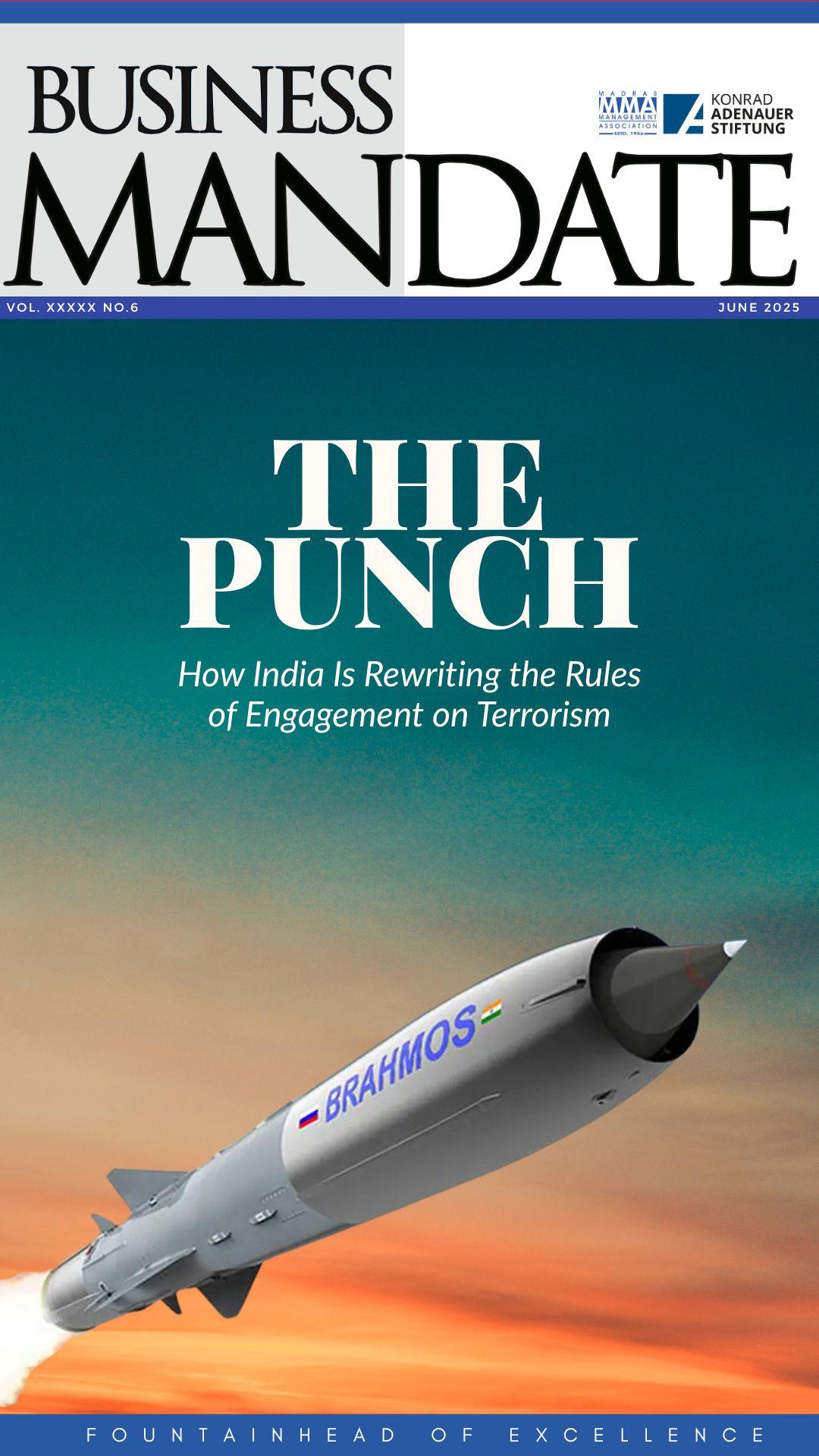

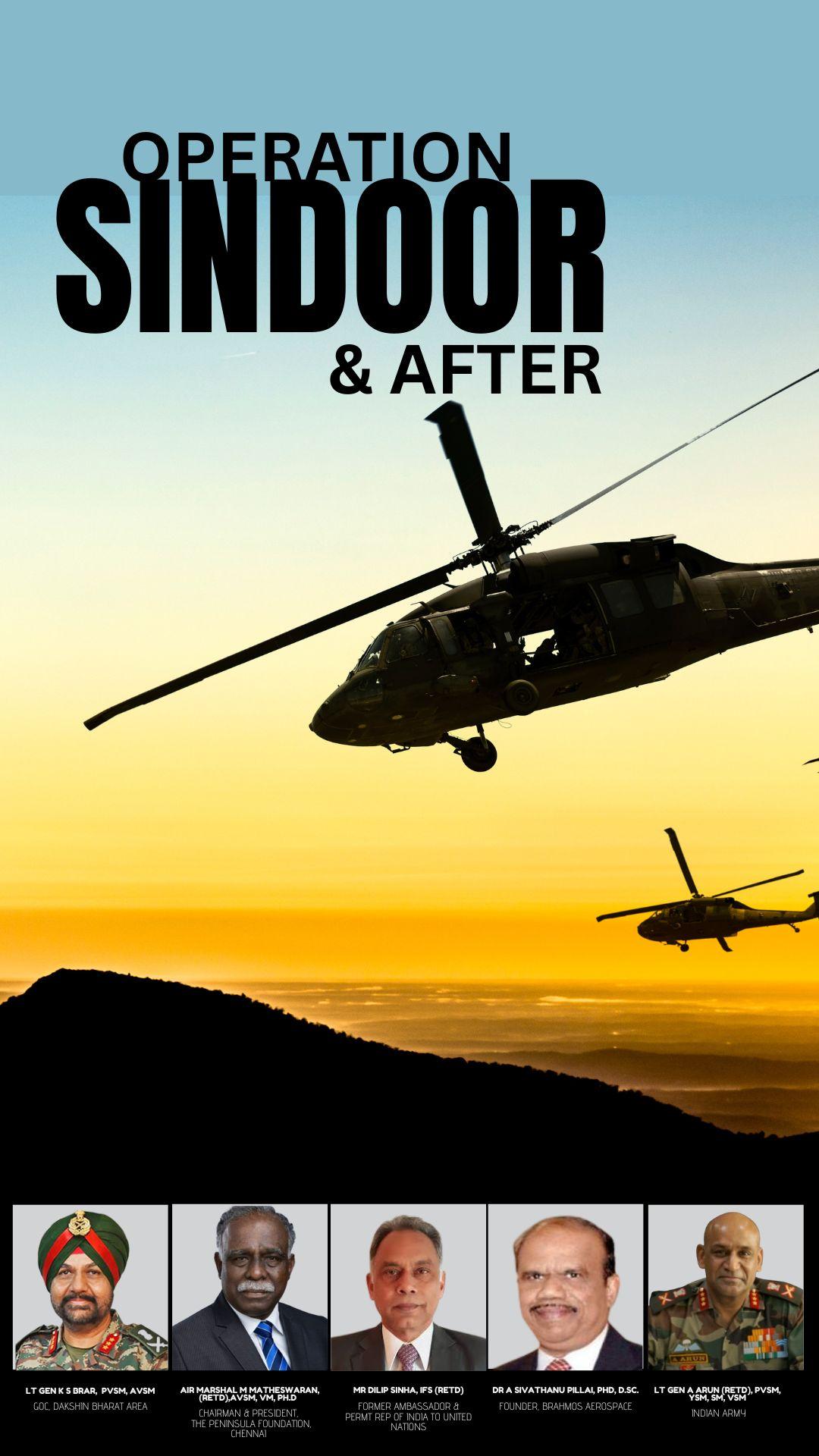

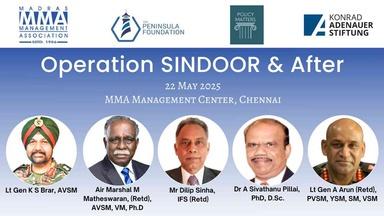

Strategic Reflections on Operation Sindoor and the Emerging India

Lt Gen A Arun ﴾Retd﴿, PVSM, YSM, SM, VSM

The new India is not just muscular, but no longer shy of its muscles. Whether it's our cricket team or our country, I’ve always maintained that we have been naturally reticent hesitant to project our strength. But that India is gone. Today’s India is confident, assertive, and unapologetic about its

capabilities. And we should not be ashamed of using our hard power when needed. Soft power has its place but sometimes, power must be seen to be believed.

The international order has collapsed. I am a vocal proponent of that view. In fact, I question whether the United Nations should even continue in its current form. I say let India pull out, just once, and see what happens. Out of the 193 members, at least 125 will find themselves adrift. The Security Council and the P5 do what suits them; little else.

POLITICAL GAINS

What did we gain politically from Operation Sindoor? Tremendous gains, I would say. We signalled clearly to Pakistan what the cost would be for any future misadventure. This cost is not only in men and material but in reputation. The Pakistan military, since the time I was commissioned, prided itself on its air defence systems. That myth lies in tatters today. Their long-held belief in superiority has been shattered.

We also recalibrated the Indus Water Treaty in

The war of the future will be different. Just as we are analysing this conflict, so are multiple nations. Our use of network-centric warfare, integration of services, and precision weaponry it all has been observed.

tone and posture. Earlier, we sought validation from powerful nations for our actions. We must stop. If others offer only polite noises while we bleed, so be it. We are big enough to fight our battles without permission or endorsement.

PSYCHOLOGICAL OBJECTIVES ACHIEVED

More than physical destruction, we struck psychologically, deep into Pakistan’s strategic hinterland. The depth and precision of our strikes have sent a clear and lasting message. We showed resolve in planning, in execution, and in managing escalation. This was not rash retaliation but a calibrated deterrence.

