the past, trading was often associated with professionals working on busy exchange floors or institutional investors with deep pockets. For everyday individuals, the market’s complexity, high cost and limited access made it seem like a world far out of reach.

However, a different story is unfolding today. Platforms are emerging that cater to modern investors, such as people who are balancing careers, studies or family responsibilities, but still want to build wealth and understand how the market works.

For this new wave of traders, simplicity and trust matter just as much as advanced tools and insights.

The role of AI in trading

One of the biggest game changers in fintech has been artificial intelligence. AI is no longer a futuristic concept but a practical tool that allows traders to interpret news, monitor trends, and act on opportunities in real time.

For example, some platforms have integrated AI tools that scan global market news and suggest actionable trading signals. Instead of sifting through hundreds of headlines, traders can instantly see how an event might affect a currency pair, stock or commodity. This blend of speed and accuracy is giving individuals a level of insight that was once reserved for large institutions.

A platform built for modern investors

Among the platforms leading this evolution is Doto, a multi-asset broker launched in 2019. While there are many trading apps available today, Doto stands out because of its mission: “Finance for all.” The platform was created to challenge traditional brokers by offering an AI-powered, userfriendly alternative that helps traders make confident decisions.

Doto’s approach combines innovation with accessibility. Its intuitive design makes trading approachable for beginners, while its advanced features, such as AI-driven market signals, transparent pricing, and instant deposits and withdrawals, appeal to experienced traders as well.

Supported by regulations across several global jurisdictions, including Cyprus (CySEC) and South Africa (FSCA), Doto has grown to serve more than 500 000 traders worldwide. In recognition of its efforts, the platform was named Best CFD Broker of 2025 at the World Financial Award and received the title of Most Trusted Broker 2024.

What traders value most

When asked what makes a platform stand out, traders often highlight three things: trust, usability and opportunity.

Trust comes from transparency and regulation. Doto, for example, is a member of the Financial Commission (FinaCom), offering its users added protection through a compensation fund.

Usability comes from design. A cluttered interface can discourage beginners, while a clear, intuitive layout helps build confidence. Doto’s platform is designed for traders at all levels, from someone making their first deposit to a professional managing a diversified portfolio.

Opportunity comes from tools and conditions. From offering CFDs on over 250 assets (stocks, indices, commodities, currencies and crypto) to providing leverage up to 1:500, modern platforms are widening the possibilities for investors worldwide.

“Simplicity and trust matter just as much as advanced tools and insights”

Recognition and growth

Doto’s journey over the past six years reflects the broader evolution of trading. What started as a newcomer in 2019 has grown into a globally recognised broker with multilingual support, localised payment options, and a strong presence in regions like the Middle East, Asia and Latin America. Its achievements at international events, including Best Newcomer Broker MEA 2024 at iFX EXPO Dubai, highlight how platforms can make a real impact by putting people first. Awards aside, its biggest success has been building trust with its global community of traders who want financial tools that work with them, not against them.

Looking ahead

As the market continues to evolve, one thing is clear: Trading is no longer just for the elite. With AI, mobile apps and simplified platforms, the new generation of traders are already looking very different from those in the past. They’re younger, more diverse and more empowered to make decisions.

Platforms like Doto exemplify this trend. By combining technology, regulation and a user-first philosophy, they are not only making trading accessible but also reshaping what financial opportunity looks like in 2025 and beyond.

In a world where financial literacy and independence are becoming increasingly important, tools that simplify complex systems will continue to play a vital role. For the everyday trader, this means one thing: The door to the global market has never been more open.

By Veronica Lukwago Associate Director: Finance Transformation, BDO SA

Enterprise Resource Planning (ERP) implementation represents far more than a technology upgrade; it’s a strategic transformation that can fundamentally reshape how organisations leverage data for profitability and growth. Having guided numerous South African businesses through this journey, I’ve seen firsthand how the right approach to ERP can turn careful planning into measurable profit. The most successful ERP implementations begin by focusing on three critical finance areas that deliver immediate value:

• Treasury Operations become streamlined through automated cash management and real-time visibility into cashflows, enabling better liquidity management and risk control.

