Japan MarketDynamics

Author Research

SeniorDirector ManabuTaniguchi

While real estate owners consider rent as a key consideration, tenants, particularly, manufacturing and retail companies, consider overall logistics cost, including rent, a more important factor.

Logistics costs divide functionally into transportation costs, storage costs and other costs including, packaging, loading, unloading, and logistics management. In Japan, transportation accounts for 576% of logistics costs, 164% for storage, and 26.0%1 for other costs. Warehouse rent is included in storage costs Although these percentages vary between companies,

transportation generally accounts for nearly half of logistics costs,whilestorageaccounts for10%-20%.

In 2024, Japan will regulate the upper limit on truck drivers working hours, thereby reducing transport distances and cargo volumes, andleadingtorisingtransportation costs.

Generally, transportation costs are proportional to the distance, and storage costs depend on the logistics base’s location. Consequently,astransportdistancesaresignificantlyaffectedby logisticsbaselocation, optimal logisticsbaselocations shift.

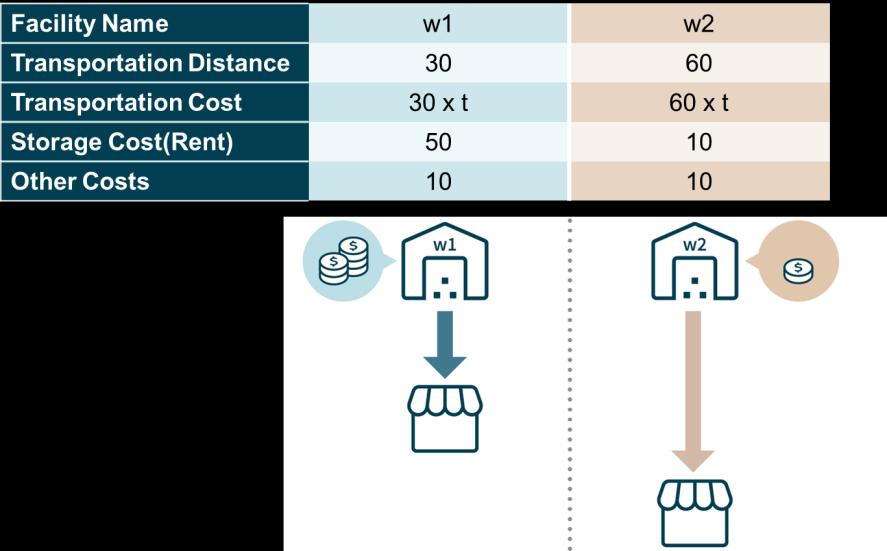

We assume two logistic bases to illustrate the impact of rising transportation costs on the logistics base location and transport distance, withthesimplificationthatstoragecostequalsrent

Logisticsfacilityw1hasashorttransportation distance(30),buthighrent, representing highstoragecost(50).

Conversely, logisticsfacilityw2hasalong transportation distance (60)butlowrent, representing lowstoragecost(10)

Let’s assume that transportation cost is calculated by multiplying the transportation distance by transportation cost per distance, denoted by“t”.Othercostsare10. Whent=1,thelogisticscostisasfollows, andchoosing w2ischeaper:

Ifw1isselected: Transportationcost30x1+Storagecost(rent)50+Other10=90

Ifw2isselected: Transportationcost60x1+Storagecost(rent)10+Other10=80

However, ifthetransportation costperdistance risestot=2,thetotallogisticscostisasfollows,andchoosing w1willresultinalower cost:

Ifw1isselected: Transportationcost30x2+Storagecost(rent)50+Other10=120

Ifw2isselected: Transportationcost60x2+Storagecost(rent)10+Other10=140

When the transportation cost per distance is less, low-rent facilities remain cost-effective, even with long transportation distances. However, as the transportation cost per distance increases, shorter-distance facilities become more economical, even with higher rents. Consequently, the demand for logistics facilities in locations with short transportation distances rises due toincreasing transportation costperdistance.

While Tokyo’s logistics facility vacancy rate remains high, the Chiba Bay Area, near the city centre, maintains zero vacancy despite rising rents. On the other hand, facilities further from the city centre exhibit high vacancy rates. Moreover, increasing construction costs will lead to approximately 50% higher future rents However, with ongoing truck drivers shortage, and the increasingdifficultytosecuredrivers,demandforlogisticsfacilities withrelativelyshorttransportdistances remainstrong.

