The business journal for doctors in private practice

In this issue

Relieve stress: live with it

Tips for managing stress on the job – without trying to eradicate it P20

The diary of a clinic build

Developing your own premises requires putting on a hard hat P34

Don’t think you can skimp on cover

A legal look at what you need to know about medical indemnity and insurance P40

Tax drive to hit doctors

By Robin Stride

Moves to improve tax compliance could backfire and lead to some doctors cutting their commitment to the private sector, specialist medical accountants warn.

HM Revenue and Customs (HMRC) has announced:

➲ A tightening up of compliance issues for ‘wealthy individuals’. Accountants say most consultants would be regarded as wealthy in the taxman’s eyes;

➲ The introduction of new technology to tackle the ‘hidden economy’ – such as a few consultants who accept cash;

➲ An increasing attack on tax avoidance schemes. HMRC believes doctors and dentists are serial users of these;

➲ New measures from April 2019 to quickly recover tax through PAYE.

‘Hidden print’ in last Autumn’s Budget suggests further trouble for private consultants and GPs who have been less than meticulous with their tax affairs.

But Ray Stanbridge, of Stanbridge Accountants, said: ‘The measures increasingly reflect HMRC’s views that the medical sector is a ripe apple to be squeezed harder and harder. Obviously, in some cases, the proposals are fully justified.

‘However, the vast majority of consultants are honest with

respect to their tax affairs. If such honest consultants are squeezed too hard and unfairly, they respond by withdrawing their labour and increasing their leisure time. The natural result is that there is less tax take – the complete opposite of what was intended.’

He said HMRC’s plan next year to be able to recover tax through PAYE might mean consultants would not be able to plan their monthly net pay if they owed tax. ‘At the very least, this could lead to some individual discomfort.’

The Government is investing a further £155m in additional resources and new technology for HMRC.

The tax authority said this was forecast to help bring in £2.3bn of additional tax revenues by allowing it to:

Transform its approach to tackling the hidden economy through new technology;

Further tackle those who are engaging in marketed tax avoidance schemes;

Enhance efforts to tackle the enablers of tax fraud and hold intermediaries accountable for the services it provides using the Corporate Criminal Offence;

Increase its ability to tackle noncompliance among midsize businesses and wealthy individuals;

Recover greater amounts of tax debt including through a new taskforce to specifically tackle tax debts more than nine months old.

David Redfern, of DSR Tax Claims, said: ‘Although it is important that HMRC is able to collect the tax revenue that they are owed, these new powers have the capacity to throw the finances of hard working taxpayers into chaos.’

HMRC must currently wait until the end of a tax year to recoup any shortfall in tax revenue from any individual taxpayer and is also required to write to inform the taxpayer that their tax code will change due to this underpayment.

He said if new powers gave it the right to deduct extra tax immediately from taxpayers’ salaries if it believed there was an underpayment of tax, then this could lead to taxpayers not knowing how much to expect in their salary each month.

Added Mr Redferm: ‘These new powers will cause major problems for taxpayers, who won’t be able to plan and budget ahead because they will be at the mercy of HMRC.

He doubted tax overpayments would be refunded as efficiently and hoped ‘good sense will prevail at HMRC’ and that the move will be delayed until its full consequences to the taxpayer had been assessed.

ONE OF A KIND: The first private hospital of its type in the UK has opened for business. Read the full story on page 8

get your skates on With the deadline nearing for filing your tax return, we give a few timely tips P14

Full steam ahead for PPUs 2018 is a great time for the nHS to invest in private patient units, an expert says P25

don’t risk your reputation advice on avoiding unforeseen mishaps that can attract the Gmc’s attention P28

when winding down your work plan for retirement by looking to dispose of notes and hand over patients’ care P38

Know your bias when investing your brain could stop you being a good investor. a look at behavioural finance P44

Suspicion of abuse business dilemmas looks at doctors’ ethical duties to domestic violence victims P46

editorial comment

Probe to have big fall-out

As the horrendous detail of the case of rogue surgeon Ian Paterson unfolded, it became clear that a much wider investigation was inevitable.

That is now about to get underway and the only surprise to us is that the Department of Health did not announce it earlier.

The independent nonstatutory inquiry, examining the circumstances and practices of this breast surgeon sentenced in August to 20 years in prison (see story on page 3), begins this New Year and could go on for a year and a half.

It is not expected to report until the summer of 2019 and,

as we went to press, independent practitioners and private hospitals were still awaiting the terms of reference.

We also wait to see how the inquiry, chaired by The Right Revd Graham James, Lord Bishop of Norwich, will be conducted and the extent of the areas it will delve into.

With the inquiry looking at the lessons that can be learned from the case, and how these can improve care, doctors and hospitals can expect no stone to be left unturned.

What emerges is likely to have some big implications for both parties.

tell US yoUr newS Editorial director Robin Stride at robin@ip-today.co.uk

University doctors face pension cut

By edie Bourne

Medical academics who are members of the Universities Superannuation Scheme (USS) are facing considerable changes to their pension following proposals to close the defined benefit section.

Universities UK, which represents 350 university employers, has announced plans to change the scheme to become a full defined contribution fund in a bid to close the reported £13bn fund deficit.

Patrick Convey, technical director of specialist financial planners Cavendish Medical, explained: ‘Consultants who have an academic element to their work and are part of the USS pension scheme could see their estimated annual pension income fall, as well as their pension contributions increase.

‘Employers and members have

been warned they might need to increase contributions by up to 7% to maintain their current benefits.’

The University and College Union (UCU), the trade union for higher education staff, points to actuarial research which suggests that even lecturers who started working in 2007 and have ten years of service will lose out on £131,000, a loss of £6,100 annually. Most academic doctors are much older, so have more to lose.

The research also notes that lecturers would be £385,000 worse off than if they worked in post1992 universities, where pensions are paid by the Teachers’ Pension Scheme rather than USS.

Changes to the scheme were first recommended by employers Universities UK in autumn 2014. The UCU is conducting a ballot to determine whether its members should take industrial action. This will close on 19 January 2018.

Check finances after Budget, doctors told

Private doctors are being advised to check their financial plans are still on the right path in the wake of the autumn’s Budget.

But excess pension savings above this can give a 55% tax charge.

Mr Convey said it was a ‘welcome reprieve’ from the predicted cuts to pension tax relief.

Phone: 07909 997340 @robinstride

to advertiSe Contact advertising manager Margaret Floate at margifloate@btinternet.com Phone: 01483 824094 to SUBScriBe lisa@marketingcentre.co.uk Phone 01752 312140

Publisher: Gillian Nineham at gill@ip-today.co.uk Phone: 07767 353897

Head of design: Jonathan Anstee chief sub-editor: Vincent Dawe Circulation figures verified by the Audit Bureau of Circulations

Cavendish Medical director Patrick Convey said they should enure that they were using all available allowances to minimise tax and would not be penalised for excess pensions’ savings because of their NHS membership.

Good news is that the pensions lifetime allowance, governing the amount which can be saved into a pension while still qualifying for tax relief, rises from £1m to £1.03m in April.

The abolition of Stamp Duty for firsttime buyers purchasing properties worth up to £300,000 is welcome news for parents helping offspring, but Cavendish warned that those buying jointly with their children will be excluded. This highlighted the need for careful planning.

See our round-up of Budget news on page 10

Outcome website ‘a big opportunity’

By robin Stride

An independent doctors’ leader has commended a new online portal as ‘a superb opportunity’ for consultants to showcase their clinical expertise and excellence.

Independent Doctors Federation (IDF) president Dr Brian O’Connor praised the Private Healthcare Information Network (PHIN) for its work providing data about consultant activities and outcomes.

Hundreds of specialists have so far been invited to view their clinical practice data on the secure portal, ordered by the Competition and Markets Authority (CMA) following its lengthy inquiry into private healthcare.

PHIN must publish hospital specialist activities including volumes of procedures, average lengths of hospital stays, infection rates, readmission rates, revision surgery rates, mortality rates and unplanned patient transfers.

It will also show patient feedback and satisfaction, measurement of health improvement

outcomes, frequency of adverse events, and any possible relevant information from clinical registries and audits.

