International Wellness & Spa Tourism Monitor 2013 (North America Edition)

The Tourism Observatory for Health, Wellness and Spa published the first benchmarking study on Spa and Wellness Tourism, titled the International Wellness & Spa Tourism Monitor in June, 2013. This path making report was prepared in cooperation with Danubius Hotels Group and enjoyed endorsement from over 50 global companies (e.g. Mandarin Oriental, Thermarium), and national and international organizations (e.g. PATA, ETC or Arizona Spa and Wellness Association). The IWSTM 2013 collected information from 50+ countries and from 420+ spa and wellness suppliers. The key objective was to identify the role travelling and vacations play at various spa and wellness suppliers worldwide.

The Report provides industry insights for operators, managers, investors and advisors. Data and information gathered is introduced and discussed in the Report in two major sections:

By regions (Africa, The Americas, Asia, Australia/NZ and Europe)

By spa and wellness supplier types.

We believe that it is essential to highlight: spa and wellness suppliers can come in numerous ways and types. The demand for these vendors is rather varied, too!

This IWSTM 2013 North America Edition provides intelligence regarding the following key themes:

Market Position of Suppliers

Supplier (types) Becoming Popular?

Services Becoming Popular?

Business Trend Forecasts for 2013 (number of customer and first time customers, average revenue per customer, number of treatments sold per visit)

Motivation of Clients

Popular Services & Treatments

Main Originating Countries (where tourists come from)

This Special North America Edition introduces information and data relevant to the North American market, both from demand and supply point of view.

The Tourism Observatory for Health, Wellness and Spa (TOHWS) an international intelligence initiative was created in 2012 by renowned advisors and researchers. The Health Tourism Worldwide is the full successor of TOHWS.

To us travel for health means travel for total health - either for medical purposes, or for wellness, holistic, spiritual, spa or medical wellness. This holistic approach to health makes HTWW the only global initiative looking at every aspect of the spectrum.

Copyrighted Material

Information, tables, and charts introduced in this document are the intellectual property of Health Tourism Worldwide. It may not be distributed or copied in any way or form, neither in parts nor as a whole without prior permission.

This report would not have been possible without the cooperation with the Danubius Hotels Group and Well-being Travel

www.danubiushotels.com

László Puczkó

Melanie Smith Ivett Sziva

Health, Wellness, Spas & Vacations

There is so much happening out in the market. The number of products and services being associated with health, wellness and spa is proliferating. The concept is being stretched and we can observe saturation in many markets (e.g. What do you think the label of ‘Car Spa’ may cause to the spa industry?).

We believe that the spectrum of travelling for health is very wide and it has many variations. The terminologies applied can differ greatly continent-by-continent or even country-by-country, culture-by-culture. That was one of the key reasons why TOHWS decided to launch its global initiative. The chart below provides us with a structured model of how we see the world of health travel and where wellness and spa may take part of that.

GlobalHealthTourismServiceGrid

The industry knows relatively little about the role of tourism and tourists in wellness and spa demand. With the IWSTM we made an attempt to map the likely importance of tourism. Also we collected information about services and trends so we can provide wellness and spa supplier managers, operators and investors with key benchmarking information.

Classification of Participating Suppliers

The world of spa and wellness suppliers is very wide and colourful. One of the key objectives of the research is to provide a better picture of this universe.

(please specify)

Spa and wellness suppliers are typically private organizations except in Central and Eastern Europe, where thermal/mineral baths are typically publically owned!

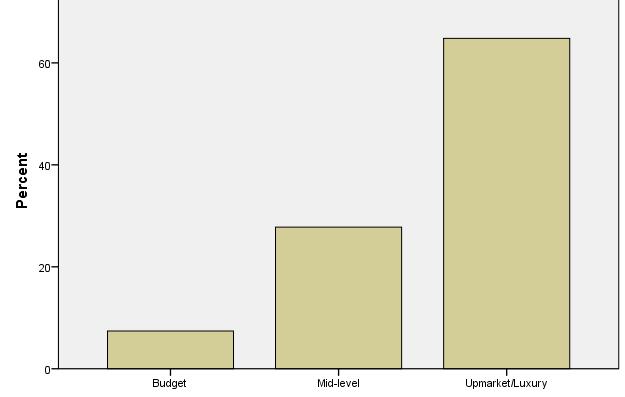

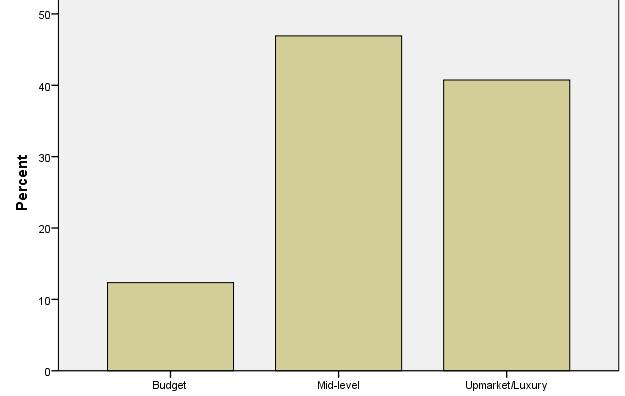

Participating suppliers could define themselves in terms of market position: budget, mid-level and upmarket/luxury. For benchmarking purposes apart from the relevant North American data we also discuss data and information from Europe.

