Blockedinputtax

Inputtaxisnotdeductible(andisknownasblockedinputtax)inrespectofthetypesof supplyinthetablebelow,thepresumptionbeingthatmostofthesesupplieswillbeputto non-businessuse.Alternatively,VATisonlycalculatedontheprofitmargin.

Theonwardsaleoftheseitems,whereinputtaxhasbeenblockedonacquisition,is exempt.

Summary

Thefollowingtypesofsupplyarediscussedintheparagrpahsindicated:

Provisionofaccommodationtoadirector

Certaingoodsinstalledindwellings

Servicesandgoodsacquiredbytouroperators

Goodsandservicesacquiredunderamarginscheme

reg6

reg12

reg4(2)

A.Motorcars-acquisitionandleasing

Subjecttotheexceptionslistedat¶20915,inputtaxdeductionontheacquisitionorleasing ofcarsisveryrestricted.Itisofcoursevitaltoknowwhetheraparticularvehicleisacar, becauseinputtaxcanbefullydeductedonothertypesofvehicle

1.Scope

Forthesepurposes,amotorcarisdefinedasavehiclewhich: –isnormallyusedonpublicroadsandhasthreeormorewheels; –isconstructedoradaptedmainlytocarrypassengers;and –hasroofedaccommodationbehindthedriver’sseat,whichisfitted,orcouldbefitted, withsidewindows.

However,thefollowingvehiclesareexcludedfrombeingacar: –ambulances,caravans,prisonvansandothervehicles(suchashearses)constructedfor aspecificpurposethatdoesnotincludethecarriageofpeople; –thosewithspaceforonlythedriver; –vehicleswithcapacityfortwelveormorepassengers; –thoseweighingatleast3tonneswhenunladen;and –vehiclesthatcancarryapayloadofatleast1tonne.

MEMOPOINTS

1.Inaddition,vehiclesthatwouldotherwisepassthe12-passengertestbutwhich havebeenadaptedforwheelchairuserswillnotfailthetestsolelybecauseofthatadaptation.

2.Fordoublecabpick-ups,whicharenotcarsifthepayloadisatleast1tonne,theadditionofa hardtopwilldecreasetherequiredpayloadby45kg

Supply Reference ¶¶

SI1992/3222

¶20835+

SI1992/3222

¶21020+

Motorcars-acquisitionandleasing

reg7

Businessentertainment

reg5

¶20620+

SI1992/3222

¶50880 Privateimports s27VATA1994 ¶83230

¶65400+

SI1987/1806

¶58000+

SI1992/3222

190INPUTTAXDEDUCTIBLEINPUTTAX 20800 s25(7)VATA1994 20805 20835 20865 SI1992/3122reg2 VIT56600

Car-derivedvans

Thesevehicleshavethefunctionalityofavan,becausetherearseatsandseatbeltsare removed,thefootwelliscoveredover,andthesidewindowsaremadeopaque

Wheresuchvehiclesarenotdesignedtocarrypassengers,itispossibletotreatthemlike vansforVATpurposes,iftheysatisfyallofthefollowingcriteria:

Vehicleproperty Criteria

Loadarea

Highlyunsuitableforpassengers Functionalityofacommercialvan

Seatbeltmountings Completelyremovedordisabledandboltholesweldeduporbonded shearboltsfitted

Seatmountings

Rearfootwell Permanentfixedcoverweldedorfixedontop Windows Madecompletelyandpermanentlyopaque Mechanismforloweringandraisingdisabledorremoved

Combinationvans

Thesehaveseats(permanentorfolding)behindthedriver’sseatandareusuallyclassed asamotorcar,exceptwhen:

–theseatbeltsandseatmountinghavebeencompletelyremovedordisabled; –theloadareaisofsuchasizethatthecarriageofgoodsisthepredominantuseofthe vehicle;or

–thepayloadcapacity(whichwillbereducedbyanyseating)isstillinexcessof1tonne

Motorcaravans

Motorcaravansarenotcars,providedthatallofthefollowingcharacteristicsarepresent: –permanentlyinstalledsinkandcooker; –atleastonebedofalengthof1.82mormore; –permanentlyinstalledfreshwatertankwithaminimumcapacityof10litres;and –seatingaroundamealtable.

