Help clients access up to $500K fast with ANZ GoBiz digital application. Funds available in just 2 days of signing up.

Music to your ears. Contact us.

CONNECT WITH US

Got a story or suggestion, or just want to find out some more information? twitter.com/MPAMagazineAU

facebook.com/Mortgage ProfessionalAU

02 Editorial

Are we going to walk the walk on DEI?

04 Statistics

Property’s million-dollar club

06 Opinion

ANZ’s Natalie Smith on why diversity o ers a competitive edge

51 Strategic leadership

The power of empathy as a leadership tool

MPA celebrates the pioneering women who are reshaping leadership in mortgage broking

Built on the decades of experience of its all-female team, SheInvests is paving the path to financial freedom for women

54 Brokerage insight

For Deb Box, being a woman in broking is no easy task, but it brings rewards

56 Other life

FEATURES THE ROAD TO GENDER EQUITY

The MFAA is pursuing a ‘whole-of-industry approach’ to achieving real change

Compassion and a commitment to giving back are at the heart of Rebecca Morgan’s brokerage

and what industry leaders have to say.

Are we going to keep brute forcing gender parity into every aspect of modern society, or are the days of diversity, equity and inclusion done for?

Donald Trump, as you might recall, returned to the White House as US president earlier this year. His victory brought with it a dizzying array of ramifications for international relations, global trade and social discourse. Almost overnight, some of the world’s biggest multinational companies began throwing their DEI departments under the bus for fear of catching the attention of Trump’s ‘anti-woke’ crosshairs.

IBM scrapped race- and gender-based supplier diversity targets. UnitedHealth Group removed its DEI web page. JPMorgan under chief executive Jamie Dimon scaled back mandatory diversity-related training programs while calling the Democrats “idiots” with “big hearts and little brains” for focusing too much on DEI. PepsiCo tossed its chief DEI o cer position onto the scrap heap. You get the point.

For the sceptics in the audience, this was hardly a surprise. Big business likes to talk

“Big business likes to talk the talk, but when it comes to catching a whiff of political or societal backlash, they’re not always so eager to walk the walk”

the talk, but when it comes to catching a whi of political or societal backlash, they’re not always so eager to walk the walk. Should we really expect anything less from these corporations? Perhaps not, but the DEI decimation that swept across the US this year is nonetheless a reminder that DEI targets are far from a universally lauded concept.

Yet here in Australia, Peter Dutton’s humiliating electoral defeat suggested that our appetite for divisive, Trump-lite anti-woke posturing is not nearly as voracious.

In my experience, that has allowed for an amiable discussion around the inherent gender disparity in the Australian mortgage broking scene. Despite being an industry that is meant to pursue the interests of all Australians, its gender balance has not only stagnated but reversed (women make up under 27% of mortgage brokers).

Some industry leaders – including women – told me we should just accept it and move on; years of trying to balance the equation have borne no fruit. Others believe we must double down and work harder to bring more women into the industry by creating an inclusive, supportive environment.

Everyone has their opinion, but one thing’s clear: women’s contributions to broking deserve equal recognition. In this DEI-focused edition of MPA, enjoy stories and insights from top female talent, and don’t miss our Elite Women 2025 Special Report on page 13.

William Farrington, editor, MPA

AUGUST 2025

EDITORIAL ENQUIRIES tel: +612 8437 4711 william.farrington@keymedia.com

SUBSCRIPTION ENQUIRIES tel: +61 2 8311 5831 • fax: +61 2 8437 4753 subscriptions@keymedia.com.au

ADVERTISING ENQUIRIES claire.tan@keymedia.com

MortgageProfessionalAustralia is part of an international family of B2B publications and websites for the mortgage industry

AUSTRALIAN BROKER simon.kerslake@keymedia.com

T +61 2 8437 4786

NZ ADVISER alex.knowles@keymedia.com

T +64 9 200 1319

CANADIAN MORTGAGE PROFESSIONAL shane.lakhani@keymedia.com

T +1 720-441-2255

MORTGAGE PROFESSIONAL AMERICA charles.weed@keymedia.com

T +1 720-441-2255

MORTGAGE INTRODUCER (UK) matt.bond@keymedia.com

T +44 203 868 3406

$204bn

Value of residential home loans settled by brokers in six months to Sept 2024

22,265

Total number of mortgage brokers as of Sept 2024 – the highest ever recorded

In 2015, just 273 suburbs had median house prices above $1 million. The most expensive were in NSW, Victoria and WA. By 2025, seven of the top 10 were NSW suburbs, and nine had medians exceeding $5 million. A total of 226 suburbs now have a median house price of more than $2 million. MILLION-DOLLAR SUBURBS: THEN VS NOW

24%

Increase in brokers writing commercial loans in year to Sept 2024

$23bn

Value of commercial loans settled by brokers in six months to Sept 2024

Source: MFAAIndustryIntelligenceService,19thEdition

Australia saw nearly 722,000 property settlements in FY25, up 3.2% from FY24, with the total value jumping 9.4% to $726.7 billion. Growth was driven by higher average prices, especially in Queensland and WA.

Median rents remain above pre-COVID levels, with strong growth from 2021 to 2024. However, the pace of growth has eased since late 2024 as vacancy rates have gradually risen across most states and territories.

Nearly 45% of Australian suburbs are at record-high housing values, led by Queensland and WA. While some cities, like Darwin and Perth, have rebounded, others lag. Momentum is building, with more suburbs expected to reach new peaks soon.

Australia’s major banks hold the largest share of residential property assets, but competition is intensifying as non-banks and customer-owned lenders expand. Industry consolidation and digital settlement solutions are reshaping

with brokers now sourcing over half of new mortgage values.

Creating an inclusive workplace strengthens businesses and develops stronger, trusted connections, says Natalie Smith, ANZ’s general manager Retail Broker

IN RECENT years, the mortgage broking industry has made strides towards greater gender representation. But progress is not always linear. Although the number of mortgage brokers has increased, progress in gender diversity remains limited. Women currently make up 27% of our industry, a figure that has remained unchanged for the past seven years. Clearly, there’s more work to do to attract, retain and support women in the broking industry.

As general manager of ANZ’s Retail Broker channel, I’ve seen how diversity strengthens

deeper understanding of people’s needs and property goals – qualities that can support better customer outcomes.

Small changes, big impact

Creating a more inclusive workplace doesn’t require a complete overhaul. Often, it starts with small, intentional changes.

Inclusive job adverts – using genderneutral language and highlighting flexible work options – can significantly widen the pool of applicants. Structured recruitment processes, including diverse interview panels

Diversity isn’t just a box to tick – it’s a competitive advantage

businesses. Diversity isn’t just a box to tick –it’s a competitive advantage. It can drive better performance, boost profitability and help access a wider pool of talent.

Diversity helps us better reflect society and our customer base, improve decision-making, innovate and enhance risk management.

Moreover, we know that mortgage broking is a relationship-driven business – and diversity plays a vital role in helping us build stronger, trusted connections with a broader range of customers. Borrowers want to deal with brokers who understand their needs and explain their loan options clearly, so it’s important that they have a strong understanding of their customers’ backgrounds and unique circumstances. Di erent life experiences bring fresh perspectives and a

and standardised criteria, help reduce unconscious bias and ensure fairer outcomes.

Supporting career returners is another powerful lever. ANZ’s award-winning Return to Work program helps women re-enter the workforce after parental leave or career breaks. Brokers might consider o ering things like mentoring, phased re-entry and tailored learning pathways to support women returning to work.

Flexible work isn’t just nice to have – it’s a powerful driver of enhanced employee engagement. It helps people to better balance their professional and personal responsibilities, which is especially important in an industry where many operate

GOT AN OPINION THAT COUNTS?

Email william.farrington@keymedia.com

as sole traders or small business owners.

