Revolutionizing Banking in Africa:

Absa Bank's Journey Towards Digital Excellence and Inclusive Growth

www.globalbankingandfinance.com Issue 59

Chairman and CEO

Varun Sash

Editor

Wanda Rich

email: wrich@gbafmag.com

Head of Distribution & Production

Robert Mathew

Project Managers

Megan Sash, Amanda Walker

Video Production and Journalist

Phil Fothergill

Graphic Designer

Jessica Weisman-Pitts

Client & Accounts Manager

Chanel Roberts

Business Consultants

Rick Saikia, Monika Umakanth, Stefy Abraham,

Business Analysts

Samuel Joseph, Dave D’Costa

Advertising

Phone: +44 (0) 208 144 3511 marketing@gbafmag.com

GBAF Publications, LTD

Alpha House

100 Borough High Street London, SE1 1LB United Kingdom

Global Banking & Finance Review is the trading name of GBAF Publications LTD

Company Registration Number: 7403411

VAT Number: GB 112 5966 21 ISSN 2396-717X.

The information contained in this publication has been obtained from sources the publishers believe to be correct. The publisher wishes to stress that the information contained herein may be subject to varying international, federal, state and/or local laws or regulations.

The purchaser or reader of this publication assumes all responsibility for the use of these materials and information. However, the publisher assumes no responsibility for errors, omissions, or contrary interpretations of the subject matter contained herein no legal liability can be accepted for any errors. No part of this publication may be reproduced without the prior consent of the publisher

Welcome to the 59th edition of Global Banking & Finance Review. Whether you are a seasoned follower of our publication or joining us for the first time, are delighted to share with you the latest insights and trends from the everevolving financial sector.

This issue, we proudly feature the dedicated team behind Absa Bank Limited on our front cover. Our leading story, "Revolutionizing Banking in Africa: Absa Bank's Journey Towards Digital Excellence and Inclusive Growth," takes an in-depth look at how Absa Bank is steering the course towards innovative banking solutions across Africa. Spearheaded by the insightful Subash Sharma, Chief Digital Officer, Absa's narrative is one of commitment to digital innovation, fostering customer trust, and spearheading inclusive growth. Delve into this compelling journey starting on page 24 and discover how Absa Bank is setting new benchmarks in the banking sector.

2024 stands at the brink of transformative changes driven by artificial intelligence (AI). "Double Clicking Into AI: How 2024 will be different for financial institutions looking to implement AI" delves into the trends and strategic insights that will shape the implementation of AI in financial institutions (FIs) this year. Following a year that marked a significant uptick in AI's integration across various sectors, particularly in enhancing customer experiences, this article draws on insights from John Willcutts, NICE’s general manager of digital and AI, to explore how the lessons learned from 2023's AI advancements are paving the way for more nuanced and impactful AI strategies within FIs. (Page 22)

At Global Banking & Finance Review, our commitment remains steadfast in providing you with comprehensive coverage and expert perspectives. Whether you're a seasoned professional or new to the world of finance, our magazine is your guide through the ever-evolving financial landscape.

Enjoy!

®

Stay caught up on the latest news and trends taking place by signing up for our free email newsletter, reading us online at http://www.globalbankingandfinance.com/ and download our App for the latest digital magazine for free on Google Play and the Apple App Store

Featured on the front cover Absa Bank Limited. Pictured: Left to right (seated) Suella Derman - Head of Risk, Digital, Phiwo Mlotshwa – Digital Portfolio Lead, (seated) Ritesh Sewsaran – Digital Portfolio Lead, Jetame Poonan – Head of Strategy and Commercialization, Maha Subramanian – Head Core Channels and Security, Alex Oloo – Head of Digital Design, Michelle Bisaro – Digital Portfolio Lead, Front (seated) Subash Sharma, Chief Digital Officer, Absa, Everyday Banking

12 42 48

Open banking must step up its fraud prevention

Tareq Shaheen

Director of Payment Solutions, Eastnets

Bridging the AI Divide: How Banks Can Responsibly Adopt Large Language Models (LLMs)

Oliver King-Smith, Founder, SmartR AI

How consumer banking trends are redefining the B2B payments experience

Preserving a digital legacy Kyra Motley, Private Client and Tax Partner, Boodle Hatfield

Fintech in 2024 – Onward Growth or Waning Momentum?

Khofiz Shakhidi, Chairman, Alif Bank

How Green is Green? Empowering ESG Investment Managers with Standard Methodology

Maria Vigliotti, CEO, Fidata and D2 Legal Technology’s Akber Datoo and Elliot Curtis

Leading a different kind of charge: Financial Institutions as climate change activists

Steve Croke, Chief Technology Officer for Financial Services at GlobalLogic

Uniting tech & financial foresight: how CFOs can ‘see’ into the future

Todd McElhatton, CFO, Zuora

How to set up your business for success in 2024

Matt Clementson

Head of Enterprise UK&I at SAP Concur

Business leaders pave the way for phishing-resistant MFA

Niall McConachie

Regional Director (UK & Ireland) at Yubico

Time to End the Trade Tagging Blame Game

Eric Mueller, Managing Director and COO, D2 Legal Technology

Emma Wooldridge Consultant, D2 Legal Technology

Marshall

2024

Tim

Steering

Guillaume

Understanding

Sumit

Solving

Neil

Nicole

Kyra Motley

Private Client and Tax Partner, Boodle Hatfield

In an era of technological advancements and an ever-growing digital landscape, international private client advisers have seen practices evolve to address new challenges and adapt to new generations. As the world becomes increasingly interconnected and asset classes grow, the importance of family governance and comprehensive estate planning has never been more crucial and clients need to consider more than bricks and mortar, businesses, heirlooms, and cash as valuable assets.

What are assets?

When considering an estate, traditional tangible assets like watches, art or classic cars may come to mind. But as the Oxford Dictionary relays, an asset is a useful or valuable thing or person. An item of property owned by a person or company regarded as having value. As we see technology advancing daily and the digital landscape growing across the globe, a rising number of estates now have a significant ‘digital footprint’ which has reshaped the definition of assets and necessitated a re-evaluation of traditional wealth management strategies.

The term ‘digital asset’ has been coined to describe a broad spectrum of assets, but often, Non-Fungible Tokens (NFTs) and cryptocurrencies will be front of mind for such term. According to Statista , an estimated 1 billion people around the world have interests in at least one form of cryptocurrency and research from Chainalysis shows that the Middle East & North Africa (MENA) is one of the most active in the world for digital asset adoption with the region witnessing 48% growth in 2022, the highest globally, followed by Latin America.

The rapid surge of virtual currencies and digital technologies has highlighted the need for a comprehensive approach to wealth management and it is now more significant than ever to consider both your palpable and digital possessions as part of your planning.

While NFTs and cryptocurrencies often steal the spotlight, figures shows that there are almost 6 billion smart phone users across the globe, which is just over 85% of people and it is essential to recognise that digital assets encompass a vast array of items. Photos and data held on ‘the cloud’ should not be forgotten either. These items can often have great emotional and sentimental value.

What are the laws surrounding digital assets?

Traditional tangible assets are dealt with under laws that have been longestablished and put in place to see the transfer of property after death. Stored photos, private keys to digital wallets, and personal data held by digital platforms are all part of an individual’s digital legacy. However, unlike tangible assets, that will be passed on to executors or administrators and then disseminated in accordance with a will or the laws of intestacy when a death certificate or grant of probate is obtained, digital possessions will not pass to a spouse or to children in the same way. On death, unless the private key or password is known and the family beneficiaries know the details of the digital wallet, there is no way of accessing the assets, or proving ownership. As reported in the New York Times , research suggests, that of the existing 18.5 million Bitcoin, around 20 percent appear to be in lost or otherwise stranded in virtual wallets.

