THE PROPERTY CHRONICLE

-· Town &Country , J Whenyou know,you know.™ JULY2023

Town & Country CONTENTS Page Letter from Principal (Brent Worthington) 4 LJ Hooker Home Smart Newsletter –Considering Purchasing a new build – Here’s what you need to know. 6 REPORTS & SURVEYS REINZ Monthly Property Report 9 • Contents Page with link to full report • Press Release (page 3) • Market Snapshot (page 4) • Annual Median Price Changes (page 7) • Seasonally Adjusted Median Price (page 9) 10 11 12 13 14 REINZ – Monthly House Price Index • Summary • Full Results with link to full report 16 REINZ & Tony Alexander Real Estate Survey ( July 2023) 19 Realestate.co.nz – The New Zealand Property Report (1-20 June 23) • More Buyers, Less Choice 26 TradeMe - Property News (May Index - 22 June 23) FINANCE & LENDING • Mortgages & Tony Alexander – Mortgage Advisors Survey July 2023 • One Roof – Looming Debt to Income borrowing rules hit buyers hard • Loan Market – Keith Jones introduction • Loan Market – Cash Rate held in July – Could debt consolidation be worthwhile? • Kainga Ora Shared Ownership Scheme 39 44 48 50 Property Management - Rent Exchange • Newsletter 53 • Unenforceable Clauses in Tenancy Agreements 56 • Carpets – replacement rules 60 Properties - LJ Hooker Town & Country • Current Listings 62 • Featured Properties • Recently Sold 65 Our People • Brent Worthington • Lina Roban • Lorretta Dale • Apollo Auctions 69 70 71 72 SuperGold Welcome Here

Newsletters

21July2023

Hi HousingMarketShowsResilienceDespiteChallenges

Inasurprisingturnofevents,theNewZealandresidentialhousingmarkethasshown remarkableresilienceinthefaceofongoingchallenges.

AccordingtothelatestdatafromtheRealEstateInstituteofNewZealand(REINZ),themonth ofJune2023witnessedanotableincreaseinsales,defyingthetraditionalseasonaltrend.

REINZchiefexecutiveJenBairdpointedoutthatJunetraditionallytendstobeaslower monthforthepropertymarket,however,thisyearwesawariseinsalescountsalongsidea hesitancyfromsellerstolist.

Thefiguresspeakforthemselves,witha14.6percentyear-on-yearincreaseinthetotal numberofpropertiessoldacrossNewZealandinJune2023.That’s5,629propertiessoldthis yearcomparedto4,912inJune2022. However,themarket'sbuoyancyisaccompaniedbyadeclineinthenumberofproperties availableforsale.AttheendofJune,thetotalnumberofpropertiesforsaleacrossNew Zealanddecreasedby6.1percentcomparedtothepreviousyear,amountingto24,676 properties.

Bairdnotedthatthischangeininventorylevelshascontributedtolowerlevelsofnew propertylistingsbuthasalsoresultedinanincreaseinthenumberofsuccessfulsales.

“Salespeopleacrossthecountryarereportingincreasedfirsthomebuyeractivityatopen homes,withtheeasingofLVRrestrictionsthatcameintoeffecton1Junebringingmore peopleoutlooking.

“Althoughactivityhasincreased,cautionremainsasinterestrates,apendingelectionand furtherstraincausedbythecost-of-livingtempersputtingpenonpaper.”

Brent Worthington Principal and Licensee Agent

continued over...

Hooker Town&Country & Property Management 1/233 Great South road, Drury 0292 965 362 Town&Country

LJ

SarahWood,CEOofrealestate.co.nz,emphasisedtheimportanceofrecognisingthe cyclicalnatureofthemarket."Inthepast10years,morethanhalfofNewZealand'sdistricts sawtheiraskingpricesatleastdouble,"Woodsaid. Sheencouragedpropertyownerstoremainpositive,remindingthemthatthemarket's fluctuationsaretemporaryandthatdownwardpricetrendsareunlikelytopersistinthe longterm.

Whilethemedianhousepricehasstabilised,independenteconomistTonyAlexander expectstheaveragehousepricetostartrising.

Heattributeshousepriceincreasesto:migration,risingrents,risingincomesandsaved deposits,easinglendingcriteria,increasedtouristnumbersleadinginvestorstoswitchto servicingforeignersinsteadoflongtermaccommodation,declineinnewhome constructionandtheactivationofreadybuyerswhowaited.

Thecombinationofincreasedbuyerinterest,limitedinventory,andapositivelong-term outlooksuggeststhattheresidentialhousingmarketremainsresilientdespitethe challengesitfaces

AsalwaysItrustyouenjoythismonth'spublication.

Kindregards

Brent

Brent Worthington Principal and Licensee Agent

LJ Hooker Town&Country & Property Management

Town&Country

1/233 Great South road, Drury 0292 965 362

Considering Purchasing a New Build? Here's What You NeedtoKnow

If you're considering buying a house, one important decision you'll face is whether to purchase an existing property or buy off the plan. Whiletheappealofabrandnew,never-lived-inhome isundeniable,thereareseveralfactorstoconsider beforemakingafinaldecision.

Onesignificantadvantageofbuyingofftheplanisthe opportunitytohaveinputintothedesignofyournew home.Thismeansyoucanhaveamodernand technologicallyadvancedhomewithouttheneedfor costlyrenovations.Additionally,youcansuggest customisationsthatcatertoyourspecificneedsand preferences.

Therearecertainbenefitsassociatedwithbuyinga newhome.Incentives,suchastheFirstHomeGrant andHomeStartGrant,offermorefinancialbackingfor firsthomebuyerswhopurchaseanewbuild.

Anotheradvantageofbuyingofftheplanisthe potentialtopurchaseatthecurrentmarketprice,even thoughthepropertywillbecompletedlaterwhen pricesmayhavelikelyincreased.

However,it'sessentialtobeawareofthedownsidesof buyingofftheplan.

Unfortunately,predictingfuturemarketconditionsis impossible,andthereisariskthathousepricesmay fallbetweenthesigningofthecontractandthe completionofconstruction.

Additionally,interestratesmayriseduringthisperiod, affectingyourfinancialsituation.

Furthermore,whenbuyingofftheplan,youarereliant onthebuilderordeveloper.It'scrucialtothoroughly researchtheirreputation,financialstability,andtrack record.Visittheirwebsite,readonlinereviews,and investigatetheirpreviousprojectstoensuretheyare reliableandtrustworthy.

Beforecommittingtoanoff-the-planpurchase,it's advisabletophysicallyinspectthebuildingsiteand reviewthebuildingplans.Familiariseyourselfwiththe localmarketconditionsinthatparticularareaand discussyourexpectationswiththebuilderordeveloper.

Tomakeaninformeddecisionwhenbuyingofftheplan, considerthefollowingtips:

ResearchtheDeveloper

Conductthoroughresearchonthedeveloper'sportfolio, previousprojects,andreputation.Lookforpositive reviewsandtestimonialsfrompastbuyers.

UnderstandtheContract

Therearetypicallytwotypesofcontractswhenbuying offtheplan.Familiariseyourselfwiththespecificterms andconditions,seeklegaladvice,andensureyou understandthedepositrequirementsandanypotential changesinpropertyvalue.

InspectSimilarProjects

Requestevidenceofthedeveloper'spastprojectsand inspectsimilar-stylehousestoassessthelayoutand buildquality.Reachouttopreviousbuyersfortheir feedbackandsearchforanynegativereviewsormedia reports.

AskaboutCustomisationOptions

Inquireabouttheflexibilityforcustomisationinthe designandlayoutofyournewhome.Understandthe optionsprovidedbythedeveloperandbuilderupfront.

ljhooker.co.nz

SecureFinancingEarly

Arrangehomeloanpreapprovalinadvanceorapply foraloanasconstructionnearscompletion Work closelywithamortgagebrokertonavigatethe uniqueaspectsoffinancinganoff-the-planproperty

BePreparedforDelays

Unexpectedconstructiondelayscanoccur,impacting yourmove-inorrentalplans Reviewthecontractfor anysunsetclausesandhaveacontingencyplanin place,includingafinancialcushionforunexpected costs

ConsidertheFutureMarket

Assessthecurrentandpredictedpropertymarket conditions,aswellasanyfactorsthatmayinfluence thevalueofyourhome Conductthoroughresearch onthelocationanditsfuturepotential

ReviewtheFloorPlanandSpecifications

Scrutinisethecontract,payingcloseattentiontothe floorplan,roomsizes,garage,grounds,andavailable colourandfinishoptions

StayInformedduringConstruction

Maintainregularcommunicationwiththedeveloperor theirrepresentativetostayupdatedonanychanges ordevelopments Seeklegaladvicefromaproperty lawyerorconveyancerexperiencedinoff-the-plan builds

Remember,buyingofftheplancanbeacomplexand lengthyprocess Byconsideringthesefactorsand seekingprofessionalguidance,youcanmakean informeddecisionthatalignswithyourneedsand preferences

Yearningforawarmtropicalgetawaybutunableto travel?AreyouseeingphotosofyourfriendsinBalior relaxingonawarm,PacificIsland?Noworries!Youcan stillrecreatetheserenityandrelaxationofatropical retreatwithintheconfinesofyourhome

Theswayingpalmtrees,gentlewaves,andwarm beachbreeze thesemagicalmomentscanstaywith youallyearround Tobringthatsenseofwellbeingand tranquilityintoyoureverydaylife,consider incorporatingelementsofthetropicsintoyourhome décor

Whileyoudon'thavetoreplicateanentireBalineseor Hawaiianabode,youcandrawinspirationfromyour favouritetropicalplaces Seekdesigncuesfromtheir colourpalettes,fabrics,andlocalplantlifewiththeir signaturescents.

Infuseyourspacewiththerelaxingvibesbychoosing therightpaintcoloursanddécor.Whetherit'sthelush greensofpalmtreesagainstablueskyorthevibrant orangesoftropicalflora,letthesenaturalhuesguide yourchoices Createaharmoniousatmosphereby integratingthesamecoloursthroughoutyourhome, ensuringconsistencyinflooringandtrim

Incorporateovergrownpottedplantsoragardenoasis toenhancethetropicalambiance.Ifyouhavea courtyard,transformitintoatrueretreatwithscented plants,atranquilwaterfeature,andacomfortable hammock Embracethesoothingelementsofnature, includingnight-bloomingflowerslikefrangipani,to immerseyourselfinatropicalparadise

CapturetheessenceofCaribbeanwaterswitha paletteofbluesandsandytones.Addanaccent colourlikeamutedgreentoaddinterest Invokethe spiritofHawaiiwithcalminggreens,captivating purples,andpink-redhues Createafreshandinviting GreekIslands-inspiredspacewithwhitesandsplashes ofspearmint,turquoise,andblue-green

Byselectingtherightcoloursandincorporating elementsofnature,comfort,andrelaxation,youcan transformyourhomeintoapersonaltropical sanctuary

Saygoodbyetotheyearningforatropicalgetaway andsayhellototheblissofbeingonvacationevery day!

