Will changes to zoning rules transform our green pasture into grey suburban sprawl? $12.50

SENTIMENT SURVEY RESULTS REVEALEDpowered by Kris Pedersen Mortgages SPECIAL REPORT

Resistance to Auckland Council development contributions heats up

RENOVATION

REGULAR FEATURES

a smarter path for

Prouse on the pros and cons of new builds.

offered by countercyclical investing.

ACCOUNTANT Do you find ‘plus GST, if any’ four scary words?

From the Publisher

Onwards and outwards

Could the loosening of greenfield land restrictions be the answer to New Zealand’s housing woes?

At Property Council’s Residential Development Summit earlier in the year, housing minister Chris Bishop passionately expounded on his vision for the future of housing. This included growing outward, as well as upward.

One way to address our high cost of housing, he stated, was by creating more supply; freeing up greenfield land around our major cities.

Much of this land is classed as highly productive under the National Policy Statement for Highly Productive Land (NPS-HPL) – which protects our domestic food supply.

But in Bishop’s analysis, the lower-quality land within this scheme could be used for housing.

At the summit he announced that cabinet had decided to remove the least productive land from under the rules governing NPS-HPL – allowing developers to access the land for development.

Running adjacent to this was the announcement of $100 million in lending from government, which allowed developers to access lower-cost finance in order to put infrastructure in place.

In our lead story this issue we ask if these changes are a silver bullet for the housing market – or a road to soulless suburban sprawl.

There are some of the opinion that we have enough new builds on the outskirts – properties sitting vacant as vendors shy away from cookie-cutter housing in the middle of nowhere.

But others feel that anything that makes development of land simpler and less mired in red-tape is a good thing. We traverse the ground between these positions and try to come to a balanced conclusion.

The results of our annual investor sentiment survey are also revealed in this issue.

There are some interesting results, particularly with regard to landlords intentions for rent increases in the year ahead.

Overall, property investors are in a holding pattern – there are opportunities out there, but the unsteady job market, geopolitical concerns, and the outflow of New Zealanders to other countries is leaving many in ”wait and see” mode.

Our profile subjects this issue are not so reticent.

Scott Unsworth and Greg Owen both have a background in highperformance sports.

And they have created a portfolio based on short-term accommodation in Auckland.

They transformed an underperforming property in Mission Bay into stylish holiday accommodation that’s commanding impressive returns. It’s all about utilising skills and understanding the importance of location – it helps that Scott’s wife is a talented interior designer who understands how to create stunning spaces.

Their winning formula has been repeated in their new venture, Stay Luxe, a luxury property management company that provides extremely high-end holiday homes for the rich (and sometimes) famous.

We hope you enjoy reading this issue as much as we enjoyed creating it. Stay warm and take care.

Joanna Mathers Publisher

property

NZ PROPERTY INVESTOR

MAGAZINE PUBLISHER

Informed Media Limited PO Box 40128, Glenfield, Auckland 0747

PUBLISHERS

Joanna Mathers and Sally Fullam

EDITOR

Joanna Mathers E joanna@informedmedia.co.nz

DESIGN DIRECTOR

Sally Fullam E sally@informedmedia.co.nz

ACCOUNT MANAGER / ADVERTISING SALES

Joanna Mathers E joanna@informedmedia.co.nz M 021 250 7101

WRITER

Sally Lindsay

PROOFREADER

Síana Clifford

SUBSCRIPTIONS

Sally Fullam

Online nzpropertyinvestor.co.nz

E subs@informedmedia.co.nz

PH 022 431 9144

TO SUBSCRIBE GO TO nzpropertyinvestor.co.nz/subscribe

NZ Property Investor has been printed on accredited and fully recyclable paper sourced from sustainably managed and legally harvested forests.

NZ Property Investor sources expert advice on a range of specialist topics. We recommend you get your own independent advice before you take any action, and any action you take is strictly at your own risk. Opinions expressed by contributors are not necessarily those of NZ Property investor or Informed Media Ltd. Informed Media is not liable for any loss or damage (included but not limited to indirect or consequential loss) or for personal injury arising from any action taken.

NZ Property Investor is published by Informed Media Limited. The contents are copyright and may not be reproduced without the consent of the Editor. All rights reserved.

PROUDLY PRINTED BY Webstar, New Zealand

MEET some of our contributors

Mark Withers

Mark Withers and his team specialise in advising on propertyrelated transactions, valuation and restructure services, and tax planning.

Debbie Roberts

Debbie Roberts is a financial adviser with 25-plus years’ property investment experience. She co-founded Property Apprentice in 2010 with her husband Paul to help others achieve financial freedom through property investment.

Shadi Salehpour

Shadi is the owner of Let’s Rent, an award-winning property management company in Auckland known for its personalised approach and commitment to excellence. With a passion for fostering strong relationships between landlords and tenants, Shadi has built a reputation for integrity, innovation, and professionalism in the industry.

Sarina Gibbon

Sarina is an independent tenancy consultant, industry advocate and established media commentator. Her clients include the Auckland Property Investors Association, Renti and several property management organisations.

Matt Ball

Matt Ball is PR and advocacy manager for the New Zealand Property Investors Federation. Matt has decades of experience in PR and politics, is a property investor and has been a renter. These experiences help him represent and advocate for property investors and push for policy changes that benefit the whole industry.

Simon O’Connor

Simon is managing director of Sentinel Planning and has more than 20 years town-planning experience in the public and private sectors. He has significant Auckland-wide and international experience as a principal planner at Auckland Council and its predecessors in the policy and regulatory divisions.

Eve Prouse

Eve Prouse is a trusted property valuer and respected media commentator specialising in Auckland property markets - in particular South Auckland. Of Pacific heritage, Eve brings a unique, communityrooted perspective to her work.

David Faulkner

David is the general manager of property management for Property Brokers and is recognised as one of the leading experts in the New Zealand property management industry. He has been involved in the industry developing robust policies and procedures, training, and consultation services for many years.

Matthew Gilligan

Matthew Gilligan is a property investor, developer and tax adviser. He is managing director of chartered accounting firm Gilligan Rowe & Associates, where he heads the specialist property and asset planning divisions.

Leonie Freeman

Leonie Freeman is the chief executive of Property Council New Zealand. She has extensive experience in the property industry, having held top positions in both the public and private sector. From creating the concept of what is now realestate.co.nz, to buying and transforming her own residential property management business, she is a leading light in the industry.

Kris Pedersen

Kris Pedersen of Kris Pedersen Mortgages is a commentator on property and finance. His team sources top finance strategies.

Rachel Radford

Rachel Radford is the marketing lead for builderscrack.co.nz, New Zealand’s largest home improvement platform that connects homeowners with tradespeople. Her journalism background, combined with the platform’s comprehensive industry data, provides unique perspectives on nationwide property repairs and renovations.

Developers set for legal challenge against Auckland Council

Developers are poised to take legal action against Auckland Council over its proposed eye-watering hike in development contributions, particularly for greenfield projects, writes Sally Lindsay .

Developers are poised to take a judicial review against Auckland Council over its proposed eye-watering hike of up to 400 per cent in development contributions (DC) .

Under the council’s Draft Contribution Policy, released late last year, projects that would cost $30 million today are inflated to a 30-year price of $250 million and developers will be paying these charges on all new consents from next month.

Last year the average Auckland development contribution (DC) was about $50,000. Over the next decade, the council is aiming to invest $93.3 billion in infrastructure related to growth. To fund this and extend estimates for 30 years’ of infrastructure, the council is proposing to lift DCs from $20,000 to $50,000 per lot or household equivalent unit (HUE). Investment priority areas including Tamaki, Mt Roskill and parts of central Auckland, could see DCs rise as high as $119,000 per lot or HUE.

Subdivision Advocacy NZ (SANZ) spokeswoman Kirsty Merriman is leading a campaign with prominent property accountant Matthew Gilligan of GRA (Gilligan Rowe & Associates) to get the council to re-examine its modelling for the DCs.

Preliminary advice obtained by SANZ, from barrister Andrew Barker KC, backs up its claims the proposed DC charges could be illegal. He noted the financial modelling errors aren’t policy decisions, but factual errors that render the DC increases unreasonable.