North America

Market Position of Suppliers

Europe

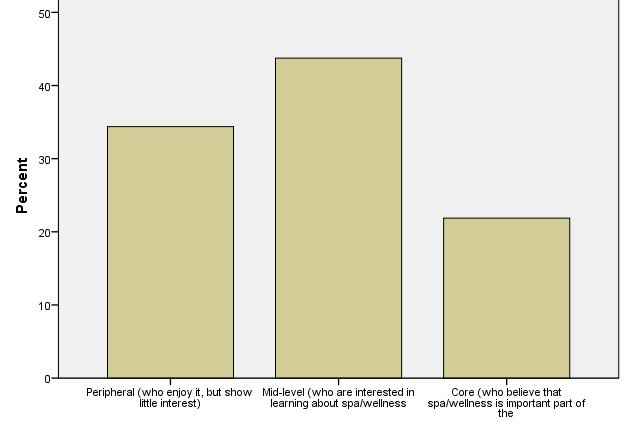

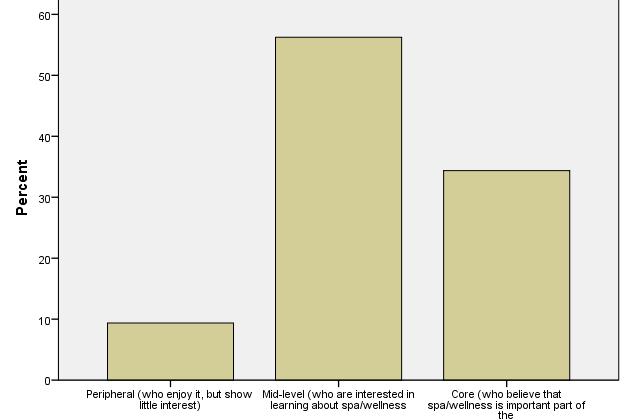

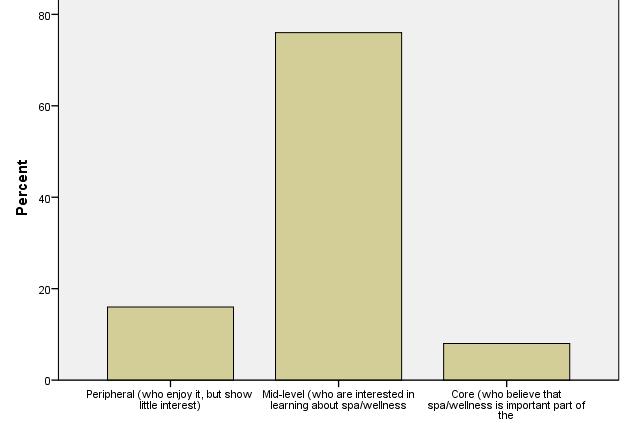

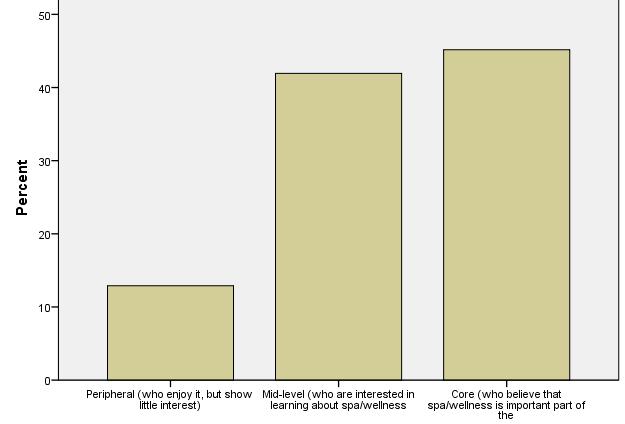

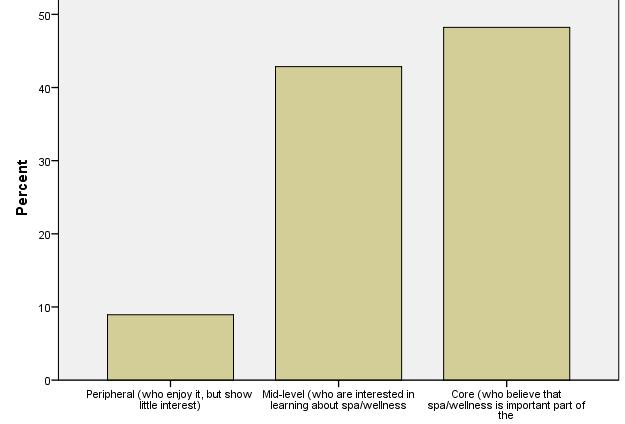

We applied the categorisation of the International Spa Association for the type of wellness and spa customers. According to ISPA:

Core clients are those who believe that spa/wellness is important part of their lifestyle

Mid-level clients are interested in learning about spa and wellness but have limited commitment

Peripheral clients enjoy spa and wellness services, but altogether show little interest.

These figures show one of the key strategic and benchmarking findings of IWSTM. International clients show strong dedication to what they are looking for, whereas domestic visitors are moderately being dedicated to spa and wellness.

This quite significant difference between the three major demand segments leaves both managers and investors with serious decisions to be made. It does not seem to be an easy conceptual and management issue to develop and run suppliers and services for a very mixed clientele. Expectations, activities and interests of local customers and foreign visitors are not the same. This anticipation and experience is confirmed by the global benchmark data.

TOHWS team has seen in many occasions that wellness and spa operations that let local market into suppliers primarily built for tourists struggled to provide servicesandqualityattheexpectedlevels!

Type of Clients

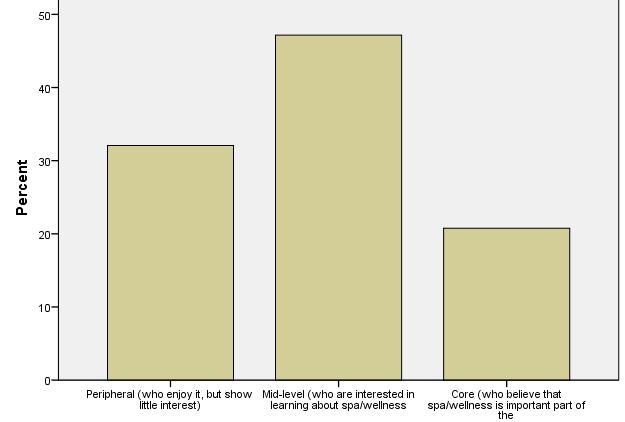

Local Market

North America shows relatively high level of market maturity in terms of local client mix. The majority of local clients show at least moderate interest for wellness and spa services, with relatively high propensity of core customers, too.

Domestic Clients

According to IWSTM North America is the most mature market since over 30% of domestic travellers are considered to be core customers who believe that wellness and spa are important part of their lifestyle.

North America

North America Europe

Interntional Clients

All assumptions are confirmed by the data describing international tourists, i.e. most of them are core customers. Australia/New Zealand is the only exception (most likely due to distances).

North America Europe

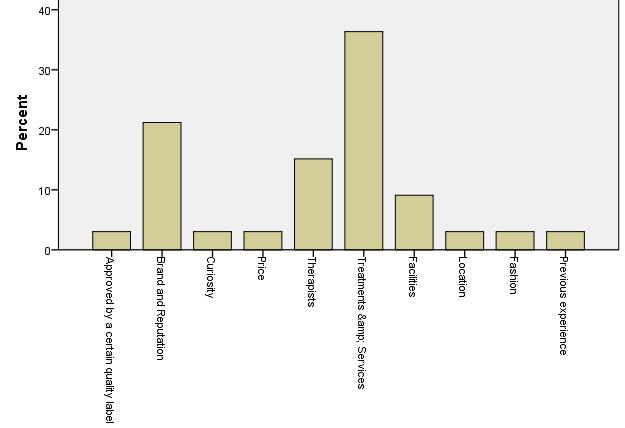

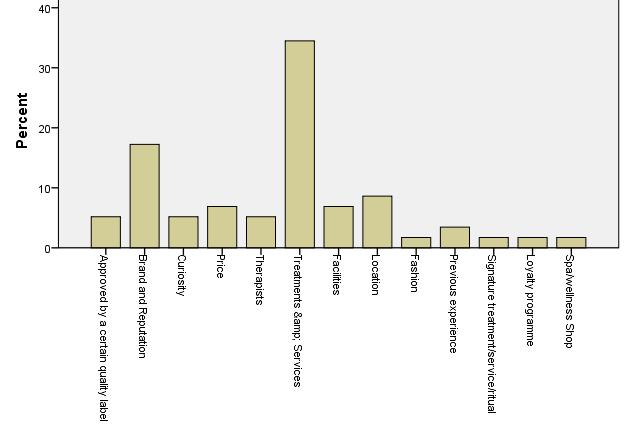

Motivations of the local market

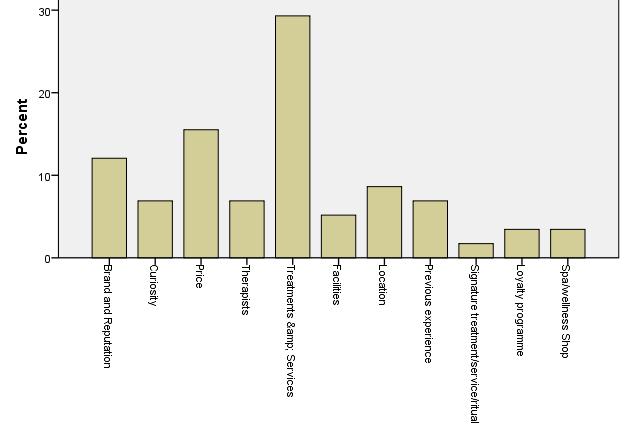

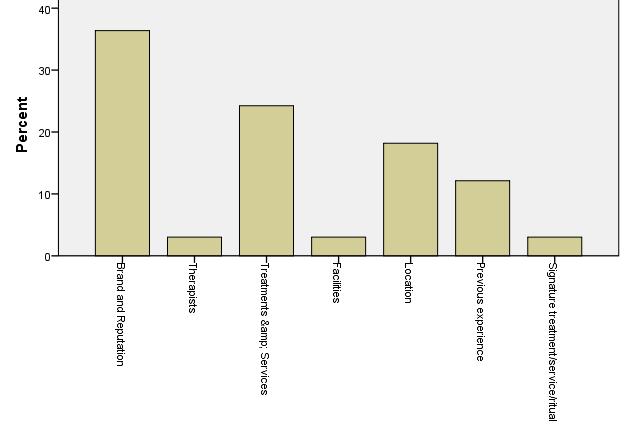

The key motivations of local market, domestic and international client tend to show similarities, but still, several and quite important differences can and have to be highlighted. Prices and therapists are (not that surprisingly) important mainly for local customers. The location and the availability of signature treatments are significant for tourists and especially for international tourists. Previous experience is not determining factor for international tourists, which means that they are visiting new sites and suppliers and show low level of loyalty.