So, what steps can be taken to mitigate the consequences of these assets becoming inaccessible on death? In most cases the initial step is to make these assets known to personal representatives and professional advisers. Preparing an inventory that captures virtual asset(s) and how to access them and ensuring it is regularly updated and kept securely, will aid with the administration of the estate. Specific authority relating to a lasting power of attorney in the event of mental incapacity, should be considered too. In turn, this will make it more likely the individual who should benefit from or control these assets will be able to do so. If the assets are not included as part of an estate plan, there is a chance that they will be irretrievable, which may not be the owner’s intention.

A Will becomes publicly available following the grant of probate, and so it is important that any sensitive information such as guidance on how to retrieve a testator’s virtual assets should be kept in a separate memorandum which is stored safely. This will support the creation of a more robust ‘digital legacy’ strategy.

As the global landscape of wealth management continues to undergo a digital transformation, the importance of family governance and wealth planning has never been more pronounced. The concept of digital assets extends far beyond ‘the cloud’ and families with international interests must approach estate planning with a global perspective, considering legal, cultural, and technological nuances. By proactively addressing the challenges associated with digital assets, individuals can ensure the preservation of their digital assets and the seamless transfer of assets across borders and generations.

By all accounts, the rise of fintech can be considered a success story. Since its inception over a decade ago, financial technologies have challenged and permanently transformed the manner in which businesses, consumers, and investors manage their banking and financial services. The success stemmed from a driven generation of entrepreneurs, leading startups, questioning the status quo, and attracting the interest of investors.

Move forward to 2024, and industry commentators are confident momentum will not just be sustained but increase. A report from the Boston Consulting Group and QED investors projects that fintech revenue will sixfold from $245 billion to $1.5 trillion by 2030. At the same time, the fintech sector’s global share of global financial services revenue is estimated to grow from 2% to 7%.

These are impressive figures, but it naturally leads to questions. Can a sector that has already successfully scaled at pace be able to accelerate its growth and reach new milestones in the coming decade? The short answer: yes. The reasons for this are multiple, and yet are all linked together by the rise of new fintech markets outside of the established jurisdictions.

The majority of fintech innovation has come from the world’s leading financial markets. The US, UK, Europe, and China have accommodated some of the sector’s biggest names, fostering an environment that promotes company growth through targeted reforms and regulations.

Alongside the recognizable unicorns based in these established hubs, we are also seeing a new wave of fintechs addressing more technical or specific gaps across the B2B and B2C space.

However, a significant share of fintech’s growth will stem from emerging markets. The UAE is a clear example of this. The UAE government has been clear in its mission to make the country not only a leading hub for fintech in MENA but recognized globally. This will reinforce the fintech trends across the GCC region with greater intra-regional connectivity over the next 10 years.

Data from Innovate Finance showed that while global investment into fintechs dropped in 2022, in the UAE, total investment flows increased by 92%; a result of accommodating regulations and the rising adoption of digital banking and tech-enabled financial tools. High investment flows also suggest a healthy collection of SMEs and startups, with investors clearly confident in the long-term prospects on display in the region.

The factors contributing to the rise of scaling markets range from statebacked initiatives to market sentiment and the innovation on display from local fintech businesses. In the UAE, an effective balance has been struck between innovation and regulatory policies, ensuring that companies have the freedom to scale at pace, attract new talent, and support their commercial targets. Advanced technological infrastructure is vital in this regard. Emerging markets have had to pool significant capital investment into the infrastructure needed to make them globally competitive with established markets. The UAE has effectively done so, with Dubai positioning itself as the city of the future. All this plays into the market potential, triggering a snowball effect that encourages new investment, business creation, and ultimately secures the long-term future of the local fintech industry.

Alongside investment, the other factor driving the rise of emerging markets is the rise of local populations who have access to the internet and rely upon smart devices to complete daily activities. In Central Asia, enhanced digital penetration through infrastructure investment, the adoption of digital over cash payments, and

Khofiz Shakhidi Chairman, Alif Bank

Khofiz Shakhidi Chairman, Alif Bank

greater consumer awareness has promoted the use of fintech solutions. Tajikistan and Uzbekistan are two countries of note, with e-commerce and banking products growing in popularity. As awareness increases, so too will the adoption of fintech solutions.

With new markets come new demands. Local needs require local solutions, with fintech companies offering products that are tailored to the habits of native populations. According to research from Mastercard, just under half (48%) of the UAE population is planning to send cross-border payments more frequently in 2024. This is due to the UAE accommodating one of the world’s largest international migrant workforces, as 87.9% of the entire population, making the case for tech-

enabled payment systems to overcome the traditional challenges faced when sending money cross-border.

Emerging fintech hubs have the benefit of learning from the experiences of the established hubs, particularly from the West. A decade ago, fintech’s integration into banking and financial practices was rapid. The heightened adoption by consumers, investors, and businesses provoked questions over whether fintech was sustainable and able to challenge the legacy enjoyed by the mainstream financial institutions. Now, emerging fintech hubs can learn from these experiences, understanding what policies can be introduced to mitigate any obstacles for growth and provide an environment that supports industry growth.

With the established fintech hubs entering a period of consolidation, we are likely to see a large share of industry growth occur in places like the GCC and Central Asia. Through investment, innovation, and higher adoption rates, these emerging hubs will be one of the central forces driving the perpetual evolution of fintech. Excitingly, it demonstrates that fintech is a global force that is not just the marriage of financial services and technology but a movement that is digitally empowering populations around the globe.

The start of 2023 has seen generative AI explode into the mainstream, with ChatGPT introducing the transformative power of this technology to a broad consumer audience. Big tech firms are taking steps to turn theory into practice, lifting AI projects out of the sandbox and into the real world. Since ChatGPT was released, a wider audience has been exposed to the emergent capabilities of Large Language Models (LLMs) to achieve results beyond the scope of their initial creation. The floodgates are creaking open, and the fourth industrial revolution is beginning.

Revolutions don’t, however, happen overnight. Behind this upsurge in interest, AI innovators have been methodically fine-tuning AI models for their breakthrough moment. Now that that moment has arrived, the appetite for AI – from both consumer and enterprise – has skyrocketed. Industrial revolutions, however, don’t take place in the consumer realm. Industry is the engine that fuels societal change, and it is through industry applications that AI will bring the most significant societal benefit.

ChatGPT is just the tip of the iceberg for generative AI capabilities, and enterprise-focused AI vendors are leading the way in bringing additional capabilities to market. Enterprise-ready AI is not the next step following ChatGPT; it’s the very foundation on which future success will be built and has proven its reliability and readiness to supercharge businesses.

Enterprise continues to lead the way in implementing AI to significantly improve customer services and operational efficiency. For example, the banking industry is already adopting advanced language models to consolidate AI sprawl into high-performance foundation models. In addition, banks have recognised that they’ve been sitting on troves of unstructured data such as emails, chat logs, voice call recordings and financial reports. As a result, we’re increasingly seeing more and more banks put AI foundation models in place to gain trapped insights from this data.

Many businesses have employed conversational AI in forms like conversational AI chatbots for many years already. However, in 2023, we have seen AI leap into the domain of genuine ROI for businesses, and the potential use cases for enterprise expand beyond what was previously thought possible.

To get the most out of AI deployment, businesses need a considered long-term strategy and the expertise and knowledge base to fine-tune their AI model. Traditionally, new technologies are judged on their ability to deliver short-term ROI. However, with the current gold rush on generative AI, this can lead to the confusion of multiple models being adopted for different use cases simultaneously, limiting scalability and, ultimately, restricting their effectiveness.