Barker says calculating DCs based on nominal future infrastructure costs without accounting for the difference between the date of payment today and the date the cost is incurred, 30 years or more later, is a “reviewable error of law or an unreasonable decision by the council”.

Auckland Council financial strategy general manager Michael Burns says while staff are looking at issues with the contribution policy brought up in submissions to

the draft plan, it disagrees with SANZ and Barker’s assessment.

“The draft policy and modelling is a robust large piece of policy work and has been subject to external technical and legal review,” he says. It also doesn’t agree there is any error of law in the policy.

“If the council does not make and implement changes, SANZ will launch a judicial review,” Merriman says.

The lobby group says the key problems with the contribution policy include failure to discount future revenue to present value-inflating costs, excessive project add-ons and contingencies, such as traffic management at 13 per cent or 20 per cent, and contingencies of 50-70 per cent, when the industry standard is 10-20 per cent, and unrealistic housing growth forecasts.

Two of the biggest areas of concern are the over-estimation of contingencies and the escalation of costs without the discounting or opposite treatment of the revenue stream, Merriman says.

Under section 111 of the Local Government Act, the council is required to follow generally accepted accounting practices and the treatment of costs and revenue must be the same.

“It clearly and most obviously is not

doing so. The council’s procurement system is broken. It is not pricing work correctly. It is spending multiples more than the private sector because staff are estimating, and using expensive estimates at that.

“By the time those costs have been escalated into the future, they become a gross, egregious, nasty cost.

“It doesn’t only affect developers but ratepayers and tax-payers also,” Merriman says.

For example, a Mangere footpath renewal is 85 per cent ratepayer funded. Along with higher-thanprivate-sector overheads, a 70 per cent contingency is applied, it is delayed for 10 years, the capital expenditure is inflated, and the original $66 million dollar project turns into a $265 million dollar development, she says.

A more horrendous calculation error showed up in official information Merriman applied for on an $800 million Tamaki greenfield scale stormwater project covering Point England, Glen Innes and Panmure.

In meetings, council staff presented an alternative private $2 billion solution.

Merriman pointed out to council staff they had double-counted the project’s ground coverage and that brought the cost back to $1 billion. A cost approach for the supply and

‘By far the biggest effect of the increases will be on affordable houses as DCs make up the bigger portion of their costs’

installation of materials for the project had also been applied at five times the value a private developer would pay and the remaining $1 billion was trimmed back to $200 million.

“I was heard, a confidential meeting was held, and council staff have now gone back to the drawing board to fix the mistakes.

“Asking developers to pay today the costs of 20, 30, 55 years inflated is not reasonable. The law is clear – you can’t do that.”

Another housing crisis looming

By far the biggest effect of the increases will be on affordable houses as DCs make up the bigger portion of their costs, SANZ says.

In its contribution policy, the council claims the DCs will have no impact on house prices. In a surprising statement it says high DCs do not influence

housing costs because developers do not pass these fees onto buyers; instead, the market determines prices.

An incredulous Gilligan says this is “nonsense” dished up by the council’s favoured economic advisers.

“Of the nine economic reports on DCs, six did not agree with this assertion. The council only referenced the three that agreed in its study on the issue. And in 2013 the council received advice from the Internal Affairs Department, clearly saying development contributions do affect houses prices.”

The relationship between DCs and housing prices is fundamentally tied to economic principles of viability, supply, and demand.

Gilligan says the council is cherrypicking economic advice and analysis to justify increased DCs, which are a taxation on developers and home builders, and is boosting policies that

Special Report

will contribute to the next housing crisis. “A significant increase in DCs directly impacts project feasibility by eroding developers’ profit margins. As a result, supply diminishes. Developers halt construction and landbank their assets, waiting for more favourable conditions.”

He says in short, supply crashes, and demand continues to build. Values get pushed up as a result, and it’s not until house prices increase that construction becomes viable, and so the end purchaser pays the higher DCs through resulting house price inflation.

Unclear approach

In his advice to SANZ, Barker says it appears the council has used contingency and growth figures, land acquisition costs, projected dates for infrastructure development and the like in its calculations, which are not supported by industry practice or the council’s practice in other areas.

“It is unclear why the council has taken the approach of maximising the amount of DCs to be paid by current developers.

“If it is to achieve a purpose other than a fair and equitable contribution to infrastructure costs, then it would be exercising its powers for an improper purpose and the policy would be subject to review on this ground also.”

Barker’s advice also points out the council’s growth projections appear to have been manipulated to shift the burden to greenfield developments.

Merriman says an important note in his advice is the policy appears to be aimed at creating a generous and immediate revenue stream that the council can apply as it likes.

‘A significant increase in DCs directly impacts project feasibility by eroding developers’ profit margins. As a result, supply diminishes. Developers halt construction and landbank their assets, waiting for more favourable conditions’

System needs disassembling

While SANZ is not opposed to DCs and sees them as necessary to pay for infrastructure, Merriman says increases need to be honest, not inflated estimates.

She says they should stay at the existing level until the government’s new system of levies kicks in, or a commissioner can review the system to make sure the council’s funding models and allocations are fair.

“The whole system for growth contributions and infrastructure needs to be disassembled and put back together with an open and transparent procurement team.

“DC costs could fall if council procurement was better. Maybe it could be made private, managed or quoted at the time to get a far more accurate figure.”

Burns says the council has undertaken a thorough consultation process on the Development Contributions Policy, as a complex but significant piece of policy that affects Aucklanders.

enables. In large-scale development areas, such as Drury, Tamaki or Whenuapai, often the infrastructure will take decades to complete.

“The policy ensures the cost of new infrastructure is fairly shared between developers and ratepayers. Without this policy, ratepayers would cover the full cost of growthrelated infrastructure.”

Dividing the total cost by the total development gives the development contribution charge, Burns says.

The majority of councils in New Zealand set this as a simple flat charge, but there is an option to have indexed or annually increasing pricing.

“A number of submissions on the draft policy raised the pricing approach, which staff have considered and will provide advice on options to the governing body, including indexed or annually increasing pricing,” he says.

Keep track of arrears, repairs, inspections, owners

“Staff are also focusing in particular on some changes to underlying financials; options for infrastructure investment; and flat vs indexed pricing.”

Create tenancy agreements

A development contributions scheme looks at the total cost of growth infrastructure and allocates that cost across the total development that it

Mobile companion apps

Changes have already been made to the draft policy and it was debated and voted on by the council’s governing policy at the end of last month. The new policy will come into effect this month. ■

Automatic bank feeds

• Keep track of arrears, repairs, inspections, owners • Create tenancy agreements • Mobile companion apps • Automatic bank feeds • From just $8.50 per month

From just $8.50 per month

CHARTERED ACCOUNTANTS SPECIALISING IN PROPERTY, TAX AND TRUSTS

Gilligan Rowe & Associates LP (GRA) is a chartered accounting practice that offers clients a full range of taxation and compliance accounting services coupled with specialist property, trust and asset planning advice. As well as completing accounting for individuals, businesses and property investors, GRA provide clients with knowledge through their educational programmes. Over the years we have helped thousands of clients increase their wealth through property investment, maximise their asset protection and minimise their tax liabilities. We are recognised as leading experts in our fields and are committed to helping our clients succeed. To that end we offer a range of services.

TAX AND LEGAL STRUCTURES

Getting your structures set up correctly from the beginning is important. We adopt a holistic approach, with a focus on both asset protection and legally reducing tax.

• Asset planning – asset protection, forming companies and trusts

• Tax advisory – tax optimisation

• Tax lawyers on staff

• Trust specialists and professional trustee services

• Assistance with IRD – litigation, audits, investigations

• Clients deal directly with their Client Services Manager (senior chartered accountant)

• Fixed fee so no surprise bills

PROPERTY

/ EDUCATION / WEALTH CREATION

Helping our clients succeed.