But I do feel that we missed an opportunity. We should have been more explicit in defining what constitutes a terrorist threat. Now people are splitting hairs: major threat vs minor threat. Any threat is a threat, and must be dealt with accordingly. Even incidents like Sopore, which some dismissed as "minor," merited retaliation.

STRATEGIC IMPLICATIONS

As someone who once served as Chief of Strategy for the Indian Army, I would be remiss if I didn’t address this. This operation marks a paradigm shift.

We have moved from strategic restraint and ambiguity to calibrated deterrence. We now dictate the tempo, shape the escalation, and control the battlefield narrative.

Our strike envelope has expanded not only in distance and precision, but in the networked synergy among our armed forces. Rather than saying ‘jointness of the forces’, I would call it ‘integration.’ Every operational briefing had representatives from the Army, Navy, Air Force, and the Ministry of External Affairs. This was a true whole-of-government approach something we’ve long preached but seldom practiced. And it worked. We discovered much about ourselves: our resilience, our capability, and our resolve. Let us not allow that learning to dissipate. Let us forge this heat into institutional steel. We showed that we don’t need anyone’s permission. Many countries didn’t stand by us and it didn’t matter. We did what we had to do. And we did it well.

The objective was limited: destroy terror infrastructure. That was accomplished. The message is clear and they are marked.

TACTICAL AFTERMATH AND NEW THREATS

Going forward, Pakistan will recalibrate its own tactics. Our red lines are now visible. Their response may be to lower the threshold and resort to more frequent, smaller-scale attacks. That presents a unique challenge. It’s easy to locate an airfield; far harder to detect a lone militant with a suicide vest. But I trust our security forces are already preparing for this scenario.

Some of the systems used by Pakistan were of Chinese origin, others American. Much of this equipment was countered but not all. We must ask ourselves: how effective was our air defence, truly? And how would it perform against a more sophisticated adversary like China? Make no mistake. China is a different cup of tea. But this conflict has allowed us to test ourselves, calibrate, and plan.

The war of the future will be different. Just as we are analysing this conflict, so are multiple nations. Our use of network-centric warfare, integration of services, and precision weaponry it all has been observed. Our muscular assertiveness will not go unnoticed. We are no longer just a yoga and Ayurveda nation.

Finally, let me be blunt Pakistan is not even a worthy adversary anymore. There are areas of improvement, and we must address them quietly, behind closed doors. That’s how we move from 85–90% effectiveness to 100% accuracy and zero Circular Error Probability (CEP). The endgame must be clear in our minds before we move the first pawn. That clarity of vision will shape our future doctrine and strategic posture.

MMA, in association with Colours of Glory, presented the Sixth S. Muthiah Memorial Lecture The lecture was delivered by Lt Gen P.R. Shankar, PVSM, AVSM, VSM ﴾Veteran﴿, Former Director General of Artillery and Professor, Department of Aerospace Engineering, IIT Madras

Acouple of years ago, a Chinese cartoon depicted a world map being pulled in four directions by the leaders of India, the United States, China, and Russia. What’s interesting is that the cartoon acknowledged India as one of the four major powers shaping the world. While the Chinese recognise our growing influence, we are yet to fully acknowledge it ourselves.

Today, the world is grappling with three major conflicts: one in Ukraine, another in Gaza and West Asia, and a third often overlooked brewing in the South China Sea. This third conflict involves rising tensions between China on one side and Taiwan, the Philippines, Japan, and others on the opposite side. Meanwhile, in relations with India, Pakistan is hot, China hotter and Bangladesh the hottest. We are living through turbulent times. But these challenges do not weaken us they make us stronger. India gains strength amid these global conflicts.

We are also in the midst of a global tariff war and it’s often unclear who is aligned with whom. This lack of clarity reflects the complexity of the new multipolar order. At times, it even feels uncertain whether countries like the United States or China are internally aligned in their own policies.

Global economic trends are diverging sharply, and the future remains uncertain. The tariff war may not lead to growth, but rather to stagnation possibly even deflation or economic regression. We are entering an era of deep unpredictability.

GLOBAL ECONOMIC SHIFTS AND INDIA’S USP

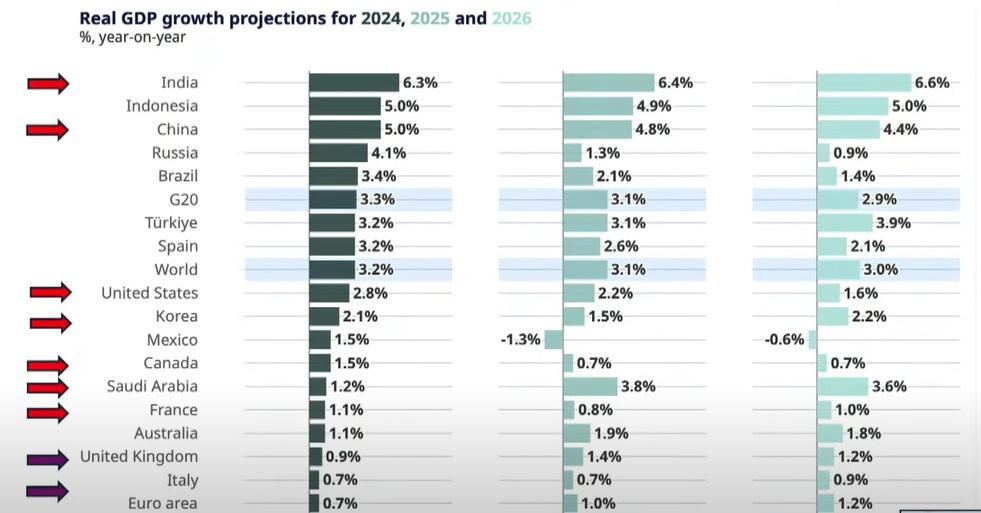

If we look at the ten or twelve largest economies by GDP many of which were once global superpowers most of them are now in decline. Italy, Germany, and Japan, for instance, have all seen their influence wane, and there’s little indication that they’ll regain their earlier stature. In fact, if anything, they may continue to regress. A key reason for this is demographic decline.

Economies are built not just by machines or military might, but by people and that’s a truth we often overlook.

Three years ago, everyone spoke of China as the world’s second-largest economy. That may still be technically true, but even today, we’re unsure of the actual size of China’s GDP. Is it $17 trillion? $12 trillion? Or even $10 trillion? The credibility of the figures is questionable.

In contrast, India is poised to sustain consistent growth over 6% annually even amid global trade wars and an uncertain economic climate. The foundation of this resilience is our people our demography. While Western nations and China are facing demographic declines on a scale unprecedented in human history, India’s youthful and growing population remains our greatest asset.

Economies are built not just by machines or military might, but by people and that’s a truth we often overlook. India’s demographic dividend, coupled

with its deep-rooted cultural fabric whether Aryan, Dravidian, Hindu, Muslim, or any other thread reflects a pluralistic society that fosters resilience and growth. We are not inventing something new; we are simply returning to the stature we once held before colonisation eroded our autonomy and degraded us.

THE GLOBAL DISORDER AND INDIA'S RISE

The rules-based international order is being disrupted in a big way primarily by China and the United States. It is within this atmosphere of disorder that India must grow and assert itself as a major power. In fact, we are already a major power.

America is striving to regain its global hegemony by acting aggressively on multiple fronts. Donald Trump, in particular, is reportedly eyeing strategic influence over Greenland, Canada, Mexico, and Panama, as part of a larger effort to revive the Monroe Doctrine asserting that the Western Hemisphere is unequivocally American turf.

Simultaneously, he is working to bring an end to the Ukraine-Russia conflict and to restore some

semblance of order in West Asia. He is also ramping up pressure on Iran and confronting China on multiple fronts. Trump appears driven by two convictions: first, that for America to be ‘great again’, it must resume its role as the world’s unquestioned policeman; and second, that China must be contained. And he is pursuing that goal step by step.

CHINA’S ILLUSION OF DOMINANCE VS. INDIA’S POTENTIAL

Many people still believe that China is poised to rise and dominate the world. That’s unlikely to happen for a simple reason: its population is shrinking. A recession is looming over China, and the demographic decline is irreversible. India, by contrast, is uniquely positioned to pull the world out of the next global recession. We are both a large consuming market and a country with the potential to manufacture at scale. India is the only real alternative to China not just in terms of capacity, but in terms of human capital as well.

Of course, we face resistance. There is a deeply entrenched bias either from the Anglo-Saxon West or from the China-oriented East that tends to deride or downplay India’s potential. That’s a challenge we must confront. Yet, increasingly, global leaders are beginning to admit: “We cannot move forward without India.”

Meanwhile, China is facing a multi-dimensional crisis. I call it ‘the crumbling Wall of China’. The country is reeling from the impacts of climate change and internal political instability. Since the eras of Mao Zedong, Deng Xiaoping, and the Tiananmen Square

protests, we haven’t seen this level of political volatility. There are growing tensions between the People’s Liberation Army (PLA) and the political leadership, as well as within the political establishment itself especially since Xi Jinping has not yet designated a successor. This power vacuum is bound to create more uncertainty. And sooner or later, that instability will spill over and affect the rest of the world.

IMPACT OF CLIMATE CHANGE

China is feeling the effects of climate change more intensely than many realise. Let me give you a simple example. If a storm hits the coast near Chennai, the damage is severe because the area is highly developed. But if the same storm makes landfall 20 or 30 kilometres down the coast where there’s little development, the impact is minimal. Maybe a few coconut trees fall, but that’s about it.

China, however, is highly developed and urbanised. Its cities are built in areas prone to natural disasters, and every year it suffers increasing climaterelated damage. This is worsened by poor environmental practices. Regions that historically never faced droughts are now experiencing them, and areas once immune to floods are seeing more frequent and intense flooding. Believe me by 2030, we will be looking at a very different China. Four years ago, when I wrote that China was headed toward a demographic decline, many people laughed. But just last year, China officially admitted that its population is shrinking and the truth is, they have no viable solutions.