Foundation models are the basis of generative AI and enterprise success

LLMs form the basis of a new generation of revolutionary AI engines. With ChatGPT, they’re showing their ability to comprehend and generate coherent language. LLMs are already being implemented across industries, generating insights from vast swathes of unstructured data. However, foundation models, the basis of generative AI and LLMs, are where the real value for enterprise can be found.

LLMs, like the GPT-based model that powers ChatGPT learn from enormous quantities of data. Unfortunately, this can lead to inaccuracies in disseminating flawed data, requiring more privacy and security for enterprise applications. Recently, we’ve seen organisations like Goldman Sachs instruct their employees to stop using the public ChatGPT model due to security concerns, and inaccuracy is simply not an option for enterprises looking to generative AI to optimise their operations.

Tailored, enterprise-ready generative AI models can avoid these problems of inaccuracy when finetuned with the firm’s own data. Businesses can reduce their tech sprawl by centralising functionality into a solitary model by utilising foundation models. Private foundation models with a business’s own data can enable companies to retain control over how that data is stored and used. Control over data is retained, and the best infrastructure for achieving strategic objectives can be utilised, both of which are top concerns for enterprises.

It’s an inspiring time to be at the forefront of generative AI as the AI gold rush kicks off in earnest. However, bringing these groundbreaking capabilities to enterprise and turbocharging business efficiency is the most exciting.

Marshall Choy, SVP, SambaNova Systems

Marshall Choy, SVP, SambaNova Systems

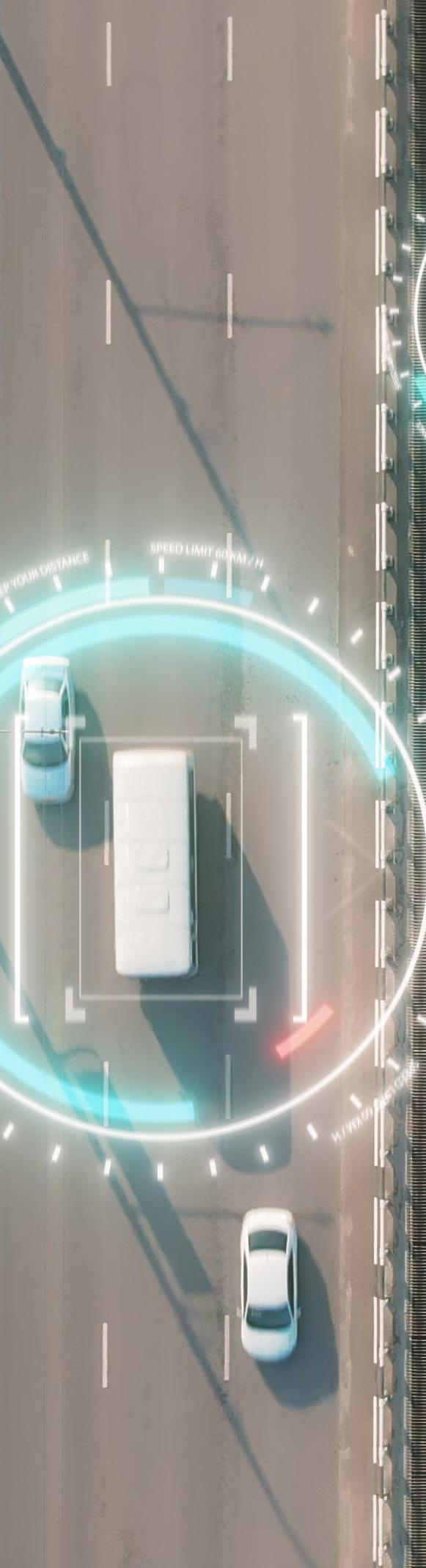

Through open banking, the European Union continues to embrace its interconnected financial ecosystem; connecting, collaborating and sharing customer data instantly.

Yet, the risk of fraud looms larger than ever. Today’s criminals are relentless architects of deception, exploiting every crack in our financial systems at the touch of a button. They threaten to undermine the foundations of the EU’s open banking market, putting its expected 63.8 million users by 2024 at risk.

Open banking simply extends the financial services ecosystem, expanding the attack surface and creating more entry points for fraudsters. Yes, it offers customers additional payment sources, but it simultaneously offers new opportunities for fraud. From phiswhing emails to ‘formjacking’ on websites that steal a user’s banking data, consumers lose on average €4,191 for fraudulent credit transfers.

Now more than ever, there is a need for a proactive, data-driven approach to fraud prevention. And the European Commission’s announcement of Payment Services Directive 3 (PSD3) is aimed to do exactly that.

WhilePSD3 is not expected to be enforced until 2026, there’s an acute need for fraud prevention now. Both banks and customers can’t afford to wait. So, how can financial institutions reduce the risk of financial fraud, today?

Open banking presents challenges in safeguarding customer data accessed by Third-Party Providers (TPPs). Currently, banks bear the risk when authenticating transactions. However, this dynamic might shift within open banking to TPPs initiating more payments and potentially taking over customer authentication.

This creates multiple vulnerabilities via Application Programming Interface (API) connections, as fraudsters exploit these gaps, employing tactics that blur the lines and make it difficult to spot the difference between authorised and unauthorised transactions.

Worse yet, fraudsters often set up a front business and pose as a fintech provider for the purpose of stealing financial data from their “clients.” Consumers tend to lack experience with TPPs and the rise of fintech apps can expose consumers to the risk of “spoofing”, among other threats.

PSD3 aims to close those gaps. It’s designed to modernise payments, and the wider financial sector, enhancing their digital capabilities and efficiency. It will introduce minimum standards for open banking APIs and employ crucial changes to help mitigate the various tactics used by cybercriminals, such as forced verification, phishing attacks and impersonation fraud. But much like implementing any legislation, it takes time.

Time that financial services providers

– and consumers – don’t have. As technology continues to evolve and expand the attack surface, so does the risk of fraud. Given the surge of API calls now exceeding over one billion per month in just Germany, France and Italy alone, there are a lot of opportunities for fraudsters to act. Time is of the essence.

Yet, current fraud prevention systems are under significant strain and struggling to keep up; the adoption of open banking services is only expected to double across European countries by 2027, putting further strain on current fraud prevention systems. Despite its popularity, open banking service providers are still new players in the industry. They don’t always have the infrastructure that traditional banks do with fraud prevention, leaving them more prone to risks associated with data breaches and cyberattacks.

From a lack of investment in the API infrastructure that open banking needs, to the underlying payment infrastructure issues in various EU countries, more must be done to protect open banking users immediately.

Banks are responsible for ensuring not only the financial safety but also the data privacy of their customers and can face regulatory fines if they share data with unauthorised third parties. What they need is better infrastructure and better fraud prevention and compliance mechanisms to mitigate these risks today.

It’s no longer about staying in line with regulations – it’s time to get ahead. This means harnessing the right technology to combat fraud. It’s a race where banks can’t afford to fall behind.

Banks must make strategic investments in cutting-edge technology, particularly fraud prevention software. By using AI, algorithms and data analytics, banks can identify suspicious patterns and anomalies before they escalate into full-blown fraud.

With better prevention systems and safer ways to store customers’ financial data, there will be less friction with transactions in the open banking user journey too. Software, such as Eastnets’ AI-driven fraud prevention solution PaymentGuard, not only protects customers but also safeguards the banks’ bottom line by preventing financial losses.

However, the stakes go beyond just financial losses.

Tareq Shaheen Director of Payment Solutions Eastnets

Tareq Shaheen Director of Payment Solutions Eastnets

Compliance with regulations is equally crucial. By deploying robust fraud detection systems today, banks will be able to get ahead of the likes of PSD3 and Payment Services Regulation (PSR); particularly as the semantics of PSD3 is leaving the details up to the European Banking Authority (EBA). From there, EBA will be updating the Regulatory Technical Standards (RTS) to improve the market. But again, this will take time. So providers must get ahead of the threat today.