We’ve seen that flexibility works; now it’s about how we’re making it a standard part of how we operate. Whether it’s remote work, flexible hours or shared caregiving policies, these arrangements make the industry more accessible and sustainable. But it’s equally important to ensure that men have access to these arrangements too. When men are supported with parental flexibility, it helps shift traditional perceptions around caregiving and encourages a more inclusive culture where flexibility is seen as a business norm, not a gendered exception.

Making these aspects of inclusion feel like the norm is key to driving meaningful change, as research shows that stereotypes, beliefs or expectations around gender roles still prevent women from entering or progressing in the broking industry.

Women often face stereotypes around leadership, caregiving and ambition. They may hesitate to apply for roles or start businesses without visible role models or supportive networks. That’s why sponsorship, not just mentorship, is critical. Sponsors advocate for women’s advancement, open doors and back them when they’re not in the room.

For brokers, the question becomes, Who are you lifting up? Creating a culture of sponsorship doesn’t require a formal program – just a willingness to notice the potential in people and advocate for growth.

In this issue, ANZ’s Elite Women report highlights the achievements of female brokers who are leading with impact. Their stories reflect resilience, innovation and the power of inclusive leadership. Their visibility matters. It inspires others, challenges outdated assumptions and shows what’s possible when businesses invest in diversity.

Natalie Smith is General Manager, Retail Broker at ANZ Banking Group (ANZ).

Prior to her appointment in February 2022, Smith held numerous leadership roles across the banking sector, including tribe lead (head of transformation) in ANZ’s Commercial division.

IN AN industry long dominated by male voices and outdated models, SheInvests has an ambitious goal in mind.

Founded by brokerage Flint and driven by a cast of women including Emma Stephens, Ana Souza, Laura Williams, Lauren Franzmann, Mia Castellarin, Sinead Grant, Tahli Elliott and Victoria Stefano, SheInvests wants to rewrite the blueprint for how women approach finance.

More than just an initiative, SheInvests is out to provide a platform for education, empowerment and lasting change.

At the helm is Emma Stephens, a seasoned broker with over two decades in finance. But SheInvests isn’t just her vision – Stephens stresses that it’s a collective response to an industry that hasn’t always made women feel seen or heard.

“SheInvests was born out of both professional insight and deeply personal experience,” Stephens tells MPA. “Now, as the conversation around women and wealth gains momentum, SheInvests o ers a much-needed space where women are seen, supported and empowered.”

Built on the lived experiences of its founders and team and powered by Flint’s national broking platform, SheInvests wants to break down the barriers women face at every stage of their lives.

“Over two decades in finance, I witnessed countless women – single mothers, business owners, professionals – hesitate to step into property ownership or investment simply because they felt the system wasn’t built for them,” Stephens says.

She recalls how her journey through career reinvention and motherhood underscored the

importance of having guidance you can trust. Now is the right time for SheInvests, says Stephens, “because the conversation around women and wealth has finally reached the mainstream.”

Women control more assets and purchasing decisions than ever before, she notes, yet they remain underserved by traditional finance. “SheInvests is here to change that narrative and build a community where women feel supported, seen and capable.”

There are a number of gaps that she hopes

at SheInvests means that “every woman who walks through our doors and walks out with a loan, a plan and a sense of power she didn’t know she had”.

As for the long term? “Nothing less than a revolution. We want to see an industry where women dominate portfolios and never again have to ask, ‘Is this space for me?’”

While SheInvests, at its core, serves to secure mortgage finance for women entering the prop-

“Now, as the conversation around women and wealth gains momentum, SheInvests o ers a much-needed space where women are seen, supported and empowered” Emma Stephens, SheInvests

SheInvests can bridge: confidence, accessibility, representation and community. “We simplify the language, address life transitions, and connect women through a support network that reflects their real experiences.”

Of course, while Stephens is the director, SheInvests is the culmination of the e orts of many remarkable women.

Mia Castellarin, Flint’s senior CX for highnet-worth individuals, is one such woman. “SheInvests isn’t just about finance; it’s about freedom,” Castellarin tells MPA. “We don’t just teach; we transform. Confidence comes when you feel understood, not judged.”

In Castellarin’s words, short-term success

erty market, it’s the support network that sets the platform apart from its contemporaries.

SheInvests has teamed up with dozens of women leaders in the finance space, including Molly Benjamin, founder of Ladies Finance Club. Benjamin says, “Emma has been one of our biggest champions – speaking at events, supporting women and helping grow our community.”

For Gemma Mitchell, financial adviser, money coach and host of the Australian Finance Podcast, SheInvests is her go-to referral for clients who need more than just a loan. “They bring strategy, empathy and results,” says Mitchell.

It’s this access to inspirational women in finance that has made SheInvests stand out in an increasingly saturated mortgage finance market.

As Ana Souza, Flint’s group operations manager, says, “Any brokerage can o er home loans. SheInvests is a safe space where women are seen, heard and supported. We’ve been underestimated too – and we lead with empathy. That’s our di erence.”

She adds, “Financial literacy is a basic right. And we’re here to make sure women have the tools, the knowledge and the support to claim it.”

Client testimonials rattle o glittering stories of how the SheInvests crew has helped them secure a home loan when other brokerages have dropped the ball. They speak of the team’s “never-say-no attitude” and Stephens being “a tireless advocate for women’s financial independence”.

For example, SheInvests can help single mothers map out a clear path to homeownership, utilising low-deposit options and government support to make this goal attainable. For young professionals, the focus could be on leveraging their income early, empowering them to start building wealth from the outset of their careers.

When it comes to women navigating significant life changes – such as divorce or a career

National masterclasses: In-person events designed to educate, inspire and connect women across all life stages with expert-led property and nance strategies

Digital education hubs: Always-on access to learning tools, resources and property guides tailored speci cally for women

Interactive webinars: Live sessions covering everything from rst home buying to building investment portfolios, hosted by the SheInvests team and special guests

Bespoke tools and templates: Goal-setting frameworks, property planning worksheets and investment calculators built with women in mind

National events and community: Expanding across major cities to create a movement of women supporting women in their property and wealth-building journeys

“Financial literacy is a basic right, and we’re here to make sure women have the tools, the knowledge and the support to claim it” Ana Souza, SheInvests

shift – Stephens emphasises the importance of providing both structure and clarity, alongside compassionate guidance. “We meet women exactly where they are,” says Stephens.

“These women are often told what they can’t do, but rarely shown what’s possible,” adds Victoria Stefano, Flint’s head of marketing (SA). We customise solutions that respect real life, factoring in income, kids, time and opportunity. No cookie-cutter advice – just strategy that honours the whole woman.”

The many women who have come together to make SheInvests a reality have a wealth of shared experiences to draw inspiration from.

Lauren Franzman, senior CX for first home buyers at Flint, recalls having to work twice as hard as her male counterparts to be taken seriously. “But I used that as motivation,” says Franzman. “I’ve built deep connections with clients, especially young women who feel the same way.”

Franzman adds, “We don’t assume or preach – we listen and tailor our support.

“It’s all about empathy and realness. Confidence comes from clarity, and that’s what we o er.”

Laura Williams, head of settlements at Flint, explains how “every part of SheInvests is informed by our journeys. We’ve all faced situations where the system didn’t quite fit us.”

Being part of a female-led initiative is “energising and meaningful”, adds Williams. “We’re not just working in finance; we’re redefining what leadership looks like.

“Being female-led allows us to challenge outdated models and bring in inclusive, human-centred perspectives. We’ve experienced being underestimated – now we lead with clarity and conviction.”

Meanwhile, Tahli Elliot, Flint’s head of operations (SA), says, “It’s both challenging and rewarding to operate in a space historically dominated by men.”

There is “motivation in defying stereotypes and creating a space where women feel represented and valued”, she adds.

SheInvests is gearing up for a major expansion, with a wave of new initiatives set to roll out nationwide.

“This is just the beginning,” says Stephens, teasing a whole load of national events, education hubs for connecting role models with aspiring investors, plus a new online platform with practical guides and interactive tools so women can access support any time, anywhere.

