South Bay's Neighbor

OCTOBER HAPPENINGS

WEDNESDAY, OCT. 15th

7:00PM-9:00PM

THE DEVIL IN NEW YORKTHE WITCHCRAFT TRIAL OF GOODY GARLICK

The Historical Society of Islip Hamlet will host Tara Rider and her presentation "The Devil in New York - The Witchcraft Trial of Goody Garlick". The program will be held at the Islip Public Library, 71 Monell Ave. Free and open to the public. For more information on this, their 2026 Holiday House Tour or to become a member, visit www. isliphamlethistory.org, or call 631559-2915

FRIDAY, OCT. 17th

SATURDAY, OCT. 18th

6:00PM-9:00PM

SPOOKTACTULAR

Enjoy eerie animal presentations, a ghostly graveyard, creepy games, scary music, and spooky night trails. Great for ghouls 7 years and up. Food Truck refreshments available for purchase! 10/17 Box Car Burgers, 10/18 Krazy Knish. Sweetbriar Nature Center - ECSS, 62 Eckernkamp Drive in Smithtown. For more information, please call 631-979-6344

SATURDAY, OCT. 18th

9:00AM-5:00PM

PARROT EXPO

Sayville VFW POST 433 400 Lakeland Avenue in Sayville. Long Island’s only major exotic bird event boasts a full day of shopping, raffles, fun and education for pet bird lovers! For more information, please call 631-957-1100

HOLIDAYS

13th - COLUMBUS DAY

INDIGENOUS PEOPLES' DAY 31st - HALLOWEEN

MAKE A SUBMISSION! Events must be submitted at least two weeks prior to the event date and will run free of charge on a space available basis. For more information, please call 631.226.2636 x275 or send events to editorial@longislandmediagroup.com

10:00AM-3:00PM

ST. PATRICK’S CHURCH

THRIFT SHOP / YARD SALE

(Rain or Shine) Thrift Shop Special Event “Pack A Bag” ($5.00) many new items in all categories, Rent A Table - $25.00. 305 Carll’s Path in Deer Park. For more information, please call 631-242-7530

10:00AM-4:00PM

HARVEST CRAFT FESTIVAL & YARD SALE

Our Redeemer Lutheran Church, 2025 Washington Avenue in Seaford. Local craft vendors, Congregational Yard Sale, pumpkin patch, painting, mums for sale, raffles, music & much more. For more information, please call 516-781-6374, office@ ourredeemerlutheran.church

10:00AM-8:00PM

BLESSING OF THE ANIMALS

All are welcome! Grace United Methodist Church, 515 S. Wellwood Ave. in Lindenhurst. For more information, please call 631-2268690, gumc.lindy@gmail.com

2:00PM

HALLOWEEN FAMILY FUN DAY

The annual Halloween Family Fun Day held in Lindenshurst features face painting, games, hay rides, pony rides, hot cocoa and more. This event is co-chaired by the Village of Lindenhurst, Mayor's Beautification Society, Rotary Club of Lindenhurst, Lindenhurst Fire Department, and the Lindenhurst Moose Club. Rain date: October 19. For more information, please call 631-957-7500

7:00PM-11:00PM

HARVEST MOON DANCE

The Knights of Columbus #11968 will be holding a Harvest Moon Dance at Our Lady of Grace Church, Father Shanahan Hall located at 666 Albin Ave. in West Babylon. For more information, please call Rob 631-7470147 or Dave 631- 357-0188.

SUNDAY, OCT. 19th

1:00PM-5:00PM

WADE BURNS VFW 7279

PSYCHIC ENLIGHTENING

Admission: $55.00 includes Psychic Christopher Allen, light lunch, beer, wine, soda and cake. Wade Burns VFW 7279 560N. Delaware Ave. in Lindenhurst. For more information, please contact 631-965- 6459

FRIDAY, OCT. 24th

DOORS OPEN 6:00PM BINGO STARTS 7:00PM WEST ISLIP FIRE DEPT LADIES AUX MUSIC BINGO FUND RAISER

West Islip Fire Dept. 309 Union Blvd West in Islip. Tickets $20 extra cards for sale, 50/50, Lotto board. Raffle baskets. for more information and for tickets, please call 516-318-530. Light food for purchase. Donate a non perishable item for a ticket to a special raffle