Wellness and spa clients in North America and Europe (also in Asia) have very diverse set of motivations. Local clients are typically motivated by wellness and spa treatments and services in most regions, with numerous exceptions.

North America Europe

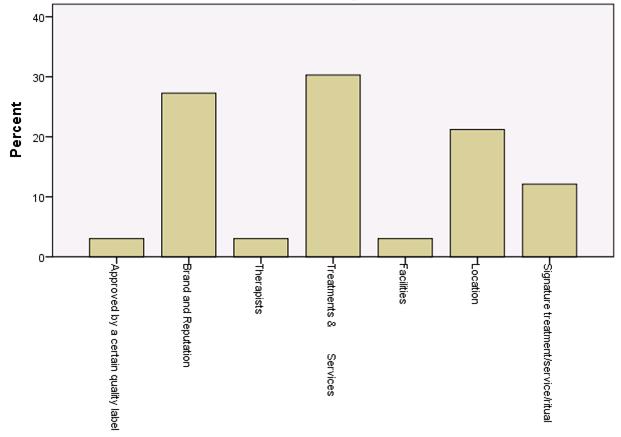

Motivations of domestic clients

Looking at the motivations of domestic tourists we can see that brands and reputation play significant role in North America and to certain degree in Europe, too.

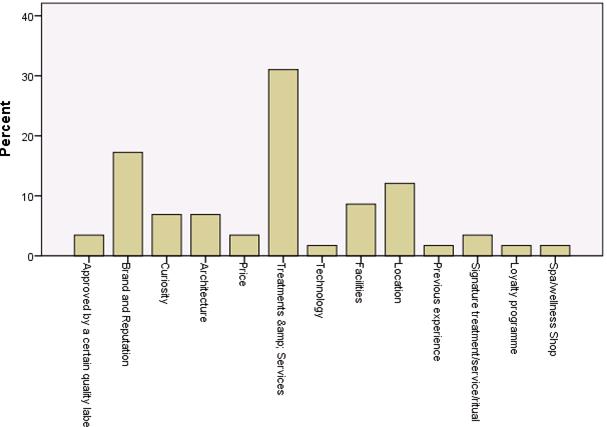

Motivations of international clients

International clients are dominantly motivated by two factors, i.e. the treatments and services offered by, and the brand and reputation of wellness and spa suppliers.

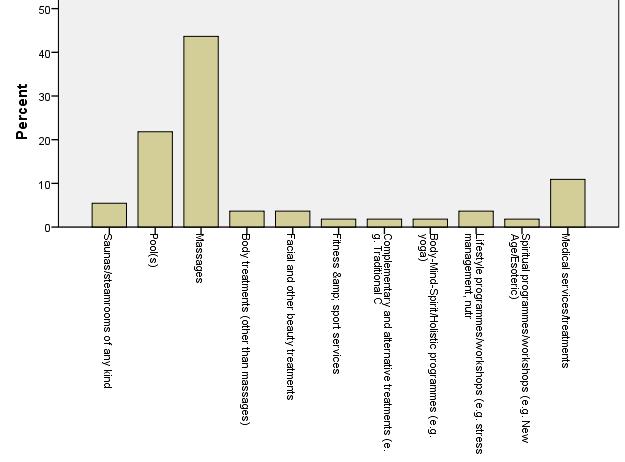

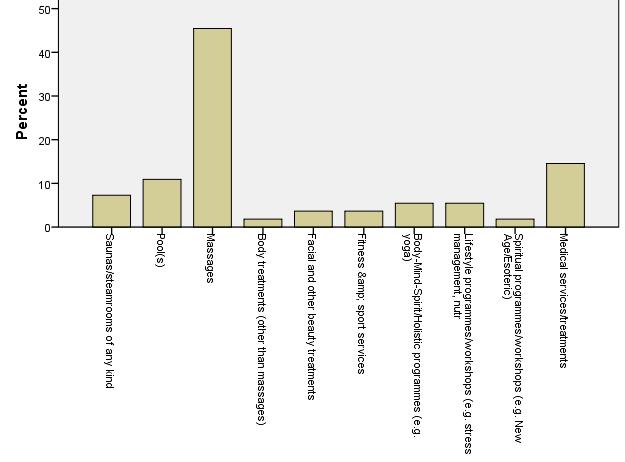

Popular services

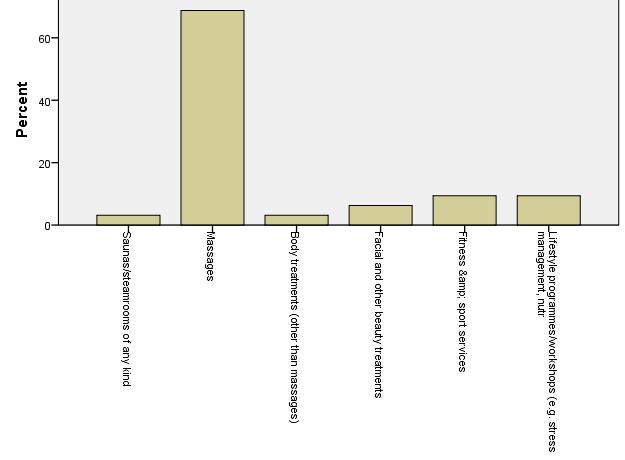

Popular services are where we can see the three guest groups being the most similar. Also not unexpectedly, massages are the most popular services on offer in wellness and spa suppliers. Saunas and steamrooms are not that significant for international client, but they show a growing interest in medical services at wellness and spa suppliers. Interestingly as we saw it before, lifestyle-oriented suppliers are getting popular, but this is not case for lifestyle programmes and workshops!The most popular services are the massages

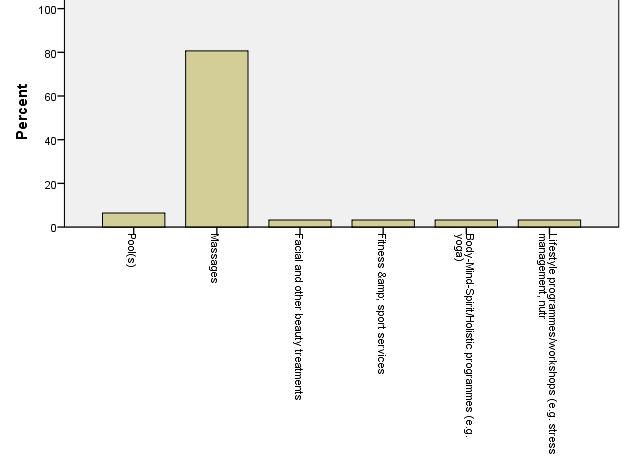

It seems that for domestic clients nothing else is important but massages! This is definitely the case in most regions analysed.

