US GULF PORTS: EXTENDING MARKET REACH

MISSISSIPPI MARKET MOVES With larger vessels now centre stage, extended market reach is a prime target for US Gulf ports. The Mississippi is a strong focus in this respect including for the potentially game changing Plaquemines project. Mike Mundy reports

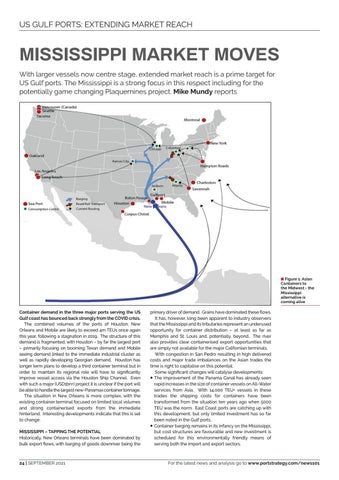

8 Figure 1: Asian Containers to the Midwest - the Mississippi alternative is coming alive

Container demand in the three major ports serving the US Gulf coast has bounced back strongly from the COVID crisis. The combined volumes of the ports of Houston, New Orleans and Mobile are likely to exceed 4m TEUs once again this year, following a stagnation in 2019. The structure of this demand is fragmented, with Houston – by far the largest port – primarily focusing on booming Texan demand and Mobile seeing demand linked to the immediate industrial cluster as well as rapidly developing Georgian demand. Houston has longer term plans to develop a third container terminal but in order to maintain its regional role will have to significantly improve vessel access via the Houston Ship Channel. Even with such a major (USD1bn+) project it is unclear if the port will be able to handle the largest new-Panamax container tonnage. The situation in New Orleans is more complex, with the existing container terminal focused on limited local volumes and strong containerised exports from the immediate hinterland. Interesting developments indicate that this is set to change. MISSISSIPPI – TAPPING THE POTENTIAL Historically, New Orleans terminals have been dominated by bulk export flows, with barging of goods downriver being the

24 | SEPTEMBER 2021

primary driver of demand. Grains have dominated these flows. It has, however, long been apparent to industry observers that the Mississippi and its tributaries represent an underused opportunity for container distribution – at least as far as Memphis and St. Louis and, potentially, beyond. The river also provides clear containerised export opportunities that are simply not available for the major Californian terminals. With congestion in San Pedro resulting in high delivered costs and major trade imbalances on the Asian trades the time is right to capitalise on this potential. Some significant changes will catalyse developments: 5 The improvement of the Panama Canal has already seen rapid increases in the size of container vessels on All-Water services from Asia. With 14,000 TEU+ vessels in these trades the shipping costs for containers have been transformed from the situation ten years ago when 5000 TEU was the norm. East Coast ports are catching up with this development, but only limited investment has so far been noted in the Gulf ports. 5 Container barging remains in its infancy on the Mississippi, but cost structures are favourable and new investment is scheduled for this environmentally friendly means of serving both the import and export sectors.

For the latest news and analysis go to www.portstrategy.com/news101