Beyond the dollar signs, Donald Trump’s Middle East agreements are poised to reshape the region’s development trajectory

Beyond the dollar signs, Donald Trump’s Middle East agreements are poised to reshape the region’s development trajectory

The Bola Tinubu administration has ushered in a period of economic uncertainty for Nigeria. The removal of fuel subsidies has plunged the country into serious financial strain, with gasoline prices soaring by nearly 500%. Additionally, between October 2023 and October 2024, the value of Nigeria's domestic currency plummeted by more than 100% following the liberalisation of the foreign exchange market. Will 2025 deliver the "renewed hope" Tinubu once pledged, or will the economic challenges facing Nigerians only deepen?

Meanwhile, in Spain, major cities are undergoing rapid transformation driven by real estate speculation and the growing dominance of tourist apartments. Skyrocketing rents are displacing long-time residents and small businesses, while international hospitality chains replace oncethriving local establishments. These developments now symbolise the broader housing crisis engulfing the European nation.

In December 2024, OpenAI introduced its latest artificial intelligence models, o3 and o3-mini, building on the earlier o1 models. These advanced "reasoning" models were evaluated using tasks designed to test general intelligence at levels comparable to that of humans. Are we closer to achieving artificial general intelligence than previously believed? Only time will tell.

Lastly, the April-June 2025 edition of Global Business Outlook will feature US President Donald Trump's recent Middle East tour as its cover story. During his three-day trip with visits to Saudi Arabia, Qatar, and the United Arab Emirates, Trump oversaw the signing of agreements worth more than $2 trillion. These deals spanned sectors including aviation, defence, technology, energy, and education. We will provide a comprehensive analysis of the strategic implications of the tour for regional and global geopolitics.

Thomas Kranjec Editor kimberly@gbomag.com

Director & Publisher

Krushikesh

Editor

Thomas Kranjec

Production & Design

Brian Williams

David Brenton

Ian Hutchinson

Shankara Prasad

Editorial

Stanley Rogers

Rachel Taylor

Lucas Cooper

Tom Hardy

Business Analysts

Adam Fagoo

Arthur Salt

Jerry Thomas

Sumith Jain

Business Development Manager

Benjamin Clive

Head of Operations

David Pereira

Marketing

Danish Ali

Research Analysts

Richard Sam, Sophia Keller

Accounts Manager

Edyth Taylor

Press & Media Contact

Craig Penn

Registered Office: Global Business Outlook Magazine is the trading name of

Business Outlook Media Ltd Winston House, 2 Dollis Park, London, England, N3 1HF

Phone: +44 (0) 207 193 3740 Fax: +44 (0) 203 725 9247

Email: media@gbomag.com

Industry

Thames Water

Analysis

GBO Correspondent

The financial troubles of Thames Water highlight the challenges facing England and Wales' privatised water industry

Sewage floating down rivers in the United Kingdom has turned into a noxious political symbol. However, a recent court decision involving Thames Water's obligations focused more on the money flow than the water and effluent flow.

Amid the chaos of England and Wales' privatised water sector, Thames Water stands out. In a last-ditch effort to escape temporary nationalisation at the end of March, the corporation, heavily indebted with roughly £19 billion, asked the court for permission to borrow an additional £3 billion from a group of current creditors.

This procedure, referred to as special administration, would protect the water supply for 16 million homes and companies in south-east England and London. However, it would also reverse Margaret Thatcher's privatisation more than thirty years ago, causing a great deal of trouble for the Keir Starmer-led Labour government and the larger water sector.

Another reason why opponents of the most recent debt agreement have called for special management is that they believe it would result in more funding for repairing leaking pipes and sewers and less for the handful of businesses that are accruing exorbitant fees as a result of Thames' problems.

Over 100 investors, bankers, attorneys, and other advisors attended the high court recently, either in two crowded courtrooms or via video conference, demonstrating the scope of the operation.

The interest expenses are egregious. Most of the time, the general public is unaware of the bond markets. However, when a business experiences severe financial difficulties, like Thames has, court cases can reveal how closely English home water rates are tied to international financing.

Two sets of possible lenders faced off against one another during the court session. An interest rate of 9.5% is being offered by one hedge fund that holds debt referred to as "class A," while the smaller group of "class B" hedge funds asserts an offer of 8%. The class A group intends to distribute the £3 billion in two lots of £750 million, after an initial £1.5 billion.

For the benefit of customers, Charlie Maynard, a former investment banker and current Liberal Democrat MP for Witney, Oxfordshire, was permitted to get involved in the case. The class A offer, he said, was "ludicrously expensive debt."

Andy Fraiser, Thames' general counsel, told the court: "You can come up with a plan which is cheaper but is not deliverable."

According to Maynard's legal team, two-thirds of the £1.5 billion would "go into the pockets of debt investors and professional advisers," including more than £440 million in fees and discounts and £245 million in interest

paid to those investors. Numerous international banks and investors showed a great deal of interest in the court case; some of them even traded the debt.

The US firms JP Morgan and Goldman Sachs, the UK banks Barclays, Lloyds Banking Group, and HSBC, the Canadian banks Scotiabank and National Australia Bank, and the French bank BNP Paribas all seemed to be online attendees. Large investors, including hedge funds, also seemed to be following.

They included hedge funds such as the Londonbased Algebris and Insight Investment, along with America's Diameter Capital, Bracebridge Capital, and Centerbridge. Additionally, well-known investors like Pimco, Corebridge, and Millennium Management were part of the group.

Although the class A group also includes hedge funds like Elliott Investment Management and Silver Point Capital, while the class Bs include Polus Capital and Covalis Capital, attendance does not always indicate

that the companies have financial exposures to Thames Water. The names of the corporations involved were not revealed by either group of creditors.

To advocate for public ownership of public utilities including libraries, railroads, and water, Cat Hobbs formed “We Own It.” She stated that to restrict the flow of funds from Thames Water, the court ought to reject the debt agreement and instead opt for special administration.

"This is merely a 'money-go-round,' and they want to continue it for as long as possible. It would be an absolute farce if it were to proceed. In the restructuring, the interests of the creditors will be given top priority, whereas, in the special administration, they would not. Armies of advisors. Even if the interest rates are high, taking risks is rewarded,” she stated.

Nevertheless, the costs paid to all of those attorneys, bankers, and public relations consultants will also cause hundreds of millions of pounds to leave Thames Water in the upcoming months. Thames has enlisted the help of the restructuring advisory firm Kroll and the "Magic Circle" law firm Linklaters.

They faced Quinn Emanuel, a class B legal firm, along with other professionals. Thames receives PR help from Edelman Smithfield,

the class A group receives guidance from Hanbury Strategy, and the class Bs are represented by Greenbrook Advisory. While rival Moelis & Company is advising the bondholders of its parent company Kemble, Thames Water has also enlisted the investment firm Rothschild & Co. to look for new equity investors to take over ownership.

Thames was incurring costs of approximately £15 million each month for restructuring, according to Alastair Cochran, the company's Chief Financial Officer.

The total cost of the process might come to over £200 million, which is a minor sum compared to the water company's enormous bank sheet but a large payout for all parties concerned. The class As, class Bs, and Thames Water all refused to provide specifics about the process fees.

Thames's rates have been increased even by the regulator, Ofwat. In its annual report released this week, it stated that it had ordered Thames to repay £6 million for work done on the business during the fiscal year 2023–2024. Lazard, Ofwat's in-house investment bank, has been brought in to provide advice. One more round. Those close to Thames Water think that if the corporation did not hire counsel, it would be criticised from the opposite side.

Whether the Thames can remain privately owned, which the business claims will save the taxpayer money on maintaining it, will be largely determined by that recommendation. The business and its creditors strongly dispute that the fees would eventually be covered by invoices, claiming that creditors will cover them when the business's balance sheet is repaired.

During an interaction with The Guardian, a Thames representative said, "Any suggestion that customers will bear costs from this process is an untrue and misleading claim that risks needlessly worrying our customers."

Customer bills won't shoot up as a result of this proposal.

“The cost of bills for the upcoming five years has already been established by Ofwat. Our strategy is still the only workable way to give the company a stronger financial foundation. Customer bills won't change if it's approved, but billions of pounds will be available for network improvements, pipe repairs, sewage treatment plant upgrades, and the preservation of clean drinking water,” the person stated.