• Property Investment and Education webinars – free to watch online

• Property School – 7-module comprehensive online course in property investment, from the basics through to more advanced strategies

• Property Development School – how to develop residential property and make a margin worth the time, effort and risk involved; ��-topic online course

• Property portfolio planning and consultation

• GRA Wealth Suite – financial self-analysis and property due diligence software

• Webinars – free webinars on property, tax and related topics

• Blogs

• Facebook – regular updates and market commentary

• Books written by the GRA directors

• Network of suppliers available to clients

• Well-connected with all major banks and finance brokers

What’s happening in the market

Sally Lindsay explores the drivers influencing property in Aotearoa.

Property

values fall as winter beckons

The average asking price for houses available for sale in April on Trade Me dropped to $855,150. Trade Me’s Property Price Index shows this was down 0.8 per cent compared to March, and down 2.6 per cent from the same month last year. Auckland fell 1 per cent compared with March – the biggest month-on-month decline in eight months. The average asking price was $1,046,900. Year-on-year, prices in Auckland

are down 3.2 per cent. The biggest decline was on the South Island’s West Coast where the average asking price in April fell 7.4 per cent from March. Otago went against the trend and posted a gain of 0.6 per cent compared to March. The total number of listings on Trade Me Property at the end of April was down four per cent from March, while use of the website by potential buyers declined by 13 per cent. Website realestate.co.nz shows the national average asking price on its

platform in April sank to $851,746, down from $884,995 in February – a drop of $33,249, or 3.8 per cent. In the main centres, asking prices declined in Auckland by $46,035, Wellington by $40,066, Canterbury by $16,347 and Otago by $50,128, exacerbated by the huge number of properties on the market. This has more than doubled over the past four years, rising steadily from 15,838 in April 2021 to 35,924 in April 2025. ■

Values lift but caution remains

Property analytics company

Cotality’s (formerly CoreLogic) data shows the national median dwelling value increased by 0.3 per cent in April to $819,096. In data terms it means values are up 0.87 per cent in the three months to April, but down 2.02 per cent compared to April last year. Queenstown-Lakes remains the most expensive district in the country with a median value of $1,658,111, although values have declined monthly by 0.95 per cent and quarterly by 1.46 per cent. Auckland’s North Shore is the next most expensive district with a median value of $1,313,091, up 0.41 per cent for the month. At the other end of the scale, the most affordable districts were Ruapehu in the central North Island at $381,483 and Buller on the West Coast at $382,837. These are the only districts where median values are below $400,000. Cotality New Zealand chief property economist Kelvin Davidson says another boom in property values is unlikely. The stock of listings remains high and as interest rates for internal serviceability tests at the banks fall to less than seven per cent, caps on debt-to-income ratios for mortgage lending are becoming a bigger consideration for more borrowers. ■

Migration gain tumbles

A record high of 123,256 people left the country in the year to March. This was up from 106,689 in the year to March 2024 and 97,584 in the March 2023 year. This, and fewer people coming here, led to a big fall in migration, with a net population gain of only 26,351 over the year. That is down 74,024, or 74 per cent, from a net gain of 100,375 in the 12 months to March last year. An estimated 149,607 people arrived on a long-term basis in the 12 months to March this year. That’s down from 207,064 a year ago. ■

New home consents rise out of the doldrums

The slump in building consents might have bottomed out. Stats NZ data shows consents for new houses throughout the country rose 15.9 per cent from March last year to 3,398 in March this year. It was the highest number of new homes consented in any month of the year since June 2023. In the March year, 34,062 new houses were consented, down 3.3 per cent compared to the previous 12 months, following a 24.9 per cent decline the previous year. There was a surge in new apartments, with 495 consented, up 121 per cent compared to March last year, while townhouses and home units were also strong with 1,452 consented during the month, up 12 per cent on the previous year. Stand-alone house consents also blipped up, with 1,374 stamped, up 9.8 per cent compared to March last year. The total construction value of the new dwellings consented was $1.41 billion. That’s up 7.9 per cent compared to March last year, another positive indicator. Meanwhile Auckland Council figures show the council issued 899 code compliance certificates (CCCs) for new dwellings in February – the lowest month for a February month since 2020. That’s down from 1,291 or 30.4 per cent in January, and down from 1583, or 43.2 per cent in February last year. On an annual basis, the number of new homes completed in Auckland has declined from a peak of 19,560 in the 12 months to May last year, to 16,811 in the 12 months to February this year. That’s a drop of 14.1 per cent. ■

High levels of listings not helping the market

Sales volumes for Barfoot & Thompson during April were at a four-year high while prices were in decline and total stock levels hit a 17-year high. Auckland’s biggest real estate agency sold 842 residential properties in April, up 19.6 per cent on April last year and the best result in April since 2021. However, prices headed down. The median at $934,000 was down by $36,000 compared to March (-3.7 per cent) and down by $73,500 (-7.3 per cent) compared to April last year. This was the lowest median selling price in the month of April since 2020. The average selling price was $1,110,689, down by $34,356, or 3 per

cent compared to March and down by $102,139, or 8.4 per cent compared to April last year. Barfoot & Thompson received 1,578 new listings in April, only two fewer than the 1,580 in April last year. The total number of properties for sale, at 6,113, is the most the agency has had at the end of April since 2008, putting stock levels at a 17-year high. Barfoot & Thompson managing director Peter Thompson says sales slowed in the early part of April when talk of tariff trade wars reached its highest but rebounded quickly toward month’s end. “From a price perspective, the market showed no signs of lifting.” ■

Market Update

Home borrowing hits a new high, but problem mortgages rise

Borrowers signed up for $8.5 billion in new mortgages last month – up 45.2 per cent from $5.8 billion in February and up 40.7 per cent from $6.035 billion March last year, the latest Reserve Bank data show. In March 2023 mortgage borrowers took out a smidgeon more at $6.036 billion. The total value of lending increased by a whopping 64.8 per cent for investors, who signed up for $1,779 billion, other owner-occupiers 39.7 per cent, who took out $4,924 billion and a lowly 24.5 per cent or $1,670 billion for first-home buyers. Investors’ share of new borrowings continues to rise and was up 0.4 per cent to 21 per cent from

20.6 per cent in February. Just a year ago investors share of new mortgages stood at a measly 17.9 per cent. While the country’s mortgage stock rose by $1.9 billion in March, the biggest monthly growth since December 2021 and the seventh month it has risen, the number of problem mortgages also rose by $61 million to $2.4 billion. Of the total $368.5 billion in outstanding bank mortgages, non-performing housing loans increased in March to $2,412 million month-on-month and $648 million or 36.7 per cent year-onyear, Reserve Bank figures show. The last time it was this high was in 2013. ■

Chilly market in autumn

REINZ data for April shows a continuation of the gradual recovery in New Zealand’s housing market. The house price index rose by 0.4 per cent in seasonally adjusted terms, a modest pickup from the 0.1-0.2 per cent gains in each of the previous five months. While prices are still down on the same time a year ago, the gap is narrowing, Michael Gordon, Westpac senior economist says. The price performance remains mixed across the country. The median price dropped by 1.1 per cent year-on-year to $781,000. Excluding Auckland, the median price remained unchanged year-on-year, at $700,000. Auckland’s median price declined by four per cent year-on-year, at $1 million. The number of properties sold rose by 9.5 per cent compared to April last year, lifting from 5,871 to 6,427 sales. Excluding Auckland, sales increased 11.1 per cent year-on- year from 4,023 to 4,470. The average time to sell improved for a fourth straight month. However, it remains longer than historic averages. “Lower mortgage rates have helped to revive interest among potential buyers since late last year. This has put only modest upward pressure on prices to date, but as the stock of unsold homes on the market is worked through, we expect to see house price growth pick up over the course of 2025,” Gordon says. ■

Taking a calm interest rate attitude

Westpac is sticking to its forecast of a 3.25 per cent OCR bottom and slightly lower interest rates, while the BNZ is predicting a base of 2.75 per cent and ANZ as well as Squirrel suggesting a drop to 2.5 per cent. Westpac chief economist Kelly Eckhold says the financial markets and some commentators’ kneejerk reactions to the uncertainties of the US-led global trade war are not helping. He says Westpac would rather take a more considered approach. “If things settle down, perhaps we have a bit of downside risk to our interest rates forecasts, but maybe not as much as some are predicting.” As for any effects on housing, Eckhold says there is no upward pressure on interest rates and house prices are going up slowly. Recent drops in wholesale interest rates are expected to lead to a cut of perhaps 20-25 basis points in fixed longer-term interest rates. “There is a decent chance there will be leg down in fixed mortgage rates again, which must be good for property investors as it will improve affordability. The bank anticipates more substantial changes in the housing market once the labour market improves.” ■

Nearly there

While further OCR cuts are likely, we may be nearing the low point for interest rates, writes Kris Pedersen .

