Established in 1956, Clark County School District is the fifth largest school district in the country, educating almost 75 percent of all students in Nevada with more than 320,000 enrolled in Kindergarten through 12th grade. The district encompasses 357 schools and approximately 8,000 square miles in southern Nevada and is a minority-majority-student district.

Age Requirements

Children must meet the following minimum age and entrance requirements on or before September 30, 2015, to be admitted to kindergarten, first, or second grade. (Nevada Revised Statutes - NRS 392.040)

Kindergarten students must have attained the age of 5 years old by Sept. 30 to attend kindergarten.

First-grade students must have attained the age of 6 years old and demonstrate proof of completing kindergarten at a public, state-licensed private, state-exempt private, or approved home school program.

Demonstrate proof of completing kindergarten and promotion to first grade while being a resident of another state in compliance with the age and entrance requirements of that state. Proof must be verified through a report card issued by the last out-of-state public or private kindergarten.

Second-grade students must have attained the age of 7 years old and demonstrate proof of completing kindergarten and first grade at a public, state-licensed private, state exempt private, or approved home school program.

Children who have attained the age of 6 and who do not meet the entrance requirements will be placed in kindergarten.

Children who have attained the age of 7 who do not meet the entrance requirements will be assessed to determine if the student is developmentally ready for first or second grade.

Proof of Address - One form of proof of address is required. A recent utility bill (telephone and cable bills are not acceptable), current mortgage statement, rental receipt, residential lease agreement, or sales contract are acceptable forms of proof of address.

Parent/Guardian Personal Identification - A driver’s license, picture identification, and/or passport are acceptable forms of personal identification. Permanent and temporary guardians should be prepared to provide proof of guardianship at the time of registration.

Proof of Child’s Identity - An original birth certificate, passport, or certified birth card issued by a health district are acceptable documents for proof of child’s identity.

NEVADA SCHOOL REPORT CARDS

This website will allow you to review school ratings for any district in Nevada.

www.nevadareportcard.nv.gov/di/

SCHOOLS

COMMUNITY COLLEGES & UNIVERSITIES

LAS VEGAS

University of Nevada, Las Vegas

702.774.8658

Desert Research Institute

702.862.5400

Wongu University of Oriental Medicine and Acupuncture

702.463.2122

Euphoria Institute of Beauty Arts & Sciences

702.341.8111

Brightwood College

702.368.2338

Le Cordon Blue College of Culinary Arts

702.365.7690

UNIVERSITY OF NEVADA LAS VEGAS

HENDERSON

College of Southern Nevada

702.651.3000

Nevada State College

702.992.2000

National University

702.531.7800

Touro University Nevada

702.777.8687

Roseman University of Health Sciences

702.990.4433

DeVry University

702.933.9700

International Academy of Design and Technology

877.863.4111

HENDERSON CONTINUED...

ITT Technical Institute

702.558.5404

Everest College

702.567.1920

The Art Institute of Las

702.369.9944

Since our first classes were held on campus in 1957, UNLV has transformed itself from a small branch college into a thriving urban research institution. Along the way, our urban university has become an indispensable resource in one of the country's fastest-growing and most enterprising cities. UNLV’s diverse faculty, students, staff, and alumni promote community well-being and individual achievement through education, research, scholarship, creative activities, and clinical services. We stimulate economic development and diversification, foster a climate of innovation, promote health, and enrich the cultural vitality of the communities that we serve.

We will evaluate our success as a leading research university by our progress on these key measures:

Impact of our research, scholarship, and creative activities.

Student achievement of learning outcomes.

Placement into preferred employment or post-graduate educational opportunities. Student, faculty, and staff diversity, including maintaining UNLV’s Minority Serving Institution (MSI) status and Hispanic Serving Institution (HSI) status.

Intellectual activity, patents, and entrepreneurial activity fostered by UNLV. Quality and impact of our clinical services.

Alignment of our physical infrastructure and organizational effectiveness with our Top Tier mission. A deeper engagement of UNLV with Las Vegas and our region to ensure ongoing alignment with our diverse community’s needs and interests.