Nevertheless, technology has become a double-edged sword.

While banks adopt digital advancements to improve customer experiences, fraudsters are quick to exploit the same innovations. Artificial intelligence is a prime example, as it’s increasingly used in scams to deceive individuals by faking language, audio and even video.

The customer now represents the potential weak link in the chain, particularly when initiating payments. Legislation won’t mitigate the risks associated with inattention, so consumers must exercise caution and take ownership, especially when making larger payments.

Therefore, more also needs to be done by firms and regulators to raise consumer awareness in the open banking ecosystem. It’s a critical step for consumers to avoid falling victim to cleverly orchestrated fraud before it even happens.

The changes being introduced by PSD3 demand that banks and financial institutions need to act. But why wait and suffer in the meantime?

To preserve their reputation within the open banking sector and effectively combat the looming threat of fraud, banks must invest in state-of-theart fraud prevention technology today, and adapt their APIs and authentication processes to align with the new requirements.

However, this isn’t just a matter of having the technology in place; it’s a chance for collaboration. Policymakers and regulators need to work together to establish consistent, highquality standards and infrastructure.

Whether it’s the technology being used for deception or the consumers’ inattention, there’s now a need for a collective effort to better safeguard the interests of all stakeholders in the open banking landscape. And they cannot afford to wait.

In today’s time of uncertainty, the role of a CFO is growing increasingly challenging. The supply chain of essential goods and services that underlie your revenue often sits outside of direct oversight and can be disrupted in unforeseeable ways. Demand patterns can shift in unpredictable ways, especially as they interact with cultural trends and brand reputation. And, perhaps above all, macroeconomic pressures can create both friction and fluidity in any given financial variable.

Yet these issues need to be tackled strategically, and CFOs need to strike a balance between staying agile in the short-term while setting a long-term strategy and sticking to it. They can’t get tied down with only addressing what is immediately in front of them. If they do, they risk fighting for a future that is unstable from the offset. As such, CFOs want to know what to expect from the future so that they can prepare without having to constantly pivot; they’re seeking greater visibility to navigate these new trends and challenges nimbly, and ultimately rise above uncertainty.

There are now a powerful range of approaches available to help CFOs meet the demands being placed on them. The fundamental agility offered by cloud platforms –enabling more flexible working styles, scalable capacity, and closely right-sized expenses – has of course been a major story over the last decade as digital transformation has ramped up across different sectors. Likewise, and even just as important, technology has empowered a more proactive approach to future revenue.

Traditionally, driving internal efficiency may have been the major way that a CFO could intervene in business challenges. However, even as market conditions have become more unpredictable and disruptive, technology has also increasingly enabled businesses to adapt their behaviour, and therefore their spend, in light of changing conditions. Business leaders can use technology to spot trends and pivot where necessary, taking the guesswork out of building a resilient strategy. This grants them a more forward-thinking, granular, and impactful way of managing spend in response to market changes.

When considering the range of stakeholders CFOs now need to support with smart planning and intervention, such visibility is incredibly valuable. For example, with the right technologies they can assure shareholders that they have a realistic runway to see projects through and invest in the future, in turn supporting job security and career ambitions. For boards of directors, these tools can help ensure that products or services adopted today will still be fully supported tomorrow, even amidst market changes.

While there is no crystal ball for the future, the reality of rising interest rates and budgets being constantly squeezed means that improving profitability and efficiencies will continue to be critical. This makes tools that automate tasks increasingly valuable in helping to streamline processes, as well as delivering a reliable and stable picture of future revenue. Survey data supports a strong desire for these tools too, with 79% of revenue accounting leaders stating that there’s a need for higher levels of automation. Despite this, many executives aren’t recognising the impact that revenue automation can have on the business, as 67% of respondents in the same survey said it’s a struggle to get buy-in from finance and accounting leadership.

While recurring revenue models are by no means new, there’s huge scope for them to offer greater long-term value while being able to respond to changes in real-time when approached strategically. As a foundation, implementing predictable business models makes it possible to confidently forecast a baseline revenue stream for the next six to twelve months, supporting much more efficient financial planning. Subscription models, for instance, offer customers goods and services for a recurring charge rather than a one-off investment. Similarly, consumption-based pricing strategies are following standard subscription models in spreading to other areas of business as a way of delivering value to the customer. There’s even an opportunity to combine subscription and consumption to balance predictability and flexibility.

What these tactics have in common is that they can deliver much greater certainty in future revenue than traditional one-off customer interactions. Businesses with subscription models can confidently predict a likely revenue range further into the future on the basis of historical user retention and real-time trends. Consumption-based pricing, likewise, incentivises ongoing custom and so levels out the peaks and troughs of revenue.

Combining these models with the right technology, such as automated revenue recognition tools, means that CFOs can accurately forecast revenue targets in real-time. For example, with access to a live view of the revenue being recognised by the business model across different geographies, they can be empowered to set targets with certainty while responding to market changes as they happen.

Whether it’s identifying causes of revenue changes or being able to proactively resolve variances in revenue recognition, they can shine a light on the landscape and plan accordingly. In turn, by responding to challenges and opportunities in real time, they can nurture stronger customer relationships, paving the way for brand equity that bolsters a more stable future forecast.

Again, it’s about finding that healthy balance: businesses can and should implement initiatives to react more quickly to changing conditions, and building the best internal workflows to turn investment into revenue is always an imperative. If they’re not also looking at how technology can clear a smoother revenue path ahead of the business’s progress, though, they are leaving a vital tool in the toolbox.

“Our systems and data are not performing as they should” is often a challenge met by frontline teams in investment, asset management risk-management, and, in fact, right across almost all functions in a bank or financial services firm when it comes to their company’s IT.

Senior executive teams should listen to them and examine more innovative approaches to data management, such as the Smart Data Fabric. Teams are frustrated because they can’t seize opportunities in the moment, making their own decisions based on evidence they can trust to deliver the right results.

Gaining better insight from many different types of data from both within and beyond the enterprise has become the new battleground in financial services. Excelling in a more unpredictable and much faster-paced world necessitates a culture of decision-making built on radically shortened time-to-insight. The rise of generative AI tools to augment human performance in financial services has also exposed the inadequacies of long-established and often ad-hoc IT set-ups.

Almost everyone in financial services needs faster time-to-insight.

But it is not just front-office revenue-generators who need insights from transactional and event data to heighten their performance and drive alpha.

Almost everyone does – from settlements, reporting and compliance to client relationship functions. They all need fast insights without relying on the expertise of scarce data scientists. The same is true for CFOs and boards, who want a more accurate, up-to-the-minute 360-degree view of performance, threats and opportunities, assets, and liabilities.

But it is not just about speed, it’s about data quality as well. To compete against more innovative competitors, financial organisations need clean, normalised and curated, timely data they can trust for faster, more informed decision-making and collaboration. Their portfolio management systems and other applications all need this higher quality of data – reliable, verified, and available in near-real-time. Predictive and prescriptive analytics offer huge gains in responsiveness and efficiency, but they, too, demand better management of data coming from inside and outside the organisation.

The problem is that traditional, heavily manual methods or ad-hoc technology stacks are no longer able to cope with the volume and complexity of data, nor the need for more sophisticated analytics in response to events and business questions.

A ‘smarter’ approach that works –the data fabric

As 2024 moves forward, organisations should adopt new approaches to bring all their data together quickly and simply so everyone can rely on it as a single source of the truth. To do so, they will turn to the data fabric – a more innovative IT architecture. The advantage of this approach is that it harmonises highly disparate data and makes it available without disruption or replacement of existing systems.

There are, however, many ways to implement a data fabric. One is to implement and integrate several different data management point solutions. But this is slow to deploy, difficult to maintain, lacks performance, and is inefficient in its use of infrastructure resources.

The smart data fabric is quicker to implement and simplifies data management.

The smart data fabric approach is preferable and has many advantages, providing the required functionality in one single product or platform. It can eliminate the errors and redundancies introduced by maintaining multiple individual data repositories that serve different consumers of the data.

Meanwhile, embedded analytics enable realtime advanced analytic processing without moving the data to a different environment. It is perfectly feasible to replace eight different technologies with a single product, gaining nine times better performance running on only 30% of the infrastructure, and with a far simpler architecture.

An independent asset manager with billions of dollars of equities and fixed income assets under management has found this approach delivers significant results after trying point-to-point integrations, platforms, data marts, data lakes, and more.

The smart data fabric has met the company’s demand for timeliness and consistency, serving the entire business and its clients. Portfolio performance has improved, as has client engagement and retention. Business users in the firm make more timely decisions, trusting the data they use. They can examine the data in as much detail as they require, answering the business questions that matter to them. The whole project has radically improved enterprise and client reporting.

The key point for senior decision-makers in the financial sector is that the smart data fabric delivers results – for lines-of-business users and back-office teams. The applications a financial institution or organisation uses are fed harmonised and trusted data, regardless of its original source of format.

In the current time of volatility and new opportunities, bottom-line performance depends on fast access to much higher-quality data than many organisations currently enjoy. As good as talented individuals may be, their performance will fail to deliver unless the financial organisations that employ them sort out their data management so they have timely access to accurate data and insights.

By transforming their approach through the smart data fabric, financial institutions are far more likely to emerge as decision-based organisations using data to be more agile, resilient, innovative, and profitable.

It’s fair to say that the last few years have been unpredictable, and the world’s economy has been turbulent. In such environments, it’s vital for businesses to be able to tackle any challenges that come their way: resilience will be the prerequisite for success in 2024. To remain successful, businesses will need to be agile and nimble – and that means using advanced tools like analytics and AI to prepare for the unexpected and to master the following four categories.

One way to mitigate against uncertainty is by mastering costs, compliance and cash flow. When costs are constantly changing and regulations are even more unpredictable, business leaders need to maximise the value of their budget and, importantly, have as much insight into expenses as possible.

Tools can help enforce travel and expense (T&E) policies by automatically reviewing every expense against companies’ policies and flagging anything that needs attention. This will help to speed up processes but also enable leaders to understand where processes and policies are working and where the business can save more money and time. In turn, this kind of automation frees up the finance team from repetitive tasks, enabling them to focus on higher value and strategic work.

In other areas, AI-based analytics can optimise costs, streamline compliance through regulatory technology solutions, and enhance cash flow management via automated invoicing and payment systems. This will allow businesses to improve efficiencies without having to worry about changing regulations and economic conditions, as financial leaders will already have all the data needed to make informed decisions in real-time.

It’s common knowledge that spending transparency is critical when it comes to assessing and amending budgets depending on new priorities. Having oversight on all your company’s spending is one thing, but in 2024, to have a competitive advantage, businesses need to go further than just seeing.

at their companies don’t have enough visibility into near-real-time employee spending data. Leaders need to not only understand exactly what is happening when it comes to spending but also have the ability to identify where the company can do better and what impact these improvements can make.

This can be achieved using the right technology, including advanced analytics to analyse data, specific reporting tools and pre-built ready-to-go dashboards. With such tools in place, business leaders can access the data needed to make better decisions, improve and optimise profitability and create more accurate forecasts.

As markets change, companies grow, and challenges crop up, it’s important to be flexible under any circumstances. With hybrid and remote working on the rise, organisations may be managing their spending with out-of-date tools, creating a disjointed and inconsistent experience for everyone and in turn, creating more manual work for each employee.

One way to improve efficiency is to have a single centralised technology solution that is easily scalable and works across a variety of locations and devices. Research from SAP Concur revealed that 78% of decisionmakers want a single solution to manage their entire travel and expense process.

With working patterns constantly changing, it’s equally valuable for IT, finance and HR teams to be able to access expert advice on any solution that they have in place. Having an alwaysavailable, 24/7 support desk can help leaders feel assured that their new policies and systems will work in the long term, no matter what issues arise.

Employee satisfaction is at the heart of every business, and prioritising their experience and retention is critical for success. However, too often cumbersome processes are blockers for productivity as they drain time and create frustration, with businesses missing the opportunity to take advantage of automation.

The key is to use the right intelligent technology solution to energise the workforce. Simplifying complex tasks and automating repetitive processes allows more flexibility, with employees able to focus on more important and creative work. A straightforward, streamlined process can also help an increasingly demanding workforce to feel satisfied and supported, even in their most day-to-day transactions.

This, in turn, will boost productivity and efficiency, benefiting not only the employees’ morale but also the profit margins of the business itself: a meta-analysis by the London School of Economics and Political Science found a substantial positive correlation between employee satisfaction and key performance indicators such as customer loyalty, productivity, and profitability. Businesses with higher levels of employee satisfaction saw increased customer loyalty and productivity, as well as decreased staff turnover.

When planning for the future, it’s important to remember that values are key and can’t be sacrificed, even in the most challenging business environment. While tools like AI have enormous potential to reshape business operations, it’s critical that these technologies are used in a mindful way that respects principles like data privacy and employee wellbeing.

Businesses should consider creating policies for their use of AI and other technologies and sharing these with employees for full visibility. It’s also important to work with long-standing technology providers who have developed extensive policies on the ethical use of AI and can be trusted to act responsibly.

In turn, businesses can then unlock incredible efficiency and personalisation in areas like travel and expenses, safe in the knowledge that data is being treated in a way that is both useful and compliant.

As 2024 unfolds, being able to adapt to the unpredictable at speed will be critical. Finance leaders will need to manage budgets nimbly, powered by data from across the business. Digital processes, powered by tools like AI, will be key –including in key areas like travel and expenses (T&E). With integrated systems, businesses can benefit from streamlined processes that can be adapted to new needs while supporting employee satisfaction and retention. This will help organisations to be successful, whatever 2024 brings.

2023 ushered in the next great wave of technology with the explosion of artificial intelligence (AI). It introduced major changes in the way we work and live with implications across all industries including customer experience (CX). John Willcutts, NICE’s general manager of digital and AI, said we saw good and bad things come out of 2023 concerning AI. What we experienced set the stage for 2024.

“2023 was the tidal wave of large language models. It exposed what was possible, and it led to a lot of organizations doing internal soul-searching on how best to deploy,” said Willcutts.

NICE, a leading global customer experience technology provider, was the first in the CX industry to integrate ChatGPT generative modeling into its AI solutions in 2023. Willcutts said LLMs (large language models), which were a large part of the AI advancements in 2023, are a piece of a larger puzzle. LLMs alone can’t transform financial institutions’ (FI) AI strategy, he said, but they play an important role.

“We're seeing organizations realizing they're going to need vendors that have a holistic approach to the entirety of the life cycle of both AI and the platforms it takes to deliver consistently for their customers,” said Willcutts. “So really large language models kicking off the tidal wave was the icing on the cake, if you will, to truly take customer experience to the next level.”

A study done by McKinsey Global Institute estimated that generative AI could add $200 billion to $340 billion (equivalent to 9 to 15 percent of operating profits) in value to the banking industry. McKinsey attributed this largely to anticipated productivity increases from the use of AI.

Willcutts said if FIs want to implement CX AI, there are some steps they can follow.