Conversions

Thepurchaseofacartoconvertitintoanothervehiclegivesrisetodeductibleinputtaxif conversionwasintendedfromthestart.Conversionfollowingachangeofintentiondoes notgiverisetoanyretrospectiverighttoinputtaxdeduction. Whereacommercialvehicleisconvertedintoacar,thereisaself-supply(¶15665+)bythe owner,whichmeansoutputtaxmustbechargedtobalancetheinputtaxalready recovered.

2.Carswhereinputtaxisdeductible Inputtaxisnotblockedonthefollowingtypesofqualifyingcar: –stockforresale; –carsacquiredforthepurposeofacar-relatedtrade;and –carsacquiredwhollyforbusinessuseandnotintendedtobemadeavailableforprivate use

Aqualifyingcarisonethathasneverenteredfinalconsumption.Inpractice,thismeans that:

–thecarhasneverbeenpurchasedbyanon-taxableperson;or –noinputtaxhaseverbeenblockedonapurchasebyataxableperson.

Whereasnewcarsobviouslyfitthesecriteria,carssoldbyleasingcompaniesarealso likelytobequalifying

DEDUCTIBLEINPUTTAXINPUTTAX191 20870 VIT50600 20875 VIT50900 20880 VIT51200 20885 SI1992/3122 reg5; VIT51800 20915 SI1992/3222 reg7(2) SI1992/3222 reg7(2A)

B.Businesssplitting

1.Generalprinciples

HMRChaspowerstointerveneifitbelievesthatasinglebusinesshasbeensplitintotwo ormorelegallyindependentpartstoavoidoneorbothbeingliabletoregisterforVAT.This issometimesknownas“disaggregation”

a.HMRCcounteraction

Assessments

HMRCmayissueassessmentsbackdatedtothedatewhenthebusinesswassplit,if: –thesuppliesexceedtheregistrationthresholdandareactuallybeingmadeby onlyoneofthebusinesses;or –theactualsuppliesmadebyoneormoreofthebusinessesexceedtheregistration threshold.

Thishasaretrospectiveeffect(¶26600)andlateregistrationassessmentscangobackas faras20years(¶36175).

Notices

HMRCmayalsoissueanoticemakingadirection(¶26035)totreattheseparatepartsasa singleentityforVATpurposes.Thiscannotbebackdated,andmayonlybeissuedwhen thesplitisconsideredbyHMRCtobeartificial.

Beforemakingadirectionnaminganyperson,thefollowingcriteriamustbesatisfied: –thepersonhasmadeorismakingtaxablesupplies; –theactivitiesperformedbytheperson,andwhichgiverisetothetaxablesupplies, formpartofalargerbusinessfunctionwithotheractivitiesbeingcarriedonby anotherpersonorpersons;and –ifallthetaxablesuppliesofthatbusinessfunctionweretakenintoaccount,a personcarryingonthatbusinesswouldbeliabletoberegistered.

EXAMPLEMrsBownsstablesfromwhichsheprovidesfullliveryservices.Herannualturnoveris £100,000andshewouldthereforeberequiredtoregisterforVAT.

However,ifthebusinesswasstructuredsuchthatMrsBonlyprovidedthestabling(withanannual turnoverof£55,000)andMrBprovidedthefeed,beddingandotherfacilities(withanannual turnoverof£45,000),thetwobusinesseswould,intheabsenceofadirection,notneedtobe registeredforVAT.

Intheseparticularcircumstances,itislikelythatHMRCwouldissueadirectiontotreatthetwo entitiesasoneforVATpurposes.

b.Whendoesbusinesssplittingoccur?

Althoughtherearenodefinitiveteststoestablishwhetherabusinesshasbeenartificially split,HMRCisrequiredbystatutetoconsiderthefinancial,economicandorganisational linksbetweenthepersons,including,forexample: –theexistenceorotherwiseofnormal,commercial,arm’slengthrelationships; –theapportionmentofoverheadcosts; –addressingofinvoices; –meansofadvertising; –segregationorotherwiseoftakings;and –theexistenceorotherwiseofseparatebankaccounts,accountingrecordsand financialstatements.