6:30PM-8:00PM

HAUNTED HIKES

Garden City Bird Sanctuary, 182 Tanners Pond Rd. in Garden City. Long Islands favorite family Haunted Hike is back. With both Scary and not so scary walks (on separate trails) a maze and some fun photo opportunities. For more information, please visit https:// thegcbs.org/gcbs-home

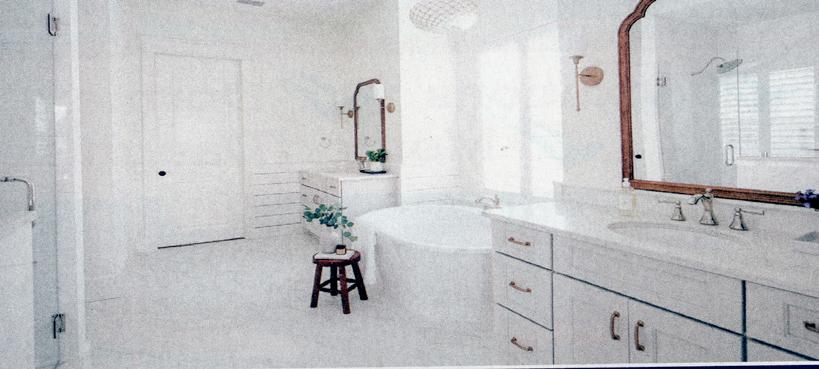

How To Boost Home Value Before Selling

People considering buying or selling a home are facing a unique market. The real estate market has been in flux for several years, and high interest rates have made it more expensive to borrow.

The Mortgage Bankers Association is projecting that 30-year mortgage rates will level out to 6.5 percent for the forseeable future. That means that people who have been waiting for changes in the real estate market could be disappointed, and hesitant buyers may finally just bite the bullet and buy even if mortgage rates are not where they hoped they’d be in 2025.

Homeowners with properties they are considering listing for sale would be wise to make certain changes that will help garner the best prices from buyers. Make kitchen and bath improvements

The kitchen is the heart of many homes. Real estate agents may recommend that homeowners make minor to moderate kitchen upgrades like resurfacing cabinets,

upgrading countertops and changing fixtures or hardware to give the room an overhaul.

Homeowners also should look to bathroom updates as smart investments that can improve home value.

Katie Severance, author of The Brilliant Home Buyer, characterizes kitchens and baths as “money rooms” that add the most value to a home.

Declutter the home

Homeowners should clean out items they no longer need. Decluttering can make a space feel bigger, which is beneficial in a market where open concept floor plans remain popular among home buyers. When buyers walk through a prospective home, they want to envision themselves living there, something that is more easily done if the home isn’t overrun with the current homeowner’s belongings.

Get to painting

Painting a home is a cost-effective renovation

with a lot of oomph. Freshly painted rooms appear clean and updated, says HGTV, and that can appeal to buyers. Homeowners should choose neutral colors to accommodate the widest array of potential buyers.

Improve the landscaping

The exterior of a home is the first thing potential buyers will see as they roll up to view a property or look at a listing online. Homeowners should start by evaluating and enhancing the landscaping. Ensure the lawn is well-maintained and add plants that provide color without a lot of maintenance.

Expand usable space

Homeowners can think about adding to the usable space in a home. This translates into finishing basements or attics or even converting garages to rooms. Or it may involve adding a threeseason room.

Homeowners can consider a number of improvements to increase the resale value of their properties.

JOB OPPORTUNITY

Medical

Position Details:

We

will have a

for

with children and supporting educators in a classroom setting.

Responsibilities:

• Assist the lead teacher in implementing lesson plans and activities

• Provide support to students with various tasks and assignments

• Supervise children during indoor and outdoor activities

• Help maintain a safe and clean learning environment

Requirements:

• High School Diploma or GED

• Ability to communicate positively, effectively, and appropriately with children

• Ability to use clear and understandable written and verbal communication

• Experience working with toddlers, preschoolers, or in a classroom setting is a plus!

• Teaching Assistant - Level Certi cate a plus! Work Schedule:

Monday to Friday from 8:15am to 2:45pm (Please note certain days will require later dismissal due to necessary professional development training.)

