Russell Berrien brings a distinctive blend of discipline, global perspective, and refined strategy to luxury real estate. A proud alumnus of Oklahoma State University with a degree in Sociology, and a master’sfrom the University of Colorado’s Graduate School of Public Affairs, Russell combines academic insight with real-world expertise to guide clients through complex, high-end transactions. His early affiliation with Tinker Air Force Base instilled in him a strong sense of integrity, precision, and commitment principles that now define his client relationships.

Aformer All-State athlete and two-time Oklahoma state champion in football and track, Russell went on to compete at the collegiate level for the Oklahoma State Cowboysfrom 1990 to1995. That same competitive spirit and team-first mindset nowfuel his real estate success, whether negotiating for buyers or curating exceptional experiencesfor luxury sellers.

Now with Keller Williams Realty, Russell pairs his passion for international travel, fine living, and upscale dining with a sharp eyefor investment and value. He is guided by the timeless principle: “Don’t wait to buy real estate, buy real estate and wait.”

For clients seeking an experienced, insightful partner in real estate, Russell delivers results rooted in trust, strategy, and excellence.

Property Details

Maps

Local Schools

Community Utilities & Resources

Title & Escrow

The information contained is provided by WFG’s Customer Service Department to our customers, and while deemed reliable, is not guaranteed.

This map/plat is being furnished as an aid in locating described land in relation to adjoining streets, natural boundaries and other land, and is not a survey of the land depicted. Except to the extent a policy of title insurance is expressly modified by endorsement, if any, the company does not insure dimensions, distances, location of easements, acreage or other matters shown thereon.

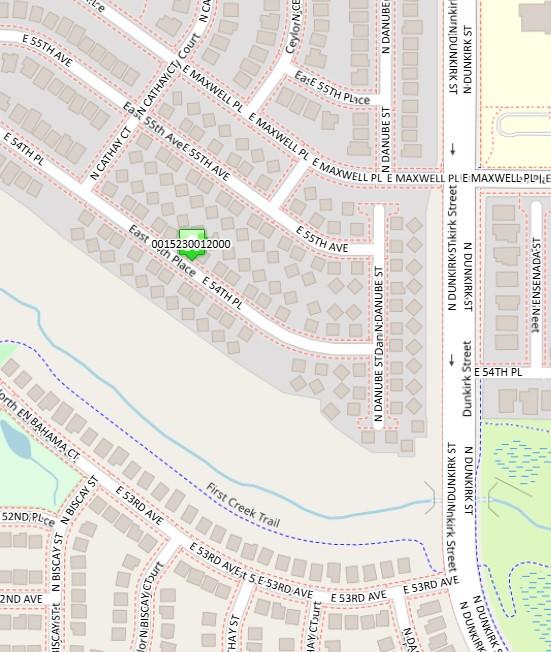

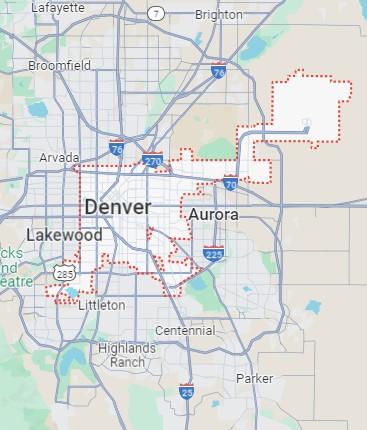

STREET MAP

This map/plat is being furnished as an aid in locating described land in relation to adjoining streets, natural boundaries and other land, and is not a survey of the land depicted. Except to the extent a policy of title insurance is expressly modified by endorsement, if any, the company does not insure dimensions, distances, location of easements, acreage or other matters shown thereon.

AERIAL MAP

This map/plat is being furnished as an aid in locating described land in relation to adjoining streets, natural boundaries and other land, and is not a survey of the land depicted. Except to the extent a policy of title insurance is expressly modified by endorsement, if any, the company does not insure dimensions, distances, location of easements, acreage or other matters shown thereon.

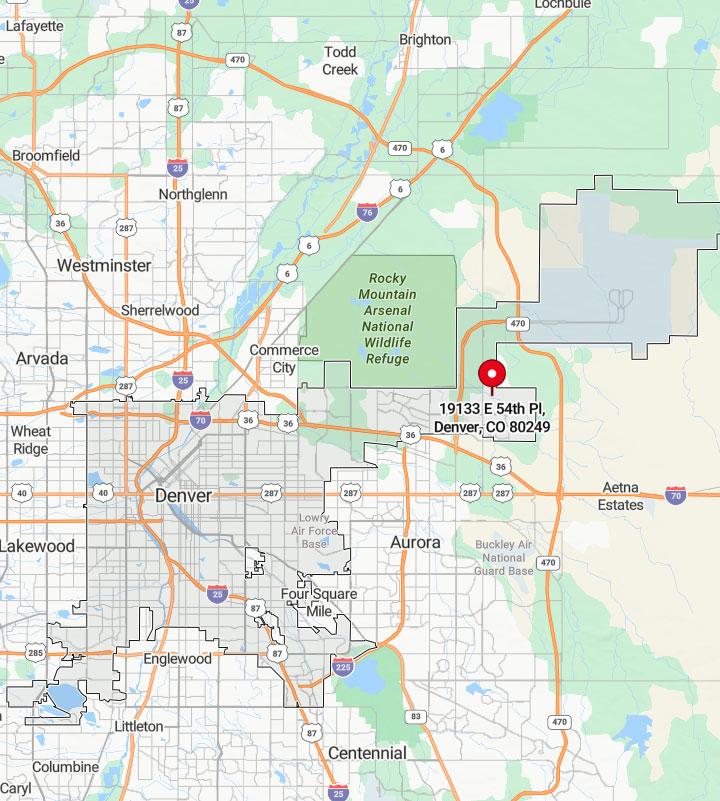

CITY BOUNDARY MAP

This map/plat is being furnished as an aid in locating described land in relation to adjoining streets, natural boundaries and other land, and is not a survey of the land depicted. Except to the extent a policy of title insurance is expressly modified by endorsement, if any, the company does not insure dimensions, distances, location of easements, acreage or other matters shown thereon.

What strategies have been put in place to address root causes?

2024-25

Where is the district focusing its attention? What issues underlie these challenges?