REGISTRATIONCOMPLIANCE273

VATDSAG 25970 25975 25995

25950 Sch1paras1A,2 VATA1994;

MEMOPOINTS 1.Publicperceptionandthetreatmentofthebusinessfordirecttaxpurposes areunlikelytobeofsignificanceforHMRC(althoughtheymaybefactorswhich,when consideredwithothers,areindicativeonewayortheother).

2.Inrelationtoholidayaccommodation,seealso¶53510.

EXAMPLE

1.Afishandchipshopandtwolaunderettebusinesseswereallegedlyrunasthreeseparate businesses,withtworunbythehusbandandtheotherbyhiswife.

However,theywereheldtobeonebusinessforVATpurposeswiththehusbandasthesole proprietor,largelyonthebasisthatthevarioustradingpremiseswereinhisnamealone,aswasthe bankaccount.Alltheinvoicesforsuppliestothebusinesseswereaddressedtohim.Thetribunal wassatisfiedthatatalltimesthe“controllingmind”ofthebusinesswasthatofthehusband.RSSahota [1997](VTD14986)

2.Itwasclaimedthatakebabandpizzatake-awayoutletwasrunastwoseparatebusinesses, withanarrangementthatthepizzaoutlettradedforonehalfoftheweek,andthekebaboutletfor theother.Eachbusinessemployeditsownstaff(apartfromonesharedemployee).However,on thefactsofthisparticularcase,andintheabsenceofawrittenagreementbetweentheparties,the activitieswereheldtoconstituteonebusiness,asthepartiesdidnotadequatelydemonstratethat therewasanormalcommercialrelationshipbetweenthem.Forexample: –therewasnoseparatechargefromthefreeholdertoeachbusinessforoverheads; –bothpartieswerecoveredbyonepublicliabilitynotice; –allpurchasesofgoodsweremadebyoneparty;and –thebusinesswaspresentedtothepublicasone,bothpartiesusingthesametradingnameand menus.L&AEleftheriou(t/aPicnicKebabHouse)[2000](VTD16659)

Extensiontoactivity

Generally,whereanexistingbusinessisextended,thenewactivitywillberegardedas beingpartoftheexistingbusinessifthenewactivitiesarerelatedtoexperienceor qualificationsusedintheexistingbusiness.

EXAMPLEAbarrister,specialisinginpatentandotherintellectualpropertylaw,lecturedonweekend coursesonanadhocbasis(every2-3years).Itwasheldthatthiswasanactivityinthecourseor furtheranceofhisexistingbusiness(asabarrister).Ashisexistingbusinesswasalready registeredforVAT,heshouldhaveaccountedforVATonthefeesreceivedfortheweekend lecturing,astheactivityamountedtoanextensionofhiscurrentbusiness.BCReid[1993](VTD11625)

Self-employment

Whereself-employedindividualsareusedbyabusinesstoprovideservicestoits customers,thekeyquestionwhichHMRCwillconsideriswhethertheself-employed individualsuppliesservicesdirectlyto:

a.thecustomers,inwhichcasethesupplywillbemadebytheself-employedperson,and itmaybethatthetradeisbelowtheregistrationlimit;or

b.themainbusiness,whichinturnsuppliesservicesdirectlytotheendcustomer(in whichcaseitmaybethatthemainbusinessisregisteredforVATandconsequentlyVAT willbedueonthesupplies).

MEMOPOINTS ForfulldetailsoftheVATrulesrelatingtoagents,see¶63000+.

2.HMRCdirections

AdirectionissuedbyHMRCmustgivethefollowinginformation: –adescriptionofthebusiness; –nameofallthepersonswhoaretobetreatedascarryingonthesinglebusiness; –broaddetailsofthereasonsforissuinganoticeofdirection;and –thedatefromwhichregistrationasasingletaxableentityistotakeplace(which cannotbeearlierthanthedateofthedirectionitself).

Itmustbeservedoneachofthepersonsnamedinit;

274COMPLIANCEREGISTRATION 26000 26005 26035 Sch1para2 VATA1994

Newbuildings

Abuildingisusuallyastructureofasubstantialsize,whichisintendedtobeenduringfora considerableamountoftime.Mostbuildingsarepermanentstructures. Thesupplyoffixtureswithabuildingistreatedaspartofthesamesupply,theVAT treatmentbeingthesameasthatfortheassociatedbuilding.