Job Type: Full-Time

Pay: $18.50 - $21.50 per hour

Work Location: In person

For Bower Location - Call - 631-590-3144 and ask for Miriam For Kellum Location - Call - 631-884-3000 and ask for Jessica McMahon

Babylon Public Library

24 S. Carll Ave. Babylon, NY

Erin White 631.669.1624

ADULT PROGRAMS

Fall Bingo

Thursday, October 16, 2:00pm - 3:00pm

Celebrate Fall with a few rounds of Bingo! Adults only, please. Registration is required.

Chef Rob’s Pink Lady Cinnamon Scones

Saturday, October 18, 2:00pm – 3:00pm

What flavors better define fall than apples and cinnamon?

Chef Rob will help you prepare this delicious recipe to bake at home. Please bring 2 apples, a box grater, a whisk, and a large and a medium bowl to class. A non-refundable $5.00 fee is due at program registration.

Shed the Meds

Monday, October 20, 11:00am – 2:00pm

Shed the Meds sponsored by NYS Senator Alexis Weik. Bring any unwanted medication for proper disposal. No sharps or liquids, please.

Beginner Knitting

Wednesdays, October 22 & 29; November 19

6:00pm – 7:30pm

Learn how to knit in this 3-session series. Aimee Saccio will introduce you to the world of knitting while helping you create a beautiful scarf. No prior knitting experience required. A non-refundable $12.00 fee is due at registration.

Career Couture Clothing Drive

Friday, October 24 at 9:30am to Friday, October 31 at 4:00pm

Donate your gently used and cleaned business attire for people entering the workforce. Acceptable donations include: suits, blazers, slacks, skirts, dresses, blouses, shoes, and accessories. Please bring clothing on hangers. All items donated will be delivered to the Suffolk County One-

Stop Employment Center in Hauppauge.

Career Couture Clothing Drive

Friday, October 24 at 9:30am to Friday, October 31 at 4:00pm

Donate your gently used and cleaned business attire for people entering the workforce. Acceptable donations include: suits, blazers, slacks, skirts, dresses, blouses, shoes, and accessories. Please bring clothing on hangers. All items donated will be delivered to the Suffolk County OneStop Employment Center in Hauppauge.

Friday Films:

Rebel Without a Cause Friday, October 24, 2:00pm - 4:00pm

Celebrate the 70th anniversary of the classic film, Rebel Without a Cause (1955). A rebellious young man with a troubled past comes to a new town, finding friends and enemies. Starring James Dean, Natalie Wood, and Sal Mineo. Running time: 91 minutes. Rated PG-13. No registration required.

The ABC’s of Hauntings, Spirits, & Ghosts

Monday, October 27, 6:00pm – 7:30pm

Step into the mysterious realm of the paranormal with the Budapest Psychic, Rev. Maria D’Andrea, as she explores the world of hauntings, spirits, and ghosts. From unexpected encounters in ordinary homes to intentional visits to famously haunted locations, these supernatural experiences are more common than many realize. Rev. D’Andrea will discuss the meanings behind such encounters, shedding light on their spiritual significance and what they may be trying to tell us. Registration is required.

Medicare: The New Rules for 2026

Tuesday, October 28, 6:30pm – 7:30pm This informative workshop

will provide you with information on Medicare’s New Ruling for 2026. Every year the government can change Medicare rules, leaving the Medicare Beneficiary searching to find out these changes on their own. This class will discuss any new changes for 2026 and how it can affect individual plans. Bring your Medicare questions and concerns to get the answers in this class discussion. The basics of Medicare and your options will be reviewed as well. Please register for this program.

TEEN PROGRAMS

Teens Dungeons & Dragons

Wednesdays, October 22 5:30pm – 7:30pm Join us in the library for Dungeons & Dragons! Build a character, choose your weapons, and lay waste to nasty critters with a roll of the dice. New and experienced players welcome! Grades 6-12. Registration required.

Teens Ghost Magnet Take & Make Pickup between Monday, October 27 at 9:30am and Friday, October 31 at 4:30pm Design your own Ghost Magnet for Halloween! Perfect size for your locker or your fridge at home – take the kit home and be creative! Grades 6-12. Registration required.

Teens Paws of War Presentation Monday, November 3, 4:00pm – 5:00pm Come and hear about the amazing work that Paws of War does! Paws of War brings together veterans, first responders, and rescued animals. Earn one hour of community service for attending. If you bring pet supplies from the Paws of War Wishlist to donate, you will receive an additional hour of community service. Grades 6-12. Registration required.