List continues. Click below to view more. Ineffective System for Differentiation and Culturally/Linguistically Resp. Prac. Ineffective Student Engagement (Attendance) Systems Inconsistent connections with families Teaching and Learning Safe and Welcoming

Post-Secondary ReadinessGraduation gaps List continues. Click below to view more.

Student Achievement: Early Literacy results are below expectations

What strategies have been put in place to address root causes?

2024-25

COMMUNITY

CITY OF DENVER

715,522 POPULATION

$48,195

MEDIAN INCOME

Denver is nicknamed the "Mile High City" because its official elevation is exactly one mile (5280 feet or 1609.344 meters) above sea level.[a][24] The 105th meridian west of Greenwich, the longitudinal reference for the Mountain Time Zone, passes directly through Denver Union Station. The 10-county Denver–Aurora–Lakewood, CO Metropolitan Statistical Area had a population of 2,963,821 at the 2020 United States census, making it the 19th most populous U.S. metropolitan statistical area

SCHOOL DISTRICTS

Denver Public Schools

Cherry Creek School District

HOUSING

2010 Census Data

19.55% of homes owner occupied

80.45% of homes rented

POPULATION DENSITY

2000 Census Data

3,922.6 inhabitants per sq. mile

338,341 housing units at an average density of 1,751 per sq. mile

AGE DEMOGRAPHIC

2010 Census Data

22.0% under age 18

10.7% between ages 18 to 24

36.1% between ages 25 to 44

20.0% between ages 45 to 64

11.3% above age 65

CITY QUICK FACTS

Most populous city in Colorado 19th most populous city in the United States

154.726 square miles

5,280 feet elevation

Highest Average Temperature 89.9º

Lowest Average Temperature 18º

The discovery in November 1858 of gold in the Rocky Mountains in Colorado (then part of the western Kansas Territory) brought on a gold rush and a consequent flood of white immigration across Cheyenne and Arapaho lands. Colorado territorial officials pressured federal authorities to redefine and reduce the extent of Indian treaty lands.

Denver County School District 1 (720) 423-3200 www.dpsk12.org

CHANGE OF ADDRESS

USPS

Below is the website if you would like to change your address online or you can visit your local post o ce, they will provide you with the change of address packet.

https://moversguide.usps.com

Bene ts you will receive when you change your address online are:

♦ Exclusive mover savings coupons

♦ Safe and secure with identity veri cation by a simple $1.00 charge to your credit or debt card

♦ Email con rmation at the end of registration of your change of address

* Must have valid email address and credit card to register online.

Colorado Department of Transportation

Below is the website if you would like to change your address online or have any questions.

Region 1 and Headquarters

Denver/Central Colorado 2829 W Howard Place Denver, CO 80204 (303) 759-2368

www.codot.gov

VOTER REGISTRATION

Below is the website if you would like to change your address online or you can ll out the paperwork provided and mail it back to your County Elections O ce listed below.

sos.state.co.us/voter/pages/pub/home.xhtml

County Elections O ce Contacts

Adams County

4430 S Adams County Pkwy 1st Floor, Suite E3102 Brighton, CO 80601 (720) 523-6500

Arapahoe County

5334 S Prince St Littleton, CO 80120 (303) 795-4511

Boulder County 1750 33rd St, Suite 200 Boulder, CO 80301 (303) 413-7740

Broom eld County One DesCombes Dr Broom eld, CO 80020 (303) 438-6332

Denver County 200 W 14th Ave Denver, CO 80204 (720) 913-8683

Douglas County 125 Stephanie Place Castle Rock, CO 80109 (303) 660-7444

El Paso County 1675 W Garden of the Gods Rd Suite 2201 Colorado Springs, CO 80907 (719) 520-6202

Je erson County 3500 Illinois Street, Suite 1100 Golden, CO 80401 (303) 271-8168

Retirement (Pension plans, 401K, Social Security, Veterans A airs)

Investments

(Investment Agencies and Brokers)

Online Bill Payer

Paypal

GOVERNMENT OFFICES

US Post O ce

Department of Motor Vehicles

(Obtain your driver’s license and change vehicle registration)

IRS

Passport O ce

Veteran A airs

Unemployment O ce

(If you are currently receiving unemployment bene ts)

HEALTH

Physician

Pharmacies

SERVICE PROVIDERS

Childcare

Housecleaning Services

Delivery Services

Lawn Care Services

Veterinarian

Pool Service

MEMBERSHIPS

Health Clubs

Membership Clubs (AAA or similar)

Community Groups (PTA, Neighborhood Associations, Civic Clubs)

Children’s Extracurricular Activities (Dance Classes, Music Lesson, Sports Clubs)

SUBSCRIPTIONS

Newspapers

Magazine (USPS will only forward 2 months)

Movie Subscriptions

(Net ix, Blockbuster, etc)

Book or Music Clubs

OTHER

Friends and Family Employers

(typically notify the Human Resources Department)

MOVING CHECKLIST

8 WEEKS BEFORE YOUR MOVE

Inventory Sheets: Create an inventory sheet of all your belongings which need to be moved

Research Moving Options: You’ll need to decide if yours is a do-it-yourself move or if you’ll be using a moving company.

Request Moving Quote: Solicit moving quotes from as many moving companies and movers as possible. There can be a large di erence between rates and services within moving companies.

Discard Unnecessary Items: Moving is a great time for ridding yourself of unnecessary items. Have a yard sale or donate unnecessary items to charity.

Packing Material: Gather moving boxes and packing material for your move.

Contact Insurance Companies: You’ll need to contact your insurance agent to cancel/transfer your insurance policy.

4 WEEKS BEFORE YOUR MOVE

Start Packing: Begin packing all things destined for your new location.

Obtain Your Medical Records: Contact your doctor, physician, dentist and other medical specialists who may currently be retaining any of your family’s medical records. Obtain these records or make plans for them to be delivered to your new medical facilities if changing. Security is critical of personal records.

Note Food Inventory Levels: Check your cupboards, refrigerator and freezer. Use up as much of your perishable food as possible.

Small Engines: Service small engines for your move by extracting gas and oil from the machines. This will reduce that chance to catch re during your move.

Protect Jewelry and Valuables: Transfer your jewelry and valuables to a safety deposit box; you don’t want them to be lost or stolen during your move.

Borrowed and Rented Items: Return items which you may have borrowed or rented. Collect items borrowed to others.