MEMOPOINTS 1.Afixtureisanassetthatisinstalledin,orotherwisefixedinorto,abuilding orlandsoastobecomepartofthatbuildingorlandinlaw(¶50385).

2.Achattelisatangibleandmoveableasset,althoughitcanbecomeafixturebybeingattached toabuildingorland(e.g.aradiator).

A.Whatisanewbuilding?

Identifyinganewbuilding,particularlywhenitisrelatedinsomewaytoanexisting building,iscrucialtoapplyingthecorrectVATtreatment.Acommercialbuilding(¶50440) istreatedasnewuntilitis3yearsold.Otherbuildingsareonlynewduringtheperiod runningfromcompletionofconstructionuntilthefirstonwardsupply.

1.Exclusions

Broadly,anewbuildingexcludesconstructioninvolvinganexistingbuilding,suchas: –theconversion,reconstructionoralterationofanexistingbuilding(specialrulesapply forthesetypesofworks(¶51470+)); –anenlargementof,orextensionto,anexistingbuilding,unlessanewdwellingiscreated (¶50465);or

–theconstructionofanannexe,unlessitistobeusedforacharitablepurposeand detailedcriteriaaresatisfied(¶50560).

Theplanningpermission,applicationandconsentfortheworkshouldidentifythenature ofthework.Themaintest,however,isthedifferencebetweenwhatexistedbeforethe constructionbeganandwhatexistsafterwardsi.e.whichphysicalcharacteristicshave changed,andwhateffecthastheworkhadonanyexistingbuildingsonthesite,including therelevantfunctionsofthebuildingsandanyinterrelation.

2.Demolition

Ifanexistingbuildingisdemolishedtogroundlevelandanotherbuildingiserected,the replacementbuildingwillbeanewbuilding(unlessitisareconstructionofthepreexistingbuilding(¶50250)).Theexistingbuildingwillstillbetreatedasdemolishedforthis purposeifasinglefaçade(doubleifacornersite)isretainedasaresultofaconditionof statutoryplanningapproval.

Ifdemolitionoftheexistingbuildingoccursafteraseparatenewbuildinghasbeen constructed,thedemolitionworkisnotpartoftheconstructionofanewbuildingforVAT purposes.

EXAMPLE

1.Adisabledpersonlivedinabungalow,whichheintendedtodemolishandreplacewithamore accessiblehome.Duringtheconstructionworksheneededsomewheretolive;duetoalackof alternatives,hehadtoremainintheexistingbungalow.Therefore,anextensionwasbuiltandthen theexistingbungalowwasdemolished. Itwasheldthatanewbuildinghadnotbeencreatedbecauseanextensionhadbeenbuiltfirst, eventhoughthepre-existingbuildingwasthenimmediatelydemolished.GrahamDavidGilder[2003] (VTD18143)

SECTION1

LANDANDPROPERTYPARTICULARACTIVITIES519

50230

50200 Notice742 para7.9

50235 Sch8Group5 notes16,17 VATA1994 50240 Sch8Group5note 18 VATA1994

50250 InformationSheet 07/17

2.However,wheretheexistingbuildingwasdemolishedandentirelyreplacedaspartofthe constructionprocessforanewbuilding,thetribunalhasheldthatthiswasnewconstruction.The factthatdemolitiondidnotprecedecommencementofconstructiondidnotdecidethematter (¶51080).JandJWatson[2019](TC07513)

HMRC’sview

HMRChasgiventhefollowingexamples:

Situation

Makinguseofthefoundationsofapreviousbuildingthathasbeen demolishedtogroundlevel

Buildingontoanexistingwallofanotherhousetoformtwosemi-detached houses;nointernalaccessbetweenthetwoandplanningconsentdoesnot prohibitseparateuse,lettingordisposal

Buildingofanewhousewithinanexistingterraceofhousesonthesiteofa demolishedhouse

Constructionofaself-containedflatthatenlargesanexistingbuilding

Constructionofagrannyannexethatcannotbeusedseparatelyfromthe mainhouse

Detachedenclosedswimmingpool

Caselaw

Thebasictestappliedincaselawiswhetherareasonablepersonwouldsaythatabuilding wasneworpartofanexistingbuilding

CommentUsually,retentionofanypartofapre-existingbuildingdemonstratesthat constructionworkissomesortofalterationtothatpre-existingbuilding,whether reconstruction,enlargementorextension.However,inrarecircumstances,acompletely newbuildingcanbeconstructed(contrastexamples5and6below).

