LOUISIANAAGENT 2025

N O V E M B E R

COMPLIANCE

Recent Fortified Roofs Program

Bulletins Reinforce Long-

Standing COI Compliance Rules

Ben Albright, IIABL CEO

balbright@iiabl.com (225) 236-1357

COMPLIANCE

Recent Fortified Roofs Program

Bulletins Reinforce Long-

Standing COI Compliance Rules

Ben Albright, IIABL CEO

balbright@iiabl.com (225) 236-1357

Benjamin Albright

Karen Kuylen

Director of Insurance Programs jnewchurch@iiabl.com (225) 236-1350

Director of Accounting & Finance kkuylen@iiabl.com (225) 236-1353

Jamie Newchurch

Director of Communications & Events koregan@iiabl.com (225) 236-1360

Kathleen O'Regan

Karson Kyle

E&O Administrator lyra roberts@iiaba net (225) 236-1352

Communications & Events Administrator kkyle@iiabl com (225) 236-1351

Lyra Roberts

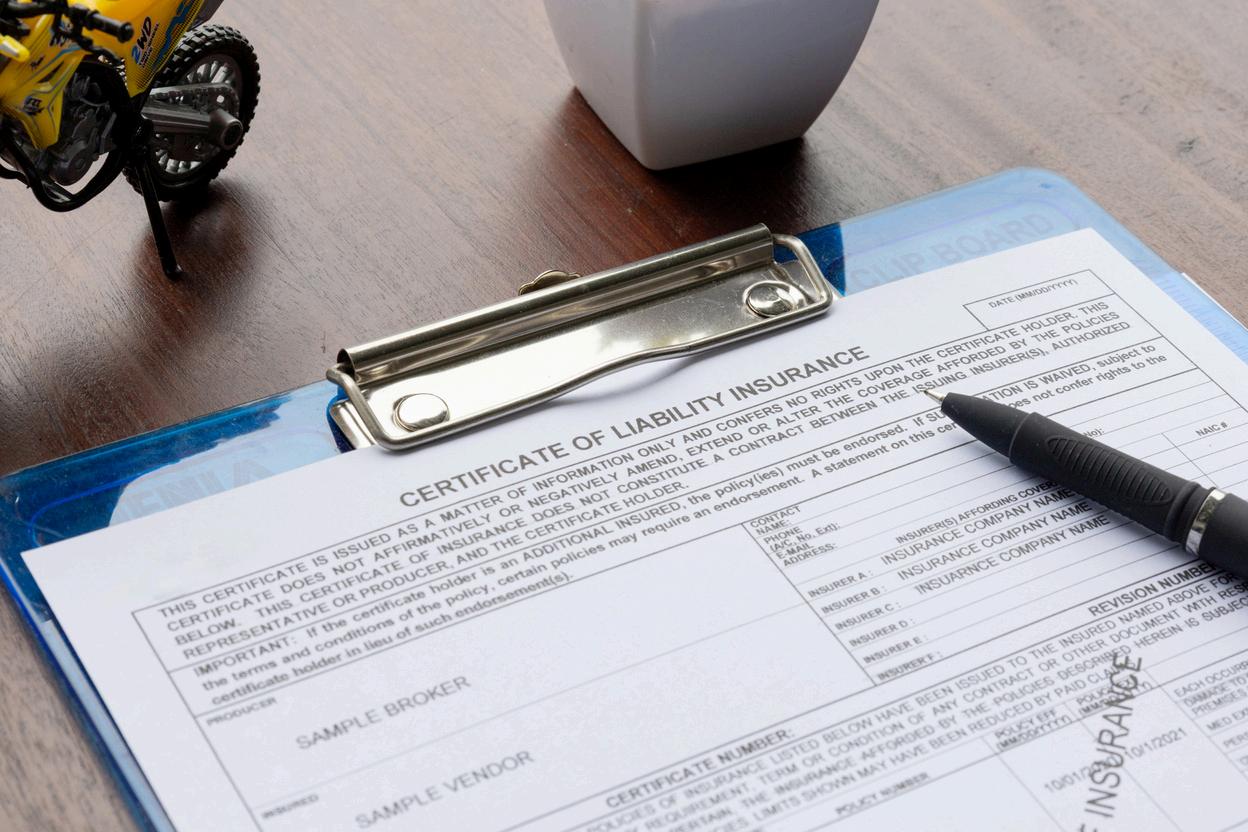

This article summarizes ongoing COI compliance issues tied to the Fortified Roofs Program and reinforces that Louisiana law, under R.S. 22:890, prohibits agents from making any coverage determinations on COIs, urging strict adherence and proper documentation.

