Global Banking & Finance Review Issue 79 - Business & Finance Magazine

Chairman and CEO

Varun SASH

Editor

Wanda Rich email: wrich@gbafmag.com

Managing Director

Martin Murphy

Project Managers

Megan S | Raj G | Chethan G

Executive Operations and Client Relations Specialist

Anupama KU

Head of Operations

Robert M

Director of Operations

Babitha G

Business Consultants - Digital Sales

Paul N | Enosh S | Rohit D

Business Consultants - Nominations

Sara Mathew | Adam Luiz

Research Analysts

Varshitha | Devendra Patil | Shilpa Churiwala

Video Production & Journalist

Phil Fothergill

Graphic Designer

Shiva K

Advertising

Phone: +44 (0) 208 144 3511 marketing@gbafmag.com

GBAF Publications, LTD

Alpha House

100 Borough High Street London, SE1 1LB United Kingdom

Global Banking & Finance Review is the trading name of GBAF Publications LTD Company Registration Number: 7403411 VAT Number: GB 112 5966 21 ISSN 2396-717X.

The information contained in this publication has been obtained from sources the publishers believe to be correct. The publisher wishes to stress that the information contained herein may be subject to varying international, federal, state and/or local laws or regulations.

The purchaser or reader of this publication assumes all responsibility for the use of these materials and information. However, the publisher assumes no responsibility for errors, omissions, or contrary interpretations of the subject matter contained herein no legal liability can be accepted for any errors. No part of this publication may be reproduced without the prior consent of the publisher

editor

Dear Readers’

Welcome to Issue 79 of Global Banking & Finance Review.

The future of finance and business is being shaped by innovation, leadership, and a focus on the customer. In this issue, we explore how institutions around the world are embracing change to redefine how services are delivered, experiences are created, and leadership is enacted.

Featured on our front cover is Absa Digital. In Digital by Design: How Women Are Engineering Absa’s Tomorrow, we spotlight the women driving digital transformation across South Africa. From shaping products and technology to redefining governance and risk, these leaders are proving that diversity and inclusion are essential to building financial services that are accessible, innovative, and human-centered (Page 24).

OCBC Securities is charting its own path of innovation. In Expanding the Edge: OCBC Securities Accelerates Innovation under Wilson He, we explore how the firm is redefining the investor experience through a focus on customer engagement and integrated platforms. By putting clients at the center, OCBC Securities is creating agility, growth, and confidence in a complex market (Page 28).

Customer experience is increasingly the driving force behind efficiency and profitability. In Driving Efficiency and Profit Through Customer-Centric Banking, Pelwasha Faquiryan of Diebold Nixdorf outlines how banks can leverage operational improvements, personalization, and seamless service to strengthen loyalty, streamline processes, and unlock growth opportunities (Page 32).

Together, these stories reflect a broader theme: leadership, innovation, and customer focus are shaping the future of finance. At Global Banking & Finance Review, we remain committed to providing expert perspectives on the strategies and trends defining today’s institutions.

Enjoy the latest edition!

Wanda Rich Editor-in-Chief Global Banking & Finance Review

Featured on the front cover from left to right: Suella Derman, Head of Risk and Control, Absa Digital, Phiwokuhle Mlotshwa, Portfolio Lead, Absa Digital, Sivan Lapidus, Head of Design, Absa Digital, Anna Nascimento, Head of Digital Adoption, Absa Digital, Michelle Bisaro, Portfolio Lead, Absa Digital, Zeenat Hassim, Interim Chief Information Officer, Absa PPB

Wanda Rich Editor

Stay caught up on the latest news and trends taking place by signing up for our free email newsletter, reading us online at http://www.globalbankingandfinance.com/ and download our App for the latest digital magazine for free on Google Play and the Apple App Store

Driving Efficiency and Profit Through CustomerCentric Banking

Pelwasha Faquiryan, Head of Global Enterprise Accounts, Banking, Diebold Nixdorf

Banking at the Intersection: From Nashville to Cannes, A Strategic Call to Action

As the sun set over Nashville this September, Intersect 2025 closed not with a whisper but with a resounding call to action. More than 330 banking leaders, technologists, economists, and innovators gathered to explore the future of financial services. From rooftop conversations to mainstage revelations, one thing became clear: the future of banking is not just digital—it’s deeply human, profoundly strategic, and increasingly urgent.

Intersect Nashville 2025 wasn’t just another conference. It was a movement. A convergence of vision, execution, and partnership. And it’s only the beginning. As we look ahead to Intersect Cannes 2026, the stakes have never been higher. Transformation is no longer optional—it’s operational. And the time to act is now.

The Renaissance of Customer Experience

Steven Van Belleghem’s keynote on the “Customer Experience Renaissance” set the tone. In a world where AI can deliver hyperpersonalized service, the human touch becomes more—not less— important. Customers are no longer comparing banks to other banks; they’re comparing us to the best experiences they’ve ever had.

The challenge is not just digital transformation—it’s emotional connection. As Steven noted, “Connection will matter more than perfection.” Banks must move beyond efficiency to empathy, designing experiences that are intuitive, inclusive, and deeply personal.

Yet 90–95% of AI projects remain internally focused, aimed at productivity rather than customer value. This imbalance is a strategic risk. As consumers shift toward algorithmic buying and single-platform decision-making, banks must evolve from segmented marketing to hyper-personalized engagement. Loyalty will hinge on the 9s and 10s—not the zeros we eliminate.

At Intersect Cannes, we’ll take this conversation further. How do we build trust in a world of synthetic interactions? How do we ensure that personalization doesn’t become manipulation? These are the questions that will shape our next chapter.

Cash Matters: Choice, Resilience, and Inclusion

Cash is not dead. It’s evolving. The Payment Choice Coalition reminded us that cash remains vital for millions, especially the unbanked, underbanked, and digitally excluded. In fact, recent data shows cash usage is rising among Gen Z, driven by budgeting needs and privacy concerns.

Cash is more than a payment method—it’s a strategic asset. In times of crisis, from natural disasters to cyberattacks, cash is the fallback that keeps economies moving. The proposed Payment Choice Act, which mandates cash acceptance for transactions under $500, is not just policy—it’s a reflection of our values.

At Intersect Cannes, we’ll explore the future of the closed cash ecosystem. How do we optimize cash handling through automation? How do we balance innovation with inclusion? Expect deep dives into cassette-based recyclers, AI-driven forecasting, and branch interoperability.

Cash Automation: The Closed Ecosystem Advantage

The session on cash automation revealed a powerful opportunity: the closed cash ecosystem. By integrating teller cash recyclers (TCRs) and ATM cash recyclers, banks can reduce operating costs, improve customer experience, and streamline branch operations.

With up to 50% of branch expenses tied to cash handling, the ROI is compelling. Institutions like PNC, U.S. Bank, and Zions Bank are already seeing gains in efficiency, uptime, and customer satisfaction. The future is not just about recycling cash—it’s about recycling trust, speed, and strategic value.

AI and Automation: From Hype to Human Impact

AI was everywhere in Nashville—from fraud detection and customer onboarding to predictive analytics and conversational interfaces. But the real insight came from Dr. Jessica Kriegel’s keynote on change management. Her “Results Pyramid” reframed the conversation: results come from actions, actions come from beliefs, and beliefs come from experiences.

This is the missing link in most AI strategies. Technology alone doesn’t transform organizations—people do. And unless we align beliefs and behaviors, AI will remain a tactical tool, not a strategic lever.

At Intersect Cannes, we’ll move from pilots to platforms. How do we scale AI responsibly? How do we govern it across silos? And how do we ensure that automation augments—not replaces—the human workforce?

Operational Excellence: Lean, Local, and Learning

Frank Bauer, Diebold Nixdorf EVP of Operational Excellence, emphasized that what gets measured improves—but what gets understood transforms. From manufacturing in North Canton, Ohio, to field service optimization, operational excellence is not just about cost—it’s about capability. It’s about reducing repeat service calls, improving uptime, and delivering seamless experiences across channels. It’s about sourcing inregion for the region and building resilience into every layer of the supply chain.

At Intersect Cannes, we’ll showcase global best practices—from Latin America to Europe to Asia. How are banks localizing operations while scaling innovation? How are they training technicians, modernizing branches, and integrating cash and digital workflows?

Strategy in Action: Branch Automation Solutions

We officially launched our Branch Automation Solutions (BAS) portfolio—a new ecosystem designed to help banks and credit unions deliver

seamless, secure, and scalable experiences across their ATM and branch networks.

