Are we on the edge of a new global economic order?

FINALIST IN THE MINDFUL MONEY AWARDS 2025 Best media reporting on ethical and/or impact investment

HISTORY LESSON

Looking back (and forward) at tariffs

MOVING ON UP

Growing small business from the ground up

FUTURE OF WORK

Integrating office design and technology

BABY BMW

New BMW 1 series hatchback will turn heads

Dame Lisa Carrington, canoe sprint gold medalist

Finn Butcher, kayak cross gold medalist

some of our contributors

What we like Cool camera, pink gin and a skincare power trio.

the winter Winter is far more enjoyable when coupled with lovely home comforts.

Subscribe and save

Get Informed Investor delivered straight to your letterbox.

New investor for a new world (order)

We are in a “hinge” moment, and the old rules of investing may no longer work, writes Shamubeel Eaqub. 20 Are tariffs really so bad?

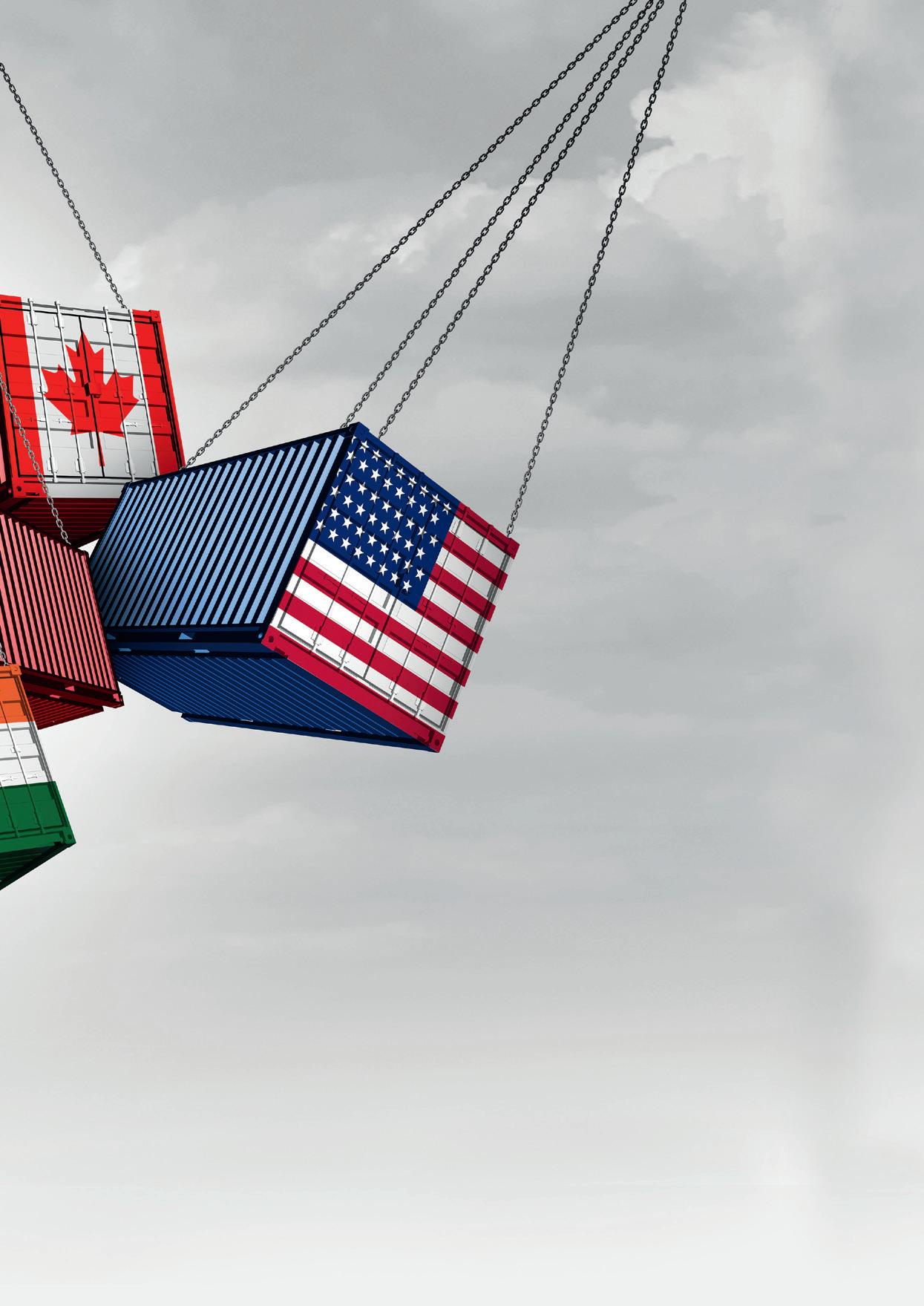

Andrew Kenningham takes us on a journey through the history of tariffs.

Tariffs, investment and opportunity

Oliver Mander of NZ Shareholders’ Association explores what Trump’s tariffs may mean for Kiwi investors.

on up

Two local businesses who have gone global.

of luxury

Turning high-end accommodation into a thriving business.

Sound advice for the self-employed

Martin Hawes on lessons he’s learned over 50 years of self-employment.

HR in an AI world

How do small and medium businesses navigate the brave new world of digital HR? 38 The bold, the brave and the burnt out

Victoria Bahadoor and Charlotte Clark, co-founders of Empower Her Community, on what it really takes for female founders to build a business.

The social science of skincare

Social media can be a powerful tool for marketing beauty products – even outside the sphere of glam influencers.

Market volatility is challenging, but staying invested and focusing on long-term goals is the clearest path to wealth creation.

It is essential to adapt how we teach young people good money habits in a cashless world.

Jason Choy from InvestNow explores the volatility of the market.

moves in uncertain times

Generate’s new retail funds are aimed at helping investors reposition for long-term growth.

Liv Lewis-Long looks at the best strategies for investing.

Forces affecting business, investment and the economies across the globe.

The year is speeding along, but the housing market isn’t.

Logitech partnered with Datacom to create an office space that seamlessly integrates with cutting-edge technology.

Andrew Nicol from Opes Partners didn’t achieve success overnight.

Liz

History repeats

A Good Time for Reflection

ROGER DOUGLAS’ NEOLIBERALIST

in the world’s economy. London-based commentator Andrew Kenningham states that while economists are often an argumentative bunch, when it comes to free trade, they tend to be fully aligned. They all believe it works.

Everyone has a different attitude to money, but to make it work for us it’s important to explore how we relate to it.

economic reforms of 1984 opened up New Zealand to global free trade. While controversial at the time, the removal of trade barriers was pursued by subsequent governments; Helen Clark’s facilitation of a free-trade agreement with China in 2008 possibly the zenith of our economic liberalisation.

It’s nearly holiday season (the year has flown by) and a good time for reflection. I’m not one for new year’s resolutions, but I do love a bit of soul searching during the spacious summer holidays.

The protectionist policies undertaken before the mass liberalism of the global economy have long been seen as a vestige of a less enlightened age. Tariffs are the ultimate outworking of these archaic policies – scoffed at by economists and politicians alike.

Tariffs were old news – until this year. And history hasn’t been kind to those who put their faith in them.

and develop over our life, and explains how people can develop better relationships with money.

Informed Investor PO Box 40128, Glenfield, Auckland 0747

Informed Investor 33 Federal Street, Auckland Central, Auckland.

Published by: Opes Media www.informedinvestor.co.nz

informedinvestor.co.nz

But under US president Donald Trump, the rules of global economic engagement are being rewritten, the clocks turned back.

This year I’m going to take a long, hard look at my predisposition to spend. I love shopping (books, clothes and music are my obsessions), but this has got me into a lot of trouble in the past. Now I’m older (and a little wiser) I make sure saving comes before spending, although my current house renovations are certainly stretching the family budget.

Money is a potent force. It can be used for good or evil and without doubt profoundly influences the trajectory of our lives.

At the time of writing, president Trump has just agreed to extend the deadline for negotiating tariffs (which he had said would be 50 per cent) with the European Union until July 9. The 145 per cent reciprocal tariff, imposed on goods from China, was paused on May 13, to be revisited on August 12.

Everyone has a different attitude to money. Some (like me) see it as a ticket to good times; others scrimp, save and fear to touch it. Our attitudes are based on a raft of factors – upbringing, financial history, pessimistic or optimistic outlooks – but to make money work for us it’s important to explore how we relate to it.

New Zealand (and the rest of the world) is still subject to his 10 per cent tariff, introduced on April 10. But given his capriciousness, anything could have happened by the time you read this.

In our lead story this issue, economist Shamubeel Eaqub, surmises the current state of play.

“The last 80 years was an aberration, not the norm. Investors need to plan for a return of less recent history.”

The lead story this issue, written by “money mentalist” Lynda Moore, delves into our “money personalities” – the way in which we relate to money.