Then there are the masterclasses, webinars and podcasts that are in the works.

“Emma’s got a big vision, and it’s moving fast,” says Stefano. “SheInvests is building more educational tools, hosting events and finding new ways to reach women who may not even realise what’s possible for them yet. It’s growing with purpose.”

SheInvests is also calling on more passionate female brokers to join and help build the community.

WHAT IT means to be a female leader in mortgage is changing, and that change is long overdue.

For years, success has been measured by a narrow standard of long hours, linear progression and singular ambition, says Justine McDonald, a franchise owner and finance specialist at Nectar Mortgages.

“We need to rethink what leadership looks like. Let’s open the door to nontraditional paths, shared roles, flexible leadership models, and mentoring that meets women where they are at,” she explains. “We also need more women speaking at industry events, leading strategy and designing the systems, not just adapting to them.”

This call for change comes as eight years of Senior Executive Census data shows incremental progress has stalled and, in some cases, gender equality is sliding backwards for the first time since the pandemic.

According to the Chief Executive Women’s Senior Executive Census 2024: Keeping Score of a Losing Game report:

• 25 women were CEOs in the ASX300 in 2024, versus 26 in 2023

• 9 out of 10 CEOs are still men

• 1 in 8 CEO appointments were women, compared with 1 in 4 in 2023

• 7 in 10 executive leadership roles remain held by men

IS THERE A LACK OF WOMEN LEADERS FOR YOUNGER WOMEN TO LOOK UP TO AND ASPIRE TO FOLLOW IN THIS INDUSTRY?

“Lead with compassion, live courageously and believe in your unique perspective. You’ve earned your seat. Embrace your successes and make space for other women”

Fatima Dib, Finsure

• 27% of ASX300 companies have gender-balanced leadership teams

• 8 in 10 CEO pipeline roles are held by men

These numbers matter, states WORK180’s What Women Want 2025 report, and women are speaking up about why. Ninety-five percent report facing at least one barrier at work, while just over half (53%) believe conditions are improving, and their top

ANZ is proud to once again sponsor MPA’s Elite Women report, now in its fourth year. This report shines a spotlight on the remarkable women shaping the broking industry.

The women honoured in this report are recognised for their dedication and expertise in helping Australians reach their homeownership or business goals, whether as brokers, aggregators or lender representatives.

These women represent the strength and diversity of our industry, and we’re delighted to celebrate their success in partnership with MPA. Acknowledging their achievements reinforces the value of inclusive leadership and the positive impact it brings to customers and communities

priority remains flexibility. In fact, 70% value it more than a top-tier salary. Pay transparency and sexual harassment policies follow closely behind as essential ingredients for thriving at work.

Within mortgage broking, concerns about representation are growing louder. In MPA’s latest three-year survey data, 91% of women in 2025 said there’s a lack of female leaders

across the country.

Kerry Sainsbury, Credit Success

to look up to in the industry, up from 78% in 2024 and 61% in 2023.

This marked rise suggests the industry is moving in the wrong direction when it comes to visible leadership. For women entering or building careers in broking, the

We remain committed to working better together with brokers, aggregators and industry partners to promote a culture that is inclusive, empowering and enriched by diversity. Through strong collaboration and shared purpose, we are helping to shape a future that reflects the communities we serve – a future driven by innovation, representation and opportunity.

It’s a privilege to continue supporting these outstanding women and recognising the vital role they play in leading our industry forward.

absence of relatable role models can reinforce self-doubt and make long-term progression feel out of reach.

Anja Pannek, CEO of the MFAA, says the industry still has work to do.

The MFAA carried out its Diversity, Equity and Inclusion Survey in February 2024 to get members’ feedback about their experiences and perceptions in the lead-up to the MFAA’s

“I’ve continued to lead with purpose and heart, advocating for clients who believe they’ve struck a credit wall and encouraging brokers around the country to provide solutions that have a genuine impact”

inaugural DEI Summit in May 2025. The survey found that over 50% of respondents believe gender barriers still exist. They identified the main barriers as being:

• unconscious beliefs about gender roles in the workplace

• an industry culture that is not inclusive

• lack of industry experience

• safety concerns

• lack of development opportunities

“Unconscious bias can affect workplace interactions, career promotion and recruitment, while a non-inclusive culture can a ect the retention of women brokers and discourage women from joining the industry,” Pannek explains.

“Acknowledging and addressing these entrenched barriers is important to ensure we can make real progress, and this starts at the top, with our industry leaders.”

She adds that retention, not recruitment, is where the real challenge lies.

“The retention of women in broking is a greater challenge than recruitment,” Pannek says. “There’s a number of steps that can be taken to bolster retention and to enhance career development for women.”

She also points out that Australia is still trailing other major markets in female representation.

The proportion of female brokers in Australia’s mortgage broking industry is slightly lower, at 26.8%, than it is in the UK (30%) and the US (32.5%).

In March of this year, MPA invited industry professionals from across the country to nominate exceptional female leaders for its Elite Women 2025 list.

Nominees had to be working in a role that related to, interacted with or in some way impacted the industry. They should have demonstrated a clear passion for their work and been never previously recognised as MPA Elite Women.

Nominators were asked to describe the nominee’s standout professional achievements over the past 12 months, their initiatives and innovations and their contributions to the mortgage industry.

After a thorough review of all the nominations, the MPA team narrowed down the list to the final 50 Elite Women who have made their mark on the industry.

MPA’s Elite Women report is proudly sponsored by ANZ.

The mortgage industry wasn’t built with women in mind, and many are still finding their place in it, McDonald says.

“Too often, women carry the mental load of both family and career. Without strong support structures, something eventually gives,” she says.

“That’s why community, coaching and permission to do business their own way matter so much.”

Pannek says the industry must do more to spotlight the unique upsides of broking for women.

“While women often have to juggle

work, family and child-caring responsibilities, there are some fantastic advantages of a career in broking, such as the freedom of running your own business and the absence of a gender pay gap,” she says. “The industry needs to promote these benefits.”

Inclusion alone isn’t enough for women. McDonald says, “They want to be supported in a way that recognises their whole life, not just their business output. Policies that enable true flexibility, mental health support, leadership coaching and pathways for career re-entry after a break are essential.”

Culture counts just as much as policy, and

women thrive where they feel safe to lead as themselves.

The proportion of female brokers in Australia remained stable at 26.8% as of September 2024, but in real terms, more women are entering the field, although at a slower rate than men.

MFAA data shows a 5.6% year-on-year increase in women joining the profession. This growth occurred as the total number of brokers reached a record high of 22,265, indicating that the rise in female participation is part of a broader expansion

across the industry, with residential and commercial lending volumes at new peaks and mortgage brokers holding a 74.6% market share.

MPA’ s 2025 Elite Women remind the industry of what it takes to move things forward. This year’s Top 50 female leaders were selected through a rigorous nomination and review process. Each has achieved standout results and driven change through innovation, mentorship and leadership that’s helping shape a new era in mortgage broking.

“There are many incredibly talented women in the mortgage and finance broking industry achieving great things for themselves, their businesses and their clients,” says Pannek.

“An Elite Woman is someone who exemplifies excellence in everything she does. She is dedicated, passionate and highly professional in serving customers, working with colleagues and industry partners.”

McDonald believes that female leadership shouldn’t be measured solely by revenue targets. Modern leadership must be about building a business that reflects personal purpose and brings others along.

“An Elite Woman measures success by whether her work gives her the life she wants,” McDonald says. “She uplifts others, builds safe spaces for honest conversations and is confident enough to ask different questions, starting with, ‘Is this business serving my life?’ instead of ‘How can I hit that next target?’”

She adds, “At Nectar, we are proud to have almost double the industry average of female brokers. That didn’t happen by chance. It came from changing the conversation, creating safer spaces and helping women build businesses that reflect the life they want, not just the targets they’re told to chase.”