In terms of technology, yes, China has made significant progress. And its military is strong on paper but it is riddled with internal problems.

The tariff war has only exacerbated the issue. Rising costs make goods unaffordable, jobs are being lost, and the general population is living with a sense of uncertainty about the future. In such an environment, people are reluctant to have children. And when birth rates fall, population declines and when population declines, the economy inevitably contracts. This is basic logic.

CHINA’S DOMESTIC STRUGGLES AND STRATEGIC FOCUS

Over the past three to four years, several pillars of China’s economy have suffered private sector growth, consumer demand, real estate, food security, employment, infrastructure, exports, and even healthcare. The government is now desperately urging people to consume: “Buy air conditioners, buy cars, buy appliances.” But it’s not working.

They’ve already experienced a massive property crash and a manufacturing slowdown. Even the socalled auto boom where Chinese cars are being heavily pushed covers a deeper issue. Inside China, there’s what I call an ‘involution’: massive production, minimal profits, and rising inefficiencies.

Despite all these internal challenges, China continues to project strength in three key areas: diplomacy, technology, and the military. These are its

strategic spearheads, even as its economic foundation becomes increasingly fragile.

FAILING DIPLOMACY AND FRAGILE MILITARY

Diplomatically, China has lost global trust especially after COVID. Its credibility is severely damaged. In terms of technology, yes, China has made significant progress. And its military is strong on paper but it is riddled with internal problems.

In the past 10 years alone, 14 full generals, 26 lieutenant generals, and 50 major generals have been sacked. This includes two defence ministers. The Central Military Commission one of the most powerful bodies in the Communist regime has been halved because many of its top officials have been arrested or purged by Xi Jinping. Worse, there are no credible replacements to fill the vacuum. That’s the real story behind China’s so-called military might. So far, I’ve spoken about the two largest global powers the United States and China. Let me now turn to Europe.

EUROPE AND THE RETURN OF MILITARISATION

Europe is in disarray. It outsourced its energy security to Russia, its manpower to Islamic countries, and its overall economic and military security to the United States. Now, with those pillars crumbling, Europe is lost and unsure of its next move. Suddenly, there's talk of remilitarisation. And history has taught us that when Europe remilitarises, the world is pushed towards war. That’s how it has always been.

In the next five to ten years, we are likely to witness a surge in militarisation across the world. And when someone becomes over-militarised, they are more likely to start a conflict. A hungry man with weapons and no way to survive will inevitably be drawn to fight. That’s the kind of global uncertainty we are walking into.

THE GREAT BALANCING PLAYER

In this context, let me focus on India. The equation between China and India will remain strained for a long time I don't think it will ever return to what it once was. China will never give up its support for Pakistan. The Chinese have been strategically foolish, as we overlooked many things and allowed them to establish a strong presence in our country until they attacked our army in Eastern Ladakh in 2020. Suddenly, the whole of India has woken up, and we are no longer interested in buying cheap Chinese goods.

India is a strategic partner of both Russia and the USA, despite the historical rivalry between the two. Can the US or Russia balance China on their own? No they need India. People often speak of a strong friendship between Russia and China, but Russia seeks a hedge against China and leverages its relationship with India. The US is determined to counter China but cannot do so without India. As a result, India has already emerged as a global balancer.

Consider it dispassionately: following the Pahalgam attack, even the Chinese ambassador in Delhi condemned terrorism in a tweet. This is the

same China that once vetoed the designation of Hafiz Saeed as an international terrorist its stance has shifted. Trump was the first to openly denounce this as 'nonsense'. Yet the same America had previously supported Pakistan during the Parliament attack. Russia has always stood by India, but even Russia now engages with Pakistan to a significant extent. In the complex web of international relations, tensions abound, but no one not even Pakistan can afford to disregard India.

THE WORLD TRUSTS INDIA

The West and the Global South trust India. Whether in Africa, Myanmar, or Southeast Asia, people trust Indians. They don't mind seeking security from the USA or relying on China to stabilise their economies, but when it comes to trust and a hedge factor, they turn to India. They need a fallback nation and that nation is India. India is emerging as a global player, and this transformation is already underway. In just five to ten years, you will see significant shifts.

We must also recognise that India sits at the heart of the world's major populations. We are positioned at the centre of key conflict zones, which presents opportunities. Nations come to us. The USA is not at the centre of population growth, nor is China. Meanwhile, India has begun exporting defence equipment, and this upward trend is irreversible. In 2010, The Hindu published an article stating that India was a country in search of artillery, and that we had artillery in search of ammunition. Yet by 2024, we are exporting both ammunition and artillery. In just 14

years, a remarkable shift has taken place.

The Indian Navy has always been Atmanirbhar self-reliant. While we are still working to strengthen our capacity, we prioritise our own needs before assisting others. Yet even so, many in the USA, which is striving to rebuild its naval strength, recognise that there is no available capacity elsewhere. Their solution? Leveraging Indian shipyards. In a year or two, you will see American stakeholders lining up here, because if they wish to remilitarise, they lack the manpower and the factories to do so. They have no choice but to turn to India they will not go to China.

Through every disaster, India has extended a helping hand whether in times of war, through vaccines for typhoid or COVID, or in the aftermath of floods and earthquakes. Time and again, we have stepped forward.

THE NEW NUCLEAR LANDSCAPE

We are also at the centre of a new nuclear growth story. People used to talk about a nuclear triangle China, India, and Pakistan. It’s no longer a triangle; China, Pakistan, Iran, India, and Israel are all there and USA is already a major nuclear power in the mix. While the global economy is going through a lot of uncertainty, India is emerging as a stabilising force. Saudi Arabia’s Mohammed bin Salman tweeted against Pakistan recently because they’ve realised that wealth alone isn’t enough. They need something deeper to sustain that wealth. If not, it will disappear either the Americans will take it, or the Chinese will. That’s why they trust India. That’s why they are coming here and

setting up the biggest oil refineries in the world.

On the other side, there’s a growing headache. China, Russia, North Korea, the USA, South Korea, and Japan are all looking to expand or upgrade their nuclear capabilities. And when they do, others will follow. That’s how a global nuclear race begins. Where is India in this nuclear race? That’s something we need to seriously think about. And we must stay ahead in this race not for military reasons alone, but because we are an energy-deficient nation. One viable path forward is nuclear energy. Alongside renewables, nuclear energy offers us a long-term solution.

THE UNSTOPPABLE INDIA

We have one of the largest untapped reserves of thorium in the world. India has already developed a three-stage nuclear program based on thorium, and it’s set to provide nearly 15% of our future energy needs. It’s happening right here in Kalpakkam. Just last year, our Prime Minister inaugurated the secondstage loading of the thorium fuel cycle. Today, most of our cities are well-connected by air. We are increasingly urbanised, mobile, and globally integrated.

India's rise is unstoppable. If you look at Germany, Japan, and China, all three were aided economies. They benefited from Western support and enjoyed a peace dividend Japan and Germany after the Second World War, and China following the Vietnam War for 30 to 40 years. India, however, had no such advantage. We faced opposition, sanctions, and wars yet we continue to grow. No matter the

circumstances, India moves forward.

We have endured proxy wars and insurgencies in Punjab and Kashmir, and we have overcome them. India stands as the only country in the world that has successfully eliminated insurgencies and restored peace perhaps with the exception of Ireland. Our approach has always been humane, ensuring that people are treated with dignity. In the long run, this approach has yielded lasting results.

CHALLENGES IN INDIA’S GEOPOLITICAL LANDSCAPE

In our immediate neighbourhood, we face the looming threat of collusion between China and Pakistan. We are operating in an intense nuclear environment and are constantly subjected to proxy warfare. This is one of the most complex and consequential regions in the world and it directly impacts India’s growth trajectory. What happened in Pahalgam is a stark reminder of this complexity.

Surrounding us are Nepal, Bhutan, Bangladesh, Myanmar, Sri Lanka, Maldives, and Afghanistan each dealing with some form of instability. Our relationships with these countries have been episodic, shifting with political winds. In Sri Lanka, it’s a revolving door: every new government brings a new foreign policy approach. It’s the same story with others. Take Afghanistan, for example. At one point, we rejected the “bad Taliban.” Today, we’re working with the “good Taliban.” That’s the nature of realpolitik. We have to engage with whoever is in power, but many of these actors pose indirect threats, often by becoming hosts for others. Bangladesh, for

instance, has increasingly become a conduit for Chinese influence. Nepal, too, has seen a rising proChina narrative even to the extent of China claiming that Buddhism originated in China. That’s the kind of narrative warfare we are up against.

ETHNIC OVERFLOW AND INTERNAL PRESSURES

Another challenge is ethnic spillover and migration pressure. Walk down any street in Chennai and you’ll find three or four Nepalese doing small jobs. We need them because local populations have moved on to better opportunities. But such demographic movements create ethnic transfers and sociopolitical ripples. This has been a recurring issue. Sri Lanka once influenced local politics in Tamil Nadu. Pakistan directly impacted politics in Punjab and Kashmir. Bangladesh is now influencing the political landscape in West Bengal. These cross-border dynamics can undermine grassroots democracy, distorting the local discourse and political stability.

This is a time to revisit the wisdom of Chanakya. In fact, studying Chanakya’s political economy may be more relevant today than courses from the Wharton School or Harvard Business School. And not just Chanakya even the Ramayana and Mahabharata offer enduring lessons in statecraft and strategy.

The world beyond our neighbourhood is also full of opportunities and challenges. Central Asia, the Middle East, Africa, South Korea, Japan, ASEAN countries, and Australia all these regions need India. They’re looking to engage with us. But we must be mindful: the Middle East is in turmoil, and Africa has

been in conflict for decades. In fact, last year saw the highest number of deaths in Africa in recent times especially in the Sahel region along the Tropic of Cancer, where dozens of people die every day due to conflict and humanitarian collapse.