He posits that we are on the verge of a time-slip; free trade’s ideological stronghold is crumbling. And the implications for investors are, at this stage, undetermined.

Kenningham discusses the “infamous […] Smooth-Hawley tariff […] passed by the US Congress in 1930. Ironically, this tariff made things worse, hastening a collapse in exports and production, and the rise in unemployment.”

We’ve also modified a quiz taken from Lynda’s website (moneymentalist.com) so you can discover your own “money personality”. It’s quick, easy, and a bit of fun, but it should also get you thinking. This is a great Christmas holiday activity to share with friends and family over a glass (or bottle) of bubbly.

Small business is also a theme of this issue. New Zealand punches above its weight when it comes to small-business success –we meet a number of small business owners who have achieved great results through clever ideas, great timing, and the boldness to stay true to their vision.

We hope you enjoy this, our second issue of Informed Investor under the ownership of Informed Media. It’s been a joy to produce!

Amy Hamilton Chadwick delves into another sort of money personality this issue: the financial pessimist. If you’ve been stung before, it makes sense that you’d be cautious around investing. But as Amy explains, fear of doing anything (or “analysis paralysis”) can prevent you from embracing a brighter financial future.

Informed Investor is an investment magazine published quarterly by Informed Media. You need Informed Investor ’s written permission to reproduce any part of the magazine.

Informed Investor is an investment magazine published quarterly by Opes Media. You need Informed Investor’s written permission to reproduce any part of the magazine.

Advertising statements and editorial opinions in Informed Investor reflect the views of the editorial contributors and advertisers, not Informed Investor and its staff.

Advertising statements and editorial opinions in Informed Investor reflect the views of the advertisers and editorial contributors, not Informed Investor and its staff.

We continue on the topic of tariffs with an excellent historical analysis of their role

Based on extensive research and the contents of her excellent book, Conversations with Money: A Love Story, she digs deep into our histories, explores how our attitudes change

Managing editor

Editor Joanna Mathers

Joanna Mathers – joanna@informedmedia.co.nz

Design director

Art Director

Sally Fullam – sally@informedmedia.co.nz

Mark Glover

Account manager

Account Manager

Joanna Mathers – joanna@informedmedia.co.nz

Stephanie Bryant – 021 165 8018

Subscriptions

Subscriptions

Sally Fullam – subs@informedmedia.co.nz

Jill Lewis – subscriptions@informedinvestor.co.nz

We are been delighted to have been nominated for an award at the Mindful Money Awards in the Best Media Reporting on Ethical and/or Impact Investment category so early in our ownership. But it is an outworking of my commitment for many years to ensure investors understand that ethics must play a role in their decision-making.

We also check out the new convertible Mini, the importance of goal setting, and how electric cars are changing transport economy worldwide.

We really hope you find inspiration in the pages of our magazine and wish you all the very best for this festive season.

Winners will be announced in late May, so by the next issue, we will know the result. Fingers crossed!

Take care and happy holidays.

Stay warm and safe

Informed Investor ’s content comes from sources that Informed Investor considers accurate, but we don’t guarantee its accuracy. Charts in Informed Investor are visually indicative, not exact. The content of Informed Investor is intended as general information only, and you use it at your own risk: Informed Investor magazine is not liable to anybody in any way at all. Informed Investor does not contain financial advice as defined by the Financial Advisers Act 2008. Consult a suitably qualified financial adviser before making investment decisions.

Informed Investor’s content comes from sources that Informed Investor considers accurate, but we don’t guarantee its accuracy. Charts in Informed Investor are visually indicative, not exact. The content of Informed Investor is intended as general information only, and you use it at your own risk: Informed Investor magazine is not liable to anybody in any way at all. Informed Investor does not contain financial advice as defined by the Financial Advisers Act 2008. Consult a suitably qualified financial adviser before making investment decisions.

Joanna Mathers Editor

Joanna Mathers Editor

Subeditors

Resident economist

Ed McKnight Printer Webstar

SÍana Clifford Mike Deacon

Printer

Webstar

Retail Distributor Are Direct

Retail distributor Are Direct

This magazine is subject to NZ Media Council procedures. A complaint must first be directed in writing, within one month of publication, to the email address, joanna@informedmedia.co.nz. If not satisfied with the response, the complaint may be referred to the Media Council PO Box 10-879, The Terrace, Wellington 6143; info@mediacouncil.org.nz. Or use the online complaint form at www.mediacouncil.org.nz. Please include copies of the article and all correspondence with the publication.

This magazine is subject to NZ Media Council procedures. A complaint must first be directed in writing, within one month of publication, to the email address, stephanie@informedinvestor.co.nz. If not satisfied with the response, the complaint may be referred to the Media Council PO Box 10-879, The Terrace, Wellington 6143; info@mediacouncil.org.nz. Or use the online complaint form at www.mediacouncil.org.nz. Please include copies of the article and all correspondence with the publication.

Informed Investor magazine does not give any representation regarding the quality, accuracy, completeness or merchantability of the information in this publication or that it is fit for any purpose.

Informed Investor magazine does not give any representation regarding the quality, accuracy, completeness or merchantability of the information in this publication or that it is fit for any purpose.

To advertise in Informed Investor, you must accept Informed Investor magazine’s advertising terms and conditions. Please contact joanna@informedmedia.co.nz about advertising.

To advertise in Informed Investor, you must accept Informed Investor magazine’s advertising terms and conditions. Please contact Stephanie@informedinvestor.co.nz about advertising.

Informed Investor is printed on environmentally responsible paper. The paper is produced using elemental chlorine-free pulp, sourced from sustainable and legally harvested farmed trees. The magazine is recyclable.

Informed Investor is printed on environmentally responsible paper. The paper is produced using elemental chlorine-free pulp, sourced from sustainable and legally harvested farmed trees. The magazine is recyclable.

PRINT ISSN 2744-6085

DIGITAL ISSN 2744-6093

PRINT ISSN 2744-6085

DIGITAL ISSN 2744-6093

Want a 6.5 x better

Meet some of our contributors

SHAMUBEEL EAQUB

Shamubeel is chief economist and head of policy at Simplicity, and a thought leader who is unafraid to take a contrarian view.

TIMOTHY GILES

Timothy Giles is our wine enthusiast. For 30 years he has been sharing his enthusiasm for fine and funky wines as a writer, trainer, list curator and podcast host. To build up a thirst he enjoys open water swimming, triathlons and is a football referee in Auckland. Dad-of-one goal is to share more of his wine cellar with his daughter than is left to her.

JASON CHOY

Jason Choy is a senior portfolio manager with InvestNow.

BRIDGETTE JACKSON

Bridgette Jackson is a CDC-certified divorce/separation coach with a postgraduate dispute resolution qualification. She is also a trained divorce mediator (AIMNZ), a relationship coach (Institute for Life Coach Training), and a member of the Institute of Executive Coaching and Leadership (accredited by the ICF –International Coaching Federation).

OLIVER MANDER

Oliver is the CEO of NZ Shareholders’ Association. He is as a strategic thinker, focused on transformative solutions, developing and implementing business strategies so that they come to life for organisations. He believes that a strategy means nothing without delivery.

CHARLOTTE CLARK & VICTORIA BAHADOOR

Charlotte, a branding strategist and alignment coach, and Victoria, a personal brand photographer and ADHD coach, empower women to build impactful businesses with confidence. Through their global community, they create opportunities for connection, growth, and visibility in a space where women feel truly seen and supported.

Meet Some of Our Contributors

Meet Some of Our Contributors

CAMERON BAGRIE

KELVIN DAVIDSON

KELVIN DAVIDSON

Cameron is the managing director of Bagrie Economics, a boutique research firm. He was previously chief economist at ANZ, a position he held for over 11 years.

Kelvin joined Cotality in March 2018 as senior research analyst, before moving into his current role of chief economist. He brings with him a wealth of experience, having spent 15 years working largely in private sector economic consultancies in both New Zealand and the UK.

Sam Bryden is Head of Distribution at Nikko AM NZ. With over 18 years’ experience in investment management and financial markets, the last six of these at Nikko AM, he is responsible for leading the firm’s sales, marketing and client servicing.

Kelvin joined CoreLogic in March 2018 as senior research analyst, before moving into his current role of chief economist. He brings with him a wealth of experience, having spent 15 years working largely in private sector economic consultancies in both New Zealand and the UK.

MARTIN HAWES

MARTIN HAWES

MARTIN HAWES

ANDREW KENNINGHAM

Martin is the chairman of the Summer KiwiSaver Investment Committee. He’s an authorised financial adviser and offers his services throughout New Zealand.

Martin Hawes is a well-known New Zealand financial author, conference speaker, and TV and radio commentator.

Martin is the chairman of the Summer KiwiSaver Investment Committee. He’s an authorised financial adviser and offers his services throughout New Zealand.