Christa Malkin General Manager, AFG

Becoming the first woman to lead AFG’s national aggregation business

Christa Malkin didn’t set out to break barriers but has done so regardless, by building trust, delivering results and earning influence across lending, broking and now aggregation.

After returning from maternity leave, Malkin joined AFG and took on leadership of its Strategic Partners program. From there, she stepped into the role of state manager for Victoria, then into the top aggregation post –a series of deliberate moves that widened her remit across the business.

As Victoria state manager, she was one of five women running AFG’s state-based teams, reshaping what leadership looked like across the country. “My replacement is a man, and he’s fabulous, but it was amazing to have five women running this key part of the business.”

Malkin doesn’t believe in performative leadership. She leads by example and expects her team to do the same. She explains, “If you say you’re going to do something, do it. Lead with authenticity. Provide people with a sense of where they’re going. If you’re not walking the walk yourself, you can’t expect people to follow.”

That approach, she says, sets the tone. “If we’re all doing that with our teams and it filters through the organisation, we create a culture where people want to do the right thing.”

Her experience across various sectors has shaped her leadership perspective. In addition to her work in banking and aggregation, she once served as general manager of a horse-

racing training business. The contrast confirmed her belief that leadership has less to do with industry and more to do with consistency.

Mentorship also runs through her work. She often hears from women who hesitate to put their hands up for leadership roles.

“If a man ticks one box out of five, he’ll go for it. If a woman doesn’t tick one box out of five, she won’t,” says Malkin. “We expect perfection from ourselves, and that holds us back.”

She reminds women that their strengths are often what set them apart. “Generally speaking, women are better organised, more likely to follow through, and bring empathy into everything they do,” she says. “That’s what clients want, someone who communicates, who delivers, who’s across everything.”

Flexibility, she believes, should be non-negotiable, especially for those raising families. “If someone needs to pick up their kids or go to a doctor’s appointment, that’s just part of life,” she says. “It’s not about clocking hours. It’s about delivering. If the work isn’t getting done, often that’s a capability issue, not a flexibility issue.”

She believes people do their best work when they’re treated like humans, not resources. “You’re going to crush people otherwise. They’ll burn out, and you’ll lose great talent.”

Shelley McGinty Managing Director, Preston Point Capital

Using community impact to build trust and business momentum

Relationships were the starting point, and word of mouth has carried Shelley McGinty’s

reputation further as she built her business by putting people first.

Her style is hands-on and personal, staying close to her clients and keeping the community at the heart of everything. Under her leadership, Preston Point Capital has won back-to-back Better Business Awards for Best Community Engagement Program and been named a finalist for Best Customer Service for two consecutive years.

“My business thrives on referrals and returning clients, a testament to the trust and satisfaction I’ve built over time,” McGinty explains. “Specialising in the investor and SMSF space, I understand the unique needs and aspirations of my clients.”

Alongside her brokerage work, McGinty plays a visible role in shaping the industry. A two-time finalist for Industry Thought Leader and a regular speaker at major events, including a recent on-stage interview at the

Better Business Summit 2025 in Queensland, she brings an insider’s view shaped by time spent with clients. She also sees business as a force for good. Through her advisory role with The Brewers Lunch, she has helped raise over $460,000 for health and community organisations across Queensland.

Inclusion is part of her day-to-day, and McGinty creates space for other voices, invites honest conversation and takes the time to listen. She asks the questions that move a team forward and speaks up when it counts.

But what defines her most is how she builds others up. Whether she’s mentoring a colleague, guiding a client, upholding ethical standards or supporting a local cause, McGinty helps others do the same. Her focus remains on helping clients and communities move forward, as those values and actions have made her a trusted leader and role model.

“I believe my influence stems from a

“We have the chance to redefine norms, inspire future generations and bring diverse perspectives that ultimately benefit clients and companies alike”

Shelley McGinty, Preston Point Capital

consistent commitment to excellence and impactful community engagement in the mortgage industry,” she adds.

Fatima Dib Head of Business Innovation,

Finsure

It’s no small task to reshape how one of the country’s leading aggregators approaches innovation and broker support.

At Finsure, Fatima Dib has built tools that brokers rely on, while strengthening the group’s global support model. She also helped drive expansion into Manila, opening the door to greater service capacity for brokers in Australia and New Zealand.

“Real innovation is a process with unique ideas that enhance e ciencies or solve new problems. People associate innovation with technology, but it’s broader,” Dib explains.

“Anyone can bring ideas forward. If you’re not innovating, you’re not being inclusive. True innovation doesn’t discriminate, it is gender-agnostic, age-agnostic and culturally agnostic. It’s a truly inclusive process.”

One of her lasting contributions is launching an industry-first scholarship program through Women in Finsure, designed to help female brokers in Australia and New Zealand build sustainable, resilient businesses. Each scholarship, valued at over $15,000, includes executive coaching, tailored marketing and IT support, financial literacy and one-on-one mentoring through the Finsure Broker Academy.

The early discomfort of feeling out of place in a male-dominated industry drove Dib to identify the barriers that kept women from entering or staying in mortgage broking.

“I sat on it, woke up the next day and said, ‘No, I’m going to be me’. At some stage, I’ll be so successful that they can’t ignore me. Industry culture will need to change, not me,” she says.

Determined to create lasting change, she collaborated with industry bodies to establish subsidised fees, mentoring programs and practical support, helping women build confidence and achieve success.

Her reach cuts across aggregation and into broader industry work. In 2015, Dib founded The iWoman Project, a social enterprise focused on financial education and empowerment. It helps women build financial independence and make informed decisions about their careers and futures through workshops and mentoring.

“I’m a big advocate for women in our industry, but it has become more personal. For me, it’s about being a role model for my four daughters and remembering that it counts even in my own home,” she says.

Christa Malkin, AFG

“They’re all older now and in their own careers, but I see it in the way they operate and realise every word and action around them is moulding them.”

“Leading with clarity and authenticity is something that I’ve done regardless of the role or the organisation, and it’s certainly something that I think my team appreciates”

Kerry Sainsbury CEO, Credit Success

Turning

Spanning credit repair, financial education and support for women, Kerry Sainsbury’s success is based on mentoring and community partnerships. Impact, she says, is achieved through small wins, from clearing a default and repairing a credit score to a client finally being able to move forward.

As CEO of Credit Success, she’s helped thousands of Australians regain financial control. Turning credit repair into a means of providing second chances for clients facing financial hardship is what underpins her dedication to helping others.

Over the past year, Sainsbury has grown the company’s broker referral network through trust and education. That same focus shapes her podcast, Wealthy and Wise with Kerry Sainsbury, which brings raw, genuine and current financial conversations to the public, often amplifying women’s voices in the process.

“What keeps me going is the passion for education and making a di erence in clients’ lives,” she reflects. “There’s not enough awareness in terms of credit reporting, in Australia in particular. The credit reporting system is evolving so much, but there’s little awareness unless it comes from a financial professional like myself or a mortgage broker.”

Clients often come to her after being denied finance due to unexpected credit issues, and her team’s ability to resolve the problems can be life-changing, restoring hope and financial opportunity.

“They come to us in such a state because they’ve realised there’s no next journey unless we can fix it,” she says. “You’ve got to come from a non-judgemental place. When we’re able to fix these issues due to errors or compassionate grounds, that’s a really nice story.”

Sainsbury has also strengthened her mentoring e orts, supporting women in business ownership and finance while continuing Credit Success’s partnership with the Safe Haven Community, which provides refuge to women and children escaping domestic abuse. What sets her apart is the ability to connect with people on a personal level. She appreciates that things can feel cold and transactional in the finance industry, but she and her team focus on empathy and trust. “I truly listen to people, understand their problems and constantly try to find a solution to make things better, even when it is hard,” Sainsbury says.

