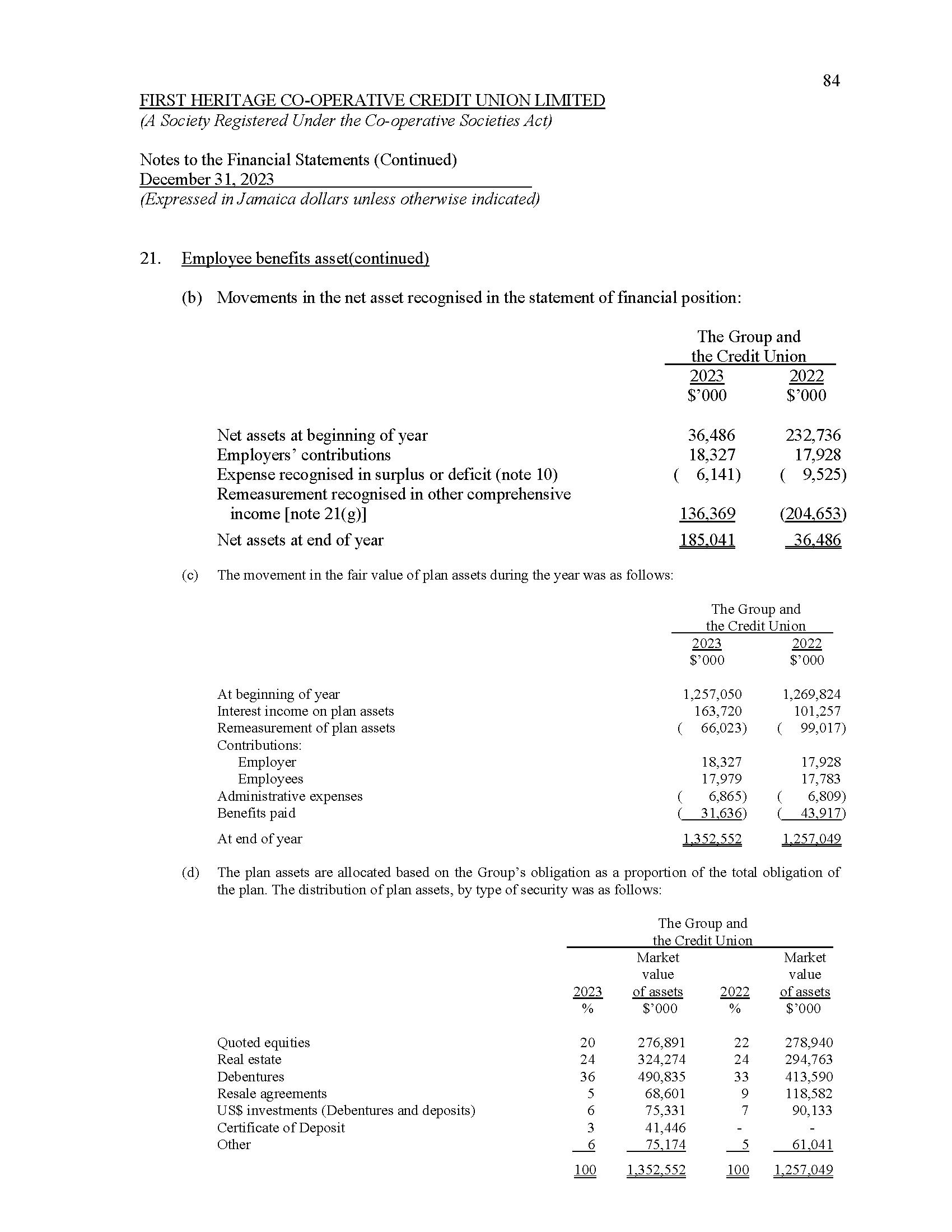

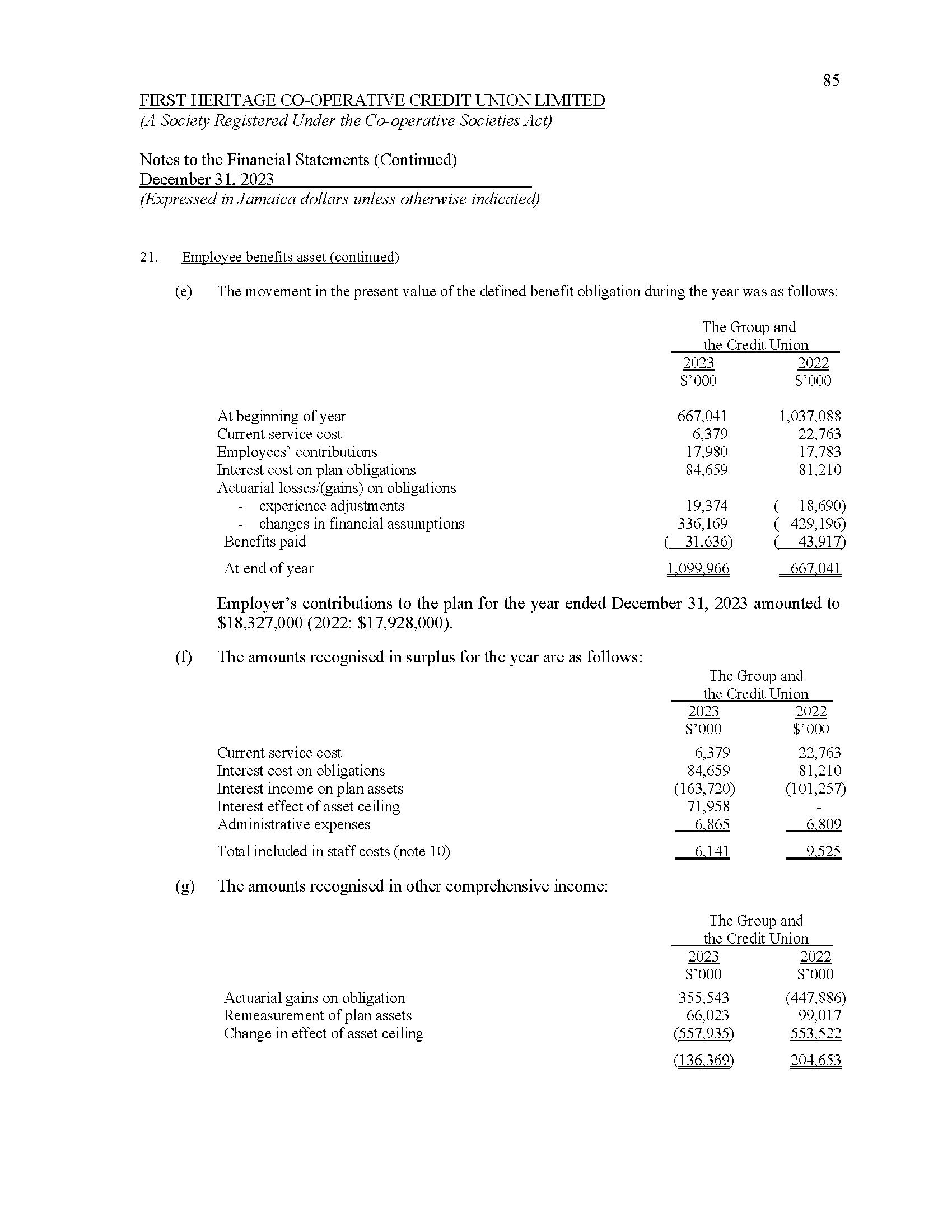

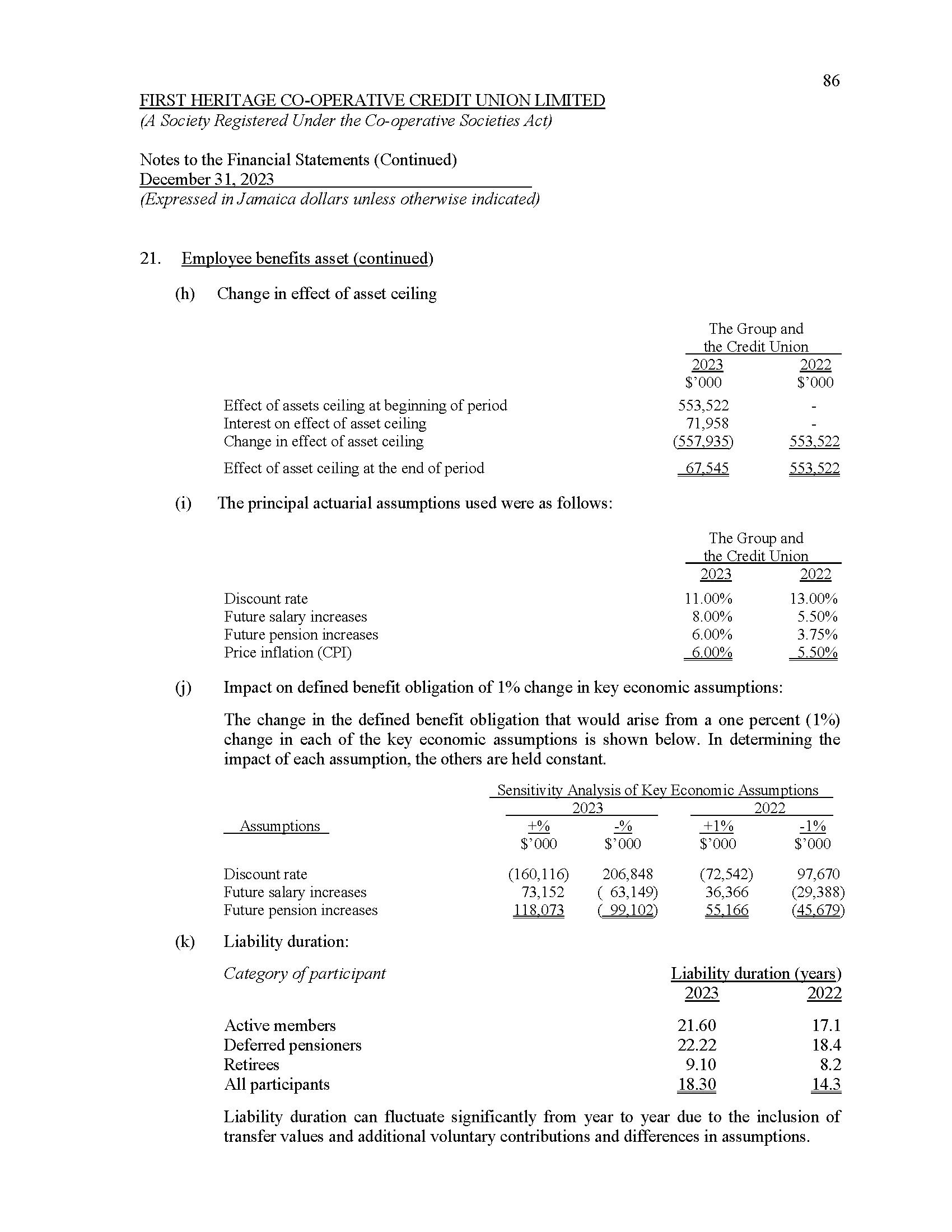

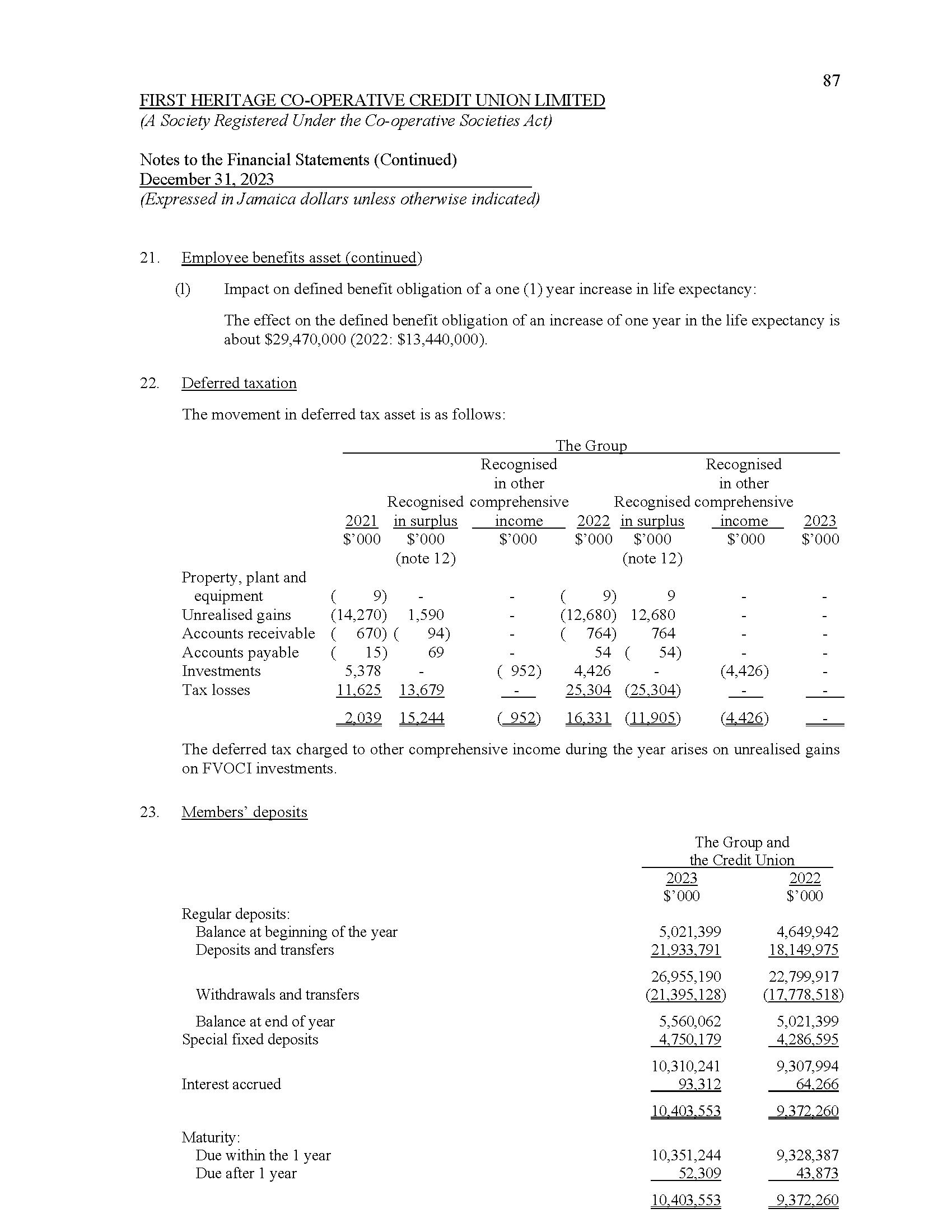

First Heritage Co-operative Credit Union - Annual Report 2023

NOTICE OF ANNUAL GENERAL MEETING

Notice is hereby given that the 12th Annual General Meeting of First Heritage Co-operative Credit Union Limited will be held in a hybrid format on Monday, September 9, 2024 commencing at 2:00 p.m. Remote access will be facilitated via the Zoom platform and a limited number of members will be hosted at The Jamaica Pegasus Hotel, 81 Knutsford Boulevard, Kingston 5.

Instructions for Attendance

Members attending physically or virtually are invited to register using the appropriately labelled link on our website https://www.fhccu.com/agm.