Powered by our cloud-native Vynamic® Transaction Middleware, BAS is turning ATMs into mini-branches, automating complex transactions, and freeing up staff to focus on revenue-generating activities. It’s built to be consumed as a service and designed to deliver:

• Availability and security

• Integrated cash management

• Branch and ATM automation

• End-to-end transaction processing

Customers like America First Credit Union are already seeing results: 2 million transactions a day, seamless integration, and a roadmap for future innovation. Their journey is proof that transformation is not only possible, but also profitable.

Leadership Transformation: Say-Do Culture and Strategic Clarity

Diebold Nixdorf President and CEO Octavio Marquez and his executive team led a powerful discussion on leadership. Their “say-do” culture— where promises are kept and feedback is acted upon—has become a model for the industry. However, leadership is not only about execution; it’s also about having a clear vision.

Jessica Kriegel’s “Surrender to Lead” framework challenged us to rethink control. True leadership is not about mandating change—it’s about creating experiences that shift beliefs. It’s about clarity, alignment, and accountability.

At Intersect Cannes, we’ll convene the next generation of banking leaders. How do we lead through uncertainty? How do we build cultures of innovation and inclusion? And how do we measure success beyond the balance sheet?

Why Cannes?

Cannes is not just a destination—it’s a declaration. It’s where strategy meets storytelling, where technology meets trust, and where leaders meet the future.

In April 2026, we’ll gather in Cannes to continue the journey we began in Nashville. We’ll bring together global perspectives, local insights, and actionable frameworks. We’ll showcase the best of what’s next—from AI to cash, from customer experience to operational excellence.

But most importantly, we’ll build a community of changemakers. Because the future of banking will not be built by algorithms alone. It will be built by people—people who believe in purpose, who lead with empathy, and who act with integrity.

Join Us on the Journey

Intersect Nashville 2025 was a celebration of progress—but it was also a call to action. To our customers, our partners, and our peers: the future of banking is being built now. And it’s being built together.

At Diebold Nixdorf, we’re not waiting for change. We’re leading it. Through innovation, collaboration, and a relentless focus on the customer, we’re helping banks transform with confidence.

If you’re ready to challenge convention, embrace bold ideas, and deliver exceptional experiences—join us at Intersect Cannes. Because transformation doesn’t happen in isolation. It happens at the intersection of vision and execution.

How Banks Can Win Back Customer Loyalty in the Digital Age

For decades, banking loyalty was almost automatic. Customers opened accounts, stayed for decades, and often passed the same institution down to their children. Today, that bond is fraying. Digital innovation has made switching banks effortless, while scandals, hidden fees, and rising fraud have weakened trust.

According to Forrester’s 2024 U.S. Customer Experience Index, customer experience scores for banks fell to a low not seen in ten years. This decline illustrates that even small lapses in service can have outsized effects on customer retention (Forrester). Every confusing fee statement or delayed response becomes a moment of friction that chips away at confidence.

Bain & Company’s 2023 Global Loyalty in Banking report shows that many customers are now unbundling their finances, keeping checking accounts at traditional banks while moving loans, savings, or investments to specialized providers. This trend highlights that convenience alone is no longer enough to secure loyalty. Trust and perceived value are critical drivers of retention.

The good news is that loyalty is not lost. It is being redefined. The banks winning customers back do so through reassurance, relevance, and respect. They protect customer funds, anticipate needs, and demonstrate fairness through action rather than slogans. In today’s digital landscape, trust is no longer assumed. It must be actively earned at every interaction.

What Customers Really Want in 2025

The modern banking customer is no longer drawn solely to flashy apps or large branch networks. They want institutions that make life simpler, safer, and more predictable. Technology alone is not enough; the experience must be seamless, intuitive, and trustworthy at every interaction.

Research by Accenture in 2025 shows that over half of banking customers would consider switching to another bank for a better digital experience or more personalised financial guidance . This statistic highlights that digital convenience is now the baseline expectation. Banks that do not deliver reliable digital services risk losing customers before trust can be established.

However, loyalty is not driven by technology alone. Accenture also found that fairness, transparency, and ethical behavior influence customer advocacy far more than product variety or marketing efforts. Customers want clear pricing, honest communication, and tangible evidence that their bank acts in their best interest. After years of economic uncertainty and inflationary pressure, trustworthiness has overtaken innovation as the most valued attribute in banking. Banks offering features without demonstrating integrity are at a disadvantage in retaining customer loyalty.

Younger generations, particularly Millennials and Generation Z, are accelerating this trend. While these customers value mobile convenience, they are equally motivated by ethics, inclusivity, and social responsibility. They reward institutions that actively demonstrate transparency and purpose, from environmental initiatives to equitable treatment of all customers. Banks

that fail to meet these expectations risk disengagement from the demographic that will constitute the largest portion of future banking revenue.

Emerging markets illustrate similar expectations. Digital payments systems such as India’s Unified Payments Interface and Kenya’s M-Pesa have redefined customer experience standards by providing fast, low-cost, and inclusive financial services. The World Economic Forum highlights that digital financial inclusion is critical to building trust and encouraging adoption in these markets. When banks simplify access and make services more transparent, customers develop confidence that their bank is reliable, secure, and aligned with their needs.

For banks around the world, the lesson is clear. Respect the customer’s time, simplify complex processes, and provide reliable, transparent services. Each interaction is an opportunity to build confidence or create friction, and banks that consistently deliver on these fronts will strengthen loyalty even in a highly competitive, digital-first marketplace.

The Trust Deficit: How Fraud and Complexity Drive Churn

Trust is the emotional currency of banking. When it is depleted, no rewards program or flashy feature can fully compensate. Every interaction that leaves a customer feeling uncertain—whether it is a poorly explained fee, a confusing statement, or a security incident—chips away at loyalty.

Consumer fraud continues to be a major driver of trust erosion. The United States Federal Trade Commission reported that consumers lost 12.5 billion dollars to fraud in 2024 . Each of these incidents represents a customer who felt unprotected, anxious, and increasingly likely to reconsider their banking relationship. Research by Bain & Company indicates that nearly two-thirds of customers who experience fraud consider switching to another bank, underscoring how central trust is to retention.

Complexity amplifies the problem. Hidden costs, opaque fee structures, and unclear terms frustrate customers and quietly drive them away. J.D. Power’s 2024 U.S. Retail Banking Satisfaction Study found that institutions with simple, transparent fees consistently scored higher in customer loyalty. Complexity may appear profitable in the short term, but it undermines long-term relationships. Each confusing fee or convoluted policy signals to the customer that the bank prioritizes revenue over their experience.

Fraud is not limited to bank systems; it often begins outside the institution, through phone calls, emails, or text messages designed to deceive the customer. Collaborative initiatives, such as the GSMA-backed Scam Signal project, enable banks and telecom providers to share real-time data, intercept suspicious communications, and prevent scams before they reach the customer. Such coordinated efforts demonstrate that proactive protection is not just risk management—it is a competitive advantage that builds confidence and loyalty.

Ultimately, loyalty erodes one interaction at a time. Each fraudulent email, unclear charge, or delayed resolution silently communicates to customers that they are on their own. Banks that consistently deliver clarity, security, and responsiveness can restore trust, but those that fail risk losing customers to competitors who demonstrate reliability and care.

Reassurance: The First Step Back to Trust

Rebuilding loyalty begins with reassurance. This involves demonstrating consistently that customer well-being is the bank’s first priority. Reassurance is no longer a compliance obligation; it is a competitive differentiator. Customers who feel safe and understood are more likely to remain loyal, even in highly competitive markets.

Digital threats have grown faster than many institutions’ defenses. Experian’s 2024 Global Fraud Trends Report predicts that online-payment fraud could cost businesses $362 billion worldwide by 2028 . This is not merely a statistic—it reflects the stakes for institutions that fail to safeguard customer funds. Fraud prevention must be treated as a core customer experience initiative, not just a back-office process.

Some banks are turning security into a visible brand promise. Singapore’s DBS Bank, for instance, invested in real-time fraud-detection systems and customer education, significantly reducing phishing incidents and winning public praise for transparency. When protection becomes part of the customer-facing identity, it strengthens loyalty in a way that traditional marketing cannot.

Transparency extends beyond technology. When Ally Bank and Capital One eliminated overdraft fees in 2023, customer satisfaction and trust increased measurably. Customers interpreted these changes as ethical choices rather than promotional tactics, signaling that the bank prioritizes fairness over profit.

Reassurance also requires attention to vulnerable groups. Older adults remain a prime target for scams, and the FBI reports that Americans aged 60 and older lose more to fraud than any other age group. Leading institutions now implement safeguards such as extra confirmation steps, automated alerts, or callback procedures for unusual transactions. These proactive measures demonstrate that the bank is actively looking out for its customers, restoring confidence across generations.

Reassurance can also be strengthened through collaboration. Fraud often begins outside the banking system, via phone calls, texts, or social media. The GSMA-backed Scam Signal initiative allows banks and telecoms to share real-time data and block scams before they reach customers. This type of ecosystem-level defense not only reduces risk but also signals to customers that the institution is proactive, connected, and trustworthy.

Ultimately, reassurance is about making customers feel secure through visible action. Banks that embed protective measures, communicate clearly, and collaborate externally build trust one interaction at a time. Those that fail to do so leave customers anxious, disengaged, and primed to explore alternatives.

Personalization That Feels Human

For years, banks have treated personalization as a data-driven checkbox rather than a core relationship-building tool. In reality, personalization defines the modern customer-bank relationship. True personalization requires empathy, timing, and understanding—it is about anticipating a customer’s needs and responding in ways that feel genuinely helpful rather than promotional.

Research by McKinsey shows that effective personalization can increase revenue by up to fifteen percent while reducing churn by around twenty percent. These figures are more than financial—they quantify the trust and engagement that personalized interactions can generate. A timely alert about an upcoming overdraft, a recommendation to adjust savings in response to expected bills, or proactive guidance on managing a loan demonstrates attentiveness and reassures customers that their bank understands their circumstances.

BANKING

The Commonwealth Bank of Australia provides a leading example. Its AI-driven Customer Engagement Engine analyzes millions of daily interactions to deliver tailored advice and alerts. Rather than pushing products, it offers guidance at helpful moments, such as alerting a customer before a large debit or congratulating them for consistent saving. Customers describe these prompts as supportive and personalized rather than sales-driven, illustrating that technology can enhance the human touch when applied thoughtfully.

Personalization must also respect privacy and remain transparent. The European Union’s AI Act requires institutions to explain algorithmic decisions and protect individuals from bias.. Banks that can clearly communicate how and why recommendations are made foster confidence far more effectively than those that rely on opaque systems. In other words, responsible use of data—not sheer volume—is what builds long-term loyalty.

Generational expectations amplify the importance of humanized personalization. Younger consumers are digitally fluent, yet they are acutely sensitive to intrusive or irrelevant communications. They reward institutions that provide value through actionable insights, timely alerts, and meaningful engagement, rather than generic marketing messages. By contrast, misaligned personalization can alienate this demographic, turning technology into a source of frustration instead of trust.

In addition, personalization can strengthen cross-channel engagement. Customers increasingly interact with their banks across mobile apps, web platforms, and physical branches. Coordinated, context-aware personalization ensures that whether a customer is receiving a mobile notification or speaking to an advisor, the experience feels seamless and attentive. Each thoughtful touchpoint reinforces the perception that the bank is listening, understands, and cares.

Ultimately, personalization is not about selling more products. It is about creating moments of recognition, reducing friction, and proactively supporting the customer’s financial goals. Banks that master humanized personalization transform routine interactions into trust-building opportunities, fostering loyalty that no loyalty program alone can achieve.

Balancing Automation and Empathy

Digital transformation has made banking faster, more convenient, and accessible across the globe. Yet this convenience often comes at a cost: the human warmth that traditionally built trust in customer relationships. Customers want technology that saves time but still allows them to feel seen, understood, and supported. The challenge for banks is to balance automation with empathy, ensuring that technology enhances rather than replaces human connection.

Accenture’s global consumer banking research shows that approximately two-thirds of customers prefer digital channels for routine transactions, such as transfers or bill payments, yet they still expect immediate access to a human representative when a problem arises. This insight underscores a critical truth: efficiency alone does not drive loyalty. Customers feel secure when they know a real person is available to intervene when issues arise.

Several banks have successfully designed digital systems that embed empathy into automation. NatWest in the United Kingdom introduced a Click to Call feature, allowing customers who notice suspicious activity to connect instantly with a fraud prevention specialist rather than navigate automated menus. The system communicates urgency, care, and attentiveness— qualities that directly reinforce trust. Similarly, Equity Bank in Kenya leverages secure video branches to connect remote customers with professional advisors. This approach preserves the personal connection of face-to-face advice while keeping operational costs manageable.

These examples illustrate a broader principle: technology itself is not the value; the experience it creates is. A well-designed chatbot can handle routine queries efficiently, but it only strengthens trust when a human can intervene promptly for complex or emotional issues. Banks that track metrics such as “time to human contact” alongside “time to resolution” are far more likely to retain customers than those that focus solely on operational efficiency.

The balance of automation and empathy also plays a crucial role in reinforcing brand values. When digital systems consistently reflect care, attentiveness, and responsiveness, they signal that the bank prioritizes the customer’s experience over pure transactional efficiency. Over time, this consistent messaging builds confidence and loyalty in a way that marketing campaigns alone cannot.

For institutions seeking to win back loyalty in the digital age, automation and empathy are not opposing forces. Instead, they are complementary tools: technology delivers speed and scale, while empathetic design ensures that every interaction reinforces trust and understanding. Banks that successfully integrate both will differentiate themselves in a marketplace where products are largely commoditized, and relationships are the true competitive advantage.

Rewarding Loyalty with Purpose, Not Perks

Traditional loyalty programs, based on points, cashback, or tiered rewards, are losing their appeal. Today’s customers, especially younger generations, are guided not just by value but by values. They seek banks that demonstrate social responsibility, environmental stewardship, and alignment with personal principles. When a bank’s incentives reflect shared purpose, it strengthens both trust and long-term loyalty.

Accenture’s 2025 Global Banking Consumer Study found that advocacy and retention increase sharply when customers believe their bank contributes positively to society. This demonstrates that loyalty is not solely transactional; it is emotional and value-driven. Customers reward institutions that integrate ethical behavior and purposeful action into their business model.

Practical examples illustrate this trend. Santander’s Eco Saver program in Spain links financial incentives to environmental responsibility. Customers who fund energy-efficiency projects or purchase electric vehicles benefit from higher interest rates. This approach ties personal financial reward directly to meaningful social impact, fostering a sense of partnership between the customer and the bank.

Similarly, Bank of America’s Preferred Rewards program combines financial education, personalized guidance, and incentives, resulting in retention rates roughly 25 percent higher among participants. Rather than merely offering discounts or points, the program encourages customers to engage in financially responsible behavior, making loyalty feel mutually beneficial rather than promotional.

Edelman’s 2024 Trust Barometer reinforces this shift. Sixty-one percent of consumers expect banks to act visibly on sustainability and inclusion. This statistic highlights a cultural expectation that banks cannot ignore: purpose is becoming a critical measure of premium service. Customers increasingly favor institutions that address societal challenges through transparent, actionable initiatives.

Purpose-driven loyalty programs do more than reward behavior; they signal the institution’s commitment to shared values. Initiatives like green mortgages, inclusive lending practices, community development loans, or carbon impact reporting demonstrate that a bank prioritizes positive impact alongside financial performance. These programs foster emotional attachment, strengthen brand identity, and cultivate advocacy, ensuring that customers remain engaged even in competitive digital environments.

Ultimately, loyalty is no longer measured solely by transactions or points accumulation. It is about creating a sense of alignment and partnership. Banks that embed purpose into their loyalty strategy strengthen their relationships with customers while contributing to broader social and environmental goals. In a world where trust is fragile, shared purpose becomes a unique differentiator that points to the next era of relationship banking.

The Operating Model Behind Trust

Loyalty cannot thrive if a bank’s internal structures reward short-term gains over long-term relationships. True customer focus requires alignment between governance, incentives, and measurement systems, ensuring that employees and leaders are held accountable for ethical performance as much as for profitability.

McKinsey’s 2025 Global Banking Review found that banks linking executive compensation to outcomes such as customer retention, complaint resolution, and fraud recovery outperform peers in both reputation and growth. This demonstrates that when leadership is incentivized to prioritize customer-centric outcomes, the organization naturally follows suit. Culture and strategy are intertwined: ethical behaviors reinforced at the top cascade throughout the institution, shaping how employees engage with clients every day.

Some banks have taken additional steps to formalize accountability. Cross-functional Loyalty Councils, for instance, convene quarterly to review customer experience data, identify friction points, and implement corrective actions. These councils bridge traditional silos, ensuring that front-line insights inform executive decisions and strategic priorities. By embedding loyalty into governance structures, institutions can respond more quickly to emerging customer concerns and maintain consistency in service quality.

Transparency is another critical component. Monzo Bank in the United Kingdom publishes detailed reports on service reliability, security incidents, and remedial actions. Rather than exposing vulnerabilities, this openness signals confidence in the institution’s ability to improve and fosters public trust. Customers and regulators alike interpret such transparency as evidence of integrity, not weakness.

When organizations measure and reward ethical behavior alongside financial performance, a culture of trust emerges. Employees internalize the importance of acting in the customer’s best interest, and leadership communication reinforces that loyalty and profitability are not mutually exclusive but mutually reinforcing. This alignment transforms trust from a marketing message into a core operating principle, guiding decision-making, risk management, and daily interactions with clients.

Ultimately, a robust operating model creates the structural foundation for all loyalty initiatives. Without governance, incentives, and transparency aligned to customer-centric outcomes, even the most innovative personalization, security, or purpose-driven programs cannot achieve lasting impact. Banks that invest in building this foundation ensure that every strategic decision and operational action consistently strengthens trust, creating loyalty that endures across economic cycles and digital disruption.

Measuring the Long Game

Many banks still treat loyalty as an intangible concept rather than a quantifiable business asset. Yet in today’s competitive environment, loyalty can and should be measured, managed, and optimized like any other key performance indicator. By tracking retention revenue, churn costs, and the return on trust-focused initiatives, institutions can turn goodwill into measurable impact.

The concept of a “Loyalty Profit and Loss” account is gaining traction. This model evaluates the financial effects of loyalty initiatives, from fraud prevention to customer education programs. For example, preventing a single fraudulent transaction can preserve thousands of dollars in lifetime customer value, offsetting the cost of proactive security measures. By quantifying loyalty in this way, executives gain a clear business case for investments in experience, security, and personalization.

Public reporting further reinforces trust. Banks that disclose service reliability statistics, complaint resolution times, and security incident data signal accountability and maturity. Such transparency demonstrates that loyalty initiatives are not merely cosmetic but are tied to measurable performance

outcomes. Customers and regulators alike interpret these disclosures as evidence of reliability, consistency, and commitment to continuous improvement.

Metrics can also provide actionable insights for targeted interventions. By analyzing which segments are most sensitive to service issues, fraud, or complex pricing, banks can prioritize initiatives with the highest potential to improve retention. For example, monitoring churn patterns among digital-native customers may highlight opportunities to enhance mobile app experiences or simplify digital onboarding processes. Similarly, tracking the impact of educational programs or sustainabilitylinked rewards can reveal which purpose-driven initiatives most strongly drive advocacy and long-term engagement.

Measuring loyalty in financial terms also shifts internal perspectives. When employees and executives can see a direct connection between trust-building actions and revenue outcomes, loyalty becomes an operational priority rather than a soft, abstract goal. Incentives tied to measurable retention, customer satisfaction, or fraud mitigation encourage a culture where every interaction contributes to sustainable loyalty.

In essence, measuring the long game transforms loyalty from a concept into a strategic asset. It allows banks to track progress, demonstrate ROI, and continuously refine programs to strengthen relationships. Institutions that embrace this approach ensure that loyalty is not fleeting or reactive but a durable, quantifiable component of business strategy.

A Practical Path Forward

Rebuilding customer loyalty does not require sweeping transformation programs or revolutionary technology. The journey begins with visible, tangible actions that demonstrate intent and earn trust. Banks can prioritize three interrelated steps: reassurance, responsible personalization, and purposeful rewards.

Reassurance through clarity and protection is the first step. Customers must feel that their bank actively safeguards their finances. This involves transparent communication about security features, simplified fee structures, and visible protections against fraud. Clearly explaining overdraft policies or proactively notifying clients about suspicious transactions signals that the bank prioritizes their wellbeing, turning abstract promises into measurable confidence-building actions.

Responsible personalization is the second critical element. Banks should leverage data to serve the customer, not simply to sell. Proactive alerts about savings opportunities, reminders to prevent overdrafts, or tailored financial guidance show attentiveness and empathy. Personalization becomes meaningful only when it is contextual, transparent, and respectful of privacy boundaries. Explaining how recommendations are generated ensures that trust is reinforced rather than undermined by opaque technology.

Purpose-driven rewards form the third pillar. Traditional points or cashback programs are increasingly insufficient to inspire loyalty. Customers now value initiatives that align with their personal and societal values, such as sustainability-linked savings programs, inclusive lending, or community development incentives. By tying rewards to behaviors that benefit both the customer and society, banks foster loyalty that is emotional, ethical, and lasting.

Each of these steps communicates a broader message: the institution is acting in the customer’s best interest. A bank that simplifies fees, prevents scams, or celebrates responsible financial behavior demonstrates integrity and builds confidence without relying on slogans or marketing campaigns. These small, consistent actions accumulate, reinforcing loyalty over time.

Moreover, these initiatives are mutually reinforcing. Clear protections reassure customers and reduce attrition, personalization demonstrates attentiveness, and purposeful rewards create emotional alignment. When combined, they establish a virtuous cycle of trust that strengthens relationships, improves retention, and ultimately translates into measurable business value.

Importantly, this approach is scalable. Whether through digital channels, mobile apps, or branch interactions, the principles of reassurance, personalization, and purpose apply universally. By embedding these elements into daily operations and aligning incentives with customer-centric outcomes, banks can institutionalize trust, making it a core part of the operating model rather than a series of isolated initiatives.

In practice, banks that adopt this path move from transactional engagement to relationship banking, where every interaction, whether a mobile alert, a branch visit, or a financial consultation, reinforces confidence, demonstrates competence, and reflects ethical behavior. Over time, these cumulative experiences reshape customer perceptions, restore loyalty, and differentiate the institution in a competitive digital landscape.

The Return of Relationship Banking

Open banking and digital competition have leveled the field in terms of products, speed, and convenience. Every bank can now offer a mobile app, instant transfers, and broad access. What cannot be automated is trust. Each interaction, whether through a mobile notification, call center, or branch visit, either strengthens or weakens that trust.

Banks that succeed in the coming decade will treat loyalty as a shared relationship rather than a performance metric. Trust becomes the core differentiator, and all customer touchpoints are opportunities to reinforce it. Security is no longer a back-office function but a promise. Personalization is no longer a marketing tactic but a service. Empathy is not optional but the infrastructure that sustains relationships.

Accenture’s Tom Meyer summarized this principle in 2025: “Technology makes banking faster; trust makes it lasting”. This insight highlights the enduring value of human-centric banking, even in a digital-first world. Customers respond to actions that demonstrate reliability, care, and ethical behavior. Technology amplifies these behaviors, but it cannot replace the fundamental need for trust.

Leading banks are embedding trust into their operating model. Real-time fraud prevention, personalized financial guidance, and purpose-driven loyalty programs are combined with transparent communication and governance structures that reward ethical outcomes. Each initiative reinforces the message that the bank is a reliable partner in customers’ financial journeys.

Relationship banking is also about anticipating needs and offering timely interventions. Proactive alerts about potential overdrafts, personalized savings recommendations, or notifications about investment opportunities demonstrate attentiveness. Customers perceive these interventions not as marketing, but as guidance, creating a deeper emotional connection. Over time, these small, context-aware actions build cumulative trust that is difficult for competitors to replicate.

In emerging markets, this principle is particularly evident. Systems like India’s Unified Payments Interface and Kenya’s M-Pesa have shown that speed, accessibility, and trust combine to create strong customer loyalty, even in highly digital ecosystems. The lesson for global banks is clear: technology must serve humans, not replace them. Simplifying experiences, safeguarding funds, and demonstrating integrity are the pillars of lasting customer relationships.

Ultimately, relationship banking is the next frontier in loyalty. Technology will continue to make banking faster, but trust, empathy, and purpose make it meaningful. Banks that invest in reassurance, transparency, personalization, and ethical practices will not only retain customers but also convert them into advocates. Loyalty will once again become the most valuable currency of all, grounded in action, integrity, and shared purpose.

The Corporate Power Shift: How Decentralized Decision-Making Is Redefining Modern Business Leadership

The corporate world is undergoing a structural power shift. For decades, leadership meant sitting at the top of a pyramid, issuing directives that cascaded down through layers of management. Today, value creation is increasingly happening at the edges of the organization—inside small, autonomous teams with direct access to data, customers, and AI tools.

From Spotify’s “squads” and Amazon’s “two-pizza teams” to Haier’s radical micro-enterprise ecosystem, leading companies are redistributing decision rights away from headquarters and closer to where work actually happens. This transformation promises speed and innovation, but it also forces leaders to rethink risk, governance, and accountability in an environment where control can no longer be equated with centralization.

From Command-and-Control to Distributed Power

Traditional corporate hierarchies were built for a world where information was scarce, markets moved slowly, and coordination required layers of managers. Decisions were centralized because the people at the top had the broadest view of the business and the best access to data and expertise.

That logic is eroding. Digital technologies now make information widely accessible, and the pace of change in most industries punishes slow, committee-based decision-making. Research on decentralized decision-making notes that pushing decisions closer

to the affected areas typically produces faster, more flexible responses and often greater innovation, because local leaders have richer, more immediate information than distant executives.

Harvard Business Review highlights a growing trend: organizations are “pushing decision-making down and out” toward the front lines to become faster and nimbler. The caveat is that not all decisions should be decentralized—leaders must be deliberate about which choices remain centralized and which can safely move outward.

The emerging view is that corporate power structures work best when they are neither fully centralized nor fully flat. The goal is a calibrated balance where strategic direction, major capital allocation, and enterprise-wide risk remain tightly governed, while everyday product, customer, and operational decisions are made by the teams closest to the work.

Flat Hierarchies and Autonomous Teams

As organizations search for that balance, many are deliberately flattening structures and organizing around small, autonomous units.

The Scaled Agile Framework synthesizes lessons from innovative companies and argues that the most adaptive organizations push decisions “as far down in the organization as possible,” allowing people at all levels to move quickly, exercise creativity, and assume responsibility for outcomes.

In practice, this has led to a shift away from monolithic departments toward cross-functional teams that own a product, service, or customer journey end-to-end. Instead of simply executing centrally crafted plans, these teams are responsible for defining problems, testing solutions, and making day-to-day tradeoffs. Their power comes not from titles but from clearly defined mandates and visibility into the data that matters.

This evolution is also closely linked to talent expectations. As digital-native professionals enter the workforce, they increasingly expect autonomy, growth, and meaningful participation in decisions. In banking, for instance, Global Banking & Finance Review describes how institutions are rethinking work design and career paths to attract digital-native skills, emphasizing innovation, flexibility, and project-based work.

The shift toward flatter, more empowered organizations is therefore not only structural, but also a response to how the next generation of employees wants to work.

Spotify: Autonomy with Alignment

Spotify has become an emblematic case of decentralized organizational design. Instead of a traditional product hierarchy, it organizes around a network of small, cross-functional units called squads, grouped into tribes and supported by chapters and guilds.

The Spotify model is described as a people-driven, autonomous approach to scaling agile, focused on culture and networks rather than rigid structures. It aims to increase innovation and productivity by emphasizing autonomy, communication, accountability, and quality.

Within this design, squads behave like mini start-ups. Each squad owns a specific part of the product, has the skills to design and ship changes, and is trusted to choose its own ways of working. External analyses of the model emphasize that success depends on maintaining both autonomy and alignment: squads need the freedom to act quickly, but they also need shared roadmaps, common cultural norms, and clear strategic direction to avoid fragmentation.

Spotify’s experience demonstrates that decentralization cannot be reduced to simply “removing hierarchy.” It requires a thoughtful architecture of roles, rituals, and information flows that allow small teams to move quickly while still pulling in the same strategic direction.

Amazon: Two-Pizza Teams and Single-Threaded Leaders

Amazon’s approach to decentralization is grounded in small, autonomous “two-pizza teams”—teams small enough that two pizzas can feed everyone in the room. The principle is simple: smaller teams coordinate more easily, move faster, and feel a stronger sense of ownership.

Amazon describes these teams as owning a product or service end-to-end, with responsibility for both building and running what they create. This design is reinforced by “single-threaded leaders,” who are dedicated to one major initiative instead of juggling multiple priorities.

Independent analyses of the two-pizza model highlight how this structure pushes decision authority closer to customers and reduces the need for slow, multi-layer approvals. But they also note that, as Amazon scaled, the company had to strengthen coordination mechanisms and clarify leadership roles when some small teams struggled with dependencies and strategic alignment.

Amazon’s story underscores a recurring theme: decentralization works best when autonomy is matched by clear ownership, strong metrics, and disciplined mechanisms for cross-team coordination.

Haier: Micro-Enterprises and the Rendanheyi Model

Haier, the Chinese appliance manufacturer, offers perhaps the most radical example of decentralized corporate power. Under the leadership of Zhang Ruimin, Haier dismantled its traditional hierarchy and adopted the Rendanheyi model, transforming into a platform of thousands of micro-enterprises that function like independent start-ups.

Academic work on Rendanheyi describes it as a management model that integrates employees (“Ren”) and users (“Dan”) so that value creation is directly tied to customer needs. Haier’s organizational structure shifted from a conventional manufacturing firm to an online, entrepreneurial ecosystem where micro-enterprises own their strategy, P&L, and customer relationships.

A detailed analysis in California Management Review shows how Rendanheyi allowed Haier to respond rapidly to changing markets by turning employees into entrepreneurs and the company into a platform for internal and external ventures.

Recent practitioner accounts reinforce this picture, describing how Haier now operates as a network of micro-enterprises with considerable decision authority and direct accountability

for outcomes, supported by shared platforms rather than managed through traditional chains of command.

Haier shows how far decentralization can go when a company is willing to rethink not just its hierarchy, but also its basic assumptions about employment, ownership, and strategy.

AI, Data Transparency, and the Infrastructure of Autonomy

The rise of decentralized decision-making is inseparable from advances in data and AI. Small teams can only make good autonomous decisions if they have access to timely, reliable information and tools that help them interpret it.

McKinsey’s research on the “organization of the future” argues that leading companies are embedding generative AI into the heart of their operating models, using it to augment human decision-making at every level. The report emphasizes that gen AI can empower people—but only if leaders intentionally redesign roles, workflows, and structures around it.

A complementary McKinsey report on AI in the workplace frames AI as a “super-agent” that can amplify human agency by automating routine tasks, surfacing insights, and enabling new forms of collaboration and creativity.

In decentralized organizations, this means AI and analytics increasingly serve as the glue that holds distributed decision-making together. When teams

across the business have access to shared dashboards, predictive models, and experimentation tools, they can align on reality even when they are making decisions independently.

Deloitte’s 2024 Global Human Capital Trends report notes that as work becomes more boundaryless and team-based, organizations are under pressure to develop new ways to measure performance beyond simple productivity counts—putting greater emphasis on innovation, learning, and human impact.

Together, these insights suggest that AI and data transparency are not just technical upgrades. They are the infrastructure that makes distributed power feasible and governable at scale.

Risk, Governance, and the New Accountability Equation

The central tension in decentralized decision-making is the trade-off between agility and control. More autonomy can lead to faster decisions and richer innovation, but it can also introduce fragmentation, inconsistent standards, and new risk exposures.

Harvard Business Review stresses that the decision to decentralize should be based on the nature of the decisions themselves: where information is local, uncertainty is high, and speed matters, decentralization often makes sense; where stakes are high, risks are systemic, or coordination is crucial, centralization may still be necessary.

The World Economic Forum, examining decentralized operations in a post-pandemic world, argues for models that are “decentralized but not fragmented.” Effective organizations, it suggests, use governance to strike a balance between local autonomy and global coherence, ensuring that decision rights are clear and that critical standards—such as safety, ethics, and cyber security—are centrally defined and enforced.

In practice, this is leading to new governance patterns. Central teams increasingly act as platform and policy owners rather than gatekeepers for every operational choice. Guardrails—such as risk limits, AI ethics principles, and regulatory policies—define what is off-limits, while dashboards and monitoring systems track outcomes rather than micromanaging inputs. Accountability shifts from “did you follow the process?” to “did your decisions create value and stay within agreed boundaries?”

Culture, Talent, and Engagement in Decentralized Organizations

Decentralization is not purely a structural change; it is also a cultural and talent transformation. When decisions move to the edges, employees must be prepared to handle greater responsibility, ambiguity, and visibility.

Deloitte’s 2024 Global Human Capital Trends emphasizes that organizations are moving toward a “boundaryless” model of work, where teams form and reform across functions, geographies, and even organizational borders. In that world, human performance—the interplay of business outcomes and human outcomes—becomes the core lens for designing roles, structures, and leadership.

The report argues that thriving in this environment requires rethinking how people are developed, measured, and supported, with a stronger focus on learning, collaboration, and adaptability.

Sector-specific evidence points in the same direction. In banking, the “talent crunch” for digital and technology skills is forcing institutions to design work in ways that appeal to digital natives, who value autonomy, growth, and meaningful impact over traditional hierarchies and rigid career ladders.

When organizations get decentralization right, employees often report higher engagement and a stronger sense of ownership. They can see the direct impact of their decisions, move between projects and teams more fluidly, and shape their own growth paths. When it is done poorly, however, decentralization can feel like abandonment: responsibilities increase, but support, clarity, and recognition do not.

Successes, Failures, and Lessons Learned

The experiences of Spotify, Amazon, and Haier show that decentralized decision-making can unlock significant gains in innovation and adaptability. But they also show that decentralization is not a one-time fix; it is a continuous design challenge.

Spotify has had to keep evolving its model as it grows, fine-tuning the balance between squad autonomy and cross-tribe alignment. https://www.atlassian.com/agile/agile-agile-at-scale/spotify

Amazon discovered that small teams alone were not enough; they required strong leadership, clear metrics, and mechanisms to manage interdependencies among services.

Haier’s journey shows that radical decentralization requires an equally radical reinvention of culture, incentives, and leadership roles, as well as robust platform capabilities to avoid descending into chaos.

Across these stories, a consistent lesson emerges: decentralization magnifies what already exists. In organizations with strong purpose, healthy culture, and solid data infrastructure, distributed decision-making can be a powerful accelerant of innovation and engagement. In organizations with weak alignment or low trust, it can amplify confusion and conflict.

The Future of Organizational Structure in an AI-Driven Economy

Looking ahead, the corporate power shift is likely to deepen as AI becomes woven into every aspect of work. But the destination is not a world without hierarchy; it is a world of more fluid, hybrid structures.

McKinsey’s view of the organization of the future suggests that leaders will increasingly rely on generative AI not just for analysis, but for designing and operating new organizational models—using AI to simulate scenarios, allocate resources dynamically, and support continuous adaptation.

Deloitte anticipates that organizations will become more boundaryless, with people moving seamlessly across internal and external ecosystems, and with HR, technology, and business leaders jointly shaping the structures that enable human and business performance.

In that future, organizational design itself may become a continuous process rather than an episodic “reorg.” Power will be less about formal titles and more about who has access to information, who can mobilize teams quickly, and who can orchestrate complex networks of people and AI agents around emerging opportunities.

Decentralized decision-making is redefining what it means to lead. Leaders can no longer rely on authority rooted solely in hierarchy and control; they must become designers of systems in which many others can exercise power responsibly.

That involves articulating a clear purpose and strategy, setting non-negotiable guardrails, investing heavily in data and AI capabilities, and building cultures that reward experimentation, learning, and ethical judgment. It also means reimagining accountability—shifting from supervising activity to owning outcomes, long-term value, and the health of the overall ecosystem.

The corporate power shift is not about leaders giving power away; it is about redistributing power so that more of the organization can see reality clearly, act quickly, and create value. In an AI-driven economy where speed, innovation, and human ingenuity define competitive advantage, the organizations that learn to combine decentralized energy at the edges with intelligent governance at the core will be the ones that lead the next era of business.

The Leadership Imperative

Digital by Design: How Women Are Engineering Absa’s Tomorrow

In the heart of South Africa’s rapidly evolving digital landscape, there is a growing number of role models in the banking industry who are breaking barriers and redefining what it means to be leaders in finance. From product management and design to cybercrime controls and governance, women are carving out spaces in the supervisory order and transforming institutions from within.

One such institution is Absa Group, a financial powerhouse that has embraced digital transformation with bold ambition and a commitment to diversity. This article explores the dynamic roles women play in South Africa’s digital ecosystem, with a spotlight on Absa’s trailblazing female professionals. Their stories reflect purpose, innovation, and a deep understanding of the unique challenges and opportunities that come with digitising financial services in a diverse and complex market.

The South African Digital Context

South Africa’s digital landscape is marked by contrasts. On one hand, the country boasts high mobile penetration and a growing appetite for digital services. On the other, South Africa’s injustices are now feeding a relatively new form of disparity, that is, digital

inequality. The harsh reality is that the lack of digital access and literacy for many in South Africa is increasing the country’s inequality gap. It grapples with deep socio-economic divides, uneven access to technology, and a persistent gender gap in STEM fields. In this context, digital transformation is more than a business imperative, it’s a social mission.

“Our digital economy is growing at an unprecedented pace. With over 43 million internet users and a mobile penetration rate exceeding 90%, the country is ripe for digital innovation. Yet, the gender gap in digital industries remains a persistent challenge”, says Phiwo Mlotshwa, Digital Portfolio Lead at Absa Digital.

According to the World Economic Forum, women make up less than 30% of the global tech workforce, and South Africa mirrors this trend. However, institutions like Absa are actively working to change that narrative. Through targeted recruitment, mentorship programs, and inclusive leadership strategies, Absa is empowering women to lead digital transformation from the front lines.

South African women transforming tech at Absa Bank

Across disciplines and departments, their contributions reflect a powerful blend of technical expertise, strategic vision, and cultural insight that

is redefining what it means to be digital in Africa. Absa has embraced this mission with clarity and purpose. As part of its broader strategy to become a digitally powered bank, Absa has invested heavily in platforms, partnerships, and people. Central to this transformation is advocating for women in digital roles, an intentional move that reflects both a commitment to diversity and a recognition of the unique value women bring to the digital table. From Johannesburg to Cape Town, Durban to Polokwane, women at Absa are shaping the bank’s digital journey in ways that are both visible and profound. Their work spans technology, product development, risk and governance management, design, cybersecurity, and digital adoption, each area contributing to a more inclusive, agile, and customer-centric financial ecosystem.

“In a space traditionally dominated by men, more women are now architecting smart, human-centric digital experiences, building IT infrastructure, systems, and applications that serve our diverse South African communities”, says Zeenat Hassim, Interim Chief Information Officer at Absa. “By blending technical expertise and visionary thinking with the understanding of our economical and geological landscape, we turn our technological capabilities into a competitive advantage.”

Building inclusive digital products for a diverse nation

“South Africa’s population is as diverse as its geography, and designing digital products that resonate across this spectrum requires empathy,

cultural fluency, and a deep understanding of local realities”, says Sivan Lapidus, Head of Design at Absa Digital. “Women at Absa are at the forefront of this effort, helping to craft digital solutions that reflect the lived experiences of South Africans. Whether it’s simplifying mobile banking for informal traders, integrating vernacular language support, or designing interfaces that accommodate varying levels of digital literacy, we ensure that technology serves everyone, not just the digitally astute”.

This commitment to inclusion is both good ethics, and good business. By expanding access to financial services and removing barriers to entry, Absa is tapping into underserved markets and fostering long-term customer loyalty. Women’s contributions to product development are central to this strategy, helping the bank deliver solutions that are innovative and impactful.

Securing trust in the digital age

As digital banking accelerates, so does the complexity of risk. In this evolving landscape, governance is not just a compliance tick box - it’s about earning trust. “Risk management in digital banking is fundamentally about building confidence,” says Suella Derman, Head of Governance and Control at Absa Digital. “We champion fraud awareness and customer education because informed customers are empowered customers.” This commitment goes hand in hand with

cutting-edge safeguards. Absa employs advanced risk analytics across its digital products, platforms, and processes, backed by comprehensive monitoring and rapid incident response. Every interaction is designed to be secure and seamless.

“Innovation is about creating a digital future where safety and simplicity coexist”, continued Suella. ”In South Africa, where financial scams often target vulnerable communities, this approach is both a strategic intent and also a social imperative. By anticipating threats and educating users, we are shaping a safer digital environment for all”.

At the heart of this effort lies a simple truth: trust is the cornerstone of every digital experience, especially with banking.

Leading change from within

“Digital transformation is more than launching new products. It’s changing how people live, work, think, and interact. We are propelling a cultural shift, helping customers embrace new technologies and ways of working”, says Michelle Bisaro, Digital Product Lead at Absa. “Managing this change is both an art and a science. We use storytelling, gamification, and customer education initiatives to make digital transformation engaging and relatable for our clients”.

The digital transformation of South Africa’s financial sector is a complex and ongoing journey. It requires a deep understanding of the country’s unique challenges and opportunities. Having a diverse and representative leadership team, Absa is playing a central role in this journey, driving digital banking across disciplines and redefining what it means to lead in digital.

Empowerment through partnership

Absa’s commitment to women in digital extends beyond its internal operations. They provide targeted financial products and business support to help women entrepreneurs launch and scale their businesses, such as their “She Thrives” program, which offers women-owned businesses low-cost banking solutions, while the “Women-in-Business Directors Training Programme” collaborates with the South African Chamber of Commerce and Industry (SACCI), offering training to help increase the number of women on corporate boards.

The “She's Next” initiative, In partnership with Visa, provides women entrepreneurs with funding, training, and mentorship to help them succeed. In 2025, the program awarded over R1 million in grant funding.

“We recognize the importance of creating pathways for more women to enter and thrive in digital careers. Because when women lead in digital, the entire nation moves forward,” says Anna Nascimento, Head of Digital Adoption at Absa. “Digital adoption encompasses consumer culture, customer education and digital dexterity. Over the past year, Absa

Digital has grown its digitally active customer base by more than 11%, introduced AI-led personalisation pilots, and strengthened digital fraud protections, all while keeping ethical innovation at the centre”.

These efforts reflect a broader vision: to empower Africa’s tomorrow through inclusive innovation. By supporting women in digital, Absa is contributing meaningfully to a more equitable and prosperous society.

The Road Ahead: Challenges and Opportunities

While progress is undeniable, challenges remain. In the industry, women in digital still face barriers such as unconscious bias, limited access to mentorship, and underrepresentation in leadership roles. Deliberate inclusion, opportunities and collaborating with external partners to support STEM education and entrepreneurship among women is key to advancement.

Looking ahead, the future of digital in South Africa will depend on how well institutions harness the full spectrum of talent. Women bring unique perspectives that are essential for building inclusive, resilient, and innovative digital ecosystems.

Women at Absa are playing a central role in its future

The women of Absa Digital’s executive committee stand for customerfirst innovation, where every product, feature, and experience begins

with a single question: How can we make banking easier, safer, and more human? Every discipline plays a critical role: Design ensures every journey is built around empathy and insight, creating digital experiences that feel intuitive and inclusive. Digital Adoption connects innovation to customers’ everyday lives, ensuring that the right solutions reach the right people in ways that build trust and confidence. Digital Products drive growth and delivery, turning ideas into scalable products that solve real customer challenges. And Operational Governance anchors it all in integrity, resilience, and responsible innovation.

“Together, we are united by a shared belief that digitalisation must start and end with the customer”, says Subash Sharma, Chief Digital Officer at Absa. “Digital progress is being powered by women across Africa. Their leadership, creativity, and persistence are transforming the way we think about technological advancement. I’m incredibly proud to witness the remarkable work being done by our women executives”.

The inspirational stories of Zeenat, Phiwo, Michelle, Sivan, Suella and Anna from Absa demonstrates that the future of digital banking is being designed, delivered, and governed by women who turn customer insight into impact and innovation into trust. As institutions continue to evolve, the involvement of women in digital roles will be essential to building systems that are resolute, and responsive to the needs of all citizens.