Fatima Dib

Head of Business Innovation, Finsure

Phone: 1300 346 787

Website: finsure.com.au

Kerry Sainsbury Director and Founder, Credit Success

Phone: +61 1800 956 694

Email: kerry@creditsuccess.com.au

Website: creditsuccess.com.au

Shelley McGinty

Managing Director, Preston Point Capital

Phone: 0474 722 722

Email: shelley@prestonpoint capital.com.au

Website: prestonpointcapital.com.au

Christa Malkin

General Manager – Aggregation, Australian Finance Group

Phone: 0428 778 443

Email: christa.malkin@ afgonline.com.au

Website: afgonline.com.au

Chuyu (Kiki) Feng

Senior Mortgage Broker, AUSUN Finance Box Hill

Phone: 042 319 5686

Email: kiki@ausunfinance.com.au

Website: ausunfinance.com.au

Diana McKenzie

Director/Senior Broker/Mentor, LoanPort

Phone: 0433 328 785

Email: diana@loanport.com.au

Website: loanport.com.au

Karlie Scharfenberg

Founder, The Loans Suite

Phone: 0406 870 080

Email: karlie@tlsga.com.au

Website: theloanssuite.com.au

Minh Beaver

Director/Financer Broker, Experity

Phone: 0412 591 428

Email: mbeaver@experity.com.au

Website: experity.com.au

Morgan Owen

Founder and Director, Penny Finance

Phone: 0459 595 999

Email: morgan@pennyfinance. com.au

Website: pennyfinance.com.au

Natalie Irvine

Chief Sales and Marketing O cer, RedZed

Phone: 0408 430 730

Email: nirvine@redzed.com

Website: redzed.com

Rachelle Kroon Director/Founder, Sphere Home Loans

Phone: 0487 004 044

Email: rachelle@spherehomeloans. com.au

Website: spherehomeloans.com.au

Akeshni Gour Treasurer, MA Money

Alana Baulch Senior Finance Broker, SLA Funding (Simmons Livingstone & Associates)

Angela Tracey Chief Marketing O cer, Loan Market

Anita Fung Business Development Manager, People First Bank

Anita Marshall Business Development Manager & Mentor, Vision Finance Collective

Anja Pannek Chief Executive O cer, Mortgage & Finance Association of Australia

Ashleigh Pakis Director, Panache Financial

Betty Lam General Manager, MortgageWorks

Caitlin Bransgrove Director and Mortgage Broker, Inspire Home Loans

Caroline Mundey Founder/Lending Specialist, Tevey Loans

Cathy Anderson Owner Manager, Mortgage Choice Blackwood & Adelaide CBD

Eli Hayes Owner Manager, Mortgage Choice, Albany

Emma Stephens Director, SheInvests, Flint

Gail Roots Mortgage Broker/Director, First Choice Home Loans Qld

Isabella ‘Izzy’ Constantinou Sales Director, Simplicity Loans & Advisory

Jennifer McLeod Mortgage Broker, Jenga Finance

Jessie Spencer Manager, Mason Finance Group

Justine McDonald Finance Specialist, Nectar Mortgages (Honeycomb Finance Group)

Katherine Persoglia Founder and Mortgage Broker, The Brokers’ Bible

Katrina Rowlands Chief Executive O cer, Mortgage Success

Kylie Quenon Principal, Go Mortgage

Madeleine Dart National Brand Manager, outsource Financial

Melissa Gielnik Managing Director, Smart Lending

Mhairi MacLeod Founder/Principal, Astute Ability Finance Group

Michelle Bannister Senior Executive, Head of Distribution, La Trobe Financial

Nicole Fox Director/Owner, Fox & Co. Finance

Nicole Kennedy Director/Finance Specialist, Verity Finance Group

Nina Batt Head of Residential, BCP Finance

Rebekah Sander

State Operations Manager, The Australian Lending & Investment Centre

Renee Dewar Broker Success Manager, Loan Market

Rhianna Farnan Director and COO, Derwent Finance

Sara Shome Mortgage Broker, Positive Money

Sarah Farrugia Finance Broker, SAF Finance

Sarah Willsallen Head of Broker Distribution, Westpac Group

Sinoma Gilbert Commercial Banker, ANZ

Suzi Trajanovski National Director of Growth, LMG

Tanya Sale CEO, Owner and Founder, outsource Financial

Veena Rughoonundun (R-Byrne) Finance Broker, Lifestyle V Finance

Zorica Grubic Partnership Manager, Connective Financial Services

Diversity is serious business at Liberty MPA sits down with the leading non-bank lender to hear how it’s setting the standard for the financial industry

LIBERTY, like all major players in the mortgage finance space, is acutely aware of the ongoing gender imbalance among Australian mortgage brokers.

While there is no shortage of industry-wide initiatives to encourage more women into broking, the data is borderline alarming.

According to the MFAA’s Industry Intelligence Service report for the six months to 30 September 2024, the proportion of women brokers has stayed flat at less than 27% since 2022. Even more concerning is the fact that female representation in the broking industry is less than it was in 2019.

MPA caught up with Liberty, one of the premier non-bank lenders in the sector, to discuss the issue and what it’s doing to

promote diversity and inclusion within the company and beyond.

According to Anne Bastian, Liberty’s chief people officer, “unconscious bias, a lack of role models, and exclusionary norms still hinder progress” on gender representation in the broking industry.

Diversity, in Liberty’s view, isn’t a box-ticking exercise; it’s a quintessential part of being a responsible, successful, publicfacing business.

“As a non-bank lender, we often serve diverse populations and individuals who may be overlooked by traditional banking methods, so understanding and reflecting that diversity

is important,” says Liberty chief executive officer James Boyle.

“Diversity and inclusion aren’t standalone initiatives; they’re integrated in the way we do business each day,” Boyle continues. “Our purpose is to help more people get financial, and when our team reflects the diversity of the communities we serve, we can gain deeper insights, stronger relationships and more inclusive solutions.”

Beyond pleasant words, Liberty is genuinely putting its money where its mouth is.

Liberty has implemented targeted initiatives to support gender and generational diversity, including its Women in Leadership and Women in Sales programs.

“These are designed to build confidence,

capability and career progression,” says Bastian. They are clearly working – women now command a 53% share of leadership roles at Liberty.

Strong leadership “is central to an inclusive culture”, says Bastian. “Our leadership team models inclusive behaviours, ensuring our values are reflected in daily practices. Senior leaders are not only visible champions of inclusion but also deeply engaged in structured initiatives such as leadership forums.

“These are designed to foster dialogue, share inclusive leadership strategies and align business goals with our DEI strategy.”

Liberty’s leadership takes part in Leadership Working Groups, which bring together cross-functional teams to develop initiatives, address inclusion challenges and drive cultural change.

“These e orts are reinforced by our cultural learning programs, including training focused on cultural awakening, LGBTQIA+ inclusion, gender equity and neurodiversity. This ensures inclusive leadership is authentically practised across the business,” says Bastian.

Cultural and community engagement is another key pillar of Liberty’s DEI strategy. This includes the company’s Innovate Reconciliation Action Plan.

“We’re proud to partner with First Nations organisations such as Kinaway, Murrup, Supply Nation and the Koorie Academy to create meaningful pathways in procurement, employment and education,” says Bastian.

Liberty has also introduced a tiered cultural learning program for all staff, co-designed with First Nations consultants, and a Reconciliation Committee to support ongoing engagement.

“We also provide cultural awareness training and host internal events that celebrate our rich mix of cultures and beliefs,” Bastian says. “We encourage team members to share their faith and cultural heritage, and these presentations are added to a growing library of lived experiences.”

Liberty stresses how important it is that, at every touchpoint, people experience an

“Beyond fostering inclusion at Liberty, our goal is to influence broader change by shifting perceptions, elevating women’s voices in lending, and addressing structural barriers such as income risk and access to networks”

Anne Bastian, Liberty

inclusive and culturally aware approach from the team. To support this, the group has introduced tailored LinkedIn Learning pathways focused on inclusive communication, cultural competence and supporting vulnerable customers.

Bastian explains, “These modules are part of our broader professional development o ering and reinforced by compulsory training on cultural protocols and inclusive practices.”