The trading firm Jefferies, another adviser to the

class As, estimates that those billions of pounds might total an additional £7 billion. These funds will need to be restructured later this year. The fees will therefore continue to be collected.

Another firm, Teneo, estimated that even in the case of a special administration, consultants would charge £98 million to arrange finance. This would include £63 million for administration costs, £25 million for legal fees, and an additional £10 million for merger consultants. Thames has paid £5 million for PR and restructuring advice to Teneo, which may be a candidate to lead the special administration.

"This is only the first of many levies that are gradually increasing in amount. There's another fees fest coming up the road,” Maynard, whose attorneys Marriott Harrison and William Day worked pro gratis, stated.

The financial troubles of Thames Water highlight the challenges facing England and Wales' privatised water

industry. As the high court deliberates on the company’s borrowing strategy, the stakes are high, not just for Thames Water but also for the millions of consumers who depend on its services.

The outcome of this case could determine whether privatised utilities can deliver on their promises or if public ownership is the only viable path forward, shaping the future of water management in Britain.

Feature

GBO Correspondent

Cuba, an island known for its resilience and revolutionary spirit, is currently facing one of the most significant energy crises in its modern history. Rolling blackouts, ageing infrastructure, fuel shortages, and an increasingly fragile economy have left millions of Cubans struggling to cope with the impacts of unreliable electricity.

We will examine the roots, scale, and implications of the Cuban energy crisis, utilising recent data, historical context, and expert insights to provide a comprehensive overview of the situation.

Everyday life of an average Cuban Blackouts lasting up to 20 hours a day have become commonplace, particularly outside Havana, where infrastructure is less robust. Food insecurity is worsening as unrefrigerated supplies spoil amid extended power cuts, directly affecting households that already spend a significant portion of their income on food. In many urban areas, running water is often disrupted because electric pumps are needed to move water from cisterns to homes.

For the average Cuban, the hardships are overwhelming. Entire families must endure relentless heat without fans or air conditioning, even during sweltering summer months. The smell of spoilt food lingers in neighbourhoods, as refrigerators are rendered useless by the frequent power cuts.

Parents face the daunting task of cooking meals with limited fuel resources, while children struggle to complete their homework by candlelight or the dim glow of a battery-powered lamp. Waiting in long lines for necessities has become an exhausting daily routine, compounded by the uncertainty of whether those items will even be available. The stress and anxiety of not knowing when electricity will

Cuba's energy infrastructure has a complex history shaped by political alliances, especially during and after the Cold War

size of neobanks from 2021 to 2023 (In Billion US

Source: Statista

Source: Statista

be restored take a toll on mental health, and many Cubans are left feeling isolated and abandoned by a system that seems incapable of providing even the most basic services.

Healthcare facilities, most of which rely on outdated generators, struggle to maintain basic services. Reports indicate that some hospitals have had to ration power, prioritising critical units like intensive care while suspending other services. The impact on public health has been severe, with increased instances of heat-related illnesses and rising mental health concerns linked to prolonged uncertainty and hardship.

Educational institutions have not been spared either. In October 2024, the government closed schools for several days, citing the need to reduce nonessential electricity consumption. This disruption in education, combined with broader economic difficulties, has added to the sense of despair among the youth of the country, many of whom believe migration is their only viable option. Indeed, between 2021 and 2023, over a million Cubans left the country, about 10% of the population, marking one of the largest emigration waves since the 1959 revolution.

Cuba's energy infrastructure has a complex history shaped by political alliances, especially during and after the Cold War.

Throughout the 20th century, Cuba's energy needs were mostly met through support from the Soviet Union, which provided the island nation with fuel and technological assistance. With the collapse of the Soviet Union in 1991, Cuba was left without its primary supplier, plunging into a severe economic downturn referred to as the "Special Period." During this time, Cuba attempted

to restructure its economy and diversify energy sources by using biomass, wind, and solar power, yet these efforts were insufficient to meet the island's energy needs.

Cuba remains heavily reliant on thermoelectric power plants, which produce around 80% of the nation's electricity. These plants are fuelled predominantly by oil, much of which historically came from Venezuela. This dependency has become increasingly problematic as Venezuela's economic crisis has limited its ability to provide Cuba with affordable oil.

In 2024, Venezuelan oil shipments to Cuba fell to 25,000-30,000 barrels per day, a significant drop from the 100,000 barrels per day supplied a decade ago, forcing Cuba to seek alternative and often more expensive sources on the global spot market.

Cuba's energy infrastructure is aged and overburdened, with most power plants well beyond their intended lifespan. The Antonio Guiteras thermoelectric power plant, located near Matanzas, is one of the largest and oldest plants, with its operations frequently disrupted due to technical failures and fuel shortages.

As of late 2024, Cuba's five main thermoelectric plants are all over 30 years old, with some approaching 50 years, significantly past their designed operational limits of 25-30 years. This has led to frequent breakdowns, decreased efficiency, and a substantial increase in the frequency of blackouts.

The Cuban National Electrical Union (UNE) has reported a high number of grid collapses recently, with four such incidents occurring in two days in October 2024. UNE officials have highlighted how obsolete equipment, lack of spare parts, and financial constraints make timely repairs nearly impossible.

The reliance on emergency measures such as floating power plants, leased from Turkey, has provided only temporary relief. These ship-based generators have limited capacity and cannot meet the energy demands of a nation with 10 million people, particularly as those demands continue to rise.

Fuel shortages are central to Cuba's energy crisis. With Venezuelan oil shipments plummeting, Cuba has attempted to compensate with oil imports from countries like Russia and Mexico, but these have also decreased. In early October 2024, a fuel tanker carrying essential supplies to Cuba was delayed due to bad weather, further exacerbating the country's inability to generate adequate power. Estimates suggest that Cuba currently generates only about 500 megawatts on the grid, compared to the three gigawatts needed to power the entire country effectively.

The United States' trade embargo, which has been in place for over 60 years, has significantly limited Cuba's ability to invest in its energy sector. The embargo prevents Cuba from accessing credit from international financial institutions and restricts the import of technology needed to modernise its infrastructure.

According to Cuban officials, the embargo has cost the island more than $130 billion in cumulative losses. The inability to access advanced equipment

has led to stagnation in progress and forced reliance on obsolete technologies that are both inefficient and costly to maintain.

The US has also been accused of orchestrating numerous covert operations intended to destabilise the Cuban government, contributing to ongoing hardships. These actions include support for anti-government groups and efforts to undermine the island's economy, making recovery from crises like the current energy situation significantly more challenging.

Cuba's political apparatus has long been marked by inefficiencies, a lack of transparency, and centralised decisionmaking that stifles innovation and local autonomy. The government's commitment to a centrally planned economy has left little room for market-driven reforms that could stimulate growth or attract foreign investment.

This rigidity has been a significant obstacle to economic diversification and modernisation, particularly within the energy sector. The decision-making process remains dominated by the Communist Party, with key roles occupied by individuals selected based on loyalty rather than expertise. This has resulted in poor policy implementation and an inability to respond quickly to crises, such as the current energy shortage.

Moreover, the Cuban government has often prioritised political stability over

Cuba's energy infrastructure is aged and overburdened, with most power plants well beyond their intended lifespan. The Antonio Guiteras thermoelectric power plant, located near Matanzas, is one of the largest and oldest plants, with its operations frequently disrupted due to technical failures and fuel shortages

The energy crisis has devastated the Cuban economy, which is already struggling with limited productivity and high inflation. Many businesses have had to close or reduce operating hours due to unreliable electricity

economic pragmatism, maintaining a tight grip on public discourse and dissent. State-controlled media outlets minimise the extent of economic problems, while authorities have been known to suppress protests and silence critics, as seen during the 2024 blackouts.

This lack of accountability not only increases public frustration but also restricts the government's ability to effectively leverage the collective ingenuity of its people. The inability of the political apparatus to adapt and reform has thus played a critical role in exacerbating the current energy crisis, with little indication of a shift towards policies that could create sustainable, long-term solutions.