Expenses To Expect Upon Buying A Home

Homeownership is often characterized as a fulfillment of a dream. Indeed, many homeowners feel their ability to buy a home is a reflection of their discipline and commitment to saving money. That discipline and dedication can set homeowners up for long-term financial health, providing a unique sense of security along the way. First-time home buyers may not know what to expect upon buying a home, and since each home is unique, it’s impossible for even long-time homeowners to say with certainty exactly how things will unfold once those new to home ownership get the keys to their first house. Various expenses might be the only common variable when it comes to homeownership, and some of those expenses may surprise first-time buyers. With that in mind, the following are some expenses first-time buyers can expect once their offers are accepted.

• Down payment: Conventional wisdom long suggested home buyers should submit a down payment of at least 20 percent of the overall purchase price upon buying a home. Buyers who want to follow that advice would need a down payment of $80,000 when buying a

$400,000 home. But many home buyers now submit down payments considerably less than 20 percent, particularly in the modern real estate market, which is characterized by high prices and low inventory. The lower the down payment, the higher your monthly mortgage payment will be, so it’s best to save as much as possible toward a down payment.

• Primary mortgage insurance (PMI): Buyers who cannot come up with a down payment of 20 percent or more will have to pay for primary mortgage insurance, which is typically a set fee that is incorporated into the mortgage payment each month. PMI fees are typically waived once the balance on the mortgage reaches 79 percent or less of the purchase price, though some lenders may waive PMI prior to that if the value of the home increases considerably before the loan balance reaches the predetermined marker.

• Closing costs: The amount of closing costs varies widely depending on a host of variables, but Bankrate. com notes it’s not uncommon for these costs to come in at somewhere between 2 and

5 percent of the loan principal. Closing costs must be paid no later than when the sale becomes official and buyers sign on the (many) dotted lines. Application and credit fees, title fees, underwriting fees, appraisal fees, and transfer tax are among the various fees that fall under the umbrella of closing costs.

• Moving: It’s also important that first-time home buyers budget for moving costs. Moving costs vary and may depend on how much buyers already own and how far they’re moving. The home renovation experts at Angi estimate that local moves typically cost somewhere between $883 and $2,568, while long-distance moves may run buyers anywhere from $2,700 to $10,000 or more.

These costs are some of the upfront fees aspiring homeowners can expect when buying a home. Longterm costs, including homeowners’ insurance (which is separate from PMI), property taxes, homeowners’ association fees, and maintenance are some additional expenses buyers can plan for as they try to determine their home buying budgets.

“If you can’t feed a hundred people, then feed just one.” – Mother Teresa

Sometimes life can become overwhelming. There are so many people who need help, but where do we even begin?

When I think about ways to show my gratitude and helping others, I think about the quote from Mother Teresa. I might not be able to feed every adult and child who is hungry today, but with your help, we can help feed some of them.

We can create a ripple effect. Someone in the next town will see what we are doing, and they will start their own food or clothing drive…and then someone in the next town, and the town after that. Pretty soon, millions of people who needed support during a tough time in their lives will nd it. Hopefully, they can pay it forward when they have the means to do so.

Gratitude causes ripples, and ripples cause change. Let’s create some ripples this month for people who can use our help. Here are the details:

What: Thanksgiving Food Drive for St Vincent de Paul food pantry

Where: Our Lady of Perpetual Help Lindenhurst.

When: The month of October. All donations must be in by Saturday, November 1st

More: We will collect nonperishable items for Thanksgiving dinners at JoAnn Cilla Real Estate, 203 E Montauk Hwy Lindenhurst NY 11757 on the following days:

• Mondays 3pm-5pm

• Wednesdays 12pm-2pm

• Fridays 11am-1pm

• Saturdays 10am-1pm

If you can’t drop off at these times or need us to pick up your donation, please call me at 631-539-6000. I am grateful for your help, JoAnn.

JOANN CILLA

Licensed Real Estate Broker

203 E. Montauk Hwy. Lindenhurst, NY 11757

Office: 631-539-6000 Cell: 516-429-1911 joann@joanncillarealestate.com www.joanncillarealestate.com

Marsala

• Chicken Francese

• Eggplant Parmigiana

• Chicken Parmigiana • Shrimp Oreganata +$15

Eggplant Rollatine

Shrimp Parmigiana +$15

Homeownership

is a dream for millions of people across the globe. The National Association of Realtors indicates real estate has historially exhibited long-term, stable growth in value. Money spent on rent is money that a person will never see again. However, paying a traditional mortgage every month enables homeowners to build equity and can be a means to securing one’s financial future.