Doubling down

In a time when some of the world’s largest corporations are throwing their social justice initiatives out the window for fear of political

and social backlash, Liberty is unwavering in its dedication to DEI.

“In 2025, our DEI e orts supported a strong year of growth,” says Boyle. “Our internal survey showed that 97% of team members are proud to work at Liberty, and 98% believe we’re genuinely committed to being a diverse and inclusive company. Our average staff tenure of nearly six years reflects this sense of belonging and purpose.”

This commitment to DEI has brought with it clear business benefits for Liberty, including increased employee engagement, strong results on mental health surveys and better team accountability. “Positive brand

sentiment and high NPS scores from both customers and brokers further demonstrate the impact of our inclusive approach,” Boyle says.

The recruitment and career-progression stages are often where unconscious biases and exclusionary norms come into play. So for a company to genuinely champion diversity and inclusion, getting these practices right is critical.

Recruitment data reinforces the challenges at hand.

Returning to the MFAA’s Industry Intelligence Service report for the six months to 30 September 2024, 535 women were recruited during the period, constituting 32%

“Diversity and inclusion aren’t standalone initiatives; they’re integrated in the way we do business each day ... When our team reflects the diversity of the communities we serve, we can gain deeper insights, stronger relationships and more inclusive solutions”

James Boyle, Liberty

of all new recruits. This proportion remained unchanged compared to the previous six months, but recruitment of women decreased by 6.46% year-on-year, while male recruitment declined by only 1.05%.

“To address these challenges, we’ve introduced culturally responsive recruitment practices, inclusive leadership development and partnerships with a nity organisations like Work180 to create more equitable pathways,” says Bastian.

“We also monitor diversity metrics throughout the staff journey, with a focus on career progression in traditionally

underrepresented areas like credit, sales and leadership.”

Shifting perceptions

“We’re focused on accelerating gender equity in the broking industry and strengthening inclusive leadership across the lending landscape,” Bastian says. “Beyond fostering inclusion at Liberty, our goal is to infl uence broader change by shifting perceptions, elevating women’s voices in lending, and addressing structural barriers such as income risk and access to networks.”

Furthermore, Liberty is in the process of

launching the ‘AdvisHer Circle’, which will o er tailored education, peer networking, mentorship, and storytelling opportunities that directly address the challenges women face in broking.

The AdvisHer Circle is “a new initiative designed to support, retain and grow the representation of women advisers and brokers in our network”, explains Bastian.

Liberty is also committed to opening recruitment pathways for women entering the industry. “Through these e orts, we hope to lead by example and show what’s possible when diversity and inclusion is embedded in strategy, culture and action,” she says.

While struggles with gender representation in mortgage finance persist, it’s encouraging to see such a prominent member of the industry doubling down on diversity.

Liberty, of course, is not going it alone. Whether it’s the She Means Business initiative launched by COSBOA (the Council of Small Business Organisations Australia) and backed by the MFAA, or MPA’s very own Elite Women awards, which cast a light on inspirational female mortgage experts, the industry is not taking the lack of representation lying down.

In an industry that is meant to represent the incredible diversity of Australia, such initiatives are more important than ever.

Achieving a broking sector that mirrors the gender balance in society will take a united industry effort, says MFAA CEO Anja Pannek

YEARS of breakneck growth in the mortgage broking industry, it’s safe to say that female representation in the profession has failed to keep pace.

According to the 19th edition of the MFAA Industry Intelligence Service report, which covers the six months to 30 September 2024, there were 3,746 female brokers in Australia as of September 2024, making up less than 27% of the broker population. While

This plateau in the growth of women in broking, Pannek tells MPA, stems from a range of factors.

“The MFAA’s Opportunities for Women research consistently highlights unconscious beliefs about gender roles in the workplace as a significant barrier, coupled with the persistent perception of an industry culture that is not inclusive of women,” she says. “This, combined with balancing work and family commit-

“While entrenched barriers to greater diversity in broking remain, recognising and addressing them creates real opportunities for progress”

Anja Pannek, MFAA

that amounted to a 0.2 percentage point increase year-on-year, the number of women recruits fell 6.46% over the same period. In fact, the proportion of women in mortgage broking has hovered around 27% since as far back as 2017.

MFAA CEO Anja Pannek believes these figures underscore the need for a continued focus and fresh strategies to drive real change.

“At the MFAA we know we have a 29% to 71% female to male membership composition. This compares to just slightly over 50% of the Australian population being female.”

ments, limited access to business support and fewer opportunities for leadership roles, has also contributed to lower retention rates among female brokers.”

But Pannek says efforts to improve gender diversity are ongoing, in broking and beyond.

As highlighted by the MFAA’s The Value of Mortgage and Finance Broking 2025 report, compiled by Deloitte, structural barriers to achieving gender equity are not unique to the broking industry. Furthermore, the report found that gender balance in broking broadly mirrors that of the wider finance industry.

“This shows that structural support is critical to bringing about change,” Pannek says. “That’s why the MFAA is actively collaborating with partners across other industries to share ideas and identify opportunities. By recognising these are shared challenges, we can work together to break down barriers and build a more inclusive future.”

The MFAA held its inaugural Diversity Equity and Inclusion Summit in May 2024, which included a survey of members to gauge their views on DEI within industry.

More than 50% of respondents believed barriers still exist, with the main barriers being unconscious beliefs about gender roles in the workplace; an industry culture that is not inclusive of women; lack of industry experience; safety concerns; and a lack of development opportunities.

“While entrenched barriers to greater diversity in broking remain, recognising and addressing them creates real opportunities for progress,” says Pannek.

“Unconscious bias can still influence recruitment, promotion and everyday workplace interactions, while a culture that is perceived as not being inclusive may discourage women from entering or remaining in the broking industry. Additionally, commissiononly pay structures can deter some women who seek more financial stability, especially when balancing caring responsibilities.”

That being said, the mortgage broker commission-only pay structure does provide one notable gender-neutral advantage, compared to the majority of other professional services industries.

“The mortgage and finance broking industry has no gender pay gap, unlike many other professions in Australia,” Pannek explains. “This factor and the freedom of running your own business are part of the unique value proposition of broking. With so many positives, there is a great opportunity to better promote our industry to women and other diverse groups.”

The MFAA’s DEI survey shows that industry leaders are overwhelmingly seen as openminded and supportive of promoting diversity and inclusion, which, says Pannek, “gives us real momentum to build on as we work to create an industry that truly reflects the communities we serve”.

The MFAA’s research highlights a worrying trend – yes, the number of women entering the broking sector has remained stable over the past few years, but retention has emerged as a significant issue.

Simply put, the profession is not doing enough to ensure female brokers remain in the industry.

Pannek believes the key to improving retention is providing a support network that helps women build long-term, sustainable careers.

“We’re seeing an opportunity to better support female brokers to stay and thrive in the industry,” she says. The Value of Mortgage and Finance Broking 2025 report identifies training, mentorship and flexible working arrangements as key enablers to achieving this goal.

Retention is far from a broking-industryspecific issue. According to the Australian Small Business and Family Enterprise Ombudsman, barriers to female retention in the workplace include prohibitive access to capital, a lack of mentorship, and the

need to balance external responsibilities.

“A whole-of-industry approach is essential to driving meaningful change,” Pannek says. “This is why the MFAA is actively pursuing partnerships that foster inclusivity.”

These include collaborating with COSBOA (the Council of Small Business Organisations Australia) on the ‘She Means Business’ pilot program. The MFAA also runs the highly successful Women in Finance Broking series.

The MFAA is not taking static female representation in the broking industry sitting down. Its annual Women in Finance Broking program is among the many initiatives in the works.

Pannek stresses that this program is not just a series of networking events. “We want to create a space where professional women can come together to share ideas, build resilience and have important conversations about the challenges and opportunities women in broking face each day,” she says.

“This year, we’ll explore how women are reshaping the future of broking and finance –and how we can show up with confidence in the moments that count.”