641,903 $53,000 34 50.39% 49.61%

Clark County

HOUSING

56.74% of homes owner occupied

43.26% of homes rented

POPULATION DENSITY

4,222.5 inhabitants per sq. mile

190,724 housing units at an average density of 1,683.3 per square mile

HISTORY

AGE DEMOGRAPHIC

25.9% under age 18

8.8% between ages 18 to 24

32% between ages 25 to 44

21.7% between ages 45 to 64

11.6% above age 65

CITY QUICK FACTS

25th most populous city in the US

A top 3 destination in the US

Incorporated in 1911

2,001 feet elevation

Highest Average Temperature 104.2

Lowest Average Temperature 30

The area was named Las Vegas, which is Spanish for "the meadows", as it featured abundant wild grasses, as well as the desert spring waters needed by westward travelers. Las Vegas was founded as a city in 1905, when 110 acres of land adjacent to the Union Pacific Railroad tracks were auctioned in what would become the downtown area. In 1911, Las Vegas was incorporated as a city. 1931 was a pivotal year for Las Vegas. At that time, Nevada legalized casino gambling and reduced residency requirements for divorce to six weeks. This year also witnessed the beginning of construction on nearby Hoover Dam. The influx of construction workers and their families helped Las Vegas avoid economic calamity during the Great Depression. The construction work was completed in 1935.

CLARK COUNTY BASE MAP

L O C A L B U S I N

L

L O C A L B U S I N

L

Foxtail Coffee - Trails Village Center

L O C A L B U S I N

UTILITIES

& R E S O U R C E S

CHANGE OF ADDRESS

USPS

Below is the website if you would like to change your address online or you can visit your local post office, they will provide you with the change of address packet. https://moversguide.usps.com

Benefits you will receive when you change your address online are:

Exclusive mover savings coupons

Safe and secure with identity verification by a simple $1.00 charge to your credit or debit card

Email confirmation at the end of registration of your change of address

* Must have valid email address and credit card to register online.

AUTO REGISTRATION AND DRIVER LICENSING

Below is the website if you would like to change your address online or you can visit your local DMV office.

Nevada Department of Motor Vehicles

DMV Services

General DMV Information Contact: (775) 684-4830

www.dmv.nv.gov/addchange.htm

Las Vegas Area Offices (702) 486-4368

Henderson

Las Vegas - West Flamingo

Las Vegas - North Decatur

Las Vegas - East Sahara

VOTERS REGISTRTION

Below is the website if you would like to register online or you can fill out the paperwork provided and mail it back to your County Elections Office listed below.

(Pension plans, 401K, Social Security, Veterans Affairs)

Investments (Investment Agencies and Brokers)

Online Bill Payer

Paypal

GOVERNMENT

US Post Office

Department of Motor Vehicles

(Obtain your driver’s license and change vehicle registration)

IRS

Passport Office

Veteran Affairs

Unemployment Office

(If you are currently receiving unemployment benefits)

HEALTH

Physician

Pharmacies

SERVICE PROVIDER

Childcare

Housecleaning Services

Delivery Services

Lawn Care Services

Veterinarian

Pool Service

MEMBERSHIPS

Health Clubs

Membership Clubs (AAA or similar)

Community Groups (PTA, Neighborhood Associations, Civic Clubs)

Children’s Extracurricular

Activities (Dance Classes, Music Lesson, Sports Clubs)

SUBSCRIPTIONS

Newspapers

Magazine (USPS will only forward 2 months)

Movie Subscriptions

Book or Music Clubs

OTHER

Friends and Family

Employers (typically notify the HR Department)

MOVING CHECKLIST

8 WEEK BEFORE YOU MOVE

Inventory Sheets: Create an inventory sheet of all your belongings which need to be moved Research Moving Options: You’ll need to decide if yours is a do-it-yourself move or if you’ll be using a moving company. Request Moving Quote: Solicit moving quotes from as many moving companies and movers as possible. There can be a large difference between rates and services within moving companies.

Discard Unnecessary Items: Moving is a great time for ridding yourself of unnecessary items. Have a yard sale or donate unnecessary items to charity.