The energy crisis has devastated the Cuban economy, which is already struggling with limited productivity and high inflation. Many businesses have had to close or reduce operating hours

due to unreliable electricity. The tourism sector, a crucial source of foreign currency, has also been severely affected. Major hotels in Havana, usually resilient due to backup power systems, ran out of fuel for their generators during recent blackouts, leading to a drop in bookings and revenue.

Cuba's GDP could shrink by 3% in 2024, marking the third consecutive year of economic contraction. Export earnings are still $3 billion short of pre-pandemic levels, and inflation has significantly eroded purchasing power.

The combination of high costs for imported fuel, reduced productivity, and limited foreign reserves has pushed Cuba into what officials have termed a “war economy,” austerity measures aimed at cutting consumption and conserving whatever limited resources remain.

Social unrest has been simmering, with small-scale protests emerging in response to blackouts and deteriorating living conditions. President Miguel DíazCanel's administration has taken a hard stance against dissent, deploying police and military units to prevent the spread of protests.

During the latest round of blackouts, Díaz-Canel appeared on television, dressed in military attire, warning against any attempts to disrupt public order, framing dissent as a product of foreign interference. Despite these warnings, frustrations continue to grow, particularly among younger Cubans who see little opportunity for economic improvement.

Efforts to address the energy crisis have included emergency measures like leasing floating power plants and importing fuel on the spot market. Still, these solutions are neither sustainable nor cost-effective in the long term. Cuba has also sought to boost its renewable energy capacity, with mixed results.

The government aims to produce 24% of its electricity from renewable sources by

2030, primarily through wind, solar, and biomass. However, as of 2024, renewables make up less than 5% of the total energy mix, hindered by a lack of investment and the challenges of importing technology.

Cuba's geographical location gives it a significant advantage in harnessing solar and wind energy, and some small-scale projects have shown promise. For instance, the solar photovoltaic park in Cienfuegos is one of the largest in the Caribbean, providing much-needed power to local communities.

However, without large-scale investments and technology transfers, these initiatives remain limited in scope. The trade embargo has also made it challenging for Cuba to access the international financing needed to scale up renewable energy projects, despite some support from European nations and China.

One potential avenue for relief lies in improved diplomatic relations with the United States. During the Obama administration, US-Cuban relations improved, leading to increased remittances and tourism that positively impacted the Cuban economy. A renewed engagement could ease access to credit and technology, although current US political dynamics make such a shift uncertain. Former President Joe Biden had relaxed some sanctions, allowing for limited remittances, but broader relief has not yet materialised, largely due to domestic political pressures in the United States.

The energy crisis in Cuba is not an isolated incident but rather a symptom of broader systemic challenges facing the island. It highlights the vulnerabilities of a centrally planned economy that could not modernise its infrastructure or diversify its energy sources effectively.

The crisis also underscores the impact of climate change on vulnerable nations. Cuba, which has faced multiple hurricanes

in recent years, lacks the resilience to quickly recover from natural disasters, which often target critical infrastructure, further deepening its energy woes.

The migration of over a million Cubans since 2022 is both a consequence and a driver of the crisis. With an ageing population and a diminishing workforce, Cuba's capacity to recover economically is further compromised. The demographic shift will likely have lasting effects, reducing productivity and increasing the dependency ratio, placing additional strain on already limited social services.

Despite Cuba's close ties with allies such as Russia and China, these nations have limited capacity to provide meaningful assistance in addressing the energy crisis. Russia, embroiled in its geopolitical struggles and economic sanctions, is focused on maintaining stability at home and supporting its involvement in other regions like Ukraine.

China's economic growth has also slowed, with domestic priorities including a struggling real estate market and its energy demands. Furthermore, China has to manage its international loans and investments carefully to avoid overextension. Other regional allies face similar limitations, leaving Cuba largely isolated in terms of receiving substantial external support.

Addressing Cuba's energy crisis will require a combination of internal reforms, international support, and, potentially, a rethinking of US-Cuba relations. Without such changes, the crisis might persist, further eroding the quality of life for millions of Cubans and pushing the nation deeper into economic stagnation and social instability. The resilience of the Cuban people has been remarkable, but without systemic change, their ability to endure these hardships is being pushed to its limits.

Cuba's geographical location gives it a significant advantage in harnessing solar and wind energy, and some small-scale projects have shown promise. For instance, the solar photovoltaic park in Cienfuegos is one of the largest in the Caribbean, providing much-needed power to local communities

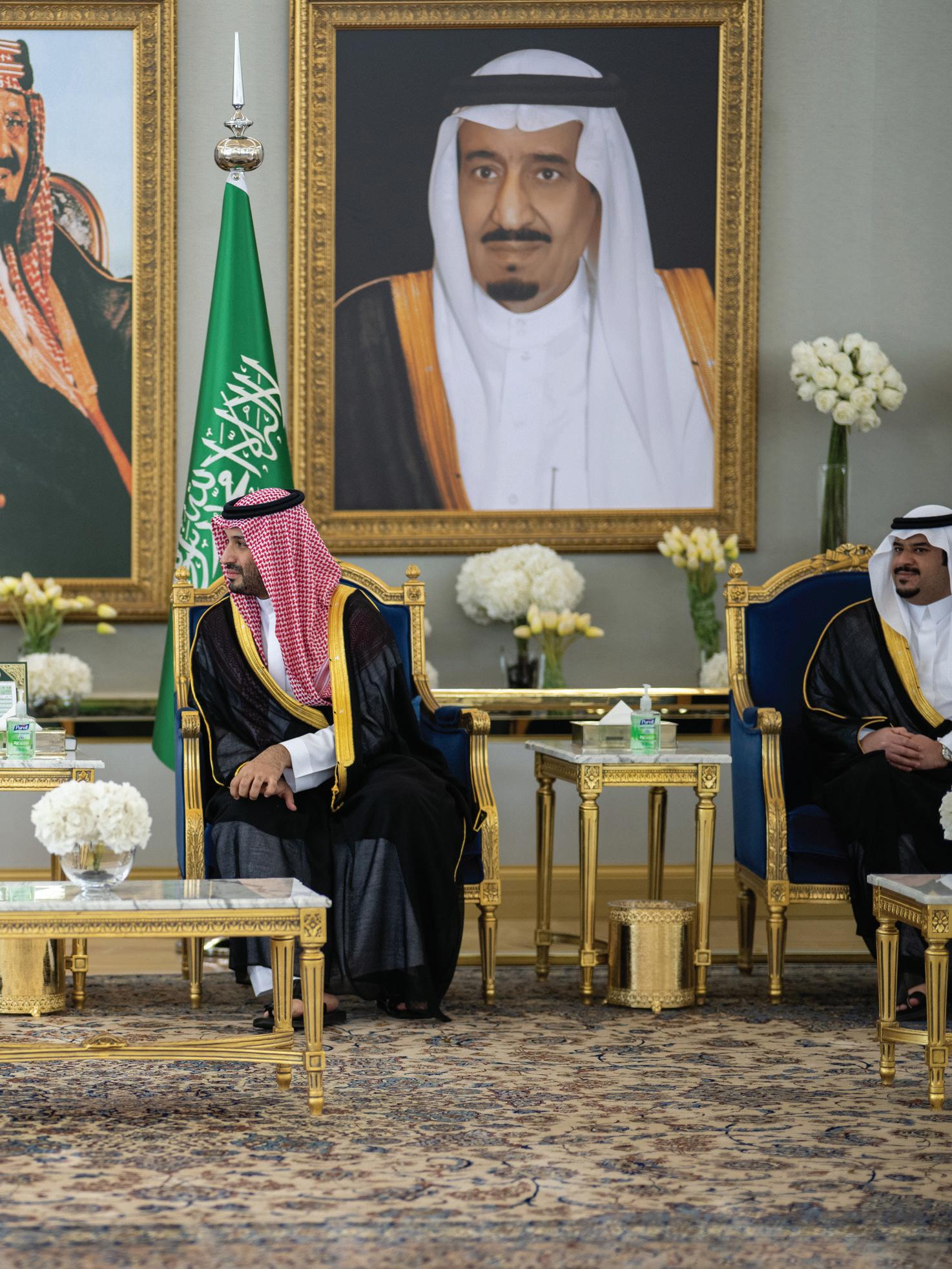

Beyond the dollar signs, Donald Trump’s Middle East agreements are poised to reshape the region’s development trajectory

United States President Donald Trump’s Spring 2025 tour of the Middle East was nothing short of momentous. Over the span of three days, with stops in Saudi Arabia, Qatar, and the United Arab Emirates, Trump presided over the signing of agreements valued at more than $2 trillion across aviation, defence, technology, energy, and education.

Greeted with lavish royal welcomes, state dinners, and even the UAE’s Burj Khalifa lit up in American colours, Trump’s visit underscored a dramatic deepening of Washington-Gulf partnerships. The White House hailed the trip as a “huge success, locking in over $2 trillion in great deals” – including a $600 billion Saudi investment pledge, a $1.2 trillion economic exchange accord with Qatar, and hundreds of billions in new trade deals with all three countries.

This massive haul of agreements signals a significant shift in tone from Trump’s first presidential foray into the region in 2017. Then, as a newly elected leader, the Republican’s focus was on arms sales and counterterrorism; in 2025, the emphasis expanded to cutting-edge tech and economic development.

“I have absolutely no doubt that the relationship will only get bigger and better,” Trump remarked in Abu Dhabi, projecting confidence that these deals mark the start of a new era in US-Middle East relations.

Surrounded by Gulf royals and a who’swho of American CEOs, Trump cast himself as dealmaker-in-chief, leveraging personal diplomacy and American commercial clout to reassert Washington’s influence in a region courted aggressively by China and others. The result was a bundle of mega-deals spanning everything from Boeing jets to artificial intelligence ventures, all forged on a foundation of mutual economic interest.

From aviation to AI, pacts galore

Trump’s itinerary – Riyadh, Doha, Abu Dhabi –brought a whirlwind of signings. In each capital, US and Middle Eastern officials inked high-value agreements cutting across many sectors. Notable deals announced during the visit include aviation, defence, technology, data, energy, education, infrastructure, and culture.

Boeing clinched historic aircraft sales in the region. Qatar Airways ordered up to 210 Boeing widebody jets (787s and 777Xs) worth $96 billion, the largest widebody purchase in Boeing’s history. In the UAE, Etihad Airways committed $14.5 billion for 28 Boeing 787 and 777X airliners powered by GE engines. These deals will upgrade Gulf carriers’ fleets and are touted to support tens of thousands of US aerospace jobs.

Security ties got a major boost. Saudi Arabia and the US signed the largest defence agreement in American history – nearly $142 billion for advanced fighter jets, missile defence, warships, and more. Riyadh is now Washington’s biggest foreign military sales customer, with active cases valued at over $129 billion.

In Qatar, Trump oversaw deals for cuttingedge weapons: Raytheon will provide a $1 billion counter-drone system, making Qatar the first international buyer of that tech, and General Atomics will sell $2 billion worth of MQ-9B Reaper drones. Qatar also inked a statement of intent outlining another $38 billion in potential defence investments – including support for the US airbase at Al Udeid and future air and naval security projects. These agreements strengthen Gulf militaries with American hardware while reinforcing US security commitments in the region.

In fact, as per the White House, the arms package was "the largest defense cooperation agreement" Washington has ever done with any country, involving more than a dozen American defence companies.

It proved to be a diplomatic victory for Uncle Sam, as it reversed the Joe Biden administration's failure of finalising a defence pact with Riyadh as part of a broad deal that envisioned Saudi Arabia normalizing ties with Israel. While the White House did not mention if Riyadh would be permitted to purchase Lockheed's F-35 jets, the cutting-edge stealth aircraft that the Kingdom has reportedly been interested in for years.

A centrepiece of the tour was unprecedented cooperation in data and artificial intelligence. The UAE will host a new five-gigawatt “AI supercampus” – the largest AI research and data centre facility outside the US – under a US-UAE tech partnership.

In parallel, Washington agreed to ease export restrictions so that the UAE can import up to 500,000 of Nvidia’s most advanced semiconductor chips for AI development, a capability previously blocked over Washington’s fears of Chinese access. Saudi Arabia struck a similar bargain: its new stateowned AI company, HUMAIN, obtained hundreds of thousands of Nvidia’s cutting-edge Blackwell AI chips, giving the Kingdom raw computing power on par with top global tech hubs.

Big American tech firms also jumped in – Cisco signed on with a UAE partner to develop local AI talent, Amazon Web Services announced cloud and cybersecurity initiatives, and Google’s Alphabet agreed to help Saudi Arabia launch a “Global AI Hub” with the Public Investment Fund. These deals marry Gulf capital with American know-how, aiming to transform the region into a leader in artificial intelligence and data services.

Several agreements advanced Gulf nations’ ambitions beyond oil. In Abu Dhabi, ExxonMobil, Occidental, and EOG Resources partnered with ADNOC (Abu Dhabi’s national oil company) on a $60 billion project to boost oil and gas output – a pact expected to create jobs in both countries and ensure stable energy supplies.

Cover Story

Trump Gulf

Trump’s 2025 Middle East foray deliberately echoed his very first trip as president in May 2017 – but with some notable twists. In 2017, Trump also landed first in Riyadh, where Saudi royals rolled out an extravagant reception and the president famously joined a sword dance amid glowing orbs and opulent decor

Meanwhile, Emirates Global Aluminium (EGA) will invest $4 billion to build a new aluminium smelter in Oklahoma – notably, America’s first new aluminium plant in 45 years –doubling US aluminium output capacity while strengthening critical mineral supply chains. In Qatar, Houstonbased McDermott secured $8.5 billion in contracts to support Qatar’s LNG expansion with offshore engineering, directly tying US expertise to Qatar’s gas infrastructure growth.

And across Saudi Arabia’s massive development projects – from the new King Salman International Airport to the Qiddiya entertainment city – American firms like Hill International and Jacobs are involved in under $2 billion worth of infrastructure and consulting contracts. These deals underscore that the partnership isn’t only about high tech – it also cements Washington’s involvement in the Gulf’s physical transformation and energy future.

Taken together, the deals paint a picture of a Middle East pivoting to a high-tech, knowledge-based future with American partnership. The breadth of cooperation – from museums to missiles – speaks to a comprehensive strategic realignment between the United States and its Gulf partners.

Trump’s 2025 Middle East foray deliberately echoed his very first trip as president in May 2017 – but with some notable twists. In 2017, Trump also landed first in Riyadh, where Saudi royals rolled out an extravagant reception and the president famously joined a sword dance amid glowing orbs and opulent decor.

Back then, Trump announced a record $110 billion arms deal with Saudi Arabia (part of a promised $350 billion over 10 years), and he convened dozens of Arab and Muslim leaders to

rally against terrorism. The tone was muscular and security-focused: Trump lauded Middle Eastern allies for “driving out” extremists and pointedly refused to lecture on human rights, signalling a transactional approach.

It was a honeymoon of sorts between Trump and Gulf monarchies – but many of 2017’s grand pledges remained aspirational. In fact, out of the $110 billion in arms sales, Trump touted in 2017, only about $30 billion had been implemented by 2025. Some business deals never fully materialised; for example, a Saudi plan to buy 50 US drilling rigs resulted in only 11 delivered in the ensuing years.

The 2017 trip’s impact was also marred by geopolitics soon after – a bitter rift erupted when Saudi Arabia and the UAE blockaded Qatar just weeks later (a move Trump initially appeared to support), revealing cracks in Gulf unity.

Fast forward to May 2025 and the landscape has evolved. The intra-Gulf feud has since healed, and Trump’s itinerary notably included Doha – a sign of Qatar’s reintegration and of Washington’s intent to balance relationships with all its Gulf partners.

In contrast to 2017’s singular focus on Saudi Arabia, the 2025 tour was a triplestop diplomatic marathon, symbolically treating Riyadh, Doha, and Abu Dhabi as co-equals in regional leadership. The focus, too, had broadened. Security cooperation was still key, but economic and technological partnerships took centre stage.

One reason is the shifting regional dynamics: Gulf leaders are now focusing more on commerce than conflict. Trump capitalised on this emerging momentum.

In place of a counterterrorism summit, he headlined business forums – rubbing shoulders with CEOs like Nvidia’s Jensen Huang, OpenAI’s Sam Altman, Tesla’s Elon Musk, Amazon’s Andy Jassy, and Palantir’s Alex Karp, who all flew

in for deals. The presence of these tech titans underscored a new tone: America’s engagement is no longer just about selling weapons, but also about jointly building the Middle East’s tech economy.

Another shift was in priorities and rhetoric. In 2017, Trump made combating Iran’s influence a marquee theme, aligning with Riyadh’s hawkish stance. In 2025, while still warning Tehran to “take a new and better path” on its nuclear programme, Trump also floated prospects of a revised deal if Iran complies. At the same time, Trump shocked some observers by holding out Saudi Arabia as a model for regional modernisation, even suggesting war-torn Syria might follow suit if given economic incentives.

The geopolitical context is also more favourable to Trump’s deal-making now. The Abraham Accords he facilitated in

2020 have endured, creating new business opportunities that span Israel and the Gulf. Though Israel was not on Trump’s 2025 itinerary, the spirit of regional integration it represents hung in the air. Gulf states, flush with petrodollar wealth after recent oil booms, are eager to invest in diversification and welcome US partnerships to balance growing ties with China.

Indeed, China’s shadow loomed over the visit: in the interim years, Beijing had courted the Gulf. One must also remember that President Xi Jinping received a red-carpet welcome in Riyadh in 2022, and China’s tech and infrastructure investments have expanded across the Middle East.

The Biden administration responded by restricting exports of top-tier US tech, like advanced microchips, to Gulf nations for fear they might leak to China.

For Donald Trump, the political payoff is clear. At home, he can tout “$2 trillion in great deals” creating jobs and exports, reinforcing his image as a master negotiator delivering results. Abroad, he has

reasserted American primacy in a region where rival powers have made inroads

Trump’s 2025 deals essentially reverse that stance – offering the UAE and Saudi Arabia access to cutting-edge US semiconductors and AI technology on the condition they “keep the tech for themselves” and enforce safeguards against diversion to rivals.

As one analysis noted, many of Trump’s new agreements “broke with the policies of Joe Biden’s administration” on tech control. Gulf leaders, for their part, appeared delighted to engage on these terms –even gifting Trump a $400 million Boeing 747-8 jet (courtesy of Qatar’s Emir) for future use as Air Force One in a symbol of personal rapport.

In sum, the 2017 and 2025 visits bookend Trump’s approach to the Middle East: the first trip was about resetting alliances and striking big defence deals, while the latest was about leveraging those alliances into broader economic win-wins.

Beyond the dollar signs, Trump’s Middle East agreements are poised to reshape the region’s development trajectory. For Saudi Arabia, the UAE, and Qatar, the deals promise not just short-term commerce but also long-term leaps in technology, infrastructure, and “digital sovereignty.”

In Riyadh, Abu Dhabi, and Doha alike, leaders have been articulating ambitious visions (Saudi’s Vision 2030, Qatar’s National Vision 2030, and UAE’s Centennial 2071 plan) to create smart, knowledge-based economies. The US partnerships announced in May 2025 directly feed those agendas in several ways:

The highlight for many in the Gulf is access to cutting-edge American technology – especially in artificial intelligence. By securing hundreds

of thousands of Nvidia’s top-tier AI chips and building massive data centres to house them, Saudi Arabia and the UAE are ensuring they can develop AI models and big data applications at a world-class level.

The ability to process and analyse one’s own data domestically, with the best hardware available. The new AI mega-campus in Abu Dhabi will reportedly have computing capacity rivalling the biggest tech labs in Silicon Valley.

Also, hand-in-hand with AI comes the realisation of smart city visions across the Gulf. Saudi Arabia’s planned city of NEOM – a futuristic metropolis of robots and renewable energy – and other gigaprojects will require sophisticated tech integration. The deals with the American companies provide vital expertise: American engineering giants such as Parsons and Jacobs are already working on Saudi smart infrastructure, with 30 major project wins valued up to $97 billion for Parsons alone, supporting thousands of US and Saudi jobs.

Those projects range from highspeed transit systems to techaugmented tourist resorts. By bringing in US partners, Gulf governments ensure their new cities are built to the highest standards and filled with the latest innovations.

Qatar, for its part, is leveraging US inputs as it builds smart infrastructure for the 2030 Asian Games and expands projects like Lusail Smart City. The $8.5 billion in LNG infrastructure contracts to McDermott also means Qatar’s energy sector will be more efficient and tech-enabled, indirectly supporting its urban development with better power and utilities.

Moreover, these ventures come with training programmes – e.g. the Quantinuum-Qatar joint venture will train a quantum computing workforce locally – ensuring Gulf nationals gain the skills to run the smart economies being built.

Crucially, digital sovereignty is a recurring theme. For instance, Saudi Arabia’s deal to buy advanced semiconductors for its PIF-owned companies means those chips will reside under Riyadh’s control, powering national projects from smart utilities to advanced R&D, rather than having to rely on foreign cloud providers who might host data abroad. The Gulf states are effectively securing the tools to become producers, not just consumers, in the technology space – a fundamental shift that these agreements accelerate.

Trump’s 2025 Middle East tour will be remembered as a watershed in USGulf relations – one that recast the alliance in terms of enterprise and innovation. In a region historically defined by oil wealth and security pacts, the visit spotlighted a broader narrative: investments, technology exchange, and joint nation-building. Sceptics note that Trump is quick to declare victory – the true test will be implementing these deals in the years ahead. Yet there is an undeniable momentum.

For Donald Trump, the political payoff is clear. At home, he can tout “$2 trillion in great deals” creating jobs and exports, reinforcing his image as a master negotiator delivering results. Abroad, he has reasserted American primacy in a

region where rival powers have made inroads.

The fact that Saudi Arabia openly aimed for a $600 billion package ahead of his visit – and achieved it – shows the degree of buy-in from Crown Prince MBS, who has emerged as a linchpin figure for US interests. In turn, Qatar’s generous gestures (including a VIP airliner gift) and the UAE’s trillion-dollar pledges signal that even smaller states see the advantage in anchoring themselves to the American orbit.

We are likely witnessing the beginning of a new chapter in the Middle East – one characterised less by ideology and more by investment. As one regional commentator put it, Gulf leaders today are “turning petro-dollars into techno-dollars.” The deals on data centres, AI labs, and smart cities suggest a future Persian Gulf that is as much a Silicon Valley as it is an oil basin. It carries profound implications: economically empowering young populations, politically stabilising nations through growth, and perhaps easing the grievances that have driven conflict. Of course, pitfalls remain–from ensuring the technology isn’t misused or proliferated, to managing great-power rivalries as the US, China, and others jostle for influence.

Analysis

GBO Correspondent

Before taking office in 2018, PM Pedro Sánchez stated that Spain had been without a state housing policy for nearly ten years

It has now turned into a mockery of itself, a place where the locals have been driven out for the sake of tourism and growing capital. Combination key safes have appeared in doorways, indicating that the unit has been turned over to vacation rentals. Shops selling ceramic bulls and flamenco dolls have taken the place of a centuryold apothecary and shirtmaker that once existed on La Rambla.

Cities around Spain are gradually changing due to real estate speculation and the rise in tourist apartments; exorbitant rents are forcing out locals and traditional businesses, and neighbourhood mainstays are giving way to international chains, gift stores, burger places, and nail parlours. Such startling facts explain Spain's housing crisis.

According to recent research conducted by the Bank of Spain, nearly half of Spain's tenants spend 40% of their income on rent and utility costs, compared to the European Union (EU) average of 27%. Rents have increased by 80% over the last ten years, exceeding salary gains.

The problem has become the main concern of Spaniards and the subject of the most recent policy dispute between the ruling socialists and their conservative opponents in the People's Party (PP). Real estate speculation and the surge in tourist apartments have exacerbated the problem by increasing living expenses.

In a speech, Prime Minister Pedro Sánchez laid out a 12-point plan to alleviate what he described as the nation's "housing situation emergency." He pointed out that social housing only accounted for 2.5% of Spain's total stock, while it made up 14% in France and 34% in the Netherlands.

"We will split European and Spanish society into two types of people," PM Pedro Sánchez said.

One inherits one or more homes from their parents and can use most of their income for travel and education, while those who

work their whole lives end up as elderly people without a home.

Before taking office in 2018, he stated that Spain had been without a state housing policy for nearly ten years. He also charged that his predecessor in the PP had gambled instead on "an ideological, neoliberal policy that had disastrous social and economic consequences."

To build "thousands and thousands and thousands" of affordable social housing units for families and young people, Sánchez, whose coalition minority government has already introduced a law allowing authorities to cap "disproportionate" rent prices in some areas, announced the transfer of 3,300 homes and 2 million square metres of land to a newly established public company. In addition, he suggested tougher regulations and greater taxes for tourist apartments, as well as incentives for those who rent out vacant buildings at reasonable rates.

However, his proposal to impose a tax of up to 100% on real estate purchased by non-residents from non-EU nations, including the United Kingdom, was arguably his most striking move.

"Approximately in 2023 alone, non-EU citizens purchased approximately 27,000 homes and apartments in Spain. They didn't do it to live there or to provide a place for their families to dwell. They did that in order to conjecture,” Sánchez stated recently.

Some parts of the UK press were not happy with the proposal, which would need to be presented to parliament and may be challenged in court. One newspaper denounced the "brutal tax hike," while another referred to it as a "war on Brits' holiday homes."

The People's Party declared that it would not back the government's "xenophobic" policy in the areas it controls. The People's Party had made its own housing proposals

the day before Pedro Sánchez's address, primarily centred on tax savings.

Sánchez claimed that his government was considering prohibiting non-EU immigrants "from buying houses in our country, in cases where neither they nor their families reside here and they are just speculating with those homes," indicating that he was willing to go even further.

Over the last 12 months, the housing issue has become a top priority on the political agenda. Several large-scale protests throughout Spain in 2024 were sparked by worries about overtourism, which was primarily caused by its distorting impact on the property market.

EU buyers, and we're talking about a relatively small amount."

Providing tax benefits to individuals who rent out their apartments at reasonable prices is insufficient, according to Claudio Milano, a researcher in the University of Barcelona's Department of Social Anthropology and an authority on over-tourism, given that 3.8 million dwellings, or 14% of the country's total supply, are vacant in Spain.

Q2

Q3

Q4

Q2

Q3

Q1

Q2

Source: Statista

Marches calling for affordable housing have also taken place in Barcelona, Madrid, and other towns.

"I think that's what it is in many ways," said Ignasi Martí, director of the social innovation section at Esade Business School and head of its decent housing observatory, about the prime minister's usage of the term "housing emergency."

"People cannot access housing; the supply is lacking, and over the past few years, subpar housing conditions have become the norm," he added.

Did the solutions come late?

All of this has primarily impacted disadvantaged socioeconomic sections until recently, but now it's also impacting the middle class and working class, Martí remarked.

People in the middle class who realise they won't be able to afford an apartment and that renting is extremely difficult, as well as those who stay in Spain until they are roughly 31-years-old, are more likely to be impacted politically.

Although he admits that the 100% tax on non-resident, non-EU buyers was a show-stopper, Martí believes it might be more of an ideological ploy than a practical fix.

"It won't fix the issue," he declared, while adding, "You can't force that on

"They must take a much more aggressive approach to the issue and stop people from purchasing apartments for speculation," he stated, while noting, "That must end immediately so that we can discuss tax benefits. Before taking further action, we must extinguish the fire, which requires prohibiting speculation in apartments."

Pablo Simón, a political scientist at Carlos III University in Madrid, said, "The question now is whether the socialists and the PP could agree on how to best address the housing crisis at a time of profound polarisation and within the constraints of Spain's complex system of central, regional, and municipal government."

On the positive side, he claimed that both sides agreed on the underlying analysis, which is that Spain lacks adequate housing.

"As you would expect a party on the left and a party on the right to do, one party is betting a little more on state intervention and the other is betting a bit more on the market. However, the diagnosis is fairly similar," he added.

Spain's two largest cities have reacted coolly to Sánchez's ideas. The government is prioritising landlords over tenants and "betting on construction as a long-term panacea" instead of addressing the current crisis, according to the Tenants' Union of Madrid, which called them "insufficient, misguided, and cowardly."

Barcelona has experienced a similar reaction, with rising rents and property values driven largely by the rapid growth of Number of residential real estate transactions in Spain from first quarter 2021 to third quarter 2023

tourist apartments over the past 15 years.

The plans are ambiguous and "very generic," according to Jaume Artigues, a spokesman for the residents' group in Barcelona's most populated neighbourhood, the Eixample, where there is one tourist apartment for every 57 residents. Regardless of whether it was luxury apartments sold to investors or tourist apartments, he said, at least the government had acknowledged that speculation was the primary source of the housing problem.

"The need for affordable public housing has increased due to evictions, which is a result of the unaffordable housing that is currently available, rather than a rise in population. Speculation lies at the core of the problem, yet it perpetuates a vicious cycle," he stated.

Amidst public protests and local discontent, critics argue that current measures are insufficient and too generic, underscoring the urgent need for decisive action to curb speculation and prioritise the construction of affordable social housing.

The future of Spain’s urban landscapes and the well-being of its residents hinges on whether political leaders can bridge their ideological divides and implement effective reforms before the crisis deepens further.

Analysis

Over the last 12 months, the housing issue has become a top priority on the political agenda. Several largescale protests throughout Spain in 2024 were sparked by worries about overtourism, which was primarily caused by its distorting impact on the property market

GBO Correspondent

What was the similarity between Disney, OpenAI and Southwest Airlines? They all encountered boardroom tensions recently, thereby grabbing the headlines for all the wrong reasons. And a couple of them got murky. Take OpenAI for example. Its CEO Sam Altman, often projected as the poster boy of generative AI, got chucked out from his own company in November 2023, only to return, all within six days. In 2024, Southwest faced a major dispute as activist investor Elliott Investment Management

intensified its boardroom battle and called for a special shareholder meeting to change the airline's leadership.

The low-cost American carrier hit back by saying that its CEO Bob Jordan was the “right leader” to successfully execute the venture's strategy to improve financial performance and drive shareholder value. And in the battle of Elliott vs Jordan, it was the latter who had the last laugh.

Tensions between corporate boards and investors persist, and it’s something completely

Effective corporate governance hinges on clear communication, accountability, and strategic decision-making during board meetings

Source: Statista

normal. Disagreements (going by human nature) are bound to emerge, be it in our friend circle or during a corporate board meeting. In the second case, improved corporate governance practices help find an amicable solution.

According to a Harvard report, what unfolded in OpenAI and other corporate biggies, since 2023 now reflects a growing consensus that many of the "disagreements" stem from poor corporate governance. This trend is backed by another McKinsey study, which revealed that around 70% of recent activist investor demands have focused on governance reform.

Neil Shah, Director of Content and Strategy at Edison Group, said, "Addressing these governance issues, especially complex topics like executive pay, isn’t straightforward. However, adopting best practices can help rebuild trust between boards and investors."

Now the question here is: what are the fixes?

"One crucial step for companies is ensuring they fully understand and comply with industry regulations. Failures in this regard have led to significant scandals, such as the collapse of the cryptocurrency exchange FTX, where poor due diligence and asset handling were partly to blame. FTX’s CEO, Sam Bankman-Fried, later admitted ignorance of many regulations, highlighting the need for boards to ensure compliance at all levels," Neil Shah added. Instead of relying solely on legal departments to handle regulations, corporate boards need a comprehensive strategy that will cover regulatory monitoring, compliance programmes, regulatory engagement, and risk management. With new regulations like the European Commission's Corporate Sustainability Reporting Directive (CSRD) on the way, boards must prepare by understanding the requirements, developing data reporting systems, and adopting frameworks like the Topics addressed

Global Reporting Initiative. This will help big businesses avoid the pitfalls of ‘greenwashing’ or ‘greenhushing’ as they navigate sustainability efforts.

"Board accountability is vital in preventing scandals and ensuring proper governance. Recent years have revealed numerous examples of companies faltering due to a lack of clear roles and transparency. One notable example is the UK Post Office scandal, where the board repeatedly failed to address management issues. Similarly, the Federal Deposit Insurance Corporation (FDIC) faced allegations of employee mistreatment that went unaddressed by its board," Neil Shah added, while suggesting boards include experts in key areas like supply chains and Environmental, Social, and Governance (ESG) to improve accountability.

These professionals will clearly define roles and responsibilities for board members, ensuring the latter can effectively oversee management, regulatory compliance, and transparency.

Neil Shah also stated that improving communication with shareholders is another key reform area every big business should look after. The use of outdated communication methods, such as paperbased ballots, has caused friction between investors and corporate leadership.

"A lack of communication has led to misunderstandings, with investors accusing companies of secrecy. ExxonMobil shareholders, for example, criticised management in 2023 for not disclosing the financial impact of its net zero proposals. Digital investor relations should become standard practice, allowing more transparent and efficient communication. This would enable boards to share documents and proposals with shareholders, while also facilitating early feedback ahead of AGMs. This approach would reduce conflicts, especially as many proxy disputes are resolved before AGMs," Neil Shah said.

Another thing corporates can do is plan the meeting ahead of time and stick as closely to the planned topics as possible. While the meeting may provide opportunities to discuss other topics, it is essential to keep the focus on the main issue at hand to ensure that the event yields a productive outcome.

The host of the meeting or an appointed attendee can take the role of guiding the discussion agenda and keeping the participating stakeholders focused on the topic. This will save everyone's time and help drive productivity within the company, apart from promoting corporate transparency.

Apart from working on the regulation and communication fronts, businesses and their boards need to be on the same page on cyberattacks, which are becoming a regular threat. Data security, confidentiality, and system resilience should be the top focus areas in board meetings, given that any incident of data breach and subsequent blackmailing by threat actors (for ransoms) will only erode the stakeholder trust, apart from denting the affected company's brand value.

Another area where companies and their boards need to find amicable solutions is executive compensation.

In the words of Neil Shah, "While there is a strong business case for competitive executive pay, boards must be transparent and communicate the benefits of attracting top talent to investors. Benchmarking executive pay against competitors can help ensure compensation is appropriate, and clear communication can reassure shareholders that these decisions benefit the company long-term."

Another contention area is ESG policies. These policies will increasingly play a crucial role in corporate governance, particularly as regulations now require companies to promote sustainability, either through initiatives or operational activities. Boards should help the companies set ESG

targets, bring in experts, and ensure compliance. At the same time, it’s essential to communicate the impact of ESG measures to avoid shareholder dissatisfaction.

The boards should set diversity targets and appoint members to promote inclusivity throughout the company. Creating subcommittees dedicated to this goal can ensure that diverse voices contribute meaningfully to corporate decision-making.

"While issues like executive compensation and ESG will continue to spark debate, the broader challenges surrounding corporate governance are solvable. By adopting straightforward reforms, companies can significantly enhance their governance practices and meet the demands of today’s business environment," Neil Shah noted.

Effective corporate governance hinges on clear communication, accountability, and strategic decision-making during board meetings. By embracing transparency, sticking to rules and regulations, and encouraging collaboration, businesses can not only resolve boardroom tensions but also build trust with stakeholders and position themselves for long-term success.

Instead of relying solely on legal departments to handle regulations, corporate boards need a comprehensive strategy that will cover regulatory monitoring, compliance programmes, regulatory engagement, and risk management

Emirates Stallions Group, the leading conglomerate with operations spanning workforce solutions, real estate development, design and interiors manufacturing, agriculture, and landscaping, and a subsidiary of International Holding Company, recently announced the launch of Royal Development Holding, a visionary boutique real estate developer aiming to evolve spaces and elevate lives.

Royal Development Holding brings together several specialised real estate development companies, such as Royal Development Company (RDC) and Royal Architect Project Management (RAPM), and opens the door for the entry of new businesses that will enhance its capabilities and market presence.

Through the formation of Royal Development Holding, Emirates Stallions will be able to strengthen its position in the

real estate value chain while building on the trust, excellence, and innovation associated with the Royal Development Company for the past 15 years.

Emirates Stallions will now enhance its offerings to provide complete, end-to-end solutions that improve living experiences and support its long-term growth strategy by incorporating boutique real estate development capabilities.

Royal Development Holding brings together several specialised real estate development companies

AMEA Power has successfully commissioned a 500-megawatt wind power plant in Egypt's Ras Ghareb city, marking the largest operational wind farm on the African continent while reinforcing the country's role as a key player in Africa’s renewable energy

transition.

A joint venture between AMEA Power, which owns 60% of the project, and Sumitomo Corporation of Japan, which owns 40%, the Amunet Wind Power Plant is expected to generate about 2,500 gigawatt-hours of electricity per

year. This prevents 1.4 million tons of carbon dioxide emissions annually and is sufficient to power over 500,000 homes.

The commissioning follows AMEA Power's November 2024 opening of a 500 MW solar PV plant in Aswan. Within six months of completing both projects, the company has now brought one gigawatt of clean energy capacity online in Egypt.

The wind farm was built two and a half months ahead of schedule, included local training programmes for young people in the surrounding communities, and, at its peak, employed over 800 workers. AMEA Power's emphasis on long-term skill development, job creation, and socioeconomic development is reflected in the initiative.

Asharami Energy, an upstream company of the Sahara Group, will continue leading the charge to promote inclusive growth and the creation of local content throughout Nigeria's energy landscape by making investments, conducting business responsibly, and working with upstream value chain stakeholders.

Leste Aihevba, Chief Technical Officer of Asharami Energy, stated during the fifth Nigerian Oil and Gas Opportunity Fair (NOGOF) that, for the industry to effectively contribute to Nigeria's energy security, local participation and capacity building must be strengthened.

According to Aihevba,

the industry's current trends indicate a growing use of local knowledge, which he called essential for stability, innovation, smooth operations, and sustainable production to promote economic development in Nigeria. Asharami Energy has nearly 100% local content participation, barring a few sophisticated technologies. Services covering subsurface reviews and studies, field development plans, well interventions, drilling, civil works, and oil and gas infrastructure projects, such as flowlines, pipelines, flow stations, roads, and location constructions, are all provided by local companies.

In order to jointly promote decarbonisation throughout the UAE, global major Siemens Energy and Al Fanar Gas Group, one of the Gulf country's top suppliers of gas and energy solutions and the energy division of EHC Investment, have signed a strategic Memorandum of Understanding (MoU). Supporting the UAE Net Zero 2050 Strategy, the agreement was signed in Abu Dhabi during the World Utilities Congress 2025.

The two companies will collaborate to create clean energy solutions that incorporate cutting-edge digital technologies into industrial and energy infrastructure, with a focus on areas like flare gas management, hydrogen, and Power-to-X, as well as electrifying ports and vessels.

The partnership will also leverage Siemens Energy's global digitalisation experience to implement intelligent systems that optimise energy use, track emissions, and simplify operations, achieving a tangible and quantifiable acceleration of the energy transition.

Al Fanar Gas Group CEO Khaled Ben said, "This partnership is not just about technology; it's about responsibility. As a UAE company, we see it as our duty to help shape an energy future."

Jordan's Minister of Energy and Mineral Resources, Saleh Kharabsheh, recently assured members of the Energy Sector Partnership Council that the country's electrical system is safe and stable. This confirmation comes despite the suspension of natural gas supplies due to the ongoing regional escalation.

While discussing the rising geopolitical tensions that are creating more challenges for the region, Kharabsheh noted that Jordan has developed backup plans to ensure a continuous energy supply. He emphasised the crucial role that domestic energy resources play in maintaining the Kingdom's power industry.

According to the minister, Jordan imports approximately 100 million cubic feet of natural gas from Egypt each day. Due to the ongoing crisis, the government is

currently paying more to meet its energy demands.

The minister emphasised the importance of ensuring a continuous supply of electricity to all sectors. To achieve this, the ministry is closely monitoring regional developments and collaborating with all relevant parties. The minister and council members also reviewed the draft bylaws stemming from General Electricity Law No. 10 of 2025.

In May 2025, Etihad Airways, the national airline of the United Arab Emirates, carried 11.7 million passengers, a 19% increase over the same month the previous year.

The passenger load factor also increased to 87% from 84% in May 2024, demonstrating Etihad's capacity

optimisation skills while sustaining strong demand.