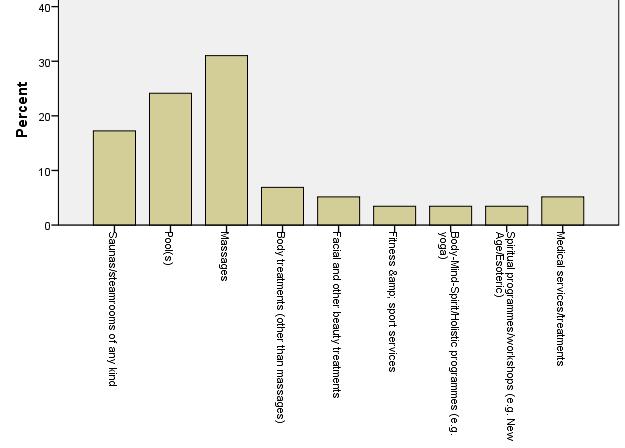

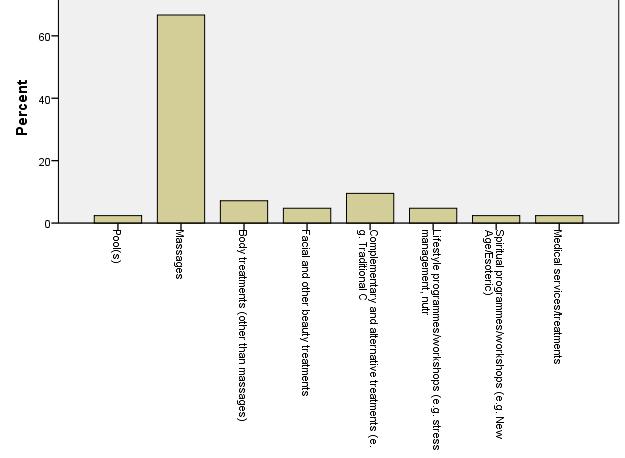

Popular Services International Clients

Foreign clients look for less number of services than domestic tourists. Evidently massages are the most popular services, but body treatments are also relatively popular.