1 WEEK BEFORE YOUR MOVE

Your Change of Address: Change your address with the USPS, DMV, Financial Institutions, Utilities, Government O ces, Health Care Service Providers, Memberships, Subscriptions and Insurance Provisions.

Bank Accounts: Transfer or close bank accounts if changing banks. Make sure to have a money order for paying the moving company.

Service Automobiles: If automobiles are to be driven long distance, you’ll want to have them serviced so you have a trouble-free drive.

Cancel Services: Notify any remaining service providers (newspapers, lawn services, etc.) of your move.

Travel Items: Set aside all items you’ll need while traveling. Make sure these are not packed on the moving truck..

Contact Utility Companies: Set utility turno date, seek refunds and deposits and notify them of your new address.

MOVING DAY

Plan Your Itinerary: Make plans to spend the entire day at the house or at least until the movers are on their way. Someone will need to be around to make decisions. Make plans for kids and pets to be at a sitters for the day.

Review the House: Once the house is empty, check the entire house (closets, attic, basement, etc.) to ensure no items are left or no home issues exist.

Double Check With Your Mover: Ensure the mover has the new property address and all of your most recent contact information, should they have any questions during your move.

Vacate Your Home: Make sure utilities are o , doors and windows are locked and notify your real estate agent you’ve vacated the property.

Questions To Ask: Where is the garage door opener? Where are the keys to the house, mailbox and other lockable area? Did you retrieve all keys from neighbors and friends?

AIRPORT

RESOURCE GUIDE

Denver International Airport (720) 730-4359 www. ydenver.com

AUTO & DRIVER REGISTRATION

Department of Transportation (303) 759-2368 www.codot.gov

Arapahoe Marketplace 8505 E Arapahoe Rd Greenwood Village, CO

Arapahoe Crossings 6400-6700 S Park Rd Aurora, CO

Bowles Crossing 8055 W Bowles Ave Littleton, CO

Centennial Promenade 9555 E County Line Rd Centennial, CO

Chapel Hills Mall 1710 Briargate Blvd Colorado Springs, CO

Cherry Creek North 299 Milwaukee St Denver, CO

Cherry Creek 3000 E 1st Ave Denver, CO

Citadel Mall 750 Citadel Dr E Colorado Springs, CO

Colorado Mills 14520 W Colfax Ave Lakewood, CO

RESOURCE GUIDE

SHOPPING

Denver Pavilions 16th Street Mall and Glenarm Pl Denver, CO

Downtown Boulder Pearl Street and Broadway Boulder, CO

Festival Shopping Center 8110 S University Blvd www.festivalshoppingcenter.com

FlatIron Crossing One W Flatiron Crossing Dr Broom eld, CO

Heritage Hills 9227 Lincoln Ave Lone Tree, CO

Larimer Square 1430 Larimer Denver, CO

Marketplace at Northglenn 104th Ave and I-25 Denver, CO

Marina Square

8101 E Belleview Ave Denver, CO

Oakbrook

311 E County Line Rd Littleton, CO

Outlets at Castle Rock

5050 Factory Shops Blvd Castle Rock, CO

Park Meadows 8401 Park Meadows Center Dr Lone Tree, CO

Shops at Highland Walk 4000 Red Cedar Dr Highlands Ranch, CO

Southlands E Smoky Hill Rd and E-470 Aurora, CO

SHOPPING

Shops at Highland Walk 4000 Red Cedar Dr Highlands Ranch, CO

Southwest Plaza 8501 W Bowles Ave Littleton, CO

The Streets at SouthGlenn 6991 S Vine St Centennial, CO

Town Center at Aurora 14200 E Alameda Ave Aurora, CO

Twenty Ninth Street

Arapahoe Ave and 28th St Boulder, CO

Willow Creek 8200 S Quebec St Centennial, CO

Village at the Peaks 1250 S Hover Rd Longmont, CO

TRANSFER STATIONS

Colorado Springs Transfer Station

wmsolutions.com 1965 Commercial Blvd Colorado Springs, CO 80906

South Metro Transfer Station wmsolutions.com 2400 West Union Avenue Englewood, CO 80110

D&R Transfer Station wmsolutions.com 6091 Brighton Blvd Commerce City, CO 80022

VOTER REGISTRATION

Adams County 4430 S Adams County Pkwy 1st Floor, Suite E3102 Brighton, CO 80601 (720) 523-6500

Arapahoe County 5334 S Prince St Littleton, CO 80120 (303) 795-4511

Boulder County 1750 33rd St, Suite 200 Boulder, CO 80301 (303) 413-7740

Broom eld County One DesCombes Dr Broom eld, CO 80020 (303) 438-6332

Denver County 200 W 14th Ave Denver, CO 80204 (720) 913-8683

Douglas County 125 Stephanie Place Castle Rock, CO 80109 (303) 660-7444

El Paso County 1675 W Garden of the Gods Suite 2201 Colorado Springs, CO 80907 (719) 520-6202

Je erson County

3500 Illinois Street, Suite 1100 Golden, CO 80401 (303) 271-8168

TITLE & ESCROW

CYBER SECURITY

Because of you… we obsess over

cyber security!

Cyber fraud and email hacking is on the rise. Fraudsters may access individual email accounts and monitor the life of your transaction. At the time funds are due to the escrow, fraudsters intercept the information for wiring funds and the fraudsters change the information without the knowledge of the sender or recipient, resulting in the funds being sent to an outside account and never credited to the intended party.

To protect and reduce your risk, WFG has implemented the following procedures for outgoing and incoming wires:

Outgoing Wire from WFG to seller or borrower for proceeds

In the escrow paperwork provided you will be asked to provide written instructions on how you want funds dispersed at the close of escrow. If you choose to have the funds sent via wire transfer, WFG will contact you by phone to con rm the wire information provided.

Incoming Wires from buyer and/or lender to WFG bank account

For funds that are to be wired to WFG for your transaction, we will send speci c wire instructions to the remitting person via an encrypted email. We recommend you reach out to your WFG contact to con rm the wire instructions prior to remittance.

We look forward to processing your escrow transaction for you. We know that this can be a stressful time and we are here to assist you in any way we can to make this a good experience.

PROTECT YOUR MONEY WHEN BUYING A HOME: YOUR WIRE FRAUD CHECKLIST

Every day, hackers try to steal your money by emailing fake wire instructions. Criminals will use a similar email address and steal a logo and other info to make it look like the email came from your real estate agent or title company. You can protect yourself and your money by following the steps below.