[1] Japan Institute of Logistics Systems Logistics Cost Survey Report 2023

Source:JLLResearch4Q24

Globalinvestmentcontinuestoexpand

Globalrealestateinvestmentcontinuestogrow, drivenbyanincrease inlarge-scaletransactions byinstitutionalinvestorsamidliquiddebtmarket. Intermsofsectors,investmentinmultifamily housingcontinuestogrow,andinvestmentin officesisalsoexpandingduetostabilizing occupier demand.

Investmentopportunitiesincrease.

Thenumberofinvestorssellingpropertiesis increasingduetochangesintheinvestment environmentwithrisingprices andinterestrates. InJapan,whereinterestratesremainlow comparedtoEuropeandtheUnitedStates, investmentdemandfromvariousinvestors, includingdomesticlifeinsurance companiesand Asianinvestors,remainsstrong,andthereal estateinvestmentmarketcontinuestothrive.

Japan’sinvestment volumeexceedsJPY twotrillioninonequarter.

Withanincrease insalesoflargepropertiesamid continuedstronginvestordemand,investment volumeinonequarterexceeded JPYtwotrillion forthefirsttime.InvestmentinTokyoCBD,where largeofficeandretailtransactionswereseen, accountedforahigh61%oftotaldomestic investmentvolume.Tokyorankedfirstinthe globalcityinvestmentranking.

4

Outlook

Despitegrowingeconomicuncertaintycentered in theUnitedStates,nomajorchangeshavebeen observed intherealestateinvestmentmarket, andtheimpactontheJapaneserealestate market isexpected tobeminor.Duetoincreased investmentopportunitiesandrobustdemand, realestateinvestmentvolumein2025isexpected toexceed thatof2024,reachingnearlyJPYsix trillion.

• In1Q25,domestic realestateinvestment volume was up28%q-o-q and23%y-o-y toJPY2,095.2billion (USD13.7billion,up20%y-o-y).

• Investment volume inasinglequarterexceeded JPY twotrillionforthefirsttimesinceJLLbegantracking in2007.Thiswaspartlyduetotransactionsofsome largeofficesincluding Tokyo Garden Terrace Kioicho andlargeretailfacilitiessuchasTokyuPlazaGinza. Source:JLL

• Theshareofofficeinvestment in1Q25was58%with aninvestment volume ofJPY1,210billion,upfrom 51%inthesameperiod oftheprevious year.Thisis thefirsttimethatinvestment volumesinasingle quarterhaveexceeded JPYone trillionsince1Q15.

• Theshareofretailinvestment was16%,with investment volumesexceeding JPY300billionforthe firsttimesince1Q15.

• Logisticsfacilityandhoteltransactionsfellsharply, accounting for6%and11%ofthetotaldomestic investment volume, respectively.

• Theshareofmultifamilyhousingremained thesame asin1Q24at9%.

Source:JLL

• Tokyo CBD,whichsawmultiplelargeofficeandretail transactionsin1Q25,accounted for61%ofthetotal domestic investment volume, exceeding 60%forthe firsttimesince1Q18.Thisisthefirsttimesince4Q07 thatinvestment volume intheTokyo CBDinasingle quarterhasexceeded JPYone trillion.

• TheshareofGreaterTokyo (excluding Tokyo), comprising Chiba,SaitamaandKanagawa prefectures, whichwasaffected byadecrease in transactionsoflogisticsfacilities,was8%,down from 9%inthesameperiod lastyear.

• TheshareofGreaterOsakawas6%,down significantlyfromtheprevious yearwhenitrecorded itshighestshare.

Source:JLL

TokyoCBD(5-ku)

GreaterOsaka

Other

Tokyo(Excluding5-ku)

GreaterNagoya

GreaterTokyo(ExcludingTokyo)

GreaterFukuoka

Note:TokyoCBC(5-kus)referstoChiyoda-ku,Chuo-ku,Minato-ku,Shinjuku-kuandShibuya-ku;GreaterTokyoreferstoTokyo,Chiba,SaitamaandKanagawa;GreaterNagoyareferstoAichi, GifuandMie;GreaterOsakareferstoOsaka,Hyogo,

andNara; GreaterFukuokareferstoFukuoka,Saga,Nagasaki,Kumamoto,Oita,Miyazaki,KagoshimaandOkinawa.