North America Europe

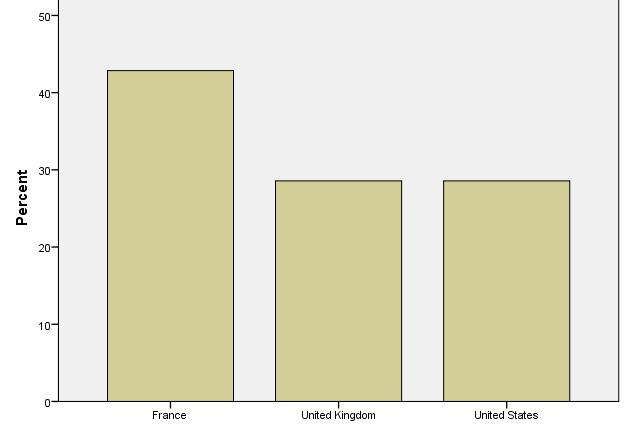

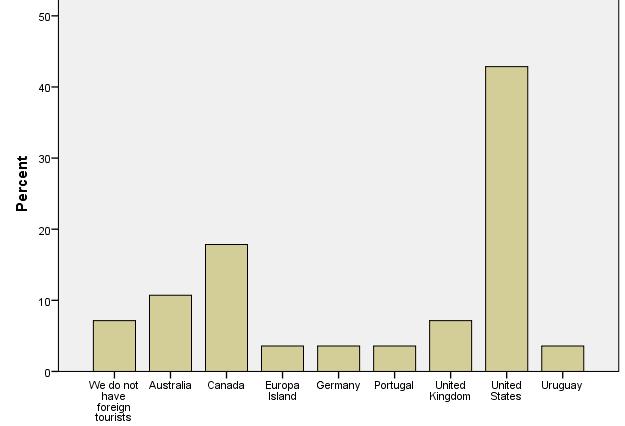

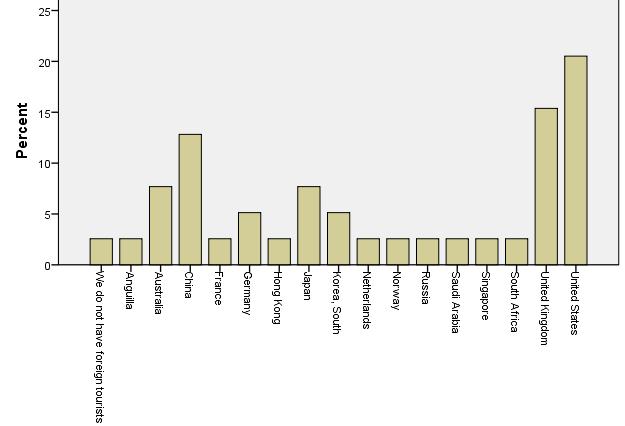

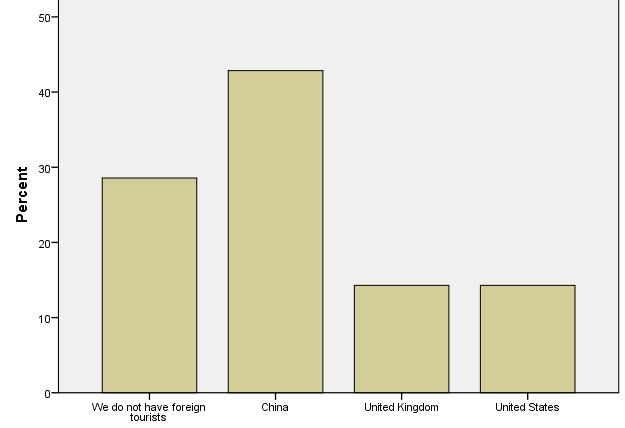

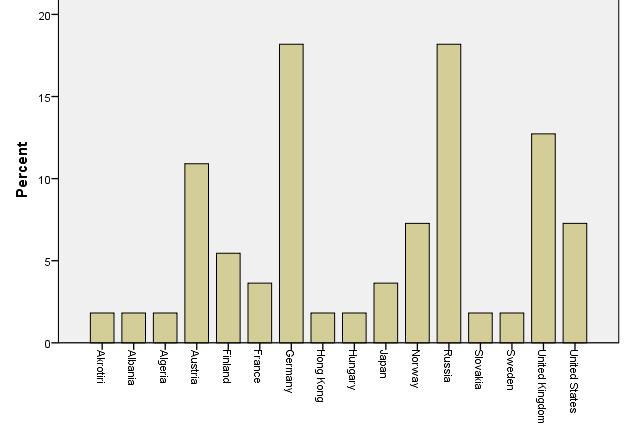

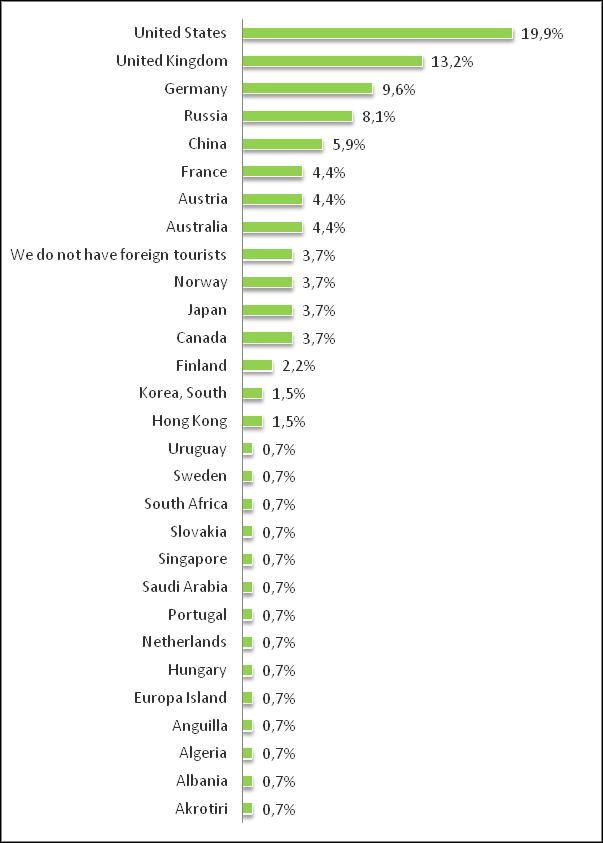

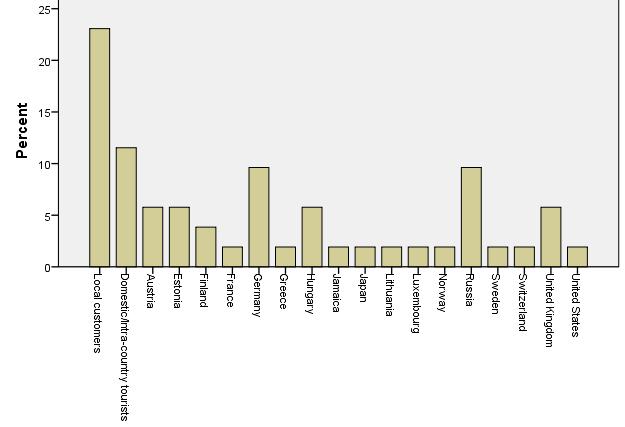

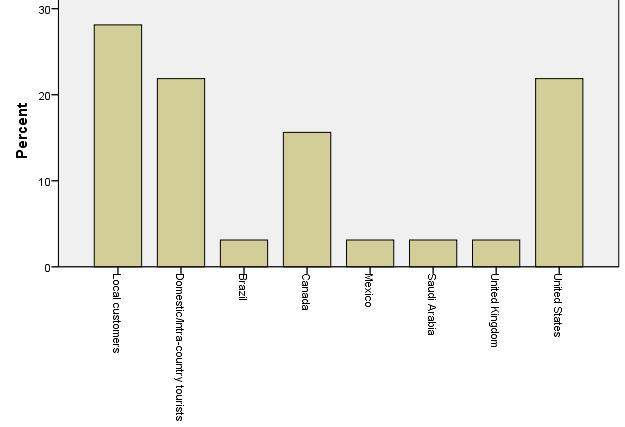

Generating Countries

IWSTM states that the USA is the leading country generating spa and wellness vacations, since in every region American travellers play significant role. This also means that the American vacationers happily travel for and use wellness and spa services almost anywhere they go.

Asia

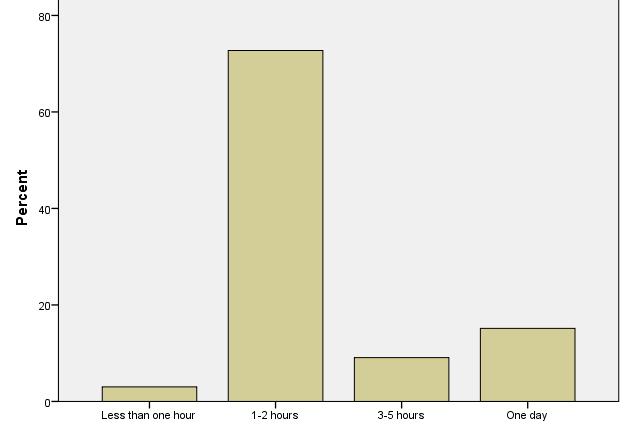

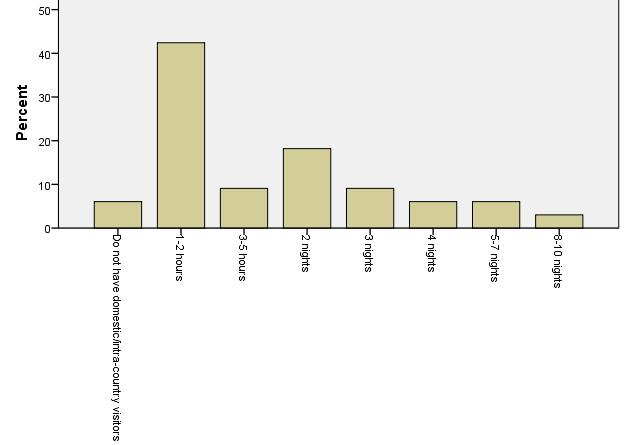

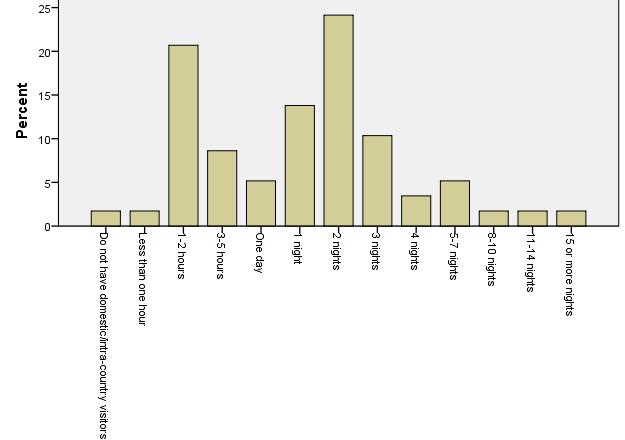

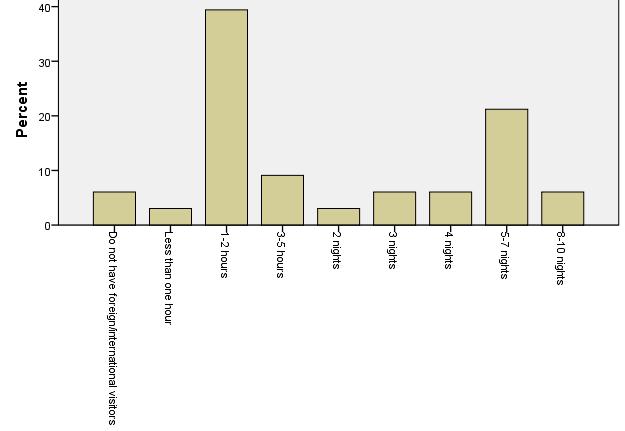

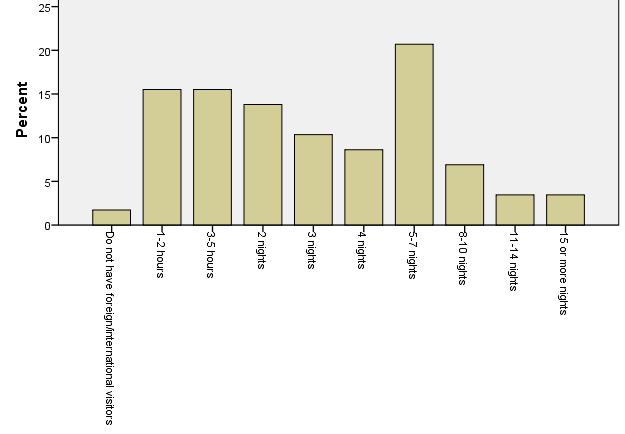

Business performance is very much linked to the average length of stay at wellness and spa suppliers. This is one of the planning and management areas that is often overlooked! Local customers spend rather short time at wellness and spa suppliers (2/3 spend less than 2 hours).

Local market Length f Stay

Length of stay

Sadly the short average length of stay also characterizes domestic and to a lesser extend foreign segments, too. Data show a typical pattern of weekender domestic market and one week long stay international clients Onetwo hour visits dominate the wellness and spa demand in every region. Although in Europe even shorter stays are not uncommon. Still, the importance of short visit customers is less influential in Europe (where the figures are under 60%).

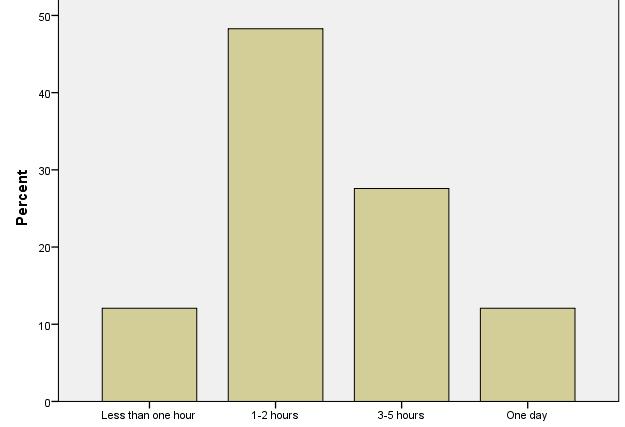

Length of stay Domestic Clients

Domestic client show different patterns in terms of their length of stay looking at the 5 regions, Europe counting for the longest average stays.

The figures for international clients indicate that international tourists often visit wellness and spa suppliers but would not stay overnight. This is due to the varying nature of suppliers, where many types do not provide accommodation (e.g. thermal baths).

