We unlock potential, creating premium, sustainable space for London to thrive

We Create Exceptional Premium Spaces in Prime Central London Locations

Through our highly active, cycle led business model, we aim to outperform the London property cycle, and our cost of capital, maximising value for our stakeholders

Today, our markets are supportive:

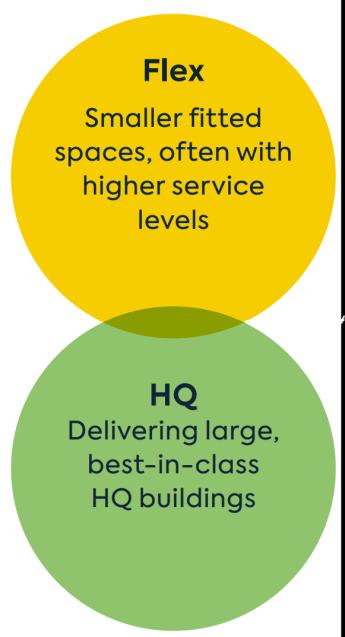

• We are profitably delivering premium HQ offices and Flex spaces into a high demand, supply-constrained market with sustained rental growth

• Investment markets have rebased, real capital values are near 2009 lows, and we are acquiring buildings significantly below replacement cost

• Our Customer First strategy is delivering differentiated premium rental growth as we deploy new capital

Backed by strong fundamentals, and a favourable rate cycle, GPE is well placed to exploit current market conditions and offers highly attractive returns for investors

GPE at a Glance

Delivering a premium office and retail offer into the most prime central London locations

