• Forecasting the Future of REO Markets: What the Next 5 Years Hold

• Buyer Behavior Shift: From Fixer-Upper Favorability to Turnkey Demand in REOs

• Preparing REO Buyers for Longer Sales Cycles: A Financial Guide

• Regional REO Hotspots: Texas, California & Florida Lead the Pack

• From Listings to Showrooms: Bringing REO Properties to Life with Home-Staging Trends

• Tech-Enhanced REO Hunting: How Analytics Are Reshaping How Agents Spot Bank-Owned Deals

• REO Myths Debunked: You Don’t Need Perfect Credit to Buy Foreclosures

• How Lowering Mortgage Rates Could Shift REO Market Dynamics

• Where REO Discounts Are Deepest: A State-by-State Analysis

• REO-to-Rental: A Strategic Pivot for Investors and Lenders

• The Lock-In Effect: Why Homeowners Staying Put Boosts REO Listings

• REOs Meet Affordability Pressures: How Price Trends Are Shifting Bargain Dynamics

• Cooling Listings and Rising Patience: What Slowed Sales Mean for REO Investors

• Myth-Busting REO: Debunking Misconceptions About Bank-Owned Homes

• REO Reality Check: Is Rising Foreclosure Activity Signaling Opportunity or Risk?

As summer fades and we step into September, the real estate industry enters one of its most critical periods of the year. With fall traditionally marking a pivot point in housing activity, professionals across the country are weighing interest rate trends, affordability constraints, and the steady demand for housing against an uncertain economic backdrop. In California, the pressure remains high: inventory is still limited, buyer sentiment is cautious, and investors are eyeing distressed assets with renewed focus. These same conditions ripple nationwide, shaping strategies for brokers, lenders, and investors as we approach the final quarter of 2025.

Welcome to the September edition of the REOBroker.com Real Estate Magazine, where we connect national policy updates with the realities of local markets. This issue delivers essential press releases and updates from industry leaders, including the National Association of Realtors (NAR), the U.S. Department of Housing and Urban Development (HUD), Fannie Mae, Freddie Mac, and other key organizations. From regulatory shifts to mortgage market forecasts and affordability initiatives, the information in these pages is designed to help you stay informed and strategically ahead.

Our continuing coverage of the REO sector remains front and center this month. As property values adjust and loan performance shows early signs of softening in some regions, REO brokers and investors are finding opportunities that demand both speed and precision. Articles in this issue highlight lender pipeline updates, pricing trends, and innovative disposition strategies to help you remain competitive in a marketplace that rewards preparation and adaptability.

September also marks the ramp-up of major industry gatherings that define the second half of the year. This issue includes a spotlight on what’s ahead in Q3 and Q4:

�� The Five Star Conference & Expo

�� Dallas, TX | Sept. 29 – Oct. 1

The leading event for the default servicing and REO industry, offering education, networking, and access to the decision-makers shaping the future of asset management.

�� NAR NXT: The REALTOR® Experience

�� Boston, MA | Nov. 3–5

Hosted by the National Association of Realtors, this event will provide critical market insights, compliance guidance, and tech-driven tools to strengthen your practice.

�� AAPL Annual Conference

�� Las Vegas, NV | Nov. 10–11

A must-attend for professionals in private lending, note investing, and REO acquisitions, featuring in-depth discussions on capital markets and portfolio growth strategies.

This September issue is designed not only to inform, but to empower. Whether you’re structuring new deals, positioning for end-of-year opportunities, or building long-term strategies, our mission at REOBroker.com Real Estate Magazine is to ensure you have access to the updates, tools, and insights that matter most.

Thank you for your continued readership and trust in us as your resource for REO and real estate intelligence.

Stay focused, stay informed and stay ready.

Asset Managers rely on REObroker.com to consistently find the nation's top REO specialists. We pre-screen our members for years of experience, training & certification, and asset manager references, holding each application to the highest standards.

The Benefits of Membership

In addition to the clear benefits of our referral network, REObroker.com members receive training, networking & advertising opportunities, and a wealth of pay-it-forward knowledge from our daily Member Discussion Forum.

REObroker.com is an esteemed designation and valuable association. Many of our members have stayed with us consistently through several REO cycles, realizing the long-term benefits.

Member Benefits

Minimum of 2 (BD) Broker Development Seminars a year

REOBroker.com Member Benefits

Minimum of 2 (BD) Broker Development Seminars a year

Access to a Minimum of 2 Zoom mastermind/training calls a month

Access to asset management company Roster

Access to Private Lender Roster

The internal chat line provides access to a wealth of knowledge and support through our diverse membership.

REOBroker.com does sponsorships with NADP, 5 Star, and other related Events.

National Exposure to asset managers and companies

Included on the REOBroker.com website with contact information and areas served

Included in REOBroker.com online HUD and Real Estate Magazines and National Campaigns

Opportunities to submit market updates and real estate articles in the magazines.

Membership benefit pricing for additional advertising in the following:

REOBroker.com HUD Magazines | REO Broker Real Estate Magazine | REOBroker TV | and Podcast.

Bob Zachmeier

Clay Strawn

Jeff Miller

Julie Bruckner

John Mason

Bob Siegmeth

Brandy Nelson

602-810-1561

480-250-0131

ARIZONA

Tucson Chandler Mesa Tempe Arizona Arizona

909-226-8038 Phoenix Arizona

602-810-1561

Lake Havasu Arizona

ARKANSAS

501-985-0755

Pulaski Lonoke & Surrounding Arkansas

CALIFORNIA

818-425-0330

760-238-0552

Darrell Isaacs 209-649-8593

David Roth

Deanna Lantieri

Dennis Mulvihill

Don Kelber

Elysia Moon

Gina Bocage

James Outland

Joe Mayol

John Costigan

Justin Potier

Mike Potier

707-446-1211

Porter Ranch

Palm Desert/Palm Springs

Stockton/San Joaquin County California

Vacaville California

760-924-5091 Mammoth Lakes California

408-489-2904

805-338-9682

949-212-6474

510-552-6480

805-748-2262

661-618-1442

619-990-3044

562-480-9884

562-708-0870

Los Gatos California

Westlake Village California

South Orange County California

Fremont / East Bay California

Pismo Beach California

Lancastor California

San Diego / El Cajon California

Los Angeles County California California

Long Bch South Bay

Pete Nyiri

Richard

Ronald

Sigifredo Ponce 805-895-1109

Timm

Tom

Warren

Yolanda

COLORADO

CONNETICUT

DELAWARE

FLORIDA

Joseph Doher

Michelle Pietrzyk

Patricia Orsini

GEORGIA

IOWA

ILLINOIS

INDIANA

KANSAS

KENTUCKY

LOUISIANA

MICHIGAN

MINNESOTA

NEW JERSEY

NEW MEXICO

RHODE ISLAND

SOUTH CAROLINA

TENNESSEE

VIRGINIA

WASHINGTON

WISCONSIN WASHINGTON

REOBROKER TV

Picture a landscape where opportunity surfaces in unexpected corners where bank-owned properties quietly shift from overlooked inventory to strategic assets. The realm of REO properties holds such intrigue for investors, agents, and property managers. As we look ahead to the next five years, understanding how this sector will evolve becomes essential for anyone aiming to thrive in the real estate field. Recent housing market studies suggest that while home sales may see modest upward movement, price gains are expected to flatten. This backdrop frames the REO market’s likely trajectory through 2030. In this post, we’ll explore what moderate sales growth coupled with subdued price appreciation means for REO strategies nationwide, offering clarity on how to position for the future in this pivotal market segment.

Sales Growth Amid Flat Price Trends

Analysts anticipate that existing home sales will climb steadily in the coming years. Forecasts show a 7–12% increase in sales in the near term, with even stronger momentum expected further out. At the same time, projections from multiple sources point to a slowdown in home price appreciation expected to hover at roughly 3–4% annually, a noticeable dip from prior years. Additional estimates suggest this moderate trajectory may extend into the latter half of the decade as affordability slowly improves. These dual trends rising transactions paired with softer pricing shape a predictable environment for REO activity.

What This Means for the REO Market

With sales rising and prices plateauing, REO properties could become more competitive but only for the well-positioned. Auction volume is expected to decline; as of early 2025, REOs fell about 25% year-over-year, though short-term foreclosure starts ticked up by approximately 1%. Forecast models from auction platforms suggest a continued downward trend of around 8% in distressed auction volume this year, under baseline conditions. - Lower foreclosure rates suggest that REO inventory may tighten, even as demand stabilizes especially if home equity and borrower resilience remain strong.

Strategic Implications for Stakeholders

Investors: With fewer REO listings expected, competition for available properties could increase. Savvy players may need to act swiftly on new listings and maintain strong relationships with lenders and servicers.

Agents: Success may hinge on quick access and marketing precision With supply tight, differentiating REO listings through staging, accurate pricing, and targeted outreach will matter

Property Managers: Efficient management of REO assets handling repairs, clean-outs, and listing preparation promptly will give you a competitive edge in a lean market.

Collectively, these trends signal a market where volume gains will rely on efficiency and timing, while price stability reinforces need for strategic focus rather than speculative upside.

In summary, the coming half-decade offers a measured but promising horizon for REO markets. As home sales improve modestly and pricing growth remains subdued, the REO landscape may narrow, becoming more competitive and precision-driven. For those prepared to act decisively whether through quick listing cycles, optimal marketing, or seamless management this environment offers consistent opportunity. The key will be in watching market indicators, forging trusted connections, and staying nimble as conditions evolve through 2030

If you’re ready to navigate the changing landscape of REO markets with confidence and insight, let us support your journey. At REObroker.com, we specialize in connecting investors, agents, and property managers with real opportunities in this sector. Visit our website at https://www.reobroker.com or reach out directly via email at info@reobroker.com or call us at 760-238-0552.

Let’s explore how strategic guidance and timely access can elevate your success in the years ahead.

In today’s real estate landscape, something noteworthy is unfolding. Investors, agents, and property managers are witnessing a shift in buyer behavior: homes that once attracted DIY enthusiasts are being sidelined in favor of fully prepared, ready-to-go properties. This trend matters because it signals a fresh reality in the REO (real estate owned) market one where speed and convenience increasingly outweigh the charm and potential of fixer-uppers.

Gone are the days when buyers gravitated toward properties labeled “needs work” or “fixer,” drawn by lower purchase prices and renovation promise. Today, especially in 2025, there’s growing appetite for homes that require no immediate repairs homes that buyers can simply walk into and begin living in or renting out. This article explores the forces behind this change, examines its impact on REO buyer profiles, and offers insights for professionals navigating this evolving terrain. We’ll look at the data driving buyer preference for move-in ready homes, the market conditions fostering this trend, and what it all means for stakeholders across the board.

A Clear Turn Toward Move-in Ready Properties

Market data shows a decisive pivot. Recent findings reveal that remodeled homes are generating about 26% more “saves” on listing platforms than fixer-upper properties, while listings labeled in need of repair have seen their sale-price premiums shrink to a 7–8% discount the largest decline in years. Buyers now appear willing to pay close to 4% more roughly $13,000 extra for homes that are already updated.

Why Demand Is Shifting

Several factors underscore this shift:

Rising renovation costs and labor shortages are making buyer-led rehabs less appealing With materials and contractor rates climbing, many prefer to avoid the hassle entirely.

Economic uncertainty and cautious borrowing behavior have buyers favoring straightforward investments, particularly as mortgage rates remain a concern; yet, they’re preparing for gradual downward movement too.

Increased inventory nearly 25% year-over-year growth means more options, but properties presented in excellent condition still sell fastest, encouraging buyers to act quickly.

Implications for REO Buyer Profiles

The traditional REO buyer seeking discounted homes to restore and resell or rent is now sharing the stage with a growing cohort focused on turnkey listings. These buyers, often investors or occupants with limited appetite for renovation, want assurance of quality, lower risk, and immediate usability. Financing also plays a role: bundling repair costs into standard financing spreads out expenditures, whereas cash renovations require upfront capital and carry more uncertainty.

Agents, investors, and property managers should take note. Presenting REO homes as turnkey highlighting recently completed updates, warranties, or staging can dramatically enhance appeal. Renovation budgets should be carefully considered, and quick cosmetic touches may produce outsized returns In short, the buyer lens has shifted: movein readiness now often trumps the “potential” narrative once tied to fixer-uppers.

In 2025, the REO market is undergoing a noteworthy transformation. Buyers particularly investors and ready-to-occupy occupants are demonstrating a clear preference for homes that require little to no work. Renovation costs, market uncertainty, and attractive financing options for updated properties contribute to this shift away from fixeruppers. For agents, property managers, and investors alike, recognizing and adapting to this tilt toward turnkey demand is critical. Emphasizing convenience, minimizing friction, and investing selectively in cosmetic upgrades or ready-to-go presentation may yield stronger interest and faster turnovers.

If your work involves navigating this evolving REO market whether sourcing, presenting, or managing properties let REObroker.com be your partner in success. At REObroker.com, we specialize in showcasing and connecting investors, agents, and managers with REOs that match the modern demand: move-in ready, efficiently presented, and valueconscious. Explore our listings and resources at https://www.reobroker.com or reach out directly via email at info@reobroker com or call us at 760-238-0552 We’re here to help you stay ahead in today’s market and turn opportunities into quick, confident transactions.

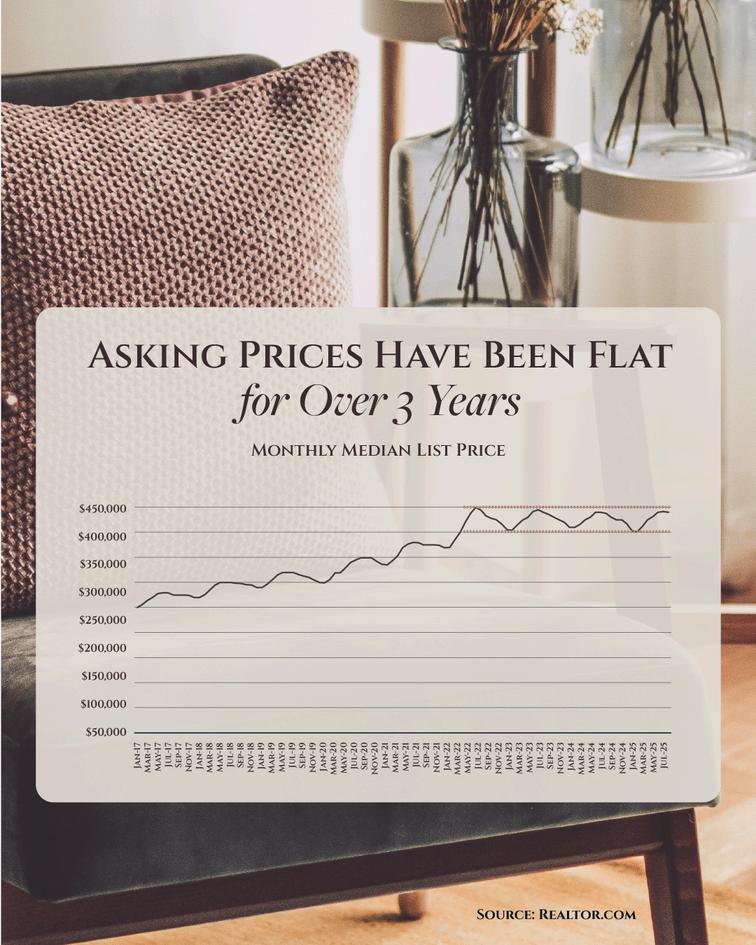

If your listing isn’t getting traction, here's what you need to realize. Homes are sitting longer today. And one of the reasons why?

Overpricing like it’s 2021 again. Unlike a normal market where list prices keep rising, they’ve actually been flat for over 3 years. And that’s a change worth paying attention to.