Homeowners typically can lean on the value of their homes should they need money for improvement projects or other plans. Reverse mortgages are one way to do just that.

Common Questions About Reverse Mortgages

Who is eligible for a reverse mortgage?

People near retirement age are eligible for a specific type of loan they can borrow against. Known as a “reverse mortgage,” this type of loan can be great for people 62 or older who perhaps can no longer make payments on their home, or require a sum of money to use right now, without wanting to sell their home.

In addition to meeting the age requirement, a borrower must live at the property as a primary residence and certify occupancy annually to be eligible for a reverse mortgage. Also, the property must be maintained in the same condition as when the

reverse mortgage was obtained, says Fannie Mae.

How does a reverse mortgage work?

The Consumer Finance Protection Bureau says a reverse mortgage, commonly a Home Equity Conversion Mortgage, which is the most popular type of reverse mortgage loan, is different from a traditional mortgage. Instead of making monthly payments to bring down the amount owed on the loan, a reverse mortgage features no monthly payments. Rather, interest and fees are added to the loan balance each month and the balance grows. The loan is repaid when

the borrower no longer lives in the home.

What else should I know?

With a reverse mortgage, even though borrowers are not making monthly mortgage payments, they are still responsible for paying propertyrelated expenses on time, including, real estate and property taxes, insurance premiums, HOA fees, and utilities. Reverse mortgages also come with additional costs, including origination fees and mortgage insurance up to 2.5 percent of the home’s appraised value, says Forbes. It’s important to note that most interest rates on these loans are

variable, meaning they can rise over time and thus increase the cost of borrowing. In addition, unlike traditional mortgage payments, interest payments on reverse mortgages aren’t tax-deductible.

How is a reverse mortgage paid back?

A reverse mortgage is not free money. The homeowners or their heirs will eventually have to pay back the loan when the borrowers no longer live at the property. This is usually achieved by selling the home.

The CFPB notes if a reverse mortgage loan balance is less than the amount the home is sold for, then the borrower

keeps the difference. If the loan balance is more than the amount the home sells for at the appraised value, one can pay off the loan by selling the home for at least 95 percent of the home’s appraised value, known as the 95 percent rule. The money from the sale will go toward the outstanding loan balance and any remaining balance on the loan is paid for by mortgage insurance, which the borrower has been paying for the duration of the loan.

Reverse mortgages can be a consideration for older adults. However, it is essential to get all of the facts to make an informed decision.

How To Determine If The Time Is Right To Downsize

Thephrase “bigger is better” has endured for quite some time. Though it may be impossible to pinpoint precisely who coined the phrase, its lesson that larger things tend to be more valuable than smaller alternatives is applicable in numerous situations. No adage applies to every situation, and in some instances, people may find that bigger is not better.

Downsizing is an approach many individuals consider after turning 50. Parents who are empty nesters and others nearing retirement may wonder if the time is right to downsize from their current homes. Though that’s a strategy millions of people have

adopted over time, the decision is not always so simple. Individuals over 50 who are trying to determine if downsizing is right for them can consider a host of factors before making a decision.

• Monthly housing expenses: Before downsizing their homes, individuals should determine just how much they’re currently spending on housing. Individuals who have fixed-rate mortgages likely know the amount of their monthly mortgage payment, but what about maintenance? Home maintenance expenses fluctuate, but a careful examination of the previous 12

months’ expenditures can give homeowners an idea of just how much they’re spending to maintain their properties. The number may be eye-opening, as Thumbtack’s “Home Care Price Index” released in the third quarter of 2024 revealed that the average annual cost to maintain a single-family home reached an alltime high of $10,433. If such expenses are preventing

homeowners from building their retirement nest eggs, then it might be time to seek alternative housing.

• Real estate prices: Real estate prices have skyrocketed in recent years, which can be both good and bad for current homeowners considering downsizing. Many people who downsize look to move from a single-family home into a condominium, where

maintenance tasks are typically handled by a homeowners’ association (HOA). Such communities typically charge HOA fees, which can be minimal or considerable. In addition, the price of condominiums has risen in recent years, with the lender New American Funding reporting in early 2024 that the median sale price of a condo reached $341,000. So homeowners who want to downsize their homes may end up taking most of the profit from selling their current properties and reinvesting it in a costly condo. Some may deem that worthwhile, while others may

find the cost savings of downsizing in the current market are negligible.