Don’t send sensitive nancial information via email.

Call, don’t email. Con rm your wiring instructions by phone using a known number before transferring funds.

We will never email wiring instructions to you nor change WFG account information after it’s been provided to you by our sta .

Keep your email account clean, remove any stale messages. Hackers can watch your business patterns and use this information against you.

Ask your bank to con rm the name on the account before sending a wire.

Call your title company or real estate agent within four to eight hours to con rm they have received your money.

This is for informational purposes only and should not be considered legal advice.

WHY IS OWNER’S TITLE INSURANCE IMPORTANT?

The purchase of a home is likely going to be one of the most expensive and important purchases you will ever make. You and your mortgage lender want to make sure the property is indeed yours and that no individual or government entity has any right, lien, claim, or encumbrance to your property.

The title insurance company’s function is to make sure your rights and interests to the property are clear, that transfer of title takes place e ciently, and correctly, and your interests as a homebuyer are protected. Title insurance companies provide services to buyers, sellers, real estate developers and builders, mortgage lenders, and others who have an interest in the real estate transfer. Title companies issue two types of policies - “Owners Policy” (which covers the homebuyer) and “Lenders Policy” (which covers the bank, savings and loan, or other lending institution over the life of a loan). Both are issued at the time of purchase for a one-time premium.

The title company conducts an extensive search of public records to determine if anyone other than you has an interest in the property before issuing a policy. The search may be performed by title company personnel using either public records, or more likely, information gathered, reorganized, and indexed in the company’s title “plant”. With such a thorough examination of records, title problems can usually be found and cleared up prior to purchase of the property. Once a title policy is issued, if for some reason any claim, which is covered under your title policy, is ever led against your property, the title company will pay the legal fees involved in defense of your rights as well as any covered loss arising from a valid claim. That protection, which is in e ect as long as you or your heirs own the property, is yours for a one-time premium paid at the time of purchase.

The title company works to eliminate risks before they develop. This makes title insurance di erent from other types of insurance. Most forms of insurance assume risks by providing nancial protection through a pooling of risks or losses arising from unforeseen events, like re, theft, or accident. The purpose of title insurance, on the other hand, is to eliminate risks and prevent losses caused by defects in title that happened in the past. Risks are examined and mitigated before property changes hands. Eliminating risk has bene ts to both of you, the home buyer, as well as the title company. It reduces the chance adverse claims might be raised, and by doing so reduces the number of claims that have to be defended or satis ed. This keeps costs down for the title company and your title premiums low. With title insurance you are assured that any valid claim against your property will be taken on by the title company, and that the odds of a claim being led is slim.

WHAT IS ESCROW

When your o er has been accepted and conveyed, escrow is opened. An escrow is an arrangement made under contract between a buyer and seller. As the neutral third party, escrow is responsible for receiving and disbursing money and/ or documents. Both the buyer and seller expect the escrow agent to carry out their written instructions associated with the transaction and also to advise them if any of their instructions are not being met, or cannot be met. If the instructions from all parties to an escrow are clearly set out, the escrow o cer can proceed on behalf of the buyer and seller without further consultation.

TYPICAL ROLES IN THE CLOSING PROCESS

The Seller/Agent

• Delivers Purchase Sale Agreement to the escrow agent

• Prepares the paperwork necessary to close the transaction

• Approves the commitment for title insurance, or other items as called for by the Purchase Sale Agreement

The Buyer/Agent

• Deposits funds required to close with the escrow agent

• Executes the paperwork and loan documents necessary to close the transaction

The Lender

• Deposits loan documents to be provided by the buyer

• Deposits the loan funds

• Informs the escrow agent of the conditions under which the loan funds may be used

The Escrow Agent

• Clears Title

• Obtains title insurance

• Obtains payo s and release documents for underlying loans on the property

• Receives funds from the buyer and/or lender

• Prepares vesting document a davit on seller’s behalf

• Prorates insurance, taxes, rents, etc.

• Prepares a nal statement (often referred to as the Closing Disclosure or CD) for each party, indicating amounts paid in conjunction with the closing of your transaction

• Forwards deed to the county for recording

• Once the proper documents have been recorded, the escrow agent will distribute funds to the proper parties

Escrow is the process that gathers and processes many of the components of a real estate transaction. The escrow agent is a neutral third party acting on behalf of the buyer and seller.

WHAT IS TITLE

Title insurance insures against nancial loss from defects in title, liens, or other matters. It protects both purchasers and lenders against loss by the issuance of a title insurance policy. Usually, during a purchase transaction the lender requests a policy (commonly referred to as the Lender’s Policy) while the buyers receive their own policy (commonly referred to as an Owner’s Policy).

It will protect against lawsuits if the status of the title to a parcel or real property is other than as represented, and if the insured (either the owner or lender) su ers a loss as a result of a title defect. The insurer will reimburse the insured for that loss and any related legal expenses.

How is title insurance di erent than other types of insurance?

While the purpose of most other types of insurance is to assume risk through the pooling of monies for losses happening because of unforeseen future events (like sickness or accidents), the primary purpose of title insurance is to eliminate risks and prevent losses caused by defects in title arising out of events that have happened in the past. To achieve this, title insurers perform a thorough search and examination of the public records to determine whether there are any adverse claims (title defects) attached to the subject property. These defects/claims are either eliminated prior to the issuance of a title policy or their existence is excepted from coverage. The policy is issued after the closing of your new home, for a one time nominal fee, and is good for as long as you own the property.

What’s involved in a title search?

A title search is made up of three separate searches:

• Chain of Title – History of the ownership of the subject property

• Lien & Encumbrance Search – Discloses liens and encumbrances on the subject property

• Exceptions from Coverage Search –Includes Easements, Covenants, Conditions and Restrictions, etc.

After the three searches have been completed, the le is reviewed by an examiner who determines:

• If the Chain of Title shows that the party selling the property has the rights to do so.

• Whether there are any unsatis ed judgments on the Judgment and Name Search against the previous owners, sellers, or/and purchasers.

Rights established by judgment decrees, unpaid federal income taxes, and mechanics liens all may be prior claims on the property, ahead of the buyer’s or lender’s rights. The title search will only uncover issues in title that are of public record and therefore allowing the title company to work with the seller to clear up these issues and provide the new buyer with title insurance.

Once the searches have been examined, the title company will issue a commitment, stating the conditions under which it will insure title. The buyer, seller, and the mortgage lender will proceed with the closing of the transaction after clearing up any defects in the title that have been uncovered by the search and examination.

WHO PAYS FOR WHAT IN COLORADO

The examples below are typical. However, the real estate purchase agreement will ultimately determine who is paying for what expenses.

The Seller

• Real Estate Commission

• Document preparation fee for Deed

• Payo of all loans in the seller’s name (or existing loan balance if being assumed by Buyer)

• Interest accrued to lender being paid o

• Statement Fees, Reconveyance Fees, and any prepayment penalties to Payo Lender

• Home Warranty (according to contract)

• Any judgments, tax liens, etc. against the seller

• Tax proration (for any taxes unpaid at time of transfer of title)

• Any unpaid Homeowners’ Association dues

• Recording charges to clear documents of record against seller

• Any bonds or assessments (according to contract)

• Any and all delinquent taxes

• Notary Fees

Personal Property vs. Real Property

The Buyer

• Title Insurance Premium for Lender’s Policy

• Escrow Fee (one half)

• Document preparation (if applicable)

• Notary fees

• Recording charges for all documents in Buyers’ names

• Tax proration (from date of acquisition)

• Homeowners’ Association transfer fee

• HOA proration (from date of acquisition)

• All new loan charges (except those required by lender for seller to pay

• Interest on new loan from date of funding to 30 days prior to rst payment date

• Assumption/Change of Record fees for takeover of existing loan (if applicable)

• Bene ciary Statement Fee for assumption of existing loan (if applicable)

• Any bonds or assessments (according to contract)

The distinction between personal property and real property can be the source of di culties in a real estate transaction. A purchase contract is normally written to include all real property; that is, all aspects of the property that are fastened down or which are an integral part of the structure. For example, this would include light xtures, drapery rods, attached mirrors, and trees and shrubs in the ground. It would not include potted plants, free-standing refrigerators, washer/dryer, microwave, bookcases, lamps, etc. If there is any uncertainty whether an item is included in the sale or not, it is best to be sure that the particular item is mentioned in the purchase agreement as being included or excluded.

DISCLAIMER:

This information is provided for informational purposes only and no warranties are made.

TITLE VESTING

TENANCY IN SEVERALTY

Ownership of property vested in one person rather than held jointly with another.

JOINT TENANCY WITH RIGHT OF SURVIVORSHIP TENANCY IN COMMON

Parties need not be married; may be more than two persons.

Parties need not be married; may be more than two persons.

Also called sole tenancy.

The sole owner may use, encumber, rent, sell, and convey at their discretion.

The owner may transfer the property via a Will, Trust, or a Bene ciary Deed upon their death.

Each joint tenant holds an equal and undivided interest in the estate, unity of interest.

Upon death, the estate of the decedent must be “cleared” through probate or adjudication.

One joint tenant can partition the property by selling his or her joint interest.

Each joint tenant holds an undivided fractional interest in the estate. May be disproportionate interest e.g. 20% and 80%; 40% and 60%; etc.

Each tenant’s share can be conveyed, mortgaged, or devised to a third party.

Requires signatures of all joint tenants to convey or encumber the whole.

Requires signatures of all to convey or encumber the whole.

Estate passes to surviving joint tenants outside of probate.

No court action required to “clear” title upon the death of joint tenant(s).

Upon death, the tenant’s proportionate share passes to his or her heirs by will or intestacy.

Upon death, the estate of the decedent must be “cleared” through probate or adjudication.

DISCLAIMER – The foregoing contains informational examples only and is not to be construed as legal advice. Given the complexities involved in acquiring and holding legal title to real property, WFG strongly recommends that you seek legal advice from an attorney prior to doing so.

55 Madison Street, Suite 690

Denver, CO 80206 (720) 475-8325

NORTH

12050 N Pescos Street, Suite 110 Westminster, CO 80234 (720) 475-8350

8610 Explorer Drive, Suite 105

Colorado Springs, CO 80920 (719) 598-5355

7800 E Union Avenue, Suite 310 Denver, CO 80237 (720) 475-8300

3. DENVER TECH CENTER / COMMERCIAL

4.

METRO OFFICE

2. COLORADO SPRINGS OFFICE

1. CHERRY CREEK OFFICE

TABLE OF CONTENTS

Altos Market Report

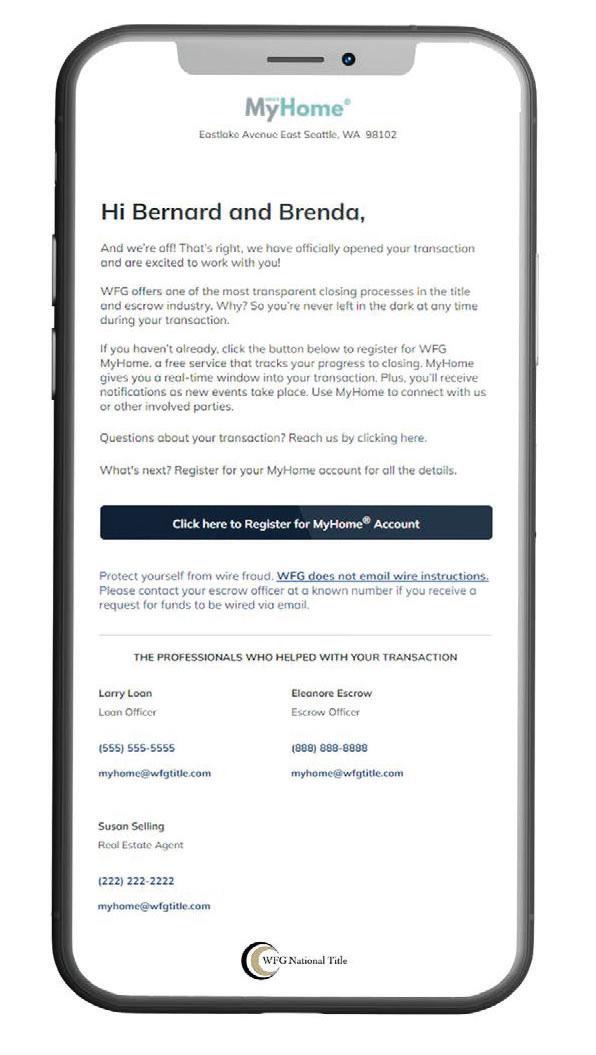

WFG’s My Home

Talking House Tent Cards

CC&R’s (if applicable)

The information contained is provided by WFG’s Customer Service Department to our customers, and while deemed reliable, is not guaranteed.

