NAB meets rising demands of today’s brokers and borrowers head-on

MAJOR LENDERS ROUNDTABLE

BROKER TECH EVOLUTION

Nation’s biggest banks gather round the table

How tech is enhancing, not replacing, human connections

FIRST HOME BUYERS REPORT

Next gen of homeowners gets clever

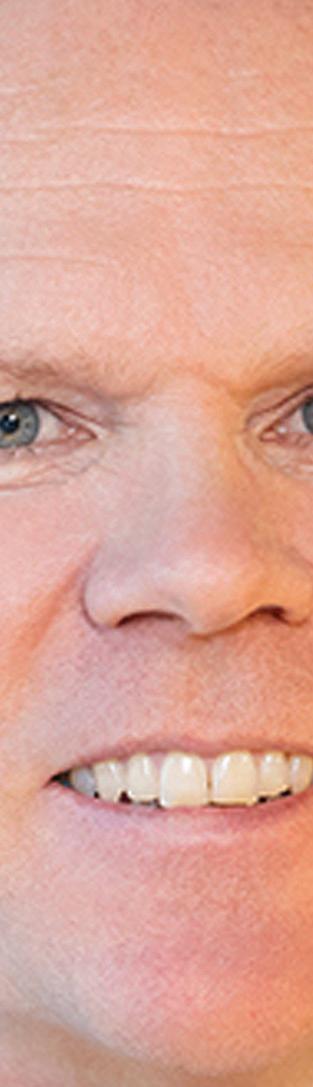

Adam Brown Executive broker distribution, NAB

Surprisingly simple property lending for

commercial brokers

Help clients grow their portfolio with simplified property investment applications under $3m.

Enough to make you smile.

CONNECT WITH US

Got a story or suggestion, or just want to find out some more information?

x.com/MPAMagazineAU

facebook.com/Mortgage ProfessionalAU

UPFRONT

02 Editorial

First home buyers are proving their mettle

04 Statistics

FEATURES MAJOR BANKS ROUNDTABLE

Latest stats from across Australia’s property landscape

06 Opinion

Broking industry must raise the entry bar to protect reputation, argues SFG’s Blake Buchanan

FEATURES

28 A winning agenda

BROKERS ON NON-BANKS

2025

Brokers’ expectations of non-banks are rising – and the sector is stepping up

NAB’s executive broker distribution on how the lending giant is meeting the evolving needs of brokers and borrowers

Bluestone cements its status as brokers’ top non-bank, driven by service, innovation and growth

48 SMEs in focus

Brokers play a crucial role amid tough times for small businesses

54 e FHB challenge

Australia’s biggest banks discuss flexible lending, channel conflict, rising competition and much more 32 FEATURES BROKER TECH EVOLUTION

How new broker tech is boosting e ciency without replacing the human touch 58

With banks and brokers behind them, aspiring homeowners are finding creative ways to buy

66 Funding the future of aged care

How BOQ Specialist’s tailored finance helps aged care businesses thrive

PEOPLE

72 Other life

Bheja.ai CEO Pravin Mahajan gets his clearest insights from long walks in nature

Minh Beaver’s journey from refugee to broker gives her resilience, integrity and a passion to help others

business strategy, and what industry leaders have to say.

Latte-swilling millennials prove naysayers wrong

Perhaps it’s ironic that the editor of MPA is currently a renter. Ironic maybe, but understandable, too, when you’ve just recently relocated from abroad to one of the most expensive cities on planet Earth.

But it also a ords me some invaluable insights into the struggles everyday Australians face in accessing this country’s housing market. So allow me to confirm what everyone should already know: saving up for a deposit is the single biggest barrier to homeownership in Australia, especially when, like me, you’re not averse to the odd takeaway latte.

It’s therefore commendable that the Labor Government has brought forward its Home Guarantee Scheme extension, which should greatly benefit people like me with hopes, dreams and minimal disposable income.

With the chips stacked against them, first home buyers … are proving impressively innovative and resilient

But there’s no denying that government intervention in the housing market has some unintended consequences – consequences that are increasingly drawing the ire of market commentators.

Stimulus, by its very definition, is inflationary. In the case of the Home Guarantee Scheme, every analyst and their dog expects it to drive up house prices even further.

But what’s the alternative? An increasingly stratified housing market where only the recipients of intergenerational wealth can a ord a 20% deposit? These are some of the conundrums tackled in this edition of MPA.

Our cover story features NAB’s head of broker, Adam Brown, who discusses the role major lenders play in helping first home buyers achieve the Australian dream. We also hear from the experts at Beyond Bank and Bankwest, who share their thoughts on the current state of the first home buyer market.

Those who turn their noses up at the lazy, latte-swilling millennials might be in for a rude awakening here – with the chips stacked against them, first home buyers, with an average age of 36, are proving impressively innovative and resilient, as evidenced by the resurgence in deal volumes.

The unprecedented diversity of alternative lending options has gone a long way in supporting this resilience. On that note, pop on over to page 12 to discover who took home the medals in MPA’s 2025 Brokers on Non-Banks survey.

William Farrington, editor, MPA

ART & PRODUCTION Designers Cess Rodriguez, Loiza Razon

and Asia MortgageProfessionalAustralia is part of an international family of B2B publications and websites for the mortgage industry

AUSTRALIAN BROKER simon.kerslake@keymedia.com

T +61 2 8437 4786

NZ ADVISER alex.knowles@keymedia.com

T +64 9 200 1319

CANADIAN MORTGAGE PROFESSIONAL shane.lakhani@keymedia.com

T +1 720-441-2255

MORTGAGE PROFESSIONAL AMERICA charles.weed@keymedia.com

T +1 720-441-2255

MORTGAGE INTRODUCER (UK) matt.bond@keymedia.com

T +44 203 868 3406

HOME VALUES CONTINUE TO RISE

SAVING LONGER FOR DEPOSITS

$857,280

National median dwelling price

0.8%

Growth in national dwelling values in September – the fastest monthly increase since October 2023

Number of consecutive months national home values have risen, indicating ongoing market momentum

0.9%

Growth in capital city dwelling values in September, outpacing regional markets' by 0.7%

Source: Cotality Property Market Trends, October 2025

AUSTRALIANS GOOGLING FINANCE BASICS

MONEYME research shows thousands of Australians google basic finance terms monthly. The most searched category is interest-related queries (9,590/month), followed by mortgage (8,900). The single most searched query is ‘mortgage meaning’, attracting 3,600 monthly searches over the past year.

PROPERTY PURPOSE REVEALED

Mortgage Choice’s survey shows most Gen Z and millennial buyers view their first property as a ‘stepping stone’, while baby boomers are more likely to buy a ‘forever home’. Investment and fixer-upper motivations are less common across all generations.

Property settlement scams are rising sharply in Australia, with millions lost annually as criminals use email fraud to trick buyers and sellers into transferring large sums to fake accounts during settlements, PEXA reports.

YOUNG AUSSIES MONETISE THEIR HOMES

More than one in four Australians are considering using their home for income, Great Southern Bank reports. Among Gen Z homeowners, 58% are exploring options: 24% plan to invest, 19% to rent a room, 16% to run a business.

Why industry entry requirements must evolve

Raising the bar for broking will protect clients and safeguard the industry’s reputation, argues

Blake Buchanan

THE MORTGAGE BROKING industry in Australia has come a long way over the past 35 years. From humble beginnings, it has grown into a sophisticated and highly competitive sector that now writes nearly all new residential loans. Yet despite this success, the entry requirements for new brokers remain a point of concern – and, in many ways, a weakness in the system.

At present, the minimum standard for becoming a broker is a Certificate IV in Finance and Mortgage Broking. While this

there are clients whose financial future was guided by someone with minimal experience and who no longer have their broker available to help workshop new scenarios, restructure debt or provide ongoing advice.

Why the diploma should be the minimum standard

To strengthen competence and confidence, the diploma should be the minimum entry requirement for all new brokers. This would bring the profession into line with its responsibilities.