As I write this, the budget has just been released.

I’m sure the Reserve Bank of New Zealand (RBNZ) was watching to see whether there was anything inflationary in it, with their next official cash rate (OCR) review announcement six days later, on May 28. By the time you read this, you will know the results.

I’m no economist, but I couldn’t see anything in the budget that should alarm them too much.

RBNZ may be feeling a bit uncomfortable, however. Their most recent business expectations survey showed that Kiwi businesses are expecting inflation to increase.

Everyone expects that there will be a further 25 basis point cut, which will take the cash rate from 3.50 per cent down to 3.25 per cent.

RBNZ commentary about what it is likely to do for the remainder of this year will be closely watched.

Investor interest

While there is definitely a large increase in investor interest, which can be seen through bank pre-approval levels in comparison to the last couple of years, the property market itself is relatively stagnant.

April had the largest level of stock overhang (the number of properties unsold at the end of each month) for any month in the last 10 years. It’s likely that this will continue for the remainder of the year, which may mean further OCR cuts. But whether we will get to the 2.50 per cent that some economists are recommending is yet to be seen.

It is fair to say that RBNZ has previously underestimated how far they will need to cut the cash rate. But mortgage arrears, credit defaults and liquidation numbers indicate the level of economic and financial pain being felt and it is likely further rate cuts will be required to turn the economy around.

Settled in

Most banks seem to have settled into the one- and two-year pricing of 4.99 per cent and it will be interesting to see if a further rate cut spurs some more competition and who will lead it.

I would expect to see a minor drop by some banks, but it appears we are quickly getting close to what may be the low point in rates this cycle. At some stage over the next 12 months there may come a time where it makes sense to lock in for a longer term.

Other than Westpac bringing out a three-year rate at 4.99 per cent, there’s been no sign of any lender going under 5 per cent for that or longer rate terms.

I suspect we may see the one-year rate head towards a low of 4.5 per cent, but for other loan terms we may not see much more downwards movement. ■

The interest rates specified in this table were accurate on 15 May 2025. Interest rates are subject to change without notice. Different fees and charges apply to each loan depending on the motgage lender. Seek expert advice to determine the mortgage lender that is right for you and your circumstances. A disclosure statement is available on request and free of charge.

Investor-targeted listings drop off

Market slows down as investors wait for a shift.

Investor-targeted listings from realestate.co.nz data have dropped 20 per cent month-onmonth – from 4,728 in March to 3,765 in April this year.

At a regional level, listings targeting investors dropped 27 per cent in Auckland (from 2,093 in March to 1,521 in April); Canterbury listings dropped from 562 to 485 (14 per cent); Wellington dropped 22 per cent (314 to 244) and Otago dropped from 136 to 116, a 15 per cent decrease.

This came down from a peak a month earlier – listings targeted at investors reached 4,728 nationally in March, up from 4,641 in February; January listings were lower than April’s at 3,382 (which is seasonally typical).

Vanessa Williams, general manager of marketing and media at realestate. co.nz, says that investors are able to be more strategic with their timing than owner-occupiers.

“It wasn’t surprising to see listings targeted at investors dip in April, which was reflective of the wider market. Unlike owner-occupiers, who often need to list their homes due to lifestyle

changes, such as growing families or separations, investors typically have more flexibility in their timing.”

Maximising rental returns

Larger homes (namely three or four-bedroom properties) were the most likely to be pitched at investors in Auckland.

There were 676 three-bedroom homes, and 512 four-bedroom plus properties, targeted at investors in Auckland: with only 272 two-bedroom homes and 61 one-bedroom homes.

“This likely comes down to return on investment,” says Williams.

“With house prices remaining high in Auckland, investors may be looking to maximise rental income by purchasing larger properties that can accommodate families or multiple tenants. A four-bedroom home naturally commands a higher rent than a two-bedroom, helping offset higher costs.”

The lack of one-bedroom units was notable across the country: only 105

realestate.co.nz has been helping people buy, sell, or rent property since 1996. Established before Google, realestate.co.nz is New Zealand’s longest-standing property website and the official website of the real estate industry.

ABOVE Smaller dwellings are less likely to be targeted at investors.

RIGHT Three- and four-bedroom homes are being marketed to Auckland investors.

one-bedroom units nationally were targeted at investors.

Williams says this is unsurprising.

“There is a limited pool of onebedroom properties listed for sale across our site nationwide, so it’s not surprising that only 105 of those are being marketed to investors,” Williams shares.

“One-bedroom homes tend to be concentrated in city and cityfringe locations, and primarily in bigger cities such as Auckland and Wellington, where purchase prices can be relatively high and therefore rental yields can be less compelling.

“A good real estate agent will know their markets well and will choose their target buyers accordingly.”

Williams feels that the slow-down in investor listings might be seen as reflective of wider uncertainty in the market at present.

“What we’re seeing here may be a sign that many investors are choosing to sit tight amid ongoing global economic uncertainty, or in anticipation of potential market shifts.” ■

Our experts address your property queries

Do you have a burning property investment question you need an answer for? Whether you are just starting out in property investment, or an experienced investor, email joanna@informedmedia.co.nz to have your questions answered.

MEET our expert panel

Matthew Gilligan Gilligan Rowe + Associates, gra.co.nz

QDoes a “security swap” exist when it comes to mortgages? We own a property valued at $1 million with a $340,000 mortgage on it. We also have another property mortgage free worth $700,000. Could we transfer the mortgage to the $700,000 property in order to make the $1 million property mortgage free?

AYes, they certainly do. Generally, there are a few things that come into the equation when banks assess whether they will or won’t do a security swap – loan-to-value ratio (LVR) and security type/suitability, and entity. In your case:

• LVR is fine on both accounts (assuming both standard residential properties), as the LVR is either 34 per cent or 48.6 per cent, which is well under the thresholds for LVR requirements.

• When it comes to security type/ suitability, what they are generally looking for is whether the property is also a standard residential property (not commercial, or specialist/unique in nature), and that there are no issues with the property (unconsented works, etc).

Something else that also can come into the equation at this point is whether the property is owneroccupied, or rental, or vacant land – all of which can be questions the bank may want to know the answers to. Then the entity generally needs to be the same (ie Smith Family Trust for Smith Family Trust) when swapping these properties. If an entity is different, provided it has the same people behind it, it’s usually okay, but can certainly add complexity. To make the process easiest, generally you want to swap something that is somewhat “like for like”. ■

Kris Pedersen

Pet rules explained

QI heard tenants will soon have the right to keep pets. I’ve had bad experiences in the past (dog urine ruined my carpet). Will I be forced to accept pets?

ANot exactly. The new law (expected later this year) will give tenants a “rebuttable presumptive right”

to have a pet, meaning landlords can’t say no without a valid reason. But you can decline pets if the property isn’t suitable, there are safety concerns, or body corporate rules prohibit them. The big difference here is liability. Unlike accidental or careless damage (where tenants often aren’t liable or are capped at the insurance excess), pet damage is

What is deductible?

QWhilst renting, I bought an investment property in 2017. In 2022, I refinanced to buy my owner-occupied house with one large loan to facilitate my investment property and my own home. The refinancing was with the same bank. How would interest from that loan be apportioned to my investment property and owner-occupied home?