• Limitedavailabilityinexistingbuildingsandcompletion offivenew buildingsresultinstrongnet absorption

• Rents riseforthefifthquarterinarow

• Regardless oftherecord-breaking amountofnewsupply, furthercompression ofvacanciestomid2%levelsisseen

According totheTankanSurveyinMarch,thediffusionindex oflarge manufacturersfell2points to12.Theindex oflargenonmanufacturersrose2pointsto35.Leasingactivityfellslightlythis quarter,however, robustdemand forleasesisseen. Netabsorption in theGradeAofficemarketinTokyo jumped to368,900sqminthefirst quarterof2025.Byindustry,thefigurewasdriven byservices, information andcommunications andmanufacturing.

FivenewGradeAofficebuildingswerecompleted inQ12025.Tokyo‘s vacancy rateintheGradeAofficemarketinQ12025averaged 2.5% andfell30bpsq-o-q anddown 170bpsy-o-y. Bysubmarket,the vacancy ratefellinbothOtemachi/Marunouchiand Akasaka/Roppongi, mostnotablyinthelatter.

Rents inTokyo’s GradeAofficemarketaveraged JPY35,520per tsubo,permonth,up1.4%q-o-qand4.9%y-o-yfromtheendof2024. Rents continued toincreaseinbothAkasaka/Roppongi and Otemachi/Marunouchi, particularlyinthelatter.

CapitalvaluesinQ12025rose3.0%q-o-q and8.3%y-o-ydueto rental riseandunchanged capratesfromthepriorquarter. Notable transactionsincluded theacquisitionofOtemachiONETower bya SPCofNippon LifeInsuranceCompany.

According toOxfordEconomics' forecastasofMarch2025expected GDPgrowth in2025is1.0%,whiletheforecastforCPIasofyear-end 2025is2.7%.Risksinclude theimpactoftariffsoncorporate activity andofficedemand, higherglobalinflation, adownturn inoverseas economies andpoliticaluncertainty fromtheupcoming Julyupper houseelection.

Leasingvolumesareprojected toexceed theprevious yearduetoa strongsupplypipeline. Thesupply-demand balanceremainstight, andrentalrisesshownosignsofabating. Risesincapitalvaluesare expected tocontinue withgradualriseinrents andlimitedorcloseto nochangesinBOJpolicyratethisyear.

Note:Financialandphysical indicatorsareforthe5KusGradeAofficemarket.Datais onanNLAbasis.

(thousands)

Netabsorption Newsupply Vacancyrate

• Robustdemand continues withasignificantconcentration oftenantsinUmeda, whereofficestockturnover isongoing.

• Thevacancyratefellfromthelastquarter,buty-o-y isstableat3.1%.

• Morelandlords liftrentlevels inamarketwithdecreasing vacancies.

TheMarchTankanSurvey forGreaterOsakashowed thatbusiness sentiment fellto10points from13forlargemanufacturers androse to30points from28forlargenon-manufacturers. Netabsorption totalled33,000sqmin1Q25.Soliddemand forofficespaces continues, driven bytheexpansion ofcompanies, theimprovement ofofficeequipment, finding betterlocationstomeet workplace hiring andretention strategies,andconsolidating locationstoencourage workercollaboration. Relocation wasevident among information servicescompanies, suchassoftwaredevelopment andbusiness processoutsourcing companies. In1Q25,thevacancy rateroseto 3.1%,down 130bpsq-o-q andunchanged y-o-y. Withsomelarge companies relocating toexistingandnew buildingsintheUmeda area,alargedecrease invacancies wasseen. Nonew projects entered themarketin1Q25. Theaveragemonthly grossrentper tsubowasJPY23,799,anincreaseof1.7%q-o-q and5.2%y-o-y. Vacanciesinbuildingscompleted in2024,thelargestsupplyyear of alltime,steadilydecreased, andgiven currentmarketconditions,

somelandlords raisedrent levelsbothinexistingandnewbuildings.

According totheOxford Economics forecastasofMarch,OsakaCity's realGDPisexpected togrowby0.2%in2025andby0.1%in2026.In therentalmarket,strongdemand fortheimprovement ofoffice equipment islikelytocontinue duetothecurrentworkforce shortage trend. Whileincreased supplythroughtwoprojects isexpected this year,andthevacancy ratewillrise,steadydemand forhigh-grade buildingsisprojected, withvacanciesfillingquickly. Inthe investment market,thesituationoffewopportunities foroffice transactionsremains duetotherebeingtoo fewassetsonthe market,althoughinvestorappetite foracquisitioninOsakaisstill solid.AnincreaseinCREsalesbylistedcompanies isexpected, but fewproperties willbesoldtoconvert tomulti-tenantofficeassets duetotheirspecifications, location, fit-outneedsorage.Investment intheOsakaofficeisexpected todecline y-o-y, thoughbetter fundamentalsareattractinginvestors.

Note:Financialandphysical indicatorsareforthe5KusGradeAofficemarket.Datais onanNLAbasis.

(thousands)

absorption Newsupply Vacancyrate

• Robustdemand isdriven byvariousindustries,including information andcommunications

• Vacancyratesfallforthefirsttimeintwoquartersamidlower vacanciesinnewbuildings

• Rents increasefortheseventhstraightquarter;capitalvaluesexpected tostabiliseamidslowingrentgrowth

TheKyushu-OkinawaTankansurveyinMarch2025was30,showinga 4-pointriseinDIforbusinesssentiment foralllargeenterprises; manufacturing improved by10pointsto29,whilenon-manufacturing declined by2pointsto30.Netabsorption totalled6,000sqmin1Q25, indicating anincreaseinleasedareadespite smallervolumes compared toprevious terms thatweredriven bymajornewsupply. Relocation demand camefrom industriesincluding theinformation andcommunications, transportation andprofessional services.

Nonewsupplycameintothemarketin1Q25.Thevacancy rate dropped to5.9%in1Q25,decreasing 110bpsq-o-q andwas unchanged y-o-y. Tenjin, AkasakaandYakuinsubmarketandGion, GofukumachiandNakasusubmarketsawreduced vacanciesinnew buildings,lowering thesubmarkets’vacancyrates.

Rents averaged JPY21,247pertsubo,permonth in1Q25,increasing

1.9%q-o-q and6.0%y-o-y. Rent growthwasobserved acrossthe marketdriven byexistingbuildings,aslandlordsadjustedrentlevels upwardsinresponse torobustdemand. Capitalvaluesincreased 3.9%q-o-q and8.7%y-o-y, reflecting rentgrowthamidstable investment yields.NoGradeAofficetransactionsoccurred inthe quarter.

Oxford Economics forecastsFukuokaCity‘srealGDPgrowthfor2025 at0.7%inMarch,aslightdowngrade fromDecember. Risksinclude theimpactoftradepoliciesinforeign economies.

Intheleasingmarket,robustdemand isexpected tograduallyabsorb majorsupply,leading togradualvacancy ratereductions andstable renttrends. Intheinvestment market,investor interestishigh,but stableyieldssuggestpricesto stabiliseandmirrorrenttrends.

Note: FinancialandphysicalindicatorsareforFukuoka’sGradeAofficemarket. DataisonaNLAbasis.

Grossrent JPY99,660pertsubop.m.

• Demand grows butslowsasluxuryconglomerates nearscompleting storerelocation projects

• Construction beginsonretailbuildingsduein2027-2028,includingNK-G3Buildingredevelopment on3Chuo-dori

• Rentalvaluesandcapitalvaluegrowth slows;futurecapitalvaluesexpected toalignwithrentincreases

Entering Q12025,realtotalemployee income hasgradually recovered whileconsumer confidence hasremained mostlystable. Thenumberofinbound touristscontinued tohitmonthly record highs.Amidthesecircumstances, retailsalestotalledJPY12.7trillion inJanuary,increasing 4.4%y-o-y. Demand fornewstoreopenings hasslowed down, asmajorluxuryconglomerates neared completion oftheirexpansion strategies.Notablenewopenings inthequarter included Brioni’sflagshipstoreatKiraritoGinzaonChuo-Doriin February.Tiffanywillopen anew flagshipstorealongsideGinza Chuo-doriinJuly.

Nonewsupplyentered themarketinQ12025.Construction ofNK-G3 Buildingredevelopment project (tentativename) inMarch.Fronting3 Chuo-dori, theten-storey retailandofficebuildingwithGFA2,100 sqmisduein2027.TheHulicAoyamaBuildingRedevelopment (tentative name)isslatedtostartconstruction inAprilatthecorner of theOmotesando andAoyamaDoriintersection. Thenine-storey buildingwithGFA9,700sqmisdueforcompletion in2028.

Rentsaveraged JPY99,660pertsubo,permonth inQ12025, increasing1.0%q-o-q and8.9%y-o-y. Thismarkedthe12th consecutive quarterofincreases,butthepaceofincreaseslowedfor thefourthconsecutive quarter. Capitalvaluesincreased by1.4%qo-qand10.8%y-o-yinQ12025.Notabletransactionsconfirmed in thequarterincluded GawCapitalandPatienceCapitalGroup’sjoint acquisitionof91%and9%,respectively, ofTokyuPlazaGinzafrom Sumitomo MitsuiTrustPanasonicFinance.

According totheMarchOxford Economics’ forecast,private consumption wasreviseddown toincreaseby0.9%in2025.Risks include trends inconsumer confidence. Intheleasingmarket,rents areanticipated tocontinue increasing, albeitatadecelerated pace duetoeasingdemand. Intheinvestment market,capitalvaluesare expected togrowintandem withrentgrowthascapratesare projected toremainstable.

Rentgrowth Y-o-Y 8.9%

Stage inrental cycle Rents Rising

Note:FinancialindicatorsarefortheprimeretailmarketsofGinzaandOmotesando, whileretailsalesgrowthfiguresareforTokyoPrefecture.DataisonanNLAbasis.

RetailSales

Growth

• Vacancyratesriseagaintoover10%duetoalargesupply

• Demandexpansioncontinues,butlocationdifferencesintensify

• Rentincreasescontinue,reflectingrisingcosts

InQ12025,net absorptionreached 588,000sqmduetosteady demand driven bye-commerce salesgrowth andalargevolume of newsupply. Astransportcostsrise,demand isstrong forproperties closetothecitycentre andwithshorttransportation distances, while properties infringeareaswithhighertransportcostsarestruggling. Thedifference intenant demand basedonlocation isintensifying.

Therewasanewsupplyof855,000sqmacrosssevenbuildings, increasingthetotalstockareaby10.1%y-o-y. Theoverallvacancy rateinGreaterTokyo reached 10.3%,up78bpsq-o-q and27bpsy-oy.Whilewell-located properties arefullyoccupied uponcompletion, someproperties inchallenging locationshavevacancieslastingover one year.

GrossrentinGreaterTokyo wasJPY4,677per tsubopermonth, down 0.2%q-o-q butup0.9%y-o-y. Thisreflectsrentdecreasesinexisting properties withprolonged vacancy periodsaftercompletion. However, thetrend ofhighrentsinnewly constructed properties

pushinguprentsinsurrounding properties continues, maintaining theoverallupwardtrend inrents.ThecapitalvalueinGreaterTokyo decreased by0.2%q-o-q. Despiterisinginterestrates,investment yieldsremain stableduetostronginvestor demand.

Rent increasesareexpected tocontinue, driven byexpanding demand frome-commerce growthandrisingconstruction costs. Investorsarelikelytoincreaserentson theirproperties more aggressivelyduetorisinginterestratesandproperty management costs.However, someareasmayseepotential rentdecreasesdueto anincreaseinvacantproperties.

Regarding theUStariffincreases,whiletheyareexpected tohave long-term effects througheconomic fluctuations,theshort-term impactondemand isconsidered limited, asmostlogisticsfacility tenantshandledomestic cargo withinJapan.

Note:TokyologisticsreferstotheGreaterTokyoprimelogisticsmarket.Dataisonan NLAbasis.

• Amplenewsupply,butthevacancyrateincreaseremainslimited

• Steadydemandcontinues;highoccupancyexpectedatnewcompletions

• Rentincreasescontinueduetorisingcostsandlowvacancyrates

InQ12025,steadydemand andalargevolumeofnewsupply resultedinanetabsorption of281,000sqm.Demands camefrom varioussectors,including e-commerce companies, 3PLcompanies andretailers.InGreaterOsaka,thedifference indemand basedon location wasnotconsidered assignificantasinGreaterTokyo.

Therewasanewsupplyof333,000sqmacrossfourbuildings, bringing thetotalstockareato7,358,000sqm,a10.3%increasey-o-y. Threeoutofthefournew buildingswerecompleted withhigh occupancy rates.Whilevacancyabsorption progressed atexisting properties, theoverallvacancy rateinGreaterOsakaroseto3.4%due toincreased vacantspaceinnewlysupplied properties, up58bpsqo-qand7bpsy-o-y.

GrossrentinGreaterOsakawasJPY4,186per tsubopermonth, up 1.3%q-o-q and2.1%y-o-y. Existingproperty rentsareincreasing, following thehighrentsofnewlyconstructed properties.

Reflecting stableinvestment yieldsandrisingrents,theupwardtrend inthecapitalvalueinGreaterOsakacontinues.

Intheleasingmarket,newsupplyisexpected toincreaseininland areasfrom2025onwards, likelycausingvacancyratestorise. However, duetosteadydemand, manyproperties areexpected to havehighoccupancy ratesupon completion, limitingtheincreasein vacancy rates,whichareforecasttoremain below5%.Properties that arecompetitive intermsoflocation, buildingspecifications andrent arefinding tenantsduringtheconstruction phase.

Rent increasesareexpected tocontinue atnewproperties dueto soaringconstruction costs.Existingproperties arealsolikelyto experience rent increases,driven bynewproperties. Whilethereare concerns abouttenants'availablerents,continued rentincreasesare anticipated duetoexpanding demand from e-commerce-related companies andthenearabsenceofvacanciesinexistingproperties.

Note:OsakalogisticsreferstotheGreaterOsakaprimelogisticsmarket.Dataisonan NLAbasis.

• Vacancyratesdecreasedespitenewsupply,drivenbystrongdemand

• Existingpropertiesmaintainhighoccupancy;rentscontinuetorise

• Increaseinnewsupplyexpectedfor2026-2027

Steady demand andnewsupplyresultedinanetabsorption of 96,000sqminQ12025.Demand expansion wasfrome-commerce companies and3PLcompanies continues.

InQ12025,therewasanew supplyof89,000sqmacrosstwo buildings,bringing thetotalstockareato1,608,000sqm,a14.7% increasey-o-y. Bothnew buildingswerecompleted withhigh occupancy rates.Vacancyabsorption alsoprogressed atexisting properties, withthevacancy ratedecreasing to4.7%,down 72bpsqo-qand84bpsy-o-y.

GrossrentinGreaterFukuokawasJPY3,543pertsubopermonth, up 0.2%q-o-q and3.1%y-on-year. Rents fornewly constructed properties continue torise,increasingbyabout10%compared to twotothreeyearsago.Rent levels insurrounding areasarealso following thisupwardtrend, withrentsatsomeexistingproperties increasing10-20%during tenantturnover.

Reflecting stableinvestment yieldsandrisingrents,theupwardtrend inthecapitalvalueoflogisticsfacilitiesinGreaterFukuokaarea continues. Investorinterestremains high,butinvestment opportunities areextremely limited.

Fewproperties havevacancies, andmany existingproperties continue tomaintainhighoccupancy rates.Thesupply-demand balanceisexpected toremaintightin2025.However, in2026-2027, newsupplyexceeding thatof2024isanticipated inareassuchas Tosu,potentially leading toanincreaseinvacancyrates.

Duetosoaringconstruction costs,rent increasesareexpected to continue forbothnewandexistingproperties. Property pricesare forecasttocontinue risingduetotheserentincreases.

s.m.

s.m.

Note:FukuokalogisticsreferstotheGreaterFukuokaprimelogisticsmarket.Datais onanNLAbasis.

• Growthcontinues, driven bythefullrecovery ofChineseinbound tourism.

• ThreeluxuryhotelssettodebutinTokyo inthelatterhalfof2025.

• Continued record highperformance.

YTDroomadditions 0rooms RevPAR growth trendY-o-Y ↑ Stage inRevPAR cycle

Note:TokyoHotelsrefertoTokyo'soverallhotelmarket.

Source:JLL,industrysources,STR

International arrivalsexceeded inQ1,whichwastheprevious record highforafirstquarter,by23.1%.Themainfactorcontributing tothis increasewasthefullrecovery ofChinesevisitors.Forthefirsttime sincetheend oftheCOVID-19pandemic, thenumberofChinese visitorsinaquarterlybasissurpassedthepre-pandemic levels ofthe firstquarterof2019.According toJapanNationalTourism Organization, Tokyo's totalnumberofovernight staysreachedanalltimehighin2024,surpassingthe2019figureby23.2%.2024markeda significantmilestone asinternational visitorsaccounted for approximately 52%oftotalovernight stays,surpassingdomestic guestsforthefirsttime.

Therewere noopenings ofnew international brandhotelsinQ12025. International brandsarestillkeentoopen newhotelsinTokyo. The latterhalfof2025issettowitnessawaveofluxuryhotelopenings, suchasFairmont,JWMarriott,and1Hotelslatedtodebutinquick succession.

InQ1,Tokyo's hotelsectordemonstrated continued growthacrossall segments intermsoftradingperformance. Theongoing increasein inbound visitorshasdriven asustainedriseinADR,whileoccupancy hasalsoshownsteadyrecovery. Intheluxuryandupper upscale segments, Q1showedsignificantimprovements compared tothe sameperiod in2024.ADRincreased by10.6%,whileoccupancy rose by6.3points. Consequently, RevPAR sawasubstantialgrowth of 20.1%.However, occupancy stilllagbehind theQ12019by5.7points.

Whilethestrong performance trendscontinued throughQ12025,the escalationofgeopolitical risksandincreasing globalinstabilityin Aprilhavecreated uncertainty. Itwillbecrucialtocloselymonitor howthesefactorsimpact theperformance ofthesecond quarter.The USD/JPY exchange rateisexperiencing significantvolatility.Given thatthepreviously weakYen hasbeen amajorfactorinboosting inbound visitornumbersanddriving upADR,anysharpappreciation oftheYen couldpotentially impacthotelperformance.

Historicalnewsupplytrends

• CASBEE-BD/-REdoublesintwoyears

• CASBEE-WOslowdowns

• Shareofgreen-certified officebuildingsincreasesinallthreecities

Green-certified projects(average q-o-q) +7.6%

• TheJapaneseversion ofSustainabilityMarketDynamics featuresSSBJ sustainabilitydisclosurestandards

NineprojectsacquiredLEEDcertificationin1Q25.Platinum-awarded projectsincludedAzabudaiHills(LEEDNDBuiltv4).Thetotalnumberof certifiedprojectssince2009hasreached315,anincreaseof2.9%q-o-q.

Fifty-fourprojectsacquiredCASBEE-BD certificationin1Q25.Thenumberof acquisitionsduringthequarterincreasedq-o-qandy-o-y,buttheshareof rankSwasdownq-o-qandy-o-y.ThetotalnumberofCASBEE-BD-certified projectsincreasedby8.2%q-o-qto526,2.1timesthenumberin1Q23.

CASBEE-REcertificationwasacquiredby282projectsin1Q25.Thenumber ofacquisitionsduringthequarterincreasedq-o-qbutdecreasedy-o-y.The totalnumberofCASBEE-RE-certified projectsreached2,388,anincreaseof 11.5%q-o-q, and2.2timesthenumberin1Q23.

FiveprojectsacquiredWELLcertificationin1Q25,withthenumberof acquisitionsduringthequarterdecreasingbothq-o-qandy-o-y. PlatinumawardedprojectsincludedMitsubishiCorporationHeadOfficeandShimizu CorporationNagoyaBranch(bothWELLv2Certification:OfficeSpaces).The totalnumberofWELL-certifiedprojectshasreached60,anincreaseof9.1% q-o-q.

NoprojectsacquiredFitwelcertificationin1Q25.Thetotalnumberof

Fitwel-certifiedprojectsremainedatfive.