Reforming entry requirements is not about gatekeeping; it’s about protecting clients and safeguarding the reputation of the industry

qualification provides a baseline understanding of lending and compliance, it is far from sucient to equip someone for the complexities of the role. Industry bodies encourage new brokers to complete a Diploma of Finance and Mortgage Broking Management within 12 months of starting, but it is not mandated as an entry requirement.

The current framework has contributed to a troubling statistic: around 60% of new brokers fail within their first year. That is unacceptable for an industry that positions itself as a trusted adviser to Australians making life’s biggest financial decisions.

The issue is not simply one of personal failure. A broker who leaves the industry after a year has still written loans. That means

A higher initial qualification sets a stronger foundation, but qualifications alone are not enough. What matters most is how new brokers enter the industry and gain realworld experience.

One of the biggest issues lies in the pathway many new entrants choose. Rather than joining an established brokerage, they set up their own company straight away, becoming their own boss from day one. For those without a finance background, this is almost always a recipe for failure. They lack not only technical grounding but also the operational support, compliance frameworks and peer learning that established brokerages provide. The data and experience show that those who attempt this path make up the bulk of the 60% who fail.

A smarter pathway

New-to-industry brokers, particularly those without prior financial services experience, must be required to work within a licensed brokerage for a minimum of two years before they are permitted to go out on their own.

This model mirrors the apprenticeship approach seen in other professions. Doctors, lawyers and accountants all undertake structured periods of supervised practice before being entrusted with independent clients. Mortgage broking should be no di erent.

Working within a brokerage provides structured mentoring by experienced brokers; exposure to a range of scenarios from other brokers; compliance oversight that reduces risk to both client and broker; and operational support such as administration, systems training and lender relationships. Brokers who start their careers in this way not only survive but tend to thrive.

At the heart of this discussion is the client. Every loan has long-term consequences for a family, an investor or a business. If more than half of new brokers leave within 12 months, the clients they served are left unsupported. Reforming entry requirements is therefore not about gatekeeping; it’s about protecting clients and safeguarding the reputation of the industry. By lifting the bar to a diploma and embedding a mandatory two-year brokerage period for those without finance backgrounds, we ensure clients are served by brokers who are properly trained, supported and committed.

Mortgage broking is a cornerstone of Australia’s financial system. With that role comes responsibility. The current model, with its low entry standards and high failure rates, is not sustainable.

It’s time for the industry to evolve. By requiring a diploma as the minimum qualification and mandating supervised brokerage experience, we can build a stronger, more resilient profession – one that serves clients better and secures the future of mortgage broking for decades to come.

Blake Buchanan is the general manager of mortgage aggregator Specialist Finance Group (SFG).

BACKING BROKERS, SUPPORTING CUSTOMERS

NAB’s Adam Brown on how the banking giant is meeting the ever-rising demands of today’s brokers and borrowers

TWO YEARS into his role as executive broker distribution at NAB, Adam Brown’s enthusiasm for the third party channel, and NAB’s position within the broking industry, is as strong as ever.

Sitting down with MPA to discuss what’s happening at the banking giant, Brown comes armed with the facts, figures and fervency of NAB’s commitment to brokers and the customers they’re ultimately there to serve.

NAB has an ace up its sleeve in an increasingly competitive mortgage market where 75% of all deals are settled by brokers. As the largest business bank in Australia, it is naturally inclined to understand the needs of Australian brokers, the majority of whom are small business owners in their own rights.

This feeds into a holistic attitude to servicing the broker channel, from being at the forefront of scam and fraud detection to supporting cash flow management, advising on how to raise debt and expand your broking business, and beyond.

“As the number one business bank in the country, we’re well equipped to help support small business owners every day,” Brown tells MPA. “As a major bank, we have a whole range of specialised functions, knowledge centres and capabilities that exist across our broader bank that we want to bring to brokers.”

NAB’s partnership with brokers doesn’t simply finish once a loan application is lodged. “We want to care for customers as well as, if not better, than brokers want to care for their customers,” he says. “Our ambition is to be Australia and New Zealand’s

most customer-centric company. What that means is getting it right for customers, getting it right for our partners. The broker channel is really key to that.”

A large percentage of broker-introduced NAB customers are coming to the bank for the first time, Brown notes. “The way we partner with our brokers in bringing that customer on board – and then how we serve that customer once they’re on board – is critical to our strategy.”

For Brown, the trick to striking the right balance between meeting the needs of brokers

on his travels is that while NAB aims to be customer obsessed, “there’s no question that customer obsession is at the heart of what brokers are about as well”.

“The best brokers have the strongest relationships with customers,” Brown says. “That’s where our absolute ambition intersects.”

While brokers absolutely need top-drawer policies and pricing processes in order to best serve their clients, “what they really want is the assistance when they need it”.

This rarely if ever means having a one-sizefits-all approach. For instance, whereas some

“Customers are becoming more educated around home lending and more demanding of what they want out of a home loan”

and delivering for customers lies in continuously seeking and acting on feedback, whether through NPS surveys or direct conversations with customers and brokers.

“It’s not always what’s most important to us as a bank, or most important to a broker, but what’s most important to a customer,” says Brown. “And so, whilst we want to make things better for a broker and easier to work with us, we’ve got an absolutely fierce determination to get it right for customers as well.”

Like any distribution head worth their salt, Brown is always out and about, hearing from the brokers on the ground. What he’s learned

brokers want face-to-face contact with a BDM, others are happy to just have a number to call when they need it.

“We have to adapt to these different needs,” says Brown. “Because what’s most valuable to one broker is very, very different to another.”

First home buyers bounce back So, what’s hot on the market right now? For Brown, all signs point to a revitalisation of the first home buyer market.

“A lot of buyers sat out of the market last year,” he says. “There were higher interest rates, and people were probably a little bit tentative.” Yet with rates coming down,

PROFILE

Name: Adam Brown

Title: Executive broker distribution

Company: NAB

Years in the industry: 17

Recent career achievements: Driving continuous improvement across NAB Broker’s policies, products and processes; overseeing the successful 2025 launch of multi-offset accounts into the broker channel; refining NAB’s policies to support more self-employed customers

BIG INTERVIEW

sentiment is bouncing back across the FHB segment. Auction bids are at their highest levels in 18 months, and listings are improving, Brown reveals.

NAB’s latest quarterly Australian Residential Property Survey shows that in the June quarter, FHBs’ market share of new housing increased to 40%, marking the highest level since 2022. Victoria is leading the way in terms of momentum after a prolonged drought period, followed by NSW.

And it’s not just in the capitals – momentum is building in the regional areas across Queensland, Victoria and WA.

Brown chalks the regional surge up to post-COVID life decisions. “Some of it’s

a large scale. The bank has a target to lend at least $6 billion by 2029 to help more Australians access a ordable and specialist housing and has provided $4.4 billion to support this ambition since 1 October 2022.

Delivering beyond the deal

One thing brokers and their homebuying clients of all stripes are demanding right now is flexibility.

Indeed, “customers are becoming more educated around home lending and more demanding of what they want out of a home loan”, says Brown.

So, how is NAB’s broker channel meeting these demands?

“As the number one business bank in the country, we’re developing o erings and services to help support small business owners every day”

weather, some of it’s lifestyle. Some of it’s been brought about because of flexible working environments and hybrid ways of working.”

A ordability is of course a major factor in the regional shift too.

First home buyers are also proving an enterprising bunch, using strategies like rentvesting and multigenerational ownership models to get onto the property ladder.

However, while NAB has modified some of its policies to help more customers through these strategies, Brown concedes it’s critical to address both demand and supply-side measures together to help more Australians buy a home.

While increasing borrowing capacity helps, housing supply remains the most significant challenge. This issue will require time, commitment and smart policy, particularly to ensure new housing is built in the locations where people want to live.

NAB is playing its part in this by financing social, a ordable and community housing on

Brown points to product o erings such as multiple o set accounts that allow customers to bucket their funds while saving on interest.

But these are just surface-level bonuses that most of NAB’s competitors can o er. True flexibility emerges when brokers make good use of the support network NAB makes available.

In Brown’s view, the expertise of NAB’s business development managers and distribution teams stretches far beyond just the loan transaction.