• Budget Planning and Forecasting transforms from manual spreadsheet exercises into centralised, automated workflows that improve accuracy and accelerate planning cycles.

• Financial Reporting and Consolidation provides a single source of truth across departments, eliminating the time-consuming reconciliation processes that plague many organisations.

Turning ERP investment into business value: A strategic approach BDO Advisory Services

These foundational improvements replace fragmented, error-prone manual processes with integrated workflows. Instead of relying on static monthly reports, managers gain access to real-time data that supports agile decision-making and strategic focus. Once core processes are automated, the real value emerges through advanced analytics and AI capabilities. Modern ERP systems don’t just centralise data, they transform it into actionable insights that drive profitability.

With integrated analytics, organisations can identify underperforming products or departments while doubling down on profit drivers. AI-enhanced scenario planning capabilities enable ‘what if’ analysis based on data rather than intuition, supporting more robust strategic planning. This analytical layer represents ERP’s true competitive advantage. Organisations applying AI tools to their ERP data are already seeing enhanced profitability through predictive insights into cashflow, market demand, and operational efficiency. While finance often leads ERP initiatives, the greatest value comes from enterprise-wide adoption. Modern ERP systems break down data silos across

procurement, supply chain, HR and sales, creating organisational alignment around a single source of truth. This integration proves particularly valuable during complex business activities like mergers and acquisitions, where disparate data sources can complicate decision-making. A well-implemented ERP provides the real-time, consolidated information essential for successful integration. The most common concern I encounter involves legacy system integration. Here’s how to approach this challenge strategically:

• Plan for complexity: Legacy systems with years of customisation require careful mapping and adjustment. Even cloud solutions marketed as plugand-play demand thoughtful integration planning. Set realistic timelines and budgets while working with experienced integration specialists.

• Implement incrementally: Rather than attempting a ‘big bang’ approach, identify the module or process offering the highest ROI and begin there. Phased implementation reduces risk, enables learning, and builds organisational confidence before expanding to other functions.

Successful ERP implementation requires treating the initiative as a business transformation rather than an IT project. By starting with core finance functions, layering on analytics capabilities, and expanding enterprise-wide adoption, organisations create a foundation for sustained competitive advantage.

At BDO South Africa, we don’t just advise, we elevate. With a global footprint across 166 countries and deep local expertise, our advisory services are designed to help businesses navigate complexity, unlock growth, and future-proof operations.

Whether you’re facing strategic, financial, operational, or digital challenges, our multidisciplinary teams deliver innovative, ethical, and sustainable solutions tailored to your needs. We are bold, collaborative, and driven to be the best, because your success is our purpose. Ready to Elevate Your Business?

Explore our full service offering or visit www.bdo.co.za

By Jaco-Chris Koorts Portfolio Manager, Glacier Invest

PHow Discretionary Fund Manager partnerships transform advisory practices

artnering with a discretionary fund manager (DFM) has long been viewed as a strategic move for advisers looking to outsource portfolio construction, their investment-related compliance burden, and access deep investment research. However, increasingly advisers are discovering that the benefits run far deeper than fund selection or absorbing regulatory burdens. A wellchosen DFM partner not only optimises clients’ portfolios, but it also frees the adviser to focus on what really matters: providing holistic financial advice, deepening client relationships, and elevating your value proposition in a dynamic market environment.

Reclaiming the heart of advice

By lifting the weight of portfolio oversight, a DFM allows advisers to reclaim their time, focus and control – not just over investment outcomes, but over their core value proposition. Imagine channelling hours once lost to fund research and rebalancing into transformative client relationships. With conversations of investment management streamlined, advisers can shift toward life-centred discussions such as financial wellbeing, legacy and goals. This builds stronger relationships, drives engagement, and helps clients see the bigger picture. Advisers can thus sharpen their focus on holistic advice.