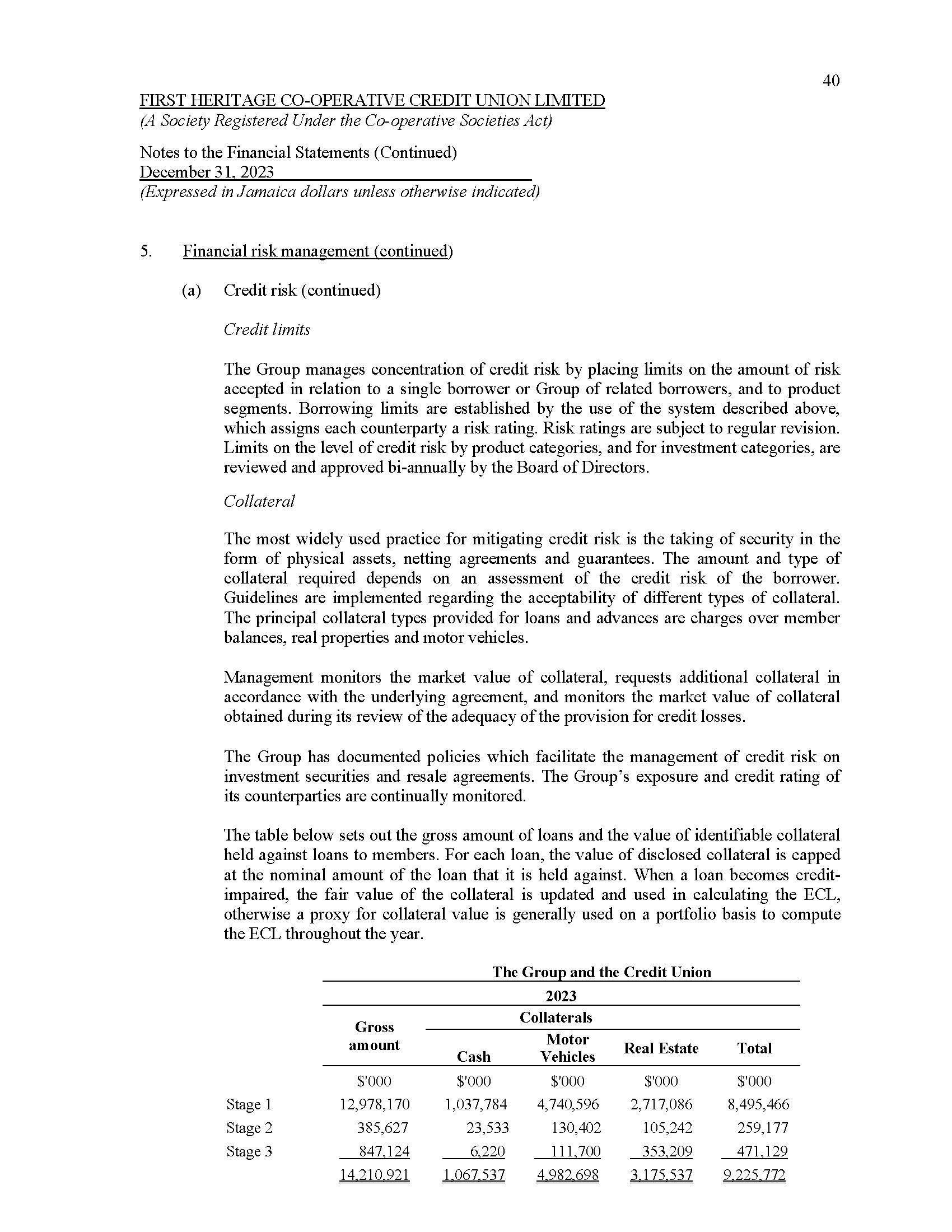

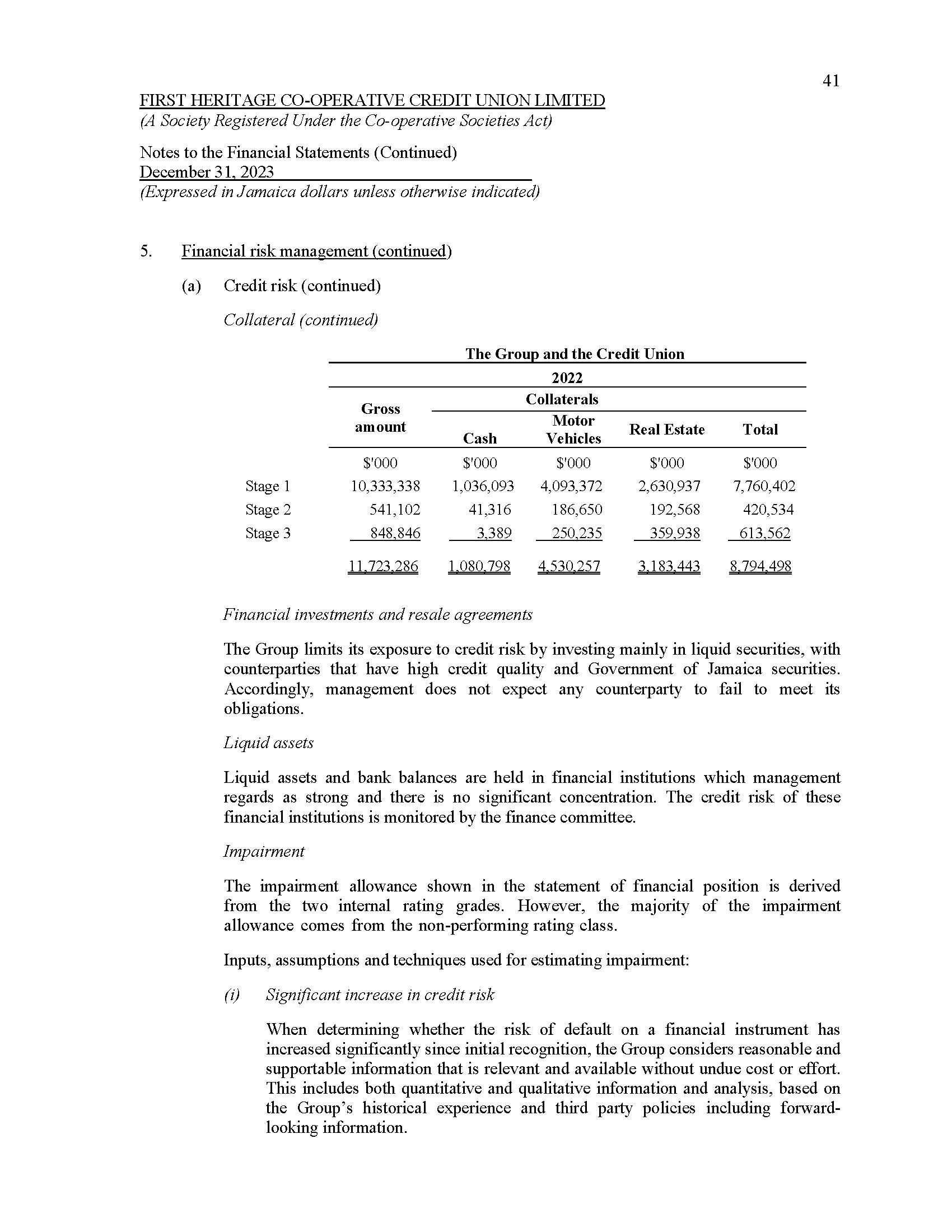

Registration is now open and will close on Thursday, September 5, 2024 at 11:59 p.m.

For more information on attendance, registration and the voting process, you may email us at info@fhccu.com, call our Member Contact Centre at 876-929-5142 or WhatsApp us at 876-551-8193.

Dated the 26th day of August, 2024

Nickeisha Walsh Secretary, Board of Directors

Ascertainment of Quorum

Call to Order and Prayer

Chairman’s Opening Remarks and Tributes

Reading and Confirmation of the Minutes of the 11th Annual General Meeting held on Wednesday, September 6, 2023

REPORTS:

Board of Directors

Management

Treasurer and Auditors

Supervisory Committee

Credit Committee

ELECTIONS:

Nominating Committee Report

Elections to:

Board of Directors

Supervisory Committee

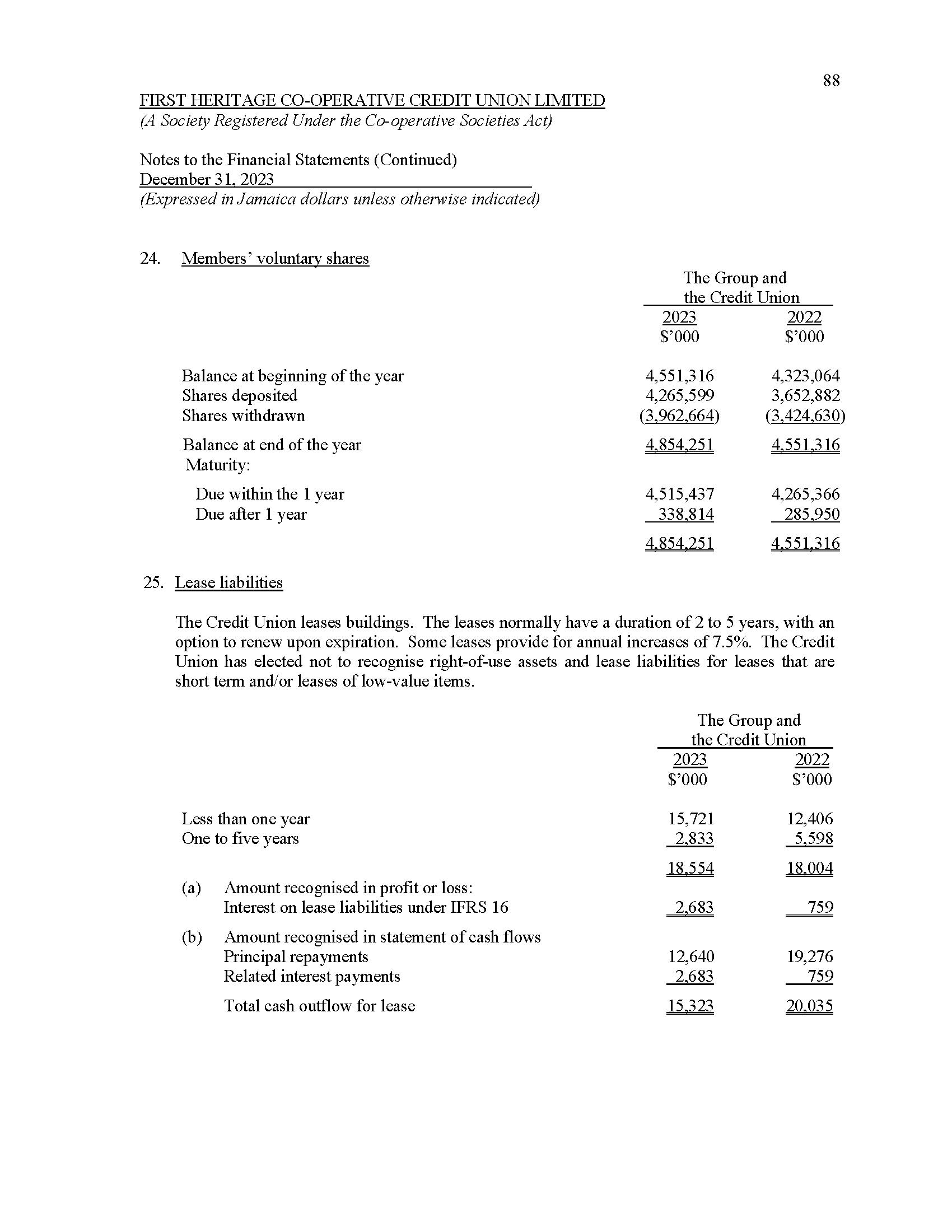

Credit Committee

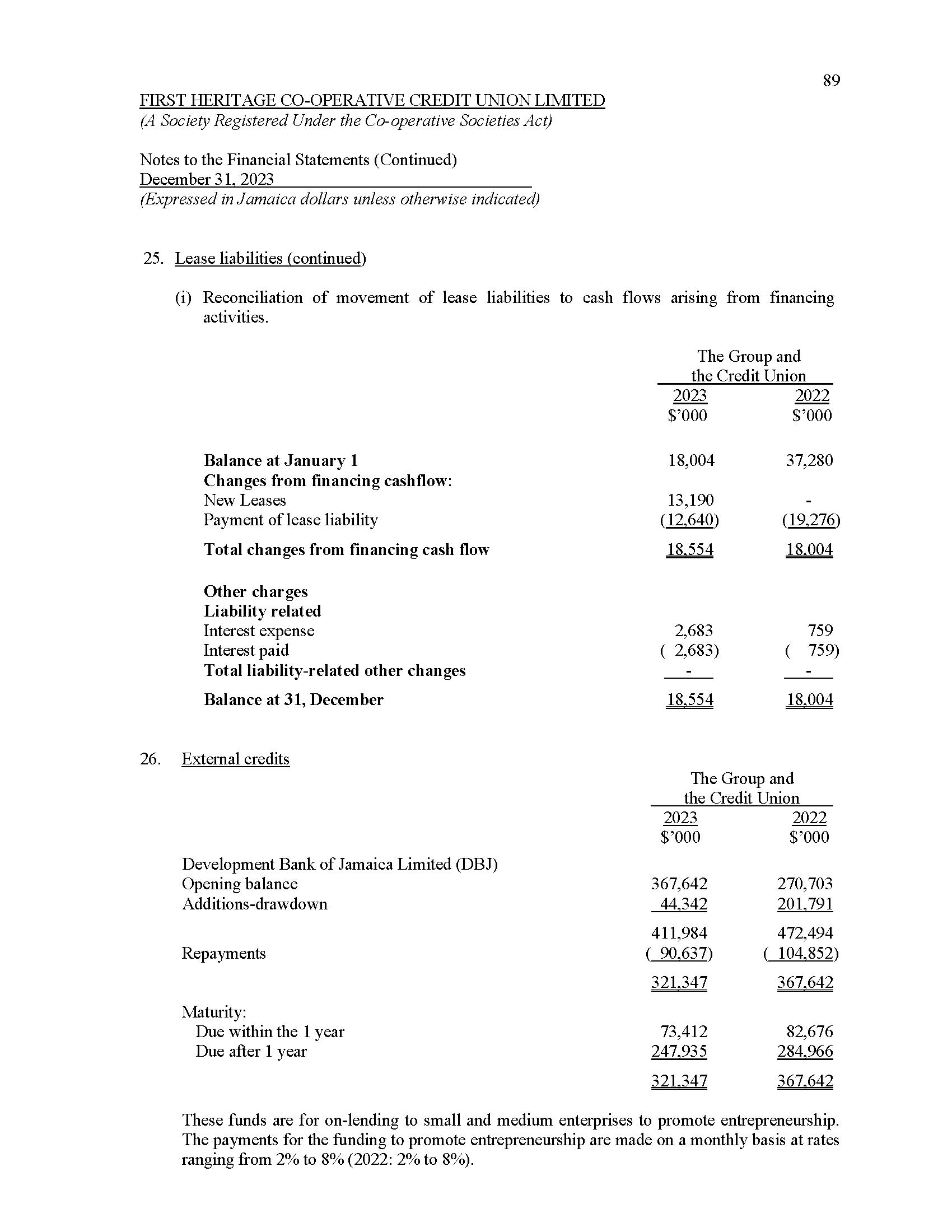

Any Other Business

Vote of Thanks

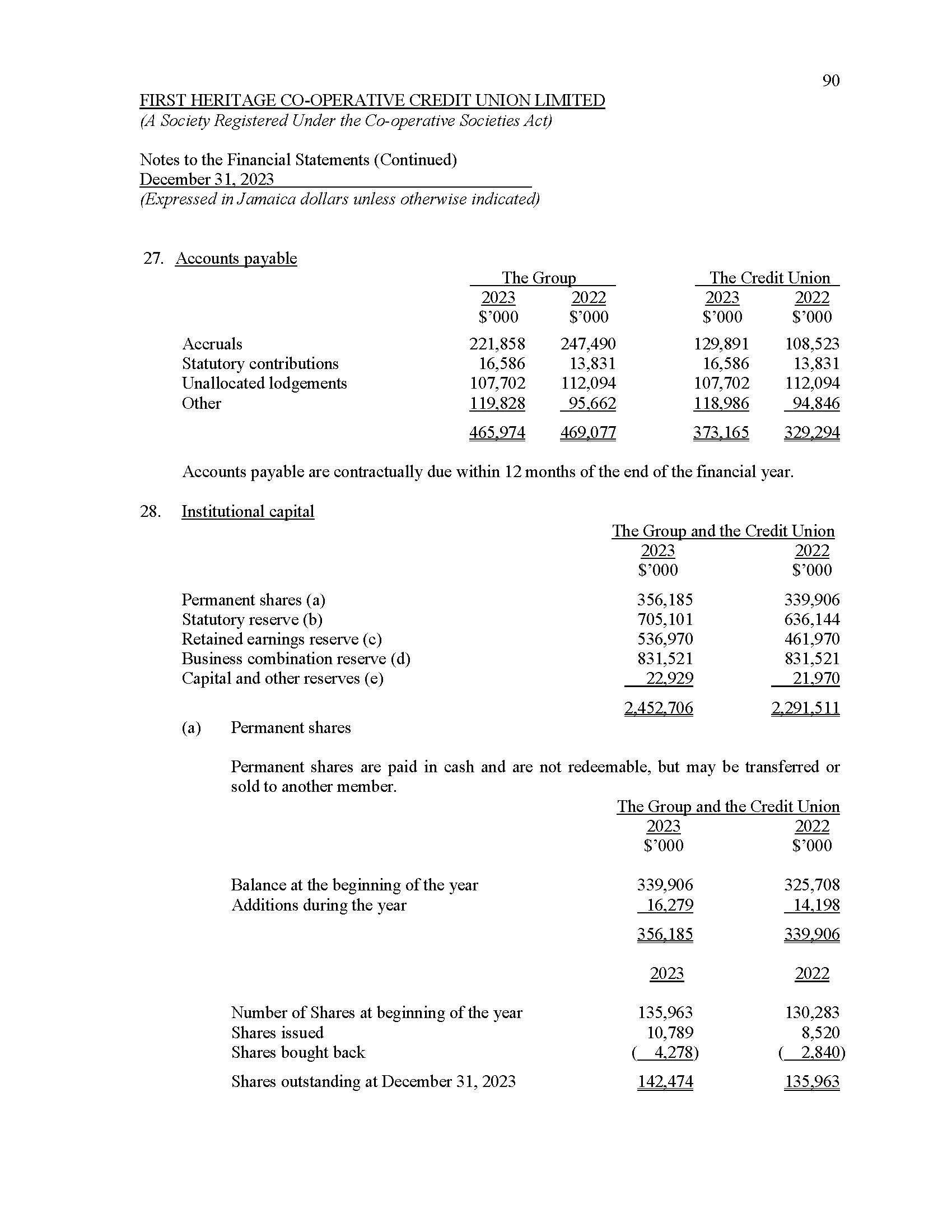

Termination

PROFILE - FIRST HERITAGE CO-OPERATIVE CREDIT UNION LIMITED

First Heritage Co-operative Credit Union Limited (FHC) was formed on August 1, 2012, from the merger of GSB Co-operative Credit Union Limited and Churches Co-operative Credit Union Limited. On March 1, 2015, the business and operations of St. Thomas Co-operative Credit Union Limited were transferred to FHC.