PHIN chief executive Matt James said there had been ‘positive’ comments from over 100 consultants who had viewed their data reports so far and they were using the feedback mechanism to help hospitals improve data quality.

He told Independent Practitioner Today: ‘While some teething issues are inevitable, we are rapidly applying fixes to improve speed and usability.’

Dr O’Connor added: ‘Obviously, the initial data gathered by PHIN

Portal.phin.org.uk provides data about consultants’ activities and outcomes

will have certain flaws and omissions. By the very nature of this new undertaking, the information gathered by hospital providers may not be a true reflection of doctors’ practices.

‘We in the IDF are very happy to work closely with PHIN to encourage our doctors to engage in this process to ensure that the PHIN portal for consultant activity is indeed a true reflection of the activities of doctors within a hospital.’

Most of the data will relate to consultants performing surgery and other procedures where outcomes are very readily measured.

Dr O’Connor said more sophisticated and mature analysis of

data would evolve and there would be better methods of capturing data on patient outcomes, satisfaction and measured improvement in health.

‘The medical profession should be greatly encouraged by this change to a transparent and open declaration of activities and we in the IDF, in conjunction with PHIN and the Federation of Ind ependent Practitioner Organisations of which we are part, will work closely with all stakeholders to ensure that the excellent care delivered in the private sector is available for access to patients.’

PHIN’s portal gives consultants a unique view of their whole practice, private and NHS, and allows them to check data ahead of any information being published. It encouraged all consultants working in private healthcare to log in, check and work with their hospitals to ensure data was complete and correct before publication.

Paterson probe to be wide-reaching

The private healthcare sector has welcomed the widening of a scrutiny into the circumstances and practices surrounding the malpractice of consultant breast surgeon Ian Paterson.

An independent nonstatutory inquiry for the Department of Health is expected to examine a wide range of issues in private care including doctors’ defence cover, providers’ insurers, responsibility for the quality of care, appraisal and ensuring validation of staff.

The scrutiny will also study safety of multidisciplinary working, information sharing, reporting of activity, and raising

concerns between the independent sector and the NHS.

Another aspect will be how data about the scope and volume of work carried out by doctors is shared with the sector.

Health Minister Philip Dunne said: ‘Ian Paterson’s malpractice sent shockwaves across the health system due to the seriousness and extent of his crimes, and I am determined to make sure lessons are learnt from this so that it never happens again in the independent sector or the NHS.’

The Association of Independent Healthcare Organisations said it looked forward to making a constructive contribution to the

inquiry. But chief executive Fiona Booth added: ‘The failings of an individual rogue surgeon such as Ian Paterson do not represent the high quality and compassionate care delivered day in and day out by the multidisciplinary teams working in both independent sector or the NHS.’

The Private Healthcare Information Network said: ‘Informationsharing, activity reporting and raising concerns in the independent sector have been cited as areas of concern in relation to the Ian Paterson case, and we welcome their inclusion as key aspects of the inquiry.

‘Almost all patients in England

who receive some privately funded treatment are also NHS patients for many other elements of their healthcare, and many thousands of consultants practise in both the NHS and private sectors.

‘It is essential that standards are aligned and information effectively shared for the protection of future patients.’

Mr Paterson, who was employed by the Heart of England NHS Trust and had practising privileges at Spire Parkway and Spire Little Aston, was found guilty in April of 17 counts of wounding patients with intent. His 15year sentence was upped in August to 20 years.

dr Brian o’connor, idF president

Eye doctors unite in Harley Street

By Edie Bourne

Arnott Eye Associates has relocated its 22a Harley Street business around the corner to the first floor of Optegra Eye Hospital London at 25 Queen Anne Street.

Director Mr Richard Packard said he chose this new home because he wanted the business to practise in a new, fully equipped facility and develop its compre

hensive ophthalmology services for current and future patients in the UK and abroad.

Around a dozen consultants have transferred to the new premises with a team of orthoptists, optometrists and staff.

The move could now bring new opportunities for other ophthalmologists, according to Optegra managing director Rory Passmore.

The arrangement brings a ready

made referral stream from Arnott, where specialists provided consultation and diagnosis.

Optegra said investing in consultation and diagnostic activity allowed it to broaden the spec

trum of services it provides to patients from its central London base.

It said it wanted to build strong and long lasting relationships with the best ophthalmologists in

THE STORY BEHINd ARNOTT EYE ASSOCIATES

Eric Arnott (1929-2011) was an original pioneer of the ‘no-stitch’ or small incision surgery techniques used to restore loss of vision due to cataracts. He was also instrumental in lens replacement vision correction being developed and recognised across the UK.

Early in his career, he identified that lens implantation was the way forward and brought the technique to Europe. He went on to design many lens implants that have restored sight to millions of people.

In 1969, he met Charles Kelman, an American ophthalmic surgeon who had recently developed phaco-emulsification, a technique which uses ultrasonic waves, making it possible to remove cataracts through a tiny 3mm incision, doing away with the need for stitches.

In 1970, Arnott invited Kelman to make a

presentation at a meeting of the Ophthalmologic Society of the United Kingdom, of which he was secretary, and the following year he became the first non-American physician to take the ‘phaco’ course which Kelman had established in New York.

On returning to the UK, he raised the money to buy the expensive equipment needed and, later the same year, he performed the first phaco-emulsification procedure outside the US, at London’s Charing Cross Hospital.

The new technique encountered strong opposition from old-school ophthalmic surgeons, so, in 1974, Arnott organised the first ‘live’ Ophthalmic Micro-Surgical Symposium, where ten of the world’s top eye surgeons performed surgery. It was relayed live to more than 300 international delegates by the BBC.

the country, and the Arnott Eye reputation, medical and service qualities, was in keeping with this goal, as it was ‘renowned well beyond London and the UK’.

‘This configuration will allow consultants to further develop their practices, and expand the services that can be offered to their patients in fivestar facilities with leading edge technologies wholly dedicated to eye health.’

In 1981, with his senior registrar at Charing Cross, Mr Richard Packard, Arnott was the first to describe the use of a soft lens material which could be folded to go through an unopened phaco-emulsification incision.

Eventually, by showing the excellent results of modern phaco surgery, Arnott succeeded in overcoming resistance in the profession. Today almost all cataract surgery in the developed world is carried out using variations of the techniques which Arnott helped to pioneer.

Lens replacement – ClarivuTM at Optegra – is now a refined and well-regarded vision correction technique, allowing the patient to restore their vision and avoid the need for future cataract surgery by replacing their natural lens with a personally tailored, artificial lens.

Launch of drive to attract self-payers

Two major campaigns aimed at driving more self pay patients towards private healthcare are being launched by the organisation representing independent hospitals.

The Association of Independent Healthcare Organisations (AIHO) is looking at the selfpay market and how it can support its members in raising awareness of the option.

It is also running a patient choice/GP education programme to try and get greater support in

primary care for referrals to private specialists.

AIHO chief executive Fiona Booth said both campaigns aimed to result in sectorwide messaging to raise awareness of selfpay.

She asked members and representatives of other healthcare organisations in the private sector to remind themselves why patients chose to use independent providers.

‘We need to work collectively to protect and enhance our strengths, and band together to improve our

offering where it needs to be strengthened, always ensuring we provide the best level of service and patient outcomes.’

Speaking at a reception in London, she said it was vitally important for the sector to continue to tell the good news of its services, shorter waiting times, its capacity and its excellent standards of care.

Ms Booth added: ‘AIHO will continue to be a strong and effective voice for the sector, but I

implore all of us to continue working together to make sure our standards remain high.’

She urged providers to look for new ways to improve patient experience, work collaboratively to improve patient choice and information, and together provide an effective voice for the sector.

‘We need to demonstrate the value we add to the UK’s health sector and healthcare economy, and emphasise the importance of patient choice.’

Optegra chief Rory Passmore

By Charles King

Doctors’ private practices will be able to operate more effectively using an enhanced version of Healthcode’s online practice management and billing system ePractice manager.

Designers say it will be particularly beneficial for larger practices with multiple locations.

The specialists in IT systems for the private healthcare sector have introduced a host of new features after consulting with users, focusing on the diary and appointments module, document management and reporting.