Here is what he said is the formula for successful CX AI implementation:

• Interaction-centric cloud platform: FIs need to store all their CX data on a single, open cloud platform. This is the first step to being able to fully realize the benefits of CX AI. It breaks down the silos that exist within organizations to be able to give AI the access it needs to generate holistic insights into CX operations. This also eliminates the complex tech stack that many FIs are saddled with.

• Purpose-built AI: AI should underpin FIs’ cloud platform, but not just any AI. Purpose-built AI is built from billions of recorded customer interactions and designed with the proper guardrails in place to ensure accurate and appropriate outputs. LLMs add the layer of semantics on top of AI outputs, translating the outputs into clear and conversational responses. This has changed the way FIs can interface with their CX data. This also transforms the level of service that FIs can provide through chatbots. If FIs implement AI the right way, customers will not be able to tell whether they are talking with a chatbot or human agent.

Willcutts said AI is transforming both agent-assisted and unassisted customer interactions. He said this goes for any organization including FIs. It also greatly improves the handoff between the two.

“What’s so important is that if you take one holistic platform and embed the automation and AI capabilities over the top, you never lose context between what used to be siloed,” Willcutts said. This means if a customer inquires about a credit card through an FI’s website and is transferred to an agent to start the application process, the agent will already know everything the customer has done up to that point. So, they don’t have to waste time getting the customer to answer the same questions again.

Data security continues to be a hot topic for FIs looking to implement AI. 2023 ushered in so many different vendors for FIs to choose from, it’s become difficult for FIs to decipher which is the right AI for them. Willcutts said that if FIs follow the formula of an interaction-centric platform underpinned by purpose-built AI, they can solve one of the top concerns with AI: bad or biased answers.

“If you have a source of truth that's developed on a single platform, you can apply that consistently across all the channels. If you do that, then you get the right answers every time with the right context written in a way that the organization would normally speak,” Willcutts explained.

A recent survey done by Omdia and NICE found that 76% of FI CX leader respondents reported that they are using generative AI to formulate responses to customers’ inquiries. It supports the idea that AI can be a powerful tool to quickly generate accurate responses to incoming

Willcutts said if FIs inject purpose-built AI into their CX operations, this will have ripple effects across the organization. He said this will make the employee experience more enjoyable thus boosting the ability to retain employees long term.

“We're going to make the agent’s job so much better, something they're going to want to do. It’s human nature to feel guilty not knowing the answer to something. That gets amplified in the customer service world because agents know when they don’t have the answer which makes a customer very angry. Now with purpose-built AI, they have the right answer at their fingertips,” Willcutts observed.

The study done by Omdia and NICE also found that of the FI agents surveyed, the number one negative aspect of working in a contact center is customer emotion and behavior, i.e. anger, rudeness, etc. FIs can resolve this with purposebuilt AI.

2024 will be the year that things come into focus better with AI, concluded Willcutts. “It’s no longer about just having AI for the sake of AI. FIs have the chance to be purposeful with what AI they choose to use. This will be the single most important factor in determining whether they reap the immense benefits AI can produce for an organization. The right technology is out there, it’s up to FIs to make the right decision.“

John Willcutts General Manager of Digital and AI at NICE

John Willcutts General Manager of Digital and AI at NICE

Absa Bank Limited is part of Absa Group, with a presence in 12 countries across the African continent. Absa’s ambition is to sustainably create shared value and play an integral role in the life journey of customers and clients, empowering them to achieve more and to recommend Absa family, friends, and business associates. Absa aspires to be a truly purpose-led organisation by making a positive contribution to the wider world, putting its purpose at the core of everything it does. Absa is at the forefront of modern banking technology with state-of-the-art digital integration, as well as being established as a key part of South African society with branches across the nation.

Absa Bank Limited received numerous honours at the 2024 Global Banking & Finance Awards for South Africa, including Best Bank Management Team, Best Digital Bank, Best Digital Wallet, Digital Banking Customer Satisfaction & Happiness, Excellence in Innovation - Digital Colleague Onboarding, and Best Use of Biometrics by a Bank in South Africa. Also, Absa IdeaLab was awarded for Excellence in Innovation – Digital Engagement Platform. Absa IdeaLab, designed, developed, and hosted by Absa’s Digital Product team, is an internal idea submission platform, as well as a knowledge transfer tool.

To find out more about the bank’s continuing success story, Global Banking & Finance Review’s Philip Fothergill spoke to Mr. Subash Sharma, Chief Digital Officer at Absa , Everyday Banking, and congratulated him on Absa’s extensive roster of awards.

“We're really proud of this particular achievement,” said Mr. Sharma. “It's a testament to all the colleagues who work within Absa , coming together and producing the goods to be able to earn these esteemed awards.”

With a solid background in mechanical engineering as well as business leadership, Mr. Sharma’s experience and expertise lend themselves to a strategic vision that drives digital innovation. “Our innovation is always commercially led; we look for commercial outcomes and we put the objectives that we are trying to meet ahead of everything else,” he explained. “We don't believe in doing innovation for the sake of innovation. Rather, it’s about how we use innovation to create results. I guess my technical background is an enabler to this, but as a leader, what I focus on is creating a culture of innovation that is not just one-dimensional, but an entire environment of colleagues coming together to be able to produce these commercial outcomes.”

Absa has been on the front line of integrating biometric technologies for enhanced security, and Mr. Sharma went on to discuss the strategic importance of this technical innovation and its impact on customer trust and banking security.

"Security has become a competitive advantage for Absa. We look at biometric security in particular, over and above all the different aspects of what we call a security layer,"

- Mr. Subash Sharma

“This has helped us in two ways. One, we provide the only Digital Fraud Warranty in our market. So, in other words, for any fraud that occurs for a customer while transacting digitally, we provide a money-back warranty. We would not be able to provide that warranty had we not had the confidence in our fraud and security capabilities, of which biometrics is one of the key components.

“The second is when we look at onboarding a customer, verifying the customer, or operationally, doing things like PIN and password resets. Our vast biometric capabilities allow us to conduct these operations digitally, end-toend, without the need for human intervention. So, in both aspects, biometrics plays a significant role in providing us with a competitive advantage in the marketplace.”

Among the innovations and services Absa provides is the Absa IdeaLab. “As I said before, creating a culture or environment where innovation thrives is critical, because we don't believe innovation happens in the mind of one or two individuals,” Mr. Sharma asserted. “The IdeaLab was created as a platform that allows colleagues from across the bank, even across the continent, to be able to log their ideas and have project teams build on those ideas, have other people vote on them and build them up into something that can be taken to market. The IdeaLab also provides employees and colleagues with access to learning materials, innovation materials, innovation techniques, presentation skills, pitch skills, the ability to create business cases. So, it fosters an environment of alwayson innovation, and this culminates in various hackathons that we hold throughout the year where we take the best ideas, build on them, and then take them to market.”

Given the largely digital world we now live in and how digital banking is rapidly evolving, Mr. Sharma offered his perspective on how Absa maintains its competitive edge and the big upcoming trends in digital banking that it plans to accommodate.

“We see people moving away not only from cash, but also in some cases from cards,” he said. “The adoption of digital wallets is becoming quite prevalent. We see digital currency, the world of the metaverse, and AR and VR also becoming key trends. In our view, as digital becomes the centre of a wide variety of banking products and services, the use of AI and GenAI is becoming a significant trend, particularly in terms of conversations and chat. The way we believe we need to set ourselves up and be competitive going into the future is by not only focusing on creating technical skills or technical capabilities, what we call ‘table stakes.’ We also look at enhancing and creating new digital products that are born digital. An example of this is our ChatWallet , which we have recently launched and is the first of its kind in the world.”

On the digital transformation journey, improved customer relations and satisfaction go hand-in-hand with security. Mr. Sharma shared an example of digital innovation directly enhancing customer service that underscores the importance of earning customers’ trust.