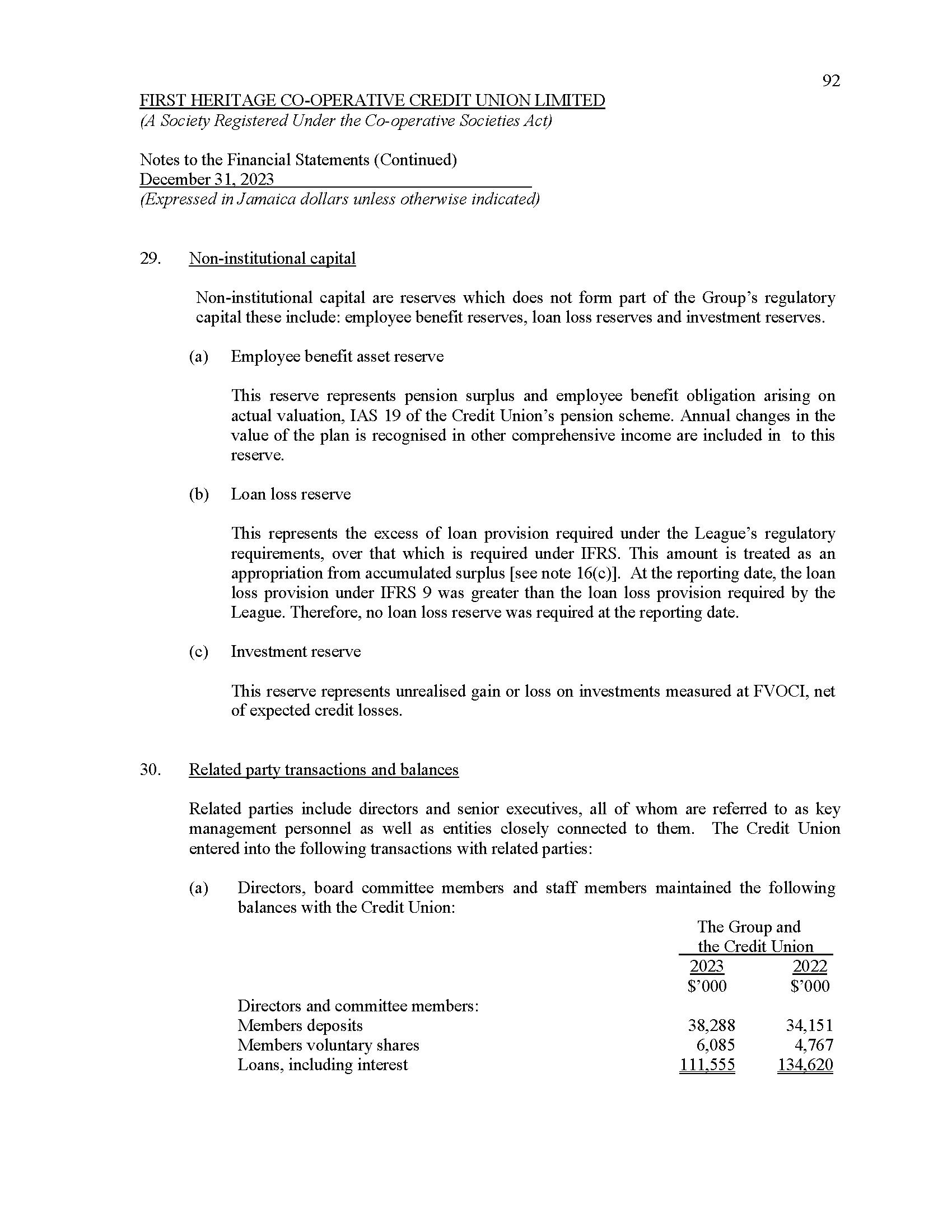

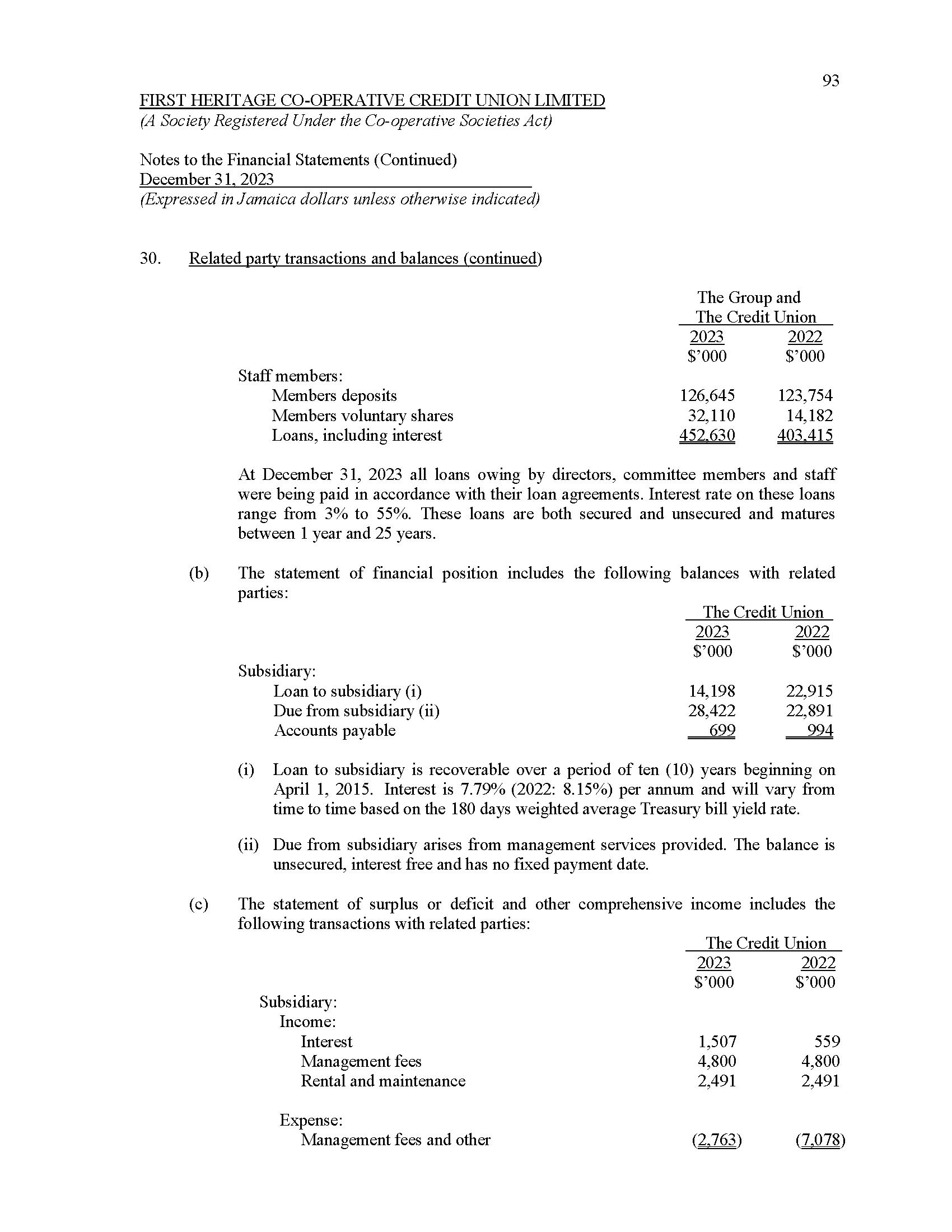

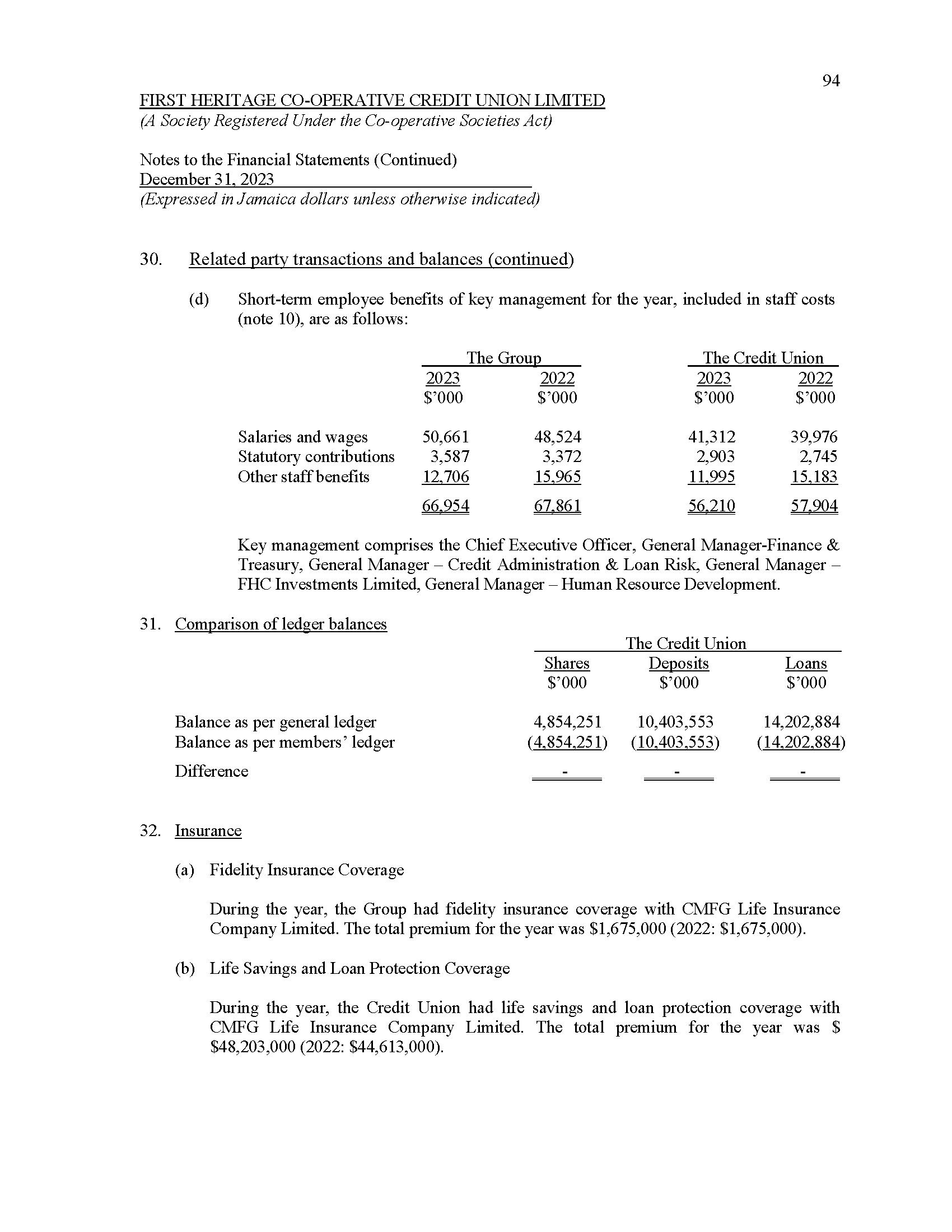

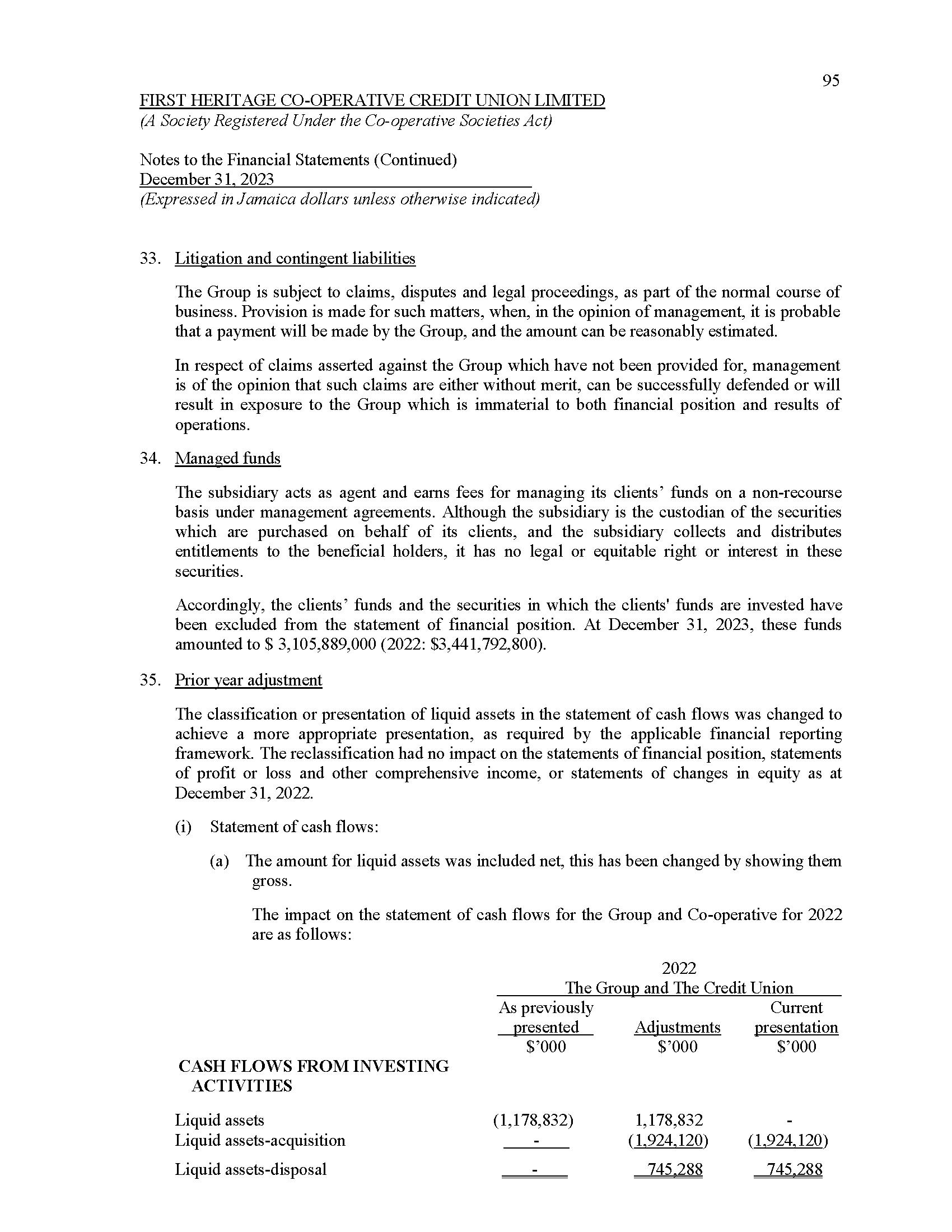

FHC’s bond includes:

a. All members of any religious bodies and affiliations in Jamaica and their families/relatives;

b. All Public Sector Employees, past and present, regardless of their terms of tenure, employed to Ministries/Departments/Agencies/Statutory Bodies/Public Corporations and their families/relatives;

c. All Professionals, their families/relatives, their employees and their families/relatives;

d. All members of Professional Associations affiliated to the Public Sector, their families/ relatives and the employees of these Professional Associations and their families/relatives;

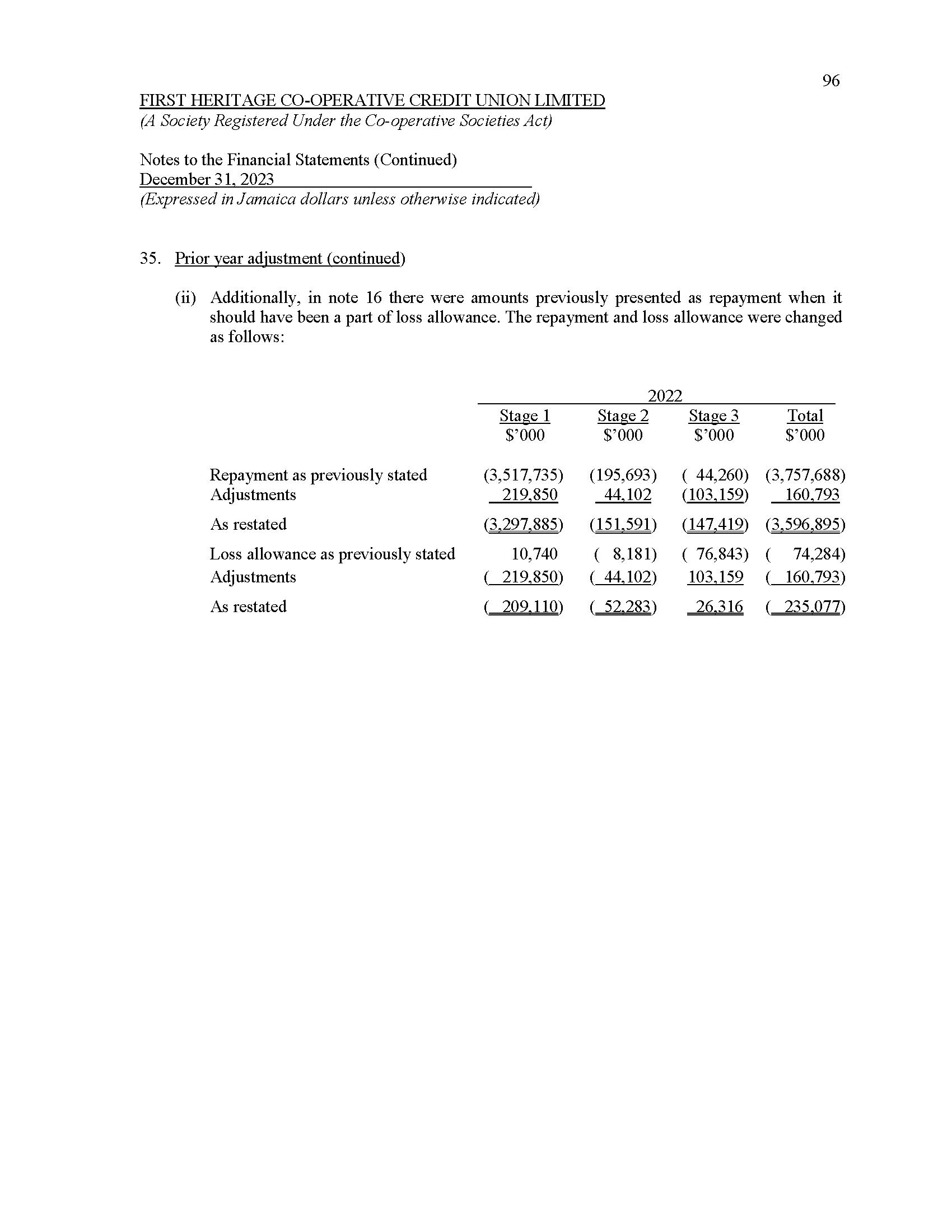

e. All Public Sector Consultants and their families/relatives;

f. All Public Sector Contractors and their families/relatives;

g. Employees, past and present, of the Credit Union and their families/relatives;

h. All Registered Co-operative Societies and members of these Societies;

i. All persons of good character of the age permitted by the Co-operative Societies Act;

j. All members and persons eligible to be members of the Credit Union that have merged with this Credit Union, provided that any person is being admitted to membership has attained the age of eighteen (18) years.