List prices have leveled off because buyers are being more selective as inventory has grown over the past few years. There are more homes on the market, and sellers need to take note.

So, if your home isn’t getting showings or offers, take it as a sign to check in with your agent. A small price adjustment could be the move that gets buyers through the door.

Because in a market like this you can’t just wait it out and hope for the best. Patience won’t sell your house. But the right price will.

exposure holding costs, inspection delays, and tough negotiations can all threaten your bottom line. Understanding how to navigate these longer sales cycles effectively isn’t just smart it’s essential.

This article will guide you through the essentials of budgeting for carrying costs, allocating resources for inspections and repairs, and negotiating strategically when the pace slows. You’ll walk away with clear, actionable strategies that keep your finances on track, even when sales drag. Ready to master the extended timeline? Let’s dig into the financial roadmap designed to protect profits and drive success.

1. Budgeting for Carrying Costs

2. Prioritizing Inspection and Repair Planning

In slower markets, inspections offer a unique advantage: negotiating power. A thorough pre-offer inspection if permitted can uncover hidden repair needs and form the basis for either major concessions or a walk-away strategy. Agents and investors frequently overlook this step and end up overextended. Always plan for both cosmetic and structural budget contingencies. Choosing contractors early and locking in quotes can help you manage timelines and cost escalation during slower sale periods.

3. Strategic Negotiation in a Slower Market

Extended listing durations often position sellers banks or lenders to be more flexible. To leverage that, support your offers with solid market data. Conduct a comparative market analysis to highlight why your price is fair and grounded in recent sales. Show that you’re serious: secure pre-approval or demonstrate access to funding, be it cash or hard money, to strengthen your negotiating stance. Remember that REO sellers usually provide limited contingencies, short inspection windows, and insist on “as-is” terms so be ready but realistic.

4. Examples and Realistic Scenarios

Imagine a property listed at a 20% discount in an open market. Holding costs of $1,500/month over 3 extra months can cut deeply into that margin. By negotiating a reduction based on estimated repair needs and slower buyer interest, you might recover $5,000–$10,000 and still stay profitable.

In another case, bringing in a trusted contractor early could reveal roof or foundation issues knowledge you can use for stronger negotiation leverage or choose to walk if the risk outweighs the reward

These scenarios illustrate how preparation and clear financial margins can shift a slower market from threat to opportunity.

Longer sales cycles in bank-owned property markets are not just challenges they’re opportunities to sharpen financial strategy By planning realistically for carrying costs, leveraging inspections, and negotiating with precision, investors, agents, and managers can protect profitability and even gain advantage The key is preparation: building in buffers, anticipating delays, and staying ready to pivot.

With the right outlook, what may seem like extended holding periods can instead become calculated moves toward a more secure and rewarding deal

If you're looking to navigate the complexities of bank-owned property investing with confidence and clarity, REObroker.com is here to help. At REObroker.com, we specialize in providing expert guidance that helps you budget wisely, assess properties thoroughly, and negotiate advantageously even when markets slow. Reach out to us via info@reobroker com or give us a call at 760-238-0552 to start building a smarter, smoother strategy for your investments because every day you wait should move you closer to profit, not farther from it

In the current real estate market, regions where bank-owned properties (REOs) cluster are capturing keen interest from investors, agents, and property managers. Right now, three areas stand out as the most active REO hotspots, drawing attention for both challenge and opportunity. With significant numbers of REOs emerging, professionals need to understand not just the data, but how to respond strategically at the local level.

Recent data from July 2025 highlights how concentrated REO activity has become, with Texas recording 377 bank repossessions, California following closely with 360, and Florida reporting 241. These figures point to markets under stress but also to windows of potential for savvy players. This article will first unpack where REOs are most concentrated and then offer tailored strategies that agents and investors can deploy in these regions. By examining real numbers and local trends, we’ll clarify how to approach these hotspots with an informed, opportunity-driven mindset.

REGIONAL REO HOTSPOTS: TEXAS, CALIFORNIA &FLORIDA LEADTHE PACK

The Numbers & What They Reveal

July 2025 data paints a clear picture: Texas leads the nation with 377 REO properties the highest count among all states closely followed by California’s 360 and Florida’s 241. These numbers reflect completed bank repossessions, signaling areas where foreclosure activity has gone through to conclusion, reaching the point of bank acquisition of property.

Why These Regions Stand Out

Texas: A booming population and diverse economic landscape create broad exposure to market shifts Houston, for example, shows high foreclosure activity, indicating that agents dealing with REOs must be prepared for fastpaced market changes.

California: Urban centers such as Bakersfield are marked by high foreclosure rates one in every 1,538 housing units making these areas critical for targeted REO efforts.

Florida: Cities like Cape Coral (1 in every 1,735 housing units) and Lakeland (1 in every 1,802 units) face elevated foreclosure challenges, suggesting persistent demand for bank-owned properties.

Strategies for Agents & Investors

Localized Market Intelligence -Conduct deep research into county- and metro-level foreclosure filings. Knowing where rates are highest such as greater Houston or particular California metros helps tailor outreach, valuations, and offers

Proactive Outreach to Banks and Servicers

-Build relationships with institutions handling REOs. Texas, with the highest numbers, likely involves numerous local and regional bank partners. Early awareness of properties entering REO status can lead to advantageous deals.

Adaptive Marketing and Pricing Strategies

-In competitive markets, readiness to adjust pricing in response to demand and inventory changes is vital. Agents can benefit from leveraging local comps and foreclosure trends to position REOs effectively

Value-Add Tactics for Property Managers and Investors

-Offer renovation and property preservation services to improve marketability In places like Florida where foreclosure pressure is acute value-add improvements can differentiate REO listings from traditional listings.

Community-Specific Messaging

-Tailor outreach and marketing to local culture. Whether highlighting affordability in certain Texas regions or forecasting seasonal demand shifts in Florida, contextsensitive communication builds trust and effectiveness.

The July 2025 data places Texas, California, and Florida at the forefront of REO activity, offering both challenges and opportunities for real estate professionals. High counts of bank-owned properties reflect stress in key markets but also provide fertile ground for well-prepared agents, investors, and managers. By combining local intelligence with strategic outreach, dynamic pricing, and value-add services, industry professionals in these hotspots can turn elevated REO activity into lasting success.

Ready to turn opportunity into action? Connect with REObroker.com for tailored insights and expert support in navigating these REO-rich markets. Whether you're investing, managing, or brokering bank-owned properties, our team is ready to guide you visit https://www reobroker com or reach out via email at

From Listings to Showrooms: Bringing REO Properties to Life with Home-Staging Trends

Imagine stepping into a gallery where every home on display feels welcoming, aspirational, and primed for action that’s the aspiration behind the latest wave in property marketing In today’s market, properties needing value-add attention like REOs can benefit immensely from next-level staging. While traditional clean and decluttered layouts once dominated, now it’s about immersion: model sales galleries that showcase lifestyle potential, alongside virtual and sensory staging tools gaining momentum. These techniques help investors, agents, and property managers shift perception from "foreclosed asset" to "high-potential opportunity." This article explores how these staging innovations can transform REOs, helping properties sell faster and command stronger offers

1. Model Sales Galleries: The New Standard for Appeal

Model sales galleries essentially showroom versions of homes are gaining ground in real estate. These curated environments let buyers experience high-end finishes, layouts, and mood of a property before committing. A leading design editorial predicts showrooms will become essential tools in sales strategies, offering immersive, handson previews for prospective buyers. These galleries highlight finishes and amenity quality in a way photos often can’t.

For REOs, which may need visible improvements to feel move-in ready, creating a minimal “gallery” space can meaningfully boost emotional engagement A clean, tastefully furnished room signals care, potential, and readiness helping overcome typical buyer skepticism

Virtual staging continues to surge as a cost-effective staging solution Advances now allow interactive AR or VR walkthroughs, where users can customize furniture, finishes, and layouts in real time. Market projections show high growth—virtual staging is expected to leap from roughly USD 1.2 billion in 2024 to USD 5.5 billion by 2033, with compound annual growth nearing 18.5 percent.

This makes virtual staging ideal for REOs needing flexible, budget-friendly ways to demonstrate potential. Instead of empty rooms, prospective buyers see possibilities. The immersive experience increases engagement, even before a physical visit.

3. Data-Led Impact: Faster Sales, Better Offers

Staging isn’t just aesthetic it delivers measurable returns A recent industry overview found that staging can sell homes significantly faster and yield offers up to 20 percent above asking price Home staging also reduces market time, with around 30 percent of agents seeing faster sales.

Notably, the most critical area to stage remains the living room 37 percent of buyer agents rate it as essential, followed by primary bedroom (34 percent) and kitchen (23 percent). For REOs, focusing staging efforts on these core zones whether physically or virtually delivers the best strategic return

4. Balancing Trend and Timelessness

While staging benefits from design flair, over-personalized choices can alienate buyers. Experts caution against overused grays, bold paint, wallpaper, or heavy drapery— preferring earthy neutrals such as taupe, soft white, or greige to maintain broad appeal. Meanwhile, emerging design trends like color-drenching with accessories (pillows, small accents), layered textures, and a mix of vintage and modern touches can create sensory interest without overwhelming. Blending subtle trend cues within a neutral foundation helps REO properties feel fresh and relevant while remaining broadly appealing.

Conclusion

Model sales galleries and immersive virtual staging are redefining how properties especially those needing improvement can be presented to buyers By offering tangible experience through showrooms or engaging digital previews, REOs can shift from overlooked listings to thoughtfully curated spaces. Stage the living areas, apply subtle design accents, and use immersive staging tools to deliver a polished, confident presentation. These strategies are proven to attract stronger interest, command higher offers, and accelerate sales cycles

If you're ready to elevate your REO listings with compelling staging that drives results, reach out today. At REObroker.com, our team specializes in turning listings into experiences. Visit https://www.reobroker.com or contact us via email at info@reobroker.com or by phone at 760-238-0552 to explore how we can bring your next property to life. Let us help you create showrooms and virtual showcases that engage buyers and accelerate your success

Imagine unlocking a toolkit that shines a spotlight on the most promising bankowned listings before they even hit mainstream markets. That’s the power analytics bring to the hunt for repossessed properties. For savvy investors, agents, and property managers, knowing where to look and when can mean the difference between chasing dead ends and closing profitable deals.

Over the last few years, property data platforms have transformed traditional listing searches into precision operations. Platforms such as ATTOM and Realtor.com now deliver foreclosure and listing data with unprecedented depth and clarity. By tapping into this rich information flow, industry professionals can pinpoint opportunities with confidence and efficiency.

In this article, we’ll explore how these platforms arm users with actionable insights from foreclosure filings, auctions, and bank-owned inventory to listing trends and regional forecasts. We’ll examine how leveraging these tools can sharpen targeting for REO opportunities and ultimately help streamline your workflow and bottom line.

Platforms Powering Insight

ATTOM stands out as a leading source of foreclosure and related data. With coverage spanning over 155 million residential and commercial properties covering nearly the entire population its database includes detailed records for every stage of the foreclosure pipeline, including auctions, default notices, and bank repossessions. This level of granularity allows agents and investors to analyze opening bids, timelines, and local patterns with ease.

On the other hand, Realtor.com delivers real-time access to bankowned listings flagged as foreclosure, helping users view photos, status, and historical listing trends in one platform. Its expansive MLSbased database combines multiple listing feeds into robust visualizations, aiding both strategic decision-making and timely action.

Turning Data into Strategy

For agents and property managers, this data becomes a tactical asset. ATTOM allows users to compare foreclosure activity by state, county, or ZIP code, helping identify “hot zones” where filings or completed repossessions are spiking. Such insights empower targeted marketing, better price assessments, and quicker responses to auctions before competition heats up.

Realtor.com complements this by showcasing visible inventory, enabling professionals to monitor new REO listings as they surface. Combining both sources ATTOM for macro trends and Realtor.com for active inventory gives a powerful, 360-degree view of opportunity and timing

Real-World Example

Consider Chicago, which led the nation in foreclosure starts during early 2025, followed by major metro areas like New York and Houston An investor could use ATTOM to track rising filing rates in key neighborhoods, then switch to Realtor com to monitor when corresponding bank-owned listings become active acting swiftly to evaluate and bid.

Value for Property Managers

For property managers juggling multiple assets and markets, this combination of broad analytics and real-time listing alerts helps anticipate shifts in bank-owned inventory, assess localized risk exposure, and align maintenance, marketing, or leasing strategies with projected foreclosure waves.

In sum, analytics have elevated the way real estate professionals hunt for bank-owned listings ATTOM equips users with deep foreclosure intelligence covering filings, auctions, and repossessions while Realtor.com fills in the details of what’s actually available in the market today. When used together, they help agents, investors, and managers anticipate, locate, and act on REO opportunities with precision and speed

By blending comprehensive trend analysis with live inventory tracking, you gain a clear edge in spotting value, reacting faster, and crafting smarter outreach strategies. Embracing these platforms means turning what was once guesswork into guided decision-making saving time, reducing risk, and unlocking new opportunities for growth.

Ready to take your approach to REO opportunities to the next level?

Reach out to REObroker.com, where we combine cutting-edge analytics with expert insight to help you target the right bank-owned deals with clarity and confidence Whether you’re an investor, agent, or property manager, let us guide you through the numbers and connect you with premium listings. Visit us at https://www.reobroker.com or send your questions to info@reobroker.com, or call us directly at 760238-0552 our team is here to help you act smarter and grow your portfolio

REO Myths Debunked:

You Don’t Need Perfect Credit to Buy Foreclosures

Foreclosures often evoke visions of perfect credit and endless paperwork Yet for many investors, agents, and property managers, this perception is simply not accurate. While the idea of purchasing bank-owned properties may sound intimidating, the truth is more inviting: you don't need a flawless credit history to successfully navigate these opportunities.

Across the market, distressed properties those repossessed by lenders present compelling value, frequently priced to move However, a widespread myth persists: that only buyers with pristine credit and ample cash can access these deals. In reality, financing options and institutional buyer flexibility have opened the door to a wider range of purchasers.

This article will explore and debunk common misconceptions surrounding credit requirements and bureaucratic hurdles in REO purchases. You’ll gain clear guidance on workable financing paths, expectations, and strategies to confidently pursue bankowned properties even with less-than-perfect credit.

Myth 1: You Must Have Pristine Credit to Qualify

It’s commonly believed that only buyers with excellent credit scores can secure financing for bank-owned properties. In fact, many mortgage programs exist for credit scores in the mid-500s to 600s For example, an FHA loan may accept a credit score around 580 with a modest down payment of approximately 3.5% though property condition and eligibility still apply. VA loans are another path where credit and down payment requirements can be relaxed for qualified buyers.

Moreover, certain lender or agency-run REO programs often feature competitive terms designed to attract more buyers, especially in markets flush with inventory The evolving landscape of financing has made these properties more accessible than many assume.

Myth 2: You’ll Face Excessive Red Tape

While banks do adhere to protocol, buying a bank-owned property often follows a process much like a standard real estate transaction especially once the home transitions into an REO listing. Many of these properties are now listed on the MLS alongside traditional homes, streamlining exposure and accessibility.

It’s true that lenders may delay responses or require unique paperwork, especially if managing large volumes of listings But smart buyers work with experienced agents, get preapproved, and tailor their offers to align with bank timelines reducing friction Ethical waiver of contingencies (like inspection periods) can also strengthen offers but should never be done without a proper inspection strategy.

Myth 3: Cash Offers Are Always Required

Another misconception: every REO purchase demands full cash. In auction scenarios, this may occasionally apply but most REO listings are handled like traditional real estate sales, meaning mortgage financing is accepted and used by many buyers

That said, banks may favor cash offers in cases where the property’s condition is poor. But for better-maintained listings, financing is often available and in some instances, buyer assistance programs or specialized loans can even make these deals feasible for those with modest credit.

In summary, the path to acquiring bank-owned properties is more accessible than many believe. You don’t need perfect credit, nor are you always blocked by red tape or forced to pay cash. With the right preparation from understanding available loan programs to partnering with knowledgeable agents REO purchases can be viable and rewarding even for buyers with moderate credit profiles.

By breaking down these misconceptions, this article lays out practical strategies: use flexible loan programs, leverage agent expertise, and craft offers that balance competitiveness with caution. With clarity and persistence, investors, agents, and managers alike can tap into these hidden opportunities and cultivate success in the foreclosure space.

If you're ready to explore REO opportunities and want expert guidance tailored to your situation, we're here to help. At REObroker.com, our dedicated team specializes in helping buyers and professionals navigate the foreclosure market regardless of credit profile. Visit us at https://www.reobroker.com or reach out anytime at info@reobroker.com or by calling 760-238-0552. Let us help you turn common misconceptions into real, tangible opportunities.

How Lowering Mortgage Rates Could Shift REO Market Dynamics

When mortgage rates ease to their lowest point of the year, the ripple effects reach far beyond traditional homebuyers. Suddenly, properties owned by lenders and sitting idle the ones waiting for a new owner spring into focus. For investors, real estate professionals, and property managers, this shift isn't just about better affordability for buyers it could reshape how these properties move through the market. As borrowing costs fall, more buyers gain access to financing, potentially accelerating the pace at which these lender-owned properties move off the market In turn, this could heighten competition for distressed listings and alter standard strategies around pricing, marketing, and turnaround timelines In this article, we’ll explore how a drop in mortgage rates can speed up sales within this segment, attract new bidders, and influence your approach as a stakeholder in the space

1. Improvements in Affordability Fuel Interest

When rates dip even modestly monthly payments become more manageable for a wider range of buyers. For instance, recent reports show the average 30-year fixed-rate mortgage now stands around 6.58%, the lowest since last fall. That eased cost threshold can make lenderowned property listings, often priced aggressively, even more appealing. As financing becomes more accessible, these properties may begin attracting buyers beyond investors firsttime homeowners, for example who are now able to participate in bidding where previously they'd been priced out

2. Faster Turnover of Lender-Owned Inventory

With affordability creeping upward, buyers won’t linger as long on the sidelines. Recent data indicates existing home sales rose by 2.0%, partly driven by a drop in mortgage rates. This uptick suggests increased confidence and purchasing activity. In parallel, properties in foreclosure let go to lender ownership may clear inventory more quickly as both demand and financing align favorably.

3. Sharper Competition for Distressed Listings

As mortgage rates pull back, previously cautious buyers might reenter the market, joining seasoned investors in the race for lender-owned deals. Reports note investor activity now accounts for roughly 20% of home sales, up from 13% a year ago. As demand intensifies, even those who traditionally avoid bidding wars may reconsider, escalating competition for these listings. That scenario pushes prices upward and can reshape negotiation dynamics for agents and managers overseeing such properties.

4. Impacts on Strategy: Pricing, Marketing, and Timing

Pricing strategies may need recalibrating. Properties that were once positioned as bargains may no longer be perceived that way in a lower-rate environment. Investors and agents should evaluate comparable sales more closely.

Marketing efforts could amplify as a broader pool of qualified buyers emerges. Highlighting favorable financing terms could turn casual interest into serious offers.

Timing matters with inventory turnover potentially quicker, efficiency in valuation, repairs, and listing becomes key. A streamlined process offers competitive advantage in securing buyers promptly. Lower mortgage rates may not deliver seismic shifts overnight, but even modest easing can unlock latent demand, particularly for lender-held properties. Improved financing conditions can galvanize buyers, hasten inventory movement, and elevate competition for distressed listings. For investors, agents, and property managers, the takeaway is clear: adapting to a market where affordability improves even incrementally can sharpen strategy and maximize outcomes. By aligning pricing, marketing, and timing with these rateinfluenced trends, professionals in this space can both anticipate change and leverage it effectively.

If you're looking to stay ahead of these shifts and capitalize on emerging opportunities, let REObroker.com be your trusted partner. From market insights to listing execution, our team is committed to delivering responsive, tailored support. Visit us at https://www.reobroker.com or get in touch via info@reobroker.com or 760-238-0552 we’re here to help you navigate this evolving market and achieve your objectives with confidence.

Imagine uncovering a property that’s priced significantly lower than its surroundings, not because it’s undesirable, but because it’s owned by a lender eager to move it on. That’s the reality for those seeking opportunities in bank-owned real estate. These listings can translate to meaningful savings for investors, agents, and property managers but the extent of that discount can vary widely across different regions.

In some states, REO properties homes seized by banks and then put on the market sell at notably lower prices than similar, non-distressed homes, making them attractive targets. The degree of discount depends on a range of factors: local market strength, property condition, and how swiftly the lender wants to liquidate the asset. In this article, we’ll look at how these discounts differ by region, using concrete examples such as the situation in Massachusetts with its valuation challenges and steep discounts. We’ll explore where the deepest savings are, what drives them, and how savvy professionals can use this knowledge to their advantage

Regional Differences in REO Pricing

Some regions see REO homes sell at 25–30% below comparable market values A study analyzing two decades of home sales in Massachusetts found that foreclosure-related sales are discounted on average by about 28% relative to what similar homes might fetch. That’s an eye-opening figure for investors evaluating returns or agents advising clients on pricing strategies

Deep Discount Zones: Massachusetts Case Study

Massachusetts offers a revealing case. Analysis of REO transactions from mid-2007 to 2008 shows that sales prices frequently lagged behind market levels, in part due to fast liquidations and appraisal inconsistencies amid market turmoil. Forced-sales often arise in neighborhoods with lower incomes or high mortgage leverage, where lenders are motivated to offload properties quickly resulting in sharper price drops Furthermore, spatial and appraisal challenges can lead to larger valuation gaps and steeper discounts.

Why Discounts Vary State-by-State

Multiple factors influence discount depth In areas with slower housing turnover or economic stress, lenders accept lower offers to limit holding costs and risks a stance informed by research on REO pricing rarely reflecting ongoing comparisons to current market values. Some regions particularly those hit harder by economic downturns show even deeper REO discounts due to local distress, stigma around lender-owned properties, or lack of buyer confidence.

Variations Across Markets

Other analyses, for instance, comparing requests for foreclosure discounts across local markets, reveal clear geographic variance. Estimates show foreclosure discounts in some states like Indiana are higher than in others like Florida, with pricing differences influenced by neighborhood characteristics and market conditions. This heterogeneity underscores the need for state-specific investigation rather than relying on national averages.

Across the country, bank-owned properties often command prices well below market comps but the magnitude of that discount can differ dramatically by state and neighborhood. In Massachusetts, for example, REO sales have historically traded around 28% below typical values, driven by market conditions and expedited sales strategies. For investors, agents, and property managers, understanding these state-level differences is essential. It enables smarter decision-making, more accurate evaluations, and the ability to leverage opportunity where property is priced most attractively. Regional nuance matters and recognizing where REO discounts are deepest can yield substantial yields.

Ready to explore the most compelling REO opportunities tailored to your market? Reach out to REObroker.com to get expert insights into state-specific trends and unmatched listings that could deliver your next big win. Whether you're seeking data-driven evaluations or hands-on brokerage support, our team is here to guide you. Visit https://www.reobroker.com, drop us a note at info@reobroker.com, or give us a call at 760-238-0552 let us help you navigate the REO landscape with confidence and precision.

REO-to-Rental: A Strategic Pivot for

Investors and Lenders

Imagine a slow but steady solution to the growing inventory of troubled properties blanketing neighborhoods. What if, instead of watching these homes deteriorate or dumping them on the market, they could be transformed into steady rental income? That’s the essence of a strategic shift gaining renewed attention: converting these properties into rentals. This approach benefits both investors looking for yield and entities seeking to stabilize markets. In this article, you’ll learn how an experimental strategy from years past could be reshaped for today’s housing landscape. We’ll explain how pilot projects have worked, the challenges and advantages involved, and why now might be the right moment to revisit this opportunity.

Pilot Programs Lighting the Way

A few years back, an initiative was launched where pools of distressed, institution-held homes were offered to investors with the stipulation that they be converted into long-term rentals. The aim was twofold: draw in private capital while absorbing excess housing stock and helping local markets recover.

Early pilots demonstrated potential by leveraging investor resources for both financial return and community stability.

Benefits for Investors

For investors and operators, this model offers access to property portfolios often sold at favorable prices. The approach aligns with known strategies like acquiring below market cost and generating ongoing rental revenue. In favorable markets, the increased value from stable rental income can even yield benefits upon eventual resale.

Advantages for Markets and Communities

Importantly, this model delivers more than financial upside It helps stabilize neighborhoods by filling vacant properties, reducing deterioration, and bringing consistent occupancy. Initial pilot efforts revealed that converting empty homes into rentals can counter declining property values and elevate local morale.

Lessons Learned from Pilots

While promising, these programs also highlighted practical hurdles investor vetting was sometimes uneven, and oversight lacked clarity. Regulatory bodies learned that to scale these efforts effectively, frameworks must ensure that investor partners are both financially capable and operationally reliable. Clear monitoring, goals, and assessments are essential for future iterations

Why It Matters Today

As foreclosure and distressed-property volumes rise again, investors are scouting low-entry opportunities. Rental demand remains strong in many markets, making this model especially relevant now. For both capital providers and property professionals, reviving REO-to-Rental strategies opens a path that balances profit with neighborhood renewal.

Transforming distressed housing into rental assets offers a compelling dual benefit: investors gain reliable income streams, and communities regain stability and occupancy. While past pilot programs taught us that program design and oversight are critical, current market pressures and demand for rentals make this strategic pivot more promising than ever. Embracing such initiatives could be a savvy, socially responsible step forward.

If you’re intrigued by the potential of REO-to-Rental pathways and want to explore how this approach could serve your investment goals or empower your brokerage or property management strategies, reach out. At REObroker.com, we're dedicated to helping investors and professionals turn opportunity into action. Visit us at https://www reobroker com or email info@reobroker com Want to talk? Call 760-238-0552 today to discover how converting challenging properties into rental solutions can align profit with purpose.

Imagine a homeowner who's proudly maintained their mortgage at a very low interest rate perhaps locked in a 3-4 percent fixed-rate loan a few years ago. Today, selling their home means taking on a much higher rate maybe 6 or 7 percent and that’s a heavy financial burden. This scenario sets up a powerful disincentive to move.

At the same time, mortgage-rate volatility makes owners hesitant to list their properties Over time, as economic stress grows or income falters, some of these locked-in homeowners do end up defaulting. That creates a wave of real estate owned (REO) listings, increasing overall inventory. This article explores how the lock-in effect works, why it suppresses for-sale inventory, and how it eventually spins off into higher REO levels.

The Mortgage Lock-In Effect and Market Behavior

When interest rates climb, homeowners with low fixed-rate mortgages hesitate to move because they’d lose favorable terms. Studies show that each 1-point rise in rates can reduce the probability of a sale by over 18%, and raise home prices by around 5.7% due to constrained supply, despite the direct cooling impact of higher rates on demand.

One research analysis found the average borrower may be sacrificing $50,000 in cumulative mortgage cost savings to hold on to their low rate, a deterrent powerful enough to cut mobility significantly

Inventory Shortages and Market Strain

With so many homeowners entrenched in their homes, listings fall sharply At one point, existing-home listings were down by up to 35 percent compared to prepandemic norms. Surveys confirm that a substantial share of homeowners staying put cite low rates as a primary reason alongside home attachment or high prices

Eventually, Defaults Rise and REO Increases

Lower listing rates tighten inventory, raising prices but not indefinitely Economic stress, job loss, or rising insurance and tax costs can push homeowners toward default. Many eventually end up in foreclosure, turning properties into REOs. Historical data during the earlier housing crisis shows how foreclosures flooded markets and created REO surges

The Lock-In Effect’s Broader Impacts

Long term, the lock-in effect foments inequality: homeowners who locked in low rates benefit enormously, while newer or prospective buyers face steeper costs and limited options. This widening gap strains affordability and market dynamics.

Conclusion

In short, rising mortgage rates create a lock-in effect that keeps many homeowners from selling While this suppresses inventory and props up prices in the short term, financial pressures eventually drive some into default boosting REO listings. For investors, agents, and property managers, recognizing this pattern is vital: supply may be tight now, but future REO inventory could surge as locked-in owners face hardship

If you’d like to stay ahead of this trend whether by spotting upcoming REO opportunities or positioning your portfolio for evolving market shifts set up a chat with us at REObroker.com. Reach out via our website (https://www.reobroker.com) or drop us an email at info@reobroker.com. Prefer a direct conversation? Give us a call at 760-238-0552—we’d be happy to discuss how you can benefit from tomorrow’s inventory dynamics

There’s a subtle yet meaningful shift underway in the real estate market one that savvy investors, agents, and property managers can’t afford to ignore. While median listing prices have inched upward hovering near $439,450, up roughly 0 5% year over year overall home value growth has stalled at just about 0.3%. This mismatch between listing expectations and actual valuation is creating a fresh kind of affordability pressure, especially for those eyeing bank-owned or distressed properties In this landscape, real estate–owned (REO) opportunities are being redefined: no longer automatic bargains, they're now weighed carefully against shifting market realities

This article explores how these affordability constraints are influencing REO buyer behavior, detailing what that means for different market participants. We’ll examine the trends driving cautious buying approaches, how pricing strategies are adapting, and what this means for your investment or portfolio strategy Let’s dive into the forces reshaping bargain dynamics in today’s housing market.

Affordability Squeezes Buyer Leverage

The modest rise in listing prices, paired with nearly static home value growth from a national average home value of about $368,580, up just 0.3% is squeezing buyer power. Even though inventory is gradually increasing, the balance still favors sellers in many markets, keeping REO discounts in check.

Inventory Shifts and Price Pressures

Data shows inventory of active listings has climbed steadily for many months, helping rebalance the market Despite this, sellers often hold firm, anchoring to peak-era price expectations and avoiding deep discounts even on REO listings. This makes thorough due diligence crucial, especially as price cuts are still noticeable across one in five listings.

Regional Divergence Shapes Tactics

Affordability dynamics are not uniform. Midwest and Northeast markets have seen modest value growth, offering more balanced conditions In the West and South where building restrictions, high demand, or coastal pressures persist savvier buyers may face inflated listing prices with fewer traditional REO opportunities Understanding these differences can help tailor pricing expectations and negotiation strategies.

REO Buyer Behavior: Strategy Over Speculation

Today’s REO purchasers are taking a more measured stance. Rather than snapping up distressed listings purely for discounts, they’re evaluating total return, cost of repairs, and financing realities. In markets where a 5%–10% growth forecast over five years is plausible, long-term value creation becomes the rationale, even if immediate deals look less compelling.

Moreover, as one industry expert noted, a modest gain in affordability due to easier mortgage payments or slightly lower rates can breathe life into buyer interest. Still, many are cautious: rising cash purchases and investor activity signal that access to capital remains a key advantage for navigating tight markets

As affordability remains stretched and price growth subdued, REO buyers are adapting their playbooks. Bargain-hunting is no longer just about securing a discount; it’s about aligning expectations with market realities, focusing on long-term value, and tailoring strategies by region. Rising listing prices, steady but slow value growth, and uneven inventory trends mean investors and agents must balance ambition with pragmatism. REO opportunities persist, but success now depends on sharp analysis, flexible pricing, and local market awareness. Understanding when and where value can emerge is the key.

If you're looking for expert guidance navigating REO opportunities in today’s affordability-challenged market, reach out to REObroker.com. Our team at https://www.reobroker.com is ready to help you uncover the insights and strategies that match your investment or property management goals—just drop us a line at info@reobroker.com or call 760-238-0552. Let us be your partner in identifying smart, valueoriented REO options and making informed decisions that deliver meaningful results We look forward to helping you unlock real potential in every deal

This slowdown in 39 of the 50 largest metro areas, especially across the South and West, is more than just a statistic; it's reshaping the landscape for REO investors in real time. As listings linger, inventory builds, and buyer behavior shifts, the balance of power is nudging toward those with capital and flexibility.

This article will explore how longer listing times are influencing REO pricing strategies, giving investors stronger negotiating positions, and helping refine the timing of acquisitions and dispositions. With careful insights and practical examples, we'll unpack what slowed sales mean for your bottom line and how you can turn these shifts to your advantage.

This trend is especially pronounced in the Sun Belt, where elevated prices and rising mortgage rates have tempered demand. Builders have also responded, adding to supply with fresh listings in a holdover from the pandemic-era housing boom

2. Pricing Power and Negotiation Leverage for REO Investors

With demand cooling and listings lingering, buyers including institutional or smallerscale REO investors find themselves in a stronger position. In many regions, over half of homes that eventually sell are closing below asking price, with a national average sales drop of around $45,000 under list price. Sellers are growing increasingly unwilling to budge, with many instead pulling listings off the market entirely rather than negotiate.

In markets like Miami, sellers are particularly stubborn choosing to delist rather than offer price reductions. Delistings there have surged, hitting 59% in June, outpacing the national norm of 21%

For REO investors, this extended time on market and heightened seller resistance can be an invitation to craft more creative offers, backed by data, to secure better terms or added concessions such as repairs, credits, or favorable financing.

3. Strategic Timing: When to Act (and When to Wait)

Longer listing times also open new timing strategies Investors can monitor stale listings those sitting for weeks without price adjustments. These homes may represent motivated opportunities, especially when combined with growing inventory and falling sales activity.

At the same time, sellers withdrawing listings change the calculus A temporarily removed property might re-enter with revised expectations making it ripe for acquisition when it returns For REO investors, patience, paired with market tracking, can yield acquisition advantages.

A market where homes stay on the shelf longer offers a renewed advantage for savvy REO investors. Slower sales and rising supply empower negotiators to shape deals more favorably At the same time, the evolving inventory dynamics call for attentive timing knowing when to strike and when to wait can make all the difference.

By reading these signs and acting decisively, investors, agents, and property managers can capitalize on a shifting market regime turning patience into performance.

If you're ready to strategically navigate this evolving market, REObroker.com is here to help Whether you’re looking to buy, sell, or evaluate REO opportunities, our team offers sharp insights and dedicated support to guide every move. Visit us at https://www.reobroker.com or reach out via email at info@reobroker.com or by phone at 760-238-0552 to connect. Let REObroker.com be your partner in turning market delay into your next opportunity.

Myth-Busting REO: Debunking Misconceptions About Bank-Owned

Homes

Imagine uncovering an opportunity many dismiss homes owned by financial institutions, often overlooked, sitting just beneath the surface of mainstream real estate Yet, contrary to popular belief, these properties can deliver surprising value to savvy investors, agents, and property managers. The idea that all bank-owned listings are mere money pits, teeming with unseen damage or requiring perfect credit to navigate, persists but it’s time to challenge those assumptions.

In the current market landscape, these homes can offer genuine advantages discount pricing, financing flexibility, and diverse investment paths. This article will challenge three common myths: that these properties are always dilapidated, demand total renovation, or are inaccessible to those without flawless credit. Drawing on recent data and expert insights, we'll illuminate the true potential of these opportunities and how professionals in the field can approach them with clarity, confidence, and strategy.

Myth 1: All Bank-Owned Homes Are in Terrible Condition

It’s easy to assume foreclosure equates to neglect but that’s not always the case While some homes do reflect deferred maintenance, many lenders invest in basic repairs before listing. According to real estate professionals, “banks are remodeling the homes they take ownership of before selling,” so overlooked properties may surprise buyers with fresh finishes or improved utilities. Moreover, recent commentary emphasizes that many foreclosures were entrusted to lenders simply due to financial hardship not intentional abandonment.

Myth 2: Every Bank-Owned Home Requires Full-Scale Renovation

A widespread misconception is that these homes are automatically renovation projects but that isn’t universally true. Some homes require cosmetic updates, while others may need minimal improvements. Still, professionals caution that estimating repair costs can be tricky One industry guide notes: "One of the most frequent mistakes investors make is underestimating the cost of repairs" highlighting the importance of a professional inspection when possible Strategically, a selective renovation approach prioritizing upgrades that add maximum value can yield strong returns without overspending

Myth 3: You Need Perfect Credit or Cash to Buy

Perhaps the most discouraging myth: the belief that buyers must have perfect credit or pay in cash. In reality, numerous financing paths exist Investors and buyers can utilize conventional mortgages, hard-money loans, VA/FHA/USDA loans, private lending, and even financing options provided directly by the lender holding the property. Some lenders are motivated to facilitate a sale and may be more flexible than traditional expectations anticipate.

Strategic

Advantages and Considerations

These properties often sell at or near market value and sometimes below, depending on condition and demand The advantages extend beyond price: they typically come with clear title (freed from lingering liens or taxes), multiple financing options, and motivated sellers. Challenges include “as-is” sales, limited property history, and competitive bidding environments. The antidote lies in preparation: secure financing early, work with agents experienced in these listings, conduct inspections, and build realistic cost contingencies.

Far from being universally dreary or out of reach, bankowned homes offer pragmatic opportunities often presenting value in surprising ways. While it’s true some properties require more attention than others, many are in better shape or financeable than commonly believed The real key is informed decision-making: proper inspections, careful budgeting, and utilizing flexible financing can unlock positive outcomes for investors, agents, and property managers alike.

By setting aside misconceptions and approaching these opportunities strategically, professionals can uncover real potential where others see only risk. This space deserves more thoughtful exploration not dismissal

Ready to turn misconceptions into opportunity? Reach out to REObroker com to learn how bank-owned properties can work for your goals. At REObroker.com, we offer tailored guidance, expert listings, and financing insights to help you capitalize confidently whether you're investing, managing, or brokering. Visit our website at https://www.reobroker.com or send us an email at info@reobroker.com to start a conversation. Prefer to talk directly? Call us at 760-238-0552 and let’s transform myth into advantage together.

About half of homes are selling for under their asking price right now

While that feels very different from the past few years, it’s actually a return to what’s considered normal for the market.

And the sellers who succeed today are the ones who recognize this shift. They price smart from day one, make their home stand out, and stay flexible when buyers ask for give-and-take.

You need to plan for the market we’re in, not the one we saw a few years back. And I can help

REO Reality Check: Is Rising Foreclosure Activity Signaling Opportunity or Risk?

A meaningful shift is quietly underway in the housing market: foreclosure filings have climbed by 13% year over year, and completed foreclosures (REOs) are up 18% These increases are gaining attention from investors, agents, and property managers alike What’s behind the rise, and what does it mean for stakeholders looking to navigate changing conditions?

This surge arrives against a backdrop of tightening economic conditions rising rates, operating costs, and squeezed household finances. Yet, overall property values remain healthy enough to help many homeowners preserve equity, offering some balance to the stress signals

In this article, we’ll explore whether the expanding inventory of REO properties presents a golden opportunity, a warning sign, or both We’ll break down what the numbers actually show, consider the drivers behind the trends, and consider how savvy professionals can interpret what’s unfolding.

1. Numbers Tell the Story

Recent data indicates 36,128 properties had foreclosure filings in July up 13% from a year earlier. Foreclosure starts are up 11%, while completed foreclosures rose by 18% year over year, though they dipped slightly from June.

That uptick in REOs reflects growing inventory for investors and agents looking for value but also points to higher strain on borrowers. The fact that completed foreclosures are increasing more than starts suggests a backlog clearing, rather than a spike in new distress.

2. Opportunity: More Inventory, Better Pricing Potential

Rising REOs mean more properties hitting the market often priced below typical market value and available to investors and managers prepared to act Markets such as Chicago, New York, Detroit, Houston, and Los Angeles show higher volumes of completed foreclosures, offering more prospects.

For investors, REOs can offer margin for value-add projects. Agents and property managers can leverage these properties to help distressed sellers or local governments stabilize neighborhoods.

3. Risk: Underlying Economic Strain and Distribution Concerns

Those filing rates aren’t uniform. Certain states like Nevada, Florida, Maryland, South Carolina, and Illinois face the highest foreclosure rates, with one in every ~2,300 to ~2,700 housing units affected.

This concentration suggests localized financial distress resulting from factors like job losses, regional downturns, or unaffordable borrowing conditions.

Moreover, while increasing REOs may signal opportunity, they also signal that more homeowners are under stress, which could weigh on property values in certain markets. Agents and managers must watch for signs of weakening demand or declining neighborhoods.

4. Balanced View: Opportunity and Caution Hand in Hand

The truth is nuanced. Growing REO inventory offers buying and management potential but it’s also a symptom of deeper economic challenges. For investors and agents, success lies in selective market targeting, rigorous due diligence, and strong risk management.

This is not a nationwide flood of foreclosures; yet persistent upward trends warrant attention The key is distinguishing regions with manageable opportunities from those with underlying vulnerabilities.

The rise in foreclosure activity and REOs reflects both opportunity and caution For professionals who move wisely, it offers a chance to acquire properties at favorable margins and deliver real value. At the same time, uneven stress levels across markets signal that risk is very real

Understanding the data, staying alert to regional differences, and applying strategic judgement will set investors, agents, and property managers on the right side of this shift. As always, being informed and nimble will matter most.

Ready to explore promising REO opportunities while navigating risk with confidence? Reach out to REObroker.com to connect with a team that specializes in matching motivated buyers and managers with high-value

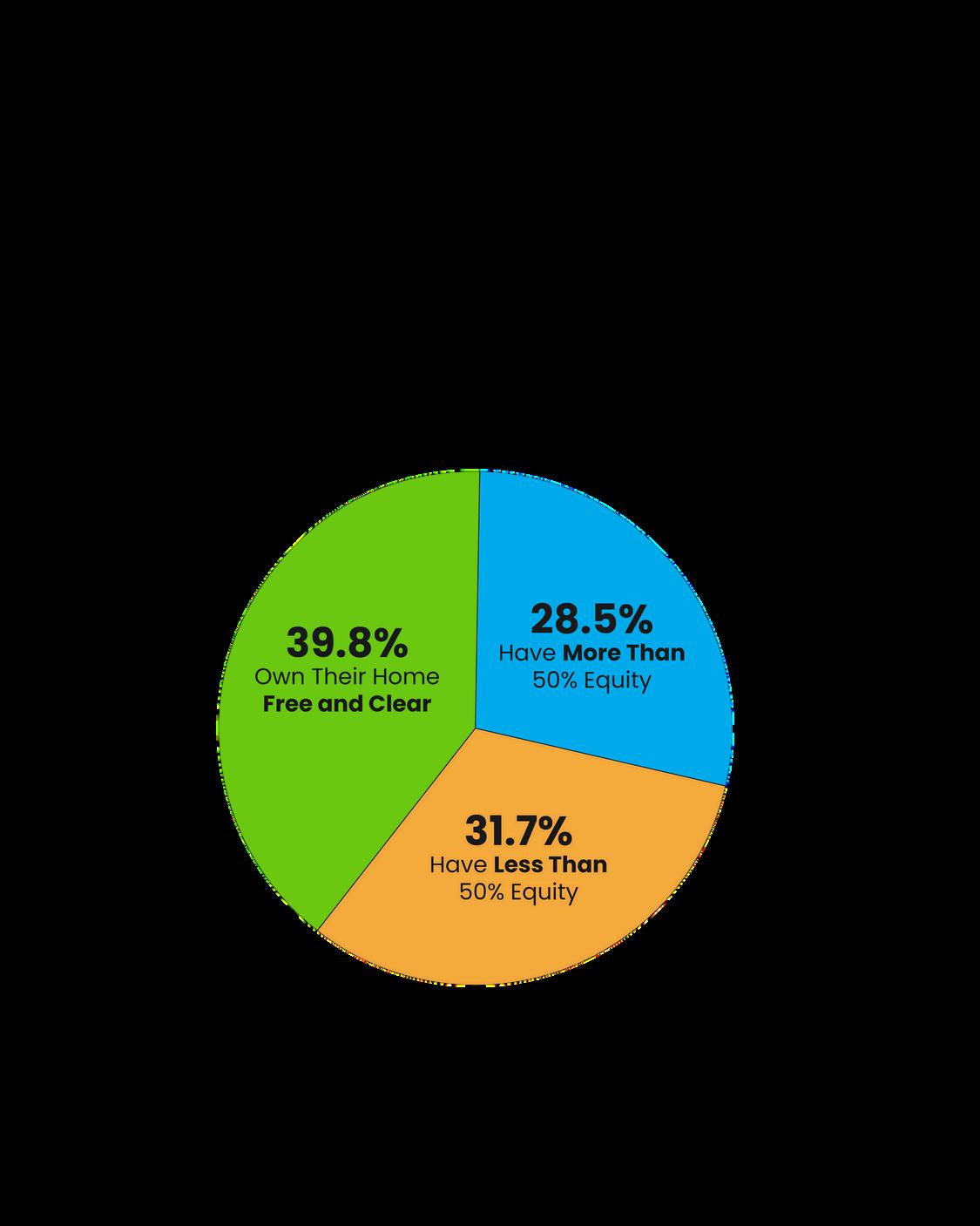

Most Homeowner

s Have a Lot of Equity Pie

Chart

If you’ve owned your home for a while, you probably have some serious equity.

Right now, over two-thirds of homeowners have either paid off their mortgage entirely or have at least 50% equity

That’s a powerful position to be in. Because that much equity gives you a strong financial cushion and an asset you can use to fund your long-term goals.

If you're thinking about moving, downsizing, or just curious what your home’s really worth, Message me and I’ll give you a personalized estimate, because your equity might be able to get you there sooner rather than later.

nancy@showcaserealty.net showcaserealty net

With over 30 years of experience, Nancy has built a powerhouse brokerage ranked in the RealTrends Top 1% of America’s Best Real Estate Agents, as featured in The Wall Street Journal.

A trailblazer, award-winning leader, and fierce client advocate, Nancy is celebrated for her unmatched negotiating skills, dedication to community, and her bold service guarantee: “Your home sold in 60 days, or we’ll pay you $2,500.”

She is more than a broker she’s a visionary, a philanthropist, and one of Charlotte’s Most Influential Women, as recognized by the Mecklenburg Times Nancy’s story is one of excellence, resilience, and leadership in REO and beyond

Stephanie D. See is the President and Co-Owner of Results Real Estate, Inc., a boutique brokerage in Largo, Florida With over 20 years of experience and a broker’s license since 2013, she and her husband, John B See, have closed more than 5,000 transactions across the Tampa Bay area Stephanie is known for her integrity, attention to detail, and expertise in residential and REO markets.

A dedicated industry leader, Stephanie has served on the Board of Directors for the National Association of Default Professionals (NADP) for eight years She is committed to raising professional standards through education, mentorship, and collaboration. Under her leadership, Results Real Estate continues to deliver client-focused service in a wide range of market conditions

Fran Altman is an Associate Broker with Coldwell Banker Realty, proudly serving the St Cloud, Minnesota area and surrounding communities A true Minnesotan through and through, Fran was born and raised in central Minnesota and loves helping others find their place here

She graduated from Apollo High School in St. Cloud before earning her Bachelor of Arts in Organizational Management with a minor in Communications from Concordia College in St Paul

Dynamic and results-driven Real Estate Broker with extensive experience as an Area Vice President at Vylla Home, spearheading growth and delivering on the company's mission Adept at empowering agents and transforming the real estate process Specializing in institutional asset sales, risk mitigation, talent acquisition/retention, and marketing, with a strong background in leadership and growth-oriented roles within both for-profit and non-profit corporations.