“A key thing that I share with brokers is that yes, we can help you with the transaction to help your customer, but we can help you with a lot more than that,” he says.

“I’m really proud of our distribution team and how we support our brokers,” adds Brown. “And part of that support is listening to feedback. We will continue to listen to feedback. We’ll continue to take action on it, and we’ll continue to deliver the things that matter for brokers and customers.”

HOW NAB SUPPORTS FIRST HOME BUYERS Commitment to First Home Guarantee

Modi ed policies to support rentvesting and multigenerational ownership models

Lending at least $6 billion by 2029 to help more Aussies access a ordable and specialist housing

BROKERS ON NON-BANKS

BROKERS ON NON-BANKS

BROKERS’ EXPECTATIONS of nonbank lenders have significantly risen in 2025, and the sector has responded by stepping up to meet them. MPA’s Brokers on Non-Banks 2025 survey reveals every metric is up relative to 2024, confirming brokers’ higher standards and the resulting improved delivery.

As outsource Financial CEO Tanya Sale explains, non-bank lenders have earned their reputation as ‘outstanding’ by filling gaps left by traditional banks – with flexible policies, strong BDM support and fast service.

“They have redefined access to credit by creating innovative lending policies, and the big one for me is that they have built up broker loyalty,” Sale says. “Brokers now see non-bank lenders as reliable partners, not just for niche deals but for mainstream lending.”

The top three broker priorities remain BDM support, credit policy and turnaround times, showing that brokers prioritise relationships and execution. Remuneration fairness and transparency are rising in importance. Product range, communications

and training and online platforms saw modest mid-tier gains.

Industry leaders confirm what more than 400 broker respondents report. While priorities are largely unchanged from last year, the score spread is smaller, and brokers now expect more from every aspect of their nonbank partnerships.

AFG’s general manager of industry and partnerships, Mark Hewitt, says, “Broker satisfaction is most strongly influenced by direct communication with credit assessors, which streamlines decision-making, coupled with a clear understanding of deal fit, helping brokers match clients with the right lender more e ciently.”

Brokers point to added resources that have improved service times, as well as “significant improvements driven by increased investment in digital platforms, process automation and streamlined assessment workflows”. As one broker remarked, the result is “fast turnarounds that mean customers walk away smiling”.

PEXA’s latest Lender Mortgage Trends report shows the same pattern. Over half of

More brokers are on board, and the scores back it up. BDMs, policy and speed lead; brand and commissions trail. Higher rates and fees still hold volumes back

new mortgage value now flows through brokers, and that share is climbing. Within this channel, non-ADI new-loan volumes rose 25.3% year-over-year in FY25, while the majors grew 3.9%, with non-banks leading non-majors for external refinances in NSW and Victoria.

That report also notes faster, more digitised settlement processes among non-ADIs, which reflects broker feedback on quicker turnarounds and smoother workflows.

Across 10 criteria, brokers evaluated nonbanks’ performance, crowning the top three in each category with gold, silver and bronze, plus honours for the overall winners. The 2025 rankings highlight that non-banks have stepped out of the specialist lane with brokers, though they still hold only a modest share of settlements. Brokers are judging them on the same broad set of factors as banks, and scores are higher across every dimension.

MFAA’s Industry Intelligence Service 19th Edition corroborates that momentum. Non-bank settlements via brokers jumped 33.2% in April–September 2024 compared

with the prior six months. After two quarters of gains, non-bank share eased 0.3 points to 5.9% in Q3 as international banks and white-label programs advanced, while total broker volume still increased 4.3% across the quarter.

“When I speak to our brokers on the main reasons they’re turning to non-banks, the resounding response is they are consistent, flexible and relationship-driven,” says Sale. “Also, they pick up the phone. If they cannot answer, you can bet they will call the broker back promptly.”

BDM support and credit policy surged to No. 1 and No. 2 in 2024 from seventh and last in 2023 and stayed there in 2025, with turnaround times placing third, confirming a service-led ranking in which responsiveness, flexible decision-making and speed outrank price and brand.

TYPICAL RESPONDENT

Turnaround performance has become more reliable in 2025, with more brokers reporting consistent service, fewer reports of deterioration and, among those who saw movement, improvement leading the way.

Interest rates stayed at fourth in 2025, rising to 4.453 from 4.283 last year. Cost matters, but 70% say higher rates and fees are the main brake on sending more business to non-banks.

Brokers appreciate quality products backed by simplicity and support, and their votes for best non-bank product went to:

• Bluestone Alt Doc: “Simple-to-use calculator, simple verification and easy documentation”

• Pepper Money Prime Alt Doc: “Fast turnaround with BDMs and credit focused on getting the deal done”

• Firstmac SMSF: “Competitive and relatively easy to use”

Commission structure moved up to eighth, overtaking product diversification, while brand recognition remained last, showing brokers prioritise competitive compensation and concrete support over brand identity.

METHODOLOGY

In this year’s survey, brokers were asked to rank non-bank lenders across 10 categories: BDM support; brand recognition; commission structure; communications, training and development; credit policy; interest rates; online platform and services; product diversification opportunities; product range; and turnaround times. Brokers could rank the non-banks with a score out of five in each category. Only those institutions that achieved a response rate of at least 10% were included in the final list.

The survey also recorded broker responses on their preferred non-banks in these areas: specialist lending; first home buyers; property investors; commercial; alt doc; SMSF; and foreign non-residents.

MPA asked the brokers a series of questions relating to their business with non-bank lenders, as well as which non-bank they would like to see added to their aggregator’s panel, but these did not influence the overall score.

Years as a broker

WHY USE A NON-BANK?

Brokers push non-bank volumes to a record, with growth concentrated in 21–40% books, with reasons centred on document flexibility, wider assessment and speed

LAST YEAR delivered a rebound, with 67% of brokers saying they sent more loans to non-banks, approaching the 2021 peak of 69%.

This year goes even further as 70% of brokers set a new high, turning 2023’s 50% low into a two-year swing of 20 points. The rise looks broader and more durable, supported by stronger service, flexible policy and quicker turnarounds, even as pricing still limits how much volume moves.

AFG’s Mark Hewitt says, “Brokers are increasingly turning to non-banks due to their willingness to consider borrowers who might fall outside of the major lenders’ standard appetite and require a bit more of a considered appraisal. This can include those with credit score challenges or variable

income streams. This willingness to work with complexity makes non-banks a valuable partner for brokers and their customers.”

In the first half of 2025, SMEs reported 55% intent to use non-banks, up seven points year-over-year, while planned bank usage was 30%, according to ScotPac’s July 2025 SME Growth Index. The reasons matched broker feedback on speed, flexible policy and tailored options.

The <20% cohort (brokers putting the lowest proportion of loans through a nonbank) keeps easing, from 60% in 2023 to 50% in 2024 to 49% in 2025. Heavy users dipped in 2025 (7% put more than 60% of loans through non-banks) after touching 10% in 2024, but brokers expect that highuse group to rebound to 10% in 2026.

Most of the growth is set to come from the middle. Non-bank users in the 21–40% band are projected to climb from 30% in 2025 actuals to 40% in 2026, pointing to broader use rather than a surge in majority non-bank books.

Non-banks have put in hard work to earn brokers’ trust, not just as an alternative but as a first-choice solution in many scenarios, notes outsource Financial’s Tanya Sale.

“The perception has shifted from ‘last resort’ to ‘distinctive value’. It also helps that non-banks have steadily lifted their profile over the past five years. It’s a testament to how far this sector has come. They play such an important part in our industry.”

Across the industry, there’s widespread acceptance that brokers are highlighting pricing and credit assessment as their primary challenges. Additionally, policy complexity, inconsistent interpretations and communication di culties, especially with o shore assessors, which lead to processing delays, are prompting brokers to favour lenders that o er faster approvals.

This year’s survey shows brokers are choosing non-banks less because majors pull back – and more because the file needs a di erent pathway. In 2025, the top reasons for choosing them are documentation flexibility and a broader assessment of the borrower, with lack of standard docs at 25.6% and taking a wider view than the credit score at 24.6%, both up more than five points on 2024.