EXAMPLE

1.Acompanyredevelopedasite,whichmeantsomebuildingsweredemolishedandanew buildingwasconstructed.

Itwasheldthattheworkconstitutedtheconstructionofanewbuilding,ratherthanthe reconstructionofanexistingbuilding,becauseitwas“notareplicationorconstructionanewof whatwastherebefore”.WimpeyGroupServicesLtdvC&E[1988]

2.Acompany,whichownedamulti-storeycarpark,obtainedplanningpermissiontobuildablock offlatsabove.

Itwasheldthattheflatswereanewbuildingbecauseitwasinappropriatetoregardtheflatsas enlargingtheexistingcarpark.TridentHousingAssociationLtd[1993](VTD10642)

3.Anewresidentialbuildingwasconstructedsothatitadjoinedanexistingoldpeople’shome. Initiallytherewasnointernalaccessbetweenthetwohomes.Threeweeksafterconstruction,an interconnectingdoorwasinstalled.Theproprietorstatedthatthiswasduetofinancialconstraints imposedbecauseoftheunexpecteddeathsoffiveresidents.

Itwasheldthattheinitialintention(decisivetotheVATtreatment)hadbeentoconstructanew building.JMBStrowbridge[1999](VTD16521)

4.Anewdwellingincorporatedasinglewallofapreviousbuilding,whichwasnotrequiredby planningconsent.

Itwasheldthattheworkrelatedtoanexistingbuilding.Eventhoughanewbuildingwas undoubtedlyconstructed,theincidentalincorporationofasmallpartofanexistingbuildingwas fataltotheappellant’scase,becausethelegislationissospecific.PhilipEvans[2001](VTD17264)

5.Anursinghomewasconstructedonthesiteofanoldchurch.Thechurchitselfwas incorporatedinthenewnursinghome,comprisingthereceptionarea.

Itwasheldthatanewbuildinghadbeenconstructed,asthenewparthadaboutfivetimesthefloor areaoftheoriginalchurch.Itsodwarfedtheoriginalbuilding,thatitwasamisdescriptiontorefer totheworkasanenlargementorextensionofthatoriginalbuilding.Ingeneral,retentionofpartor allofanoriginalbuildingdoesnotprecludearulingthatanewbuildinghasbeenconstructed, albeitthatthecircumstanceshavetobeveryunusualforthattobethecase.HMRCvAstralConstruction Ltd[2015]

Constructionofa newbuilding?

✓

✓

✓

✓

x

x

520PARTICULARACTIVITIESLANDANDPROPERTY

50245 Notice708 paras3.2.1,3.2.2

2.DIYhousebuilders

HMRCwillrefundanyVATchargeableonthesupply,acquisitionorimportationofany goodsusedinconnectionwithbuildingsconstructedotherwisethaninthecourseof business.

Timelimit

Since5December2023,refundsmustbeclaimedwithin6monthsofthebuildingwork beingcompleted,thedateofwhichhasbeensubjecttomuchcaselaw

MEMOPOINTS 1.HMRC’spolicyistoallowonlyonerefundclaim,butitwillaccept supplementaryclaimsinrelationtoworkscarriedoutbeforetheoriginalclaimwassubmittede.g invoiceswhichhavebeenleftoutinerrororissuedlatebythecontractor

2.Theclaimperiodforclaimssubmittedpriorto5December2023was3months.

EXAMPLE

1.Ithasbeenheldthatthecertificateofcompletionissuedbytheclaimant’slocalauthorityisthe onlypracticalwaytodecidewhenabuildinghasbeencompleted.ThispreventsHMRCarguing thatthetimelimithasbeenmissedbecausethebuildingwascompletedbeforethecertificateof completionwasissued.Itremainsopentotheclaimanttoapplyearlier,inwhichcaseHMRCwill considertheevidenceofcompletionprovidedintheabsenceoftheusualcertificate.LiamDunbar [2019](TC07504)

2.Inamorerecentappeal,contradictingexample1above,itwasheldthateachcasemustbe decidedonitsownmerits.