Over the past few weeks, IIABL has sent multiple member alerts regarding improper Certificate of Insurance (COI) requests arising from the Louisiana Fortified Roofs Program. These requests—coming from contractors, IBHS, the Louisiana Contractors’ Board, and occasionally the Louisiana Department of Insurance—have ranged from questionable wording to outright demands for coverage statements that would put an agency in violation of state law.

These recent reminders present a perfect opportunity to revisit Louisiana’s guidelines for COIs, particularly the requirements found in R.S. 22:890, and to reinforce the best practices that protect both agencies and insureds.

R.S. 22:890

Louisiana law is among the most explicit in the nation when it comes to COI compliance, and that’s no accident. IIABL worked hard for many years to pass nation-leading protections for agents regarding certificates. Under R.S. 22:890, agents are prohibited from issuing (and others are prohibited from requiring an agent to issue) a Certificate of Insurance that:

· Amends, alters, or extends coverage

· Confirms coverage terms not found in the policy

· Makes statements about coverage applicability

· Suggests that certain exclusions do or do not apply

· Describes conditions or obligations not actually included in the insurance contract

In short: A COI cannot—and must not—make any representation that changes or interprets the policy. It can only reflect information that already exists in the contract exactly as written such as listing specific endorsements on the policy.

This applies universally, whether the request comes from a mortgagee, general contractor, parish official, lender, Fortified program contractor, or the Department of Insurance, themselves.

In our recent bulletins, IIABL highlighted a wave of COI requests tied specifically to the Fortified Roofs contractor community. Some contractors have requested language certifying:

· That policy coverage applies to residential roofing

· That no exclusions exist for “normal roofing operations”

· That coverage applies to subcontractors

· And many other requests.

Any such statement would be a coverage determination, which agents absolutely cannot provide. Only the insurer can make a determination of coverage.

1. Never add custom language unless it exists in the policy

· Beyond listing specific forms on the policy, agents should not customize COIs to describe coverage applicability

2. Decline any request that asks for confirmation of coverage applicability

· You cannot state whether coverage will or will not apply to a future loss. This determination can only be made by the insurer.

· If a COI requestor insists, send them R.S. 22:890 which explicitly prohibits them from requiring, or you from providing a coverage determination on a COI

3. Redirect parties to the policy, not your interpretation

· If someone wants proof or clarification, send them (with permission from the insured) the policy document.

· LDI’s Fortified Homes program and IBHS are both satisfied with documentation from the policy in lieu of a COI with customized language.

4. Document all unusual requests

· Keep a paper trail in your agency management system.

· Document requests, correspondence with underwriters, and any other relevant communications.

We know this issue is burdensome for agents. COI abuse—especially in construction and public-works environments— has long been a point of frustration for our members.

IIABL is actively advocating with regulators, contractors, insurers, Fortified program administrators, and other stakeholders to curb inappropriate demands and clarify the responsibilities of each party.

Our recent bulletins on the Fortified Roofs Program were sent because we heard directly from members facing repeated, high-pressure requests that would have forced them into non-compliance. You are not alone in this.

If a COI Request Makes You Uncomfortable, Call Us

Anytime you receive wording requests or pressure that “doesn’t feel right,” you should not respond under stress or urgency.

Instead:

Contact Ben Albright at IIABL!

Ben is happy to review the language and help you understand your obligations under Louisiana law. Many agents find that one quick conversation can avoid a compliance issue or an unintended E&O exposure.

Certificates of Insurance are meant to be simple, factual, policy-reflective documents— not negotiation tools, not contract compliance instruments, and certainly not coverage opinions.

KATHLEEN O’REGAN

IIABL DIRECTOR OF COMMUNICATIONS AND EVENTS

This article reflects on IIABL’s impactful year, highlighting major legislative wins in auto and property insurance, strengthened advocacy efforts, and great eevent

As we close out another fast-moving year in the independent agency world, it is worth pausing to appreciate just how much this association has accomplished. At IIABL, we measure success not by how busy we are, but by whether our work moves the needle for agencies across Louisiana. In 2025, the needle did more than move, it surged.