Banks tightening credit policy slid to 16.3% from 23.4% last year, while regulatory factors ticked to 11.0% and personalised HAVE

service held near 7.3%. The trend from constraint-driven to borrower-fit choice reflects rising mid-band usage and the SME intent data, and it explains why speed, policy flexibility and hands-on support keep pulling more business to non-banks.

Brokers reach for non-banks when the deal needs borrower-fit solutions. That means alt/low-doc paths, policies that take a broader view of credit history, and specialist segments such as SMSF. Their reasons included:

• “Diversified credit policy and appetite, along with greater scope to look outside the box”

• “Credit impaired, ATO debt consolidation”

• “Better borrowing, easy to deal with and less documentation”

Non-banks’ serviceability settings can deliver higher borrowing capacity, and the packaging is often simpler, with lighter documentation and faster progress to yes.

TOP 5 REASONS YOU WOULD PICK A NON-BANK LENDER OVER A BANK

CONVERSION DECIDES THE WINNERS

Brokers reward lenders that make complex files easy. The standouts deliver hands-on BDM support, confident credit assessment and a toolkit that helps brokers grow

BROKERS’ 2025 ratings of the benefits of using non-bank lenders point to rising year-over-year mainstream acceptance and reinforce the sector’s strong competitive position.

Client openness to considering non-bank products is consistent across the market. In 2025, 85% of clients were open to considering a non-bank, a pullback from the 91% peak in 2024 but still above 82% in 2023.

The yes-to-no ratio is about 6:1 in 2025, down from 10:1 in 2024 but above 4.6:1 in 2023. The dip points to tougher pricing rather than waning interest, and price remains the biggest hurdle to converting openness into deals.

With most clients open to non-bank options, the battleground for winning their business is conversion. The leading nonbank lenders turn intent into settlements by

BROKERS ON NON-BANKS

making non-standard files easy to place with:

• clear alt-doc paths

• nuanced credit decisions

• fast, consistent turnarounds

• BDMs who stay close from scenario to settlement

These lenders back that with straightforward, competitive price and fee settings that are simple to explain, so brokers can close in one conversation. In short, they win on fit, speed and consistency, which helps overcome rate di erentials and keeps deals moving.

Turning to performance, there’s clear daylight at the top of the podium. The overall gold medallist scored 4.43 out of 5 versus 3.57 for second, a 0.86-point gap, while silver and bronze were split by just 0.09.

The top three non-banks collectively amassed a substantial medal haul that surpassed last year’s accolades. Bluestone, Pepper Money and Liberty collected 10 golds, eight silvers and nine bronzes across the 10 categories.

Bluestone won nine of the 10 golds and took silver in brand recognition, retaining first place in BDM support. Liberty added five silvers and three bronzes, including silver for credit policy and a shared bronze for BDM support. Pepper Money claimed the remaining gold for brand recognition, plus two silvers and six bronzes, also sharing bronze for BDM support.

In the mid-table results, Thinktank secured silver for interest rates, Firstmac took bronze in the same category, Resimac picked up bronze for product range, and La Trobe Financial, fourth overall, earned silver for BDM support.

OnDeck emerged among the top three non-bank lenders brokers would like added to their aggregator panel in 2025, followed by Better Choice Home Loans and Bluestone.

In 2025, 70.11% of brokers named higher rates and fees as the main reason they are not sending more business to non-banks, up from 67.69% in 2024. That figure is about

HIGHLIGHTS: BENEFITS OF USING A NON-BANK

BDM support

Commission structure

policy

seven times the next hurdle, lack of brand awareness at 9.68%, and it outweighs the rest of the barriers combined.

Brokers weighed in with their thoughts on pricing:

• “Rates and fees are still too high for most customers”

• “The fees and rates are sometimes a killer, but they do provide options”

• “I think their rates for more standard lending scenarios are too far from standard lenders”

• “Non-bank lenders need to introduce products and rates that compete directly with the majors”

Credit

Bluestone Liberty and Pepper Money (tie)

La Trobe Financial

Bluestone

Pepper Money Liberty

Bluestone

Pepper Money Liberty

• “They have continued to put pressure on mainstream lenders with policies and competitive rates on a range of products”

• “A little movement of interest rates would make a big impact”

As AFG’s Mark Hewitt says, “Brokers and aggregators are placing greater emphasis on longevity in the market and a proven track record of supporting customers through interest rate fluctuations and economic cycles.”

Brand and branch concerns eased to 9.68 and 4.95%, respectively. Service complaints fell to 1.94%, while speed issues edged up to 4.09%.

Access and administrative hurdles remain small but ticked up, with not-on-panel at 2.80% and poor commission at 1.08%.

‘Other’ slipped to 5.38%, pointing to broker pain points concentrating around price.

Other reasons brokers noted include:

• “Di cult to understand which product is available to the client. Ends up being unexpected”

• “Don’t have a lot of clients in this market sector”

The medals for commission structure matched the overall standings, with Bluestone first, Liberty second and Pepper Money third.

Reflecting on the factors that most strongly influence broker satisfaction with non-banks, outsource Financial’s Sale says the word ‘flexible’ comes up again and again.

“Outstanding non-bank lenders understand that not every borrower fits a one-sizefits-all mould,” she adds. “Whether it’s selfemployed clients, those with non-standard income, or more complex scenarios, brokers appreciate lenders who assess deals on merit rather than [using] a rigid checklist.

“In these cases, the non-bank BDM works closely with the broker and the credit assessor when they believe a deal is there, to ensure a strong outcome for the broker’s client.”

HIGHLIGHTS: PRODUCTS AND BRANDING

TECHNOLOGY, TURNAROUND AND SERVICE

Most brokers enjoyed faster turnarounds and credited non-banks for their digital upgrades and responsive service, while calling for more BDMs and assessors

ON SPEED, the best non-banks didn’t blink. In 2025, nine out of 10 brokers said turnaround times had either improved or stayed the same, rising to 92.1% from 87.5% last year.

The share reporting deterioration fell to 7.9% from 12.5%. Among those who did see movement, improvement outweighed worsening by about six to one. Notably, significant improvement nudged up to 10%, while significant worsening stayed uncommon at 0.95%.

Consistent speed underpins broker confidence, which matters most when clients sit outside a major’s credit box.

“There’s a growing recognition of the important role non-banks play in supporting borrowers who don’t fit the traditional bank profile,” says AFG’s Hewitt. “Brokers now better understand the value and reliability non-banks bring to the lending ecosystem.”

Brokers say non-banks have sped up with:

• faster pick-ups and decisions: many report files picked up within 24–48 hours and two to three days to conditional

• tech and workflow upgrades: brokers credit new digital platforms, automation, e-submission and online tracking portals for the speed-up

• people who move a file: direct lines to assessors and responsive BDMs are a big part of the improvement

The small group of brokers who believed times had worsened noted the increased complexity of some deals and operational

ine ciencies as reasons, as well as higher volume leading to slower turnaround times, and “inappropriate” sta ng levels.

Where speed broke down, brokers cited:

• capacity and resourcing: more files are landing with non-banks, and some teams are understa ed, so pick-up times blow out, and phones go unanswered

• poor communication and

transparency: SLAs are unclear or undisclosed, status tracking is weak, and repeated emails or calls to BDMs go unanswered

• process deadlock: too much back-and-forth for basic documents, and assessors ask for information late in the process

• inconsistent performance: Some lenders lag, and delays worsen during busy periods

HOW HAVE TURNAROUND TIMES AND COMMISSION STRUCTURES CHANGED OVER THE PAST YEAR?

$3,000 bonus offer for eligible first home buyers with an ANZ home loan of $250k+

BROKERS ON NON-BANKS

Turnaround times gold medallist Bluestone is operating in a di erent gear, at 0.51 points ahead of silver winner Liberty, while Pepper Money finished a competitive third.

Last year’s overall silver medallist, RedZed, received the lowest broker rating for its perceived slowness. It narrowly missed out on being one of the lenders brokers wished were added to their panel, placing fourth.