Women in Finance Broking events will be held in:

Sydney – 22 August

Perth – 2 September

Melbourne – 5 September

Brisbane – 9 September

Adelaide – 16 September

The series will feature a keynote presentation exploring the changing landscape of financial decision-making and what that means for your business – as well as unpacking the complexities of leadership, gender representation and some of the challenges in the industry today.

These events will provide tools and materials to deal with challenges in operating or working in a broking business. Pannek says, “Broking can sometimes be a lonely profession, and it’s natural for brokers to focus heavily on growing their businesses, which leaves little time to reach out to their peers for support. This is especially true of women, many of whom are also juggling other responsibilities.

“Women in Finance Broking allows female brokers to connect with those who are experiencing the same things they are. It’s

Source: MFAA Diversity, Equity and Inclusion Survey, February 2024

“A whole-of-industry approach is essential to drive meaningful change. This is why the MFAA is actively pursuing partnerships that foster inclusivity” Anja Pannek, MFAA

about inspiring confidence in women to take the next step in building a successful career, to refuel and to understand their strengths.”

Then there is the She Means Business pilot program. Developed by COSBOA and funded by the federal government, it is designed to increase gender diversity among small broking businesses. Open exclusively to MFAA mortgage and finance broking businesses employing fewer than 20 sta , the program recognises the unique challenges and opportunities for women in the sector.

Earlier this year, the MFAA invited member businesses in NSW, Queensland and Victoria with a passion for improving gender diversity to apply for the pilot program. The 10 businesses selected will receive funding and

tailored training to support their growth, develop leadership skills and build other key capabilities, all while contributing to greater industry diversity and innovation. This includes in-person mentoring, interviews, training sessions and ongoing feedback loops.

She Means Business participants will gain valuable insights and practical skills they can apply directly in their businesses and initiatives and ideas that can be shared across the broader membership base that have actionable opportunities.

“This is an incredibly exciting initiative, and we’re proud to partner with COSBOA to promote broking as a rewarding career option, inspiring the next generation of female broker business leaders,” says Pannek.

When the MFAA convenes for its 2026 Diversity, Equity and Inclusion Summit, the focus will be on what can be done to e ect genuine change. “We see this as a significant opportunity to move beyond simply acknowledging the importance of inclusion, to bringing about real change through actionable, data-driven strategies that will reshape our industry,” says Pannek.

Data will play an integral role in this mission. Pannek says, “We have a clear picture of gender representation, but there’s gaps in our understanding of broader diversity across the mortgage and finance broking industry –including cultural background, disability and other factors that shape lived experience.

“By mapping this data, we can spark a meaningful conversation about representation, opportunity and the steps needed to ensure broking is truly reflective of the communities it serves.”

Pannek also believes more must be done to promote broking as an industry of choice and inclusion to the younger generations. “That means providing insights and pathways to those leaving school or those in the VET and higher education sectors, so they see broking as a meaningful career option.”

She adds that brokers play a critical role not only in helping Australians secure finance but also in promoting financial literacy, particularly among women and marginalised communities. “Trust is central to this work, and when brokers don’t reflect the diversity of their communities, there is a risk that key groups remain underserved and excluded from the benefits of quality financial guidance.

“Ultimately, we want the DEI Summit to inspire and empower industry leaders to take deliberate action, foster an inclusive culture within their businesses, and champion diversity as essential to both commercial success and community wellbeing,” Pannek says. “By elevating this conversation, we can help create a more vibrant, resilient broking industry – one that earns and retains the trust of all Australians.”

Into people. Not just transactions.

We partner exclusively with mortgage brokers to help them achieve the very best outcomes for their clients and their business, every time.

•Full, Mid and Quick Doc commercial up to $8M and LVR up to 80%*

•Full and Mid Doc residential up to $5M and LVR up to 80%*

•SMSF options for commercial (up to $8M) and residential (up to $5M)

• Commercial Lease Doc (25 year) standalone servicing with 2 year arm’s length remaining lease term

Short term private lending with flexible servicing secured against residential, commercial or residual stock properties

* Use our online postcode calculator to determine loan sizes and LVRs in your security location

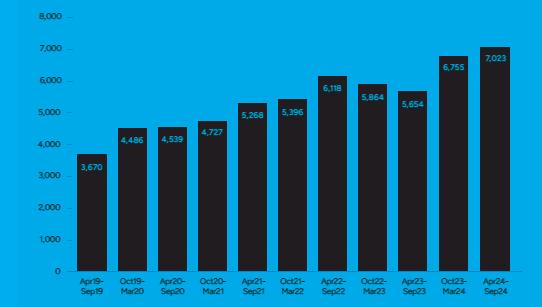

BROKERED COMMERCIAL finance is going through a boom phase. According to MFAA data, the number of brokers writing commercial loans was up over 24% year-onyear as of September 2024. Between September 2019 and September 2024, total brokered commercial lending nearly doubled from $43.1 billion to $85.9 billion, with a

record 7,000 brokers writing commercial loans through their aggregator at latest count.

The maturation of the space was evident at MPA’s 2025 Commercial Lenders Roundtable, which brought together a diversity of industry voices befitting the diversity focus of this issue of the magazine. The insights o ered – by representatives of major

and regional banks, non-bank lenders, aggregators and brokers – made it clear that the commercial lending space comprises many moving parts that come together to serve the interests of Australian business.

The challenges are real for brokers and businesses alike. For SMEs, access to a ordable, flexible funding is an enduring struggle.

The number of brokers writing commercial finance has soared to unprecedented levels, bringing fresh challenges and opportunities for brokers and lenders alike. MPA brings together leading industry voices to discuss the evolving state of commercial lending

For brokers, the challenge lies in how they go about entering the daunting world of commercial finance amid unprecedented levels of market competition.

Discussing these themes and more at the roundtable were Belinda Wright, head of partnerships and distribution at Thinktank; Siobhan Williams, head of mortgages – retail

broker at Pepper Money; Stephen Scahill, group executive, commercial and asset finance at LMG; Jason Arnold, group executive – origination at Pallas Capital; Mathew Clowes, head of credit and settlements at Resimac; Chris Thomas, executive commercial broker and equipment finance sales at NAB; Karen Carter, general manager, commercial third

party at BOQ Business; Grant Smith, chief lending o cer at ORDE Financial; George Lyall, head of origination at Millbrook; and Cory Bannister, chief lending o cer at La Trobe Financial, who joined remotely. Billy Moskovich, executive director of commercial finance brokerage Stamford Capital Australia, also joined as guest broker.

How are you forging and maintaining strong broker–lender relationships and reducing barriers to doing business with you?

Belinda Wright from Thinktank kicked the conversation off by stressing the importance of maintaining a robust dialogue. “We seek to proactively reduce barriers to doing business by staying connected and responsive,” she said.

Communication forms a major piece of this, with Thinktank taking brokers’ feedback and responding accordingly. “This direct feedback loop has resulted in several recent enhancements to our product suite, ensuring we stay ahead of the curve and adaptable,” Wright added.

Siobhan Williams explained how Pepper Money’s focus is on improving the broker experience through technology. The highprofile non-bank lender has rolled out new features like digital loan documents across commercial and SMSF segments, plus a new AltDoc Xpress process for accounts letter sign-off and customer self-

declarations, all with the intention of improving the speed to yes.

“We have a raft of educational digital content webinars leveraging our head of commercial credit,” added Williams. “These are also available on demand so that brokers, if they missed out on the live

LMG’s Stephen Scahill said, “As an aggregator, we see our role as ensuring that brokers that want to participate in commercial are suitably trained and skilled to do so.”

More brokers are pushing into the commercial space than ever, Scahill reminded the roundtable, and it’s up to

“Flexibility for us begins with actively listening to broker feedback and responding in a meaningful way that adds value”

Belinda Wright, Thinktank

session, can watch back through our broker hub in their own time.”