“With the trend of digital migration, we believe that fraud security has become vital,” he said. “In the lives of our customers, there is nothing that creates more anxiety than that feeling of being defrauded, the feeling of not being secure, the feeling of losing your hard-earned money. What we have created in our digital capability, over and above the warranty that we provide our customers, is the assurance that should anything happen, we are the safety net to make sure that your money is protected”.

“As a group, our ESG strategy is quite significant,” he said. “We have three main goals and areas that we’re focusing on. First and foremost, we want to promote financial inclusion; second, we want to make sure that we promote diversity and inclusion, and third, we need to make sure that we do this in a climate-sensitive and environmentally friendly way.”

- Mr. Subash Sharma Suella Derman Head of Risk, Digital

Suella Derman Head of Risk, Digital

“We have created a security hub within our digital estates that allows customers to monitor whether they are being spoken about on the dark web, and whether their security credentials or personal data are being shared. They can be alerted should these activities be happening. We then provide them with the capability to secure themselves, not only from a banking perspective but in their daily lives. I think in helping our customers manage these things, we have found a better relationship between what the bank does and the needs of the customer.”

With sustainability being such a watchword these days, Mr. Sharma pointed out how increasingly important it has become for Absa to ensure that its digital growth is sustainable, both in terms of business and its impact on society and the environment.

Mr. Subash Sharma Chief Digital Officer Absa, Everyday BankingFurthering the topic of inclusion, he went on to describe the ChatWallet platform, Absa’s all-in-one banking solution that allows customers to bank freely. “There are no recurring monthly charges associated with ChatWallet , and customers are able to get access to a bank colleague by simply having a conversation on WhatsApp. What this does is reduce the barrier to entry and promote significant financial inclusion amongst those who currently don't have bank accounts. This is one particular example of how we, as digital innovators are providing opportunities for financial inclusion. And in all of the themes that we’ve spoken about in terms of our strategy, digital is a significant contributor.”

Mr. Sharma concluded by highlighting a number of key strategic initiatives that Absa is focusing on to further strengthen its position as a leader in digital banking.

“If we look at the trends, we see significant work being done in the adoption of wallets, and we through our API marketplace and our wallet products that we have launched in the market are at the forefront of these particular trends. We are also at the forefront of the security trends that we see playing a significantly more vital part in the digital landscape of financial services. With the combination of both our digital and business capabilities, what we are doing now is to ensure that we design products and services that are born digital, are fit for purpose, and meet the needs of our customers not only for today, but as part of the evolving landscape of our country and our continent.”

Aligned Green, Social, Sustainability, Sustainability-Linked and Transition (ESG bonds or GSS+) finance volumes passed the $4trillion mark in H1 2023, according to the Climate Bonds Initiative (CBI). But how green is green? And how confident are fund and asset managers about the quality and integrity of the data required to support Environmental, Social and Governance (ESG) fund management decisions?

There is widespread consensus that climate change is impacting the profitability of financial institutions, hence it is imperative to not only deploy the appropriate risk model, but also to gather and maintain accurate data to ensure that transition and physical risks can be effectively monitored. The respective roles of Risk and Compliance officers are therefore evolving, as they’re tasked with ensuring data availability, quality, and governance to fulfil disclosure obligations, while also monitoring and assessing risk within portfolios. The current regulatory landscape necessitates the management of both compliance and ESG-risk exposures, with increasing scrutiny in the face of greenwashing allegations. The nuances of data have never been so key.

With a better approach now vital, Maria Vigliotti, CEO at Fidata and D2 Legal Technology’s Akber Datoo and Elliot Curtis discuss the power – indeed, necessity – of technologies which enable financial market participants to have a common ESG understanding and support greener investment decisions. Is this the moment for AI?

Analysis from McKinsey estimates that the investment in new infrastructure and systems needed to meet international climate goals could be $9.2 trillion a year annually through 2050 – a figure estimated to be at least $3.5 trillion more a year than the current level of investment in both low-carbon and fossil-fuel infrastructure and changes in land use.

The EU is leading the world in its commitment to achieving change and the financial services market is recognised as a vital element in driving the fight against climate change. The SFDR is key to achieving the level of investment required to support innovation and compel companies to evolve towards more sustainable operations. It is fast-becoming the pre-eminent financial regulation in respect to combatting greenwashing, building on the work already done at the retail/product level to hold companies to account for all their activities.

However, the lack of trusted data and inaccurate risk modelling remains a massive concern that is without a doubt constraining the pace of ESG-led change. Compliance and Risk officers are the custodians of regulatory compliance, yet this is a transition which cannot be achieved without the correct technology enablers. If the investment industry is not confident in the quality of data or, critically, able to make valid comparisons between business ESG performance, global opportunities to deliver on environmental strategies will be lost.

Under the European Union’s Sustainable Finance Disclosure Regulation (SFDR), which imposes mandatory ESG disclosure obligations for financial markets participants, fund and asset managers are required to provide more detailed disclosures to justify the categorisation of their light green Article 8 (environmental and/or social characteristics) and dark green Article 9 (environmental and/or social objectives) funds. Yet a lack of confidence in data, combined with the use of multiple different standards, raises fears about non-compliance, leading some to rebrand dark green funds as light green simply to mitigate the risk of punishment. While article 8 and 9 funds are making waves in the ESG investment sphere, the risks associated with regulatory non-compliance threaten to ultimately undermine sustainable investment.

A lack of consistent data is somewhat inevitable given the immaturity of the ESG market. However, adding to the problem is the arrival of multiple, incompatible standards and frameworks that are making it incredibly difficult to confidently compare the performance of ESG bonds. Are companies measuring their performance based on the Climate Bond Initiative’s (CBI) Climate Bonds Taxonomy, the EU’s taxonomy for sustainable activities or the International Capital Market Association’s (ICMA) Green Bond Principles?

Each of these – and there are many others evolving across the world – sets out a framework for disclosing and reporting on ESG bonds, but each has a different set of requirements which make it very difficult, time-consuming, and expensive to truly understand comparative performance and climate risk.

This problem affects every part of the hugely complex and diverse ESG-led investment concept. Take the area of buildings renovation to reduce carbon emissions, for example. The CBI requirements will demand different approaches depending on whether the building is new or old, commercial or residential, and where it is located across the world. This requires a significant amount of work to assess different impacts in France, for example, compared to Australia.

An alternative approach could be to adhere to the ICMA model, which simply considers the site and the carbon reduction level. Meanwhile, the EU taxonomy demands adherence to the relevant national standard legislation. In some cases, this will allow the creation of an Environmental Performance Certificate (EPC) without the need to measure carbon reduction. While each approach is legitimate, they are significantly different. So how are fund and asset managers to confidently make comparisons between bonds?

In theory, the problem could be resolved if a fund’s risk model required reporting to all three standards, but the cost would be prohibitive given both the lack of skilled resources in this nascent area and difficulties in securing relevant, consistent data. Essentially, while the thinking behind each taxonomy and model is laudable, the existence of multiple standards is creating significant barriers to progress in a vital area of investment.

Consistency is essential if the ESG bond market is to fulfil its potential. Risk and Compliance officers need to establish rigorous data governance frameworks and structured methodologies to enable the effective comparison of performance and risk. Using the right taxonomy, it is possible to overcome the fragmentation and provide valid information that not only supports fund management decisions, but also compliance with regulations such as the SFDR.

Today, fund and asset managers are rightly nervous. They are concerned about the reputational risk and the real prospect of fines for SFDR non-compliance and, as a result, there are increasing reports of billion-dollar downgrades, where dark green (Article 9) funds are being downgraded to light green (Article 8) as part of a risk mitigation exercise. This is ultimately undermining the value of ESG activity, and clearly illustrates the current issues being faced in the realm of compliance risk.