Denver, CO

REPORT FOR 5/22/2025

Single-Family Homes

This week the median list price for Denver, CO 80249 is $509,900 with the market action index hovering around 36. This is less than last month's market action index of 37. Inventory has increased to 115.

Market Action Index

This answers “How’s the Market?” by comparing rate of sales versus inventory.

Slight Seller's Advantage

Market Narrative

The market has been cooling over time and prices plateaued for a while. Despite the consistent decrease in MAI, we’re in the Seller’s zone. Watch for changes in MAI. If the MAI resumes its climb, prices will likely follow suit. If the MAI drops consistently or falls into the Buyer’s zone, watch for downward pressure on prices.

Market Segments

Each segment below represents approximately 25% of the market ordered by price.

Median List Price

Again this week we see prices in this zip code remain roughly at the level they’ve been for several weeks. Since we’re significantly below the top of the market, look for a persistent up-shift in the Market Action Index before we see prices move from these levels.

Segments

In the quartile market segments, we see prices in this zip code have settled at a price plateau across the board. Prices in all four quartiles are basically mixed. Look for a persistent shift (up or down) in the Market Action Index before prices move from these current levels.

Price Per Square Foot

While prices have been basically flat, the price per square foot has been heading downward. While not a sign of broad strength in a market, larger homes are coming more available and buyers are tending to get more home for their money.

Inventory has been climbing lately. Note that rising inventory alone does not signal a weakening market. Look to the Market Action Index and Days on Market trends to gauge whether buyer interest is keeping up with available supply.

Market Action Index

The market has been cooling over time and prices plateaued for a while. Despite the consistent decrease in MAI, we’re in the Seller’s zone. Watch for changes in MAI. If the MAI resumes its climb, prices will likely follow suit. If the MAI drops consistently or falls into the Buyer’s zone, watch for downward pressure on prices.

Not surprisingly, all segments in this zip code are showing high levels of demand. Watch the quartiles for changes before the whole market changes. Often one end of the market (e.g. the highend) will weaken before the rest of the market and signal a slowdown for the whole group.

Median Days on Market (DOM)

The properties have been on the market for an average of 121 days. Half of the listings have come newly on the market in the past 46 or so days. Watch the 90-day DOM trend for signals of a changing market.

Segments

It is not uncommon for the higher priced homes in an area to take longer to sell than those in the lower quartiles.

Instant access to

WFG’s MyHome® provides full transparency, real-time updates, and post-closing home information in a secure built with YOU in mind.

Contact information for

Sign up for an account at https://myhome.wfgtitle.com today!

Click Register for MyHome® account on a MyHome® email to https://myhome. wfgtitle.com

Complete a brief registration form. Use your email address on immediate access.

via text, email, or

for your transaction

your escrow team

CONSUMER EXPERIENCE TIMELINE

TRANSACTION CLOSED

GATHER UP

SIGNING SCHEDULED

CLOSE TO SIGNING

TITLE CLEARED

UPDATER INVITATION

TITLE REPORT DELIVERED

TRANSACTION STARTED

MIDPOINT FEEDBACK

EARNEST MONEY

THINGS TO REMEMBER

Covenants, Conditions & Restrictions

We believe these are the correct conditions and restrictions.

However, no examination of title has been made and WFG National Title assumes no liability for any additions, deletions or corrections.

Mortgage Pre-approval Checklist

Before you can start the search for your dream home, you need to know your budget. After all, what’s the point of shopping if you don’t know what you can spend?

If you’re like most homebuyers, you’ll be using a mortgage to finance the purchase of your new home. Getting a mortgage isn’t complicated, but there is a fair amount of paperwork necessary to get pre-approved and start your home search off on the right foot. Here’s a list of all the things you’ll need to get the preapproval process started.

Here’s a list of all the things you’ll need to get the pre-approval process started.

Identification: A driver’s license or state-issued ID card works best here, but any sort of government-issued ID like a passport, military ID works too.

Last Two Years of Federal Tax Returns: Mortgage lenders are looking to establish a financial understanding of you; tax returns demonstrate your income history and help support your ability to pay back your potential loan.

Last Two Years of W-2 / 1099 / K-1 Statements: These statements help corroborate the financial picture your tax returns paint and are an important verification step for mortgage underwriters.

Paystubs Covering the Previous 30 Days: If your taxes and W-2s help the bank understand your financial past, your paystubs help them understand the present. Generally, only one paystub is necessary if it contains year-to-date payment information on it.

P&L Statements (if you’re a business owner): If your income depends on the operation of a business, the bank will want to support your paystubs with profit & loss statements from any businesses you operate.

Asset Statements: In order to assess your ability to make payments on a loan, mortgage companies also want to get an idea of your current assets, including balances in checking and savings accounts, retirement/401k/IRA accounts, and any investment portfolios you have.

Copy of Current Mortgage Statement (if applicable): If you’re already the owner of a home or property and have a current mortgage on it, your lender will want to review the documentation for that loan (even if they are the lender on that property too).

Copy of your Property Tax Statements (if applicable): Like a mortgage statement, your property tax statements will help a lender determine your payment history and ability.

Is something missing from this list? There is no standard document requirement for the industry; different lending institutions may require different documentation. Make sure to connect with your lender to make sure there’s nothing else they need to get you pre-approved.

Successful House Hunting Worksheet

Buying a home is an emotional experience. There is something unmistakable about standing in the living room of a property and realizing that you are, in fact, home. But, this emotional reaction to a house can sometimes overwhelm our more logical and objective processes when it comes to house hunting, which makes a successful house hunting checklist even more important.

Take a moment and fill out the checklist below; then, whenever you visit (or even consider) a new property make sure it meets all your required criteria before you start making emotional decisions about it.

How many bedrooms does my new home need to have to meet my or my family's needs?

How many bathrooms does my new home need to have to meet my or my family’s needs?

What is the minimum number of square feet my new home needs to have to meet my or my family’s needs?

Now that you know a little more about what your next home must or mustn’t have, use this checklist whenever visiting (or considering) a new home to see if it is worth considering further.

Feature Love It It's OK Hate It

Home Exterior

Living Room

Kitchen

Dining Room

Main Bedroom

Bedroom #2

Bedroom #3

Bedroom #4

Bathroom #1

Bathroom #2

Bathroom #3

Utility Room

Garage

Storage

Appliances

Heating/Cooling

This home satisfies all of my must-haves.

This home avoids all of the things I've identified as deal-breakers.

This home has the following from my “would be nice” list:

Based on my experience so far with this home, I’m ready to:

Schedule a (another) showing Request more information Write an offer

Consider the home as a possibility in the future Eliminate the home from consideration

Open House Attendance Checklist

Open houses are a great way to check out homes. But if you’re visiting an open house without your buyer’s agent, it’s easy to forget to ask some important questions.

Here are the most important questions you need to ask whenever you’re visiting an open house.

“May I Please See the Property Seller’s Disclosure Statement?” The SDS will give you insight into the physical condition of the property, including the legal disclosure of any sort of water, fire, or other damage that may have been concealed by remodeling.

“When were the heating / cooling systems last serviced or inspected? Were they found to be in good working order?” A seller’s disclosure statement isn’t required to tell you about service history. If a working furnace requires a visit every other month from a tech to keep it that way, you’ll want to know.

“What improvements have been made to the property since the seller purchased it?” Though most agents are happy to share the upgrades and improvements made to a property, they aren’t required to do so. Asking about remodeling and renovation projects is also a great way to get information on whether the work was done by licensed professionals or by the homeowner themselves.

“What is the age of the current roof?” A standard SDS requires a seller to share whether or not there are defects or leaks in a roof, but not always the age of the roof. Most roofs have an estimated 20year lifespan, so even a functioning roof that happens to be 17 years old may wind up being a capital expense in a few years.

“What is the age of the current septic system?” Verification of a working septic system is important, but the age of the infrastructure is important too. Like a roof, the mechanicals in a septic system won’t last forever, and problems here often go undetected until it’s too late because they’re buried underground. An old septic system is worth inspecting prior to moving forward with a purchase to make sure you know what you’re working with.

“May I please have the contact information for the HOA?” If the home you’re considering is a part of an HOA, make sure you request a copy of the HOA bylaws as well as review any membership information they have. HOAs are typically not too expensive in terms of the money they charge, but they can be a level of control that many homeowners aren’t prepared for. If the home you’re considering is part of an HOA, make sure you know your rights and responsibilities therein.

““Have there ever been incidents involving flooding in the home?” A standard SDS requires homeowners to disclose if there were water issues as a result of leaks, natural disasters, or water entering the home from the outside in any way. However, it does not require a homeowner to disclose an incident like a bathtub being left running; something that could cause equal damage.

“Has there been an inspection recently conducted on the property? If so, may I see a copy of it?” Some homeowners will actually get a home inspection prior to listing the home for sale in an attempt to fix anything that might come up in the inspection process. Though a home seller isn’t required to provide this report to a buyer, it never hurts to ask!

Writing a Successful Offer Checklist

Finding the home of your dreams is only part of the process in becoming a homeowner; you’ve also got to be able to write an acceptable offer that will entice the seller with terms that are compatible with your finances and timing. Below are all the terms and conditions common to a real estate contract.

Fill in the blanks below to create a strategy guide for you and your agent to write successful offers.

Financing:

Are you pre-approved for a mortgage? If so, from where and for how much?

How much are you willing to commit as a down payment?

How much are you willing to commit as an Earnest Money Deposit?

Do you have money set aside for an “appraisal gap” should one occur?

Will you be asking the seller to cover part or all of the closing costs?

Inspection:

Do you have a preferred home inspector?

Is your inspector aware that you are actively seeking a home?

Has your inspector provided you with an estimate for when they could complete an inspection?

Is there a minimum condition threshold you’re expecting from your inspection?

Closing & Possession:

Is there a window within which you must close your purchase?

Is there a window within which you must take possession of your new purchase?

Is there a title company you prefer to work with as a part of your closing?

Contract to Closing Checklist

Congrats! You’ve found the home of your dreams; it’s time to get you to the closing table. A lot needs to happen during the 30-45 days between a property going under contract and when you’re able to close on the home. Here’s a breakdown of what you need to do and when.

As Soon As You Are Under Contract

Submit your contract to your mortgage lender, verify there’s no other contract-related paperwork they need from you to begin the approval process

Schedule a home inspection

Immediately pause any plans for major purchases that would involve changes to your credit

Stop all major credit card spending

Three Weeks Before Closing

Order an appraisal (this is usually done through your bank, but you’ll need to pay for it upfront)

Begin the title search process to verify the property’s title is free of encumbrances (this is something you can coordinate with your Realtor® to order through your title company of choice)

Confirm your plans to vacate your existing property

Book any moving services necessary

Check-in with your mortgage lender on the process of your loan approval

Two Weeks Before Closing

Lock in your home insurance for your new home

Verify the removal of home insurance for your existing property effective on your estimated closing date (if necessary)

Verify the transfer of your utility service to your new home effective on your estimated closing date (if necessary)

Check-in with your mortgage lender on the progress of your loan approval

One Week Before Closing

Schedule a final walkthrough of your new property prior to closing

Confirm you’re clear to close with your lender

Confirm your closing date with your Realtor and the Closing Company, verifying that it meets any mandatory waiting periods between receiving a clear to close and closing

Order any certified checks necessary for down payments, direct payments to sellers for furnishings, etc.

The Day of Closing – Don't Forget to Bring:

Photo IDs for anyone signing paperwork

Required certified checks

Activated homeowner’s insurance policy

A new keychain & a bottle of champagne!

Home Inspection Worksheet

Questions to Ask Before the Home Inspection

We put together this list of critical questions to ask potential home inspectors to make sure you find just the right qualified professional.

Home Inspection Worksheet

8. Do you re-inspect if necessary?

9. Will you answer questions after the inspection?

10. Can you share your references?

11. What type of report will you deliver? Will it have digital photos?

Additional notes:

Home Inspection Worksheet

Questions to Ask During the Home Inspection

When you're tagging along on your home inspection, your inspector could be a source of useful information. Be sure to take this list of questions along and take great notes.

1. I don't know what that means. Can you clarify [ ]?

2. Do you see any major red flags? 3. What are the most costly repairs needed? 4. Is the home well-insulated? 5. Are there any drainage issues I should be concerned about? 6. How's the HVAC?