Length of stay International Clients

Complementary products and services of customers

There are heated industry discussions about with what kind of other services can wellness and spa be packaged together. Somehow unexpectedly business events were mentioned as the one that can most likely be complemented with wellness and spa.

Conferences, congresses, business meetings

Religion/spiritual sites and events

The first position of business events is very much questions since conference and meeting organizers had to recognize that participants of business events and congresses may not want to socialize with colleagues or bosses in a wellness supplier or in a spa (or in the sauna!). Business events often organized in wellness or spa hotels and resorts. The use of wellness and spa suppliers, however, is rather low.

Weddings and honeymoons, or golf or the sea have traditionally been strong ‘allies’ for wellness and spa services. Local specialities are still important, e.g. ski and spa (during the skiing season) is a very competitive package.

Mountain locations, adventure and eco activities have recently become interesting alternatives and partners for wellness and spa suppliers and services.

Complementary products and services of customers

Elements of Packages

Nr 1

The regional comparison of popular complementary products show somewhat different focus points, but do not differ greatly.

Religion & spiritual sites and events Eco activities Sea

Business changes 2012/2011

Global recession did not leave the wellness and spa demand unaffected. Suppliers reported close-to-zero increase in the main business indicators for 2012 over 2011. Still, the relative growth of first time local customers can be considered as really good news!

Number of first time customers?

Average revenue per customer?

Number of customers using spa/wellness treatments, programmes?

Number of customers (altogether)?

Average length of stay per visit?

Number of treatments sold per visit?

Europe experienced the worst performance in 2012 over 2011 since most indicators were either stagnating or decreasing. Africa and Australia/New Zealand, on the contrary showed healthy growth regarding local cusromers, especially in customer numbers. Indicators also show that the average revenue per customer grew at higher rate than the number of treatments sold, i.e. the average revenue per treatment per customer had better results than one year before.

Average revenue per customer?

Number of treatments sold per visit?

Average length of stay per visit?

Number of customers using spa/wellness treatments, programmes?

Number of first time customers?

Number of customers (altogether)?

Business changes

2012/2011

Figures for local customer and for domestic tourist show remarkable similarities, which is again linked to the economic recession in 2011 and 2012. Still the moderate growth of average revenue per customer shows signs of slow recovery.

Number of customers (altogether)? Average revenue per customer?

Number of first time customers?

Number of customers using spa/wellness treatments, programmes?

Number of treatments sold per visit?

Average length of stay per visit?

Those wellness and spa suppliers that cater for tourists, too, seemingly had a better year than those concentrating on local customers only. Even in Europe, where the general picture is not positive, the results from domestic tourism are better. Domestic/intra-country tourists had a rather positive contribution to business performance in The Americas, in Australia/New Zealand, and Africa’s figures indicate steady growth of domestic wellness and spa oriented tourists!

Average revenue per customer?

Number of treatments sold per visit?

Average length of stay per visit?

Number of customers using spa/wellness treatments, programmes?

Number of first time customers?

Number of customers (altogether)?

Business changes 2012/2011

In spite of all that economic trouble, international tourism for wellness and spa services showed a relatively good performance! Number of customers, number of treatment and revenues as well could grow.

revenue per customer?

Number of customers using spa/wellness treatments, programmes?

Number of first time customers?

Number of customers (altogether)?

Number of treatments sold per visit?

Average length of stay per visit?

One might find unexpected, but as in many other aspects of the economy, Africa showed remarkable growth in international tourism performance in 2012. Even in Europe, where local and domestic demand had a negative zero result, international tourism achieved relatively good results.

Average revenue per customer?

Number of treatments sold per visit?

Average length of stay per visit?

Number of customers using spa/wellness treatments, programmes?

Number of first time customers?

Number of customers (altogether)?

Business Forecasts for 2013

2013 seems to bring great news in terms of first time visitors, since those who come to wellness and spa suppliers for the first time outnumbers other key growth factors.

Average length of stay?

Number of treatments sold per visit?

Average revenue per customer?

Number of customers (altogether)?

Number of customers using spa/wellness services?

Number of first time customers?

The forecast by regions shows a bright year for The Americas in terms of customer growth, whereas suppliers in Australia and New Zealand will welcome high number of first time customers.

Average revenue per customer?

Number of treatments sold per visit?

Number of customers using spa/wellness treatments, programmes? Average length of stay per visit?

Number of first time customers?

Number of customers (altogether)?

Altogether 43% of all spa & wellness customers are considered to be tourists, i.e. operators and investors need to take the needs and expectations of tourists into serious consideration. Spa and wellness suppliers can count on tourists in 2013 in terms of length of stay and treatments sold. This is in contrast with what is forecasted for local customers!

Business Forecasts for 2013

Average length of stay?

Number of treatments sold per visit?

Average revenue per customer?

Number of first time customers?

Number of customers (altogether)?

Number of customers using spa/wellness services?

In terms of visitor numbers Europe and Asia can count on spa and wellness tourists, which can provide a relief to Europan suppliers, which are still affected by the recession in Europe.

Clear message to spa and wellness operators. If they want or need to have local customers to their tourism suppliers they should think of family oriented and aco-minded suppliers

Suppliers Becoming Popular

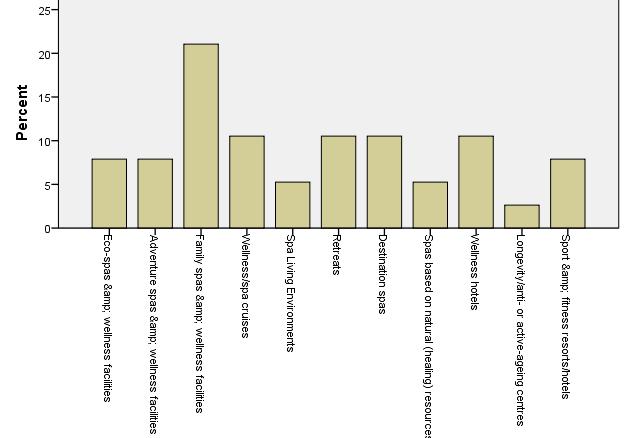

The product width is widest in Europe and North America, i.e. developers and managers from these markets can think of the most types of spa and wellness services, but with significant differences in regional focus points. Family and ecoorientation are important on these markets, but natural (healing) resources will enjoy special attention in The Americas, but much less of in Europe (since it is already more established there).

Note: anti-ageing or longevity seem to be important services, but travellers may not choose to visit spa and wellness suppliers that are specialized to such treatments!

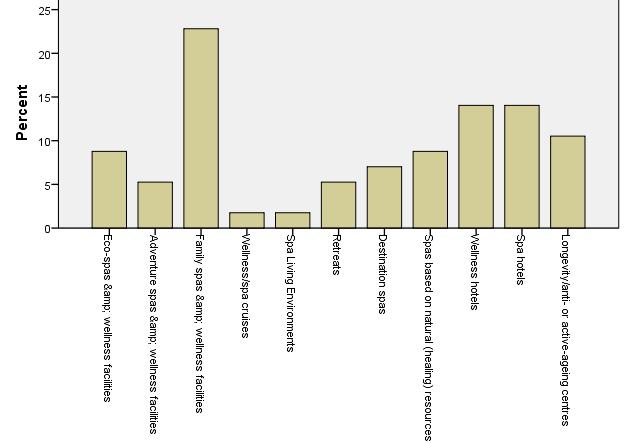

Domestic travellers show similar patterns to local customers, which makes product development and supplier management easier. Still, wellness hotels and destination spas are more; sport & fitness resorts are less popular among them.

Suppliers

Becoming Popular

There is little similarity between the projections for the domestic market for the five regions: except family orientation which seems to be the most likely direction everywhere, except in Australia, where eco-orienation is the clear leading trend.

Europe

Hint: look for how similarities and differences in terms of supplier types and service offer! Popular service concepts can be adapted (and not copied!) to various spa and wellness supplier types!