When it comes to wish lists, the ask has moved from tech and paperwork to people and capacity. More BDMs/credit assessors are now the top broker suggestion at 23.10% – up 5.29 points from 2024 – for how non-banks could improve their service. Results also showed:

• Simpler income verification fell to 16.19% (down 7.09pts), suggesting lodgement jams are easing and documentation paths are clearer

• Better technology dipped to 20.95% (down 2.80pts) but remains the No. 2 request, so workflow tools still matter

• Training needs rose to 13.33% (up 1.93pts) and communication to 12.86% (up 1.70pts), pointing to ongoing demand for clearer updates and more broker training

For the first time, one of the top three nonbanks, Bluestone, scored well above four out of five from brokers for its online platform and services, showing that digital is now a frontline di erentiator. Liberty won silver, while Pepper Money took the bronze.

HIGHLIGHTS: TURNAROUND, TECH, COMMUNICATION

HOW COULD NON-BANKS IMPROVE THEIR SERVICE LEVELS?

WHAT YOU’RE SAYING

“No. They need to sharpen the pencil and fix their tech to stay in the race”

“Non-bank policies tend to be more lenient and understanding of a client’s financial position”

“Yes, generally they have. When needed, you can usually find an option to suit all borrowers”

“Yes, but they need to improve as banks are also moving to regain market share from brokers”

“I think their interest rates need to be more in line with banks to be truly competitive”

Do you think the non-banks have provided enough competition to the banks over the last year? Why/why not?

“Yes, and there seem to be more non-banks and asset finance companies at our aggregator learning days than there are mainstream lenders”

“Yes. They have taken on niches that mainstream banks won’t touch. The no-clawback features some of them offer are stellar”

“They seem to be trying; however, the non-bank industry needs to concentrate on innovation, as those of us who love using them always want more reasons to do so”

“Not with rates or fees, but definitely with policy”

“Yes, especially since more of our self-employed clients prefer non-bank lenders due to simplified income verification documents and the certainty of approval”

FINAL RESULTS

Bluestone defends its overall gold in Brokers on Non-Banks 2025 with a near clean sweep of golds across the board and is named brokers’ preferred lender in six of seven categories

BLUESTONE secured nine golds and one silver in the 10 survey categories, a sweep that underscores its standing as a trusted partner to brokers. For chief commercial o cer Tony MacRae, this widespread approval is the product of a culture built on relationships, consistency and a service-first approach.

“We’re incredibly proud of this recognition; it’s a reflection of the deep commitment our team brings to supporting brokers every single day,” says MacRae.

He points to the role of Bluestone’s BDMs as central to that success. They are accessible, responsive and genuinely invested in broker outcomes, ensuring support flows seamlessly from first contact through to settlement.

“These awards are a testament to the trust we’ve earned by showing up, listening and delivering on our promises. It’s that human connection that drives our performance and keeps us striving to do better.”

That ethos translates into tangible value in day-to-day interactions. Fast and transparent turnaround times, proactive communication and practical, tailored solutions are the cornerstones of Bluestone’s o er.

MacRae stresses that listening to broker feedback and using it to refine processes, from credit policy to post-settlement support, has been essential to sustaining performance across the board.

Bluestone sees scope to take its partnership model further. Personalisation through datadriven insights, combined with an expanded product o ering, will allow brokers to serve a wider range of clients, particularly those who don’t fit the traditional mould.

“For us, it’s about being more than a lender; we aim to be a true partner,” MacRae says.

BROKERS’ PREFERRED LENDERS BY CATEGORY

FINAL RESULTS

BROKERS ON NON-BANKS

OVERALL RANKING: RUNNERS-UP COMMENTS

LIBERTY

Liberty secured strong placement across five key categories, from commissions and credit policy to turnaround times. What does this feedback tell you about where brokers see Liberty delivering, and where do you think there’s room to improve?

David Smith, chief distribution officer: At Liberty, we’re proud to be a leading lender across multiple categories such as commissions, credit policy and turnaround times, which are critical to broker success. This feedback tells us that brokers recognise the strength and consistency of our partnership and performance, and that our commitment to supporting their business is hitting the mark.

This recognition reflects the solid foundations we’ve built over nearly three decades now, and our commitment to the broker channel, especially in areas that directly impact their business success, e ciency and productivity.

Just as importantly, they signal that brokers are ready for us to push even further. We see this as a positive challenge. It’s clear that brokers value what we’re delivering, and they’re looking to us to keep raising the bar. Whether it’s smarter systems or more responsive support, we’re focused on refining our processes and enhancing our practices to help brokers be even more productive and successful.

PEPPER MONEY

LA TROBE FINANCIAL

La Trobe earned silver for BDM support in a year when brokers ranked it as their number one priority. What steps have you taken to build that strength, and how do you plan to keep raising the bar in this area?

Cory Bannister, chief lending officer: We are incredibly proud to have earned silver for BDM support, especially in a year when brokers made it clear this was their top priority. At La Trobe Financial, we’ve invested heavily in building a team of highly engaged, credit-skilled and responsive BDMs who genuinely understand the broker business, and our credit appetite, with multiple BDMs having served for over a decade with our company. With our 73-year history of tailoring square-peg solutions, we’ve built long-standing relationships by keeping our approach simple: be accessible, add value, and act as true partners in every deal. Brokers know that when they run a scenario with us, we will go above and beyond to find a solution to help their clients. We’ll continue to strengthen this support through ongoing training and deeper national coverage to ensure brokers have what they need, when they need it.

You also earned multiple placements, including for BDM support. How is Liberty working to strengthen broker relationships so that these touchpoints become a clear competitive edge?

DS: We know brokers value high-touch, personalised support, and our BDMs work tirelessly to deliver just that. From the initial scenario right through to settlement, they’re there every step of the way, helping brokers find the most suitable solutions for clients.

Beyond day-to-day support, we’re focused on broker education. Through targeted training in business development, customer engagement, relationship management and across our broad product suite, we help brokers confidently embrace product diversification. By equipping them with the tools to o er more free-thinking solutions, we’re helping them stay relevant to a wider range of borrowers.

Liberty sees BDM support as a key opportunity to deepen broker relationships and deliver even more value. Over the next year, we’ll continue investing in BDM training and tools to ensure brokers receive timely, tailored support that helps them grow. Whether it’s expanding their o ering or strengthening client relationships, we’re committed to helping brokers succeed across the widest product suite in the market.

La Trobe was also singled out by brokers as their preferred non-bank for commercial lending. How do you see that strength helping you stand out in the sector, and what opportunities are you prioritising for future broker rankings?

CB: Being recognised by brokers as their preferred non-bank for commercial lending is a tremendous endorsement of the strength of our o ering in this space, which has been built and tested over many decades. At La Trobe Financial, we’ve long understood that commercial lending requires flexibility, speed and a genuine understanding of complex borrower needs – all areas where brokers tell us we continue to deliver. This recognition continues to set us apart as a category leader and reinforces the value of our tailored, solutions-based approach.

We are prioritising further investment in product innovation and deeper education and support for brokers to help grow commercial broker market share. It’s a segment in which we know we can help to unlock tremendous value for brokers.

BLUESTONE DOES IT AGAIN

For the second year running, Bluestone has taken home gold in MPA’s Brokers on Non-Banks survey. Chief commercial officer Tony MacRae discusses another year of major achievements

ANYONE CAN fluke a one-off win, but when you take home gold in MPA’s Brokers on Non-Banks survey for two years running, there is clearly more than luck at play.

In winning the gong, Bluestone was praised by brokers for its turnaround times, online platform, BDM support, commission structure and credit policy, among other features. In fact, the lender scooped up nine of 10 golds, while taking home silver for brand recognition.

On a pure numbers basis, Bluestone’s victory makes perfect sense. For the second year in a row, it has more or less doubled its origination volumes.

The past 12 months have been particularly strong for Bluestone, as reflected in the swathe of new recruits coming into the company, at a time when some of Australia’s biggest and most profitable lenders are cutting head counts by the thousands.

Bluestone’s team of business development managers was particularly supercharged in recent times in order to better service its vast broker network.