Home Inspection Worksheet

Home Inspection Worksheet

13. Any tips on maintaining [ ]?

14. How long will it take to get the report?

Additional notes:

Home Inspection Worksheet

Questions to Ask After the Home Inspection

After the inspection, you'll want to follow up with your inspector to make sure you fully understand the report and next steps. Cover these questions after the inspection is complete.

1. What if I have more questions?

2. Who do you recommend for repairs?

3. How can I best maintain my new home?

Additional notes:

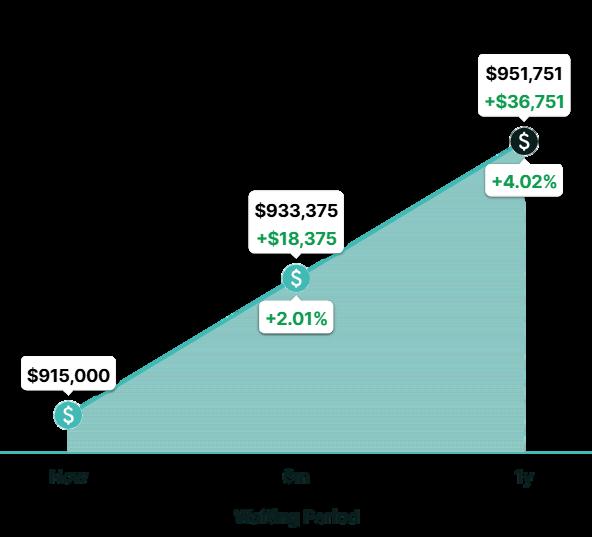

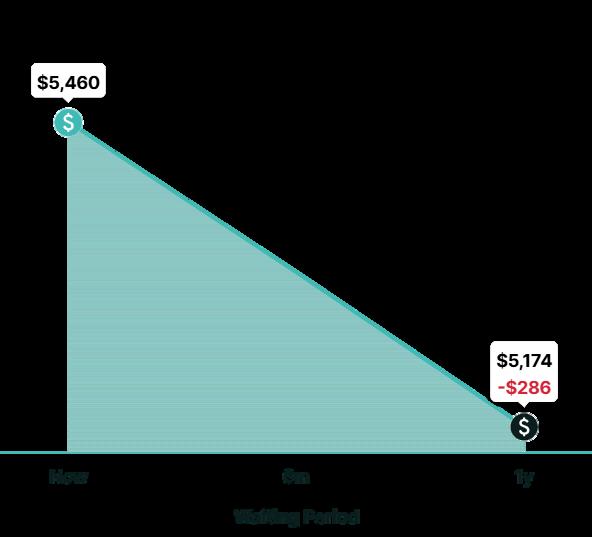

Benefit of Buying Now $2 9, 3 1 9 $ 36,751 $ 3,432 Appreciation Gain (+4.02%)

Cumulative mont hly payment difference for buying now vs waiting Cost of Refinance $ 4,000

Appreciation Gain

Proper ty value in 1 year: $951,751

Based on +4.02% cumulative appreciation

Nick Maccarrone

NMLS# 234538 • Oxford Mor tgage, LLC

Cell: (720) 217-5953

nick@oxfordmtgc com www oxfordmtgc com

6300 S Syracuse Way #155, Centennial, CO 80111

Payment Difference

Mont hly: -$286

Cumulative (1 year): -$3,432

See how waiting to buy affects a proper ty's value and t he loan for it.

Why Buy New Construction?

Superior Energy Efficiencies & Advanced

Building Technologies - save on monthly utility bills; enjoy easier & lower cost home maintenance Builder Warranties - protect your investment & not found in re-sell

Builder Financing - financing options most existing banks/mortgage brokers can’t/won’t offer Nothing Feels Better Than New – don’t settle for old decor choices, appliances that don’t work or inefficient floor plans

Benefits of New-Build Homes

Homes New construction homes offer more freedom – a new home is easier and less expensive to maintain

New construction homes SAVE MONEY – energy efficiency means much lower monthly utility bills

New construction homes are connected – built-in features meet future technology demands

Personalize your dream home – choose the perfect floor plan & select your desired interior décor finishes

Convenient financing – work with Builder’s mortgage professionals who help determine the best loan options Builder Warranties protect your investment – protection not found in re-sale

Variety of house plans & locations fit personal requirements – handicap access, multi-car garage, urban infill, suburban setting, 55+ active adult…

Environmentally sustainable – a new home uses less energy, reduces water usage, preserves natural resources & reduces pollution along total supply chain

Affordable – new home prices are competitively priced with existing homes

Did You Know Builders Require Buyer Appointments With All Buyers?

When a buyer has chosen to purchase a new-built home, they will participate in a sequence of Builder required appointments in order to complete and close the home in an organized manner. These appointments are necessary for two reasons:

1. Clearly identify the personalization choices of the buyer to the Builder.

2. To define the Builder’s process and expectations to the buyer.

While the following appointment titles may vary from Builder to Builder, this comprehensive list is in chronological order as if the buyer purchased a home to be built on a chosen home site.

Contract Appointment w/Builder Representative Selection of Structural Options Needed For Building Permit & Buyer Signatures On Purchase Agreement Mortgage Appointment w/Builder’s Lender Confirm Buyer’s Ability To Obtain Loan & Start Loan Process Listing Appointment w/Realtor If Purchase Contingent Upon Sale Of Current Home

Design Studio Appointments

Personalize Interior Decor With Professional Designer

Pre-Construction Appointment Meet Superintendent; Discover Builder’s Construction Process Open-Wall Walkthrough w/Superintendent Inspection Of Purchased Electrical Options Before Drywall Installation

Homeowner Orientation Walkthrough Learn Recommended Care Of Home; Identify Cosmetic Issues Needing Attention Before Closing Closing Day

First At New Home To Inspect & Approve Cosmetic Repair, Then To Location Of Builder’s Choice To Authorize Final Loan Paperwork Transferring Title From Builder To New Owner

Depending upon the stage of construction of a home, a buyer may not need to participate in every appointment. For example, the listing, pre-construction, design studio & open-wall walkthrough appointments may be unnecessary if the house is move-in ready and can close immediately

Ofc/Fax: 303-835-6415 PO Box 22174 Denver, CO 80222 www.BRCDenver.com