Afully the tenant’s responsibility – no cap. You can also require a professional carpet cleaning if a pet is kept indoors. While you may not have as much control as before, there are still protections in place for landlords. ■

Ryan Weir

Interest deductibility is determined by the use to which the borrowed money is put rather than the security for the lending. So, only the interest on the portion of the new debt that refinanced the original loan for the investment property is tax deductible. None of the interest on the portion of debt that was used to buy the non-income-earning personal home is deductible. ■

Mark Withers

Change of structure

QI have been given conflicting advice on whether I should move my owner-occupied home to a look-through company when it becomes a rental in a few weeks or just leave in in my name. How do I know which is the right way? The rental was purchased in 2017 and has a value of $670,000, a mortgage of $670,000 and rents for $700 a week. The owneroccupied home bought in May this year has a value of $675,000 and a mortgage of $420,000. The rental will not make a profit. What should I do?

AThat is an excellent question. Before I comment on the optimal structure for your existing home once it becomes a rental, I want to highlight how the tax rules work when it comes to assessing what

interest is deductible. Now that the interest limitation rules have been repealed, interest is deductible if incurred on money borrowed to buy, or improve a property that is generating rental income.

You state that there is $670,000 of bank borrowing in relation to your rental, which was bought in 2017 and has a current value of $670,000. The question here is how much of this $670,000 of bank borrowing traces back to the purchase, or improvement of, the rental? My suspicion is that a far lower amount of borrowing traces back to the purchase or improvement of the rental, and therefore the amount of borrowing on which you can claim an interest deduction is likely to be lower. With this in mind, you are highly likely to be better off carrying out a restructure of the existing home at the point of conversion to rental use and the purchase of a new home. I would also generally

recommend that the new home is settled into a trust for longterm asset protection and estate planning purposes. Having said this, without further analysis I cannot definitively say that you should do this because there are a number of other considerations that need to be taken into account before you proceed. Transferring the existing home into a rental entity can give rise to tax consequences, such as a resetting of the brightline “clock” and you need to be conscious of these consequences. Furthermore, whether the rental entity should be an LTC, or an “ordinary” company, or a “rental” trust is another issue that requires deeper consideration. In short, you should seek further advice here before you proceed. ■

Matthew Gilligan

Unlawful entry

QI visited my rental property a few days after a flat inspection to do some work on it. The tenant did not know I was going to visit, and they were away. The house was in a terrible state – do I have any right to demand they clean it up? As I stated, they did not know I was going to be there – have I done anything wrong by visiting the property without telling the tenant? Not sure how to proceed.

AThe issue here is that you’ve discovered a potential breach of the Residential Tenancies Act (RTA) while committing an unlawful act yourself. To put it another way, if in the course of robbing a bank, you witness another crime – would you make a citizen’s arrest? I know!

Unless you’ve given 24-hour notice or obtained your tenant’s specific consent before entering the property to carry out repairs, your entry is most

likely unlawful under Section 48 of the RTA, and the maximum penalty is $1,500.

Now, compare that to the potential breach under Section 40(1)(c) – the tenant’s failure to keep the premises “reasonably clean and tidy”. This is not an unlawful act, and no penalty is attached. That should tell you where the bigger problem lies.

Now, turning to the state of the property: It’s clear that it was up to standard during the original inspection – otherwise, you would have flagged it then. So the tenant tidied up before the inspection and then let things slip afterward. This is not uncommon. Who hasn’t cleaned up when they know someone’s coming over?

The key here is that this may not even be a breach of Section 40(1)(c) at all. The law says tenants must keep the property “reasonably clean and tidy” – not “absolutely spotless” or “clean to the landlord’s standards”. Remember, your property is your tenant’s castle.

As long as they’re not breaking the law, they get to live how they want.

So, what does this mean for your next steps? Here’s the thing: tenancy compliance is the easy part. Yes, everyone should follow the Act, but the real art of property management lies in human relationships. Your rental business’s long-term success depends on fostering trust, respect, and open communication with your tenants. If your interaction with this tenant is solely about RTA compliance, you risk turning a small issue into a big one, damaging not just the relationship, but also the future profitability and longevity of your rental portfolio.

My suggestions:

1. Front foot the unlawful entry. Apologise for the mistake, explain the steps you’ve taken to avoid it in the future. A little contrition, transparency, and personal accountability go a long way.

2. Wait for the appropriate standdown period, and then schedule another inspection with the correct notice (no less than 48 hours, no more than 14 days).

3. If the property remains in poor condition, have a constructive, adult conversation with your tenant. Be tactful and respectful. Don’t just focus on compliance – use this opportunity to align expectations. Let your tenant know that maintaining a clean and tidy property is important to you both, and ensure they understand the standards moving forward. Follow up with a 14-day notice to remedy if needed, and schedule a re-inspection with the appropriate notice. Always maintain a balance between enforcement and respect for the fact that it is their home.

Look beyond the knuckle-head stuff and focus on your mission, which is to build sustained and profitable tenancy relationships. You can know the Act inside out, but still flush your rental portfolio down the toilet if you lack tact, care, and a deep understanding of why you have rentals in the first place. ■

Sarina Gibbon

Pet peeves

There’s a lot of concern about what the new rules around pets could mean for landlords, as Matt Ball explains.

Political Update

One of the best parts of my job is travelling around the country talking to property investor associations. It’s great to meet people, find out what’s happening in their area, hear their concerns and update them on the work being done on their behalf by the Federation.

The mood around the country is subdued, with many areas having more rentals than tenants and landlords having to drop rents. Lots of factors affect the rental market, but is it just a coincidence that rents are dropping now that interest deductibility and 90-day no-stated-cause terminations are back?

No-one’s grizzling, this is business, and we’re used to dealing with ups and downs. I love how investors are still looking for that next deal that is going to give them a good return or the opportunity to add value or both. You’re an optimistic, innovative bunch. One thing that is consistently worrying investors, though, is pets. There’s a lack of detail about the pet rules coming into force later this year, a lack of clarity that’s creating uncertainty, which is never good. I’ll try to help with that.

Pet rules

The new pet rules are due to come into force later this year, once the arrangements for taking pet bonds have been put in place. Think October/ November. So do your prep now.

Some landlords have already been asked by tenants if they can have a pet, thinking the changes were in effect. They’re not, so you don’t have to grant a pet request, and you must not take a pet bond. Here’s a fishhook – you can’t add a pet bond to an existing tenancy after the changes come into effect. If you agree to a pet now, you can’t charge a bond for it later.

Once the new law comes into effect there will be a presumption that a tenant can keep a pet or pets unless a landlord has “reasonable” grounds not to allow them.

However, that presumption doesn’t mean they can just turn up with a pet without telling you. There must be written consent to keep a pet, either in the tenancy agreement or a separate document. If you do not allow a pet, the document must state the reasons why.

‘Lots of people have asked me “what’s a pet”, worried they’re going to end up with a horse or a goat’

Existing tenants may put in a request to have pet. You’ll have 21 days to respond, in writing. The response needs to include your decision, any conditions you may have on keeping a pet and – if you refuse to allow a pet –the grounds for refusal.

The act gives some examples of what reasonable grounds for refusal might be, or reasonable conditions for keeping a pet, but these aren’t exhaustive, and I suspect that what’s “reasonable” will be subject to some debate and a few tenancy tribunal hearings.

Reasonable grounds for excluding pets include:

• the property isn’t suitable (size, fencing, or “other unique features”)

• a rule or bylaw prohibits pets –I believe this includes body corporate rules

• the tenant has previously not complied with relevant by-laws relating to the pet or type of pet

• the number of pets

• the size or type of pet

• the pet causing damage or being disruptive

• a dog that has been classified as dangerous or menacing under the Dog Control Act or if you have reason to believe it has attacked people, pets or livestock previously

• the tenant has not agreed to a reasonable condition for keeping a pet

• the tenant previously failed to comply with a reasonable condition relating to keeping a pet.

You’ll note that some conditions are general in that they apply to the property in relation to keeping pets, and others are specific to the pet, type of pet or the tenant.

Reasonable conditions you may set if you consent to pets include:

• that the tenant pays a pet bond (up to two weeks rent)

• that pets are restrained while a landlord enters the property

• if a pet is allowed inside the house, you can include a condition requiring carpets to be cleaned to a professional standard at the end of the tenancy. Note the “professional standard” wording – you can’t require that the carpets are professionally cleaned.

These are good examples, but they don’t cover every possibility and how landlords apply them may differ, so that’s where the reasonable test may come in and cause trouble. If you and your tenant can’t agree on what’s reasonable the decision may be made for you by a Tenancy Tribunal adjudicator. To make life easier I suggest using one of the examples above if you are refusing consent or setting conditions unless you have no other choice.

What is a pet?

Lots of people have asked me “what’s a pet”, worried they’re going to end up with a horse or a goat! A pet isn’t defined in the act, but most cases should be covered by the tests in the act. Clearly an apartment isn’t large enough for a horse, and few city places would be suitable for a goat (though I do have a goat story to share from my Auckland flatting days – ask me next time you see me).

An annoying rooster or other screeching bird would come under the “being disruptive” condition above, and possibly under a local by-law. What I’m saying is don’t worry about this bit so much, the pet rules are mostly intended for people with cats and dogs.

There are also changes in the act that deal with damage, but this article is long enough and that discussion will have to wait for a future date.

I hope this has been useful. To keep across this and other important topics, sign up for our weekly newsletter at nzpif.co.nz/#mailinglist. ■

Profile Scott Unsworth and Greg Owen

INVESTING IN LUXURY

Scott Unsworth and Greg Owen have built up a highly successful short-term property portfolio and have built a luxury accommodation business in its wake, writes Joanna Mathers .

Photography by Stephanie Creagh.

When beautiful property and thoughtful interior design partner together, magic can happen. Property investors Greg Owen and Scott Unsworth understand this magic; together they have grown a successful portfolio, and a new business, in the luxury property space.

When Scott invested in a commercial/residential property on the corner of a popular street in Mission Bay in 2012, the properties were initially attracting a yield of 3 per cent. Having pivoted to short-term holiday accommodation with Greg’s help, the yield across the portfolio is 15 per cent. Their success has been based on many factors – the ability to read the market, understand trends, and utilise interior design to attract visitors – and their new luxury short-

stay accommodation business Stay Luxe is drawing on the lessons learned through this journey.

Sporting success

Scott is the founder of Orca, a leading sportswear brand that the former triathlon champion successfully licensed internationally. He lived overseas for many years, before returning to New Zealand in 2011 from Hong Kong; purchasing a property in the prestigious suburb of Kohimarama.

He and his wife Hildegard knew the property had potential but needed to be renovated – a project that took much longer than expected. But it was worth the wait.

“Hildegard is an interior designer, and she completely transformed the space,” says Scott. “By the time it was finished the value of the property had increased by 50 per cent.”

Scott Unsworth and Greg Owen specialise in the high-end holiday market, such as this home on Takapuna Beach.

Profile Scott Unsworth and Greg Owen

So enjoyable (and profitable) was the project that Scott decided he should find an investment property that he could work magic on again. In 2012, Scott found a mixed-use commercial and residential property in Mission Bay (a Chinese medicine practitioner used the top space and there was a residential tenant in the below apartment) that had a lot of potential.

While the location was great, others weren’t so keen. Neither the office space or the apartment was in great condition and Scott was new to the property investment, so the results were far from certain. But he was convinced.

Scott laughs when he remembers the rookie mistakes made when bidding for the property at auction.

“I put my hand up for everything,” he chuckles. “It was going up in

$1,000 increments and it hadn’t met the reserve.”

The properties didn’t sell at auction, but Scott negotiated with the buyer two days later, and the deal was sealed.

But the two properties were never his end game. There were four units in the building, the other two owned by elderly owner-occupiers who didn’t want to sell. But Scott wanted to own the entire corner site and was tenacious in his attempts to purchase them.

“I kept offering to buy the units, but they kept turning me down,” he says. “They were adamant that they would stay there for the rest of their lives.”

Eventually, one of the owners put their property on the market without telling him. He discovered that there was going to be an auction for the property and attended in secret –buying the property for $30,000

Scott and Greg have been friends for years and have turned their expertise in elite sport into success with high-end property.

above what the bank would lend him.

The final unit took some time to secure. Scott offered the owner a price he felt wouldn’t be bettered in the market. “I told him that this was his only chance at this price; that if he didn’t accept the offer, that was final.”

The owner didn’t accept the offer –but contacted Scott later to say he was ready to sell.

“I told him that original offer no longer stood, and I ended up paying $200,000 less than the original offer.”

Complete transformation

Scott had four units in a great location in Mission Bay. But he was aware that keeping them as residential or commercial tenancies wasn’t going to achieve the results he wanted.

Enter Greg Owen. The highperformance sports coach, who owned an organisation that had worked alongside many of New Zealand’s elite athletes, had been friends with Scott for many years. He was looking for a new project, so Scott brought him on board to help oversee the transformation of his corner site into something more lucrative.

They had become aware of the potential for significantly higher yields in the short-term holiday rental market: “in fact, we would be attracting two or three times the income that you can achieve with long-term rentals,” says Scott.

Scott and Greg worked together on transforming the property into a series of charming coastal getaways. They oversaw the renovation of the units, with Hildegard helping with the interior design.

The four units were split into eight one-to-four bedroom apartments.

They decided on a coastal theme for the units – keeping the interiors the same, using the same kitchen in each. The units are targeted at the middle range of the market, not too expensive, not too cheap.

They had a good builder who explained everything to them as they went along, plus excellent architects and engineers. They also used a home design app that gave them

3D visualisations of what they wanted to achieve, which they would take to the architect.

“We changed plans a lot, which was sometimes hard on the builders,” laughs Scott.

Greg explains that the Mission Bay property has ended up bringing in excellent revenue: “It’s great because of the coastal location and it looks really prestigious,” he explains.

Covid inevitably had an impact on the Mission Bay property. With visitors locked out, they changed some of the rentals to long-term; and a lot of returning Kiwis needed a place to stay. (They have since changed the units back to short-term rentals).

But once the lockdown restrictions were lifted, there was the opportunity to repeat the winning formula with another coastal property. The five-bedroom home with a small self-contained dwelling was located in Tauranga, next to the beach. It was a run down 60s property, but the location was ideal. They repeated the formula – turning the property into four holiday units.

‘This provides the owners with a great income stream; and they are able to sell later if the opportunity arises’

“We were all on the tools,” explains Scott. “We managed to turn this one around very quickly.”

They ended up selling the Tauranga property last December, walking away with a considerable profit after the renovations.

The pair now have the Mission Bay and a Takapuna property – marketed under the brand Stay Mission and Stay Coastal. The Takapuna home is and a stunning four-bedroom beachside property. The interior design is courtesy of Hildegard; and the properties all perform extremely well.

Scott and Greg have recently launched a new venture, Stay Luxe, that offers luxury holiday accommodation for wealthy visitors to Auckland.

They were aware that there was a gap in the luxury accommodation

market and used the lessons they learned in creating beautiful holiday homes to market the properties to the right clients.

They are managing properties owned by high-net-worth individuals, some of whom are unable to sell their multi-million-dollar homes in the current market.

“This provides the owners with a great income stream; and they are able to sell later if the opportunity arises,” says Greg.

Greg helped build the website for Stay Luxe and he manages the business.

It’s been successful so far and this is a testament to the strength of their friendship and background in elite sport – bringing their expertise in the sporting world to New Zealand’s high-end holiday home market. ■

FADE TO GREY

The coalition government has changed the rules around productive land, in order to facilitate future housing development. Is it a silver bullet or a fast-track to grey suburban sprawl? Sally Lindsay and Joanna Mathers investigate.

Property Development

Keith Aldous (of Aucklandbased We Subdivide) shoots from the hip.

He’s aware of how the subdivisions that spread out from city centres into pastureland can become ugly and undesireable.

“There are numerous examples around Papakura and Papatoetoe in the south [Auckland] which look awful and they are not selling. They’re built quickly, cheaply, they’re not insulated properly and neighbours can hear each other.”

Aldous is pondering the changes to greenfield zoning rules that housing minister Chris Bishop announced at the Property Council Residential Development Summit earlier this year.

The changes relate to the National Policy Statement for Highly Productive Land (NPS-HPL), which was introduced by the last government to protect New Zealand’s highly productive soils.

The NPS-HPL protects a total of 15 per cent of the country’s landmass – an area nearly as large as Otago. Much of this protected land is around our biggest centres, and in Bishop’s view, the rules are impeding “growth busting to get out”.

“[We need to strike a balance]

‘They’re built quickly, cheaply, they’re not insulated properly and neighbours can hear each other’

KEITH ALDOUS

between how we protect our most productive land, and the development of more homes,” he stated.

In order to facilitate this, cabinet has removed the protected status of land with lower quality soil (classified as LUC-3 land), and opened it up for housing.

Gone is the previous government’s focus on intensification – Bishop wants New Zealand to grow up and out. To that end, government is also offering developers affordable finance to facilitate infrastructure for these developments.

The development phase of a project is often the riskiest – and private financiers reflect this by charging higher interest rates.

This being the case, National

ABOVE Suburbs will begin to spill into greenfield land under the changes to zoning rules introduced by the current government.

Infrastructure Funding and Financing (or NIFFCo) will be providing $100 million for low-cost financing of medium-sized greenfield developments over the development period.

NIFFCo will charge approximately what private financiers would charge for completed developments – saving developers money, which should be passed on to homebuyers.

But while the expansion of available land for housing makes sense in an theoretical sense – supply and demand, more houses, lower prices –Bishop’s plan is not without its flaws.

And some are concerned it may cause more problems than it solves.

Superlot suburbs

Development in greenfield around the edges of cities can be problematic. Subdivision at scale is often standardised – endless streets of identical houses. The funding available favours large developers – who create at scale.

Clever master planning is needed to ensure bland suburban sprawl is avoided.

Aldous points to Milldale, on the northern outskirts of Auckland city, as an example of bland suburban sprawl. And he feels that the development changes will favour mega-developers.

“It will be the same old story, five or six builders buying superlots and creating generic two-storey box-standard houses”.

Even though there are some nice properties being built, he says “developers also run into problems when there is no overall design concept.

“The builders just put their own spin on what they want to build and nothing flows between them. There needs to be careful consideration before any development takes place. There needs to be more overall master planning of suburbs.”

South Auckland-based Ray White AT Realty Group director and branch manager Tom Rawson foresees another issue – a glut of new homes that no one wants to buy or rent.

HOW THE FUNDING WORKS

The $100 million is being made available through National Infrastructure Funding and Financing (NIFFCo) for low cost financing of medium-sized greenfield developments – about 1,000 to 2,000 houses.

Under the new Greenfield Model, NIFFCo will lend to selected developers through Special Purpose Vehicles (SPV) at competitive interest rates for water and bulk transport, community and environmental resilience, infrastructure (eg roads, stormwater, public transport, cycleways and flood-protection design, consenting and delivery costs), to allow a project to progress.

Once the development is completed, the debt will be refinanced to private markets and the funding will ultimately be repaid by future homeowners through an annual levy based on factors such as land area, value and use.

The levy will be capped, but homeowners will know in advance how much they will need to pay and over what timeframe. When the property owners sells, the requirement to pay the levy will shift to the new owners. The levy ends once the infrastructure is paid for. Bishop claims the lower funding interest rate will mean an average

“We have ended up with hundreds of new homes in the rental pool, because developers can’t get the sale prices they want to make a decent margin,” he says.

He continues that taxpayers need to question why the government needs to fund developers at all? Is it because the banks won’t?

“Developers have probably been lobbying for this, saying the banks won’t lend them money and they need cheaper finance. For this type of funding to work (and address affordability) it has to be economical for developers to to buy the land, design, provide the services, build,

finance and sell the properties.

“At the moment it isn’t. And that’s true. But the banks aren’t lending the money because they see many greenfield subdivisions and developments as risky.”

Bigger developments on greenfield land have more risk. Infill developments in the city are seen as less risky as they are proven.

Easier access to land

Canterbury-based construction expert Mike Blackburn has a different take. He says that anything that makes it easier, cheaper, faster and simpler to bring houses to the market is a good idea.

ABOVE AND LEFT Darfield and Amberly in Canterbury are experiencing significant demand from buyers who want a home with a backyard at a competitive price.

But he wonders if the $100 million allocated to funding will go far enough.

“One of my clients spent $500,000 just on an application to the local council for a 150-200 lot subdivision. That is $2,500 per section before a bulldozer even gets to the site. And that cost goes on the retail price of the house when it is completed.

“Developers spend that sort of money upfront in the hope they are going to get their developments across the line. If for whatever reason they don’t, then that money is just gone.”

He also questions whether developers will want to go through government scrutiny for their projects.

“Obviously sticking your hand out for any sort of loan from the government will come with a series of hooks regarding transparency and accountability for delivery.”

Nevertheless, Blackburn says that a significant percentage of the population don’t want to live in medium-density, multi-unit apartment or terraced complexes (he points to the thousands of unsold two-storey terraced houses around the country).

Having access to more land could be a great selling point.

“There is significant demand for greenfield developments, which is why fringe towns, such as Darfield and Amberley, are becoming popular because buyers can get a good size section with a backyard at a competitive price, within a 30-40-minute drive of Christchurch CBD. “[The changes] will give confidence to the industry, and with a bigger pipeline of land coming through, it will boost supply and keep prices down.”

State of play

NIFFCo has started working on a pipeline of medium-sized developments and says it will announce projects when transactions have “a high certainty of proceeding”.

At this stage only a small number of developers have made inquiries to NIFFCo about the funding and it will work with them to establish whether their developments are suitable for the funding.

Any additional funds above the $100 million will be subject to future ministerial decisions.

Property Development

‘There is significant demand for greenfields developments, which is why fringe towns, such as Darfield and Amberley, are becoming popular because buyers can get a good size section with a back yard at a competitive price’

The agency says the new tool makes the cost of new infrastructure more transparent, while ensuring it falls primarily on the property owners who benefit across generations.

It’s useful to take the changes in context. In 2019 Auckland Council’s then chief economist David Norman said developing greenfield land was eye-wateringly expensive and had to be staged.

The (then) Future Urban Land Supply Strategy allowed for the staged development of about 140,000 greenfield dwellings over 30 years, with an estimated cost of council-

provided water infrastructure and central government-funded transport infrastructure at $21 billion (or about $140,000 per dwelling).

Developers contributed typically about a third of the cost.

This is where NIFFCo’s loan will help developers. The lower-cost financing over the development period will be at rates similar to what private financiers charge for completed developments. “This support will bridge the financing gap and help ensure that new homes continue to be built in areas where they are needed most,” a NIFFCo spokesperson explained. ■

BUSINESS AS USUAL

Investors don’t have high expectations of the year ahead, but their concerns around availability of credit and high interest rates have reduced, according to our 2025 survey.

The muted property market has been reflected by a muted response from the investors who took part in the latest New Zealand Property Investor magazine investor sentiment survey.

House prices are currently stagnant – the most recent data from Cotality (formerly CoreLogic) reveals that shows that median property values have edged up by only 1 per cent in the past 3-4 months.

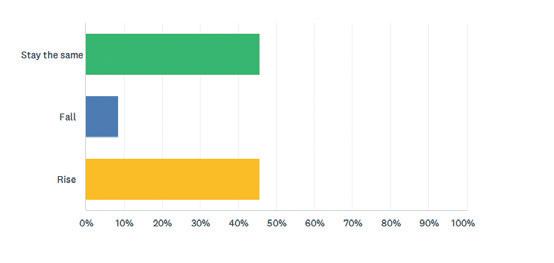

And investors are feeling this. When asked around expectations of property values, 45 per cent stated that prices would stay the same. Even though this was offset by the 45 per cent who felt prices may rise, the remaining 8 per cent believed the prices would decline – tipping the scale towards neutral of negative sentiment.

The changes to legislation around the 90-day, no-stated-cause terminations, the reinstatement of interest deductibility, and lower interest rates were predicted to increase buyer activity. But this hasn’t played out the way pundits thought – other factors including the soft labour market and debt-to-income ratio limits for mortgage lending, are keeping the market in in check.