New and improved features for ePractice manager users include the ability to:

Block time to show when specialists are unavailable or dealing

with administration, as well as clinics and consultations;

Record when patients have arrived for their appointment;

Email appointment confirmations to patients;

Create GP letters from a template which automatically includes GP details and a patient summary;

Personalise letters to patients efficiently with a feature which automatically completes designated fields with the correct patient name and appointment details;

Assign appointments to a cost centre within the organisation;

Record how patients heard about the practice to inform marketing;

Create additional management reports, including ones showing

invoices and aged debt analysis by cost centre.

As ePractice is an online service, ePractice manager subscribers will be able to access the new functions when they log onto Healthcode. They will not have to purchase a new version of the software.

Healthcode’s managing director

Peter Connor said: ‘We know that a growing proportion of Healthcode practices have several specialists who treat patients at multiple locations. The latest version of ePractice manager reflects this growing complexity.

‘As always, our aim is to help expanding practices provide the most efficient service for patients, operate costeffectively and adapt to the latest challenges in private healthcare.’

Leg ulcers are theme at veins conference Healthcode boosted Bupa starts cancer self-referral service

Bupa has launched the UK’s most comprehensive selfreferral cancer service – Cancer Direct Access.

Patients experiencing cancer symptoms need not wait for a GP referral but can call the insurer’s Cancer Direct Access team to have an appointment booked with a specialist consultant.

Bupa said its team of specialist advisers used the latest National Institute for Health and Care Excellence (NICE) guidance to establish whether a customer needed specialist referral.

The launch of Cancer Direct Access builds on the insurer’s direct access service for breast and bowel cancer. Most customers referred to a consultant under the scheme will be seen within a week and, if diagnosed with cancer, would begin their treatment within a month.

Bupa UK medical director Dr Steve Iley said: ‘Oneintwo people in the UK will be diagnosed with cancer during their lifetime, but the good news is that survival rates continue to improve.

‘Early cancer detection can have a significant impact on an individual’s chance of survival and reduces their need for complex and invasive treatment.

‘However, we know that diagnosis and treatment are often delayed as people can’t find the time to book a GP appointment, or worry about wasting the doctor’s time.

‘Cancer Direct Access removes the need for a GP referral and allows customers to access specialist diagnosis services in a way that is easy and convenient for them.

‘In some cases, it offers peace of mind and reassurance that an individual’s symptoms are not cancer or allows them to quickly access the appropriate medical support and treatment for their diagnosis.’

The Direct Access Cancer Service covers the following cases: bladder, breast, colorectal, endometrial, head and neck, lung, oesophageal, oral, pancreatic, renal, skin, stomach and testicular.

www.bupa.co.uk/direct-access

Seniors go extra mile as trainers

Senior doctors are going above and beyond the call of duty in the time they give to helping shape the careers of the next generation of consultants and GPs.

According to a new GMC report, the education and training for young doctors is too reliant on the goodwill and sacrifices made by senior colleagues who act as trainers.

The report, based on its annual survey answered by more than 75,000 doctors, reveals the pressures faced by consultants who provide junior training.

Doctors acting as trainers must try to fit their training roles around daily NHS duties and, in many cases, private work as either consultants or GPs. Nearly half told the GMC that, to do so, they must work beyond their rostered hours each week. Nearly a third do so daily.

Around one in three trainers report that their job plans do not allow them enough time to fulfil their trainer role.

Leg ulcers and pelvic congestion syndrome head the bill at the 2nd international veins meeting being held in London from 1416 March.

A spokesman said: ‘Whether you are new to phlebology or an experienced venous practitioner, there will be something educational for you at the meeting.’

It will be opened by Ellie Lindsay OBE, who set up the Lindsay Leg Clubs spreading through the UK and now abroad. However, these nurseled clinics currently do not look for, nor treat, curable venous leg ulcers due to superficial venous reflux –around half the total.

The meeting aims to provide ‘a perfect amalgamation of nurses and doctors working together to sort out which patients are curable and which need longterm care.’

Judy Holdstock, winner of the first prize at the American College of Phlebology for her work in pelvic venous duplex, will run courses on transvaginal venous duplex.

www.collegeofphlebology. com/meeting2018

GMC chief executive Charlie Massey said trainers were the backbone of medical education, but more needed doing to value them and to give them the support they need.

‘Employers must ensure trainers receive the resources and time they need to meet their education and training responsibilities. Job plans must include adequate provision for senior doctors to provide training.

‘Doctors in training are in a live learning environment, but for that to continue, it has to be made sustainable in the long term. It is not right that there is such a reliance on trainers always somehow finding the time, often their own time, to keep the system going.’

Yet despite the pressures, most doctors in training continue to rate the quality of their training highly. Just over 75% described the quality of teaching in their post as ‘good’ or ‘very good’.

Key findings from the report are available at www.gmcuk.org/keyfindings31410.asp.

By Robin Stride

Doctors who find they are suffering from working under increased pressure are being targeted for help in a new campaign run by a medical charity.

Doctors fail to seek help Medicine fades as a career of choice

According to a Royal Medical Benevolent Fund (RMBF) survey, there is still a stigma among doctors about asking for help and support.

Although more than half (55%) of those responding thought that doctors’ ‘personality type’ makes them particularly resilient when working under increasing pressure, 75% claimed there was a lack of sympathy within the medical profession for doctors seeking help for stress and mental health issues.

The RMBF believes this could be explained by a perceived ‘bravado culture’ among doctors, with 92% of those surveyed thinking that doctors place value on one another’s ability to work under pressure and cope with long hours without complaint.

Chief executive Steve Crone said many doctors felt unable to ask for help when things were not going well for them, either personally or professionally.

But he added: ‘The Royal Medical Benevolent Fund is here to offer confidential support and advice, so I really would urge anyone who needs help to come forward.’

A new RMBF campaign, ‘Together for Doctors’, is highlighting the need to offer vital support to medical professionals working under rising pressure and is urging any doctor in difficulty to reach out.

For help, ring 020 8540 9194 or email help@rmbf.org.

How to cope with burn-out, see page 20

HOW THE RMBF CAn

HELP

The RMBF website and its online resources, such as The Vital Signs, signpost an extensive list of specialist helplines, many of which are available around the clock, every day of the week. These include: BMA Counselling, Sick Doctors Trust, Cruse Bereavement Care and the Samaritans.

The RMBF’s own phone support operates during weekday working hours (9-5pm) and focuses on assisting prospective and existing beneficiaries through the application process for financial support.

It also signposts alternative sources of support for those it is unable to assist directly.

Twothirds of doctors would now not recommend medicine as a career to their children, according to a survey of senior hospital doctors, GPs and trainees.

Nine in ten of those polled by the Royal Medical Benevolent Fund (RMBF) thought UK hospital working conditions had deteriorated in the past decade and were concerned by the number of doctors leaving the profession.

They thought current NHS issues were having a detrimental effect on recruitment, and said hospital doctors were forced into uncomfortable decisions such as discharging patients early to free up beds.

The RMBF annually supports hundreds of doctors and their families who are struggling with financial concerns, ill health or addiction.

The charity also has a free down

loadable online guide for professionals, called The Vital Signs. Authored by Dr Richard Stevens, a coach with Thames Valley Professional Support Unit, the guide highlights key pressure trigger points for doctors and signposts organisations and support networks for those in need of help and advice.

The charity, which relies solely on voluntary donations, is also hoping the campaign will encourage doctors to fundraise for the RMBF and support their colleagues by organising a ‘hospital hopping’ fund raising walk or teaming up for a ‘wear green and purple’ day at work.

To help, visit www.rmbf.org/getinvolved/fundraising or text RMBF17 £5 to 70070 to donate.

1,845 doctors surveyed in July and August 2017 via Survey Monkey

When the team at Spire Bushey Hospital was looking for someone to open their new £11m diagnostic centre, they looked no further than one of their own ‘very satisfied’ patients.

June Thompson has been a regular visitor to the hospital and was treated at the new facility on the first day it was opened to the public.

She said: ‘There have been two

or three times when doctors here saved my husband’s life, so I have spent a fair amount of time at the main hospital.

‘Over the years, you get to know the consultants and nurses; it’s like a great big family – everyone is always so welcoming.’

The centre in Centennial Park, Elstree, Hertfordshire, includes 14 consulting suites and two treatment rooms.

The RMBF’s poster for a campaign offering help to stressed doctors

Blue ribbon event: Patient June Thompson, second right, with consultant dermatologist Dr Hady Bayoumi, hospital director Lisa Trybus and outpatient and cardiac manager Jay Buckley at the official opening

Insurance tax rise hurts

By Leslie Berry

Independent practitioners have lost nearly 200,000 potential patients in the past three years due to the rising taxes on health insurance.

This is the number of customers who have dropped their policies to depend solely on the NHS, according to the first research to assess the impact of insurance premium tax increases on the UK’s health and social care system. Insurance premium tax, added to many insurance policy premiums including private medical health insurance, has doubled since 2015 and currently stands at 12%.

The study was run by the Centre for Economics and Business Research (Cebr) and commissioned by Bupa. It found each percentage point tax increase led to an estimated 21,000 health insurance customers cancelling their policies. The tax avoided a further rise in the Autumn Budget after these figures were revealed.

Summit will unite medic investors and creators

The Paris region is pushing to be known as ‘the world capital of health innovation’.

To add weight to the claim, the Medicen Paris Region competitiveness cluster, the Paris Region and drug firm Sanofi are teaming up to launch MedXperience, which is being billed as the first international summit on the future of healthcare.

It will be held in the French capital on March 15 and 16.

The event aims to bring together doctors, health industries, startup companies, global investors and local stake holders to promote health innovation and its transformation into business processes,

Bupa warned that increasing insurance premium tax again could see even more people cancel their health insurance or reduce their level of cover.

It said this could lead to the unintended consequence that the revenue collected from health insurance fell and NHS demand rose.

The insurer warned the Government that the tax hit hardest on those who most needed it, because older patients with riskier health profiles paid higher premiums and more tax.

Another study last October found that twothirds of people consider health insurance allows others to access NHS treatment earlier and 55% see it as important in relieving NHS pressure. The online research was conducted by Opinium among a nationally representative sample of 2,000 UK adults.

Bupa Insurance chief executive Alex Perry said: ‘The taxes on health insurance are unfair and counterproductive. As insurance

medical practices and economic development.

Organisers said: ‘During two days, international participants will discuss their practices, achievements and ambitions in new therapies and innovative technologies in the healthcare industry.

‘MedXperience is an opportunity for startups and innovative companies to present their solutions to doctors, clinicians, researchers and investors and to meet experts, future partners and health professionals from around the world.

‘Doctors and organisations, both public and private, will discover innovations and their implementation as well as new tools to help them optimise their work.

‘Investors will be able to meet young start ups with proven experience and will be able to get involved in their development.’

Details available from www. medXperience.org

premium tax on health insurance has increased, we’ve seen hundreds of thousands of people who used to pay for their own health insurance drop out of the market to depend solely on the NHS.

‘This means longer waiting times for everyone else for treatments such as cancer care and cataracts, and even more pressure

on overstretched NHS finances.’

Bupa said cost was the main factor for people when choosing to buy health insurance and this explained the high attrition rates for individual policies as taxes have increased.

A third of people questioned in its survey would consider taking out insurance if costs were lower and a similar number would consider cancelling their policy if their premium went up.

Cebr chief economist Oliver Hogan said: ‘The impact of the tax has not been considered by the Government and we hope this research will make for interesting reading for the industry, the Government and the public.

‘As this is a tax that has increased successively over the last three years, and may increase further in the future, research into the financial implications for the NHS and the welfare impact on patients and society is needed.’

See ‘Bid to avert rise in insurance tax’, page 12

MP backs call to alter negligence system

An MP has urged the Government to continue to explore legal reform to tackle rising clinical negligence costs – the underlying problem behind doctors’ rocketing defence subscriptions.

Alex Chalk said those who suffer as a result of clinical negligence must be properly compensated, but affordability should also be considered.

He was speaking to MPs, peers and health leaders at a Parliamentary event organised by the Medical Protection Society (MPS).

TELL uS yOuR STORy

The MPS has put forward a package of legal reforms that it says could control spiralling costs and strike a balance between reasonable and affordable compensation.

These include the introduction of a limit on future care costs based on the realities of providing homebased care, and fixed recoverable costs to stop lawyers charging disproportionate legal fees. Defence bodies also want swift reform to how the discount rate is set to avoid further sudden shocks to the cost of compensation.

Share your experience of what has and has not worked in your private practice. Even if it’s bad news, let us know and we can spread the word to prevent other independent practitioners falling into the same pitfalls.

Contact editorial director Robin Stride at robin@ip-today.co.uk or phone him on 07909 997340

Alex Perry: said taxes on health insurance were counterproductive

First private unit of its kind opens

By Robin Stride

One Healthcare has opened a new 34-bed, private hospital with six operating theatres in Hatfield, Hertfordshire.

Billed as ‘the first private musculoskeletal-centric centre in the UK’, it follows the opening of the company’s first hospital, One Ashford, in Kent in April 2016.

Others are planned over the next few years in the M25 area.

Company founder and chief executive Adrian Stevensen told Independent Practitioner Today that the opening in late November was the culmination of years of engagement with consultants from a wide catchment area and representing a diversity of specialties.

They formed a steering group to work with the company on every aspect of the scheme including:

Optimum site location;

The range of specialties to be offered;

Functional content including the number and type of operating rooms and the design of patient pathways to improve care;

Key personnel to be employed and sitting on interviewing panels for them;

Advising on governance;

Networking with colleagues to create a peer group of leading consultants to act as ‘catalysts and enablers’ to build and sustain specialists’ interest in and commitment to the project.

Around 190 consultants, drawn from central London, Hertfordshire, Essex and Buckinghamshire, have practising privileges, but this is set to rise as Mr Stevensen said the company was ‘always looking for more’.

He said the hospital’s strategy had been led by musculoskeletal

(MSK) consultants and leading private medical insurers, who were keen that One Hatfield had this unique selling point and differentiated its services from traditional private hospitals.

Other specialties represented include anaesthetics and pain management, cardiology, ENT, general surgery, gynaecology, upper- and lower-GI, urology, pathology and radiology.

One Healthcare said its first hospital in Ashford, Kent, had established a strong local presence, was performing well and had been particularly successful in attracting self-pay patients.

Added Mr Stevensen: ‘We set out to change how private healthcare is delivered and to design modern, welcoming hospitals putting our clinical teams, patients and other customers –including medical insurers – at the heart of our plans.

‘We have embarked on a rapid development programme and have a number of schemes in our pipeline to follow Ashford and Hatfield.’

Plans were supported by the major private medical insurers, who shared the company’s vision for modern, safe and efficient private healthcare within the highest-quality surroundings.

One Healthcare said its centres would enable patients requiring elective surgery and diagnostics to access purpose-built, cost-effective and accessible care closer to home and remove the need to be referred to tertiary centres typically in major cities such as London.

This reduced costs and improved outcomes by applying rapid-recovery programmes to enable patients to minimise their time in hospital.

Each hospital is run as a separate local entity rather than adhering to a standard corporate template.

Consultant orthopaedic surgeon Mr Rajeev Sharma, One Hatfield director of consultant development, said: ‘From a consultant perspective, One Hatfield hospital is unique in the UK

regarding the way they prioritise the patient-physician relationship’.

He said the hospital’s Medical Society incorporated both consultants and GPs and introduced a formal governance structure which placed the views of physicians at the top of the management tree.

Mr Stevensen added: ‘The MSK market has grown consistently over recent years, yet private healthcare facilities have been slow to adapt. We believe that One Healthcare offers a new model of MSK-centric services which are attractive to consultants, patients and insurers.

‘The UK private medical insurers have been really supportive of our plans to change the dynamics of MSK delivery in what is the major sector of the UK market.’

Further centres around London and major commuter areas in south-east England will use a similar, MSK-centric template.