The Credit Union has a membership base of approximately 200,000 members across a network of eleven (11) branches strategically located across the island; offering a suite of forty-four (44) products and services. Our extensive array of products and services include a variety of loans, savings, term deposits for both personal and business purposes. In addition, we have investment and pension options from our subsidiary, FHC Investments Limited (FHCIL).

Our products and services are specifically designed to meet the needs of members at every stage of their lives.

Micro and Small Business Financing

The Micro and Small Business Loan business line reflects an ongoing commitment on the part of the Credit Union to foster the growth of entrepreneurship in Jamaica as a major driver of the economy. It also reflects the decision of FHC to widen the scope of its services and diversify its product range in a structured manner to provide more specific and targeted entrepreneurial opportunities. This will serve to increase employment, the standard of living of borrowing members and also contribute to the GDP of the country.

PROFILE

- FIRST HERITAGE CO-OPERATIVE CREDIT UNION LIMITED

The Micro and Small Business Unit was created in 2006. The Unit is a member of the Caribbean Micro Finance Alliance which acts as a catalyst for the development of micro finance in the Caribbean. The Unit was recognized worldwide as a finalist in the Caribbean Micro Finance Competition in 2012 for its impact in Jamaica. Currently, we have representatives located in Kingston, May Pen, Spanish Town and Mandeville.

Jamaicans have a rich entrepreneurial spirit and FHC is the home for financing these opportunities. The Credit Union’s commitment remains to generate continual benefits to our valued members and other stakeholders.

Subsidiary - FHC Investments Limited (FHCIL)

FHC Investments Limited (FHCIL), is a limited liability company and a wholly owned subsidiary of FHC, established to provide investment opportunities for members and non-members of the Credit Union. It is located at 20 Dominica Drive, Kingston 5. The company’s products and services may also be accessed through representatives at several FHC branch locations. FHCIL offers competitive rates of return and portfolio management services to its clients by a team of industry experts with over 30 years of combined experience.

FHCIL provides a suite of products and services to meet the needs of clients. These include:

• Stock Brokerage/Equities

• Bonds (local and foreign)

• Corporate Financing Structures

• Money Market Instruments

• Portfolio Management

• Investment Advisory

• Retirement Planning

The Investment company has products and services for the conservative investors as well as those with a greater risk appetite, some of which are offered in both foreign and local currency. FHCIL is also the Investment Manager and Administrator of the Credit Union’s Retirement Scheme.

PROFILE - FIRST HERITAGE CO-OPERATIVE CREDIT UNION LIMITED

Retirement Scheme

The FHC Retirement Scheme (formally Churches Co-operative Credit Union Retirement Scheme) referred to as “the Scheme” was established by Churches Co-operative Credit Union Limited as a defined contribution plan with effect from June 1, 2004, by Trust Deed to provide pension benefits for members and their beneficiaries at retirement and ancillary benefits in the event of death or termination. The strategic objective of the Scheme is to ensure that more Jamaicans have a retirement plan to which they are consistently contributing, thus safeguarding their retirement.

THE

CREDIT UNION MOVEMENT LOGO

The “hands, family and globe” symbol, represents credit unions worldwide. This trademark represents credit unions in any language. The theme is universal and conveys the image of all credit unions.

THE GLOBE - This represents the international network of credit unions.

THE FOUR SILHOUETTES - This represents the family of mankind working for the mutual benefit of all.

THE HANDS -This represents the self-help nature of credit unions.

PRODUCTS & SERVICES

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

MINUTES OF THE 11TH ANNUAL GENERAL MEETING OF FIRST HERITAGE CO-OPERATIVE CREDIT UNION LIMITED HELD HYBRID ON FRIDAY, SEPTEMBER 8, 2023 AT THE JAMAICA PEGASUS HOTEL 81 KNUTSFORD BOULEVARD, KINGSTON 5

1. ASCERTAINMENT OF QUORUM AND CALL TO ORDER

A quorum having been attained, the Chairman, Mrs. Leodis Douglas, called the meeting to order. She invited the Board Secretary, Mrs. Tamara Riley-Dunn, to read the notice convening the meeting.

This was followed by the playing of the National Anthem.

2. PRAYER

Prayer was offered by Ms. Latoya Latibeaudiere.

3. OPENING REMARKS, APOLOGIES AND TRIBUTES

The Chairman noted that this was the 11th Annual General Meeting of First Heritage Co-operative Credit Union, since its formation on August 1, 2012, by way of a merger between the Churches and GSB Credit Unions; and a transfer of engagement of the business of St. Thomas Credit Union.

The Chairman then invited the meeting to observe a minute’s silence for the members who passed during the year as outlined on pages 232 to 234 of the Annual Report.

The Chairman then invited the Board Secretary, Mrs. Francis Riley-Dunn to welcome the specially invited guests.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

Mrs. Francis Riley-Dunn extended a warm welcome to the following persons:

Mr. Errol Gallimore Department of Co-operatives and Friendly Societies

Mrs. Sheryll Brown Department of Co-operatives and Friendly Societies

Ms. Vanessa Porter Allen Department of Co-operatives and Friendly Societies

Mr. Bornette Donaldson National Union of Co-operative Societies Limited

Mr. Dennis Brown Jamaica Co-operatives Insurance Agency Limited

Ms. Tricia Bonfield KPMG

Apologies for absence were received on behalf of the following persons:

Ms. June Parks

Ms. Greta Bernard Creary

Ms. Sandra Dowe

Ms. Neisha Wizzard

Ms. Carissa Parks

Mr. Donald Creary

The Chairman then introduced the following Directors and the Chief Executive Officer (CEO):

Directors

Mr. Kevin Forbes First Vice-Chairman

Mr. Edmund Jones Second Vice-Chairman

Mrs. Tamara Francis Riley-Dunn Board Secretary

Mr. Cranston Ewan Treasurer

Mrs. René Gayle Roper Assistant Board Secretary

Mr. Balvin Vanriel

Mr. Richard Ranger

SSP Michael James

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

Executive Leadership

Ms. Roxann Linton Chief Executive Officer

She also introduced herself as the Chairman of the Board of Directors.

The Chairman invited the team from the Department of Co-operatives and Friendly Societies to introduce themselves. An apology for lateness was tendered for the Registrar, Mr. Errol Gallimore.

4. READING & CORRECTION OF THE MINUTES OF THE 10TH AGM

The minutes were taken as read on a motion moved by Member, Ms. Dionne Thompson, seconded by Director, Mr. Richard Ranger.

The Board Secretary took the meeting through the Minutes commencing on page 14 through to page 39.

Corrections:

Page 38 - under “Credit Committee”, Member, Mr. Earl Bailey was nominated for two years and not one.

Page 36 – In the 1st paragraph, the last line should read “to have it passed”.

There being no further corrections, the Minutes were unanimously confirmed on a motion moved by Member, Ms. Janet Harrison, seconded by Volunteer, Ms. Shauna-Kay Gordon.

5. MATTERS ARISING FROM THE MINUTES OF THE 10TH AGM

Member, Mr. Michael Burke noted the recent passing of Mr. Lincoln McIntosh at 96 years and stated that he was the President of GSB Credit Union from 1991 to 1993. The Chairman expressed sadness at the loss of a stalwart who served the GSB at a very high standard.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

6. BOARD OF DIRECTORS’ REPORT

The report was taken as read on a motion moved by Member, Ms. Clivia Green and seconded by Member, Mr. Sydney Manhertz.

The Chairman stated that she was privileged to be the first female Chairman of FHC Credit Union, having served in the capacities of Board Secretary and 1st Vice-Chairman previously.

She then highlighted the following:

The Credit Union experienced a number of key successes which led to a strong performance for the year 2022, due in part to the easing of the COVID-19 restrictions which led to higher demand for financial services.

In 2022, FHC realized a surplus of $184.25 Million. Total assets grew to $17.19 Billion in 2022 compared to $16.45 Billion the previous year. Coupled with this, the organization successfully upgraded its core banking system, and opened a new state of the art branch office in St. Thomas. She also noted that preparations continued for the imminent Bank of Jamaica supervision of Credit Unions.

The Chairman reported that the requisite steps, including training, were being undertaken to align the organisation for the implementation of the Data Protection Act on December 1, 2023.

Mrs. Douglas reported that FHC’s subsidiary, FHC Investments Limited (FHCIL), reported a net loss of $23.5 Million for the year ended December 31, 2022, compared to $3.6 Million the previous year. The decline in profitability was attributed to a 21.58% decrease in Net Interest and Other Income.

In relation to the FHC Retirement Scheme, there was growth in the client base, with 9 new clients joining, moving from a total of 83 clients in 2021 to 92 clients in 2022. The company also realized growth in member contributions of 20%, ending the year at $155.22 Million. However Net Assets Available for Benefits declined marginally ending the year at $1.46 Billion.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

Under the FHC Foundation, a total of $1.03 Million was donated to 16 recipients, who were awarded scholarships under the Annual FHC Scholarship Awards Programme for PEP, the Oswald Thorbourne and Renald Mason Scholarships. Additionally, $1.5 Million was awarded to a recipient under the Annual FHC Entrepreneurship Awards. It was also noted that a new FHC Sports Education Scholarship valued at $500,000 would be awarded for the 2023/ 2024 academic year. These scholarships, the Chairman noted, continued to go a long way in advancing education and the development of the young people of Jamaica.

The Chairman highlighted that amidst the economic challenges, the team continued to put members at the centre by addressing their needs through the creation of innovative products and skill-building strategies.

On behalf of the Board of Directors, she extended appreciation to all the retiring Directors for their selfless service, and asked them to stand and be recognized. She expressed thanks to the Volunteers, Credit and Supervisory Committee Members, the Leadership team, team members of both FHC Credit Union and FHC Investments Limited and loyal members and clients for their continued dedication and unwavering support.

In closing she assured the meeting that the member-at-the-centre focus remained central, and would be maintained to facilitate the continuous enrichment of services to the members. The group, she stated, remained dedicated to promoting and expanding financial inclusivity with the youth, the underbanked and the underserved, and the organization would progressively expand efforts in this direction.

The Board of Directors, she noted, remained confident in the commitment of the Leadership team to realising the Credit Union’s strategic vision and to perpetuate the legacy of a solid past and a secure future.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

Comments & Questions

Member, Ms. Althea Daley queried whether there was a timeframe set within which the Bank Of Jamaica (BOJ) regulations would be implemented, to which the Chairman answered that no definitive timeline was indicated, but assured her that the Credit Union was in a state of readiness.

Following this, Member Ms. Althea Daley inquired of the initiatives that have been put in place to address FHC Investments Limited’s (FHCIL’s) loses. In answer to Ms. Daley, the CEO, Ms. Linton, explained that most of the losses seen were related to the legacy portfolios and the performance of the Jamaica Stock Exchange, as well as the Bond market. She noted that these conditions did not allow for recovery from those valuation losses on the books. The CEO further stated that the new General Manager, had been working assiduously to expand the service offerings, so as to move away from products and services that were linked to market movement, and trend towards fee based offerings. She expressed the hope that in short order, FHCIL would become profitable as the market conditions improve and the suite of offerings become diversified.

Member, Mr. Burke reiterated his numerous suggestions made, to include a Bed and Breakfast Programme in Trench Town last year, and asked whether they had been placed in “File 13”. He further queried whether the Board had looked at the suggestion of applying to be a member of the Jamaica Fishermen’s Co-operative, as this could generate employment among the members of that Cooperative, on the condition that they save in the Credit Union. The Chairman thanked Mr. Burke for his ideas and assured him that they were never relegated to File 13.

There being no further questions, the Board of Directors’ Report was unanimously accepted on a motion moved by Member, Ms. Dionne Thompson and seconded by Member, Ms. Marcia Price.

7. MANAGEMENT REPORT

The Management Report was taken as read on a motion moved by Member, Mr. Earl White and seconded by Member, Ms. Marcia Lewis, with one abstention given online by Member, Mr. Dwayne Goodison.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

Ms. Linton extended thanks to all present. She noted the late holding of the AGM which usually takes place in May, and attributed the delay to challenges associated with the new core banking system, resulting in a protracted audit exercise. She expressed gratitude to the members for their patience and understanding.

Ms. Linton then highlighted the following achievements:

That the charge for 2023 was “Dream, Dare and Deliver” which was carried through, resulting in the excellent performance, and contributed to making the Credit Union future-ready in every aspect of its growth.

The new core banking system was implemented which had significantly bolstered the Credit Union’s technological efficiency.

FHC was the first individual Credit Union to acquire a Stock Brokerage Licence through its subsidiary, FHC Investments Limited (FHCIL); and that FHCIL had diversified its income stream and was now earning fee income.

She noted that there was the historic passing of a resolution in relation to FHC to effect a starter membership tier that would provide access and allow service to the unbanked and underserved communities.

The St. Thomas Branch was relocated to a new permanent office during the period under review. This move is indicative of FHCCU’s continued commitment to the Parish.

For the year under review, the Credit Union made a net surplus of $184.25 Million and disbursed $5.21 Billion. These achievements, she attributed to the ongoing dedication and unwavering commitment of team members.

MINUTES

OF THE 11TH ANNUAL GENERAL MEETING

Team members were trained in the new core banking system enabling them to function in the new system environment; they also underwent fraud awareness and sensitisation in light of the current heightened fraud risk environment; anti money laundering compliance training; and leadership development training for emerging team leaders.

Over the course of the year, team members received recognition and rewards through a variety of channels to celebrated their exceptional and significant contributions to the organisation. These efforts were aimed to inspire, show appreciation and foster both a high-performance culture and a sense of belonging within the team.

The CEO indicated that by recognising the importance of mental and emotional health in the workplace, the Credit Union proactively took steps to create an environment where team members felt motivated, connected and energised by facilitating a diverse range of team engagements and fun activities. Special recognition was paid to the FHC Sports Club for bolstering a dynamic group of team members known for their creativity and dedication.

The Credit Union continued to focus on its ‘Member at the Centre’ ethos as seen from the activities put on during the Civil Servants Week and the FHC Civil Servants of the Year Awards, where the following members received awards: Mr. Lennox Wallace in the Management category employed to the Ministry of Health and Wellness; Mr. Oliver Morris, Middle Management category, from the Ministry of Justice; Ms. Simone Turton, Technical Support category, Ministry of Health and Wellness; and Ms. Sophia Molton, the inaugural People’s Choice Awards winner, Office of the Prime Minister. FHC also hosted an online Christmas Show which was well supported and which provided another avenue for connecting with members.