CHANGING POWER EQUATIONS

In our neighbourhood, we have abundant energy and trade linkages. Many of them are deeply rooted in civilisational history. Take Malappuram in Kerala, for instance. It is a Muslim-majority belt not because of invasion, but because of historical trade with the Arabs. The Islam practiced in Kerala is very different from the Islam seen in the north. One came through commerce, the other through conquest. This distinction is important because it tells us something: for a growing economy and a growing population like ours, these civilisational trade linkages are a massive opportunity. Countries like Japan have stood by us in our most difficult times over many decades. That loyalty matters, and we must not forget it.

When we talk about arms and ammunition dependency, it doesn’t stem just from what we buy today. It comes from the long history of defence procurement. For instance, we still fly Mirage jets, which means we need spares from France. Our army still runs Russian tanks. Even if we don’t buy new ones from Russia now, we still depend on them for maintenance and spares. These are forward linkages, and they shape long-term strategic partnerships. That’s why Russia and France have remained dependable allies. We’ve procured Rafales from France, and for the next 50 or 60 years, we’re locked

into that ecosystem regardless of the fact that France may also sell Mirages or Rafales to Pakistan. That’s the reality of power politics. But we are emerging as a major power, and we have to manage these relationships as a mature nation. These are part of the changing global power equations.

OUR CHALLENGES AND FOCUS AREAS

We are disaster-prone. When storms strike every year, someone has to step in to rescue people and we rescue each other. Over time, we have developed ways to cope with the challenges posed by climate change.

Beyond that, we face strategic dependencies. We must develop our own technology, which presents a significant challenge. Then there is politics never quite healthy in India. Politicians tend to care only if and when their party is in power. In the past ten years, Centre–State relations have deteriorated from bad to worse. Our politics have become increasingly polarised on religion, language, and other identitybased factors. These are essentially power struggles, and as we grow, these divisions could deepen and be exploited by others. We lack a strategic culture. We don’t think big.

The situation in Jammu & Kashmir is showing signs of improvement, notwithstanding the recent incident in Pahalgam. However, Manipur remains in turmoil. Ethnic and religious divisions continue to affect many parts of our society. We also lack a strong defence industrial base. And last but not least, we suffer from inadequate budgets and limited capacities. These are the issues we must address and manage.

Under the “Read & Grow” series, MMA held a discussion on the theme of the book “The Lean Startup: How Constant Innovation Creates Radically Successful Business” by Eric Ries.

Sreenivassan Ramaprasad, Director, CADD Centre Training Services led the conversation with S Srikanth, Management Consultant & Executive Coach and Kannan Gopalakrishnan, Co‐founder, Habitat Design Studio

Sreenivassan Ramaprasad: Startups are the backbone of our economy as we move forward. In The Lean Startup, Eric Ries provides a new perspective on how startups should think. He introduces a scientific approach to entrepreneurship, focussing on efficiency, learning, and adaptability to minimise risk and uncertainties while maximising success.

BUILD, MEASURE, LEARN

The first key concept is what he calls the BuildMeasure-Learn loop, an iterative process. Many organizations, when they come up with a new idea, invest heavily in building a product before testing it. Later, if the product fails, the entire investment is lost. Ries suggests building a Minimum Viable Product (MVP), releasing it to the market, measuring its performance, gathering quick customer feedback, and then iteratively improving the model. For example,

Dropbox initially launched just a video demonstrating its benefits for file management. Once they received significant interest, they began full-scale product development.

The Minimum Viable Product (MVP) is the foundational skeleton of a product. It is the simplest version that allows startups to gather maximum validated learning, based on the assumption that the product or concept will work. Start small, test assumptions, and avoid over-engineering before meeting customer needs. Ries gives the example of Zappos, an online shoe retailer. Initially, they only displayed photographs of shoes with prices online to test whether customers were willing to buy shoes digitally. Once they saw strong demand, they developed a full-fledged platform, eventually selling the company to Amazon for a significant value within ten years.

VALIDATED LEARNING

The third key concept is Validated Learning,

which refers to systematically testing ideas through experiments and customer feedback. Entrepreneurs test hypotheses to determine what works and what doesn’t. Ries cites IMVU, where he was a co-founder. Initially, the platform introduced avatars for chatting, assuming users would embrace this feature. However, after testing, he realised it wasn’t gaining traction. Because he had not heavily invested in this direction, he was able to pivot efficiently. This illustrates the importance of validating assumptions with an MVP before full-scale development.

The next concept is Innovative Accounting, a framework for measuring progress in startups that focuses on actionable metrics rather than vanity metrics. For example, if you develop an app, don't just

The idea is to build only what is necessary, eliminating waste and optimising efficiency.

measure downloads analyse actual usage. Ries gives an example of a fitness app: if people download it but don’t use it, it holds no value. Instead, tracking engagement with core features provides meaningful insights for further development.

PIVOT OR PERSEVERE

Another key principle is Pivot or Persevere, which involves deciding whether to make a significant change to the product or strategy or continue on the same path based on insights from the Build-MeasureLearn loop. Ries explains that Groupon originally started as a platform for collective action and fundraising. However, the founders realised users were more engaged with group discounts and deals rather than activism. This insight led them to pivot toward the group-buying model, ultimately shaping Groupon into a successful business.

In CADD Centre, when we started, our original intention was to provide CAD related printing services. However, after a few months, we realised that the market was not ready there was little demand for CAD prints. By the third or fourth month, revenue was stagnant. Instead of investing heavily in printing machinery, we quickly pivoted to training services, which led to significant growth, making us one of the largest training providers in the Asia-Pacific region.

Another crucial concept is Continuous Deployment, which involves rapidly deploying updates and iterations to gather quick feedback and respond to customer needs. Startups must quickly adapt to changing demands while minimising wasted effort. Ries discusses how Amazon continuously deploys small updates and new features, testing customer responses to inform further development.

Next is Lean Thinking, a concept derived from Toyota’s Lean Manufacturing principles. The idea is to build only what is necessary, eliminating waste and optimising efficiency. In Lean Thinking, startups focus on value creation, resource optimisation, and risk reduction to improve efficiency in operations.

The book is structured into three parts:

Vision: This part discusses the entrepreneurial mindset. Many believe that only creativity is required for success, but Ries emphasises the importance of strong management principles. Entrepreneurs, regardless of company size, must adopt structured decision-making similar to large organizations.

Steer: This covers the Build-Measure-Learn feedback loop and explains how startups can either pivot or persevere based on expert insights. For example, Instagram initially started as a check-in app with multiple features, but after analysing user behavior, the founders discovered that photo sharing was the most used feature. This led them to pivot into a dedicated photo-sharing platform, which became a massive success.

Accelerate: Once a startup identifies what customers want, it should scale in that direction. If

Eric Ries defines a product as anything that delivers value to a person who is, or is willing to become, a customer.

demand is lacking, a pivot is necessary. Airbnb’s success stemmed from enhancing trust between hosts and guests by introducing features like host verification and professional photography, which significantly contributed to its growth.

Srikanth: Lean manufacturing is well-known in industrial circles, but applying it to startups is quite intriguing. I have interacted with many startup founders and entrepreneurs, and one common pattern I observe is that they often become fixated on a single idea. They continue investing resources into it, even at the cost of financial losses for their investors. If they embraced the Pivot or Persevere concept, they might recognise the need to change direction sooner.

Eric Ries defines a product as anything that delivers value to a person who is, or is willing to become, a customer. I find this definition very insightful.

Kannan Gopalakrishnan: Managing a startup requires a completely different mindset compared to traditional management. Closing the feedback loop is a brilliant concept. Over time, businesses often fall into complacency, assuming that customers will always love their products and services. However, that assumption like a soap bubble can easily burst, leading to failure. The real magic happens when customer feedback is actively integrated into the

process and system, driving continuous improvement and innovation.

Sreenivasan Ramaprasad: Among all the concepts, which one resonated with you the most?

Srikanth: Pivot or Persevere, for sure. Also, in the Build-Measure phase, Ries introduces the Value Hypothesis and Growth Hypothesis concepts that many startups overlook. The Value Hypothesis must be tested periodically, and the only true validator is the customer.

Startups cannot take customers for granted. Sometimes, even customers themselves don’t fully understand their needs, so how do you address that? Ries makes an important point: don’t rely on feedback from just one customer or a small group. Instead, collect data from a broad customer base, analyse it statistically, and identify trends.

If startups follow this approach, they can bring their product to market faster, align with real customer needs, and avoid costly mistakes. It's not just about wasted money many failed entrepreneurs regret the lost time more than anything else.

Kannan Gopalakrishnan: A couple of concepts deeply resonated with what we do. One is quick testing rolling out a product before it’s 100% complete and presenting it to the client for feedback. The client doesn’t need to see the full picture to give you an initial sense of whether they like it or not.

For example, if I design a residence a beautiful bungalow with neoclassical semicircular arches and white marble and the client responds with, “Oh no,

I’m looking for a postmodern building with steel and concrete,” then all the hours I invested in that design are wasted. I once showed a sketch of a building to a client, proud of my work, only for them to dismiss it, saying, “That’s just a sketch.” That experience taught me an important lesson in how to effectively pitch an idea to future clients.

Metrics are also crucial. In my business, I typically measure success by revenue earned, total square footage designed, or the number of projects completed. However, we rarely talk about quality, even though it’s a critical metric. The way we define success directly impacts growth, which is why we constantly refine our metrics to ensure we measure what truly matters.

Sreenivasan Ramaprasad: Are these concepts truly relevant to your business? Or are they only applicable to startups?

Kannan Gopalakrishnan: I watched a video by Simon Sinek, the author and motivational speaker, where he discussed SEAL Team Six. In his interaction with the team’s captain, he asked, “What qualities do you look for in a SEAL Team Six member?”