The aviation giant currently has 100 aircraft in operation, which supports its expanding network and service improvements. During the first five months of 2025, Etihad carried 8.4 million passengers, a

Jordan imports approximately 100 million cubic feet of natural gas from Egypt each day

17% increase over the same period in 2024. The airline also maintained an impressive average passenger load factor of 87%.

Etihad Airways CEO Antonoaldo Neves said, "With May's passenger numbers increasing by 19% yearover-year, we saw a pleasing continued growth in our momentum, underscoring our position as the fastest-growing Middle East airline. Our year-to-date results show more than eight million customers have flown with us in 2025, and our rolling 12-month figure now stands at almost 20 million, a testament to the trust placed in Etihad’s service. We reached an exciting milestone in May as our fleet number reached the 100 mark."

Etihad’s active fleet also reached 100 aircraft, supporting the airline’s growing global network.

GBO Correspondent Analysis

SME lending is changing as a result of the continuous digital revolution

The SME lending environment has changed significantly in recent years, as the introduction of advanced technologies and changing consumer needs have forced lenders to reconsider their risk management plans. One such transformation has been in the financial institutions' adoption of intelligent automation tools. Rich data sources are now enabling auto-decisioning engines, offering, in turn, a chance to improve operational resilience, save costs, and expedite the lending process.

Not only are these machine learning-based technologies improving the speed and precision of credit decision-making, but they are also ensuring that the criteria for making decisions remain clear and understandable, thereby avoiding potential selection biases.

Data analytics has emerged as the foundation of contemporary frameworks for risk management. By using extensive datasets, lenders are effectively spotting trends and abnormalities, which, in turn, is helping them proactively manage and reduce risk factors. Smart automation and advanced data analytics are now working together to usher in a new era of precise lending that is making it possible for smaller businesses to swiftly and effectively access financial resources.

The use of customer-centric strategies is becoming more and more important as lenders continue to benefit from technological developments. Developing customised goods and services that meet the particular requirements of SMEs is part of this strategy. At the same time, technology has the potential to improve the lender-client relationship by streamlining the credit approval process, reducing bureaucratic friction, and aligning them with a clear business vision.

Effective risk management requires the integration of governance and controls throughout the credit cycle. Lenders

can reduce risks and guarantee regulatory compliance by utilising machine learning methods with a focus on explainability and transparency. In order to protect against unforeseen consequences, such as biases in credit allocation, such measures are crucial.

Strong anti-money laundering (AML) regulations must be put in place in light of the growing concerns about money laundering activities. To prevent financial systems from being abused, the compliance infrastructure must include advanced transaction monitoring systems and improved identity verification tools.

SME lending is changing as a result of the continuous digital revolution. McKinsey noted that the banks and other financial institutions are utilising big data analytics and digital platforms to enhance their risk decision support systems. In addition to improving underwriting procedures' efficiency, this development also enhances portfolio monitoring procedures.

Geopolitical risks are now an indisputable fact for financial institutions that lend to SMEs in the quickly

shifting global landscape. Supervisors are stressing more and more how crucial it is for banks to be able to spot declines in asset quality and implement suitable provisioning procedures. To protect financial stability, this entails keeping a close eye on geopolitical developments and quickly adapting to new threats.

Through the use of early warning tools and systems, such proactive monitoring helps lenders stay ahead of possible financial distress. By evaluating both qualitative and financial metrics, these systems provide a safeguard against unanticipated economic downturns by identifying possible problems before they show up in the financial statements.

As fintech innovations gain traction, SMEs are increasingly looking to alternative financing sources. By facilitating faster access to capital, platforms that provide services such as invoice financing and short-term loans enhance cash flow management and lessen dependency on conventional banking techniques. These fintech platforms democratise financing by making it easier to obtain capital

Source: Statista

and encouraging innovation in the expansion of SMEs.

Fintech innovation has changed the game by lowering the entry barriers for small and medium-sized businesses seeking capital. Through quicker approval processes, less red tape, and increased transaction transparency, online alternative finance platforms are promoting a more inclusive financial ecosystem. This change highlights how traditional lenders must be flexible to maintain their competitive advantage.

To successfully capitalise on these new trends, financial institutions need to create thorough strategic plans that prioritise implementing digital innovations and customer-centric methodologies. For organisational goals to be aligned, this calls for crossfunctional cooperation between the IT, risk management, compliance, and business development teams.

The incorporation of adaptive technologies such as artificial intelligence and machine learning into fundamental operational frameworks is essential to this implementation. Through the integration of these tools into routine procedures, lenders can strengthen customer engagement metrics, advance predictive analytics, and make better data-driven decisions. A flexible and responsive risk management framework is made possible by these technological advancements, which are essential for navigating the changing SME lending market.

Effectively involving stakeholders is crucial as institutions shift to these developments. Regulatory bodies, fintech companies, SME clients, and internal employees are just a few of the important parties that lenders need to actively include in the transition process.

Addressing the issues and demands of every group will be made easier with open communication and teamwork, which will promote trust and alignment with strategic goals.

Additionally, to guarantee that internal teams have the skills needed to take advantage of new technologies and procedures, continuous education and training programmes should be created. The successful implementation of creative risk management techniques across the company can be fuelled by such programmes, which can enable employees to take on the role of change agents.

It is crucial to incorporate environmental, social, and governance (ESG) factors into risk management as financial institutions grow more aware of these issues.

ESG considerations affect consumer perceptions and reputational risk in addition to being crucial in determining the ethical standing and long-term viability of investments.

Lending practices that align with ESG standards allow financial institutions to build long-term value for their stakeholders and the general public. To guarantee that lending decisions promote innovation and sustainable business practices, this entails creating risk assessment frameworks that take ESG factors into account.

The drive for ESG compliance presents a chance for lenders to stand out from the competition. Sustainable business practices are becoming more and more valued by investors, partners, and customers.

Aside from drawing in clients who care about sustainability, incorporating ESG into the lending process can strengthen moral leadership in the financial industry and provide access to green finance markets.

Prioritising ESG compliance in initiatives can also help reduce the risks brought on by shifting societal expectations and regulatory changes. Financial institutions can take the lead in a seismic shift in global finance by embracing an innovative approach to ESG integration.

The path ahead offers both difficulties and unmatched opportunities as we stand on the precipice of revolutionary shifts in SME lending and risk management. By adopting customer-centric models, embracing digital innovation strategically, and adhering to ESG principles, financial institutions can rethink their roles in the global financial ecosystem. This proactive adaptation guarantees that these institutions continue to be at the forefront of sustainable growth and innovation while also boosting resilience and agility in an unpredictable economic environment.

Lenders can further their goals while also making a significant contribution to the growth of SMEs and the overall economy by adjusting their operational plans to meet the changing needs of the market.

Going forward, the long-term success and influence of financial institutions will be determined by their vision, flexibility, and moral leadership.

Meanwhile, the foundation of the global economy is made up of small and medium-sized businesses, which account for 90% of all businesses, employ roughly 70% of the workforce worldwide, and contribute 50% to GDP.

However, banks are not following up with solutions that cater to the needs of SMEs. In light of this, banks are taking advantage of the chance to reallocate expenses to ecosystem platforms and exponential technology investments. Some banks are strategically remaking their operations to better meet the needs of SMEs rather than just responding to passing trends.

The IBM study offers strategic perspectives on the present and future of fintech in SME banking. The IBM Institute for Business Value (IBM IBV) and the Banking Industry Architecture Network (BIAN) collaborated to conduct the study, which takes advantage of the knowledge of the SME Finance Forum, which is run by the International Finance Corporation (IFC).

Fintech innovation has changed the game by lowering the entry barriers for small and medium-sized businesses seeking capital. Through quicker approval processes, less red tape, and increased transaction transparency, online alternative finance platforms are promoting a more inclusive financial ecosystem

The EF market generated an estimated 20-30 billion euro in Europe in 2023, about 3% of total banking revenues

GBO Correspondent

The July 2020 report from EY revealed that COVID-19 impacted the financial sector, as the need for different strategies around innovation and digital banking became apparent. As technology develops, it also results in a rise in customer expectations of banking. What fintechs have done is cash in on the sentiment, by collaborating with tech giants and offering instant and personalised services. And the broader impact has been felt across the legacy banking sector, as the latter has understood the need to go digital to remain relevant.