Above: One Hatfield’s management team, including chief executive Adrian Stevensen (left) and surgeon Mr Rajeev Sharma (second left)

The atrium of the One Hatfield Hospital, Hertfordshire

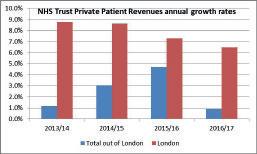

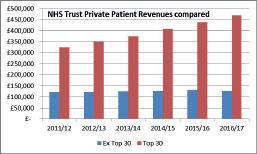

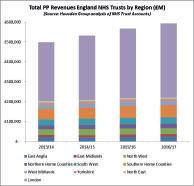

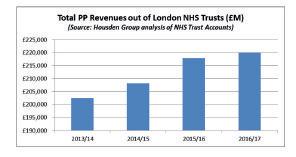

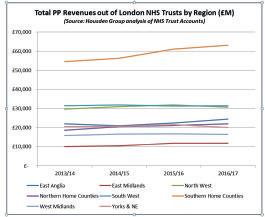

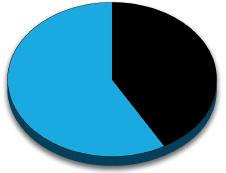

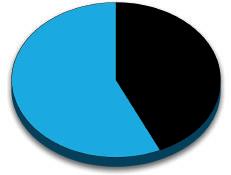

Incomes from NHS PPUs go up by 4.6%

By Philip Housden

NHS trusts again achieved record incomes from private patients, an analysis of recently published 2016-17 annual accounts shows.

There are some marked trends apparent from the data compiled by the Housden Group.

Total revenues were up £26m to a high of £594m for NHS trusts in England (£568m in 2015-16) – an increase of 4.6%.

This growth rate is marginally down on the 6-7% rate achieved in each of the previous four years.

Revenues for trusts in London climbed to £373m, up from £349m the previous year. And this was the main engine of growth, with incomes out of London essentially flat at £220m, up £2m on the year before.

The extent to which growth was skewed is shown in figure 1.

Again, the top ten trusts by revenue were all in the capital, with Royal Marsden at £91.8m and Great Ormond Street Hospitals at £55m, earning 25% of all England NHS trust incomes.

Indeed, the top ten trusts

increased their market share from 57% to over 59% of all private patient earnings.

The top 30 trusts now account for 79% of the total. Indeed, while the top 30 trusts have together grown by 25% in the past three years, overall revenues outside of that group have been flat for some time.

Future articles will analyse NHS private patient performance by region, starting with London in the next issue, discussing present trends and the potential for future growth.

What these trends suggest is that where trusts invest in the development of private patient services and treat the service as a regular part of what the trust does, they then reap the rewards. Even though medical insurance is more prevalent in the Southeast, there are opportunities for growth across the NHS – albeit many unrealised.

Philip Housden (right) is director of Housden Group

What these trends suggest is that where trusts invest in the development of private patient services ... they then reap the rewards

A bright future for PPUs?

So do NHS private patient units have a future given the increasing pressures on daytoday core services?

In the first of two articles, Philip Housden argues they have never been more relevant to the health service than now – and 2018 is a great time for the health service to invest in them.

See page 25

Figure 1

bUdgET RoUnd-Up

What that red box contained

Independent practitioners will be affected by a wide range of changes announced in Chancellor Philip Hammond’s latest Budget. Susan Hutter (right) provides a round-up and some useful tips

pEnsions TAx REliEF

No changes have been announced to the Annual Allowance limits which remain at £40,000 for individuals earning below £150,000.

Those doctors with income of more than £150,000 will be subject to the allowance being tapered by £2 for every £1 of income earned above £150,000, with a minimum allowance available to those earning over £210,000 of £10,000.

The Lifetime Allowance limit will be increased to £1,030,000 – from the £1m first introduced in April 2016 – with effect from April 2018.

Doctors are advised to take specialist advice, especially relevant to those who have an NHS pension as well as a private one.

TAx-FREE AllowAncEs

And TAx bAnds

The Government has announced that the capital gains tax annual exemption for individuals and personal representatives has been increased to £11,700 (from the current £11,300) for 2018-19. The amount available to most trusts and settlements will be £5,850.

The income tax personal allowance will increase to £11,850, from the current £11,500, and the basic rate tax top threshold will go up by £1,350 to £46,350.

The dividend allowance will reduce to £2,000 in accordance with previous announcements.

Make sure that you utilise as many allowances and as much of the lower-rate band as possible. Consider transferring incomeearning assets to a lower-earning spouse.

The ‘residence nil rate band’ limit for inheritance tax purposes will increase to £125,000 with effect from April 2018.

MilEAgE RATEs FoR

UnincoRpoRATEd pRopERTy bUsinEssEs

For those independent practitioners who own investment properties, there is a simplification in

claiming motor expenses and it could work out to be more generous, which is always welcome.

The Government has announced that it will permit the use of mileage rates as an allowable method of calculating the allowable deduction in respect of motoring expenses incurred for the purposes of a property business.

In most cases, mileage rates will not be available in respect of vehicles for which capital allowances have already been claimed or for which expenditure in acquiring the vehicle has been deducted in a business using the cash basis.

However, transitional arrangements will be introduced in these cases.

Currently, the mileage rates are 45p per mile in respect of the first 10,000 business miles and 25p thereafter.

nATionAl insURAncE conTRibUTions (nic)

Class 1 NIC will be payable by employees at 12% on their weekly employment income between £162 and £892 and at 2% thereafter in 2018-19.

The threshold for the employers will increase to £162 per week –above which Class 1 secondary contributions will be due at 13.8%.

The ‘small profits threshold’ for Class 2 NIC purposes will be increased by £180 to £6,205 and the weekly rate of the contributions will go up by 10p to £2.95.

Class 4 NIC will be due at 9% on annual profits between £8,424 and £46,350 and at 2% thereafter.

The tax-free limit for the ordinary cash/stock and shares ISAs will remain £20,000, of which £4,000 can be saved into a Lifetime ISA. For higher-rate tax payers, this is worth considering, especially as interest rates are on the increase. ➱ p12

THE FIRST 9-VALENT HUMAN PAPILLOMAVIRUS (HPV) VACCINE

GARDASIL® 9 contains 9 HPV types that account for 89% of HPV-related anogenital cancers and 90% of genital warts in Europe.1,2*

* Cervical, vulval, vaginal and anal cancers caused by oncogenic HPV types 16, 18, 31, 33, 45, 52 & 58 genital warts caused by HPV types 6 & 11. Not all cases of anogenital cancer are caused by HPV. The HPV prevalence is: ~100% in cervical cancer; ~88% in anal cancer; ~19% in vulval cancer; ~71% vaginal cancer.2

GARDASIL® 9 is indicated for active immunisation of individuals from the age of 9 years against premalignant lesions and cancers affecting the cervix, vulva, vagina and anus caused by vaccine HPV types and genital warts caused by speci c HPV types. The indication is based on data in males and females aged 9-26 years.

GARDASIL® 9 is not the vaccine offered in the national immunisation programme. The use of HPV vaccines should be in accordance with of cial recommendations.

For information on ef cacy rates and safety considerations, refer to the Summary of Product Characteristics available on the eMC website.

To order please contact AAH on 0844 561 8899.

GARDASIL ® 9 ▼

Human Papillomavirus 9 valent Vaccine (Recombinant, adsorbed))

PRESCRIBING INFORMATION

Refer to Summary of Product Characteristics before prescribing

Adverse events should be reported. Reporting forms and information can be found at www.mhra.gov.uk/yellowcard. Adverse events should also be reported to MSD (Tel: 01992 467272).

PRESENTATION Gardasil 9 is supplied as a single dose pre- lled syringe containing 0.5 millilitre of suspension. Each dose of vaccine contains highly puri ed virus-like particles (VLPs) of the major capsid L1 protein of Human Papillomavirus (HPV). These are type 6 (30 mg), type 11 (40 mg), type 16 (60 mg), type 18 (40 mg), type 31 (20 mg), type 33 (20 mg), type 45 (20 mg), type 52 (20 mg) and type 58 (20 mg). USES Gardasil 9 is a vaccine for use from the age of 9 years for the prevention of premalignant lesions and cancers affecting the cervix, vulva, vagina and anus caused by vaccine HPVtypes and genital warts (condyloma acuminata) caused by speci c HPV types. The indication is based on the demonstration of ef cacy of Gardasil 9 in males and females 16 to 26 years of age and on the demonstration of immunogenicity of Gardasil 9 in children and adolescents aged 9 to 15 years. The use of Gardasil 9 should be in accordance with of cial recommendations. DOSAGE AND ADMINISTRATION Individuals 9 to and including 14 years of age at time of rst injection: Gardasil 9 can be administered according to a 2-dose schedule. The second dose should be administered between 5 and 13 months after the rst dose. If the second vaccine dose is administered earlier than 5 months after the rst dose, a third dose should always be administered. Gardasil 9 can be administered according to a 3-dose (0, 2, 6 months) schedule. The second dose should be administered at least one month after the rst dose and the third dose should be administered at least 3 months after the second dose. All three doses should be given within a 1-year period. Individuals 15 years of age and older at time of rst injection: Gardasil 9 should be administered according to a 3-dose (0, 2, 6 months) schedule. The second dose should be administered at least one month after the rst dose and the third dose should be administered at least 3 months after the second dose. All three doses should be given within a 1-year period. It is recommended that individuals who receive a rst dose of Gardasil 9 complete the vaccination course with Gardasil 9. The need for a booster dose has not been established. Studies using a mixed regimen (interchangeability) of HPV vaccines were not performed for Gardasil 9. Subjects previously vaccinated with a 3-dose regimen of quadrivalent HPV types 6, 11, 16, and 18 vaccine (Gardasil or Silgard), hereafter

referred to as qHPV vaccine, may receive 3 doses of Gardasil 9. The use of Gardasil 9 should be in accordance with of cial recommendations. Paediatric population (children <9 years of age): The safety and ef cacy of Gardasil 9 in children below 9 years of age have not been established. No data are available. Population ≥ 27 years of age: The safety and ef cacy of Gardasil 9 in individuals 27 years of age and older have not been studied. The vaccine should be administered by intramuscular injection. The preferred site is the deltoid area of the upper arm or in the higher anterolateral area of the thigh. Gardasil 9 must not be injected intravascularly, subcutaneously or intradermally. The vaccine should not be mixed in the same syringe with any other vaccines and solution. CONTRAINDICATIONS Hypersensitivity to any component of the vaccine including active substances and/or excipients. Individuals with hypersensitivity after previous administration of Gardasil 9 or Gardasil /Silgard should not receive Gardasil 9. PRECAUTIONS The decision to vaccinate an individual should take into account the risk for previous HPV exposure and potential bene t from vaccination. As with all injectable vaccines, appropriate medical treatment and supervision should always be readily available in case of rare anaphylactic reactions following the administration of the vaccine. The vaccine should be given with caution to individuals with thrombocytopaenia or any coagulation disorder because bleeding may occur following an intramuscular administration in these individuals. Syncope (fainting), sometimes associated with falling, can occur following, or even before, any vaccination, especially in adolescents as a psychogenic response to the needle injection. This can be accompanied by several neurological signs such as transient visual disturbance, paraesthesia, and tonic-clonic limb movements during recovery. Therefore, vaccinees should be observed for approximately 15 minutes after vaccination. It is important that procedures are in place to avoid injury from fainting. Vaccination should be postponed in individuals suffering from an acute severe febrile illness. However, the presence of a minor infection, such as a mild upper respiratory tract infection or lowgrade fever, is not a contraindication for immunisation. As with any vaccine, vaccination with Gardasil 9 may not result in protection in all vaccine recipients. Gardasil 9 will only protect against diseases that are caused by HPV types targeted by the vaccine. Therefore, appropriate precautions against sexually transmitted diseases should continue to be used. The vaccine is for prophylactic use only and has no effect on active HPV infections or established clinical disease. The vaccine has not been shown to have a therapeutic effect and is not indicated for treatment of cervical, vulvar, vaginal and anal cancer, high-grade cervical, vulvar, vaginal and anal dysplastic lesions or genital warts. It is also not intended to prevent progression of other established HPV-related lesions. Gardasil 9 does not prevent lesions due to a vaccine HPV type in

9-VALENT HPV PROTECTION

individuals infected with that HPV type at the time of vaccination. Vaccination is not a substitute for routine cervical screening. There are no data on the use of Gardasil 9 in individuals with impaired immune responsiveness. Safety and immunogenicity of a qHPV vaccine have been assessed in individuals aged from 7 to 12 years who are known to be infected with human immunode ciency virus (HIV). Individuals with impaired immune responsiveness, due to either the use of potent immunosuppressive therapy, a genetic defect, Human Immunode ciency Virus (HIV) infection, or other causes, may not respond to Gardasil 9. Long-term follow-up studies are currently ongoing to determine the duration of protection. There are no safety, immunogenicity or ef cacy data to support interchangeability of Gardasil 9 with bivalent or quadrivalent HPV vaccines. Pregnancy, lactation and fertility: There are insuf cient data to recommend use of Gardasil 9 during pregnancy, therefore vaccination should be postponed until after completion of pregnancy. The vaccine can be given to breastfeeding women. No human data on the effect of Gardasil 9 on fertility are available. SIDE EFFECTS Refer to Summary of Product Characteristics for complete information on side-effects. Very common side effects include: erythema, pain and swelling at the injection site and headache. Common side effects include: pruritus and bruising at the injection site, dizziness, nausea, pyrexia and fatigue. The post-marketing safety experience with qHPV vaccine is relevant to Gardasil 9 since the vaccines contain L1 HPV proteins of 4 of the same HPV types. The following adverse experiences have been spontaneously reported during post-approval use of qHPV vaccine and may also be seen in post-marketing experience with Gardasil 9: urticaria, bronchospasm, idiopathic thrombocytopenic purpura, acute disseminated encephalomyelitis, Guillain-Barré Syndrome and hypersensitivity reactions, including anaphylactic/ anaphylactoid reactions. PACKAGE QUANTITIES AND BASIC NHS

COST Single pack containing one 0.5 millilitre dose pre- lled syringe with two separate needles: £105.00 per dose Marketing

References: 1. GARDASIL® 9 SmPC, 2017. 2. Hartwig S et al

Estimation of the epidemiological burden of HPV‐related anogenital cancers, precancerous lesions, and genital warts in women and men in Europe: potential additional bene t of a nine‐valent second generation HPV vaccine compared to rst generation HPV vaccines. Papillomavirus Res 2015; 1:90–100.

Date of preparation: October 2017 VACC-1231710-0006

➱ continued from page 10

The Junior ISA and Child Trust Fund subscription limits will increase to £4,260. This is effective from April 2018.

Enterprise investment scheme (Eis)

Changes will be introduced to the EIS legislation to encourage investments in knowledge-intensive companies. The changes will apply to shares issued on or after 6 April 2018.

The EIS investment limit will be increased for individuals to £2m – from £1m – provided that any amount over £1m is invested in one or more knowledge-intensive companies.

Many doctors may be interested in this, as a number are involved in start-ups in this field.

stamp duty land Tax (sdlT)

The Government has introduced a new relief for first-time buyers of residential property worth £500,000 or less whereby the first £300,000 of the property costs will be subject to stamp duty at 0% and the following £200,000 at 5%.

The standard SDLT rates will apply to properties costing more than £500,000.

Anti-avoidance rules have been introduced with effect from 22 November 2017 in relation to the 3% stamp duty surcharge where an individual acquires a second residential property.

From 22 November 2017, the relief from the surcharge will only be available where the purchaser of the second residential property disposes the whole of their former main residence to someone other than their spouse.

This new measure now also grants relief where:

A divorce-related court order prevents someone from disposing their interest in a main residence;

A spouse or civil partner buys property from another spouse or civil partner;

A deputy buys a property for a child subject to the Court of Protection;

A purchaser adds to their interest in their current main residence.

Susan Hutter is a partner at Blick Rothenberg and part of the team that advises medical practitioners

Bid to avert rise in insurance tax

By Robin Stride

The independent healthcare sector is being urged to intensify its fight to protect insurance premium tax on private medical insurance from a further increase.

Private consultants, hospitals and insurers breathed a sigh of relief at the end of Chancellor Philip Hammond’s Autumn Budget speech as health cover escaped from suffering yet another tax rise.

But many still fear that private medical insurance could be in for another hit in future with an increase from the current 12% to match the VAT rate of 20%.

A leading voice in the campaign to protect private medical insurance from yet more insurance premium tax increases is the leader of the trade body whose members find the insured customers for consultants and insurers.

Association of Medical Insur ance Intermediaries (AMII) executive chairman, Mr Stuart Scullion, expressed ‘delight’ that the Treasury decided not to impose further increases.

ance products such as life or critical illness.’

But he told 200 members at their Health and Wellbeing Summit in Westminster that the anti-tax lobby must now keep up the pressure.

Mr Scullion continued: ‘We are calling on the Government to commit to stability for insurance premium tax in relation to healthcare during this Parliament, however long that might be, by freezing the rate of insurance premium tax on healthcare spend.

‘Furthermore, we are asking the Government to reappraise how health insurance and cash plans are treated in the fiscal system in line with other zero-rated insur-

Referring to a recent poll for Bupa (see page 7), he added: ‘We know cost is the main factor in the decision to purchase and maintain health insurance cover, with the poll confirming a third (33%) saying they would consider taking out insurance if costs were lower, while 33% of policyholders said they will consider cancelling their policy if their premium goes up.’

Mr Scullion said the research suggested insurance premium tax was contributing to thousands of individuals giving up their policies, resulting in nearly 200,000 customers cancelling their policies in the past three years.

He told the summit: ‘Every 1% increase in insurance premium tax is leading an estimated 31,000 health insurance customers every year to depend solely on the NHS for all of their healthcare.

‘The report reaffirms what I have said previously that insurance premium tax has a greater impact on people who have the most need to keep their health

Every 1% increase in insurance premium tax is leading an estimated 31,000 health insurance customers every year to depend solely on the NHS for all of their healthcare

insurance, such as older individuals with riskier health profiles who pay higher premiums.’

The poll of 2,000 people found 63% said health insurance allows others to access NHS treatment earlier and 55% view it as important in relieving pressure on the NHS.

Mr Scullion said he understood from pre-Budget conversations that the Chancellor had commented on seeing increased commentary and resistance in relation to insurance premium tax.

The AMII had positively contributed to this lobbying, alongside some of its corporate member firms (insurers) and other industry bodies.

He reported that efforts to raise AMII’s profile were working and he was engaged in regular dialogue on healthcare matters, including insurance premium tax, with Craig Tracey MP, chairman of the All-Party Parliamentary Group on Insurance and Financial Services. AMII said it had positive feedback from its first education event about understanding the UK health insurance market, which was run to support employers with members of staff who are new to the industry.

StuaRt SCullioN

PRESCRIBING INFORMATION

AVAXIM®, suspension for injection in a prefi lled syringe.

Hepatitis A vaccine (inactivated, adsorbed). Refer to Summary of Product Characteristics for full product information.

Presentation: Suspension for injection. Available as a 0.5 millilitre single dose prefi lled syringe containing 160 antigen units of inactivated hepatitis A virus. Indications: For primary or booster immunisation against infection caused by hepatitis A virus in susceptible adults and adolescents aged 16 years and above. AVAXIM is to be used on the basis of offi cial recommendations. Dosage and administration: A single 0.5 millilitre dose should be administered by intramuscular injection in the deltoid region. Immediately before use the syringe should be shaken well to obtain an homogenous suspension. To provide long term protection, a booster should be given between 6 and 36 months later. AVAXIM may be used as a booster in subjects from 16 years of age, vaccinated with another inactivated hepatitis A vaccine (monovalent or with purifi ed Vi polysaccharide typhoid) 6 months to 36 months previously. The vaccine is to be injected intramuscularly. AVAXIM may be administered subcutaneously under exceptional circumstances (e.g. in patients with thrombocytopenia or in patients at risk of haemorrhage). Do not inject intravascularly. Also avoid administration into buttocks. Contra-indications: Hypersensitivity to the active substance(s), to any of the excipients or following a previous injection of this vaccine. Known hypersensitivity to neomycin (which may be present in the vaccine in trace amounts). Vaccination should be delayed in subjects with acute severe febrile infections. Warnings and precautions: The effect of AVAXIM on individuals late in the incubation period of hepatitis A has not been documented. Immunogenicity could be impaired in immunosuppressed patients. AVAXIM is unnecessary for individuals raised in areas of high endemicity and/or with a history of jaundice as they may be immune to hepatitis A. Testing for antibodies to hepatitis A prior to a decision on immunisation should be considered in such situations. If not, seropositivity against hepatitis A is not a contraindication. AVAXIM is as well tolerated in seropositive as in seronegative subjects. Caution is advised for the use of AVAXIM in patients with liver disease. No clinical data on concomitant administration of AVAXIM with other inactivated vaccine(s) or recombinant hepatitis B virus vaccine have been generated. AVAXIM can also be given at the same time as immunoglobulin but at different sites, however, antibody titres could be lower than after vaccination with AVAXIM alone. AVAXIM must not be mixed with other vaccines in the same syringe. AVAXIM can be administered at the same time as Vi polysaccharide typhoid vaccine or with a yellow fever vaccine reconstituted with a Vi polysaccharide typhoid vaccine, but at different sites. Syncope (fainting) can occur following, or even before, any vaccination especially in adolescents as a psychogenic response to the needle injection. This can be accompanied by several neurological signs such as transient visual disturbance, paraesthesia and tonic-clonic limb movements during recovery. It is important that procedures are in place to avoid injury from faints. Pregnancy and lactation: AVAXIM should not be used during pregnancy unless clearly necessary and following an assessment of the risks and benefi ts. There are no data on the effect of administration of AVAXIM during lactation. AVAXIM is therefore not recommended during lactation. Undesirable effects: Very common side effects include: asthenia and mild injection site pain. Common side effects include: myalgia/ arthralgia, headache, gastrointestinal tract disorders (nausea, vomiting, decreased appetite, diarrhoea, abdominal pain) and mild fever. In post-marketing experience other adverse reactions have been reported and include vasovagal syncope in response to injection. For a complete list of undesirable effects please refer to the Summary of Product Characteristics. Marketing authorisation holder: Sanofi Pasteur Europe, 2 Avenue Pont Pasteur, 69007 Lyon, France. Further information is available from the Distributor: UK: Sanofi, One Onslow Street, Guildford, Surrey GU1 4YS Tel: 0845 372 7101; Ireland: sanofi -aventis Ireland T/A SANOFI, Citywest Business Campus, Dublin 24, Ireland Tel: 01 403 5600 Package quantities and basic NHS cost: Single dose prefi lled syringes in single packs, basic NHS cost £18.10; packs of 10 single dose prefi lled syringes, basic NHS cost £181.00. Legal category: POM Marketing authorisation number: UK : PL 46602/0001 Ireland: PA 2131/002/001 ® Registered trademark Date of last review:

ACCoUnTAnT’s CliniC: TAx RETURns

Get your skates on

If you haven’t prepared the information for your 2016-17 tax year, you need to get your skates on, as the filing date is 31 January 2018. Susan Hutter (below) gives some top tips about submitting a tidy tax return

Don’t adopt the ostrich approach

With the best will in the world, there are times when administration takes a back seat. Particularly the tax return.

However, I know too many medics who procrastinate and adopt the ostrich approach when it comes to such matters.

Confront your tax affairs now!

Apart from anything else, you will need to know how much tax to pay. The sooner you know what the amount is, the better, as you haven’t much time to get reserves ready so that you can pay your bill at the end of January 2018.

Planning ahead – The paperwork

To those of you who like to plan ahead for your 2017-18 tax return – always advisable – you should start gathering the paperwork as soon as the tax year ends on 5 April 2018.

I know too many medics who procrastinate and adopt the ostrich approach when it comes to such matters. Confront your tax affairs now!

Some information will be supplied by third parties; for example, P60s for salaries (NHS salaries, private pensions, NHS pension if you are drawing on that, and your own salary if also working in the NHS) as well as a P11D if you trade within a company and, for example, you have taxable benefits like a company car.