The general took out a piece of paper and drew a graph. On the Y-axis, he wrote performance, and on the X-axis, he wrote trust. He explained: “High performance? I triple-check; Low performance? I check only once. If a high performer has low trust, they become a toxic presence within the team. On the other hand, a high-trust individual with low performance can always improve their skills.” This made me realise the importance of defining the right metrics, just as

Eric Ries emphasizes in The Lean Startup.

Getting customers is one thing, and marketing is another. But how customers react to your product, how they engage with it, and the quality of that engagement are even more crucial. Ries’ insights made me rethink how we define our customers and our business. In fact, the questions customers ask about us often shape our identity. That was a powerful realisation for me one that applies not just to startups, but to everyday business discussions and decisions.

Srikanth: I’m a consultant and a practicing Chartered Accountant. Our firm has been around for 50 years with well-established processes. However, I see a lot of potential in applying lean concepts to service industries, and I can certainly introduce these ideas to my clients. One of the key goals of lean methodology is cycle time reduction, and Ries emphasises reducing work in process. I believe this is a powerful strategy that can significantly enhance efficiency.

Sreenivasan Ramaprasad: What are the typical challenges startups face today, and does the author offer any solutions?

Srikanth: I have a feeling and don’t get me wrong that many startup entrepreneurs assume they can operate in the red indefinitely. I understand that startups involve risk and uncertainty, but even conventional businesses are facing unpredictability today.

What Ries suggests can help startups shorten their learning curve and accelerate their journey to

99 percent of startup ideas don't get funded. You have to fund it yourself. The author guides those 99 percent of people to survive when they don't have deep pockets.

profitability. One of his key warnings is about vanity metrics many entrepreneurs focus on numbers and metrics that don’t actually impact the bottom line.

The real question is: How long can this last? How long will funding continue to support an unsustainable model? Startups need to shift focus from vanity metrics to meaningful, actionable data that drives real business growth.

Kannan Gopalakrishnan: 99 percent of startup ideas don't get funded. You have to fund it yourself. The author guides those 99 percent of people to survive when they don't have deep pockets. In my opinion, three to five years is fair enough to succeed, but people still have to eat. Make sure that your business is afloat and you're making a dent in people's minds, maybe not in their pockets. People should buy into the idea that there is marketable potential in your concept. The FBI says that you need to have actionable intelligence. In the same way, you need to have actionable metrics. Learn along the way and see what works and what doesn't.

Under the “Read & Grow” series, MMA organised a discussion on the book, “The Art of Execution: How the World's Best Investors Get It Wrong and Still Make Millions,” by Lee Freeman‐Shor Babu Krishnamoorthy, Chief Sherpa, Finsherpa Investments Pvt Ltd led the conversation with A.K. Narayan, Managing Partner, Scripbox com India Pvt Ltd, and Loganathan, Chief Business Officer, Sundaram Asset Management Company

Babu Krishnamoorthy: Investing has become much easier today. But as Warren Buffett said, “Investing is simple, but not easy.” That’s absolutely true. Anyone can invest in stocks or mutual funds, but there’s no guarantee of making a profit.

Just two months ago, SEBI Chairperson Madhabi Puri Buch, while addressing a seminar, revealed that 97% of all retail investors who traded in the Futures and Options (F&O) market ended up losing money. That’s a staggering figure. A large number of people especially youngsters are putting their hard-earned money into the markets, only to face losses. It’s important that we demystify some of the concepts around investing.

Each person enters the stock market with a different mindset and perspective. Moreover, there are

no clear guidelines. Should you sell when the market goes up? Or when it goes down? Should you buy when stocks rise, or when they fall? There is no universally right or wrong answer.

The book The Art of Execution by Lee FreemanShor offers deep insights into this paradox. Lee is a practitioner, researcher, writer, mentor, public speaker and most importantly, a seasoned fund manager. In 2012, he was ranked among the top fund managers, managing over $2 billion across five equity and five multi-asset funds. He also holds a master’s degree in psychology and neuroscience from King’s College London and is a certified mentor and trainer.

Lee’s investment strategy was deceptively simple. The book is based on real-life experiences gathered over a seven-year period. He worked with 45 of the world’s top fund managers, allocating each of them between $25 million and $100 million to invest on his behalf. His instructions were straightforward: they could invest only in their top 10 ideas at any given time.

We tend to buy at the wrong time or sell at the wrong time. The author of The Art of Execution categorises investors and highlights their behavioural traits.

It sounded like a foolproof plan entrust the best fund managers with large sums and focus on only their best ideas. What could go wrong? These were some of the sharpest minds in investing. Yet, surprisingly, many of their top ideas lost money. In fact, randomly tossing a coin to pick a stock might have yielded similar results. And yet, despite being wrong much of the time, many of these investors still made significant profits. This brings us to a crucial question: How can someone be wrong in investing and still be profitable?

The answer lies in two key aspects of any action: knowing and doing. The doing part is what we call execution. There is something fundamentally different about how successful investors execute their trades something that makes the difference between loss and profit, even when the stock pick itself turns out to be wrong.

A.K. Narayan: When we look at our investment portfolios, we often find ourselves dissatisfied. We tend to buy at the wrong time or sell at the wrong time. The author of The Art of Execution categorises investors and highlights their behavioural traits. For example, he describes a certain type of investor as a “rabbit” one who is constantly anxious and impulsive, and therefore, unlikely to succeed. Ultimately, his core message is that successful investing is all about execution.

Lee Freeman-Shor suggests that before you enter a trade, you should have a predefined plan: What will you do if the stock drops 10%, 15%, or 20%?

In real estate, the key to success is location if you buy in the right place, you’re likely to see strong returns during a boom. Similarly, in the stock market, execution is the key to success. One of the biggest issues today is that people monitor their investment portfolios minute by minute. That’s unfortunate. When you buy a piece of land, you hold on to it for 20 or 30 years without checking its value. You buy gold and lock it away for years without worrying about its price fluctuations. But when it comes to equities, we become hyper-focused, checking prices constantly, and then conclude that the market is irrational.

The author emphasises that successful investors are regular and disciplined, and maintain a diversified portfolio. These are universal principles found in almost every investment book. They remain timeless: think long-term and practice patience. Unfortunately, while we all know this, we struggle to follow it. We essentially have four asset classes: fixed income, gold, real estate, and equity. Why do we treat equity so differently and label it as inherently risky? It’s not risky if you understand it and learn to manage it wisely.

Loganathan: As the author rightly points out, materially adapting is not just a valuable investing lesson it’s a life lesson. Almost every day, we encounter challenges. What sets successful people

apart from others is their ability to adapt whether the situation is favourable or adverse. It all comes down to how we respond.

Suppose you buy a stock today, and by next week it’s down 20%. What will you do? Most people react like a rabbit caught in the headlights frozen and unsure. The author emphasises that you should not make decisions in that emotionally charged moment, because they are likely to be wrong. Instead, you should plan your course of action in advance. To me, that was a very powerful insight.

Lee Freeman-Shor suggests that before you enter a trade, you should have a predefined plan: What will you do if the stock drops 10%, 15%, or 20%? Not taking any action is not an option. You will have to act either buy more, sell, or exit. Simply waiting and hoping is often the worst mistake an investor can make.

The key takeaway for me is this: we need to materially adapt, have a clear, pre-defined plan, and then execute it without hesitation. Ideally, this execution should be automated through stop-loss orders or predefined buy/sell instructions so that emotional biases don’t interfere with our decisions.

Babu Krishnamoorthy: We’ve all gone through the challenges of COVID and adapted, eventually bouncing back successfully. A couple of months ago, I came across a YouTube video of Roger Federer speaking at a graduation ceremony. He said something that really struck me: over his entire career, he lost 54% of all the points he played. Now, as someone who was the world champion for the longest time, we’d expect him to

have dominated most points. But that wasn’t the case.

Similarly, Lee Freeman-Shor says that even the best fund managers often get it wrong. They’re not very different from you and me. The only difference is when we get it wrong, we freeze, like rabbits, unsure whether to buy more or sell. A professional fund manager, on the other hand, acts. Federer also said that whenever he lost a point, he would immediately forget about it and focus on the next one. That mindset is what made him a champion.

This book categorizes investors into five behavioural types: Rabbits, Assassins, Hunters, Raiders, and Connoisseurs.

When things go wrong, a Rabbit does nothing. They just stay put, hoping the situation will resolve itself which, more often than not, never happens. In contrast, the Connoisseur is a successful investor. The term reminds me of a wine connoisseur. He doesn’t gulp down the wine. Instead, he carefully selects the finest wine, smells it, swirls it, takes a tiny sip, and truly experiences it. Over an entire evening, he may have just half a glass but he fully savours it.

Lee describes the Connoisseur investor in a similar way. This type of investor identifies highpotential but overlooked companies businesses that are not yet in the limelight. He does deep research, finds beauty in the ordinary, and has a strong conviction that these companies will perform well. He’s not content with modest returns he looks for multibaggers that can give 5x or 10x returns. He invests a significant portion of his capital into just two or three high-conviction stocks. And if the market

When someone once asked Warren Buffett about his preferred holding period, he said: “Forever.” That’s the mindset of big investors.

tumbles, he doesn’t panic he buys more of those stocks.

When someone once asked Warren Buffett about his preferred holding period, he said: “Forever.” That’s the mindset of big investors. They hold with conviction over the long term. What Lee says in the book strongly resonates with my own observations of the stock market and investing. It’s not just about picking the right stock it’s about having the right mindset and executing with discipline.

A.K. Narayan: I began investing in 1984, gradually accumulating shares of various companies both through IPOs and the secondary market. Back then, even SEBI didn’t exist. There was no regulatory framework, and the system was quite chaotic. Despite that, some of the IPOs I invested in turned out to be phenomenal.

I remember one such company GSK, which used to manufacture Iodex. They issued shares at a premium of Rs.8 on a face value of Rs.10. I was allotted about 50 shares in that public issue. I’ve held those shares since 1984 and they’ve consistently yielded dividends of Rs.5,000 to Rs.6,000 every year. Eventually, GSK transferred the Iodex brand to SmithKline Beecham, but the value of that investment has continued to grow steadily.

During the dot-com boom around 2000, stock prices soared. I recall a company named VisualSoft from Hyderabad. It had a face value of Rs.10. I bought the shares and later sold them at Rs.2,000. But the stock eventually went on to hit Rs.10,000! When I pick stocks, I focus on three key things: good management, strong corporate governance, and a quality product. If the promoter is credible, the product is sound, and the company is generating profits, then it’s worth buying. If not, I don’t even consider it. That’s the approach I’ve always followed, and it has served me well. I often share this principle with others too.

Equity is just another asset class like real estate or fixed income. Buy good companies, hold them for the long term, and expect reasonable returns. Don’t look for phenomenal returns, and definitely don’t expect to get rich overnight. If you lose 10% or 20%, it’s best to exit and consider it a learning experience.

Most importantly, you must be a contrarian. When things look bad for a sector, that might be the right time to invest. I remember when Ashok Leyland was trading at Rs.27. People said the company was operating only three days a week due to a lack of orders. But I thought, if it starts operating six days a week, the stock might shoot up to Rs.150 or Rs.200 and it did. That’s the mindset you need: think ahead, apply your judgment, and stay calm in the face of market noise.

Loganathan: Roger Federer lost 54% of the points he played and still became a champion. Why? Because he won the points that mattered. This is exactly what applies to investing as well. These investors when they win, they win big. You can suffer several small

losses, but one big win can more than compensate. The key is: first, have patience, and second, make the most of the winning opportunities.

I’d say I’m a connoisseur-type investor, but I became one purely by accident not through deliberate learning. My first real investing experience dates back to 1991, when the Harshad Mehta scam wiped out whatever I had invested. It was a painful but valuable lesson. I realised that markets can burn you badly.

For the next five or six years, the market went nowhere. During that time, I moved toward mutual funds. I instinctively avoided direct stock picking. Because stock investing involves two critical and difficult steps: analysis and execution. Analysing a stock is one challenge but executing your plan is a whole different ball game. As Lee Freeman-Shor rightly says, “Buying is easy. Execution is harder.” Just like how making money is one thing, but preserving it is even harder.

I stopped investing in individual stocks partly because of the information asymmetry and potential manipulations. Instead, I stayed a mutual fund investor. Interestingly, I was overseas at the time, and there was no app to check the portfolio every day. I looked at it maybe once in three or six months. And the best thing I did? I did nothing. I didn’t react. And surprisingly, that worked. After five or six years, I realised that this hands-off approach was the most profitable. That’s how I inadvertently became a connoisseur investor, and it’s a philosophy that has served me well for the last 15 to 20 years.

I also disagree with Lee Freeman-Shor when he suggests that mutual fund managers are doomed to fail. That might be true in developed markets, but not in India...

In a country like India, it’s not difficult to be a connoisseur. If you believe in the long-term growth of the Indian economy and if the economy grows at 6–6.5% real GDP, and 12–13% nominal GDP then any decent company should grow at least 1.5x that rate. So a 14–15% return over the long term is very achievable, with a diversified portfolio.

I also disagree with Lee Freeman-Shor when he suggests that mutual fund managers are doomed to fail. That might be true in developed markets, but not in India, where long-term patient investing can still deliver double-digit returns. The structure of the Indian market still supports disciplined investing through funds. It would’ve been difficult to be an Assassin or a Hunter the other investor archetypes that Lee describes.

For instance, an Assassin ruthlessly cuts their position if the stock falls 20%. But how many times can you do that? It requires immense discipline and courage. You have to take large positions, and when 20% of that is gone, you have to cut it. That’s emotionally and behaviourally very hard for most people.

Similarly, being a Hunter someone who buys more when the stock falls is also difficult. Sure, in hindsight, we say we should have averaged down. But in real-time, when your stock is down 20% or more,

putting in more money feels terrifying. And as Lee points out, only 30% of stocks that fell by 20% eventually recovered. The remaining 70% never bounced back. So just buying more at lower levels doesn’t always work. The key question is: If you didn’t own the stock, would you buy it now, knowing what you know? That’s a tough question to answer honestly when you're already nursing a loss.

Then there are the Raiders probably the most common type among today’s retail investors on platforms like Groww and Paytm. They buy, see a 2% gain, and sell immediately. But over time, these small trades don’t add up. In fact, you might make five rupees, lose seven, and the only one making money is your broker.

Considering all this, I believe it’s actually easiest and most rewarding to be a Connoisseur. You don’t have to be a genius. All you need is patience, belief in the India growth story, and a long-term view. If the economy grows, your stocks will grow. Sit back and stay the course. That, I think, is my biggest takeaway as an investor: know your type, and be comfortable in your own skin. Don’t try to be an Assassin or Hunter if you’re a Rabbit or a Connoisseur. Investing is not about becoming someone else. It’s about finding what works for you and sticking with it.

Babu Krishnamoorthy: In our life journeys as investors, I’m sure all of us have made our share of mistakes. I certainly have, and I still do. Some of those early mistakes stay with me even now, and I can clearly relate to them when I reflect on the past.

One such story is about Times Bank. It was a bank

owned by the Times of India group, and they came out with an IPO. I was one of the lucky ones to get allotted 1,000 shares. For a year or two, the share price barely moved. It remained stagnant until HDFC Bank came along and acquired Times Bank through a share swap deal. I received a bunch of HDFC Bank shares in exchange for my Times Bank holding.

After the conversion, the price went up slightly. I was sitting on about a 15% gain over three years just 5% a year. I rushed to my broker (this was before online trading, when everything was physical) and told him to sell. I thought, “15% is good enough.” I sold it all around 400 or 500 shares of HDFC, face value Rs.10 each.

Years later, I realised that if I had held on to those HDFC shares, they would have been worth Rs.12–14 lakhs today. The most frustrating part? I don’t even remember what I did with the money. It came into my bank account, and just disappeared spent somewhere, forgotten.

That’s exactly the kind of situation Lee FreemanShor describes when he talks about “Hunters” in his book. He says: Don’t chase small gains in stocks. Don’t sell out for just a 5–10% profit. It’s like cricket when you step out of your crease to take a big shot, you’re taking a risk. You could be stumped or run out. So if you do take that risk, make sure the payoff is worth it go for a six, not a single.

Similarly, in investing, if you’re going to take the risk of equity investing, then have the conviction to stay in hold on, do your homework, and aim for a big multiple. I didn’t do that back then. I lacked the

conviction, and frankly, I didn’t do enough homework either. That was 20 years ago. I’d like to think I’m wiser now. I don’t invest much in individual stocks these days, but I truly believe that you have to give time for investments to mature. That’s one of the biggest learnings from my journey.

A.K. Narayan: Anyone who has been investing for decades is bound to have some regrets myself included. Over the years, so many companies have come and gone. I started investing in 1984, and one memorable story goes back to the time of the Ketan Parekh scam.

I had sold some shares and went to my broker to collect around Rs.40,000. He said, “Sir, I don’t have the cash right now. I can give you shares instead.” I was surprised but he added, “The Ketan Parekh scam has broken out, and I’m shutting my office tomorrow morning. Take the shares now.”

So I asked what shares he had. He said, “I’ll give you 1,000 shares of Eicher Motors.” I’d heard of the company and thought it was decent. He also gave me some shares of Shipping Corporation of India for the rest of the amount. Before I left, he said one thing: “Sir, don’t sell Eicher Motors.” I laughed and thought here he is, closing his office, and still giving advice!

Anyway, I didn’t do anything with those shares. The next year, Shipping Corporation gave a huge dividend Rs.18 per share. That covered most of my original investment, so I considered that part a bonus and forgot about it.

Then Eicher Motors suddenly jumped from Rs.10 to Rs.100. It had grown 10x. I wasn’t in touch with the

broker anymore, but others told me the company had good potential. Eventually, the stock hit Rs.1,000. I started selling in lots 100 shares, 200 shares until it hit Rs.2,000. But can you believe it? The stock went on to touch Rs.35,000! That’s Rs.3.5 crore from an initial Rs.10,000 investment. And the worst part? I still hold the Shipping Corporation shares because they were “free”! That’s regret number one.

Another time, a gentleman came to me and strongly recommended a stock called J. Kumar Infraprojects (J Corp), priced at Rs.5. I hesitated but eventually bought 1,000 shares. It shot up to Rs.100 a 20x return so I decided to sell. He came back and said, “Sir, buy more!” I refused. Then it went to Rs.500. Again, he said “buy,” and again I said no. At Rs.750, I started selling in parts. By the time I exited fully, it was Rs.1,500. Can you guess how high it went? Rs.21,000! From Rs.5 to Rs.21,000. That’s not just regret that’s a masterclass in loss of potential profit.

Loganathan: My most recent regret is not fully capitalising on the post-COVID market rally. In hindsight, had I seen it clearly, I would have invested a lot more especially in mutual funds and perhaps stayed away from direct stocks.

Babu Krishnamoorthy: It just shows that even after so many years in the investment world, you can still make mistakes. You believe you're well-informed, that you understand the markets, but when the time comes, emotions take over. Investing right after COVID required more courage than usual, and I didn’t act decisively enough. My biggest takeaway is this: no matter how experienced you are, emotions can still cloud your judgment.

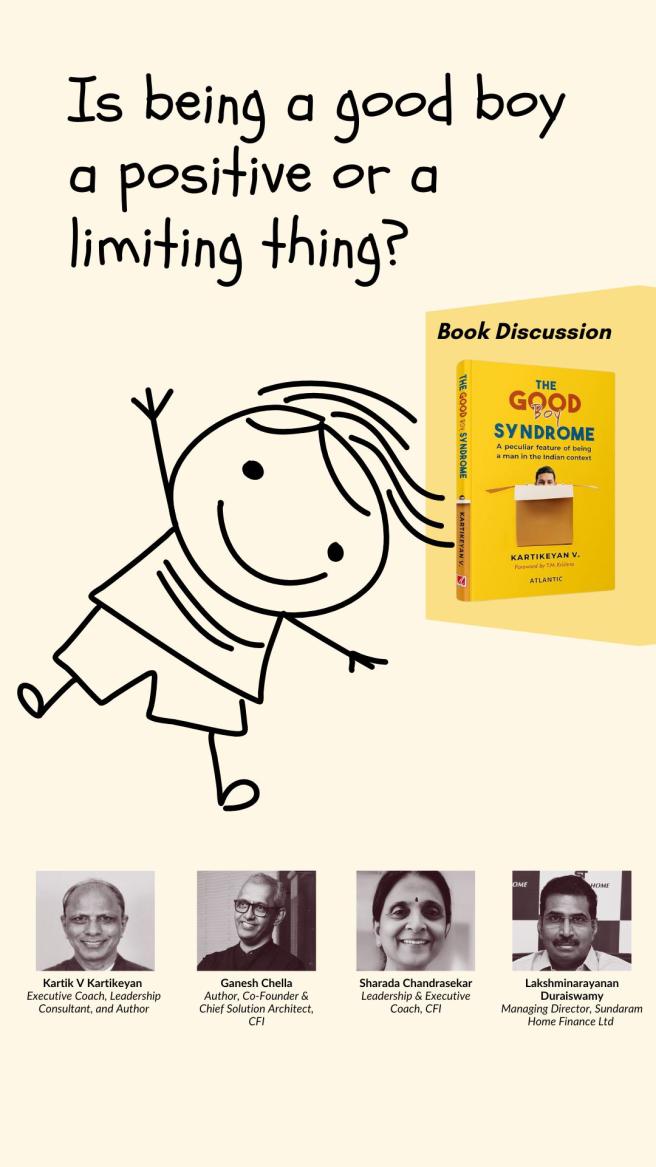

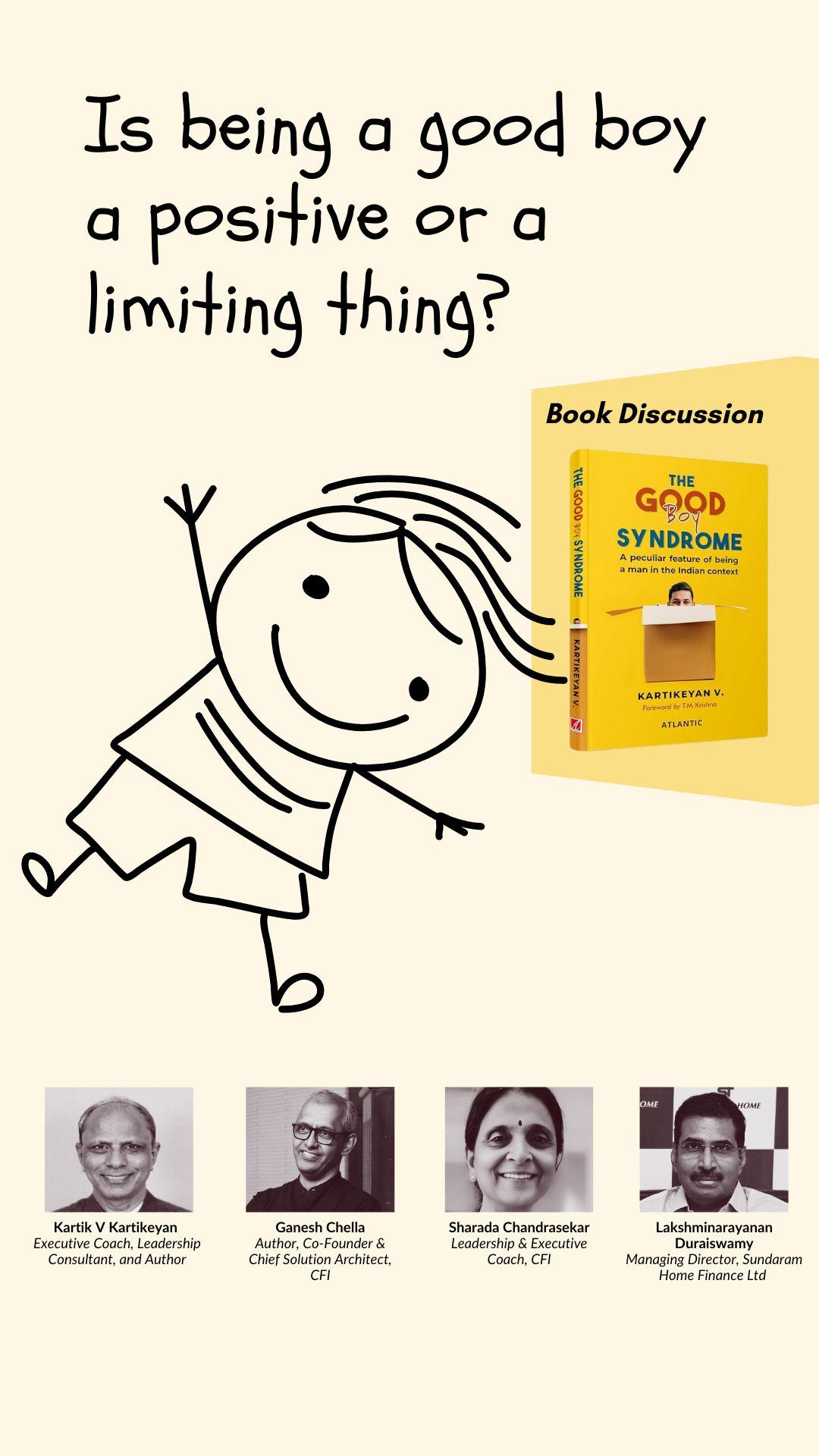

MMA organised a discussion on the book, "Good Boy Syndrome: A Peculiar Feature of Being a Man in the Indian Context, " by Kartik V. Kartikeyan, Executive Coach, Leadership Consultant, and Author The session featured an engaging conversation between the author and a distinguished panel comprising Ganesh Chella, Author, Co‐Founder & Chief Solution Architect, CFI; Sharada Chandrasekar, Leadership & Executive Coach, CFI; and Lakshminarayanan Duraiswamy, Managing Director, Sundaram Home Finance Ltd

Ganesh Chella: The Good Boy Syndrome is an intriguing term. As a coach, a student of human behavior, and an observer of social change, I think that understanding the Indian male his role in society, at home, and at work is essential today, more so because the Indian female is evolving at an astronomical pace. Many questions about social dynamics today could be better answered by exploring the evolving identity of the Indian male. So perhaps we can begin by asking you, Kartik, to describe what you mean by the "good boy." How can someone reflect and ask themselves: Am I a good boy? And more importantly, Is being a good boy a positive or a limiting thing especially in organisations?

Kartik V. Kartikeyan: The “Good Boy” is within each of us it’s not strictly about gender. Whether you’re a man or a woman, there’s a part of us that wants to be ‘good,’ to be accepted, to do what is expected. Of course, society and biology shape different expectations of what being a “good girl” or a “good boy” means.

As I reflected on my own life what it has been about, what I’ve done I began noticing patterns. These weren’t just personal. I saw the same behaviours all around me. That’s when I realised: the “Good Boy” isn’t rare or hidden. He’s everywhere. He is the one who upholds the existing order whether it’s the expectations of family, society, the organisation, or even children. He doesn’t just comply; he sustains, reinforces, and spreads those expectations. He becomes a custodian of the status quo. But the “Good Boy” isn’t without cost. He carries joys,

The good boy isn’t the captive property of any particular system. What’s interesting is that this concept isn’t strictly about a moral compass what society sees as good or bad.

sorrows, and silent struggles often in isolation.

In a patriarchal society like India, the “Good Boy” plays a crucial role in sustaining that patriarchy. Even as structures of patriarchy are questioned or deconstructed, it remains in the system’s interest to keep the “Good Boy” alive. And this dynamic isn’t limited to families or society it’s deeply embedded in organisational life as well. The corporate world is no exception.

Lakshminarayanan Duraiswamy: Can we draw parallels between the "Good Boy" and corporate life? In a corporate setup, the good boy might be defined by his performance, loyalty, or a few other traits. What’s your perspective on that?

Kartik V. Kartikeyan: The good boy isn’t the captive property of any particular system. What’s interesting is that this concept isn’t strictly about a moral compass what society sees as good or bad. Rather, the good boy adapts to the context he is in and plays by those rules.

Take, for instance, the practice of honour killing not just in India, but in many

countries. It’s a shocking, deplorable, and shameful reality. Often, it’s the brother of a girl who has married outside her caste who carries it out. In the eyes of the family, he’s considered a good boy, even though it’s a criminal act.

The same applies to corporate settings. The good boy upholds the order he lives by what he has learned and aligns with what the organisation seeks to create. In my interviews with various people, most described the good boy as someone who values and lives by organisational norms.

But there are limitations to being that good boy and that’s an important aspect to reflect on.

Sharada Chandrasekar: In my long experience of working with many men in the corporate sector and increasingly with women I’ve observed that quite a few women also exhibit strong “good boy” qualities. Recognising that you are a “good boy” is, in itself, an act of self-awareness. And it is this self-awareness that becomes the starting point for transformation. The “Good Boy Syndrome” can play a significant role in sustaining relationships whether in families, marriages, or teams.

As a parent, I often found myself uncertain about how to help my children set boundaries. I used to think of boundaries as restrictive but over time, I’ve come to see that they can also be profoundly

enabling. They are not about confinement, but about creating the space necessary for autonomy and growth. Carl Jung once said, “The hardest boundaries to set are often the ones that free us most.” That insight resonates deeply with me.