LMG, as a leading aggregator – and one that’s heavily pushing itself as the aggregator of choice for diversified brokers – has an important role to play in fostering strong broker-lender relationships.

aggregators like LMG “to provide pathways in terms of training to make sure that the quality of advice to customers and lenders submissions continues”.

Pallas Capital has seen significant growth over the last five years “by taking a deliberately localised approach to origination and

credit”, said Jason Arnold. “Expanding into markets like Adelaide, Canberra, alongside Sydney, Brisbane, Melbourne, allows us to employ experienced originators and credit professionals on the ground.”

Arnold expressed the importance of “going back to the old-school values of meeting in person, working things through and workshopping a deal over a coffee or beer”.

Switching over to Resimac, Mathew Clowes explained how the non-bank lender is “focused on strengthening our broker partnerships by offering a truly diversified and comprehensive range of product solutions”.

Simplicity and consistency are integral to the Resimac experience, added Clowes. “We’re constantly looking at how technology can make doing business with us simpler and more efficient. That means making sure our BDMs are not only knowledgeable about our full suite of offerings but also accessible and responsive when brokers need support.”

As the sole broker voice at the roundtable, Bill Moskovich has seen the market become extremely competitive over the past few years, particularly with the rise of private credit –which is another discussion.

“I think there’s more money in market than actual deals,” said Moskovich. “The proactive and successful lenders are making a great effort to forge relationships with brokers.”

Chris Thomas added, “NAB is the largest business bank in the country, and we see brokers as essential partners in supporting our customers. For us, that means bringing the best of NAB – our broad credit appetite

alongside brokers across a wide range of industries, “helping to reduce friction and make it easier to do business with us”.

ORDE’s Grant Smith noted that education and support of the broker “is critical, both for new brokers wanting to diversify in commercial, but also established commercial writers”.

He stressed how important it is for ORDE, as a relatively new lender to the scene (five years and counting), to ensure brokers under-

“It’s important for us as lenders to balance the priorities that the broker and customer might have”

Siobhan Williams, Pepper Money

and our extensive distribution network – into play, ensuring brokers are connected with bankers in local communities.”

NAB is “committed to investing in the broker channel to ensure brokers have the support they need to take care of their customers”, Thomas said. He highlighted that NAB has more than 600 bankers working

stand the nuances of its policies. “We’re tackling that through what we define as our ‘One Lending Team’ – aligning our distribution, credit and settlement functions so that the broker gets the support they need, from beginning to end.”

At BOQ, Karen Carter said, “We offer specialised education to our broker market in niche areas. Our focus is on collaborating with commercial brokers who possess extensive experience in business lending and have strong relationships with their clients.”

Carter also explained how BOQ employs a ‘three-way triage system’ that involves brokers, BDMs and bankers “to ensure that our level of service and care is unparalleled in the industry”.

It’s all about accessibility and trust at Millbrook, said George Lyall, who pointed out that brokers have direct access to the nonbank lender’s credit decision-makers.

“Transparency is another pillar for us,” Lyall added. “We’re upfront about how we assess deals, how we structure them, and what brokers and their clients can expect from the process. That level of openness builds confidence and helps reduce friction.”

La Trobe Financial, said Cory Bannister, commits to being a true alternative for

commercial brokers through its product range, reliability and certainty of execution.

“We are also investing further in highly skilled credit BDMs and have one of the largest sales teams nationally, ensuring both exceptional responsiveness and a comprehensive understanding of each broker’s business,” Bannister said.

Brokers are telling MPA that speed to market and time to yes have crept out. Why is this the case, and what are you doing to fix it?

There is no imagining it – turnaround times for both home loans and commercial finance have stretched out. It has emerged as a source of concern for brokers, who are under pressure to deliver the best results for their clients.

However, it became evident during this roundtable that speed, though important, is not the sole concern for borrowers.

While timing is key, “I think what’s more important is setting and meeting expectations,” Scahill said. “Because that could go into the consideration of which lenders have the best solution for the customer.”

space use these deals “as a bit of a testing ground”.

She said, “Whilst speed to yes is important, a lot of brokers are getting into this space for the first time. In this instance they are actually after a bit of handholding, understanding how it works, so it’s important that we still

“As an aggregator, we see our role as ensuring that brokers that want to participate in commercial are suitably trained and skilled to do so”

Stephen Scahill, LMG

Williams added, “It’s important for us as lenders to balance the priorities that the broker and customer might have. In some instances, time to yes is extremely crucial, which is why we have an express queue.”

Pepper Money’s wheelhouse is predominantly in the smaller-ticket commercial real estate space, which naturally makes for an easier loan process. But Williams is seeing brokers who are getting into the commercial

take the time to call them and discuss the term sheet when the loan is approved. That extra touch helps to take the broker along that journey to ensure they’re providing a good customer experience and educating them along the way.”

Bannister explained that time frames are largely influenced by the complexity of each transaction. “Although efficiency is important, our main focus remains on accuracy and

providing tailored solutions – especially with commercial transactions,” he said.

Bannister added that, while some commercial SMSF transactions and leasedoc loans may move quickly, “we are currently seeing fewer ‘low-touch’ commercial transactions due to lingering market effects from the pandemic period. Our expertise centres on loans that tend to fall outside the standard criteria of major banks, which naturally means these processes often take longer”.

At Thinktank, Wright said, “We have worked hard to ensure that our SLAs have remained consistent, despite higher year-onyear volumes”, but she acknowledged that brokers are experiencing longer-thanpreferred time frames for credit decisions and settlements in some parts of the industry, including commercial.

“Over the past few years, we’ve prioritised transparency and clarity around our turnaround times, providing brokers with consistent updates on our SLAs and where their deals stand in the pipeline,” Wright added.

ORDE, as the newest lender at the table, has worked to implement a service platform with efficiency at its core. Smith highlighted

that ORDE’s process uses “one accreditation, one credit policy, one application form and one SLA across all products”.

While AI and tech play a big role in maintaining efficiency, Smith noted that “tech frees up our team to focus on what matters: supporting brokers and working directly with them to deliver solutions as quickly and efficiently as possible”.

For Moskovich’s part, he has seen a creepout in turnaround times, although he contended that this is not necessarily the lenders’ fault. He said, “I think everything is just taking a lot longer, particularly in New South Wales, with all the class-two regulations coming in. You used to be able to get occupational certificate and strata registration in a month from achieving practical completion; it’s now blowing out to two, three months. As for construction certificates, it used to take three months; now it’s taking up to nine months.”

While Arnold stated that speed to market hasn’t necessarily blown out at Pallas, he said the real challenge “lies in obtaining the relevant information from external sources like regulatory bodies, builders, consultants, etc.”

He continued, “We’re specialists in the

open communication is so important. We’re making sure we’re transparent about timelines and that we’re managing expectations effectively from the start.”

To help with this increased complexity,

“You’re better off earning a portion of a fee and getting a free education along the way than walking away with nothing”

Jason Arnold, Pallas Capital

mid-market property and construction space, and our strength lies in the expertise of our team in that space, particularly development finance. So, while we move quickly and accurately on our side, we’re often at the mercy of third parties when it comes to timelines.”

Clowes noted that rapid growth in the commercial broker space has increased deal complexity, explaining, “More nuanced scenarios mean more detailed assessments, which can take more time. That’s why clear,

Resimac is investing in technology, data and AI to streamline the assessment process, added Clowes.

Carter stressed that BOQ’s speed to market “has remained relatively stable over the past couple of years”.

Furthermore, the bank is currently collaborating with mortgage aggregators to implement an API that will streamline processes for banks and brokers even further.

BOQ has undergone some significant

expansion, with 10 new BDMs added to the third party channel and 30 new banks added to BOQ Specialist in just six months. “This expansion is a key component of our strategic plan to enhance our presence and accessibility in key markets, with a particular focus on Queensland,” said Carter.

Lyall agreed that “there is no doubt the industry as a whole has seen timelines drag out”. This, he said, is partially due to “increased credit scrutiny, more complex deals and a shift in risk appetite across many lenders”.