Creating premium spaces Development & refurbishment

Customer First Premium offer: High NPS +26

Sustainability An economic imperative

Low financial leverage 10%-35% through the cycle

Disciplined capital management Raise to acquire, distribute excess

Match risk to cycle Growth; market supportive

• 2.9 million

across 41

Average capital value £1,153 psf • HQ Development: 0.5 million sq ft on site

• Flex offices: 582,000 sq ft committed

• 5.5%/6.8% equivalent/reversionary yield

• Anticipated FY ’26 rental growth

Portfolio: 4.0%-7.0%

6.0%-10.0%

Contra Cyclical Track Record: We've Been Here Before

Extensive experience of exploiting London’s cyclical markets

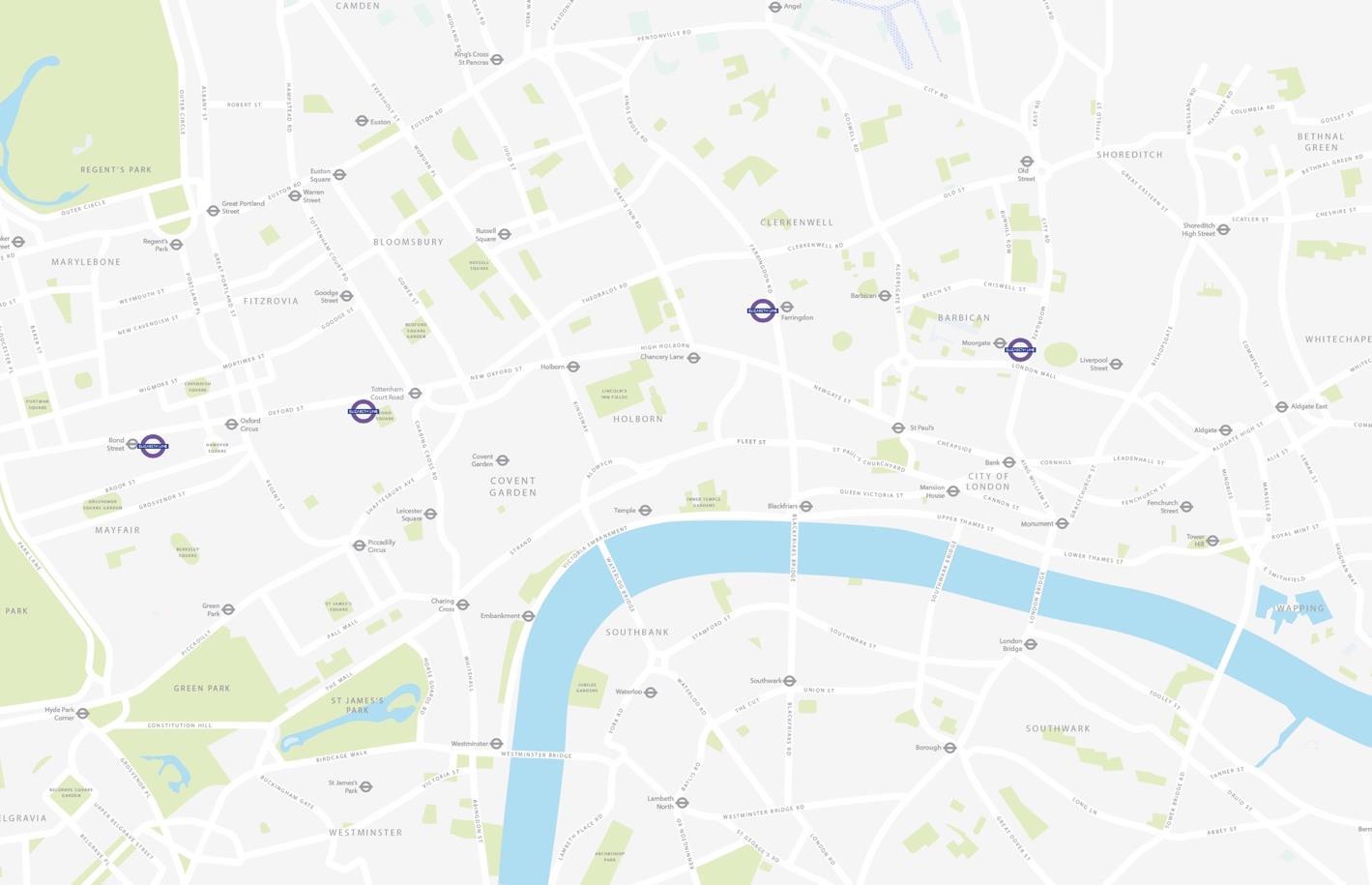

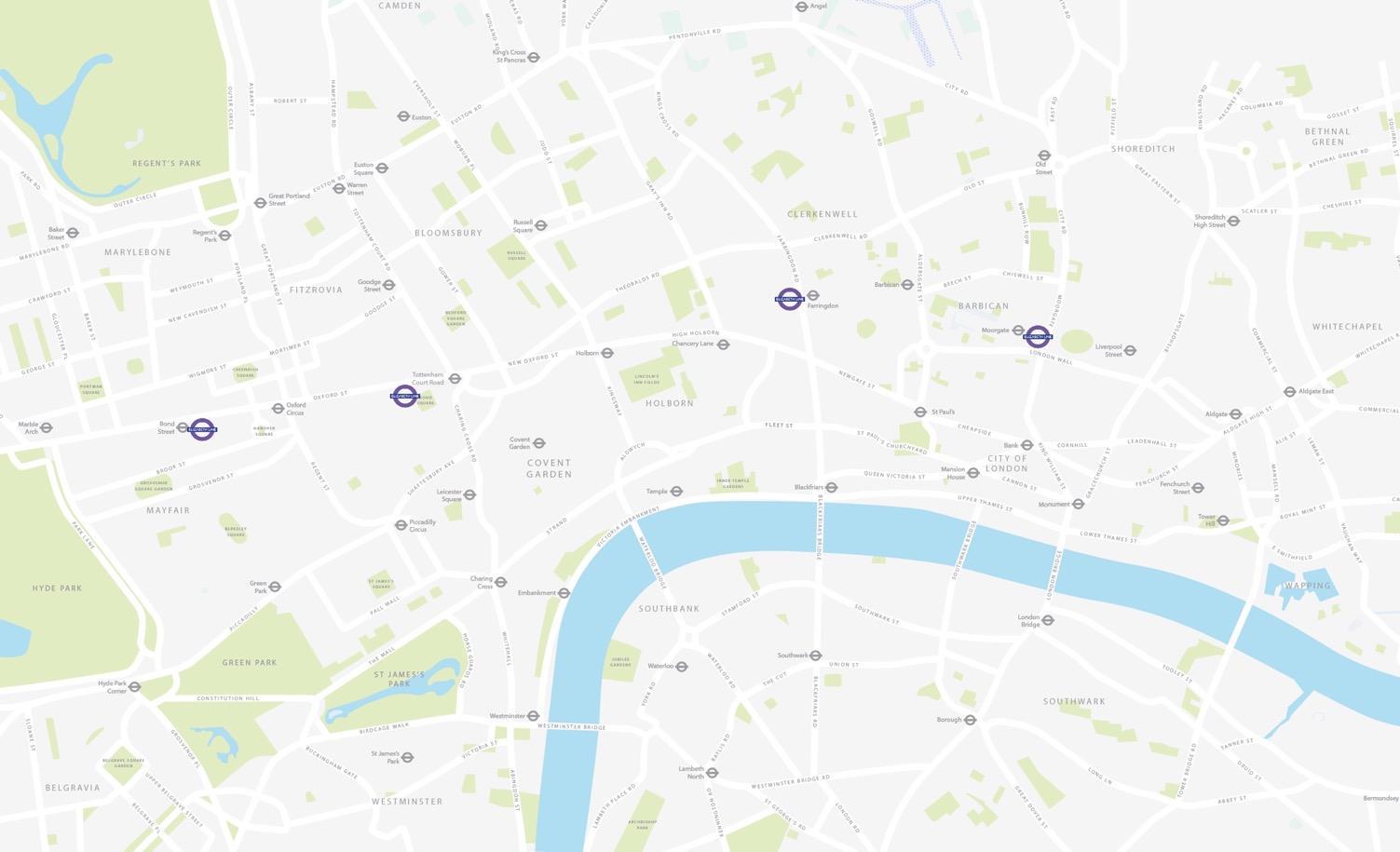

Portfolio: 100% Prime Central London

Highly concentrated portfolio in prime locations; West End focus

Hanover Square, W1

2 Aldermanbury Sq, EC2

30 Duke Street, WC1

Minerva House, SE1

200 Gray’s Inn Road, WC1

1 Newman Street, W1

Structural Growth: Why London

Global city; outperforming UK and EU capital cities

• Largest city economy in Europe; fast-growing

• c.24% of UK GDP; forecast growth: 1.3% for 2026

• Global leadership in finance, services, tech and retail

• #1 European city for digital technology FDI1

• Growing educated population and workforce

• 9.6 million by 20352

• Three of top ten universities globally in London hinterland

• Significant investment in infrastructure and public transport

• Elizabeth line opened; HS2 under construction

• Large, liquid real estate market, leading destination for global investment

• Strong rule of law; favourable time zone; common language

• 440m sq ft of office and retail space

• Structural undersupply of prime, sustainable, high-quality space

• Forecast construction needs to grow by 74% to meet current demand

Structural Growth: Supportive Themes

Driving occupational demand for premium spaces and prime rents

The Evolving Premium Workplace; Quality Matters

• No longer purely a physical setting for work

• Foster belonging, collaboration & productivity

• Attract and retain top talent

• Quality matters:

• Close proximity to public transport

• Amenity rich, both in and around the building

• Outside space: terraces, gardens

• Flexible work settings; supports hybrid working

• Supports health & wellbeing/sustainability agenda

• Prime rents 42% outperformance v secondary

• Demand>supply; 74% additional supply required

Sustainability; an Economic Imperative

• Built environment c.40% of global carbon footprint

• Real estate a critical part of corporate sustainability strategies

• Demand for sustainable space outstripping demand

• Continued Flex growth towards 1 million sq ft ambition

• Underpinning sector leading earnings growth

• Deliver HQ development schemes with further pre-lettings

• 2 Aldermanbury Square, EC2, Minerva House, SE1, 30 Duke Street, SW1 to complete in next 18 months

• Significant development surpluses to come; £220m to £342m (with 10% rental growth)

• Rising to £576m with 20% rental growth and 25bps yield compression

• Supporting NTA growth

• Commit to next wave of HQ developments

• Soho Square Estate, W1 and Whittington House, WC1 to commence 2025

• Exploit attractive investment markets

• More accretive acquisitions to come; stocking the Flex/HQ pipeline

• Rotate towards sales; crystallising surpluses

• Set to deliver 10%+ ROE into medium term (pre-yield compression)

• NAV growth driven by developments surpluses and rental value growth

• Dividend growth driven by rent roll and EPS growth

• Results HY25: 19 November 2025

GPE Investment Case

Our Compelling Investment Case

100% prime central London locations; global city, outperforming both UK and EU capitals

100% premium spaces; creating luxury HQ & Flex offices and retail, high NPS & customer retention

Highly active, cycle led business model; supported by structural change, tailwind for prime rents

37% of portfolio ‘in production’; profitably delivering into dramatic shortage and rental growth

Driving innovation; shaping products to demand with Flex; pioneering the circular economy

Investment markets at attractive entry point; past the trough; building on successful contra-cyclical track record

Strong balance sheet, low leverage; capacity for expansion

Set to deliver strong EPS & NAV growth over medium term; 10%+ ROE p.a.

Unlocking potential in prime central London supported by structural tailwinds yet discounted share price

Disclaimer

This presentation contains certain forward-looking statements. By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances. Actual outcomes and results may differ materially from any outcomes or results expressed or implied by such forward-looking statements.

Any forward-looking statements made by or on behalf of Great Portland Estates plc (GPE) speak only as of the date they are madeand no representation or warranty is given in relation to them, including as to their completeness or accuracy or the basis on which they were prepared. GPE does not undertake to update forward-looking statements to reflect any changes in GPE’s expectations with regard thereto or any changes in events, conditions or circumstances on which any such statement is based.

Information contained in this presentation relating to the Company or its share price, or the yield on its shares, should not be relied upon as an indicator of future performance.

We unlock potential, creating sustainable space for London to thrive

Strong Track Record of Acquisitions

Acquisitions of £1.7bn since 2012

Strong Track Record of Creating Premium Spaces

33 Margaret Street, W1

240 Blackfriars Road, SE1

12/14 New Fetter Lane, EC4

Rathbone Square, W1

160 Old Street, EC1

Hanover Square, W1

Strong Track Record of Portfolio Management

Low vacancy; high NPS; leasing consistently ahead of ERV

Our Diverse Customer Mix

What they say about us

“It is really easy to deal with our customer experience managers on a daily basis. We get on very well with them, and I would say we are very lucky to have them in this building and to get the excellent service provided.”

World Rugby, Woolyard

"I would absolutely recommend GPE to anybody looking for office space in London. They are an amazing company to deal with and, as far as I'm concerned, they are the best landlord I've had so far."

Nordstar Partners, Foxglove House

"I just wanted to write and say thank you for welcoming the team and for all your thoughtfulness and kindness. All of your efforts paid off to make our arrival as smooth as possible. The whole team is re-energised by the move and really enjoying the new space."

BBL/P, Alfred Place

"Communication with our CXM is very positive as they introduced a weekly newsletter, always keeps us updated, and I am very happy with the style and frequency of content of his communication with me."