Andrew is the chief Europe economist for Capital Economics.He was previously an economic adviser for the United Kingdom Foreign Exchange.

CAMERON BAGRIE

KELVIN DAVIDSON

LIV LEWIS-LONG

Cameron is the managing director of Bagrie Economics, a boutique research firm. He was previously chief economist at ANZ, a position he held for over 11 years.

Kelvin joined CoreLogic in March 2018 as senior research analyst, before moving into his current role of chief economist. He brings with him a wealth of experience, having spent 15 years working largely in private sector economic consultancies in both New Zealand and the UK.

Liv is a passionate finance educator, writer and podcaster, and set up Simplicity’s Money Made Simple podcast to help level up financial literacy in NZ. She also heads up its marketing team, with over 15 years’ experience in brand, communications and storytelling.

Kelvin joined March 2018 analyst, before his current economist. a wealth of spent 15 years in private sector consultancies Zealand and

MARTIN HAWES

ANDREW KENNINGHAM

ANDREW KENNINGHAM

Andrew is the chief Europe economist for Capital Economics. He was previously an economic adviser for the United Kingdom Foreign Exchange.

Andrew is the chief Europe economist for Capital Economics.He was previously an economic adviser for the United Kingdom Foreign Exchange.

Martin is the chairman of the Summer KiwiSaver Investment Committee. He’s an authorised financial adviser and offers his services throughout New Zealand.

Mike has been InvestNow launch, March past 20+ years senior management some very well-known international brands – TAB, Reuters and

ANDREW NICOL

STEPHANIE WHITTAKER

SAM STUBBS

Andrew is an authorised financial adviser and the managing partner of Opes Partners. He has more than 15 years’ experience in banking, finance, and property.

Andrew is an authorised financial adviser and the managing partner of Opes Partners. He has more than 15 years’ experience in banking, finance, and property. Oyster’s

Stephanie is a Generate adviser specialising in KiwiSaver and managed funds. Along with her Level 5 Certificate in Financial Services, she has a degree in Education and more than 13 years’ teaching experience in NZ and the UK. Her passion is financial literacy and translating complex financial concepts into clear, personalised advice.

Sam is the founder and MD of Simplicity, New Zealand’s only low-cost, nonprofit funds manager. Previously from the banking world having worked for Goldman Sachs and NatWest Markets in London and Hong Kong, Sam believes the finance industry should be as much a force for good as a source of profit.

ANDREW NICOL

ANDREW NICOL

SAM STUBBS

Andrew is an authorised financial adviser and the managing partner of Opes Partners. He has more than 15 years’ experience in banking, finance, and property.

Andrew is an authorised financial adviser and the managing partner of Opes Partners. He has more than 15 years’ experience in banking, finance, and property.

Sam is the founder and MD of Simplicity, New Zealand’s only low-cost, nonprofit funds manager. Previously from the banking world having worked for Goldman Sachs and NatWest Markets in London and Hong Kong, Sam believes the finance industry should be as much a force for good as a source of profit.

ANDREW NICOL

MIKE HEATH

SAM BRYDEN

SAM STUBBS

Sam is the founder Simplicity, New low-cost, nonprofit Previously from having worked and NatWest and Hong Kong, the finance much a force of profit.

KELVIN DAVIDSON

What we like

Cool camera, pink gin and a skincare power trio for winter.

Picture perfect

FUJIFILM has just launched, the GFX100RF, the first camera in the GFX series to feature a built-in lens, while also being the lightest body yet, weighing just 735g. Designed for exceptional performance, it seamlessly blends innovation with Fujifilm’s signature craftsmanship. One of its standout features is the new aspect ratio dial, delivering an analogue-inspired experience that allows users to fine-tune their framing with ease. The GFX100RF also offers carefully curated shooting formats, which allow photographers to bring their creative vision to life with precision. RRP $9,999 from leading camera retailers.

Pink as a posy

Posy – Pink Gin from Hastings Distillers is a playful floral blend combining the freshness of citrus and raspberries with sweet, spicy notes. The gin is batch distilled in its 150L Arnold Holstein still and cut to strength with Kaweka spring water. The gin has top notes of raspberry, citrus and juniper, with flowering lemon myrtle; lavender and lime bring lifted citrus and floral notes. Added after distillation, organic raspberries and hibiscus flowers give Posy a delicate pink hue and subtle sweetness. Serve long with tonic or soda. $80 from hastingsdistillers.com

London calling

Power trio

Skinsmiths has just dropped a new skincare trio powered by biotech-fermented vitamin B12 and antioxidant-rich SauvigNZ – an extract from Marlborough sauvignon blanc grapes. The range is all about calming, hydrating, and restoring stressed-out skin – perfect for winter barrier support. The range includes:

• B12 Multi-Cleanser, RRP $65

• B12 Hydra-Cream Mask, RRP $124

• B12 Ceramide Cream, RRP $90

Each formula is designed to soothe and strengthen, with SauvigNZ clinically proven to protect against environmental stress and support collagen production. Available at Caci Clinic Stores nationwide, or skinsmiths.com

Jo Malones London’s English Pear and Freesia is a scent that opens with the juicy freshness of ripe pear, wrapped in the soft floral of white freesia. Add a touch of patchouli for warmth and depth, and you have a perfectly balanced blend of fruit and florals. The fragrance is light, elegant and effortlessly wearable – a modern classic with timeless charm. 100ml is $282.

Resene Scoria

Resene Tarzan

Resene Yogi

Resene Seaweed

Resene Time Traveller

Business

biz-nəs

“a commercial or sometimes an industrial enterprise”

Merriam Webster dictionary

“Business opportunities are like buses, there’s always another one coming”

– Richard Branson

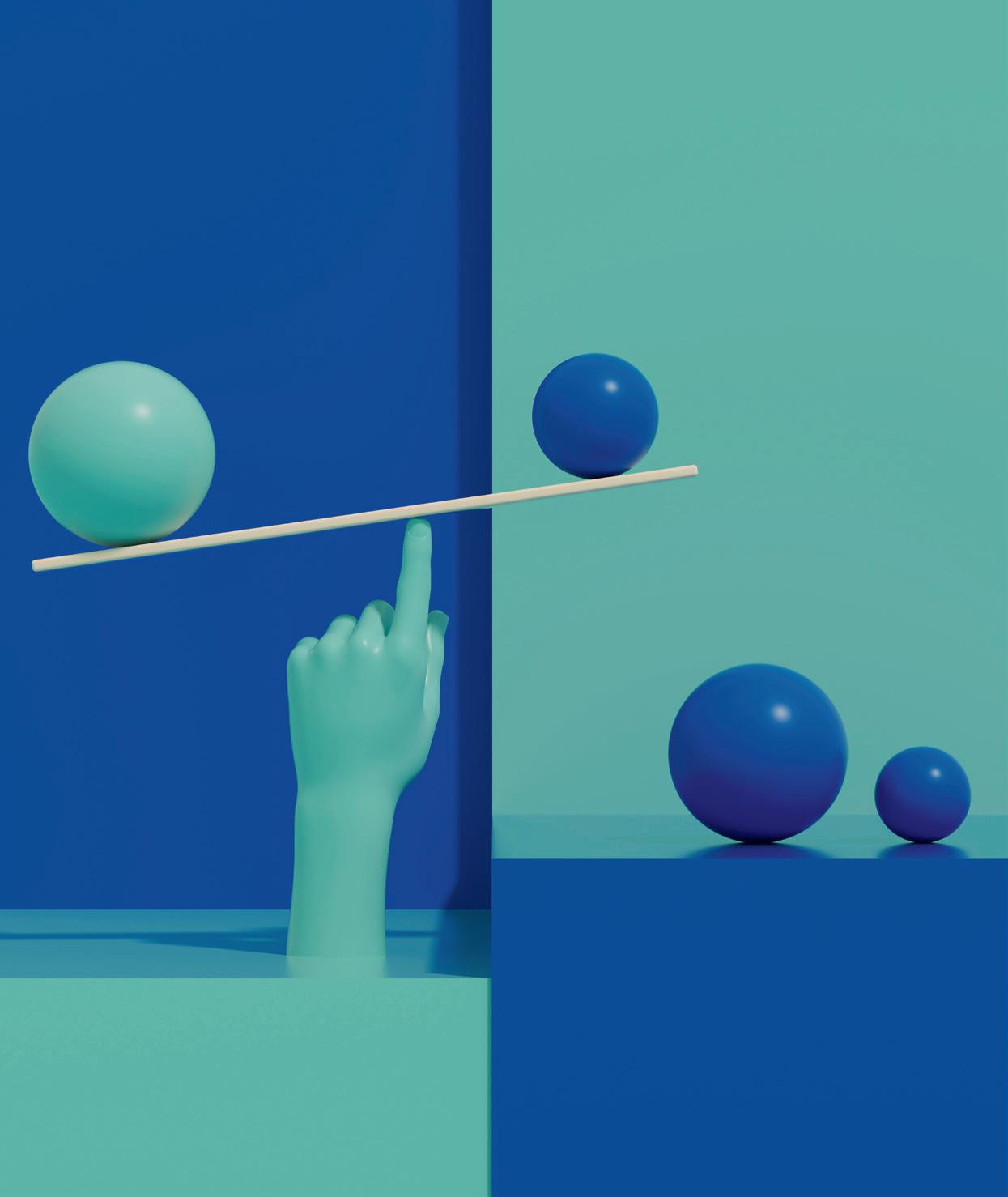

New investor in a new world (order)

We are in a ‘hinge’ moment, living through a major regime shift, says economist Shamubeel Eaqub. Old ways of investing, especially using the rules of thumb learned over recent decades, may no longer work.

THE NEXT GENERATION of successful investors will likely look very different to what we see today. They will have to grapple with a complete rewiring of the global economy. Investment is fundamentally a bet on rising economic prosperity and managing uncertainties. For active investors, this also means betting on specific sectors and/or businesses – a tough ask in the face of increasing uncertainty.

Return of history

The peace-driven global order established after the world wars – which has defined geopolitics, trade, economics and investing – is ending. The last 80 years of this regime was led and held together by the USA, who are now walking away from it under the Trump administration. This administration is also actively undermining the very beliefs that underpinned it (closer cooperation and shared prosperity), and the institutions that enforced the regime.

The new order, what it will look like –

and if any one country or one group of countries will dominate –is very uncertain. The last 80 years was an aberration, not the norm, and investors need to plan for a return of less recent history.

This means adopting a more zero-sum mentality where one nation’s prosperity is believed to sap another, even though theory and experience shows that should not be the case.

This “us vs them” mentality is leading to a more nationalist and imperialist approach to national and international policy in many countries, and a lack of coordination and coherence in how policy is made around the world. This is what matters the most – a shift in fundamental norms.

Old grievances

The new zero-sum mentality has not emerged in a vacuum. The experience of the last 80 years shows many benefits, especially in the education, urbanisation and industrialisation of many poorer nations that are enabled by globalisation.

‘The last 80 years was an aberration, not the norm, and investors need to plan for a return of less recent history’

It’s progress that has lifted billions of people out of poverty. The sheer breadth and scale of increased economic prosperity is unprecedented. But it has come with two key costs.

First, climate change – which is not the focus of this article, but an issue that investors will need to grapple with.

Second, the same forces that lifted billions out of poverty around the world did not improve inequality and poverty within richer countries.

While inequality between countries diminished, inequality within countries became entrenched … or worsened. If improving economic standards leave too many people behind, then their grievances against the current economic system are understandable and perhaps justified.

These are old grievances, renewed.

The experience of inequality within advanced economies follows a similar pattern. After WWII, inequality fell sharply with the widespread adoption of the welfare state and remained low until the 1970s. Then the neoliberal reforms of the 1970s and 1980s increased inequality – the hope was that after an initial increase, renewed economic dynamism would reduce inequality.

Unfortunately, inequality just became entrenched or rose.

Much of this inequality had a weird quality: many things became easier and cheaper (think phones, entertainment, fast food), but many of the basics became more expensive or rationed (think housing, health and fresh food).

The frivolities of life are now much more affordable, but the basics of life and dignity are not. For those less fortunate, this erodes peoples’ satisfaction with life, their trust in each other, their community and their institutions (like courts, politicians, and democracy).

It’s a breakdown of social cohesion that moves us towards polarisation.

New Zealand is not immune. While not as polarised as the USA, recent comparison with Australia (in the Helen Clark Foundation Social Cohesion report) showed we are less cohesive than in Australia. The biggest fracturing is explained by the rich-poor divide, as well as political alliances, ethnicity and age. The more entrenched inequality and poverty become, the bigger the risks to the foundations of national economic prosperity.

‘The frivolities of life are now much more affordable, but the basics of life and dignity are not’

Political events

The current polarisation in politics around the world can seem sudden, but is actually a slow rot that has been spreading for decades.

In the USA, polarisation of political views has been hardening for around two decades. The current tariff wars and attacks on American institutions by the Trump administration is a crystallisation of these long-running forces. It reflects other expressions of similar discontent, such as Brexit in 2020 and the current rise of the far right in Europe.

For investors, it is about understanding and adapting to immediate investment consequences of policy changes like tariffs.

It’s also a general step shift upwards of uncertainty and risk, because politics has become polarised. This leads to more frequent changes in governments, rapid implementation (and reversal) of unorthodox and less credible policies, institutions under attack to do the bidding of the government of the day, increasing civil and global conflict, ongoing fiscal pressures and a desperate lift in defence spending.

Keys to prosperity

What describes economic prosperity? Capital, labour and technology. These are the proximate drivers; that is, they describe and drive economic growth but do not explain why. So, what causes economic prosperity? Culture, institutions, geography and luck. Luck can’t be managed, but the others can.

Today we are observing a rejection of the previously seen closer economic and defence cooperation between countries. A large group of these countries had been reshaping geography, becoming the dominant geopolitical norm of the last 80 years.

‘The more entrenched inequality and poverty become, the bigger the risks to the foundations of national economic prosperity’

This rejection is happening because of fraying social cohesion in many countries, which reflects changing culture in these nations. The resulting upheavals are changing the institutions who have upheld previous norms.

The future: uneven and unpredictable

It seems the three fundamental drivers of prosperity are less assured: geography, culture and institutions. The future need not be bleak, but progress from here is likely to be less predictable and more uneven.

For investors, this matters. The risks

that were moderated in the last 80 years, will return with a vengeance, which means understanding new risks.

Importantly, there may be wild gyrations depending on political climate in and between countries, meaning the need to either be more aware and nimbler, or more disciplined at staying calm and investing with a long-term perspective. The critical qualities for investors in this environment will be humility and curiosity. T

Shamubeel Eaqub is chief economist and head of policy at Simplicity, and a thought leader who is unafraid to take a contrarian view.

Informed Investor is New Zealand’s only dedicated investment magazine. Every quarter we dive deeply into the world of investing, economics, ethical investment, small business, world events and property – with a dash of fashion, luxury goods and cars thrown in for good measure. Subscribe today and receive the spring issue, released in early September, straight to you letterbox.

1

2

(8

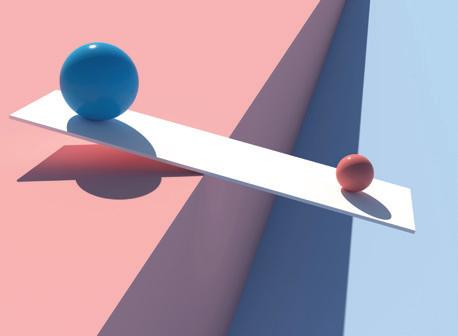

Are tariffs really so bad?

Support of free trade has been called ‘the economists’ creed’. As Trump champions tariffs, Andrew Kenningham explains why economists tend to universally reject them.

ECONOMISTS TEND TO disagree on pretty much everything. Often called the dismal science for its gloomy outlook on the world, the discipline could just as well be called the argumentative science.

But there is one area on which economists are unusually aligned: trade policy. Indeed, the Nobel Prize winner and New York Times columnist Paul Krugman once joked that if there were an economists’ creed it would end: “I believe in free trade”.

The re-election of President Trump has brought the issue of tariffs back to centre stage.

So – the most beautiful word in the English language, according to President Trump, or a scourge on prosperity, as suggested by economists?

What is a tariff?

A tariff is a tax on trade. So, it has the unhappy effect of shifting production towards less efficient locations. As an illustration, suppose Iceland imposed a tariff on tropical fruits, it could possibly grow mangoes and pineapples in greenhouses. But that would plainly be less efficient than importing them from abroad.

But what about manufactured goods and services, which can be produced in any climate? The same logic applies. Certain areas of the world have fostered particular skills, such as textile workers in Vietnam or machine engineers in Germany. It’s better to take advantage of these learned specialisms.

Even if a country is more efficient at producing every single product it consumes, economics suggests it would be better off to specialise in those goods at which it is “relatively more efficient”. All countries will be better off if they specialise and trade – this is a theory known as comparative advantage.

It’s similar to professions. We could be

a jack-of-all-trades, but it makes sense to specialise. When I learnt economics back in the 1980s, the textbook suggested that even if an author is faster at typing than her secretary, she should still focus on her writing and pass it to the secretary to type it up.

How tariffs harm growth

For those still not convinced, what about the impact of tariffs on economic growth?

By hampering foreign competitors with taxes, tariffs allow inefficient or out-ofdate companies to survive. In former communist East Germany, factories made basic consumer goods but survived. As soon as reunification took place they had to close because West Germany products were far superior.

What’s more, international companies learn from each other, and competition raises the bar for everyone. So, in this way, too, tariffs stifle the economy.

But at this point, I should concede that there are some arguments in favour of tariffs.

Perhaps the oldest defence of tariffs is the so-called “infant industry” argument. This is the idea that firms need protection when they’re starting out. The theory behind this view is a bit hazy but some countries – including the US in the 19th century – saw industries develop behind protectionist taxes.

Tariffs have also been justified for the opposite reason – to support declining or “sunset” industries. The idea is to allow an economy and society time to adjust when an industry is in terminal decline – like coal or steel in western countries these days.

Another justification for tariffs is as a defence against foreign firms if they threaten to undercut domestic business with very low prices – a practice is known as predatory pricing. Tariffs to prevent this happening are called anti-dumping duties. For example, the European Union imposed tariffs on Chinese solar panels after finding that Chinese companies were selling them below their cost of production in Europe.

‘Ironically, this tariff made things worse, hastening a collapse in exports and production, and the rise in unemployment’

Foreign policy considerations are also used to justify tariffs. The US aims to be less dependent on China for anything from semiconductor chips to rare earths used in EV batteries and personal protective equipment such as medical masks. High tariffs are one means of reducing those imports.

Also, governments may choose to pay a price in material terms to protect a way of life that they value. Farmers often argue that they need protection to preserve the countryside. Many small farms in Europe and Japan survive only because of tariffs.

It would be cheaper for British consumers to import all their lamb from New Zealand, where the conditions for sheep farming are much better. But many Brits want sheep on the Welsh hills for aesthetic or sentimental reasons.

An archaic tax

Before reaching a conclusion, it’s worth taking a quick look at history.

Tariffs have been around for millennia because they are a relatively easy tax to collect.

and objected to tariffs because they kept food prices high to support the landed gentry. The urban middle classes also wanted foreign markets to sell to. So, in 1846 the British parliament abolished the Corn Laws that kept tariffs high.

Around that time the first modern economists – like Adam Smith and David Ricardo – developed key economic theories demonstrating that free trade is the most efficient system. Before long, the British government was promoting the idea of free trade and pushing other governments to remove their trade barriers. And in due course, export markets were opened up for British manufacturers.

The inter-war period saw a resurgence of tariffs around the world due to nationalism and economic insecurity. The most infamous example is the SmoothHawley tariff that was passed by the US Congress in 1930.

Ironically, this tariff made things worse, hastening a collapse in exports and production, and the rise in unemployment.

After the end of the World War II, countries dismantled their tariffs. Following a flurry of trade deals, the World Trade Organization was eventually established with the aim to keep trade as free and easy as humanly possible. When China finally joined the WTO in 2001, trade rose exponentially – as did global GDP.

And that pretty much brings us up to date and the latest swing of the pendulum back towards protectionism.

The verdict

So, let’s take stock.

Most of the arguments in defence of tariffs are not really economic arguments – they’re more to do with politics.

But even if you think the political objectives of protectionism are valuable, there are often other ways to achieve them. A direct subsidy for farmers would be more transparent and less costly for the economy than a tariff, for instance.

And tariffs may be justified if a foreign government sets very low tax rates to attract business. Ireland, for instance, has set a very low corporate tax rate and enticed US pharmaceutical firms to manufacture drugs like Viagra and Botox. President Trump is perhaps right to argue that more of that tax should be paid in the US.

The earliest recorded tariffs were in Mesopotamia in around 2000 BC while the Egyptians, Greeks and Romans also used them. And the very first act of the US Congress in 1789 was to introduce a tariff in the Hamilton Act – named for a character you may well be familiar with.

But after the industrial revolution things began to change in England. The urban industrial class was getting stronger

Ultimately, tariffs are widely disliked by economists for very good reasons. The current “trade war” risks substantially dampening growth in some countries – notably the US, Mexico and China – although President Trump’s recent decisions to row back on previous tariff announcements suggests that we can hope a global recession will be avoided.

So, true to my economists’ creed, I think the balance of arguments is strongly in favour of free trade. T

Tariffs, challenges and opportunities

Oliver Mander, CEO of NZ Shareholders’ Association, looks at the effect Trump’s tariff may have on Kiwi investors.

THE LATEST ANNOUNCEMENT came on Saturday May 24, NZ time.

“Trump threatens 50 per cent EU tariff as talks hit wall” screamed the Fox News headline, quickly echoed on all major news networks in the US and around the world.

It’s the latest in a blizzard of announcements from President Trump in his second term, all creating a deep sense of uncertainty for investors and disruption across investment markets.

Of course, it wasn’t the “latest” announcement. That actually came late yesterday (May 25) as Trump announced a reprieve, to allow time for further negotiations.

Trump’s tariff rollercoaster

Trump’s tariff playlist is a bit like a tour of my personal Spotify account – eclectic, random and difficult to keep track of. But just like any good music playlist, there is a common theme to it all – Trump has believed in the value of interventionist

economics, in the form of tariffs, for a long time. In fact, US trade actions implemented during his first term as president (20172021) acted as a clear warning of his likely actions during his second term.

In late January 2018, Trump slapped duties on large residential washing machines and on imported solar panels.

Just over a month later (March), steel and aluminium were hit with 25 per cent and 10 cent tariffs respectively, with a later announcement of a detailed probe into China’s trade practices.

By June 2018, this had led to a 25 per cent duty on US$50 billion of Chinese goods, later increased to an additional 10 per cent spanning US$200 billion.

During 2019, Trump’s focus swung back to Canada and Mexico – with the threat of a 5 per cent tariff. This was never implemented, in favour of a security investigation into the supply of car parts.

While this was an interesting backdrop for New Zealand investors, our lack

of exposure to those tariffs mean that they never captured the imagination of local investors. Nonetheless, the moves offered a directional signal for the global economy – reflecting increasing policy shifts to protectionism and even economic isolationism, bucking the prevailing economic wisdom of the last 40-odd years.

Fast-forward to 2025

Three months after his election, Trump made his intentions plain.

On February 10, 2025, steel and aluminium tariffs were re-imposed at a flat 25 per cent on all countries—no more exemptions. This was a mere appetiser to the main course, however, with “Liberation Day” on April 2 unveiling a 10 per cent universal tariff on virtually everything across all countries and territories around the world, plus bespoke “reciprocal rates” for some 60 trading partners.

Sadly, these “reciprocal rates” appear to have been based on some unusual calculations.

Rather than tariff rates, the objects of Trump’s ire appeared to be those nations who operated a trade surplus with the US.

This is significant for New Zealand; our little nation recorded a $7.8 billion trade surplus with the United States in the year to April 2025, including a record monthly surplus of $1.4 billion in April itself.

As consumers, we make similar decisions. I maintain a significant trade deficit with my dentist; given his capability at dentistry compared with my own, it’s a trade imbalance I am happy to encourage. There is no “tariff” levied by my dentist, other than the cost of his time and materials.

However, there is GST. Fair enough – at a macro level, it diversifies New Zealand’s tax base away from a sole reliance on income tax and also means that those who spend more, pay more. The benefits of different forms of tax are indeed a whole different conversation.

Unless you are President Trump. His view appears to hold out that New Zealand’s GST is indeed a “tariff” unfairly levied on US companies.

Tariffs crank up

Shortly after “Liberation Day”, Trump cranked up China-specific duties to 145 per cent in response to Beijing’s countermeasures. On May 12, Trump removed all “reciprocal rates” for the next 90 days.

While offering a short-term reprieve, eventual outcomes will be dependent on what can be negotiated by August 12.

New Zealand has unashamedly embraced the core tenets of economic liberalism since the mid 1980s.

While controversial at the time, the reforms started by the fourth Labour

government, and followed by subsequent governments, formed a core foundation for our economy in the decades that followed.

Free-market principles mean that New Zealand imports products that it cannot produce efficiently – most products are imported duty-free to New Zealand. Conversely, we export the goods and services that we are really good at producing, which include primary sector goods (ie, agriculture).

A free market-led economy is now the cultural norm in New Zealand. New Zealand punched above its weight in global free-trade leadership, with a leading position in the interminable General Agreement on Tariffs and Trade (GATT) rounds that concluded in 1993.

It is telling that much of the local business commentary that has covered the events of the last 60 days has relied on anecdote and evidence dating back to the 1970s. If the world continues down a path of economic isolationism, New Zealand will be forced to reshape its own economic identity to adapt to the new reality.

Which Kiwi companies might be impacted?

From a local investor perspective, as an export-led economy, many of our companies are likely to be directly affected, either by reduced demand or increased costs.

The examples of direct impacts below are just that – examples. Investors will be looking for evidence that their management teams are minimising the impact.

Note that companies operating solely within New Zealand (or with limited US exposure) may also be indirectly affected, as companies domiciled in other countries affected by the US tariff regime compete more vigorously in other markets.

Fisher & Paykel Healthcare (NZX: FPH) With around 45 per cent of its manufacturing in Mexico (of which 60 per cent heads to the United States), FPH has warned that while FY25 profits will dodge a “material impact”, its path to a 65 per cent gross margin could be delayed by up to three years as tariffs bite into costs.

Mainfreight (NZX: MFT) In its May 2 “Trading Conditions Update”, Mainfreight noted a slowdown in forward sea-freight bookings on the Transpacific lane as customers adopt a “wait-and-see” posture until tariff talk turns to action.

Tourism Holdings (NZX: THL) THL’s April trading updates flagged uncertainty in North America’s RV market – don’t forget Canada’s tit-for-tat potential – and by midApril warned FY 2025 net profit would undershoot consensus amid a US travel

‘Rather than tariff rates, the objects of Trump’s ire appeared to be those nations who operated a trade surplus with the US’

slump and tariff headwinds, with the share price subsequently falling to near five-year lows.

Factors to consider

Capital markets are famous for valuing certainty, with relative economic stability reflected in share price valuations and investor sentiment following the global financial crisis right up until the onset of Covid-19. Things have been more volatile since then – a slew of factors including government monetary policy, increasing interest rates, inflation and lower global economic growth have made for a complex investing landscape.

Risk: The on-again, off-again nature of Trump’s proclamations on tariffs are not helping create certainty in the market.

While global markets reacted negatively to “Liberation Day” and have (mostly) recovered following Trump’s May 12 announcements, it is clear that short-term market movements are being determined by both the pace and volatility of Trump’s tariff policy.

While it’s the long-term that matters for most investors, increasing volatility in share price movements should make investors pause for thought.

Increasing volatility in share price movements is a reflection of increasing risk for asset values and operations – leading to an increase in structural risk. An investment strategy may aim to generate a defined level of long-term return for the lowest possible risk. In this situation, an investor is likely to be taking on an increase in risk, with no commensurate increase in return.

Pricing power: Tariffs imposed on goods coming into the US are paid by the consumer or the importer. For goods manufactured in NZ and exported to the US, consumers may be willing to bear a 10 per cent increase in price if a product commands strong pricing power. However, where a NZ product has to compete with many other products, the company may choose to absorb the tariff, thereby reducing its gross margins. Both scenarios have negative impacts for shareholders: if the

consumer price increases, the company may sell less, while a company taking a haircut on its margins will likely have a profitability impact. The same applies for investors in US companies – to what extent are they able to pass on tariffs to their domestic customers?

Regulatory whiplash: We’ve already seen investment markets react to Trump’s announcements. Regardless of the day-today announcements, there are a few key dates that investors should be aware of. August 12 is looming large, as the expiry of the 90-day stay of execution for the reciprocal tariffs. Keep on expecting the unexpected – and think hard about the level of risk you are prepared to accept.

Conscious decisions: Investors who have a long-term outlook may decide that the best move is to sit this out. Others will take advantage of “peak prices” in the volatility cycle to crystallise long-term gains and maintain an oversize cash position. Yet others will decide to trim their long-term allocation to US-exposed companies. All actions might be valid for different styles of investor. Whatever you do, however, make conscious decisions that make sense for your investment strategy and reflect your own risk profile.

In the short-term, navigating Trump’s tariff rollercoaster requires vigilance and agility – because in this trade war, the only thing you can count on is that nothing will stay the same for long.

Longer-term, there is nervousness surrounding global investor appetite for US-based investments.

A stable, certain and rational market environment with quality companies underpins investor confidence in any stock market. Depending on what happens later this year, it may be that investor confidence in US equities will be further shaken. T

This content contains general information only and should not be construed as financial advice. Prior to making any investment decision, you should seek professional advice from a licensed financial advice provider. To the maximum extent permitted by law, New Zealand Shareholders’ Association Inc. will not be liable (whether in tort, including negligence, or otherwise) to you or any other person for the information provided in this commentary.

Moving on up

Small New Zealand businesses often punch above their weight when it comes to international success. Joanna Mathers meets the owners of two businesses who’ve smashed boundaries and grown their ventures from the ground up.

NEW ZEALAND IS a country enamoured by DIY. And it’s not just in the home improvement sector; according to Statistics New Zealand data, of the 612,417 businesses registered here, 97 per cent are small and owner-operated.

Interestingly, 448,233 of these businesses have zero employees – they are one-person or one-family businesses, powered by number-eight-wire ingenuity and effort.

While some small businesses happily tick along – paying the bills and funding the occasional holidays – others are set to scale. It’s not hard to find Kiwi success stories in this space – Xero, Serato, or video games studio Ninja Kiwi, which sold to a Swedish company for $203 million in 2021.

Identifying a niche, perfecting your product, marketing to the right audience, and a good dollop of good luck (and timing) are key ingredients for transforming small businesses into major players.

We meet the founders of two home-grown businesses who have utilised creativity, clever marketing, and the power of the internet to exponentially scale up.

Clever Poppy

During Covid lockdowns, we had a lot of time on our hands. Stuck at home we yearned for ways to busy ourselves outside of Netflix and endless walks around the block.

Fuelled by a desire for “simpler times”, the need for distraction from monotony, and the mental health benefits of working with our hands, crafting underwent a renaissance during this time.

Shares in DIY crafting site Etsy almost

quadrupled during the pandemic. And Julie Stuart, co-owner and founder of Clever Poppy, was in the right place at the right time to capitalise on this trend.

Her embroidery-kit business has morphed from start-up to smash-hit in less than 10 years, with Covid providing the momentum for its growth.

While Julie is the creative brains behind the business, her husband Matt – a mechanical engineer by trade – has been the force behind the company’s impressive scaling.

He’s spent hundreds of hours perfecting the art of Meta advertising, and his understanding of the algorithms has launched Clever Poppy into the highly lucrative US market. So successful has this targeting been, that they sold a whopping 100,000 kits last year – the vast majority to buyers in the US.

Creative pivot

Julie has a background in commercial law but moved away from this “really dry” discipline after the birth of her two children. Auckland-based (at the time,) she became interested in DIY when she was pregnant with her first child in 2014.

“I wanted nice things for the house, so I started making them myself –upholstered headboards, other small DIY projects. I launched Clever Poppy on Instagram to share what I was doing with others,” she explains.

Her first attempt at monetising her crafty creations came in 2015, when she began selling kits for painted baskets at a local market and sharing online.

Her Instagram timing was perfect – in the middle of last decade it wasn’t proliferated with influencers, and her content stood out.

Julie Stuart created her embroidery kit business, Clever Poppy, during lockdown when she had time on her hands and the motivation to learn new skils.

members in the first membership, which quickly grew to 200-300.

Learning together

While Julie was a lover of arts and crafts as a child, she learned embroidery, punch needle and weaving through trial and error as an adult.

She was shoulder-tapped by Warehouse Stationery and 3M to create content using their products, which was very helpful for bringing in money for the family.

But embroidery, punch needle, and weaving were increasingly capturing her attention, and when Covid hit in 2020, the corporate gigs dried up, and she had the space to work out how to monetise her current passion.

“Matt suggested a membership model, in which people paid a small fee for me to teach them embroidery via video. I had 20,000 followers on Instagram at the time; I went to the audience and asked if this was something they would be interested in.”

For a fee of $10 a month, Stuart offered her followers a monthly project, access to a library of downloadable patterns (that she created herself) and all the information about what you would need for the project. They started with 170

“I had made mistakes and learned, and I could share this with others via tutorials.”

She was professional and articulate; her legal background meant she was able to distil complex information and share it with others: “basically, I could explain without waffling,” she laughs.

In the early days of Covid, she had a good solid membership with people paying their monthly fee.

Initially the supplies weren’t part of the package, but she realised that it would be great for members to have “everything they needed handed to them on a platter,” she says.

So, by November 2020, they started selling kits. Finding suppliers who had high-quality products was complex and time-consuming, but they eventually sourced (from China) all the components, which were sent to New Zealand, packed, and sent to customers.

By 2022, Matt realised that they needed to enter the US market. The joy of Meta advertising is that it can be targeted to different global markets; his investigations led to a highly effective sales strategy, which utilised Julie’s most successful videos, as the basis for targeted campaigns.

“We targeted the ads to people in the United States, and it was extremely successful,” says Matt.

Initially the orders from the States were shipped from New Zealand, which was “super expensive”.

So, they started to use a third-party logistics (3PL) operator in the US, who would receive the packs which had been kitted in New Zealand. This evolved to shipping the kits from China straight to the consumer in the US; now the USbased orders are compiled in the States and sent direct to customers.

Clever Poppy now has over 500,000 Instagram followers, and nine staff. The Stuarts have moved to their family to Kerikeri, where they both work full-time on the business.

Bump in the road

Things were going swimmingly, until

ABOVE Clever Poppy sold over 100,000 embroidery kits last year, most of them to the United States market.

RIGHT Julie and Matt Stuart.

Trump’s return to power this year.

With Trump’s tariffs policies in a state of constant flux, and China a particular target, Clever Poppy has had to be cautious and strategic about how they distribute the goods that are turned into kits in the States.

At the time of writing, there is a 30 per cent tariff on goods import from China, which is a significant increase from the pre-Trump, when tariffs hovered between the 10-20 per cent mark.

It is, however, a significant drop from the 145 per cent retaliatory tariff Trump announced on April 10 but subsequently

dropped to 30 per cent on May 12. If this is reintroduced, Julie says “we just have to think on our feet and be really adaptable.”

When asked if they ever would consider selling Clever Poppy, Julie and Matt’s answer is considered.

“We have thought about it, but as we love what we do, we would only sell for a very high figure,” Julie says.

A number in the $20-million zone has been discussed: “but it is unlikely that anyone would pay that,” says Julie.

But given the lightning-fast trajectory of their business thus far, nothing would be surprising.

‘We targeted the ads to people in the United States, and it was extremely successful’

Easy Crypto

In 2014, Bitcoin was either: a dodgy esoteric scam that existed in the digital netherworld, and best avoided; or, a presage of our digital monetary future, highly likely to handsomely reward early adopters.

Those who tended towards the latter option have been proven correct. When Bitcoin peaked at an all-time high of US$111,000 ($184,707) in late May this year, you could almost see the crypto OGs rubbing their hands with glee.

Janine Grainger, co-founder of Easy Crypto, was firmly in the latter camp. The finance and economics graduate, who started her career in banking, had a crypto epiphany that year.

In an increasingly digital world, it made a lot of sense to her – an unregulated, global currency that superseded the strictures of traditional banking.

She started researching and was soon the expert on crypto at Westpac, where she was working: “I became an overnight expert on blockchain,” she laughs. “I was asked to give talks about it to the staff.”

At the time, it was hard for cryptocurious Kiwis to get their hands on Bitcoin or any of the other cryptocurrencies on offer.

Most crypto trading platforms were located overseas and it was hard to access them. And while there were few small New Zealand-based platforms, the price was highly inflated.

“There was about a 15 per cent price difference buying in New Zealand compared to overseas. It was really unfair,” Janine shares.

Janine’s brother Alan, felt the same –and decided to do something about it.

While he worked in IT, he had no coding experience, but he saw the potential for an exchange that allowed Kiwis to trade without the headaches and, in 2017, decided to create one. Researching the appropriate coding language on Google, he created the exchange that was to become Easy Crypto in just five days.

But while he had the tech savvy, he needed someone who was able to turn the platform into a business – this person was Janine.

Soft launch

After a soft launch in 2017, Easy Crypto (named because it was intended to make buying crypto easy) was taken offline for a time so Janine could get all the regulatory ducks in a row.

“There is a misconception that crypto is completely unregulated,” says Janine.

“But any crypto exchange in New Zealand is regulated, in a general sense, by a number of acts,” she says.

“Crypto exchanges are considered financial services providers and are covered by rules around that. They need to adhere to the rules of the Anti-Money Laundering and Countering Financing of Terrorism Act (AMLCFT). And there’s the FMA Act, and the fair-trading standards, that need to be adhered to.”

Janine ensured the boxes were ticked and that Easy Crypto adhered to all the appropriate regulations before relaunching in early 2018.

Search, check out, pay

Easy Crypto instantly differentiated itself from the competition. The traditional model of a crypto exchange is clunky: funds are sent to the exchange to facilitate a trade, assets are purchased, and if a sale takes place withdrawals need to be made from the online “wallet”. The process can take days.

Easy Crypto had a different model, acting more like online shopping: search for a product, check out, and pay. And this happens in seconds.

While the model was simple, setting it up as a business was not.

Crypto was not something bankers or insurers wanted to touch; they struggled to find a bank and they weren’t allowed to advertise on places like Google or Facebook because they had “no-crypto” policies.

But even at this early stage, there were plenty of Kiwis hungry for crypto. Janine was networking like crazy, putting herself in the midst of the local crypto community.

And they liked what Easy Crypto offered: old-fashioned word-of-mouth saw the advanced digital platform record $200 million-plus in sales by 2020. Then, as with Clever Poppy, Covid saw the platform’s performance skyrocket.

Covid boom

What could have been a catastrophe ended up a boon for Easy Crypto and crypto assets in general. People were forced to work from home, and connecting online became the norm. Zoom took the place of work meetings and the world went virtual. This familiarity with digital meant people were more comfortable with crypto as a concept.

As Janine explains, 2020-2021 were massive years for Easy Crypto. The success reflected the explosion internationally: between March 2020 and October 2021, Bitcoin rose in value from just over US$6,000 to US$61,800, but it wasn’t going to last.

In 2021, Easy Crypto raised $17 million in a Series A funding, led by sovereignbacked Nuance Connected Capital. The funding round was significantly oversubscribed (by 50 per cent), with Easy Crypto having far more interest from investors than what was hoped for –and setting a new record in New Zealand, as the largest first funding round ever completed by a New Zealand firm.

It wasn’t all good news. Crypto is volatile: the “crypto winter” of 2022 saw prices plummet. Triggered by the United States inflation surge, and the sell-off of risk assets by spooked investors, crypto currencies LUNA and TerraNova collapsed, Bitcoin dropped by nearly 70 per cent, and then FTX happened.

For Janine, FTX’s collapse was “really disappointing”, but she doesn’t view the scam as related to crypto. Instead, she sees it as a Bernie Madoff-style Ponzi scheme, motivated by greed and hubris.

“But it gave the industry a bad name,” says Janine.

It was a terrible time for the business. After the exponential growth during Covid, the bottom fell out of the crypto market. They had fundraised and scaled up, then the wheels fell off – she remembers being called into a meeting by the board and being told that they had to bring the company back to cash neutral.

“We had to make half of the team redundant,” she says.

“It is something I never want to do again, but I feel I managed it with integrity.”

International reputation

But despite the hardships, Easy Crypto’s reputation was growing. In 2023, they were approached by an (unnamed) international firm with an interest in buying the company. “I started thinking, ‘is this a good time for me to look for an exit strategy’?” says Janine.

This was coinciding with a period of increasing costs, which were becoming harder to manage. And there was an awareness that if they were to partner with a larger, international firm, this could make sense.

While it took over a year to facilitate, on March 31, Easy Crypto announced that Brisbane-based exchange Swyftx had taken ownership of the company, for an undisclosed sum.

The Easy Crypto brand would be retired and the Swyftx name used.

“They are bigger than us and have similar values,” says Janine. “There is a real alignment, which they can offer to customers.”

Janine is currently still with Easy Crypto, facilitating the transfer of ownership. Once this is complete (there is no fixed ETA for this) she plans to “have a bit of downtime and pick up again next year”.

“But I really don’t know what I will be doing at this stage,” she shares.

Janine’s nutshell tips for business success are simple.

“I really believe in the power of using networks. You are only one step away from anything if you use your network, reach out and then you can pay it back.”

She says she couldn’t have done any of this without her brother Alan: “we have both struggled through hard stuff and have been through it all together”. T

‘You are only one step away from anything if you use your network, reach out and then you can pay it back’

JANINE GRAINGER

The art of luxury

Stay Luxe is creating an elegant niche in the luxury short-term accommodation space, as Joanna Mathers discovers.

WITH BACKGROUNDS IN highperformance sport, Greg Owen and Scott Unsworth are uniquely placed to understand the needs of those at the top of their field.

Greg was formerly the highperformance director at Canoe Racing New Zealand and Scott is a former a world-class triathlete and founder of internationally successful sports brand Orca.

Together, the friends have transferred their skills into an equally demanding sector, the provision of luxury accommodation.

Their business, Stay Luxe, offers discerning travellers ultra-luxe accommodation options when they are visiting New Zealand; and providing owners of the properties a means by which to monetise their mansions.

Natural progression

Greg and Scott’s journey into luxury short-term accommodation has been a natural outworking of a major renovation they’d undertaken previously.

Scott owned a block of four units on a corner site in Mission Bay, Auckland. But he was aware that residential or commercial tenancies didn’t have the power to generate the yields he was looking for: short-term holiday rentals could attract two or three times the income achieved with long-term rentals.

Scott asked Greg to help to project manage the transformation of the properties into charming coastal getaways. The four units turned into eight; targeted at the middle sector of the market, they soon started paying their way.

The returns immediately leaped from 3 to 15 per cent; the units’ amazing location, next to one of Auckland’s best-loved beaches, attracting much tourist interest.