Our biggest headline of the year? A legislative session that proved why advocacy consistently ranks among the most valuable benefits of IIABL membership. With legal system abuse continuing to drive unaffordable auto premiums and market instability, Ben Albright and our legislative team worked tirelessly at the Capitol to secure meaningful reforms.

Louisiana made meaningful progress this year on long-standing cost drivers in both auto and property insurance. The most significant auto reform was the passage of HB 431, which updated Louisiana’s modified comparative fault standard. Under this change, an injured party may only recover damages if they are less than 51 percent at fault for the accident. This shift moves Louisiana closer to national norms and helps curb inflated litigation costs that have contributed to rising premiums.

On the property side, lawmakers strengthened underwriting and claims clarity with a new roofing permit requirement (HB 85), a fortified roof tax credit of up to $10,000 (SB 28), and clearer claims-handling and proof-of-loss standards through HB 437. Together, these reforms create a more stable, predictable insurance environment and give agents stronger tools to support clients when it matters most.

In a year when complicated, politically charged insurance issues dominated the landscape, IIABL remained a respected, credible voice, one that legislators listened to even when conversations were difficult. Our work is far from finished, but the progress is real, measurable, and deeply impactful for every agency and insured in our state.

It is impossible to recap 2025 without highlighting the Women in Insurance Conference. A high-energy event that shattered attendance records and brought powerful momentum to one of our most meaningful initiatives.

From dynamic speakers to actionable leadership sessions to the connection-building energy that filled the room, this event set a new standard for what professional development can look like in our industry. Members consistently cited it as one of the most impactful programs we delivered this year. Planning is already underway to make 2026 even bigger.

Our Annual Convention blended a country-club-chic theme with robust education, a vibrant exhibit hall, and family-friendly programming. Craig Zablocki’s keynote energized the crowd, Casino Night sparkled, and members made the most of their time in Sandestin with both business and beachside memories.

Our Young Agents Conference with Mississippi continued its growth streak with top-tier speakers, fresh engagement activities, and a theme that resonated deeply with emerging leaders. This event remains one of our most important pipelines for agency leadership development and 2025 proved exactly why.

One of the most inspiring parts of 2025 was watching our regional chapters lead with purpose in their own backyards. Local activity was not just strong, it was impactful, charitable, and deeply connected to the issues that matter most to our members and communities.

Greater New Orleans hosted two high-energy Town Halls focused on this year’s legislative developments, giving agents direct access to discussions shaping their daily work. They also organized a successful charity golf tournament benefiting Take Paws Rescue, raising funds and awareness for a cause loved by the local community. Baton Rouge delivered a full calendar with three luncheons; two dedicated to unpacking major legislative changes. They also hosted their annual Top Golf tournament supporting the Trusted Choice Disaster Relief Fund. Their Fall Social was another standout, raising money and collecting an impressive number of coats for Pat’s Coats for Kids, helping children across the region stay warm this winter.

Shreveport–Bossier remained an essential hub for industry conversations, hosting two legislative-focused luncheons that helped members stay informed amid a rapidly changing regulatory environment.

Northeast Louisiana matched that commitment with two of their own legislative luncheons, ensuring members across the region had access to timely updates and in-depth discussion.

Our Young Agents Committee truly embodied service this year. In addition to hosting their signature conference, they put on a spirited cornhole tournament, laced up for the Crescent City Classic, and adopted a family for Christmas through Life of a Single Mom that brings joy, connection, and support to a family in need.

Across every corner of the state, our chapters demonstrated that when independent agents gather with intention to learn, volunteer, or support local causes they create real change. This regional strength is one of IIABL’s greatest assets, and 2025 proved just how powerful it can be.

Ben Albright

December 2023

This fall’s Member Satisfaction Survey offered one of the clearest affirmations of all: our members see value. Agencies reported strong usage of IIABL products and services that directly improve efficiency, productivity, and bottom-line ROI from our competitive E&O program to trusted RLI products and education offerings that keep teams informed and compliant

Members also described IIABL in ways that reinforce our mission: reliable, supportive, essential, and advocates. Many agencies credited our communications for helping them stay ahead of rapidly changing legislative and market developments

Perhaps most meaningful were the heartfelt testimonials we received:

“We know who to call when an issue arises and can always expect expert guidance and leadership ” –Jay Garcia

“IIABL has been instrumental in the success and growth of our agency.” – Matthew de Blanc

“Governmental affairs alone is worth the amount we pay in dues then you add the other services, and it is the best use of agency resources I can think of ” –Bret Hughes

These endorsements matter to us, not because they praise our team, but because they confirm that the work you invest in through membership creates real, tangible value for your agency

Like any year, 2025 brought challenges: continued market instability, rising costs, talent shortages, technology stressors, and competitive pressures from every direction But those same challenges reminded us why a strong association matters Your feedback, engagement, and participation shaped our priorities and strengthened our determination.