She gave her commitment that the team would continue to identify different ways, including digital channels that would enable the membership to have an interactive experience with the Credit Union; and informed the members that during the year the range of financial solutions was expanded and refined, offering avenues for members to pursue their financial aspirations with added ease and convenience, noting that an enrolment drive was now on for the Family Indemnity Plan and the Family Critical Illness Insurance Plan, and as such the Referral and Rewards Promotion was reignited.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

It was reported that the new AccessPlus Debit Mastercard was launched and that this card offers expanded accessibility for conducting transactions, both locally and internationally, as well as online. She urged all who had not yet gotten their new cards to do so and refrain from sharing their card information with other individuals.

The CEO acknowledged that the wait time in branches had increased and attributed this to challenges in recruiting frontline team members. She however assured the meeting that the team was working assiduously to address the recruitment issue.

Members were informed that the Member Assistance Relief Programme continued, where members experiencing difficulties were accommodated through waivers, moratoria or other options to tailor their payment arrangements for greater comfort and convenience. She reminded the members of FHC’s unwavering commitment to open conversations and communication with those experiencing financial challenges.

Ms. Linton mentioned the recently concluded investment summer promotion where a number of members opened accounts at a 50% reduction in both the opening fee as also the brokerage fee. This offer, she indicated, would be reopened before the end of the year. She outlined the various activities being undertaken to yield greater visibility for the FHCIL brand and drive demand for services. She also noted that Dr. Sara Lewis was appointed the first Brand Ambassador of FHC Investments Limited and that she would assist in this regard.

She stated that emphasis continued to be placed on risk management and that the risk management approach remained a strong part of the Credit Union’s culture. During the period under review, frameworks were established to facilitate responsible credit risk management, anti-money laundering and counter terrorism financing controls, cyber security safeguards and a comprehensive business continuity plan.

The Credit Union continued its preparation for the implementation of the Data Protection Act on December 1, 2023 and she assured the meeting that the Credit Union was compliant and would be ready.

MINUTES OF THE 11TH ANNUAL

Looking towards the future, she expressed optimism and determination in the organisation’s ability to continue to adapt to the dynamic and rapidly changing environment. Quoting from a song from Grammy Award winner, Koffee, that “gratitude is a must”, she thanked everyone for their contribution to the success of financial year 2022, to include the valued members, the committed Board of Directors and volunteers and her dedicated team.

The Floor was then opened for questions.

Member, Ms. Althea Daley commended Ms. Linton on a comprehensive presentation and extended congratulations to the Credit Union for its outstanding performance. She thereafter asked when the Credit Union would introduce a mobile app. Ms. Linton acknowledged the significance of having a mobile app and explained that the Credit Union had been diligently working on its development with a view to releasing the first generation version of the mobile app by the end of the first quarter in 2024. She stated that considerable efforts and resources had been dedicated to the project as they were cognisant of the growing appeals for the app.

Member, Mr. A.N. Harris, Esq. expressed his appreciation for the excellent presentation and sought clarification on whether Dr. Sara Lawrence Lewis’ involvement as the Brand Ambassador was limited to the local market or extended to the diaspora. The Chairman pointed out that while Dr. Lawrence Lewis’ face-to-face engagements were confined to activities within Jamaica, these interactions are shared on various social media platforms, and that this approach was aimed at ensuring that the members in the diaspora and other locations have access to the promotional activities, effectively spreading the message globally.

Member, Ms. Sheryl Rambolt noted that when conducting transactions at a particular branch, customers did not receive the balance on their deposits unless they pay a fee of $50 for a statement and questioned the fairness of such an arrangement, as this practice represented a double charge for members. Ms. Linton explained that, in the past, the Credit Union used to issue receipts outlining the balance, and that the decision to discontinue this practice was deliberate, as the detailed information on the receipts posed a potential security risk if lost or misplaced. To address this, she stated that the Credit Union had implemented alternative options for members to obtain their statements without

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

incurring a cost. Member Rambolt added that this information needed to be disseminated within the branches, in response to which Ms. Linton assured the meeting that the Credit Union would reinforce the message regarding the availability of account balance information without incurring charges.

There being no further questions, the Management Report was unanimously approved on a motion moved by Member Ms. Althea Daley and seconded by Member Ms. Janyce Robinson.

8. AUDITORS’ REPORT

The Chairman invited Ms. Tricia Bonfield, representing KPMG, to present and abridged version of the Auditors’ Report.

On a motion moved by Director, Mr. Balvin Vanriel, seconded by Member, Ms. Shauna Kay Gordon, the Auditor’s Report was approved to be presented.

Ms. Bonfield, read the Auditors’ opinion which stated, among other things, that in their opinion, proper accounting records were maintained based on the examination of those records, and that the financial statements, which accord with those records, give the information required by the Cooperative Societies Act.

The Chairman thanked Ms. Bonfield, for taking the meeting through the Auditors’ Report.

9. TREASURER’S REPORT

The Chairman invited the Treasurer, Mr. Cranston Ewan, to present the report for 2022.

The report having been circulated was taken as read on a motion moved by Member, Ms. Dionne Thompson and seconded by Member, Mr. Sydney Manhertz.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

He then highlighted the following:

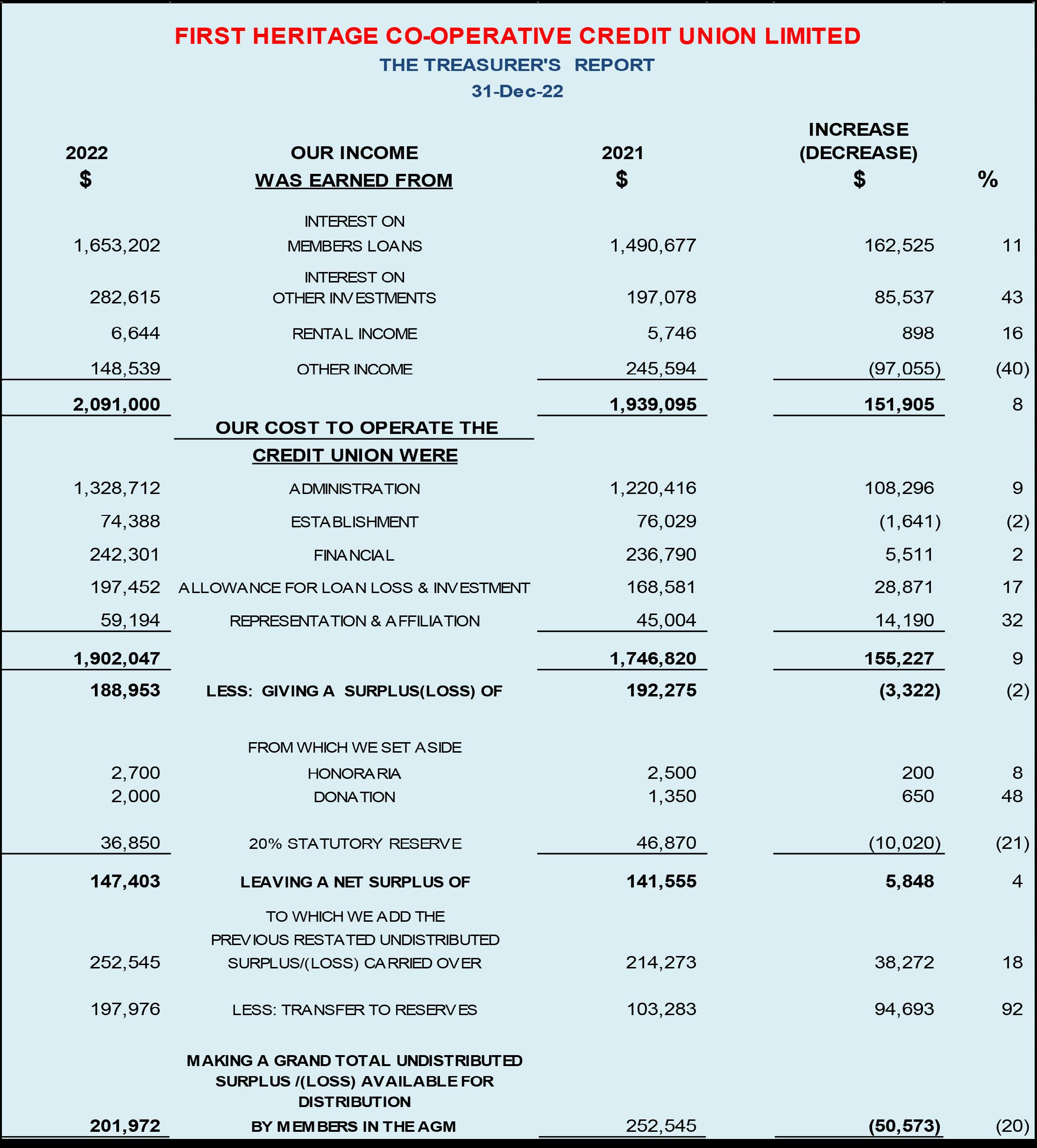

He gave a brief overview on the Jamaican economy which grew by an estimated 5.20% in 2022. He noted that the Jamaican dollar appreciated by 1.96% against the United States dollar, closing the year at $152.05 to $1. Inflation ended the year at 9.4% after peaking at 11.8% in April 2022, and the BOJ increased its policy interest rate from 2.5% to 7% in December, an increase of 450 basis points.

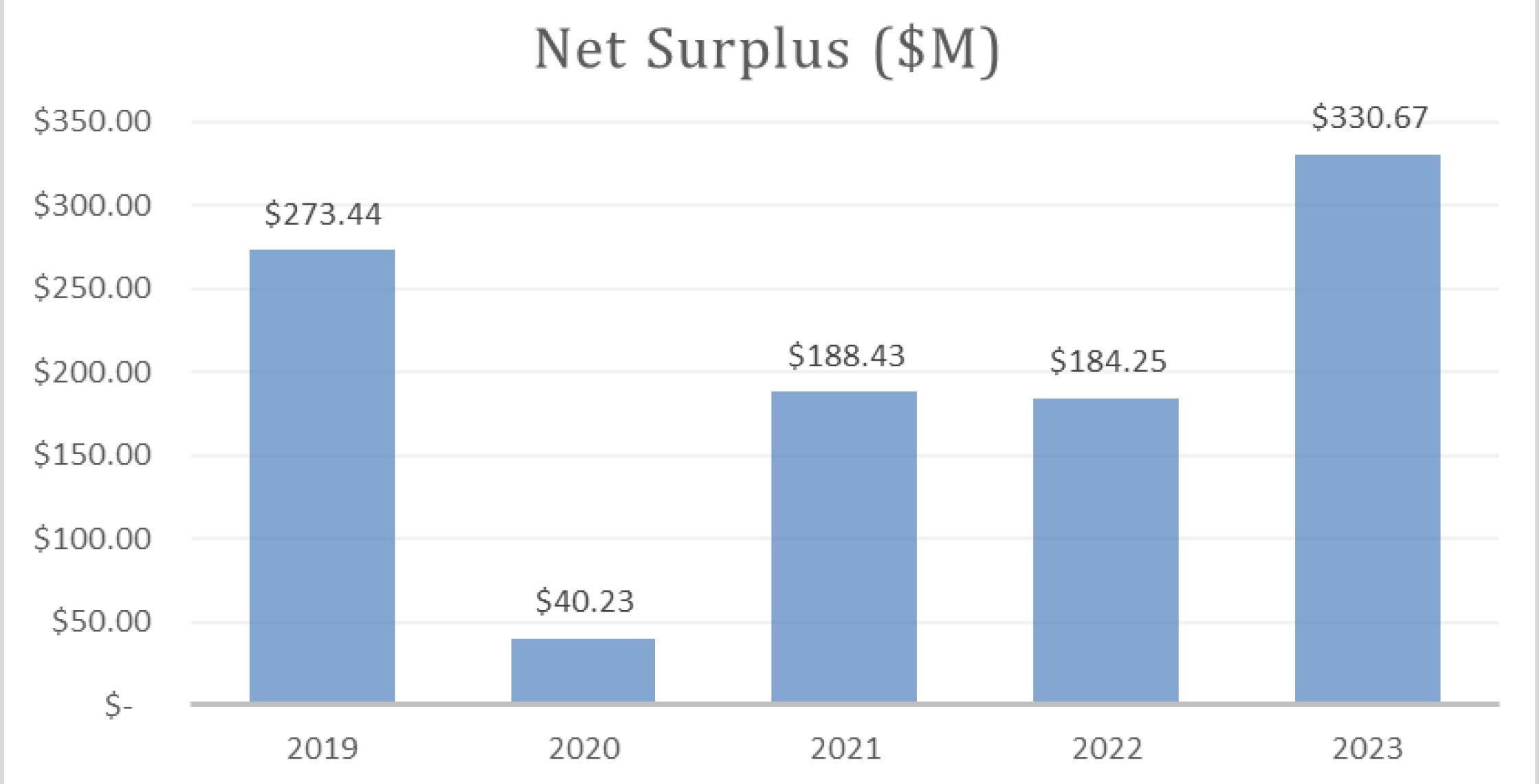

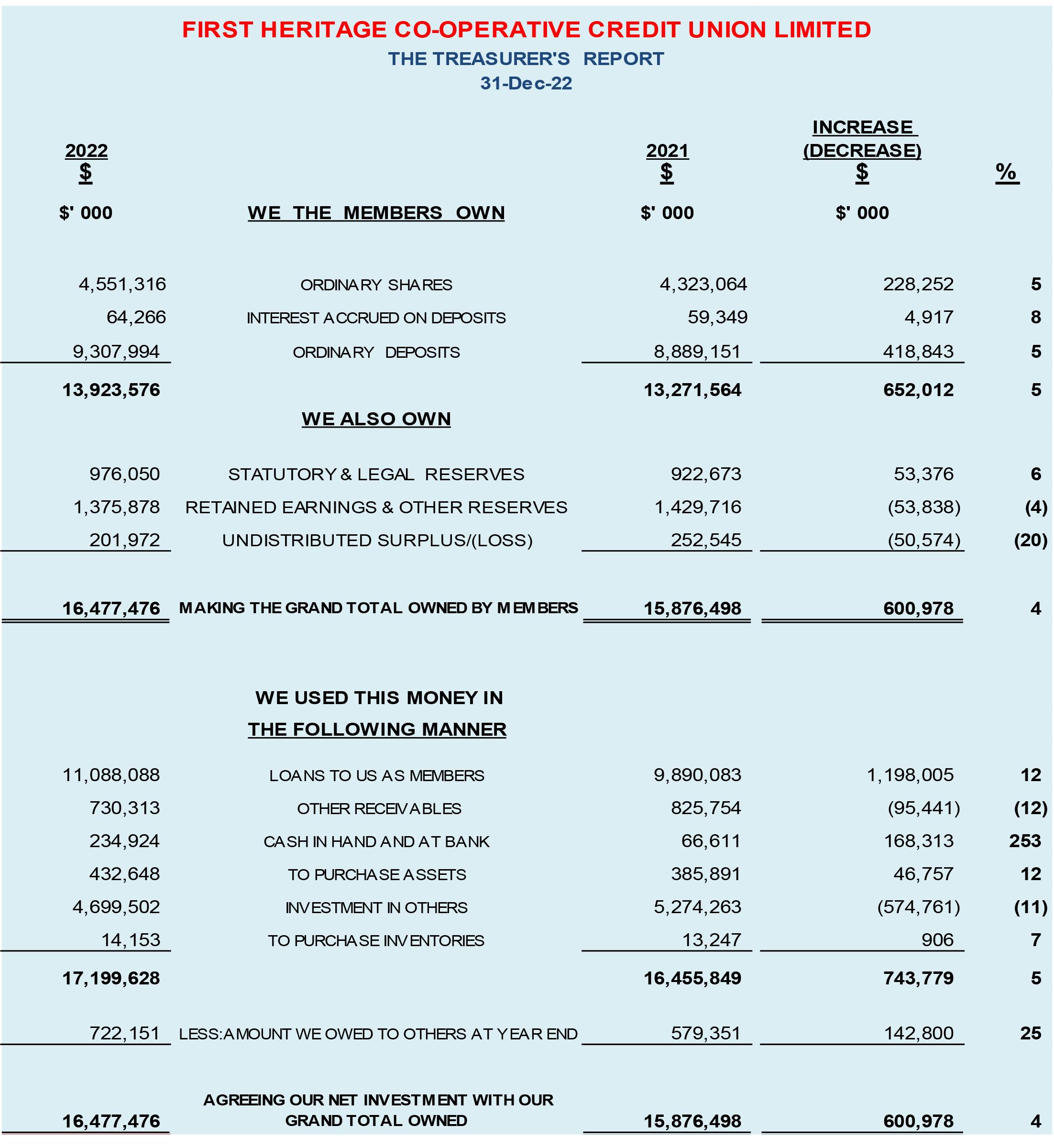

The Credit Union made a surplus of $184.25 Million for 2022, compared to $188.42 Million the previous year.