• Emotional attachment: Downsizing may be considered with cost savings in mind, but it’s important to consider your emotional attachment to your current home. Many homeowners over 50 raised their families in their current homes, and letting go of a property where so many memories were made can be difficult. Homeowners who are not prepared to move on from properties that are meaningful to them and their families can consider additional ways to downsize their financial obligations.

Come October 31, there is extra mischief in the air, and who knows what might be lurking around those dim corners? Halloween is a time when the line between having fun and being scared is easily blurred.

While trick-or-treating and attending parties are ways to enjoy the final day of October, there are plenty of other ways to make Halloween more fun.

• Read some scary stories. There’s something to be said about reading scary stories or poems on Halloween. Readers’ imaginations take over on Halloween as they envision scary characters and scenarios. Edgar Allen Poe, author of many notably macabre works, is a popular read come Halloween.

• Go pumpkin picking. Most people already make pumpkin picking an annual treat. Don’t overlook mishappen

Get Into The Spooky Spirit This Halloween

pumpkins that can be carved into spooky jacko’-lanterns. Also, enhance Halloween decor with pitted and warty gourds that lend that scary appeal.

• Create a haunted house. Instead of going elsewhere to get chills and thrills, transform your house or yard into a spooktacular vision and invite neighbors to explore.

• Make creepy crafts. Children can get a kick out of crafting Halloween decorations. Drape a piece of muslin over a beverage bottle and spray it with laundry starch. Let sit and the muslin will stiffen when it dries. Paint on black circles for eyes and hang your “ghost” from a string.

• Whip up Halloween treats. Candied apples, extra-rich brownies and mini hot dogs wrapped in crescent rolls to look like mummies are just some

of the ways to create a scary Halloween feast.

• Have a costume theme. Everyone in the household can get in on the fun by planning costumes to fit a theme. For example, everyone can dress like the Addams family.

• Host a Halloween book club. Those who love to read can ensure the October gathering of a book club is one that features a discussion of a scary book. Those looking for a scare can explore horror authors like Stephen King, Anne Rice, Dean Koontz, Clive Barker, Shirley Jackson, and Tananarive Due.

• Host an outdoor movie. Projectors can now be hooked up to smartphones and tablets, so it’s easier than ever to watch movies outside. Simply project a device onto a screen, white fence or even a bedsheet. Since it gets

dark somewhat early in October, the movie doesn’t have to start very late. Depending on the audience, choose a movie that is very scary or only mildly so if children will

be viewing.

• Organize a Halloween treat exchange. Similar to a Christmas “Secret Santa,” participants put together a wrapped gift of homemade or store-bought foods and exchange with others. Halloween can be made even more entertaining with some extra activities that appeal to people of all ages.

How To Navigate A Challenging Real Estate Market

Realestate has long been touted as a worthy long-term investment. With that conventional wisdom in mind, young adults often make buying a home one of their first bigticket purchases. Though real estate remains a potentially lucrative investment, the market for homes has been difficult to navigate for several years running.

High mortgage interest rates and low inventory have left many buyers feeling priced out of the real estate market. Others may find the competitive nature of the modern real estate market too stressful. No one can predict if or when the real estate market might be less

challenging, but the following are some ways those looking for a house can navigate that process.

• Ready your finances. It goes without saying that prospective buyers must get their financial affairs in order before they begin shopping for a house. But finding a home in the current market takes time, and some buyers might have let their mortgage preapproval letter expire without realizing it. Others might have experienced a dip in their credit rating as they turned to credit cards to confront inflation. That means buyers who began looking for a home

months or even years ago might not be positioned to buy now, should they find a home to their liking. Revisit your finances if it’s been a while. Pay off any consumer debt that has accumulated in recent months and reapply for mortgage preapproval if necessary.

• Be ready to pounce. Data from the National Association of Realtors

found that the average home spent 32 days on the market before being sold in November of 2024, which was a full week longer than a year earlier. That’s good news for buyers, but it still means buyers must be ready to pounce if they find a home and a home price to their liking.

• Hire a real estate agent. The hectic pace

of the modern real estate market can be difficult for anyone to keep up with. But real estate agents keep up with the market for a living, and they can be invaluable resources for buyers whose commitments to work and family are making it difficult to keep pace.