Scott also owns a property on Takapuna Beach; this was also renovated and targeted at the upper end of the shortterm market.

In the process of converting Scott’s properties to short-term rentals, the pair became aware of a notable gap in the luxury accommodation space.

High net-worth individuals coming to Auckland didn’t have a dedicated platform on which they (or more likely their assistants) could source properties of the quality they expected.

Instead, they would need to set strict search criteria and scroll through the likes of Airbnb to find what they needed.

Scott and Greg had contacts with luxury apartments and properties in Auckland that weren’t being used – many that had been taken off the market because they weren’t selling.

So, last year, the pair decided to launch a dedicated luxury short-term accommodation website, which they called Stay Luxe.

Invest in luxury

Greg was the brains behind the Stay Luxe website and has been active in growing the business. And since its inception, the business has grown to incorporate 30 properties, mainly in Auckland, but also in Taupo and Nelson.

The properties range from $500 a night for one or two-bedroom dwellings, to $20,000 a night for penthouse apartments.

There’s the clifftop mansion with Hamptons’ style architecture, a pool and a spa, in Auckland’s East Coast Bays ($8,000 a night); and Kinloch Manor on Lake

With Stay Luxe, Scott Unsworth and Greg Owen bring luxury short-term rental management to NZ.

Taupo, located on 254 hectares of land.

Stay Luxe utilises Google Ad Words and Airbnb Luxe to market their properties: 60 per cent of the bookings they receive go directly to their site.

Accommodation scouts who source luxury properties for the rich and famous have taken notice already: “We had Pink lined up to come and stay when she was touring, but the swimming pool in the property she was looking at wasn’t ready, and her children wanted a pool, so sadly that fell through,” says Scott.

Attention to detail is key in this space. One of the most important aspects of luxury accommodation is ensuring the homes maintain an extremely high level of cleanliness.

“We have very stringent standards for

cleaning our properties,” says Scott.

“This is extremely important; when you are paying large amounts of money for short-term accommodation, everything needs to be perfect.”

Another important component of the business is creating networks with others in this space.

Scott and Greg are members The Luxury Network New Zealand, an international luxury marketing group that helps creates new business partnerships through strategic alliances, endorsements and B2B networking. It’s ideal for them and they have been able to create great connections through this platform.

Greg and Scott are very much still the early stages of the brand; they are looking to grow their portfolio of properties and further their reach into the international market.

“The majority of our guests come from the United States, so we really want to increase our visibility in that market,” says Greg. T

Sound advice for the self-employed

Martin Hawes considers the lessons he’s learned over 50 years of self-employment.

FEW IN PERSONAL finance take much account of the self-employed. Whether banks or KiwiSaver providers, articles or websites, the examples and advice that they give is on the basis of a knowable income with a similarly knowable surplus after living costs have been paid. Such assumptions do not describe the position of the self-employed.

Often the self-employed do not have the same reliable cash flow as those with salaries and are, in fact, constantly juggling so that they can pay their bills and have something left over to live on.

In difficult times like these, that juggling may be tricky as customers are slow to pay their bills and suppliers want their money sharp on time.

And yet, most of us run our businesses in the hope that we will at some point achieve financial freedom. We need to save and invest like everybody else, manage our mortgages and budget. We are just as much in need as those with salaries.

Lumpy incomes

Perhaps the biggest difference between the self employed and those who earn salaries is that the self-employed tend to have lumpy income and lumpy outgoings.

The salaried can meet their mortgage payments and buy the groceries with some confidence – the self-employed have another job, which is to manage their uncertain cash flow.

Sometimes that’s a big job! Take real estate agents as an example of the self-employed. They may make a decent income annually, but they never quite know where their next sale will come from – nor when. They may have a flutter of sales one month, but that may be it for a couple of months … or longer.

The self-employed may also have lumpy

tax to pay. Both GST and income tax requirements can come in big dollops and catch out those who do not allow for them. People who are self-employed cannot simply take each payment and spend it – they have business costs that need to be met, tax to pay, and they ought to save for the future.

Managing cash flow

I have been self-employed since I left teaching in 1977. Over that period (nearly 50 years) I have found that the easiest way to manage cash flow is to run several different bank accounts, each with its own purpose. At its most simple, these accounts may be named something like:

• My business costs

• My tax

• My living costs

• My future

Each payment I receive is split to each account at a different percentage. Each account will get a set percentage so that I know how much of each payment that I receive will go into each account.

Figuring out these percentages will take a bit of work (and possibly some help from your accountant). It may take a few goes to get the amounts right but it is well worth persevering so that you are never taken by surprise when any bill appears. The important thing is that each category is properly catered for as the money comes in.

I have run this system personally for 30 years or so and it has become almost second nature for me. My business has mostly had a small number of larger payments each month and that makes it easier. If your business has a lot of small payments (eg a retailer or in hospitality), you can easily take a week’s turnover and split your takings into the accounts accordingly.

By way of example, my own percentages and the amounts that I would put to each account if I received a $5,000 payment would be like this:

My business costs: 10 per cent $500

My tax: 35 per cent $1,750

My living costs: 45 per cent $2,250

My future: 10 per cent $500

You should note that I am starting to become a bit older and, therefore, not working or earning as much as I was. This means I have less requirement to put money aside for the future. There are three main advantages of the system.

1. You have money put aside to meet bills (including tax) when they come in. If you are struggling to meet bills, the chances are your percentages might need some adjusting.

2. Assuming these bank accounts are interest bearing, you should receive some interest income. It may not add up to a big amount, but you may as well have the interest rather than the bank.

3. You are treating your future seriously and not simply leaving it to chance. Having a bank account labelled “My future” should serve as a reminder of why you are trying to grow your wealth.

Although the “my future” category is last on this list, it is not least priority. Like everyone else, the self-employed need to be sure that they have their futures funded – after all, it is the future where you will spend the rest of your life! T

Martin Hawes is a financial author and presenter. He is not a financial adviser. To find out more, visit martinhawes.com

HR in an AI world

The HR function has changed forever — so how do small and medium businesses keep up with the pressure? Sanam Ahmadzadeh Salmani, New Zealand employment law compliance lawyer at Employment Hero, investigates.

NOT

TOO LONG ago, HR was seen as a back-office function by business owners. It was a department responsible for paying people on time, tracking annual leave and (hopefully) keeping employment contracts somewhere safe in the filing cabinet.

Fast forward to 2025, and the picture is now radically different. HR teams are now expected to lead engagement, drive culture, help plan career pathways, manage onboarding, retain top talent and navigate a maze of ever-shifting regulations – often all at once. The brief hasn’t just expanded; it’s exploded.

So how can businesses, especially small and medium-sized ones, keep up with

the pace and pressure? The answer lies in recognising that HR is no longer just about administration – it’s all about strategy. What’s more, tapping into the power of technology to streamline systems and unlock greater efficiency, insight and resilience is key.

Expanding role of HR

In this new era, HR is charged with creating environments where people can thrive. This means driving employee engagement through recognition, feedback and well-being initiatives.

It’s evolved to be about managing career trajectories, not just filling roles. Winning the war for top talent, in a global,

digital-first labour market, is increasingly important when it comes to building a competitive team.

And once you’ve hired top talent, speeding up onboarding, without compromising on culture or compliance, helps drive better business performance.

In addition, staying compliant, even as regulation becomes more dynamic and demanding, is also a central responsibility of modern HR functions.

It’s a tall order and to do all of this as the demands on HR teams increase, businesses simply can’t afford to keep relying on disconnected tools, manual processes and reactive workflows.

What’s needed is a modern operating

system – one that centralises, automates and empowers.

Put simply, in today’s environment, strategic HR is powered by smart technology and to meet rising demands and stay ahead, businesses are embracing tools that do more than just automate admin – they enable smarter, faster and more resilient HR operations.

Here are three critical tech shifts shaping how modern HR teams work and win.

Shift 1: Smart companies are centralising their HR systems

The concept of an employment operating system (eOS) is rapidly changing how businesses approach workforce management. Think of it as the “central nervous system” for all things employment – a single, cloudbased platform where everything from recruitment to payroll, performance reviews to compliance tracking, lives under one digital roof.

Instead of juggling multiple subscriptions and logins, agencies or spreadsheets, an eOS brings it all together:

• onboarding becomes seamless and consistent

• payroll syncs automatically with hours, leave and entitlements

• engagement tools like surveys and shoutouts help track morale in real time

• compliance is maintained with live updates, templated policies and alerts.

More importantly, an eOS turns scattered HR data into real-time, actionable insights and having a unified view means leaders can spot trends, address gaps and make better decisions based on data a lot faster.

When businesses consolidate their HR systems into a unified eOS, they don’t just save time; they save money as well as reduce errors and free up their people to focus on high-impact work.

Shift 2: Tech is becoming an essential tool for managing the compliance burden