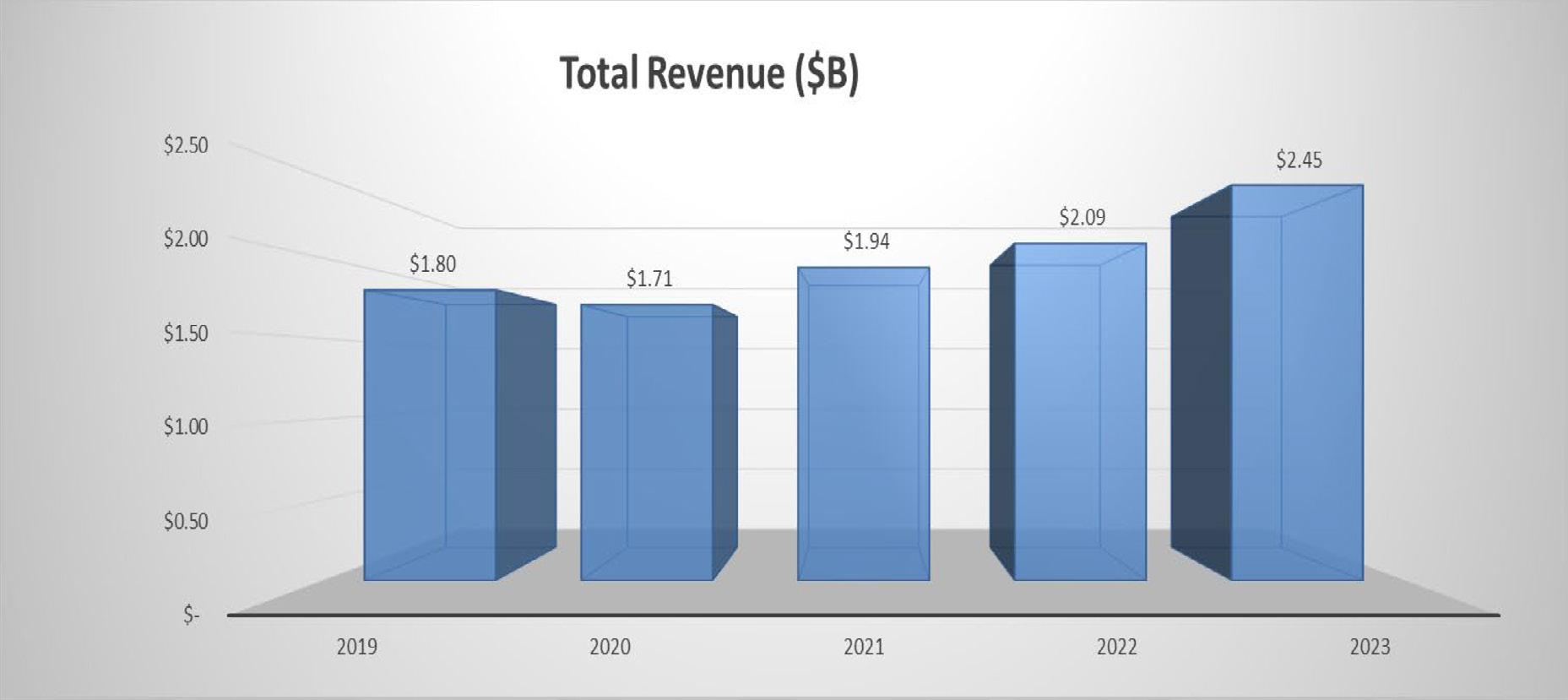

Total Revenue surpassed the $2 Billion mark ending the year at $2.09 Billion.

FHC Investments experienced a loss of $23.58 Million compared to a profit of $3.63 Million the previous year. Mr. Ewan assured the meeting that the Board was aware of the challenges faced by FHCIL and was dedicated to ensuring the company’s viability.

Accumulated surplus for the year amounted to $201.97 Million; while Total Assets increased to $17.36 Billion.

The group’s Net Loan portfolio ended the year at $11.08 Billion.

Deposits grew to $13.92 billion, compared to $13.27 billion the previous year.

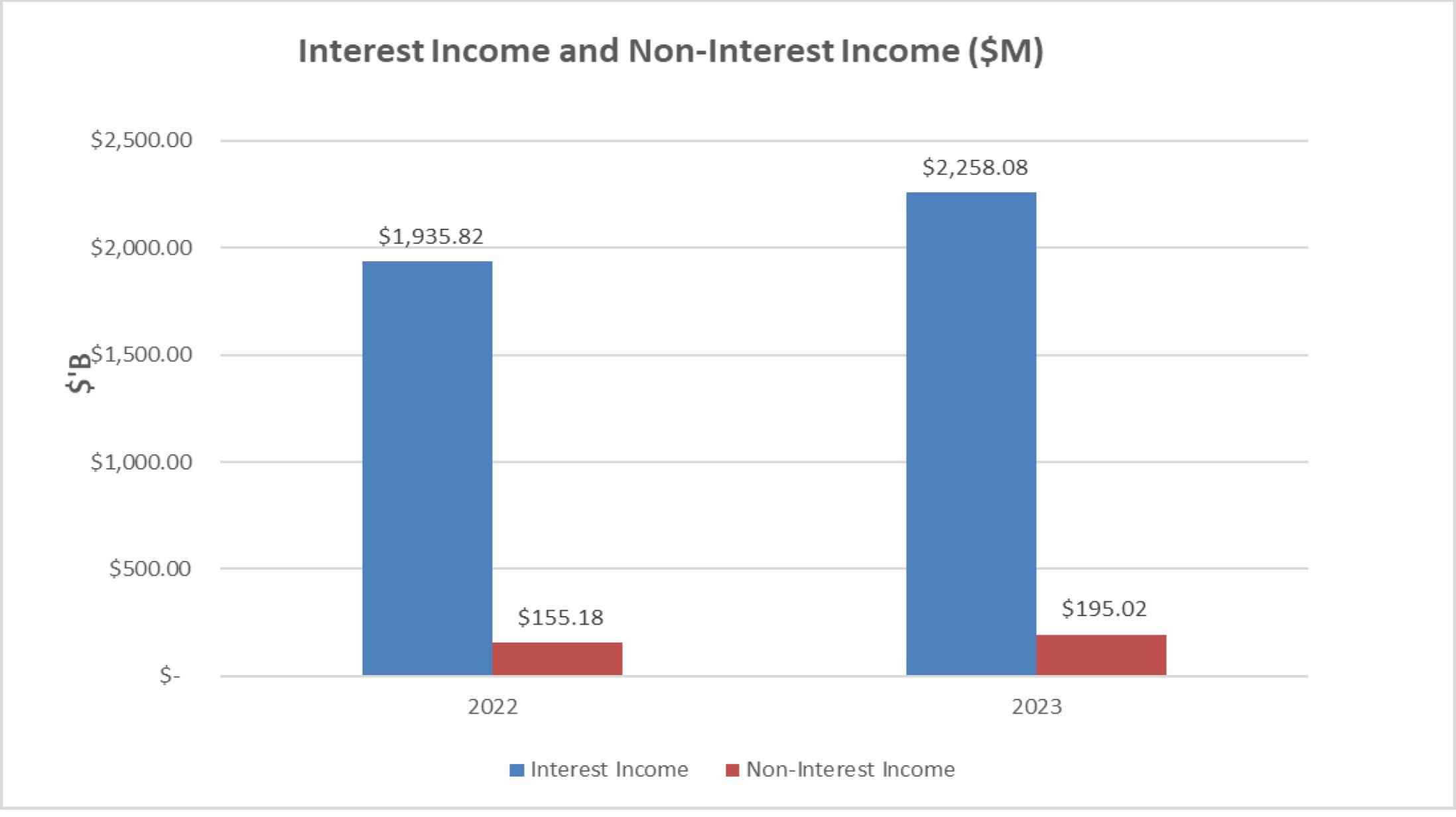

Interest income increased by $14.7 Million, moving from $1.6 Billion in 2021 to $1.94 billion in 2022.

Non-Interest Income decreased to $155.18 million in 2022, compared to $251.34 million in 2021.

Interest Expense ended the year at $242.30 million compared to $236.79 million the previous year.

Operating Expenses increased by $120.85 million or 9% ending the year at $1.46 billion compared to $1.34 billion the previous year.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

Past Due loans (30 days and over) to Gross Loans ended the year at 10.04% compared to 7.97% in the prior year.

Provision for Loan Losses, net of recoveries, amounted to $198.75 million compared to $161.21 million in 2021.

Accumulated Surplus available before distributions decreased by $50.8 Million moving from $252.55 Million in 2021 to $201.97 million in 2022.

Institutional Capital to Total Asset ratio stood at 10.77% as of December 31, 2022, compared to 9.86% in 2021.

He pointed out that key ratios such as Capital and Liquidity remained above the benchmark, reinforcing the Credit Union’s ability to execute key strategies.

He commended the Credit Union’s performance in 2022 and thanked the Executive Management Team for navigating the challenges faced throughout the year and extended his appreciation to KPMG for ensuring the accuracy of the financial reports and providing a favourable audit report. He assured all present that the Credit Union remained financially strong and sound.

He expressed gratitude to the departing members of the Board of Directors for their dedication and camaraderie, and his heartfelt thanks to the valuable stakeholders, to include the volunteers, managers, and team members, for their contributions, and the loyal members for their continued support as the Credit Union would not exist without them.

Comments & Questions

Mr. Robert Kelly raised a personal issue he was having with the Credit Union and was informed by the President that she would support him in seeking to resolve the matter after the meeting.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

There being no further questions, the Treasurer’s Report was approved on a motion moved by Member Ms. Dione Thompson and seconded by Member Ms. Doreen Stennet.

10. DISTRIBUTION OF SURPLUS

The Treasurer tabled the Distribution of Surplus as presented in the Annual Report, outlining the proposed distribution of $201 Million for 2023 as follows:

Dividend on Permanent Shares

Honoraria

Donations

Special Donation to the FHC Foundation

Transfer to Retained Earnings Reserve

Accumulated Surplus

$28 Million

$5.53 Million

$1.95 Million

$1 Million

$75 Million

$89 Million

This was unanimously approved on a motion moved by Treasurer, Mr. Cranston Ewan and seconded by Member, Ms. Althea Daley.

11. MAXIMUM LIABILITY

In keeping with the rules of the Credit Union, it was proposed by the Treasurer that the Maximum Liability be fixed at 20 times that of the Credit Union’s share capital.

This was unanimously approved on a motion moved by Director, Mr. Richard Ranger and seconded by Member, Ms. Marcia Pryce.

12. SUPERVISORY COMMITTEE REPORT

The report, which was presented by Member, Ms. Shauna-Kaye Gordon, was taken as read on a motion moved by Member, Mrs. Eulalee Grant Smith and seconded by Member, Ms. Arlene Thomas.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

Ms. Gordon highlighted that the role of the Supervisory Committee was that of supporting the Board of Directors to fulfil its responsibilities by providing oversight on the internal control systems through the Internal Audit Department.

She then introduced the Committee members which included herself, Mrs. Karlene Mitchell-Gordon, Committee Secretary, Mrs. Carol Dallas-Robinson, Ms. Tanisha Thompson, and Ms. Jacqueline Roberts.

Ms. Gordon shared that there were seven planned audits in 2022, five from 2022 and two from 2021, all of which were completed, with the actual completion rate exceeding the target of 70%.

The audits carried out were in relation to the Teller End-Of-Day balancing activity report; AntiMoney Laundering (AML) and Counter Financing Terrorism Compliance Review for 2021; the review of the Special Investigation Process; Debit Card Management; FHC Investments Limited Retirement Scheme; Electronic Funds Transfer, and Compliance with the Real Estate Appraisal Process.

She reported that two audits were still in progress; the Interest Rate Management and Anti-Money Laundering (AML) and Counter-Financing of Terrorism (CFT) Compliance for 2022.

A detailed review of the findings for each audit completed was provided. It was noted that Management implemented operational controls to mitigate against the recurrence of identified issues.

In relation to the Bank Reconciliation review, it was reported that some challenges were experienced in reconciling items since the implementation of the new core banking system, however, substantial improvement had been made by the Information Technology Department.

Two connected party and volunteer loans were outstanding for more than 30 days as of December 31, 2022.

In conclusion, Ms. Gordon expressed gratitude to the Nominating Committee, the members of the

Credit Union, the Management Team and Team Members, the hardworking Internal Audit Department, and the Board of Directors. She also thanked her Committee members for their dedication and service and for their time spent deliberating and performing the work of the Credit Union.

Comments & Questions

When asked by Member, Ms. Dionne Thompson about the status of the two outstanding audits, Ms. Gordon stated that one had since been completed and the other was nearing completion.

Member Thompson noted that the implementation of the electronic money transfer was initially planned to be implemented in 2023 and enquired if a new timeline had been set. Ms. Gordon informed the meeting that significant work was being done to address the issue though she was not in a position to provide the specific timeline to completion.

Regarding Past Due loan balances held by staff, volunteers, and connected parties, Member, Mr. A. N. Harris, Esq. enquired as to the number of loans outstanding and whether any sanctions had been taken against these volunteers. Ms. Gordon stated that two loans were outstanding for more than 30 days, and instead of imposing sanctions, the Management Team engaged the individuals involved and since then those volunteers became compliant.

There being no further questions, the Supervisory Committee Report was adopted on a motion moved by Member, Ms. Charmaine Allen and seconded by Member, Ms. Suzette Grant.

13. CREDIT COMMITTEE REPORT

The Credit Committee Report was taken as read on a motion moved by Director, Mr. Richard Ranger and seconded by Member, Ms. Charmaine Allen.

Ms. Clivia Green, took the meeting through the report and highlighted the following:

She introduced the Committee members to include Mr. Donald Williams, Chairman; herself; Secretary, Ms. Keslyn Gilbert-Stoney, Dr. Earl Bailey and Ms. Janyce Robinson, and outlined that the MINUTES OF THE 11TH ANNUAL GENERAL MEETING

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

responsibility of the Credit Committee was making decisions and recommendations to the Board on loan requests that exceeded the authority of the loan officer or required special attention.

For the period under review the Credit Union disbursed $5.22 Billion in loans. The loan portfolio grew by 12.38% moving from $10.4 Billion in 2021 to $11.72 Billion in 2022.

Ms. Green shared that the Past Due rate increased by 2.07% moving from 7.97% in December 2021 to 10.04% in December 2022. She reported that the Micro and Small Business Loans Unit recorded a decrease in disbursements moving from $256.82 Million in 2021 to $230.25 Million in 2022 and the Past Due rate for these loans moved from 30.27% in 2021 to 38.8% in 2022. She encouraged the members to assist in reducing the Past Due rate by ensuring timely loan repayments.

In closing Ms. Green expressed gratitude to the Board of Directors, the Credit Committee, the Supervisory Committee, and FHC’s valued members for their support and dedication.

Comments & Questions

In response to a member who questioned the percentage rate compliance in relation to repayment of loans, Ms. Green restated the Past Due rate of 10.04%, which she noted would equate to approximately 90%.

Member, Ms. Althea Daley queried the cause for the decline in disbursements and was informed by Ms. Linton that the decline was largely attributed to the ongoing impact of the COVID-19 pandemic and pointed out that this was not unique to FHC but the Small & Medium Enterprise sector that was still recovering from the effects of the pandemic.

In answer to a question from Member, Mrs. Jackie Brown Kinghorn relating to the processing time for personal loans, Ms. Linton stated this could be processed within three weeks depending on the timely submission of documents required but it may take a little longer for a mortgage loan.

There being no further questions, the Credit Committee Report was adopted on a motion by Member,

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

Mrs. Nicola Franklin Hunt and seconded by Member, Ms. Charmaine Allen.

14. NOMINATING COMMITTEE REPORT

The Nominating Committee Report which was presented by Board Secretary, Mrs. Tamara Francis Riley-Dunn was taken as read on a motion moved by Director, Mr. Noel Francis and seconded by Member, Mrs. Romaine Robinson Munroe.

Mrs. Francis Riley-Dunn noted that the Nominating Committee was appointed in accordance with the rules of the Credit Union and consisted of herself, as Chairman, Member, Mr. Richard Picart and the CEO, Ms. Roxann Linton.

She reported that the Board size would be returning to 9 members and explained that it was increased from 9 to 13 members in 2021 to facilitate a seamless transition due to the retirement of the following members:

• Mr. O’Neil Grant

• Mr. Edmund Jones

• Mr. Kevin Forbes

• Retired SSP Michael James

• Mr. Balvin Vanriel

• Ms. Rene Roper (not seeking re-election)

• Mr. Richard Ranger (renominated)

Mrs. Francis Riley-Dunn then advised that the following persons were nominated for a term of 2 years:

• Justice Evan Brown

• Ms. Nickeisha Walsh

• Mr. Stephan Richards

• Mr. Richard Ranger

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

She read the profiles of the new Board Members, and indicated that the above mentioned persons would be joined by the following Directors who will be retiring in 2024:

• Mrs. Leodis Douglas

• Mr. Noel Francis

• Mr. Cranston Ewan

• Mr. Wayne Jones

• Mrs. Camelle Ricketts-Moore

On behalf of the Credit Union, she expressed gratitude to the retiring Board Members for their commitment, support, and contribution to the success of the organisation over the years.

Supervisory Committee:

Mrs. Francis Riley-Dunn stated that the 5 sitting members would be retiring and the Committee had renominated them for a term of 1 year:

• Ms. Shauna-Kay Gordon

• Ms. Tanisha Thompson

• Ms. Jacqueline Roberts

• Mrs. Carol Dallas-Robinson

• Mrs. Karlene Mitchell-Gordon

Credit Committee:

Retiring were Mrs. Keslyn Gilbert-Stoney and Ms. Clivia Green while Mr. Donald Williams had resigned. Nominated were Mrs. Althea Daley, Mrs. Keslyn Gilbert-Stoney and Ms. Clivia Green; who would be joined by Ms Janyce Robinson and Mr. Earl Bailey who retire in 2024.

Comments & Questions

Member, Mr. Michael Burke expressed disappointment with the Nominating Committee Report not

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

being included in the abridged booklet and emphasised the importance of it being included going forward. These sentiments were echoed by Member, Mr. A.N. Harris Esq. Mrs. Francis Riley-Dunn apologised for the omission and assured the meeting that this would not reoccur going forward.

There being no other questions or comments, Board Secretary, Mrs. Francis Riley-Dunn asked for a motion to adopt the Nominating Committee Report. The motion was moved by Member, Ms. Doreen Stennett and seconded by Member, Ms. Marcia Lewis.

15. ELECTION

Ms. Sheryll Brown was invited to conduct the election.

After ascertaining that there was still the presence of a quorum she instructed the meeting as to the voting procedure. She noted that as per the Credit Union rules, nominations from the floor were invited as the Credit Union had not yet passed the resolution to disallow such practice and asked the Chairman to ensure that this was done for the coming year.

Board of Directors:

Mrs. Brown asked for nominations from the floor three times and hearing none she declared Mr. Richard Ranger, Mr. Evan Brown, Ms. Nickeisha Walsh, and Mr. Stefan Richards duly elected to the Board of Directors for a term of 2 years.

This was accepted on a motion moved by Member, Mr. Michael Burke and seconded by member, Mrs. Romaine Robinson Munroe from the online platform.

Supervisory Committee:

Mrs. Brown invited nominations from the floor three times and hearing none, she declared Ms. Shauna-Kaye Gordon, Ms. Tanisha Thompson, Ms. Jacqueline Roberts, Mrs. Carol Dallas-Robinson and Mrs. Karlene Mitchell-Gordon duly elected to the Supervisory Committee for a term of 2 years.

This was accepted on a motion moved by Member, Mrs. Debbie Ann Edwards Kennedy and seconded by Member, Mrs. René Gayle-Roper.

Credit Committee:

Having invited nominations from the floor three times and hearing none Mrs. Brown announced that Mrs. Althea Daley was duly elected to serve for a 1 year term to complete the unexpired term of Donald Williams and Mrs. Keslyn Gilbert-Stoney and Ms. Clivia Green for a term of two years.

This was accepted on a motion moved by Member, Ms. Nicola Franklin Hunt, seconded by Director, Mr. Kevin Forbes.

Delegates to the League and Various Other Agencies:

Mrs. Brown asked that the meeting give the Board permission to elect the delegates and alternate delegates as was customary.

This was accepted on a motion moved by Member, Ms. Althea Daley and seconded by Director, Mr. Edmund Jones.

She reminded the Board and other committees to meet within 10 days to elect the officers and submit the information to the Department of Co-operatives and Friendly Societies and to the League and any other affiliate associations.

She further reminded the Board that within 30 days of a Board member resigning, the information regarding the replacement should be submitted to the Department. The Chairman extended thanks to Mrs. Brown for conducting the elections in an efficient manner.

16. ANY OTHER BUSINESS:

As it concerned the FIP product, a member asked for the new plan options that were recently announced, and Ms. Georgia Morrison from CUNA Caribbean who was invited to answer the question outlined that the new plans ‘H’ to ‘K’ provided the following coverage amounts: Plan H pays a coverage benefit of $1.3 Million; Plan I, $1.6 Million; Plan J, $1.8 Million; and Plan K, $2 Million. MINUTES OF THE 11TH ANNUAL GENERAL

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

Member, Ms. Shauna-Kaye Gordon expressed satisfaction with the up-to-10% term deposit rate and noted that this was in stark contrast to 5%-1% offered in the industry. The Chairman clarified that the rate was 8.75%, but emphasised that it was still a significant improvement compared to other financial institutions.

The Chairman announced that the Board took a decision to reduce the Maintenance Fee for senior citizens aged 65 and over by 50% effective June 2023 as a way of giving back to members for their decades of support to the Credit Union.

Member, Mr. Sydney Manhertz expressed disappointment with the quality of service at some of the branches, particularly the flagship branch in Cross Roads where the turnaround time was unsatisfactory. The Chairman assured him that his comment was noted and would be acted on. He also commended the organisers for a well-timed and well-flowing AGM.

Member, Ms. Tanisha Thompson acknowledged pleasure at having a female Chairman, a sentiment echoed by the other members through the thunderous applause.

Member, Mr. Michael Burke suggested that a subcommittee be formed to explore co-operative opportunities specific to the Credit Union focusing on tourism industry initiatives that would benefit its lowest-paid individuals, and offered his service on such subcommittee to contribute his expertise. The Chairman assured the meeting that efforts had always been made to explore co-operative opportunities aligned with the Credit Union’s mission.

Queried as to the location of the St. Thomas branch, the Chairman stated that it was conveniently situated near the courthouse and the fire station at 2 Debtors Lane.

Giveaway Exercise

Ms. Michelle Tracey was invited to take the meeting through this exercise.

MINUTES OF THE 11TH ANNUAL GENERAL MEETING

17. VOTE OF THANKS

Board Secretary, Mrs. Tamara Francis Riley-Dunn expressed gratitude to the over 100 physical and over 200 virtual attendees for their participation. She thanked the Chairman for ably managing the meeting, the Krystal Clear Productions team, the Jamaica Pegasus Hotel, and the Marketing, Communications & Member Experience team for their contributions to a successful AGM.

18. TERMINATION

The Chairman terminated the meeting at 6 o’clock.

Nickeisha Walsh

Secretary, Board of Directors

CORPORATE GOVERNANCE STATEMENT

First Heritage Co-operative Credit Union Limited (FHC) prioritizes effective corporate governance to ensure the safe growth of our co-operative and to protect the interests of our valued members. We recognize that good corporate governance is fundamental to maintaining the trust and confidence of our members, team members, and stakeholders, and for safeguarding the financial well-being of our Credit Union.

Our corporate governance framework is guided by the following principles:

1. Strong Board Oversight: Our Board of Directors is composed of highly experienced individuals who provide governance oversight using their diverse skills and expertise. The Board provides strategic direction and oversight, ensuring that FHC’s activities are in line with our vision, mission and values. Board members act in the best interests of our members and diligently exercise their fiduciary duties to safeguard our members’ financial interests. Our Board has established various committees, including a Supervisory Committee, Credit Committee, Corporate Governance Committee and an Audit and Risk Management Committee , among others, to provide specialized oversight and ensure that specific areas of governance are addressed in depth. These committees are composed of independent directors and volunteers and are responsible for providing recommendations and guidance to the Board.

2. Culture: Our Board of Directors and Management Team set the tone at the top of this organization by exemplifying the highest standards of integrity, transparency and accountability. This unwavering commitment to ethical conduct inspires our team members to uphold the principles of integrity, honesty, and professionalism in their dealings with members, colleagues, and stakeholders. Through regular communication and by leading by example, we create a corporate culture that fosters a sense of responsibility and respect for protecting our members’ resources.

3. Risk Management: We have robust risk management practices in place to identify, assess, and mitigate risks that may impact our Credit Union’s safety and soundness. These practices are regularly reviewed and updated to align with changing market conditions, technological developments, industry best practices, and regulatory requirements. We place a high emphasis on maintaining adequate capital levels, managing credit risk, liquidity risk, operational risk, and cybersecurity risk, among others.

CORPORATE GOVERNANCE STATEMENT

4. Internal Controls: We have instituted effective internal control mechanisms to safeguard the accuracy and integrity of our financial reporting, as well as the effectiveness and efficiency of our operations. We conduct regular internal audits and risk assessments to identify and address any control weaknesses and ensure compliance with policies and procedures.

5. Compliant Posture: We are committed to compliance with all applicable laws, regulations, and industry standards. We maintain strong relationships with regulatory authorities and proactively address any compliance or legal matters that may arise. We also have a comprehensive compliance program in place to ensure strict adherence to Anti-Money Laundering (AML) Regulations and other relevant laws.

6. Continuous Improvement: We are committed to continuous improvement and regularly review and update our corporate governance practices to ensure that they remain effective and aligned with our Credit Union’s strategic objectives, member needs and regulatory requirements. We welcome feedback from our members, employees, and stakeholders and use it as an opportunity to learn, adapt, and improve our governance practices.

7. Member-Centric Approach: Our Credit Union exists to serve our members, and their best interests are at the forefront of our decision-making processes. We believe that member engagement is critical to understanding their needs, expectations and concerns, and we strive to align our strategies and operations accordingly.

In conclusion, at FHC, we are dedicated to maintaining the highest standards of corporate governance to ensure the safe and sound growth of our Credit Union and to protect the interests of our members and all other stakeholders.

Mrs. Leodis Douglas is currently the Principal Lecturer, Head of Department (HOD) at the G. C. Foster College of Physical Education and Sport. Prior to that, she was the Director of Human Resources for 12 years at the institution.

Mrs. Douglas holds, amongst her many qualifications, a Masters Degree in Business Administration from Florida International University (FIU), a Bachelor of Science in Human Resource Management, graduating Summa Cum Laude and a Diploma in Education with Honors. She is also certified in Executive Management, Six Sigma Project Lean Processes and is Six Sigma Black Belt Certified.

Mrs. Douglas currently serves as the Chairman of the Board of Directors of First Heritage Co-operative Credit Union and is also the Chairman of the FHC Foundation.

PROFILE OF BOARD OF DIRECTORS

Mr. Jones currently holds the post of Deputy Financial Secretary in the Ministry of Finance and Public Service and is in charge of Strategic Human Resource Management. Mr. Jones is an accomplished Human Resource Practitioner with over thirty-five years’ of experience in the field of Industrial Relations and Employment Management. He is a graduate of the University of the West Indies, City & Guild Institute of London, and a certified Change Management Specialist.

Mr. Jones is a former President of the Jamaica Civil Service Association (JCSA) and General Secretary of the Jamaica Confederation of Trade Unions (JCTU). At the regional and international levels, he held the presidency of the Caribbean Public Services Association and sat on the Executive Board of Public Services International as representative of the InterAmericas Region. He is also the recipient of an Oder of Distinction by the Jamaican Government and is a Director of FHC Credit Union.

Mr. Francis, a Commissioned Land Surveyor and a Class 1 Hydrographer, is an Associate of the Royal Institution of Chartered Surveyors. His work experience includes the management of the Survey Department as Deputy Director of Surveys, serving as a consultant in Dredging Engineering, Consultant to the Commonwealth Secretariat and the United Nations and serving as a Lecturer at the University of Technology.

Educated at the University of the West Indies, University College London, University of Toronto, Texas A&M University and Nova Southeastern University. Mr. Francis’ qualifications include a Bachelor’s of Sciences Degree (BSc.) and a Master of Arts in Business Administration (MBA).

Mr. Francis currently serves on the Board of the Jamaica Copyright Agency as Treasurer and sits on the Past Due Committee of FHC as well as the Board of Directors. Mr. Francis has been honored by the Jamaican Government with an Order of Distinction.

PROFILE OF BOARD OF DIRECTORS

Mr. Ewan is currently the CEO of 138 Student Living Jamaica Limited. He is a certified accountant, a Fellow of the Association of Chartered Certified Accountants (ACCA) and holds a Master’s Degree with a concentration in Finance from the Manchester Business School (UK). Mr. Ewan has vast experience in several industries, spanning Accounting, Shipping, Education, Energy Efficiency, and the Distributive Trade. His expertise includes accounting, finance, management consulting, human resource management, facilities management and leadership.

He is presently the Treasurer on the Board of Directors, Director of FHC Investments Limited and the Chairman of the Finance and Operations Committee.

Mr. Ranger is a Chartered Accountant, a member of the Association of Chartered Certified Accountants (ACCA) in the United Kingdom and a member of the Institute of Chartered Accountants of Jamaica (ICAJ). He has over fifteen years’ of experience in external and internal auditing, accounting and business operations. Mr. Ranger has worked with PricewaterhouseCoopers, Boldeck Jamaica Limited and the Neal and Massy Group, specializing in audit and assurance, accounting and income tax services.

He is presently the Principal of Ranger and Associates and previously served as a volunteer in the capacity of a member of the Credit Committee. He is a Director of FHC Credit Union.

PROFILE OF BOARD OF DIRECTORS

Ms. Walsh is currently the Executive Director of the Students’ Loan Bureau. She is a qualified Accountant, a Fellow with the Institute of Chartered Accountants of Jamaica and a member of The Association of Chartered Certified Accountants (ACCA).

Ms. Walsh possesses over 15 years of accounting and finance experience and has performed on assignments within various government sectors. Her expertise includes accounting, finance, management consulting, human resource management, strategic planning and leadership.

Mrs. Ricketts-Moore possesses over 18 years’ experience in the field of Accounting, Internal Auditing and General Business Operations, acquired mainly from the manufacturing, distribution and retail industries. She previously worked with the Grace Kennedy Company Limited for 11 years and is currently the Managing Director of Sangster’s Book Stores Limited.

Mrs. Ricketts-Moore is a Chartered Accountant and holds a MBA from the Manchester School of Business. She is also a Certified Information System Auditor (CISA) and a Certified Internal Auditor (CIA).

She previously served as a Volunteer in the capacity of Chairperson on the Supervisory Committee at First Heritage Co-operative Credit Union Limited and is a Director of FHC Credit Union.

PROFILE OF BOARD OF DIRECTORS

The Honourable Mr. Justice Evan Brown, Judge of Appeal, is a highly accomplished legal professional with a distinguished career in the Jamaican legal system. In 2010 he was appointed to act as a Puisne Judge, a role he held until 2012. He rose through the ranks within the judiciary and was elevated to the post of Judge of Appeal in 2022.

With over three decades of legal experience, the Honourable Justice of Appeal has presided over numerous cases, demonstrating a commitment to the principles of justice and fairness. His extensive legal knowledge and expertise makes him a highly respected member of the Jamaican legal community and his appointment to the Court of Appeal is testament to his dedication and hard work.

Mr. Richards is a driven and accomplished professional with extensive experience in international development, finance, and strategy consulting. He is a graduate of SOAS, University of London with a Master of Science in Development Studies (Economics) and a Bachelor of Arts in Economics and French from Vassar College in the United States.

At the Inter-American Development Bank, Mr. Richards served as a trusted advisor to the Executive Director for the Caribbean and the Minister of Finance Jamaica, approving loan and guarantee proposals, shaping the team’s knowledge on private-sector operations, policies, diversity, equity, and inclusion. Mr. Richards is a Maguire Fellow, a Distinguished Delegate at the National Model United Nations, a Davis Scholar, and a Shirley Oakes Butler Scholar.

BOARD OF DIRECTORS’ REPORT

We are immensely pleased with the high level of performance of First Heritage Co-operative Credit Union Limited (FHC) throughout 2023. The year was characterized by the accomplishment of several milestones, attributable to the sustained commitment of the Management Team and wider FHC team members, coupled with the ongoing support and strategic direction of the Board of Directors. As the island begin to see significant signs of recovery from the COVID-19 pandemic, there was a distinct uptick in the demand for FHC’s products and services. Alongside this, we saw conservative, but encouraging numbers in membership growth and business from new members which would also have contributed to our success. We remain grateful for our members who have been highly supportive of our organization and we continue to place them at the centre of our decision-making process; ensuring that each touch point supports our thrust towards accessibility, inclusivity and financial wellness.

We closed the 2023 financial year having realized a surplus; of note, we also experienced the highest volume of loan disbursements in a single month in the history of our Credit Union for three months consecutively, greatly surpassing our aspirational target. Aligning closely with this, has been the review of our operational capacity and procedures by our Management Team, ensuring that the organization was suitably resourced to offer the highest level of service to meet the demand of our members. While our loan performance has been noteworthy, we have also retained a keen focus on the growth of our deposit portfolio, both with a view to encouraging our members to continually enhance their financial wellbeing, as well as to bolster liquidity.

Our Board of Directors continues to be inspired by the leadership team and remains confident in the capability of our team members to deliver the highest standard of service and the best products within the financial industry, to our members and clients alike. Our commitment to excellence drives our spirit of innovation, as we distinguish ourselves as a dynamic firm with a hallmark of innovation and elevate the standard of success for our Credit Union; taking pause only, to celebrate our accomplishments along the way.

FINANCIAL PERFORMANCE

The 2023 financial year closed with exceedingly positive results, of which we are proud as a collective entity. Our Credit Union achieved a Net Surplus of $330.66 Million as against $184.25 Million in 2022.