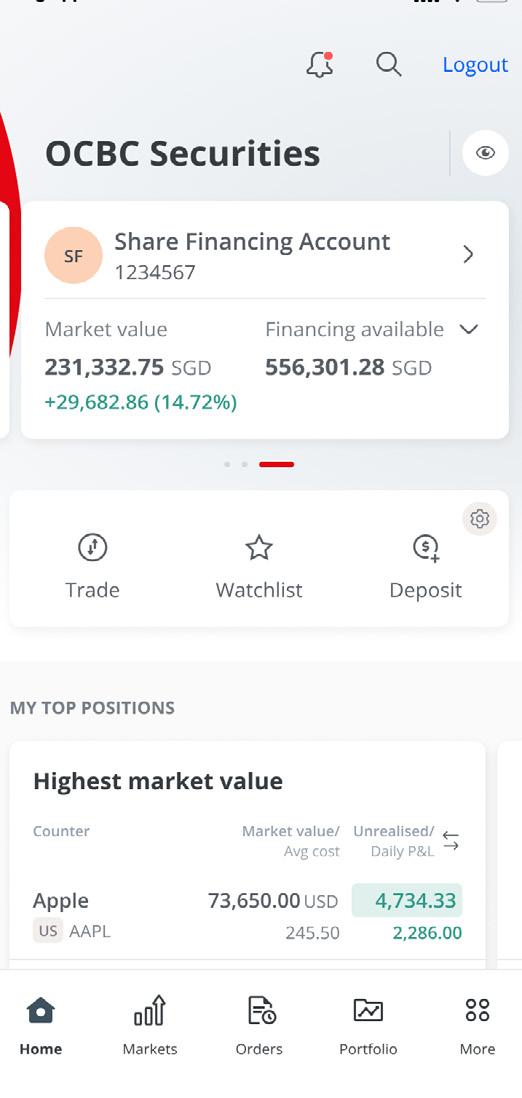

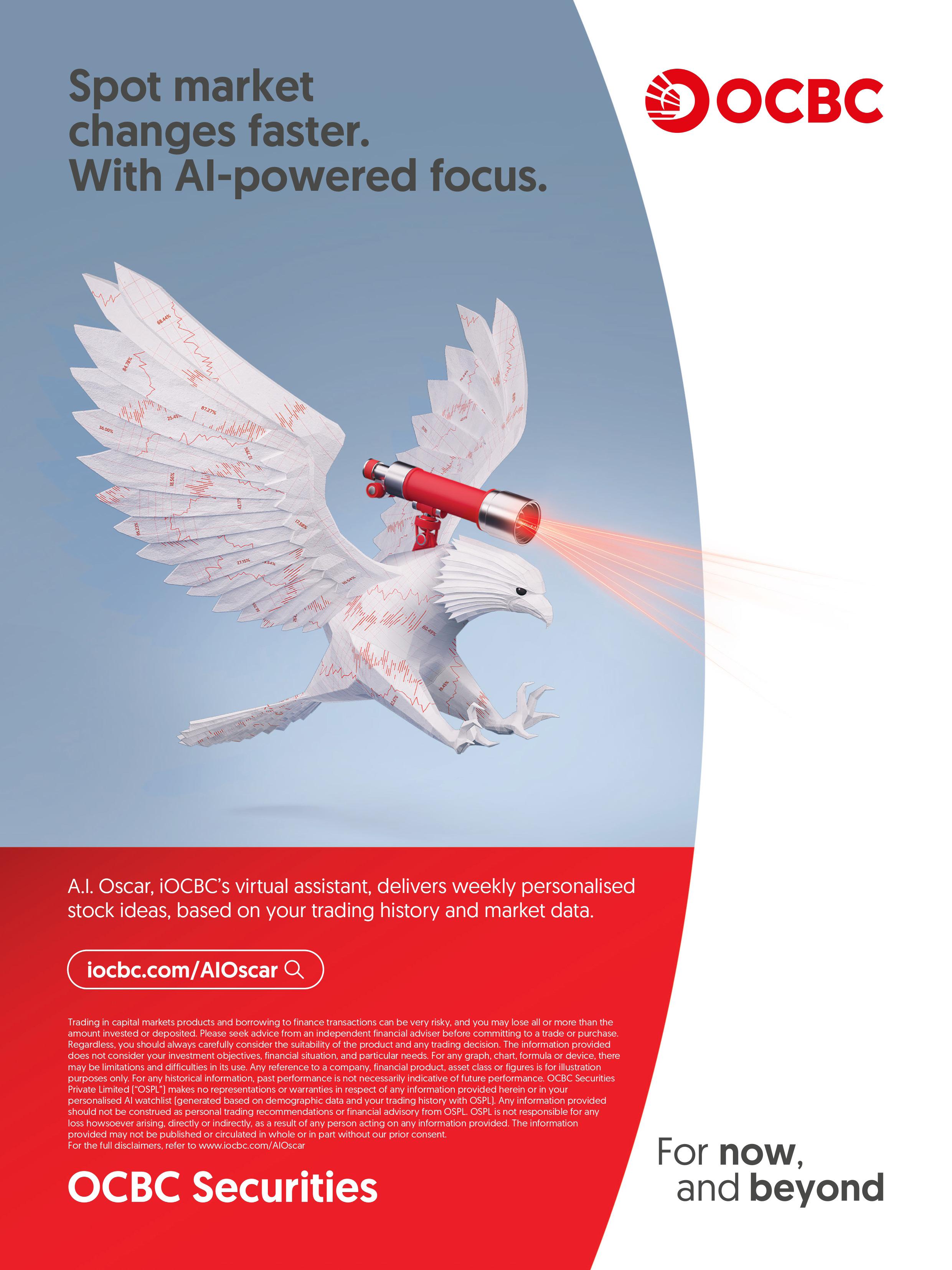

Expanding the Edge: OCBC Securities Accelerates Innovation under Wilson He

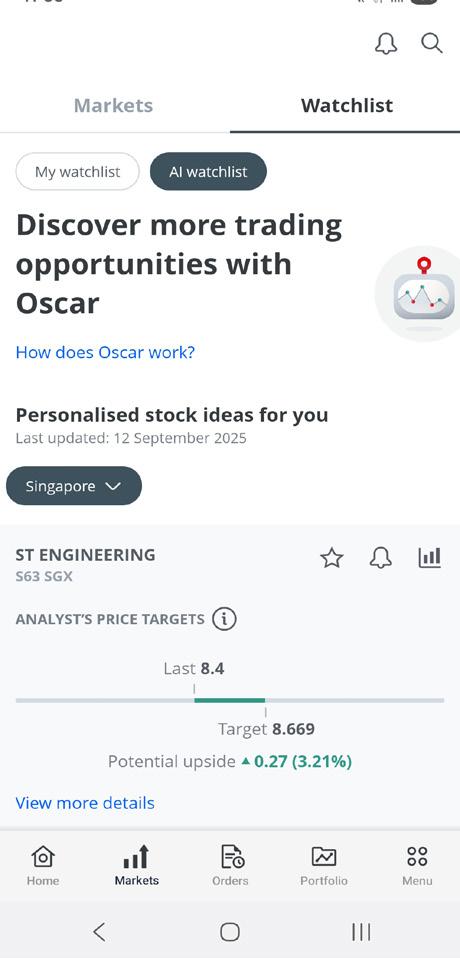

OCBC Securities, a wholly owned subsidiary of OCBC and one of Singapore’s leading brokerage firms, is expanding its edge in the market through focused innovation—enhancing platform capabilities, leveraging Artificial Intelligence in customer-centric ways, and building on its integration with OCBC. Under the direction of Managing Director Wilson He, the firm has continued to advance its digital roadmap, including the rollout of A.I. Oscar, an innovative artificial intelligence powered virtual trading assistant, which provides personalised stock ideas based on a customer's trading history and basic demographic data. Alongside ongoing upgrades to the iOCBC trading platforms and the continued success of the co-branded ETFs with Lion Global Investors, OCBC Securities is deepening its commitment to giving investors more responsive tools, broader access, and a seamless trading experience.

We caught up with Wilson to explore how these initiatives— spanning artificial intelligence, platform upgrades, and product development—are shaping OCBC Securities’ vision for a more agile, integrated trading experience.

Expanding Access Through A.I. Oscar

In June of 2024, A.I. Oscar began providing stock ideas for the U.S. and Hong Kong markets. By November, the number of unique monthly users had almost doubled. Wilson said the growth reflected the tool’s ability to deliver timely and relevant stock ideas based on customers' trading history.

“In the current volatile environment, our customers want insights that add value,” Wilson said. “A.I. Oscar has proven itself to be an indispensable tool in providing just that.”

A real-time example came in April 2025, when an unexpected tariff hike announced by President Trump triggered market turbulence. "A.I. Oscar rapidly generated a list of potential stock ideas for our customers," Wilson said.

While the tool was initially expected to appeal to younger users, adoption has extended across age groups. “We’ve found that seasoned investors and traders are also incorporating A.I. Oscar as part of how they monitor market movements and potential opportunities,” Wilson added.

Thematic push notifications have also helped maintain engagement by keeping users up to date on the latest market trends and potential opportunities.

Improving Infrastructure and Trading Access

OCBC Securities has focused on improving how customers manage both funding and trading activity across its platforms. As part of its infrastructure integration with OCBC, the firm now enables instant fee-free fund transfers across up to 11 different currencies between their Basic Trading Account and eligible OCBC bank account.

“Our enhanced fund transfer service helps ensure that investors can respond quickly to opportunities and maintain sufficient balances when needed,” Wilson said.

This capability gives customers round-the-clock access to their balances through the iOCBC trading platforms. “The aim is to make trading simpler, more efficient, and more accessible,” Wilson added.

In May 2025, OCBC Securities introduced a refreshed interface for its mobile trading app—part of ongoing updates to the iOCBC trading platforms. Wilson said the revamp focused on making the app easier to use, particularly for investors who trade while on the move. The update included a customisable shortcuts panel and improved access to weekly stock ideas from A.I. Oscar.

Wilson pointed to the addition of a new screen that displays bid-ask prices, trading ranges, and volume in a single view. “Customers can now view live bid-ask prices, daily trading ranges, and market volume all in one place,” he said. “It removes the need to switch between screens and helps users stay on top of market movements more efficiently.”

The project, Wilson explained, was informed by feedback gathered through OCBC’s customer labs, where users test new features and share insights directly with the team. “We’re constantly reviewing how our

Wilson He Managing Director, OCBC Securities

customers interact with the platform and using those insights to guide our product roadmap,” he said. “There are additional features in the pipeline that will continue to build on this foundation and improve the trading experience over time.”

Enhancing Portfolio Control Through Consolidation

Consolidating securities within OCBC Securities allows customers to better monitor portfolio performance, rebalance holdings, and respond to market shifts more effectively. “When everything is under one roof, it becomes easier to make timely adjustments,” Wilson said.

He added that this also improves how customers use A.I. Oscar. “The tool is able to generate more relevant stock ideas when it has access to a fuller view of a customer’s trading history and behaviour,” Wilson said. “That additional context helps surface ideas that are better aligned with how each customer typically interacts with the market.”

Wilson said the firm offers a share financing option that enables customers to use their existing stockholdings as collateral. "They can access up to 4 times the value of their current stockholdings without having to sell their positions," he said. “It’s about unlocking value that’s already in the portfolio and keeping investors in control of their strategy.”

Delivering Thematic Investment Access Through ETFs

OCBC Securities has partnered with Lion Global Investors to co-launch a suite of exchange-traded funds that give investors access to targeted themes and sectors across Asia. "These ETFs are designed to support different trading strategies for both new and experienced investors," Wilson said.

A notable example is the Lion-OCBC Securities APAC Financials Dividend Plus ETF, which was launched in May 2024 and tracks the iEdge APAC Financials Dividend Plus Index. It offers exposure to 30

leading financial institutions1 across the Asia Pacific region, including banks, insurers, and investment services firms and is designed to deliver dividends. It was named Top New ETF by AUM on SGX in 2025 and awarded Best New ETF (Singapore) by Asia Asset Management in 20252

The diversified Lion-OCBC Securities ETFs range include thematic products tailored to different investor goals. These span from sustainability-focused funds like the Lion-OCBC Securities Singapore Low Carbon ETF, which tracks the iEdgeOCBC Singapore Low Carbon Select 40 Capped Index, to other funds like the Lion-OCBC Securities China Leaders ETF, which was the best performing China equities ETF on SGX in 20243

Maintaining the Human Element

Although platform development remains a key focus, Wilson said that OCBC Securities continues to rely on its Trading Representatives as a central part of the client experience. We support our Trading Representatives by providing them access to timely market insights and information," he said. "That enables them to respond quickly when clients require assistance."

The team also draws on partnerships with organisations including Nasdaq, the Hong Kong Stock Exchange, Bank of Singapore, and OCBC Wealth Advisory. These relationships ensure representatives are informed on regulatory changes, macro events, and market shifts.

“Our goal is to ensure that customers have access to both timely information and experienced support when it matters most,” Wilson said.

Strategic Priorities for Platform and Product Development

Looking ahead, Wilson said OCBC Securities remains focused on helping investors navigate fast-changing market conditions. “Our customers lead full, often fast-paced lives,” he said. “We want their trading experience to be straightforward—easier to access, easier to understand, and supported by tools that help them make more informed decisions.”

He added that the firm is continuing to refine A.I. Oscar and the iOCBC trading platforms, while expanding product options to meet growing demand for more investment offerings. “We’re investing in our systems, our product lineup, and our people to ensure we can keep pace with customer expectations and support them as those expectations evolve,” Wilson said.

Driving Efficiency and Profit Through Customer-Centric Banking

Did you know that the majority of banking customers say their experience with their bank influences their loyalty more than rates or products? In today’s hyper-competitive landscape, customercentric banking isn’t just a buzzword—it’s a business imperative.