“Bluestone has seen significant growth over the past 12 months, and we’re incredibly grateful to the broker community for their continued support,” chief commercial officer Tony MacRae tells MPA. “Our success

“Bluestone has seen significant growth over the past 12 months, and we’re incredibly grateful to the broker community for their continued support”

is built on strong relationships and exceptional service, not just competitive pricing. We focus on finding solutions for brokers and their customers, being available when needed and delivering timely, commonsense decisions.”

Bluestone saw a fresh lick of paint in a quite literal sense this year when, to celebrate 25 times around the sun, the group overhauled its branding to reflect what MacRae dubbed “a bold way forward”.

“The brand refresh is all about reflecting on the past and showing that we’ve been around for a long time … We’re not just the new kids on the block,” he said at the time of the rebrand.

It was also “a nod to the future”, MacRae added, as well as “showing the strength of the brand and of Bluestone and that we’re absolutely committed to continuing to provide solutions and choice to brokers and borrowers”.

Embracing challenges

Speaking to MacRae, it’s clear that broker experience has been front and centre of this growth agenda, whether that’s about maintaining market-leading turnaround times of three days or less in most cases; hosting sold-out webinars, roadshows and broker events; or growing Bluestone’s BDM team.

The end goal, explains MacRae, is to deliver the best relationships and service in the industry, while “ensuring that we provide insights and information to show brokers new ways to provide solutions for customers they may have thought they weren’t able to help, and indeed help them grow their businesses”.

A key part of Bluestone’s competitive advantage, MacRae says, is maintaining a curious attitude and asking the right questions – whether it’s through BDMs working with brokers, credit teams assessing deals, or Bluestone’s specialist sales team hosting

Title: Chief commercial officer

Company: Bluestone Home Loans

Years in the industry: 25

Recent career achievements: Bluestone topping

MPA Broker on Non-Banks survey for second year in a row; being named in 2024 Global 100 list

Name: Tony MacRae

EXPERT SPOTLIGHT

workshops, webinars, roadshows or simple co ee clusters.

“Helping brokers find solutions and grow their business is a real passion amongst the team,” MacRae says.

Of course, building up a business to become one of the biggest non-bank lenders in the country was never going to happen without encountering a few hurdles along the way –especially when “the market continues to throw up challenges every day”.

MacRae cited an influx of new competitors into the alternative lending scene, aggressive pricing of mortgage products, and the disruptive nature of new technologies such as AI as just a few of these challenges.

Nonetheless, “we have embraced these challenges head-on but have never forgotten that at the end of the day we are a relationship and service business,” he says. “As with brokers advice and support is a key di erentiator, it is with Bluestone and continuing to

all their customers’ mortgage needs.”

Technology will also play a part in helping the company retain the competitive advantage that has led to brokers crowning Bluestone as Australia’s best non-bank for two years running.

“Bluestone will continue to evolve by adopting leading-edge technology – including AI – where appropriate whilst also ensuring we remain faithful to educating brokers and finding solutions that help brokers grow their businesses,” says MacRae.

“We will look to further partner with aggregators to ensure that together we are able to provide seamless solutions for brokers and their customers and market-leading education and events.”

On a personal note

For the past 12 years, MacRae has sat on the board of directors of the Royal Flying Doctors Service [RFDS] (South Eastern section).

“Helping brokers find solutions and grow their business is a real passion amongst the team”

ensure this is at the forefront of how we deliver initiatives and ensure we remain relevant to brokers and their customers.”

When it comes to plans for the year ahead, it’s all about making the process of working with Bluestone more streamlined and hopefully faster.

“Continuing to simplify our processes and digitalise our platforms will be a key priority,” MacRae says. “Giving brokers confidence that they can get a quick, common-sense decision with consistent application will be key to continuing to win in the future.”

As for specifics, MacRae teased an exciting year for Bluestone with the launch of a number of new products.

“We’ve recently launched expat loans and are currently testing an additional two new products with a small number of brokers with a view to launching by the end of the year,” he said, adding that “Bluestone aims to be the preferred partner for brokers for

Over this period, he has served as treasurer and then chair of the Finance, Audit and Risk Committee and member of the Board Aviation Committee.

In his role, MacRae has provided oversight, strategy direction and governance of an organisation with a turnover of approximately $90 million that provides aeromedical services to the communities of regional, rural and remote NSW.

“It has been my absolute privilege,” says MacRae of his time with the service, which is soon coming to an end.

“Involvement with the Royal Flying Doctor Service has been a wonderful distraction. If ever I think I’m having a bad day, I am reminded of the stories from the RFDS of people doing it much harder, and I realise I don’t really have bad days.

“It has been a great honour to serve the board and organisation and the wonderful team that makes a di erence every day.”

BLUESTONE BY THE NUMBERS

Team size: 140 Assets under management: >$7.2bn

Years in operation: 25

Annual originations: Approx. $5bn

Popular products: Alt doc, near prime, specialist and SMSF

MacRae clearly has a deep passion for the RFDS. Without it, “many of our regional and rural communities would simply not exist”, he says. He explains how it has evolved from its historical provision of retrieval services and aerial patient transport to providing mental health services, alcohol and other drugs services, permanent GP clinics, wellbeing centres and dental services, among many others.

These are “all essential services for any community but ones that wouldn’t exist in many parts without the Royal Flying Doctor Service”, says MacRae.

“The motto of the Royal Flying Doctor Service is ‘The furthest corner, the finest care’, and this really sums up what this wonderful organisation does. I am proud to have played a very small role.”

Build a business for yourself, not by yourself.

When you join the Mortgage Choice network, you tap into a wealth of experience and resources designed to build your knowledge, skills and confidence. Our franchise structure provides all the support you need, from technology and marketing to compliance and business development.

BANKING ON THE MAJORS

When brokers and borrowers are demanding more flexibility than ever before, how are Australia’s largest lenders rising to the challenge?

ANYONE EXPECTING a buttoned-up, conservative a air when representatives from Australia’s biggest banks – nay, biggest corporations – gathered for MPA’s Major Banks Roundtable at Cafe Sydney in September would have had a pleasant surprise.

Rather, participants had a lively, animated and kinetic discussion about the biggest themes impacting the broking market in 2025. Their passion for the mortgage industry shone throughout the hour-long, seven-question roundtable, as did their abundance of knowledge on themes spanning broker demands, channel conflict, digital mortgages, market competition and merger activity.

It was perfect timing for such a discussion, occurring in the hours preceding the Reserve Bank of Australia’s August interest rate call. As we now know, the RBA chose to cut rates for the third time in a year. An avalanche of correspondence from the very banks represented around the table immediately followed.

Each of the five major banks present at the table – Commonwealth Bank (represented by general manager of third party banking Baber Zaka), NAB (executive, broker distribution Adam Brown), ANZ (head of strategic partnerships, retail broker, Ben Magnus), Westpac (head of broker distribution Sarah Willsallen) and Macquarie Bank (head of

broker distribution Wendy Brown) – opted to pass on the 25 basis points cut in full, albeit with varying degrees of immediacy.

It was a perfect illustration of the pressure Australia’s largest financial institutions face in providing the best products on market to attract brokers’ and customers’ attention.

Roundtable participants also heard from two of Australia’s leading brokers – Amelia Pignone of LendX and Jim Psirakis of Pegasus Home Loans – who grilled them on matters close to the broking industry’s hearts.

As some of the biggest companies in Australia with many moving parts, how do you ensure that you provide the flexibility that today’s broker demands?

Sarah Willsallen dove right in, stating that flexibility “is at the heart of our approach at Westpac as we want to support as many customers as we can”.

She pointed to Westpac’s credit scenario hotline as a perfect example of the bank’s approach to flexibility. Run by senior credit managers, the hotline gives brokers direct access to senior credit managers to brainstorm, you guessed it, credit scenarios.

“We’re always listening and adapting to broker feedback, including where they’d like us to see us change or amend the hotline,” said Willsallen.

MAJOR BANKS ROUNDTABLE 2025

THE PANELLISTS

BANKERS

BROKERS

Broker feedback was certainly a running theme of the roundtable discussion.