Packing Material: Gather moving boxes and packing material for your move.

Contact Insurance Companies: You’ll need to contact your insurance agent to cancel/transfer your insurance policy.

1 1 Your USPS Office

1 WEEK BEFORE YOU MOVE

Your Change of Address: Change your address with the USPS, DMV, Financial Institutions, Utilities, Government Offices, Health Care Service Providers, Memberships, Subscriptions and Insurance Provisions.

Bank Accounts: Transfer or close bank accounts if changing banks. Make sure to have a money order for paying the moving company.

Service Automobiles: If automobiles are to be driven long distance, you’ll want to have them serviced so you have a trouble-free drive.

Cancel Services: Notify any remaining service providers (newspapers, lawn services, etc.) of your move.

Travel Items: Set aside all items you’ll need while traveling. Make sure these are not packed on the moving truck.. Contact Utility Companies: Set utility turnoff date, seek refunds and deposits and notify them of your new address.

4 WEEK BEFORE YOU MOVE

4 BEFO

Start Packin location

4

Start Packing: Begin packing all things destined for your new location.

Obtain You dentist and an records or m

Obtain Your Medical Records: Contact your doctor, physician, dentist and other medical specialists who may currently be retaining any of your family’s medical records. Obtain these records or make plans for them to be delivered to your new medical facilities if changing. Security is critical of personal records.

Note Food Inventory Levels: Check your cupboards, refrigerator and freezer. Use up as much of your perishable food as possible.

Small Engines: Service small engines for your move by extracting gas and oil from the machines. This will reduce that chance to catch fire during your move.

Protect Jewelry and Valuables: Transfer your jewelry and valuables to a safety deposit box; you don’t want them to be lost or stolen during your move.

Borrowed and Rented Items: Return items that you may have borrowed or rented. Collect items borrowed to others.

* DA

MOVING DAY

Plan Your the house

Someone

Plan Your Itinerary: Make plans to spend the entire day at the house or at least until the movers are on their way. Someone will need to be around to make decisions. Make plans for kids and pets to be at a sitters for the day.

Review the House: Once the house is empty, check the entire house (closets, attic, basement, etc.) to ensure no items are left or no home issues exist.

Double Check With Your Mover: Ensure the mover has the new property address and all of your most recent contact information, should they have any questions during your move.

Vacate Your Home: Make sure utilities are off, doors and windows are locked and notify your real estate agent you’ve vacated the property.

Questions To Ask: Where is the garage door opener? Where are the keys to the house, mailbox and other lockable area? Did you retrieve all keys from neighbors and friends?

MOVING RESOURCES

THE HOME DEPOT

(800) 466-3337 wwwomedepot.com

Lamb Blvd 1401 S Lamb Blvd, Las Vegas, NV 89104

Henderson 1030 W Sunset Rd, Henderson, NV 89014

Tropical Pkwy 7881 W Tropical Pkwy, Las Vegas, NV 89149

LOWES

(800) 466-3337 www.lowes.com

Pavilion Center 851 South Pavilion Center Drive Las Vegas, NV 89144

West Washington 7550 West Washington, Las Vegas, NV 89128

Charleston Blvd 2875 E. Charleston Boulevard, Las Vegas, NV 89104

DONATION FACILITIES

Goodwill (800) 741-0186 locator.goodwill.org

The Salvation Army (800) 958-7825 www.salvationarmyusa.org

US Highway 93, Boulder City, Nevada www.usbr.gov/lv/hooverdam wfgtitle.com/nevada

TITLE & E S C R O W

CYBER SECURITY

Because of you… we obsess over cyber security!

Cyber fraud and email hacking are on the rise. Fraudsters may access individual email accounts and monitor the life of your transaction. At the time funds are due to the escrow, fraudsters intercept the information for wiring funds, and the fraudsters change the information without the knowledge of the sender or recipient, resulting in the funds being sent to an outside account and never credited to the intended party.