Silencing the compliance noise

South Africa’s regulatory landscape demands meticulous documentation that can drown advisers in paperwork. Advisers face increasing regulatory demands around investment suitability, portfolio construction, and ongoing governance. Meeting these compliance requirements requires significant time, resources, and robust governance frameworks. Herein lies a profound DFM benefit: a DFM can absorb the day-to-day portfolio oversight, monitoring and identifying compliance breaches more quickly, and then adjust portfolios timeously. They ensure Regulation 28 adherence, maintain auditable rebalancing trails, and document best-execution practices using verified research tools. By acting as your institutional-grade safeguard, DFMs mitigate regulatory risk while you concentrate on pure advisory work – turning investment compliance from a threat into a managed function. The operational efficiencies gained by utilising a DFM, such as rebalancing all clients linked to a specific model portfolio at the same time, also means your practice runs like a well-oiled machine.

The scalability imperative

“A DFM can create the space for advisers to evolve as business owners”

Advisers can expand into untapped client segments, such as the next generation of wealth, small business owners, or even underserved demographics, without diluting the quality of advice given. They can also develop scalable advice models using digital tools or hybrid solutions to service the wider client base. Reduced investment admin means more time to work on their practice, not just in it. Whether it’s refining the client proposition, mentoring junior advisers, or improving internal processes, a DFM can create the space for advisers to evolve as business owners. DFMs handle the mechanics of portfolio management – from asset allocation to tactical shifts – freeing the adviser to focus on deeper client relationships and business growth. This is where true adviser value lives: not in spreadsheets, but in the trusted human connection that clients cannot replicate via algorithms or online platforms.

As advisory practices grow, in-house portfolio management can quickly reach a breaking point. What may begin as a cost-effective and controlled approach often becomes weighed down by hidden or escalating costs – salaries for analysts, premium data terminals, and proprietary software – creating unsustainable fixed expenses. These costs have the potential to erode profitability and make it harder to scale sustainably. Moreover, the risk of staff turnover introduces a real vulnerability: a key member leaves during a critical market cycle, disrupting client portfolios and compromising client outcomes. Most crucially, capacity constraints emerge as more time must be spent on portfolio oversight. Contrast this with an outsourced DFM solution where all these risks are mitigated, and the high fixed costs are exchanged for a variable cost linked to AUM. This model transforms scalability from a logistical challenge into a strategic accelerator, granting immediate access to local and global research and execution capabilities.

Redefining client perception

In today’s market, clients seek advisers who act as strategic architects – not product salespeople. Industry research indicates that clients perceive DFM-backed advisers as

significantly more credible for complex wealth management. This partnership elevates your proposition profoundly: you become the conductor orchestrating specialists, rather than trying to play every instrument yourself. By entering into a strategic partnership with a DFM, you gain the ability to offer world-class investment strategies through cutting-edge research, access to alternative investments, and dynamic asset allocations – democratising solutions once exclusive to the ultra-wealthy. Your clients now view you as their lifelong wealth strategist, not a transactional vendor.

Choosing your strategic ally

Selecting the right DFM demands careful consideration of philosophical alignment and operational fit. Choose a partner whose investment approach mirrors yours – whether that’s active alpha generation or low-cost passive blends, or a combination of the two. Demand absolute fee transparency, including both management fees and underlying costs, and insist on clear and efficient operational processes and reporting standards. Crucially, verify their local expertise: Can they articulate how South African realities influence portfolio decisions, and how this scales up into a globally relevant portfolio? Finally, assess customisation depth: Ensure they can accommodate client-specific exclusions without compromising the servicing and investment model’s integrity. As Solutions Architects, Glacier Invest ticks all these boxes.

The strategic horizon

For South Africa’s financial advisers, the DFM partnership represents far more than operational relief. It’s a fundamental repositioning – from a potentially overwhelmed portfolio administrator to an empowered wealth visionary. By delegating investment execution, you reclaim your highest-value role: understanding your clients’ deepest financial aspirations and guiding them with behavioural wisdom. In an era of relentless complexity, integrating a DFM into your advisory practice is becoming essential to sustainable growth. The most successful future practices will leverage these partnerships to redefine the very essence of trusted advice in our uniquely challenging market.

DFMs are moving the SA advice industry forward

By Sandy Welch Editor, MoneyMarketing

The role of Discretionary Fund Managers (DFMs) in South Africa has changed dramatically over the past decade, shaped largely by regulatory developments and the need for greater professionalism in investment management.