Thereisnohard-and-fastrulethatthedateofacompletioncertificategovernsthetimelimitfor makingaclaim.PaulandStephenWedgbury[2020](TC07619)

3.InScotland,itisnotlawfultoinhabitapropertyuntilaNotificationofAcceptanceofa CompletionCertificatehasbeenissuedbythelocalauthority. Ithasbeenheldthatcompletioninthiscontextcannotoccurbeforeissueoftheacceptance.Simon andJoanneCotton[2020](TC07553)

4.TheappellantsmadetwoclaimsundertheDIYbuilders’scheme.HMRCpaidthefirstbut refusedthesecond,onthegroundsthatthelegislationprovidesforonlyoneclaim. Itwasheldthat,althoughthelegislationrefersto“theclaim”,itisabasicruleofstatutory interpretationthatthesingularincludesthepluralandviceversa.Hence,morethanoneDIYclaim canbemadeandHMRCoughttohavepaidthesecondone.Incidentally,thefirstclaimhadbeen madebeforecompletionoftheproperty,soHMRCwouldhavebeenwithinitsrightstorefusethat claimbuthadnotdoneso.AndrewEllisandJaneBromley[2021](TC08277)

Onlineapplication

Adigitalclaiminrespectof:

newpropertymustbecompletedattiny.cc/vm51105N;or

conversions,shouldbemadeattiny.cc/vm51105C. HMRCshouldcommunicatetheclaimreferencenumberwithin2weeksaftersubmission. Theclaimshouldthenbeprocessedwithin3weeksofallinformationrequestedbeing produced.

Paperforms

Apaperclaimisstillpossible,althoughanyrepaymentmaybedelayed.Thefollowing documentsmustbesubmittedtotheaddressat¶90120: Form Covers

VAT431NB Constructionofnewbuildsdesigned: –asdwellings;or –forusesolelyforcertainresidentialorcharitablepurposes