Beforemakinganydecisionsyoushouldconsultalegalor professionaladvisorLJHookerNewZealandLtdbelievestheinformationinthispublicationiscorrectandithasreasonablegroundsforanyopinionorrecommendationcontainedinthis publicationonthedateofthispublication NothinginthispublicationisorshouldbetakenasanofferinvitationorrecommendationLJHookerNewZealandLtdacceptsnoresponsibilityfor anylosscausedasaresultofanypersonrelyingonanyinformationinthispublication ThispublicationisfortheuseofpersonsinNewZealandonlyCopyrightinthispublicationisownedby

Theinformationcontainedinthispublicationisgeneralinnatureandisnotintendedtobepersonalisedrealestateadvice

LJHookerNewZealandLtd

LicensedREA2008

Youmustnotreproduceordistributecontentfromthispublicationoranypartofitwithoutpriorpermission

ljhooker.co.nz

Reports & Surveys

MONTHLY PROPERTY REPORT. 13 July 2023

2| REINZ Monthly Property Report Contents 3 PressRelease 4 MarketSnapshot 7 AnnualMedianPriceChanges 9 SeasonallyAdjustedMedianPrice Regional Commentaries Northland ........................................................................................................................................................... 10 Auckland .............................................................................................................................................................. 12 Waikato 14 Bay of Plenty 17 Gisborne 20 Hawke’s Bay 22 Taranaki 24 Manawatu/Whanganui 26 Wellington 39 Nelson/Marlborough/Tasman 32 West Coast 34 Canterbury 36 Otago 39 Southland 42 CLICKHEREFORFULLREPORT

REINZ June data: Buyer activity and sales up, new listings still lag

The Real Estate Institute of New Zealand’s (REINZ) June 2023 figures show a renewed level of activity emerging.

REINZ Chief Executive Jen Baird says June traditionally tends to be a slower month for the property market, however this month we are seeing a rise in sales counts alongside a hesitancy from sellers to list.

Compared to June 2022, this month has shown a notable increase in sales. The total number of properties sold across New Zealand in June 2023 was 5,629, up from 4,912 in June 2022 (+14.6%), year-on-year. New Zealand excluding Auckland sales counts increased by 17.4% year-on-year from 3,203 to 3,761.

At the end of June, the total number of properties for sale across New Zealand was 24,676, down 6.1% (1,595 properties) from 26,271 year-on-year, and down 7.5% month-on-month. New Zealand excluding Auckland was down from 15,820 to 15,655, a decrease of 165 properties annually.

“With sales counts up year-on-year but down slightly month-on-month, the change in direction of the national inventory level is driving ongoing lower levels of new property coming to market and an increase in the number of sales being made,” says Baird.

Historical data tells us that we typically expect a decrease in sales when moving from May to June across New Zealand. When that seasonal trend is considered, by applying seasonal adjustment to the sales count figures, we see those sales this June exceeded expectations when compared to the sales count in May 2023.

Nationally, new listings decreased by 21.2%, from 7,893 listings to 6,218 year-on-year, and a 15.5% decrease compared to May 2023 from 7,359. New Zealand excluding Auckland listings decreased 19.8% year-on-year from 4,994 to 4,005.

“Salespeople across the country are reporting increased first home buyer activity at open homes, with the easing of LVR restrictions that came into effect on 1 June bringing more people out looking. Although activity has increased, caution remains as interest rates, a pending election and further strain caused by the cost-of-living tempers putting pen on paper,” states Baird.

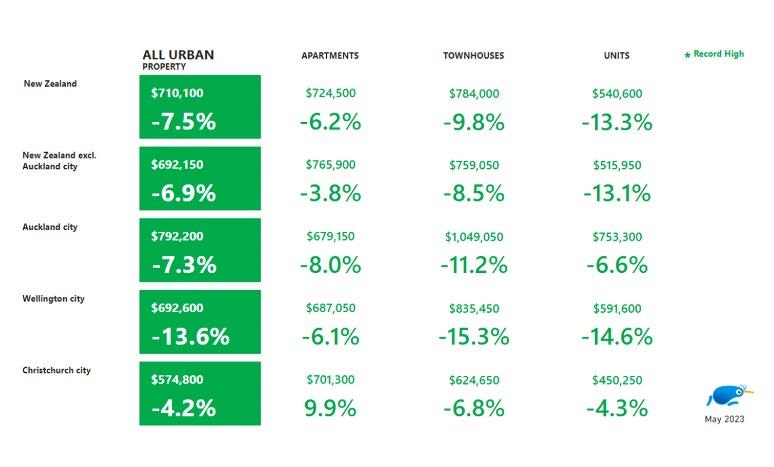

Nationally, the June 2023 median price decreased 8.2% year-on-year to $780,000 from $850,000. Days to sell have risen to 49 days for June 2023 — up 4 days compared to June 2022 and no change from May 2023. The West Coast and Tasman regions saw an annual increase in median price — up 8.1% to $400,000 and 7.4% to $800,000 respectively.

“In the last three months ending June 2023, 15,934 sales have occurred, a 1.2% increase year-on-year. A lack of listings and the challenge of navigating the current economic climate are putting pressure on the market. Commentators say there are harder times ahead, but sales are still happening, people are still making choices about where and how they live, and these choices necessitate a property transaction,” adds Baird.

The REINZ House Price Index (HPI) for New Zealand, which measures the changing value of residential property nationwide, showed an annual decrease of -9.0% for New Zealand and a -8.0% decrease for New Zealand excluding Auckland.

PRESSRELEASE13July2023 Page3

MEDIAN HOUSE PRICE YEAR-ON-YEAR ... National $780,000 -8.2% ... NZ excl Aki $680,000 -8.1% ... Auckland $1,000,000 -12.5% MEDIAN HOUSE PRICE MONTH-ON-MONTH ► National $780,000 0.0% ... NZ excl Aki $680,000 -0.7% ... Auckland $1,000,000 0.8% 49 Median Days to sell nationally +4 days year-on-year REINZ HOUSE PRICE INDEX YEAR-ON-YEAR Q ... National 3,518 -9.0% ... NZ excl Aki 3,667 -8.0% ... Auckland 3,310 -10.6% REINZ Monthly Property Report SALESCOUNT YEAR-ON-YEAR � ... National 5,629 14.6% ... NZ exclAki 3,761 174% .. Auckland 1,868 9.3% SALES COUNT MONTH-ON-MONTH � ... National 5,629 -4.1% ... NZ exclAki 3,761 -6.7% Auckland 1,868 1.9% 49 • NZ exclAki +4 days 47

Auckland +2 days SEASONALLYADJUSTED SALES COUNT MONTH-ON-MONTH ���<I C> �Pv�� ... ... ... National 6.9% NZ exclAki 6.2% Auckland 14.7% RElNZ REAL ESTATE INSTITUTE OF NEW ZEALAND Page4

Market Snapshot -June 2023

•

Page7

Median Prices

Our two biggest cities have seen ongoing year-on-year median price declines for the beginning of 2023.

There were no record median prices at the regional level.

West Coast was the only region to have a median price increase year on year.

There were no record median prices at the regional level this month. There were no Territorial Authority record median prices this month, the first time this has happened in the month of June since 2011.

Three quarters (75%) of all Territorial Authorities have had no median record price in any of the past 12 months

Sales counts

Historical data tells us that we typically expect a decrease in sales when moving from May to June. When that seasonal trend is taken into account by applying seasonal adjustment to the sales count figures, we see those sales this June exceeded expectations when compared to the sales count in May 2023.

Five regions had increases in sales counts month-on-month from May 2023 to June 2023.

The average number of sales in the past 10 years for the month of June is 6,506.

Days to Sell

Over the last ten years the average of the median days to sell for the month of June is 38 days.

West Coast had the highest median Days to Sell since September 2022

Southland had the lowest median Days to Sell since November 2022

Page9

In terms of the month of June, June 2023 had the highest median Days to Sell in

• Nelson since 1999

• NZ since 2008

• Otago since 2009

• NZ Excl. Auckland, and Wellington since 2011

• Tasman since 2012

• Gisborne, Manawatu-Whanganui and Taranaki since 2014

• Marlborough since 2015

House Price Index (HPI)

No regional HPI records this month.

Wellington, for the first time in 19 months, is not in the bottom two ranked regions for the YOY HPI movement.

Southland is the top-ranked HPI year -on-year movement this month. Otago is second and Taranaki is third.

Inventory

Six of fifteen regions had at least a 10% YOY increase in inventory.

Seven regions had less inventory than they had one year ago.

Listings

All regions had a decrease in Listings since June 2023 except for Northland, a notable exception with a 19.0% increase in listings.

Eight of fifteen regions have had listings decrease by more than 20% year on year.

Inventory and listing data come from realestate.co.nz.

Auctions

Nationally, 9.8% (549) of properties were sold at auction in June 2023, compared to 11.7% (575) in June 2022.

New Zealand excluding Auckland saw 6.6% of properties (250) sell by auction compared to 9.1% (290) the year prior.

© REINZ - Real Estate Institute of New Zealand Inc. MONTHLY HOUSE PRICE INDEX REPORT 13 July 2023

REINZ House Price Index (HPI)

As one of the country’s foremost authorities on real estate data, we are proud to bring you the REINZ HPI (House Price Index). It provides a level of detail and understanding of the true movements of housing values over time to a higher standard than before. The REINZ HPI was developed in partnership with the Reserve Bank of New Zealand and provides a more complete picture of the New Zealand housing market.

BENEFITS OF THE REINZ HPI

Data on median and average house prices is open to being skewed by market composition changes. This means observed changes in these values could be almost entirely due to the changed nature in the underlying sample (e.g. an unusually large representation of high end housing sales) rather than changes in the true market value. The REINZ HPI takes many aspects of market composition into account resulting in greater accuracy.

ABOUT REINZ HPI

The REINZ HPI is based on the SPAR methodology and has been proven to be the most comprehensive tool to understand the housing market for four main reasons:

• Timeliness - This is the number one advantage of REINZ HPI. REINZ data is based on sales as they occur (unconditional) so is the most up to date data source in NZ.

• Accuracy - REINZ data is supplied by the actual sales prices supplied by its members so has a high level of accuracy.

• Stability - REINZ has the most data available to it so can provide the most stable and complete one month indices.

• Disaggregation - Indices can be disaggregated to a lower level than before. Disaggregation means you can focus on a smaller data set, allowing comparison of building typology and suburbs, i.e. Three bedroom houses in Manukau.

EXPERT INDUSTRY FEEDBACK

“I have had the opportunity to utilise the REINZ HPI website, and have been involved in advising on the HPI’s preparation. The new index fills a gap in providing reliable up to date information on house price developments across all of New Zealand’s local authorities. It’s wonderful to see REINZ providing this level of detailed data for wider public use. I am already planning to use this data in my own research.”

Dr Arthur Grimes Senior Fellow, Motu Research; and Adjunct Professor, Victoria University of Wellington

“Accuracy and timeliness of information on house price movements is vital for home buyers, sellers, agents, and analysts such as myself. The data from REINZ meets both requirements and gives New Zealand a collection of house price series comparable with the best overseas.”

Tony Alexander Independent Economist and Speaker

“The Real Estate Institute of New Zealand’s Market Intelligence portal opens up to users the ability to interactively compare price trends amongst a wide range of local council regions. Users can pick and choose regions of interest and use the chart tools to instantly compare price performances. For those wanting to look at house prices in more depth there is the capability to download the data in spreadsheet format all the way back to 1992 when the Institute started recording sales price information.”

Nick Tuffley Chief Economist, ASB

The number one advantage between REINZ data and other housing data on the market is that REINZ has access to sales data from the time the price is locked in (unconditional data) as opposed to when the house changes hands (settlement date) which can often be weeks/months later. Therefore, the REINZ HPI is the best and most timely measure of recent housing market activity.

2 | REINZ Monthly House

Index Report

Price

For more information visit: reinz.co.nz/reinz-hpi

JUNE 2023 RESULTS REINZ HOUSE PRICE INDEX

Looking at the REINZ HPI for June 2023, the ‘gold standard’ for New Zealand house price analysis, Jen Baird, Chief Executive at REINZ, says:

The REINZ House Price Index was developed in partnership with the Reserve Bank of New Zealand.

Already being used by the Reserve Bank’s forecasting and macro financial teams, plus the major banks, the REINZ HPI provides a level of detail and understanding of the true movements of housing values over time. It does this by analysing how prices in a market are influenced by a range of attributes such as land area, floor area, number of bedrooms etc. to create a single, more accurate measure of housing market activity and trends over time. Using the Reserve Bank’s preferred Sale Price to Appraisal Ratio (SPAR) methodology, the REINZ HPI uses unconditional sales data (when the price is agreed) rather than at settlement, which can often be weeks later. It is therefore more accurate and timely.

“The REINZ HPI takes many aspects of market composition into account and thus provides more accurate results. When applied to the June data, the HPI indicates that the housing market value nationwide has dropped 9.0% year-on-year. In Auckland, the value decreased by 10.6% and decreased by 8.0% outside of Auckland. Southland takes the top spot in the 12-month ending percentage changes. Otago and Taranaki came second and third, respectively, for annual percentage movement.

“The importance of the HPI is evident in the Otago region this month, where the median sale price tells a different story to the HPI.

“The median sale price in the region decreased 13.3% over the past year, the fourth weakest return compared to the other regions. This suggests a market where performance is very poor in the long term compared to other regions.

“However, the Otago region had the second strongest annual performance of all regions in HPI over the past year with a decrease of 3.0%. Sample composition changes — such as the size of properties or the underlying value of properties sold — can change statistics, such as median, that are purely based on price. However, because the underlying value of each property sold is considered by the HPI, such sample changes have little effect on HPI results. In summary, long-term property value growth in Otago is decreasing at a slower rate than most other regions, a fact that would have remained hidden from those monitoring statistics without access to the HPI.”

3 | REINZ Monthly House Price Index Report

Year-on-year, the HPI indicates that housing market value nationwide has fallen 9.0%, down in Auckland by 10.6% and down outside Auckland by 8.0%.

CLICKHEREFORFULLRESULTS

REINZ & TONY ALEXANDER REAL ESTATE SURVEY

July 2023

CONTENTS

Page 1

• Are more or fewer people showing up at auctions?

• Are more or fewer people attending open homes?

Page 2 Page 3 Page 4

• How do you feel prices are generally changing at the moment?

• Do you think FOMO is in play for buyers?

• Are you noticing more or fewer first home buyers in the market?

• Are you noticing more or fewer investors in the market?

• Are you receiving more or fewer enquiries from offshore?

• Are property appraisal requests increasing or decreasing?

• What are the main concerns of buyers?

Page 5

• Are investors bringing more or fewer properties to the market to sell than three months ago?

• What factors appear to be motivating investor demand?

• Regional results

views of licensed real estate agents all over New Zealand regarding how they are seeing conditions in the residential property market in their areas at the moment. We asked them how activity levels are changing, what the views of first home buyers and investors are, and the factors which are affecting sentiment of those two large groups.

Disclaimer: This report is intended for general information purposes only. This report and the information contained herein is under no circumstances intended to be used or considered as legal, financial or investment advice. The material in this report is obtained from various sources (including third parties) and REINZ does not warrant the accuracy, reliability or completeness of the information provided in this report and does not accept liability for any omissions, inaccuracies or losses incurred, either directly or indirectly, by any person arising from or in connection with the supply, use or misuse of the whole or any part of this report. Any and all third party data or analysis in this report does not necessarily represent the views of REINZ. When referring to this report or any information contained herein, you must cite REINZ as the source of the information. REINZ reserves the right to request that you immediately withdraw from publication any document that fails to cite REINZ as the source. ISSN: 2703-2825 This publication is written by Tony Alexander, independent economist. Subscribe here https://forms.gle/qW9avCbaSiKcTnBQA To enquire about having me in as a speaker or for a webinar contact me at tony@tonyalexander.nz Back issues at www.tonyalexander.nz Tony’sAim To help Kiwis make better decisions for their businesses, investments, home purchases, and people by writing about the economy in an easy to understand manner. This survey gathers together the

MARKET UPTURN UNDERWAY

Welcome to the REINZ & Tony Alexander Real Estate Survey. This survey gathers together the views of licensed real estate agents all over New Zealand regarding how they are seeing conditions in the residential property market in their areas at the moment. We ask them how activity levels are changing, what the views of first home buyers and investors are, and the factors which are affecting sentiment of those two large groups.

The key results from this month’s survey include the following.

• FOMO is rising while FOOP (fear of overpaying) is declining.

• More people are attending open homes and auctions.

• Buyers are getting more concerned about the number of properties available for purchase.

ARE MORE OR FEWER PEOPLE ATTENDING OPEN HOMES?

A net 41% of our 463 respondents have reported that more people are attending open homes. This confirms the strong result in late-May and as is the case for auction attendance is the strongest reading since the start of 2021. Agents in some parts of the country have reported quite large numbers of people attending certain open homes, mainly in the lower to middle end of the price spectrum.

ARE MORE OR FEWER PEOPLE SHOWING UP AT AUCTIONS?

The small net proportion of agents which last month reported seeing more people attending auctions has grown this month to a net 18%. This is the strongest result since late-February 2021 immediately before changes to loan-to-value rules and then alterations to the investor tax regime.

1

HOW DO YOU FEEL PRICES ARE GENERALLY CHANGING AT THE MOMENT?

Only a net 8% of responding agents have reported that they feel prices are falling in their location. This is the least weak outcome since November 2021 when price change observations were undergoing a rapid change downward following the credit crunch of October and November of that year.

ARE YOU NOTICING MORE OR FEWER FIRST HOME BUYERS IN THE MARKET?

For the second month in a row a very strong net proportion of agents have reported seeing more first home buyers in the market. The latest result of a net 56% matches May’s 55% and is well up from the net 16% at the end of 2022 observing fewer young buyers in the residential real estate market.

DO YOU THINK FOMO IS IN PLAY FOR BUYERS?

FOMO = Fear of missing out

A key characteristic of the frenzy pandemic period from mid-2020 to the end of 2021 was a strong concern on the part of many buyers that if they delayed their purchase they risked missing out – either in terms of having to pay a higher price or the type of property they desired not being available. At 18% of agents reporting FOMO on the part of buyers, we are nowhere near that period of rapid price rises. However, the latest result is a doubling of 9% FOMO in May and a clear break from the low levels between 4% and 9% in place for all other months since February 2022.

ARE YOU NOTICING MORE OR FEWER INVESTORS IN THE MARKET?

We are not in a situation where more agents feel that investors are returning than feel that they are leaving the market. However at 15% the net proportion saying that they are seeing fewer investors is the least negative since February 2021 and well away from the net 69% at the end of last year saying that they were seeing fewer investors. This shift towards less pessimism on the part of investors likely reflects talk of the housing market bottoming out and interest rates peaking. But the high level of interest rates alongside the progressive removal of interest expense deductibility explains why the result is negative and not positive as is the case for first home buyers.

2

ARE YOU RECEIVING MORE OR FEWER ENQUIRIES FROM OFFSHORE?

As ever there is little net interest in New Zealand property from offshore. Nevertheless, the easing trend in this gauge is in line with the direction of change for all the other variables which we track.

WHAT ARE THE MAIN CONCERNS OF BUYERS?

The three main worries buyers have continue to be rising interest rates, access to finance, and concerns that prices will fall after they make a purchase.

ARE PROPERTY APPRAISAL REQUESTS INCREASING OR DECREASING?

A net 13% of agents have reported that they are receiving more requests for property appraisals. This is little changed from the result late in May and perhaps mainly tells us that there is no flood of property being placed on the market by potential vendors.

This month’s survey has shown a firm decline in the proportion of agents reporting that buyers are concerned about prices falling – to 39% from 49% in May and 68% in April. At the same time there has been a noticeable lift in the proportion of agents noticing that buyers are concerned about the stock of listings – to 34% from 25% in May and 14% in April.

3

ARE INVESTORS BRINGING MORE OR FEWER PROPERTIES TO THE MARKET TO SELL THAN THREE MONTHS AGO?

As has been the case for almost all months since the middle of 2022, there is no sign of a wave of investors looking to sell. This is in spite of the high interest rates and tax changes.

We can see in the following graph that while there is no trend change underway in bargain buying hopes, there has been an upward shift in expectations that house prices will rise.

WHAT FACTORS APPEAR TO BE MOTIVATING INVESTOR DEMAND?

When asked about the factors which are motivating investors, 41% of agents say nothing and that their demand is in fact weakening. But 43% say that they are motivated by hopes of finding a bargain while 17% say investors expect house prices to rise.

4

REGIONAL RESULTS

The following table breaks down answers to the numerical questions above by region. No results are presented for regions with fewer than 7 responses as the sample size is too small for good statistical validity of results. The three top of the South Island regions are amalgamated into one and Gisborne is joined with Hawke’s Bay.

Best use of the table is achieved by picking a variable and comparing a region’s outcome with the national result shown in bold in the bottom line. For instance, nationwide 19% of agents say they are seeing buyers display FOMO. But in Auckland this is much stronger at 27%, while Wellington is at 28% and Canterbury 24%.

The table shows net percentages apart from the FOMO question in column F. The net percent is calculated as the percentage of responses saying a thing will go up less the percentage saying it will go down.

A. # of responses

B. Are property appraisal requests increasing or decreasing?

C. Are more or fewer people showing up at auctions?

D. Are more or fewer people attending open homes?

E. How do you feel prices are generally changing at the moment?

F. Do you think FOMO is in play for buyers?

G. Are you noticing more or fewer first home buyers in the market?

H. Are you noticing more or fewer investors in the market?

I. Are you receiving more or fewer enquiries from offshore?

J. Are investors bringing more or fewer properties to the market to sell than three months ago?

This publication is written by Tony Alexander, independent economist. You can contact me at tony@tonyalexander.nz Subscribe here

This publication has been provided for general information only. Although every effort has been made to ensure this publication is accurate the contents should not be relied upon or used as a basis for entering into any products described in this publication. To the extent that any information or recommendations in this publication constitute financial advice, they do not take into account any person’s particular financial situation or goals. We strongly recommend readers seek independent legal/financial advice prior to acting in relation to any of the matters discussed in this publication. No person involved in this publication accepts any liability for any loss or damage whatsoever which may directly or indirectly result from any advice, opinion, information, representation or omission, whether negligent or otherwise, contained in this publication.

5 A #obs B Appraisals C Auctions D Open H. E Prices F FOMO G FHBs H Invest. I O/seas J Inv.selling Northland 2615-88 -27 00-35-58-38 Auckland 161 1945551 27 63-5-19-5 Waikato 5014-1442-121856-4-22-2 Bay of Plenty 38322653-8 24 66-26-1314 Hawke's Bay 17121871-12082 24 -290 Taranaki 5 00000000 Manawatu-Wanganui19-11-55-26063-16-32-5 Wellington 39-13286252872-26-38-16 Nelson/Tasman 2114038 -57 1462-14-29-14 Canterbury 45294 24 -11 24 56 -27-24 -9 Queenstown Lakes9-56-44-4401111-33-33-56 Otago exc. Q'town15-33 -7 0207 47 -7 -20-13 Southland 6 00000000 NewZealand462131841-81956-15-27-8

Newdatafromrealestate.co.nzshowsthatwhilenewlistingsweredown, moreKiwissearchedforpropertylastmonththantheydidayearago.

• LowestJuneonrecordfornewlistingsnationallyandin12regions

• Nationalaverageaskingpricestable. AucklandandCanterburyshow signsofflattening

• Aneconomicmicro-climatefortrend-buckingCentralOtago/Lakes District?

• Onlytwobuyers'marketsremaining

Thenumberofpeoplesearchingforpropertyonrealestate.co.nzwasup8.6% comparedtothesametimein2022*.Butwiththenumberofnewlistingscomingonto thesitedownby21.2%nationally,thoselookingfortheirperfectpropertyhad significantlylesstochoosefrom.

"Justover6,000propertieswerelistedlastmonth– almost2,000lessthaninJune 2022.Yet,westillhadmorepeoplesearchingforpropertythaninJunelastyear."

"Youshouldalwaysbuyandsellbasedonyourcircumstances.ButifIwereplanning tosellin2023,I'dseriouslyconsiderlistingnowwhilecompetitionbetweenvendorsis low,"saysVanessaWilliams,spokespersonforrealestate.co.nz.

Totalstocklevelswerealsodownyear-on-yearby6.1%nationallyinJune,further confirmingthelackofchoiceforbuyersinthemarket.Butit'snotjustlesscompetition thatmakescurrentconditionsripefortransactingproperty.

"Theremightbealittlemorecertaintycomingforbuyersandsellers.TheReserveBank ofNewZealandhassignalledwecouldbeattheendofitsrecentinterestratehikes. While,nationally,averageaskingpriceshavebeenstableforthepastfewmonths, perhapsgivingbothsidesmoreconfidenceonwhattoexpect,"saysVanessa.

New listings

6,218

or21.2%decrease year-on-year

Total housing stock

24,676

or61% decrease year-on-year

National average asking price

$859,871

or8.7% decrease year-on-year

National market sentiment

Sellers' market

LowestJuneonrecordfornewlistingsnationallyandin12regions Nationally,andinAuckland,Waikato,BayofPlenty,Gisborne,Hawke'sBay, Wellington,Southland,Coromandel,CentralOtago/LakesDistrict,Wairarapa,

CentralNorthIsland,andManawatu/Whanganui,newlistingswereat recordlowsforanyJunesince2007.

Year-on-year,listingsweredownbymorethan20%inthenational marketandin12ofour19regions.

VanessasaysKiwisremainedhesitanttolisttheirpropertieslast month–potentiallybecauseofeconomicfactors:

"WeknowthatKiwisarefeelingtheeffectofinflationandrising interestratesintheirpocketsrightnow,andIthinksomeproperty ownersarewatchingtoseewhathappensnext.Wemayseethis pent-upsupplyhittingthemarketlaterintheyear."

Sheaddsthat,despitesomesellersholdingoff,peoplestillbuyand sellpropertyregardlessofwhatishappeningintheworld.

"Thereisstillactivityinthemarket,"saysVanessa.

Northlandwastheonlyregionwherenewlistingnumbersincreased year-on-year.Up19.0%comparedtoJune2022,300propertiescame ontothemarketintheregionlastmonth.

Nationalaverageaskingpricestable.AucklandandCanterburyshow signsofflattening

Thenationalaverageaskingprice,whichhassatrelativelyflatsince March2023,remainedstableduringJunewithamarginaldecreaseof 0.9%comparedtoMay.AucklandandCanterburyalsoshowedsigns ofstabilising.

Vanessasuggeststhiscouldbeasignofthingstocome:

"Typically,trendsstartinourmaincentresbeforetheyemergeinother regions.Weareseeingsomepricefluctuationaroundthemotu,but thisnationalflatteningcombinedwithearlysignsinAucklandand Canterburycouldmeanmoreofthisontheway."

Aneconomicmicro-climatefortrend-buckingCentralOtago/LakesDistrict?

Continuingtobuckthefallingaverageaskingpricetrend,Central

Otago/LakesDistricthitanall-timerecordhighof$1,484,600inJune.The regionhasseenpricestrendingupwardssincethebeginningof2022,in directcontrasttothenationalaverageaskingprice,whichhasfallenby $129,812.

anessasaysthetourismmeccaseemstobelessimpactedbythe economicfactorsaffectingotherregionsinNewZealand: "TheCentralOtago/LakesDistrictisalmostinitsowneconomicmicroclimate.Demandisstillhighforpropertyinthisregion,anditwould seemthatbuyersarenotasimpactedbyrisinginterestratesandrising householdinflation."

"Plus,manypeoplebuyinginthisregionarefromoverseas,wherethey potentiallyhavehigherincomesandfavourableexchangerates."

Sheaddsthatmostpeoplesearchingforpropertyintheregionwere locatedfurtherafield.ThelargestnumberofpeoplesearchinginCentral Otago/LakesDistrictinJune2023wereinAuckland,followedby CanterburyandNewSouthWales.OtherAustralianstates,Queensland, VictoriaandWesternAustraliawerealsoamongthetoptenlocations forsearchers.

Onlytwobuyers'marketsremaining

Justtworegions,AucklandandTaranaki,wereinbuyers'markets duringJune– achangefromthesevenregionsfavouringbuyersat thecloseof2022.

VanessasaysthatwhileAucklandhasbeeninabuyers'marketfor severalmonths,itappearstobeweakening.

"Ifnonewpropertiesweretocomeontothemarket,thenumberof weeksitwouldtaketosellthecurrentsupplyinAucklandismoving closertothelong-termaverage.Thistellsusthatpropertyismoving slightlyfasterinAucklandthanitwasatthebeginningoftheyear."

NathanMiglani,ManagingDirectorforNZMortgages,saysthey,too, areseeinganincreaseinmarketactivity:

"We may be in a 'technical recession', but we’re seeing a warming of the realestate market. News of a decline in inflation is giving buyers confidence, andmomentumisbuildingwithincreasing activity."

"Onedayearlierthisweek,fourclientscompetedatauctions.One missedout,butthreeweresuccessful– andeveryoneofthose auctionshadmultiplebidders."

Vanessahasalsoheardthatsuccessfulauctionsalesarerisingfrom therealestateindustry.

*Source:Internalmetrics(1June-29June2022vs1June-29June 2023)

Formediaenquiries,pleasecontact:

HannahFranklin|hannah@realestate.co.nz

TRADE ME May Property Price Index

NewZealandpropertypricedropseaseasWest Coastjoinsthedecline.

22June2023

TradeMe’sPropertyPriceIndexforMaysawyear-on-yearhousepricesinthe WestCoastdipforthefirsttimeinthepost-Covidpropertymarket,asprice dropsstarttosoftenacrossAotearoa.

NewZealand’saverageaskingpricefell$99,500from2022to$850,150aftertwo consecutivemonthsofsix-figureyear-on-yeardrops,TradeMePropertySales DirectorGavinLloydsaid.

“Forthelastsevenmonths,thenationalaverageaskingpricehasfallen, includingyear-on-yeardecreasesin14ofthe15regionswemonitor.However, theWestCoast,NewZealand’scheapestregion,wasanoutlier,withasking pricescontinuingtoincreasedespitedropseverywhereelse.Thatchangedin Maywhentheregion’saverageaskingpricesalsodropped,”MrLloydsaid. TheaffordabilityoftheWestCoast,whichhadanaverageaskingpriceof $409,700inMay,gaveitgreaterimmunitytothepropertymarketdrops,Mr Lloydsaid.

“Whileitwasaveryslightdropof0.1percentfrom2022itwasstillau-turn, signallingtheongoingeffectstheincreasedinterestratesandcostoflivingare havingonhousesales,”MrLloydsaid.

However,MrLloydsaidthereweresignsthemarketwaslevellingout.

“May’snationalaverageaskingpricefellby10.5percent,easingfromthe10.9 percentfallswesawinbothMarchandApril,”MrLloydsaid.

“Declinesinpropertyvaluesareslowingandasweapproachtheendof interestraterises,thisgivespromisethatbuyersandsellerswillbothhave morecertaintyasweheadoutofthewintermonths.”

Regionalpricestempering

TherateoffallingpropertypricesintwoofthemostbuoyantmarketsWellingtonandBayofPlenty-hassloweddown,MrLloydsaid.

Wellington’saverageaskingpricessliddown$126,800fromMay2022to $837,550.“Whileonthefaceofitthedropishigh,theregion’syear-on-year pricesfellby$139,700inAprilwhichis$13,000morethanMay,suggesting we’reatthestartofaflatteningmarket,”MrLloydsaid.

AsimilarpatternintheBayofPlenty,withitsyear-on-yearaverageasking pricedropping$104,050to$881,050-$7000lessthanApril’sfall.

“Whilewearestillseeingareversalofthepandemicpricegains,itappears thatinsomeregionswemaybeclosetothebottomofthemarket.”

TheAucklandmarketwasyettoseepriceseasewiththeaverageasking pricefalling$161,500from2022tojustoveramilliondollarsat$1,065,350.

“Thiswasourmostheatedmarket,whichiscorrectingtomoresustainable levels,”MrLloydsaid.

Thetwistsandturnsofsupplyanddemand

GisborneandHawke’sBaybothsawsubstantialdropsinbothsupplyand demandfromMay2022,followingtheimpactsofCycloneGabrielle.

Gisborne’ssupplydroppedby33percent,anddemand21percentfrom May2022.WhileHawke’sBay’ssupplydroppedby14percentanddemand by7percent.

“Asasmallmarket,theshiftsintheGisbornepropertymarketappearalot moredramatic,butbothregionsarefeelingthepainofGabrielle,”MrLloyd said.

“Astheyrecoverfromthedevastationweexpecttheretobelessinterestin thepropertymarketsthere,withpeoplewaitingfordecisionstobemade,” MrLloydsaid.

Elsewhereinthecountry,bothTaranakiandSouthlandincreasedtheir supplyby23percentinMay2023,whileWellington’ssupplydroppedby thatsameamountof23percent.

“Wellingtonvendorsappeartobeholdingtighttoseewhathappensinthe marketandiffactorssuchastheReserveBank’smovetoincreasethe capacityoflowdepositlendingimprovesconditionsforselling,”MrLloyd said.

Christchurchgains

TheonlypropertiesinAotearoatoincreaseinaverageaskingpriceyearon-year,wereinOtautahi.Christchurchapartmentsrose10percentto $701,300,whiletheGardenCity’slargerhousesof5+bedroomsspiked7.5 percentto$1,221,900.

“ŌtautahiisNewZealand’scityofthemoment,withrealenergyand momentum,”MrLloydsaid.

“Thelegacyoftheearthquakerebuildisanongoingstory.Alotof theapartmentsinChristchurchhavebeenrebuilttoahighquality,whichis partofthereasontheyaregettinghealthyprices,”MrLloydsaid.

Finance&Lending

& Tony Alexander MORTGAGE ADVISERS SURVEY July 2023 ISSN: 2744-5194

TonyAlexander: Buyer’smarketisaboutto cometoashudderingend

SurveyresultssuggestAucklandwillleadtherebound.

TonyAlexander

28Jun2023

AgentsinAucklandseethebalancepowerhas shiftedfrombuyerstosellers.

ANALYSIS: Thegeneralviewamongstpropertymarketanalystsis thatthehousingmarkethasalmostcertainlybottomedoutand fromherepricesaremorelikelytoedgeupratherthandownwhile turnoverclimbs.Wecanalreadyseerisingsalesinthenear19% seasonallyadjustedriseinnationwidesalesinthethreemonthsto MaycomparedwiththethreemonthstoFebruary. Priceshowever havesimplyflattenedoutandhaveyettostartrisingonaverage. Butwedon’tseemfarofffromthathappeningandcometheend oftheyearapaceofpricegainbetween5%and10%isquite possible.

Ihaverepeatedlyhighlightedthefactorsbehindmyviewofprices risingthisyearandtheyincludeamigrationboom(muchbigger thanexpected),fallingnewhouseconstruction,improvingbank willingnesstolend,highjobsecurity,thepushfromrisingrents, andinterestratespeaking. Yettocomeintoplayisafallingstock oflistings,butwhenthathappensthelargequeueofbuyerswho havebeenholdingbacksinceearly-2021islikelytogetactivated intoaction.

MylatestsurveyofrealestateagentsundertakenwithREINZis increasinglytellingusthatthislargenumberofpeopleisstarting togetofftheircouchesandre-engagewiththemarket. The measuresIhavefrommylatestsurveyforwhichmostresponses arealreadyinhandaretoonumeroustocoverhere. Buthereare themaininsights. Thefullwrite-upwillbereleasednextweekwith regionalbreakdowns.

FOMOiscomingback. Approximately19%ofagentssaythat buyersaredisplayingsignsofafearofmissingout. Thisisthe highestreadingsincethe22%ofJanuary2022thoughiswell belowlevelsabove90%earlyin2021.

FOOP– fearofover-paying– isfalling. Only38%ofagentssaythat buyersareworriedaboutpricesfallingaftertheymakea purchase. Thisisdownfrom49%inMay,andlevelscloseto70%for allothermonthssinceMarchlastyear. FOMOandFOOParen’t crossingyet– butthateventlooksimminent.

Thestrongbuyer’smarketwhichhasbeeninplacesinceFebruary 2022isalmostgone. Onlyanet7%ofagentssaythatbuyershave theupperhandintheirarea. Lastmonth’sreadingwas29%,April was30%,andMarch41%.

34% of agents say that buyers are expressing concern about a shortage of listings. This is up from 25% last month and only 9% in January, but still well down from 82% in the middle of 2021 when worries about the shortage of listings propelled prices higher at the time despite rising interest rates and much tighter lending conditions.

Buyers still remain concerned about access to finance and the high level of interest rates. So, the settings of the Reserve Bank are still placing a high degree of restraint on the market. In that regard nothing suggests that the market is about to boom. But it has turned. If there is a boom this cycle, it will come over 2024- 25 as interest rates decline.

Independent economist Tony Alexander: “Approximately 19% of agents say that buyers are displaying signs of a fear of missing out.”

Photo / Fiona Goodall

Independent economist Tony Alexander: “Approximately 19% of agents say that buyers are displaying signs of a fear of missing out.”

Photo / Fiona Goodall

One other point I have been making regarding the market when it turns is that Auckland is under- priced based on some long- term analytics I run, and it will outperform the regions this cycle as generally defined. We can already see that in my survey of real estate agents this month. All of the readings for Auckland are stronger than for the rest of the country on average, and the city is back into the state of being a seller’s market with a net 8% of agents saying power now lies with the vendor.

- Tony Alexander is anindependent economics commentator. Additionalcommentary from him can be found atwww.tonyalexander.nz

on.

What?’Loomingdebttoincome borrowingrulescouldhitbuyershard.

WhatKiwisneedtoknowaboutDTIs.

DianaClement 26Jun2023

TheReserveBankhasindicatedthatDTIscouldbeimplementedas earlyasMarchnextyear.

Withthehousepriceslumpatitsendpoint,thefocusisnowshifting towardsquestionsaroundarevivalinthemarket.Forecastsrange fromamodestpick-upinpricestoa16%surge,withbullish predictionscitingtherecentspikesinnetmigration,theexpected cutsininterestrates,andadrop-offinresidentialconstruction.

Thoseexpectingthemarkettoremainsubduedhighlightcontinued affordabilityconstraintsandtheexpectedintroductionofdebtto incomerules(DTIs).

CoreLogicchiefeconomistKelvinDavidsonsaysnotenoughpeople aretalkingaboutDTIs,andlikeLVRs(loantovalueratios)andthe CCCFA,bothofwhichhavebeenrecentlyrelaxed,theruleswillhave animpactonhowmuchbuyerscanborrowandultimatelywhatthey canpay.

Backin2021theReserveBankofNewZealandwasgrantedtheright toaddDTIlendingrestrictionstoitstoolkit.Therestrictionscaphow muchmoneyapersoncanborrowbasedonafixedmultipleoftheir income.

InAprilthisyeartheRBNZreleasedtheframeworkfortheDTI restrictionsandindicatedthattheycouldbeimplementedasearlyas March2024.DavidsonsaidKiwiswerenotpayingsufficientattention towhatDTIsmightmeanforthem,andwhiletherewasnoguarantee theRBNZwouldimplementthenewrules,bankswere”definitely preparing”forthem.

“Ithinkwe'llseetheminMarchorAprilnextyear.TheReserveBankwill say,‘Yip,wenowhaveDTIs.’Thatwillbeaprettybigshift,butMarch 2024isninemonthsaway,andpeopleareworriedaboutotherthings. We’vegotanelectionandwhateverelseinthemeantime.”

‘Hang

DavidsonsaidimposingDTIsatamultipleofsevenwouldlikelylimit housepriceinflationto3-4%peryearcomparedtothe6-7%that homeownershavetraditionallycometoexpect.

WhenDavidsonexplainedDTIstorecentpropertyinvestorevent,the topic“cannibalisedthewholesession”,hesaid. Peopleweresaying, ‘Hangon.What?WHAT?’.”

WhileLVRsalsohavethepotentialtorestrictbuyers,theyweremore aboutprotectingthebanks,ratherthanprotectingborrowers, Davidsonsaid.

WithLVRs,homeownersandinvestorscanextractnewdepositsfrom equitywhenhousepricesrise,butwithDTIsthey’llstillneedtomeet strictincomerequirementsbeforetheycanborrow. UnderaDTI system,it’sallaboutyourincome,andyoucan'tchangethateasily. That'sadistinctionthatmaybepeopledon'tquitecottononto,” Davidsonsaid.

DTIs,hesaid,wouldlimitthenumberofhomesanygivenindividual couldown. Somebodywho'salreadytappedoutondebtwon’tbe abletogetanotherpropertyuntiltheirincomehasgrown.TheReserve Bankhasdoneheapsofmodellingandsaysitcouldbefive,seven,10 yearsuntilsomebodycanbuythenextone.”

IfDTIsareintroducednextyear,thebigquestionwillbewhichincome multiplewilltheybesetat.“TheReserveBankindicatedmaybeseven, butthat’sstillupforgrabs.Wedon'tknowwherethey'regoingtobe set,whetherit’ssevenoreight,or15.”

TherearelikelytobesomeexceptionstotheDTIrules.TheReserve Bankhasindicatedthatbankswillbeabletolendabout15%oftheir totalmortgagesoutsideoftheDTIlimit,andthatborrowerslookingto purchasenew-buildsarelikelytobeexempt,aswillnon-bank mortgagesfromfinancecompaniesandotheralternativelenders.

DavidsonsaidDTIswereunlikelytohaveanimmediateimpacton borrowing,buttheywouldlimitthesizeofthenexthousingmarket upswing.“HighDTIlendingisalreadyundercontrol.Atthepeakofthe market,about40%inloanstoinvestorsweregoingoutatahighDTI. Thatfigurenowisaround10%andthat’safunctionofhouseprices falling.Youdon’tneedasmuchdebtandincomeshavegoneup.So theratioismorefavourable.

“It’smoreaboutthenextcycle.ThisisabouttheReserveBank saying‘Wedon’twanttoseeanother40%riseinhouseprices’ andabouttyinghousepricesmuchmorecloselytoincome overthelongrun.”

InfometricseconomistGarethKiernansaidhighinterestrates wouldlimittheimpactDTIsonthemarket.“Atthemoment,the liftinmortgageratessincelate2021iseffectivelyconstraining theamountthatbanksarewillingtolendtopeoplerelativeto theirincomeanyway.People’sabilitytoservicealarge mortgageismuchlessthanwhenmortgagerateswere2.5% andtestrateswere6%in2021,”hesaid.

CoreLogic chief economist Kelvin Davidson: “Under a DTI system, it’s all about your income, and you can't change that easily.” Photo / Peter Meecham

CoreLogic chief economist Kelvin Davidson: “Under a DTI system, it’s all about your income, and you can't change that easily.” Photo / Peter Meecham

“Asaresult,anyDTIrestrictionswouldprobablyhavelittleeffect ontheamountoflendinggettingdoneand,byimplication, housepriceoutcomes.

“TheReserveBank’sconsultationdocumentssuggestthe effectsmightbegreateroninvestors’potentialtoborrow,so DTIsmightleadtoastepchangeintheamountofinvestor borrowingoccurring.ButIwouldn’texpectthattohavea sustainedeffectleadingtoimprovedhousingaffordability,in muchthesamewaythatLVRrestrictionshavehadtemporary effectsonthemarket,buthavenotledtoasustained improvementinhousingaffordability.”

Kiernansaidthekeytohousingaffordabilitywassupply. Until supply-sideimpedimentsarealleviatedorovercome,noamountof tinkeringwithdemand-sidefactorsisgoingtofixtheaffordability crisis,”hesaid.

OpesPartnerseconomistEdMcKnightsaidDTIswouldfurthertipthe balanceforinvestorstowardsnew-builds.Investorswerealready leaningthatwaythankstolowerLVRsfornew-buildsandthefact theycanstilldeductinterestcostsonnew-buildinvestments.

McKnightsaidthespectreofDTIswaspushingsomeinvestorsto bringforwardpurchasingdecisions.

“Thereareanumberofinvestorswhohaveapproachedmeand said,‘Wearegoingtobuynow,beforedebttoincomeratioscome in.’Theyseeanopportunitywherehousepricesonaveragehave gonedownabout18%inNewZealand.Sothey'resaying,‘We'renear thebottomofthemarket,Icangetagoodpricetodayandin12 months’time,Imightnotbeabletobuyahouse,orImightnotbe abletobuyaninvestmentpropertybecausethedebttoincome ratiosaregoingtocomeup.’”

ReserveBankgovernorAdrianOrr.ThebankhassaidinAprilitwouldgivebanks12months topreparetheirsystemsforpossibleimplementationofDTIrestrictions.Photo/Getty Images

IIt’srareinlifethatwegetsomethingfornothingwithnostringsattached,especiallyif itgenuinelyaddsvalue.Nevertheless,that’spreciselywhatIwillgiveyou.

Expert home loan advice which has reliably proven to offer significant long-term financial advantage. Keeping strict tabs on the country’s largestnetwork ofbanks and numerous smaller second-tier lenders, so youdon’thaveto.

What’s more, this comes at no cost to you because your chosen bank pays for the privilege.You have nothing to lose,yet have a higher chance of securing better terms. Rest assured - if there’s a superior deal out there for you, I’ll findit.

Inthe typicallystoicalworldoffinance,we offera pointofdifference.Not onlywillyou receive excellent independent and impartial advice, but you’llhave fun doing it. Even after 15 years in the mortgage arena, our enthusiasm for objectives and commitment to clients shines through at every turn. Endorsement comes from countless glowing testimonials and Keith's own words: “We are at our happiest helping people navigate through difficultsituations,giving hope and concrete opportunity where they previously hadnone.”

Since 2002, Ihave helped countless clientsachieve their goals and dreams, either purchasing their firsthome, their next or buildinga forever home, or to arrangefinanceto acquire an investment property or asset finance.Annually, I willalso review your existing lending, loan structure or assist with debt consolidation.Being solutionfocused to obtain the ‘best outcomes financially’ and deliveringthe ‘most suitable solutions’foryour financialsituation,is whatdrives me. No matter what age or stage you are, working alongside my team, we willrepresent you and your situation honestly, with integrity and professionalism. Check out my Google reviews. I look forward to journeyingonthispathwithyou.

KeithJones MortgageAdviser

021849767

keith.jones@loanmarket.co.nz

CashrateheldinJuly:coulddebtconsolidationbe worthwhile?

At the Reserve Bank of New Zealand’s (RBNZ) meeting today, it opted to hold the cash rate at 5.50%.

According to the RBNZ, 'the OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1 to 3% annual target range, while supporting maximum sustainable employment’.

Despite the hold, rates are still high, leaving many homeowners looking for ways to save costs. One way they may have considered is debt consolidation. This can be a beneficial decision for a number of reasons, but it may not be right for everyone. We explore who this might be better suited to.

Whyconsiderdebt consolidations?

Debt consolidation is where you roll multiple debts, such as personal loans, car loans and credit cards, into one account. This can help simplify repayments as it will only be one rather than multiple. It could also potentially save you money if the consolidated debt is being charged a lower interest rate than when the debts were separate.

There are a number of ways you could consider consolidating debt. These include combining into one personal loan or adding it to your home loan.

Keyconsiderationsbeforeconsolidatingdebt

Consolidating debt could be beneficial for many people, however there are a number of factors that need careful consideration before choosing to do so. The main questions to ask include:

• Are there any fees for paying any of the debts off early?

• Are there any application, legal or valuation fees?

• Are you comfortable with the security? For example, if rolling unsecured personal loans or credit cards into your home loan, your home is used as security. This means should anything happen that means you can no longer meet repayments, the lender could be within its rights to sell your home to recoup costs.

• Will the new debt have a longer loan term, which could mean paying more interest over time?

Can debt consolidation impact my

credit score?

Credit scores can be impacted in the short term when lines of credit are applied for, particularly if multiple applications are made within a short period of time. However, if you consolidate debt and consistently make your repayments, it could potentially improve your score.

Why see an adviser about consolidating debt?

As you can see, debt consolidation can be an effective way for some people to save money and make repayments simpler. However there are a number of considerations to ensure it is the right strategy for you. We will get to know your situation and goals and crunch the numbers for you to determine whether debt consolidation could be the right choice for you. We also have access to over 20 lenders to find one that suits your needs and offers a competitive rate.

Published: 12/7/2023

Kainga Ora Shared Partnership Scheme

First Home Partner, is when Kāinga Ora make a financial contribution to purchase and share ownership of a home...

This scheme applies to existing brand-new homes built or to be built (turn-key deals) The Kainga Ora amount is to be repaid to Kainga Ora interest free over the next 15 years.

The income cap for the last 12 months earnings for a household is $130,000.

Clients must have either of the following.

• NZ residency

• NZ permanent residency

• NZ Citizenship

Process

• Clients apply to Kainga Ora Shared Partnership Scheme and get preapproval.

• Next, Clients are qualified by the bank for the maximum amount of lending that the bank can approve them for.

• Then, clients put in their deposit from Savings, Kiwisavers, Subsidy and Gifts.

• Then, Kainga Ora put in the remaining amount up to $200,000 for the purchase of the property, or up to 25% of the purchase price (whichever is lower)

Clients must own and live in the property for a minimum of 3 years.

Example of a $1,000,000 property

A couple earning $65,000 salary each with no debts or children apply (note the $130,000 income cap).

Based on an average cost of living (as at 03/05/2023) this couple can afford $730,000 in lending. They have $70,000 from savings and Kiwisaver. Kainga Ora will put in $200,000 equity. Meaning they can buy a home of around $1,000,000.

For complete details Contact: Kainga Ora or check their website

Phone: 0508 935 266

Email: firsthome.enquiries@kaingaora.govt.nz

When you know, you know. ™

TNBPropertyServicesLimited,LicensedREAA(2008) https://drury.ljhooker.co.nz/

Property Management Newsletter& Blogs

Onthefollowingpagesyouwillfindourlatest propertymanagementnewsletter.Pleasedon't hesitatetocontactourteamwhocanablyassist youwithanypropertymanagementmatters youmayhaveorifyouhaveanyquestionsabout anythinginthenewsletterorproperty managementingeneral.

Town&Country

EnhanceYourRentalIncomewithSimpleProperty Improvements

Maximisingtherentalincomeofyourpropertyisatoppriorityforsavvypropertyinvestors Fortunately,boostingyourrentalreturnsdoesn'thavetobeadauntingorexpensivetask.

Bymakingsomesimplebuteffectiveimprovements, youcansignificantlyincreaseyourproperty'sappeal andrequesthigherrentalprices

Herearesomestrategiesthatwillattracttenantsand elevateyourrentalincome

CaptivatingStreetAppeal

Firstimpressionsmatter,especiallywhenitcomesto rentalproperties

Ifyouownahousewithafrontgarden,investtimein tidyingupthegardenbeds,removingweeds,cleaning paths,andrefreshingthefence Forapartments, consideraddingwindowboxes,sprucingupthefront doorwithafreshcoatofpaint,andplacinganew welcomingdoormat

Creatingapositiveinitialimpressionenticesrenters andencouragesthemtopaymoreforawellmaintainedproperty.

RevitalisetheBathroom

Acleanandwell-maintainedbathroomcanmakea significantimpactonrentalvalue.However,youdon't needtoembarkonanexpensiveoverhaul.Instead, considerpaintingoutdatedorstainedtileswithtile painttogivethemafreshlook.

Replaceoldshowercurtains,showerheads,and fixtures,eradicateanymould,andifnecessary,install anewvanity.Theseaffordableupgradesenhancethe bathroom'spresentation,providingrenterswitha modernandinvitingspace.

KitchenMagic

Thekitchenistheheartofanyhome,andrenters arewillingtopaymoreforawell-designedand appealingkitchen

Contrarytopopularbelief,akitchenmakeover doesn'thavetobreakthebank Simplyapplyinga freshcoatofpaintcanworkwonders

Considerreplacingcabinetdoorsor,ifthat'snot feasible,upgradethehandlesoncupboardsand drawers

Tenantsappreciatemodernappliances,soifyour currentonesappearoutdated,contemplate investinginnewoneslikeadishwasher,oven,or fridge Rentersarewillingtopayapremiumfor theseconveniences

Off-StreetParking

Inhigh-densitylivingareassuchasinner-cityor beachsidesuburbs,theavailabilityofoff-street parkingisasignificantadvantage.Addinga carportorcreatingadrivewaycansubstantially increasethevalueofyourproperty,astenants preferhassle-freeparkingoptions.

Thecloseryourpropertyistothecity,themore valuabletheparkingspacebecomes.

OptimiseLivingSpaces

Thenumberofbedroomsdirectlyinfluencesrental value.

ljhooker.co.nz

Assessyourproperty'slayouttoidentifypotential opportunitiesforadditionalbedrooms.Repurpose separatediningrooms,convertunused"dead space, "orconsidersplittinganextra-largeroom.By addinganextrabedroom,youcancommand higherrentandattracttenantsseekingmorespace

Additionally,tenantsappreciatedesignated laundries,whichcanbecreatedbyoptimising underutilisedareaswithoutincurringexcessive costs

EmbraceStorageSolutions

Storageishighlysoughtafterbytenants,soadding wardrobesinbedroomsisacost-effectivewayto increaserentalappeal

Budget-friendlyoptionsfromretailerslikeBunnings provideattractiveandpracticalstoragesolutions Ensuringamplestoragespaceallowstenantsto envisionlivingcomfortablyinthepropertyand increasestheirwillingnesstopaymore

OutdoorEntertainingBliss

Anoutdoorentertainingareaisamajordrawcard forrentersandaddsvaluewhensellingyour property

Youdon'thavetosplurgetocreateaninviting space Consideraddingadeck,tilingacourtyard, incorporatingagazeboandBBQ,andfurnishingthe areawithoutdoorfurniture

Theseadditionsenticetenantsandmakeyour propertystandout

Pet-FriendlyPolicies

Pet-friendlypropertiesarehighlydesirable,asmany rentalpropertiesprohibitpetsaltogether By allowingpets,youexpandyourpoolofpotential tenantsandcanchargeahigherrent

Mitigaterisksassociatedwithpetsbyincluding safeguardsinthetenancyagreement,suchas specifyingrenterresponsibilityforcarpetcleaningor coveringpet-relateddamages

IlluminateandEnlarge Darkroomsareunappealingtoprospective tenants.Brightenupyourpropertybycleaninglight fittingsandreplacingbulbswithbrighteroptions.

Well-litspacescreateawelcomingatmosphere andgivetheimpressionofopennessandspace Renterswillgladlypaymoreforapropertythat feelslightandspacious

AdjustRentAccordingtotheMarket

Regularlyresearchingtherentalmarkethelpsyou stayinformedaboutprevailingrentalratesinyour area

Ifyourcurrentrentisbelowmarketvalue,consider adjustingittomatchorslightlyexceedthemarket standard Whentenantsseethatyourproperty offerscomparablerates,they'relesslikelytoexplore alternatives,ensuringasteadystreamofinterested renters

PrioritiseSafety

Safetyisakeyconsiderationfortenants,andthey areoftenwillingtopayextraforasecurehome

Enhancepropertysecuritybyinstallingtamperproofscreendoors,reliablelocks,andaSmart HomeSystemwith24/7securitymonitoring Keep entrancesclearofobstructionsandensure sufficientlightingaroundtheproperty,includingthe frontporchandparkingspaces

Renterslivinginsecurehomesoftenreceive discountsontheircontentsinsurance,justifyinga slightlyhigherrent

BenefitfromaPropertyManager'sExpertise Engagingaprofessionalpropertymanagerisan assetforoptimisingyourrentalreturns

Propertymanagersoffervaluableinsightsand guidanceonpropertyimprovementsandattracting therighttenants Theypossesstheknowledgeand expertisetoassistyouinmaximisingthepotential ofyourinvestmentproperty

Beforemakinganydecisionsyoushouldconsultalegalor professionaladvisorLJHookerNewZealandLtdbelievestheinformationinthispublicationiscorrectandithasreasonablegroundsforanyopinionorrecommendationcontainedinthis publicationonthedateofthispublication NothinginthispublicationisorshouldbetakenasanofferinvitationorrecommendationLJHookerNewZealandLtdacceptsnoresponsibilityfor anylosscausedasaresultofanypersonrelyingonanyinformationinthispublication ThispublicationisfortheuseofpersonsinNewZealandonlyCopyrightinthispublicationisownedby LJHookerNewZealandLtd

Theinformationcontainedinthispublicationisgeneralinnatureandisnotintendedtobepersonalisedrealestateadvice

LicensedREA2008

Youmustnotreproduceordistributecontentfromthispublicationoranypartofitwithoutpriorpermission

ljhooker.co.nz

Book a rental appraisal for your chance to WIN a year of free management fees*

Scan to Request an Appraisal

UnenforceableclausesinTenancyAgreements.

WhenatenantorlandlordbreachestheResidential TenanciesAct,it’simportanttounderstandwhatyoucando toputitright.

Youcan’twriteclausesintotenancyagreementsthat conflictwiththeAct.TheTenancyTribunalmayconsider suchclausestobeunenforceable–meaningtheyhaveno effectandinsomecasestheseclausesmayamounttoan unlawfulact.

Generallyclauseslikelytobeunenforceableareclausesthat:

•askatenanttodomorethantheActrequiresthemto do

•trytoremoveorreducethetenant’srightsorgivethe landlordmorerights

•evadetherequirementsoftheAct.

Followingaresomeexamplesofclausesthatwouldnotbe enforceable.

CLAUSES LIKELY TO BE DEEMED 'UNENFORCEABLE'

REASON WHY

Carpets must be professionally cleaned at the end of the tenancy.

A tenant only has to leave the premises in a reasonably clean and tidy condition. Tenants do not have to have the carpets professionally cleaned.

Tenants must replace stove elements, fuses and tap washers as they wear out.

A landlord is responsible for maintaining the premises to a reasonable state of repair.

Tenants must give more than 28 days' written notice to end a periodic (ongoing) agreement.

Under the Act, the tenant only needs to give at least 28 days' written notice to end this type of agreement.

A tenant must pay four weeks' bond plus two weeks' extra bond for the landlord allowing a dog.

The law only allows a maximum of four weeks' rent as a bond.

The landlord can raise the rent with one weeks’ notice.

The Act states the process for raising the rent, which must be complied with.

The tenant cannot have visitors without the landlord's consent.

The tenant is entitled to quiet enjoyment of the property while they are renting it. This clause would breach that entitlement.

The tenant can only have a party with the landlord's consent.

This clause would also breach the tenant's right to quiet enjoyment of the property.

The tenant will pay for fixed water charges.

The Act states that landlords are responsible for paying fixed water charges

The tenant will install smoke alarms that meet the legal requirements.

Landlords are responsible for installing smoke alarms and making sure they’re in working order.

If you think there are clauses in your tenancy agreement that are unenforceable, you should discuss these with your landlord. You can also contact Tenancy Services for advice.

If the clause or request cannot be agreed on, you can apply to the Tenancy Tribunal to have the issue resolved.

ResidentialPropertyManagement CARPETS...

Ifthetenantiswantingthecarpetsinarentalpropertytobe changedduetothecarpetsbeingold,canthelandlordenter intoanagreementwiththetenantforthetenanttopaya portionofthereplacementcost?

UnderSection49AResidentialTenanciesAct1986,itisa GeneralPrinciplethat-

(1)Exceptasprovidedinsection49B,atenanthasnoliability orobligation,andmustnotberequired,to—

(a)meetthecostofmakinggoodanydestructionof,or damageto,thepremises;or

(b)indemnifythelandlordagainstthecostofmakinggood thedestructionordamage;or

(c)paydamagesrelatedtothedestructionordamage;or (d)carryoutanyworkstomakegoodthedestructionor damage.

(2)Atenantisnot,inanycase,liableforfairwearandtear.

Ifthecarpetsrequirereplacementduetonormalwearand tear,itisthelandlord'sresponsibilitytobeartheentirecostof replacement.Itisalsoimportanttoconsiderthatthe TenancyTribunalmaydeclareanyspecialclauseinthe tenancyagreementunenforceableifitimposesobligations onthetenantbeyondwhatisrequiredbythelaw.

Properties

LJHooker

30 Franklyne Road, Otara NZ

§3 bl �1

URGENT SALE-MAKE AN OFFER

Currently tenanted, this 985m2 site (more or less) is a developers dream. Zoned Residential (9D), re...

For Sale By Negotiation

View ByAppointment

Brent Worthington 029 2965362

brent.worthington@ljhooker.co.nz

https://drury.ljhooker.co.nz/

1 Luke Place, Otara NZ

§5 b2 �2

URGENT SALE-MAKE AN OFFER

* Prominent site

* PrimeLocation

* Huge development potential

114 Harbourside Drive, Karaka NZ §- b-�-

RIPEFOR DEVELOPMENT in KARAKA

Located in the "sought after" Karaka Harbourside Estate, the opportunity to purchase another land ho...

For Sale Price By Negotiation

View ByAppointment

Brent Worthington 029 2965362

brent.worthington@ljhooker.co.nz

For Sale By Negotiation

View ByAppointment

Brent Worthington 029 2965362

brent.worthington@ljhooker.co.nz

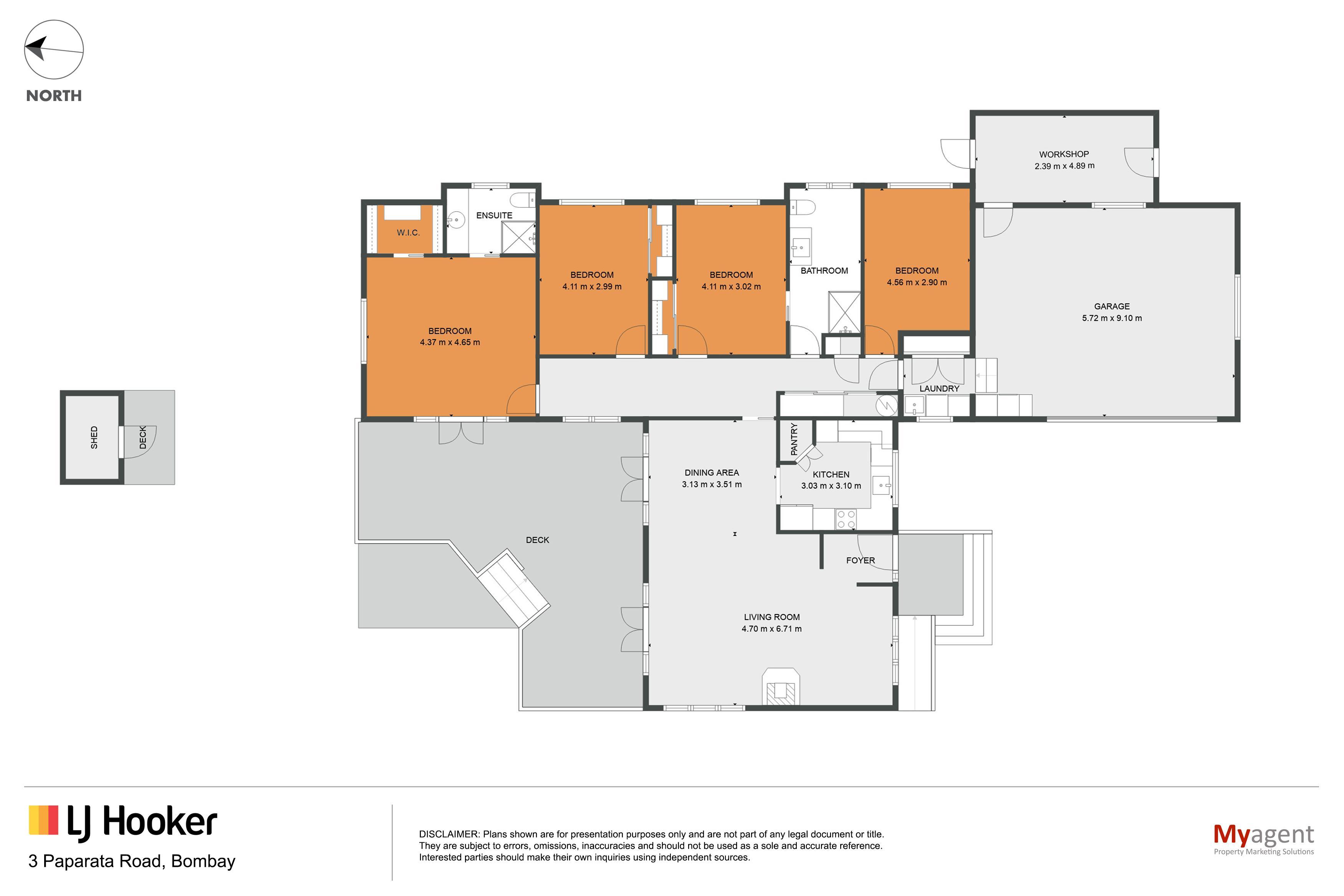

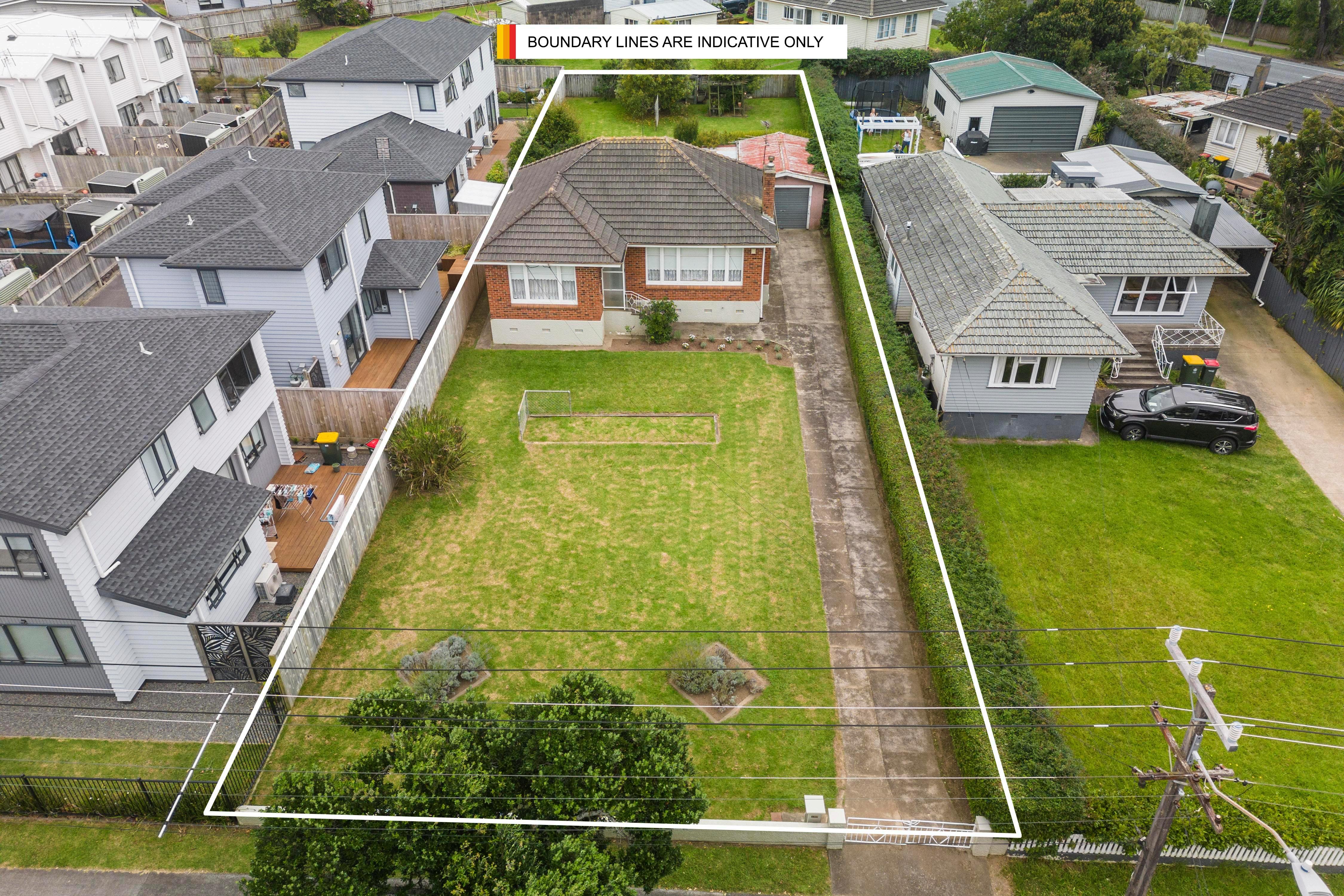

3 Paparata Road, Bombay NZ

§4 b2 �s

BOMBAY BEAUTY - BOXES TICKED!

*4 Double bedrooms.

* Master with ensuite.

* Impeccably cared for and presented. < ...

26 Dawson Road, Otara NZ

§3 bl �10

UNIQUEINVESTMENT with HUGEPOTENTIAL

Located on the Flat Bush-Otara boundary, this property is all about potential. DEVELOP, DEVE...

For Sale Price By Negotiation

View Sunday July 23rd, 01:00PM 01:45PM

Brent Worthington 029 2965362

brent.worthington@ljhooker.co.nz

For Sale By Negotiation

View ByAppointment

Brent Worthington 029 2965362

brent.worthington@ljhooker.co.nz

09 294 7500

OUR LISTINGS

20th,Jul2023

1/233 Great South Road Drury NZ 2113 drury@ljhooker.co.nz

IPE FOR DEVELOPMENT in KARAKA

Located in the "sought after" Karaka Harbourside Estate, the opportunity to purchase another land holding of this size and zoning is unlikely.

Currently consented for a 7 Lot residential subdivision, the property is also subject to Auckland Council's Plan Change 78Intensification proposed 18/08/2022. Possibly greater development opportunities!

ByBy Negotiation

(2008)

114HarboursideDrive KARAKA

Contact BrentWorthington 0292965362 CLICKHERETOVIEWFULLDETAILSONOURWEBSITE

CLICKHERETOVIEWFULLDETAILSONOURWEBSITE

3PaparataRoad BOMBAY

BOMBAY BEAUTY - BOXES TICKED!

Sited for all day sun and situated close to so many amenities and locations!

1006 sqm

4 Bedrooms

2 Bathrooms incl Ensuite Walk-in robe

Separate Laundry

Large Double Garage with Internal Entry Minimal care grounds with safe and secure rear for children and pets.

ByNegotiation

ByAppointment orOpenHomeasadvertised

_____________________________________________________________

(2008)

2

LJHooker

Drury-Town&Country

91 Beatty Road, Pukekohe NZ §8 b7 �

uNuM1TED POTENTIAL

On the market for the first time in 43years. The 630m2 dwelling is set on a 2,379m2 site (more or I...

17th,

https://drury.ljhooker.co.nz/

35 Briody Terrace, Stonefields NZ §4 bl �4

STAND ALONE IN STONEFIELDS

Set on a 372m2 site (more or less) this 243m2 Fletcher designed and built dwelling will definitely i...

Sold Brent Worthington 029 296 5362 brent.worthington@ljhooker.co.nz

102 Mountain Road,Mangere Bridge NZ §2 bl �1

LOCATION - LOCATION - LOCATION CONJUNCTIONALS ARE WELCOME.

On the market for the first time ever, this offering is p...

Sold Brent Worthington 029 296 5362 brent.worthington@ljhooker.co.nz

151 Barrack Road,Mount Wellington NZ §4 bl �6

"' UNIQUE INVESTMENT with HUGE POTENTIAL

Located in the geographical centre of metropolitan Auckland, this property is all about potential. D...

Sold Brent Worthington 029 296 5362 brent.worthington@ljhooker.co.nz

Sold ina Roban 021 022 88521 lina.rob@ljhooker.co.nz

09 294 7500

Jul 2023

1/233 Great South Road Drury NZ 2113 drury@ljhooker.co.nz

RecentlySOLD

2 1 1 brent.worthington@ljhooker.co.nz (2008) FIRSTTIME valuableland,currently closeproximity SOLD Contact

0 (2008) DEVELOP-DEVELOP andsubject SOLD-Auction Contact

OurPeople

BRENTWORTHINGTON

BrentWorthington LicensedAgent&Principal

0292965362

Brent.worthington@ljhooker.co.nz

There’s not much Brent doesn’t know when it comes to selling real estate. This town andcountryagenthashadasuccessfulcareerinthepropertymarketandisnowthe proud owner of his own business. Definitely a quality over quantity man, when you bring Brent on board, you’ll find that accumulating listings is far less important to him than making each one as good as it can get. He prides himself on telling it like it isknowing you’ll be able to make better decisions with a person and information you cantrust.

Complementing Brent’s practical

and credible approach is a background full to the brim of industry knowledge and business expertise from 30 years working within the construction industry. His capabilities have been well proven as a highly successful businessowner.

A family man, with a proven track record of success, Brent has earned an excellent reputationandthetrustofhislocalcommunityandbusinesscolleagues.

He places huge emphasis on customer satisfaction, attention to detail and conducting his business with a genuine duty of care. Brent has gained many awards asabusinessleaderduringhis12-yeartenureinRealEstate.

Hisentrepreneurialstyleensureshereachesoutandconnectspeoplewithlikeminds. Heimpartshiswisdominawarmandfriendlymannerandhelpspeopletomakewise andrightdecisionsbeforeinvestinginthepropertymarket,Aucklandwide.

Ifyouareconsideringalifestylechange,investingforyourfutureorsimplywantingto know the worth of your property in this fluctuating market, feel welcome to call or emailBrenttoreceivethelatestupdatesonthetrendsandstatisticsinyourarea.

When

™ TNBPropertyServicesLimited,LicensedREAA(2008)

youknow,youknow.

LinaRoban

LINAROBAN

lina.roban@ljhooker.co.nz

Prior to entering the world of real estate, driven by her love of meetingand helping people, Lina had an impressive 20 year career in sales and marketing roles in the telecommunications and corporate marketing industries where her expertise in communication and negotiation always resulted in the delivery of superior customerservicetoherclients.

Originally from Fiji, Lina epitomises energy, passion integrity and hardworkineverythingsheturnsherhandto.

When not delivering superior service to her clients,Lina loves spending time with her family and is a passionate cyclist, owning both road andmountain bikes.With her three children allhaving "flown the coop",Lina andher husband alsohave plenty of time to enjoy their love of travel and some of their more memorable adventures include extensive journeys throughout South East Asia, the USAandtheSouthPacific.

LicenseeSalesperson

02102288521

TNB Property Services Limited, Licensed REAA (2008 drury@ljhooker.co.nz https: //drury.ljhooker.co.nz) When

Town&Country

youknow,youknow.™