Ben Magnus explained how ANZ uses its ‘voice of broker’ survey to guide policy rollout. The survey “gives us great intel into where we need to be better and stronger from a process or policy perspective”, said Magnus.

“We’ve been using our survey results to craft the new initiatives that we’re going to roll out,” he added, calling attention to enhancements to ANZ’s broker portal and

hear them out in person. “Quite often, we bring brokers together for around-the-table conversations,” Brown said. “It’s a chance for us to propose ideas and gather feedback but also invite brokers to share what’s on their minds.”

He stressed the importance of brokers adapting to their customers’ needs. “Brokers are not only small business owners themselves; they also play a critical role in supporting other business owners and

“It’s a strength of the industry that we allow such competition. It’s one of the reasons I love this industry”

Baber Zaka, Commonwealth Bank

home loan calculators as examples. “We encourage our brokers to continue to give us feedback.”

At Macquarie Bank, Wendy Brown said, “we’re built for brokers to confidently deliver better outcomes – and flexibility is at the core of that. We know that no two brokerages are the same, so we actively listen to feedback from sole operators right through to the largest o ces to make sure our support works across the full spectrum.”

Macquarie Bank has also built the ability for pooled support sta to access its broker portal, allowing brokers and their support teams to see status updates and existing customer information whenever they need it.

“They can also chat with us securely 24/7 so they can manage their workloads more flexibly and leverage a broader range of expertise to better serve their clients,” Brown said. “Our focus is not just on supporting new business but also on helping brokers look after their existing clients, making it simpler and faster to deliver the right outcomes, every time.”

Adam Brown at NAB also drilled home how important broker feedback is in adapting policy. The bank goes the extra mile by conducting broker forum groups to

customers,” he reminded the roundtable. To assist, NAB regularly shares insights such as business sentiment surveys and customer trend data with brokers to support their decision-making and client conversations.

Before the discussion moved to Baber Zaka from CommBank, the two brokers present shared their thoughts on whether their flexibility needs are being met by the big banks.

Jim Psirakis from Pegasus Home Loans explained how he had seen di erent majors develop di erent niches over time, whether that was Westpac’s one-year o ering for selfemployed clients, ANZ’s Simpler Switch policy or the 1% assessment rates from NAB and CommBank.

The banks are reacting fast to market changes, said Psirakis, adding that BDM support remains good across the board. “It helps our business, it makes us e cient and knowledgeable, it makes the banks look productive, and it keeps the clients happy,” he said.

Amelia Pignone at LendX echoed Psirakis’ positive comments, particularly around policy changes in the self-employed space.

Speaking of niches, Zaka then explained how CommBank’s role is to enable brokers to

Adam Brown Executive, broker distribution, NAB

Ben Magnus Head of strategic partnerships, retail broker, ANZ

Baber Zaka General manager of third party banking, Commonwealth Bank

Wendy Brown Head of broker distribution, Macquarie Bank

Sarah Willsallen Head of broker distribution, Westpac

Jim Psirakis, Principal and nance broker, Pegasus Home Loans

As a 100% customer-owned bank, we always put the needs of our customers first. So, you can recommend Beyond Bank with confidence.

We take the same approach to maintaining mutually rewarding relationships with our broker partners.

• Our customer satisfaction score is 95% with our broker network.

• We offer genuine support, with open access to our Australian-based broker support team.

• Continuity of service is assured with our team owning each file from lodgement to settlement.

Beyond Bank is a B Corp certified bank. We use our business as a force for good to drive positive outcomes for our people, customers, communities and planet. We commit to balancing purpose with profit by meeting the highest verified standards of social and environmental performance, accountability and transparency.

Our broker support team will work for you and with you to help your customers with their lending needs. Chat the team on

990 or email brokerloans@beyondbank.com.au

MAJOR BANKS ROUNDTABLE 2025

tap into different segments of the market as they see fit, allowing them to develop unique selling points to offer customers.

How does CommBank do that? “That all comes down to having a fundamental, deep knowledge of our brokers through our relationship managers and of our customers,

brokers still cite channel conflict as a concern for them: 35% of brokers, to be precise, per MPA’s 2025 Brokers of Banks survey.

Channel conflict occurs when lenders compete with brokers by offering better deals and exclusive incentives to borrowers for taking out loans directly with the bank.

“We know some customers are doing it tough, and we’ve been providing tools to both brokers and customers to support them where they may want to manage their repayments”

Adam Brown, NAB

ultimately to understand what the needs of those segments are,” said Zaka.

Zaka brought up CommBank’s new broker-tiering model, which offers different levels of relationship manager support to brokers at different stages of their career. The goal is to “provide brokers with the services that they need to flexibly grow their business”, he said.

Representatives from the broking community tell me that channel conflict is an ongoing concern. What’s being done to tackle this?

Though it’s become less of an issue over time,

It was pertinent to kick this discussion off with Zaka, given that CommBank has copped the most flack over alleged channel conflict.

“We take channel conflict very seriously and have measures to address it. This includes a team that investigates and works with brokers to ensure a fair decision,” Zaka said in response to the question.

The table then heard about the brokers’ experience with channel conflict. “It’s a real thing, it’s happened to us,” said Pignone.

However, she acknowledged that it works both ways – brokers must provide “the best level of service so that the customer doesn’t feel the need to go into a branch”.

Nonetheless, Pignone rattled off numerous instances of a bank approaching one of her clients with an enticing deal.

Psirakis has encountered similar situations, though he agreed that it “probably comes down to a branch level as opposed to a bank-wide issue”. But it does happen, “and we are reluctant to send out clients to the branch for this reason”, he added.

Magnus shared that ANZ has an understanding “around the value a broker brings to the bank”. ANZ’s home loan business has full oversight of broker, branch and mobile distribution – the accountability lies with the bank to ensure that broker-originated customers are respected for the channel they have chosen to use.

At Macquarie – a branchless bank with over 95% of its home loans coming from brokers – channel conflict is obviously less of an issue. But at prior organisations, Brown has seen channel conflict play out across the industry, and she had some thoughts on how to address it.

“If a customer comes to us through a broker, we firmly believe that relationship should be maintained,” she said. “We ask all customers coming to our direct channel whether they’re working with a broker. If they are, the customer is referred back to the broker to ensure consistency and support for that relationship.”

The discussion shifted to NAB, with Adam Brown emphasising that banks seek to support customers through their channel of choice.

OVER TWO THIRDS OF BROKERS BELIEVE CHANNEL CONFLICT EXISTS

“Channel conflict arises when you don’t have clarity of roles,” he said. “We’ve worked hard to ensure that clarity. In our contact centres, broker-introduced customers are directed to a dedicated broker-service team, so their relationship is recognised and protected.”

Brown added that NAB has reinforced this approach by developing scripts for its service teams and aligning resources so that customers are always supported through the channel they choose, delivering a more consistent and enhanced customer experience as a result.

At Westpac, Willsallen drew attention to recent leadership changes. Willsallen is relatively new to the role, having taken over from Warren Shaw in January, while Shaw moved internally into the role of national general manager, home lending distribution.

“We’re very fortunate,” Willsallen said of the Westpac leadership team. “Warren

“From a channel perspective, we want to ensure that we serve and support customers irrespective of the channel they choose to engage”

Ben Magnus, ANZ

Shaw [is] passionate about mortgage brokers. He understands the industry and the important role brokers play in supporting customers to achieve their home loan dreams.”

Westpac’s culture “is one of collaboration”, said Willsallen. That includes collaboration between direct and brokered home lending channels. “On the infrequent occasions when channel conflict does arise, we act promptly and decisively to resolve matters,” she said.

Broker question: Major banks have launched multiple digital home loan offerings, including Unloan, ANZ Plus and Westpac Digital, in the last few years. Are you looking to invest more heavily in this space, and will it be to the detriment of investment in the broker channel? Psirakis fielded the first broker question of the day with a pointed question about where major banks’ priorities lie. Broadly speaking, the responses reiterated that the

MAJOR BANKS ROUNDTABLE 2025

customer experience must come first –although digital mortgages only make up a slither of these experiences for now.