It is time for Compliance and Risk officers to find better ways to measure and compare performance, while accurately assessing climate risk to portfolios. This is the time for systems which will be able to algorithmically traverse across these differing standards and frameworks, assessing, cleansing, standardising, and only then utilising the data to make the right decisions. Doing this at scale necessitates complex algorithms combined with a deep understanding of this area of ESG. A number of AI approaches, including Natural Language Processing (NLP) and ESG machine learning classifiers for accurate prediction of risk, are being developed. In relation to the Task Force on Climate-Related Financial Disclosures (TCFD) for example, ClimateBERT, a deep neural language model, has analysed the disclosures of TCFD-supporting firms and was able to conclude that firms have tended to cherry-pick to report primarily non-material climate risk information. While ClimateBERT has helped to highlight trends in climaterelated disclosures, AI technologies will be of limited use in the absence of accurate and more broadly, appropriate data governance.

The EU is at the vanguard of sustainable investment and, as such, the world is watching. Greater international consensus is clearly required to accelerate investment in innovative ESG activity and that will only be achieved when fund and asset managers globally have the data, methodology and systems required to confidently discharge their responsibilities.

Now must be the time to implement the right methodologies and systems, or the threat of fines will become a reality as regulators continue to adopt a hard-line approach to greenwashing. But now is not the time for investment funds and asset managers to dial back. It is essential to move the dial on sustainability-driven activity and the market opportunity is enormous. Fund and asset managers that proactively embrace a methodology that brings together different standards and data sources will not only safeguard SFDR compliance, but also achieve new levels of investment clarity.

Steve Croke Chief Technology Officer for Financial Services at GlobalLogic

Steve Croke Chief Technology Officer for Financial Services at GlobalLogic

Steve Croke is the CTO Financial Services at Globallogic, a Hitachi company. In this role, he drives the technological vision and strategy of the Financial Services Business Unit, designing innovative, relevant solutions and providing technology direction to key clients. He has over 30 years experience in Financial Services Technology and has worked extensively throughout North America, South America, Europe, and Asia.

Prior to joining Globallogic, Steve held senior technology roles at HSBC, NatWest, and Discover Financial Services. These included overseeing the delivery of a new Core Banking system for HSBC and heading up the Core Banking and Payments Technology divisions for NatWest, one of the UK’s largest banks. He is passionate about developing high-performing teams and embracing innovation.

GlobalLogic is a leader in digital engineering. We help brands across the globe design and build innovative products, platforms, and digital experiences for the modern world. By integrating experience design, complex engineering, and data expertise—we help our clients imagine what’s possible and accelerate their transition into tomorrow’s digital businesses.

Headquartered in Silicon Valley, GlobalLogic operates design studios and engineering centers around the world, extending our deep expertise to customers in the automotive, communications, financial services, healthcare and life sciences, manufacturing, media and entertainment, semiconductor, and technology industries. GlobalLogic is a Hitachi Group Company operating under Hitachi, Ltd . (TSE: 6501), which contributes to a sustainable society with a higher quality of life by driving innovation through data and technology as the Social Innovation Business.

Steve Croke, Chief Technology Officer for Financial Services at GlobalLogic, explains how the financial sector has the potential to be an essential vehicle for the net zero journey

Climate change affects the physical environment, threatening all aspects of natural and human systems, and directly contributes to humanitarian emergencies. With 3.6 billion people already living in highly susceptible areas, between 2030 and 2050, it is expected to cause around a quarter of a million additional deaths per year.

According to the UN, we are at a critical moment for humanity; the window to limit dangerous global warming and ensure a sustainable future is quickly closing.

Yet, despite overwhelming scientific evidence and decades of campaigning against fossil fuels, the world’s biggest 60 banks have financed expansion operations in the industry by a staggering $3.8 trillion since 2015. It’s time for the financial sector to change and lead a different kind of charge–climate activism.

The global financial sector’s commitment to net zero is beyond question. At COP 26, over 450 financial institutions in 45 countries pledged to contribute to the goal of limiting greenhouse gas emissions . In its 2023 Progress Report , this coalition – known as the Glasgow Financial Alliance for Net Zero (GFANZ) – showed growing participation and tangible momentum across key metrics.

However, banks need additional funding and facilitation to transition to low-carbon options. This takes investment into new technology and altered business practices, which raise risk-related red flags and complications around third-party management and data limitations.

Investors, stakeholders and customers compound pressure by demanding accountability over fair, transparent and secure conditions that prioritise their interests. All of this hinders banks from taking action.

Rather than battling headwinds, banks must align on global climate initiatives and create supporting tailwinds with new policy. That was the rallying cry of ESG expert Abyd Karmali , Bank of America’s managing director of ESG and sustainable finance at Sibos 2021 –a sentiment I share.

We’re starting to see real progress with initiatives like Sibos that enable ongoing conversations between regulators and industry and drive best practices. Still, change only happens when people want it to.

NatWest , under its previous climate advocate Chief Executive, Alison Rose , put words into action. Not only did it sponsor COP26, but the bank is making strategic moves. In an effort to cut back on fossil fuel exposure, it pledged £100 billion for sustainable energy projects by 2025 and phasing out all global coal-sector lending by 2030. We’ve seen similar pledges from other banks, such as Lloyds and HSBC

We’ve also witnessed a wave of green-inspired technologies—for example, the app calculator Sugi tracks and compares individual investments’ annual carbon impact. The cloud-based software service Doconomy Åland Index API enables the tracking of CO2 emissions across every consumer transaction.

The latest ESG regulations emphasise measurability and accountability, which removes ambiguity around sustainability goals. It’s also a nod to the vast amounts of data financial institutions hold. This data provides a wealth of information about consumption patterns and preferences and is vital to furthering the green agenda. However, banks can only drive transformational change if data is unified and used correctly– this is where enterprise tech solutions come into play.

Recognising the need to organise and unify hundreds of data sources, ranging from legacy, host and technical debt, GlobalLogic has, for instance, helped develop the architecture to support an in-house data model capable of sourcing, storing and evaluating all data. This repeatable and scalable model produces real-time reporting for regulatory obligations and banking customers and is successfully in use at a top five UK bank serving 19 million customers annually.

The risk to an investment portfolio is dependent on economic and environmental changes. In a recent use case, GlobalLogic established a framework, building out processes and controls to evolve our client’s choice of data model into a sophisticated analytics tool. Assessment of environmental factors before lending, investing or insuring decisions was consequently made possible.

These and other innovative solutions help to further the net zero agenda in the industry, but enterprise tech solutions are only part of the picture. It is through the alignment of advocacy, policy, and engagement efforts that financial institutions will ultimately power the green transition and lead a different kind of charge–transformational climate change.

The financial ecosystem is currently experiencing a remarkable evolution, triggered by technological progress and novel trends that are redefining traditional payment practices and consumer habits. These innovations range from contactless and mobile payments, instantaneous transactions, open banking, Machine Learning (ML), biometric authentication, Web3, and IoT, all of which are reshaping our business operations and visions for future commerce. These tech advancements serve more than just problem-solving purposes; they add immense value to businesses, giving them a competitive edge in the marketplace.

We are witnessing a significant shift towards a cashless society, driven by the convenience, speed, and security that digital payments offer. As we continue this journey, it’s crucial to balance the benefits these technologies bring with their potential societal and environmental impacts. In this article, we delve into the progression of payment systems and their repercussions for businesses, financial institutions, and consumers.

Unquestionably, the Covid-19 pandemic has been a catalyst for the digitalisation of payment solutions, leading to a worldwide increase in digital payment usage.