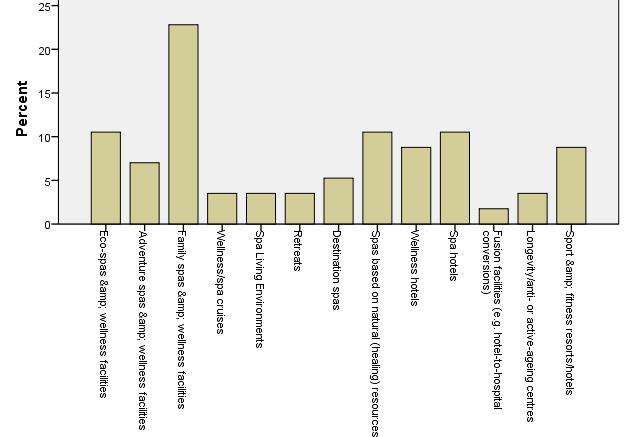

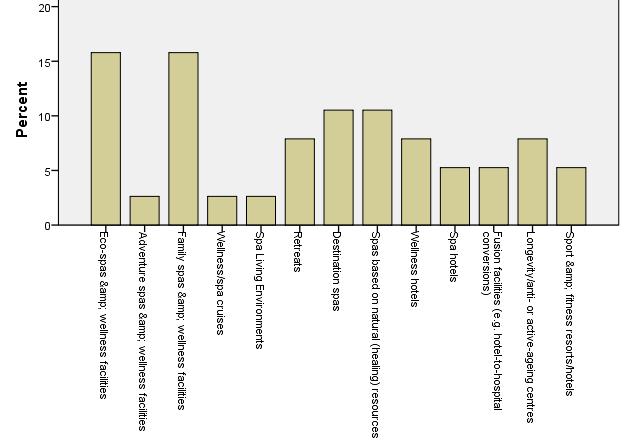

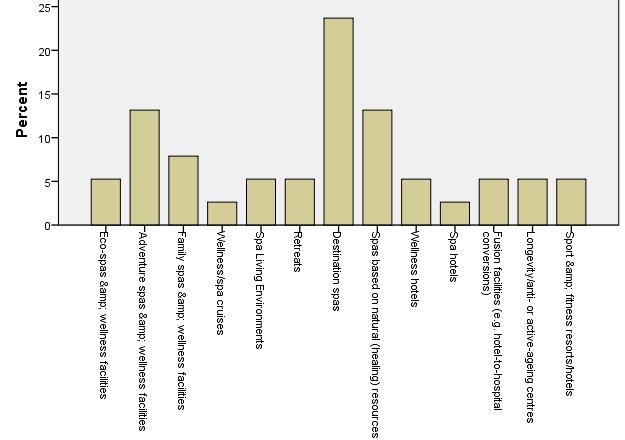

North America

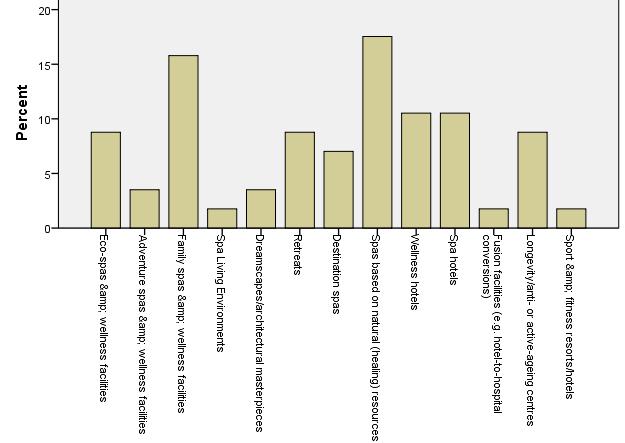

Great to see that the market is moving on from the standard wellness hotels and spa hotels which were the leading suppliers some 5 years ago. As of 2013 destination spas are taking the lead and became the most attractive suppliers for international tourists. International clients can also be attracted by spas based on natural (healing) resources. Eco-spas and wellness suppliers have also gained significant role in the last couple of years. International tourists are very sophisticated and do know rather well what they are looking for. Make sure you avoid spa or wellness washing (e.g. labelling your services something which actually it is not)!

Europe North America

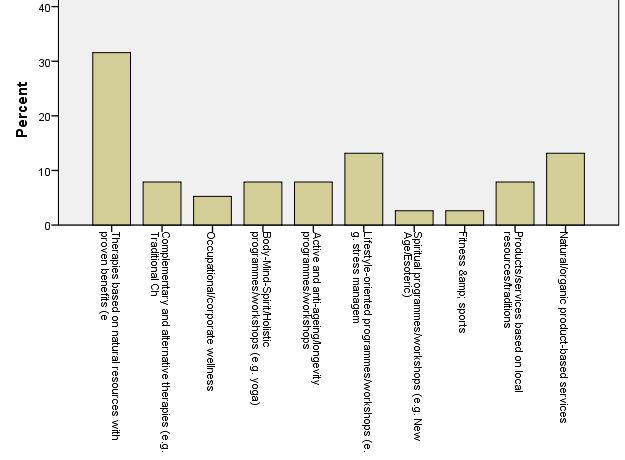

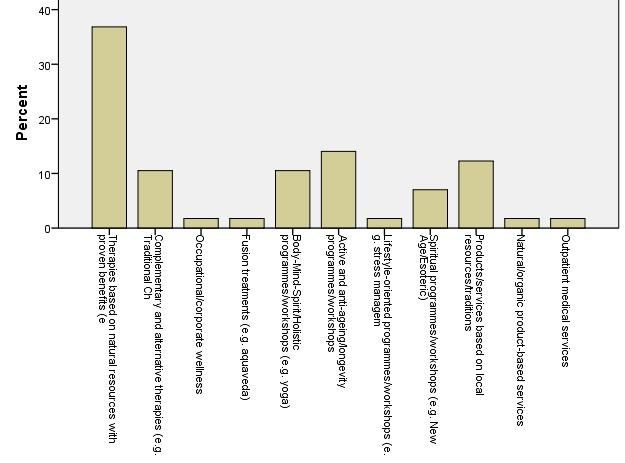

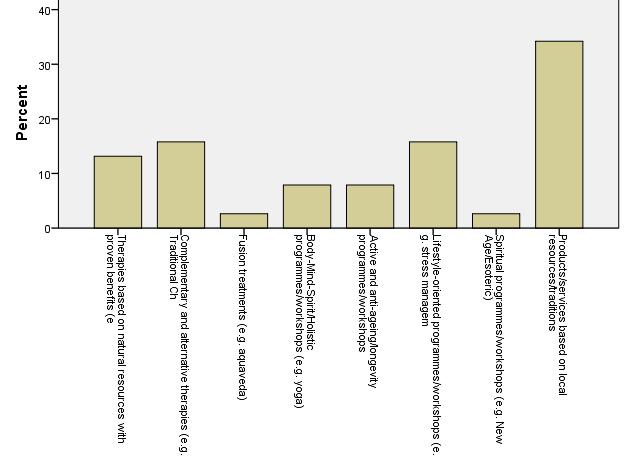

Services Becoming Popular

Operating and investing in spa and wellness in The Americas leaves interested parties with many options, since the market is mature and happily welcomes wide variety of services. The product width is also very wide in Asia and Europe, but there are clear leaders in the market.