To protect and reduce your risk, WFG has implemented the following procedures for outgoing and incoming wires:

Outgoing Wire from WFG to seller or borrower for proceeds

In the escrow paperwork provided you will be asked to provide written instructions on how you want funds due you sent to you at the close of escrow. If you choose to have the funds sent via wire transfer, WFG will contact you by phone to confirm the wire information provided.

Incoming Wires from the buyer and/or lender to WFG bank account

For funds that are to be wired to WFG for your transaction, we will send specific wire instructions to the remitting person via an encrypted email. We recommend you reach out to your WFG contact to confirm the wire instructions prior to remittance.

We look forward to processing your escrow transaction for you. We know that this can be a stressful time and we are here to assist you in any way we can to make this a good experience.

The purchase of a home is likely going to be one of the most expensive and important purchases you will ever make. You and your mortgage lender want to make sure the property is indeed yours and that no individual or government entity has any right, lien, claim, or encumbrance to your property.

The title insurance company’s function is to make sure your rights and interests to the property are clear, that transfer of title takes place efficiently, and correctly, and your interests as a homebuyer are protected. Title insurance companies provide services to buyers, sellers, real estate developers and builders, mortgage lenders, and others who have an interest in the real estate transfer. Title companies issue two types of policies - “Owners Policy” (which covers the homebuyer) and “Lenders Policy” (which covers the bank, savings and loan, or other lending institution over the life of a loan). Both are issued at the time of purchase for a one-time premium.

The title company conducts an extensive search of public records to determine if anyone other than you has an interest in the property before issuing a policy. The search may be performed by title company personnel using either public records, or more likely, information gathered, reorganized, and indexed in the company’s title “plant”. With such a thorough examination of records, title problems can usually be found and cleared up prior to purchase of the property. Once a title policy is issued, if for some reason any claim, which is covered under your title policy, is ever filed against your property, the title company will pay the legal fees involved in defense of your rights as well as any covered loss arising from a valid claim. That protection, which is in effect as long as you or your heirs own the property, is yours for a one-time premium paid at the time of purchase.

The title company works to eliminate risks before they develop. This makes title insurance different from other types of insurance. Most forms of insurance assume risks by providing financial protection through a pooling of risks or losses arising from unforeseen events, like fire, theft, or accident. The purpose of title insurance, on the other hand, is to eliminate risks and prevent losses caused by defects in title that happened in the past. Risks are examined and mitigated before property changes hands. Eliminating risk has benefits to both of you, the home buyer, as well as the title company. It reduces the chance adverse claims might be raised, and by doing so reduces the number of claims that have to be defended or satisfied. This keeps costs down for the title company and your title premiums low. With title insurance you are assured that any valid claim against your property will be taken on by the title company, and that the odds of a claim being filed is slim.

WHAT IS ESCROW?

Understanding the Escrow Process

An escrow is an arrangement in which a neutral third party (the escrow agent) assembles and processes many of the components of a real estate transaction, records the transaction, and ultimately, disburses and distributes funds according to the buyers’, sellers’ and lenders’ instructions. Your transaction is typically closed by an Escrow Officer. People buying and selling real estate usually open an escrow for their protection and convenience. Both the buyer and seller rely on the escrow agent to carry out their written instructions relating to the transaction and to advise them if any of their instructions are not mutually consistent or cannot be carried out. If the instructions from all parties to an escrow are clearly drafted, the escrow officer can proceed on behalf of the buyer and seller without further consultation. This saves much time and facilitates the closing of the transaction.

TYPICAL ROLES IN THE CLOSING PROCESS

The Seller/Agent

Delivers Purchase Sale Agreement to the escrow agent.

Prepares s the paperwork necessary to close the transaction.

The Buyer/Agent

Deposits funds required to close with the escrow agent.

Approves the commitment for title insurance, or other items as called for by the Purchase Sale Agreement.

Executes the paperwork and loan documents necessary to close the transaction.

The Lender

Deposits loan documents to be executed by the buyer

Deposits the loan proceeds.

Directs the escrow agent of the conditions under which the loan funds may be used

The Escrow Agent

Clears Title

Obtains title insurance

Obtains payoffs and release documents for underlying loans on the property Receives funds from the buyer and/or lender. Prepares vesting document affidavit on seller’s behalf.

Prorates insurance, taxes, rents, etc.

Prepares a final statement (often referred to as the “HUD Statement” or ”Settlement Statement”) for each party, indicating amounts paid in conjunction with the closing of your transaction. Forwards deed to the county for recording. Once the proper documents have been recorded, the escrow agent will distribute funds to the proper parties.

In Summary

Escrow is the process that assembles and processes many of the components of a real estate transaction. The sale is officially closed when the new deed is recorded and funds are available to the seller, thus transferring ownership from the seller to the buyer. The escrow agent is a neutral third party acting on behalf of the buyer and seller.

WHAT IS TITLE?

About Title Insurance

Title is a bundle of rights in real property. Protecting purchasers and lenders against loss is accomplished by the issuance of a title insurance policy. Usually, during a purchase transaction, the lender requests a policy (commonly referred to as the Lender’s Policy) while the buyers receive their own policy (commonly referred to as an Owner's Policy).

In short, the policy states that if the status of the title to a parcel of real property is other than as represented, and if the insured (either the owner or lender) suffers a loss as a result of a title defect, the insurer will reimburse the insured for that loss and any related legal expenses, up to the face amount of the policy, subject to exceptions and exclusions contained in the policy.

Typically there are two policies issued. The Mortgagee’s Policy insures the lender for the amount of the loan. The Owner’s Policy insures the purchaser of the purchase price.

How is title insurance different from other types of insurance?

While the function of most other forms of insurance is risk assumption through the pooling of risks for losses arising out of unforeseen future events (such as sickness or accidents), the primary purpose of title insurance is to eliminate risks and prevent losses caused by defects in title arising out of events that have happened in the past. To achieve this goal, title insurers perform an extensive search and examination of the public records to determine whether there are any adverse claims (title defects) attached to the subject property. Said defects/claims are either eliminated prior to the issuance of a title policy

or their existence is excepted from coverage. Your policy is issued after the closing of your new home, for a one-time nominal fee, and is good for as long as you own the property.

What’s involved in a title search? A title search is actually made up of three separate searches:

Chain of Title – History of the ownership of the subject property

Tax Search – The tax search reveals the status of the taxes and assessments

Judgment and Name Search – Searches for judgment and liens against the owners’ and purchasers’ names

Once the three searches have been completed, the file is reviewed by an examiner who determines:

Whether or not the Chain of Title shows that the party selling the property has the right to do so. The status of taxes for the subject property. The Tax Search will also indicate the existence of any special assessments against the land and whether or not these assessments are current or past due.

Whether there are any unsatisfied judgments on the Judgment and Name Search against the previous owners, sellers, or and purchasers.

Rights established by judgment decrees, unpaid federal income taxes and mechanic liens all may be prior claims on the property, ahead of the buyer’s or lender’s rights. The title search will only uncover defects in title that are of public record, thus allowing the title company to work with the seller to clear up these issues and provide the new buyer with title insurance.

In Summary

After the searches have been examined, the title company will issue a commitment, stating the conditions under which it will insure title. The buyer, seller and the mortgage lender will proceed with the closing of the transaction after clearing up any defects in the title that have been uncovered by the search and examination.

.

WHO PAYS WHAT IN NEVADA

SELLER PAYS

BUYER PAYS

TYPICAL COSTS

Real Estate Commission

Document preparation fee for Deed

Payoff of all loans in the seller’s name (or existing loan balance if being assumed by Buyer)

Interest accrued to lender being paid off Statement Fees, Reconveyance Fees, and any prepayment penalties to Payoff Lender

Termite Inspection (according to contract)

Home Warranty (according to contract)

Any judgments, tax liens, etc. against the seller

Tax proration (for any taxes unpaid at time of transfer of title)

Any unpaid Homeowners’ Association dues

Recording charges to clear documents of record against seller

Any bonds or assessments (according to contract)

Any and all delinquent taxes

Notary Fees

Escrow Fee (one half)

Title Insurance Premium of Owner’s Policy

Personal Property vs. Real Property

TYPICAL COSTS

Title Insurance Premium for Lender’s Policy

Escrow Fee (one half)

Document preparation (if applicable)

Notary fees

Recording charges for all documents in Buyer’s name

Termite Inspection (according to contract)

Tax proration (from date of acquisition)

Homeowners’ Association transfer fee

HOA proration (from date of acquisition)

All new loan charges (except those required by lender for seller to pay)

Interest on new loan from date of funding to 30 days prior to first payment date

Assumption/Change of Record fees for takeover of existing loan (if applicable)

Beneficiary Statement Fee for assumption of existing loan (if applicable)

The distinction between personal property and real property can be the source of difficulties in a real estate transaction. A purchase contract is normally written to include all real property; that is, all aspects of the property that are fastened down or which are an integral part of the structure. For example, this would include light fixtures, drapery rods, attached mirrors, and trees and shrubs in the ground. It would not include potted plants, free-standing refrigerators, washer/dryer, microwave, bookcases, lamps, etc. If there is any uncertainty whether an item is included in the sale or not, it is best to be sure that the particular item is mentioned in the purchase agreement as being included or excluded.

TITLE VESTING Common ways to hold title to real property

SOLE OWNERSHIP

A man or woman who is not married. An unmarried man/woman. A man or woman, who having been married are legally divorced. A married man/woman, as his/her Sole and separate property: when a married man or woman wishes to acquire title as their sole and separate property, the spouse must consent and relinquish all right, title, and interest in the property by signing a disclaimer deed or other written agreement.

CO-OWNERSHIP

Community Property with Right of Survivorship

Under this form of property ownership, both spouses hold undivided shares of the whole. When one spouse dies, the surviving spouse gains ownership of the whole property without the need for probate, and both halves receive a new tax basis equal to the fair market values as of the date of death.

Community Property

Any property acquired during a valid marriage is presumed to be community property. Excluded is any property acquired by gift, bequest, devise, descent, or as the separate property of either.

Joint Tenancy

Joint and equal interests in land owned by two or more individuals created under a single instrument with right of survivorship.

Tenancy In Common

Under tenancy in common, the co-owners own undivided interests; but unlike joint tenancy, these interests need not be equal in quantity and may arise at different times. There is no right of survivorship; each tenant owns an interest, which on his or her death vests in his or her heirs or devisee.

Note: Nevada is a community property state and property that is acquired by a husband and wife is presumed to be community property unless legally specified otherwise. Title may be held by one spouse as “Sole and Separate,” if the married person acquires title as sole and separate, and his or her spouse executes a Disclaimer Deed to avoid the presumption of community property. Parties may choose to hold title in the name of an entity, e.g., a trust, corporation, or a limited liability company (general or limited). Each method of taking title has certain significant legal and tax consequences, therefore, you are encouraged to seek and obtain advice from an attorney or other qualified professional.

ARROYO CROSSING

7450 Arroyo Crossing Parkway Suite 270

Las Vegas, NV 89113

702-777-8292

HENDERSON

9041 S Pecos Road Suite 4200 Henderson, NV 89074

702-789-7201

SAHARA

702-728-5295 1 2 3

9580 W Sahara Avenue Suite 120

Las Vegas NV 89117

4

ELKO

905 Railroad Street Suite 204 Elko, NV 89801

775-440-6377

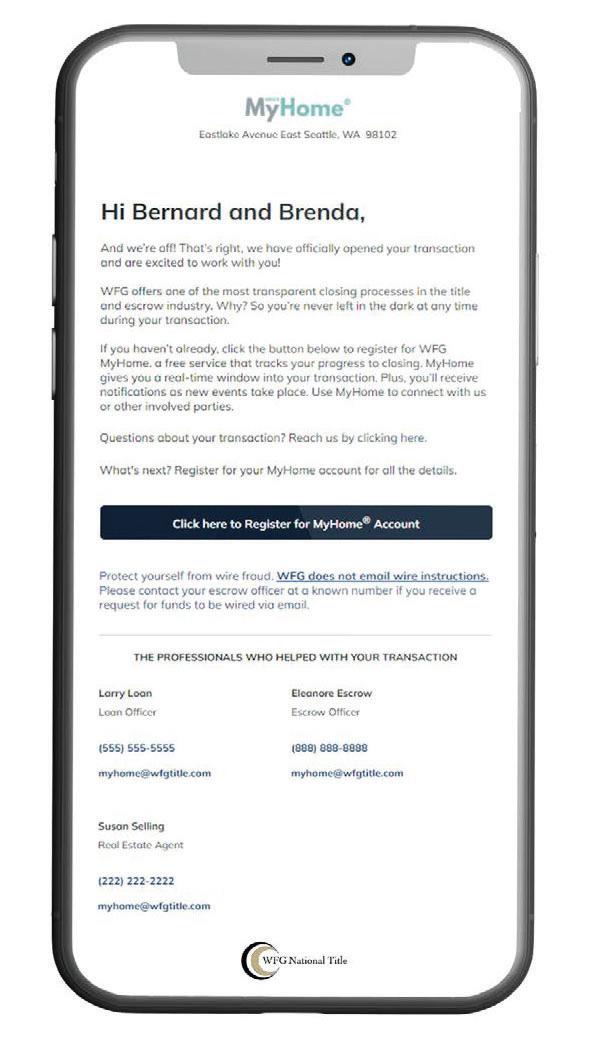

Altos Market Report

WFG's My Home

The information contained is provided by WFG’s Customer Service Department to our customers, and while deemed reliable, is not guaranteed.

Las Vegas, NV 89144

REPORT FOR 4/11/2025

Single-Family Homes

This week the median list price for Las Vegas, NV 89144 is $749,999 with the market action index hovering around 43. This is less than last month's market action index of 44 Inventory has increased to 51

Market Action Index

This answers “How’s the Market?” by comparing rate of sales versus inventory

Real-Time Market Profile

Slight Seller's Advantage

Market Narrative

In the last few weeks the market has achieved a relative stasis point in terms of sales to inventory However, inventory is sufficiently low to keep us in the Seller’s Market zone so watch changes in the MAI If the market heats up, prices are likely to resume an upward climb

Market Segments

Each segment below represents approximately 25% of the market ordered by price

Advantage

Median List Price

Again this week we see prices in this zip code remain roughly at the level they’ve been for several weeks. Since we’re significantly below the top of the market, look for a persistent up-shift in the Market Action Index before we see prices move from these levels.

Segments

In the quartile market segments, we see prices in this zip code generally settled at a plateau, although Quartile 1 is on a bit of an up trend in recent weeks. We'll need to see a persistent shift in the Market Action Index before we see prices across the board move from these levels.

Price Per Square Foot

The market plateau is seen across the price and value. The price per square foot and median list price have both been reasonably stagnant. Watch the Market Action Index for persistent changes as a leading indicator before the market moves from these levels.

Inventory has been climbing lately. Note that rising inventory alone does not signal a weakening market. Look to the Market Action Index and Days on Market trends to gauge whether buyer interest is keeping up with available supply.

Market Action Index

In the last few weeks the market has achieved a relative stasis point in terms of sales to inventory. However, inventory is sufficiently low to keep us in the Seller’s Market zone so watch changes in the MAI. If the market heats up, prices are likely to resume an upward climb.

Market Action Segments

Not surprisingly, all segments in this zip code are showing high levels of demand. Watch the quartiles for changes before the whole market changes. Often one end of the market (e.g. the highend) will weaken before the rest of the market and signal a slowdown for the whole group.

Median Days on Market (DOM)

The properties have been on the market for an average of 85 days. Half of the listings have come newly on the market in the past 56 or so days. Watch the 90-day DOM trend for signals of a changing market.

Segments

It is not uncommon for the higher priced homes in an area to take longer to sell than those in the lower quartiles.

• Instant access to

WFG’s MyHome® provides full transparency, real-time updates, and post-closing home information in a secure built with YOU in mind.

Sign up for an account at https://myhome.wfgtitle.com today!

Click Register for MyHome® account on a MyHome® email to https://myhome. wfgtitle.com

Complete a brief registration form. Use your email address on immediate access.