BOARD OF DIRECTORS’ REPORT

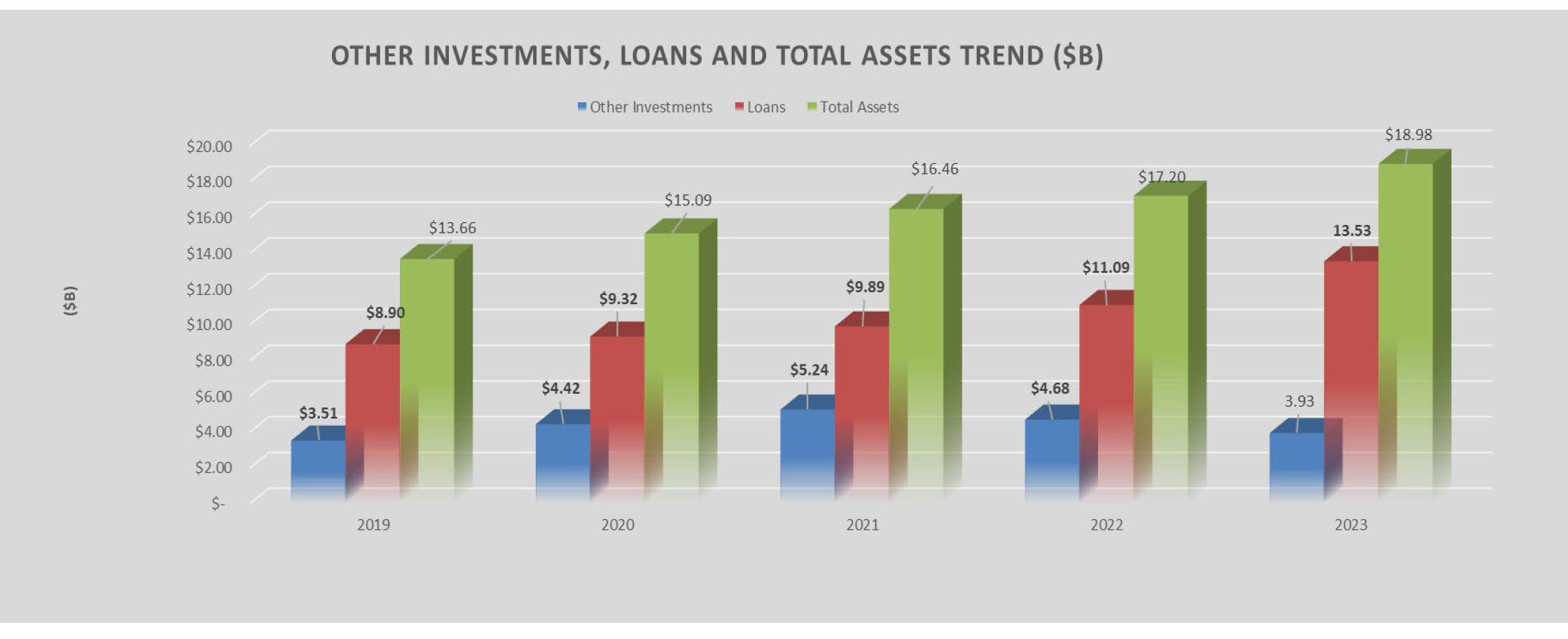

Additionally, the Company’s asset base grew to $18.98 Billion, up from $17.19 Billion in 2022, a stellar performance attributable to increased support from our members through the uptake of our products and services. We would also have seen a modest increase in new membership and business from new members, which drove our improved position year over year.

In anchoring our performance for longevity, our Management Team engaged in a number of initiatives to drive our deposit taking activities. Notably, the market has seen a shift to most financial institutions seeking to enhance their liquidity position, given the favourable loan interest rates that would have been accessible throughout the market in recent years. While interest rates generally began to increase, recovery from the COVID-19 pandemic spurred heightened economic activity and as such, the market actively pursued both personal and business goals, thus driving the uptick in demand for loan services. We believe that our Credit Union has been proactive in creating a balance between our lending and deposit taking activities and with the continuation of this, we anticipate the steady growth of both segments of the business over the coming financial year.

STRATEGIC VISION

The Board of Directors, Committees and leadership team remain committed to realizing our 2040 Vision. In executing our annual review and alignment with our three-year strategic plan to advance vision 2040, we developed a robust plan for 2023 to 2026 having delivered on our 2021 to 2023 plan over the past three years, with some core initiatives being retained and advancing into the new strategic plan.

Technological solutions remains a crucial part of our strategy to attract and retain young members; having established our Digital Transformation Roadmap, the team has commenced preparations to aggressively execute on these initiatives in financial year 2024 onwards. Concurrently, as we seek to explore expansion into the diaspora markets, our technological interventions will enable a new level of accessibility to FHC Credit Union and support our omni-channel framework.

OUR SUBSIDIARY

FHC Investments Limited (FHCIL)

In 2023, the Jamaican economy continued on its positive growth path. Preliminary data from the Planning

BOARD OF DIRECTORS’ REPORT

Institute of Jamaica (PIOJ) revealed that Jamaica’s national output grew by 2.6% during the calendar year 2023, when compared to the similar period of 2022. The improved performance resulted largely from improved tourism arrivals, increased alumina production, a stronger labour market and robust remittance inflows as the economic conditions of our main trading partners, primarily the US, remained resilient despite the tighter financial climate. The positive contribution from these key areas helped offset the downward pressures on national output from tight domestic monetary policy and adverse weather conditions that weighed on agriculture. This positive economic performance, when combined with the government’s strong commitment to prudent fiscal policies and debt reduction, led to the country’s credit rating being upgraded to ‘BB-‘ STABLE. For the remainder of fiscal year 2023, Jamaica’s positive economic growth is expected to continue, albeit at a moderate pace, with Fiscal Year 2023/2024 GDP growth expected to be around 1.7%.

As the private sector continued to expand business activity to fulfil the growing consumer demand, businesses have increased their demand for labour, which resulted in the record low unemployment rate of 4.5%, achieved in July 2023. Throughout the 2023 calendar year, it was observed that the Bank of Jamaica’s efforts to lower elevated inflation was yielding success as the inflation rate declined from 8.1% in January to 6.9% in December. During this period, the point-to-point inflation rate was within the BOJ’s 4% to 6% target band on three readings. Rising transport costs ticked annual inflation higher, reaching 6.9% in December 2023, which is the highest level since February 2023 and above the BOJ’s target band.

FHC Investments Limited (FHCIL) recorded a decline in financial performance for the year 2023 which was primarily attributable to the continued challenging macro-economic conditions, spurred by the ongoing war between Russia and Ukraine and characterized by rising inflation, increasing interest rates and the resultant reduction in liquidity conditions in the market. FHCIL recorded a 19.30% decline in Net Interest Income of J$2.94 Million over the corresponding period for the financial year ending December 31, 2023. Other Income decreased significantly compared to the prior year, due to the fair value losses on local stocks.

Net Loss before taxation for the year ended December 31, 2023 was $44.26 Million, which compares unfavorably against Net Loss of $38.82 Million reported for the same period in 2022. The decline in

BOARD OF DIRECTORS’ REPORT

profitability was mainly attributable to an 8.83% decrease in Net Interest and Other Income, when compared with the prior year. As inflation rose, yields on global corporate and sovereign debt followed, which adversely impacted the value of these assets in the investment portfolios and reduced the potential for trading gains. Furthermore, as global recessionary fears led to a substantial contraction in demand for investment products, this resulted in a falloff in fee based income, categorized in the Other Income category of revenues. This is in contrast to the prior year when investor sentiment was moderately high and interest rates were low.

The Funds Under Management declined by 9.74% year over year to $3.11 Billion. The general weakness in market conditions and lower asset prices tempered the growth in the Assets Under Management, both in the fixed income and equity markets, when compared to the similar period last year. No significant deterioration in the credit quality of the company’s assets occurred in the financial year.

FHC Retirement Scheme

The FHC Retirement Scheme has experienced commendable incremental growth, a testament to the diligent efforts of the FHCIL team and the strategic oversight of our Board of Directors. We are pleased with the consistent progress made in enhancing the scheme’s value and are confident that the upcoming strategic initiatives will further solidify this positive trajectory.

Growth was experienced in all respects as 95 new members were enrolled when compared with 92 in the prior year. While Members’ contribution totaled $154.12 Million which was a 0.72% decrease over the prior year, Net Assets Available For Benefits grew by 7.05% to end the year at $1.57 Billion.

Our commitment to robust financial stewardship and innovative planning positions us well for continued improvement, ensuring that the FHC Retirement Scheme remains a trusted and secure choice for our members’ future.

Investment Industry Outlook

Global growth is expected to slow in 2024. This general slowdown of growth in US and China, two of our key trading partners, combined with still high interest rates, underscore what will continue to

BOARD OF DIRECTORS’ REPORT

be a challenging environment for local financial institutions. In addition, we do expect some level of uncertainty to continue as geopolitical unrest and global inflation persist. Notwithstanding, we expect the Bank of Jamaica to begin interest rate cuts in the second half of the year as inflation continues to cool. Jamaica’s GDP growth for the 2024 fiscal year may be supported by several factors such as strong tourism demand, the record low unemployment level and increased wages under the government’s restructuring exercise which may drive consumer spending. The local economic recovery is expected to continue but we believe that it will be constrained by the Bank of Jamaica’s steps to control inflation and currency devaluation through interest rates. Current and past Administrations have shown a commitment to improving key fiscal metrics, setting the framework for business and investor confidence.

As we look into 2024, we are taking the opportunity to continue positioning ourselves for sustainable growth over the long term by accelerating the building out of our Non-Interest Income streams. We have been making strategic investments in our team and processes with the goal of fostering a highperformance culture and winning team mindset, conditions which we believe are conducive to delivering excellent, trustworthy service to our clients. We are confident that these investments will position us for sustainable, long term growth. These strategic initiatives include refining our processes and improving the service delivery throughout our channels with the aim of making it easier to do business with us.

FHC FOUNDATION

Our Board of Directors is pleased that, throughout 2023, we donated a total of $1.87 Million to 17 recipients as a part of our annual Scholarships, Bursaries and Grants, namely our Primary Exit Profile (PEP), Oswald Thorbourne and Renald Mason Scholarships, along with the FHC Sports Education Scholarship.

The then, newly minted FHC Sports Education Scholarship, was awarded for the very first time to a student of the G.C. Foster College of Physical Education & Sport who is pursuing studies to attain a Bachelor of Education in Physical Education and Sport. The scholarship is valued at approximately $500,000 and will see the recipient going on to undertake various engagement activities as an ambassador for FHC Credit Union while he continues to pursue higher education.

Our Entrepreneur Awards grants valuing $1.5 Million were successfully awarded to the 2022 recipients. Having enriched last years’ programme to include, for the first time, a two day Incubator Session, with one of Jamaica’s most outstanding Business Coaches; the 2023 staging saw this Incubator Session extended

BOARD OF DIRECTORS’ REPORT

to three days to facilitate expansion of the curriculum and now also includes a quarterly temperaturecheck.

We congratulate all our beneficiaries, members and YOUTH Savers, and encourage them to continue to demonstrate an exemplary level of work, dedication and commitment to success.

Since 2013, when the FHC Foundation was established, it has continually upheld its mission to promote the development of young Jamaicans through our three pillars Youth, Education and Sport; with Sports Education as a core thematic area. With this in mind, the FHC Foundation continues this new focus with a view to sifting out opportunities and aligning with or creating initiatives that will see the Foundation focusing on Sports Education amongst the youth population.

THE WAY FORWARD

As we look to the future, the Board of Directors is committed to working closely with the Management Team to chart a strategic course that will drive the company forward. Together, we will develop and execute a series of initiatives aimed not only at fostering growth within the local market but also expanding our reach into the diaspora. This forward-thinking approach is designed to enhance our market presence and capitalize on new opportunities, ensuring sustainable success and long-term value for all our stakeholders.

BOARD OF DIRECTORS’ REPORT

In this next phase of our journey, our focus will be on leveraging our core strengths while exploring innovative avenues for growth. By harnessing the collective expertise of our Board and Management Team, we will implement strategies that align with emerging trends and meet the evolving needs of our members both locally and abroad. This expansion into the diaspora represents a significant milestone in our company’s evolution, and we are confident that our strategic initiatives will position us as a leader in this new frontier, delivering value and enhancing our competitive edge.

Technology

As we move forward, advancing our strategic initiatives around technological solutions and integration will be a key priority. We are committed to adopting and implementing cutting-edge technologies that will enhance our service delivery, streamline operations, and provide our members with more efficient, seamless experiences. By integrating these advanced solutions, we aim to better serve our members, offering them omni-channel access to the Credit Union using innovative tools that meet their evolving needs in an increasingly digital world.

Cybersecurity

In tandem with our technological advancements, we will place a strong emphasis on bolstering and strengthening our cybersecurity measures. We note that globally, cyberattacks have been sharply on the rise, constituting a trillion dollar business. As an organization, earlier this year (2024) we experienced the effects of this increasing challenge when we faced a system outage. The outage would have resulted in loss of access to business by our members for three days. Our Board commends the swift and focused action of the Management Team and team members in restoring member services. Since then, we have and continue to take steps to identify optimal solutions that will mitigate the recurrence of this cyber event; and remain vigilant knowing that attempted cyber-attacks remain active in the space, and that it is only through the implementation and sustenance of robust defenses, that we can continue to safeguard the assets of our members and organization alike.

Protecting our members’ information and our organization’s assets is of paramount importance, and we are continually investing in vigorous cybersecurity infrastructure to guard against emerging threats. Our proactive approach will ensure that our members can have confidence in the safety and security of their data, as we continually monitor and enhance our defenses to stay ahead of potential risks.

BOARD OF DIRECTORS’ REPORT

Member at the Centre

At the heart of all our initiatives is a steadfast commitment to our members. We will continue to foster and embody the spirit of “Member At The Center” ensuring that every decision we make, every product and service we offer, and every enhancement to our operations is guided by the goal of enriching our members’ experience. By placing our members as the focal point, we are dedicated to delivering personalized, high-quality service that meets their unique needs and exceeds their expectations at every touchpoint.

RECOGNITION

The Board of Directors is pleased to extend our heartfelt gratitude to the entire team for their exceptional dedication and hard work throughout the year 2023. Your unwavering commitment to excellence has driven our business activities and initiatives to new heights, ensuring that we continue to thrive and achieve our strategic goals. Your collective efforts have not only strengthened our market position but also fostered innovation and resilience within our organization. It is with immense pride that we acknowledge the outstanding contributions of each team member, whose diligence and perseverance have been instrumental in our success.

We would like to particularly recognize the efforts of the Executive Team, whose visionary leadership has guided us through the complexities and challenges of the past year. Their strategic foresight and ability to adapt to changing market dynamics have been critical in steering our company towards sustained growth and profitability. Additionally, our middle management and operational staff have been the backbone of our daily operations, ensuring seamless execution and maintaining the high standards that our stakeholders have come to expect. Your collaborative spirit and unwavering dedication have been pivotal in driving our projects and initiatives to fruition.

Lastly, we extend our sincere thanks to the Board of Directors and Volunteers for their steadfast support and invaluable insights. Your guidance and strategic direction have been paramount in shaping our business strategies and ensuring our long-term success. The collective wisdom and experience that you bring to the table have been the cornerstone of our achievements throughout 2023. As we reflect on our accomplishments and look forward to the future, we remain deeply grateful for the commitment and excellence demonstrated by our entire team and the steadfast support of our Board and Committees.

Thank you for your unwavering dedication and contributions to our continued success.

ORGANIZATIONAL OUTLOOK

Our outlook for the coming financial year remains optimistic. Despite ongoing global economic uncertainties, such as geopolitical tensions and supply chain disruptions, the market has shown resilience. Inflationary pressures are beginning to ease, and interest rate hikes by central banks have started to stabilize. This stabilization is crucial for maintaining investor confidence and ensuring steady growth in various sectors, including real estate and consumer finance, which are vital to our Credit Union’s portfolio.

On the economic front, the labor market continues to demonstrate strength, with unemployment rates remaining low and job creation steadily increasing. Consumer spending, a critical driver of economic growth, has been robust, supported by rising wages and strengthened household savings. However, it is essential to monitor potential risks, such as the possibility of an economic slowdown or recession, which could impact loan demand and repayment rates. Our Credit Union must remain vigilant and adaptive to these economic shifts to safeguard our members’ financial well-being.

Looking ahead, our Credit Union is well-positioned to navigate the evolving financial landscape enabling us to secure our legacy of a solid past and a secure future for our members. We are committed to leveraging our strong capital position and prudent risk management practices to capitalize on growth opportunities. Strategic investments in technology, member services and member satisfaction will continue to enhance our competitive edge. By maintaining a focus on sustainable growth and financial stability, we aim to deliver long-term value to our members and ensure the continued success of our Credit Union in an ever-changing economic environment.

Chairman, Board of Directors

EXECUTIVE TEAM

MANAGEMENT DISCUSSION & ANALYSIS

A Year of Remarkable Performance

In 2023, our company embarked on a journey of exploration, growth, and achievement under the theme “New Horizons…Dream, Dare, Deliver”. This theme encapsulated our collective aspirations, our boldness in pursuing them, and our commitment to achieving them through focused strategies. As we reflect on the year gone by, we are proud to report that our company has not only met but exceeded the goals we set out to achieve. Our performance has been nothing short of exceptional, and we are excited to share the highlights of our achievements.

FINANCIAL PERFORMANCE