Kartik V. Kartikeyan: Carl Jung’s quote is a very profound statement. The "Good Boy" exists on a spectrum of multiple identities. On one end, there’s the self-centric boy. There are no truly “bad boys.” Then there’s the equivocal boy neither self-centric nor clearly a good boy he lives in between. And then, we have the “ungood boy.” He’s not bad either but he stands in contrast to the good boy. The ungood boy is what you begin to uncover when you engage deeply with Jung’s insight. He struggles with setting boundaries, because doing so doesn’t come naturally to him. The good boy, on the other hand, doesn’t have to set boundaries he adapts to and lives within the ones that are given to him by the system.

I grew up as a Tamil Brahmin boy. I studied in Vivekananda College and pursued a B.Com degree. The family expectation was clear I was supposed to do a CA. If I’d taken the science stream, then engineering or medicine would have been the acceptable paths. None of these felt right to me. I didn’t feel confident enough to pursue CA. A friend suggested I try for an

The good boy does have a certain modicum of autonomy what I would call conditional autonomy.

MBA. I got into XLRI and everything changed. The rules, regulations, and boundaries I had grown up with were blown away by the winds of XLRI. It challenged all my assumptions about what it means to live within boundaries. That was the first time I started exploring the "ungood boy" within myself.

One of the defining features of all human systems is boundaries. These can be physical, psychological, emotional, or social. Boundaries are meant to protect the well-being of those within the system. But they also define the scope of your autonomy what you can and cannot do. The good boy carefully figures out what he can do and more importantly, what he’s not expected to do. If, by chance, he steps outside those expectations, he risks being seen by the system as a “bad boy.”

Boundaries are often shaped by the expectations of those around us. These expectations frequently take the form of unspoken commandments like: take responsibility, be the provider, contain your emotions, respect your elders, don’t ask too many questions. They are rarely questioned, yet deeply influential, quietly defining the limits of who we’re allowed to

be. The "ungood boy" begins to question these. He asks, Why should I accept these boundaries? Why can’t I set my own? He’s like a cricketer stepping out of the crease and hitting a boundary and exercising autonomy. How boundaries are drawn, held, or challenged determines whether someone is seen as a good boy or an ungood boy.

Sharada Chandrasekar: Some behaviours that signify being a good boy can actually be limiting. The question is how can he begin to explore his own autonomy by stepping out of that shell? How does he break free from the constraints of the 'good boy' identity in order to discover who he truly is?

Kartik V. Kartikeyan: The good boy does have a certain modicum of autonomy what I would call conditional autonomy. It may sound like an oxymoron, but it’s real. He has autonomy to operate within a defined radius. Now, that radius may be narrow, constrictive, or relatively wider it depends on the context, whether it's the family or the organisation he's part of. Different settings offer different diameters of boundaries within which the good boy can function.

Societal norms have also evolved significantly. Practices that were uncommon 30 years ago like dating or live-in relationships are increasingly part of today’s social fabric. So, a person who embraces these may still be considered a

Many of these male leaders may themselves be “good boys” or self-centric boys, operating within a patriarchal framework.

good boy, as long as he operates within the autonomy permitted by his current context.

Being a good boy isn’t a moral label. Goodness here is defined by the expectations of the context in which a person lives. The ungood boy, in contrast, operates from a different kind of autonomy one that is self-authored, not conditional. He defines and claims his own space.

Ganesh Chella: Organisations continue to struggle with women’s participation in the workforce. We often find that beyond a certain level, the number of women progressing to middle or senior management positions is limited. While part of this is shaped by what women themselves choose or want, how much of it could be attributed to the Good Boy Syndrome?

Kartik V. Kartikeyan: I believe the Good Boy Syndrome is a fairly significant contributor to this phenomenon. Let me explain why. Traditionally, organisations are hierarchical and power is delegated downward. If I’m the executive head of an organisation, it’s often easier for me to maintain control and continuity by promoting the “good boy”

someone who upholds the existing order. This happens even if the individual isn’t fully competent or suited for the senior role. His “good boyness” may not lead to real effectiveness, but from a leadership standpoint, it serves the interests of those in power to support and promote such individuals. The good boy continues to enjoy the protective patronage of senior leaders because it helps them preserve their own agendas and organisational culture.

Now, if we bring women into this picture, their increased participation often presents challenges to these traditional bastions of male leadership. Many of these male leaders may themselves be “good boys” or self-centric boys, operating within a patriarchal framework. And let’s not forget India is still very much a patriarchal society.

That patriarchy is just as present in corporate boardrooms as it is in rural villages. So, in such systems, it’s more likely for good boys or self-centric boys to rise to the top. We may see more ungood boys emerge over time too. But both the rise of ungood boys and increased women participation introduce a level of disruption and inconvenience for traditional male power structures.

Ganesh Chella: One paradigm of the Good Boy could be the belief that men must be the providers,

while women should be the caregivers. That’s also a possible interpretation. But the larger question is: will the Good Boy be willing to re-examine these structures and boundaries, especially when greater women participation in the workforce demands it?

Sharada Chandrasekar: I absolutely believe the time has come for the Good Boy Syndrome to be explored deeply and personally by individuals in every kind of relationship and context, even as team players. The question to ask is: What am I losing out on by being a good boy? And more importantly: What more can I become if I step out of that identity?

I’ve come across many men in my coaching practice often spouses of the women I coach who carry this Good Boy dimension. And many of these women don’t know how to challenge it, because their own expectations and identities are evolving very rapidly perhaps even more rapidly than those of their male partners. And I say this with a great deal of compassion. Men also need support. They need workshops, programs, and safe spaces just like women have had to step out of traditional roles and discover who they truly are.

Kartik V. Kartikeyan: The good boy is not a trap. If we say it is a trap, then there is no hope for the good boy.

Ganesh Chella: In many organisations, especially in the early stages, we emphasise compliance and conformance to processes. This helps drive scale, discipline, operational excellence things run smoothly that way. But then, suddenly, we expect people to be innovative, think outside the box, and deal with disruption. Do you see any connection between this shift and the Good Boy archetype?

Lakshminarayanan Duraiswamy: Absolutely. We tend to typecast the Good Boy as someone who follows the rules, conforms to processes, and obeys orders qualities that leaders often appreciate. But in today’s organisations, there’s also a large number of people who don’t conform to any of these processes yet they perform, and they deliver results.

It’s a paradox. Many of us come from structured environments Six Sigma, quality systems, compliance-heavy cultures. And then we find ourselves leading teams with a fair number of what I’d call “cowboys” people who operate on their own terms and get the job done, even if they ignore every standard process along the way.

So now, as leaders, we’re managing two very different groups: the Good Boys, who conform, and the non-conformists, who often outperform but don’t fit the mould. In some teams take large sales forces, for

instance you can’t realistically associate strict compliance or structured processes with how they operate. And I say that with no disrespect. You need both types to coexist. You can’t build an organisation solely around conformists and expect to thrive, especially in today’s dynamic, results-driven environment.

This paradox isn’t as stark in family settings. There, if someone doesn’t conform to family values, they become an outcast. But they’re not expected to contribute in any material way either. In organisations, however, you have to include everyone and still deliver results.

And to me, this paradox isn’t new. Organisations have always had both compliance-oriented teams like finance or operations, and then others who work more instinctively, creatively, or chaotically. What’s changed now is the proportion. In the new economy especially with startups and more agile environments the number of nonconformists is growing. Meanwhile, the traditional conformists are slowly decreasing in number. That’s creating a new imbalance and leadership today has to reckon with how to manage this evolving mix.

Kartik V. Kartikeyan: Yes, the shift is definitely happening. Organisations today are increasingly demanding what I would call a

bit more ungoodness a willingness to challenge, disrupt, question norms.

Based on the data I’ve collected, around 80% of Indian males identify with what we call Good Boy traits. These identities include roles like custodian, provider, guide, or mentor. When I narrow the data to Indian males with less than 10 years of work experience, the percentage drops slightly from 80% to about 70%. So yes, there is movement, but it’s not a dramatic shift yet.

Ravi Kyran, the CHRO of Bajaj Auto said something insightful. He noted that 30 years ago, the biggest struggle for corporate leaders was guilt “Have I gone over budget? Did I make a mistake?” But today, what troubles leaders most is anxiety a persistent unease about the future, change, disruption.

Ganesh Chella: How much of the Good Boy Syndrome is peculiar to the Indian context? Would its characteristics differ globally?

Kartik V. Kartikeyan: The characteristics certainly differ from context to context. Cultural and social settings shape how the Good Boy manifests.

Sharada Chandrasekar: While there are cultural differences, I also believe there are many underlying similarities. In most cultures, individuals are exposed to a mix of societal and familial expectations. Even if the

society itself seems quite different, especially for the younger generation, these influences often mirror each other. So, while the form may vary, the relevance of the Good Boy construct may still be significant across different cultures though it may manifest or be interpreted differently.

Kartik V. Kartikeyan: That makes sense. If I were to consider the United States or other developed nations in the Global North, the peculiarity there might come more from the archetype of the dominant male. So yes, there's still a peculiarity, but it’s rooted in a very different cultural context than ours. Now, addressing another question was there a personal turning point when I recognised the Good Boy in myself?

Yes, painfully so. But it wasn’t like I woke up one morning and suddenly realised, ‘Oh, my life has been that of a good boy.’ It has been more of an ongoing inquiry an evolving self-exploration over time. Since the 1990s, I’ve been associated with two significant institutions: Sumedhas and Group Relations India. Both are rooted in behavioural sciences and have offered me structured spaces to reflect and question myself. These settings consistently invited introspection asking questions like, ‘What are you doing with your life? Who are you? What are you really up to?’ So, rather than a single dramatic moment, it was more of a

turning arc a gradual unfolding of selfawareness through continuous inquiry and reflection.

Ganesh Chella: When you associate a voice with the Good Boy, is it the voice of the mother or the spouse?

Kartik V. Kartikeyan: It’s the mother especially in the early stages of identity formation.

Ganesh Chella: What needs to change?