As we look to 2026, our focus remains clear: deliver measurable ROI, protect and elevate the independent agency system, and help every member feel supported, informed, and empowered

Thank you for being part of IIABL, for showing up, for speaking up, and for believing in the work we do. Together, we are not just responding to an evolving industry, we are helping shape its future

Continued from page 12

crcgroup.com

The Independent Insurance Agents of Baton Rouge (IIABR) hosted their November luncheon on November 20 at Juban’s Restaurant & Bar, featuring guest speaker Christopher Patin, Shareholder at Laperouse Patin, LLC. Members gathered for an afternoon of insight, good conversation, and a great meal together.

Patin is a practicing attorney licensed in both Louisiana and Texas, with experience across all levels of state and federal court, including the U.S. Fifth Circuit Court of Appeals. His diverse background allows him to bring practical legal perspective to the insurance and business community, and his presentation reflected that strength.

During his talk, Patin walked attendees through several legal considerations that agents may encounter in today’s environment, offering clear explanations and helpful examples based on his active litigation work. Members appreciated his straightforward approach and the relevance of the issues he highlighted.

In addition to the educational portion, the luncheon provided valuable time for members to connect and enjoy the atmosphere at Juban’s. The conversation flowed easily, and the meal made for a warm, enjoyable setting to wrap up the afternoon.

IIABR extends its thanks to Christopher Patin for sharing his expertise and to all members who attended. We look forward to seeing everyone at future events as we continue building a strong, engaged insurance community in Baton Rouge.

CRC

Gulf

Homebuilders

Step by step, shot by shot, decision by decision. Behind every successful agent is a workers’ compensation partner they can trust completely.

IIABL 2025-2026

CHAIRMAN, ROSS HENRY

CHAIRMAN-ELECT, JOE KING MONTGOMERY

SECRETARY-TREASURER, CHRIS HAIK

NATIONAL DIRECTOR, JOEY O’CONNOR

PAST CHAIRMAN, BRET HUGHES

YOUNG AGENT REP, MICHAEL MOBLEY

IASC REP, DAVID DETHLOFF

ANN BODKIN-SMITH

MATTHEW DEBLANC

CHRISTY DESOTO

DOMINIQUE DICARLO CROUCH

ROB W. EPPERS

KARA GARZOTTO

MATT GRAHAM

BEAU HEAROD

CHARLES H. LEBLANC

CRAIG MARTEL

LYDIA MCMORRIS

EUGENE MONTGOMERY, III

HARTWIG "ROBBY" MOSS, IV

SETH OSTENDORFF

ROBERT LOUIS PALMER, JR.

RANDY PERISE

ROBERT STONE

JEFF ZEAGLER

Henry Insurance Service, Inc. - Baton Rouge

Community Financial Insurance Center, LLC - Monroe

Higginbotham Insurance Agency - Lafayette

Assured Partners - Metairie

Hughes Insurance Services, Inc - Gonzales

Moore & Jenkins Insurance Agency, LLC - Franklinton

Dethloff & Associates, Inc. - Shreveport

Thomson Smith & Leach Insurance Group - Lafayette

Continental Insurance Services - Marrero

1st Insurance of Marksville - Marksville

Riverlands Insurance Agency - LaPlace

Risk Services of Louisiana - Alexandria

DJW Insurance Agency - New Iberia

Lincoln Agency - Ruston

Jeff Davis Insurance - Jennings

Bourg Insurance Agency, Inc - Donaldsonville

Insurance Unlimited of LA, LLC - Lake Charles

Alliant Insurance Services - Baton Rouge

Community Financial Insurance Center, LLC - Monroe

Hartwig Moss Insurance - New Orleans

Dethloff & Associates - Shreveport

Insurance Underwriters, Ltd. - Metairie

Blumberg and Associates - Ponchatoula

Stone Insurance, Inc. - Metairie

McClure, Bomar & Harris - Shreveport