Europe

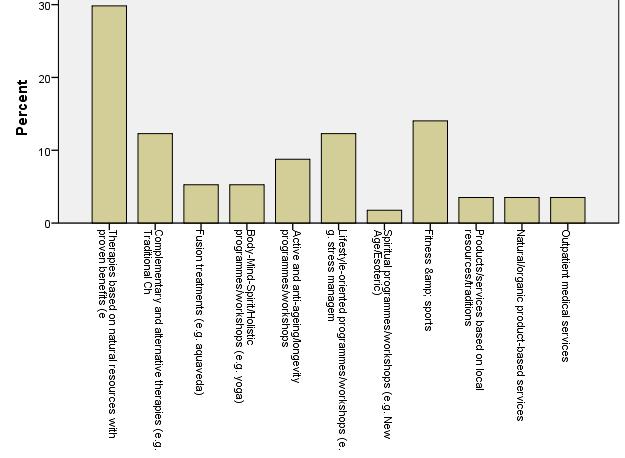

America follows a different pattern from the other regions, since longevity programmes are the leading services for local customers. Customers in other regions look more for services based on natural resources. This is partially due to the lack of data, evidence and tradition of how services and treatments based on natural resources can be used in spa and wellness suppliers in the Americas.

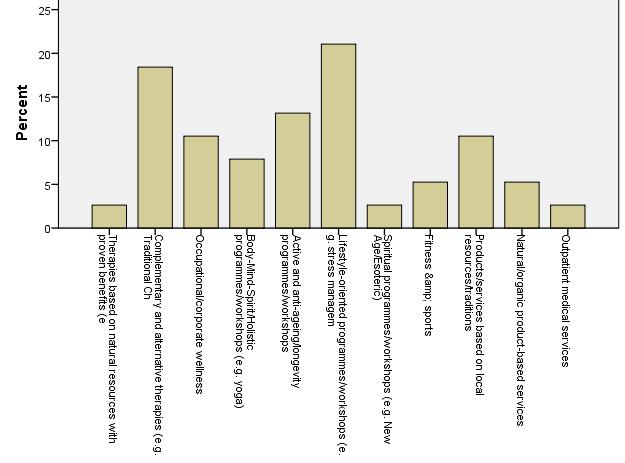

Domestic tourists show a somewhat different interest. Although therapies based on natural resources are clearly the most attractive ones, natural and organic products used in therapies and treatments are also play important role. That is somewhat unexpected that domestic tourists do not find spirituality and fusion therapies and treatments too attractive. Interesting, however that occupational and corporate wellness programmes are more and more combined with travelling away from the workplace.

Since family oriented suppliers are expected to be popular, lifestyle and anti-ageing services can and should be developed and offered to various segments. Especially if those are based on natural resources!

Services

Becoming Popular

Africa shows an interesting trend: domestic travellers are getting more sophisticated in terms of services (and less in terms of supplier interests). In Australia, on the other hand, tourists are attracted by only a few services.

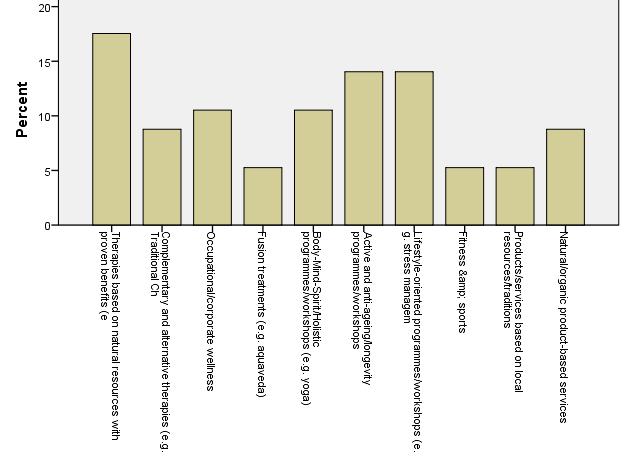

International tourists seem to be primarily motivated by treatments and therapies that are somehow based on local assets, resources and traditions.

Holistic approaches or holism is often considered to be similar or equal to spirituality. This is misunderstanding can lead to unsuccessful operation and/or disappointed customers. Interestingly fusion treatments did not become influential, although it seemed otherwise some years back.

Besides the importance of natural (healing) resources, lifestyle-oriented programmes and treatments are becoming influential in Asia and Europe. Active and anti-ageing also gains importance in Europe together with occupational and corporate wellness services away from the workplace and away from home.

Wellness and spa services that are based or influenced by holistic approaches can really motivate tourists to go on a foreign trip. This include body-mind-spirit, lifestyle-oriented and active or antiageing programmes and workshops.

Africa

Becoming Popular

Europe Americas Services

Global averages could easily hide significant regional differences. International tourists to wellness and spa suppliers in The Americas are nothing like the ones in Asia or Europe

The evidence and the traditions. These are the most significant differences between therapies based on natural resources (important in the Americas) and resources with natural healing properties (important in Europe or Asia). Providing customers/tourists with sound, proven and reliable evidence can and will make a difference.

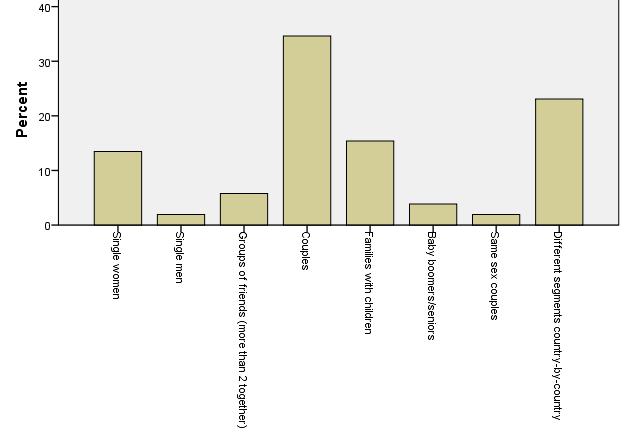

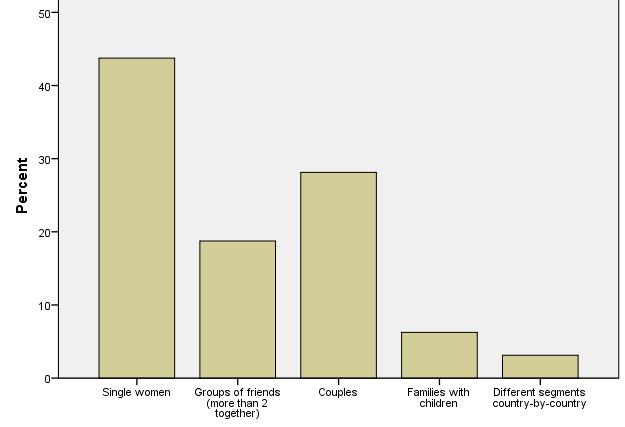

Target markets No1

Wellness and spa suppliers could list their key target markets (note: these can be different from the actual key markets seen in corresponding data!). Information shows that the five regions follow different market targeting strategies.

Targeted key segments

One industry rule-of-thumb for many year seems to become an old wisdom. Couples as most important target segments took over the leading position from single women.

Local customers are the most important market segment followed by domestic tourists (with the exception of Africa). Local customers represent upto 30% of targeting, i.e. some 70% of customers at wellness and spa suppliers are expected to be either domestic or international visitors. Previously could see that the average share of tourists was about 43%, i.e. suppliers are working on to attract more tourists!

Having a close look at the data we can see that the wellness and spa demand shifted to become a social consumption: couple, families, groups of friends give the majority of the demand. Several other segments, such as GenZ, Less able-bodied customers and mother & baby/child groups seem to be not at all important to operators. This is especially interesting since we know that 50% of the world’s population is under 30 years of age, i.e. GenZ should play much more important role that it actually does nowadays.

Proper and focused segmentation is essential. This is a key rule for any marketer, manager or developer. And that is why we cannot say that wellness or spa customers are uniform. Europe Americas

Contemporary segmentation is lifestylebased and that is completed with demographic information. Lifestyle-based segmentation, however, is a very much different region-by-region, or even cultureby-culture!

Wellness and spa visits are clear social occasions in Australia/New Zealand, whereas Europe remains to be the most challenging region

Should you wish to learn more about where and how the world of health tourism is going look for the second and revised edition of our book titled: Health, Tourism and Hospitality. Wellness, Spas and Medical Travel (published by Routledge, in Q4 2013).

Worldwide coverage, in-depth industry analysis, 40+countries, 50+ case studies