NineprojectsacquiredCASBEE-WOcertificationin1Q25,includingone projectrecertifiedduetoexpirydate.Thenumberofacquisitionsduringthe quarterdecreasedq-o-qandy-o-y. ThetotalnumberofCASBEE-WOcertifiedprojectswas174,up1.2%q-o-qand1.9timesthenumberin1Q23.

InTokyo,theacquisitionofDBJ-GB andCASBEE-RE hasprogressed,and theshareofgreen-certifiedlargeofficebuildingsin1Q25reached72%,up7 ptsq-o-q. Theshareofwellness-certifiedlargeofficebuildingswas6%, down1ptq-o-q, duetothelowcertificationrateforbuildingscompleted duringthisquarter.

InOsaka,theacquisitionofCASBEE-REhasprogressed,andtheshareof green-certifiedlargeofficebuildingsin1Q25reached45%,up3ptsq-o-q. Theshareofwellness-certifiedlargeofficebuildingsremainedat10%asno buildingsobtainedcertificationthisquarter.

InFukuoka,onebuildingacquiredCASBEE-REcertification,resultinginthe shareofgreen-certifiedlargeofficebuildingsrisingto30%in1Q25,up3pts q-o-q. Theshareofwellness-certifiedlargeofficebuildingsremainedat9% asnobuildingsobtainedcertificationthisquarter.

Note:LEED,WELLandFitwelrefertoallratings.CASBEE-BD,CASBEE-REand CASBEEWOrefertoB+andabove.

Source:JLL,USGBC,IBECs,IWBI,Fitwel

Historicalvalidgreencertificationbycertifiedyear

Source:JLL,USGBC,IBECs

Tokyo Headquarters

KioiTower, Tokyo Garden Terrace Kioicho

1-3Kioi-cho Chiyoda-ku, Tokyo 102-0094

+81343611800

Fukuoka

FukuokaDaimyoGardenCity

2-6-50Daimyo, Chuo-ku,Fukuoka-shi

Fukuoka810-0041

+81922336801

Kansai

Nippon Life

Yodoyabashi Building

3-5-29KitahamaChuo-ku, Osaka541-0041

+81676628400

Nagoya

JPTowerNagoya

1-1-1Meieki, Nakamura-ku,Nagoya-shi

Aichi450-6321

+81528563357

JLL’s research teamdelivers intelligence, analysisand insight through marketleading reports and services that illuminatetoday’scommercialrealestatedynamicsandidentifytomorrow’schallengesandopportunities Our more than 550 global research professionals track and analyze economic and property trends and forecast future conditions in over 60 countries, producing unrivalled local and global perspectives Our research and expertise, fueled by real-time information and innovative thinking around the world, creates a competitive advantageforourclientsanddrivessuccessfulstrategiesandoptimalrealestatedecisions

For over 200 years, JLL (NYSE: JLL), a leading global commercial real estate and investment management company,hashelpedclientsbuy,build,occupy,manageandinvestinavarietyofcommercial,industrial,hotel, residential and retail properties A Fortune 500® company with annual revenue of $234 billion and operations in over 80 countriesaroundthe world, our more than 112,000 employees bring the power of a global platform combined with local expertise Driven by our purpose to shape the future of real estate for a better world, we help our clients, people and communities SEE A BRIGHTER WAYSM JLL is the brand name, and a registered trademark,ofJonesLangLaSalleIncorporated Forfurtherinformation,visitjllcom

This reporthasbeenpreparedsolelyforinformationpurposesanddoesnotnecessarilypurporttobeacompleteanalysisof thetopicsdiscussed, whichareinherentlyunpredictable.Ithasbeenbasedonsourceswebelieve tobereliable,butwe havenotindependentlyverified thosesourcesandwedonotguaranteethattheinformationinthereportisaccurateor complete.Anyviewsexpressed inthereportreflectourjudgmentatthis dateandaresubject tochangewithoutnotice. Statementsthatareforward-lookinginvolveknownandunknownrisks anduncertaintiesthatmaycausefuturerealitiesto bemateriallydifferentfromthoseimpliedbysuchforward-lookingstatements.Advice wegivetoclientsinparticular situationsmaydifferfromtheviews expressedinthisreport.Noinvestmentorotherbusinessdecisionsshouldbemade basedsolelyontheviewsexpressedinthisreport.