“From a channel perspective, we want to ensure that we serve and support customers irrespective of the channel they choose to engage,” said Magnus. “We need to be clear on process and systems to be able to do that and ensure the proposition o ered meets the needs of customers and brokers. It doesn’t impact or challenge the direct investment of the broker because we’ll go where the customer tells us to.”

Magnus drew attention to customers’ overwhelming preference for working with brokers. “As we know, over 76% of customers choose to use a broker – that’s over 65% for ANZ from a flow perspective – so we’ll continue to be sharp and invest in our broker channel,” he said.

At Westpac, “we see technology investment as channel agnostic because it’s the same

mortgage origination system”, said Willsallen. “We innovate to provide a really simple, clean, easy experience for all our customers, regardless of the channel.”

Wendy Brown said, “Taking out a mortgage isn’t like buying a jumper online; it’s the biggest financial decision most people will make. So it’s not surprising that more and

“The segment is less than 5% and has been for years, so for now it’s not a sizeable market.” However, that could change in the future, he added. “I go back to my comment around being where the customer wants to be. If the customer wants to be digital at some point in the future, as a major bank you want to be there, sure. But it’s not growing, it hasn’t grown, so we’re not there at this point.”

Unloan is one of the most prominent digital loan products on the market, but Zaka doesn’t see digital loan investment as detrimental to brokers.

“They’re two very di erent product and service propositions for very distinct customer bases,” said Zaka. “The customer who wants to go and get advice and actually have a relationship that’s more than just foundational with a broker, that’s multi-years or the whole life cycle, is not the same customer that would be comfortable with going through a digital channel.”

Zaka also noted, “I have seen the type of personal support brokers o er their customers – and they’ve got nothing to worry about.”

We’re in the midst of a longawaited rate-cutting cycle. How are you driving your third party channel to seize the opportunities and safeguard itself against market competition?

Wendy Brown reminded the roundtable that Macquarie Bank was quick o the starting

We want to do things really well, but we want them done really quickly”

Amelia Pignone, LendX

more customers are choosing to use a broker – they get the benefit of an expert with lots of experience, they get a highly personalised experience, and they don’t have to pay for it.”

Brown also noted that digital mortgages remain a very small part of the overall market.

NAB’s Adam Brown echoed this, saying,

blocks following the RBA’s May rate cut, having passed the 25bps reduction through to customers after three days, compared to the 12-day market average. And Macquarie did it again on the same day the roundtable met.

“So we’re very responsive, and the feedback from customers has been great,” said Brown.

MAJOR BANKS ROUNDTABLE 2025

“We also make sure that we’re equipping brokers with the right tools. Tools like our servicing calculator are updated immediately as well, so brokers can have a lot of confidence they’re absolutely up to date and are giving customers the recommended outcome.”

Magnus leaned into ANZ’s reputation in the self-employed space, saying, “We’ve homed in on ensuring that our self-employed policy meets or even exceeds the expectations of where customers need to access funding.

“We’ve recently launched some changes to make it easier for self-employed customers to secure funding from ANZ and to remove friction points in the assessment of selfemployed income.”

Westpac is “proud to have made substantial improvements to the overall broker experience in the last few years”, said Willsallen. “We’ve reduced our time to decision by 43%, and we’re now leading the majors on one-day settlement, enabling us to seize the opportunity in the current market.”

“Taking out a mortgage isn’t like buying a jumper online, it’s the biggest financial decision most people will make. So it’s not surprising that more and more customers are choosing to use a broker”

Wendy Brown, Macquarie Bank

Willsallen highlighted the investments Westpac has made in processing systems and people alike. The bank has without a doubt been on a hiring spree, with industry figureheads Adam Croucher, Ray Esho and Louise Rainger coming into the Westpac fold in recent times.

“These are established industry people with deep connections and experience. They

know the broker value proposition,” said Willsallen. “We want to really show that we’re a brand who believes in broker and we’re here to win.”

NAB’s economic team has been forecasting the rate reduction cycle, explained Adam Brown. “We know some customers are doing it tough, and we’ve been providing tools to both brokers and customers to support them where they may want to manage their repayments.”

Brown gave some examples of how NAB is putting this into action, including different models of repayment reductions, multioffset accounts that give customers flexibility to manage savings across multiple accounts while reducing interest, and adding HELP debt assessment into serviceability.

CommBank is “very aware” of the spike in broker activity during rate movements, said Zaka. “Customers want to know, ‘What does this mean for me?’ and that creates real pressure.”

To support brokers during this period, Zaka explained how the bank is rolling out targeted educational content that brokers can share directly with clients, reducing repetitive tasks.

“We’re redesigning tools and processes to cut through the noise so brokers can focus on what matters,” he said. “It’s about helping brokers work more efficiently and protect their competitive edge.”

CommBank is looking into “how we give our

top-tier brokers tips and suggestions on using the data that we have and which customers they should be reaching out to”, Zaka added.

It’s a fine line between reaching out to brokers and spamming them with communication, though. As Pignone said, “When a rate cut happens, we’re flooded with communication.”

In Psirakis’ opinion, the banks should mainly focus their communication on when their new rates kick in. “That’s important for us as well, just to get a guide,” he said.

Broker question from Amelia Pignone: Australia’s mortgage market is one of the most competitive in the world, and brokers play a huge part in driving that competition. How do the major banks plan to remain competitive in a broker-driven landscape that increasingly rewards transparency and speed? And should we be expecting loyalty discounts for brokers in the form of LMI benefits?

Wendy Brown made clear that LMI benefits are not part of the plan.

Lenders mortgage insurance is certainly a hot topic. Used for low-deposit home loans, LMI is taken out by a bank to safeguard itself against default risk, with the cost passed down to the borrower.

Most banks have LMI waivers for eligible professionals such as doctors, lawyers and accountants. However, Brown is sceptical about their usefulness.

“The segments that actually have been given LMI waivers aren’t 100% the bestperforming segments,” she said. “For us, we haven’t seen it as a great customer outcome or opportunity for our brokers.”

Credit policy should first and foremost be driven by market demand, Willsallen explained, saying, “When we’re looking at what areas we want expand our appetite in, we will ask, ‘how big is the cohort, how many people does it impact, and therefore how big is the market opportunity?’ ”

WHAT DO BROKERS WANT FROM BANKS?

A great deal of time, effort and resources goes into implementing policy changes, added Willsallen. “When we’re prioritising [policy changes], we assess how many customers we’d get to help, as a key criteria in determining what we pursue.”

Zaka said, “What I firmly believe in is that brokers who do consistent business with us, we should give a premium service to. While we want to give a great service to all brokers, and all customers will receive the same experience behind it, we want to

grow brokers who want to consistently consider CBA offering to support the needs of their customers.”

NAB has seen success in leveraging the bank’s capabilities and knowledge to support brokerages seeking growth, Adam Brown explained. “Our professional services team has had success working with broker businesses in helping fund their growth,” he said. Access to NAB’s support systems isn’t limited by the size of the brokerage. “The opportunity for major banks is to help smaller

MAJOR BANKS ROUNDTABLE 2025

SHARE OF BROKER-ORIGINATED LENDING BY LENDER SEGMENT

Credit unions, building societies and mutuals Non-bank lenders

Any other type of lender Brokers’ white label loans

International banks (eg ING Direct, Citi etc)

Independent regional banks (Suncorp, Bendigo)

Regional banks owned by or aligned with major banks

Major banks (ANZ, CBA, NAB, Westpac)

brokerages grow by providing services and scale that second-tier lenders can’t always o er,” Brown said.

“At ANZ, we focus on our proposition rather than LMI waivers,” Magnus said. “Our Brokerology education platform is just celebrating its first year. That has on-demand training for brokers no matter where they’re at in their journey.”

Magnus believes LMI plays a role in providing protection for potential high-risk lending, and that waivers could increase risk exposure; however, certain industries and

professionals already benefit from waivers due to the strength of these segments.

There have been ebbs and flows over time, but the data shows that major banks’ share of brokeroriginated lending has reduced over the years. Why is that, and is it a concern for you?

“I think the brokers have created the competition,” Magnus kicked o with. “It’s a competitive market, so brokers that have come to the market have found avenues for