Osaka Office Market Summary

Q2 2024

The June Tankan Survey for Greater Osaka showed that business sentiment rose to 10 points from 6 for large manufacturers and to 33 points from 30 for large non-manufacturers.

Net absorption totalled +21,000 sqm in 2Q24. Demand for expansion and higher-quality spaces kept firm due to the increase in hiring with business expansion. Manufacturing, IT and wholesale and retail stood out, while various industries have active demand.

There were two new completions in 2Q24: Osaka Dojimahama Tower (Kita-ku, GFA 67,000 sqm) in April and Inogate Osaka (Kita-ku, GFA 60,000 sqm) in June.

The 2Q24 vacancy rate rose to 4.1%, an increase of 100 bps q-o-q and 30 bps y-o-y. Although a wave of new supply comes on the largest supply year, the rise in vacancy rate stayed small due to beyond-expected demand.

Take-up (net) Completions Future Supply Vacancy Rate

For 2019 to 2023, take-up, completions and vacancy rate are year-end annual. For 2024, take-up, completions and vacancy rate are as at 2Q24. Future supply is for the remainder of 2024.

Source: JLL

The average monthly gross rent per tsubo was JPY 22,684, an increase of 0.3% q-o-q and 0.4% y-o-y. New completions with higher rents pushed up the market average for a second consecutive quarter.

Capital values increased 1.0% q-o-q and 1.0% y-o-y in 2Q24, due to current rent trends. Cap rates were stable from the previous quarter. There were no Grade A office transactions in Osaka this quarter.

Investment Market

The office investment volume in Osaka Prefecture in 2Q24 was JPY 16.4 billion, a decrease of 84.1 % and an increase of 45.4% y-o-y. The volume in the first half of the year was JPY 119.7 billion, an increase of 102.9% yo-y.

There were no Grade A office transactions in Osaka this quarter.

Outlook

According to Oxford Economics forecast as of June, Osaka City’s real GDP is expected by grow by0.6% in 2024 and to 0.2% in 2025.

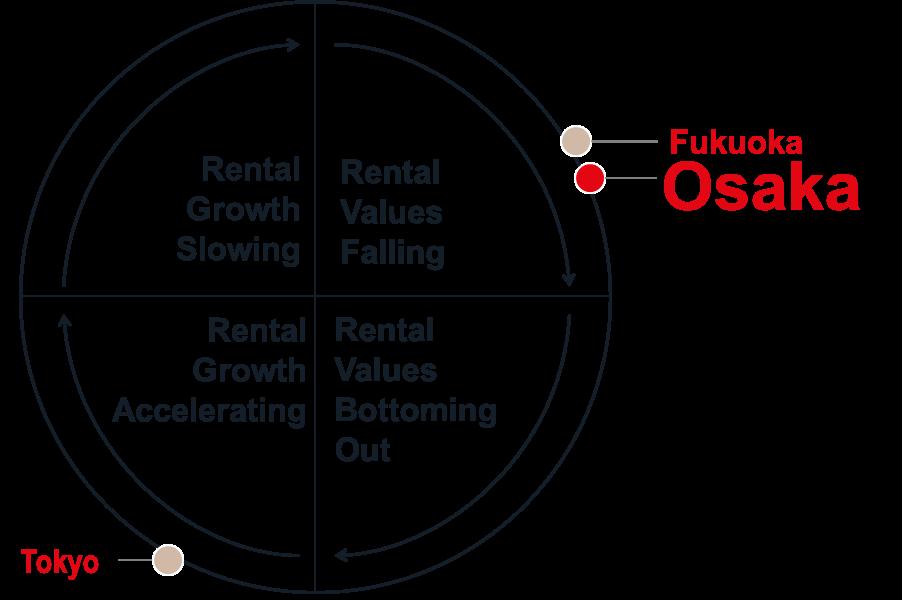

In the rental market, demand for superior office space is solid from companies with aspirations for equipment investment and talent hiring. However, some buildings with high rents, excessive age or undesirable locations struggle to attract demand and hold prolonged vacancies. Considering the large supply at the end of the year, the vacancy rate is likely to rise and drive rents lower.

In the investment market, investors have priced in supply-demand loosening and rent declines due to the large supply and are still actively seeking assets expected solid demand with good locations and low adjusted rents. The market is likely to remain active.

Source: JLL, 2Q24

Tokyo Headquarters Kioi Tower, Tokyo Garden Terrace Kioicho

1-3 Kioi-cho Chiyoda-ku, Tokyo 102-0094

+81 3 4361 1800

Fukuoka Office

Daihakata Bldg.

2-20-1 Hakata-ekimae, Hakata-ku, Fukuoka-shi Fukuoka 812-0011

+81 92 233 6801

Osaka Office Nippon Life

Yodoyabashi Building

3-5-29 Kitahama Chuo-ku, Osaka 541-0041

+81 6 7662 8400

Nagoya Office

JP Tower Nagoya 1-1-1 Meieki, Nakamura-ku, Nagoya-shi

Aichi 450-6321

+81 52 856 3357

Contact

Takeshi Akagi Head of Research Research - Japan takeshi.akagi@jll.com

Yuki Matsumoto Manager Research - Japan yuki.matsumoto@jll.com

Takeshi Yamaguchi Research Director

JLL Japan Osaka Office takeshi yamaguchi@jll.com

About JLL

For over 200 years, JLL (NYSE: JLL), a leading global commercial real estate and investment management company, has helped clients buy, build, occupy, manage and invest in a variety of commercial, industrial, hotel, residential and retail properties A Fortune 500® company with annual revenue of $20 8 billion and operations in over 80 countries around the world, our more than 108,000 employees bring the power of a global platform combined with local expertise Driven by our purpose to shape the future of real estate for a better world, we help our clients, people and communities SEE A BRIGHTER WAYSM JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated For further information, visitjll com

About JLL Research

JLL’s research team delivers intelligence, analysis and insight through marketleading reports and services that illuminate today’s commercial real estate dynamics and identify tomorrow’s challenges and opportunities. Our more than 550 global research professionals track and analyze economic and property trends and forecast future conditions in over 60 countries, producing unrivalled local and global perspectives. Our research and expertise, fueled by real-time information and innovative thinking around the world, creates a competitive advantage for our clients and drives successful strategies and optimal real estate decisions.