• Emphasize long-term growth and value when assessing properties. According to Zillow, the median list price of homes in the United States was just under $387,000 by the end of January 2025. But buyers must also recognize that 22.4 percent of homes sold above list price in that month, according to a Redfin

analysis of MLS data and/or public records. Buying a home is more than an investment in a property. It’s also, in some way, an investment in the town where the home is located and in a homeowner’s future. So while it can be tempting to buy a home with the lowest asking price, homebuyers should also seek homes that figure to experience the best long-term growth in value. Homes situated in safe and welcoming towns with good schools are arguably a better investment than homes with lower sticker prices but no such amenities.

BHS Students Earn National Merit Accolades

Cassidy Hayes And Aiden Shek Recognized Among Top Students In The Nation

Babylon Junior-Senior High School is proud to announce that seniors Cassidy Hayes and Aiden Shek have been named a Semifinalist and Commended Student, respectively, in the

2026 National Merit Scholarship Program.

The prestigious academic competition honors the highest-scoring students on the Preliminary SAT/ National Merit Scholarship Qualifying Test (PSAT/ NMSQT), which is taken during the student’s junior year.

Cassidy is one of roughly 16,000 semifinalists named nationwide, representing the top one percent of all U.S. high school seniors.

This designation provides the opportunity to continue in the competition for some 7,000 National Merit Scholarships worth nearly $26 million that will be offered next spring.Aiden is one of about 34,000

Commended Students recognized for their exceptional academic promise, placing him among the top five percent of scorers in the country.

“Congratulations to Cassidy and Aiden for this outstanding academic achievement,” said Principal Al Cirone. “This recognition is a testament to the pair’s hard work, intellectual curiosity, and dedication to excellence.”

Cassidy Hayes with her counselor Tracy Lesnick. Photos courtesy of the Babylon Union Free School District

Aiden Shek with his counselor Rebecca Cifelli.

CUSTODIAL WORKER-P/T

Seeking an honest, reliable person to perform P/T cu stod ia l duties for nights and

Must be exper ienced. Clean driver's licen se and high schoo l diploma or equivalent required. Excellent sa lary If

Kitchens, Floo ring, Inte rior Doors Sh eetrock, Trim, Plumbing Crown Molding, Plumbing, etc. OWNER OP ERATED

Minor Repairs to Major Renov ations Tile Work, Painting Sheetrock, Spackle Flooring, Roof Repairs Deck Construction & Repair & mu ch more J&J Pr emier General Construction (516) 523-5591

WHOLE HOUSE CLEAN OUTS & MOVE OUTS

BASEMENTS, ATTICS, GARAGES CLEANED OUT

SHEDS,DECKS POOLS, ETC DEMOLISHED AND REMOVE D NO DUMPSTER ON YOUR PROP ERTY WE HAUL EV ERYT HING AWAY

CALL BEN 631 44 5- 1 668

Ki tchen & Baths

COMPLETE BATHROOM RENOVATION SPECIAL starting at $4,995

COMPLETE DEMOLITION NEW SHEETROCK PLUMBING TILE FLOORS, TOILET, SINK, FAUCETS, VANITY

DESIGN TO COMPLETION ACE CONTRACTING (licensed & insured) CALL or TEXT OWNER (631) 432 3892

y

y ALL MASONRY WORK AND BLACKTOP DRIVEW AYS APRONS ASPHALT,

Hope For The Warriors To Present Free Career Readiness Webinar

HAVE AN APARTMENT TO RENT?

Place your ad in our Classifieds 631 -2 26- 2636 Ex t. 276

LOOKING TO ADVERTI SE YOUR BUSINES S?

Call Classified and one of our experienced sales representatives will help you. BIG BUDGET? SM ALL BUDGET? 631-226-2636, press 276

BUYING? SELLING? RENTING? Place your ad in the Classifieds 631-226-2636 Ext. 276

Geared for the military community, Hope For The Warriors will present a free, virtual career workshop with Robert Half, a talent solutions and business consulting firm, Thursday, October 16, from 11 a.m. to noon. EST.

Working with a Staffing Firm: Myths, Facts & How to Maximize the Relationship will tackle the utilization of staffing firms, showcase Robert Half’s process of working with candidates/employers, what to expect from the placement process, temporary to permanent opportunities, and navigating Robert Half’s job portal.