Matt Ball from New Zealand Property Investors Federation (NZPIF) says that the low-key sentiment expressed in the survey reflects what they are seeing on the ground.

“The feedback is that there are still opportunities for the canny investor, who puts in the time and effort to find that property with a good yield or potential for improvement, but there are a number of factors holding back a wider market recovery.

“Income (rent) is down, and costs (rates, insurance, maintenance) are up. Interest rates are falling, but it will be 6-12 months to feel the full benefit and the money clawed back will largely be used to make up for previous losses or cover higher costs.”

The spectre of global economic unrest due to Trump tariffs is also lingering – plus uncertainty about next year’s election.

‘New build has limited opportunities to add value, and you are competing against the same product in the same market. In the case of twobedroom townhouses, good luck having a point of difference in rentals or when selling’ SURVEY RESPONDENT

“There is a lack of confidence that interest deductibility will remain in place. Add in low migration, high unemployment and a subdued New Zealand economy, and it’s not hard to see why many are in wait-and-see mode.”

Let’s dig down into the results to find out how New Zealand investors are feeling about the market.

The basics

Auckland once again topped the charts when it came to the amount of investment properties. Forty per cent of respondents stated that they owned properties in Auckland, with Canterbury coming second on 22 per cent, and the Wellington region on 20 per cent.

The stats shows that the vast majority of landlords weren’t “megalandlords” – it’s a sector proliferated with “mums and dads” who invest for future security.

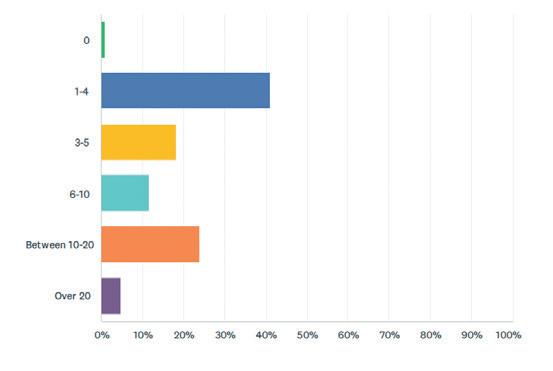

Forty per cent of respondents stated that they owned between one and four properties, 18 per cent

owned between six and ten, and 23 owned between 10 and 20 properties. Only four per cent owned more than 20 properties.

The section on motivations reflect the preponderance of landlords investing sensibly for the future.

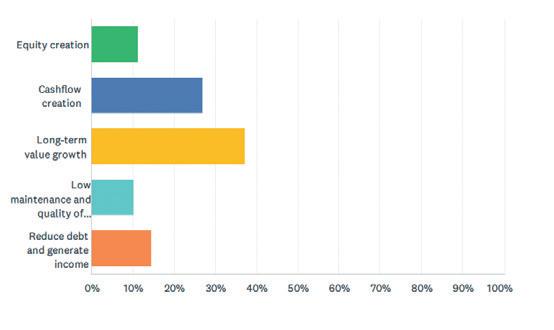

When asked the most important driver when considering investment properties, 37 per cent listed longterm value growth. Cash-flow creation came in second, with 26.8 per cent of respondents listing this as their most important driver. The least important drivers were equity creation, followed by reduction of debt and generation of income.

Landlord concerns

Landlord concerns have changed considerably since the survey was conducted last year.

In 2024, an overwhelming 85 per cent stated interest rates were their

primary concern; this year the 62 per cent of respondents listed that finding good tenants was at the top of mind. Ball states that this also aligns with what NZPIF is hearing.

“This is not surprising given what we hear from landlords around the country daily, and it’s just simple supply and demand.

“There are a record number of properties for rent – the highest in a decade according to Trade Me – and there isn’t the demand there for that supply. End result is it’s harder to find good tenants and rents are under pressure, with significant falls in rent in some places.”

Key survey results

How many investment properties do you own?

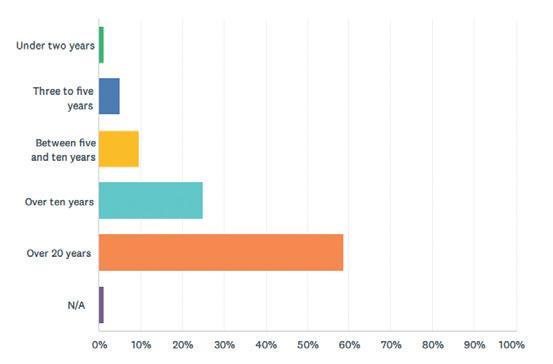

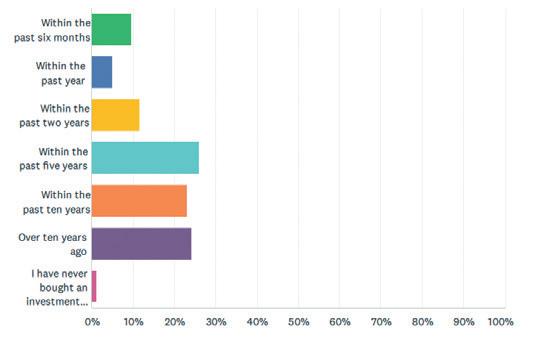

How long have you been investing for?

What is the most important driver when considering an investment property?

David Faulkner, general manager of property management at Property Brokers, says there are other factors coming into play.

“There are a multitude of reasons why landlords are finding properties hard to rent. Net migration, sluggish economy, increase in stock and less tenant movement are probably the biggest drivers.”

Low yields are also a concern, at 52 per cent, with lender’s servicing criteria and interest rates coming third at 30 per cent.

Credit availability

When the Credit Contracts and Consumer Finance Act (CCCFA) rules were ramped up in November 2021, mortgage advisors and those in the market for a new mortgages were thrown in the deep end.

The previous rules had been around since 2015, but the new tightening of the rules meant banks needed to scrutinise every Netflix bill and Uber Eats meal their client dialled up after a hard day in the office.

It led to loans being declined for ridiculous reasons, and made credit harder to come by.

Outcry ensued and the Labour government softened the rules; and these were further modified in July last year, enabling banks to have more wriggle room when assessing discretionary spending.

The outcome of this has flowed on to investors. When asked last year if they had any difficulty getting access to finance, 43 per cent stated “yes”. This has been reduced to 33 per cent this year.

“The test rates that banks use to assess affordability have dropped very fast in recent times which has made it a lot easier for lenders to meet bank requirements,” says Pedersen.

“While I still think some parts of the criteria are unnecessarily onerous, there is overall a lot more common sense being used than what we saw a few year ago with the CCCFA debacle, which effectively shut down mortgage credit for a while.”

Our respondents are loyal to their lenders – 56 per cent have lending with just one lender, with 17 per cent having two lenders and 26 per cent using three or more.

But Kris Pedersen, this year’s survey sponsor and owner of Kris Pedersen

Mortgages, says this is not ideal

“We do not recommend it. Banks definitely make the process easy, but investors need to keep in mind that they cross-secure the loans and properties together behind the scenes and this can cause multiple issues –from making it hard to continue to grow your investment portfolio if that lender says no, to having full control if the investor ends up in a difficult position and may need to sell.

“Investors need to keep in mind that it is now common practice for lenders to put you through a full application process if you are looking to discharge a security and retain debt with a bank. What has happened a lot in recent years is investors selling down because of the higher interest rate environment only for the bank to take all of the sales proceeds because of the cross-security and the client’s inability to meet the banks current lending requirements.”

Non-bank lenders are also increasing in popularity, with nearly 60 per cent using (or considering) non-bank lenders.

“Awareness [around non-bank lenders] has grown significantly in recent years,” says Paul Bendall, CEO of First Mortgage Trust.

“This shift is part of a broader global trend toward private credit. As traditional banks continue to be inflexible in their approach to lending, particularly when transactions are complex or fall outside standard criteria, borrowers are seeking more pragmatic, solutions-focused alternatives.”

ON THE UP

Kris Pedersen says there is optimism in the market, if you look beneath the surface.