–

–

554PARTICULARACTIVITIESLANDANDPROPERTY 51075 s35VATA1994

reg201 HMRCBrief08/22 51105 51110

51100 SI1995/2518

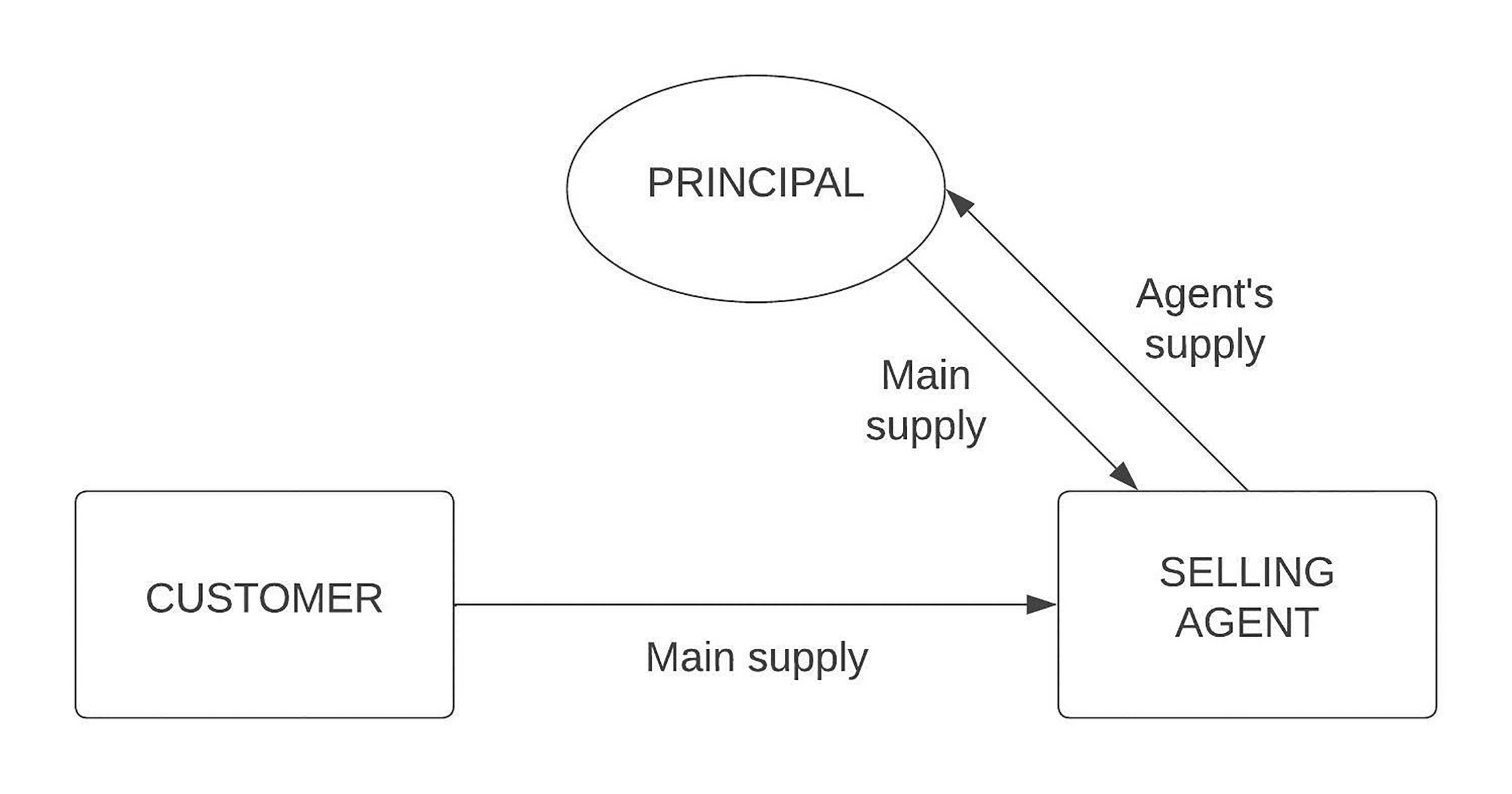

B.Undisclosedagents

Inanarrangementinvolvinganundisclosedagent,thecustomerwillonlydealwiththe agent,andindeed,willonlyreceiveaninvoiceintheagent’sname.Astheprincipal’s detailswillnotbedivulged,thecustomermaynotevenbeawareoftheprincipal’s existence

ForthepurposesofVATregistration,allsuppliesmadebytheagent(includingthoseby theprincipal)aremeasuredagainsttheregistrationthreshold(¶90000).

TheVATtreatmentdependsonwhetherthemainsupplyismadewhollywithintheUK,or whethertheprincipalorcustomerbelongsoutsidetheUK.Itshouldbenotedthat, irrespectiveoftheVATposition,thelegalstanceremainsunchanged.

MEMOPOINTS

1.Theprovisionofelectronicallysuppliedservicesortelecommunication services(¶62000+)throughanagentistreatedbothasasupplytotheagentandasasupplyby theagent.Fordigitalplatforms,see¶61205.

2.Foruseofthesecond-handmarginschemebyagentsandtheirprincipals,see¶58285.

3.Fortheprovisionoftravelinsurancebyatravelagent,see¶65730.

b.Treatmentasanagent

Treatmentasanagentisonlyavailablefordomesticsupplies(whenboththeprincipaland thecustomer,orsupplier,arelocatedwithintheUK).

Sellingagent

Inthiscase,thesellingagentaccountsforboththemainsupplyandthecommissionas separateoutputsontheVATreturn,recoveringinputtaxonthesupplyfromtheprincipal. Theself-billingprocedure(¶28925+)maybeused(subjecttoHMRC’sapproval).

EXAMPLEALtdactsasanundisclosedsellingagentforPLtd,whoisVAT-registered.ALtdarranges asaleofgoodstoMrsCfor£600(netofVAT)andchargescommissionof10%. PLtdraisesaninvoicetoALtdfor£600plusVAT. ALtdraisestwoinvoices: –£600plusVATtoMrsC;and –£60plusVATtoPLtd.

63500

s47(4)VATA1994

63560 63565

AGENTSPARTICULARACTIVITIES745

s47VATA1994; Notice700 para22.6

63570 Notice700para 23.1.2