As a part of Hope For The Warriors’ Warrior’s Compass transition program, the free, virtual career workshop series provides free training to help prepare those in the military landscape for a job search in today’s civilian climate. The workshops offer tools and tips, as well as opportunities to network with other service members, military spouses, and companies committed to hiring those with military backgrounds.

There will be one more workshop in 2025, taking place on December 11.

Did You Know?

Outdoor living spaces are a good investment for homeowners seeking to enjoy their home exteriors to the fullest, and that investment continues to pay dividends when homes are put on the market. According to Remodeling magazine’s Cost vs. Value report, a number of outdoor living upgrades provide a sizable return on investment (ROI) when homeowners put their properties up for sale. According to the report, a wood deck could recoup up to 82 percent of the original cost at resale, meaning a job that comes in around the national average price of $17,000 could net $14,000 at resale. An outdoor kitchen could prove an even better investment in terms of ROI, as Remodeling magazine indicates such a feature nets a return between 55 percent and 200 percent at resale depending on the location of the home and the materials used for the project.

For the first 15 participants who attend the October event for its entirety, Robert Half will provide 30-day access to its Percipio learning platform. Percipio features thousands of career development resources, including courses on resume writing, interview prep, leadership, Microsoft Office skills, and more. The goal of the self-guided program is to help users sharpen their skills and explore new interests to help take the next step in their career journey.

To register for the free workshop, visit hopeforthewarriors.org.

A Guide To Mortgage Interest Rates

Buying a home is the most expensive purchase many people make in their lifetime. Some people do it only once, while others are in the market with greater frequency. In any instance when the home-buying process involves securing a mortgage, buyers can benefit from knowing a thing or two about mortgage interest rates.

A mortgage interest rate can help buyers determine if a given home is affordable or beyond their budget. Rocket Mortgage says mortgage interest rates can have a major impact on long-term costs, so it is imperative to seek the lowest rates possible. However, an assortment of economic variables affect mortgage interest rates, and conditions unique to each buyer also can affect the rate they’re eligible to obtain.

Understanding home loan rates can help potential buyers better navigate the complex process of buying a home.

What is mortgage

interest?

When a person buys a home with a mortgage, he or she doesn’t just pay back the amount borrowed, which is called the principal. The loan also requires paying interest, which is essentially the cost of borrowing money. Mortgage interest is calculated as a percentage of the remaining principal, says Investopedia.

How are mortgage rates set?

Mortgage rates are not determined by a single variable. They are derived from a combination of factors that include the Federal Reserve’s monetary policy, economic conditions, and a borrower’s personal financial situation. The Federal Reserve (in the United States) influences the overall rates by adjusting the federal funds rate, or the rate at which banks lend to each other overnight. This not only impacts mortgage rates, but also additional interest rates, according to Fannie Mae. Lenders will ultimately decide on the specific rates to offer borrowers.

How does a borrower’s financial situation affect mortgage rates?

Lenders will conduct a thorough assessment of a potential borrower’s creditworthiness. They will look at, among other things, a borrower’s credit score and debt-to-income ratio. A higher credit score typically results in a lower interest rate. A lower DTI indicates a lower risk to the lender, also potentially resulting in a lower interest rate. Squaring away finances well in advance of applying for a mortgage can help home buyers secure lower interest rates that could save them considerable sums of money over the life of their mortgages. How do loan types affect mortgage interest?

A home buyer will pay interest no matter

the mortgage type, but there are options to select a fixed or adjustable interest rate, or even an interest-only mortgage.

According to Bankrate, with a fixed-rate mortgage, the interest rate remains the same throughout the life of the loan, meaning the payment for principal and interest will remain consistent. Additional charges that are wrapped into mortgage payments could change, however. Property taxes and homeowners’ insurance charges could increase, for example. Fixed rates tend to be lower when the term of the mortgage is shorter, so borrowers can opt for a 20-year mortgage over a 30-year to save some money on interest.

An adjustable-rate mortgage (ARM) will see the interest rate change during the repayment period. It may start with a low introductory rate for the first several years of the loan, but then it can go up or down depending on market indexes and benchmarks. Many lenders put a cap on how high the interest rate can go, however. Various factors determine mortgage interest rates for home buyers, including market conditions, credit standing, federal rates, the type of loan, and term length.