Your will also need to gather tax certificates received from banks and building societies.

Even though tax is deducted at source, you still need to declare this information on your tax return, as most consultants and private GPs are higher-rate tax payers and only base rate tax is deducted at source.

Sometimes bank and societies need reminding and therefore do chase them if you have not received a certificate three months after the tax year end.

In addition, you will need dividend vouchers if you have shares

in listed companies – and also dividend vouchers if you trade via a company and drew dividends. Your accountant should have the latter, as they probably prepared them on your behalf.

Check list

Use your prior year’s tax return as a check list for the year you are preparing for now.

But make sure you do not follow it blindly – because you could have new sources of income since the last tax return date, such as opening a new bank account or you purchased a rental property.

Don’t forget things such as writing or lecture fees. Talk to your accountant as to how he/she would like the information presented – if presented clearly, it will save on accountancy fees.

Prioritise practice accounts

Make sure your practice accounts are prepared as soon as possible, whether you are a sole trader or a limited company.

Gather the information first, as this is the biggest thing and takes

the longest. If you have a rental property, you need to gather details for all rental income and expenditure.

Also, if you let it through an agent, you will need to provide your agent’s statement, your own bank records and a record of expenses such as for decorating/ cleaner. Your accountant won’t want the receipts for these items, but it is important that you retain them.

Put money in reserve

If you haven’t left your tax return to the last minute – put some money aside for a tax reserve.

Your accountant will point you in the right direction as to how much you will need to reserve, as most independent practitioners know the tax is due in two instalments on 31 January and 31 July each year. This is your chance to get ahead and make sure you always have a tidy tax return.

Avoiding the taxman, see p48

Susan Hutter is a partner at Blick Rothenberg and part of the team that advises medical practitioners

OR RUSHING TO A&E?

Check if your patients need vaccination against rabies before they go:1

PRESCRIBING INFORMATION

Rabies Vaccine BP ≥2.5 IU/ml, Powder and solvent for suspension for injection

Refer to Summary of Product Characteristics for full product information.

• Visiting an area where rabies is common and taking part in higher risk activities e.g. cycling or running?

• Working abroad in close contact with animals?

• Staying in an at-risk area for more than 1 month?

Rabies Vaccine BP from Sanofi Pasteur offers pre- and post-exposure protection against rabies.2

Order at www.vaxishop.co.uk or telephone our Customer Service team on 0800 854 430

Presentation: A single dose vial of powdered vaccine and pre-fi lled syringe of solvent for suspension for injection. After reconstitution, each 1 millilitre dose contains rabies virus (inactivated, strain PM/ WI 38 1503-3M) not less than 2.5 International Units of rabies antigen. Indications: Prophylactic immunisation against rabies and treatment of patients following suspected rabies contact. Dosage and administration: The dose of reconstituted vaccine in all cases is 1 millilitre given by intramuscular injection into the deltoid region. Reconstitute with the solvent supplied and shake carefully to ensure complete reconstitution. Following reconstitution the vaccine will be a pinkish colour and free from particles. Once reconstituted, the vaccine must be used immediately. DOSAGE FOR PROPHYLAXIS: 1 millilitre given on days 0, 7 and 28. For those at regular and continuing risk, a single reinforcing dose of vaccine should be given at 1 year after the primary course has been completed. Further doses should be given at three- to fi ve-year intervals thereafter. For travellers at intermittent risk of exposure, booster doses may be given in line with offi cial recommendations. DOSAGE FOR TREATMENT: For those known to have adequate prophylaxis - 1 millilitre should be given on day 0 and on day 3 following contact with a suspected rabid animal. For those with no, or possibly inadequate prophylaxis - the fi rst injection should be given as soon as possible after suspected contact (day 0) and followed by four further 1 millilitre doses on days 3, 7, 14 and 30 (the earliest that the 5th dose can be given is day 28 as per WHO recommendations). The use of Rabies Immunoglobulin should be considered in unimmunised or incompletely immunised subjects or those with uncertain immune status in accordance with official recommendations and/or expert advice. The treatment schedule may be stopped if the animal concerned is found conclusively to be free of rabies. Subjects with incomplete prophylaxis or unknown history of immunisation should be treated as non- immune. Contra-indications: Pre-exposure: Known systemic hypersensitivity to Rabies Vaccine BP or any of its components; febrile and/or acute disease. Post-exposure: no contra-indications. Warnings and precautions: Appropriate facilities and medicines should be readily available in case of anaphylaxis or hypersensitivity following injection. The vaccine may contain traces of neomycin and betapropiolactone which are used during the manufacturing process. If Rabies Immunoglobulin is indicated in addition to Rabies Vaccine BP, then it must be administered at a different anatomical site to the vaccination site. Rabies Vaccine BP should not be administered to patients with bleeding disorders or to persons on anticoagulant therapy unless the potential benefi t outweighs the risk of administration. The potential risk of apnoea and the need for respiratory monitoring for 48- 72 h should be considered when administering the primary immunisation series to very premature infants (born ≤ 28 weeks of gestation) and particularly for those with a previous history of respiratory immaturity. As the benefi t of vaccination is high in this group of infants, vaccination should not be withheld or delayed. Anxiety-related reactions, including vasovagal reactions (syncope), hyperventilation or stress-related reactions can occur following, or even before, any vaccination as a psychogenic response to the needle injection. This can be accompanied by several neurological signs such as transient visual disturbance and paraesthesia. It is important that procedures are in place to avoid injury from faints. Corticosteroids and immunosuppressive treatments may interfere with antibody production, check antibodies 2 to 4 weeks after course. Pregnancy: The potential risk of administration of Rabies Vaccine BP during pregnancy is unknown. Due to the severity of the disease, pregnancy is not considered to be a contra-indication to post-exposure prophylaxis. If risk of exposure is substantial, pre- exposure prophylaxis may also be indicated. Lactation: It is not known whether the vaccine is excreted in human breast milk. Due to the severity of the disease, breast-feeding is not considered a contraindication. Undesirable effects: Very common side effects include: lymphadenopathy, nausea, diarrhoea, injection site reactions (pain, erythema, pruritus, induration), chills, malaise, headache, arthralgia and myalgia. Common side effects: injection site bruising, dizziness, respiratory manifestations (dyspnoea, wheezing), angioedema, pyrexia, abdominal pain, vomiting and allergic reactions with skin disorders (urticaria, rash, pruritus). Other undesirable effects have been reported, although their frequency is not known. These include serum sickness type reactions, anaphylactic reactions, oedema, encephalitis, convulsion, Guillain-Barré Syndrome, paresis, neuropathy, paraesthesia and asthenia. For a complete list of undesirable effects please refer to the Summary of Product Characteristics. Marketing authorisation holder: Sanofi Pasteur Europe, 2 Avenue Pont Pasteur, 69007 Lyon, France. Further information is available from the Distributor: UK: Sanofi, One Onslow Street, Guildford, Surrey GU1 4YS Tel: 0845 372 7101; Ireland: sanofi -aventis Ireland T/A SANOFI, Citywest Business Campus, Dublin 24, Ireland Tel: 01 403 5600 Package quantities and basic NHS cost: One single dose vial (powder) and one pre-fi lled disposable syringe containing 1 millilitre of solvent with 2 separate needles, basic NHS cost £40.84. Legal category: POM Marketing authorisation number: UK : PL 46602/0004 Ireland: PA 2131/004/001 Date of last review: February 2017

Suspected adverse events should be reported Reporting forms and information can be found at www.mhra.gov.uk/yellowcard and www.hpra.ie

Suspected adverse events should also be reported to Sanofi Tel: 08000 902 314 (for UK) and Tel: 01 403 5600 (for Ireland).

References: 1. Department of Health. Immunisation against infectious disease. Chapter 27: Rabies. Accessed November 2017 2. Rabies Vaccine BP Summary of Product Characteristics SAGB.RABIE.17.10.1326 11/17

ExEcUTivE inFoRmATion

How to figure out what you’re doing

Executive information is increasingly important for private doctors. Jane Braithwaite (below) shows how to analyse your business and make changes based on practice data