Bose, Dufour's Place

"Treatwell is proud to be one of the first customers of this incredible building in another outstanding location, and we are super keen to work with the GPE team to put our own stamp on it. We are a pan European brand with unique offices in every market we serve and are delighted that our new London home is SIX."

Treatwell, SIX

“As the UK’s largest pub, cider and beer company, it’s really important that we have an exceptional office space in central London, that reflects the personality of our business and our collaborative ways of working… the new space at wells&more, fits all the criteria.”

Heineken UK

"The security team is very nice and attentive, and the building feels secure and well monitored."

Morgan Stanley, Kent House

0

"Recently, it has been very easy to work with GPE, and we have just met GPE's Customer Relationship Lead. I find the senior team at GPE to be available and accessible when we need them."

Airfinity, Orchard Court

Strong Track Record: Diverse Customer Base

Customer First approach; high levels of satisfaction, occupancy and retention1

Strong Track Record of Recycling

Investing to Deliver Value Growth

Deliver surpluses of £340m+ through capex and crystallising returns through sales

Sustainability Statement of Intent

Embedded across the business; ambitious targets set

• Address the transitional risks of climate change and implement net zero carbon transition plans at each asset

• Integrate climate adaptation and resilience measures into our buildings

• Work with our supply chain partners to improve the climate resilience of our supply chain

• Support our communities to become more climate resilient

• Reduce embodied carbon by 52% across new build developments and major refurbishments by 2030

• Embrace the circular economy

• Reduce energy intensity by 47% across our occupied portfolio by 2030

• Engage with our value chain, to understand customer and supply chain sustainability ambition

• Decarbonise our energy supplies, removing fossil fuel energy generation on-site and from the energy we procure

• Manage residual carbon emissions only once the above measures have been addressed

• Integrate wellbeing considerations into the external and internal design of our spaces

• Use nature-based solutions to support improved external air quality

• Manage and monitor indoor air quality to support the health and wellbeing of our customers

• Promote initiatives to support the health and wellbeing of our people, customers and supply chain partners

• Create at least £10 million of social value in our local communities by 2030 and prioritise improving access to nature

• Support charitable and non-profit organisations that challenge inequality, champion diversity and tackle health and wellbeing

• Champion diverse skills and accessible employment

– Support the growth of local business and social enterprises

Our Sustainability in Action

An imperative: innovative approach embedded across the business

First Net Zero Development; 50 Finsbury Square, EC2

• 100% Pre-let to Inmarsat; sold 2022, 3.85% yield

• Exemplar sustainability credentials:

• 128,100 sq ft refurbishment, reuse and recycle approach

• 80% embodied carbon saving against new build

• Reuse of glazing and repurposing of stone cladding

• Fossil fuel free; WELL enabled

• BREEAM Excellent; EPC B

• £365,000 contribution to GPE decarbonisation fund

• Net Zero Carbon verified

Innovative Use of the River Thames

• Minerva House located on the south bank of the River Thames

• Refurbish and retrofit project; reusing 70% of existing fabric

• Barge utilised to remove materials on site during deconstruction

• River Thames primary route for transport

• Heavy good vehicles to site reduced by 65%

• Reducing air pollution and noise

Market Leading Approach to Material Reuse

• Previous building at 2 Aldermanbury Square deconstructed to extract steel columns and beams

• 1,700 tonnes of steel recovered ,refurbished & recertified

• 211 tonnes utilised in new 2 Aldermanbury Square

• 900 tonnes utilised in 30 Duke Street, W1

• Reducing embodied carbon from the steel by >95%

• Removes need for on floor columns = best in class space

• Lessons learned informing next phase of development projects

Creation of New Circularity Score

• Targeting 52% reduction in embodied carbon by 2030

• Requires minimising the use of virgin materials in development

• Pioneering with a new Circularity Score

• Targeting a percentage of reused materials in development: